what consequences for the russian gas strategy in view of ... · what consequences for the russian...

TRANSCRIPT

What consequences for the Russian gas strategy in view of the Ukrainian

crisis?

Dr.Prof. Andrey A.Konoplyanik,Adviser to Director General, Gazprom export LLC,

Professor, Chair “International Oil & gas Business”,Russian State Gubkin Oil & Gas University

FEEM GAS TALKS 2014 BRAINSTORMING WORKSHOP, Session 2, 20-21 November 2014, Milano, Italy

Demand for adaptation: not UA per se, but general economic trends incl. UA

• Since 2009 radical changes in architecture of EU internal gas market => 4 group of factors:– 2 economic (on demand & supply side)– Institutional (Third Energy Package)– Political (RF-UA gas transit crises Jan’s2006&2009)

• Consequences for all segments/players of gas value chain within “Broader Energy Europe”

• Ukraine is only one (important, but additional) element among other factors of gas market changes:– UA story has radicalized & made demand for changes

more/most urgent– UA energy turned into political issue + time constrains =>

mythologization of the RF-UA gas story in Western media– Virtual picture vs real facts => deviations from balanced

picture & neutrality are not helpful for achieving new equilibrium A.Konoplyanik, FEEM Gas Talks, Milano, 20-

21.11.2014 2

Adaptation of Russia’s gas export strategy in Europe• General rule: maximization of marketable Hotelling/resource rent

within competitive (NWE) &/or non-competitive (CEE/CIS) markets (resulted from adequate/inadequate CAPEX in EU/CIS infrastructure development)

• From sole oil-indexed LTGEC in undersupplied growing EU gas market - to flexible & adaptable two-segment structure in oversupplied (contractually &/or physically) EU mature market

• Then & now: 2 contractual structures/pricing mechanisms (though quite different):• Then (1968-2009): economic vs political

– EU = LTC + replacement value = economic pricing from the very start– COMECON = political cost-plus till end-1990s/2004 => economic pricing afterwards– CIS = political till 2006/2009 => economic pricing with concessions afterwards (UA)

• Now onwards (2009+): contractual vs spot – NWE = (i) LTC (volume) + replacement value (oil-indexed pricing) & (ii) spot (volume)

+ spot (hub-based pricing); – CEE & CIS = LTC + replacement value (+ price concessions from Groningen-formula-

based oil-indexed price to UA) => no adequate technical background for competition – yet... A.Konoplyanik, FEEM Gas Talks, Milano, 20-

21.11.2014

3

New model for EU: Evolution of gas value chain & pricing mechanism of Russian gas to EU (1)

GazpromWholesale EU

buyers/ resellers (trade & delivery)

End-use EU customers

Gazprom

Wholesale EU buyers/

resellers (trade & delivery)

End-use EU customers

Past (Pre-2009) – growing EU market

Oil-indexation

Hub-indexation

Oil-indexation

Oil-indexation

Common interests

Common interests

Request for hub-indexation where hubs

are relatively liquid

Request for hub-indexation both where hubs are relatively liquid & where there is no hubs or they are not yet liquid at all (f.i. under

threat of arbitration)

EU hubs

Non-EU customers (f.i. reverse flows to

CIS/UA)

Gazprom as price-taker from oil

market

Gazprom as price-taker from oil

market

Gazprom as price-taker from OIL

market

Nowadays (Post-2009) –oversupplied (in NWE segment -?)

EU market with not yet clear future trends

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014

New model for EU: Evolution of gas value chain & pricing mechanism of Russian gas to EU (2)

GazpromWholesale EU buyer / reseller

(trade & delivery)

End-use EU customer

Gazprom

Wholesale EU buyer / reseller

(delivery)

End-use EU customers (delivery)

Future (“NO GO” contractual scheme under any (?) supply-demand scenario)

Future (what competitive niche for oil-indexed LTC & spot deliveries & trade to/within EU?)

Hub-indexation

Hub-indexation

Hub-indexation

Oil-indexation (adapted)

Common interests – downgrading price spiral for (RUS) gas

Common interests

Gazprom as price-taker from GAS BUYER’s market (with no

participation on it)? => NO GO

Oil

EU hubs (trade)Gazprom as one of price-

makers at emerging EU

market

Role of DG

COMP?

Traditional flexibility for buyer (TOP)

Direct supplies to EU end-users

UGS(UA?)

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014

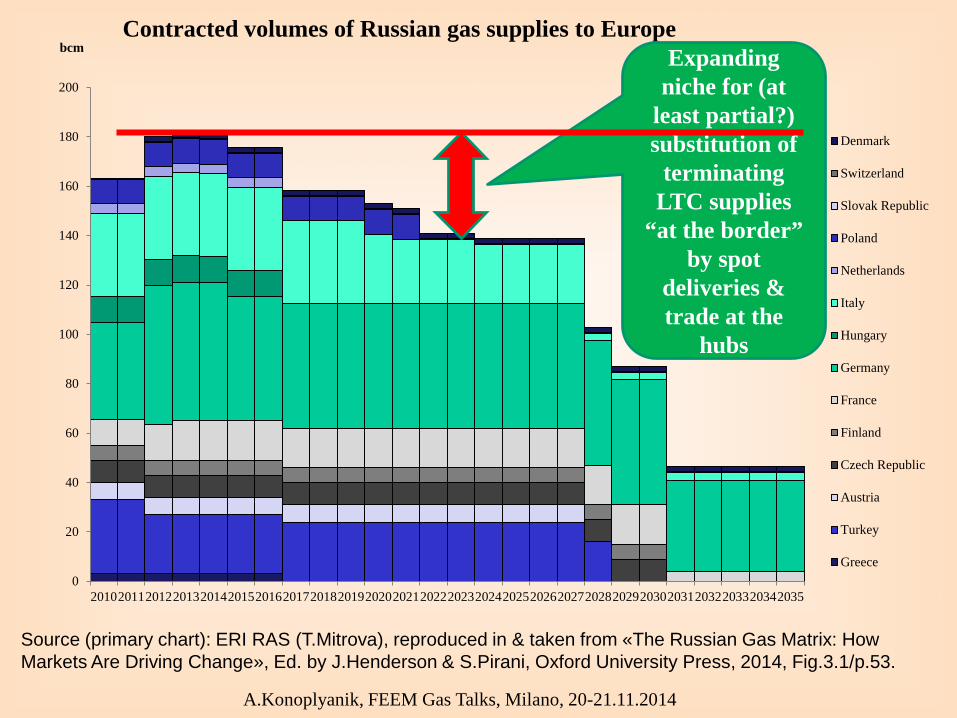

0

20

40

60

80

100

120

140

160

180

200

20102011201220132014201520162017201820192020202120222023202420252026202720282029203020312032203320342035

bcmContracted volumes of Russian gas supplies to Europe

Denmark

Switzerland

Slovak Republic

Poland

Netherlands

Italy

Hungary

Germany

France

Finland

Czech Republic

Austria

Turkey

Greece

Source (primary chart): ERI RAS (T.Mitrova), reproduced in & taken from «The Russian Gas Matrix: How Markets Are Driving Change», Ed. by J.Henderson & S.Pirani, Oxford University Press, 2014, Fig.3.1/p.53.

Expanding niche for (at

least partial?) substitution of

terminating LTC supplies

“at the border” by spot

deliveries & trade at the

hubs

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014

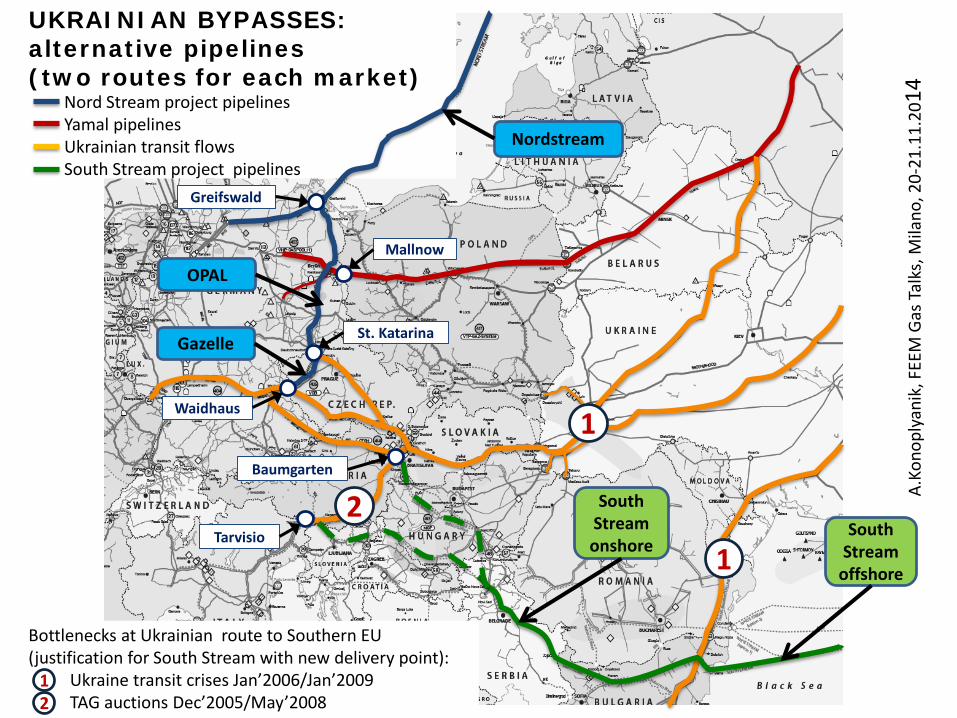

Russia’s gas export strategy: from “Russia & Europe” to “Russia & Europe & Asia”

• From priority of EU gas export market (when domestic supplies underpriced) – to dynamic balancing within three markets (EU export, RF domestic, Asian export) with (to be achived) price parity

• From one export market (Europe) - to two export markets (Europe & Asia) balanced/interconnected through RUS domestic market infrastructure:• general adaptations of RF export strategy since first RF-UA crisis (2006) (or

even since pre-Orange revolution/2004+) => lengthy process, so• new concept have materialised in new (Asian) contracts just now• “after” [2014] Ukrainian crisis does not mean “in result of” it

• Russia vs Europe & Asia: • Then => one export market => USSR/GOSPLAN => «one market = 1 pipe» • Now onward => since USSR & COMECON dissolution (transit risks) & RF-UA

transit crises => two export markets concept (1 existing + 1 emerging) => “one market = 2 pipes/means of supply (pipeline &/or LNG)”

• Still open question: Whether both pipes to each EU market will be used:– NWE: UA GTS +/vs (Nordstream+OPAL+Gazelle)– SE: UA GTS +/vs South Stream (off-shore + onshore)

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.20147

UKRAINIAN BYPASSES:alternative pipelines (two routes for each market)

Nord Stream project pipelinesYamal pipelinesUkrainian transit flowsSouth Stream project pipelines

Bottlenecks at Ukrainian route to Southern EU (justification for South Stream with new delivery point):

Ukraine transit crises Jan’2006/Jan’2009TAG auctions Dec’2005/May’2008

2

12

1

Mallnow

Greifswald

St. Katarina

Waidhaus

Baumgarten

Tarvisio

1

Nordstream

OPAL

Gazelle

South Streamonshore

South Stream

offshore

A.Ko

nopl

yani

k, F

EEM

Gas

Tal

ks, M

ilano

, 20-

21.1

1.20

14

0

1

2

3

4

5

6

7

8

9

10

12.3

0.08

2.28

.09

4.30

.09

6.30

.09

8.31

.09

10.3

1.09

12.3

1.09

2.28

.10

4.30

.10

6.30

.10

8.31

.10

10.3

1.10

12.3

1.10

2.28

.11

4.30

.11

6.30

.11

8.31

.11

10.3

1.11

12.3

1.11

2.29

.12

4.30

.12

6.30

.12

8.31

.12

10.3

1.12

12.3

1.12

2.28

.13

4.30

.13

6.30

.13

8.31

.13

10.3

1.13

12.3

1.13

2.28

.14

4.30

.14

6.30

.14

8.31

.14

“tra

nsit

inte

rrup

tion

prob

abili

ty”

inde

x Ukraine: “transit interruption probability” index (2009–2014)

Calculated by M.Larionova, Russian Gubkin State Oil & Gas University, Chair “International Oil & Gas Business”, Master’s programme 2013-2015, based on the methodology jointly developed with the author

To evaluate possible interruptions of transit supplies we consider 1009 newsbreaks, related to gas relations between Russia and Ukraine through 30.12.2008 to 10.10.2014 period. These newsbreaks were taken from the newswire http://newsukraine.com.ua/ (prior to 28.02.2014) & http://km.ru/ (after 28.02.2014). Then they were filtered to 170 newsbreaks which, in case of their realization, would have a main effect on interruption of gas flows in transit within the Ukrainian territory.

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014

Russia & Europe in the past vs Russia & Europe & Asia in the future

Nadym-Pur-Tazovsky& Yamal

East-Siberianonsore Sakhalin

offshore

Pipeline supplies

LNG supplies

Resource bases

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014 10

Source of original map: http://www.gazprom.ru/about/production/projects/pipelines/ykv/

Thank you for your attention!

Disclaimer: Views expressed in this presentation do not necessarily reflect (may/should reflect) and/or coincide (may/should be consistent) with official position of Gazprom Group (incl. Gazprom JSC and/or Gazprom export LLC), its stockholders and/or its/their affiliated persons, and are within full personal responsibility of the author of this presentation.

The way forward for EU-Russian gas relations

Dr.Prof. Andrey A.Konoplyanik,Adviser to Director General, Gazprom export LLC,

Professor, Chair “International Oil & gas Business”,Russian State Gubkin Oil & Gas University

FEEM GAS TALKS 2014 BRAINSTORMING WORKSHOP, Session 3, 20-21 November 2014, Milano, Italy

RF-EU gas relations: corridor of opportunities

• To understand new post-2009 realities in “Broader Energy Europe”:– new risks & uncertainties within new realities =>– whether “no return points” are passed through? =>– to search for new opportunities => – only mutual & multilateral compromise possible

• Driving/balancing principle: to diminish risks & uncertainties to [mutually] tolerable level (P.Lowe/GAC RF-EU)

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014 13

What to be done by EU• To stop ASAP anti-Russian sanctions:

– mutually negative for RF & EU, – aimed at slowing down EU economic recovery & at getting rid of EU

as US competitor in global competition/recovery• To implement adequate investment rules for existing capacity:

– stop blocking OPAL (prevents pay-back of CAPEX already made => Art.13 ECT)

• To develop adequate investment rules for new capacity which: – will enable development & operation of South Stream (& similar

projects) within Third Energy Package rules based on standard project financing principles

– will depoliticize regulatory procedures• To invest adequately in UA transition towards “Euro-

integration” to escape negative results of earlier under-investing in CEE transition to EU rules (infrastructure density)

• To stop base its energy policy on perceptions, esp. on wrong perceptions

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014 14

What to be done by Russia

• To stop treating Third EU Energy Package as deviation from the rules, not by the new rules– Sovereign choice of sovereign states (incl. EU) to

develop its internal legislation, even if economically imbalanced (inter alia, trade vs investment stimuli)

• To stop treating implementation of Third package rules (EU energy acquis) in UA as pure political anti-Russia action, not as objective result of UA sovereign choice of accession to the Energy Community Treaty

A.Konoplyanik, FEEM Gas Talks, Milano, 20-21.11.2014 15

Thank you for your attention!

Disclaimer: Views expressed in this presentation do not necessarily reflect (may/should reflect) and/or coincide (may/should be consistent) with official position of Gazprom Group (incl. Gazprom JSC and/or Gazprom export LLC), its stockholders and/or its/their affiliated persons, and are within full personal responsibility of the author of this presentation.