westlife development limited - aceanalyser meet/105533_20141107.pdf · • this document or...

TRANSCRIPT

Westlife Development Limited November 2014

1

• This document or presentation has been prepared by, and is proprietary to, Westlife Development Limited and its subsidiary (“The Company”)

• This presentation does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase or subscribe for or otherwise

acquire, any securities in the Company or in the other entities referred to herein or in its or their respective affiliates or associates, nor shall it or any part of it

form the basis of or be relied on to any extent or in any manner in connection with any contract therefore or in relation thereto

• The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice. The

information in this presentation has not been verified by the Company, its advisors or any other person and is subject to updating, revision and amendment.

No representation or warranty, express or implied, has been, is or will be given by the Company, any of its affiliates or any of their respective advisers,

directors, officers, employees, associates or agents, as to the accuracy, reliability or completeness of the information or opinions contained in this

presentation or in any revision of the presentation or of any other written or oral information made or to be made available to any interested party and no

reliance should be placed on them. To the extent permitted by law or regulation, none of them accepts any liability whatsoever for any loss howsoever

arising, directly or indirectly, to any extent and in any manner whatsoever to any person from any use of this presentation nor its contents or any part

thereof have been cleared or approved by any regulatory, statutory or government authority, agency or body located in any country, territory or

jurisdiction and that none of the aforesaid shall be responsible to any extent or in any manner for the same

• Neither this presentation nor any copy of it may be taken, transmitted or distributed, directly or indirectly, into Canada, Australia, Japan, South Africa, the

United Kingdom and the Republic of Ireland or the United States of America, its territories or possession or passed to US persons (as defined in Regulation S of

the United States Securities Act of 1933 (as amended)), United States residents, corporations or other entities or individuals or entities in Japan, Canada, Australia, South Africa, the United Kingdom or the Republic of Ireland, save pursuant to an applicable exemption. Neither this presentation nor any copy of

it may be taken or transmitted into any jurisdiction outside India or distributed to persons with addresses outside India. Distribution on this presentation in the

United States may constitute a violation of United States securities law and the distribution of this presentation in or to persons subject to such other

jurisdictions set out may be restricted by law set out herein may be restricted by law and persons into whose possession this document comes should inform

themselves about, and observe, any such jurisdictions. Any failure to comply with these restrictions may constitute a violation of the laws of the relevant

jurisdiction, attracting penal consequences

• This presentation contains forward-looking statements in the nature of certain operational and financial projections, and those who view or access or come

across this presentation are cautioned that actual results could differ from those in such projections

• All those who view or who otherwise come across or who have otherwise have access to this presentation shall, in consideration of being made aware of

the contents hereof, be irrevocably bound to keep such contents strictly confidential and not disclose them to any extent in any manner to any third party.

• All those who may view or come across or otherwise have access to this presentation shall be irrevocably deemed to have been fully aware of and to

have fully understood and accepted this disclaimer

disclaimer

2

Highest Annual Sales Per Store

Fortune India 2011

Interbrand 2013 World’s 7th most valuable brand

Most Admired Company – Fortune 2014

McDonald’s leads globally

3

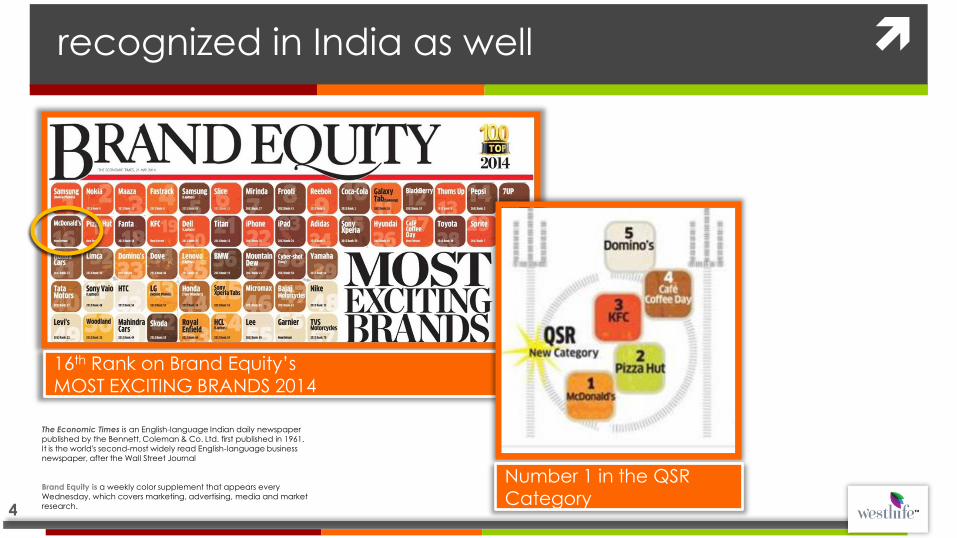

16th Rank on Brand Equity’s MOST EXCITING BRANDS 2014

The Economic Times is an English-language Indian daily newspaper

published by the Bennett, Coleman & Co. Ltd. first published in 1961.

It is the world's second-most widely read English-language business

newspaper, after the Wall Street Journal

Brand Equity is a weekly color supplement that appears every

Wednesday, which covers marketing, advertising, media and market

research.

Number 1 in the QSR Category

recognized in India as well

4

HRPL BACKGROUND :

•Started as a Joint Venture in 1995 •Ownership status changed to DL* in May 2010 •DL develops sites at their own cost and pays

a royalty

MFA# KEY HIGHLIGHTS : •Right to own and operate McDonald’s

restaurants in Western and Southern India until 2030

• HRPL pays royalty and fees to McDonald’s

Corporation

First Restaurant in

Mumbai, 1996

HARDCASTLE RESTAURANTS

PVT. LTD.

(HRPL )

West and South

CONNAUGHT PLAZA

RESTAURANTS PVT. LTD.

(CPRL)

North and East

*DL: Development Licensee A Development Licensee, in the context of McDonald’s, means an entity which is granted franchise rights, by McDonald’s Corporation or its affiliates, to own and operate McDonald’s restaurants, to adopt and use the McDonald’s system to develop and run McDonald’s restaurants in a given area, and to advertise and use the McDonald’s brand name and trademarks for products sold at such restaurants. •Map of India is indicative # MFA : Master Franchise Agreement

5

ownership structure

Westlife Development Ltd

(BSE : 505533)

100% Hardcastle

Restaurants Pvt. Ltd.

FII and Public

38% Promoter

Group

62%

Shareholding Pattern*

*As at Sep 30, 2014

• On 19 July, 2013, Bombay High Court approved a scheme of arrangement making HRPL a direct subsidiary of Westlife Development. Post issuance of shares pursuant to the scheme, the number of shares expanded to ~155 Mio. Also, on July 23rd, the Board of Westlife approved a preferential allotment of ~5.4m equity shares to Arisaig India Fund at an issue price of Rs. 333.05 per share aggregating to Rs. 1.8bn (~US$30m) • Post the Preferential allotment, Arisaig India Fund had ~3.47% stake invested at a valuation of Rs. 50+ Billion. The fund raised would be used for financing the capital expenditure, working capital requirements and general corporate purposes of the Company and its subsidiaries

6

building the eco system 1995-2012

1995-2012

Glocal 1995-96

Building the

FOUNDATION 1997-2003

GROWING the Category

2003-2012

7

building the eco system

glocal: cultural sensitivity

Only country to have

SEPARATE Vegetarian and

Non Vegetarian Kitchens

8

building the eco system

glocal: menu localization

Local tastes like “Aloo Tikki” in a uniquely McDonald’s form

Adapting popular

forms like the

PUFF

McAloo Tikki

Chicken McGrill

Pizza McPuff

9

building the eco system

glocal: building a local supply chain

Developed a

cold chain

Global suppliers with

local production

Creating direct linkage

to the farms

10

Over 95% localization

building the eco system

glocal: developing sustainable unit economics

• Local supply chain for equipment

• Right Sizing Restaurants • Optimizing Kitchen Capacity

• Over 95% of produce locally sourced

• Tax Rationalization • Increased supplier capacity through

3rd party business

2003

1996

2003

-X%

2240 basis points improvement 1X

0.4X

Average Development Cost Restaurant Operating Margins

19

96

* Graphs not to scale, for representational purpose only

11

creating the category Quick Service Restaurants (QSR)

12

creating the category

nascent category in 2003

Eating out was an

occasion

Of the 100 eating

occasions in a month, people were eating

out only 3 times*

‘Housewives’

Our Number 1 competitor

* Source: Brand Track, Mumbai

13

creating the category

driving up the average unit volume

CONVENIENCE For servicing all

occasions

VALUE For driving new

users and

frequency

MENU To provide

modern choices

for all day parts

14

creating the category

value: building block approach

Everyday

Affordability Filling

Affordable

Meals Place

to

refuel

2004 2009 2012

15

creating the category

through new stores and brand extensions

McDelivery Breakfast Kiosk

For all OCCASIONS that

the customer eats out

And for all

DAY PARTS

Across CUSTOMER segments

18

55

130

1996-2003 2004-2008 2009-2012

Store Count

16

creating the category

menu: modern choices with taste that consumers like

Chicken

McNuggets

2010

McFlurry

2011

McEgg

2012 Spice Fest

2012

McSpicy

2011

McAloo Tikki

2004

Breakfast

2009

17

creating the category

we drove the growth in the category

3

7.8

2003 2012

IEO Monthly Frequency, MUMBAI

1x

1.74 x

2003 2012

HRPL Average Volume Growth

Per Annum

(INR Mio)

* Source: Brand Track, Mumbai

IEO : Informal eating Out

18

grow and dominate 2013 onwards

19

changing profile of category

QSR moved

from being an

occasion to a

destination to

refuel

As a Fad As a

status symbol

As a

necessity

2003 2009 2014

20

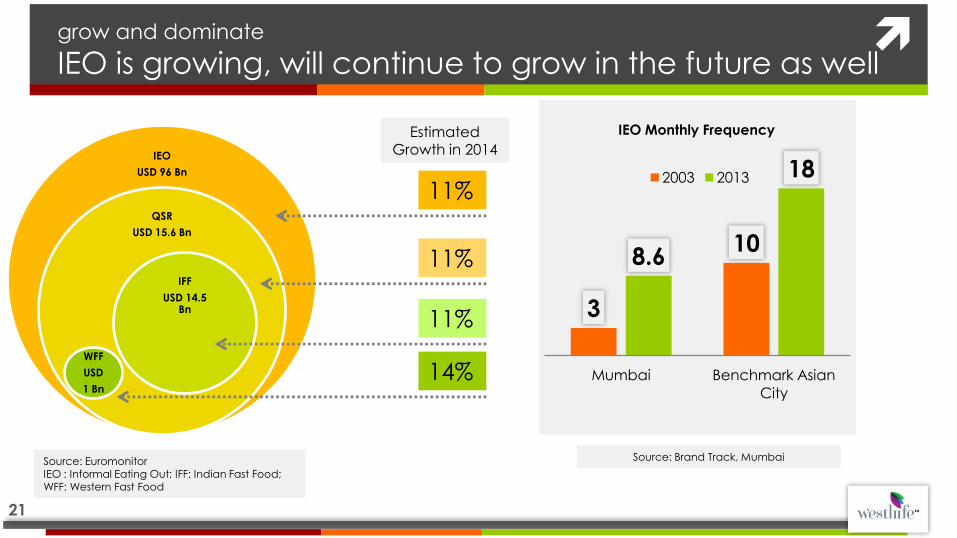

IEO

USD 96 Bn

QSR

USD 15.6 Bn

IFF

USD 14.5 Bn

WFF

USD

1 Bn

11%

11%

11%

14%

Estimated Growth in 2014

grow and dominate

IEO is growing, will continue to grow in the future as well

3

10 8.6

18

Mumbai Benchmark Asian

City

IEO Monthly Frequency

2003 2013

Source: Euromonitor IEO : Informal Eating Out; IFF: Indian Fast Food; WFF: Western Fast Food

Source: Brand Track, Mumbai

21

60% of the population below

the age of 30

Western fast food driven by

Teens and YANKS

Macro factors will drive further growth

1x

1y 1z

1.7x

1.8y 2.8z

IEO IFF WFF

2008 2013

Source: Euromonitor Graph not to scale, for representation purpose only

22 22

levers for growth over the next 5 years

23

levers for growth

1. Broadening Accessibility

3. Margin

Expansion

2. Growing Baseline

Sales

4. Growth through people

24

broadening accessibility

Grow store

footprint

Unit

Economics

25

High Streets

broadening accessibility

grow responsibly

BUILD REAL ESTATE

COMPETITIVE ADVANTAGE

• Balance between quality

real estate and pace

• Portfolio Approach

• Long Term Deals

Includes 2 Franchisee stores As of March 2013

Malls GROW RESPONSIBLY

• Getting the business

model and profit formula

right before scaling

• Keep evolving with

changing cost realities

7

YEA

RS

7 Y

EA

RS

3 Y

EA

RS

18 STORES

69 STORES

74 STORES

1997 - 2003 2004-2010 2011-2013

26

broadening accessibility

building unit economics

Average investment of INR 25-30 Mio

Stores typically need 2-3 years to establish,

depending upon the brand

awareness in the city

Year 3:

Sales: INR 40-50 Mio

Cash ROI: 22% - 25%

1/3 of Key,

Core and Non Core Cities Un-

penetrated

Balance

Potential of

600+ stores

Basis Global Index of an Asian city

1.32 restaurants per 100,000 people

190 Cities untapped in our region, since

current presence in 20 cities

broadening accessibility

improve brand access

Tamil Nadu

12 Stores

Chattisgarh 0 Stores

Madhya Pradesh 3 Stores

Kerala 3 Stores

Gujarat 22 Stores

Telangana 17 Stores

Karnataka 44 Stores

Maharashtra

91 Stores

Significant potential in existing towns

and cities

Most cities and towns significantly

under penetrated

Indicates the number of stores in each state as

of September 2014 29

7 Y

EA

RS

7 Y

EA

RS

3 Y

EA

RS

1997 - 2003 2004-2010 2011-2013

NEX

T 5

YEA

RS

175 – 250 Stores

74 STORES

69 STORES

18 STORES

2014 Onwards

175 - 250 new stores over the next 5 years

30

Years denote fiscal years

growing base line

Value

Menu

Brand

Extensions

31

Making the brand ACCESSIBLE in NEW MARKETS

providing VALUE FOR MONEY, not a price point

Ad

din

g N

EW

USER

S t

o t

he

bra

nd

in

EX

ISTI

NG

ma

rke

ts

32

growing base line

new menu platforms

Platforms that leverage EXISTING

INVESTMENTS and capacity

Providing modern choices to

consumers of today

33

growing base line

brand extensions

Brand extensions will continue to add to the baseline as our

offerings and reach grow

75-150 McCafé's over the next 3-5 years

24/7 McDelivery Service Breakfast Dessert Kiosks 34

re-imaging with brand extensions

Modernize the customer experience through restaurant re-imaging initiatives

Providing contemporary restaurant designs & relevant

experience to our consumers

35

Base Line Value Menu Brand

Extensions

QSC Increased

Base Line

growing base line

through occasions, day parts and customer segments

Graph not to scale, for representation purpose only

36

margin expansion

37

margin expansion

operating leverage

Bulk of the cost incurred for operating In Store

Adding brand extensions helps grow sales, while optimizing assets

Diagram representative, not indicative of size of impact

In-store Business

McCafé

24 Hours

Breakfast McDelivery

Menu Management

Leverage cost

through scale

via effective

supply chain

management

margin expansion

operating leverage

Building block on margin

All levers of the

business model

coming together

EBITDA Gross

Margin

Operating

Leverage

Royalty G&A EBITDA

Graph not to scale, for representation purpose only

39

people

40

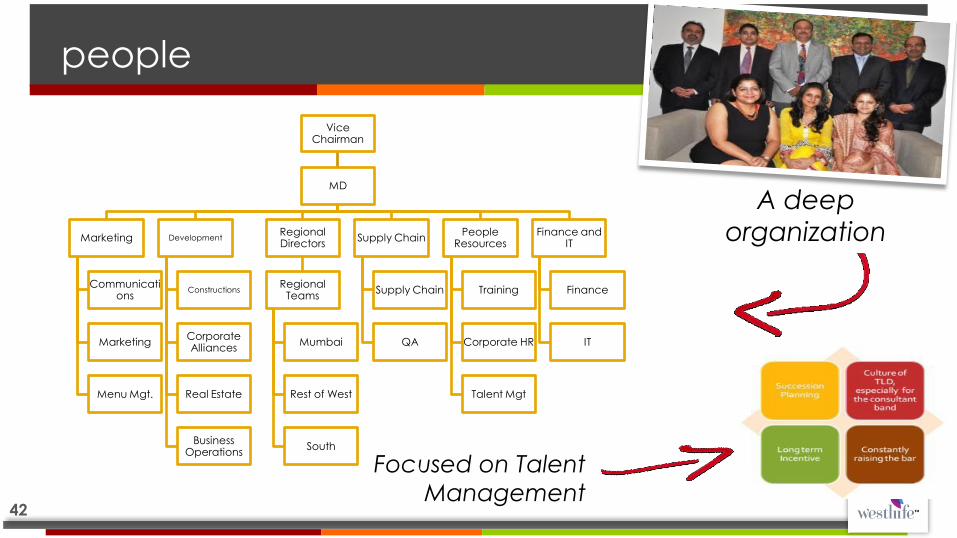

people pipeline

Strong LEADERSHIP TEAM providing

strategic direction backed by an

experienced CROSS

FUNCTIONAL TEAM managing execution

Leadership team

committed to TALENT

MANAGEMENT,

investing over 20

days each year for

building pipeline

Investments in

LEARNING AND

DEVELOPMENT ,

especially in mid

management to

build skills for the

future

Engaging

7500+ people

across 20

cities

41

42

Vice Chairman

MD

Marketing

Communications

Marketing

Menu Mgt.

Development

Constructions

Corporate Alliances

Real Estate

Business Operations

Regional Directors

Regional Teams

Mumbai

Rest of West

South

Supply Chain

Supply Chain

QA

People Resources

Training

Corporate HR

Talent Mgt

Finance and IT

Finance

IT

people

A deep

organization

Focused on Talent

Management

175-250 new stores

in the next 5 years

Growing baseline

Margin Expansion

People

in summary

43

financial summary

44

store growth, sales and comparable sales trends

55 74 87 107 130

161 184

10 20 14 21 24

32 29

-100

-80

-60

-40

-20

0

20

40

0

20

40

60

80

100

120

140

160

180

200

FY08 FY09 FY10 FY11 FY12 FY13 FY14

Total Stores New Stores

1,604 2,104 2,772 3,793

5,445

6,810

7,384

41%

31% 32% 37%

44%

25% 8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

(1,000)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY08 FY09 FY10 FY11 FY12 FY13 FY14

Sales ( INR Mio) Sales Growth %

29% CAGR

45

19% 9% 12%

17% 22%

6%

-6% FY08 FY09 FY10 FY11 FY12 FY13 FY14

Comps%

margin trajectory

46

54.7%

56.0% 56.7%

57.1%

55.6% 55.0%

57.0%

53.5%

54.0%

54.5%

55.0%

55.5%

56.0%

56.5%

57.0%

57.5%

FY08 FY09 FY10 FY11 FY12 FY13 FY14

Gross Margin %

76 52 120 400

672 627 490

4.8% 2.5%

4.4%

10.5% 12.3%

9.2%

6.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-

100

200

300

400

500

600

700

800

FY08 FY09 FY10 FY11 FY12 FY13 FY14

INR Mio

EBITDA EBITDA %

general & administration (G&A)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

FY09 FY10 FY11 FY12 FY13 FY14

G&A Headcount 47

established model for tapping into the

potential

Real Estate

portfolio array

Provides competitive

differentiation

World’s

Largest QSR Brand

Brand connect with the target audience

Favorite Place and way

to eat

48

Indigenous Supply Chain for competitive

advantage

Farm to FORK

thank you

49