westpac and the new financial regulations do we think that basel’s faulty?

Post on 18-Dec-2015

215 views

TRANSCRIPT

Westpac and the new financial regulations

Do we think that Basel’s faulty?

Westpac’s Basel II experienceSlide 2

Contents

• A brief biography – how did I end up running the Basel program?

• A brief description of Westpac – how does it compare to global peers?

• Westpac and Basel II

Westpac’s Basel II experienceSlide 3

My resume

• Law school dropout

• Honours in Pure Maths and Statistics

• UNSW graduate

• 8 years experience in Australian banking industry

• Manage Westpac’s sponsorship of Co-op program

• Responsible for Basel II and Active Portfolio Management

Westpac’s Basel II experienceSlide 4

Why would a quant be interested in Basel II?

• New global financial regulations from 2007

• 3 Pillars

- Regulation, Supervision, Disclosure

• The regulations favour banks with sophisticated credit and operational risk management data, processes and analysis

- ie, all Australian major banks

- APRA requires the Australian majors to be compliant with the most sophisticated approaches for both credit and operational risk

Westpac’s Basel II experienceSlide 5

Economic Capital has been an area of intensive research for the last 8 years

• Current banking regulations are not risk-sensitive

• Basel II permits different methods for measuring credit and operational risk

• If sophisticated methods are used, there is greater alignment between

the capital needed in order to operate

and

the capital needed in order to be allowed to operate

An introduction to Westpac Banking Corporation

Westpac’s Basel II experienceSlide 7

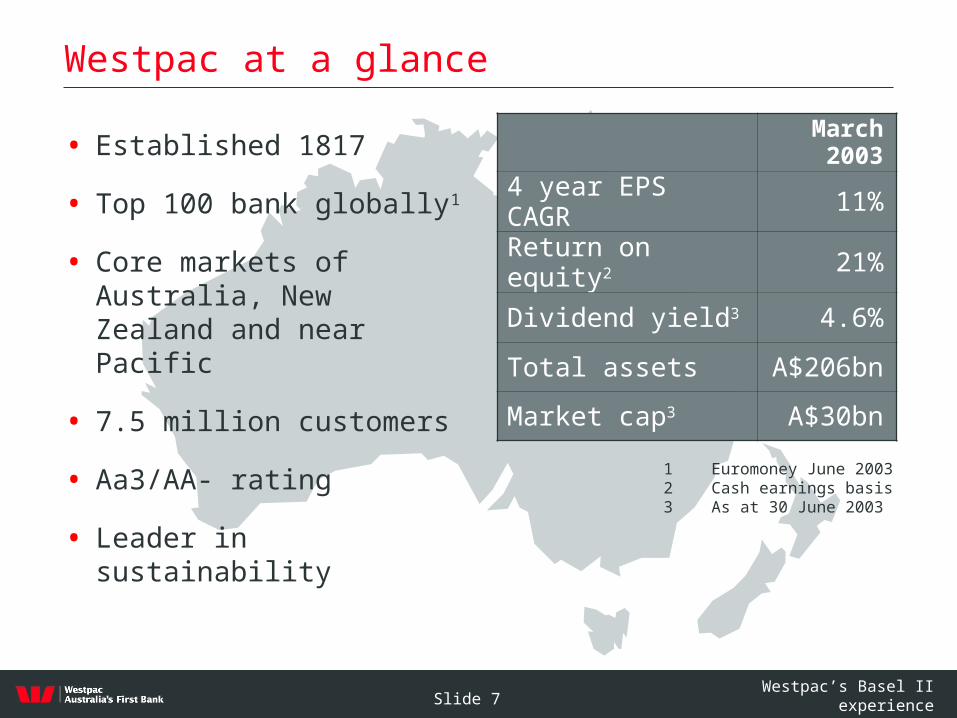

Westpac at a glance

• Established 1817

• Top 100 bank globally1

• Core markets of Australia, New Zealand and near Pacific

• 7.5 million customers

• Aa3/AA- rating

• Leader in sustainability

March 2003

4 year EPS CAGR 11%

Return on equity2 21%

Dividend yield3 4.6%

Total assets A$206bn

Market cap3 A$30bn

1 Euromoney June 20032 Cash earnings basis3 As at 30 June 2003

Westpac’s Basel II experienceSlide 8

Westpac at a glance

Over a period of 5 years total return for Westpac has been in excess of 59%

Westpac operates a full range of traditional banking services with operations focused across Australia, New Zealand and Pacific Region

NPAT by business segment

Net profit after tax Share price performance

Global locations

993

1,0511,018

979

924897

818

755

701

181

500

600

700

800

900

1,000

1,100

1,200

NPAT Significant items

A$m

993

1,0511,018

979

924897

818

755

701

181

500

600

700

800

900

1,000

1,100

1,200

NPAT Significant items

A$m

$6

$8

$10

$12

$14

$16

$18

31/0

3/98

30/0

9/98

31/0

3/99

30/0

9/99

31/0

3/00

30/0

9/00

31/0

3/01

30/0

9/01

31/0

3/02

30/0

9/02

31/0

3/03

All business segments contributed to the 1H03 result with Business & Consumer Banking providing the largest contribution

Westpac has 24 hour global coverage, with offices in Australia, New Zealand, New York and London

New YorkLondon

Sydney

Wellington

Business & Consumer Banking

56%Institutional

Bank20%

NZ Retail16%

Wealth8%

Westpac’s Basel II experienceSlide 9

Consistent shareholder return

100

150

200

250

300

Com

mon

wea

lth B

ank

of A

ustr

alia

Uni

Cre

dito

Ital

iano

Wes

tpac

Ban

king

Cor

pora

tion

The

Dex

ia G

roup

Dan

ske

Ban

k

BN

P P

arib

as

Am

erci

an In

tern

atio

nal G

roup

Citi

grou

p

Fift

h T

hird

Ban

corp

Sw

iss

Rei

nsur

ance

Com

pany

Nor

ther

n T

rust

Cor

p

Aus

tral

ian

and

New

Zea

land

Ban

king

Gro

up L

imite

d

Mar

sh a

nd M

cLen

nan

Com

pani

es In

c

The

Roy

al B

ank

of S

cotla

nd

Cap

ital O

ne F

inan

cial

Cor

pora

tion

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Oliver, Wyman & Company global Shareholder Performance Index1 (SPITM) - 2002

1 Shareholder Performance Index – annual benchmark for volatility-adjusted shareholder value performance amongst the largest financial institutions in the world.

Westpac’s Basel II experienceSlide 10

Leader in sustainability – gaining recognition

2003 Social Impact Report1 Reporting on Westpac’s corporate responsibility policies, practices and performance

1 Available at www.westpac.com.au under ‘Westpac Info’, then ‘Social accountability’

• Ranked number one in the global banking sector by the Dow JonesSustainabilityIndex

• Ranked third globally in the banking sector by oekom Corporate Responsibility Rating

• United Nations Association of Australia Triple Bottom Line Award 2002

Westpac’s Basel II experience

What are the two most important things to know?

Westpac’s Basel II experienceSlide 12

Number 1… Basel is a long way away

Westpac’s Basel II experienceSlide 13

Number 2… Basel II is very good news

• Good for APRA

• Good for Australian banks

• Good for investors and those who analyse Australian banks

• Despite the challenges…

• Basel II is good for Westpac

Westpac’s Basel II experienceSlide 14

Basel II is good for APRA

• Provides deeper insight into bank risk management

• Gives greater comfort in the robustness of risk management practices in Australia

• Compliance simplifies operational risk management practices

• APRA has provided significant input to the Accord

Westpac’s Basel II experienceSlide 15

Basel II shows Australian banks to be safe

• APRA expects the 4 Australian majors to comply with the most sophisticated models

• International peer analysis shows Australian bank risk-adjusted assets to decrease by more than any other jurisdiction

- APRA expects “moderate” capital relief for the 4 majors and “modest” relief for regional banks

• Differences are attributable to:

- balance sheet structure

- different risk profiles

Westpac’s Basel II experienceSlide 16

Eq

uit

y in

vest

ors

/an

alys

ts

Basel II is good for bank stakeholders

Consistent disclosure

More finely honed modelling assessing relative risk

between issuers

Global comparability

Greater rigour of balance sheet analysis

Better understanding ofrisk / reward

Fundamental value

Deb

t investo

rs&

R

ating

Ag

encies

Westpac’s Basel II experienceSlide 17

Increased transparency

Reduced ‘Black Box’

Today Pillar 3

Ris

ks

Basel II reduces the perceived ‘black box’ component of a bank’s business

Disclosed risks

Undisclosed risks

Disclosed risks

Undisclosed risks

Westpac’s Basel II experienceSlide 18

Westpac disclosed its Basel II results early

Westpac’s Basel II experienceSlide 19

….which is starting to pay dividends

• Equity investors:

- Preliminary results support relative improvement in P/E’s of Australian Banks

- Tangible evidence of lower risk profile of Westpac

- Equity investors starting to engage on Basel II

• Debt investors:

- Australian issuers already starting to see price differential in offshore capital markets

- Greater data granularity will lead to refinement of pricing decisions (measured in bps)

Westpac’s Basel II experienceSlide 20

Basel II compliance hurdles can be overcome

• Making credit data accessible is time consuming

• Discretion needed to avoid disrupting the Australian Securitisation Industry

• Proposing an objective way to make LGD’s conservative

• Suggestions that a significant pro-cyclicality capital buffer be required – not supported by Westpac stress testing

Westpac’s Basel II experienceSlide 21

Conservative LGDs – part of pillar 1

“… it is important that banks utilise default-weighted averages… in computing loss severity estimates. Moreover, for exposures for which LGD estimates are volatile over the economic cycle, the bank must use LGD estimates that are appropriate for an economic downturn if those are more conservative than the long-run average” – Para 430

• US and UK regulators have not provided clear guidance on what this means

Westpac’s Basel II experienceSlide 22

Westpac’s LGDs are both conservative and compliant

LGD by year of default

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Mea

n L

GD

Benchmark LGDs Definition of Default

Basel II

WBC QIS3

Raw LGDNo costs1

No discounting 28 41

LGD with costs1

Cost estimates includesNo discounting 36 51

LGD with costs1 and discountingCost estimates includedDiscounting at cost of equity 64

100 (benchmark)

WBC submission in QIS 3 study WBC actual LGD

1Costs include legal fees and other workout costs

Westpac’s Basel II experienceSlide 23

Why not discount at the cost of equity?

• Basel II implementation should not get any more complicated

• US and UK proposals for conservative LGDs introduce subjectivity where none need exist

• The 4 major Australian banks report very similar costs of equity so LGDs will be readily comparable between peers

Westpac’s Basel II experienceSlide 24

Credit stress tests are becoming an increasingly important part of the Accord

“…the bank must perform a credit risk stress test to assess the effect of certain specific conditions on its IRB regulatory capital requirements. …. The bank’s stress test in this context should, however, consider at least the effect of mild recession scenarios. In this case, one example might be to use two consecutive quarters of zero growth to assess the effect on the bank’s PDs, LGDs, and EAD, taking account – on a conservative basis – of the bank’s international diversification” - Para 397

“… the bank must include a consideration of….. the ratings migration of at least some of its exposures” - Para 398

Westpac’s Basel II experienceSlide 25

Basel II is good for Westpac

• Westpac has been working on Basel compliance for three years

• Early results support the hypothesis that we were “safer” than previously perceived

• Deeper analysis with each iteration of the Accord - yet to find evidence to contradict this assertion

• Feedback from stakeholders has been positive

Westpac’s Basel II experienceSlide 26

And isn’t that good news!