when maximizing

TRANSCRIPT

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 1/21

WHEN MAXIMIZING SHAREHOLDERS’ WEALTH IS NOT

THE ONLY CHOICE

Dusan Mramor

Aljosa Valentincic

Address correspondence to:Faculty of Economics, University of LjubljanaKardeljeva ploscad 171000 LjubljanaSlovenia

Tel: (+386 1) 589-2442

Fax: (+386 1) 589-2698E-mail: [email protected]

This paper can be downloaded from theSocial Science Research Network Electronic Paper Collection:

http://papers.ssrn.com/paper.taf?abstract_id=258269

We are grateful to Myron Gordon, George Frankfurter, Elton McGoun and Ales Berk for helpful comments onearlier drafts of this paper.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 2/21

1

Abstract

In this paper we present the empirical analysis of financial behavior of Slovenian firms. Itfocuses on the goal of the firm, capital budgeting, capital structure and dividend-payoutdecisions. Three theories of financial behavior (neoclassical, post-Keynesian and employee

governance) with three different goals of the firm (maximization of share value, maximization of long term probability of survival and maximization of wages) provide the theoreticalbackground. A sample of 51 important Slovenian firms is analyzed using the data from aquestionnaire for chief financial officers and financial statement data. Two additional samples of listed and privatized firms are analyzed through financial statements only. We conclude that theaverage investigated Slovenian firm is still governed, as it was before privatization, byemployees, its primary goal is maximization of wages, it does not have net capital investment, isfinanced predominantly by equity, and pays very low dividends.

INTRODUCTION

In the pre-transition period in former socialist countries it was widely believed that theintroduction of private owners of capital would change the corporate governance of firms.1 InSlovenia, where the firms were mainly governed by workers (or the state), it was stronglybelieved that governance would shift to shareholders (or at least managers), changing theobjective of wage maximization to maximization of share prices and thus increase the efficiencyof these firms and the economy as a whole. What is the objective of a privatized firm today,several years after the privatization of majority of them is completed, and thus who is governingit, is the major question we shed light on in this paper.

We approach this question from the financial behavior point of view.2 Identifying the kind of

financial decisions that are actually made in these firms and comparing them to the set of decisions expected for financial behavior consistent with different objective functions of thefirm, we make inferences on the objective function(s) that is(are) actually followed.

Financial theory as a discipline consists of many competing theories and the first challange is tochoose which of these to use in the analysis. We decided to study three objective functions thatare best defined and analyzed in financial research and, in our opinion, most relevant foreconomies in transition: maximizing shareholders' wealth, maximizing long term probability of survival and maximizing wages.

The neoclassical financial theory is based on the assumption that the firm is governed by

shareholders and is therefore pursuing the goal of maximizing their wealth with maximizingmarket value of equity. What is the expected financial behavior of firms following this objectivefunction is already well presented in textbooks on corporate finance (e.g. Brealey, Myers, 1999;

1 For a more extensive analysis of opinions prevalent at that time see Mramor (1996).2 The term financial behavior of a firm embraces both the firm’s financing and investment decisions concerning bothdirect financial investments as well as investment in tangible and intangible assets. The financial function of amodern firm is not only to ensure short- and long-term liquidity, but also requires the analysis of a firm’s investmentopportunities.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 3/21

2

Brigham, Gapenski, Daves, 1999), investments (e.g. Bodie, Kane, Marcus, 1999), accountingand other subjects. It is based on a large body of literature. Some of the most importantmilestones in development of this theory, keeping in mind that the list is far from complete, are:the beginnings of the efficient market hypothesis in financial markets (Bachelier, 1900; Kendal,1953), the concept of internal rate of return (Fisher, 1930), the introduction of the assumption of

rational behavior of economic subjects in the field of corporate finance (Modigliani, Miller,1958), the development of the Capital Asset Pricing Model (Sharpe, 1964), efficient markethypotheis (i.e. Fama, 1970) and the option-pricing model (Black, Sholes, 1973). A number of authors have tested these hypotheses and models and today we have a widely-developed systemof quantitative models and qualitative theories of the logic of financial decision-making.

However, despite the large body of apparent empirical support of the neoclassical theory, thereare a number of dilemmas concerning the appropriateness of this theory in different settings.Qualitative analysis (e.g. Frankfurter and McGoun, 1996) and, to a certain extent also empiricalresearch (e.g. Haugen, 1997), have shown some serious weaknesses in the underlyingassumptions of the neoclassical theory, like the assumptions on the firm's objective to maximizesharholders wealth and on rational behavior of economic subjects. There are several ways inwhich alternative financial theories are developed but we use the findings of the theory thatassumes managers govern the firm and their objective function of maximizing long-term survivalof the firm is predominant. Following Gordon (1994), who first developed it, we use the termpost-Keynesian theory of investment and financing decisions.

The elements of previous economic systems are still present in economies of transition. Forexample, Slovenia's former economic system was based on workers' self-management of firmsand on the concept of social capital.3 The general behavior of firms governed by workers, and inparticular their financial behavior, has been the subject of a number of studies. Among the firstwas Ward (1958), and later Vanek (1970), Furubotn (1971), Mead (1972), Jensen and Meckling(1979), Horvat (1983), Ribnikar (1984), Prasnikar (1988), Kornai (1990), Nuti (1997) and othersfollowed. It is difficult to conclude unequivocally that there exists a well-supported and widely-accepted theoretical explanation of the behavior of these firms. However, there are someelements that are widely accepted, among them the third firm's objective considered in this paper- to maximization of wages.

Our starting hypothesis is that Slovenian firms are governed by managers pursuing the goal of long-term survival. We based our hypothesis on the fact that (outside) shareholders are not activeenough to take control because of the lack of knowledge and the lack of concentration of votingrights in their hands as the legal system and its enforcement do not allow their full governance.On the other side, the governing position of workers has decreased substantially with theintroduction of a new constitution and other (“capital oriented”) legislation. Therefore, we expectthat post-Keynesian theory would explain best the financial behaviour of Slovenian firms.Contrary to our hypothesis, we find that the financial behavior of a Slovenian firm conformsmost closely to the objective function of maximizing wages and, as we conclude, that it is stillpredominantely governed by employees.

3 The ther social capital is the equivalent of equity capital in firms operating in market economies, but to which nospecific owner can be attributed. The details and functioning of the system and the peculiarities in self-managedfirms are well explained in Ribnikar (1997).

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 4/21

3

The rest of the paper is organized as follows. In the next section we present the theoreticalframework of each of the three maximization objectives. This is followed by the empiricalanalysis. First, we present in empirically testable form the main differences between the threetheories concerning the goal of the firm, investment decisions and decisions on the capital

structure and dividends. A description of data for the three groups of firms analyzed here: 1) asample of larger Slovenian firms that answered a special questionaire for CFOs, 2) publiccorporations traded on the Ljubljana Stock Exchange, and 3) privatized firms, is given next.Results and interpretation represent the most extensive part of this paper and are followed byconclusion and discussion, where we present some views on the possible impact of identifiedfinancial behavior on the future economic development.

1. THEORETICAL FRAMEWORK OF FINANCIAL BEHAVIOR OF

FIRMS

We limit this part only to the most important elements of the financial behavior of firms that weare able to test with the data available to us. We focus on the goal of the firm and on its long-term investment and financing decisions.

Neoclassical Theory4

As we have already stated, neoclassical theory assumes the interests of shareholders as the mostimportant factor in financial decision-making. The goals of other interest groups represent onlyconstraints to the achievement of the owners' goals. Neoclassical theory further assumes that themaximisation of the market value of a share allows the shareholder to attain the highest-possibleutility from her equity investment in the firm.

The most important hypothesis regarding the functioning of capital markets is that they areefficient. The efficient market hypothesis (EMH) states that prices of financial assets reflect allpublicly-available information and is based on the assumption of rational behavior of marketparticipants. On the basis of this hypothesis models have been developed that allow estimates of the value of assets, expressed as the present value of its expected future cash flows. Thesemodels also allow estimates of market required rates of return on assets.

According to the neoclassical theory, the firm undertakes all investment projects whose netpresent value is greater than or equal to zero or whose internal rate of return is higher than themarginal cost of capital needed to finance them. Net present value and internal rate of return are

therefore the primary investment criteria. The estimate of cost of capital (equity) for aninvestment project at a certain point of time is based on market estimates of its riskiness. Therelevant risk is only the asset's market risk and investment decisions independent from capital-structure and dividend policy decisions.

The level of debt a firm uses depends on a number of factors, but an important part could beattributed to the costs of financial distress. The lower the probability of financial distress and the

4 Under the term Neoclassical Theory we understand its present form that also allows “market imperfections”.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 5/21

4

lower the costs of financial distress, the higher the level of debt financing a firm uses, as moredebt creates tax-shield effect of interest as a tax-deductible item. Therefore, highly-profitablefirms and firms that have relatively higher stocks of tangible fixed assets should be using moredebt. The probability of financial distress in these firms is relatively low and even if financialcrisis does occur, the cost of such crisis is relatively low, as lenders will be repaid from the sell-

off of fixed tangible assets. The liquidation value of fixed tangible assets is usually much closerto their going-concern value as opposed to intangible assets where the liquidation value might besignifically lower and in some cases even zero. The reverse is true for low-profitability firms andthose with a significant proportion of intangible assets.

Dividend policy is independent of investment and capital-structure decisions for firms that havefree access to capital markets. Therefore there is no relationship between the proportion of retained earnings and proportion of net investment in net income. The neoclassical theory doesnot come to a firm conclusion what dividend decisions firms make. Based on explanations of different factors that influence the dividend-payout ratio one might even conclude that thedividend policy does not have an important effect on the market value of a share of stock.

Post-Keynesian Theory

Agency relationships are crucial to this theory. It assumes that managers (and professionals)follow primarily their own goals when managing a firm. Further it assumes that a firm's failure(liquidation, bankruptcy) represents such a big loss to key personnel that they try to lower theprobability of failure in the long run with all their business decisions. In other words, the goal of the firm is the maximization of probability of long-term survival of the firm . It is assumed thatshareholders accept this behavior and that they see the costs associated with such behavior(agency costs) as a constituent part of costs of management and employees.5

According to this theory, the idea of efficient capital markets is very questionable. It is far moredifficult to state what are appropriate (objective) prices than it is believed under the neoclassicaltheory.

Investment decisions are primarily dependent on the size of equity capital, on the expected returnon these investments and on the riskiness of their expected returns. The market value of equity of mature firms is almost always relatively higher (e.g. per employee), and if these firms follow thegoal of maximization of probability of long-term survival, then they undertake relatively lowernet investment as compared to net income and their growth rate of fixed assets is relatively low.They also choose less risky investments. The relatively low level of net investment is also aconsequence of lower expected returns on investments of these firms. It is sensible, however, fornewer firms, which usually have lower levels of equity, to invest a relatively high proportion of net income (possibly over 100%) and to invest in relatively risky projects.6 Expected returns onthese projects are usually high. Therefore, the criteria of net present value and internal rate of return are not the only important ones – the estimates of stand-alone risk and within-firm risk of

5 Gordon (1994, p. 16) states that financial and investment decisions that do not lead to maximum market value of shares, but rather maximize the probability of long-term survival of the firm, should be treated in the same manneras wages, bonuses, share options and other perks attributed to managers for their services in managing shareholders’assets and creation of market value.6 For a theoretical explanation see Gordon (1994, pp.33-36).

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 6/21

5

projects are also important. Firms assess stand-alone and within-firm risk by means of scenarioand sensitivity analyses, but also with payback period or, indirectly, with the internal rate of return. The post-Keynesian theory also postulates that the cost of equity is lower than the cost of equity predicted by the neoclassical theory, and it is positively related to the proportion of netinvestment in net income.

A firm's riskiness is also related to the amount of debt used in financing the firm. Firms with lowlevels of equity financing (e.g. per employee) will maximise the probability of long-termsurvival if they finance their relatively large projects (high net investment to net income) of highexpected return and high risk, with debt. Therefore, such firms use more debt capital. Thereverse is true for mature firms with high absolute level of equity. They will investcomparatively less and will be predominantly financed with equity.

According to this theory, dividend policy is not independent of investment and capital structuredecisions. A firm that maximises the long term probability of survival pays out relatively lowdividends (possibly none), if it invests heavily. The payout ratio and the share of net investmentoutlay in net income should be, therefore, negatively correlated. The Post-Keynesian theory alsoconcludes that a firm's dividend payout will be low when the return on equity is high, when thevariability of this return is high, and when debt ratio is high.

The Theory of the Employee-Governed Firm7

This theoretical framework assumes either implicitly or explicitly that employees, not managersor shareholders, govern a firm. Governance by employees can be attributed to differentownership, legal or other characteristics of a firm's economic environment. Employees as aninterest group can together hold a high overall proportion of outstanding shares, with eachemployee's holding represents only a relatively small proportion of her wealth. Also, the legalframework and/or other reasons (e.g. cultural) may allow for major corporate influence byemployees.

The theory assumes that the goal of employees is to maximize wages. Wages in this context aredefined broadly as material benefits from the firm that include wages, perks, good workingconditions, short work time, but also dividends, if employees are shareholders. It is usuallyassumed that the goals of employees are relatively short-termistic.

The firm prefers investment projects with shorter payback periods and relatively higher internalrates of return compared to the cost of capital.8 However, this estimated cost of capital isrelatively low. Especially mature firms do not need much additional external equity financing,which enables them to value the cost of internally-generated equity as being low, in someinstances even zero.9 The estimated internal rate of return is not used as a measure of change in

7 It has been already emphasized that the theoretical framework of an employee-governed firm has not reached apredominant consensus among different authors. The theory described in this paper partly reflects our personalviews.8 Employees are willing to give up part of their current wages only if they can expect a significant increase in wagesin the as-near-as-possible future.9 Such firms would be obvious take-over targets; however, they are usually well protected by the law and alsothrough effective use of poison pills.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 7/21

6

shareholders' wealth, as the returns above the cost of capital are mainly intended to be paid out aswages.

Mature firms controlled by employees make few investments, because short-term wagemaximization is given priority. Higher investment layouts would impose a constraint on wage

increases over and above increases in productivity. Employee-governed firms also on averageinvest less if they are already financed to a larger extent with equity. This existing equity allowsfor a more longer-term maximisation of wages, of course to the ultimate detriment of shareholders' funds in the long run. The capital markets impose capital constraints on such firmsand they have to rely on internal sources of equity financing.

As the cost of internal equity is low, then the optimal capital structure is the lowest possible debtratio in order to maximize wages. The most important factors of each firm’s capital structure areinitial level of debt (when privatized), profitability and the total value of available (potentially)highly profitable capital investments. If profitability is low, highly profitable investment projectsare financed with debt, as it is not reasonable for employees to use very expensive externalequity financing coupled with the possible dillution of their control.

Dividend policydepends on investment and capital structure policies. The firm retains theamount of net income needed to finance acceptable investment projects. A firm with goodinvestment opportunities will, therefore, have higher levels of retained earnings than firms withfewer investment opportunities. As mature firms rarely have a large investment-opportunity set,they usually desinvest (make negative net investments) and use the proceeds to increase wages.This is the reason why labor productivity increases at a slower growth rate than wages.

»Dividends« in an employee-governed firm can take on very different forms and can be paid notonly to shareholders but also to workers. How much of the residual earnings allocated to be paidout is actually paid out in the form of dividends to shareholders depends on the proportion of shares held by employees, on the tax system, and the marginal tax rates. The firm will pay outsuch a share of residual earnings in the form of dividends that employees will maximize theircash flow from the firm. This cash flow is maximized when the sum of tax-payments andpayments to external shareholders are minimised. Therefore, dividends might even equal zero,and employees award themselves additional wages, bonuses and other perks.10 In the case of high growth firms that will potentially need to raise external equity, some “appropriate” level of dividends are paid to avoid capital constraints. Firms with high profitability also have a higherpayout ratio, as wages, bonuses and other perks, are usually progressively taxed. On the contrary,more indebted firms tend to retain more earnings to repay more expensive debt and build up (lessexpensive) equity financing.

Financial Behavior of a Slovenian Firm

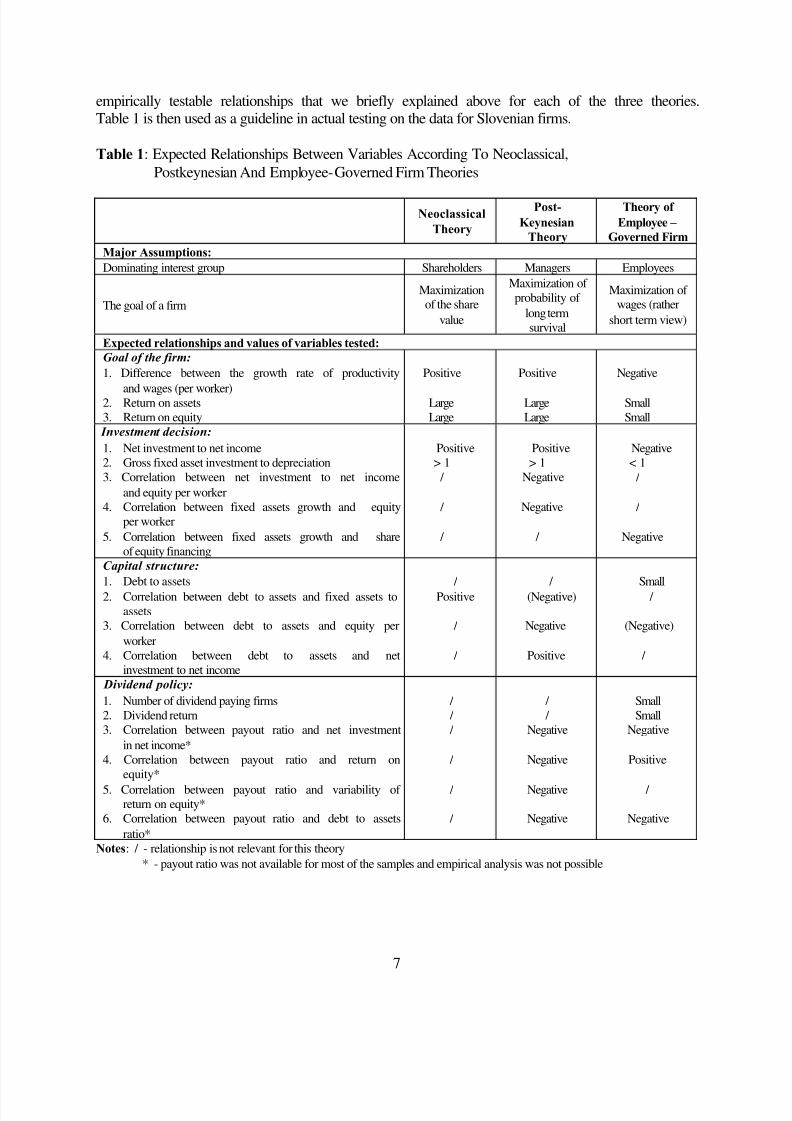

In order to allow for an empirical analysis of financial behavior of Slovenian firms, to find theirobjective function and dominanting interest group, we first summarise in Table 1 those

10 Treven (1995) has developed a dividend-payout model that shows, for a given tax system, the proportion of sharesheld by employees needed to make a payout of true dividends rational for employees-shareholders.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 8/21

7

empirically testable relationships that we briefly explained above for each of the three theories.Table 1 is then used as a guideline in actual testing on the data for Slovenian firms.

Table 1: Expected Relationships Between Variables According To Neoclassical,Postkeynesian And Employee-Governed Firm Theories

Neoclassical

Theory

Post-

Keynesian

Theory

Theory of

Employee –

Governed Firm

Major Assumptions: Dominating interest group Shareholders Managers Employees

The goal of a firmMaximizationof the share

value

Maximization of probability of

long termsurvival

Maximization of wages (rather

short term view)

Expected relationships and values of variables tested: Goal of the firm:

1. Difference between the growth rate of productivity

and wages (per worker)2. Return on assets3. Return on equity

Positive

LargeLarge

Positive

LargeLarge

Negative

SmallSmall

Investment decision:

1. Net investment to net income2. Gross fixed asset investment to depreciation3. Correlation between net investment to net income

and equity per worker4. Correlation between fixed assets growth and equity

per worker5. Correlation between fixed assets growth and share

of equity financing

Positive> 1 /

/

/

Positive> 1

Negative

Negative

/

Negative< 1 /

/

Negative

Capital structure:

1. Debt to assets2. Correlation between debt to assets and fixed assets to

assets3. Correlation between debt to assets and equity per

worker4. Correlation between debt to assets and net

investment to net income

/ Positive

/

/

/ (Negative)

Negative

Positive

Small /

(Negative)

/

Dividend policy:

1. Number of dividend paying firms2. Dividend return3. Correlation between payout ratio and net investment

in net income*4. Correlation between payout ratio and return on

equity*

5. Correlation between payout ratio and variability of return on equity*

6. Correlation between payout ratio and debt to assetsratio*

/ / /

/

/

/

/ /

Negative

Negative

Negative

Negative

SmallSmall

Negative

Positive

/

Negative

Notes: / - relationship is not relevant for this theory* - payout ratio was not available for most of the samples and empirical analysis was not possible

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 9/21

8

2. DATA

We use three sets of data to test the relationships outlined in Table 1. The first set of data wascollected with a questionnaire for Chief Executive Officers (CFOs) for a sample of 51 privatizedSlovenian firms, that we term herein as interviewed firms. In 1996, the Faculty of Economics,

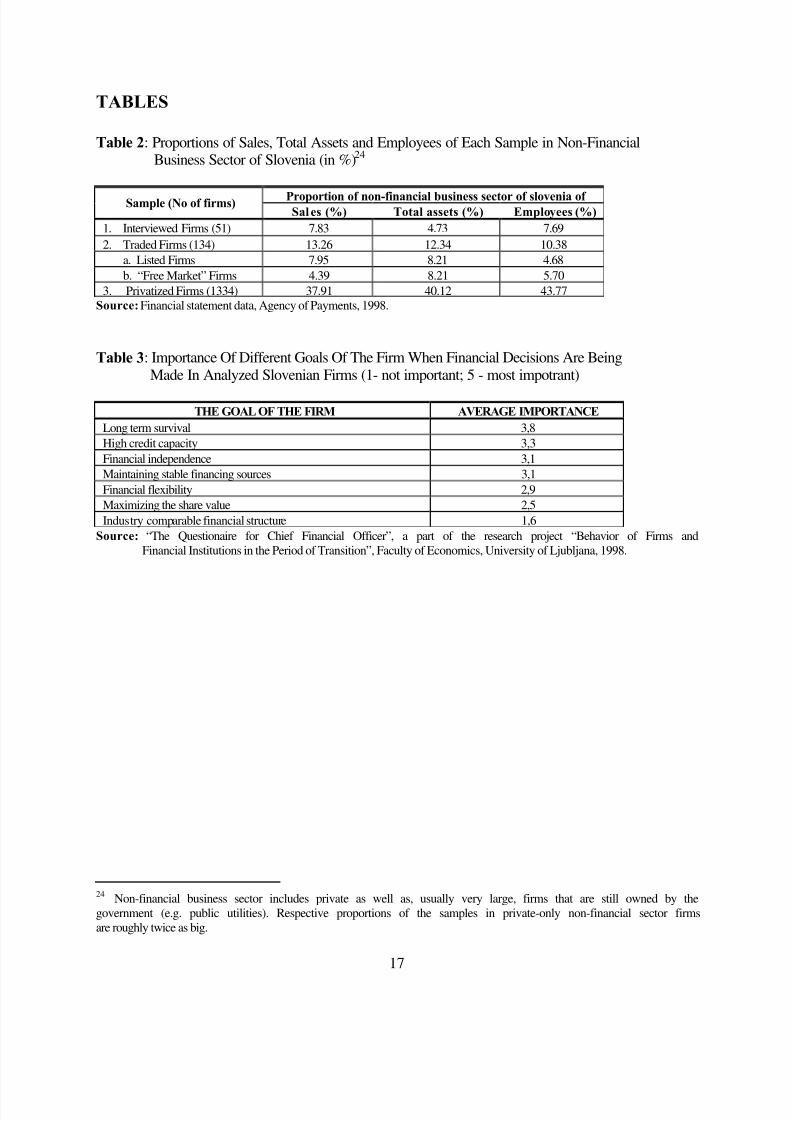

University of Ljubljana, Slovenia, started an extensive five-year research project on the behaviorof Slovenian firms in transition. Financial and other data were collected, and an extensivequestionnaire was prepared for the management. Hundred largest Slovenian firms were selectedto be investigated, and for 51 of them, mainly in 1998, CFOs completed the part of questionnairethat was aimed at investment and financing decisions. For these 51 firms data financial statementdata were also collected for the year 1998. This set of data gives us valuable insights into thedecision processes of Slovenian CFOs, unfortunately for only a rather small number of otherwiseimportant Slovenian firms, as can be seen from Table 2.

The second and third set of data was drawn from the database of the Agency for Payments of Slovenia.11 The former data set consists of the financial statements' data for the period 1994-

1999 of 134 public firms that are traded on the Ljubljana Stock Exchange (LJSE) – termedherein as traded firms.12 This sample consists of public corporations where the pressure of thecapital market could influence their objective function. They represent an important part of thenon-financial business sector in Slovenia. We have also divided these firms into two subsamples– those listed on the LJSE and those trading on the so-called “free market” that are not requiredto comply with listing requirements – we term them “free market” firms13 herein. We haveanticipated different financial behavior of listed firms than those trading on the free market as thepressure of the capital market (outside shareholders) on listed firms is presumably biggest. Table2 shows importance of these firms in the non-financial sector.

<TABLE 2 ABOUT HERE>

The third data set consists of financial statement data for the period 1994-1999 for all privatizedfirms for which data was available.14 There are 1,334 firms in this sample that we term privatized firms. A big majority of these are closed corporations, predominantly employee and managementowned, and a different objective function can be expected than for firms in the first and secondsamples. This is also the biggest sample with respect to its economic importance as it representsthe major part of private non-financial business sector of Slovenia.

11 The Agency of Payments currently still acts as the central institution that maintains the payment system amongfirms in Slovenia. The payments among firms are not, therefore, done through banks, as is normal in developedeconomies. This is being introduced only now – at present, only a handful of firms are included in this scheme. As acorollary of its functions, firms are required by law to provide financial statement data to the Agency.12 Of the 51 firms in the first sample, 17 are traded on LJSE, while the rest are closed corporations.13 LJSE is divided into “official” market, where only listed firms are traded, and “free” market, where any otherpublic corporation can be traded. Therefore, we distinguish between “traded on LJSE”, that applies to both markets,“listed”, which applies only to offical market and “traded on free market”.14 Some of the privatized firms have undergone extensive programs of restructuring and have not submitted thefinancial statement data to the Agency of Payments.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 10/21

9

3. EMPIRICAL RESULTS AND INTERPRETATION

In this section we presenting the results of empirical analysis and discussing them following theoutline from Table 1.

The goal of the firm. Table 3 presents the summary of answers of CFOs on the questionsconcerning the goal of the firm.

<TABLE 3 ABOUT HERE>

From these answers it could be concluded that maximization of the probability of long-termsurvival is the goal of a Slovenian firm. However, it might be the case that the overall goal isdifferent than the one stated by CFOs. If the actual overall goal leads to illiquidity andinsolvency, CFOs could, in order to fullfill their direct job requirement of maintaining theliquidity and solvency of the firm, follow the goal of long-term survival with maintaining highcredit capacity, stability of financial sources, financial independence (e.g. with low indebtness),

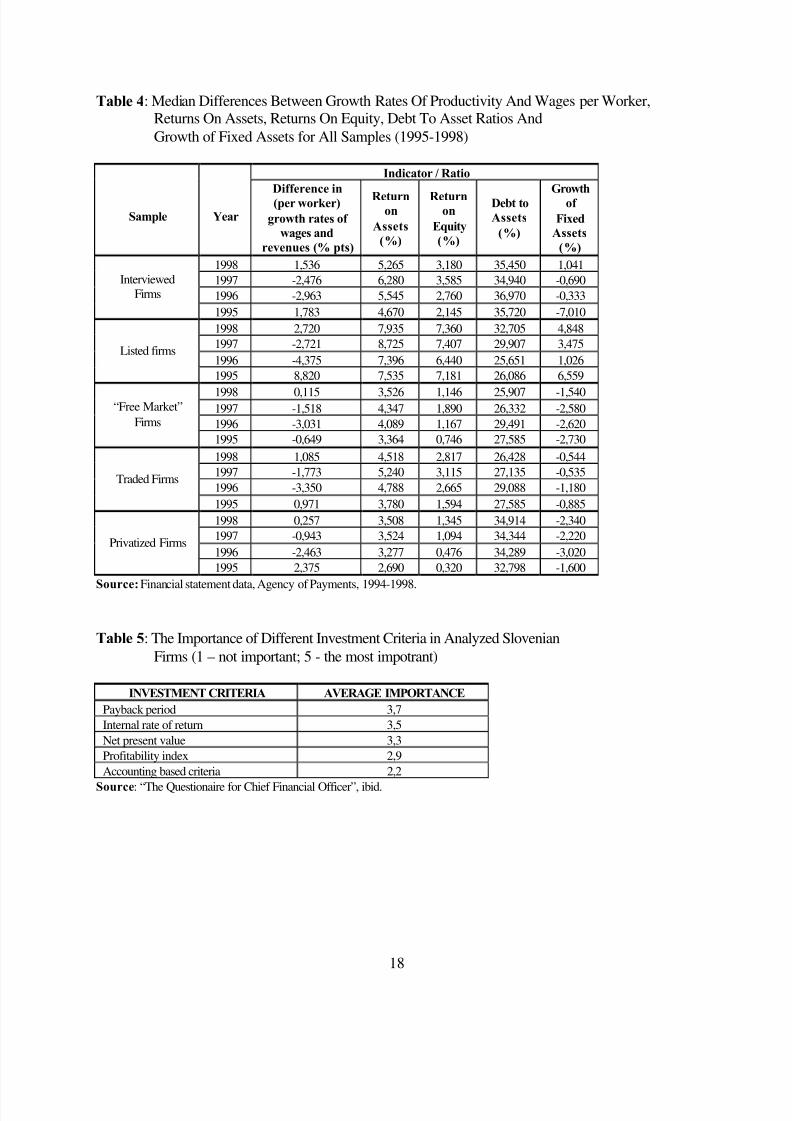

etc. This might in turn lead to the answers as presented in Table 3, although in a normal situationthey might follow any of the other goals, stated or not in the table. As financial data could reveala clearer picture of the actual goal of a Slovenian firm, we calculated the difference betweengrowth rate of wages per worker and growth rates of productivity per worker, return on assets,and return on (book) equity ratio for all samples. Results are presented in Table 4.

<TABLE 4 ABOUT HERE>

First coloumn in Table 4 shows the differences between growth rates of wages and growth ratesof productivity per worker. It can easily be observed that time pattern of the sign of thedifference is practically the same for all samples. In 1995 and in 1998 wages have grown faster

than productivity and slower in the years 1996 and 1997. However, we should mention thatbonuses and other perks were not included among wages and we suspect that their inclusionwould increase a number of positive signs.15 Nevertheless, the explanation of this time pattern israther straightforward. In 1995, before the actual impact of private ownership, wages per workerwere growing faster than the total revenue per worker, as firms were governed the same way asin the previous economic system. In 1996 and 1997 the firms experienced for the first timeprivate owners and their demands. They responded by slightly increasing returns on assets andequity, also by reducing the growth of wages. But after these first two years of experience withprivate ownership, wages have resumed their excessive growth over productivity-growth at therate ranging from 0.257 to 2.720 percentage points in 1998. We might conclude, therefore, thatthe goal of most firms in the sample is the maximization of wages. This is also supported by the

fact that the median return on equity of the firms in all samples is very low and that it 1998 itwas even lower than in 1997. The same also applies for return on assets.16 However, on the basisof data presented in Table 4 one could conclude that firms with more exposure to the capitalmarket and thus outside shareholders (i.e. listed firms) have higher median return on equity (andon assets) and that their objective function might be different from oter firms' objectivefunctions. But the starting levels of these ratios in 1995 should not be neglected. These firms

15 Data on bonuses and other perks are not publicly available, not even for listed firms.16 It is important to stress that return on assets is higher than return on equity in all years and all samples.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 11/21

10

were more profitable at the beginning of privatization process and they have not increased theirrates of return on equity (or assets) more than other firms in the period from 1995 to 1998.

Such a policy of earnings distribution in favor of wages reduces substantially the probability of long term survival of the firm, and it is more or less clear to CFOs that they will have great

difficulties in maintaining liquidity and solvency. In our opinion this is the reason that led CFOsto presented answers concerning the goal of the firm are in accordance with post-Keynesiantheory, while the majority of firms is in reality following the goal of maximizing wages. Of course there are differences among firms. However, on the basis of financial data and answers of CFOs, only a handful of firms can be identified that pursue the goal of maximizing the marketvalue of shares, while other non-employee governed firms are governed by the management andtry to maximize long term probability of survival.

The Slovenian capital market is, according to empirical research completed so far, not efficienteven in the weak form (e.g. Dezelan, 1996 and Aver, Petric, Zupancic, 2000). Therefore, it is fairto assume that prices of securities are different from their intrinsic values and it is thereforeproblematic for firms to rely on market prices and rates of returns in their financial decision-making as is suggested by the neoclassical theory.

Investment decisions. Concerning the importance of different investment criteria, CFOs answersare presented in Table 5.

<TABLE 5 ABOUT HERE>

Payback period, being the most important investment criteria, excludes the possibility to explaincapital investment behavior of Slovenian firms with the neoclassical theory. The order of importance indicates either behavior in accordance with employee-governed or, possibly, post-Keynesian theory.17 When we add answers to the questions concerning the estimates of the costsof different forms of capital, there is little doubt left that the theory of the employee-governedfirm best explains the capital investment behavior of Slovenian firms. 90% of the analysed firmsestimate that the cost of equity is zero, and and another 8% estimate these costs to be smallerthan the costs of long term debt. In addition, only 36% of firms analyse the riskiness of investment projects and consider risk as an important element in investment decision, which is atthe core of post-Keynesian theory.

Further, firms invest little. As can be seen from Table 4, except for the listed firms, netinvestment was negative (negative growth rate of fixed assets) in the whole period studied. Asfirms have not invested even in the amount of depreciation expenses, this does not seem toconform with neither neoclassical nor post-Keynesian theory.

In Table 6 we present the results of correlations concerning investment behavior, specified inTable 1. These correlations are testing the accordance of the behavior with the Post-Keynesiantheory and the Theory of employee-governed firm.

17 Following the post-Keynesian theory we could expect internal rate of return being more important than paybackperiod, as IRR is most likely a better measure of relative riskiness of an investment project than payback period.However, we aware that such a statement is more or less subjective.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 12/21

11

<TABLE 6 ABOUT HERE>

The results of cross-sectional regressions presented in Table 6 show that after controling for thedifference in capital intensivness (fixed asstes per worker) between firms, the only statisticallysignificant (negative) relationship is for the firms traded on the free stock market. This

relationship is also in accordance with Post-Keynesian theory implying that investment behaviorof these firms is primarily driven by the goals of managers. Statistical significance for thisrelationship for traded firms is only a consequence of the fact that the sample of traded firms alsoincludes “free market firms”, while the relationship for listed firms is not statistically significant.It is quite obvious from the third relationship tested (fixed asset growth as the dependentvariable) that listed firms behave more like employee-governed firms, as the correlation betweenfixed assets growth and equity to assets is negative and statistically significant on 5% level,which is in accordance with theoretical explanation.

Capital structure. From the answers of CFOs concerning the policy of financing (capitalstructure), the following can be concluded. To the question of which are the most importantfactors involved in capital structure decisions, a large majority of CFOs answered that expectedfinancing needs of investment projects are the most important. Capital structure decisions are,therefore, closely tied to investment decisions. This excludes neoclassical behavior, where thesedecisions are in principle independent. Dependence of these decisions is assumed by post-Keynesian and employee-governed firm theories. In Table 7 we present the views of CFOs onthe attractivness of different forms of financing.

<TABLE 7 ABOUT HERE>

It is clear from the Table 7 that by far the most attractive source of financing is internal equitycapital. Much less attractive forms of financing are outside bank long term loans and externalequity capital.18 This result is in accordance with the pecking-order theory (Myers and Majluf,1984), one branch of neoclassical theory based on assimetric information. However, thedifference between the attractivness of inside equity and debt is most likely overstated andexplains only a part of the differences among firms. The result of course contradicts mainstreamneoclassical theory, as heavy reliance on costly equity capital does not lead to minimum costs of capital. It is more likely that the high attractivness of inside equity financing is in accordancewith the employee-governed firm theory, as explained above.19 However, since most of the firmsin the sample are mature, it is difficult to exclude the post-Keynesian theory, where mature firmsmaximize the probability of long term survival if they are financed predominantely with equity.

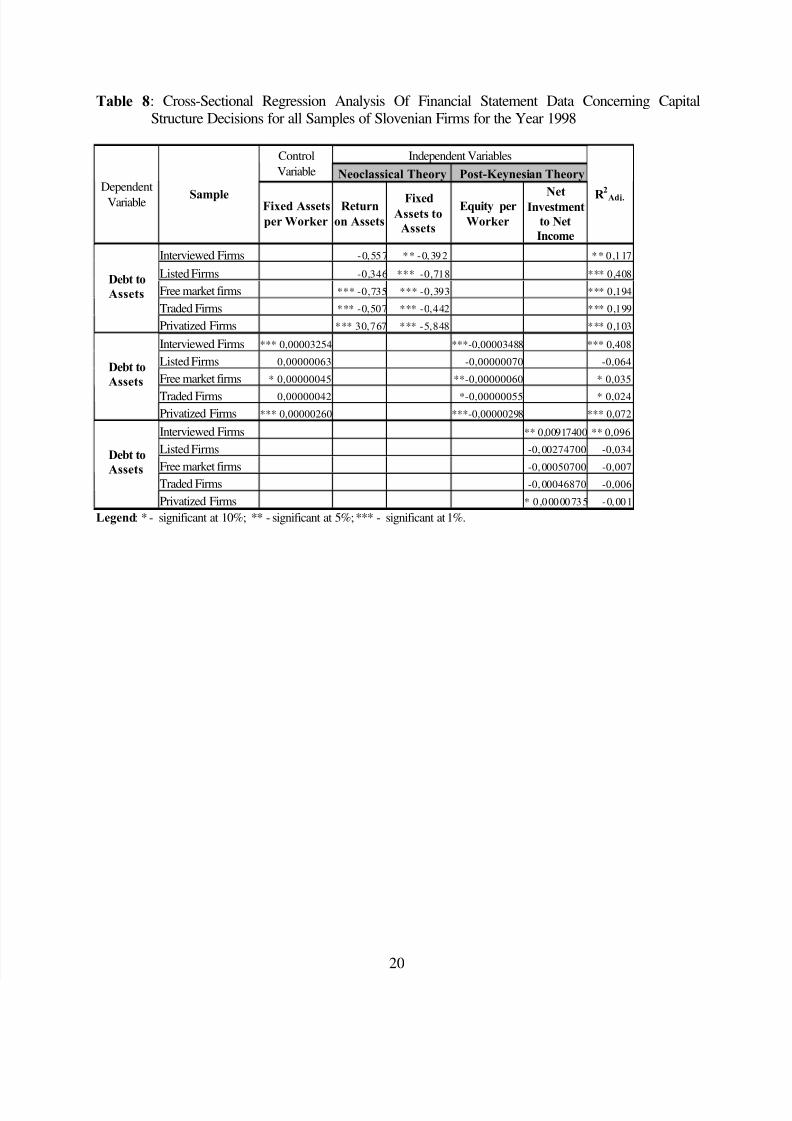

The regression analysis of financial statement data presented in Table 8 leads to the rejection of the neoclassical capital structure behavior of the firms.

<TABLE 8 ABOUT HERE>

18 Such an order of attractiveness means that dividend policy is not independent on capital structure.19 Since there are predominantly mature firms in the sample, a post-keynesian approach also cannot be completelyruled-out. According to the post-keynesian theory, mature firms make less risky decisions, including financing withmore equity, to maximize the probability of long-term survival.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 13/21

12

It can be observed in Table 8 that the correlation between profitability, measured as return onassets, and the proportion of debt financing used, is negative and statistically significant in mostsamples. There is also a strong negative correlation between the proportion of fixed assets anddebt financing for all samples in 1998. These relationships are in contrast to one of the corepropositions of the neoclassical theory that require positive correlations among these variables.

These results could be more in line with the post-Keynesian theory where less risky operationsare financed with less with debt and more with equity. For example, the operations of a firm withmore fixed assets are presumably less risky, as there is a large stock of fixed assets that might beused as a collateral. Also, there is negative correlation between equity per worker and theproportion of debt financing for all samples, which is in accordance with Post-Keynesian theory.Low median level of debt to assets ratio (see Table 4) and the fact that inteviewed and listedfirms are predominantely mature firms, additionally enforce the above conclusions.

However, these results are not in contrast with the behavior of the employee-governed firm andthis explanation becomes even more probable when these results are compared to the answers of CFOs to the questionnaire regarding the capital structure (Table 7).

Dividend policy.Concerning dividend policy, the CFOs considered stability of dividends, andwell-informed shareholders when changes in this policy occur as the two most important factors.Not much different in ranking of importance was the alignment of dividend policy with the needsof financing planned investment projects.

As already stated, the firms in the sample of interviewed companies have on average negative netcapital investments, high growth rates of wages and very low returns on equity (median ROE around 3%). Even from this data alone we can conclude that dividends are not of primaryconcern. This conclusion is further supported by CFO's opinions on the most appropriate payoutratio of 31% (in 1996 it was actually 55%, but only 40% of firms in the sample of interviewedfirms paid dividends). This is similar to the average payout ratio of listed firms in 1998 (31.4%),where 85% of firms paid dividends. However, only 30% of firms traded on the free market paiddividends in 1998.

Although these average payout ratios are in accordance with payout ratios in developedeconomies, they are based on very low net income levels. Therefore, these dividends representonly a very small proportion of total distrubuted residual earnings that are much bigger than netincome, where wages for employees (and management), in the broader meaning of the word,represent the most important part.20 This is of course contrary to neoclassical behavior of firms.If one used the term »dividends« for all distributed residual earnings (to employees andshareholders), she could claim that Slovenian firms in the sample of interviewed firms behaveaccording to post-Keynesian theory. Namely, they are mainly mature firms they have lowinvestment outlays and pay out high dividends. However, such »dividend« policy, tied toinvestment and financing policies as explained above, does not maximize the probability of longterm survival, as assets and equity decrease over time. Therefore, the competitivness of these

20 An explanation of the problems of dividend (or “dividend”) policy of Slovenian firms can be found in Mramor(1996).

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 14/21

13

firms on a global market declines in the long run. In our opinion it is better to conclude that thisis not Post-Keynesian behavior but the behavior of employee-governed firms.

4. DISCUSSION AND CONCLUSION

The above analysis leads us to the reasonable conclusion that an average privatized Slovenianfirm does not pursue the goal of maximizing the market value of its shares in its financialdecisions. Thus, neoclassical theory based on shareholders primacy does not apply. For amajority of these firms it is also most probable that they do not maximize the probability of longterm survival as assumed by post-Keynesian theory, where managers are the most importantinterest group. Rather, they pursue wage-maximization. Empirical results are inconclusive onlyfor capital structure decisions. However, if we assume a certain consistency in financialdecisions taken by any particular, we have to reject our hypothesis of post-Keynesian behaviorfor capital structure decisions as well.

The financial behavior of privatized Slovenian firms in our samples is best explained asemployee-governed behavior. Such behavior assumes that employees are the governing interestgroup as the goal of these firms is (rather short term) maximization of wages. Relatively largefirms in our samples on average decrease their assets, are financed predominantely by equity,have very low returns on assets and equity, pay very low dividends and have higher growth rateof wages than productivity.

There are a number of possible reasons for such financial behavior, even several years afterprivatization. We consider five here. The first concerns the majority shareholding by employeesin most privatized firms and an important share in others. A part of these shares was granted toemployees, and the other part was bought by them with a substantial discount. Since each

employee has a small fraction of shares, investment in shares of the firm might not be regardedas a significant proportion of wealth in comparison to her wage (in its broader meaning).However, the larger firms in our first sample and listed firms are majority-owned by outsideinvestors. Important shareholders in these firms are usually block-holding financial institutions(privatization investment funds) that often take on active roles on the boards. As these firms alsoin general behave like other firms, ownership structure can not solely explain financial behavior.

The second reason is the two-tier governance system, with employee participation on both thesupervisory and management boards of medium and large firms, which is a consequence of thecorporate law implemented as a part of transition process.21 In our opinion this is also not thesole reason, as with one member of the management board, half or less members on the

supervisory board and no members on the shareholder’s assembly (the highest coporate body),employees can not outweight managers and shareholders. The third reason could be strong laborunions as an external factor that contributes to increasing wages.

21 Firms over 500 employees must have a representative of the employees on the management board and at least onethird of the members of the supervisory board, while for firms with more than 1000 emplyees this number rises to atleast one half of supervisory board. For an excellent treatment of the legal framework of Slovenian companies, seeGregoric, Setinc-Tekavec (2000).

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 15/21

14

But it is our belief that the fourth and most important factor is cultural. Decades of labourmanagement where employees were governing firms through workers’ councils and electingmanagers resulted in a special kind of relationships between workers and management.Managers were just first among equals pursuing the goal of maximizing wages. Changing from“a friend” with the same goal to a person who is pursuing mainly his own goal or even the goal

of somebody else (shareholders') at the expense of workers, is in a close society of a smallcountry a very long-term process. During this process, the so called “soft budget constraint” willstill apply to wages.

According to some CFOs who are well educated and trained in the “West”, a fifth reason wassuggested. It is simplyy the lack of knowledge of existing CFOs that have for decades used acertain logic and tools appropriate for the former economic system, but inappropriate forprivatized firms.22 In our opinion the combination of all these reasons leads to the explainedbehavior of Slovenian firms.

Some authors consider this behavior a serious problem and propose different legal and othermeasures reducing the governing powers of employees and increasing the influence of managers(e.g. Prasnikar and Gregoric, 1999, p. 49; Bohinc and Bainbridge, 1999). In this respectPrasnikar and Gregoric assume that maximization of the probability of long term survival of firms is, from the macroeconomic point of view at this stage of development, a more appropriategoal than maximization of wages or maximization of the market value of shares.23 Bohinc andBainbridge are concerned with possible self-dealings of Slovenian block shareholders (primarilyfinancial institutions) if their governing power would be increased to the level known in the U.S.,but without the neccessary minority shareholder protection. Implicitly, they also perceivemanagers' objectives as most benefitial for the creation of value for the society as a whole.However, it is a question if Slovenian firms with managers' governance would be long-runsurvivors in global competition where equity capital is becoming an increasingly importantgoverning force of firms.

22 A detailed description of the level of knowledge among financial professionals in Slovenian firms can be found inMramor (1998).23 They assume that maximization of the market value of shares is not an appropriate goal of Slovenian firms withthe current structure of shareholders who base their share valuation predominantly on expected dividends in the verynear future.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 16/21

15

REFERENCES

1. AVER, B., PETRIC, M. in ZUPANCIC, B.,”Effeciency of the Capital Market”, inMRAMOR, D. (ed.): Capital Market in Slovenia. (in Slovene) Gospodarski vestnik, 2000,301-354.

2. BACHELIER, L.: Theorie de la Speculation. Gauthier-Villars, Paris, 1900.3. BLACK, F. in SCHOLES, M., "The Pricing of Options and Corporate Liability", Journal of Political Economy, May-June 1973, 81, 637-654.

4. BODIE, Z., KANE, A. and MARCUS, A.J.: Investments. (4th ed.) Irwin, Chicago, 1999.5. BOHINC, R. and BAINBRIDGE, S.M., “Corporate Governance in Post-Privatized

Slovenia”, http://papers.ssrn.com/paper.taf?abstract_id=199548, 1999.6. BREALEY, R.A. and MYERS, S.C.: Principles of Corporate Finance. (6th Ed.) McGraw-

Hill, New York, 1999.7. BRIGHAM, E.F., GAPENSKI, L.C. and DAVES, P.R.: Intermediate Financial

Management. (5th ed.) Dryden Press, New York, 1999.8. DEZELAN, S., “Efficiency of the Capital Market: Theory, Empirical Findings, and the Case

of Slovenia”, (in Slovene) MSc Thesis, Faculty of Economics, University of Ljubljana,1996.9. FAMA, E.F., “Efficient Capital Markets: A Review of Theory and Empirical Work”,

Journal of Finance, May 1970, 25, p. 383-416.10. FISHER, I.: The Theory of Interest. Augustus M. Kelley, New York, 1965 (reprint).11. FRANKFURTER, G.M. and MCGOUN, E.G.: Toward Finance With Meaning : The

Methodology of Finance : What It Is and What It Can Be. JAI, 1996.12. FURUBOTN, E.G., " Toward a Dynamic Model of the Yugoslav Firm", Canadian Journal

of Economics, 2/1971, 4, 182-197.13. GORDON, M.J.: Finance, Investment and Macroeconomics – The Neoclassical and a Post

Keynesian Solution. Edvard Elgar, Aldershot, 1994.

14. GREGORIC, A. and TEKAVEC-SETINC M.: The legal framework of Slovenian corporategovernance. Working paper, University of Ljubljana, 2000.15. HORVAT, B., Political Economy of Socialism. Globus, Zagreb, 1983.16. HAUGEN, R.: The New Finance; The Case Against Efficient Capital Markets. Prentice

Hall, 1995.17. JENSEN, M.C., MECKLING, W.H., "The Theory of The Firm: Managerial Behavior,

Agency Costs and Capital Structure", Journal of Financial Economics, 3 (1976), 305-360.18. JENSEN, M.C., MECKLING, W.H., "Rights and Production Functions: An Application to

the Labor-managed Firms and Codetermination", Journal of Business, 4/1979, 72, 469-506.19. KENDALL, M. G., “The Analysis of Economic Time-Series, Part I. Prices”, Journal of

Royal Statistical Society, 1953, 96, 11-25.

20. MCGOUN, E.G., “A Re-evaluation of Market Efficiency Measurement”, CriticalPerspectives on Accounting, 1996, 1, 263-274.21. MEADE, J.E., "The Theory of Labour-Managed Firms and of Profit Sharing", Economic

Journal, March 1972 (suppl.), 82, 402-428.22. MODIGLIANI, E. in MILLER, M.H., "The Cost of Capital, Corporation Finance and the

Theory of Investment", American Economic Review, June 1958, 48, 261-297.23. MRAMOR, D., “Dividend Policy in the World and in Slovenia”, (in Slovene) Slovene

Economic Review, June, 1996, 47, 191-202.24. Mramor, D., "Primary Privatization Goal in Economies in Transition", The International

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 17/21

16

Review of Financial Analysis, Vol. 5, No. 2, 1996, pp. 131-143.25. MRAMOR, D., “What is Transition and Transition to What? : Business Finance in

Transition Economy of Slovenia”, in 4th Conference on Alternative Perspectives on Finance,August 6-8, Turku, 1998, 17-1 – 17-18.

26. MYERS, S.C. in MAJLUF, N.S., “Corporate Financing and Investment Decisions When

Firms Have Information That Investors Do Not Have”, Journal of Financial Economics,1984, 13, 187-22227. NUTI, D.M., “Employeeism: Corporate Governance and Employee Share Ownership in

Transition Economies”, in SKREB, M. (ed.): Macroeconomic Stabilization in Transition

Economies. CUP, Cambridge, 1997, 126-154.28. PRASNIKAR, J. in GREGORIC, A., “Worker’s Participation in Slovenian Firms – Ten

Years After”, in PRAŠNIKAR, J. (ed.): Postprivatization Behaviour of Slovenian Firms. (in Slovene) Gospodarski vestnik, Ljubljana, 1999, 27-56.

29. PRAŠNIKAR, J., SVEJNAR, J., “Enterprise Behavior in Yugoslavia”, Advances in theEconomic Analysis of Participatory and Labour-Managed Firms, 3, 1988, 237-312.

30. RIBNIKAR, I., “Business Sector and Inflation”, (in Slovene) Banèni vestnik, no.. 9(September), 1984.

31. SHARPE, W.F., "Capital Asset Prices: A Theory of Market Equilibrium under Conditionsof Risk", Journal of Finance, September 1964, 19, 425-442.

32. TREVEN, M., "Dividend Policy in Slovenian Firms", BA Thesis, Faculty of Economics,University of Ljubljana, Ljubljana, 1995.

33. VANEK, J.: The General Theory of Labor-Managed Market Economies. CornellUniversity Press, Ithaca, 1970.

34. WARD, B., "The Firm in Illyria: Market Syndicalism", The American Economic Review,September 1958, 48, 566-89.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 18/21

17

TABLES

Table 2: Proportions of Sales, Total Assets and Employees of Each Sample in Non-FinancialBusiness Sector of Slovenia (in %)24

Proportion of non-financial business sector of slovenia of Sample (No of firms)Sales (%) Total assets (%) Employees (%)

1. Interviewed Firms (51) 7.83 4.73 7.692. Traded Firms (134) 13.26 12.34 10.38

a. Listed Firms 7.95 8.21 4.68b. “Free Market” Firms 4.39 8.21 5.70

3. Privatized Firms (1334) 37.91 40.12 43.77Source: Financial statement data, Agency of Payments, 1998.

Table 3: Importance Of Different Goals Of The Firm When Financial Decisions Are BeingMade In Analyzed Slovenian Firms (1- not important; 5 - most impotrant)

THE GOAL OF THE FIRM AVERAGE IMPORTANCE

Long term survival 3,8High credit capacity 3,3Financial independence 3,1Maintaining stable financing sources 3,1Financial flexibility 2,9Maximizing the share value 2,5Industry comparable financial structure 1,6

Source: “The Questionaire for Chief Financial Officer”, a part of the research project “Behavior of Firms andFinancial Institutions in the Period of Transition”, Faculty of Economics, University of Ljubljana, 1998.

24 Non-financial business sector includes private as well as, usually very large, firms that are still owned by thegovernment (e.g. public utilities). Respective proportions of the samples in private-only non-financial sector firmsare roughly twice as big.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 19/21

18

Table 4: Median Differences Between Growth Rates Of Productivity And Wages per Worker,Returns On Assets, Returns On Equity, Debt To Asset Ratios AndGrowth of Fixed Assets for All Samples (1995-1998)

Indicator / Ratio

Sample Year

Difference in

(per worker)

growth rates of

wages and

revenues (% pts)

Returnon

Assets

(%)

Returnon

Equity

(%)

Debt to

Assets

(%)

Growth

of

Fixed

Assets

(%)

1998 1,536 5,265 3,180 35,450 1,0411997 -2,476 6,280 3,585 34,940 -0,6901996 -2,963 5,545 2,760 36,970 -0,333

InterviewedFirms

1995 1,783 4,670 2,145 35,720 -7,0101998 2,720 7,935 7,360 32,705 4,8481997 -2,721 8,725 7,407 29,907 3,4751996 -4,375 7,396 6,440 25,651 1,026

Listed firms

1995 8,820 7,535 7,181 26,086 6,559

1998 0,115 3,526 1,146 25,907 -1,5401997 -1,518 4,347 1,890 26,332 -2,5801996 -3,031 4,089 1,167 29,491 -2,620

“Free Market”Firms

1995 -0,649 3,364 0,746 27,585 -2,730

1998 1,085 4,518 2,817 26,428 -0,5441997 -1,773 5,240 3,115 27,135 -0,5351996 -3,350 4,788 2,665 29,088 -1,180

Traded Firms

1995 0,971 3,780 1,594 27,585 -0,8851998 0,257 3,508 1,345 34,914 -2,3401997 -0,943 3,524 1,094 34,344 -2,2201996 -2,463 3,277 0,476 34,289 -3,020

Privatized Firms

1995 2,375 2,690 0,320 32,798 -1,600

Source: Financial statement data, Agency of Payments, 1994-1998.

Table 5: The Importance of Different Investment Criteria in Analyzed SlovenianFirms (1 – not important; 5 - the most impotrant)

INVESTMENT CRITERIA AVERAGE IMPORTANCE

Payback period 3,7Internal rate of return 3,5Net present value 3,3Profitability index 2,9Accounting based criteria 2,2

Source: “The Questionaire for Chief Financial Officer”, ibid.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 20/21

19

Table 6: Cross-Sectional Regression Analysis Of Financial Statement Data ConcerningInvestment Decisions for all Samples of Slovenian Firms for (1998)

Independent Variables ControlVariable Post-Keynesian

Theory

Theory of Employee

- Governed FirmDependent

Variable

Sample

Fixed Assets

per WorkerEquity per Worker Equity to Assets

R 2

Adj.

Interviewed Firms ** 0,00069900 ** -0,00069490 * 0,058

Listed Firms 0,00007305 -0,00006643 0,05

Free market firms 0,00000914 -0,00000769 -0,018

Traded Firms 0,00000782 -0,00000561 -0,013

Net

investment to

net income

Privatized Firms 0,00013020 -0,00013430 -0,001

Interviewed Firms * 0,00001202 -0,00001187 0,019

Listed Firms -0,00000039 0,00000066 0,041

Free market firms *** 0,00000116 *** -0,00000123 *** 0 ,079

Traded Firms ** 0,00000109 ** -0,00000107 * 0,024

Fixed Assets

Growth

Privatized Firms -0,00000019 0,00000109 -0,002

Interviewed Firms * -0 ,21100000 * 0,047

Listed Firms ** -0,33700000 **- 0,058

Free market firms 0,14000000 0,031

Traded Firms 0,01857000 -0,007

Fixed Assets

Growth

Privatized Firms 0,00207400 0,000

Notes: * - significant at 10%; ** - significant at 5%; *** - significant at 1%.

Table 7: The Attractivness of Different Sources of Financing in Analyzed SlovenianFirms (1 – not important; 5 - most impotrant)

SOURCES OF FINANCING AVERAGE IMPORTANCE

Internal equity capital 3,5

Long term bank loan 2,5External equity capital 2,2

Convertible debt 1,5Converible preferred shares 1,1Prefered shares 1,0

Source: “The Questionaire for Chief Financial Officer”, ibid.

8/3/2019 When Maximizing

http://slidepdf.com/reader/full/when-maximizing 21/21

Table 8: Cross-Sectional Regression Analysis Of Financial Statement Data Concerning CapitalStructure Decisions for all Samples of Slovenian Firms for the Year 1998

Independent VariablesControlVariable Neoclassical Theory Post-Keynesian Theory

DependentVariable Sample Fixed Assets

per Worker

Return

on Assets

FixedAssets to

Assets

Equity per

Worker

NetInvestment

to Net

Income

R 2

Adj.

Interviewed Firms -0,557 ** -0,392 ** 0 ,117

Listed Firms -0,346 *** -0,718 *** 0,408

Free market firms *** -0,735 *** -0,393 *** 0,194

Traded Firms *** -0,507 *** -0,442 *** 0,199

Debt to

Assets

Privatized Firms *** 30,767 *** -5,848 *** 0,103

Interviewed Firms *** 0,00003254 ***-0,00003488 *** 0,408

Listed Firms 0,00000063 -0,00000070 -0,064

Free market firms * 0,00000045 **-0,00000060 * 0,035

Traded Firms 0,00000042 *-0,00000055 * 0,024

Debt to

Assets

Privatized Firms *** 0,00000260 ***-0,00000298 *** 0,072

Interviewed Firms ** 0,00917400 ** 0,096

Listed Firms -0,00274700 -0,034

Free market firms -0,00050700 -0,007

Traded Firms -0,00046870 -0,006

Debt to

Assets

Privatized Firms * 0 ,00000735 -0,001

Legend: * - significant at 10%; ** - significant at 5%; *** - significant at 1%.