what you need to know for the reg exam (including ... · pdf filewhat you need to know for the...

TRANSCRIPT

What You Need to Know for the REG Exam (Including Strategies to Pass Before April 1)October 11, 2016

Introductions

• Denise ProbertCPA, CGMAWiley Director of Curriculum,Accounting Test Prep

• Julie SnowWiley CPAexcel Product Support

Webinar Agenda

• Current format of the REG exam• Current content tested on the REG exam• Format and content changes expected to the REG exam on

and after April 1, 2017• Tips and techniques for passing REG• Raffle• Ask the Expert

Testlet 124

MCQs

Testlet 224MCQs

Testlet 324

MCQs6 TBSs

Current Format of the REG Exam

60%40%

% of Exam Contents15 - 19% Ethics, Professional, and Legal Responsibilities

17 – 21% Business Law

11 – 15% Federal Tax Process, Procedures, Accounting, and Planning

12 – 16% Federal Taxation of Property Transactions

13 – 19% Federal Taxation of Individuals18 – 24% Federal Taxation of Entities

Current Content Tested on the REG Exam

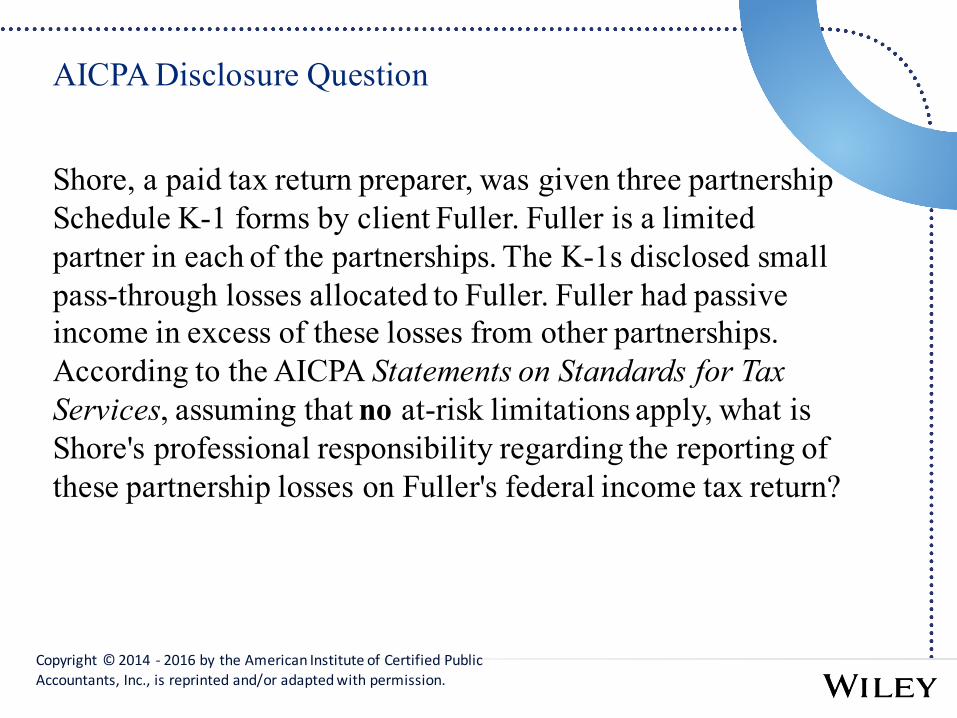

AICPA Disclosure Question

Shore, a paid tax return preparer, was given three partnership Schedule K-1 forms by client Fuller. Fuller is a limited partner in each of the partnerships. The K-1s disclosed small pass-through losses allocated to Fuller. Fuller had passive income in excess of these losses from other partnerships. According to the AICPA Statements on Standards for Tax Services, assuming that no at-risk limitations apply, what is Shore's professional responsibility regarding the reporting of these partnership losses on Fuller's federal income tax return?

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question (cont.)

A. To verify the client’s basis by examining client’s records from the initial investment to the present.

B. To accept the information without further inquiry unlessShore has reason to believe that the information is incorrect.

C. To verify the initial investment in each partnership entity unless Shore has reason to believe that the information is incorrect.

D. To request the complete partnership returns of the partnership entities unless Shore has reason to believe that the information is incorrect.

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

Which of the following types of conduct renders a contract void?A. Mutual mistake as to facts forming the basis of the contract. B. Undue influence by a dominant party in a confidential

relationship. C. Duress through physical compulsion. D. Duress through improper threats.

Copyright © 2013-‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

What is the due date of a federal estate tax return (Form 706), for a taxpayer who died on May 15, year 2, assuming that a request for an extension of time is not filed? A. September 15, year 2.�B. December 31, year 2.�C. January 31, year 3.�D. February 15, year 3.

Copyright © 2013 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

A sole proprietor of a farm implement store sold a truck for $15,000 that had been used to make service calls. The truck cost $30,000 three years ago, and $21,360 depreciation was taken. What is the appropriate classification of the $6,360 gain for tax purposes? A. Ordinary gain.B. Section 1231 (Property Used in the Trade or Business and

Involuntary Conversions) gain.C. Long-term capital gain.D. Short-term capital gain.

Copyright © 2014 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

Randolph is a single individual who always claims the standard deduction. Randolph received the following in the current year:

What is Randolph’s gross income?

Copyright © 2013-‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question (cont.)

A. $22,000B. $28,425C. $32,000D. $32,425

Copyright © 2013 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosure Question

Which of the following statements about qualifying shareholders of an S corporation is correct? A. A general partnership may be a shareholder. B. Only individuals may be shareholders. C. Individuals, estates, and certain trusts may be shareholders.D. Nonresident aliens may be shareholders.

Copyright © 2011 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

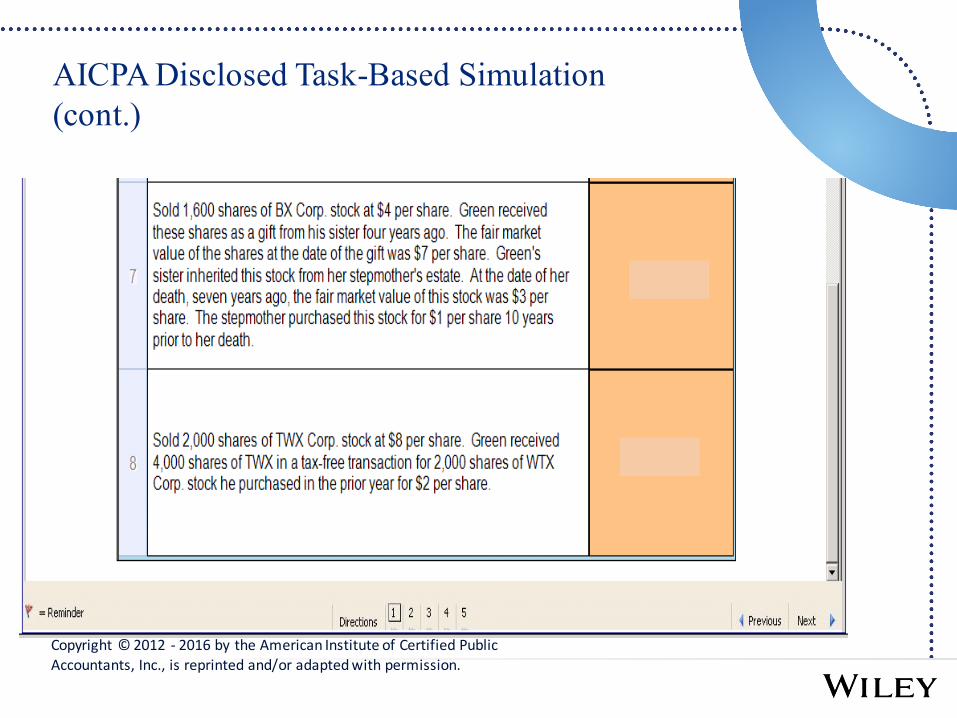

AICPA Disclosed Task-Based Simulation (cont.)

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation (cont.)

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation (cont.)

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation—Answers

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation—Answers (cont.)

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation—Answers (cont.)

Copyright © 2012 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation

Copyright © 2011 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

AICPA Disclosed Task-Based Simulation—Answer

Copyright © 2011 -‐ 2016 by the American Institute of Certified Public Accountants, Inc., is reprinted and/or adapted with permission.

REG Exam – April 1, 2017

• Major Exam changes:– Focus on and enhance the testing of higher-order

cognitive skills– Reallocate skills and content– Increase number of task-based simulations (TBSs) and

increase in MCQs for REG– Replace content specifications outlines (CSOs) with

blueprints – Increase in testing time – Change structure of Exam– Redistribute score weighting for TBSs and MCQs

Higher-Order Cognitive SkillsThe Next CPA Exam

Evaluation

Analysis

Application

Remembering and Understanding

Current Exam Focus

Next Exam Focus

Higher-Order Cognitive SkillsRegulation

Evaluation

Analysis

Application

Remembering and Understanding

Current Exam Focus

Next Exam Focus

Higher-Order Cognitive Skills

SKILL LEVELS

Evaluation The examination or assessment of problems, and use of judgment to draw conclusions.

Analysis The examinationand study of the interrelationships of separate areas in order to identify causes and find evidence to support inferences.

Application The use or demonstration of knowledge, concepts or techniques.

Remembering and understanding

The perception and comprehension of the significance of an area utilizing knowledge gained.

Source: AICPA Next Exam Structure – White Paper

Higher-Order Cognitive SkillsRegulation

SKILL LEVELSEvaluation The examination or assessment of problems,

and use of judgment to draw conclusions.Analysis The examinationand study of the

interrelationships of separate areas in order to identify causes and find evidence to support inferences.

Application The use or demonstration of knowledge, concepts or techniques.

Remembering and understanding

The perception and comprehension of the significance of an area utilizing knowledge gained.

Source: AICPA Next Exam Structure – White Paper

Reallocation of Higher-Order Cognitive Skills

Section Remembering and Understanding

Application Analysis Evaluation

Current Exam

ALL 50% 50% N/A N/ANext Exam

REG 25%-‐35% 35%-‐45% 25%-‐35% N/A

Reallocation of REG Content

I. Ethics, Professional and Legal Responsibilities

15% -‐ 19% I. Ethics, Professional Responsibilities and Federal Tax Procedures

10% -‐ 20%

I. Business Law 17% -‐ 21% II. Business Law 10% -‐ 20%

III. Federal Tax Process, Procedures, Accounting and Planning

11% -‐ 15% III. Federal Taxation of Property Transactions

12% -‐ 22%

IV. Federal Taxation of Property Transactions

12% -‐ 16% IV. Federal Taxation of Individuals 15% -‐ 25%

V. Federal Taxation of Individuals 13% -‐ 19% V. Federal Taxation of Entities 28% -‐ 38%

VI. Federal Taxation of Entities 18% -‐ 24%

AUD Exam Score Weighting

60%

40%

MCQs

TBSs

Current Exam

50%50%

MCQs

TBSs

Next Exam

Source: AICPA Next Exam Structure – White Paper

Tips and Techniques for Passing REG!

• Commit to your study planner• Life is too short – do it now• Be optimistic• Work as many questions as you can –

answer explanations are important to your understanding

• Do include a final review • Time management• Answer every question on the exam• Be confident!

Photo Credit: Probert, 2016

Raffle Time!

And the winner is…

We are awarding aWiley CPAexcel Test Bank REG Section Retail value: $150

• 1,200+ REG CPA Exam Questions with Detailed Answers

• 40 Task-based Simulations, including New DRS

• Replicates the Prometric Interface

Ask the Expert