wha corporation public company limited opportunity day q2...

TRANSCRIPT

0

Q2’ 2015 Result Opportunity Day WHA Corporation Public Company Limited

The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in WHA Corporation Public Company Limited (“WHA” and shares in WHA, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever. In addition, this presentation contains projections and forward-looking statements that reflect the Company's current views with respect to future events and financial performance. These views are based on a number of estimates and current assumptions which are subject to business, economic and competitive uncertainties and contingencies as well as various risks and these may change over time and in many cases are outside the control of the Company and its directors. You are cautioned not to place undue reliance on these forward looking statements, which are based on the current view of the management of the Company on future events. No assurance can be given that future events will occur, that projections will be achieved, or that the Company's assumptions are correct. The Company does not assume any responsibility to amend, modify or revise any forward-looking statements, on the basis of any subsequent developments, information or events, or otherwise. These statements can be recognized by the use of words such as “expects,” “plans,” “will,” “estimates,” “projects,” or words of similar meaning. Such forward-looking statements are not guarantees of future performance and actual results may differ from those forecast and projected or in the forward-looking statements as a result of various factors and assumptions.

DISCLAIMERS

1

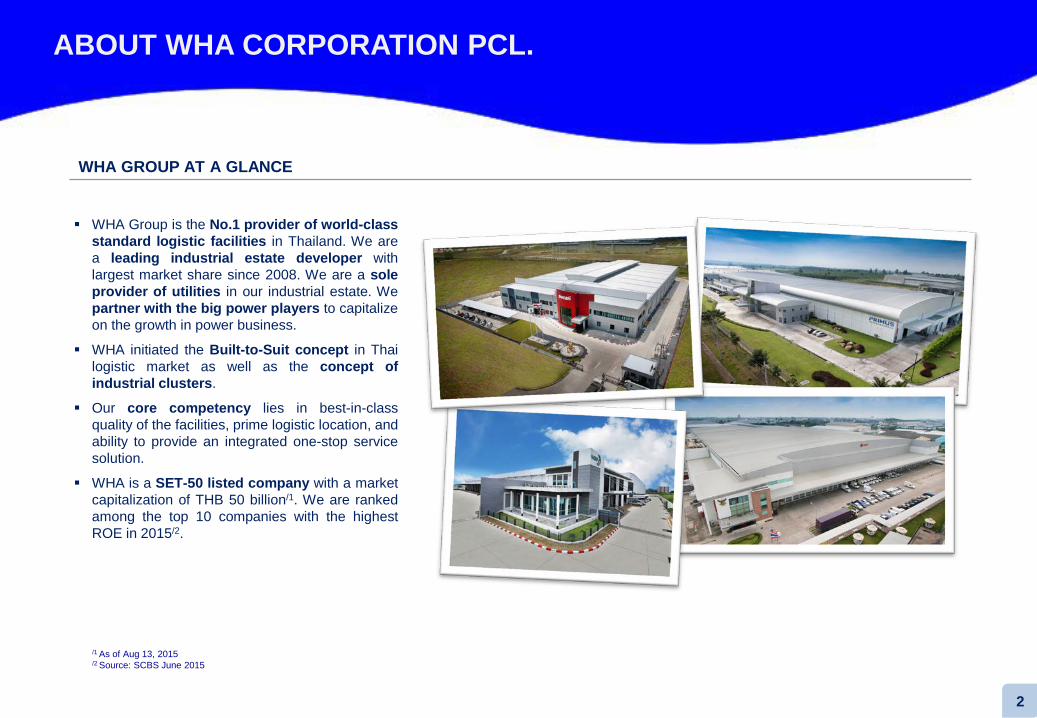

WHA GROUP AT A GLANCE

WHA Group is the No.1 provider of world-class standard logistic facilities in Thailand. We are a leading industrial estate developer with largest market share since 2008. We are a sole provider of utilities in our industrial estate. We partner with the big power players to capitalize on the growth in power business.

WHA initiated the Built-to-Suit concept in Thai logistic market as well as the concept of industrial clusters.

Our core competency lies in best-in-class quality of the facilities, prime logistic location, and ability to provide an integrated one-stop service solution.

WHA is a SET-50 listed company with a market capitalization of THB 50 billion/1. We are ranked among the top 10 companies with the highest ROE in 2015/2.

2

/1 As of Aug 13, 2015 /2 Source: SCBS June 2015

ABOUT WHA CORPORATION PCL.

A GREAT SPRING FORWARD • Acquisition of Hemaraj via conditional

Voluntary Tender Offer was completed on Apr 20, 2015 with 92.88% acquisition stake

• Establishment of WHA Venture Holding Co., Ltd. to conduct the VTO transaction

• Prior to Tender Offer, the capital increase was successfully completed via Right Offering with the right ratio of 2.75: 1 shares with free warrants—3 newly subscribed share to 1 warrant—raising up the registered capital to THB 1,431mm and paid-up capital to THB 1,314mm

GROWING PHASE • Monetization of the assets to WHAPF

with the value of THB 2,046mm (69,529 sqm) in the 1st quarter and injected another lot of THB 4,536mm worth of assets (173,367 sqm) in 4th Quarter which makes total fund size of THB 9,308mm

• This year WHA offered 2 stock dividends to existing shareholders on May, 2013 (5:1) and on September, 2013 (2:1)

• WHA is rated A- with stable outlook by Fitch Ratings (Thailand)

ESTABLISHMENT OF PUBLICLY LISTED FUND (WHAPF)

Establishment of WHAPF (initially known as M-WHA) with the total fund size of THB 1,283mm or USD 42.77mm with total leasable area of 39,808.80 sqm of 2 warehouses and 1 factory

ESTABLISHMENT OF WHA CORPORATION

WHA Corporation was founded on September 25, 2007 with a registered capital of THB 170mm by Mr.Somyos Anantaprayoon, founder, and Mrs.Jareeporn Anantaprayoon, cofounder. WHA Corporation focuses on developing high quality of warehouses, distribution centers, and factories to suitly serve the demand of the clients

WHA’S FIRST & THE BIGGEST DCs IN SEA

Establishment of Warehouse Asia Alliance (partner with GLOMAC, Malaysia) and WHA Alliance (partner with CWT, Singapore) to develop distribution centers for DKSH healthcare and consumer on Bangna-Trad km.19 and km.20 each with the leasable area of 53,000 sqm

KEY MILESTONES AND DEVELOPMENTS

3

PRE-IPO RESTRUCTURING • WHA Corporation restructured itself

by acquiring 99.99% of WHA Alliance from CWT (Singapore) and co-founder, as well as 99.99% of Warehouse Asia Alliance from GLOMAC (Malaysia) and co-founder to become WHA Corporation’s subsidiaries.

• Development of first warehouse farm on Bangna-Trad km.18 with the leasable area of 72,179.48 sqm

2007

2006

2010

2011

IPO AND LISTED COMPANY • Monetization of 3 warehouses and 1

factory to WHAPF with the value of THB 1,827mm (107,277 sqm)

• On Nov 8, 2012, WHA Corporation became to be listed Co. and first traded in SET, raising up the capital to THB 1,709mm or USD 56.97mm

• The post-IPO paid-up capital was THB 510mm

2013

2012

NEW OPPORTUNITIES • Establishment of WHA REM to pave

the way to set up new WHA REIT • Commence of solar energy sale

revenue recognition in May • More value-added services focus i.e.

cold storage, online warehouse, and other comprehensive services

• Tap into built-to-suit office and acquire a new office place on Vibhavadi-Rangsit Rd.

• Executed Share Purchase Agreement with major shareholders of Hemaraj

2014

2015

AGENDA

I. Business Overview

IV. Recent Developments & Key Events

VI. Appendix

V. Q1 2015 Financial Performance

II. Key Business Plan III. Business Updates

4

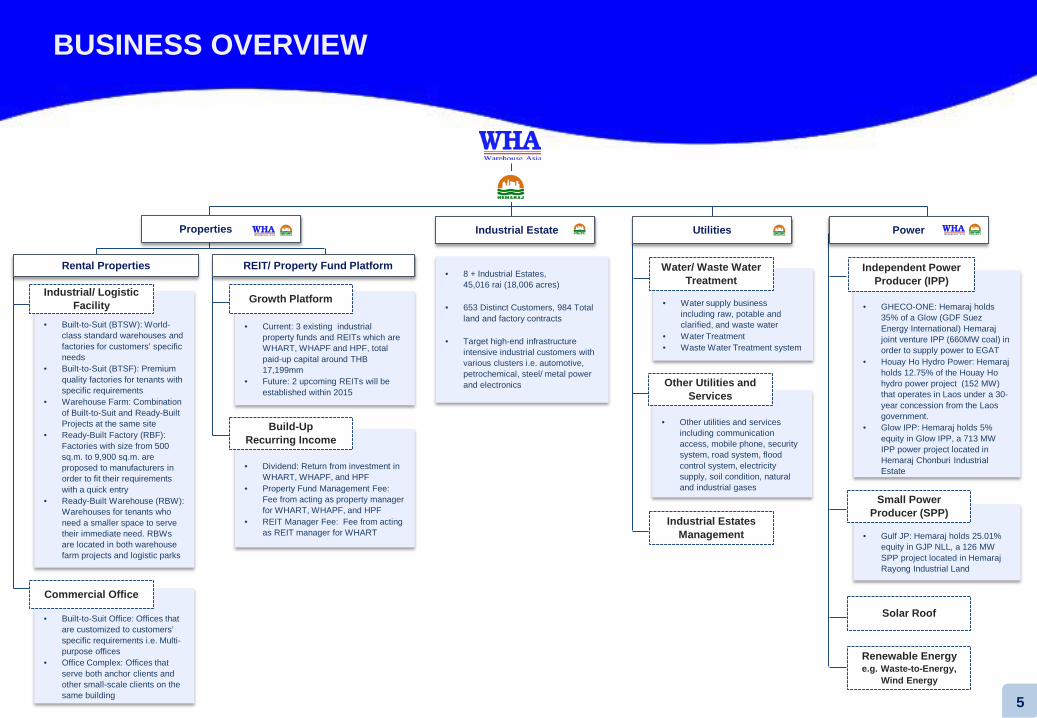

BUSINESS OVERVIEW

• Gulf JP: Hemaraj holds 25.01% equity in GJP NLL, a 126 MW SPP project located in Hemaraj Rayong Industrial Land

• Dividend: Return from investment in WHART, WHAPF, and HPF

• Property Fund Management Fee: Fee from acting as property manager for WHART, WHAPF, and HPF

• REIT Manager Fee: Fee from acting as REIT manager for WHART

• Current: 3 existing industrial

property funds and REITs which are WHART, WHAPF and HPF, total paid-up capital around THB 17,199mm

• Future: 2 upcoming REITs will be established within 2015

• Built-to-Suit Office: Offices that are customized to customers’ specific requirements i.e. Multi-purpose offices

• Office Complex: Offices that serve both anchor clients and other small-scale clients on the same building

• Built-to-Suit (BTSW): World-

class standard warehouses and factories for customers’ specific needs

• Built-to-Suit (BTSF): Premium quality factories for tenants with specific requirements

• Warehouse Farm: Combination of Built-to-Suit and Ready-Built Projects at the same site

• Ready-Built Factory (RBF): Factories with size from 500 sq.m. to 9,900 sq.m. are proposed to manufacturers in order to fit their requirements with a quick entry

• Ready-Built Warehouse (RBW): Warehouses for tenants who need a smaller space to serve their immediate need. RBWs are located in both warehouse farm projects and logistic parks

• Other utilities and services

including communication access, mobile phone, security system, road system, flood control system, electricity supply, soil condition, natural and industrial gases

• Water supply business

including raw, potable and clarified, and waste water

• Water Treatment • Waste Water Treatment system

Small Power Producer (SPP)

Solar Roof

Renewable Energy e.g. Waste-to-Energy,

Wind Energy

• 8 + Industrial Estates, 45,016 rai (18,006 acres)

• 653 Distinct Customers, 984 Total land and factory contracts

• Target high-end infrastructure intensive industrial customers with various clusters i.e. automotive, petrochemical, steel/ metal power and electronics

Water/ Waste Water Treatment

Other Utilities and Services

Industrial Estates Management

Industrial/ Logistic Facility

Commercial Office

Growth Platform

Build-Up Recurring Income

• GHECO-ONE: Hemaraj holds

35% of a Glow (GDF Suez Energy International) Hemaraj joint venture IPP (660MW coal) in order to supply power to EGAT

• Houay Ho Hydro Power: Hemaraj holds 12.75% of the Houay Ho hydro power project (152 MW) that operates in Laos under a 30-year concession from the Laos government.

• Glow IPP: Hemaraj holds 5% equity in Glow IPP, a 713 MW IPP power project located in Hemaraj Chonburi Industrial Estate

Independent Power Producer (IPP)

Power Industrial Estate Properties Utilities

Rental Properties REIT/ Property Fund Platform

5

The Group offers a Total Solution Package—comprehensive, customized, and best-in-class

COMPREHENSIVE ONE-STOP SERVICE

6

INDUSTRIAL ESTATE

RENTAL PROPERTIES

POWER

UTILITIES (water)

Quality developed land with supporting infrastructure

3Yr (2012-2014) average land sale of 1,659 rai with 20 to 60 new contracts per annum of which 20% to 40% from existing customer expansions

Supply of raw, potable, and

clarified water Industrial services e.g.

waste water treatment and facility management

Average daily water demand of ~261,000 m3 with increasing growth rate originated from power plants

Total ~538 equity MW with PPA signed 5 existing projects totaling ~318 equity MW (COD) 7 new projects totaling ~220 equity MW (non-COD, Negotiating SPA)

Partner with international power experts i.e. Glow, Gulf JP and B-Grimm Total solar rooftop with COD approx. 4.1 MW and equipped with combined

capacity of 2 million sqm. of roof area which can generate up to 200 MW

Built-to-Suit or Ready-Built warehouse and factory both in prime logistic location and in industrial Estate

Warehouse Farm Built-to-Suit office and Office

Complex

Clients can choose to buy developed land in the Industrial Estate and build their own factories or let us build the customized high-standard ones and lease them from us.

We provide both Built-to-Suit and Ready-Built warehouses in Industrial Estate and Industrial Park to support full chain of clients’ operation.

We offer Built-to-Suit warehouses and distribution centers in prime logistics location for warehousing and distribution operation.

We provide a wide range of complementary businesses such as water, power, waste management, and other industrial services to support clients’ operation in Industrial Estate.

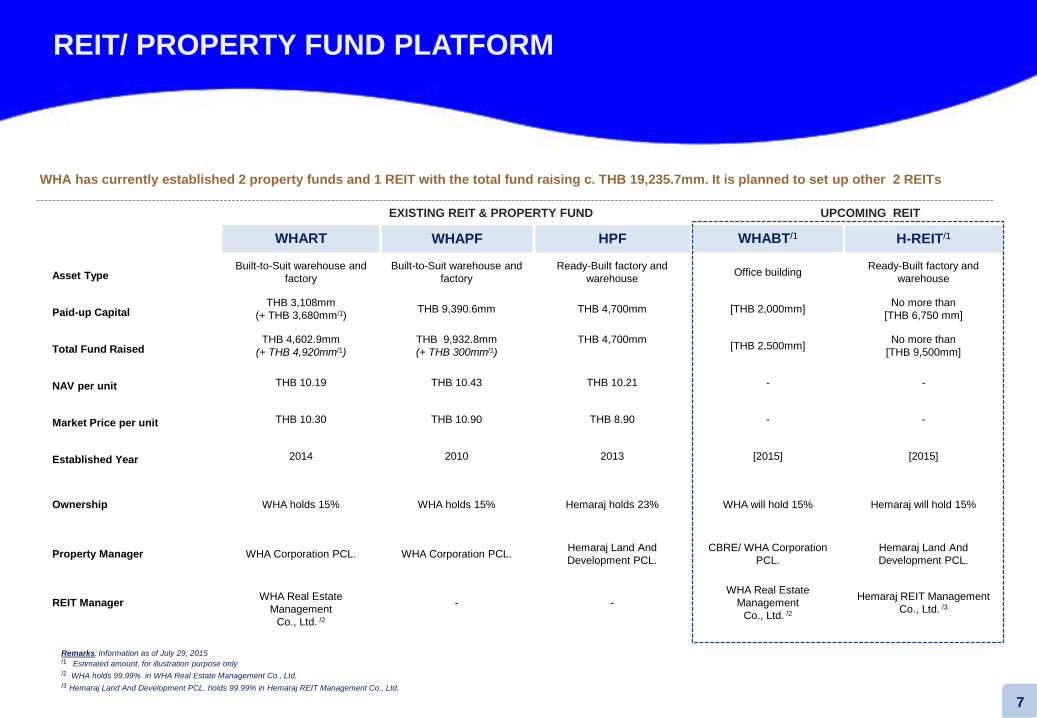

REIT/ PROPERTY FUND PLATFORM

Asset Type Built-to-Suit warehouse and

factory Built-to-Suit warehouse and

factory Ready-Built factory and

warehouse Office building Ready-Built factory and warehouse

Paid-up Capital THB 3,108mm

(+ THB 3,680mm/1) THB 9,390.6mm THB 4,700mm [THB 2,000mm] No more than [THB 6,750 mm]

Total Fund Raised THB 4,602.9mm

(+ THB 4,920mm/1) THB 9,932.8mm (+ THB 300mm/1)

THB 4,700mm [THB 2,500mm] No more than

[THB 9,500mm]

NAV per unit THB 10.19 THB 10.43 THB 10.21 - -

Market Price per unit THB 10.30 THB 10.90 THB 8.90 - -

Established Year 2014 2010 2013 [2015] [2015]

Ownership WHA holds 15% WHA holds 15% Hemaraj holds 23% WHA will hold 15% Hemaraj will hold 15%

Property Manager WHA Corporation PCL. WHA Corporation PCL. Hemaraj Land And Development PCL.

CBRE/ WHA Corporation PCL.

Hemaraj Land And Development PCL.

REIT Manager

WHA Real Estate

Management Co., Ltd. /2

- - WHA Real Estate

Management Co., Ltd. /2

Hemaraj REIT Management Co., Ltd. /3

WHART

Remarks: Information as of July 29, 2015 /1 Estimated amount, for illustration purpose only /2 WHA holds 99.99% in WHA Real Estate Management Co., Ltd. /3 Hemaraj Land And Development PCL. holds 99.99% in Hemaraj REIT Management Co., Ltd.

WHA has currently established 2 property funds and 1 REIT with the total fund raising c. THB 19,235.7mm. It is planned to set up other 2 REITs

H-REIT/1 HPF WHABT/1 WHAPF

EXISTING REIT & PROPERTY FUND UPCOMING REIT

7

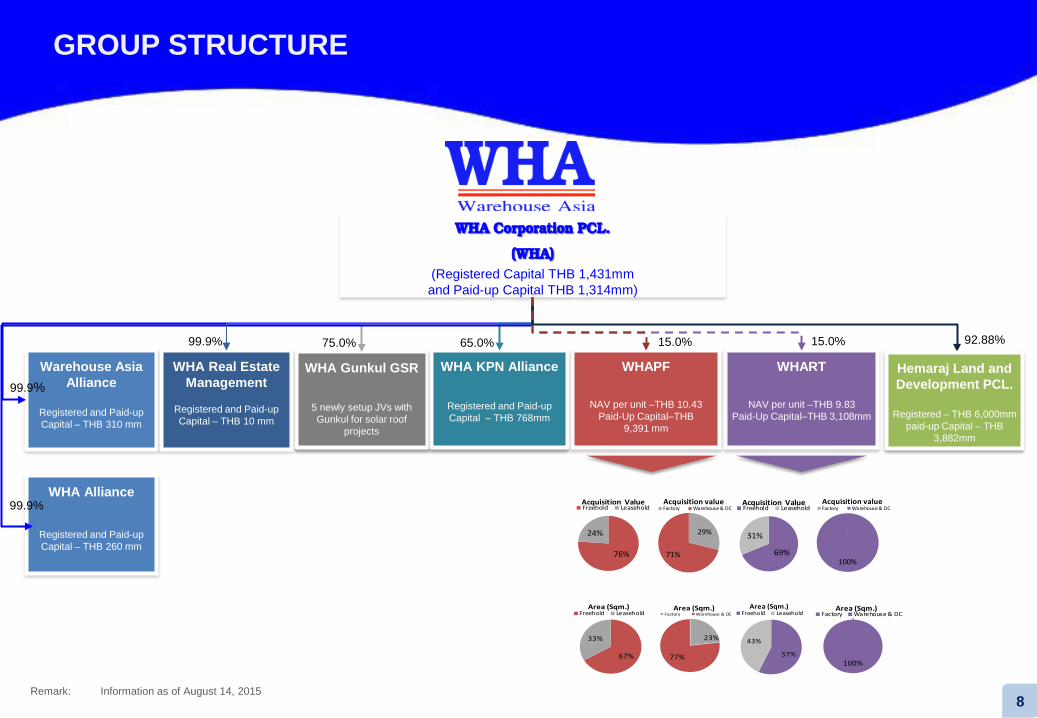

Warehouse Asia Alliance

Registered and Paid-up Capital – THB 310 mm

WHA Alliance

Registered and Paid-up Capital – THB 260 mm

WHAPF

NAV per unit –THB 10.43 Paid-Up Capital–THB

9,391 mm

WHA Gunkul GSR

5 newly setup JVs with Gunkul for solar roof

projects

99.9%

15.0% 75.0%

WHA Corporation PCL.

(WHA) (Registered Capital THB 1,431mm and Paid-up Capital THB 1,314mm)

WHA KPN Alliance

Registered and Paid-up Capital – THB 768mm

76%

24%

Acquisition ValueFreehold Leasehold

29%

71%

Acquisition valueFactory Warehouse & DC

67%

33%

Area (Sqm.)Freehold Leasehold

23%

77%

Area (Sqm.)Factory Warehouse & DC

65.0% 99.9%

WHA Real Estate Management

Registered and Paid-up Capital – THB 10 mm

99.9%

Remark: Information as of August 14, 2015

WHART

NAV per unit –THB 9.83 Paid-Up Capital–THB 3,108mm

15.0%

69%

31%

Acquisition ValueFreehold Leasehold

100%

Acquisition valueFactory Warehouse & DC

57%

43%

Area (Sqm.)Freehold Leasehold

100%

Area (Sqm.)Factory Warehouse & DC

GROUP STRUCTURE

8

Hemaraj Land and Development PCL.

Registered – THB 6,000mm

paid-up Capital – THB 3,882mm

92.88%

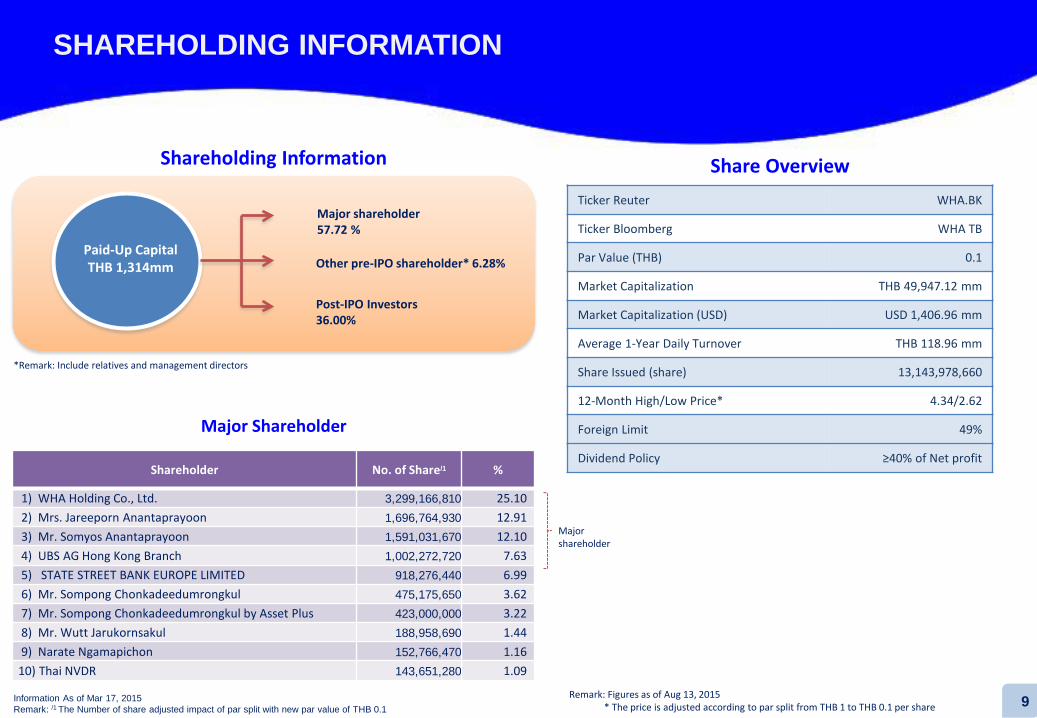

Shareholding Information

Major Shareholder

Shareholder No. of Share/1 %

1) WHA Holding Co., Ltd. 3,299,166,810 25.10 2) Mrs. Jareeporn Anantaprayoon 1,696,764,930 12.91 3) Mr. Somyos Anantaprayoon 1,591,031,670 12.10 4) UBS AG Hong Kong Branch 1,002,272,720 7.63 5) STATE STREET BANK EUROPE LIMITED 918,276,440 6.99 6) Mr. Sompong Chonkadeedumrongkul 475,175,650 3.62 7) Mr. Sompong Chonkadeedumrongkul by Asset Plus 423,000,000 3.22 8) Mr. Wutt Jarukornsakul 188,958,690 1.44 9) Narate Ngamapichon 152,766,470 1.16 10) Thai NVDR 143,651,280 1.09

Paid-Up Capital THB 1,314mm

Major shareholder 57.72 %

Other pre-IPO shareholder* 6.28%

Post-IPO Investors 36.00%

Share Overview

Information As of Mar 17, 2015 Remark: /1 The Number of share adjusted impact of par split with new par value of THB 0.1

*Remark: Include relatives and management directors

Remark: Figures as of Aug 13, 2015 * The price is adjusted according to par split from THB 1 to THB 0.1 per share

Ticker Reuter WHA.BK

Ticker Bloomberg WHA TB

Par Value (THB) 0.1

Market Capitalization THB 49,947.12 mm

Market Capitalization (USD) USD 1,406.96 mm

Average 1-Year Daily Turnover THB 118.96 mm

Share Issued (share) 13,143,978,660

12-Month High/Low Price* 4.34/2.62

Foreign Limit 49%

Dividend Policy ≥40% of Net profit

Major shareholder

SHAREHOLDING INFORMATION

9

WHA GROUP’S BUSINESS PLATFORM AND STRATEGIES

10

Fully Integrated Industrial & Logistic Facility Developer to Provide Total Solution for Both Inbound And Outbound Investment Opportunities

Realignment of Recurring Income Base from Industrial, Logistic, Utility & Power, And Digital Hub

Asset-Light Model by Recycling Capital to Enhance Shareholder Value

New Product Initiatives by way of Partnership with Various Strategic Investors

1

2

3

4

Upward Integration Complementary Business

Industrial Estate

Built-to-suit

• Utilities (Water) • Power

Horizontal Integration

• Warehouses • Factories

Ready-built Factories

11

Ready-built warehouses

• Move up value chain by immediately having land bank located in strategic locations (Central and Eastern region, all of which are non-flood area)

• Apart from 538 equity MW under IPP and SPP in our portfolio which will grow in line with the growth of IEs, we also focus on the high-value product from utilities and power business particularly renewable energy e.g. waste-to-energy and solar rooftop to generate stable income whilst serving the customers on the industrial estates

• Increase its product variety of Ready-Built warehouse and factory to cover full logistic value chain and expand its customer base

WHA Together with Hemaraj Becomes Fully-Integrated Industrial & Logistic Developer

• WHA together with Hemaraj would be renowned for its excellence in providing total solutions for industrial and trade inbound investments

• Increase our readiness to spearhead neighboring countries expansion i.e. Cambodia and Vietnam by leveraging on current Hemaraj’s effort to create IE platform in those countries

• Upon the opening of AEC in late 2015 and future infrastructure development among ASEAN countries, Thailand would be investment hub of increasing importance and thus we would be more than ready to tap these new opportunities

WHA is Well-Equipped for Both Inbound and Outbound Investment Opportunities

1) FULLY INTEGRATED INDUSTRIAL & LOGISTIC FACILITY DEVELOPER READY FOR INBOUND AND OUTBOUND INVESTMENT OPPORTUNITIES

Enhance WHA’s built-to-suit warehouse and factory business by increase product variety and move up value chain

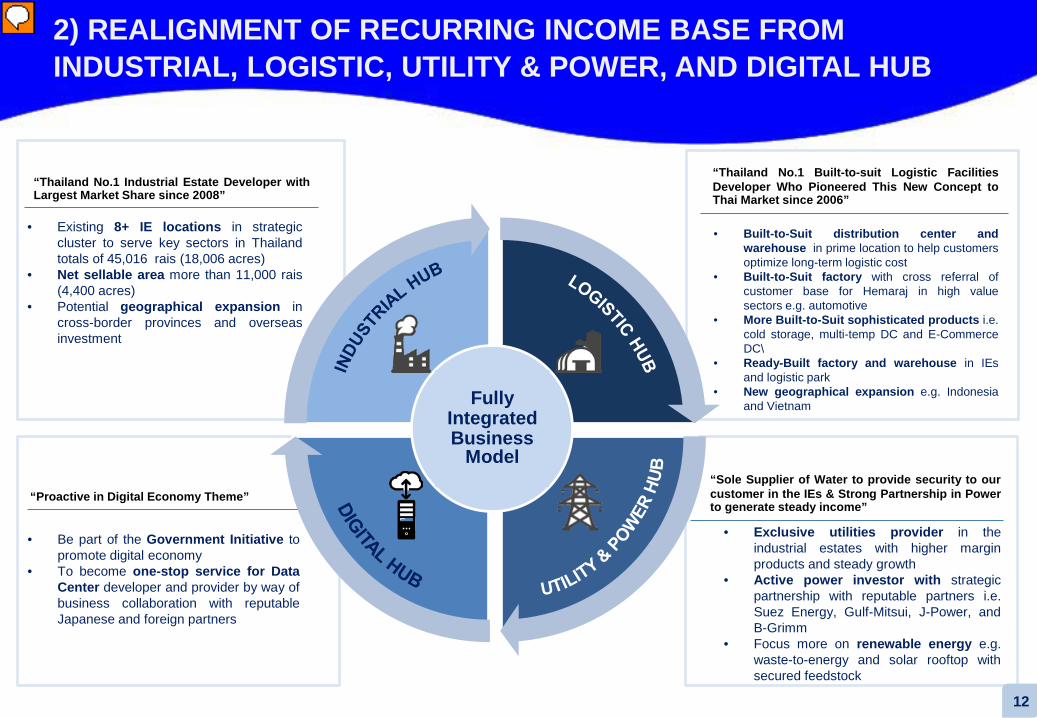

2) REALIGNMENT OF RECURRING INCOME BASE FROM INDUSTRIAL, LOGISTIC, UTILITY & POWER, AND DIGITAL HUB

• Be part of the Government Initiative to promote digital economy

• To become one-stop service for Data Center developer and provider by way of business collaboration with reputable Japanese and foreign partners

• Existing 8+ IE locations in strategic cluster to serve key sectors in Thailand totals of 45,016 rais (18,006 acres)

• Net sellable area more than 11,000 rais (4,400 acres)

• Potential geographical expansion in cross-border provinces and overseas investment

“Thailand No.1 Industrial Estate Developer with Largest Market Share since 2008”

“Proactive in Digital Economy Theme”

• Exclusive utilities provider in the industrial estates with higher margin products and steady growth

• Active power investor with strategic partnership with reputable partners i.e. Suez Energy, Gulf-Mitsui, J-Power, and B-Grimm

• Focus more on renewable energy e.g. waste-to-energy and solar rooftop with secured feedstock

• Built-to-Suit distribution center and warehouse in prime location to help customers optimize long-term logistic cost

• Built-to-Suit factory with cross referral of customer base for Hemaraj in high value sectors e.g. automotive

• More Built-to-Suit sophisticated products i.e. cold storage, multi-temp DC and E-Commerce DC\

• Ready-Built factory and warehouse in IEs and logistic park

• New geographical expansion e.g. Indonesia and Vietnam

“Thailand No.1 Built-to-suit Logistic Facilities Developer Who Pioneered This New Concept to Thai Market since 2006”

“Sole Supplier of Water to provide security to our customer in the IEs & Strong Partnership in Power to generate steady income”

Fully Integrated Business

Model

12

Highly Stable CF from

Investment

Utilize Recurring

Income Stream

Well-balanced Portfolio and

Capital Structure

All Invested Assets Generate Revenue

Strong track record in terms of occupancy rate

To hold minimal non-income generating assets

Strong Stability of Rental Profit

Secured LT contract with growth in rental rate

Attractive EBITDA margin

Low maintenance cost

Capital Structure Optimization

Asset-Optimization Model

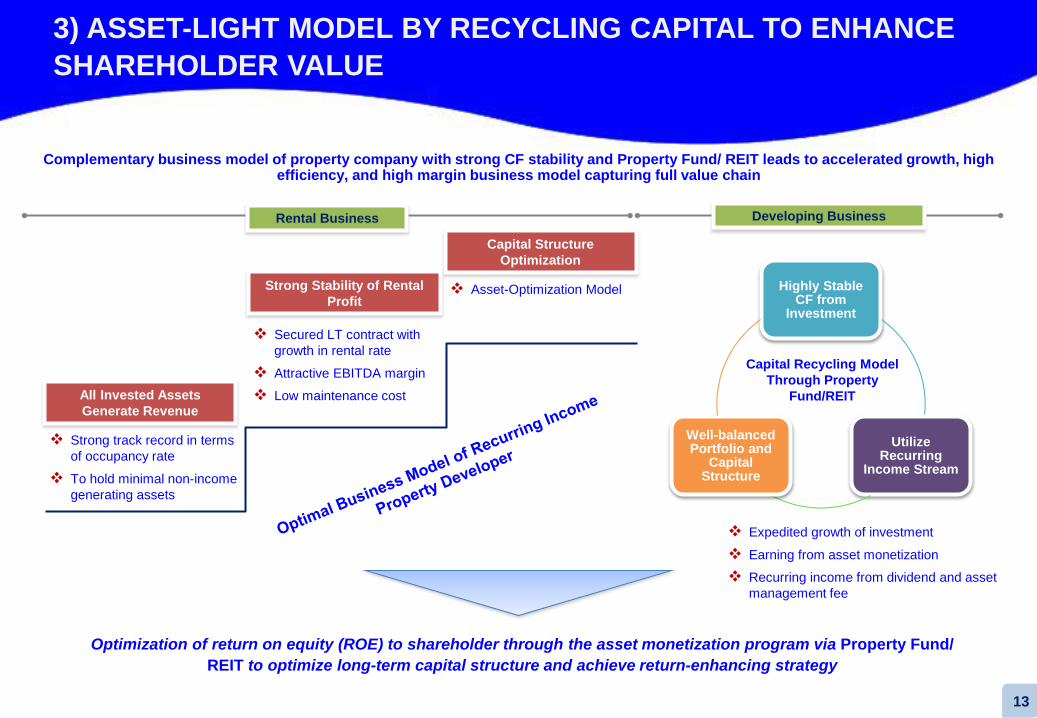

Optimization of return on equity (ROE) to shareholder through the asset monetization program via Property Fund/ REIT to optimize long-term capital structure and achieve return-enhancing strategy

Rental Business Developing Business

Expedited growth of investment

Earning from asset monetization

Recurring income from dividend and asset management fee

Complementary business model of property company with strong CF stability and Property Fund/ REIT leads to accelerated growth, high efficiency, and high margin business model capturing full value chain

Capital Recycling Model Through Property

Fund/REIT

13

3) ASSET-LIGHT MODEL BY RECYCLING CAPITAL TO ENHANCE SHAREHOLDER VALUE

4) NEW PRODUCT INITIATIVES BY WAY OF PARTNERSHIP WITH VARIOUS STRATEGIC INVESTORS

14

Built-to-Suit Logistic Facilities - Warehouse - Distribution Center

Built-to-Suit Factory

Warehouse Farm

Other Recurring Asset - Office

Other Potential Utilities

Products

Utility Business Industrial Estate Power

Business

Renewable Energy (VSPP) + +

Ready-built warehouse &

factory

+ Data Center

Other Multi-Modal

Logistic Mode

- Right of use from gas and steam pipeline

- Revenue-sharing from telecommunication cable

- Waste-to-energy - Solar Rooftop

New product initiatives

Spearheading into new frontiers or entering into new business ventures, WHA will leverage on the business partnership with local partners and/or strategic investors to succeed in the new initiatives

Strategic Partnership

II. Key Business Plan III. Business Updates

IV. Recent Developments & Key Events

VI. Appendix

V. Q1 2015 Financial Performance

I. Business Overview

AGENDA

15

WHA’s Key Business Plan for Hemaraj

Execution of Debt Take-Out Plan

Create Solid Growth Platform For New and

International Expansion

Focus More on Energy, Utilities, and New

Infrastructure-Related Business

WHA – Key Business Strategies for Hemaraj

16

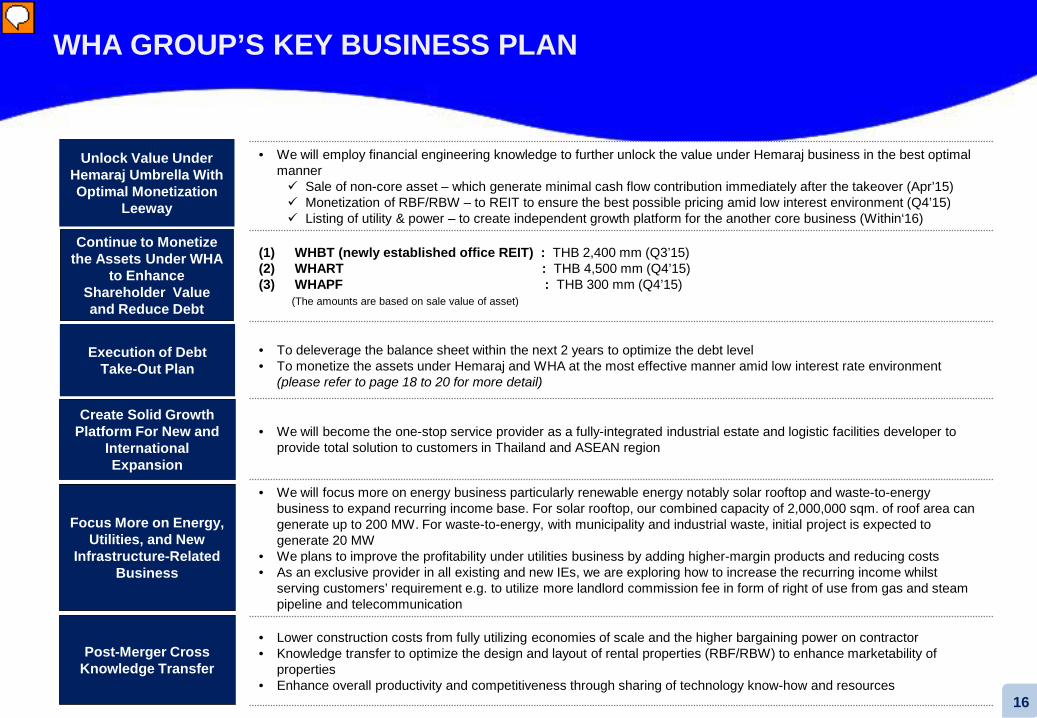

WHA GROUP’S KEY BUSINESS PLAN

Continue to Monetize the Assets Under WHA

to Enhance Shareholder Value and Reduce Debt

• We will employ financial engineering knowledge to further unlock the value under Hemaraj business in the best optimal manner Sale of non-core asset – which generate minimal cash flow contribution immediately after the takeover (Apr’15) Monetization of RBF/RBW – to REIT to ensure the best possible pricing amid low interest environment (Q4’15) Listing of utility & power – to create independent growth platform for the another core business (Within‘16)

(1) WHBT (newly established office REIT) : THB 2,400 mm (Q3’15) (2) WHART : THB 4,500 mm (Q4’15) (3) WHAPF : THB 300 mm (Q4’15) (The amounts are based on sale value of asset)

• To deleverage the balance sheet within the next 2 years to optimize the debt level • To monetize the assets under Hemaraj and WHA at the most effective manner amid low interest rate environment

(please refer to page 18 to 20 for more detail)

• We will become the one-stop service provider as a fully-integrated industrial estate and logistic facilities developer to provide total solution to customers in Thailand and ASEAN region

• We will focus more on energy business particularly renewable energy notably solar rooftop and waste-to-energy business to expand recurring income base. For solar rooftop, our combined capacity of 2,000,000 sqm. of roof area can generate up to 200 MW. For waste-to-energy, with municipality and industrial waste, initial project is expected to generate 20 MW

• We plans to improve the profitability under utilities business by adding higher-margin products and reducing costs • As an exclusive provider in all existing and new IEs, we are exploring how to increase the recurring income whilst

serving customers’ requirement e.g. to utilize more landlord commission fee in form of right of use from gas and steam pipeline and telecommunication

• Lower construction costs from fully utilizing economies of scale and the higher bargaining power on contractor • Knowledge transfer to optimize the design and layout of rental properties (RBF/RBW) to enhance marketability of

properties • Enhance overall productivity and competitiveness through sharing of technology know-how and resources

Unlock Value Under Hemaraj Umbrella With Optimal Monetization

Leeway

Post-Merger Cross Knowledge Transfer

KEY EARNING OUTLOOK

17

Leader in Industrial & Logistics in the Region

with Comprehensive Utilities and Power

Business

Post-Merger Integration

Completion of Debt Take-Out

Plan

Solid Platform for Multi-Modal Expansions

• Substantial debt take-out to lower interest cost every year without significant impact on recurring earning/ cash flow

• Potential group restructuring to fully integrate the business platform e.g. share swap

• Expand to selected new frontiers • Recurring gain from monetization

program

Post-Merger Transition

• New business ventures to fulfill group policy

• Full realization of utility and power business

• Full business collaboration and synergy with in the group

• Full enhancement of productivity of human capital

Solid Geographical Expansion & Multi-Modal Effect

2015

onwards

2017

18 Strictly Private & Confidential

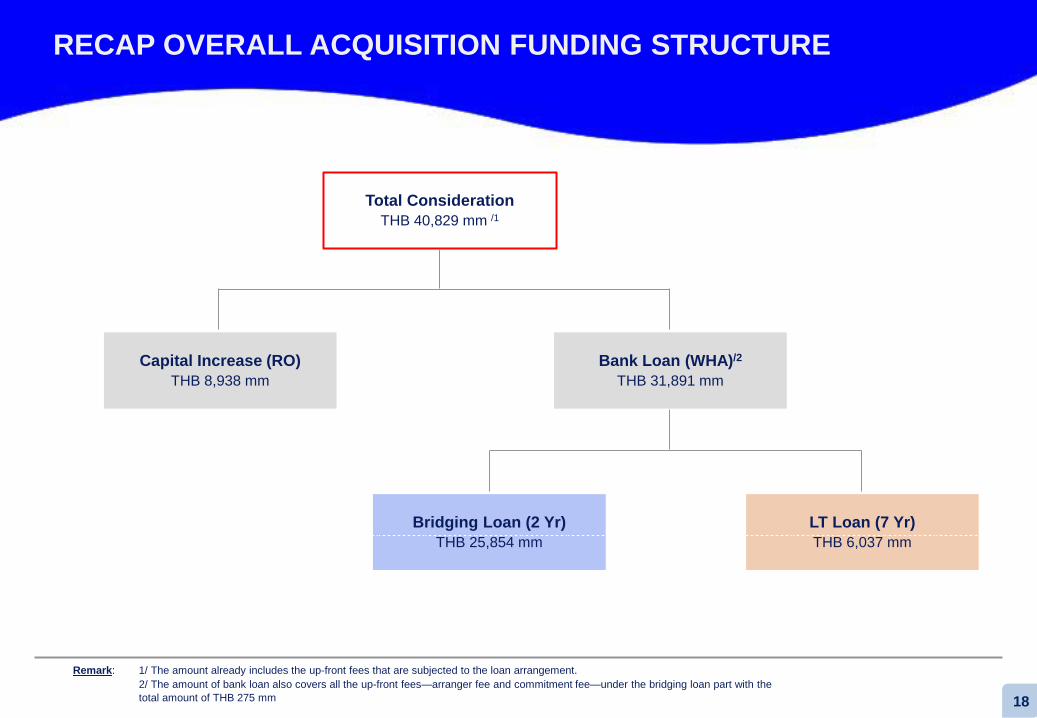

Total Consideration THB 40,829 mm /1

Capital Increase (RO) THB 8,938 mm

Bank Loan (WHA)/2

THB 31,891 mm

Bridging Loan (2 Yr) THB 25,854 mm

LT Loan (7 Yr) THB 6,037 mm

Remark: 1/ The amount already includes the up-front fees that are subjected to the loan arrangement. 2/ The amount of bank loan also covers all the up-front fees—arranger fee and commitment fee—under the bridging loan part with the

total amount of THB 275 mm

RECAP OVERALL ACQUISITION FUNDING STRUCTURE

18

19 Strictly Private & Confidential

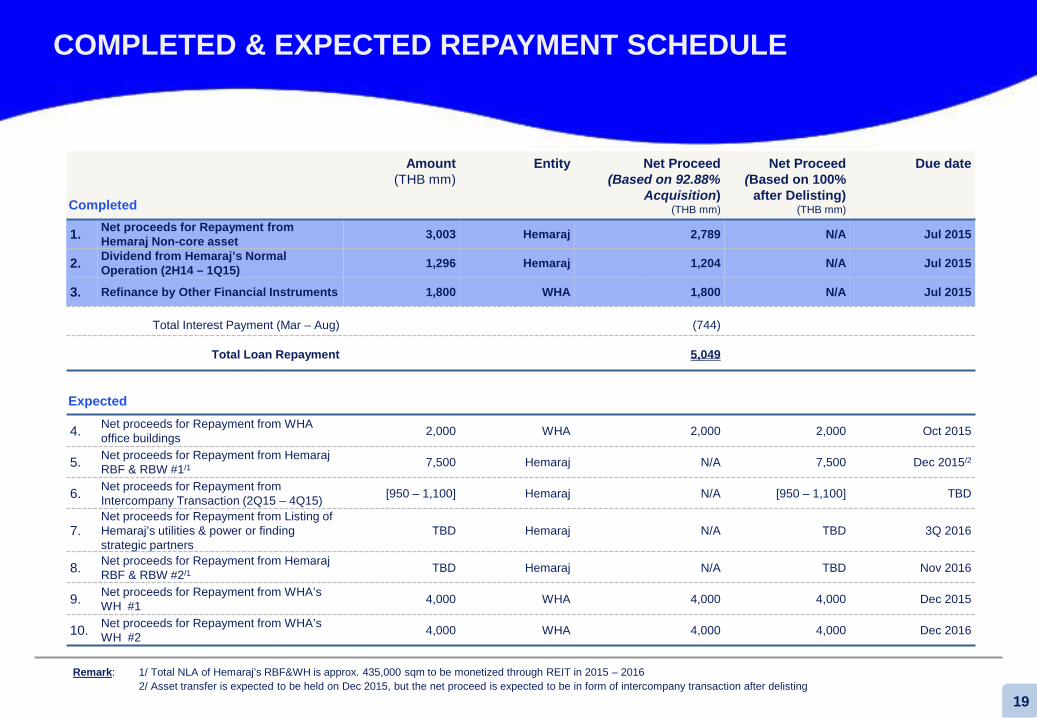

Amount (THB mm)

Entity Net Proceed (Based on 92.88%

Acquisition) (THB mm)

Net Proceed (Based on 100%

after Delisting) (THB mm)

Due date

1. Net proceeds for Repayment from Hemaraj Non-core asset 3,003 Hemaraj 2,789 N/A Jul 2015

2. Dividend from Hemaraj’s Normal Operation (2H14 – 1Q15) 1,296 Hemaraj 1,204 N/A Jul 2015

3. Refinance by Other Financial Instruments 1,800 WHA 1,800 N/A Jul 2015

Total Interest Payment (Mar – Aug) (744)

Total Loan Repayment 5,049

Remark: 1/ Total NLA of Hemaraj’s RBF&WH is approx. 435,000 sqm to be monetized through REIT in 2015 – 2016 2/ Asset transfer is expected to be held on Dec 2015, but the net proceed is expected to be in form of intercompany transaction after delisting

COMPLETED & EXPECTED REPAYMENT SCHEDULE

19

4. Net proceeds for Repayment from WHA office buildings 2,000 WHA 2,000 2,000 Oct 2015

5. Net proceeds for Repayment from Hemaraj RBF & RBW #1/1 7,500 Hemaraj N/A 7,500 Dec 2015/2

6. Net proceeds for Repayment from Intercompany Transaction (2Q15 – 4Q15) [950 – 1,100] Hemaraj N/A [950 – 1,100] TBD

7. Net proceeds for Repayment from Listing of Hemaraj’s utilities & power or finding strategic partners

TBD Hemaraj N/A TBD 3Q 2016

8. Net proceeds for Repayment from Hemaraj RBF & RBW #2/1 TBD Hemaraj N/A TBD Nov 2016

9. Net proceeds for Repayment from WHA’s WH #1 4,000 WHA 4,000 4,000 Dec 2015

10. Net proceeds for Repayment from WHA’s WH #2 4,000 WHA 4,000 4,000 Dec 2016

Expected

Completed

20 Strictly Private & Confidential

Consolidated Gearing Ratio 2.99x

3.42x 3.30x

1.91x 1.68x 1.64x 1.32x 0.95x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

1Q'2015 2Q'2015F 3Q'2015F 4Q'2015F 1Q'2016F 2Q'2016F 3Q'2016F 4Q'2016F

Hemaraj REIT

GEARING RATIO

20

Projected Gearing Ratio

Utility & Power Spin-Off

WHA Office REIT

Proceed from Warrant Exercise

WHART Capital Increase Hemaraj REIT

Capital Increase

WHART Capital Increase

Target 2.5x

Remarks: Excluding the impact of normal debt arising from normal CAPEX

III. Business Updates II. Key Business Plan

IV. Recent Developments & Key Events

VI. Appendix

V. Q1 2015 Financial Performance

I. Business Overview

AGENDA

21

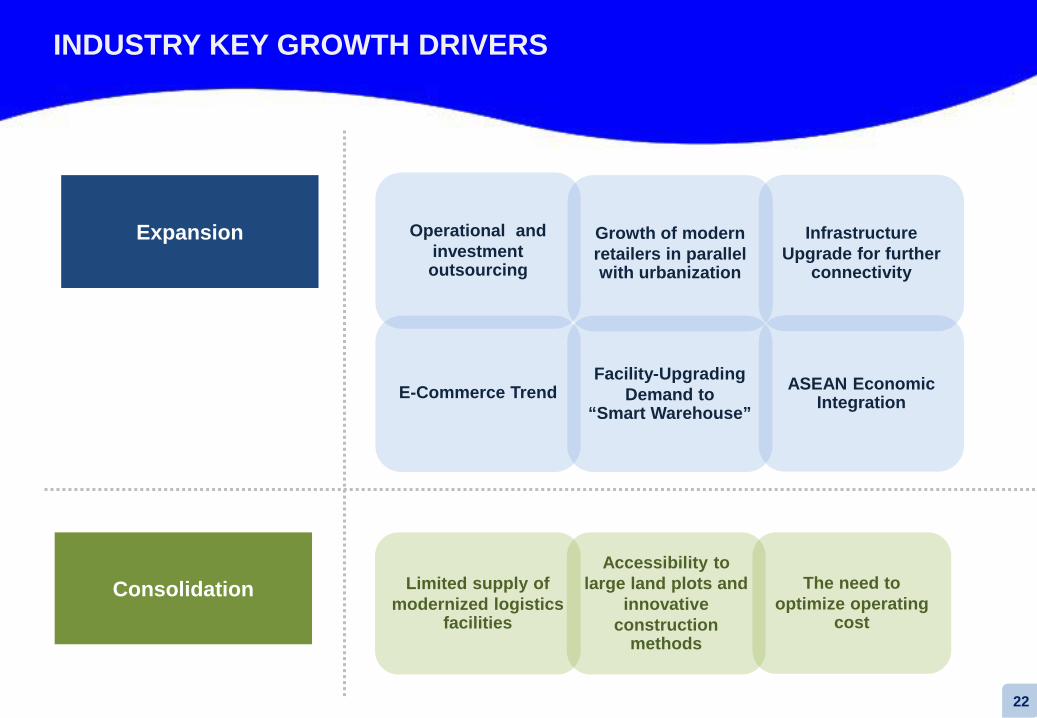

Expansion

Consolidation

Operational and investment outsourcing

Growth of modern retailers in parallel with urbanization

E-Commerce Trend Facility-Upgrading

Demand to “Smart Warehouse”

Limited supply of modernized logistics

facilities

Accessibility to large land plots and

innovative construction

methods

INDUSTRY KEY GROWTH DRIVERS

22

Infrastructure Upgrade for further

connectivity

ASEAN Economic Integration

The need to optimize operating

cost

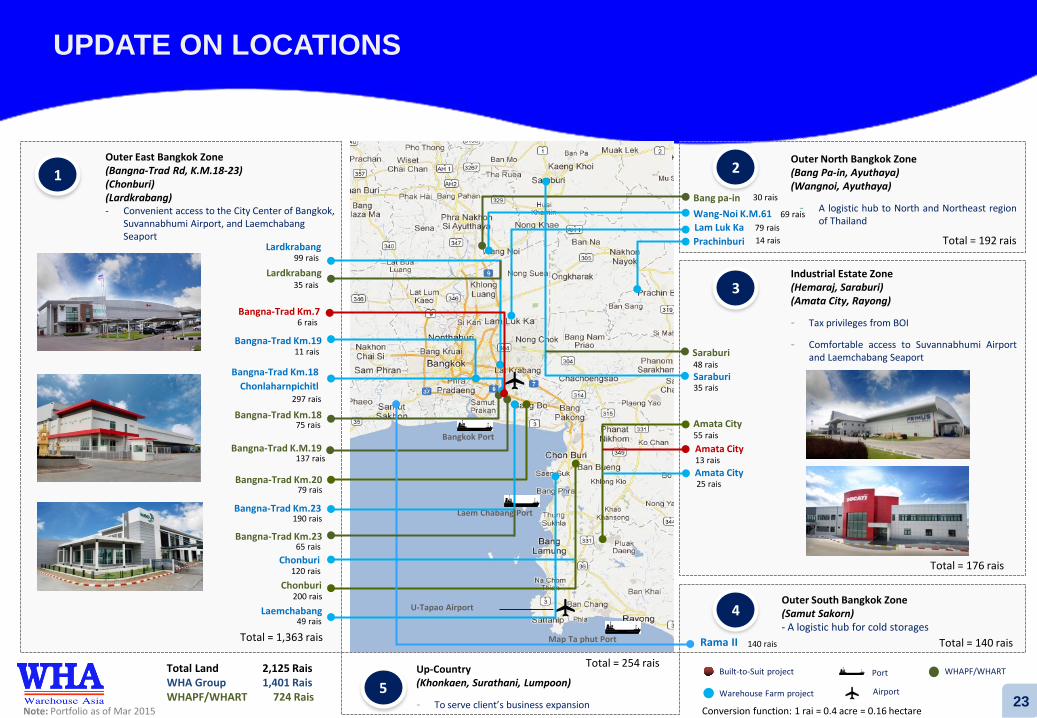

U-Tapao Airport

Bangkok Port

Laem Chabang Port

Map Ta phut Port

Bangna-Trad K.M.19

Bangna-Trad Km.18

Bangna-Trad Km.19

Lardkrabang

Chonburi

Bangna-Trad Km.20

Saraburi

Amata City

Bang pa-in Wang-Noi K.M.61

Outer East Bangkok Zone (Bangna-Trad Rd, K.M.18-23) (Chonburi) (Lardkrabang) - Convenient access to the City Center of Bangkok,

Suvannabhumi Airport, and Laemchabang Seaport

Industrial Estate Zone (Hemaraj, Saraburi) (Amata City, Rayong)

- Tax privileges from BOI

- Comfortable access to Suvannabhumi Airport and Laemchabang Seaport

2 Outer North Bangkok Zone (Bang Pa-in, Ayuthaya) (Wangnoi, Ayuthaya)

- A logistic hub to North and Northeast region of Thailand

Note: Portfolio as of Mar 2015

Built-to-Suit project

Warehouse Farm project

WHAPF/WHART Port

Airport

Bangna-Trad Km.23

3

1

Prachinburi

Bangna-Trad Km.18 Chonlaharnpichitl

Laemchabang 4

Rama II 140 rais

99 rais

11 rais

297 rais

75 rais

137 rais

79 rais

190 rais

200 rais

49 rais

30 rais

14 rais

35 rais

55 rais

69 rais

Total = 1,363 rais

Total = 192 rais

Total = 176 rais

Outer South Bangkok Zone (Samut Sakorn) - A logistic hub for cold storages

Total Land 2,125 Rais WHA Group 1,401 Rais WHAPF/WHART 724 Rais

135 rais

Up-Country (Khonkaen, Surathani, Lumpoon)

- To serve client’s business expansion 5

Total = 254 rais

Total = 140 rais

Conversion function: 1 rai = 0.4 acre = 0.16 hectare

Lardkrabang 35 rais

Bangna-Trad Km.23 65 rais

48 rais

Saraburi

Amata City 13 rais

Bangna-Trad Km.7 6 rais

Chonburi 120 rais

23

UPDATE ON LOCATIONS

Lam Luk Ka 79 rais

Amata City 25 rais

2006 2007 2008 2009 2010 2011 2012 2013 2014 Q2 2015

294,261

389,982

147,086

256,434

258,330 152,532

1,921,021

863,2111

Remarks: 1) This area is calculated from the estimated ratio of 1-rai of land = 1,000-sqm leasable area; the actual constructed area is subject to change depending on actual design to suit with clients’ requirement

Key Takeaways

During Q2 2015, WHA secured pre-lease area/ new contracts for 22,897 sqm. Majority of the available area in this quarter is newly constructed general warehouses in prime area such as Bangna-Trad area and

Lardkrabang SJ Infinite 1 business complex also performs well, it can secure contract close to 60% while another 7% are under offer with high

potential WHA targets to secure pre-leased area/ new contract around 200,000 sqm. this year

Developed/ Developing & Occupied area for 2006-1Q15

Unit: Sqm.

88,913 141,619 141,619

169,433 192,341 298,139

505,051

1,108,740

891,286

Area Completed– Area that currently generates revenue Area Available for Lease – Area that is available to serve immediate demand Area Pre-Leased – Area that is leased before the construction is finished Area Sold to WHAPF/WHART – Area that is sold to the property fund or REIT Land Held for Future Development – Area that is reserved for future development

63,159 207,043

101,531

65,120

259,269 233,030

255,462

557,089 557,089

280,120

1,161,598

OR 100% 100% 100% 100% 100% 100% 100% 100% 80% 81%

IMPRESSIVE TRACK RECORD OF GROWTH

24

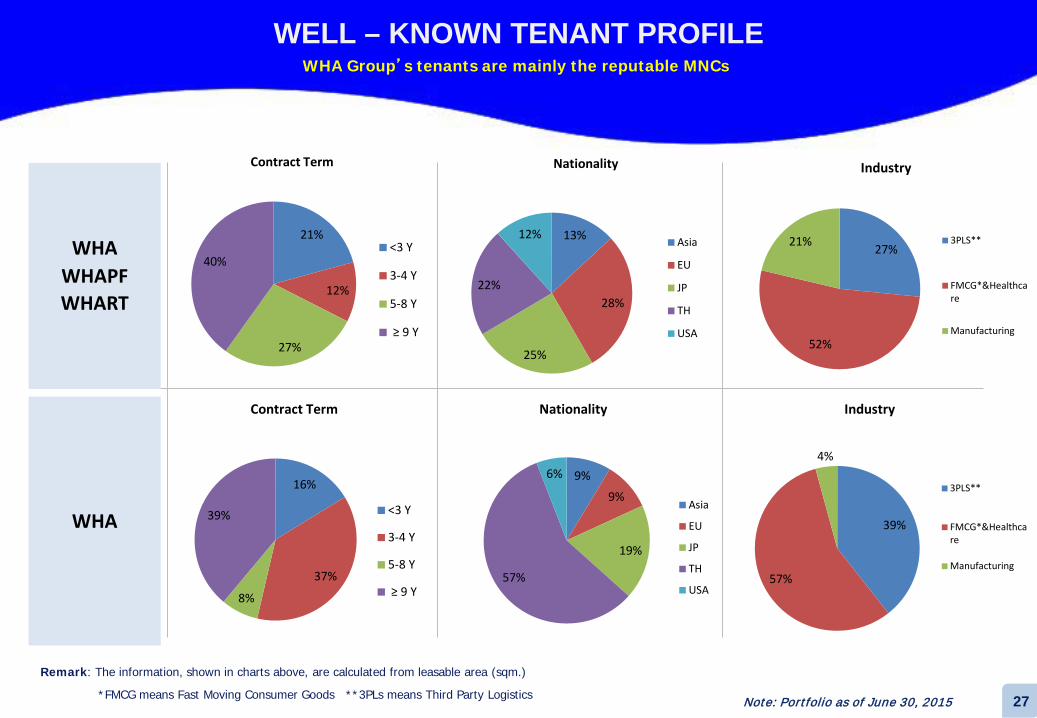

WHA Group’s tenants are mainly the reputable MNCs

Note: Portfolio as of June 30, 2015

WELL – KNOWN TENANT PROFILE

25

WHA Group’s tenants are mainly the reputable MNCs

USA Europe Thai Japan Asia

WELL – KNOWN TENANT PROFILE

26 Note: Portfolio as of June 30, 2015

WHA Group’s tenants are mainly the reputable MNCs

Remark: The information, shown in charts above, are calculated from leasable area (sqm.)

*FMCG means Fast Moving Consumer Goods **3PLs means Third Party Logistics

WHA WHAPF WHART

WHA

Note: Portfolio as of June 30, 2015

WELL – KNOWN TENANT PROFILE

27

16%

37%

8%

39% <3 Y

3-4 Y

5-8 Y

≥ 9 Y

Contract Term Nationality

9%

9%

19%

57%

6%

Asia

EU

JP

TH

USA

39%

57%

4%

3PLS**

FMCG*&Healthcare

Manufacturing

Industry

21%

12%

27%

40% <3 Y

3-4 Y

5-8 Y

≥ 9 Y

Contract Term

13%

28%

25%

22%

12% Asia

EU

JP

TH

USA

Nationality

27%

52%

21% 3PLS**

FMCG*&Healthcare

Manufacturing

Industry

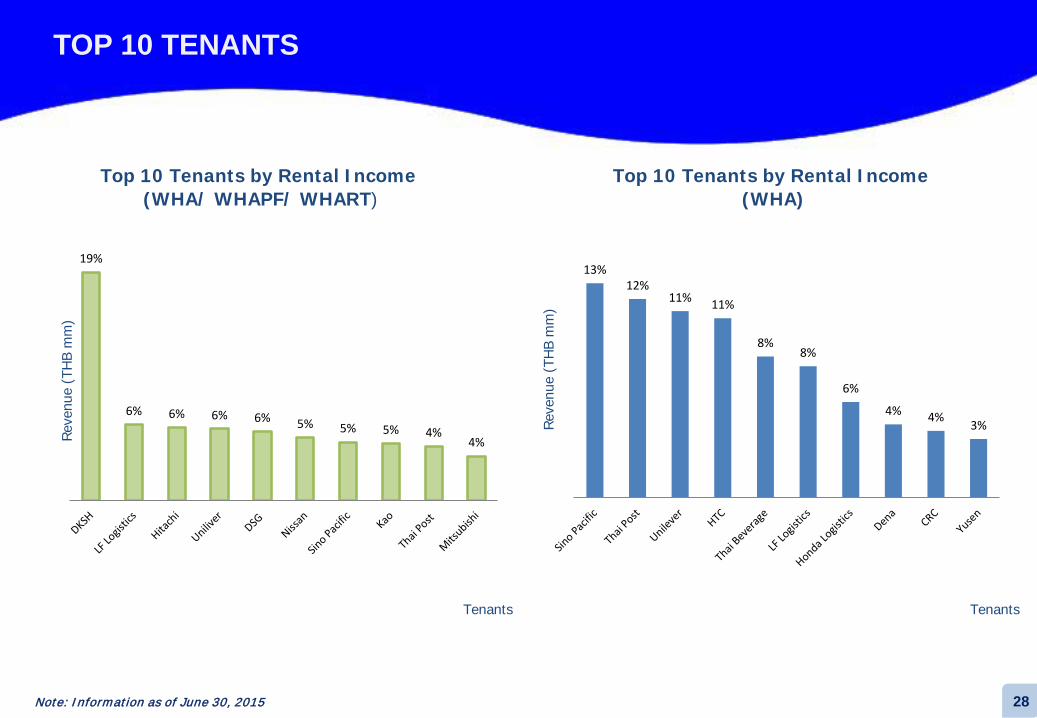

Top 10 Tenants by Rental Income (WHA)

Top 10 Tenants by Rental Income (WHA/ WHAPF/ WHART)

Reve

nue

(TH

B m

m)

Tenants

Reve

nue

(TH

B m

m)

Tenants

19%

6% 6% 6% 6% 5% 5% 5% 4% 4%

Note: Information as of June 30, 2015

TOP 10 TENANTS

28

13% 12%

11% 11%

8% 8%

6%

4% 4% 3%

I. Business Overview II. Key Business Plan

IV. Recent Developments & Key Events

VI. Appendix

V. Q1 2015 Financial Performance

AGENDA

III. Business Updates

29

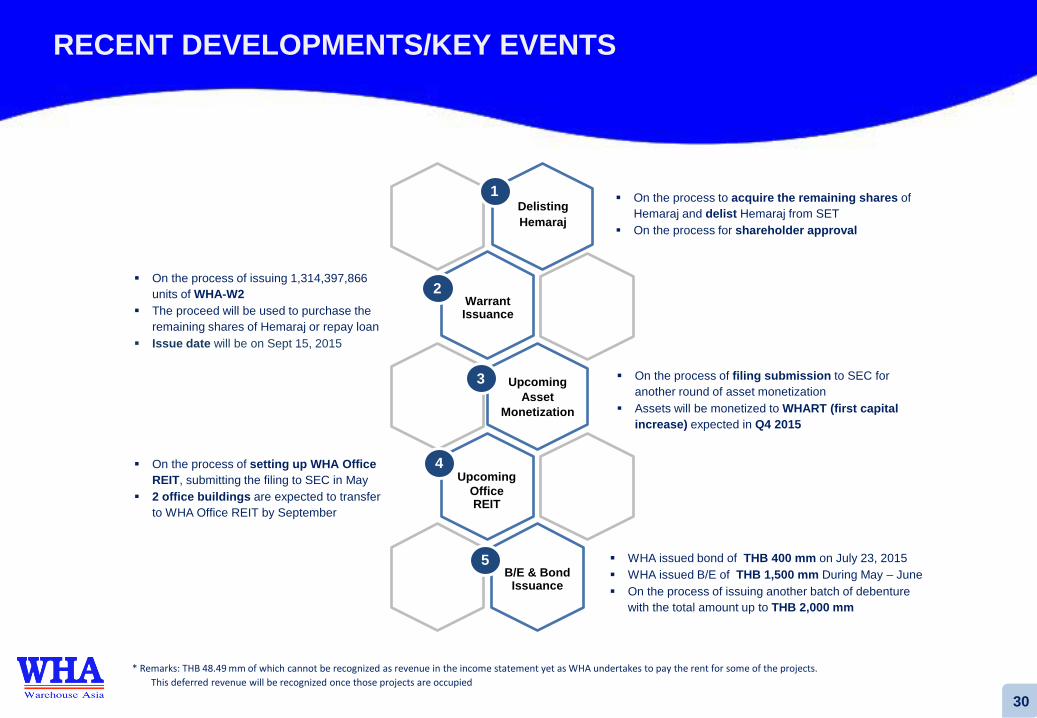

1

2

3

On the process of filing submission to SEC for

another round of asset monetization Assets will be monetized to WHART (first capital

increase) expected in Q4 2015

WHA issued bond of THB 400 mm on July 23, 2015 WHA issued B/E of THB 1,500 mm During May – June On the process of issuing another batch of debenture

with the total amount up to THB 2,000 mm

On the process to acquire the remaining shares of

Hemaraj and delist Hemaraj from SET On the process for shareholder approval

* Remarks: THB 48.49 mm of which cannot be recognized as revenue in the income statement yet as WHA undertakes to pay the rent for some of the projects. This deferred revenue will be recognized once those projects are occupied

On the process of issuing 1,314,397,866

units of WHA-W2 The proceed will be used to purchase the

remaining shares of Hemaraj or repay loan Issue date will be on Sept 15, 2015

4

5

Delisting Hemaraj

Warrant Issuance

Upcoming Asset

Monetization

On the process of setting up WHA Office REIT, submitting the filing to SEC in May

2 office buildings are expected to transfer to WHA Office REIT by September

RECENT DEVELOPMENTS/KEY EVENTS

30

Upcoming Office REIT

B/E & Bond Issuance

31 Strictly Private & Confidential

HEMARAJ’S DELISTING PROCESS

Delisting Hemaraj 1

RECENT DEVELOPMENTS/KEY EVENTS (CON’T)

31

WHA Shareholders’ Approval Process

(1) Approve warrant Issuance – 75% vote

(2) Approve delisting – 50% vote

4 September 2015

Hemaraj Shareholders’ Approval Process

(1) Approve delisting – 75% vote + 10% veto right 30 September 2015

SET Approval Process

(1) Delisting

(2) Tender Offer

October – November 2015

Tender Offer Period

(45 Business Day) November 2015 – January 2016

Settlement Process End of January 2016

Delist End of January 2016

1

32 Strictly Private & Confidential

WHA WARRANT NO.2 (WHA-W2)

Warrant Issuance 2

RECENT DEVELOPMENTS/KEY EVENTS (CON’T)

32

Allocation methods : WHA-W2 is issued and allocated to existing shareholders

Number of warrants issued : 1,314,397,866 units

Price per unit : THB -0-

Exercise ratio : One unit of WHA-W2 Warrants for one ordinary share

Exercise price : Baht 2.70 per share

Issuance date : 15 September 2015

Allocation ratio : 10 existing ordinary shares to one unit of WHA-W2 Warrants

Purpose of the issuance of WHA-W2 :

• To purchase the shares of Hemaraj Land and Development Public Company Limited for delisting of its shares from the Stock Exchange of Thailand; or

• to repayment of loan of financial institution; or • to use as working capital of the Company

2

Asset Approx. NLA Snapshot

WHA Mega Logistics Center Wangnoi 61 Wangnoi, Phranakhon Si Ayutthaya

60,000

sqm

WHA Mega Logistics Center Chonlaharnpichit km 4 Chonlaharnpichit Rd, Samutprakarn

80,000

sqm

WHA Mega Logistics Center Saraburi Hemaraj Saraburi Industrial Land, Saraburi

32,900

sqm

TO WHART

Asset Approx. NLA Snapshot

Two Buildings in WHA Mega Logistics Center Bangna-Trad km.19* Bangna-Trad km 19, Samutprakarn

14,000

sqm

DSG Modification Nongkae, Saraburi

-

TO WHAPF

• Expected total sale value of approx. THB 4,800 mm • Target to complete within 4Q2015

* All the remaining buildings have already been monetized into WHAPF

Upcoming Asset Monetization 3

UPCOMING ASSET MONETIZATION 3

RECENT DEVELOPMENTS/KEY EVENTS (CON’T)

33

Upcoming Office REIT 4

4 UPCOMING OFFICE REIT

Asset SJ I Infinite Business Complex

Ownership Land: Freehold ownership

Building: Freehold ownership

Leasable Area

GFA: 42,905 sqm. NLA: 21,993 sqm.

Completion Date 2014

Asset Bangna Business Complex

Ownership Land: Leasehold right (30 years)

Building: Freehold ownership

Leasable Area

GFA: 9,860 sqm. NLA: 9,335 sqm.

Year Operate 2014

RECENT DEVELOPMENTS/KEY EVENTS (CON’T)

34

Detail

Type Unsecured and unsubordinated debenture entered in name without debenture representative

Currency Thai Baht

Amount THB 400 mm

Interest Rate 3.95 %

Maturity 2 years from the issuing date

Allocation methods Sell to specific buyers no more than 10 names

Purpose 1. To refinance existing loan to reduce cost of financing; or

2. to use as working capital of the Company

Call Option No call option

Underwriters Siam Commercial Bank Public Company Limited; and United Overseas Bank (Thai) Public Company Limited

5 BOND ISSUANCE

RECENT DEVELOPMENTS/KEY EVENTS (CON’T) Bond Issuance 5

35

IV. Performance Outlook

I. Business Overview

IV. Recent Developments & Key Events

VI. Appendix

AGENDA

II. Key Business Plan III. Business Updates

36

PERFORMANCE AND LONG-TERM OUTLOOK BY BUSINESS

37

RENTAL PROPERTY BUSINESS SALE OF PROPERTY BUSINESS

359.93 500.50 551.13

359.93

500.50 551.13

39.1%10.1%

-

100

200

300

400

500

600

2012 2013 2014

1,300

380

1,680

2019

OUTLOOK

4,660

6,980

11,640

2019

1,808.85

6,584.95

4,336.76 1,808.85

6,584.95

4,336.76

264.0%

-34.1%

0

0

0

0

0

0

0

2012 2013 2014

OUTLOOK

Consist of monetization of assets and sale of industrial estate

Consist of monetization of assets

UTILITIES BUSINESS

-

-

2014

-

2,840

2,840

2019

OUTLOOK

1.79

2014

60

1,750

1,810

2019

OUTLOOK

Consist of share of profit and dividend from power business

WHA 2019 – based on the assumption that solar rooftop business will be conducted under WHA itself rather than under JV, hence revenue instead of share of profit will be realized by then

470

280

750

2019

38.38 66.81

146.74

6.27 16.71

23.06

(1.26) (9.53)

44.65 82.26

160.27

84.2%94.8%

2012 2013 2014WHA - Dividend & PM & RMWHA - Other incomeWHA - Share of loss from JV

OUTLOOK

POWER BUSINESS PM RM DIVIDEND & OTHERS

Unit: THB mm

Growth

WHA HEMRAJ

Consist of property and REIT management fee, dividend from property fund and REIT, share of profit from property fund, and other income

1,680

11,640

2,840

1,810

750

18,720

2019

500 551

6,585

4,337

-

-

-

2

82

160

7,168

5,050

2013 2014

TOTAL REVENUE

Rental property Sale of propertiesUtilities PowerPM RM Dividend & Others

OUTLOOK

Remark: Total revenue include share of profit from JV’s and Associates in relation to each business

Unit: THB mm

578.0

- --

578.0

53.7%

0%

2013 2014 2 Q 2 0 1 4 2 Q 2 0 1 5

WHA HEMRAJ Margin Growth

359.9 500.5 551.1

121.4 187.7

228.3 359.9

500.5 551.1

121.4

416.0

69.8%70.5%

39.1% 10.1%

242.7%

-80

12

32

52

72

2012 2013 2014 2 Q 2 0 1 4 2 Q 2 0 1 5

WHA HEMRAJ Margin Growth

44.7 82.3

160.3

28.8 77.8

191.1

44.7 82.3

160.3

28.8

269.0

84.2% 94.8%

832.6%

2012 2013 2014 2 Q 2 0 1 4 2 Q 2 0 1 5

WHA HEMRAJ Growth

1.8 0.1 2.1

383.9

1.8 0.1

386.0

553,980%

2013 2014 2 Q 2 0 1 4 2 Q 2 0 1 5

WHA HEMRAJ Growth

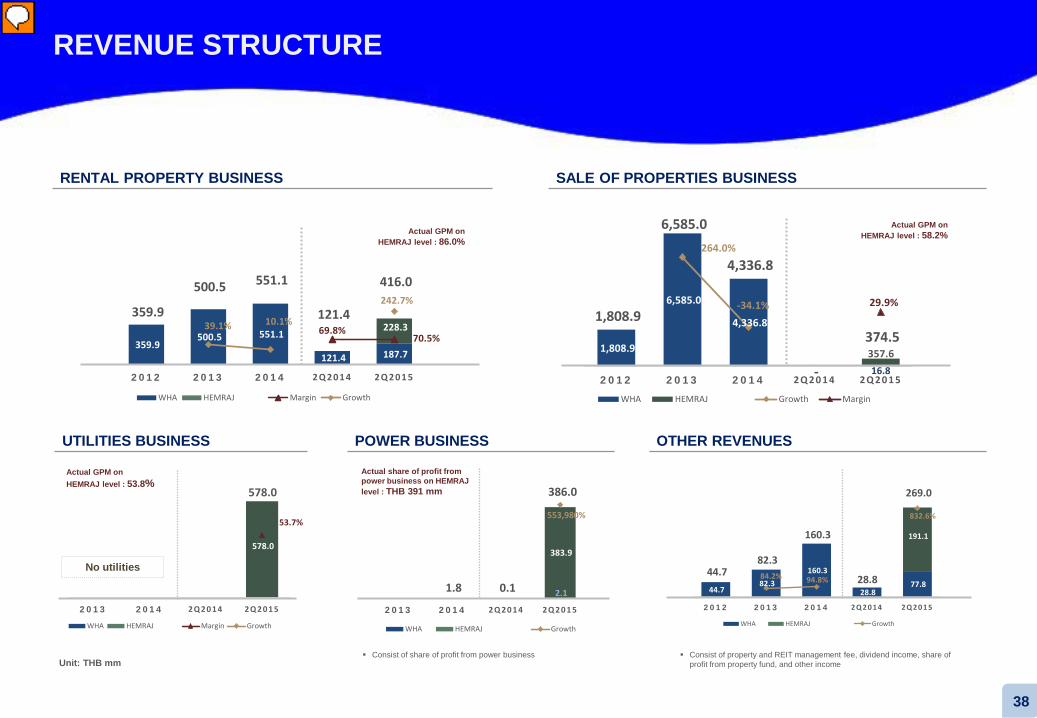

REVENUE STRUCTURE

38

RENTAL PROPERTY BUSINESS

UTILITIES BUSINESS POWER BUSINESS OTHER REVENUES

SALE OF PROPERTIES BUSINESS

Consist of share of profit from power business Consist of property and REIT management fee, dividend income, share of profit from property fund, and other income

No utilities

Actual GPM on HEMRAJ level : 58.2%

Unit: THB mm

1,808.9

6,585.0

4,336.8

- 16.8 357.6

1,808.9

6,585.0

4,336.8

-

374.5

264.0%

-34.1% 29.9%

2012 2013 2014 2 Q 2 0 1 4 2 Q 2 0 1 5

WHA HEMRAJ Growth Margin

Actual GPM on HEMRAJ level : 53.8%

Actual share of profit from power business on HEMRAJ level : THB 391 mm

Actual GPM on HEMRAJ level : 86.0%

Unit: THB mm

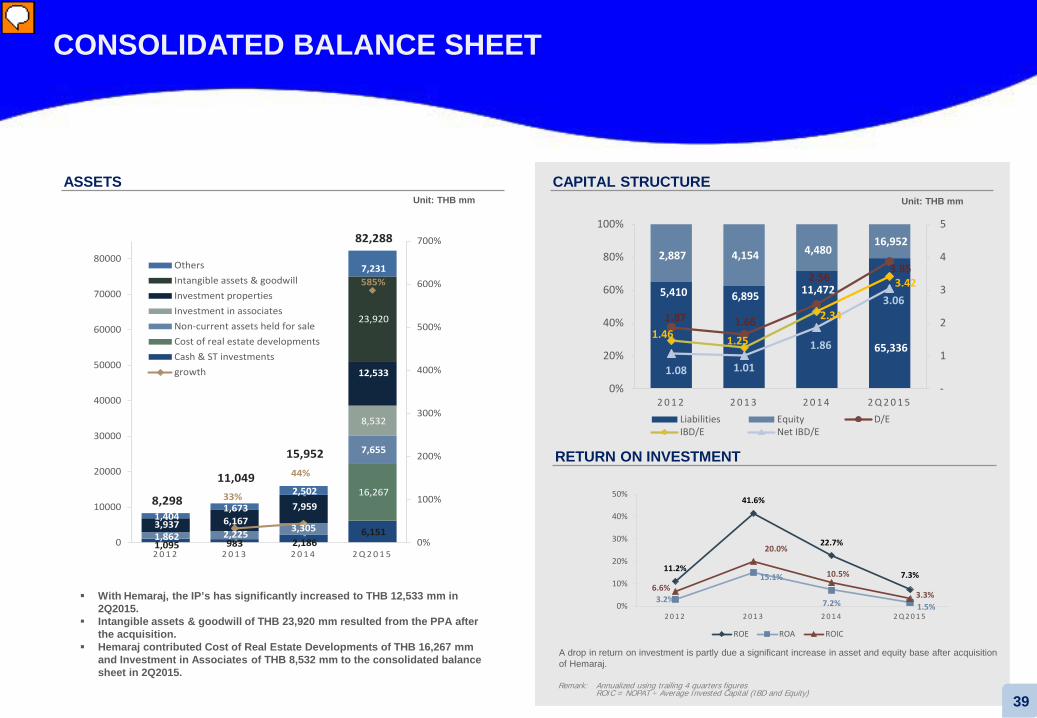

CAPITAL STRUCTURE ASSETS Unit: THB mm

RETURN ON INVESTMENT

Remark: Annualized using trailing 4 quarters figures ROIC = NOPAT ÷ Average Invested Capital (IBD and Equity)

With Hemaraj, the IP’s has significantly increased to THB 12,533 mm in 2Q2015.

Intangible assets & goodwill of THB 23,920 mm resulted from the PPA after the acquisition.

Hemaraj contributed Cost of Real Estate Developments of THB 16,267 mm and Investment in Associates of THB 8,532 mm to the consolidated balance sheet in 2Q2015.

A drop in return on investment is partly due a significant increase in asset and equity base after acquisition of Hemaraj.

CONSOLIDATED BALANCE SHEET

39

1,095 983 2,186 6,151

- - -

16,267

1,862 2,225 3,305

7,655

- --

8,532

3,937 6,167 7,959

12,533

--

-

23,920

1,404 1,673

2,502

7,231

8,298

11,049

15,952

82,288

33%

44%

585%

0%

100%

200%

300%

400%

500%

600%

700%

0

10000

20000

30000

40000

50000

60000

70000

80000

2 0 1 2 2 0 1 3 2 0 1 4 2 Q 2 0 1 5

OthersIntangible assets & goodwillInvestment propertiesInvestment in associatesNon-current assets held for saleCost of real estate developmentsCash & ST investmentsgrowth

5,410 6,895 11,472

65,336

2,887 4,154 4,480 16,952

1.87 1.66

2.56 3.85

1.46 1.25

2.34

3.42

1.08 1.01

1.86

3.06

-

1

2

3

4

5

0%

20%

40%

60%

80%

100%

2 0 1 2 2 0 1 3 2 0 1 4 2 Q 2 0 1 5Liabilities Equity D/EIBD/E Net IBD/E

11.2%

41.6%

22.7%

7.3%

3.2%

15.1%

7.2% 1.5%

6.6%

20.0%

10.5%

3.3%0%

10%

20%

30%

40%

50%

2 0 1 2 2 0 1 3 2 0 1 4 2 Q 2 0 1 5

ROE ROA ROIC

2.49%B/E790

4.75%Term Loan

3,245

4.31%Bond7,200

5.53%Acquisition Loan

30,882

4.73%Term Loan

3,281

4.31%Bond7,200

5.60%Acquisition Loan

21,525

Remark: Total loan related to acquisition of HEMRAJ amounted to THB 31,891.91 mm

END OF 1Q2015 Unit: THB mm

Unit: THB mm

END OF 2Q2015

Weighted Average Interest Rate

5.22%

Unit: THB mm

Unit: THB mm

149.30 182.87

294.83

-

200

400

2012 2013 2014

F IN AN C E C O S T

WHA’S DEBT PROFILE – EXCLUDING HEMRAJ

40

Weighted Average Interest Rate

5.20%

50.13

560.93

-

1,000

2 Q 2 0 1 4 2 Q 2 0 1 5

F IN AN C E C O S T

Finance cost related to acquisition of HEMRAJ in 2Q2015: THB 447.3 mm

* Not include HEMRAJ’s finance cost; Consolidated finance cost totaled THB 730.05 mm

*

790

2,040

94 108 126 136 154 176 190 105 115

1,630

500 570

500

700

1,110

435

385

600

280

200

290

2,830

1,724

2,443

986

1,631

154

776

190 105

395

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

B/E Term Loan Debenture 9/2013 (3) Debenture 9/2013 (4) Debenture 9/2013 (5)Debenture 2/2014 (3) Debenture 5/2014 (3) Debenture 5/2014 (5) Debenture 7/2014 (3) Debenture 7/2014 (5)Debenture 7/2014 (7) Debenture 7/2014 (10) Debenture 10/2014 (2.9) Debenture 11/2014 (4)

Unit: THB mm As of 30 Jun 2015

DEBT MATURITY PROFILE – EXCLUDING ACQUISITION LOAN

Remark: Does not include loan related to acquisition of HEMRAJ

WHA’S DEBT PROFILE – EXCLUDING HEMRAJ (CONT’D)

41

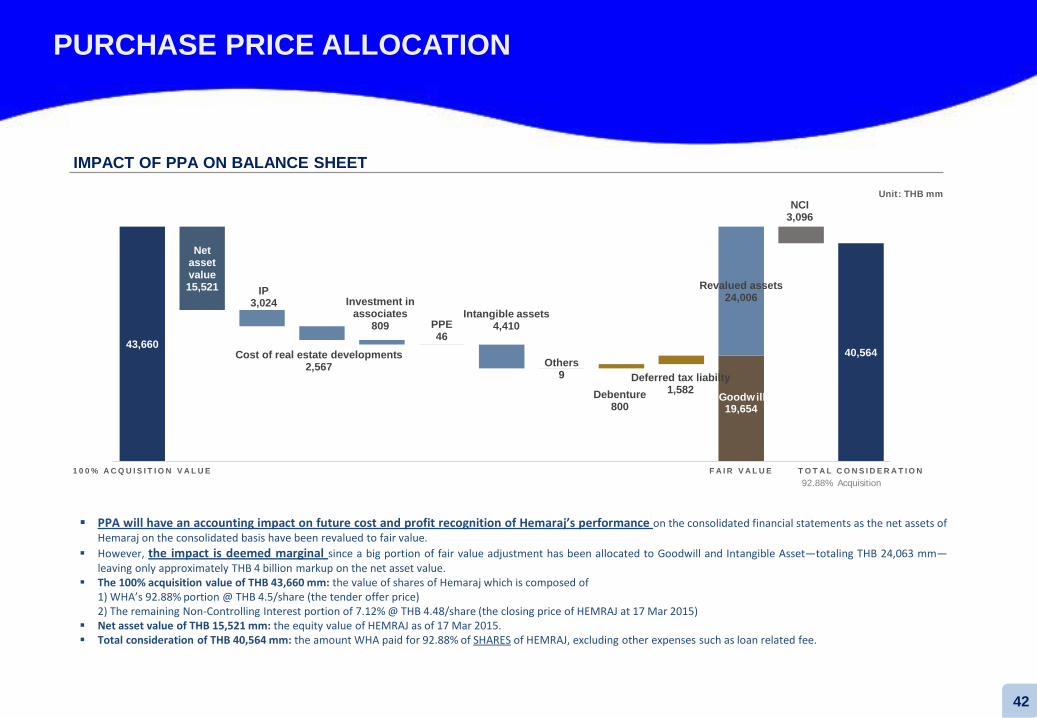

43,660

28,13825,114 22,547 21,737 21,691

17,281 17,272 17,272 18,072 19,654

40,564 40,564

Net asset value15,521 IP

3,024

Cost of real estate developments2,567

Investment in associates

809 PPE46

Intangible assets4,410

Others9

Debenture800

Deferred tax liabilty1,582

Revalued assets24,006

NCI3,096

1 0 0 % A C Q U I S I T I O N V A L U E F A I R V A L U E T O T A L C O N S I D E R A T I O N

Goodwill

92.88% Acquisition

Unit: THB mm

IMPACT OF PPA ON BALANCE SHEET

PPA will have an accounting impact on future cost and profit recognition of Hemaraj’s performance on the consolidated financial statements as the net assets of Hemaraj on the consolidated basis have been revalued to fair value.

However, the impact is deemed marginal since a big portion of fair value adjustment has been allocated to Goodwill and Intangible Asset—totaling THB 24,063 mm—leaving only approximately THB 4 billion markup on the net asset value.

The 100% acquisition value of THB 43,660 mm: the value of shares of Hemaraj which is composed of 1) WHA’s 92.88% portion @ THB 4.5/share (the tender offer price) 2) The remaining Non-Controlling Interest portion of 7.12% @ THB 4.48/share (the closing price of HEMRAJ at 17 Mar 2015)

Net asset value of THB 15,521 mm: the equity value of HEMRAJ as of 17 Mar 2015. Total consideration of THB 40,564 mm: the amount WHA paid for 92.88% of SHARES of HEMRAJ, excluding other expenses such as loan related fee.

PURCHASE PRICE ALLOCATION

42

IV. Appendix

I. Company Overview

IV. Recent Developments & Key Events

V. Q1 2015 Financial Performance

AGENDA

II. Key Business Plan III. Business Updates

43

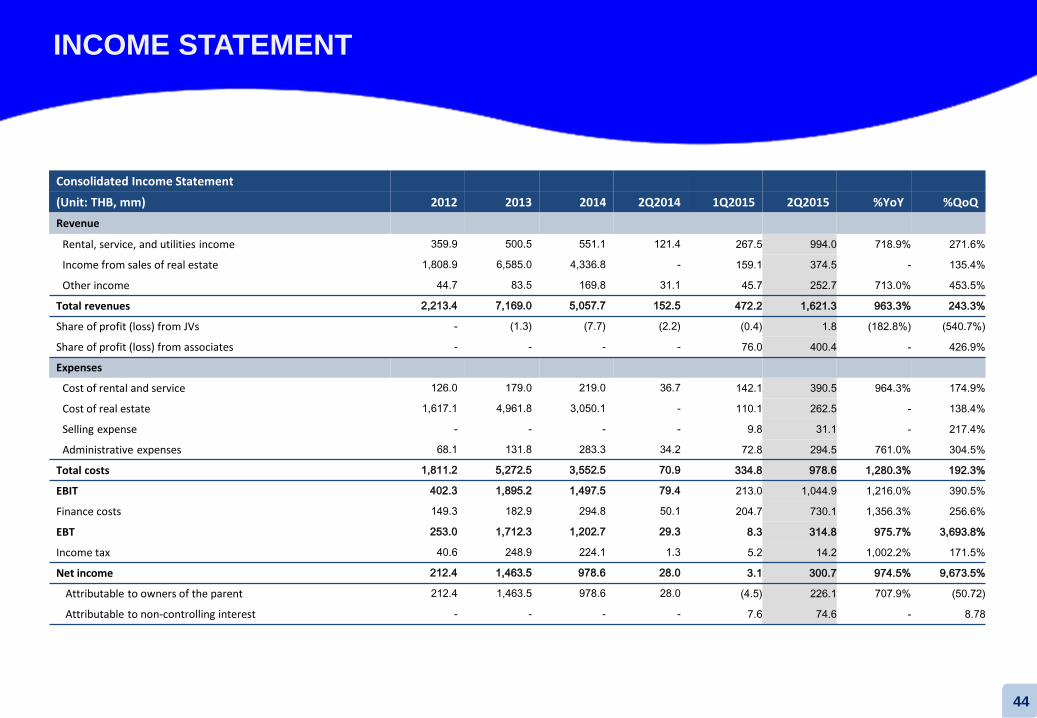

Consolidated Income Statement

(Unit: THB, mm) 2012 2013 2014 2Q2014 1Q2015 2Q2015 %YoY %QoQ Revenue

Rental, service, and utilities income 359.9 500.5 551.1 121.4 267.5 994.0 718.9% 271.6%

Income from sales of real estate 1,808.9 6,585.0 4,336.8 - 159.1 374.5 - 135.4%

Other income 44.7 83.5 169.8 31.1 45.7 252.7 713.0% 453.5%

Total revenues 2,213.4 7,169.0 5,057.7 152.5 472.2 1,621.3 963.3% 243.3%

Share of profit (loss) from JVs - (1.3) (7.7) (2.2) (0.4) 1.8 (182.8%) (540.7%)

Share of profit (loss) from associates - - - - 76.0 400.4 - 426.9%

Expenses

Cost of rental and service 126.0 179.0 219.0 36.7 142.1 390.5 964.3% 174.9%

Cost of real estate 1,617.1 4,961.8 3,050.1 - 110.1 262.5 - 138.4%

Selling expense - - - - 9.8 31.1 - 217.4%

Administrative expenses 68.1 131.8 283.3 34.2 72.8 294.5 761.0% 304.5%

Total costs 1,811.2 5,272.5 3,552.5 70.9 334.8 978.6 1,280.3% 192.3%

EBIT 402.3 1,895.2 1,497.5 79.4 213.0 1,044.9 1,216.0% 390.5%

Finance costs 149.3 182.9 294.8 50.1 204.7 730.1 1,356.3% 256.6%

EBT 253.0 1,712.3 1,202.7 29.3 8.3 314.8 975.7% 3,693.8%

Income tax 40.6 248.9 224.1 1.3 5.2 14.2 1,002.2% 171.5%

Net income 212.4 1,463.5 978.6 28.0 3.1 300.7 974.5% 9,673.5%

Attributable to owners of the parent 212.4 1,463.5 978.6 28.0 (4.5) 226.1 707.9% (50.72)

Attributable to non-controlling interest - - - - 7.6 74.6 - 8.78

INCOME STATEMENT

44

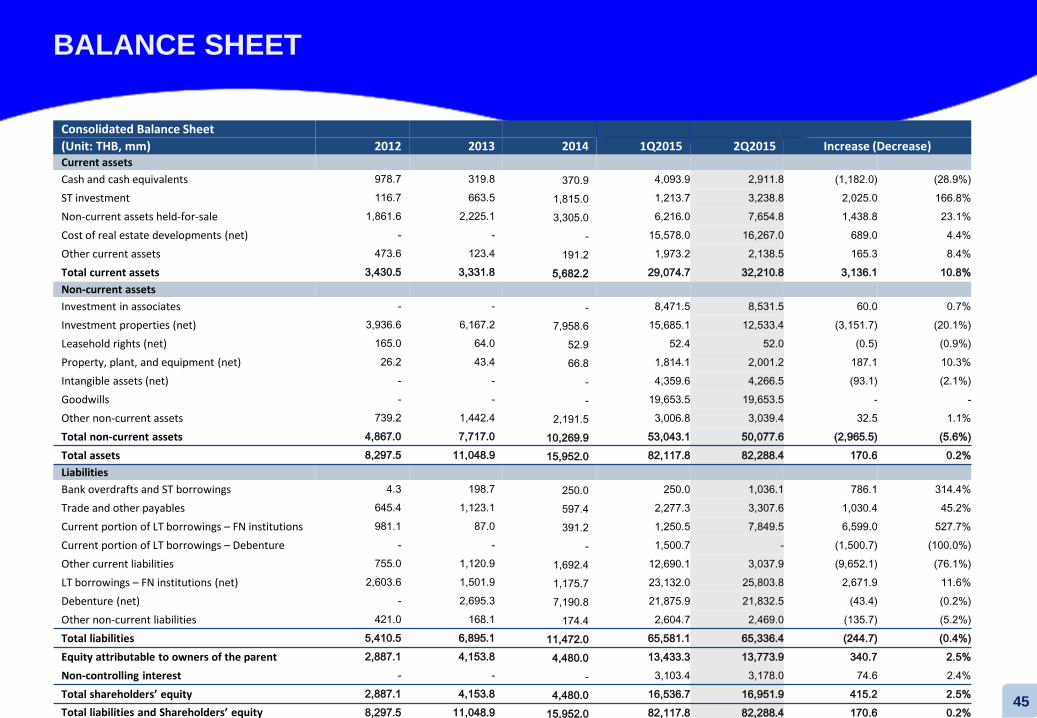

Consolidated Balance Sheet (Unit: THB, mm) 2012 2013 2014 1Q2015 2Q2015 Increase (Decrease) Current assets Cash and cash equivalents 978.7 319.8 370.9 4,093.9 2,911.8 (1,182.0) (28.9%) ST investment 116.7 663.5 1,815.0 1,213.7 3,238.8 2,025.0 166.8% Non-current assets held-for-sale 1,861.6 2,225.1 3,305.0 6,216.0 7,654.8 1,438.8 23.1% Cost of real estate developments (net) - - - 15,578.0 16,267.0 689.0 4.4% Other current assets 473.6 123.4 191.2 1,973.2 2,138.5 165.3 8.4% Total current assets 3,430.5 3,331.8 5,682.2 29,074.7 32,210.8 3,136.1 10.8% Non-current assets Investment in associates - - - 8,471.5 8,531.5 60.0 0.7% Investment properties (net) 3,936.6 6,167.2 7,958.6 15,685.1 12,533.4 (3,151.7) (20.1%) Leasehold rights (net) 165.0 64.0 52.9 52.4 52.0 (0.5) (0.9%) Property, plant, and equipment (net) 26.2 43.4 66.8 1,814.1 2,001.2 187.1 10.3% Intangible assets (net) - - - 4,359.6 4,266.5 (93.1) (2.1%) Goodwills - - - 19,653.5 19,653.5 - - Other non-current assets 739.2 1,442.4 2,191.5 3,006.8 3,039.4 32.5 1.1% Total non-current assets 4,867.0 7,717.0 10,269.9 53,043.1 50,077.6 (2,965.5) (5.6%) Total assets 8,297.5 11,048.9 15,952.0 82,117.8 82,288.4 170.6 0.2% Liabilities Bank overdrafts and ST borrowings 4.3 198.7 250.0 250.0 1,036.1 786.1 314.4% Trade and other payables 645.4 1,123.1 597.4 2,277.3 3,307.6 1,030.4 45.2% Current portion of LT borrowings – FN institutions 981.1 87.0 391.2 1,250.5 7,849.5 6,599.0 527.7% Current portion of LT borrowings – Debenture - - - 1,500.7 - (1,500.7) (100.0%) Other current liabilities 755.0 1,120.9 1,692.4 12,690.1 3,037.9 (9,652.1) (76.1%) LT borrowings – FN institutions (net) 2,603.6 1,501.9 1,175.7 23,132.0 25,803.8 2,671.9 11.6% Debenture (net) - 2,695.3 7,190.8 21,875.9 21,832.5 (43.4) (0.2%) Other non-current liabilities 421.0 168.1 174.4 2,604.7 2,469.0 (135.7) (5.2%) Total liabilities 5,410.5 6,895.1 11,472.0 65,581.1 65,336.4 (244.7) (0.4%) Equity attributable to owners of the parent 2,887.1 4,153.8 4,480.0 13,433.3 13,773.9 340.7 2.5% Non-controlling interest - - - 3,103.4 3,178.0 74.6 2.4% Total shareholders’ equity 2,887.1 4,153.8 4,480.0 16,536.7 16,951.9 415.2 2.5% Total liabilities and Shareholders’ equity 8,297.5 11,048.9 15,952.0 82,117.8 82,288.4 170.6 0.2%

BALANCE SHEET

45

“Target at Well-known MNCs”

“Currently 80% of our customers are well-known MNCs because they realize the importance of logistic system that can substantially save their operating costs. Even though our price per sq.m. is 30-50% over that of the industry average, it’s worth investment for them”

Source: Business Thai

“ The largest premium warehouse in Southeast Asia”

“WHA aims to build large distribution centers that suit the customer’s specific needs. Right now, we are the largest premium warehouse in Southeast Asia constructed under well accepted international standard and equipped with innovative technology”

Source: logistic Digest

Dr. Somyos Anantaprayoon Chairman & Chief Executive Officer A Director since incorporation Group’s CEO who originated the idea of

world-class standard Built-to-Suit Warehouse and DC

Ms. Jareeporn Anantaprayoon Managing Director A Director since incorporation Assist the CEO in business strategy

development Responsible for Group’s sales and

marketing

Mr. Surathian Chakthranont Director Advise on business strategy &plan Previous President of SC Asset

Corporation, PCL (1995 – 2005) More than 10 years experience in Real

Estate sector

Dr. Pichit Akrathit Independent Director Chairman of the Audit Committee An advisor to several leading companies

Mr. Jakrit Chaisanit Director Head of Construction Management Division

Mr. Narong Kritchanchai Director

Mr. Somsak Boonchoyruengchai

Director Head of Accounting division

Dr. Somsak Pratomsrimek Independent Director Member of the Audit Committee

Dr. Kritsana Sukboonyasatit Independent Director

Mr. Arttavit Chalermsaphayakorn

Director Chief Financial Officer

“WHA Expertise”

“WHA Corporation is regarded as the world class built-to-suit warehouse developer with strong reputation in selecting prime location, operational efficiency and after sales service”

Source: www.freightmaxad.com

Dr. Apichai Boontherawara Independent Director Member of the Audit Committee

BOARD OF DIRECTORS

46

47

1121 Moo.3 Theparak Rd., Theparak, A. Muang, Samutprakarn 10270 Thailand

Tel. +66 (0) 2 753 3750

Fax. +66 (0) 2 753 2750

e-mail: [email protected] Website: www.wha.co.th

WHA Corporation PCL.