wfp response to the food and financial crises€¦ · wfp: 2/3 of 56 countries: cost food basket:...

TRANSCRIPT

McGill Conference on Global Food Security

5-7 October 2009

Henk-Jan Brinkman,Senior Adviser for Economic Policy

WFP Response to the Food and Financial Crises

Key messages

Global financial and economic crisis has worsened the effect of high food prices

The impact of these crises is long-term

Green economic shoots, but no social ones

Need for urgent and comprehensive response

Food access compromised long-term impact

Food access = f (prices, incomes)High food prices pricesGlobal financial crisis incomes

Vulnerability at household level:High % of income spend on foodBuy more food than sell (net-buyer)High % of income from exportsHigh % of income from remittancesFew coping mechanisms

Food prices soared and fell but stay high

Food prices high at local level

FAO:

WFP: 2/3 of 56 countries: Cost food basket: > 20% above 5-year average

Wheat price ($/MT)

Prices up coping

Live

lihoo

d Diversify incomes

Spend less on non-essentials Selling some assets

Drop out of school Migration

Child labor Borrow

Selling of produc-tive assets

Selling of all assets

Spend less on essential items

Hea

lth

thre

aten

ing

activ

ities

Food

/Nut

rtio

n Cheaper food

Less nutritious food

Reduce size / number of meals

Consume wild foods, seeds

Begging for food

Entire day without eating

Eat ab normal items (e.g. plants and insects)

Chi

ld

mal

nutr

ition

Prices nutritional status: Bangladesh

Rice prices up non-rice expenditures (vegetables, protein) down underweight

Poor nutrition < age 2 stunted for life

45

50

55

60

65

70

75

80

85

90

0 6 12 18 24

Age (Months)

Leng

th (C

entim

eter

)

USAOmanNorwayIndiaGhanaBrazilBolivia

Impact of child nutrition is life long

Higher productivity

Cognitive development & education

Better health & lower health costs, including of next generation

Guatemala: Nutritious drink wages 46% higher after 30 years!

40 assessments in 2008: Food consumption down

• Quantity and quality food consumption down• School drop-out rates up in some• Sale of economic assets in some

• Impacts in absolute terms higher in towns, but severity was higher for rural poor

• New face of hunger: Salaried workers in towns and agriculturalists near towns (Ethiopia, Pakistan and Tajikistan)

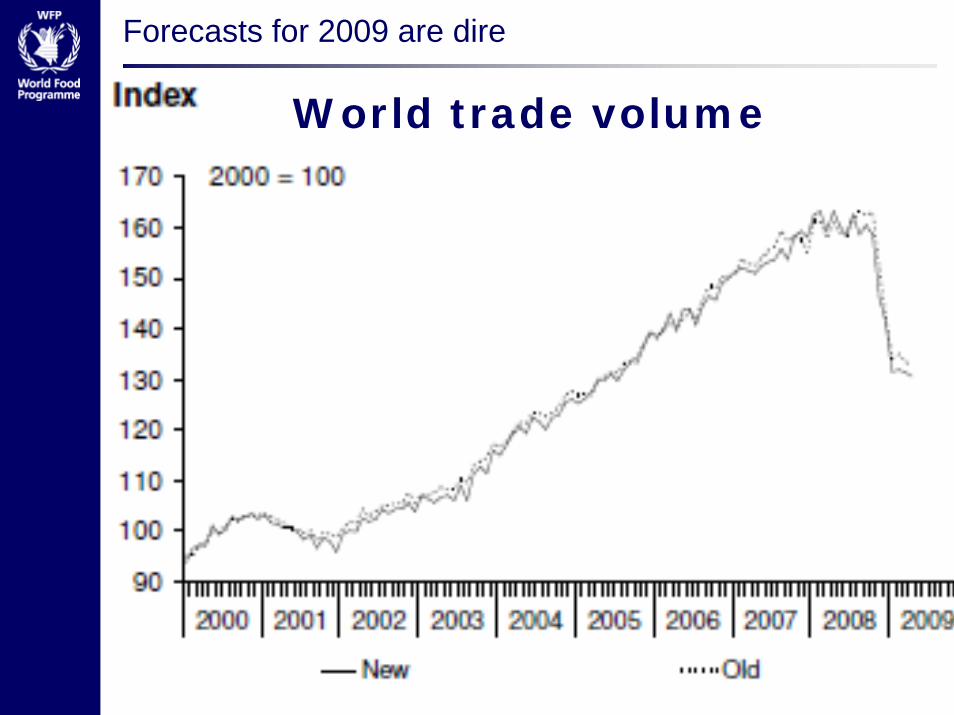

Food prices will remain high

Forecasts for 2009 are dire

World trade volume

13

Framework to analyze transmission from Wall St to hungry

Exc

han

ge

rate

Exc

han

ge

rate

MACROMACRO--LEVELLEVEL HOUSEHOLD HOUSEHOLD LEVELLEVEL IMPACTSIMPACTS

HealthHealth

EducationEducation

FoodFoodinsecurity/insecurity/

HungerHunger

Reduced Reduced copingcoping

capacitycapacity

Tensions

GDP growth

Imports

Remittances

ODA

Tourism

GDP growth

Employment

Finance

Exports

Return migr

Remittances

Gvt spending

Investment

Food prices

Incomes/wages

Remittances

Social transfers

Developed countries

Developing countries

Finance

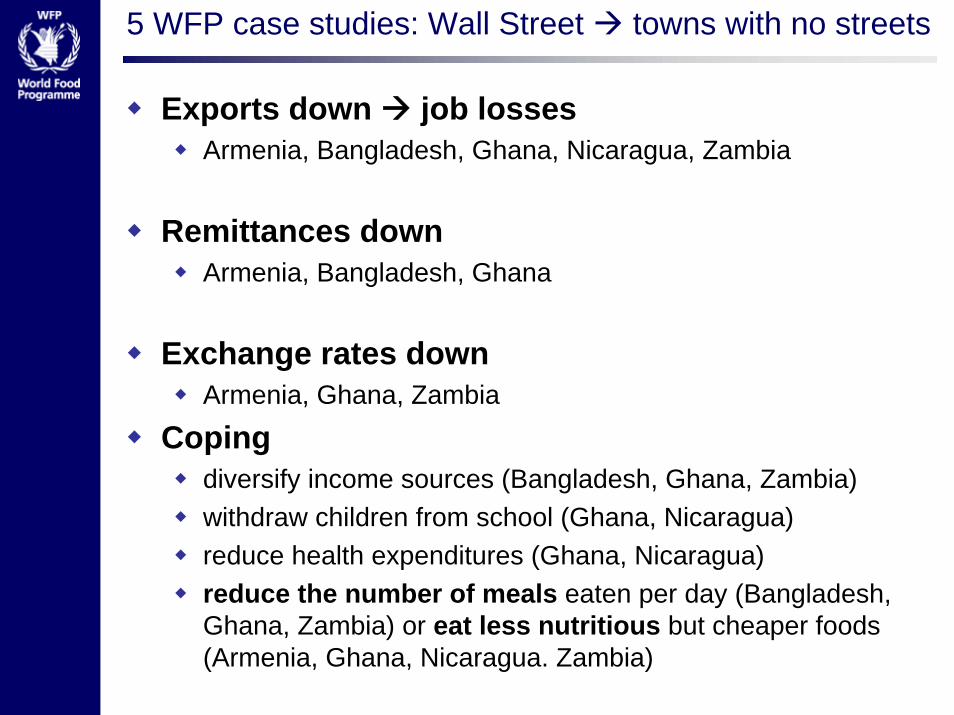

5 WFP case studies: Wall Street towns with no streets

Exports down job lossesArmenia, Bangladesh, Ghana, Nicaragua, Zambia

Remittances downArmenia, Bangladesh, Ghana

Exchange rates downArmenia, Ghana, Zambia

Copingdiversify income sources (Bangladesh, Ghana, Zambia)withdraw children from school (Ghana, Nicaragua)reduce health expenditures (Ghana, Nicaragua)reduce the number of meals eaten per day (Bangladesh, Ghana, Zambia) or eat less nutritious but cheaper foods (Armenia, Ghana, Nicaragua. Zambia)

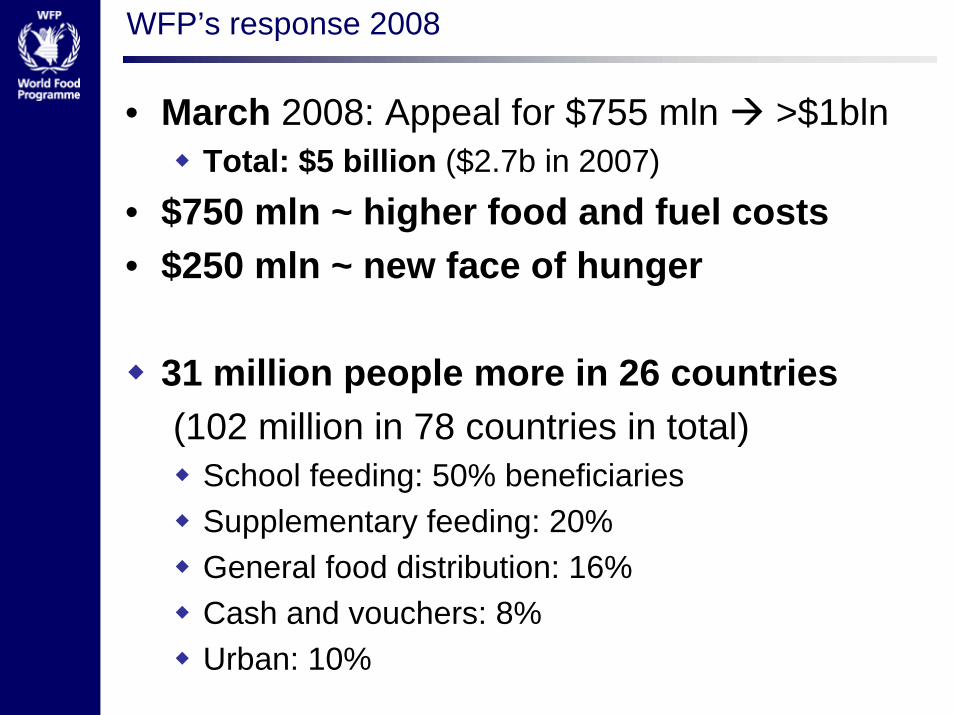

WFP’s response 2008

• March 2008: Appeal for $755 mln >$1blnTotal: $5 billion ($2.7b in 2007)

• $750 mln ~ higher food and fuel costs• $250 mln ~ new face of hunger

31 million people more in 26 countries(102 million in 78 countries in total)

School feeding: 50% beneficiariesSupplementary feeding: 20%General food distribution: 16%Cash and vouchers: 8%Urban: 10%

WFP activities

• School meals: upscaled 17 programmes: 5 million beneficiaries (children and their family) – e.g. Bangladesh, Haiti, Pakistan, Philippines, Senegal,Tajikistan

• Supplementary nutritious food: 2 million children, pregnant and lactating women, other vulnerable – e.g. Bangladesh, Haiti, Guinea and Yemen

• Safety nets, including Food-for-Work: expanded in 13 countries, > 6 million beneficiaries – e.g. Ethiopia, Nepal, Pakistan, Senegal

• Urban food assistance: 19 countries

• Targeted food rations to vulnerable groups: 10.5 million beneficiaries in 17 countries

Challenges create opportunities: Innovations

• Cash or voucher programmes in 24 countries

• New nutritious foods: in 17 countries (e.g. MixMe™ was used in Bangladesh and Nepal)

• Index-based weather insurance: China

• Purchase for Progress (P4P): 14 of 21 countries implementation; 17,235 MT procured as of August 2009

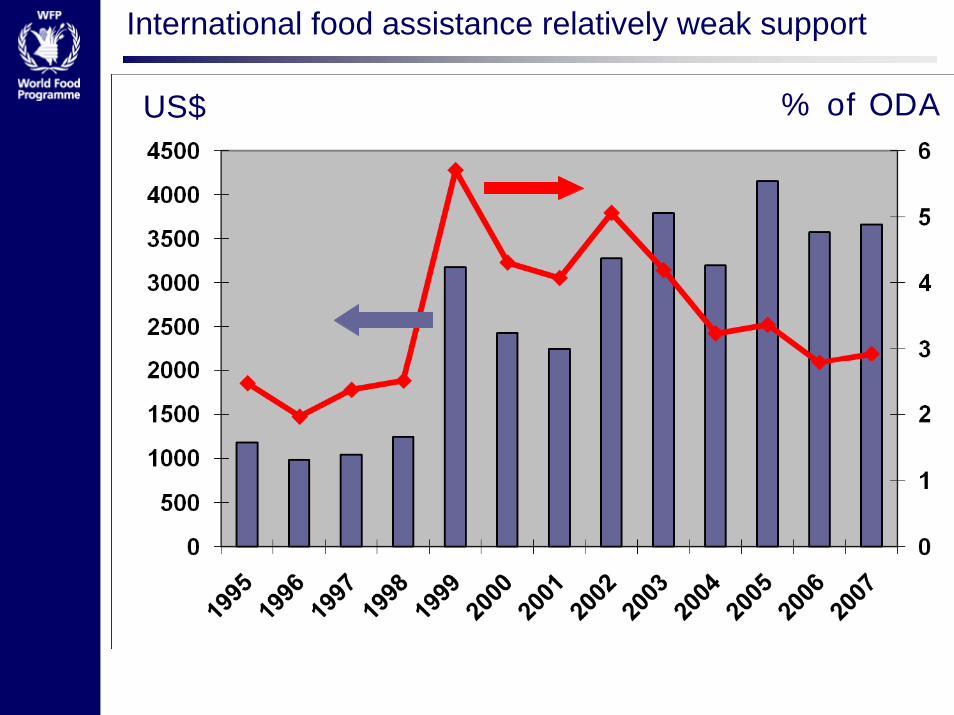

International food assistance relatively weak support

US$ % of ODA

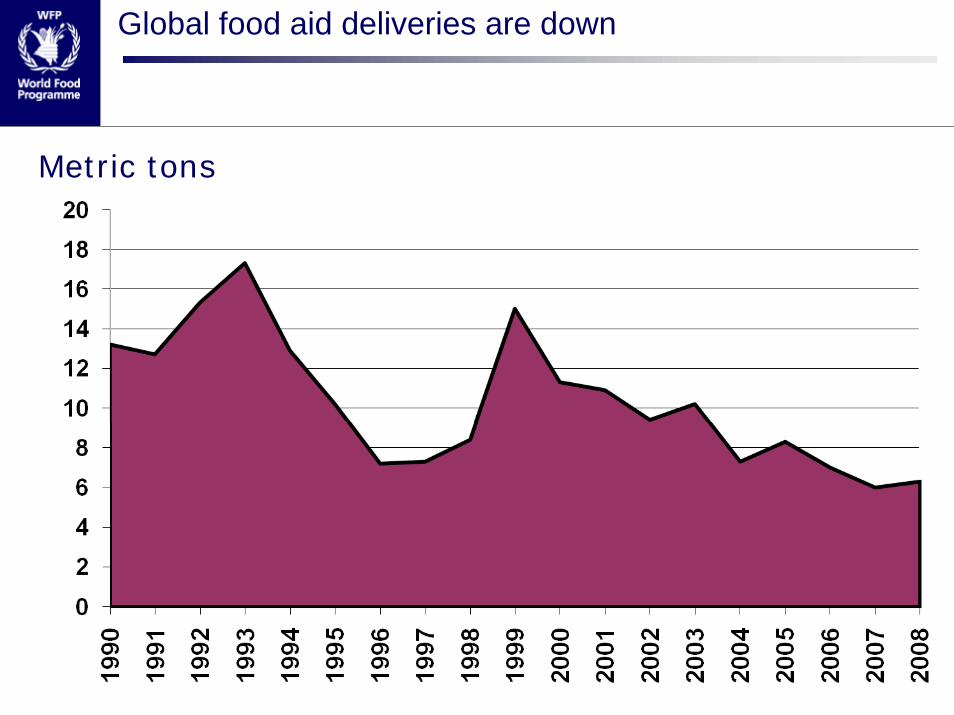

Global food aid deliveries are down

Metric tons

Thank you

Demand > Supply prices up: Agreement on list, but not on relative weight

DemandEmerging markets, changing demand patterns BiofuelsInstitutional investorsDepreciating dollar

Supply Low stocksWeather-related shocksLow productivity growthExport restrictionsOil price

Inputs: Fertilizer and transport costsOutputs: Link between food and energy prices

Poor spend more on food

01020304050607080

2 3 4 5 6 7Log of per capita income in U.S. dollars

Food

wei

ght i

n C

PI (%

)

USA

Bangladesh

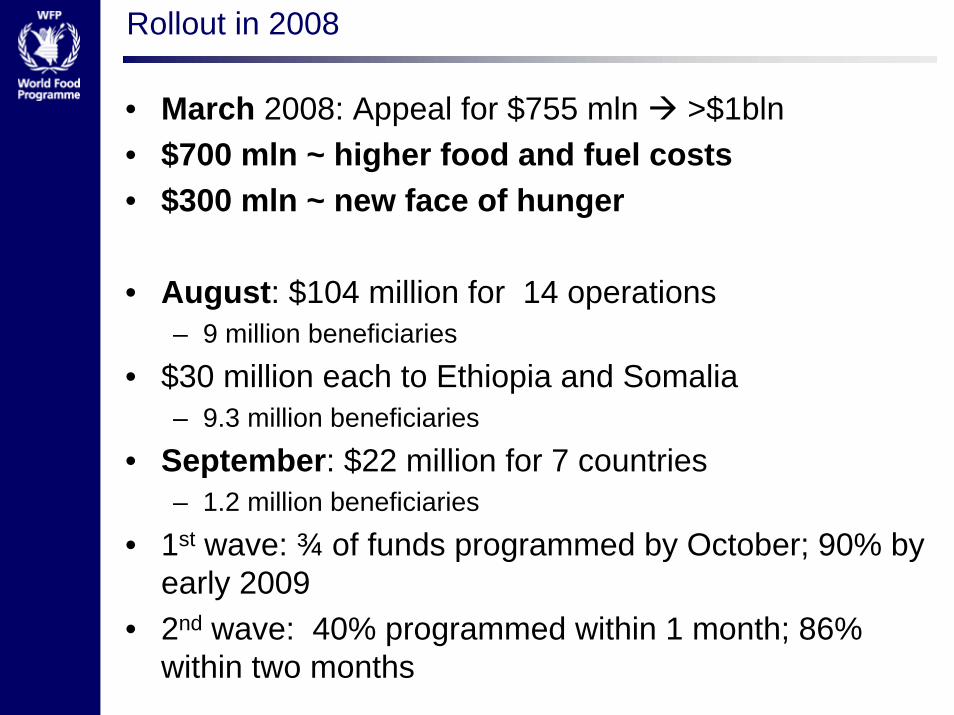

Rollout in 2008

• March 2008: Appeal for $755 mln >$1bln• $700 mln ~ higher food and fuel costs• $300 mln ~ new face of hunger

• August: $104 million for 14 operations – 9 million beneficiaries

• $30 million each to Ethiopia and Somalia – 9.3 million beneficiaries

• September: $22 million for 7 countries – 1.2 million beneficiaries

• 1st wave: ¾ of funds programmed by October; 90% by early 2009

• 2nd wave: 40% programmed within 1 month; 86% within two months

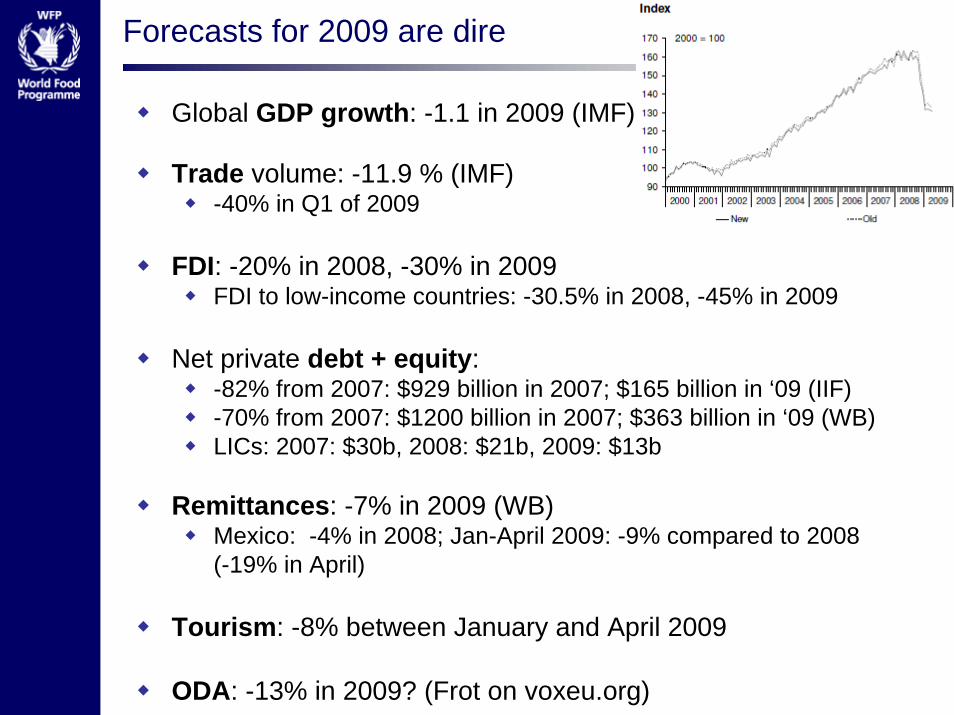

Forecasts for 2009 are dire

Global GDP growth: -1.1 in 2009 (IMF)

Trade volume: -11.9 % (IMF) -40% in Q1 of 2009

FDI: -20% in 2008, -30% in 2009FDI to low-income countries: -30.5% in 2008, -45% in 2009

Net private debt + equity:-82% from 2007: $929 billion in 2007; $165 billion in ‘09 (IIF)-70% from 2007: $1200 billion in 2007; $363 billion in ‘09 (WB)LICs: 2007: $30b, 2008: $21b, 2009: $13b

Remittances: -7% in 2009 (WB)Mexico: -4% in 2008; Jan-April 2009: -9% compared to 2008 (-19% in April)

Tourism: -8% between January and April 2009

ODA: -13% in 2009? (Frot on voxeu.org)

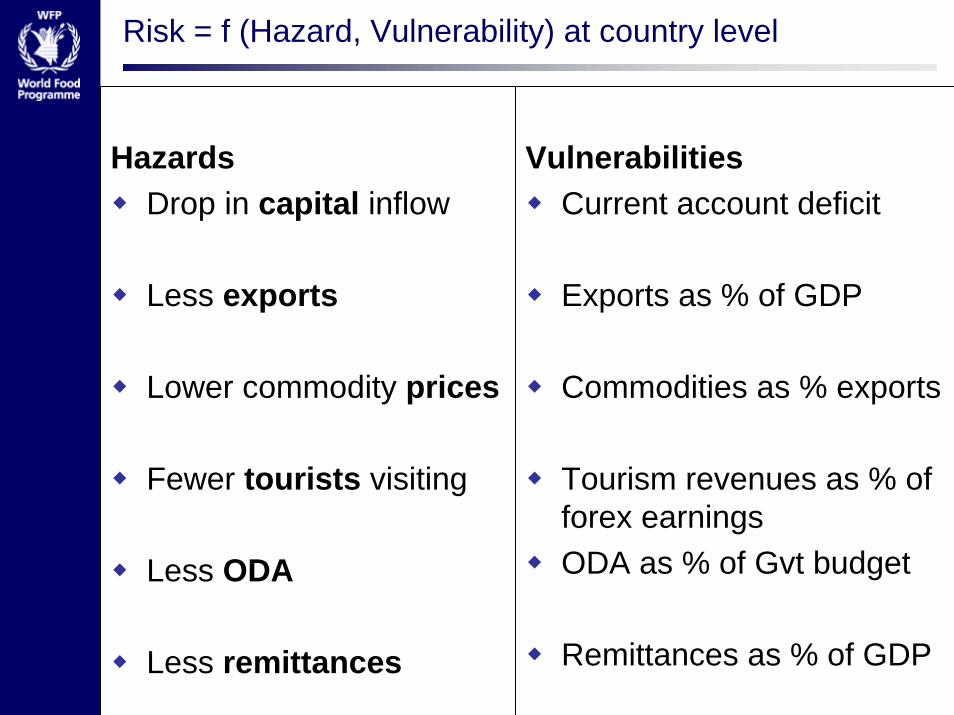

Risk = f (Hazard, Vulnerability) at country level

HazardsDrop in capital inflow

Less exports

Lower commodity prices

Fewer tourists visiting

Less ODA

Less remittances

VulnerabilitiesCurrent account deficit

Exports as % of GDP

Commodities as % exports

Tourism revenues as % of forex earningsODA as % of Gvt budget

Remittances as % of GDP

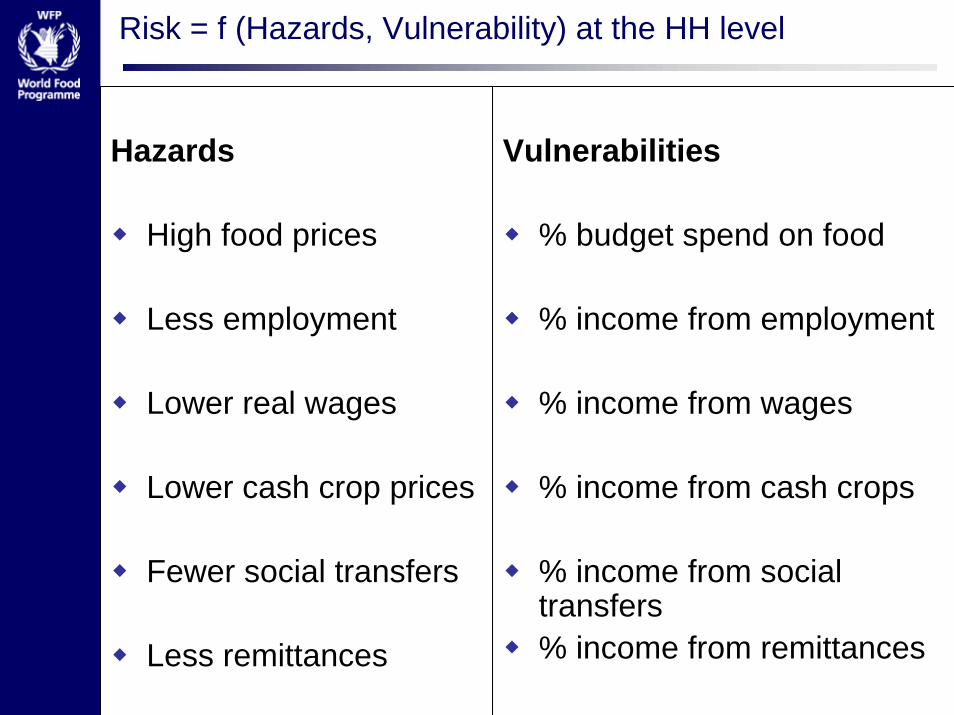

Risk = f (Hazards, Vulnerability) at the HH level

Hazards

High food prices

Less employment

Lower real wages

Lower cash crop prices

Fewer social transfers

Less remittances

Vulnerabilities

% budget spend on food

% income from employment

% income from wages

% income from cash crops

% income from social transfers% income from remittances