why invest!!

TRANSCRIPT

What’s your future in RETIREMENT?

Retirement Concerns

- Impact of Inflation - means erosion of purchasing power, the money value has shrunk, you can buy less for the same amount of money.

- Longer Life Expectancy - Means longer retirement period. How much would you need on a monthly basis for at least 20 years after the onset of retirement.

- Rising Medical Cost – you can be young without money but you can’t be old without money

ALL these factors lead to a requirement for a HIGHER RETIREMENT FUND

IS it going to be a NEW LEASE OF LIFE, no longer bound by the constraints of work and freedom to pursue new goals and enjoy a more leisurely life OR A FEAR OF NOT HAVING ENOUGH MONEY.

TRY AS ONE MAY, TIME CANNOT BE STOPPED OR EVEN DELAYED

WHAT IS THE AMOUNT YOU WOULD REQUIRE ON THE ONSET OF YOUR RETIREMENT?

Say the inflation rate is 4%

Projected inflation rate 4% 4% 4%

Monthly Expenditure 2,000 5,000 10,000

Number of retirement years 20 20 20

Your Required Retirement fund (RM) 735,994 1,839,986 3,679,972

So depending on your monthly requirement, the retirement fund required for 20 years after the onset of retirement is as follows:

At RM2,000 a month expenditure, you would require RM 735,994.

At RM5,000 a month expenditure, you would require RM 1,839,986.

At RM10,000 a month expenditure, you would require RM 3,679,972.

Say you live for another 20 years after the onset of retirement and continue to maintain your lifestyle

WILL YOU OUTLIVE YOUR RETIREMENT FUND OR WILL YOUR RETIREMENT FUND OUTLIVE YOU?

YES, YOU NEED TO MAKE YOUR MONEY WORK HARD TOO!!

1. Is your EPF savings sufficient to last out your retirement period?

2. Will you have sufficient to continue your existing lifestyle?

3. What dependable sources of income will you have when you retire?

4. What are your plans in saving towards your retirement?

5. Do you have investments apart from your EPF?

6. Are your investments diversified?

QUESTIONS

IMPACT OF INFLATION ON REAL MONEY WORTH

At inflation 4% (say)

Value now 1,000.00

In these many

yrs

RM1k will be

worth

Also it will take this

much money to buy

what RM1k will

buy today

5 821.93 1,217

10 675.56 1,480

15 555.26 1,801

20 456.39 2,191

Value now 100,000 In these many

yrs

5 82,193

10 67,556

15 55,526

20 45,639

SO HOW DO WE BEAT INFLATION?

You have to make your money work hard to grow at a rate which is higher than the rate of inflation.

So say you want to know the real worth of your money in years to come by just

leaving it alone and letting inflation erode its value.(assuming an inflation of 4%)

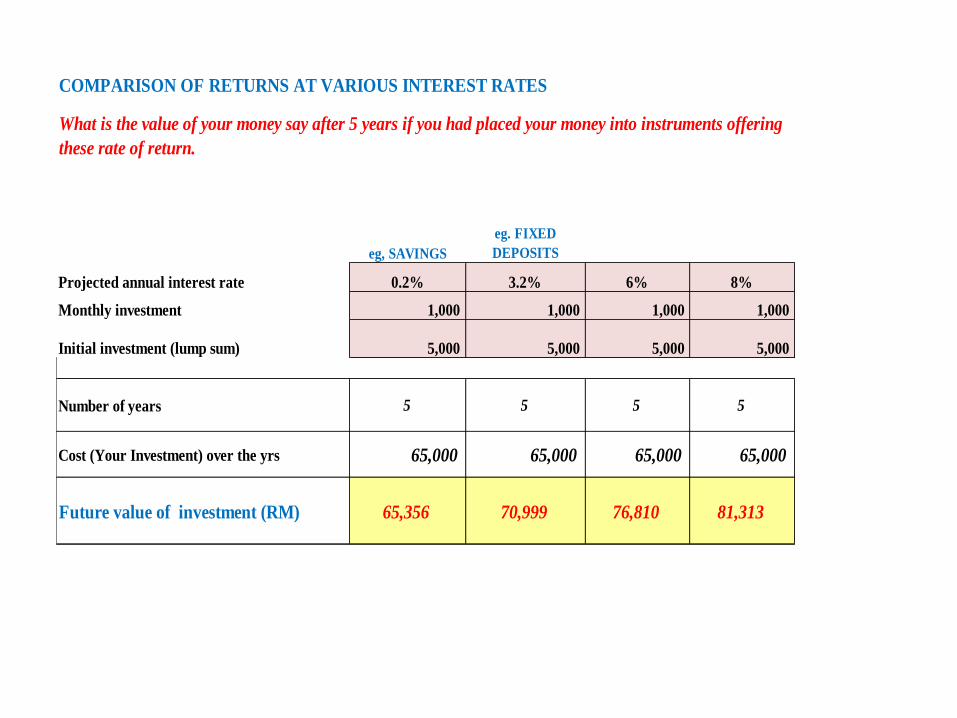

COMPARISON OF RETURNS AT VARIOUS INTEREST RATES

eg, SAVINGS

eg. FIXED

DEPOSITS

Projected annual interest rate 0.2% 3.2% 6% 8%

Monthly investment 1,000 1,000 1,000 1,000

Initial investment (lump sum) 5,000 5,000 5,000 5,000

Number of years 5 5 5 5

Cost (Your Investment) over the yrs 65,000 65,000 65,000 65,000

Future value of investment (RM) 65,356 70,999 76,810 81,313

What is the value of your money say after 5 years if you had placed your money into instruments offering

these rate of return.

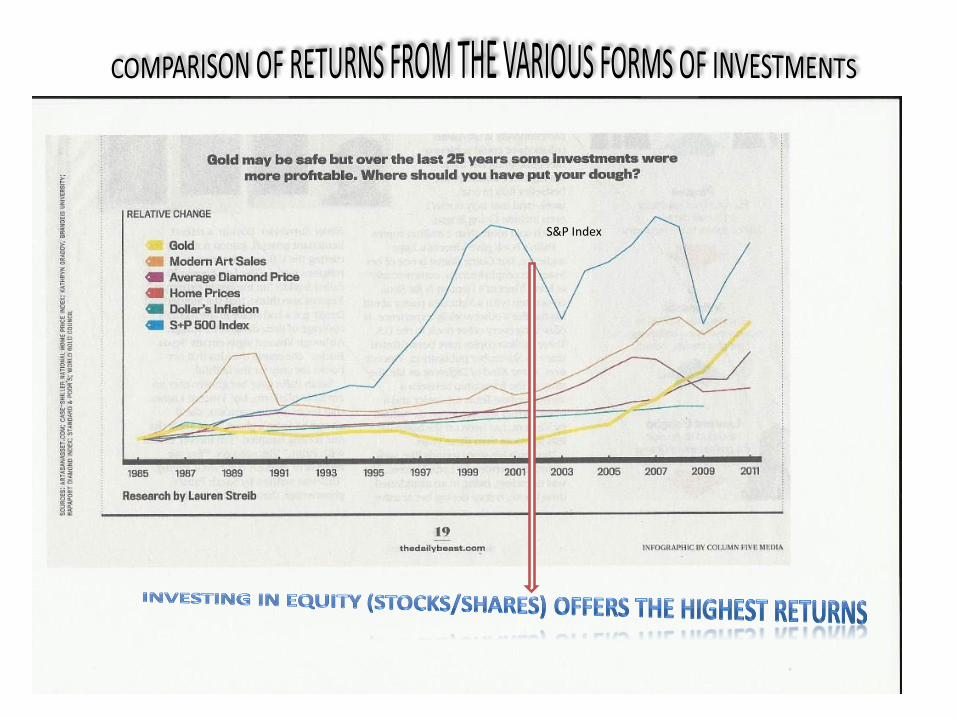

Investment Channel

S&P Index

1. Borrow To Invest.

2. Invest All Your Money.

3. Invest Money You Need Soon.

4. Get Emotional And Panic.

5. Do Keep Investing And Stay Invested.

6. Do Diversify.

7. Do Take Professional Advice.

8. Do Give Your Investments Time To Grow.

AFTER RETIREMENT ITS PURELY CONSUMPTION. ARE YOU READY FOR IT??

In October 2008, when the world was reeling from the global financial crisis, the sage of Omaha told The New York Times: “Over the long term the stock market news will be good. In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497”

To Warren Buffet investing is about foregoing consumption now in order to have the ability to consume more at a later date.

SO WHEN WE INVEST, OUR AIM IS TO BUY AN ASSET WHOSE PRICE WILL GROW FASTER THAN INFLATION OVER TIME.

THE ONE ASSET CLASS WHICH HAS DEMONSTRATED ITS ABILITY TO DO THAT OVER THE LONG TERM IS EQUITIES

1997 - Asian Economic Crisis2000 - Dotcom bubble burst2008 - Global Financial Crisis2011 - European Sovereign Debt Crisis

Rule 4. Get Emotional And Panic.

Jun-06 914.69

Mar-07 1246.87

Jun-07 1354.38

Dec-07 1445.03

Mar-08 1247.52

Jun-08 1186.57

Sep-08 1018.68

Dec-08 876.75

Mar-09 872.55

Jun-09 1075.24

Sep-09 1202.08

Dec-09 1272.78

Mar-10 1320.57

Jun-10 1314.02

Sep-10 1463.50

Dec-10 1518.91

Mar-11 1545.13

Jun-11 1579.07

Sep-11 1387.13

Dec-11 1530.73

Mar-12 1536.33

Jun-12 1599.15

Sep-12 1636.66

Dec-12 1688.95

Mar-13 1671.63

Jun-13 1773.54

Sep-13 1768.62

Dec-13 1866.96

Mar-14 1849.21

Jun-14 1882.71

Sep-14 1846.31

700.00750.00800.00850.00900.00950.00

1,000.001,050.001,100.001,150.001,200.001,250.001,300.001,350.001,400.001,450.001,500.001,550.001,600.001,650.001,700.001,750.001,800.001,850.001,900.001,950.00

Jun-

06

Sep

-06

Dec

-06

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

I

N

D

E

X

Performance of FTSE Bursa Malaysia KLCI

6yrs after 2008

T H E R E S U LT S

Investing in Equities - Medium to Long Term (Via – Direct Investing in stock market & unit trust)

Invest in 1,000 shares atRM6.55 – Total outlay RM6,550.

In 2010, the shareholder would have 1,043 shares

worth

(Based on closing price of RM13.02)

2005End 2010

Total Gross dividends received for 5 yrs is RM3,420.

Annual rate of return on investment of 24.3% for each of the 5 yrs.

In 2013, the shareholder would have 1,043 shares

worth (Based

on closing price of RM19.40)

End 2013

Total Gross dividends received for 5 yrs is RM2,735.

Annual rate of return on investment of 21.0 % for each of the 5 yrs.

2008

Invest in 1,000 shares atRM8.85 – Total outlay RM8,850.

Medium Term Returns – 5 yrs

Rule 8: Do Give Your Investments Time To Grow.

Source :Public Bank Berhad Annual Report 2013

Invest in 1,000 shares and assuming shareholder had subscribed for all rights issues and not sold any shares, total investment of

In 2010, the shareholder would have

worth (Based on closing price of RM13.02)

1967 ( date of listing) End 2010

Total Gross dividends received in the 43 yrs

Annual rate of return on investment of 19.7% for each of the 43 yrs.

In 2013, the shareholder would have 135,398 shares

worth (Based on closing price of RM19.40)

End 2013

Total Gross dividends received in the 46 years

.

Annual rate of return on investment of 19.6% for each of the 46 yrs.

Long Term Returns

Source: Public Bank Annual Report 2013

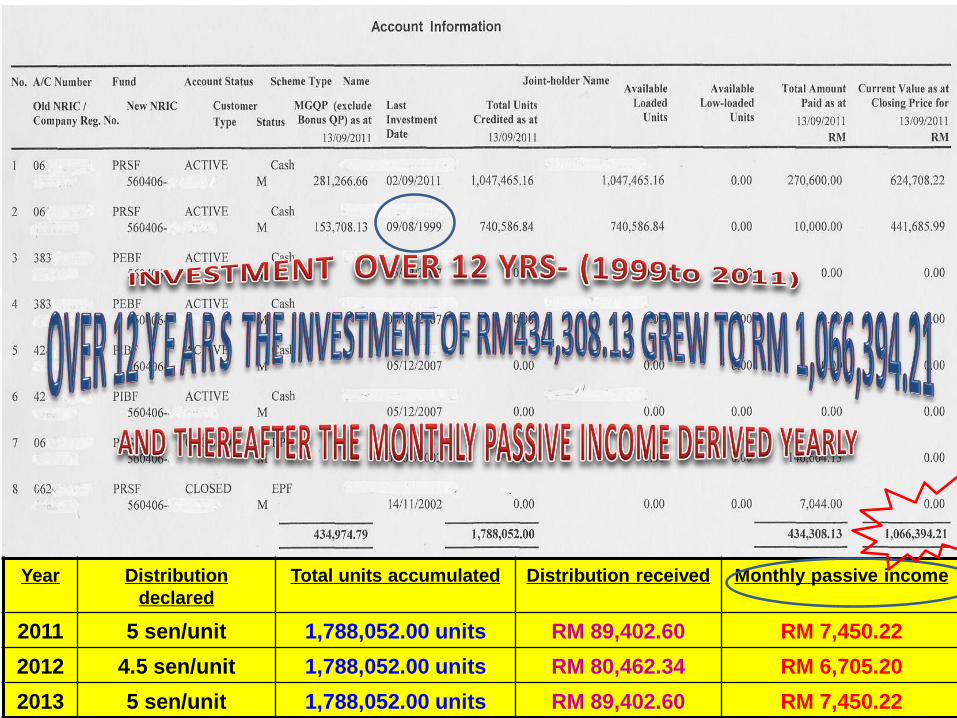

Year Distribution

declared

Total units accumulated Distribution received Monthly passive income

2011 5 sen/unit 1,788,052.00 units RM 89,402.60 RM 7,450.22

2012 4.5 sen/unit 1,788,052.00 units RM 80,462.34 RM 6,705.20

2013 5 sen/unit 1,788,052.00 units RM 89,402.60 RM 7,450.22

The secret to ensure that your savings will grow faster than inflation and that you will increase your odds of meeting your financial goals is:

ONE – consistently invest in a diversified basket of stocks that represents the real economy over the long term;

TWO – Don’t bail out at the worst of times. All the more, if you can afford it, put in more money at the most depressed of market conditions.

Rule 6. Do Diversify.

Rule 4. Get Emotional And Panic.

Rule 5. Do Keep Investing And Stay Invested.