wfsn in community colleges - achieving the dream · 2017-11-15 · payday and auto-title loans,...

TRANSCRIPT

WFSN in Community

Colleges Financial Services and

Asset Building Prototypes

Webinar Panelists

Sarah Griffen, Consultant

Ashvin Prakash, CFSI

Nancy Castillo, CFSI

Wendy De La Rosa, Irrational Labs

Susan Gewirtz, Consultant

Webinar Goals

Review six financial prototypes developed by CFSI and Irrational Labs

Establish process for indicating interest and selection process for colleges to participate and receive TA to implement prototypes

The WFSN strategy

The WFSN strategy involves intentionally integrating and sequencing three distinct but related priorities:

1. Education and employment advances – education, job readiness, training, and placement

2. Income and work supports – access to student financial aid, public benefits, tax credits, and free tax assistance

3. Financial services and asset building – financial education and coaching linked to affordable products and services to help families build self-sufficiency, stabilize their finances, and become more economically competitive

© 2014 Center for Financial Services Innovation

Financial health for community college students

Improving the financial health of students has the potential to improve their ability to pursue educational attainment and achieve greater success.

Day to Day Management

Resilience to weather ups and downs

Long-term Opportunity

Elements of Financial Health

Enable students to manage their money effectively, pay bills and conduct transactions easily, and live within their means.

Ensure students have access to appropriate savings or financial cushion to deal with unexpected shocks.

Provide a pathway to continued financial stability and growth.

Students practice better financial behavior and are more financially capable, enabling them to tackle financial challenges that may otherwise hinder their ability to progress through their classes.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Psychology of Choice

Psychology of Money

Opportunity

Cost Neglect

Hyperbolic

Discounting

Default Bias

Mental

Accounting

Choice Overload

We categorize and treat money differently

depending on where it came from and where

it is going

We fail to recognize what we are giving up

when we make spending decisions

We put an unrealistically high value on the

here and now and an unrealistically low value

on the future

We tend to make the easiest choice possible -

often by not doing anything

We tend to not act when faced with too many

choices

IRRATIONALLABS

Behavioral barriers students face

© 2014 Center for Financial Services Innovation

Barriers to achieving financial health

Inability to manage cash flow

Lack of a financial cushion

Ability to build credit

Day to Day Management

Resilience to weather ups and downs

Long-term Opportunity

In improving the overall financial health of students to increase completion rates, Achieving the Dream will focus on identifying strategies to tackle the following three challenges.

Elements of Financial Health Core Financial Challenges

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype ideation

Webinar with community colleges Community college survey

In-depth interviews with 8 community colleges Half-day working session with 7 community colleges

To identify unique challenges faced by community college students and brainstorm solutions that are feasible, viable, and sustainable for community colleges to implement, the project team leveraged the following resources:

Based on the resources leveraged, the project team has identified 6 prototypes aimed to address the financial challenges faced by community college students, empowering them to overcome

barriers to course completion.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Overview of prototypes

IRRATIONALLABS

Prototype Challenge addressed

1/ Modifying distribution of financial aid

Inability to manage cash flow

2/ Renaming financial aid refunds Inability to manage cash flow

3/ Providing emergency grants or loans with vehicle for future cushion

Lack of a financial cushion

4/ Automatic allocation to savings Lack of a financial cushion

5/ Credit building tools Ability to build credit

6/ Improving Financial Literacy efforts

Inability to manage cash flow/ Lack of a financial cushion/ Ability to build credit

© 2014 Center for Financial Services Innovation

Prototype 1: Modifying distribution of financial aid

Current challenge Students are receiving lump payments of

their financial aid at the beginning of each semester. This is a significant source of

income for many students, and we find that many students are unable to budget the

funds accordingly to last them the full length of the semester, leaving them financially

vulnerable towards the end of the semester.

Proposed solution By dividing up the funds into separate payments, students will be better positioned to manage their monthly spend to align with their income, improving their overall financial health and budgeting capabilities.

Outcome: Students have a more consistent cash inflow, enabling them to make smarter spending decisions.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

What this looks like

Students receive multiple disbursement of financial aid over the course of the semester

Implementation tactics

Consider partnering with a third party financial institution to hold funds and administer monthly payments

Create barriers to opting out of program (need to meet with financial advisor to receive full amount)

Key requirements

Sizeable student financial aid refund ($500+)

Capability and capacity to administer

Strong financial institution partner

Student and administration buy-in

Prototype 1: Modifying distribution of financial aid

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Construct Delivery channel

Requirements Measurable impact Engagement strategy Issues for consideration

Multiple disbursements of financial aid over the course of the semester

Financial aid office or third party financial institution

• Sizeable student financial aid amounts ($500+)

• Student and admin buy-in

• Capacity/ infrastructure to process multiple payments OR financial institution partner willing to hold and release deposits

• Two consecutive semesters to measure impact

• % of students receiving modified financial aid distribution who complete semester vs. % of students who are not receiving financial aid distribution

• % of students receiving modified financial aid distribution who request emergency financial assistance vs. % of students not receiving modified financial aid distribution

• Pre and post survey on spending and savings behavior between those receiving multiple disbursements vs. those not

• Have as default option for students receiving financial aid disbursements (require those who want the full amount to opt-out)

• Have financial service partner on-site during disbursement to enroll students into a checking account

• Connect roll-out to financial education curriculum

• Deliver at end of month

• What is the right frequency for your school?

• How can you ensure students are still enrolled before making disbursements through the quarter?

• Administrative costs?

Prototype 1: Modifying distribution of financial aid - detail

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 2: Renaming financial aid refunds

Outcome: Students view their refunds as a source of income and spend more cautiously.

Current challenge Students are receiving refunds from their Pell grants or scholarships at the beginning

of each semester. However, the term “refund” is a term associated with “free”

money or “plush funds.” It does not encourage good financial decision making.

These refunds make up a large percentage of a student’s income.

Proposed solution By renaming refunds from financial

aid to another term that triggers feelings for conservative spending, like “reserved education income,” we can nudge students to make better financial decisions with

relatively little effort.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 2: Renaming financial aid refunds

IRRATIONALLABS

What this looks like

Rename the financial aid distribution

Potential options include:

Allocation

Education reserve

Reserved income

Stipend

Implementation tactics

Rebrand refund language through all communication channels

Key requirements

Majority of students currently receiving refunds

Capacity to rebrand language throughout all communication channels

© 2014 Center for Financial Services Innovation

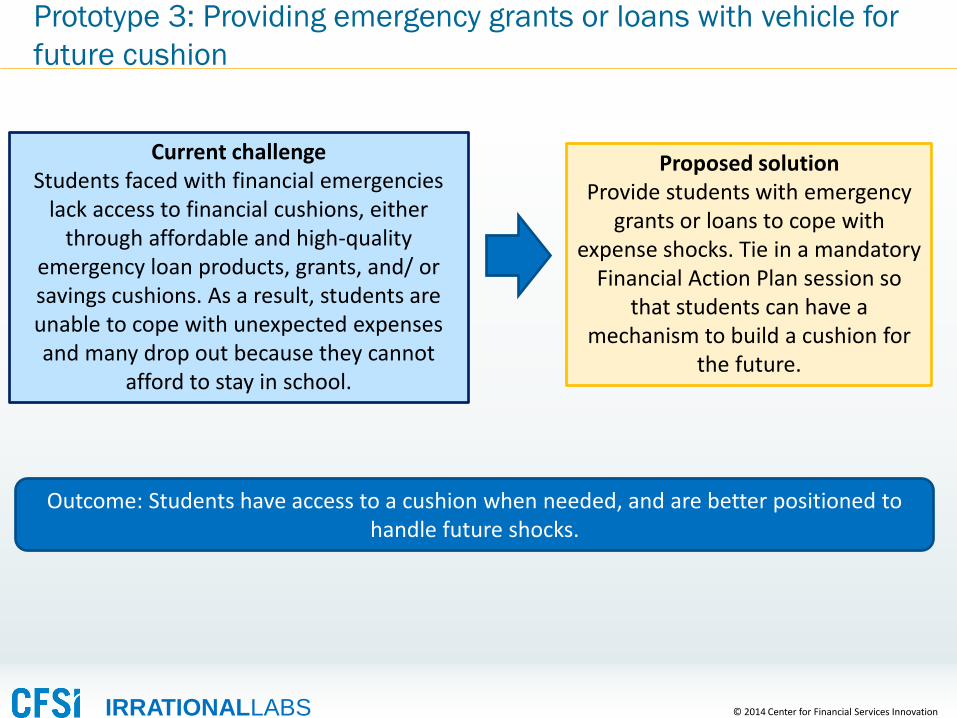

Prototype 3: Providing emergency grants or loans with vehicle for

future cushion

Outcome: Students have access to a cushion when needed, and are better positioned to handle future shocks.

Current challenge Students faced with financial emergencies

lack access to financial cushions, either through affordable and high-quality

emergency loan products, grants, and/ or savings cushions. As a result, students are unable to cope with unexpected expenses and many drop out because they cannot

afford to stay in school.

Proposed solution Provide students with emergency

grants or loans to cope with expense shocks. Tie in a mandatory

Financial Action Plan session so that students can have a

mechanism to build a cushion for the future.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 3: Providing emergency grants or loans with vehicle for

future cushion

IRRATIONALLABS

What this looks like

Colleges identify funds to grant to students facing financial hardships

Upon delivering emergency funds to student, students are required to complete a financial action plan and commit to ongoing savings

Implementation tactics

Inform students of program through standard resources guide already used by college

If possible, deposit an extra $50 into a savings account on behalf of the student, who can then access it after they have completed the financial action plan

Key requirements

Ability for college to identify grant funds

© 2014 Center for Financial Services Innovation

Prototype 4: Automatic allocation to savings

Current challenge Many community college students do not

have savings, leaving them financially vulnerable. There is a need to help students

increase their ability to save.

Proposed solution Automatically deposit

10% of a student’s refund into savings.

Outcome: Students have increased savings by eliminating barriers to action.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

What this looks like

Split financial aid distribution into two checks – 90% for their regular distribution, 10% for savings

Deposit 10% check directly into a student’s savings account

Implementation tactics

Create savings account for students

Have financial institution on-site when refund is disbursed for easy access to set up a savings account

Create barrier to opt-out (need to meet with financial counselor)

Key requirements

Sizeable student refund ($500+)

Strong financial institution partner

Student and administration buy-in

Prototype 4: Automatic allocation to savings

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 5: Credit building tools

Outcome: Students have a pathway to improve their credit and ability to access high-quality financial products in the future.

Current challenge Students today with damaged credit profiles

or no credit score are forced to rely on payday and auto-title loans, which are often loaded with high-fees and lead to a cycle of

debt.

Proposed solution By providing a low-risk credit

building tool, students can improve their credit ratings over the course of a few months, improving their

ability to access mainstream credit products to better manage

financial emergencies.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 5: Credit building tools

IRRATIONALLABS

What this looks like

College to partner with financial institution to offer credit builder loans (student makes monthly deposits of $30, at the end of semester the balance is returned to them and have received positive credit reporting)

College to partner with financial institution to offer secured cards

Implementation tactics

Position credit builder loan as a end of semester savings program, with added benefit of improving credit

Leverage a portion of a student’s aid as collateral for secured card

Tie with financial education around credit, and promote program through financial literacy courses

Key requirements

For employed students seeking to rebuild or establish credit

Strong financial institution partner

Student buy-in and authorization

© 2014 Center for Financial Services Innovation

Prototype 6: Improve Financial Literacy efforts

Outcome: Student’s become better financial actors by adopting behaviors promoted through sessions.

Current challenge: Financial literacy alone, with out action-based interventions, do not change students’ financial behaviors.

Proposed solution Integrate behavior based action plans into current financial literacy efforts.

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 6: Improve Financial Literacy efforts

IRRATIONALLABS

What this looks like

Rename Financial Literacy Programs to “Financial Action Plan”

Tie lessons to concrete actions (e.g. opening a savings account, create budget)

Time delivery of information based on student’s financial lifecycle

Implementation tactics

Make session mandatory for first time students

Key requirements

Capacity to administer and deliver session

© 2014 Center for Financial Services Innovation

Recap of prototypes

IRRATIONALLABS

Prototype For colleges that

1/ Modifying distribution of financial aid Distribute sizable ($500+) refunds to a large

portion of students

2/ Renaming financial aid refunds Distribute refunds to students

3/ Providing emergency grants or loans with vehicle for future cushion

Offer emergency assistance to students or have a strong financial institution partner

4/ Automatic allocation to savings Distribute sizeable refunds to students

5/ Credit building tools

Have grant funds or sizable refund, high percentage of employed students, and a

strong relationship with a financial institution partner

6/ Improve Financial Literacy efforts All

© 2014 Center for Financial Services Innovation

Long-term goals of prototypes

Improved student financial health

Higher completion rates

Improved operational efficiency

Students are better positioned to weather emergencies and avoid cash shortages that may have prevented them from course completion in the past.

Fewer costs associated with financial aid repayment can result in cost savings for school.

Colleges provide valuable financial resources and guidance to improve financial livelihoods of students.

Students are better financial actors, and empowered to pursue their goals and aspirations.

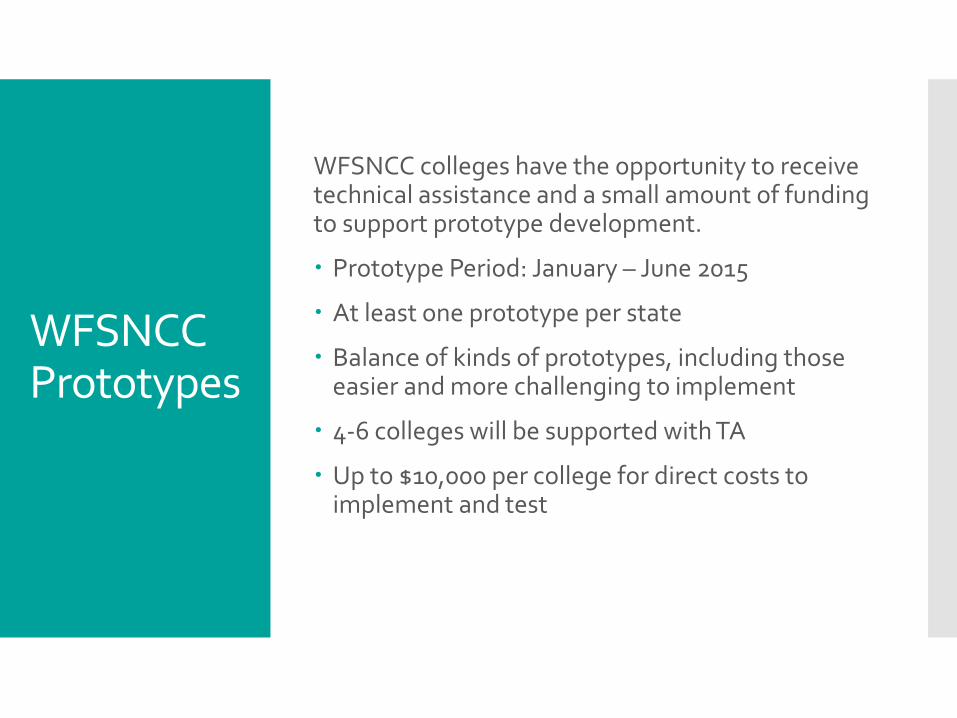

WFSNCC Prototypes

WFSNCC colleges have the opportunity to receive technical assistance and a small amount of funding to support prototype development.

Prototype Period: January – June 2015

At least one prototype per state

Balance of kinds of prototypes, including those easier and more challenging to implement

4-6 colleges will be supported with TA

Up to $10,000 per college for direct costs to implement and test

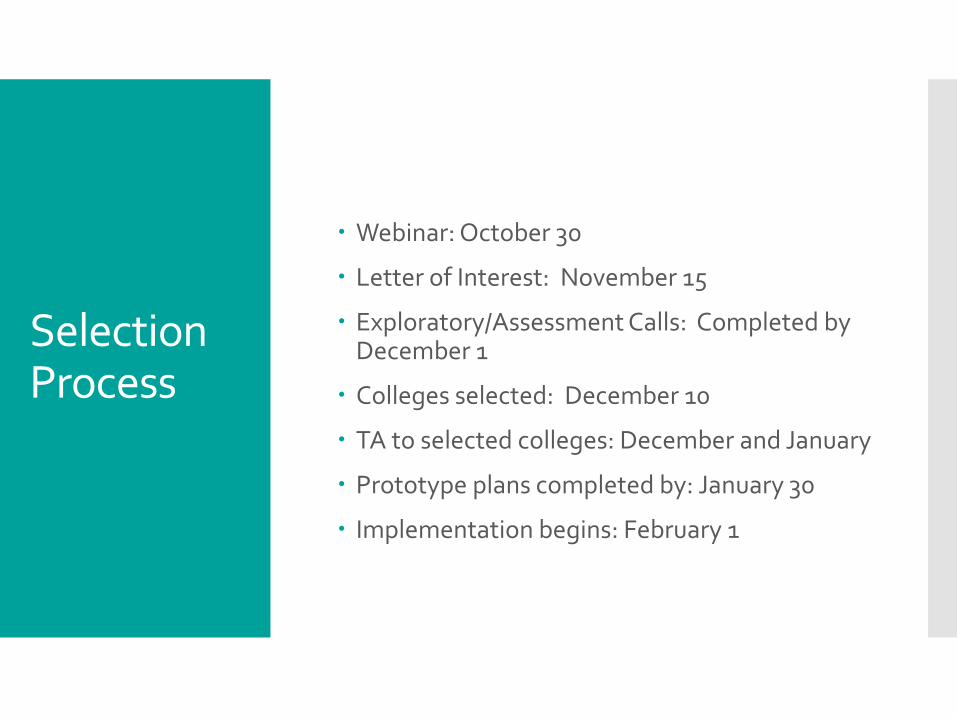

Selection Process

Webinar: October 30

Letter of Interest: November 15

Exploratory/Assessment Calls: Completed by December 1

Colleges selected: December 10

TA to selected colleges: December and January

Prototype plans completed by: January 30

Implementation begins: February 1

Letter of Interest

• Due November 15

• One page letter • Identify category of prototype

• One paragraph statement of why

prototype is of interest

• Sign-offs from relevant departments

• Point person identified

• Willingness to participate in exploratory/assessment conversation with member of TA team

Q&A

Appendix

© 2014 Center for Financial Services Innovation

Prototype 1: Modifying distribution of financial aid - Overview

Goal: Improve the way students spend their financial aid refunds by restructuring the delivery of funds.

Current challenge: Students are receiving lump payments of their financial aid refund at the beginning of each semester. This is a significant source of income for many students, and we find that many students are unable to budget the funds accordingly to last them the full length of the semester, leaving them financially vulnerable towards the end of the semester.

Proposed solution By dividing up the funds into separate payments over the course of the semester, students will be better positioned to manage their monthly spend to align with their income, improving their overall financial health and budgeting capabilities.

Multiple disbursements of refund over the course of the semester

• Deliver refund amount over multiple disbursements to students

Colleges currently delivering one-time distribution of financial aid

Colleges with typical refund distributions exceeding $500

Colleges with infrastructure/capacity to administer multiple payments

Constructs Applicable to Design considerations

Partner with third party financial service provider to hold refund deposits and administer refunds over the course of the semester

Behavior Economic Principles Utilized

Reducing mental accounting biases by -bucketing money on the behalf of students

Eliminating hyperbolic discounting by delivering funds over multiple time periods

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Construct Delivery channel

Requirements Measurable impact Engagement strategy Issues for

consideration

Multiple disbursements of financial aid over the course of the semester

Financial aid office or third

party financial

institution

• Sizeable student refund amounts

($500+) • Student and admin

buy-in • Capacity/

infrastructure to process multiple

payments OR financial institution partner willing to hold and

release deposits • Two consecutive semesters to measure

impact

• % of students receiving modified refund distribution

who complete semester vs. % of

students who are not receiving refund

distribution • % of students receiving modified refund distribution

who request emergency financial assistance vs. % of

students not receiving modified refund

distribution • Pre and post survey

on spending and savings behavior between those

receiving multiple disbursements vs.

those not

• Have as default option for students

receiving Pell refund of scholarship disbursements

(require those who want the full amount

to opt-out) • Have financial service

partner on-site during disbursement

to enroll students into a checking

account • Connect roll-out to

financial education curriculum

• Deliver at end of month

• What is the right frequency for your

school? • How can you ensure

students are still enrolled before

making disbursements

through the quarter?

• Administrative costs?

Prototype 1: Modifying distribution of financial aid - Detail

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 2: Renaming financial aid refunds - Overview

Goal: Improve the way students spend their refund/scholarships by renaming the “refund.”

Current challenge: Students are receiving refunds from financial aid at the beginning of each semester. However, the term “refund” is a term associated with “free” money or “plush funds.” It does not encourage good financial decision making. These refunds make up a large percentage of a student’s income.

Proposed solution By renaming financial aid refund to another term that triggers feelings for conservative spending, like “reserved education income,” we can nudge students to make better financial decisions with relatively little effort.

Rename the “Refund” to “Allocation”

Rename the “Refund” to “Education Reserve”

Rename the “Refund” to “Reserved Income”

Colleges currently delivering financial aid refunds

Colleges with typical refund distributions exceeding $500

Colleges with infrastructure/capacity to change all communications (emails, website, financial aid advisors)

Potential Constructs Applicable to Design considerations

Consider your financial advisor training and how it needs to be updated to reflect this change in wording

Behavior Economic Principles Utilized

Reducing mental accounting biases by -bucketing money on the behalf of students

New term triggers thoughts on opportunity costs

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Construct Delivery channel

Delivery type

Requirements Measurable impact Engagement strategy Issues for

consideration

Rename the refund.

Potential options may

include: [reserved income,

education reserve,

allocation]

Financial aid office

Business Services

office

Email, Website, Printed

Materials, Verbal

• Sizeable student refund amounts

($500+) • Student and admin

buy-in • Capacity/

infrastructure to process to change all communications • Two consecutive

semesters to measure impact

• % of students receiving [reserved

income] who complete semester

vs. % of students who are receiving a

refund • % of students receiving [reserved

income] who request emergency financial assistance

vs. % of students who are receiving a

refund • Pre and post survey

on spending and savings behavior between those

receiving [reserved income] vs. those

not

• Create a consistent message around

the [reserved income]

• Train all financial advisors and

business services administrators to

discuss the refund as a [reserved

income] • Connect roll-out to

financial education curriculum

• What other ways can you rebrand

the refund? • How can you

ensure that financial advisors

are using your updated

language? • Administrative

costs?

Prototype 2: Renaming financial aid refunds - Detail

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

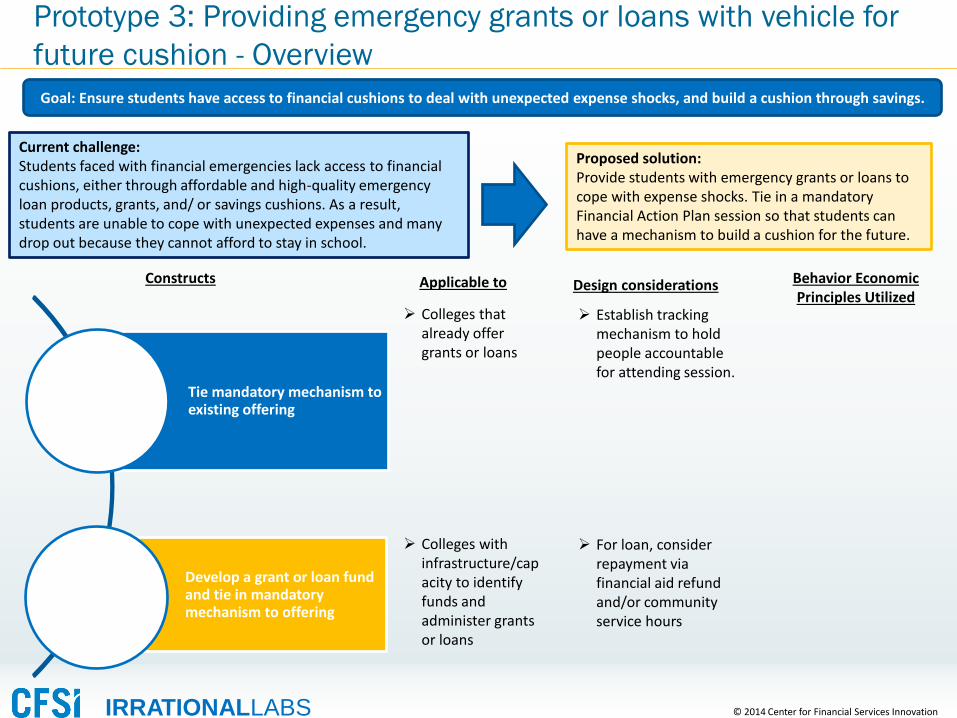

Prototype 3: Providing emergency grants or loans with vehicle for

future cushion - Overview

Goal: Ensure students have access to financial cushions to deal with unexpected expense shocks, and build a cushion through savings.

Current challenge: Students faced with financial emergencies lack access to financial cushions, either through affordable and high-quality emergency loan products, grants, and/ or savings cushions. As a result, students are unable to cope with unexpected expenses and many drop out because they cannot afford to stay in school.

Proposed solution: Provide students with emergency grants or loans to cope with expense shocks. Tie in a mandatory Financial Action Plan session so that students can have a mechanism to build a cushion for the future.

Tie mandatory mechanism to existing offering

Develop a grant or loan fund and tie in mandatory mechanism to offering

Colleges that already offer grants or loans

Colleges with

infrastructure/capacity to identify funds and administer grants or loans

Constructs Applicable to Design considerations

Behavior Economic Principles Utilized

Establish tracking mechanism to hold people accountable for attending session.

For loan, consider

repayment via financial aid refund and/or community service hours

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Construct Delivery channel

Requirements Measurable impact Engagement strategy Issues for consideration

Tie mandatory mechanism to existing offering

• Office that handles loans or grant

• Financial education mechanism

• Student and admin buy-in

• Capacity/ infrastructure to process loans or grants.

• Two consecutive semesters to measure impact

• % of students who in an emergency received loans/grant who complete semester vs. % of students who in an emergency did not receive who complete semester.

• % of Pre and post survey on savings behavior (length of time, amount saved) between those receiving loan/grant with savings vs. loan/grant without savings

• Instances of other types of loan products [credit cards, payday loans] used by students who received the loan/grant vs students who did not, or compared to if student did not have access to the loan/grant.

• Make mechanism to build a cushion a requirement of grant/loan

• Connect roll-out to financial education curriculum

• How to communicate the loan/grant to students?

• How to communicate cushion mechanism aspect to students?

• Administrative costs • What are the right

impact to loss rates for your college?

Develop a grant or loan fund and tie in mandatory mechanism to offering

Prototype 3: Providing emergency grants or loans with vehicle for

future cushion - Detail

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 4: Automatic allocation to savings - Overview

Goal: Increase savings behavior by automatically directing part of the refund to a savings account .

Current challenge: Many community college students do not have savings, leaving them financially vulnerable should any emergency occur. Thus, there is a need to help students increase their ability to save.

Proposed solution Assign 10% of a student’s financial aid refund to a savings account. If a student wishes to opt-out of the program, they would need to make an appointment with a financial aid advisor.

Allocate 10% of refund to a savings account

Provide a check for 10% of financial aid refunds, reassigned to savings

Colleges with typical financial aid refund distributions exceeding $500

Colleges with the capacity to distribute funds electronically

Constructs Applicable to Design considerations

Partner with third party financial service provider to help students create a savings account

Behavior Economic Principles Utilized

Harness the power of default students into saving

Reduce choices to make financial decision making easier

IRRATIONALLABS

Colleges with typical financial aid distributions exceeding $500

Colleges without the capacity to distribute funds electronically

Partner with third party financial service provider to help students create a savings account at the point of delivery

© 2014 Center for Financial Services Innovation

Construct Delivery channel

Delivery type

Requirements Measurable impact Engagement strategy Issues for

consideration

Allocate 10% of aid to a

savings account

Financial aid office

or business service office

[depending on

college]

Electronic Distributi

on of funds to a Checking

and a Savings Account

• Sizeable student refund amounts

($500+) • Student and admin

buy-in • Capacity/

infrastructure to process electronic or check payments

• Financial institution partner willing to provide savings

accounts • Two consecutive

semesters to measure impact

• % of students who complete semester

vs. % of students who opted out

• % of students who request emergency financial assistance

vs. % of students who opted out

• Pre and post survey on spending and savings behavior

• Have a financial institution partner

on-site during disbursement to enroll students

into a checking / savings account

• Connect roll-out to financial education

curriculum • Deliver at end of

month • Ask that students

meet with a financial advisor if they want to opt

out

• What is the right savings % for your

school? • Administrative

costs?

Provide a check for 10%

of the financial aid

refund, reassigned to

savings

Separate Check or prepaid

cards

Prototype 4: Automatic allocation to savings - Detail

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Prototype 5: Credit building tools - Overview

Goal: Provide pathway to improved credit to help improve access to high-quality financial services in the future.

Current challenge: Students today with damaged credit profiles or no credit score are forced to rely on payday and auto-title loans, which are often loaded with high-fees and lead to a cycle of debt.

Proposed solution By providing a low-risk credit building tool, students can improve their credit ratings over the course of a few months, improving their ability to access mainstream credit products to better manage financial emergencies.

Secured credit card

• Leverage a portion of a financial aid or grant funds as collateral for a secured credit card

Credit builder loan

• Have students make monthly deposits over the semester that are reported to credit bureaus, with funds returned to student at end of semester

Colleges with financial institution partners who offer secured cards and credit builder loans

Students with steady income and credit repair need

Constructs Applicable to Design considerations

Partner with third party financial service provider to administer products

Consider easy enroll options when students are receiving their refund

Integrate into financial coaching and literacy classes for credit building opportunities

College to hold a portion of financial aid to make automatic deposits on behalf of student

Position as a savings vehicle that enables students to build credit

Opportunity to match contributions

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

Construct Delivery channel Requirements Measurable impact Engagement strategy Issues for

consideration

Secured credit card

Financial institutions (referenced

through Financial Literacy classes)

• $300-$500 in student refund or grant to fund initial security deposit

• Student must have steady income streams for

repayment • Credit improvements

for students who engage with product

• % of students who utilize product and complete semester

vs. % of students who do not engage with

product and complete semester

• Offer at point of refund or when in

emergency • Highlight benefits and

usage through well timed financial

literacy program

• Need to ensure selection of a high-quality product with low fees and

APR • Need to deliver

adequate financial

education to students prior

to utilizing card • Opportunity to offer

IDA like match to those who complete

program • Position as savings

program, where students forgo

receiving funds today to receive more in

the future, in addition to improving

their credit score • Community college to

hold funds and make payments on behalf

of students

Credit builder loan

• Student must be able to make monthly deposits of

$25-$50

• Can colleges make loan

payments on behalf of students?

• Contingency plan for if

student urgently needs funds?

Prototype 5: Credit building tools - Detail

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

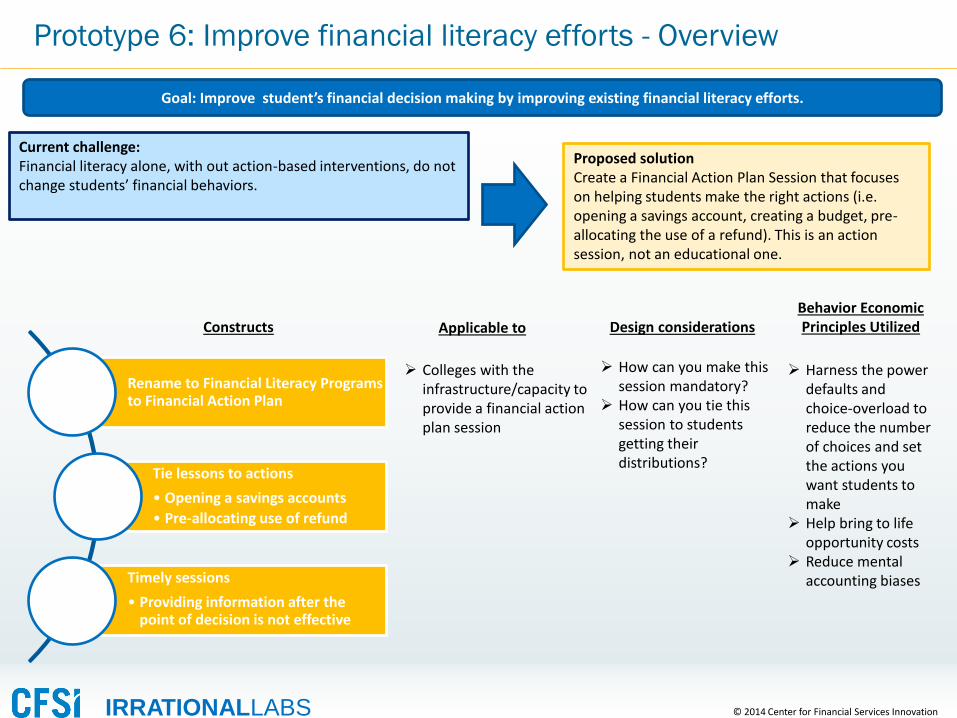

Prototype 6: Improve financial literacy efforts - Overview

Goal: Improve student’s financial decision making by improving existing financial literacy efforts.

Current challenge: Financial literacy alone, with out action-based interventions, do not change students’ financial behaviors.

Proposed solution Create a Financial Action Plan Session that focuses on helping students make the right actions (i.e. opening a savings account, creating a budget, pre-allocating the use of a refund). This is an action session, not an educational one.

Rename to Financial Literacy Programs to Financial Action Plan

Tie lessons to actions

• Opening a savings accounts

• Pre-allocating use of refund

Timely sessions

• Providing information after the point of decision is not effective

Colleges with the infrastructure/capacity to provide a financial action plan session

Constructs Applicable to Design considerations

How can you make this session mandatory?

How can you tie this session to students getting their distributions?

Behavior Economic Principles Utilized

Harness the power defaults and choice-overload to reduce the number of choices and set the actions you want students to make

Help bring to life opportunity costs

Reduce mental accounting biases

IRRATIONALLABS

© 2014 Center for Financial Services Innovation

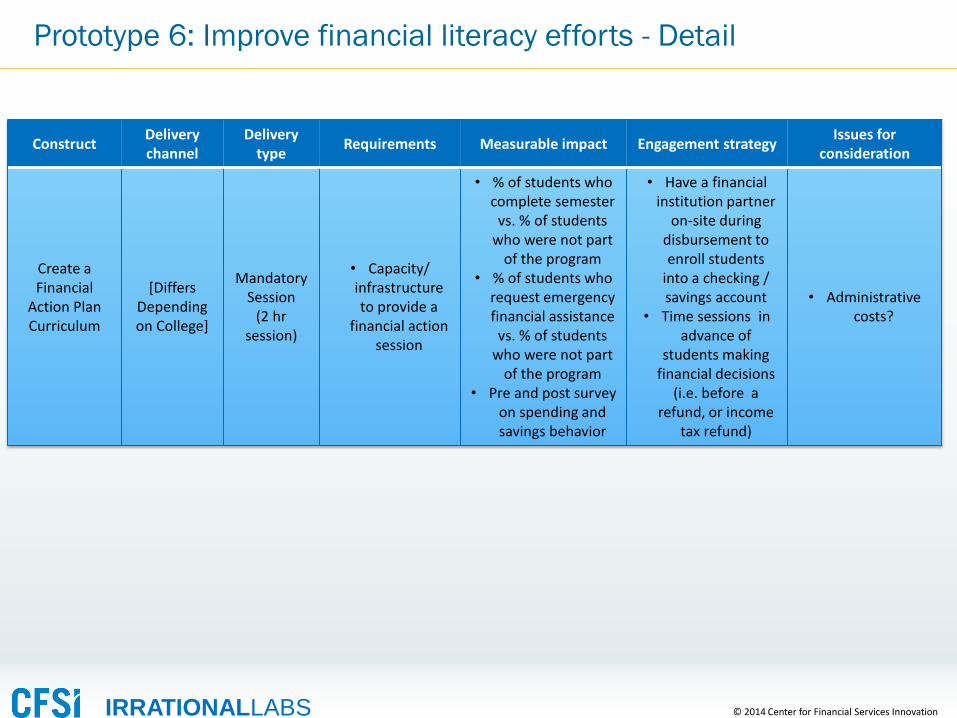

Construct Delivery channel

Delivery type

Requirements Measurable impact Engagement strategy Issues for

consideration

Create a Financial

Action Plan Curriculum

[Differs Depending on College]

Mandatory Session

(2 hr session)

• Capacity/ infrastructure to provide a

financial action session

• % of students who complete semester

vs. % of students who were not part

of the program • % of students who

request emergency financial assistance

vs. % of students who were not part

of the program • Pre and post survey

on spending and savings behavior

• Have a financial institution partner

on-site during disbursement to enroll students

into a checking / savings account

• Time sessions in advance of

students making financial decisions

(i.e. before a refund, or income

tax refund)

• Administrative costs?

Prototype 6: Improve financial literacy efforts - Detail

IRRATIONALLABS