what if joseph had used derivatives? hedging commodity price risk 1. many developing countries are...

TRANSCRIPT

What If Joseph Had Used Derivatives?Hedging commodity price risk

1. Many developing countries are highly dependent upon commodity production for exports, and also dependent upon some key commodity imports for food and energy. Thus exposes them to substantial amounts of commodity price risk.

2. Correlation between commodity prices, revenue, exports and output

3. Prices are VOLATILE -

4. Long swings

5. Long-term impact of short-term problem

Long swings in commodity prices• Raul Prebish, Singer (confirmed by Kindleberger) secular fall relative to

manufactured goods• Problem for terms of trade, national income and development• Attempts at import substitution• Attempts at commodity pools• Trend problems comes to fore when price take deep downward dive• This is sometimes misleadingly referred to as volatility

Export Dependence of Developing Countries

Africa Asia

Mauritania 99.8 Gambia, The 92.8 Yemen, Rep. 99.4

Mali 99.8 Malawi 92.7 Papua New Guinea96

Nigeria 99.3 Ghana 92.3 Kuwait 95.3

Ethiopia 99.3 Cameroon 92 Saudi Arabia 93.2

Chad 99.1 Madagascar 85.6 Syria 90.8

Rwanda 98.4 Mozambique 83.9 Mongolia 89.8

Gabon 98.1 Guinea-Bissau 82.5 Myanmar 88.6

Angola 97.8 Burkina Faso 80.1 Iran 86.5

Congo, Rep. 97.9 Tanzania 78.2 Oman 86.1

Nigeria 97.6 Senegal 74.6 Cambodia 82.8

Algeria 96.3 Kenya 71.7 Laos 71.3

Libya 96.1 Uganda 70.7 Vietnam 63.7

Benin 95.4 Zimbabwe 70.4 Jordan 61.3

Sudan 95.4 Cote d'Ivoire 68.7 Latin America

Zambia 95.4 Namibia 68.4 Ecuador 91.1

Togo 93.6 Egypt, Arab Rep. 68.4 Venezuela 88.5

Burundi 93.5 Sierra Leone 57.8 Chile 85.3

Guinea-Bissau 93.1 Central African Rep 57.4 Peru 84

South Africa 50.8 Bolivia 84

Paraguay 83

Panama 79.7

Russian Federation83.3 Costa Rica 75.5

Kazakhstan 82.2 Argentina 69.9

Georgia 82.2 Honduras 69.5

Turkmenistan 78.1 Guatemala 69.3

Moldova 77.3 Nicaragua 66.3

Tajikistan 75.3 Colombia 65.8

Azerbaijan 73.2 Uruguay 63.9

Ukraine 66.5 Trinidad and Tobago61.3

Bulgaria 64.5 El Salvador 58.8

Kyrgyz Republic 61.6

Armenia 56.1

Macedonia, FRY 52.5

Yugoslavia, FR 51.1

Commodities as % of Total Merchandise Export (1996)

Europe & Central Asia

Commodities as % of exports in 1996

TABLE 2 Correlations with Major Export Commodity Price

Country Commodity GDP Exports Revenue

Burundi Coffee -0.55 0.44 1

Colombia Oil 0.05 0.3 0.62

Ethiopia Coffee 0.44 0.33 0.36

Ghana Cocoa 0.75 0.22 0.72

Kazakhstan Oil 0.65 0.9 0.44

Nicaragua Coffee 0.48 0.4 0.48

Nigeria Oil 0.3 0.66 0.11

Uganda Coffee 0.65 0.52 0.64

Uruguay Beef 0.2 0 0.45

Venezuela Oil 0.01 0.71 0.5

-- GDP and Revenue in real 1995 local currency values

-- Exports in nominal U.S. dollar values

-- International Financial Statistics

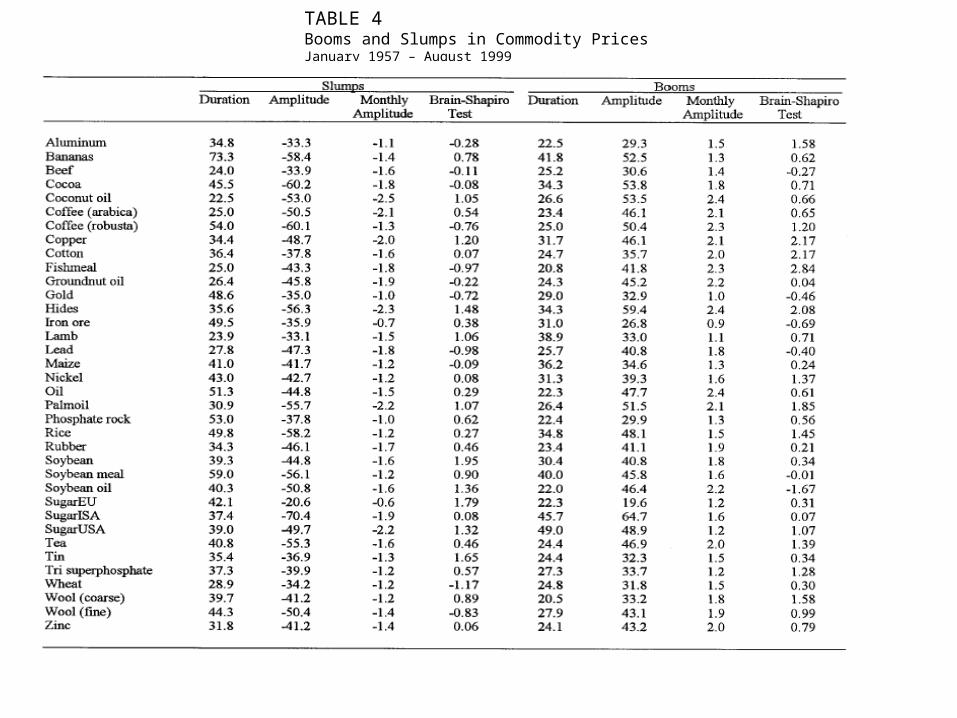

TABLE 4Booms and Slumps in Commodity PricesJanuary 1957 – August 1999

TABLE 3

PermanentAluminum 29 (1 & up) Beef 57, (20 & up) Coffee 150, (26 & up) Cocoa beansFishmeal 45, (18 & up) Coconut oil 70, (22 & up) Cotton 152, (26 & up) Coffee

(Robusta)Gasoline 44, 8 & up) Copper 81, (23 & up) Nickel 175, (26 & up) 103 (24 & up)

GoldIron Ore 32, (15 & up) Groundnut oil 58, (20 & up) Rice Hardwood (logs)Lamb 14, (9 & up) Lead 64, (21 & up) Natural gasRubber 43, (18 & up) Maize 55, (20 & up) PetroleumSoybean meal 26, (14 & up) Palm oil 64, (21 & up) SawnwoodSoybean 30, (15 & up) Phosphate rock 49, (19 & up) TinSugar (U.S.) 27, (14 & up) Soybean oil 51, (0 & up) TobaccoWheat 44, (18 & up) Wool (coarse) 70, (22 & up) TSP

Wool (fine) 57, (20 & up)Zinc 94, (24 & up)

Note: Estimated average duration (half-life) of price shocks (in months) is given by the first number in each relevant column and is followed by range of duration in parentheses.

Source: IMF Finance & Development (2001) “Do Commodity Price Shocks Last Too Long for Stabilization Schemes to Work? “

Duration of Commodity Price Shocks: 1957–199812 to 28 months 48 to 96 months 96 to 216 months

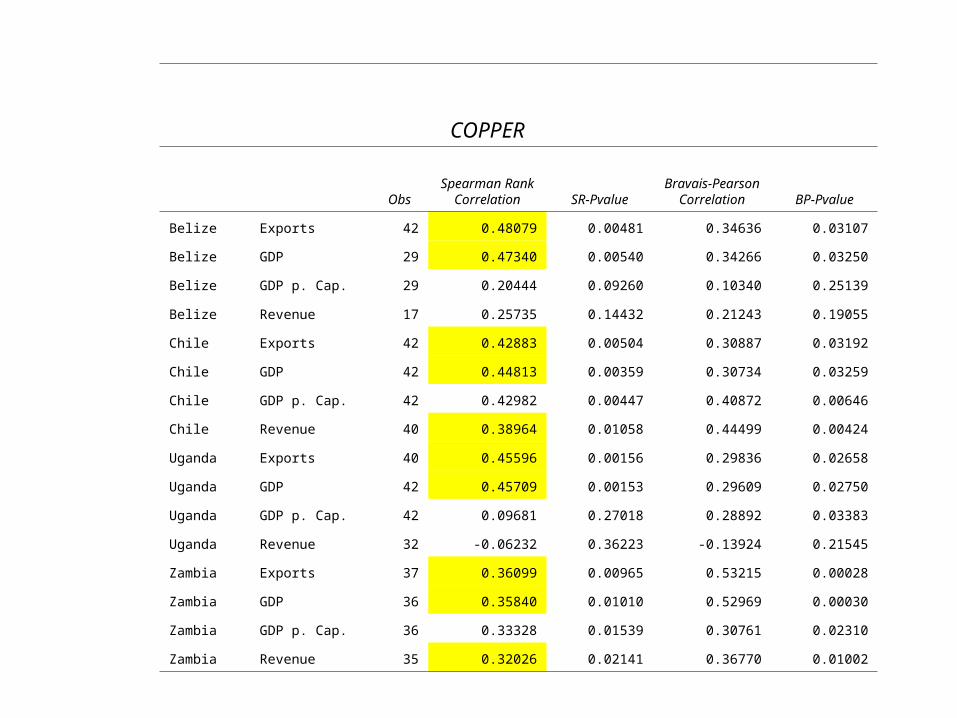

COPPER

ObsSpearman Rank

Correlation SR-PvalueBravais-Pearson

Correlation BP-Pvalue

Belize Exports 42 0.48079 0.00481 0.34636 0.03107

Belize GDP 29 0.47340 0.00540 0.34266 0.03250

Belize GDP p. Cap. 29 0.20444 0.09260 0.10340 0.25139

Belize Revenue 17 0.25735 0.14432 0.21243 0.19055

Chile Exports 42 0.42883 0.00504 0.30887 0.03192

Chile GDP 42 0.44813 0.00359 0.30734 0.03259

Chile GDP p. Cap. 42 0.42982 0.00447 0.40872 0.00646

Chile Revenue 40 0.38964 0.01058 0.44499 0.00424

Uganda Exports 40 0.45596 0.00156 0.29836 0.02658

Uganda GDP 42 0.45709 0.00153 0.29609 0.02750

Uganda GDP p. Cap. 42 0.09681 0.27018 0.28892 0.03383

Uganda Revenue 32 -0.06232 0.36223 -0.13924 0.21545

Zambia Exports 37 0.36099 0.00965 0.53215 0.00028

Zambia GDP 36 0.35840 0.01010 0.52969 0.00030

Zambia GDP p. Cap. 36 0.33328 0.01539 0.30761 0.02310

Zambia Revenue 35 0.32026 0.02141 0.36770 0.01002

COTTON

ObsSpearman Rank

Correlation SR-PvalueBravais-Pearson

Correlation BP-Pvalue

Chile Exports 42 0.40199 0.00459 0.45343 0.00165

Chile GDP 42 0.40264 0.00453 0.45395 0.00163

Chile GDP p. Cap. 42 0.10607 0.24591 0.02586 0.43344

Chile Revenue 40 0.35610 0.01216 0.32709 0.01929

Colombia Exports 42 0.45450 0.00161 0.43064 0.00263

Colombia GDP 42 0.45612 0.00156 0.43005 0.00266

Colombia GDP p. Cap. 42 0.40183 0.00460 0.41971 0.00326

Colombia Revenue 8 0.38095 0.14063 0.27729 0.21644

Nigeria Exports 42 0.32907 0.01648 0.17580 0.12728

Nigeria GDP 42 0.33004 0.01622 0.17523 0.12805

Nigeria GDP p. Cap. 42 0.49097 0.00073 0.32366 0.01797

Nigeria Revenue 37 0.37767 0.01080 0.34330 0.01839

Peru Exports 13 0.36813 0.09220 0.51960 0.03050

Peru GDP 13 0.36813 0.09220 0.51841 0.03080

Peru GDP p. Cap. 13 0.43956 0.05650 0.23068 0.20278

Peru Revenue 12 0.51049 0.03850 0.61456 0.01663

Zambia Exports 37 0.30785 0.03237 0.47792 0.00207

Zambia GDP 36 0.32124 0.02696 0.47466 0.00220

Zambia GDP p. Cap. 36 0.33807 0.01987 0.44638 0.00331

Zambia Revenue 35 0.39328 0.00999 0.55155 0.00055

PETROLEUM

Obs

Spearman Rank

Correlation SR-

Pvalue

Bravais-Pearson

Correlation BP-

Pvalue Bahrain Exports 36 0.51770 0.00357 0.35603 0.03216 Bahrain GDP 27 0.48962 0.00548 0.35915 0.03101

Bahrain GDP p. Cap. 27 0.82537 0.00000 0.88841 0.00000

Bahrain Revenue 27 0.62576 0.00057 0.44926 0.00979 Belize Exports 42 0.54187 0.00176 0.53663 0.00193 Belize GDP 29 0.55764 0.00134 0.54879 0.00156

Belize GDP p. Cap. 29 0.41194 0.00380 0.37678 0.00731

Belize Revenue 17 0.70588 0.00180 0.33723 0.08220 Colombia Exports 42 0.25023 0.05244 0.27126 0.03938 Colombia GDP 42 0.26407 0.04351 0.27303 0.03841

Colombia GDP p. Cap. 42 0.32335 0.01806 0.26561 0.04259

Colombia Revenue 8 -0.14286 0.34308 -0.08472 0.40531 Cote d'Ivoire Exports 42 0.36097 0.00966 0.13182 0.19647 Cote d'Ivoire GDP 42 0.35380 0.01093 0.12626 0.20661 Cote d'Ivoire

GDP p. Cap. 42 0.38556 0.00623 0.23194 0.06640

Cote d'Ivoire Revenue 5 0.10000 0.41153 0.06426 0.44287 Nigeria Exports 42 0.33100 0.01597 0.29239 0.02905 Nigeria GDP 42 0.33003 0.01623 0.29144 0.02946

Nigeria GDP p. Cap. 42 0.57496 0.00010 0.74699 0.00000

Nigeria Revenue 37 0.39497 0.00814 0.51574 0.00085 Venezuela Exports 42 0.26879 0.04076 0.47233 0.00110 Venezuela GDP 42 0.24811 0.05392 0.46489 0.00129

Venezuela GDP p. Cap. 42 0.71274 0.00000 0.87463 0.00000

Venezuela Revenue 41 0.31051 0.02339 0.72440 0.00000

-30

-20

-10

0

10

20

30

40

50

1970 1975 1980 1985 1990 1995 2000

World Coffee Prices (NY): Monthly Nominal Percentage Changes

-20

-10

0

10

20

30

1970 1975 1980 1985 1990 1995 2000

World Cocoa Prices: Monthly Nominal Percentage Changes

-20

0

20

40

60

80

100

1970 1975 1980 1985 1990 1995 2000

Average Crude Petroleum Prices: Monthly Nominal Percentage Changes

-30

-20

-10

0

10

20

30

1970 1975 1980 1985 1990 1995 2000

World Cotton Prices: Monthly Nominal Percentage Changes

-20

-10

0

10

20

30

1970 1975 1980 1985 1990 1995 2000

US Gulf Wheat Prices: Monthly Nominal Percentage Changes

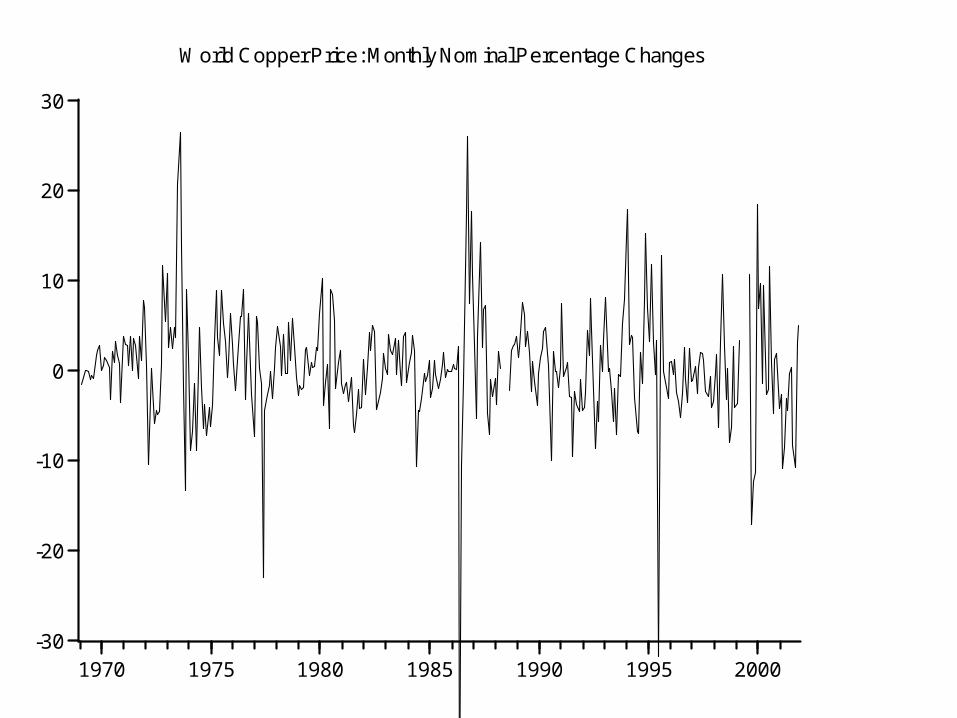

-30

-20

-10

0

10

20

30

1970 1975 1980 1985 1990 1995 2000

World Copper Price: Monthly Nominal Percentage Changes

4000

8000

12000

16000

20000

24000

28000

32000

36000

40000

1970 1975 1980 1985 1990 1995 2000

R_ALU

0

1000

2000

3000

4000

5000

1970 1975 1980 1985 1990 1995 2000

R_COBNY

0

400

800

1200

1600

2000

2400

1970 1975 1980 1985 1990 1995 2000

R_COCONY

0

5000

10000

15000

20000

25000

30000

35000

1970 1975 1980 1985 1990 1995 2000

R_COPPA

200

400

600

800

1000

1200

1400

1600

1970 1975 1980 1985 1990 1995 2000

R_COTTUSO

0

100

200

300

400

500

600

700

800

1970 1975 1980 1985 1990 1995 2000

R_PETRACP

0

50

100

150

200

250

300

350

1970 1975 1980 1985 1990 1995 2000

R_SUGCAR

0

40000

80000

120000

160000

200000

1970 1975 1980 1985 1990 1995 2000

R_TIN

0

500

1000

1500

2000

2500

3000

3500

4000

1970 1975 1980 1985 1990 1995 2000

R_WHUS

0

5000

10000

15000

20000

25000

30000

1970 1975 1980 1985 1990 1995 2000

R_ZINC

Real Commodity Prices: Absolute Values (Deflated by World CPI (IFS)), Monthly 1969 - 2001, Source: Unctad

Short-term price fluctuations• Although the focus of many observers and economists has been towards long-term price movements, the importance of short-term fluctuations did not go unnoticed. Singer (1950, 1958) made several observations about their importance.• “fluctuations in the volume and value of foreign trade tend to be proportionately more violent in that of underdeveloped countries and therefore a fortiori also more important in relation to national income.” Singer (1950, p. 473)• “The case for stabilization of terms of trade … has, it seems to me, nothing to do with the existence of their secular trends but a great deal to do with their large and extremely damaging cyclical and short-term fluctuations. Long-run trends are if anything an argument against stabilization of terms of trade, as I believe most sensible people agree. But the violent cyclical and short-term fluctuations certainly add to the underlying difficulty discerned by Prebisch and others.” Singer (1958, p. 85)• A clear and simple method for analyzing price movements is to break them down into movements along a trend and then movements around that trend. The former are associated with long-term economic factors while the latter are short-term fluctuations that are associated with either short-term factors or even “noise.”

The costs of volatility• Volatility interrupts investment, development and growth• Income variability retards development by slowing savings, discouraging investment and lowering living standards• Hampers ability to service debt• Reduces social welfare because the because of concave utility functions, i.e. diminishing marginal utility of income means that benefit of upswing is less then cost of downswing.• Government budget are correlated with commodity prices, and so fiscal policy becomes pro-cyclical. • Also, the volatility of prices of primary exports shapes the credit rating of the developing country government. High volatility can thereby lead to higher borrowing costs because investors take into consideration the dependence of the government on export commodity prices for their revenue needed to service foreign debt.• Effect on the integrity of prices as market signals, and use of signals for short and long term signals for consumption and investment decisions

Commodities vs Stocks

0

50

100

150

200

250

300

350

400

Cocoa

Coffee

Copper

Oil

Rubber

S&P

Commodities vs Stocks

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

19

93

M2

19

93

M8

19

94

M2

19

94

M8

19

95

M2

19

95

M8

19

96

M2

19

96

M8

19

97

M2

19

97

M8

19

98

M2

19

98

M8

19

99

M2

19

99

M8

20

00

M2

20

00

M8

20

01

M2

20

01

M8

20

02

M2

20

02

M8

Cocoa Coffee

Copper Oil

Rubber S&P