western australian beef commentary - department of ... number: 12 date: august 2016 western...

TRANSCRIPT

Issue Number: 12

Date: August 2016

Western Australian Beef Commentary Prepared by the Department of Agriculture and Food, Western Australia

Summary

The Western Australian (WA) beef cattle herd increased 14% year on year to 2.24 million

head in 2014/15

Total turn-off fell 6% from 717 000 in 2013/14 to 675 000 in 2014/15

Between 2012 and 2015 there was an increase of 10% for WA cattle slaughter and beef

production, with 2% more male cattle than female cattle slaughtered in 2015.

Between 2012 and 2015 WA beef exports increased 72% in volume to 43 million

kilograms and 170% in value to A$184 million. Korea was WA’s largest market for boxed

beef by volume in 2015 and the United States of America (USA) was the largest by value.

Vietnam was the largest market by volume and value for WA live cattle exports in 2015,

accounting for 28% of the volume and 29% of the value of live cattle exported.

During 2016 WA cattle market indicators have been very strong compared to previous

years. In July 2016:

o The feeder yearling indicator averaged 329 cents/kilogram (c/kg)

o The heavy cow indicator averaged 242c/kg

o The pastoral cow indicator averaged 210c/kg

o The light bull sale yard indicator averaged 307c/kg

2

Contents Current herd situation in WA ............................................................................................................ 3

Cattle turn-off and beef production ................................................................................................... 3

Cattle slaughter ............................................................................................................................ 4

Beef production ............................................................................................................................ 6

Boxed beef exports .......................................................................................................................... 7

Volume ......................................................................................................................................... 7

Value ............................................................................................................................................ 8

Live exports .................................................................................................................................... 10

Volume ....................................................................................................................................... 10

Value .......................................................................................................................................... 12

Market indicators ............................................................................................................................ 13

Competitor analysis - New Zealand ............................................................................................... 15

Market analysis - Korea ................................................................................................................. 17

Weather watch ............................................................................................................................... 19

Appendix ........................................................................................................................................ 21

Sources

Australian Bureau of Statistics (ABS)

Meat and Livestock Australia’s National Livestock Reporting Service (NLRS)

Statistics New Zealand

Meat and Livestock Australia (MLA)

Beef & Lamb New Zealand

Wagyu International

Statistics Korea

The Bureau of Meteorology

Contact

Kate Pritchett Research Officer, Grains and Livestock Industries, Department of Agriculture and Food, WA +61 (0)8 9821 3252 +61 (0)429 700 317

Important disclaimer

The Chief Executive Officer of the Department of Agriculture and Food and the State of Western Australia

accept no liability whatsoever by reason of negligence or otherwise arising from the use or release of this

information or any part of it.

Copyright © Western Australian Agricultural Authority, 2016

3

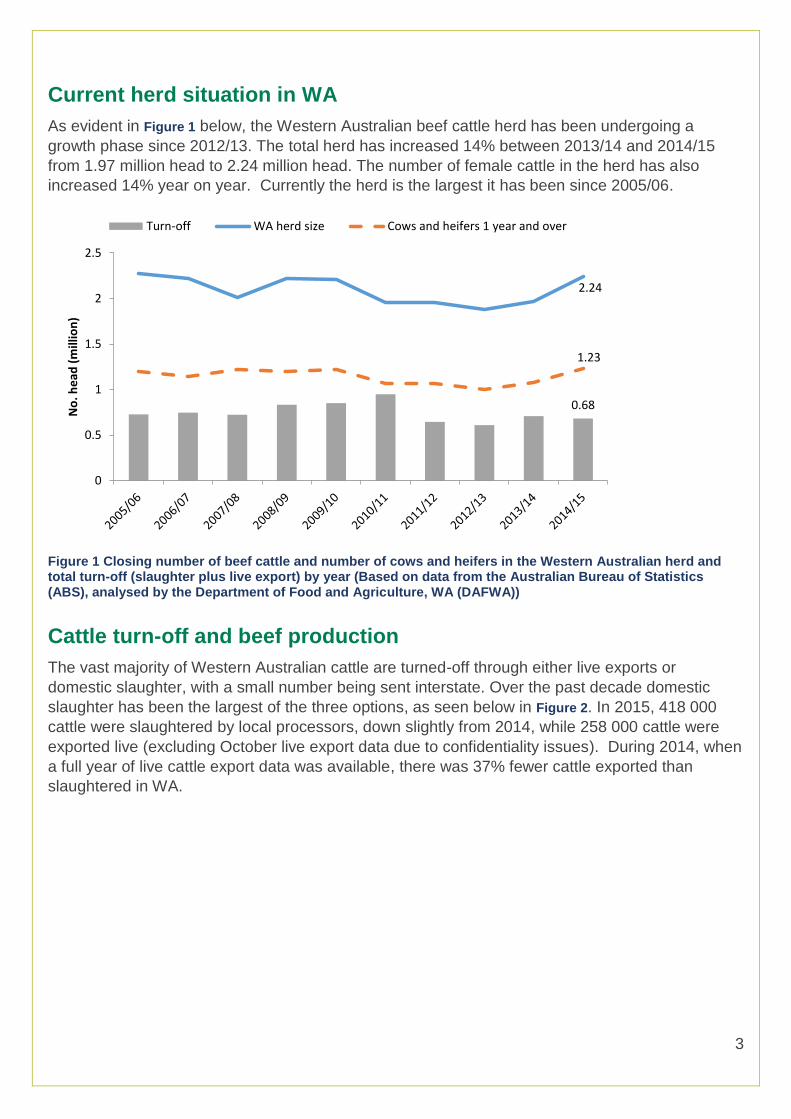

Current herd situation in WA

As evident in Figure 1 below, the Western Australian beef cattle herd has been undergoing a

growth phase since 2012/13. The total herd has increased 14% between 2013/14 and 2014/15

from 1.97 million head to 2.24 million head. The number of female cattle in the herd has also

increased 14% year on year. Currently the herd is the largest it has been since 2005/06.

Figure 1 Closing number of beef cattle and number of cows and heifers in the Western Australian herd and total turn-off (slaughter plus live export) by year (Based on data from the Australian Bureau of Statistics (ABS), analysed by the Department of Food and Agriculture, WA (DAFWA))

Cattle turn-off and beef production

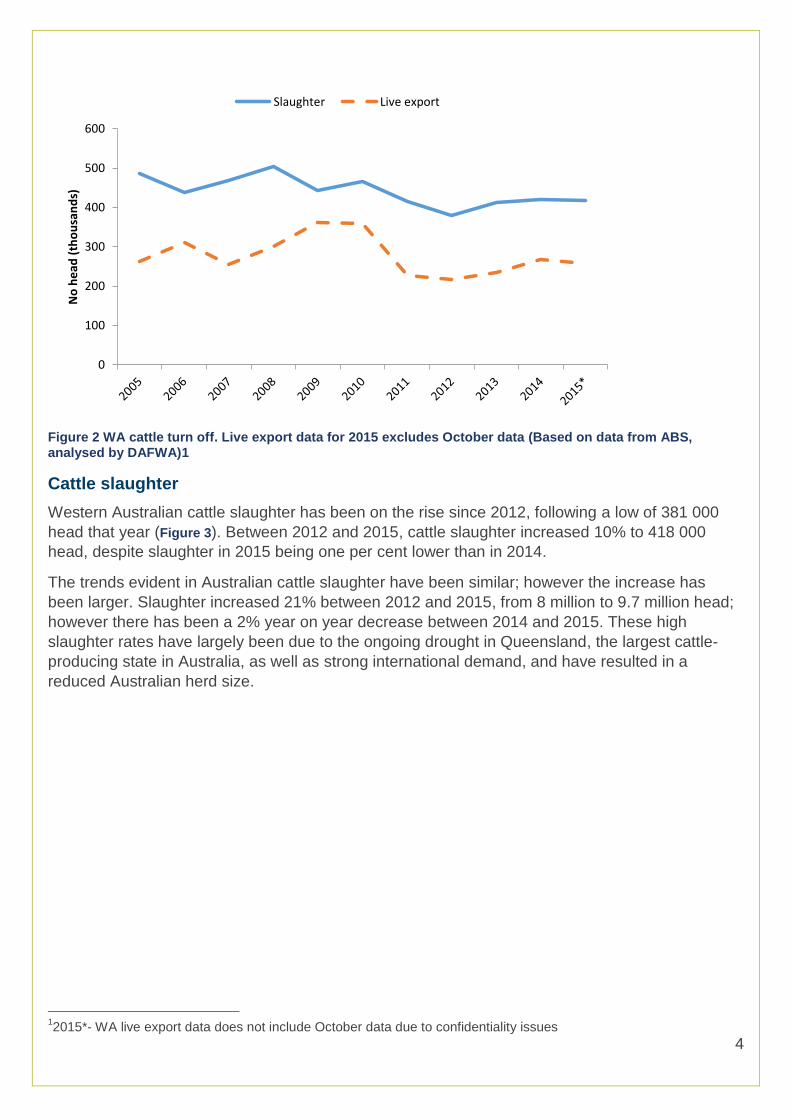

The vast majority of Western Australian cattle are turned-off through either live exports or

domestic slaughter, with a small number being sent interstate. Over the past decade domestic

slaughter has been the largest of the three options, as seen below in Figure 2. In 2015, 418 000

cattle were slaughtered by local processors, down slightly from 2014, while 258 000 cattle were

exported live (excluding October live export data due to confidentiality issues). During 2014, when

a full year of live cattle export data was available, there was 37% fewer cattle exported than

slaughtered in WA.

0.68

2.24

1.23

0

0.5

1

1.5

2

2.5

No

. he

ad (

mill

ion

)

Turn-off WA herd size Cows and heifers 1 year and over

4

Figure 2 WA cattle turn off. Live export data for 2015 excludes October data (Based on data from ABS, analysed by DAFWA)1

Cattle slaughter

Western Australian cattle slaughter has been on the rise since 2012, following a low of 381 000

head that year (Figure 3). Between 2012 and 2015, cattle slaughter increased 10% to 418 000

head, despite slaughter in 2015 being one per cent lower than in 2014.

The trends evident in Australian cattle slaughter have been similar; however the increase has

been larger. Slaughter increased 21% between 2012 and 2015, from 8 million to 9.7 million head;

however there has been a 2% year on year decrease between 2014 and 2015. These high

slaughter rates have largely been due to the ongoing drought in Queensland, the largest cattle-

producing state in Australia, as well as strong international demand, and have resulted in a

reduced Australian herd size.

12015*- WA live export data does not include October data due to confidentiality issues

0

100

200

300

400

500

600

No

he

ad (

tho

usa

nd

s)

Slaughter Live export

5

Figure 3 Annual cattle slaughter for Australia (Left Hand Side (LHS)) and WA (Right Hand Side (RHS)) excluding calves (Based on data from ABS, analysed by DAFWA)

Prior to 2012, a much larger proportion of cows and heifers were slaughtered in WA compared to

bulls, bullocks and steers. However, as demonstrated in Figure 4 below, the numbers began to

converge in recent years. In 2014 the situation was reversed when slightly more male cattle were

slaughtered than female cattle (211 000 males and 209 000 females). This difference edged

higher during 2015, with 2% more male cattle slaughtered than females (210 000 compared to

205 000). The 33% fall in the number of female cattle slaughtered between 2010 and 2015 is likely

contributing to the expansion of the WA herd.

Figure 4 WA cattle slaughter by animal type (Based on data from ABS, analysed by DAFWA)

0

100

200

300

400

500

600

0

2000

4000

6000

8000

10000

12000

WA

cat

tle

an

d c

alf

slau

ghte

r (h

ead

)

Au

stra

lian

cat

tle

an

d c

alf

slau

ghte

r (h

ead

)

AU WA

0

50

100

150

200

250

300

350

Nu

mb

er

of

anim

als

slau

ghte

red

(h

ead

)

Bulls, bullocks & steers Cows & heifers

6

Beef production

As seen below in Figure 5, the volume of beef produced follows the same pattern as seen for

slaughter in Figure 3. Between 2010 and 2012, the volume of beef produced in WA fell by 17%,

from 118 million kilograms to 99 million kilograms. Since 2012, the volume of beef produced has

increased to 108 million kilograms, an increase of 10%, but is yet to reach the volumes reported

prior to 2010.

Figure 5 Volume of beef produced (million kilogram carcase equivalent weight) by Australia (LHS) and WA (RHS) (Based on data from ABS, analysed by DAFWA)

The majority of WA beef is consumed on the domestic market as seen in Figure 6 (domestic

consumption is estimated as total production minus export volume); however the proportion of

beef exported has been increasing in recent years. Between 2012 and 2015, the proportion of

beef exported has increased from 25% to 40%. When beef production was low in 2012, the

proportion of beef consumed on the domestic market was at its highest due to a limited capacity to

service overseas markets. However in recent years, due to heightened global demand, the

proportion of beef exported has increased.

0

20

40

60

80

100

120

140

0

500

1000

1500

2000

2500

3000

WA

be

ef

pro

du

ctio

n (

mill

ion

kg

ceq

)

Au

stra

lian

be

ef

pro

du

ctio

n (

mill

ion

kg

ceq

)

AU WA

7

Figure 6 Western Australian beef consumption by market (Based on ABS data, analysed by DAFWA)

Boxed beef exports

Volume

The volume of beef exported from WA fell from 47 million kilograms (carcase equivalents (ceq)) in

2008 to 25 million kilograms (ceq) in 2012; however between 2012 and 2015 WA beef exports

have increased 72% to 43 million kilograms (ceq). The volume exported in 2015 was just 9% less

than the highest volume exported over the last decade, recorded in 2008.

Beef exports from Australia as a whole prior to 2012 were relatively stable; however since then

exports have been rapidly increasing. Between 2012 and 2015 beef exports increased 31% from

1.47 billion kilograms (ceq) to 1.93 billion kilograms (ceq). This increase was partly due to the

opening up of markets such as China, Malaysia and Vietnam and the sell-down of the herd due to

sustained dry periods in Queensland and New South Wales.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

export

domestic

8

Figure 7 Volume of beef exported (million kilograms carcase equivalent weight) by Australia (LHS) and WA (RHS) (Based on ABS data, DAFWA analysis)

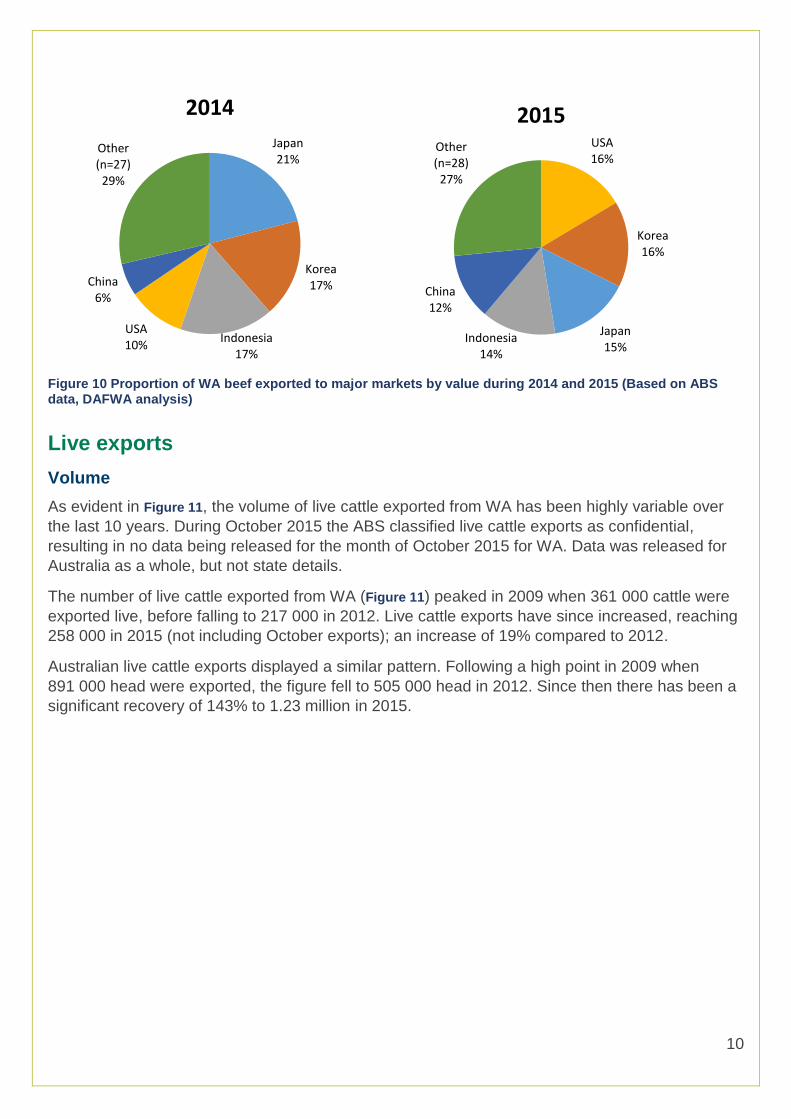

During 2014 the largest market by volume for WA beef was Japan, which accounted for 27% of all

beef exported (Figure 8). During 2015 however, the Japanese market only accounted for 16% of

WA beef exports.

China, which imported just 6% of beef exports in 2014, doubled its share to 12% in 2015 and the

USA increased its beef imports from 8% of WA exports in 2014 to 15% in 2015.

Figure 8 Proportion of WA beef exported to major markets by volume (ceq) during 2014 and 2015 (Based on ABS data, DAFWA analysis)

Value

The value of WA beef exports, while displaying a trend similar to that of volume, has been even

more dramatic. As seen below in Figure 9, the value of WA beef exports hit a low point in 2012 of

0

5

10

15

20

25

30

35

40

45

50

0

500

1000

1500

2000

2500

Vo

lum

e o

f W

A b

ee

f e

xpo

rts

(mill

ion

kg

ceq

)

Vo

lum

e o

f A

ust

ralia

n b

ee

f e

xpo

rts

(mill

ion

kg

ceq

) AU WA

Japan 27%

Indonesia 17%

Korea 17%

USA 8%

China 6%

Other (n=27)

25%

2014 Korea 18%

Japan 16%

USA 15%

Indonesia 15%

China 12%

Other (n=28)

24%

2015

9

$68 million, but has since increased 170% to $184 million in 2015. This is the highest beef export

value reached to date.

There has been a similar increase in that timeframe in the value of Australian beef exports. In

2012 the value of Australian beef exports was $4.8 billion, but that figure has risen 96% to $9.3

billion in 2015. This also, is the highest beef export value achieved in history.

Figure 9 Value (A$ million) of beef exported from Australia (LHS) and WA (RHS) (Based on ABS data, DAFWA analysis)

Due to the different cuts preferred by individual countries, the proportion of value attributed to

international markets can be different to that attributed to them based on volume.

In 2014 the largest market by value for WA beef was Japan which accounted for 21% of the value

of WA beef exports. This was followed by Korea and Indonesia with 17% each, the USA with 10%

and China with 6%. In 2015 the USA became the largest market by value for WA beef, accounting

for 16% of the value of WA beef exports, just slightly higher than Korea which also took 16%.

Japan slipped back to third largest market accounting for 15% of the value of WA beef exports,

Indonesia fell to 14% and China grew to 12%.

0

20

40

60

80

100

120

140

160

180

200

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

WA

be

ef

exp

ort

val

ue

(A

$ m

illio

n)

Au

stra

lian

be

ef

exp

ort

val

ue

(A

$ m

illio

n)

AU WA

10

Figure 10 Proportion of WA beef exported to major markets by value during 2014 and 2015 (Based on ABS data, DAFWA analysis)

Live exports

Volume

As evident in Figure 11, the volume of live cattle exported from WA has been highly variable over

the last 10 years. During October 2015 the ABS classified live cattle exports as confidential,

resulting in no data being released for the month of October 2015 for WA. Data was released for

Australia as a whole, but not state details.

The number of live cattle exported from WA (Figure 11) peaked in 2009 when 361 000 cattle were

exported live, before falling to 217 000 in 2012. Live cattle exports have since increased, reaching

258 000 in 2015 (not including October exports); an increase of 19% compared to 2012.

Australian live cattle exports displayed a similar pattern. Following a high point in 2009 when

891 000 head were exported, the figure fell to 505 000 head in 2012. Since then there has been a

significant recovery of 143% to 1.23 million in 2015.

Japan 21%

Korea 17%

Indonesia 17%

USA 10%

China 6%

Other (n=27)

29%

2014

USA 16%

Korea 16%

Japan 15%

Indonesia 14%

China 12%

Other (n=28)

27%

2015

11

Figure 11 Number of cattle exported live from Australia (LHS) and WA (RHS) (Based on ABS data, DAFWA analysis) 2

During 2014 the largest market for WA’s live cattle exports was Indonesia, accounting for 43% of

cattle, followed by Israel with 27%, Malaysia with 11%, Egypt with 9% and Vietnam with 4%.

During 2015 (October exports excluded), while the destinations were the same, the proportion of

live cattle exported to each market changed dramatically. The proportion of cattle exported to

Vietnam increased from 4% in 2014 to 28% in 2015, making it the largest market by volume for

WA live cattle exports. Live cattle exports to Indonesia fell from 43% to 26%, Israel fell to 22%,

Malaysia remained at 11% and Egypt took 7% of WA’s live cattle exports (Figure 12).

Figure 12 Proportion of cattle exported live to major markets from WA by volume in 2014 and 2015* (Based on ABS data, DAFWA analysis)2

2 2015* -WA data does not include October exports due to confidentiality issues.

0

50

100

150

200

250

300

350

400

0

200

400

600

800

1000

1200

1400

Nu

mb

er

of

WA

live

exp

ort

s (t

ho

usa

nd

he

ad)

Nu

mb

er

of

Au

sltr

alia

n li

ve e

xpo

rts

(th

ou

san

d

he

ad)

AU WA

Indonesia 43%

Israel 27%

Malaysia 11%

Egypt 9%

Vietnam 4%

Other (n=6)

6%

2014

Vietnam 28%

Indonesia 26%

Israel 22%

Malaysia 11%

Egypt 7%

Other (n=7)

6%

2015*

12

Value

The value of WA live cattle exports has also been quite variable over the last decade, as seen

below in Figure 13.

In 2010 WA live cattle exports were worth $233.1 million before falling to $154.2 million in 2012.

Since then, it recovered to $253.3 million in 2015, up 64% from 2012 and the highest value

reached over the last decade, despite October data not being included.

The value of Australian live cattle exports reached $551.5 million in 2009 before falling to $353

million in 2012. Since then there has been significant recovery, with the value of live cattle exports

reaching $994.1 million in 2014 and $1.2 billion in 2015, an increase of 249% since 2012.

Figure 13 Value (A$ million) of cattle exported live from Australia (LHS) and WA (RHS) (Based on ABS data, DAFWA analysis)2

In 2014, the largest market by value for live cattle exports from WA was Indonesia which

accounted for 44% of the total value of live cattle exports. This was followed by Israel worth 26%,

Malaysia valued at 11%, Egypt worth 8% and Vietnam at 4%.

During 2015 (October data excluded), the largest market by value was Vietnam which accounted

for 29% of the value of live cattle exported from WA, as seen in Figure 14. The second largest

market by value was Israel with 24%, followed by Indonesia with 23%, Malaysia with 12% and

Egypt with 7%.

-

50

100

150

200

250

300

-

200

400

600

800

1,000

1,200

1,400

Val

ue

of

WA

live

exp

ort

s (A

$ m

illio

n)

Val

ue

of

Au

stra

lian

live

exp

ort

s (A

$ m

illio

n)

AU WA

13

Figure 14 Proportion of WA cattle exported live to major markets by value in 2014 and 2015 (Based on ABS data, DAFWA analysis)2

Market indicators

Between January and July 2016, cattle market indicators across the board in WA have been very

strong.

As seen below in Figure 15, the WA feeder yearling saleyard indicator has been well above that

reported for the corresponding months in the previous three years and the prices quoted have

been 10% to 21% higher than the corresponding months in 2015, which was also a well-priced

year. As of July 2016, the feeder yearling indicator was 329c/kg compared to 289c/kg at the same

time in 2015.

Figure 15 Trend in WA feeder yearling saleyard indicator (c/kg liveweight) (Based on data from MLA/NLRS, analysed by DAFWA)

Indonesia 44%

Israel 26%

Malaysia 11%

Egypt 8%

Vietnam 4%

Other (n=6)

7%

2014 Vietnam

29%

Israel 24%

Indonesia 23%

Malaysia 12%

Egypt 7%

Other (n=7)

5%

2015*

0

50

100

150

200

250

300

350

2013

2014

2015

2016

14

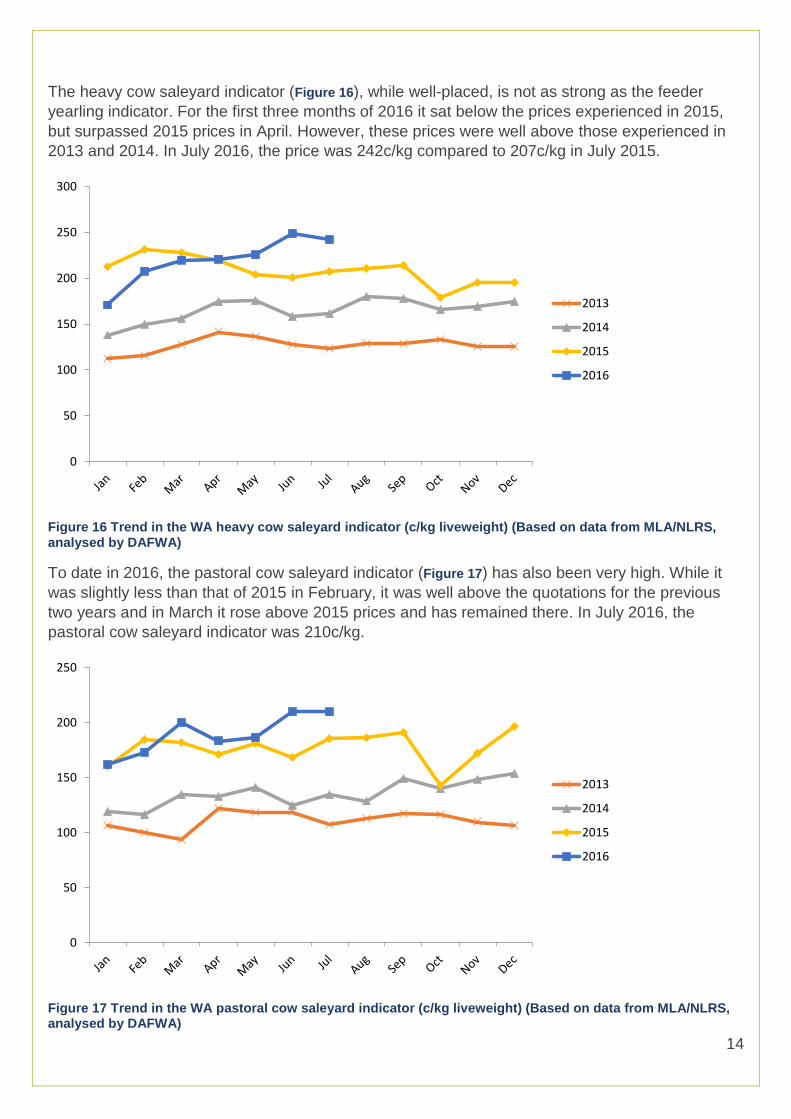

The heavy cow saleyard indicator (Figure 16), while well-placed, is not as strong as the feeder

yearling indicator. For the first three months of 2016 it sat below the prices experienced in 2015,

but surpassed 2015 prices in April. However, these prices were well above those experienced in

2013 and 2014. In July 2016, the price was 242c/kg compared to 207c/kg in July 2015.

Figure 16 Trend in the WA heavy cow saleyard indicator (c/kg liveweight) (Based on data from MLA/NLRS, analysed by DAFWA)

To date in 2016, the pastoral cow saleyard indicator (Figure 17) has also been very high. While it

was slightly less than that of 2015 in February, it was well above the quotations for the previous

two years and in March it rose above 2015 prices and has remained there. In July 2016, the

pastoral cow saleyard indicator was 210c/kg.

Figure 17 Trend in the WA pastoral cow saleyard indicator (c/kg liveweight) (Based on data from MLA/NLRS, analysed by DAFWA)

0

50

100

150

200

250

300

2013

2014

2015

2016

0

50

100

150

200

250

2013

2014

2015

2016

15

The light bull saleyard indicator (Figure 18) has been well above the prices experienced during the

previous three years and has been between 11% and 40% stronger than the corresponding times

in 2015. In July, the light bull saleyard indicator was averaging 307c/kg.

Figure 18 Trend in the WA light bull saleyard indicator (c/kg liveweight) (Based on data from MLA/NLRS, analysed by DAFWA)

Competitor analysis - New Zealand

The New Zealand cattle industry is comprised of beef cattle and a large dairy cattle component.

The total cattle population in New Zealand during 2015 was 10 million head, down from 10.4

million in 2014, as seen in Figure 19. This consisted of 3.5 million beef cattle and 6.5 million dairy

cattle (Statistics New Zealand).

Due to recent growth in the New Zealand dairy industry, which has caused displacement of beef

cattle and other animals, there has been a downward trend in the number of beef cattle. The

proportion of dairy cattle has grown from 53% in 2005 to 65% in 2015, as illustrated in Figure 19

(Statistics New Zealand).

0

50

100

150

200

250

300

350

2013

2014

2015

2016

16

Figure 19 Total cattle population of New Zealand (Based on Statistics New Zealand data, DAFWA analysis)

New Zealand beef production generally peaks during late autumn or early winter when dry

conditions and low feed availability cause producers to sell down. Calf slaughter generally occurs

in August and September when the dairy herds are calving (MLA). Around 70% of beef is

produced in the North Island, as seen in Figure 20.

New Zealand has a relatively small beef industry compared to Australia. In 2015, New Zealand’s

beef production totalled 656 million kilograms of beef compared to Australia’s 2547 million

kilograms. Despite this, New Zealand is a major international competitor, exporting about 95% of

production (MLA). Between 2013 and 2015, beef production increased 11% from 589 million

kilograms to 656 million kilograms, due in part to the growth of the dairy sector as excess animals

were turned off for meat (Figure 20).

0

2

4

6

8

10

12

No

he

ad (

mill

ion

)

Beef cattle Dairy cattle

17

Figure 20 New Zealand beef production (million kilograms cwt) (Based on data from MLA, DAFWA analysis)

Most of the beef exported from New Zealand is manufacturing beef from cull cows, a by-product of

the dairy industry. The largest export destination by volume is North America which took over 150

million kilograms during 2014/15, followed by North Asia which took over 60 million kilograms.

North Asia is a quickly-growing market and so far in 2015/16 has grown to 80 million kilograms,

due largely to growth in the Chinese market (Beef & Lamb NZ).

Market analysis - Korea

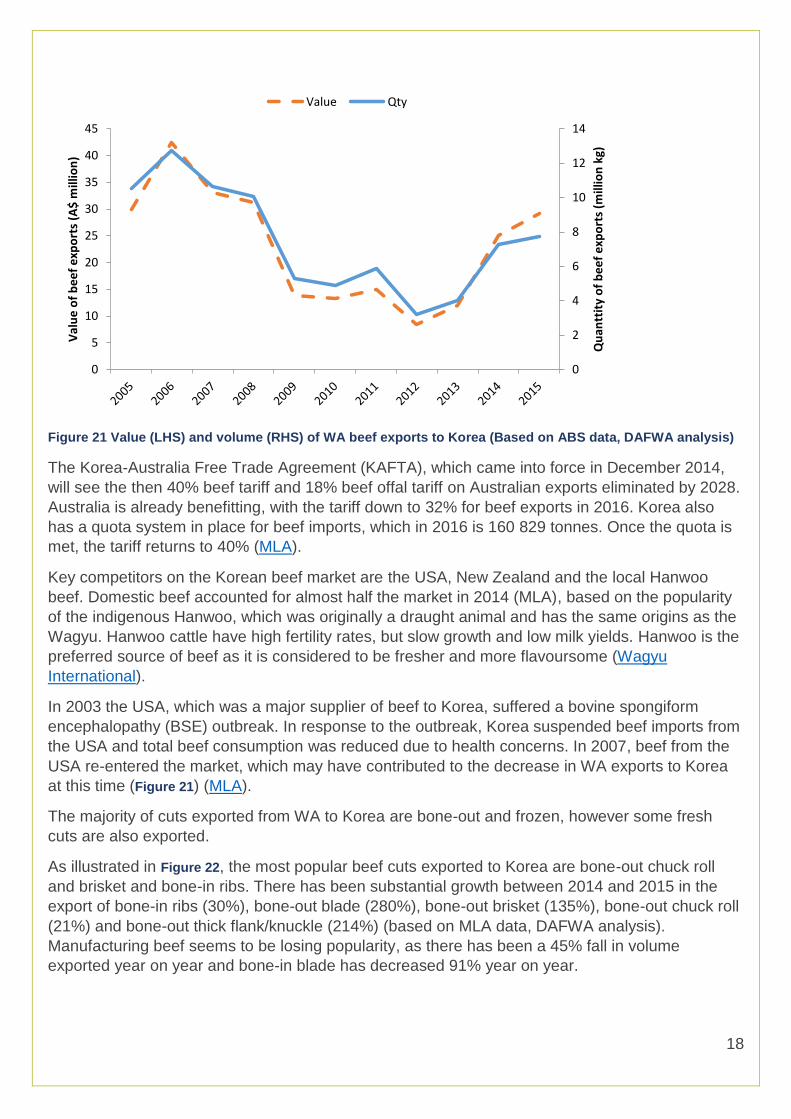

In 2015 Korea was Western Australia’s largest market for boxed beef by volume, accounting for

18% of the market or 7.8 million kilograms, an increase of 7% year on year (Figure 8). Korea was

the second largest market in value terms, worth $29.2 million during 2015, an increase of 17%

year on year (Figure 10).

Between 2012 and 2015 there has been remarkable growth in beef exports to Korea, both in value

and volume, as seen below in Figure 21. In that period there has been a 141% increase in volume

from 3.2 million kilograms to 7.8 million kilograms, and a 244% increase in value from $8.5 million

to $29.2 million.

0

100

200

300

400

500

600

700

Be

ef

pro

du

ctio

n (

mill

ion

kilo

gram

s cw

t)

South Island North Island

18

Figure 21 Value (LHS) and volume (RHS) of WA beef exports to Korea (Based on ABS data, DAFWA analysis)

The Korea-Australia Free Trade Agreement (KAFTA), which came into force in December 2014,

will see the then 40% beef tariff and 18% beef offal tariff on Australian exports eliminated by 2028.

Australia is already benefitting, with the tariff down to 32% for beef exports in 2016. Korea also

has a quota system in place for beef imports, which in 2016 is 160 829 tonnes. Once the quota is

met, the tariff returns to 40% (MLA).

Key competitors on the Korean beef market are the USA, New Zealand and the local Hanwoo

beef. Domestic beef accounted for almost half the market in 2014 (MLA), based on the popularity

of the indigenous Hanwoo, which was originally a draught animal and has the same origins as the

Wagyu. Hanwoo cattle have high fertility rates, but slow growth and low milk yields. Hanwoo is the

preferred source of beef as it is considered to be fresher and more flavoursome (Wagyu

International).

In 2003 the USA, which was a major supplier of beef to Korea, suffered a bovine spongiform

encephalopathy (BSE) outbreak. In response to the outbreak, Korea suspended beef imports from

the USA and total beef consumption was reduced due to health concerns. In 2007, beef from the

USA re-entered the market, which may have contributed to the decrease in WA exports to Korea

at this time (Figure 21) (MLA).

The majority of cuts exported from WA to Korea are bone-out and frozen, however some fresh

cuts are also exported.

As illustrated in Figure 22, the most popular beef cuts exported to Korea are bone-out chuck roll

and brisket and bone-in ribs. There has been substantial growth between 2014 and 2015 in the

export of bone-in ribs (30%), bone-out blade (280%), bone-out brisket (135%), bone-out chuck roll

(21%) and bone-out thick flank/knuckle (214%) (based on MLA data, DAFWA analysis).

Manufacturing beef seems to be losing popularity, as there has been a 45% fall in volume

exported year on year and bone-in blade has decreased 91% year on year.

0

2

4

6

8

10

12

14

0

5

10

15

20

25

30

35

40

45

Qu

antt

ity

of

be

ef

exp

ort

s (m

illio

n k

g)

Val

ue

of

be

ef

exp

ort

s (A

$ m

illio

n)

Value Qty

19

Figure 22 Major meat cuts exported from WA to Korea (Based on MLA data, DAFWA analysis)

In 2015 the Korean population was estimated to be approximately 50 million and beef

consumption was approximately 11 kilograms per capita per year (MLA).

The Korean national cattle herd (including dairy cattle) peaked in 2012 at 3.5 million head but was

down to 3 million in March 2016 (Statistics Korea).

The number of Korean cattle farms has been in a state of decline over the last 30 years. About

17% of the national cattle herd comes from cattle farms that have less than 20 head, and these

small farms comprise more than 65% of cattle farms in Korea. The proportion of larger farms has

been increasing over recent years and as of 2014, a third of cattle were contained on farms with

over 100 head (MLA).

Weather watch

In Western Australia, and Australia as a whole, the period from November 2015 to August 2016

provided a mixed season as far as rainfall was concerned, as seen in Figure 23. Much of the

southern half of WA has experienced a relatively wet first half of 2016, reporting rainfall in deciles

eight and above. The amount of rainfall received between 1 November 2015 and 31 July 2016

was above average or very much above average. This was welcome news as the previous winter

had been very dry in parts, resulting in low stock water levels.

The situation has not been as favourable in the northern parts of the State, with the wettest part of

the year providing average to very much below average rainfall levels. Parts of the Kimberley and

Pilbara reported rainfall deciles between one and three. Conditions in many parts of these regions

led to producers commencing mustering earlier than usual and selling a large number of cattle in

the first trimester of 2016. Significant rainfall in May resulted in useful pasture growth in parts of

the Kimberley and Pilbara, which produced much-needed additional feed. However, lower than

average rainfall may result in a difficult season and excess cattle may come onto markets, either

for live export or come south for slaughter due to a lack of feed availability in the north.

0

100

200

300

400

500

600

700

800

900

Bla

de

Rib

s

Sho

rt R

ibs

Bla

de

Bri

sket

Ch

uck

Ro

ll

Man

ufa

ctu

rin

g

Silv

ers

ide

/Ou

tsid

e

Thic

k Fl

ank/

Kn

uck

le

BONE IN BONE OUT

Be

ef

exp

ort

in t

on

ne

s

2014

2015

20

Over the last nine months, the majority of Queensland and NSW have also received variable

rainfall, varying from very much below average to very much above average in parts. In June the

Eastern States experienced widespread rain. While still drought-declared, the rain has been

welcomed by producers and may lead to the start of herd rebuilding.

Figure 23 Rainfall deciles from November 2015 to August 2016 (Source: The Bureau of Meteorology)

Appendix