why invest in dutch npl's - presentation debt sale event london

TRANSCRIPT

Why invest in Dutch portfolios and NPLs?

Casper Sonnega – Head of Collections Business Unit Benelux

CBU Benelux | London | GDI Forum 2016 | 09.02.2016 |

2

Disclaimer

The views, interpretations, analyses, data, information and opinions expressed in and during this presentation are solely those of the author (in his private capacity) and do not reflect the official policy, opinion or position of Santander Group, Santander Consumer Finance or any of it’s affiliates nor is it endorsed or approved by them.

The information in this presentation is based on carefully selected sources by the author and believed to be reliable. However the author does not provide any guaranties to its accuracy or completeness. This presentation does not constitute legal, expert or professional advice. Any opinions herein reflect the authors judgement at the date hereof and can be subject to change or misinterpretations. This presentation is given before an audience of professionals, deemed competent to evaluate the significance and limitations of its content.

Any data or information provided during this presentation are provided for general information purposes only and cannot substitute the obtaining of independent and or expert advice. Investors should obtain professional advice before making any investment decisions.

The author denies any and all responsibility for application of the stated information, analyses or opinions and or the accuracy of the content or sources presented and shall under no circumstance be liable for any loss or damage arising from reliance on or use of any content or principles contained in this presentation. Unless otherwise indicated, all materials in this presentation are copyrighted to the author. All rights reserved. Reproduction, modification or retransmission in any form is strictly prohibited without the prior written consent of the author.

Viewing, participating in or using this presentation represents your agreement with this disclaimer and the terms stated above.

3

1. Introducing The Netherlands

2. Doing business with the Dutch

3. Investing and collecting in the Dutch market

Macro economics

Overview of the buyer landscape

Legal situation and workout of debt / collections

Take-aways

4. Questions

Agenda

4

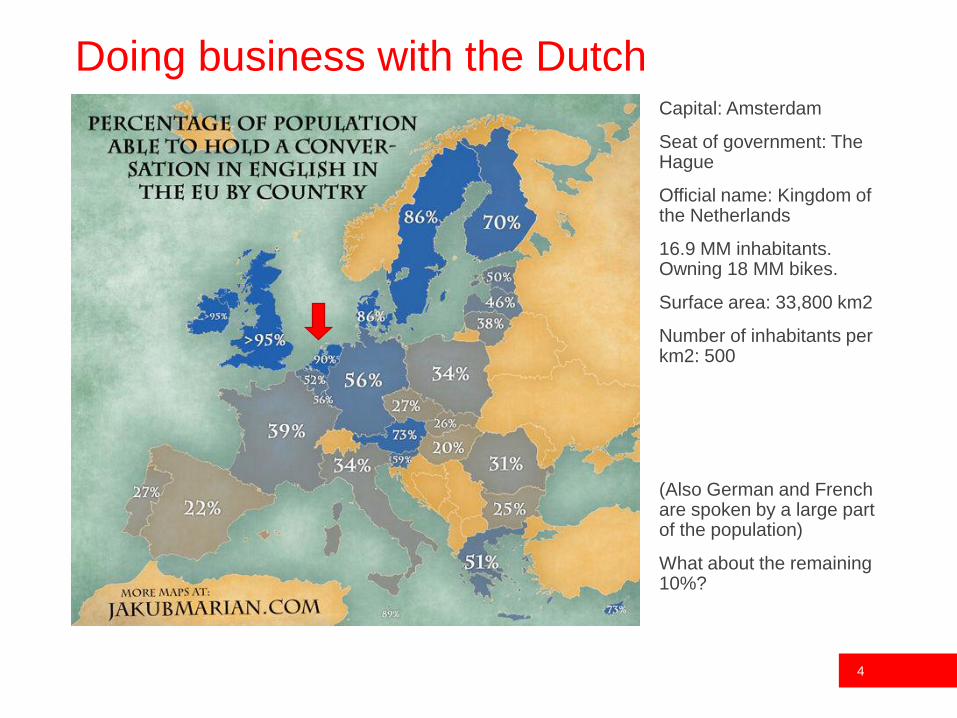

Doing business with the DutchCapital: Amsterdam

Seat of government: The Hague

Official name: Kingdom of the Netherlands

16.9 MM inhabitants. Owning 18 MM bikes.

Surface area: 33,800 km2

Number of inhabitants per km2: 500

(Also German and French are spoken by a large part of the population)

What about the remaining 10%?

5

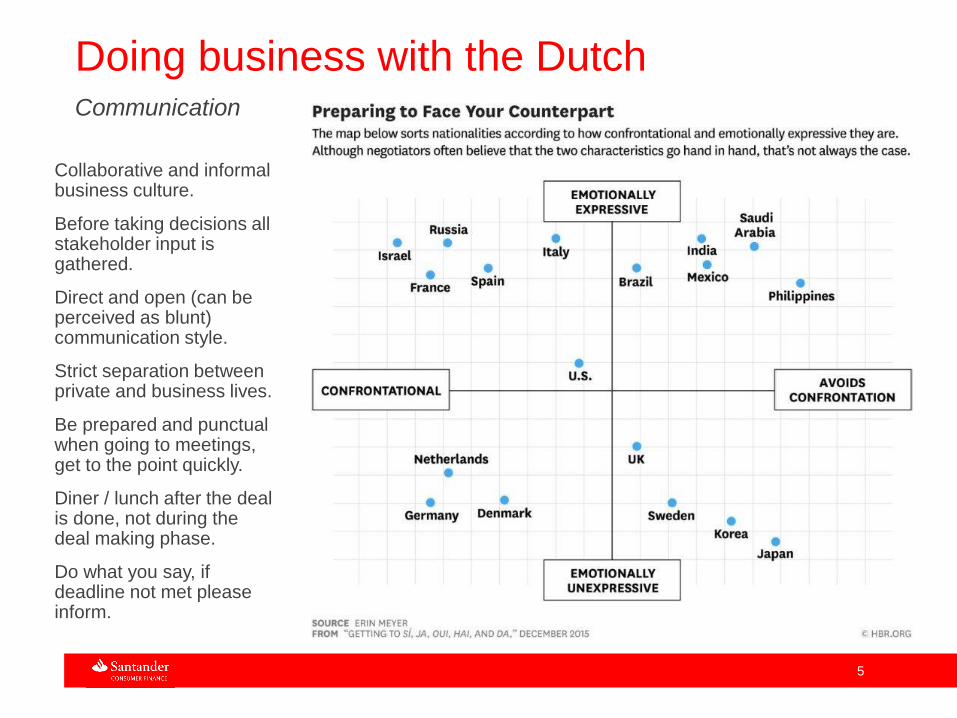

Doing business with the DutchCommunication

Collaborative and informal business culture.

Before taking decisions all stakeholder input is gathered.

Direct and open (can be perceived as blunt) communication style.

Strict separation between private and business lives.

Be prepared and punctual when going to meetings, get to the point quickly.

Diner / lunch after the deal is done, not during the deal making phase.

Do what you say, if deadline not met please inform.

Investing and collectingin the Dutch market

7

Investing / collecting in the Dutch marketMacro economic situation

• Good infrastructure (roads and airport) and digitalization. Trading nation located centrally within the EU. Well educated workforce.

• Strong international focus (7th

largest investor other countries / 11th in receiving investments | 1tn – 700bn) , well established practice of doing business with multinationals and working with expats. Supported by the government and tax treaties.

• Ranked 5th on the worldwide innovation index / ranked 3rd in terms of GDP per hour (productivity index).

• GDP 663 MM

Source of table: http://ec.europa.eu/economy_finance/eu/countries/netherlands_en.htmIn

formal observations, market data, personal opinion / report pwc-doing-business-in-the-netherlands-2015.pdf

8

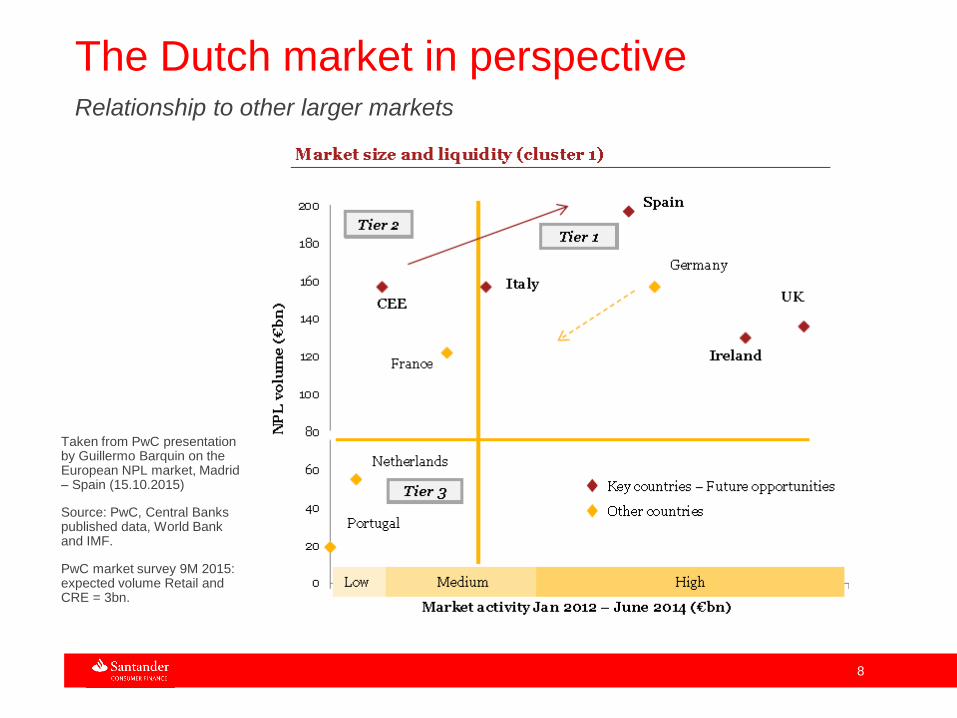

The Dutch market in perspectiveRelationship to other larger markets

Taken from PwC presentation by Guillermo Barquin on the European NPL market, Madrid – Spain (15.10.2015)

Source: PwC, Central Banks published data, World Bank and IMF.

PwC market survey 9M 2015: expected volume Retail and CRE = 3bn.

9

The Dutch market in perspectiveParties active in the (NPL, but also performing) market

(CRE, real estate, morgages, etc. excluded)

Locals

Source: personal observations, informal information

10

Legal Legal considerations when purchasing NPL's in The Netherlands

• No (late/arrears) fees allowed under Dutch law (WCK – consumer finance law) Legislator assuming all cost paid out of regular interests and delay interests.

• (delay) Interest to be charged after termination and no higher then agreed interest in terminated contract.

• Laws governing the charging of late fees as stipulated in the WIK (law on collection fees) do not apply to consumer finance.

• Management of receivables requires a license from the regulator (AFM - Authority Financial Markets). Legal ownership of CK receivables can be obtained without a license, however no management (collect, receive payments, etc.) can be done.

• To obtain an AFM license a membership of the Dutch credit bureau (BKR) is required.

• The buyer or investor can rely on a servicer who has these licenses.

• A movement is visible in the market of more servicers / buyers applying for a license.

Source: personal opinions, public information

11

• Limitation period after termination between 2 and 5 years, depending on type of consumer finance.

• Limitation period of a verdict is 20 years (fixed on the amount as stipulated in the verdict), any delay interests after the verdict have a limitation period of 5 years).

• Limitation periods can be extended by sending the consumer a letter (please take receiving theory risk into consideration) or summons by a bailiff (no or very limited risk). Extension for no longer then 5 years.

• Efficient court system, in majority of cases verdict will be obtained within 3 months. Estimated 70-80% of legal collection verdicts granted without debtor actively participating in proceedings.

• For court cases concerning consumer finance no lawyer representation is needed up to 40k.

• Most but not all legal collection cost will have to be paid by the debtor if convicted.

Legal Legal considerations when purchasing NPL's in The Netherlands

Source: personal opinions, public information

12

Workout / collections Collection agencies (DCA's)

• Debt collection agencies are governed by a limited number of specific collection laws. The larger DCA’s are a member of the Dutch association of collection companies (NVI) and adhere to their rules and regulations. There are between 550 and 600 DCA’s registered in the Netherlands, however the larger NVI members (#30) cover some 70% of the market.

• There have been bankruptcies / restructuring / FTE reductions within the sector. A further shakeout and / or consolidation is expected.

• Specialized (medium sized) DCA’s seem to be performing better then (large) all round DCA’s.

• Increased competition and pressor on prices / margin can be observed when tendering DCA but also bailiff services.

• In recent years the cost of legal collections (mainly court fees) have increased significantly. Also, the rules have changed regarding the possibilities for bailiffs pre-financing the out of pocket cost of legal collections and NCNP constructions. Reducing the number of legal collection cases (-30%). After the implementation of WIK in 2012 a trend is visible of companies using DCA’s less for amicable collections and moving those activities in-house, viewing collections as a profit centre.

Source: public sources, news articles, court studies.

13

Workout / collectionsCollection agencies (DCA's)

• Bailiffs are appointed by the Crown, but are also businesses that need to generate a profit. Out of pocket + commission based on success is allowed. The top 5 bailiff companies cover some 50% of the market volume.

• They are governed by specific sections of the law, their trade organization (KBvG) and the bureau of financial oversight (BFT). Fee’s charged to consumers are regulated by law (Btag).

• Bailiffs can represent the creditor in court, vast majority of legal collections cases are managed by Bailiffs. Usage of law firms for legal collections (BtC) is very limited.

• Bailiffs are allowed to offer amicable collection services, thereby competing with DCA’s. Estimated that some 40% of bailiff turnover is generated by amicable collection activities.

• Individual bailiffs (some 950) are a member of the Royal Professional Organization of Judicial Officers (KBvG).

• Fragmented bailiff market with a lot of small and medium sized companies. Number of companies in the Netherlands between 150-200, 400MM+ turnover. There have been bankruptcies / restructuring / FTE reductions within the sector. A further shakeout and / or consolidation is expected.

• Digitalization (government driven program KEI) in different stages of implementation.

Source: public information, trade organizations, research by ING, ABN AMRO, other public sources.

14

Take-away’sSome conclusions

• You can expect and ask for post deal service and aftercare.• Information, digital files and financial data well developed and available. • Relatively smaller deals, spot sales and forward flow are well established. • Interest of the regulator (AFM) in debt sales increasing, market adjusting. Not

comparable however to for example the UK. • Know the legal and compliance requirements. Imbed customer centricity* into your

processes and offer. • Straight forward NPL’s, specials usually already internally managed. • Creditor friendly environment. Sufficient options for amicable and legal collections.

Cost of legal collections has increased over time.• Competitive bailiff and DCA market, strong negotiation position. • Collections friendly market. Strong legal creditor position. • Well developed DCA / bailiff market, sensitive to competition, eager. • Seller side developing, market appetite for opportunities. Activity increasing, but

relative to other countries still low. • Sufficient benchmark and deal experience available at seller, legal, servicer and

buyer side.

* Translation of Klant Belang Centraal

Source: personal opinions / informal information.

15

Questions

Our purpose is to help people and

businesses prosper.

Our culture is based on the belief that

everything we do should be

Thank you

Thank you

17

AppendixYour speaker details and contact information

Casper SonnegaDirector Collections & Recovery Benelux

Contact details: Mobile : +31(0)6 – 10 90 72 23E-mail : [email protected] Website : www.santander.nl

www.linkedin.com/in/caspersonnega