wi cobra ref guide updated 060211 - billing services€¦ · employer reference guide cobra...

TRANSCRIPT

COBRA Administration Employer Reference Guide

M47409-B 6/11 © 2011 United HealthCare Services, Inc.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

T A B L E O F C O N T E N T S

I n t r o d u c t i o n

P r o c e s s O v e r v i e w

T i m e l i n e

A d m i n i s t r a t i v e S e r v i c e s

W h o M u s t C o m p l y

T i m e R e q u i r e m e n t s a n d P a y m e n t t r a c k i n g

P e n a l t i e s

R e p o r t s

O n l i n e A c c e s s

E m p l o y e r R e s p o n s i b i l i t i e s

N o t i f i c a t i o n s

C o m p l i a n c e

T i m e T a b l e s

A p p e n d i x A F r e q u e n t l y A s k e d Q u e s t i o n s

A p p e n d i x B R e n e w a l P r o c e s s O v e r v i e w

A p p e n d i x C G l o s s a r y

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

I N T R O D U C T I O N Congratulations on your decision to take advantage of the COBRA administration services available from UnitedHealthcare. UnitedHealthcare is furnishing this guide to provide your organization with detailed, in-depth reference material to assist you with the compliance of the many facets of COBRA administration. We are confident you will find this manual a useful tool in working with us on your COBRA Administration. We also offer a website demo to help walk you through some of the most common COBRA transactions at www.uhcservices.com or www.welcometouhcservices.com

UnitedHealthcare P.O. Box 1470

Brookfield, WI 53008 www.uhcservices.com

Telephone: (800) 318-5311 Business Hours: 7:00 a.m. to 6:00 p.m. (Central Time)

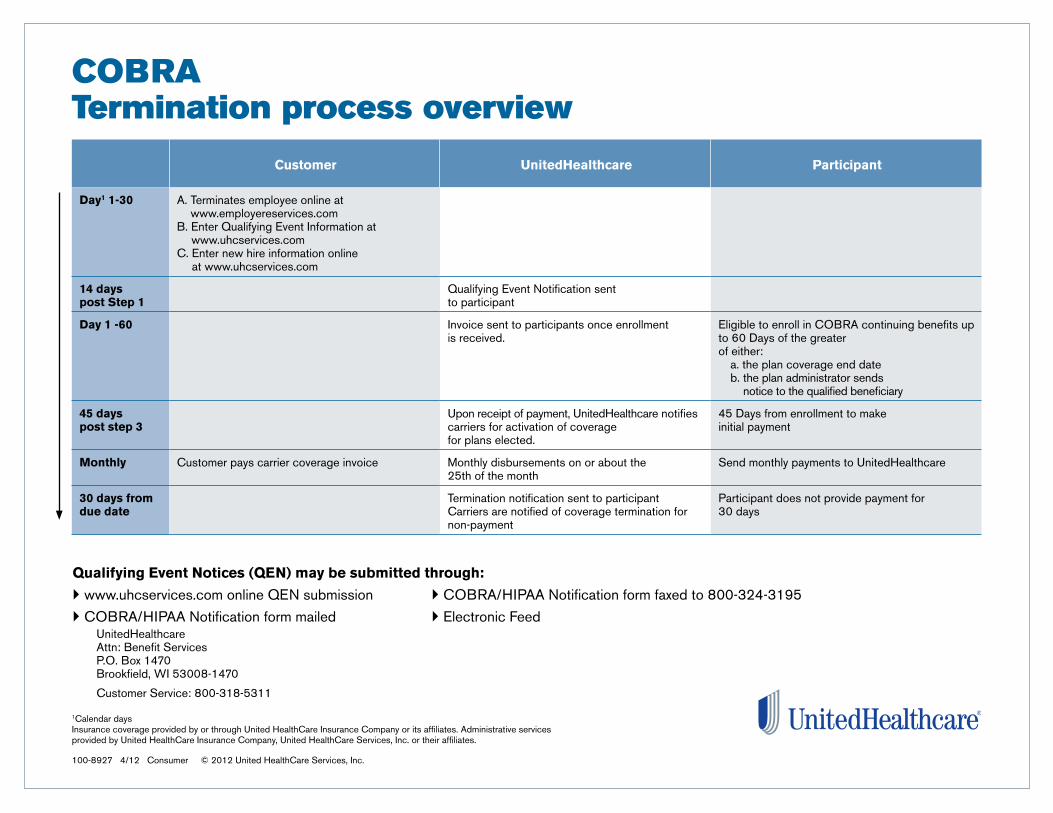

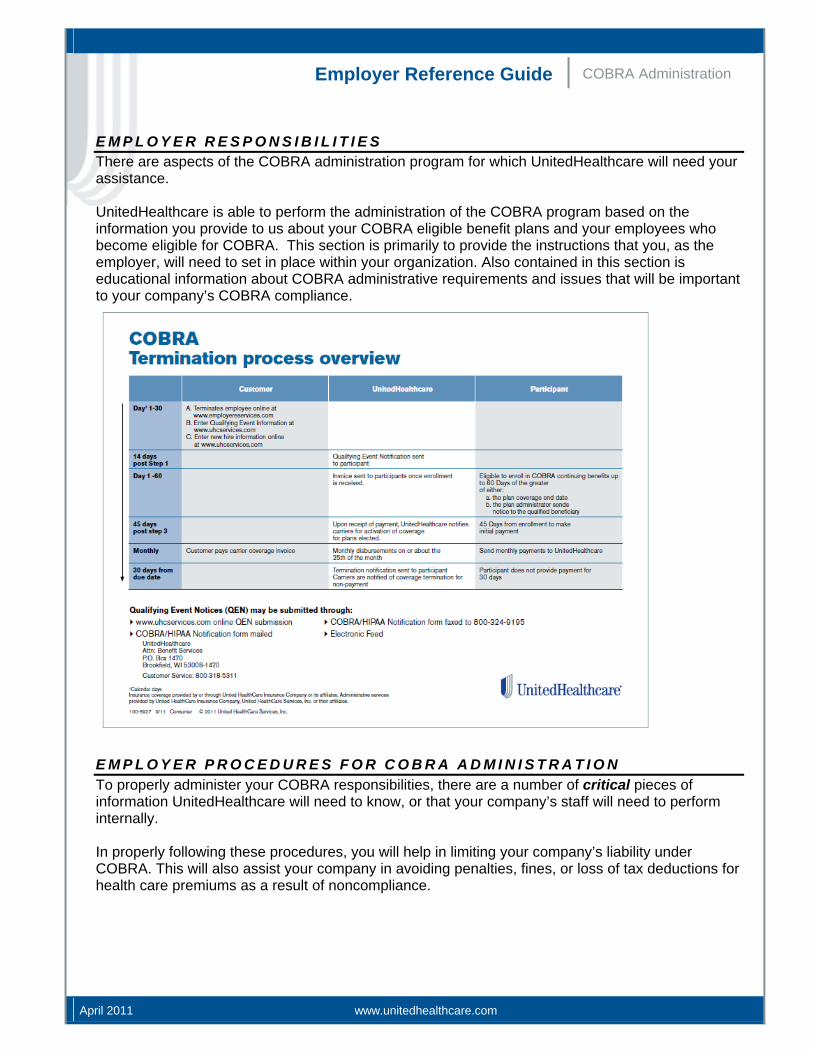

COBRA Termination process overview

Customer UnitedHealthcare Participant

Day1 1-30 A. Terminates employee online at www.employereservices.com

B. Enter Qualifying Event Information at www.uhcservices.com

C. Enter new hire information online at www.uhcservices.com

14 days post Step 1

Qualifying Event Notification sent to participant

Day 1 -60 Invoice sent to participants once enrollment is received.

Eligible to enroll in COBRA continuing benefits up to 60 Days of the greater of either:

a. the plan coverage end dateb. the plan administrator sends

notice to the qualified beneficiary

45 days post step 3

Upon receipt of payment, UnitedHealthcare notifies carriers for activation of coverage for plans elected.

45 Days from enrollment to make initial payment

Monthly Customer pays carrier coverage invoice Monthly disbursements on or about the 25th of the month

Send monthly payments to UnitedHealthcare

30 days from due date

Termination notification sent to participantCarriers are notified of coverage termination for non-payment

Participant does not provide payment for 30 days

Qualifying Event Notices (QEN) may be submitted through:

} www.uhcservices.com online QEN submission } COBRA/HIPAA Notification form faxed to 800-324-3195

} COBRA/HIPAA Notification form mailed } Electronic FeedUnitedHealthcareAttn: Benefit ServicesP.O. Box 1470Brookfield, WI 53008-1470

Customer Service: 800-318-5311

1Calendar daysInsurance coverage provided by or through United HealthCare Insurance Company or its affiliates. Administrative services provided by United HealthCare Insurance Company, United HealthCare Services, Inc. or their affiliates.

100-8927 4/12 Consumer © 2012 United HealthCare Services, Inc.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

C O B R A A D M I N I S T R A T I V E S E R V I C E S UnitedHealthcare COBRA administration services are listed for your convenience in this section. We are confident that we are able to provide one of the most comprehensive COBRA administration service programs available in the market today. Here is a breakout of the many responsibilities and tasks we perform for you as part of our COBRA administration and processing: Take over administration of current COBRA participants Ongoing U.S.P.S mailing of qualifying event notices with proof of mailing Expedient review and processing of COBRA elections Numerous written communications and reminders to participants and qualified beneficiaries

regarding their account status, including eligibility for COBRA disability extensions Monthly premium collection from participants, including notices of partial or late payments Optional monthly premium withdrawal from COBRA continuants checking or savings

account at no extra charge Delivery of a monthly Electronic Funds Transfer (EFT) to you for received COBRA premiums Toll-fee Customer Care Center support Online access for COBRA beneficiaries to review account status Employer reports available on the web 24 hours a day, 7 days per week Appropriate distribution of HIPAA certificates when COBRA coverage is discontinued or

expired Payment invoices sent to all participants affected by new benefit plans or premium renewal

rates Minimum seven year archival of data for ERISA compliance Technical assistance on questions about COBRA administration or compliance at no

additional cost Distribution of newsletters to advise you of any changes in the regulations that affect

COBRA Thorough management reports are provided as part of our COBRA administration services.

C O B R A M A D E E A S Y F R O M U N I T E D H E A L T H C A R E The Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) introduced a fair and equitable avenue to continue insurance for employees and dependents who no longer qualify under an employer-provided group benefit plan. COBRA represents a maze of compliance rules for you to understand and follow. Even with the best of intentions, COBRA laws not understood and/or properly implemented have the potential to cost your organization thousands, even hundreds of thousands, of dollars in penalties, fines, medical claims and liability suits W H O M U S T C O M P L Y If you offer a group health plan and had 20 or more employees on at least half of the business days in the prior calendar year, you must comply with COBRA. COBRA applies to group health, dental and vision plans as well as retiree health plans, medical flexible spending accounts, medical reimbursement plans, health reimbursement arrangements, and some employee assistance plans. Its rules and regulations have far-reaching implications.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Q U A L I F I E D B E N E F I C I A R I E S “Qualified beneficiaries” are individuals who have been on your group plan. They must be offered the opportunity to continue the same type of coverage as they had with their group plan when certain “qualifying events” occur. Examples of such events include employee terminations, long-term disability, divorce, dependents no longer meeting the plan’s eligibility requirements, etc.. T I M E R E Q U I R E M E N T S A N D P A Y M E N T T R A C K I N G The maximum required time period for COBRA coverage depends on the type of qualifying event - 18 months up to 36 months. COBRA notices must be provided to each beneficiary when coverage is first obtained, such as when newly hired. Another notice is required when a qualifying event occurs and benefit coverage is lost. It is essential COBRA payments are tracked to ensure claims are not paid if the COBRA premium has not been received on time, or paid incorrectly. P E N A L T I E S Failure to provide the required notices can leave you with an open-ended liability for each qualified beneficiary. The penalties are assigned by the court at its discretion and allow the court to award other relief as it deems necessary to correct the situation. This means that you may not only have to pay up to $110 a day for each violation for each beneficiary, but you can also be held liable for any unpaid claims and the value of future coverage. No matter how many different qualified plans, number of employees, number of carriers, or different rates an employer has, the administrative services provided by UnitedHealthcare are up to the task. UnitedHealthcare provides streamlined COBRA administration with the assurance of compliance and effective record-keeping. When a qualifying event occurs, an employer simply notifies UnitedHealthcare online and we do the rest. Efficient processing of administration services is one of our hallmarks. And we keep you informed every step of the way. I N T E R N E T E M P L O Y E R M A N A G E M E N T R E P O R T S Comprehensive employer reports are available online 24 hours a day, 7 days per week! You can download detailed reports at your convenience. The reports available include:

• Enrolled COBRA participants with payment status • Qualified beneficiaries notification status • COBRA coverage terminations

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

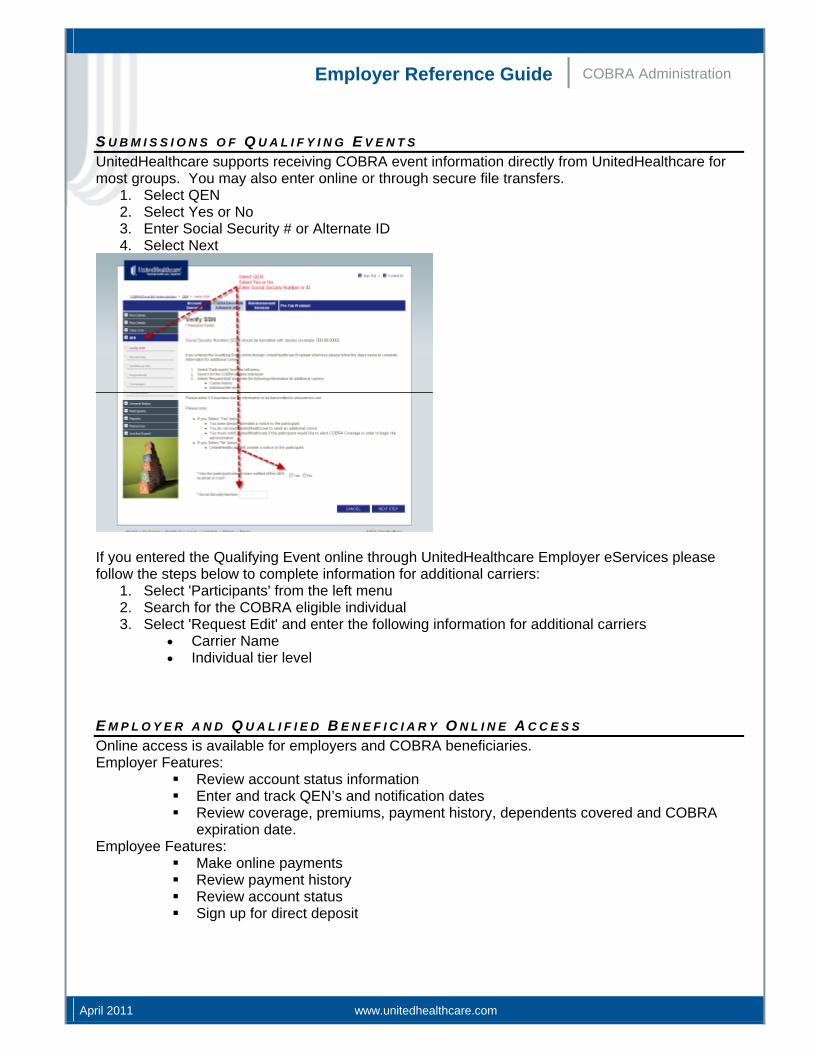

S U B M I S S I O N S O F Q U A L I F Y I N G E V E N T S UnitedHealthcare supports receiving COBRA event information directly from UnitedHealthcare for most groups. You may also enter online or through secure file transfers.

1. Select QEN 2. Select Yes or No 3. Enter Social Security # or Alternate ID 4. Select Next

If you entered the Qualifying Event online through UnitedHealthcare Employer eServices please follow the steps below to complete information for additional carriers:

1. Select 'Participants' from the left menu 2. Search for the COBRA eligible individual 3. Select 'Request Edit' and enter the following information for additional carriers

Carrier Name Individual tier level

E M P L O Y E R A N D Q U A L I F I E D B E N E F I C I A R Y O N L I N E A C C E S S Online access is available for employers and COBRA beneficiaries. Employer Features:

Review account status information Enter and track QEN’s and notification dates Review coverage, premiums, payment history, dependents covered and COBRA

expiration date. Employee Features:

Make online payments Review payment history Review account status Sign up for direct deposit

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

E M P L O Y E R R E S P O N S I B I L I T I E S There are aspects of the COBRA administration program for which UnitedHealthcare will need your assistance. UnitedHealthcare is able to perform the administration of the COBRA program based on the information you provide to us about your COBRA eligible benefit plans and your employees who become eligible for COBRA. This section is primarily to provide the instructions that you, as the employer, will need to set in place within your organization. Also contained in this section is educational information about COBRA administrative requirements and issues that will be important to your company’s COBRA compliance.

E M P L O Y E R P R O C E D U R E S F O R C O B R A A D M I N I S T R A T I O N To properly administer your COBRA responsibilities, there are a number of critical pieces of information UnitedHealthcare will need to know, or that your company’s staff will need to perform internally. In properly following these procedures, you will help in limiting your company’s liability under COBRA. This will also assist your company in avoiding penalties, fines, or loss of tax deductions for health care premiums as a result of noncompliance.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

I N F O R M A T I O N A N D N O T I F I C A T I O N S F O R U N I T E D H E A L T H C A R E The following notifications or information will need to be submitted to UnitedHealthcare in a timely manner: 1. Notification of ANY event in which the employee or a dependent will lose health-related benefit coverage, including: Termination (whether voluntary or discharge) Reduction of hours (includes leaves of absence where coverage is lost after a certain time

period) Divorce or legal separation Employee entitled (covered) by Medicare Dependent over “normal” age (or dropping full time college course work) Dependent reaching maximum age (defined by your OBRA-eligible plans) Employee’s death

2. Notification of address changes.

3. Inform UnitedHealthcare of any status changes requested by COBRA participants to add or drop coverage. 4. Advise UnitedHealthcare of any Social Security Determination Letters sent to the employer regarding an employee’s disability status. 5. Immediately notify UnitedHealthcare of any changes in carriers. 6. Notify UnitedHealthcare of any changes in rates as soon as the information is received from the carrier(s). UnitedHealthcare will implement the new rates on the first of the month following 30 days after our receipt of the new rates. UnitedHealthcare requires advance notice in order to update rates in our system, reprint notices and mail all the new information to the current COBRA participants. 7. Advise UnitedHealthcare of any situation where the qualified beneficiary or COBRA participant is unable to make timely payments and where you wish to continue COBRA coverage. E M P L O Y E R I N T E R N A L P R O C E D U R E S F O R C O B R A C O M P L I A N C E The following information or procedures should be established internally by your company to ensure COBRA compliance: Understand COBRA requirements in general terms (aided by UnitedHealthcare). Please

refer to “Commonly Asked COBRA Questions” and “Explanation of COBRA Terms” for assistance in this area.

Understand what authority your company has to make changes to or decisions about your COBRA-eligible plans, and what plan requirements your carrier imposes that may not be overridden by the employer.

Distribute a “General COBRA Notice” to EACH employee or spouse at the time they are enrolled in benefit coverage.

If you receive notification from an employee or dependent of an event that is determined not to be eligible for COBRA continuation coverage, the Department of Labor requires you to

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

provide a written explanation as to why the individual is not entitled to continuation coverage. In these circumstances Notice of Unavailability of COBRA coverage must be provided by you to the employee or dependent within 14 days.

Advise all departments that may receive calls from individuals about coverage changes, divorces, address changes, etc, that a call to them may be considered legally a ‘notice to the company”, and should be conveyed to you and your staff immediately for proper notification to UnitedHealthcare.

C O B R A T I M E T A B L E S COBRA law allows for specific timetables for notification to the qualified beneficiary, plan administrator, service provider and payment. These timetables are represented below. Employer has 30 days to notify UnitedHealthcare of a Qualifying Event (termination, lay off,

divorce, etc.) UnitedHealthcare has 14 days to notify the Qualified Beneficiaries of their eligibility for

continuation coverage under COBRA. Qualified Beneficiaries have 60 days from the later of the date coverage is lost or the date

of the Notification letter to decide whether or not to elect COBRA coverage. Qualified Beneficiaries may enroll or waive coverage at any time within their 60-day election

period. On the 60th day (postmarked date) UnitedHealthcare will uphold the last decision made by the Qualified Beneficiary.

Once COBRA coverage has been elected, Qualified Beneficiaries have another 45 days to make the first and any subsequent payments due for the time the original coverage was lost, to the date they elected COBRA coverage.

There is a mandatory minimum 30-day grace period for each regular monthly payment before coverage can be cancelled. UnitedHealthcare will use the date of the postmark on the COBRA participant’s envelope. NOTE: 18 Months COBRA Continuation for termination or reduction of hours. 29 Months COBRA Continuation for disability established within the first 60 days of

coverage and as long as disability continues beyond 18 months. If the disability ends during the 11-month extension period, participants are no longer eligible for COBRA as of the 1st of the month that begins more than 30 days after a final determination under Social Security that the individual is no longer disabled.

36 Months COBRA Continuation for employee’s entitlement to Medicare, employee’s death, divorce, or loss of dependent status.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

A P P E N D I X A : F R E Q U E N T L Y A S K E D Q U E S T I O N S

Q. Which employers must comply with COBRA?

A. COBRA applies to employers that offer their employees health coverage and that employed 20 or more employees on 50 percent of the business days during the preceding calendar year. All full and part time employees are considered in determining whether an employer had fewer than 20 employees; however, each part-time employee counts as a fraction of a full-time employee.

Q. Last year for the first time our workforce dropped below 20 employees; therefore, we qualify for COBRA's small employer exception. Are we still responsible for administering COBRA for the period that we employed more than 20 employees?

A. Yes. Under the Internal Revenue Code (but not necessarily ERISA or the Public Health Service Act), once an employer is subject to COBRA, it continues to be responsible for qualifying events that occur while COBRA applies, regardless of whether or not the employer subsequently qualifies for COBRA's small-employer exception.

Q. Who must be offered COBRA continuation coverage?

A. Employees, spouses and dependent children who have been covered on an employer's plan at least the day before the qualifying event, for which coverage would be lost.

Q. What are the events and time frames for which COBRA must be offered?

A. Termination of employment and reduction of hours for the employee qualify for 18 months of COBRA coverage; disability determined by Social Security qualifies for up to 29 months; divorce or legal separation, loss of dependent eligibility, death of or entitlement to Medicare for the employee qualify for 36 months for the spouse and/or dependent children.

Q. Is there a minimum waiting period before a covered employee is eligible for COBRA coverage?

A. To be eligible for COBRA coverage, an employee must be enrolled in the group health plan on the day before the qualifying event takes place. Beyond that requirement, no minimum waiting period exists under COBRA. (Note, however, that some state laws include minimum periods of participation in a plan).

Q. A student lost dependent status when he stopped attending school and then elected COBRA coverage. The student later went back to school and was re-enrolled in the plan as an active dependent child. However, the student has again stopped attending school. Do we have to offer him COBRA coverage a second time?

A. Yes. COBRA does not set a limit on the number of times an individual can become a qualified beneficiary and offered COBRA coverage. As long as the basic criteria are met (that is, a qualifying event followed by a loss of coverage) the individual who goes from active coverage status to qualified beneficiary status and back to active coverage status again can elect COBRA coverage when another qualifying event is incurred.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Q. How soon after a qualifying event do we have to notify qualified beneficiaries of their COBRA rights?

A. Once a qualifying event occurs, employers have 30 days to notify the plan service provider. Once notified, the plan service provider has 14 days to notify all affected qualified beneficiaries of their COBRA rights.

Q. What notices are employers required to send to qualified beneficiaries?

A. The employer is required to send the following notices:

The general notice advising newly covered employees and their spouses of their COBRA continuation rights

The notice of election rights sent at the time of the qualifying event A notice of unavailability of COBRA provided when it is determined an employee or

dependent are not eligible for continuation coverage A notice of early termination of COBRA is sent when COBRA coverage terminates

before exhaustion of coverage A notice advising COBRA participants of their conversion coverage rights, if applicable

Q. Are we required to pay medical bills incurred by qualified beneficiaries during the election period but before they elect to continue coverage?

A. Once the enrollment form is received from the participant, UnitedHealthcare will enroll the participant but we do not update eligibility until the initial payment is received which will hold claims payment from being made which follows the COBRA regulations.

Q. A former employee has been having medical treatment during his COBRA election period, but has not yet elected or paid for COBRA coverage. What should we say when the provider contacts us about his coverage status?

A. The IRS final regulations of February 1999 require that a plan providing COBRA coverage must make a complete response to any provider inquiry regarding a qualified beneficiary's right to coverage during the election period. Therefore, a plan must either state that:

If the qualified beneficiary is covered, that coverage is subject to retroactive termination if the COBRA election and premium payment are not made or If the qualified beneficiary is not covered, coverage will be reinstated retroactively if the election and payment are made on time Q. Do we have to offer COBRA coverage to employees on military leave?

A. Yes. A federal law enacted in 1994 requires employers to offer up to 18 months of continuation coverage to employees and their dependents who take military leave. Furthermore, IRS Notice 90-58 and IRS regulations also provide that employers offer COBRA coverage due to military leave. Though not a requirement under COBRA, the Veterans Benefits Improvement Act was signed into law in December of 2004. It requires under the Uniform Services Employment and Reemployment Act that continuation of employer provided health coverage be offered for up to 24 months of coverage for employees who are called into active military service.

Q. An employee and her spouse recently annulled their marriage. Is this a qualifying event?

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

A. COBRA only specifies that divorce and legal separation are qualifying events. However, before applying the statute narrowly, employers may want to consider factors such as Congressional intent to protect plan participants and their family members from loss of coverage State law regarding the dissolution of marriage Plan documents. Therefore, employers should obtain the advice of legal counsel before any determination is made not to offer COBRA coverage in cases of annulment.

Q. COBRA allows employers to deny continuation coverage to former employees who are discharged for gross misconduct. What actions constitute gross misconduct?

A. The courts and the U.S. Office of Personnel Management have issued limited guidance concerning the definition of gross misconduct under COBRA. The IRS has issued no guidance in this area, and has indicated that it does not intend to do so. Therefore, employers have to judge for themselves what constitutes gross misconduct. Crimes committed in the workplace, such as embezzlement or theft, could constitute gross misconduct, depending on the severity of the conduct in question. However, discharges for poor performance or incompetence are probably not adequate grounds to deny former employees continuation coverage. Employers must carefully evaluate each case to determine if the conduct in question constitutes gross misconduct and should obtain the advice of legal counsel before any determination is made.

Q. A former employee was terminated for gross misconduct. He is not being offered COBRA coverage; however, could we still offer it to his spouse and dependent children?

A. COBRA's statutory language provides that if an employee is terminated for gross misconduct, a qualifying event has not occurred. Therefore, COBRA coverage would not have to be offered to the employee, the spouse or any dependent children. COBRA is a minimum requirement, however. The employer can voluntarily provide COBRA coverage to the ex-employee's spouse or dependent children or even to the former employee, if it so chooses.

Q. Can we require qualified beneficiaries to elect continuation coverage that is not as good as what they had as active employees?

A. The law specifies that qualified beneficiaries must be allowed to continue coverage that is identical to the coverage that they received before the qualifying event occurred. This means that if an employee was covered under a special type of plan, such as one that provided annual physicals, he or she would have to be allowed to continue that coverage.

Q. A qualified beneficiary has become entitled to Medicare. Can we drop this former employee's coverage for herself and her husband, who is covered under her family coverage?

A. The former employee can be dropped from COBRA as a result of becoming entitled to Medicare after the date of her COBRA election. However, her husband must be allowed to stay on COBRA for up to 36 months from the date of the termination of employment or reduction in hours provided the original event would have been considered a loss of coverage. Note that if the qualified beneficiary had become entitled to Medicare before she elected COBRA coverage, she would be eligible for COBRA coverage.

Q. A qualified beneficiary who has COBRA coverage under our medical and dental plan has become entitled to Medicare. We plan to terminate his medical coverage, but do we have to keep him on the dental plan because Medicare doesn't cover dental benefits?

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

A. The statute does not distinguish between core and non-core benefits when it allows COBRA coverage to be cut off once a qualified beneficiary becomes entitled to Medicare after the date of the COBRA election. Therefore, employers can drop dental or any other non-core benefits in such situations. However, some employers do choose to continue those benefits because they are not provided under Medicare.

Q. When coordinating COBRA and other coverage under the pre-existing condition rule, which employer's plan is primary and which is secondary?

A. The statute fails to address this subject, and the IRS has not issued any guidance. However, under general coordination of benefits guidelines developed by the National Association of Insurance Commissioners, the COBRA provider would pay claims related to the pre-existing condition and the new employer's plan would pay any other claims.

Q. What do we do if we have discovered that after electing COBRA coverage, a qualified beneficiary became covered under another group health plan that covers all of the individual's pre-existing conditions and the individual has not informed us of that coverage?

A. IRS regulations do not address this point. Certainly, an employer would be justified in terminating a qualified beneficiary's coverage in such a situation. However, an employer would first have to analyze the other employer's plan to verify whether or not it covers the individual's pre-existing conditions. Once verified, an employer must then determine if claims have been paid while the beneficiary was covered under another plan. If claims have been paid, the employer or its insurance carrier would probably have to sue the individual involved to recover any money paid under that claim if the qualified beneficiary refused to return the payments. In certain situations, an employer may be limited in its ability to obtain such amounts.

Q. We offer a severance or retirement package that includes health insurance, but it is not as comprehensive as COBRA coverage. What does COBRA require in that instance?

A. If the alternative coverage is not identical to COBRA coverage or costs more than the active coverage, the IRS final regulations of February 1999 provide that a qualified beneficiary must be allowed to elect COBRA coverage. However, if the qualified beneficiary rejects the COBRA coverage in favor of alternative coverage, the alternative coverage is not treated like COBRA coverage.

Q. Do we have to offer COBRA coverage after the alternative coverage period has expired?

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

A. When the alternative coverage period expires, the covered individual does not have to be offered a COBRA election. If one of the individuals receiving alternative coverage is an employee participant, and the spouse or dependent child would lose that alternative coverage as a result of a qualifying event (such as death of the employee or divorce), the spouse or child must be allowed to elect to continue that alternative coverage. The maximum period would be 36 months (like COBRA), and the start date of the 36 months would be from the date of the qualifying event, rather than from the date the alternative coverage started for the employee participant (unlike COBRA) Finally, the employer may also offer alternative coverage that is identical to "regular" coverage as part of the COBRA eligibility period. For instance, as part of a severance package, an employer may pay for 3 months of coverage, and then offer the employee COBRA. If the coverage is identical, except for the cost of the premium, the employer may start the "COBRA clock" ticking on the date of the qualifying event, not when coverage is lost …3 months later.

Q. How do I coordinate both the state continuation coverage law and federal COBRA law?

A. Generally, in coordinating COBRA and a state law, whichever provision gives qualified beneficiaries the best benefits or most rights is the one that takes precedence. For example, a state law may require employers to give terminated employees 24 months of continuation coverage but may not require them to extend continuation rights to their spouses and dependents. However, employers in that state would also have to allow those spouses and dependents to continue coverage for at least 18 months, as required by federal COBRA law.

Q. Can an employee elect COBRA but request that premium payment begin at a later time?

A. To be considered timely, a qualified beneficiary's first payment for COBRA coverage must be made within 45 days after the date of the election. Employees cannot be required to pay more frequently then on a monthly basis. An employer can offer, but not require, qualified beneficiaries to pay for COBRA coverage at various intervals other than monthly (for example, quarterly or semiannually).

Q. Out of an entire family that was covered under our group health plan, only the dependent is electing COBRA coverage. Should we charge him a portion of the family rate or the rate for single coverage?

A. Because there will be one person – the dependent - electing COBRA coverage, generally (and absent detailed regulatory guidance to the contrary), that person should be charged the premium rate for a similarly situated active employee. Therefore, in this case, you would charge the premium rate for single coverage.

Q. Can we offer COBRA coverage for longer than the required period?

A. COBRA's coverage requirements are intended to be minimum standards. Employers are permitted to offer qualified beneficiaries more extensive coverage or coverage for a longer duration if they choose to do so. Remember you should always treat similarly situated employees in the same manner as not to discriminate.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Q. Can we be held liable if a covered employee drops his or her spouse from our plan in anticipation of a divorce or other qualifying event?

A. Just as employers cannot negate their COBRA responsibility by canceling the coverage of covered employees in anticipation of a qualifying event; covered employees are not permitted to drop family members from their coverage in similar situations. If an employer learns that this has occurred, it should offer the dropped family member continuation coverage from at least the date on which coverage was lost due to the qualifying event. For example, if a covered employee dropped his wife from his employer-provided family coverage two weeks before their divorce became final, the employer should offer the employee's wife coverage at least from the date on which she would have lost coverage due to the divorce.

Q. We have separate group health contracts for each of our four different office locations. We recently closed one of those offices. If the insurers at each of the other three locations won't pick up COBRA-eligible persons from the closed office, are we in violation of COBRA?

A. A COBRA violation occurs if an employer does not offer continued health benefits to employees who are terminated because of an office or plant shut-down. COBRA coverage is generally the employer's responsibility. However, if the insurer failed to cooperate in providing COBRA coverage, the insurer could be liable for an excise tax. The continuation of coverage should be explored with the carrier that insured the closed office or plant. (Note: This type of situation, in which insurers have refused to accept COBRA beneficiaries into a new plan, appears to be a growing problem. Employers should review their plan contracts and determine where their insurers stand on this matter. Also, the COBRA excise tax sanction could apply to certain noncompliant insurers).

Q. We want to terminate our current group health plan and contract with another insurance carrier, but the new carriers we talk to say they won't take our COBRA qualified beneficiaries. Is this legal?

A. More and more employers wanting to change insurance carriers are discovering that potential insurers only want to cover active employees. Unfortunately, because the insurance company and employer are not yet under contract, companies may find it difficult to require potential insurance carriers to cover qualified beneficiaries. An employer may want to make the insurance carrier aware that they can be liable for excise tax sanctions for making the employer out of compliance with COBRA regulations. However, it is important to remember that it is the employer who has the ultimate responsibility to provide coverage and therefore it may be prudent to make arrangements to keep the qualified beneficiaries covered under the current benefit plan.

Q. Can someone who has been on COBRA for several months end their coverage, due to failure to pay (for example), and later be reinstated?

A. Generally, once a qualified beneficiary fails to pay a COBRA premium by the end of the 30-day grace period for premium payment, UnitedHealthcare will terminate the participant permanently from COBRA coverage and would not be eligible for reinstatement.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Q. Who exactly is liable for COBRA violations?

A. Generally, under ERISA, an employer may be liable for medical expenses and other fines and penalties if it fails to provide notice(s) to qualified beneficiaries on a timely basis. Failure to provide a COBRA election notice within the required time lines could expose the employer to statutory penalties of up to $110 per day. Under the Internal Revenue Code, excise tax sanctions can be imposed against the employer, the insurer, the TPA or other plan fiduciaries (such plan fiduciaries may also incur liability under ERISA). ERISA penalties can also include lawsuits and the payment of attorney's fees. Other penalties may be assigned at the court's discretion and can include any unpaid claims, the value of future coverage and even awards for pain and suffering.

Q. Once we recognize our noncompliance, apart from complying in the future, should we retroactively rectify the situation by providing notices and honoring elections?

A. Employers that find they have committed violations should make efforts to correct them as quickly as possible. Not only must employers make available all of the coverage lost, but also it is essential that they make the qualified beneficiaries whole with regard to health care claims. This means that employers may have to pay any medical expenses that would have been covered had benefits been continued in accordance with the law. Employers may want to discuss these options with their carriers, attorneys or other advisors. Employers should establish "good faith" procedures to demonstrate compliance to avoid the various penalties for violating COBRA.

Q. What should we do if our benefit provider is unwilling to provide COBRA coverage?

A. The excise tax sanctions for non-compliant employers could also apply to benefit providers, as well as ERISA penalties. This could give employers some additional bargaining power with reluctant providers. Ultimately though, complying with COBRA remains the employer's responsibility. The best way for employers to protect themselves is to enter into a written, legally enforceable agreement with the provider that spells out each party's responsibilities.

Q. Must an HRA comply with certain COBRA requirements if an individual elects COBRA continuation coverage?

A. An HRA is a group health plan generally subject to the COBRA continuation coverage requirements. If an individual elects COBRA continuation coverage, an HRA complies with these COBRA requirements by providing for the continuation of the maximum reimbursement amount for an individual at the time of the COBRA qualifying event and by increasing that maximum amount at the same time and by the same increment that it is increased for similarly situated non-COBRA beneficiaries (and by decreasing it for claims reimbursed).

Q. What HRA election options are available to a beneficiary who is eligible for COBRA?

A. A qualified beneficiary who chooses to elect COBRA continuation coverage may only elect the HRA in conjunction with the major medical plan. However, a qualified beneficiary may choose to elect COBRA continuation coverage for only the major medical plan.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

A P P E N D I X B : C O B R A R E N E W A L O V E R V I E W

UnitedHealthcare COBRA and Retiree Renewal KitUnitedHealthcare COBRA and Direct Bill Administrative Services

Thank you for allowing UnitedHealthcare to serve your benefit plan for your COBRA and/or Direct Bill needs for the policy year ending. Now its time to begin making plans for the coming year.

COBRA Qualified Beneficiaries, including those in their enrollment period, must be offered the same rights as active employees. This includes the same right to change group health plan(s) as well as add or remove dependent(s). When you distribute enrollment materials to your active employees, you must also notify COBRA participants of new rates and benefit plan or carrier changes. COBRA participants must also be provided the same length of time to make their selections and return their paperwork.

This packet contains the information you need to complete your COBRA and/or Direct Bill Renewal. We have consolidated and streamlined our renewal process to provide you with all of the information you need and outlined the steps to successfully complete your annual renewal.

If you would like to set up a conference call to walk through this information and fill out the document together — we are happy to do so.

We’re looking forward to another year of serving you and your participant’s administrative needs. Please take this time to review the information provided. Please contact me at with any questions.

Sincerely

UnitedHealthcare COBRA and Direct Bill Administrative Services

Review Checklist of things to do 2

Consider Your options 3

Identify Changes on your renewal 4

Impacts Eligibility and disbursements 6

Appendix 7

New carrier information 8

Submit Email to finalize your renewal 9

How to use this document:

UnitedHealthcare

COBRA and Direct Bill

Administrative Services

Review

2

This renewal workbook includes the forms needed to process the renewal information and provides your options for communicating information to your current participants and those in notified status.

The renewal kit includes:} Questions about your annual enrollment process

} Carrier/Plan renewal information sheet which must be completed for each plan with separate rates.

Self-Insured Plans:To make the process easier for you we can access any changes to your self-insured plans but we will need the rates that will be charged to the participants without the 2% administrative fees. The carrier/plan renewal information sheet can be used to provide the appropriate information.

Fully Insured Plans:We can access any changes to your fully insured plans. Therefore, if you only have fully insured plans with UnitedHealthcare, we can update your renewal information as soon as the rates are available.

Non-UnitedHealthcare Plans:We will need your assistance for any plan that is not administered by UnitedHealthcare. You will need to provide any plan or rate changes required.

} Participant change worksheet to report changes to the COBRA / Direct Bill enrollment.

} A sample enrollment form you can use for collecting enrollment information.

} UnitedHealthcare will add the additional administration fee (typically 2%) to the rates you provide, if indicated to do so. Please do not include the administrative fee in the rates you provide.

} If any plans have been discontinued, please note that accordingly.

Rate changes must reach UnitedHealthcare no later than 45 days prior to their effective date if we are not supporting your annual renewal notifications to your participants.

This will allow UnitedHealthcare to:

} Enter the rate/plan information into the system

} Provide time for the participant to receive the required notice, elect coverage and receive new billing information

} Communicate updated eligibility information to any outside carriers. Please note that most carriers will require eligibility to be provided the first week of the month prior to the effective date in order to provide ID cards.

Task list of things to do:

} Provide the requested

information within

this packet

} Provide rate information

} Identity enrollment process

Consider

New enrollment tools and support are available to you from UnitedHealthcare COBRA/Direct Bill

Our website is available to the participants for the renewal period. If you would like to use this service, let your service consultant know. Direct the participants in your enrollment information to visit www.uhcservices.com and request the change to their plan/enrollment online.

- or -UnitedHealthcare can process enrollment forms sent on your behalf to a COBRA participant and those in their enrollment period. If this is a service that you would like for us to provide, direct the participants to mail the election form to:

UnitedHealthcare Attn: COBRA/Direct Bill Department – Annual Enrollment

- or - We can also provide enrollment-mailing services. If you need support in the notification process of your COBRA/Direct Bill participants, please let your service consultant know you are requesting a price quote for the service.

Once your enrollment process is complete, please send any changes to

3

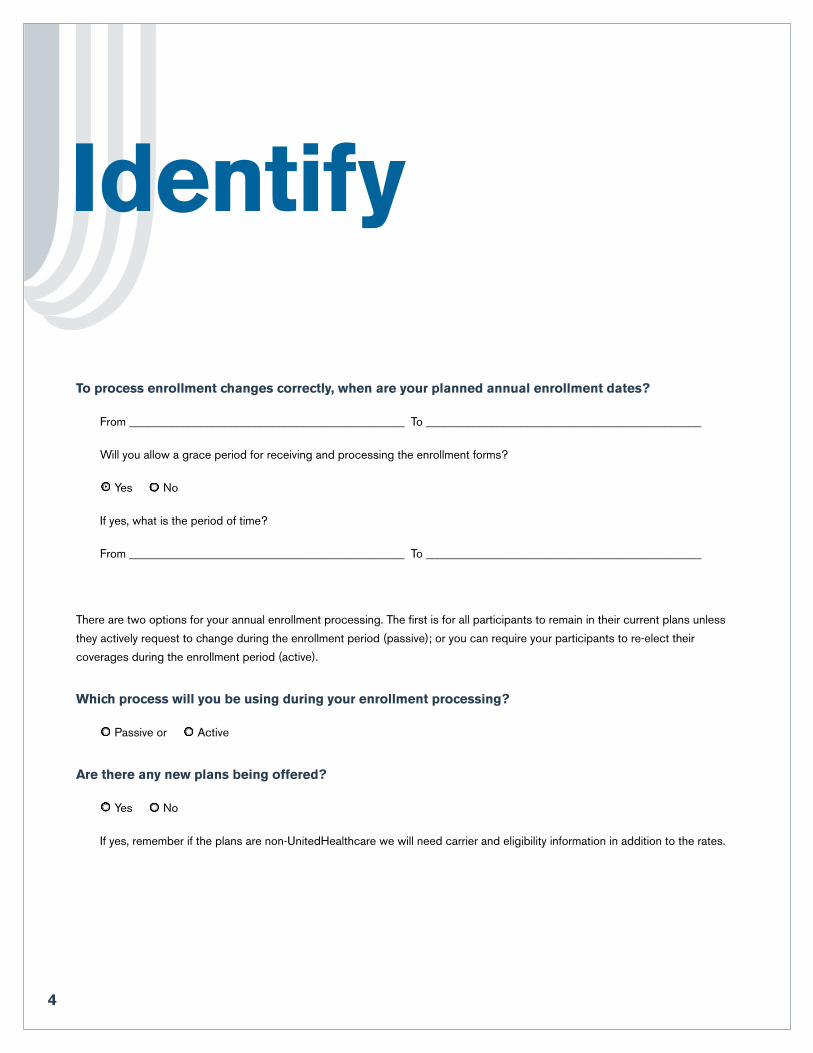

Identify

4

To process enrollment changes correctly, when are your planned annual enrollment dates?

From ______________________________________________ To ______________________________________________

Will you allow a grace period for receiving and processing the enrollment forms?

Yes No

If yes, what is the period of time?

From ______________________________________________ To ______________________________________________

There are two options for your annual enrollment processing. The first is for all participants to remain in their current plans unless

they actively request to change during the enrollment period (passive); or you can require your participants to re-elect their

coverages during the enrollment period (active).

Which process will you be using during your enrollment processing?

Passive or Active

Are there any new plans being offered?

Yes No

If yes, remember if the plans are non-UnitedHealthcare we will need carrier and eligibility information in addition to the rates.

5

Are there any plans being removed from your current offering?

Yes No

If yes and your enrollment process is passive, what plan will be the replacement plan for the plan expiring?

Current Plan _____________________________________________________________________________________________

Default Plan _____________________________________________________________________________________________

Note: if there are multiple plans, please list each current plan and default plan

If you are performing the renewal enrollment process, will you need a mailing list from us?

Yes No

If you are performing the renewal enrollment process, when will the information be mailed so that if the participants call the customer care center we can support the participant’s questions?

Date of Mailing: ______________________________________________

How will you be reporting the enrollment information to us?

Spreadsheet of changes emailed to

Using www.uhcservices.com

Enrollment forms sent to UnitedHealthcare COBRA/Direct Bill

UnitedHealthcare COBRA/Direct Bill mailing the enrollment information

Do you want UnitedHealthcare COBRA/Direct Bill to mail a rate change notice to the participants?

Yes No

Who should questions be directed to?

Name: __________________________________________________________________________________________________

Email: __________________________________________________________________________________________________

Phone: _________________________________________________________________________________________________

6

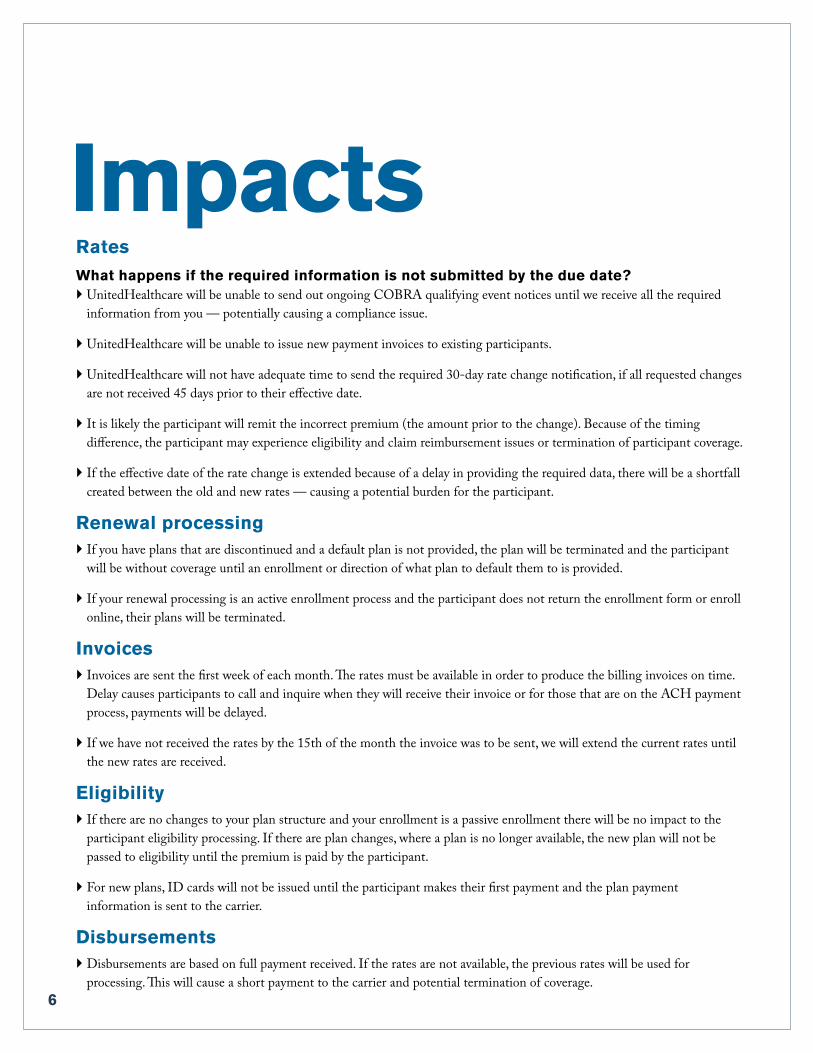

ImpactsRatesWhat happens if the required information is not submitted by the due date?} UnitedHealthcare will be unable to send out ongoing COBRA qualifying event notices until we receive all the required

information from you — potentially causing a compliance issue.

} UnitedHealthcare will be unable to issue new payment invoices to existing participants.

} UnitedHealthcare will not have adequate time to send the required 30-day rate change notification, if all requested changes are not received 45 days prior to their effective date.

} It is likely the participant will remit the incorrect premium (the amount prior to the change). Because of the timing difference, the participant may experience eligibility and claim reimbursement issues or termination of participant coverage.

} If the effective date of the rate change is extended because of a delay in providing the required data, there will be a shortfall created between the old and new rates — causing a potential burden for the participant.

Renewal processing} If you have plans that are discontinued and a default plan is not provided, the plan will be terminated and the participant

will be without coverage until an enrollment or direction of what plan to default them to is provided.

} If your renewal processing is an active enrollment process and the participant does not return the enrollment form or enroll online, their plans will be terminated.

Invoices} Invoices are sent the first week of each month. The rates must be available in order to produce the billing invoices on time.

Delay causes participants to call and inquire when they will receive their invoice or for those that are on the ACH payment process, payments will be delayed.

} If we have not received the rates by the 15th of the month the invoice was to be sent, we will extend the current rates until the new rates are received.

Eligibility} If there are no changes to your plan structure and your enrollment is a passive enrollment there will be no impact to the

participant eligibility processing. If there are plan changes, where a plan is no longer available, the new plan will not be passed to eligibility until the premium is paid by the participant.

} For new plans, ID cards will not be issued until the participant makes their first payment and the plan payment information is sent to the carrier.

Disbursements} Disbursements are based on full payment received. If the rates are not available, the previous rates will be used for

processing. This will cause a short payment to the carrier and potential termination of coverage.

Appendix

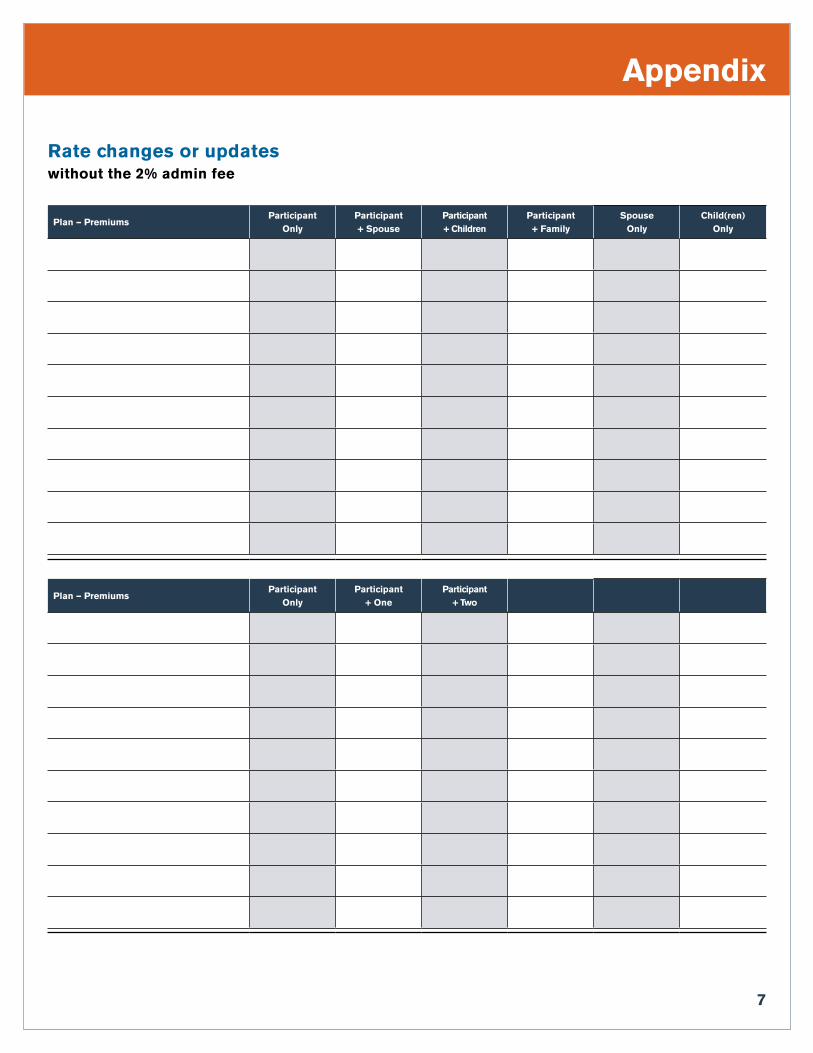

Rate changes or updates without the 2% admin fee

Plan — PremiumsParticipant

OnlyParticipant + Spouse

Participant + Children

Participant + Family

Spouse Only

Child(ren) Only

Plan — PremiumsParticipant

OnlyParticipant

+ OneParticipant

+ Two

7

New carrier and plan information

Please complete a separate form for each new plan.

Insurance Carrier Name ___________________________________________________________________

Group / Policy # ___________________________________________________________________

COBRA PVRC Codes (UnitedHealthcare only) ___________________________________________________________________

Plan Name ___________________________________________________________________

Carrier Eligibility Contact ___________________________________________________________________

Email Address ___________________________________________________________________

Phone Number ___________________________________________________________________

Address ___________________________________________________________________

City, State and Zip ___________________________________________________________________

Fax Number ___________________________________________________________________

Coverage Type (i.e., Medical, Dental, etc.) ___________________________________________________________________

Disbursement Process ___________________________________________________________________ (i.e., to the carrier, to the client)

Rates without the 2% admin fee

Plan — PremiumsParticipant

OnlyParticipant + Spouse

Participant + Children

Participant + Family

Spouse Only

Child(ren) Only

8

Submit } For quickest processing email to: With a cc to:

} Mail to: UnitedHealthcare Attn: COBRA/Direct Bill Renewal Information

9

M48447 11/10 © 2010 United HealthCare Services, Inc.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

A P P E N D I X C : G L O S S A R Y

Anticipation of a Qualifying Event: Most commonly referenced when an employee drops coverage on a spouse because a divorce is pending. If this happens the spouse would not be eligible for COBRA coverage in the event of divorce because he or she did not have health-related coverage on the date of the divorce. Once an employer discovers this, they are obligated by law to offer COBRA coverage at least back to the date of the divorce.

Conversion Coverage: Refers to an option that may be available in an employer COBRA-eligible plan that allows a COBRA participant additional coverage after the COBRA coverage period has ended. It is typically different coverage than COBRA, and may have lesser benefits with higher premiums. The COBRA participant must be notified that the option is available within 180 days of the COBRA coverage end date.

COBRA: Consolidated Omnibus Budget Reconciliation Act of 1985.

COBRA Continuation Coverage: Refers to the 18, 29, or 36 month period of time that a qualified beneficiary who has elected COBRA coverage has to remain covered under COBRA. COBRA coverage is a term used interchangeably with COBRA continuation coverage.

COBRA-Eligible Plans: Benefit plans that provide health-related benefits for the diagnosis, cure, or treatment of a health condition, including mental health. Most common plans are health, dental, vision, employee assistance plans (that provide more than referrals), medical flexible spending accounts, health reimbursement arrangements, medical reimbursement plans, wellness or physical evaluation programs, and even on-site medical care provided to employees and/or their dependents.

COBRA Participant: Refers to a qualified beneficiary who has elected COBRA coverage.

COBRA Timetables: Refers to the specific COBRA coverage periods required to be offered for different qualifying events that result in loss of coverage:

Termination of employment or reduction of hours for the employee is a coverage period of 18 months.

If the qualified beneficiary is disabled (by Social Security determination) prior to or within the first 60 days of COBRA continuation coverage, and remains disabled, up to an additional 11 month extension of coverage is available.

A spouse or dependent of the employee is eligible for up to 36 months in the event of divorce or legal separation, loss of dependent status, employee’s entitlement to (covered by) Medicare, or the death of an employee.

A retired employee and his or her qualified dependents are eligible for up to 36 months in the event the employer files for bankruptcy under Title XI, United State Code and the employee loses coverage up to a year before or a year after such filing.

Covered Employee: Any employee who is (or was) provided coverage under a group health plan through that individual’s employment or previous employment.

Covered Employer: An employer who is required to comply with the COBRA law because they had 20 or more employees in the previous year, as counted on a “typical” business day. Part-time employees may be counted as full-time equivalents (FTE) based on their average hours, rather than as one employee.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Determination of Disability: COBRA law allows a qualified beneficiary who has been considered disabled according to Social Security, an additional extension of up to 11 months of coverage beyond the normal 18 months. This applies as long as:

the qualified beneficiary notifies the employer or United Healthcare within 60 days of the Social Security determination

and that the determination is made or remains in effect as of at least one day before or within 60 days after the COBRA coverage begins

Election Period: The 60 day period of time that the employee, spouse or dependents have to actually choose or “elect” COBRA coverage. The election period is measured from the later of the “loss of coverage date” or the date the qualified beneficiary was sent the “notice of election rights”. The election period does not affect the overall COBRA coverage period. If a qualified beneficiary does not elect COBRA coverage by day 60, he or she has no further legal rights to COBRA coverage.

General COBRA Notice: The IRS Code and ERISA each provide that a group health plan must provide a written notice to each covered employee and spouse of the employee (if any) of the rights provided under COBRA. A General Notice can be provided through the COBRA-eligible plan booklets or summary plan descriptions, or it can be a separate document. The separate document can be provided to employees through orientation, or through the new hire paperwork. If the employee adds his/her spouse to the coverage at the time of his/her first eligibility, a written notice must also be delivered to the spouse. This is usually done through a first class mailing to the home address. If a spouse is added at a later time, such as through open enrollment or marriage, a separate Notice must be delivered.

Grace Periods: Refers to the time periods that a COBRA participant has to pay the premiums due. For instance, once the qualified beneficiary has elected COBRA coverage, he or she has 45 days to pay any premiums due between the qualifying event date and the date of election. He or she also has a 30 day grace period for monthly premium payments, as well as an additional 30 day grace period for making up a partial payment. Finally, a participant's grace period may be put on "hold" if it is found that he or she is mentally or physically incapable of making timely payments, until arrangements for payment can be made on his or her behalf.

Individual Rights of Election: Each qualified beneficiary has the right to independently elect COBRA coverage. The employee or the spouse may also elect coverage on behalf of other family members as qualified beneficiaries. However, the employee or spouse may not decline coverage for a qualified beneficiary age 18 or older. For example, an employee may not decline for a spouse, or for an 18-year-old dependent.

Insignificant Amount: Defined as the lesser of either $50.00 or 10% of the COBRA premium due.

Loss of Coverage Date: The date that the qualified beneficiary actually loses "regular" coverage from the employer's plan. This may be a different date than the “qualifying event date." For instance, an employee has a qualifying event of a reduction in hours on the 15th of the month, but the coverage is not actually lost until the end of the month. The last day of the month would then be the "loss of coverage date." The 18, 29 or 36 month COBRA coverage period, however, is typically counted from the date of the qualifying event, rather than the loss of coverage date.

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Multiple Qualifying Events: An event that happened more than once that would allow an employee and his/her covered dependents to elect COBRA coverage each time "regular" coverage is lost. There is no limit to the number of times an employee or qualified beneficiary can elect COBRA coverage, as long as there continues to be events in which "regular" coverage through the employer is lost.

Notice of Election Rights: This is an additional notice requirement that must be delivered to all qualified beneficiaries regarding their COBRA election rights within 14 days of being notified of a qualifying event.

Partial Payment: Refers to a COBRA participant making less than the full payment due. However, if the partial payment is of an "insignificant amount", the employer may not cancel coverage, and must allow another 30 day grace period to make the full payment. Coverage may be canceled if full payment is not made within the second 30 day grace period. The required additional grace period does not affect the due dates for subsequent months' billing.

Qualified Beneficiary: Refers to an employee or a dependent that is covered on an employee's group health-related plan the day before the qualifying event takes place. As an example, if an employee and a dependent gained coverage on the first of the month, and the employee terminated on the 15th of that month he and his eligible dependent(s) would be eligible for coverage under COBRA. A newborn or adopted child may also be added to a covered employee's COBRA as a qualified beneficiary even after the original qualifying event.

Qualifying Event: The date on which a situation occurs that might cause an employee or his dependents to lose coverage under an employer's group health related plan, such as for:

Termination of Employment, this includes layoff

Reduction in hours, this includes leave of absence

Employee’s entitlement to (covered by) Medicare

Divorce or legal separation

Death of employee

Dependant reaching maximum age of coverage

Bankruptcy of the employer for which a retiree and dependents were previously eligible for coverage

Qualifying Event Notice (QEN): United Healthcare must provide a Qualifying Event Notice to all qualified beneficiaries informing them of their right to elect COBRA. This notice must be sent within 14 days from the day that UnitedHealthcare received notification of the qualifying event. UnitedHealthcare will receive terminations for most small business UnitedHealthcare customers; you may also enter the Qualifying Event online at uhcservices.com. Once entered, the Qualifying Event Notice will be generated and sent to the participant.

Qualifying Event Notice Form (QE Form): The actual form that contains the Qualifying Event Notice (QEN).

Employer Reference Guide COBRA Administration

April 2011 www.unitedhealthcare.com

Retroactive Reinstatement: Refers to the status of coverage after an employee has had a qualifying event. That is, typically, coverage is canceled with the carrier on the date coverage is lost. Then, if the qualified beneficiary elects coverage, the employer will notify the carrier of the reinstatement of coverage, back to the date coverage was lost.

Second Qualifying Events An additional qualifying event that occurs during the first period of COBRA coverage that may qualify for an extension of COBRA coverage. For example, if a former employee who elects for 18 months of COBRA coverage for his family because of a termination of employment, then later divorces, his former spouse and any eligible dependents would be eligible to elect up to a total COBRA continuation period of 36 months. (Can also be referred to as a subsequent or multiple qualifying event). The maximum period of COBRA second or subsequent qualifying event coverage is a total of 36 months, as counted from the date of the first qualifying event. COBRA coverage is not extended if the original qualifying event already provides for 36 months of COBRA coverage. If a second qualifying event occurs, involving the spouse or dependent children, the employee, or the spouse must notify the employer or UnitedHealthcare in writing within 60 days of the second event. Failure to notify within that time period would disqualify the qualified beneficiaries from obtaining an extension of COBRA coverage, if eligible.

State Continuation Law: Some states have their own continuation coverage requirements. An employer must offer the more generous of the provisions between the state and federal laws. Typically, the COBRA coverage is more generous.

Termination of COBRA: COBRA can be terminated earlier than the full COBRA time period for several reasons:

Failure by the participant to make timely payments

Employer ceases to provide any health insurance coverage

The participant becomes covered under another plan which doesn't limit or exclude for pre-existing condition

Medicare entitlement

Unavailability of COBRA Coverage: The regulations define that if an employee or dependent submit notification that an event has occurred, or make a request for COBRA coverage, they expect continuation coverage is available. If continuation coverage is not available, the Department of Labor requires a notice of unavailability of COBRA to be sent within 14 days.

Waiver of Coverage During the 60 day election period, a qualified beneficiary has the right to decline coverage and then revoke the declination or "waiver" (in effect, electing coverage). In fact the qualified beneficiary may waive and then revoke the waiver as many times as they wish during the 60 day election period. The last change received by the 60th day (postmarked) will be the qualified beneficiary's decision that is upheld by the employer - whether that is to waive coverage or elect it.