wholesale banking - nordea abg investor... · well diversified income and lending mix operating ......

TRANSCRIPT

1

Wholesale Banking

Martin Persson, Head of Wholesale Banking

Stockholm 2017-11-13

Wholesale Banking contribution to group

2

OPERATING INCOME OPERATING PROFIT ECONOMIC CAPITAL FTEs

Nordea Group Wholesale Banking

Key figures – YTD 17 (Q1-Q3)

22% 21% 30% 12%

Simple and flat business structure

3

Income

€ 1.6bn

Key figures – YTD 17 (Q1-Q3)

FTE

~4000

C/I

44%

RoCaR

8%

Governance

Wholesale

Banking

Russia COO C&IB* Markets

*Includes Shipping oil & offshore

Unique strategic positioning

4

Strategic position

Local competition

International

competition

Customer dimension:

Intensity

(Local presence and customer closeness)

Pro

duct dim

ensio

n:

Rele

van

ce

(Siz

e a

nd s

pan o

f c

om

pete

nces)

Market leader

Strong corporate client momentum in Sweden

5

6

Well diversified income and lending mix

Operating income split YTD - 17 (Q1-Q3) Lending per industry - 17 Q3

*Operates on a global basis

**Include holding companies

SE

NO

FI DK

FIG

SOO

Russia 21%

13%

13% 17%

14%

14%

8%

*

*

SOO

Real Estate

Institutional Industrial

Retail

Utilities

Energy

Material

Consumer

Transport

Other 18%

18%

14% 10%

8%

4%

4%

3%

3%

2%

17%

**

Transition from bank to capital markets financing

7

47% 42% 43% 46%

42% 37% 37%

32% 38% 36% 28% 34% 35% 35%

21% 19% 22% 26% 24% 28% 28%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 2017 Annualised

Net Interest Income Net Fair Value Net Commision Income Economic Capital

Income Economic capital

Active business selection and de-risking of loan portfolio

8

50

60

70

80

90

100

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17

WB SOO Russia WB excluding Russia & SOO

Net interest income (Q1 2016 rebased to 100)

102

52

88

86

Strategic focus in growing ancillary income

9

Debt Capital Markets deal value, €bn

Equity Capital Markets deal value,€bn

Mergers & Acquisitions deal value, €bn

+28%

Nordic Equity Prospera ranking

*Annualised

**Growth is calculated as Compounded Annual Growth Rate between 2011-2016

+89%

0

10

20

30

40

50

60

70

2011 2012 2013 2014 2015 2016 2017*

Th

ou

san

ds

0

2

4

6

8

10

12

2011 2012 2013 2014 2015 2016 2017*

Th

ou

san

ds

0

2

4

6

8

10

12

2011 2012 2013 2014 2015 2016 2017*

Th

ou

sa

nd

s

+9%**

2011 2012 2013 2014 2015 2016

1

5

10

15

**

**

Leading Nordic franchise in debt capital markets

10

Shipping oil and offshore

11

Loan Losses, % Average 0.43%***

0.19 -0.1 0.03 -0.1 -0.1 -0.01 0.00 0.08 0.75 0.33 1 1.85 0.83 -0.32 0.05 1.22 1.27

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2017

YTD

RoCaR development*

*Assuming Economic Capital in % of lending in line with 2011-2016 average

** YTD = Q1-Q3- 2017

***Average calculated between 2001-2016

0%

5%

10%

15%

20%

25%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD**

Average***

13.2%

Nordea Markets - resilient income generation despite record low volatility

12 *Stability fund fees and IAS adjustment have been excluded.

0

5

10

15

20

25

30

35

40

45

jan feb mar apr maj jun jul aug sep

2017 2016 2015 2014

VIX index YTD 17 Markets income €bn

1.2

1.5 1.4 1.4

2014 2015 2016 2017Annualised

Wholesale Banking transformation

13

Distribution/

Channels/

Service model

Credit proc. &

Prod.

IT &

Operations

Key support

functions

Business strategy unchanged, #1 relationship bank in the Nordics

• Streamlined customer service

• Further explore digital channels and services

Re-positioning of Markets

• Implement new cross-Nordic operating model for Markets business with

stronger customer ownership and clearly defined service and value

offerings

• Cross-sell and capital markets financing

Operational excellence,

• Simplified IT infrastructure, robotics and near-shoring to Poland

Strengthened capital governance and risk management

• Increase capital velocity

• Consolidate SOO franchise and normalised loan losses

Key transformation initiatives Cost efficiencies and quality gains

Where do the cost efficiencies come from?

Medium

Operational excellence,

• Simplified IT infrastructure, robotics and near-shoring to

Poland

Improved customer satisfaction

• Client coverage: A more coordinated, dedicated and holistic

approach to customer interaction

• Research: High uniform quality, easier and more transparent

to deal with and utilise pan-Nordic capacity

High High

Medium

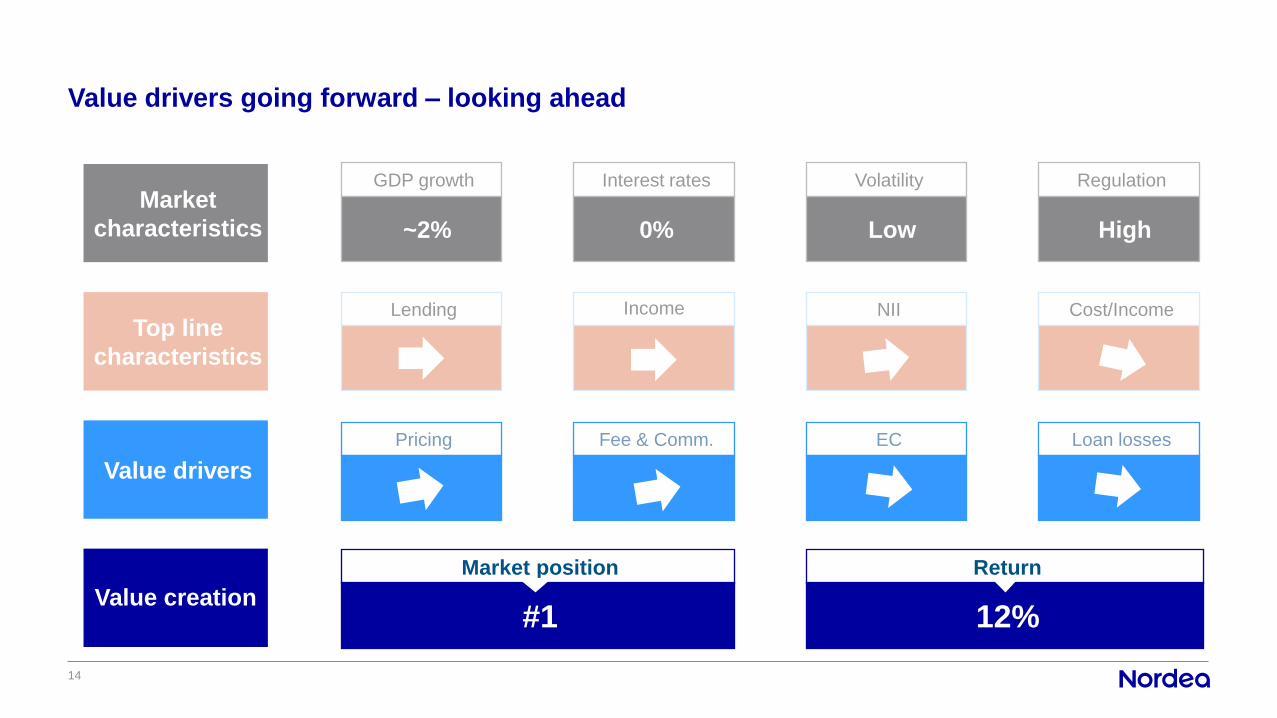

Value drivers going forward – looking ahead

14

Top line

characteristics

Value drivers

Value creation

Market

characteristics

GDP growth

~2%

Interest rates

0%

Volatility

Low

Regulation

High

Lending Income NII

Pricing Fee & Comm. EC Loan losses

Market position

#1

Return

12%

Cost/Income

15

Thank you!