wide screen template - home.kpmg tax update 7 december.pdf · — taar disregards arrangements main...

TRANSCRIPT

Welcome

UK Tax Update Jason Laity—7 December , 2016

2

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

8:35-8:55 UK residential property – Jason Laity

8:55-9:25 Long term UK residents, including rebasing, mixed funds, trust protections – Greg Limb & Anna Warren

9:25-9:45 HMRC’s approach to offshore – Derek Scott

9:45-10:00 Questions

8:30-8:35 Introduction – Jason Laity

Residential Property

Jason Laity

December 7, 2016

4

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The property landscape— Significant number of complex changes in a short space of time

21 Mar 201215% SDLT ‘enveloped’rate >£2m

ATED threshold >£500k

17 Jul 2013IHT debt restrictions

6 Apr 2014PPR Changes

6 Apr 2015NRCGT & PPR changes

Apr 2016Wear and tear allowance one

Apr 2017Interest relief restriction for landlords

Apr 2013ATED threshold >£2m

20 Mar 201415% SDLT ‘envelope’ rate >£500k

Apr 2017IHT if UK property held via companies or trust

4 Aug 2014Changes to debt remittance rules

1 Apr 2015ATED threshold >£1m

1 Apr 2016SDLT surcharge

4 Dec 2014New SDLT rates/bands

201720162015201420132012

Changes already in place

6

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

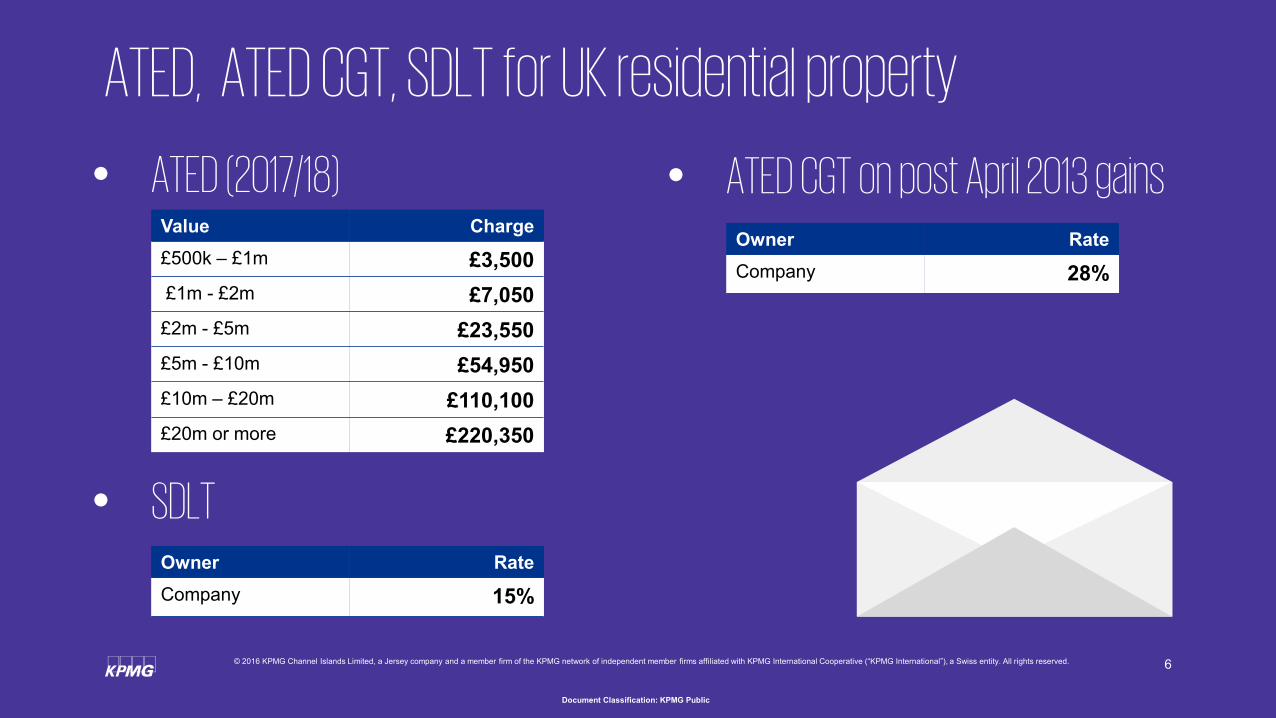

ATED, ATED CGT, SDLT for UK residential property

• ATED (2017/18)Value Charge£500k – £1m £3,500£1m - £2m £7,050£2m - £5m £23,550£5m - £10m £54,950£10m – £20m £110,100£20m or more £220,350

• ATED CGT on post April 2013 gainsOwner RateCompany 28%

Owner RateCompany 15%

• SDLT

7

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 7

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

NR CGT, SDLT for UK residential property

• “Additional property” SDLT rates • NR CGT on post April 2015 gainsOwner RateIndividual 18%/28%Trustee 28%Company 20%

Band Previous residentialSDLT rates

New additional property

SDLT rates

£0* – £125k 0% 3%

£125k – £250k 2% 5%

£250k - £925k 5% 8%

£925k - £1.5m 10% 13%

£1.5m + 12% 15%

Changes from April 2017

9

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Inheritance tax on UK residential properties— Interest in close company, partnership or loan not excluded property if attributable to UK

residential property

Value of non-UK company in trust attributable to UK residential property relevant property and liable to UK IHT on 10 year charge or death of settlor (if GROB)

Value of non-UK company attributable to UK residential property relevant property and liable to UK IHT on death of shareholder or gift of shares with 7 years of death

— Deduction for debt in close company, but note that loan itself subject to IHT

— Odd provision stops sale proceeds of non-UK company, partnership or loan attributable to UK residential property being excluded property for further 2 years

— NR CGT definition of UK residential property i.e. no minimum value and no letting relief

— TAAR disregards arrangements main purpose of which to “avoid or minimise” IHT on UK residential property

— Proposal to impose liability on any person who has legal ownership of property, including non-residents, has been dropped

— No mention of proposal to prevent sale of property until IHT paid

10

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 10

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Existing structuresRestructure ?— Make gifts pre-April 2017 whilst excluded property to avoid gift being

considered a PET — Loans

De-envelope ?— No de-enveloping relief so SDLT / ATED CGT/ s87 & s13 TCGA 1992— Case by case e.g. could de-envelope just to trust level if settlor dead

11

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 11

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

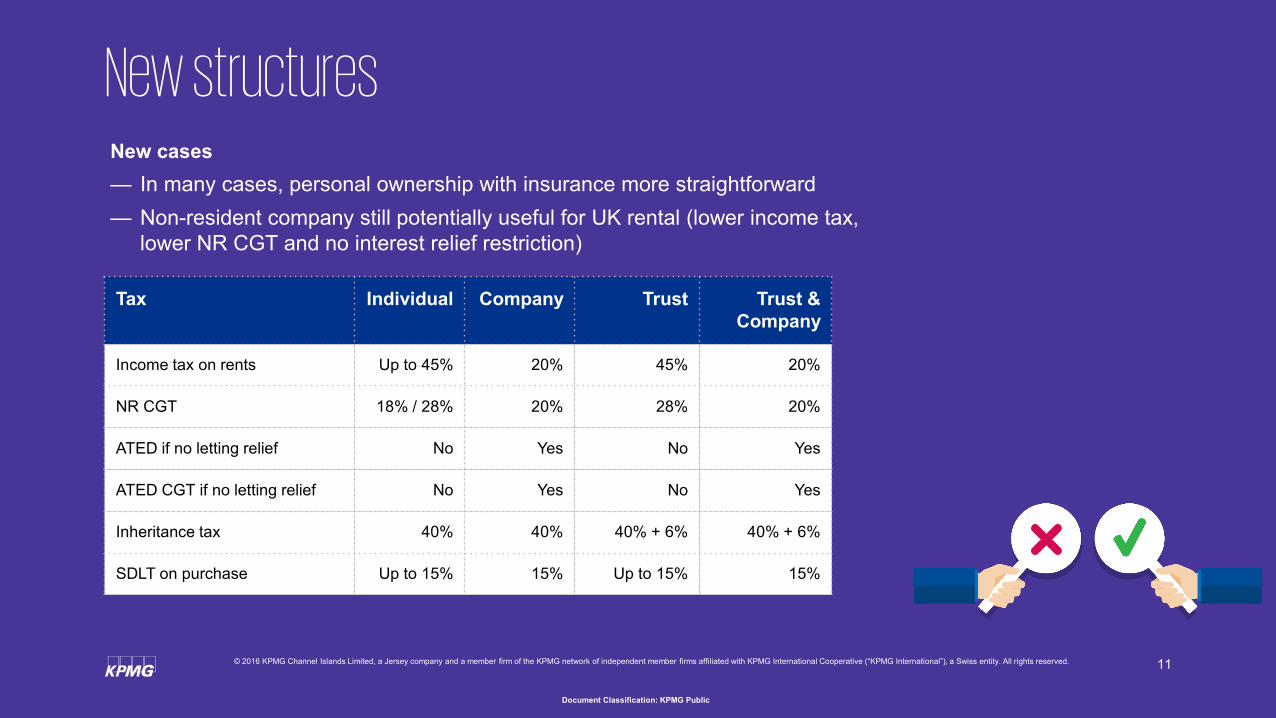

New structures

Tax Individual Company Trust Trust & Company

Income tax on rents Up to 45% 20% 45% 20%

NR CGT 18% / 28% 20% 28% 20%

ATED if no letting relief No Yes No Yes

ATED CGT if no letting relief No Yes No Yes

Inheritance tax 40% 40% 40% + 6% 40% + 6%

SDLT on purchase Up to 15% 15% Up to 15% 15%

New cases— In many cases, personal ownership with insurance more straightforward— Non-resident company still potentially useful for UK rental (lower income tax,

lower NR CGT and no interest relief restriction)

Long term UK residents

Greg Limb and Anna Warren

December 7, 2016

13

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

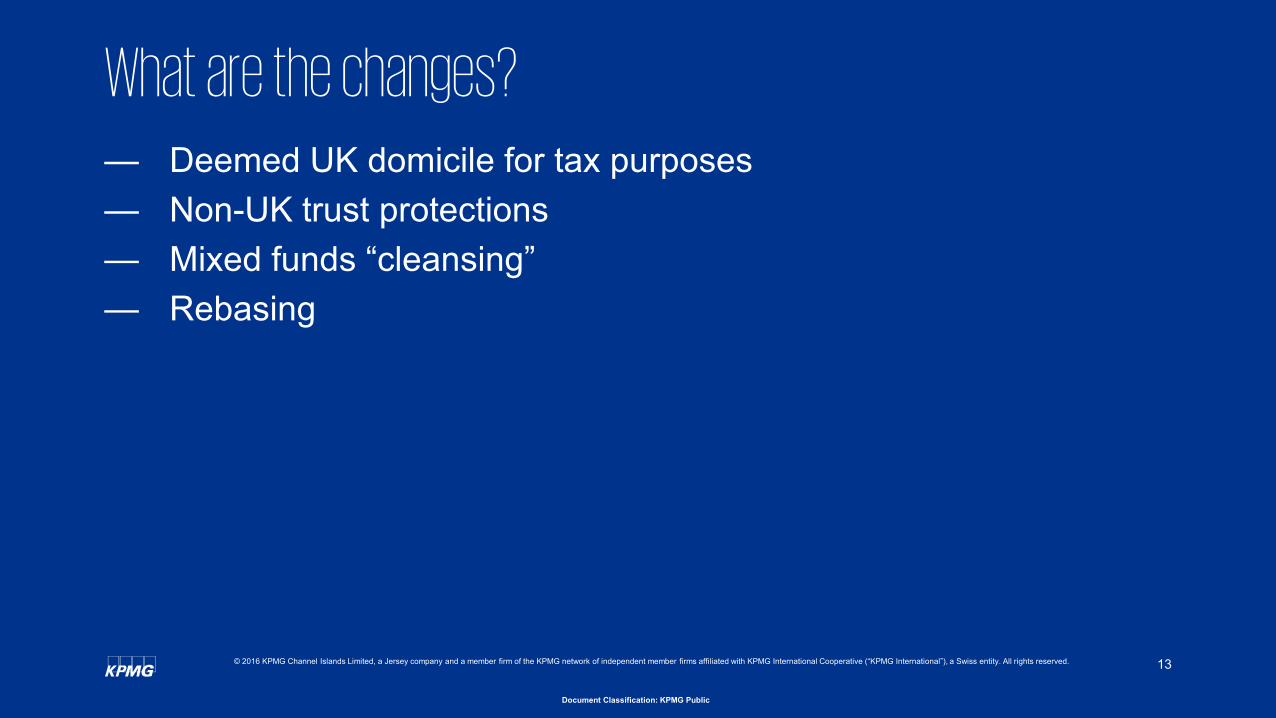

What are the changes?— Deemed UK domicile for tax purposes— Non-UK trust protections— Mixed funds “cleansing”— Rebasing

Deemed domicile

15

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

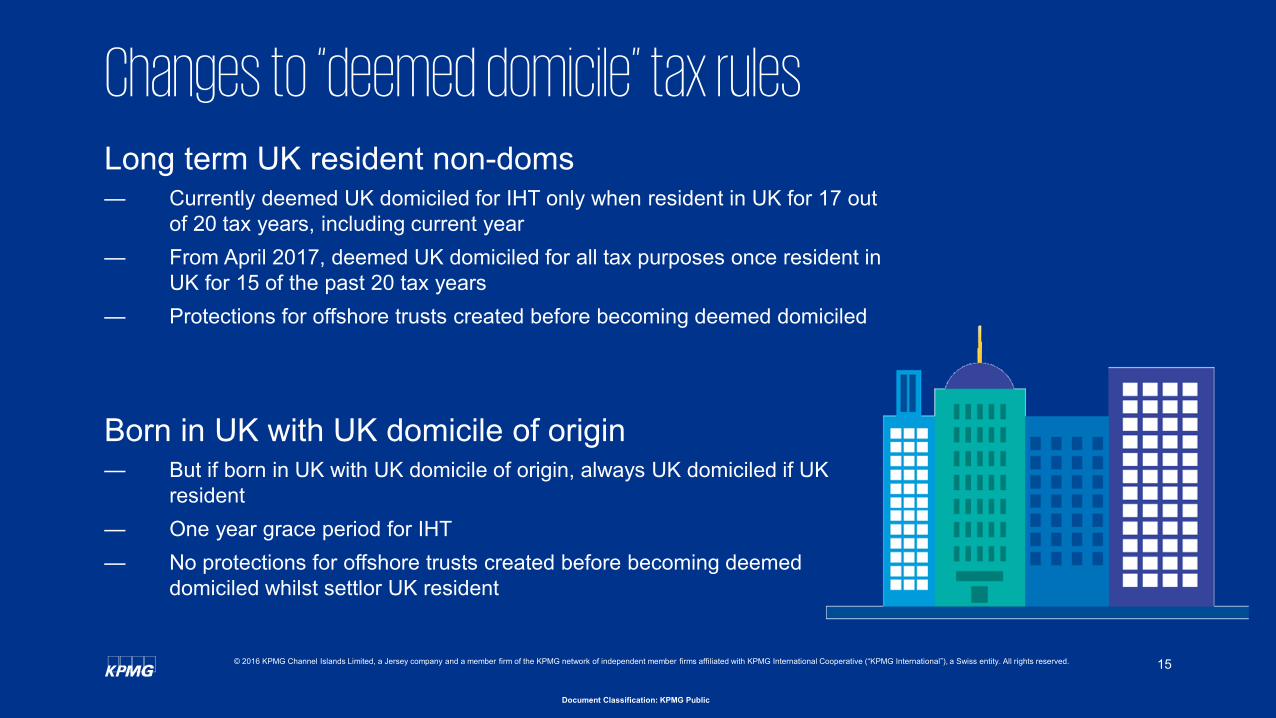

Changes to “deemed domicile” tax rulesLong term UK resident non-doms— Currently deemed UK domiciled for IHT only when resident in UK for 17 out

of 20 tax years, including current year— From April 2017, deemed UK domiciled for all tax purposes once resident in

UK for 15 of the past 20 tax years — Protections for offshore trusts created before becoming deemed domiciled

Born in UK with UK domicile of origin— But if born in UK with UK domicile of origin, always UK domiciled if UK

resident— One year grace period for IHT— No protections for offshore trusts created before becoming deemed

domiciled whilst settlor UK resident

Non-UK trusts

17

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

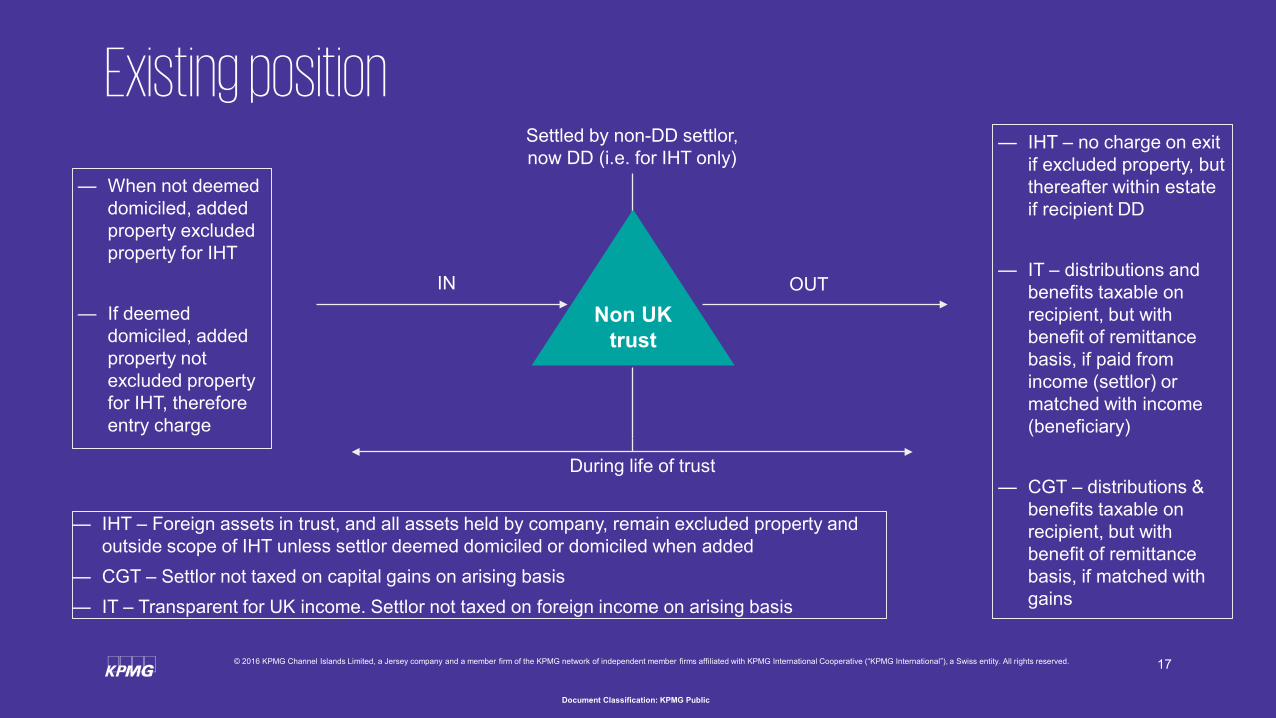

Existing position

— IHT – Foreign assets in trust, and all assets held by company, remain excluded property and outside scope of IHT unless settlor deemed domiciled or domiciled when added

— CGT – Settlor not taxed on capital gains on arising basis— IT – Transparent for UK income. Settlor not taxed on foreign income on arising basis

IN

During life of trust

Settled by non-DD settlor, now DD (i.e. for IHT only)

OUT

Non UK trust

— When not deemed domiciled, added property excluded property for IHT

— If deemed domiciled, added property not excluded property for IHT, therefore entry charge

— IHT – no charge on exit if excluded property, but thereafter within estate if recipient DD

— IT – distributions and benefits taxable on recipient, but with benefit of remittance basis, if paid from income (settlor) or matched with income (beneficiary)

— CGT – distributions & benefits taxable on recipient, but with benefit of remittance basis, if matched with gains

18

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Draft provisions per Finance Bill 2017— Tainting – trust

protections lost if property added to protected trust when deemed domiciled (exceptions for arm’s length transactions, pre 5/4/2017 liabilities & expense deficits)

— New trusts will not benefit from protections

— IHT – Foreign assets in trust and all assets in company remain excluded property and outside scope of IHT (except UK residential property), unless settlor deemed domiciled or domiciled when added

— CGT / IT – Settlor not taxable on capital gains or on foreign income on arising basis, unless protections lost due to addition. Transparent for UK income

— CGT / IT – distributions / benefits* to UK resident settlor matched with income / gains and then taxable on settlor, with no remittance basis if deemed domiciled

— CGT / IT – distributions / benefits* to close family (spouse & minor children) matched with income / gains and then taxable on UK resident settlor, if not already taxed on recipient, with no remittance basis if settlor deemed domiciled

— *Benefits – valued at cost x ORI less amount paid. Interest free & interest bearing loans at ORI less amount paid

— CGT – no cleansing of stockpiled gains to NR beneficiary after 5/4/2017 (regardless of settlor’s domicile)

— Recycling - capital payment to non-resident / non-close family member taxable on UK beneficiary if given / lent to them within 3 years

IN OUT

During life of trust

Settled by non-DD settlor, now DD (i.e. for IHT, CGT & IT)

Non UK trust

DANGER! SUBJECT TO CHANGE & INCOME TAX RULES NOT YET PUBLISHED

Cleansing Mixed Funds

20

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Mixed Funds— Two year window to ‘turn back the clock’ and separate cash ‘mixed funds’

into component parts.

— Only applies to “money” – assets must be liquidated

— Applies to all resident non-doms not just those becoming deemed domiciled on 6 April 2017

— Not available to “returning non-doms”

— Must have claimed remittance basis for tax year before 2017/18.

— Must be able to identify the composition of the mixed fund.

— Huge opportunity to review accounts for all Non-dom clients.

Rebasing

22

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Deemed domon 6 April 2017

Foreign assets

at a gain

Paid the RBC

Rebasing - Who does it apply to?Individuals who:

?

23

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Rebasing - Who won’t qualify?Individuals:

- Not UK deemed dom at 6 April 2017

- Born in the UK with a UK dom of origin

- Never paid the RBC

- Automatically qualify for the remittance basis

Trustees

Partnerships

Companies

24

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What does it apply to?What’s in

Non-UK situs assets giving rise to capital gains, e.g.:

- Land

- Shares and securities

- Share for share exchanges if both the original and new shares were non-UK situs during period 16 March 2016 to 5 April 2017

What’s out

Assets already in the UK

Assets situated in the UK at any time from 16 March 2016 to 5 April 2017.

Trust assets

Partnership assets

Income based assets

- Bonds

- Offshore funds

- Deeply discounted securities

Wasting assets

25

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

How will it work?

HMRC’s approach to offshore

Derek ScottHead of Tax Investigations—

27

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Key messages

• Step change in approach by HMRC

• Tax Amnesties are no more….

• Final chance to take corrective action is now

• Thereafter significant new sanctions- civil and criminal

• Impacts taxpayers and enablers

• Underpinned by AEOI/CRS

28

Document Classification: KPMG Public

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What tax authorities want, in a word, is…

INFORMATION

29

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Requirement to Correct (RTC)— Will apply to all offshore tax non-compliance issues that exist up to and including 5

April 2017

— Wider than tax evasion - all non compliance

— Taxpayers will have until 30 September 2018 to make any correction required

— Includes offshore trustees

— IT/CGT/IHT

— HMRC expect people to review their affairs and take advice if necessary

30

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Requirement to Correct (RTC)— Covers any taxpayers that have a UK tax liability that relates wholly or in part to an

offshore issue, meaning:

- Income arising from a source in a territory outside the UK

- Assets situated or held in a territory outside the UK

- Activities carried on wholly or mainly in a territory outside the UK, or

- Anything having effect as if it were income, assets or activities of a kind described above

— Or, where funds connected to a tax loss are received in a territory outside the UK or are transferred to a territory outside the UK.

31

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Requirement to Correct (RTC)— Significant new set of sanctions for ‘Failure to Correct (FTC):

- Penalties of 100% to 200% of the tax not corrected, and

- Penalties up to 10% of the value of the relevant asset in the most serious cases and involved over £25,000 tax in any tax year, and

- A 50% additional penalty for seeking to avoid RTC via asset moves, and

- ‘Naming and shaming’ in the most serious cases and where over £25,000 in total

— Only defence for FTC is someone had a reasonable excuse not to correct

— 100-200%? penalties are reduced to reflect co-operation and whether prompted/unprompted

32

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Example – Requirement to Correct Mr X has undeclared income from an overseas investment portfolio with value of £7 million that has not been reported on his tax return for the last six years. This has equated to tax owing of approximately £100,000 per annum over 6 years.

— Tax due £600k— Provided that the error was careless

and was an unprompted voluntarily disclosed, no penalties will be due

Current Regime

— Mr X will still owe the £600,000 of tax

— Mr X will also have additional penalties of 100% (min) of tax due – £600,000

— Additional penalties of 10% of the underlying asset? – £700,000

— Naming and shaming?

Failure to Correct Regime

33

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Worldwide Disclosure Facility (WDF)— Opened 5 September 2016

— Disclose UK tax liabilities that relates wholly or partly to an offshore issue

— No immunity from prosecution

— No beneficial financial terms- but lower penalties/sanctions compared to those who are later discovered

— Two stage process –(1) Notification, (2) Complete disclosure & pay tax, interest and penalties within 90 days

— Complex matters?- procedure to engage with HMRC to discuss

— Need to consider alternative disclosure options- eg Contractual Disclosure Facility (COP 9)

34

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Autumn statement 2016Tackling offshore tax evasion: a requirement to notify HMRC of offshore structures Consultation on a new legal requirement for intermediaries arranging complex structures for clients holding money offshore to notify HMRC of the structures and the related client lists.

Consultation period runs to 27 February 2017

35

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Broader transparency issues

Circa 50 countries to exchange details of beneficial ownership of trusts and companies

Multi agency task force – Panama papers

Corporate Criminal Charge - Failure to prevent the criminal facilitation of tax evasion (to be introduced September 2017)

36

Document Classification: KPMG Public

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Client action & summing up - RTC

Income and assets all declared- no further action required

Income and/or assets knowingly undeclared – take advice to disclose now

Client thinks everything is ok – is it? RTC is a step change and consequences if no correction made when needed are significant

Unless client has absolute certainty tax advice to gain reassurance is strongly recommended

RTC extends to non residents (e.g. overseas trustees) with UK tax reporting obligations

Document Classification: KPMG Public

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2016 KPMG Channel Islands Limited, a Jersey company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Derek ScottPartner, KPMG LondonTel: +4420 [email protected]

Greg LimbPartner, KPMG LondonTel: +4420 [email protected]

Anna WarrenManager, KPMG LondonTel: +4420 [email protected]

Jason LaityChairman, KPMG Channel Islands LimitedTel: +441534 [email protected]