william p. mako and chunlin zhang world bank office

TRANSCRIPT

Management of China’s State-Owned Enterprises Portfolio: Lessons from International Experience

William P. Mako and Chunlin Zhang World Bank Office, Beijing

September3, 2003

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

Executive Summary Analysis of China’s portfolio of 174,000 state-owned enterprises (as of end-2001) reveals a clear split. China has some reasonably profitable large SOEs, many of which are centrally administered and/or publicly listed – including some on the Hong Kong and New York stock exchanges. But just over half of China’s SOEs are loss-making. The great majority of loss-makers are small/medium SOEs. Locally-administered SOEs pose significant risks of a “localization of benefits” (e.g., wages) and a “nationalization of liabilities” (e.g., additional bank re-capitalization requirements for non-performing loans, un-funded pension liabilities). Thus, China’s SOE portfolio poses two issues for the management of State capital. First, what should be done with the cash generated through dividends or proceeds from the sale of relatively good SOEs? Second, what should be done to contain operating losses and the creation of new liabilities from China’s many bad SOEs? A modern capital management system. The preservation and enhancement of State capital will require implementation of a “modern capital management system” through (a) more widespread accounting and auditing reforms; (b) a segmented approach to the management of SOE portfolios; (c) a systematic approach to SOE dividend policy and capital re- investment; (d) central/local agreement on sharing of proceeds and curtailment of liabilities; and (e) enhanced risk management: (a) Accounting standards now applied to listed companies and foreign- invested enterprises should also be applied to all medium/large SOEs. It would be useful for all large SOEs to experience the discipline of a public share offering (including the accounting standards, public disclosure, controls on related party transactions, and independent directors) – even including large SOEs that are not suitable for a public share offering. There should be a regular accounting for the central State Assets Supervision and Administration Commission (SASAC) portfolio and the portfolio of each local SASAC. Financial reporting for each SASAC portfolio should similarly reflect international accounting standards, with due consideration for unique Chinese circumstances. Improved management information systems should enable SASAC portfolio managers to focus on key portfolio performance measures. Given the “public” nature of SOEs, including those that are not publicly- listed on stock exchanges, it would be appropriate to increase the transparency of all large SOEs and SASAC portfolios – e.g., by requiring quarterly and annual financial statements and making these available to the public. (b) It would also be useful for the central SASAC to develop guidelines for segmenting SOE portfolios and managing portfolio segments accordingly. Likely portfolio segments include the following: • Small/medium SOEs ready for near-term ownership transformation; • Medium/large SOEs in need of operational and/or financial restructuring; • Medium/large SOEs whose business is non-viable, which should be liquidated; and • Reasonably healthy large SOEs suitable for “normal” corporate governance.

ii

Accurate cash flow reporting and projections are the starting point for assessing restructuring options. In turn, higher-quality accounting information is needed to provide accurate cash flow reports and projections. (c ) Large SOEs should each have a formal dividend policy based on a realistic assessment of alternative uses of surplus cash. Cash surpluses on which management cannot expect to earn an adequate risk-adjusted return through reinvestment should be distributed to company shareholders, either through regular dividends or a 1-time dividend. SOE management and boards should avoid ill-considered diversification (“diworseification”). (d) Proceeds from SOE ownership transformation (e.g., sales) should be used to fund pension liabilities or reduce State debts instead ongoing operating expenses. Central institutions – especially the central SASAC, Ministry of Finance (MOF), large banks, China Banking Regulatory Commission, and National Social Security Fund (NSSF) – should liaise with local counterparts on how to control “localization of benefits-nationalization of liabilities.” Current concerns about avoiding “loss of assets” should be complemented with concerns about avoiding additional accretions of liabilities. (e) Large SOEs that remain in SASAC portfolios should each implement an appropriate risk management program. “Hard budget constraints,” from adequate systems for creditor right/insolvency and supervision of financial institutions, are needed to support governance at large SOEs and at small/medium enterprises that undergo ownership transformation. Ownership transformation. The most basic issue is whether China should follow an “open” or “closed” approach to SOE ownership transformation. Over the past decade, except for 1000 or so initial public offerings (IPOs) and foreign- invested joint ventures, ownership transformation has largely proceed through the closed process of management buy-outs (MBOs) or management-employee buy-outs (MEBOs). Apart from offering greater speed and flexibility, closed processes may forestall political debates on the merits of ownership transformation. But worldwide experience conclusively demonstrates the great advantages – both to the State shareholder/seller and individual enterprises – from an open process. Additional empirical work in China to examine this issue would be useful. It is useful to think about ownership transformation in terms of discrete stages: (a) goals and policies; (b) institutional framework; (c) preparations for sale; (d) conduct of sale; and (e) after-sale: (a) The goals of ownership transformation should be to maximize sales proceeds and to create the most favorable possible conditions for the future development of former SOEs. Outsiders should have an equal opportunity to compete with insiders to purchase enterprises. It is clear from international experience that outside owners are likely to be more effective in post-sale restructuring and in improving enterprise productivity and profitability. The ownership transformation process should be as open as possible, for

iii

example, through an emphasis on open auctions or open tenders. Open processes are needed to encourage bids from outsiders (who may well be more-qualified buyers), to maximize sales proceeds, and to provide needed transparency. (b) Transparency and centralized decision-making are essential. Transparency is needed to maintain public support for ownership transformation and to forestall future allegations of corruption. Necessary transparency results from publication of clear and comprehensive rules and procedures to govern enterprise sales; publicity on upcoming sales; dissemination of reliable information on enterprises; a competitive sales process (e.g., public auction, tender, or share offering); equal treatment of domestic and foreign investors; rules on real or potential conflicts of interest; publication of enterprise sales results; and oversight by an appropriate public entity. At least for large or complex sales, use of an outside financial advisor should enhance transparency and sale results. SASACs should have wide discretion to organize and conclude ownership transformations, subject to higher- level approval only for particularly large or important transactions and to post-transaction reviews. (c ) The pre-sale restructuring of SOEs should be minimized. Elaborate calculations of the “going concern” value of medium-sized SOEs are a waste of time and effort. A book value valuation, so long as it includes the value of any real estate (e.g., land use rights), is an adequate reference point for auctions or tender negotiations. An SOE is worth only what a ready and willing buyer will pay for it. Thus, rather than focusing beforehand on calculations of “enterprise value,” SASACs should instead focus on procedures (e.g., bidder access to enterprise information, warranties or indemnifications to manage risks to the buyer, advertising) to maximize competition among potential buyers and minimize their potential uncertainty. This is the most practical approach to maximizing sales proceeds and attracting the most qualified buyers. (d ) The sales method used in each ownership transformation should suit the characteristics and needs of each particular SOE: • The sale of small SOEs and their valuation should focus on the transfer of real estate

or access to real estate (e.g., land use rights, leaseholds). Adding other assets (e.g., inventory, fixtures) and liabilities (e.g., debt) to the transaction needlessly complicates the sale of small SOEs. If at all possible, small SOEs should be sold simply for the highest price through a public auction. From our analysis, it is clear that small/medium SOEs do not belong in China’s SOE portfolio. Small/medium SOEs tend to be loss-makers; to diminish rather than enhance State capital; and to cumulatively pose significant liability risks. Full and rapid implementation of the 1999 4th Plenum Decision to “let go” small and medium SOEs and “grasp” the large makes more sense than ever. This, however, will precipitate a huge number of transactions. Hence, an efficient sales program for small/medium SOEs will be especially important.

• Liquidation of small SOEs as well as medium-sized SOEs that are insolvent or difficult-to-audit, through asset sale and separate settlement of claims, can be an extremely efficient method for ownership transformation.

iv

• For the great majority of medium/large SOEs, a “trade sale” to a dominant shareholder (e.g., strategic investor) should be the preferred method for ownership transformation.

• Except in a few select cases, initial public offerings (IPOs) will not be worth the additional time, effort, expense, and risk to public shareholders. The use of IPOs should be limited to large, well-known, and well-run SOEs, whose public offering would contribute to capital market development and where protections for minority shareholders are adequate.

• Closed processes such as MBOs/MEBOs should be avoided, except perhaps in the case of small SOEs that are particularly dependent on the scientific/technical skills of enterprise staff. If an MBO/MEBO is used, insiders should be required to pay something for their shares – albeit perhaps at some discount to market value.

• Mixed sales, such as a trade sale plus an IPO, are a good way to combine the best features of different methods. For practical reasons (e.g., cost, complexity), however, mixed sales should be limited to medium/large SOEs able to attract strategic (e.g., foreign) investors.

(e) Appropriate post-sale conditions are essential to accomplish the main goals of maximizing sales proceeds and promoting future development of former SOEs: • Post-sale restrictions on the SOE or SOE buyer (e.g., on line of business, enterprise

re-sale, worker layoffs) should be avoided, since these are unlikely to achieve any lasting effect – other than reducing sales proceeds.

• Similarly, post-sale commitments by the buyer (e.g., on capital investment, technology transfer) can be difficult and expensive for the State seller to monitor and enforce. A higher sales price is preferable to equivalent post-sale commitments by the buyer.

• Government regulations and incentives to deal with SOE environmental damage should be clear and predictable.

• SASACs should not insist on retaining residual shares, especially in the case of a trade sale.

• “Golden shares” – which may convey special powers to approve or veto such major initiatives as enterprise re-sale to a third party, sale of major assets, liquidation, or reorganization – should be used as infrequently as possible. Any golden share powers should be narrowly-defined, time- limited, and usable only under clearly-specified circumstances.

• Because a lack of wealth or access to financing will constrain many domestic buyers, at least for medium-sized SOEs, SASACs will continue to need to be prepared to agree to purchase financing through installment payments. Installment payments, however, should be carefully monitored. In cases where buyers fall behind on installment payments, it may make sense for SASACs to “outsource” resolution of the problem by selling delinquent balances to private investors or hiring commercial collection agents.

• The successful post-sale development of former SOEs will require complementary policies in a wide range of areas, including the liberalization of new business entry, macroeconomic stabilization, trade liberalization, creditor rights, banking reform, and business law reform.

v

• Finally, the clarification and protection of private property rights is essential. Past ownership transformations – even those resulting from questionable, non-transparent processes – should be respected. No enterprise owner should ever be divested or driven out of business – including for environmental, health, or safety reasons – by the government without “due process” according to clear and well-established rules, standards, and procedures.

Institutional capacity. The quality of its SOE portfolio will determine institutional requirements for each SASAC. Centrally-administered SOEs are more profitable, less indebted, and less likely to be in distress than locally-administered SOEs. Hence, the central SASAC as well as local SASACs with higher-quality portfolios (e.g., Beijing, Shanghai) will be able to focus more on maximizing returns on SOE equity and the exercise of normal corporate governance. Core activities at such SASACs should include the monitoring of SOE business planning and performance; participation in annual and extraordinary shareholder meetings; development of SOE boards of directors; and the appointment of SOE directors. Periodically, these SASACs can also be expected to organize share sales in large SOEs. The central SASAC should also be prepared to liaise with local SASACs as well as national institutions to control liabilities growth among locally-administered SOEs. Among large and stable SOEs, their boards will be able to focus on director nominations, board committee structure, and procedures to enhance board oversight of SOE management. Management of such SOEs will be able, in turn, to focus on business plans, investments, and operations to maximize returns on State capital. Based on a portfolio of 196 SOEs, the central SASAC may need 40-100 staff to monitor these SOEs and a cadre of 200-300 individuals to serve as independent non-executive directors.1 To reinforce the distinction between administrative power and shareholder rights, civil servants should not be appointed as SOE directors. Establishment of a Directors Training Institute and directors accreditation program should facilitate the adoption of international best practices by directors at SASAC portfolio companies. At the majority of local SASACs, there will be a much greater need for skills in organizing small/medium SOE sales and in restructuring or liquidating distressed or non-viable SOEs. As the nominal owner of these distressed SOEs, local SASACs should also be prepared to negotiate agreements with SOE workers, suppliers, financial institution creditors, and social insurance programs on loss-sharing. Local SASACs will need some training and institutional development in these “special situation” topics as well as in traditional corporate governance tasks. Since the great bulk of small/medium SOE sales, liquidations, and restructuring should occur over the next five years, local SASACs should seek to “outsource” SOE sale, restructuring, and liquidation functions as much as possible – instead of building in-house staff to perform temporary functions.

1 This assumes that each SASAC staff could monitor 2-5 portfolio companies. It is further assumed that each SOE board will average 7 members, including 3 independent directors, and that each independent director could serve on average on 2-3 SOE boards. Rules to prevent conflicts of interest would be needed.

vi

Market-based working conditions (including compensation) and performance monitoring will be important to attract appropriately-qualified individuals to serve as SASAC staff or SOE directors and to motivate superior performance. Thus, this background note focuses on China’s current SOE portfolio, development of “a modern capital management system,” and SOE ownership transformation. A previous background note looked at state asset management reform and steps to enhance corporate governance at large SOEs.2 A future background note will consider issues and recommendations for enterprise restructuring.

2 William P. Mako and Chunlin Zhang, Exercising Ownership Rights in State-Owned Enterprise Groups: What China Can Learn from International Experience , December 2002.

1

I. Introduction This background note builds upon the World Bank’s previous background note Exercising Ownership Rights in State-Owned Enterprise Groups: What China Can Learn for International Experience. That background note broadly considered the issues of state asset management reform. It identified needs to consolidate the State’s ownership rights and responsibilities in SOE Ownership Agencies, to focus on the efficient use of state capital, to “let go” small and medium SOEs in order to focus better on governance of large SOEs, to organize new Ownership Agencies according to market principals, to pay more attention to risk management, to create or strengthen SOE boards of directors and rely on these for governing large SOEs, and to transform 2nd tier shareholders (especially enterprise group parent companies) so that they can play an effective role in governance. Decisions at the 16th CPC Congress in November 2002 and the 10th National People’s Congress in March 2003 to enable the central and local governments to exercise the rights of shareholders and to establish a central State-owned Assets Supervision and Administration Commission (SASAC) and local counterparts may profoundly enhance state assets management in China. Success will depend, however, on appropriate organization and operation of the SASACs; adequate controls over the use of State capital; market-based ownership transformation; resolution of distressed SOEs; and effective governance of large SOEs remaining in the State portfolio. This background paper does not delve into linkages among SOE restructuring, financial sector restructuring, social safety nets, and fiscal sustainability. These linkages are important. For example, the resolution of non-sustainable debt at many SOEs is likely to diminish the capital of state-owned commercial banks. On this issue, there has not been sufficient access to data or demand from the authorities to warrant a closer examination of enterprise-financial sector linkages. Neither does this paper consider regulated infrastructure (e.g., power, telecoms). The focus is on manufacturing and service enterprises in the “tradeables” sector. The previous background paper provided detailed recommendations on such corporate governance topics as the normal exercise of shareholder rights; selection of directors; organization and working procedures for SOE boards of directors; and typical working relations between shareholders and boards and between boards and management. Hence, this background paper is organized as follows: Section II assesses China’s current SOE portfolio; Section III highlights key issues in the management of State capital; and Section IV compares China’s ownership transformation experience with international experience and draws lessons for China. A future background paper will examine SOE restructuring.

2

II. China’s Current Portfolio of State Owned Enterprises (SOEs)

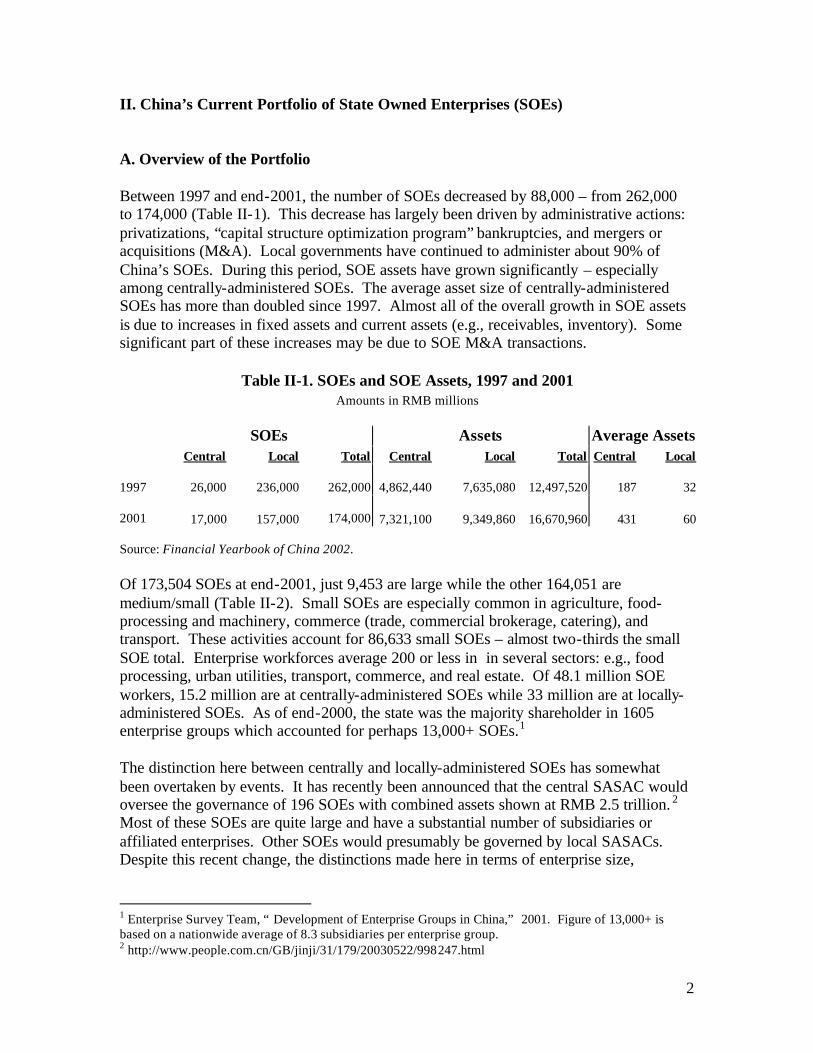

A. Overview of the Portfolio Between 1997 and end-2001, the number of SOEs decreased by 88,000 – from 262,000 to 174,000 (Table II-1). This decrease has largely been driven by administrative actions: privatizations, “capital structure optimization program” bankruptcies, and mergers or acquisitions (M&A). Local governments have continued to administer about 90% of China’s SOEs. During this period, SOE assets have grown significantly – especially among centrally-administered SOEs. The average asset size of centrally-administered SOEs has more than doubled since 1997. Almost all of the overall growth in SOE assets is due to increases in fixed assets and current assets (e.g., receivables, inventory). Some significant part of these increases may be due to SOE M&A transactions.

Table II-1. SOEs and SOE Assets, 1997 and 2001 Amounts in RMB millions

SOEs Assets Average Assets Central Local Total Central Local Total Central Local

1997

26,000 236,000 262,000 4,862,440 7,635,080

12,497,520 187 32

2001

17,000 157,000 174,000 7,321,100 9,349,860

16,670,960 431 60 Source: Financial Yearbook of China 2002. Of 173,504 SOEs at end-2001, just 9,453 are large while the other 164,051 are medium/small (Table II-2). Small SOEs are especially common in agriculture, food-processing and machinery, commerce (trade, commercial brokerage, catering), and transport. These activities account for 86,633 small SOEs – almost two-thirds the small SOE total. Enterprise workforces average 200 or less in in several sectors: e.g., food processing, urban utilities, transport, commerce, and real estate. Of 48.1 million SOE workers, 15.2 million are at centrally-administered SOEs while 33 million are at locally-administered SOEs. As of end-2000, the state was the majority shareholder in 1605 enterprise groups which accounted for perhaps 13,000+ SOEs.1 The distinction here between centrally and locally-administered SOEs has somewhat been overtaken by events. It has recently been announced that the central SASAC would oversee the governance of 196 SOEs with combined assets shown at RMB 2.5 trillion. 2 Most of these SOEs are quite large and have a substantial number of subsidiaries or affiliated enterprises. Other SOEs would presumably be governed by local SASACs. Despite this recent change, the distinctions made here in terms of enterprise size,

1 Enterprise Survey Team, “Development of Enterprise Groups in China,” 2001. Figure of 13,000+ is based on a nationwide average of 8.3 subsidiaries per enterprise group. 2 http://www.people.com.cn/GB/jinji/31/179/20030522/998247.html

3

performance and financial strength – as well as the implications for portfolio management – remain valid.

Table II- 2. SOE Size, Workers, and Administration by Sector, 2001 Enterprises Workers (000s) Large Medium Small Total Central Local Total Average Workers Agriculture 264 1,136 9,066 10,466 1,663 3,163 4,826 0.46Industry: Coal 206 335 1,067 1,608 104 3,219 3,323 2.07 Petroleum 36 23 35 94 1,056 21 1,077 11.46 Metallurgy 362 563 815 1,740 553 2,347 2,900 1.67 Building materials 249 708 1,992 2,949 60 1,005 1,065 0.36 Chemicals 601 1,135 2,345 4,081 190 1,837 2,027 0.50 Forestry 70 102 554 726 36 483 519 0.71 Food 241 859 5,289 6,389 32 783 815 0.13 Tobacco 48 72 57 177 203 22 225 1.27 Textiles 442 821 1,203 2,466 122 1,641 1,763 0.71 Petrochemicals 65 39 62 166 546 100 646 3.89 Medical 188 323 599 1,110 49 440 489 0.44 Machinery 1,211 2,525 6,409 10,145 1,081 3,167 4,248 0.42 Military 284 184 226 694 922 54 976 1.41 Electronics 289 444 921 1,654 146 445 591 0.36 Powe r 208 658 1,705 2,571 1,132 893 2,025 0.79 Urban utilities 107 285 1,857 2,249 7 484 491 0.22

Other 436 1,055 4,298 5,789 130 1,452 1,582 0.27 5,043 10,131 29,434 44,608 6,369 18,393 24,762 Construction 775 1,418 3,355 5,548 1,381 2,163 3,544 0.64Geo/Water 65 195 1,551 1,811 158 137 295 0.16Transport 843 2,849 21,759 25,451 3,013 2,652 5,665 0.22Communications 129 35 117 281 1,304 60 1,364 4.85Commerce 1,274 7,454 44,110 52,838 751 3,690 4,441 0.08Real estate 215 1,312 4,570 6,097 25 316 341 0.06Social services 303 1,553 9,945 11,801 149 1,459 1,608 0.14Health/welfare 1 14 242 257 3 12 15 0.06Education etc 42 230 3,866 4,138 41 235 276 0.07Scientific 97 178 2,485 2,760 148 90 238 0.09

Other 402 1,022 6,024 7,448 217 588 805 0.11Total 9,453 27,527 136,524 173,504 15,222 32,958 48,180 Source: Financial Yearbook of China 2002. Data on SOE financial performance and position present significant methodological issues (see Section III.A). However, it appears that SOE profitability has increased since 1998-1999. Net profitability has roughly doubled to 3.7% and the proportion of loss-making SOEs has been reduced from about two-thirds to about half (Table II-3).

4

Economic growth, debt/equity conversions by AMCs, and other decreases in interest expense have presumably contributed to improved profitability. But SOE privatizations, mergers, and bankruptcies may have been more important. Notably, the 84,000 decrease in loss-making SOEs since 1997 almost equals the 88,000 decrease in total SOEs. However, 51% of SOEs were still loss-making in 2001. For 2001, China’s SOEs showed RMB 281 billion in overall profit, with profitable SOEs contributing RMB 480 billion and loss-making SOEs destroying RMB 199 billion in value. In addition, a high and increasing level of current assets-to-sales indicates an SOE liquidity problem. Current assets have increased to 313-325 days of sales since 1997. Unless SOEs are maintaining large cash balances, which seems unlikely, this suggests that increasing amounts of working capital are tied up in possibly un-collectible receivables and un-saleable inventory.

Table II-3. SOE Profitability and Liquidity, 1997-2001 Amounts in RMB millions

1997 1998 1999 2000 2001

Sales revenue 6,813,200 6,468,510 6,913,660 7,508,190 7,635,550 SOE profits n.a. 328,020 329,070 467,980 480,470SOE losses n.a. (306,650) (214,490) (184,600) (199,360)Net profit 79,120 21,370 114,580 283,380 281,120 Net profitability 1.2% 0.3% 1.7% 3.7% 3.7% Percentage loss-making 65.9% 68.7% 53.5% 50.7% 51.2%Profitable SOEs 89,000 74,000 101,000 94,000 85,000Loss-making SOEs 173,000 164,000 116,000 97,000 89,000Total SOEs 262,000 238,000 217,000 191,000 174,000 Current assets 5,369,850 5,575,110 5,935,170 6,682,560 6,678,560 Current asset-days 1/ 288 315 313 325 319 Source: Financial Yearbook of China 2002. 1/ Represented as days of sales. SOE profitability varies by locality. In 2001, over 60% of SOEs in Beijing and Shanghai were profitable (Table II- 4). By contrast, over 60% of SOEs were unprofitable in the northeast provinces of Liaoning and Jilin; the central provinces of Anhui, Henan, and Hubei; the southwestern provinces of Guangxi, Hainan, Chongqing, Sichuan, and Yunnan; and the northwestern province of Gansu.

5

Table II-4. Profitability of Locally-Administered SOEs by Region, 2001 (Amounts in RMB 100 million)

Number of Sales Profit Profit- % Loss- Enterprises Revenue ability Making Beijing 4,211 1,915.8 52.9 2.8% 36.1%Tianjin 4,987 1,123.3 10.1 0.9% 49.9%Hebei 7,583 1,732.4 -2.6 -0.2% 42.6%Shanxi 5,872 1,023.6 -3.7 -0.4% 42.1%Inner Mongolia 2,131 559.1 -0.8 -0.1% 44.9%Liaoning 5,462 1,789.7 -39.1 -2.2% 63.0%Jilin 3,325 627.6 -14.4 -2.3% 62.0%Heilongjiang 6,323 705.4 -33.0 -4.7% 53.2%Shanghai 13,398 4,861.8 198.3 4.1% 33.4%Jiangsu 8,108 3,234.4 2.3 0.1% 53.8%Zhejiang 5,393 2,606.1 101.6 3.9% 40.4%Anhui 4,798 1,238.5 16.8 1.4% 64.2%Fujian 5,594 1,202.9 25.3 2.1% 49.3%Jiangxi 4,548 745.2 -5.4 -0.7% 56.3%Shandong 7,807 3,347.4 51.3 1.5% 47.1%Henan 8,289 1,488.5 6.1 0.4% 64.3%Hubei 5,724 1,087.0 -20.0 -1.8% 61.0%Hunan 6,575 1,016.6 -2.7 -0.3% 58.2%Guangdong 11,523 4,922.6 220.7 4.5% 55.3%Guangxi 6,617 739.6 -2.6 -0.4% 62.9%Hainan 1,408 130.9 -0.9 -0.7% 71.5%Chongqing 2,141 565.1 -7.3 -1.3% 66.0%Sichuan 4,781 1,087.5 8.1 0.7% 60.9%Guizhou 3,261 328.8 -0.3 -0.1% 55.0%Yunnan 4,494 761.3 -3.1 -0.4% 60.9%Tibet 531 30.0 -1.7 -5.7% 53.9%Shaanxi 4,757 753.9 -5.9 -0.8% 53.0%Gansu 3,443 436.7 -10.0 -2.3% 62.4%Qinghai 691 86.7 0.6 0.7% 59.2%Ningxia 698 179.7 0.3 0.2% 59.0%Xinjiang 2,063 328.4 -5.8 -1.8% 51.9%Totals 156,536 40,656.5 535.1 1.3% 51.2%

Source: Financial Yearbook of China 2002.

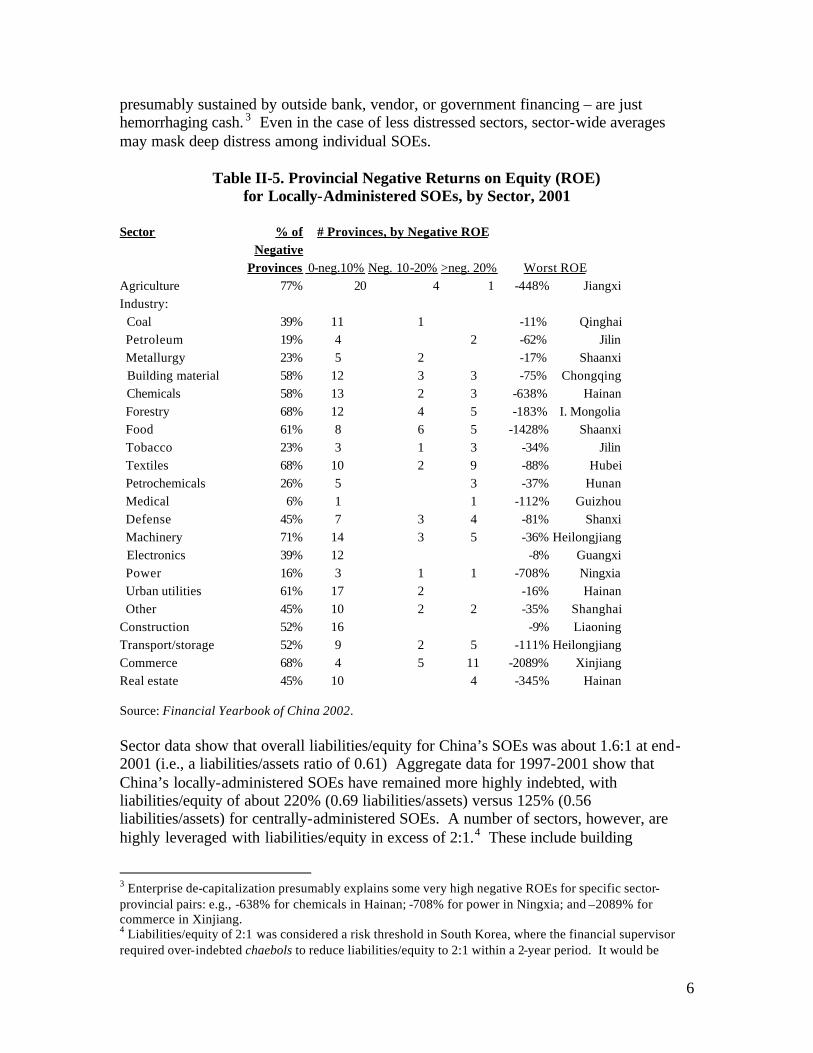

The most-distressed SOE sectors are building materials, chemicals, forestry, food processing, textiles, machinery, urban utilities, construction, transportation/storage, and commerce. In 2001, these sectors showed province-wide losses in more than half of China’s provinces (Table II-5). Returns on equity were worse than negative 20 percent in about 1/3 of China’s provinces in the case of textiles and commerce. In many cases, it appears that SOEs have been de-capitalized as a result of ongoing losses and –

6

presumably sustained by outside bank, vendor, or government financing – are just hemorrhaging cash. 3 Even in the case of less distressed sectors, sector-wide averages may mask deep distress among individual SOEs.

Table II-5. Provincial Negative Returns on Equity (ROE) for Locally-Administered SOEs, by Sector, 2001

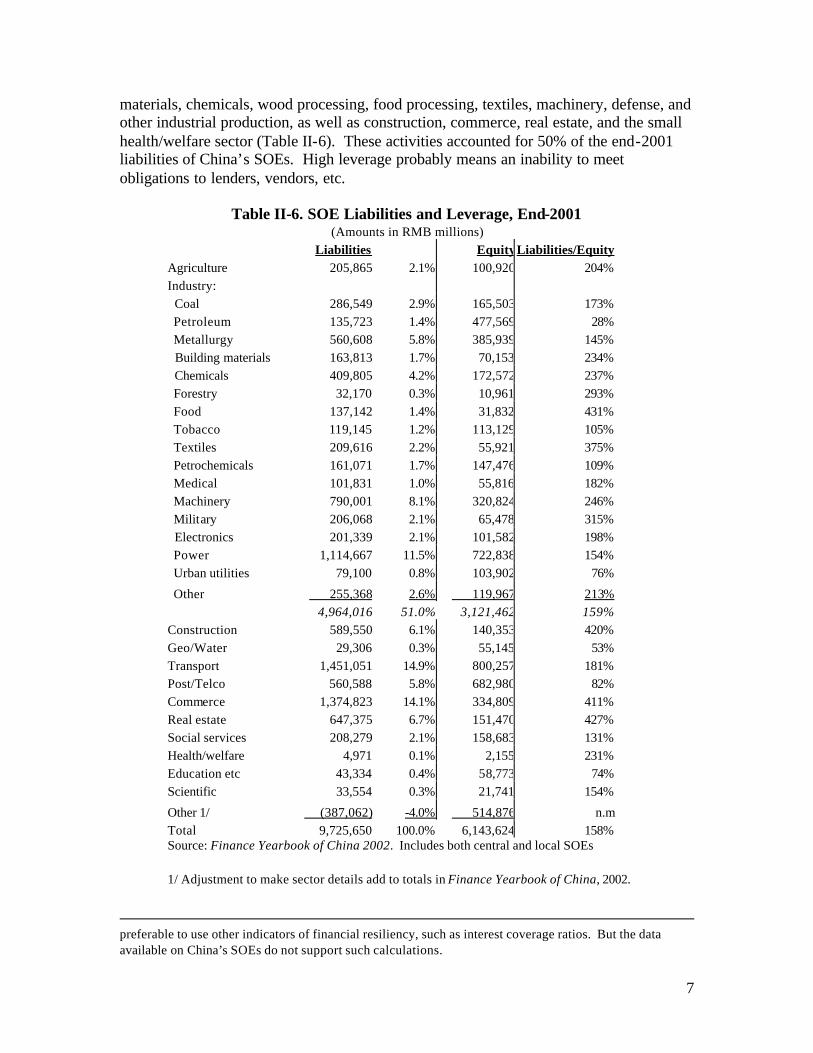

Sector % of # Provinces, by Negative ROE Negative Provinces 0-neg.10% Neg. 10-20% >neg. 20% Worst ROE Agriculture 77% 20 4 1 -448% JiangxiIndustry: Coal 39% 11 1 -11% Qinghai Petroleum 19% 4 2 -62% Jilin Metallurgy 23% 5 2 -17% Shaanxi Building material 58% 12 3 3 -75% Chongqing Chemicals 58% 13 2 3 -638% Hainan Forestry 68% 12 4 5 -183% I. Mongolia Food 61% 8 6 5 -1428% Shaanxi Tobacco 23% 3 1 3 -34% Jilin Textiles 68% 10 2 9 -88% Hubei Petrochemicals 26% 5 3 -37% Hunan Medical 6% 1 1 -112% Guizhou Defense 45% 7 3 4 -81% Shanxi Machinery 71% 14 3 5 -36% Heilongjiang Electronics 39% 12 -8% Guangxi Power 16% 3 1 1 -708% Ningxia Urban utilities 61% 17 2 -16% Hainan Other 45% 10 2 2 -35% ShanghaiConstruction 52% 16 -9% LiaoningTransport/storage 52% 9 2 5 -111% HeilongjiangCommerce 68% 4 5 11 -2089% XinjiangReal estate 45% 10 4 -345% Hainan Source: Financial Yearbook of China 2002. Sector data show that overall liabilities/equity for China’s SOEs was about 1.6:1 at end-2001 (i.e., a liabilities/assets ratio of 0.61) Aggregate data for 1997-2001 show that China’s locally-administered SOEs have remained more highly indebted, with liabilities/equity of about 220% (0.69 liabilities/assets) versus 125% (0.56 liabilities/assets) for centrally-administered SOEs. A number of sectors, however, are highly leveraged with liabilities/equity in excess of 2:1.4 These include building

3 Enterprise de-capitalization presumably explains some very high negative ROEs for specific sector-provincial pairs: e.g., -638% for chemicals in Hainan; -708% for power in Ningxia; and –2089% for commerce in Xinjiang. 4 Liabilities/equity of 2:1 was considered a risk threshold in South Korea, where the financial supervisor required over-indebted chaebols to reduce liabilities/equity to 2:1 within a 2-year period. It would be

7

materials, chemicals, wood processing, food processing, textiles, machinery, defense, and other industrial production, as well as construction, commerce, real estate, and the small health/welfare sector (Table II-6). These activities accounted for 50% of the end-2001 liabilities of China’s SOEs. High leverage probably means an inability to meet obligations to lenders, vendors, etc.

Table II-6. SOE Liabilities and Leverage, End-2001 (Amounts in RMB millions)

Liabilities EquityLiabilities/Equity Agriculture 205,865 2.1% 100,920 204% Industry: Coal 286,549 2.9% 165,503 173% Petroleum 135,723 1.4% 477,569 28% Metallurgy 560,608 5.8% 385,939 145% Building materials 163,813 1.7% 70,153 234% Chemicals 409,805 4.2% 172,572 237% Forestry 32,170 0.3% 10,961 293% Food 137,142 1.4% 31,832 431% Tobacco 119,145 1.2% 113,129 105% Textiles 209,616 2.2% 55,921 375% Petrochemicals 161,071 1.7% 147,476 109% Medical 101,831 1.0% 55,816 182% Machinery 790,001 8.1% 320,824 246% Military 206,068 2.1% 65,478 315% Electronics 201,339 2.1% 101,582 198% Power 1,114,667 11.5% 722,838 154% Urban utilities 79,100 0.8% 103,902 76%

Other 255,368 2.6% 119,967 213% 4,964,016 51.0% 3,121,462 159% Construction 589,550 6.1% 140,353 420% Geo/Water 29,306 0.3% 55,145 53% Transport 1,451,051 14.9% 800,257 181% Post/Telco 560,588 5.8% 682,980 82% Commerce 1,374,823 14.1% 334,809 411% Real estate 647,375 6.7% 151,470 427% Social services 208,279 2.1% 158,683 131% Health/welfare 4,971 0.1% 2,155 231% Education etc 43,334 0.4% 58,773 74% Scientific 33,554 0.3% 21,741 154%

Other 1/ (387,062) -4.0% 514,876 n.m Total 9,725,650 100.0% 6,143,624 158%

Source: Finance Yearbook of China 2002. Includes both central and local SOEs

1/ Adjustment to make sector details add to totals in Finance Yearbook of China, 2002. preferable to use other indicators of financial resiliency, such as interest coverage ratios. But the data available on China’s SOEs do not support such calculations.

8

As noted earlier, a rising ratio of current assets/sales revenue suggests increasing liquidity problems for SOEs. Indeed, there has been an attempt to identify “unhealthy” assets (e.g., outmoded fixed assets, un-collectible receivables, un-saleable inventory). Table II-7 shows estimates of unhealthy assets relative to total assets and equity for locally-administered SOEs as well as the effect write-downs of assets and equity for unhealthy assets would have on liabilities/equity ratios: • Unhealthy assets are minimal (i.e., less than 10% of total assets) in a few locales:

Beijing, Shanghai, Zhejiang, and Fujian. • However, unhealthy assets represent more than 20% of assets in ten provinces:

Liaoning, Jilin, Heilongjiang, Jiangxi, Hubei, Hunan, Guangdong, Chongqing, Shaanxi, and Xingjiang.

• With no adjustment for unhealthy assets, only seven provinces show liabilities/equity worse than 200% (i.e., liabilities/assets worse than 0.67): Jilin, Heilongjiang, Jiangxi, Henan, Hubei, Shaanxi, and Xinjiang.

• With adjustment, all but four provinces (Beijing, Shanghai, Zhejiang, Tibet) show liabilities/equity worse than 300% (i.e., liabilities/assets worse than 0.75).

• Moreover, with adjustment, the SOE sector in five provinces (Jilin, Heilongjiang, Jiangxi, Hubei, and Shaanxi) would be insolvent (i.e., negative equity). In these provinces, liabilities exceed adjusted assets by RMB 90 billion.

• Adjusting for unhealthy assets reduces equity in locally-administered SOEs by more than half, from RMB 2.9 trillion to RMB 1.4 trillion. Overall liabilities/equity go from 252% to 632% (i.e., to 0.86 liabilities/assets).

As serious as these figures are, it is not clear whether there has been adequate accounting for SOE liabilities. For example, if SOE accruals for interest expense and worker pensions have been inadequate, full accounting for these liabilities would further raise liabilities/equity ratios.

9

Table II-7. Effects of “Unhealthy” Assets on

Solvency of Locally-Administered SOEs, 2001 (Amounts in RMB millions)

Unadjusted Adjusted for Unhealthy Assets Locality Assets Liabilities Equity Liabilities/ Unhealthy Assets Equity Liabilities/

Equity Assets/ Equity

Equity

Beijing 556,120 372,800 183,320 203% 22.60% 514,690 141,890 263%Tianjin 320,340 210,060 110,280 190% 44.50% 271,265 61,205 343%Hebei 419,150 308,840 110,310 280% 58.40% 354,729 45,889 673%Shanxi 284,050 203,240 80,810 252% 49.50% 244,049 40,809 498%In. Mongolia 162,860 118,080 44,780 264% 55.00% 138,231 20,151 586%Liaoning 515,890 386,160 129,730 298% 91.00% 397,836 11,676 3307%Jilin 317,890 290,650 27,240 1067% 259.30% 247,257 -43,393 -670%Heilongjiang 317,890 278,010 39,880 697% 187.80% 242,995 -35,015 -794%Shanghai 1,178,510 794,880 383,630 207% 28.40% 1,069,559 274,679 289%Jiangsu 617,520 429,270 188,250 228% 38.30% 545,420 116,150 370%Zhejiang 453,330 279,860 173,470 161% 13.40% 430,085 150,225 186%Anhui 295,090 219,250 75,840 289% 69.30% 242,533 23,283 942%Fujian 262,610 170,920 91,690 186% 27.50% 237,395 66,475 257%Jiangxi 196,350 150,740 45,610 330% 108.30% 146,954 -3,786 -3982%Shandong 674,820 484,400 190,420 254% 43.10% 592,749 108,349 447%Henan 377,900 289,250 88,650 326% 76.10% 310,437 21,187 1365%Hubei 304,530 235,930 68,600 344% 107.50% 230,785 -5,145 -4586%Hunan 259,530 186,610 72,920 256% 78.80% 202,069 15,459 1207%Guangdong 1,108,630 775,220 333,410 233% 42.80% 965,931 190,711 406%Guangxi 216,030 138,490 77,540 179% 55.60% 172,918 34,428 402%Hainan 72,070 52,920 19,150 276% 54.10% 61,710 8,790 602%Chongqing 168,620 124,890 43,730 286% 92.30% 128,257 3,367 3709%Sichuan 297,470 195,780 101,690 193% 49.40% 247,235 51,455 380%Guizhou 120,680 87,470 33,210 263% 57.80% 101,485 14,015 624%Yunnan 203,040 145,340 57,700 252% 45.40% 176,844 31,504 461%Tibet 13,850 6,370 7,480 85% 33.30% 11,359 4,989 128%Shaanxi 212,470 167,260 45,210 370% 104.90% 165,045 -2,215 -7550%Gansu 136,120 93,820 42,300 222% 58.50% 111,375 17,555 534%Qinghai 28,920 21,070 7,850 268% 54.50% 24,642 3,572 590%Ningxia 43,150 30,500 12,650 241% 52.40% 36,521 6,021 507%Xinjiang 81,820 63,640 18,180 350% 94.70% 64,604 964 6605%

Totals 10,217,250 7,311,720 2,905,530 252% 8,686,963 1,375,243 632% Source: Finance Yearbook of China 2002. The foregoing problems notwithstanding, a small top tier of Chinese enterprises has shown strong financial performance as well as reasonable disclosure and governance.

10

For example, Chinese companies with shares listed in Hong Kong generally showed a strong 2001 performance in terms of returns on equity (Table II-8). These companies show adjustments to their Chinese-statutory accounting for international and U.S. accounting standards; retain Big 4 auditors who follow Hong Kong auditing standards; limit and disclose related party transactions in conformity with Hong Kong regulations; retain international investment banks to value major acquisitions; and – while still majority state-owned – include one or more director-representatives from strategic/financial investors on their boards.5 Given the apparent success of such publicly- listed corporations in terms of financial performance and corporate governance, it may be useful for all large SOEs to experience the discipline of a public offering (especially the international accounting standards, extensive public disclosure, controls on related party transactions, and independent directors) – even including large SOEs that are not actually suitable for a public share listing.

Table II-8. Returns on Equity (ROE) for Selected H Shares, 2001

Angang New Steel 4.6%Qingling Motors 6.6%Tsingtao Brewery 3.3%China Aluminum 11.3%Jiangxi Copper 7.4%Yanzhou Coal Mines 12.2%PetroChina 15.9%Sinopec 9.7%Beijing Yanhua -5.2%Shanghai Petrochemical 0.9%Yizheng Chemical 1.9%Zhenhai Refining 5.6%Beijing Datang 10.4%Huaeng Power 12.2%Shandong Power 19.2%Great Wall Technology 3.7%Travelsky Technology 18.9%Nanjing Panda 30.0%Beijing Capital Airport 5.8%China Eastern Airlines 1.8%China Shipping Development 6.1%China Southern Airlines 9.0%Guangshen Railway 7.5%

Source: JPMorgan.

5 For example, see China Petroleum and Chemical Corporation (Sinopec), Annual Report and Accounts 2001, pp. 55-57; China Mobile and Rothschild, “Major Transaction and Connected Transactions,” 27 May 2002; and Huaneng Power International and JPMorgan, “Connected Transaction,” 22 November 2002. In 2001, Sinopec’s board included directors from Exxon Mobil and Cinda AMC.

11

B. Implications for State Asset Management The split nature of China’s SOE portfolio – some reasonably profitable large SOEs and many distressed SOEs of all sizes, but mostly small or medium – has important implications for implementation of the state asset management reforms mandated by the 16th CPC Congress and the 10th National People’s Congress: 1. Additional reforms are needed to facilitate not just more efficient use of State capital,

but its actual preservation. 2. Up to 150,000 small and medium SOEs should be “let go” within the next five years

– a huge task that will require efficient approaches to ownership transformation and restructuring or liquidation.

3. Resolution of large numbers of distressed SOEs will require market-based allocations of losses plus more capacity to do operational and financial restructuring.

4. While central SASAC may be able to focus on SOE governance, local SASACs will need to focus more on SOE ownership transformation and restructuring.

1. State capital

China’s SOEs pose two issues for the management of State capital. First, what should be done with the cash generated through dividends or sales proceeds from relatively good SOEs? The second is less pleasant – i.e., how to contain and share operating losses, losses on sale, and restructuring losses from China’s many bad SOEs? Historically, China’s SOE sector has overwhelmingly emphasized jobs preservation over the efficient use of capital. This is clear from such indicators as the maintenance of 89,000 loss-makers in the SOE portfolio, the progressive de-capitalization of at least ten sectors, and the insolvency of five provincial SOE portfolios. From the earlier description of locally-administered SOEs, there appears to be a significant “localization of benefits” (e.g., preservation of jobs, “leaking out” personal gains) leading to a “nationalization of liabilities.” These national liabilities are almost certain to include additional requirements for the eventual re-capitalization of state banks, to cover losses from non-performing loans (NPLs) to SOEs, and for the National Social Security Fund (NSSF) to cover local social insurance shortfalls for workers. Thus, the most urgent task is preservation of State capital. The prompt sale of small/medium SOEs is likely to be the most obvious way of mitigating the risk of “localization of benefits – nationalization of liabilities.” Also urgent is the restructuring or liquidation of distressed or non-viable SOEs. The process of selling or restructuring SOEs, however, will precipitate the recognition of losses from excess claims and require some resolution. Dividends and sales proceeds from good SOEs will provide some financial resources to cover claims. In at least some provinces, however, local financial resources will probably not suffice to cover claims.6 Thus, it will be important for the central and local 6 This applies both to privatization and liquidation. Most often, claims on an enterprise are paid out of sale proceeds or enterprise assets. Excess pools of financial resources – e.g, to satisfy financial institution

12

authorities to work out arrangements for sharing of gains and losses as well as appropriate financial management systems. The central SASAC should be in a leading position to work with the local SASACs and liaise with other national authorities (e.g., the state banks, NSSF, and Ministry of Finance) to facilitate SOE ownership transformation and restructuring and to make arrangements for the sharing of gains and losses. To make sound decisions on dividend policy, enterprise valuations, and enterprise restructuring, SASAC staff will need better accounting data. As suggested earlier, there is no cause for confidence that current data on the financial performance and position of China’s SOE portfolio is materially correct. Finally, to address the “localization of benefits – nationalization of liabilities” issue, the authorities (especially central SASAC) will need to give serious attention to risk management. 2. Ownership transformation Small and medium enterprises (SMEs) do not belong in China’s SOE portfolio. The data suggest that small/medium SOEs diminish rather than enhance State capital. Small/medium SOEs tend to be perpetual loss-makers. In addition, because their finances are especially non-transparent, small/medium SOEs pose high risks of additional liabilities. While individually insignificant, the large numbers of SMEs represent a collectively large claim on the attention of officials and a distraction from the potentially more rewarding enhancement of large SOE governance. While full and rapid implementation of the 1999 4th Plenum Decision to “let go” small SOEs and “grasp” large SOEs makes more sense than ever, this would precipitate a huge number of transactions. Leaving aside small/medium SOEs that may be affiliated with enterprise groups, as many as 150,000 small/medium SOEs should be “let go.” Profitability and solvency data (Tables II-4, 5, 6, & 7) suggest that perhaps half of these could be sold as viable businesses while asset sales/liquidations would be more appropriate for the other half. Implementation of a program for selling small/medium SOEs will need to guard against the “loss of state assets” through asset-stripping and unreasonably low sale prices for SOEs. But professional and independent valuations for up to 150,000 small/medium SOEs seem impractical. Alternative means (e.g., better information, seller warranties, advertising) for getting the highest possible sales price are discussed in Section IV.B). 3. SOE restructuring SOE restructuring will be more carefully examined in a subsequent background paper. But it is clear that SOE restructuring raises two big issues.

creditors and social insurance obligations – are unlikely to be available at the municipal or provincial level in most cases.

13

First, how will losses from SOE restructuring be allocated? The claims of employees, suppliers, financial institution creditors, and social insurance programs, utilities, and tax authorities will likely exceed the value of distressed SOE assets. Hence, losses will need to be shared among claimants in a way that balances immediate social needs with needs (e.g., creditor rights) for development of a market economy. Second, who will provide the institutional capacity? As seen in the recent East Asia crisis, the operational and financial restructuring of distressed enterprises is time-consuming and labor- intensive. China is fortunate in that significant enterprise restructuring experience already exists in some enterprise groups and the four asset management companies (AMCs).7 4. Institutional capacity Portfolio quality will determine institutional requirements. Centrally-administered large SOEs are more profitable, less leveraged, and less likely to be in distress than locally-administered SOEs. Hence, central SASAC as well as local SASACs with stronger portfolios (e.g., Beijing, Shanghai) will be able to focus more on maximizing returns on SOE equity and the exercise of normal corporate governance. Core activities at such SASACs will include the monitoring of SOE business planning and performance; participation in annual and extraordinary shareholder meetings; development of SOE boards; and appointment of board members. Periodically, these SASACs can also be expected to organize share sales in large SOEs. As suggested above, the central SASAC should also be prepared to liaise with local Ownership Agencies and other national institutions. As for large and stable SOEs, their boards will be able to focus on director nominations, committee structure, and procedures to enhance board oversight of SOE managements. Management of these SOEs will be able, in turn, to focus on business plans, investments, and operations to maximize returns on State capital. Based on a portfolio of 196 SOEs, the central SASAC may need 40-100 or so staff to monitor these SOEs and a cadre of 200-300 or so individuals to serve as independent non-executive directors.8 Establishment of a Directors Training Institute and directors accreditation program should facilitate the adoption of international best practices by directors at SASAC portfolio companies. At most local SASACs, however, there will be much greater need for skills in organizing small/medium SOE sales and in restructuring or liquidating distressed or non-viable SOEs. As nominal owner of these distressed SOEs, local SASACs should also be

7 For example, SAIC in autos, Jawa in consumer products, Sinopec in refining/petrochemicals, and Haier in white goods already have experience in restructuring/liquidating SOEs. Much of this experience, however, has involuntarily resulted from administratively-mandated M&A takeovers of highly distressed SOEs. There is wide agreement that M&A activity needs become based more on market principals. 8 This assumes that each SASAC staff monitors 2-5 portfolio companies. It is further assumed that each SOE board will average 7 members, including 3 independent directors; and that each independent director serves on an average of 2-3 SOE boards. Rules to prevent conflicts of interest would be needed. While appointed by SASAC, independent directors (as well as executive directors) should not be civil servants so as to reinforce the necessary distinction between administrative power and shareholder rights.

14

prepared to negotiate agreements with SOE workers, vendors, financial institution creditors, and pens ion programs on cost-sharing and assumption of remaining liabilities. Some training and institutional development is obviously important for local SASACs in these topics as well as in traditional corporate governance tasks. Since the great bulk of small/medium SOE sales, liquidations, and restructuring should occur over the next five years, the local SASACs should look to “outsource” these functions as much as possible. Market-based employment conditions (including compensation) and performance monitoring will be important to attract appropriately-qualified individuals to serve as SASAC staff or SOE directors and to motivate superior performance.

15

III. A Modern Capital Management System Over the past two decades, China has steadily moved to implement a modern enterprise system. The goal has been to improve the competitiveness of China’s enterprises. Somewhat analogously, the preservation and enhancement of State capital will require implementation of a modern capital management system through (a) more widespread accounting and auditing reforms; (b) a segmented approach to the management of SOE portfolios; (c) a systematic approach to SOE dividend policy and capital re- investment; (d) agreement between central and local governments on sharing of SOE ga ins and losses; and (e) enhanced risk management, including hard budget constraints on SOEs. For each of these topics, this section compares what is known about current practice in China with international best practices. A. Accounting and Auditing Accounting and auditing reforms should cover individual SOEs and enterprise groups as well as the SOE portfolios of the central SASAC and each local SASAC. 1. SOE and enterprise group accounting Accurate financial statements are essential for investors to make realistic decisions on enterprise performance, valuation, sale, restructuring, or re-investment. Accounting standards now applied to listed companies and foreign-invested enterprises should also be applied to all medium/large SOEs. Listed SOEs (i.e., about 1000 enterprises) as well as foreign- invested enterprises (FIEs) are obliged to follow the new Accounting Systems for Business Enterprises (ASBE). ASBE standards, where they have been developed, are reasonably close to International Accounting Standards (IAS). Problems arise from the fact, however, that the great majority of SOEs continue to follow older accounting regulations which are sometimes much less conservative than IAS and sometimes much more strict (see Table III-1).

Table III-1. New vs. Old Accounting Standards for Chinese Enterprises: Selected Accounting Items

Accounting Item

Joint Stock Companies and Foreign-Invested Enterprises

Other State-Owned Enterprises

Short-term investments

• Short- vs. long-term based on management’s intention

• Shown at lower of cost or market value

• Impairment provision in case of a permanent impairment of value

• No guidance on classification • Shown at cost

16

Accounts receivable

• Provision for bad debts should be based on management’s experience and judgment. May be applied to specific balances, as a % of overall balance, or by applying different % to different receivables age brackets

• Provision for bad debt may not exceed 0.3-0.5% of accounts receivable balance

Inventories • Carried at lower of cost or net realizable value

• Impairment treated as general and

administrative expense

• Carried at cost. Provision for diminution in value generally not allowed without approval from authorities

• Impairment treated as a selling cost

Long-term investments

• Carried at cost unless there is a permanent diminution in value. Then an impairment provision should be made for the difference

• Accounted for using equity method if investment >20% of investee voting rights or able to control investee

• Carried at cost • If investment >20% of investee equity

and significant influence can be demonstrated, investor has option to use equity method

Consolidated financial statements

• Required if company holds >50% of another entity’s equity or with smaller ownership has the ability to exercise control

• Focuses on percentage of ownership; not control

Fixed assets - depreciation

• Useful life of asset based on management’s judgement

• Depreciation method is based on management experience and judgement

• Depreciation method may be straight-line or accelerated

• Useful life determined by government; may not be realistic

• Depreciation method set by government • Straight-line depreciation generally

prescribed Fixed assets - impairment

• Impairment provision required in case fixed asset is damaged; not in use and not expected to be used in foreseeable future; technically obsolete; used to produce sub-standard products; or no longer beneficial to company

• Not addressed

Finance leases • Liability and asset shown • Only lease expense is shown Construction in progress

• Carried at cost unless impaired, in which case provision similar to other fixed assets impairment

• Carried at cost; impairment not addressed

Land use rights • If not idle (“intangible asset”) or recent construction (“construction in progress”), shown as separate LUR line item

• Shown in separate LUR line item

Foreseeable liabilities

• A provision should be made for foreseeable liabilities, such as restructuring costs, redundancy costs, or warranty costs

• Not addressed; some of these costs could be accrued in “other liabilities”

Source: accounting industry. See also Nicholas R. Lardy, China’s Unfinished Economic Revolution, (Brookings Institution, 1998), pp. 33-47.

17

Thus, old-style non-ASBE accounts can vary from modern ASBE accounts in the following important ways: • Short-term and long-term investments valued at cost may be over-valued if there has

been a decline in market value. This could also lead to an overstatement of income and equity.

• Accounts receivable are almost certainly overvalued, since bad debts are always more than the 0.5% permitted by regulation. This would cause income and equity to be overstated.

• Inventories (along with income and equity) may be overstated if there is a lot of inventory that is obsolete or sub-standard and cannot be sold.

• There may be an under-consolidation of accounts, which could result in overstatements of revenues, income, and equity as a result of related party transactions.

• Fixed assets may be over-stated, due to too-slow depreciation, or overstated due to a failure to show effects of impairment from damage, obsolescence, or non-use.

• Fixed assets and liabilities may be understated from failure to account for financial leases.

• Fixed assets will be understated if there has been inadequate accounting for the market value of land use rights.

• Failure to account for foreseeable liabilities – e.g., restructuring costs, redundancy costs – would cause an overstatement of income and equity.

Some simple examples in just one of these areas – accounts receivable – illustrates the potential impact from adoption of new international standards, i.e., ASBE. The switch to realistic bad debt accounting from a statutory maximum of 0.5% can require a major 1-time provision that would reduce income and equity. Companies listed on the Hong Kong Stock Exchange, for example, have already made this adjustment. By comparing actual reported receivables with what would have been reported net of a 0.5% bad debt allowance, it appears that just this switch to ASBE accounting for receivables could cause a 1-time reduction in net income (and retained earnings) of at least 20-25%.1 Other old-style treatment of items, especially land use rights, may tend to understate SOE accounts. But in the great majority of differences, old-style accounting is likely to overstate SOE income, equity, and assets and to understate SOE liabilities. In the case of affiliated SOEs – for example, in many of China’s state-majority enterprise groups – it appears that there is no proper consolidation of accounts except in the case of listed SOEs. In most cases, the accounts of multiple affiliated SOEs (including the effects of cross-affiliate sales) may be simply combined rather than consolidated to eliminate the effects of inter-affiliate transactions. This would tend to overstate revenues, income, and equity within enterprise groups. 1 The 20-25% figure is based on an analysis of SOEs listed on the Hong Kong and New York Stock Exchanges. These are among China’s best companies. Thus, the impact of a switch to ASBE receivables accounting for other less-good companies would almost certainly be more severe.

18

2. Portfolio accounting

Similarly, periodic financial statements for each SASAC portfolio will be needed to assess each SASAC’s management of its assigned portion of State capital. Austria’s OIAG state shareholding fund is probably the most complete example of accounting for an SOE portfolio.2 OIAG’s annual financial statements provide a public accounting for portfolio assets, liabilities, and income (Box III-1).

Box III-1. Accounting Practices at Austria’s OIAG SOE Fund As of end-2001, OIAG’s holdings included 7 publicly- traded companies (or subsidiaries) and 7 non-public companies, including 100% of Austria Post. These holdings, some investment securities, and cash represent most of OIAG’s assets. Market values are available for the publicly-traded companies. OIAG typically values all holdings at cost (book value), however. Holdings are depreciated at annual rates of 20-33%. Any long-term impairment in the value of a holding is accounted for by an extraordinary depreciation charge. OIAG’s mandate includes sale of State shares in SOEs. At the time of sale, a holding is “written up” if actual market value exceeds its cost basis. This write-up appears as operating income on OIAG’s income statement. OIAG shares 80% of the profits from any sale of a holding with Austria’s Ministry of Finance. Such profit-sharing is treated as an operating expense. OIAG’s liabilities include provisions for severance payments, pensions, all identifiable risks, and un-quantifiable liabilities. OIAG segments some of its earnings in several reserve funds. The sale of a holding may precipitate a provisions cancellation and/or reserves release, which would count as operating income. OIAG’s net profit for 2001 was ATS 341 million. OIAG’s supervisory board concurred with management’s recommendation to carry this amount forward as retained profit. For 2001, OIAG’s accounts were audited by the local affiliate of Ernst & Young (E&Y), an international accounting firm. E&Y certified that OIAG’s “accounts and annual financial statements comply with the relevant legal provisions” and that OIAG’s financial statements “observe the principles of adequate and orderly accounting and to the maximum extent possible present a true and fair view of the company’s assets, financial situation and profitability.” 2 New Zealand has recently improved government accounting for SOEs. Before July 2002, the government’s financial statements showed a consolidated net surplus for all SOEs in the government’s operating balance (income statement) and a consolidated net investment value for all SOEs in the government’s balance sheet. Since July 2002, the government’s financial statements and forecasts show consolidated revenues, expenses, surplus, assets, liabilities, and equity for all SOEs. R. Hamilton, “New Zealand Accounting Policies on SOEs,” correspondence, July 29, 2003. Singapore’s Temasek SOE fund does not make public its financial statements.

19

Source: OIAG, Annual Report 2001. Periodic financial statements for each SASAC portfolio should similarly reflect international accounting standards. China’s ASBE standards already provide a starting point for SASAC portfolio accounting. According to ASBE, short-term equity investments should be carried at the “lower of cost or market.” For long-term equity investments where a SASAC owns 20 percent or more of the enterprise’s equity – or can otherwise exert control or influence – the “equity method” of accounting should apply. Under the equity method, which would likely apply to most of the medium/large SOEs in SASAC portfolios, SOE profits would increase the SASAC’s investment balance and investment income; SOE losses would decrease the SASAC’s investment balance and investment income; and SOE dividends would increase the SASAC’s cash balance while reducing its investment balance. For either long- or short-term equity investments, any permanent reduction in value should be reflected in a provision to the SASAC’s investment balance and a realized loss of investment income. In overseeing the implementation of improvements in financial reporting for SASAC portfolios, it would be useful for the central SASAC to seek advice from a qualified international accounting firm. It may be necessary to address additional accounting issues not yet covered by ASBE. In addition, while implementing international accounting standards, careful consideration should be given to the unique circumstances of China’s SOE portfolios (e.g., large numbers of non-tradable shares, significant minority shareholdings, insolvent provincial portfolios). Lastly, it would be a good idea to resolve valuation issues (e.g., for “unhealthy” SOE assets) before establishing initial balance sheets for central and local SASAC portfolios. Any international accounting firm that has had a major presence in China over the past 1-2 decades could usefully advise central SASAC on these matters. Any such international firm would also be able to advise and assist SASACs in improving their management information systems and identifying appropriate portfolio performance goals (e.g., returns on equity). These additional steps are also necessary to support the effective management of State capital. Given the “public” nature of SOEs, even those that are not publicly-listed on stock exchanges, it would be appropriate to increase the transparency of all large SOEs and SASAC portfolios. This could involve, for example, a requirement for annual and quarterly financial reporting and a commitment to make these reports available to the public.

3. Auditing The material accuracy of financial statements should be independently audited according to international audit standards. All countries have some financial mis-reporting. China is no exception. An official investigation of almost 200 Chinese companies found that 54 percent mis-reported profits in 2001.3 Independent audits conducted according to international audit standards are an important deterrent to

3 China Daily, January 10, 2003.

20

financial mis-reporting. The effective implementation of adequate audit standards also depends on SOE boards of directors and external auditors. The board of dir ectors should be responsible for the integrity of financial statements prepared by management and for overseeing external auditors. External auditors should be responsible for validating the SOE’s financial statements and the adequacy of other information disclosures. B. Portfolio Segmentation Other countries with large SOE portfolios that include a significant number of distressed SOEs have segmented the portfolio and applied an appropriate method(s) to each segment of the portfolio. As indicated in Section II, about half of China’s SOEs are unprofitable and likely in moderate-to-severe distress. This is not dissimilar to past situations facing the SOE portfolios of other transition or OECD countries: • In Italy, the IRI state holding company’s portfolio was highly distressed by 1992-9:

annual losses were $8.3 billion and consolidated debt was $58 billion. Per Italy’s agreement with the European Union to repay these debts and reduce its debt/equity ratio to about 1:1. During 1992-2000, IRI conducted 160 major asset sales – e.g., two banks, auto maker SEAT, Rome airport, toll roads, 31 percent of Alitalia airline, and most of the Finmeccanica aerospace company – for Lira 65 trillion (about $53 billion). IRI itself was liquidated in 2000. Its remaining shareholdings – public television RAI, 30 percent of Finmeccanica, and 54 percent of Alitalia – were transferred to the Italian Treasury. While a failure at financial management and enterprise restructuring, IRI succeeded in liquidating itself and – like OIAG in Austria – stimulating development of Italy’s capital market. Former IRI companies account for 45 percent of Italy’s current stock market capitalization. 4

• In East Germany, the Treuhandanstalt transformed over 12,000 SOEs. Of these, 53 percent were sold, 30 percent were liquidated, and 17 percent were transformed through restitution or other means.5

• In Poland, between 1990 and end-1996, about 40 percent of 8,441 medium/large SOEs entered ownership transformation through a liquidation or insolvency process (see Table IV-3).

Thus, depending upon the size and condition of any particular SOE in a SASAC portfolio, any of the following may be most appropriate: sale as a “going concern,” asset sale or liquidation, operational and/or financial restructuring, or normal corporate governance. It would be useful for the central SASAC to develop some guidelines for segmenting local SASAC portfolios (as well as its own portfolio) and managing portfolio segments accordingly. Segmentation should reflect SOE size plus financial performance and condition. It makes sense to sell small/medium SOEs, either as “going concerns” or

4 Olivier Butzbach, background note on IRI, May 23, 2002, mimeo. 5 Final Report of the Treuhandanstalt, December 31, 1994, Bundesanstalt fur vereinigungsbedingte (Federal Agency for Unification Tasks), pp. 1-5.

21

through asset sales/liquidations.6 Many medium-sized SOEs, however, may need “operational restructuring and/or “financial restructuring” before they could be sold.7 Similarly, some large SOEs destined to remain in the State portfolio may need operational and/or financial restructuring. Ultimately, some medium/large SOEs may be non-viable because of basic business flaws and would better be liquidated. Company cash flows are a good preliminary indicator of the health or distress of individual enterprises. The need for accurate cash flow reporting reinforces the need for more widespread implementation of accounting reforms. Such an analysis of 2000+ enterprises in Central Europe in 1992-94 showed a high-but-declining incidence of distress (Table III-2). At one extreme, profitable companies (Column A) are candidates for “normal” corporate governance. At the other extreme, companies that cannot pay all wages or suppliers (Column D) are candidates for extensive operational restructuring or liquidation. Between these extremes, a company may have enough cash flow to service its debt, but still show an accounting loss when depreciation is included as an expense (Column B). Such companies are prime candidates for operational restructuring to increase earnings. Other more-distressed companies may be able to pay wages and vendors, but unable to meet all debt service obligations (Column C). Such companies would need more extensive operational restructuring. If it appears that operational restructuring cannot suffice, then some financial restructuring to reduce corporate debt to a sustainable level would become appropriate.

Table III-2. Application of Segmentation

To Enterprises of Selected Countries, 1992-1994 (percentages of enterprises, weighted by employment)

Unprofitable Profitable Positive Cannot Cannot Cash service pay all Flow all debt wages or suppliers Country Year A B C D TotalBulgaria 1992 20 2 35 43 100 1994 33 9 30 28 100Czech Rep. 1992 60 13 7 20 100 1994 81 11 4 4 100Hungary 1992 59 6 15 20 100 1994 67 12 8 13 100Slovakia 1992 61 17 7 15 100 1993 71 15 3 11 100UK 1992 93 5 1 1 100

Source: World Bank, Restructuring Large Industrial Firms in Central and Eastern Europe, 1996, p. 7.

6 See Section IV for further discussion of the merits of selling small SOEs – even healthy small SOEs – through asset sales. 7 “Operational restructuring” includes discontinuation of less-profitable or loss-making businesses, layoffs of excess labor, and other cost reductions to increase a company’s earnings and debt service capacity, plus sales of non-core businesses and assets (e.g., real estate) to retire debt. “Financial restructuring” may include term extensions, rate reductions, or conversion of debt into equity or into convertible bonds.

22

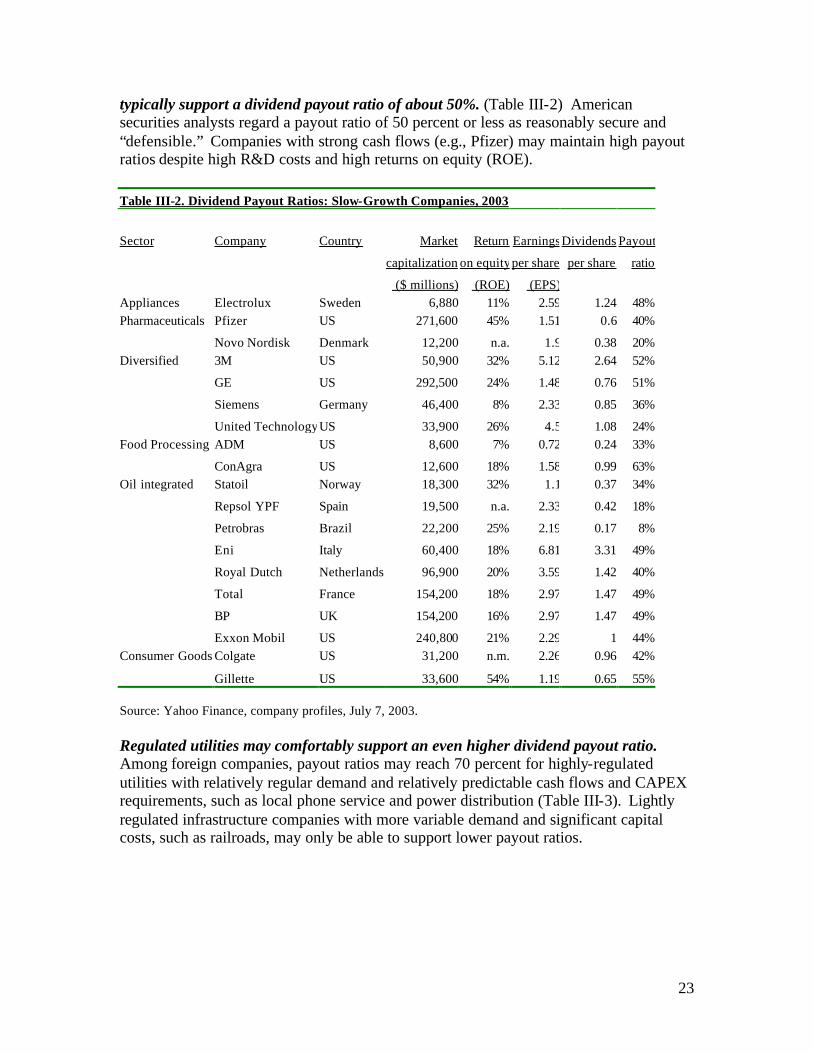

C. Dividend Policy and Capital Reinvestment Dividend payments, by those companies that pay dividends, are usually regular (e.g., quarterly) and somewhat predictable. Occasionally, a company may make a special one-off dividend payment, especially if it has a large cash balance that cannot be invested at an adequate expected return. A key measure is the “dividend payout ratio” – the ratio of dividends to net income. The appropriate dividend payout ratio for a particular company will depend on its growth prospects, capital structure, and investment opportunities. China’s best SOEs, such as those listed on the Hong Kong and New York Stock Exchanges, seem to follow international best practices in terms of dividend policy and the payment of dividends (see Box III-3).

Box III-3. Dividend Policy at a Major SOE Dividend policy for one SOE listed on the Hong Kong and New York stock exchanges is subject to approval by the company’s Board of Directors. Up to 35 percent of net income can be paid out as dividends. Actual dividend payments in 2001 and 2002 were at this maximum dividend payout ratio. Each year’s dividend payment is proposed by company management. It must then be approved by the Board and finally approved at the annual general meeting (AGM) of shareholders. In making its dividend decisions, the Board’s Strategic Committee and company management jointly review cash projections, debt/equity structure, and capital expenditure (CAPEX) needs. Any proposed CAPEX should clear a specified “hurdle rate” (14 percent return on capital invested) in order to be approved. It appears, however, that the great majority of China’s medium/large SOEs take a much less formal approach to dividend policy and in fact do not pay dividends. This may reflect a widespread attitude that SOE managements have a “management right” to decide themselves on the use of excess cash. This informality may lead to the accumulation of large cash balances and the opportunistic and un-disciplined investment of these cash balances. For example, some major Chinese SOEs have acquired or sought significant stakes in the initial public offerings (IPOs) of completely non-related businesses. Chinese SOEs also make private equity investments in unrelated non-core businesses.8 Internationally, dividend payout ratios tend to reflect the growth prospects of each company. For example, companies with relatively slow and dependable growth can

8 For example, World Bank staff are familiar with one capital goods company that has maintained long-term equity investments in such unrelated businesses as securities, mineral water, traditional Chinese medicine, and advertising. This is in spite of the fact that this company does not pay dividends, allegedly needs additional funds for CAPEX, and is in increasing arrears on debt service to creditors.

23

typically support a dividend payout ratio of about 50%. (Table III-2) American securities analysts regard a payout ratio of 50 percent or less as reasonably secure and “defensible.” Companies with strong cash flows (e.g., Pfizer) may maintain high payout ratios despite high R&D costs and high returns on equity (ROE). Table III-2. Dividend Payout Ratios: Slow-Growth Companies, 2003

Sector Company Country Market Return Earnings Dividends Payout

capitalization on equityper share per share ratio

($ millions) (ROE) (EPS)Appliances Electrolux Sweden 6,880 11% 2.59 1.24 48%Pharmaceuticals Pfizer US 271,600 45% 1.51 0.6 40%

Novo Nordisk Denmark 12,200 n.a. 1.9 0.38 20%Diversified 3M US 50,900 32% 5.12 2.64 52%

GE US 292,500 24% 1.48 0.76 51%

Siemens Germany 46,400 8% 2.33 0.85 36%

United TechnologyUS 33,900 26% 4.5 1.08 24%Food Processing ADM US 8,600 7% 0.72 0.24 33%

ConAgra US 12,600 18% 1.58 0.99 63%Oil integrated Statoil Norway 18,300 32% 1.1 0.37 34%

Repsol YPF Spain 19,500 n.a. 2.33 0.42 18%

Petrobras Brazil 22,200 25% 2.19 0.17 8%

Eni Italy 60,400 18% 6.81 3.31 49%

Royal Dutch Netherlands 96,900 20% 3.59 1.42 40%

Total France 154,200 18% 2.97 1.47 49%

BP UK 154,200 16% 2.97 1.47 49%

Exxon Mobil US 240,800 21% 2.29 1 44%Consumer Goods Colgate US 31,200 n.m. 2.26 0.96 42%

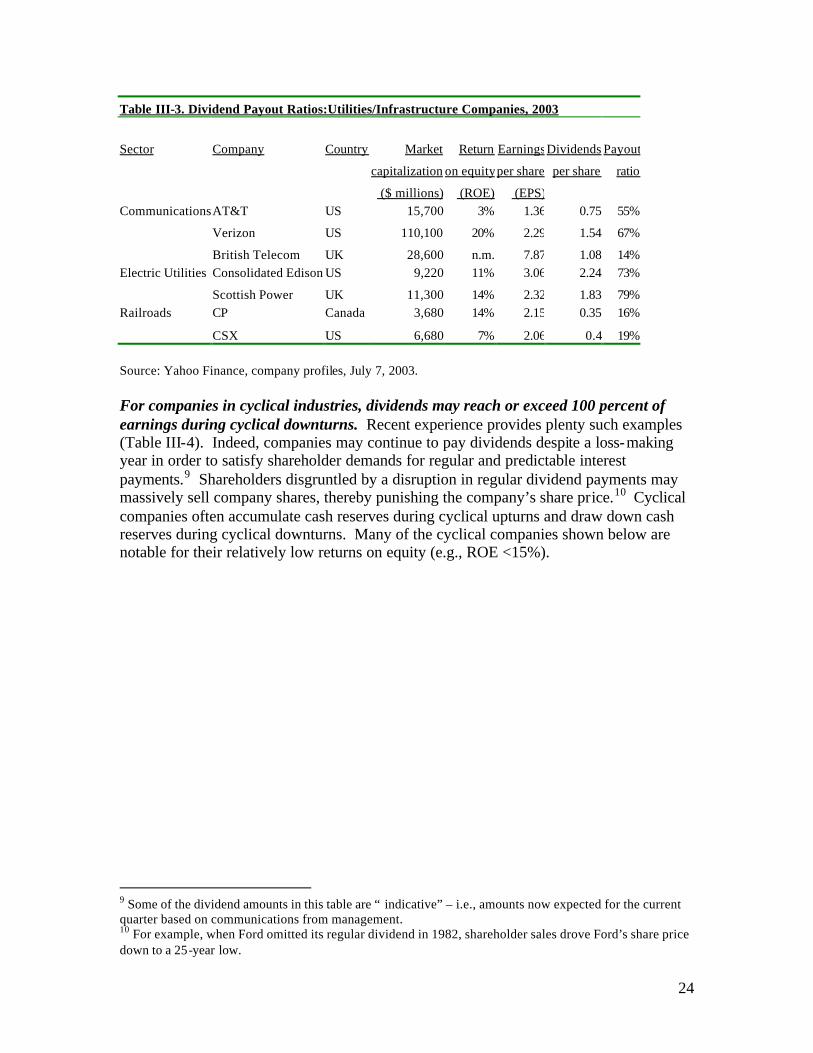

Gillette US 33,600 54% 1.19 0.65 55% Source: Yahoo Finance, company profiles, July 7, 2003. Regulated utilities may comfortably support an even higher dividend payout ratio. Among foreign companies, payout ratios may reach 70 percent for highly-regulated utilities with relatively regular demand and relatively predictable cash flows and CAPEX requirements, such as local phone service and power distribution (Table III-3). Lightly regulated infrastructure companies with more variable demand and significant capital costs, such as railroads, may only be able to support lower payout ratios.

24

Table III-3. Dividend Payout Ratios:Utilities/Infrastructure Companies, 2003

Sector Company Country Market Return Earnings Dividends Payout

capitalization on equityper share per share ratio

($ millions) (ROE) (EPS)CommunicationsAT&T US 15,700 3% 1.36 0.75 55%

Verizon US 110,100 20% 2.29 1.54 67%

British Telecom UK 28,600 n.m. 7.87 1.08 14%Electric Utilities Consolidated Edison US 9,220 11% 3.06 2.24 73%

Scottish Power UK 11,300 14% 2.32 1.83 79%Railroads CP Canada 3,680 14% 2.15 0.35 16%

CSX US 6,680 7% 2.06 0.4 19% Source: Yahoo Finance, company profiles, July 7, 2003. For companies in cyclical industries, dividends may reach or exceed 100 percent of earnings during cyclical downturns. Recent experience provides plenty such examples (Table III-4). Indeed, companies may continue to pay dividends despite a loss-making year in order to satisfy shareholder demands for regular and predictable interest payments.9 Shareholders disgruntled by a disruption in regular dividend payments may massively sell company shares, thereby punishing the company’s share price.10 Cyclical companies often accumulate cash reserves during cyclical upturns and draw down cash reserves during cyclical downturns. Many of the cyclical companies shown below are notable for their relatively low returns on equity (e.g., ROE <15%).

9 Some of the dividend amounts in this table are “indicative” – i.e., amounts now expected for the current quarter based on communications from management. 10 For example, when Ford omitted its regular dividend in 1982, shareholder sales drove Ford’s share price down to a 25-year low.

25

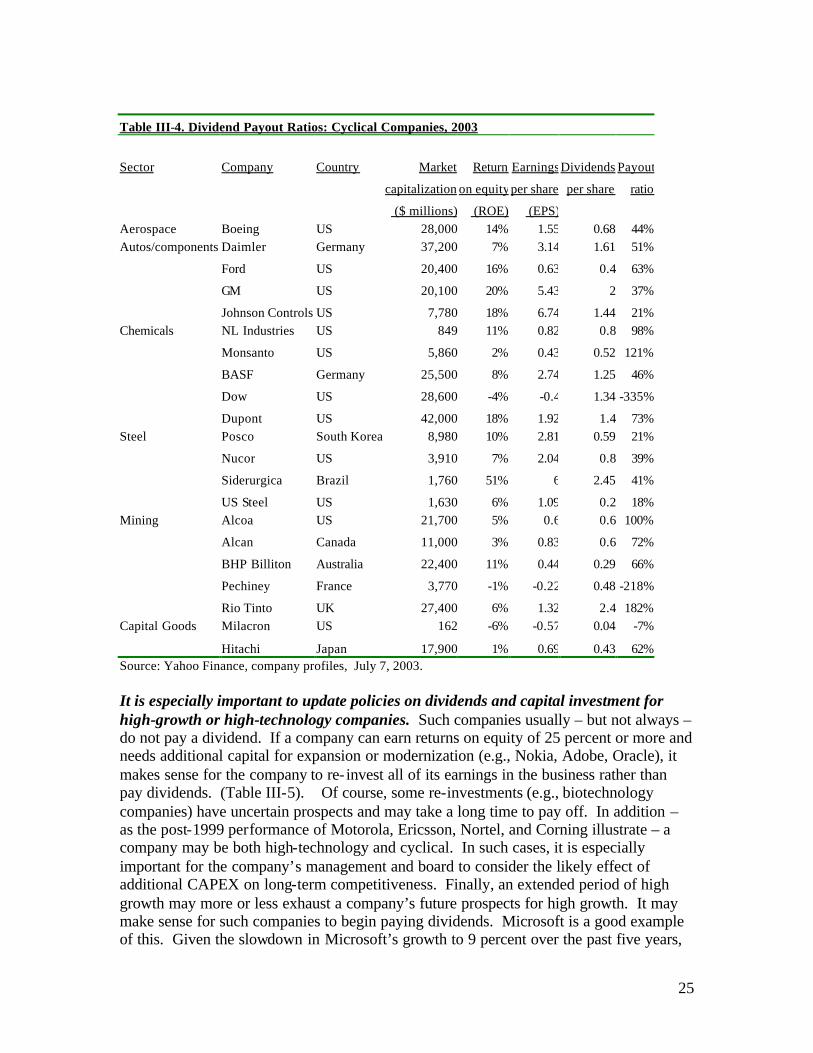

Table III-4. Dividend Payout Ratios: Cyclical Companies, 2003

Sector Company Country Market Return Earnings Dividends Payout

capitalization on equityper share per share ratio

($ millions) (ROE) (EPS)Aerospace Boeing US 28,000 14% 1.55 0.68 44%Autos/components Daimler Germany 37,200 7% 3.14 1.61 51%

Ford US 20,400 16% 0.63 0.4 63%

GM US 20,100 20% 5.43 2 37%

Johnson Controls US 7,780 18% 6.74 1.44 21%Chemicals NL Industries US 849 11% 0.82 0.8 98%

Monsanto US 5,860 2% 0.43 0.52 121%

BASF Germany 25,500 8% 2.74 1.25 46%

Dow US 28,600 -4% -0.4 1.34 -335%

Dupont US 42,000 18% 1.92 1.4 73%Steel Posco South Korea 8,980 10% 2.81 0.59 21%

Nucor US 3,910 7% 2.04 0.8 39%

Siderurgica Brazil 1,760 51% 6 2.45 41%

US Steel US 1,630 6% 1.09 0.2 18%Mining Alcoa US 21,700 5% 0.6 0.6 100%

Alcan Canada 11,000 3% 0.83 0.6 72%

BHP Billiton Australia 22,400 11% 0.44 0.29 66%

Pechiney France 3,770 -1% -0.22 0.48 -218%

Rio Tinto UK 27,400 6% 1.32 2.4 182%Capital Goods Milacron US 162 -6% -0.57 0.04 -7%

Hitachi Japan 17,900 1% 0.69 0.43 62%Source: Yahoo Finance, company profiles, July 7, 2003. It is especially important to update policies on dividends and capital investment for high-growth or high-technology companies. Such companies usually – but not always – do not pay a dividend. If a company can earn returns on equity of 25 percent or more and needs additional capital for expansion or modernization (e.g., Nokia, Adobe, Oracle), it makes sense for the company to re- invest all of its earnings in the business rather than pay dividends. (Table III-5). Of course, some re-investments (e.g., biotechnology companies) have uncertain prospects and may take a long time to pay off. In addition – as the post-1999 performance of Motorola, Ericsson, Nortel, and Corning illustrate – a company may be both high-technology and cyclical. In such cases, it is especially important for the company’s management and board to consider the likely effect of additional CAPEX on long-term competitiveness. Finally, an extended period of high growth may more or less exhaust a company’s future prospects for high growth. It may make sense for such companies to begin paying dividends. Microsoft is a good example of this. Given the slowdown in Microsoft’s growth to 9 percent over the past five years,

26