what basel says about expected credit loss (ecl)

TRANSCRIPT

WHAT BASEL SAYS ABOUT

EXPECTED CREDIT LOSS

(ECL)

Graham DyerSr. Manager – Financial Institutions

Grant Thornton

Tuesday March 24th, 2015

PRESENTED BY:

Emily BoganSr. Risk Management ConsultantSageworks

Questions

+ A copy of the slides and webinar recording will be emailed to you following the webinar

+ To ask a question during the webinar, enter it into the chat box in the GoToWebinar panel on right side of screen:

+ Brief Q&A held at end of webinar

About Sageworks

+ Financial information company that provides credit and risk management solutions to financial institutions

+ Data and applications used by thousands of financial institutions and accounting firms across North America

+ Named to Inc. 500 list of fastest growing privately held companies in the U.S.

+ Named to Deloitte’s Technology Fast 500

+ NC Tech Awards: Excellence in Customer Service

About Grant Thornton

At Grant Thornton, we provide clear insights and practical solutions, helping you navigate the complexities of today's business landscape. Our financial services is one of Grant Thornton’s largest industry practices and consists of

+55 dedicated partners +Over 500 professionals

For more than 80 years, we have been serving financial services companies and financial institutions. Nationally, we have worked with

+2,200 public and private financial services companies +350 are banking clients

The practice is comprised of senior partners who have served in various C-suite executive roles in the industry; while others have served as former bank regulators. This experience enables us to provide a unique, strategic perspective on current industry matters, as well as implement best practices to position leaders for the future.

To learn more, visit us at www.grantthornton.com.

Who will be speaking?

Emily Bogan Sr. Risk Management

ConsultantSageworks

Graham DyerSr. Manager – Financial

InstitutionsGrant Thornton

Ed BayerVice President

Sageworks

Learning Objectives

+ What is the Basel Committee on Banking Supervision (BCBS)?

+ What document did they release?

+ What is the document’s purpose?

+ Why should I care?

+ Principles underlying the document

+ Risk management maturity model

+ Key takeaways

+ Conclusion

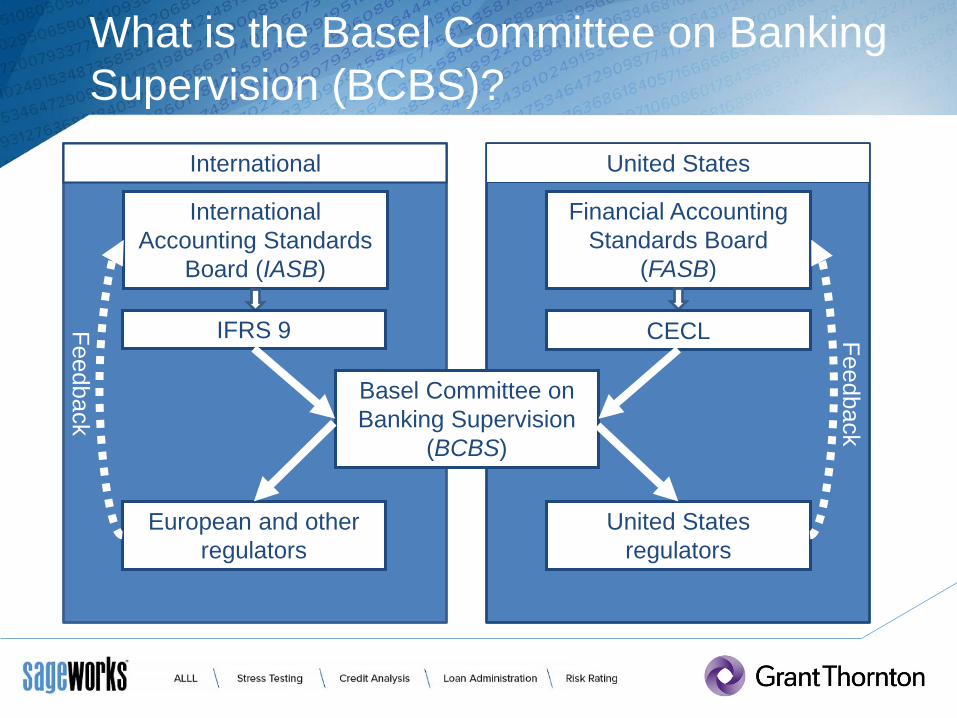

What is the Basel Committee on Banking

Supervision (BCBS)?

+ Basel Committee on Banking Supervision (BCBS)

+ Primary global standard-setter for the prudential regulation of banks

+ Strengthens regulation, supervision and practices of banks worldwide with the purpose of enhancing financial stability

+ Basel’s accords enacted by respective governing authorities (ex. Basel III enforced by U.S. regulatory bodies)

+ Accounting experts group advises BCBS on accounting matters and has significant influence on standard setting bodies, especially in Europe

What is the Basel Committee on Banking

Supervision (BCBS)?

International United States

International

Accounting Standards

Board (IASB)

Financial Accounting

Standards Board

(FASB)

IFRS 9 CECL

Basel Committee on

Banking Supervision

(BCBS)

European and other

regulators

United States

regulators

Feedback

Feedback

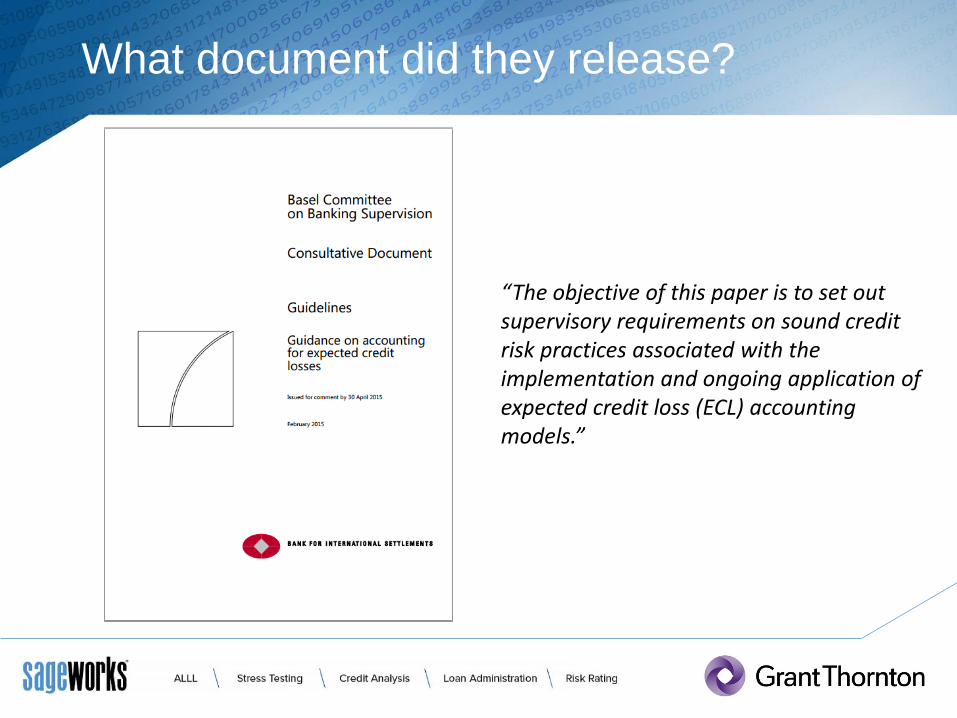

What document did they release?

“The objective of this paper is to set out supervisory requirements on sound credit risk practices associated with the implementation and ongoing application of expected credit loss (ECL) accounting models.”

What is the document’s purpose?

+ “The requirements described in the main section of this paper are equally applicable under all accounting frameworks.”…(inclusive of GAAP)

+ “Representatives of IASB provided opportunity to comment on document but have not identified any aspects preventing bank from meeting impairment requirements of IFRS 9.”

+ Sets baseline expectations for both regulators & auditors

+ Next “piece of the puzzle” on expectations for CECL

Why should I care?

+ First significant guidance on expectations for implementation of expected loss model

+ Sets the tone

+ BCBS guidance is very influential for US regulators, who participate significantly in drafting BCBS guidance

+ Also influential to auditors looking for standards by which to evaluate client processes

Principles underlying the document

+ Link to full document to be sent out following today’s webinar

+ 39 pages

+ Summary of principles to ensue

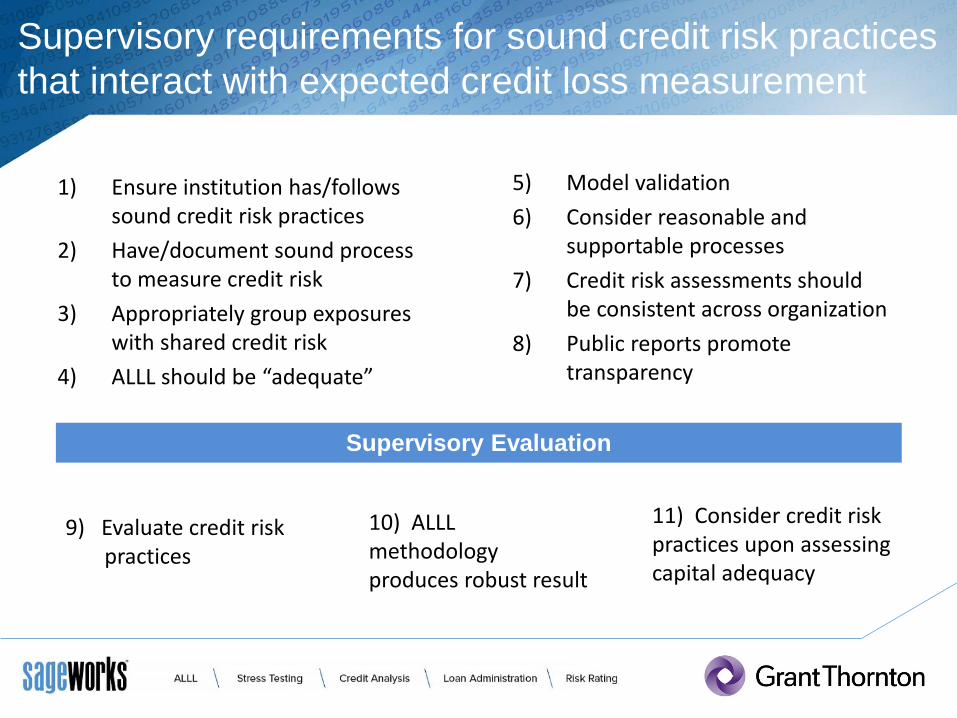

Supervisory requirements for sound credit risk practices

that interact with expected credit loss measurement

1) Ensure institution has/follows sound credit risk practices

2) Have/document sound process to measure credit risk

3) Appropriately group exposures with shared credit risk

4) ALLL should be “adequate”

1) D

2) D

3) D

4) d

5) Model validation

6) Consider reasonable and supportable processes

7) Credit risk assessments should be consistent across organization

8) Public reports promote transparency

Supervisory Evaluation

9) Evaluate credit risk . practices

10) ALLL methodology produces robust result

11) Consider credit risk practices upon assessing capital adequacy

Principles underlying the document

+ Principle 1:

+ A bank’s board of directors (or equivalent) and senior management are responsible for ensuring that the bank has appropriate credit risk practices, including effective internal controls, commensurate with the size, nature and complexity of its lending exposures to consistently determine allowances in accordance with the bank’s stated policies and procedures, the applicable accounting framework and relevant supervisory guidance.

Principles underlying the document

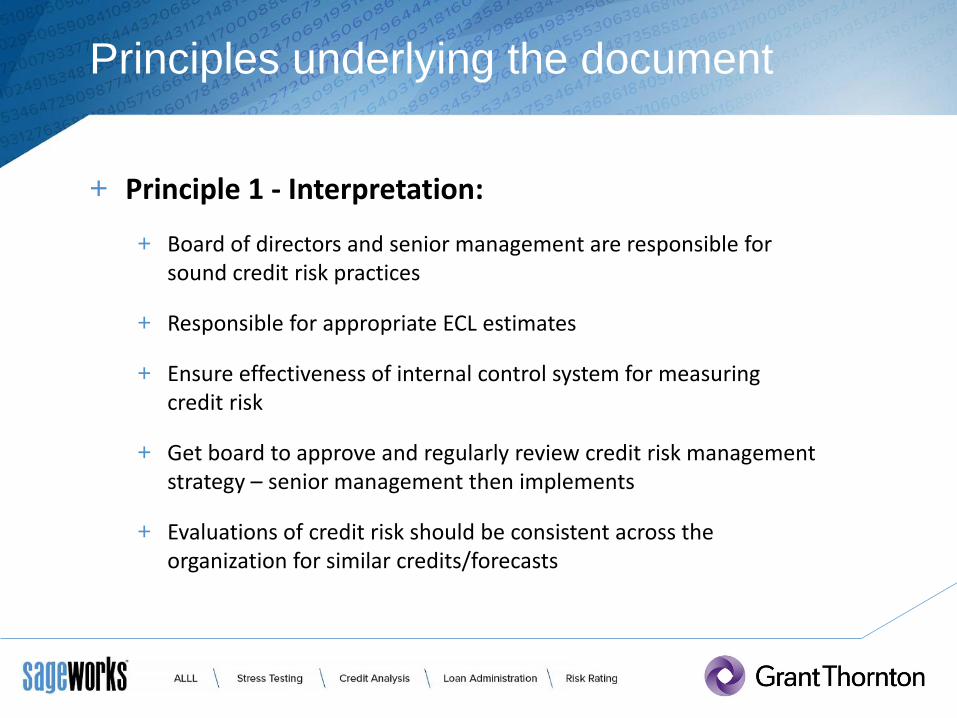

+ Principle 1 - Interpretation:

+ Board of directors and senior management are responsible for sound credit risk practices

+ Responsible for appropriate ECL estimates

+ Ensure effectiveness of internal control system for measuring credit risk

+ Get board to approve and regularly review credit risk management strategy – senior management then implements

+ Evaluations of credit risk should be consistent across the organization for similar credits/forecasts

Principles underlying the document

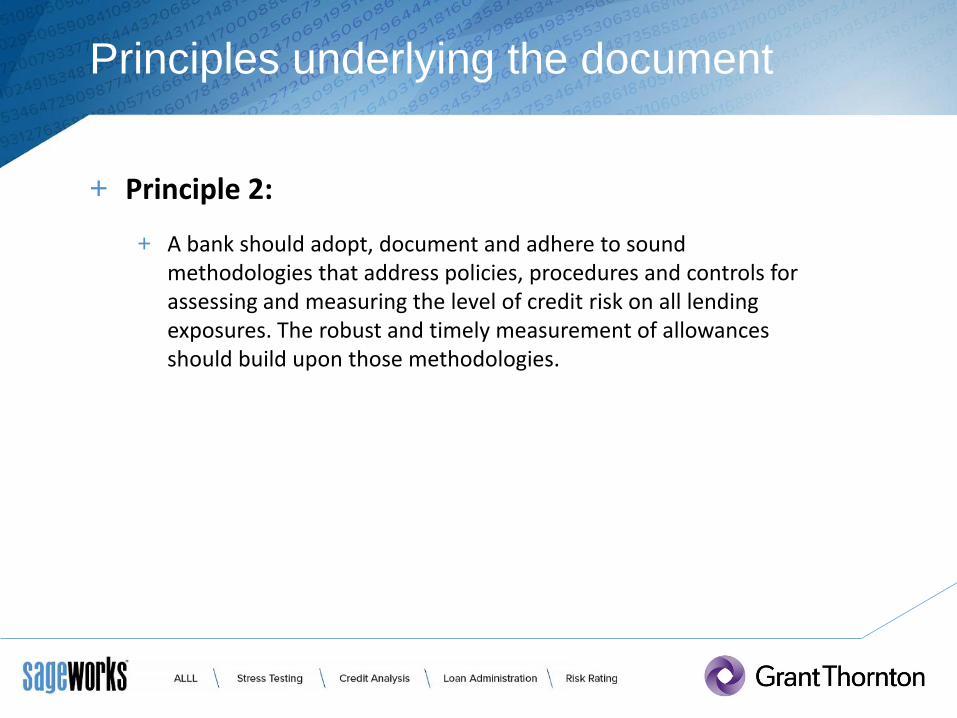

+ Principle 2:

+ A bank should adopt, document and adhere to sound methodologies that address policies, procedures and controls for assessing and measuring the level of credit risk on all lending exposures. The robust and timely measurement of allowances should build upon those methodologies.

Principles underlying the document

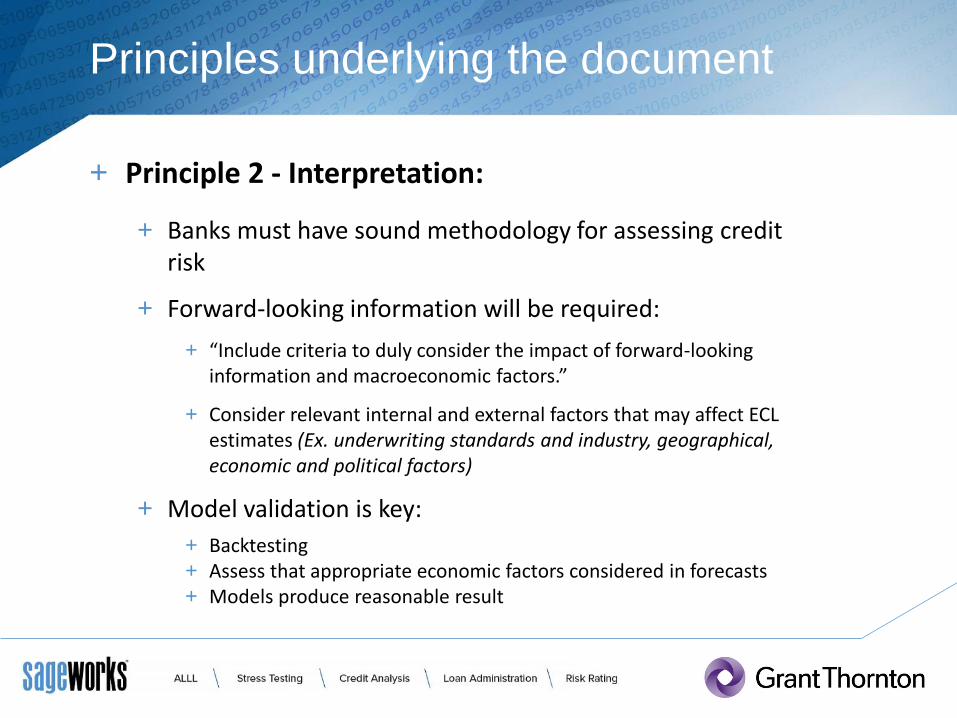

+ Principle 2 - Interpretation:

+ Banks must have sound methodology for assessing credit risk

+ Forward-looking information will be required:

+ “Include criteria to duly consider the impact of forward-looking information and macroeconomic factors.”

+ Consider relevant internal and external factors that may affect ECL estimates (Ex. underwriting standards and industry, geographical, economic and political factors)

+ Model validation is key:

+ Backtesting+ Assess that appropriate economic factors considered in forecasts + Models produce reasonable result

Principles underlying the document

+ Principle 3:

+ A bank should have a process in place to appropriately group lending exposures on the basis of shared credit risk characteristics.

Principles underlying the document

+ Principle 3 - Interpretation:

+ An effective risk rating methodology should incorporate all pertinent forward-looking/macroeconomic factors

+ Consistency in credit risk evaluations throughout institution

+ Groups of lending exposures into portfolios with shared credit risk characteristics must be re-evaluated regularly (including re-segmentation upon relevant new information)

+ Objective tests to validate groupings?

+ Will banks have enough data points to validate groupings empirically?

+ Portfolio as a whole should migrate to a higher credit risk rating if level of credit risk assessed to have increased on a group basis

Principles underlying the document

+ Principle 4:

+ A bank’s aggregate amount of allowances, regardless of whether allowance components are determined on a collective or an individual basis, should be adequate as defined by the Basel Core Principles, which is an amount understood to be consistent with the objectives of the relevant accounting requirements.

Principles underlying the document

+ Principle 4 - Interpretation:

+ Adequate, as defined by Basel Core Principles

+ Robust methodologies to calculate ECL should consider full spectrum of reasonable information and different potential scenarios

+ Pooling guidance:

+ Pool based on shared credit risk characteristics

+ Guidance suggests should pool as many loans as you can, as long as their credit risk is similarly responsive to changes in forward-looking economic factors

+ FASB: If you can pool, you must

+ Do not rely on biased or overly optimistic judgments

Principles underlying the document

+ Principle 5:

+ A bank should have policies and procedures in place to appropriately validate its internal credit risk assessment models.

Principles underlying the document

+ Principle 5 - Interpretation:

+ Given the additional complexities and introduction of judgment for forward-looking criteria, model validation ever more important

+ Should be conducted annually at a minimum

+ Should be done by independent third party

+ OCC 2011-12: Supervisory Guidance on Model Risk Management

Principles underlying the document

+ Principle 5 – Interpretation (cont’d):

+ Elements of sound model risk management program:

+ Governance

+ Clear roles & responsibilities

+ Validation scope & methodology

+ Model inputs

+ Model design

+ Model output & performance

+ Documentation

+ Independent review

Principles underlying the document

+ Principle 6:

+ A bank’s use of experienced credit judgment, especially in the robust consideration of forward-looking information that is reasonably available and macroeconomic factors, is essential to the assessment and measurement of expected credit losses.

Principles underlying the document

+ Principle 6 - Interpretation:

+ The Committee recognizes that incorporating forward-looking information and macroeconomic factors into the estimate of ECLs is challenging, costly and requires significant judgment. However, the consideration of forward-looking information and macroeconomic factors is critical to a robust implementation of an ECL model.

+ “The associated costs should not be avoided on the basis that they are excessive or unnecessary”

+ Institution’s experienced credit judgment must bridge the gap where formal statistical information and credit risk cannot be linked

+ Will you have to defend what you did not consider to reach your estimate?

Principles underlying the document

+ Principle 7:

+ A bank should have a sound credit risk assessment and measurement process that provides it with a strong basis for common systems, tools and data to assess and price credit risk, and account for expected credit losses.

Principles underlying the document

+ Principle 7 - Interpretation:

+ Implement processes, systems and tools to strengthen reliability and consistency across institution and increase transparency of ECL estimates

+ Data is key

+ Document transition to ECL, document any changes to model thereafter

+ Migration analysis can be useful in tying ALLL to credit risk

+ Incorporates view of how credits migrate through various risk levels

Principles underlying the document

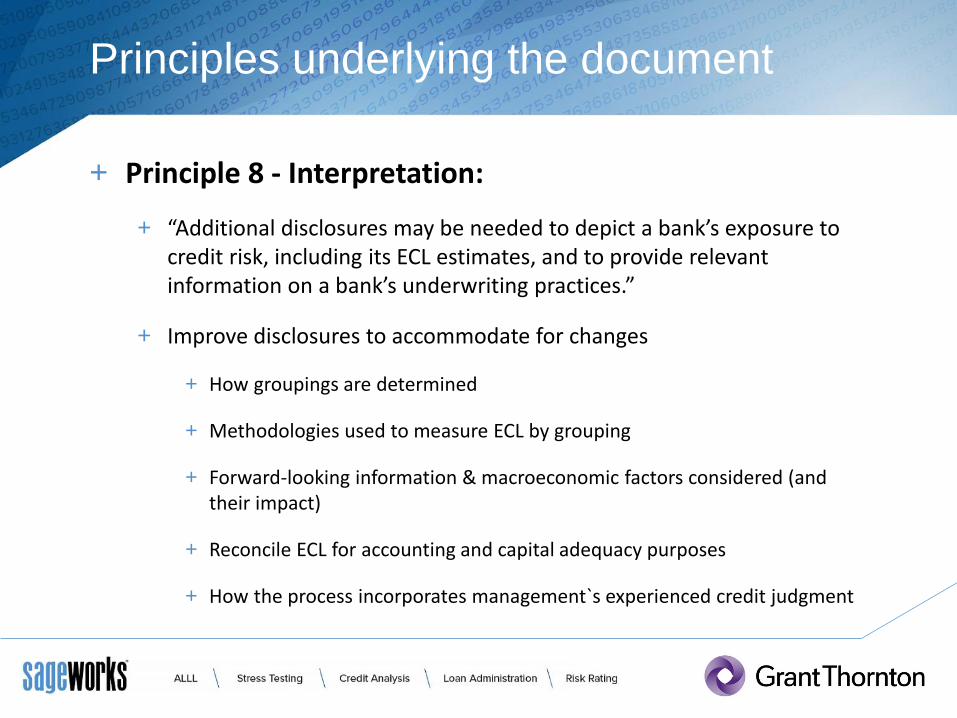

+ Principle 8:

+ A bank’s public reporting should promote transparency and comparability by providing timely, relevant and decision-useful information

Principles underlying the document

+ Principle 8 - Interpretation:

+ “Additional disclosures may be needed to depict a bank’s exposure to credit risk, including its ECL estimates, and to provide relevant information on a bank’s underwriting practices.”

+ Improve disclosures to accommodate for changes

+ How groupings are determined

+ Methodologies used to measure ECL by grouping

+ Forward-looking information & macroeconomic factors considered (and their impact)

+ Reconcile ECL for accounting and capital adequacy purposes

+ How the process incorporates management`s experienced credit judgment

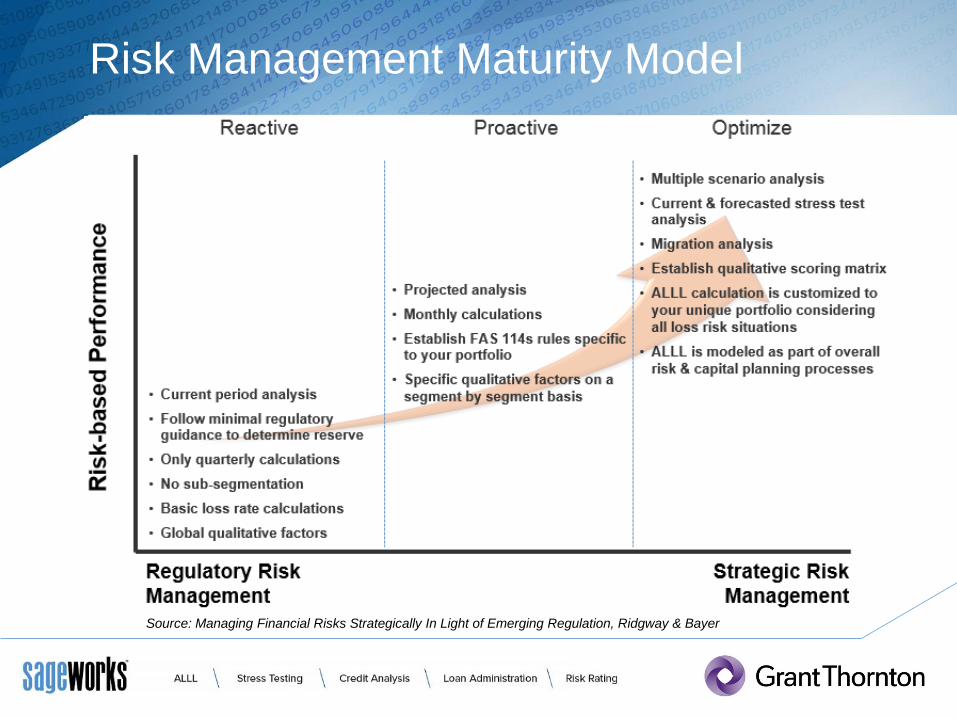

Risk Management Maturity Model

Source: Managing Financial Risks Strategically In Light of Emerging Regulation, Ridgway & Bayer

Risk Management Maturity Model

Source: Managing Financial Risks Strategically In Light of Emerging Regulation, Ridgway & Bayer

Source: Managing Financial Risks Strategically In Light of Emerging Regulation, Ridgway & Bayer

Key takeaways

+ Integrating credit risk to the ALLL

+ Multiple scenarios important under ECL

+ Model validation

+ Automation can assist in reliability, consistency and transparency

+ Data

+ Be aware of and don’t spare costs

+ Consistency of credit risk evaluation throughout organization

+ Documenting bases for:

+ Loan groupings

+ Decisions on forecasts

+ ALLL assumptions

+ Foundation is strong credit risk practices

Contact Information

Graham DyerSenior Manager – Financial Services

Grant Thornton

Emily BoganSenior Risk Management Consultant

Sageworks

Resources

+ The destination website for the ALLL calculation

+ Latest news, peer discussions, industry expert opinions

+ ALLL Forum for Bankers

+ Commercial Credit Risk Professionals

+ www.sageworksanalyst.com

+ Whitepapers, webinars, thought leadership

Resources (cont’d)

+ CECL Webinar

+ Fill out form, we’ll email you invite when guidance passed

+ Web.sageworks.com/CECL/

+ Brief survey following webinar: topics for

upcoming webinars? Speaker feedback?

+ 2015 Annual Risk Management Summit (ALLL + ST)

+ Chicago, IL Sept 23 – 25

+ Sageworks.com/Summit

Questions?