winning in us commercial staffing - randstad/media/files/r/randstad-ir/documents...winning in us...

TRANSCRIPT

winning in US commercial staffing

Capital Markets Day London Randstad Holding nv November 20, 2014

Traci Fiatte, President Randstad General Staffing USA

ober 30, 2014 third quarter results 2014 - roadshow version 2

agenda

introduction and definitions US market and Randstad General Staffing US how did we get here? history and methods

going forward

WINNING

what is winning?

3

Profitable Sustainable Growth that outperforms the market

Capital Markets Day 2014 November 20, 2014

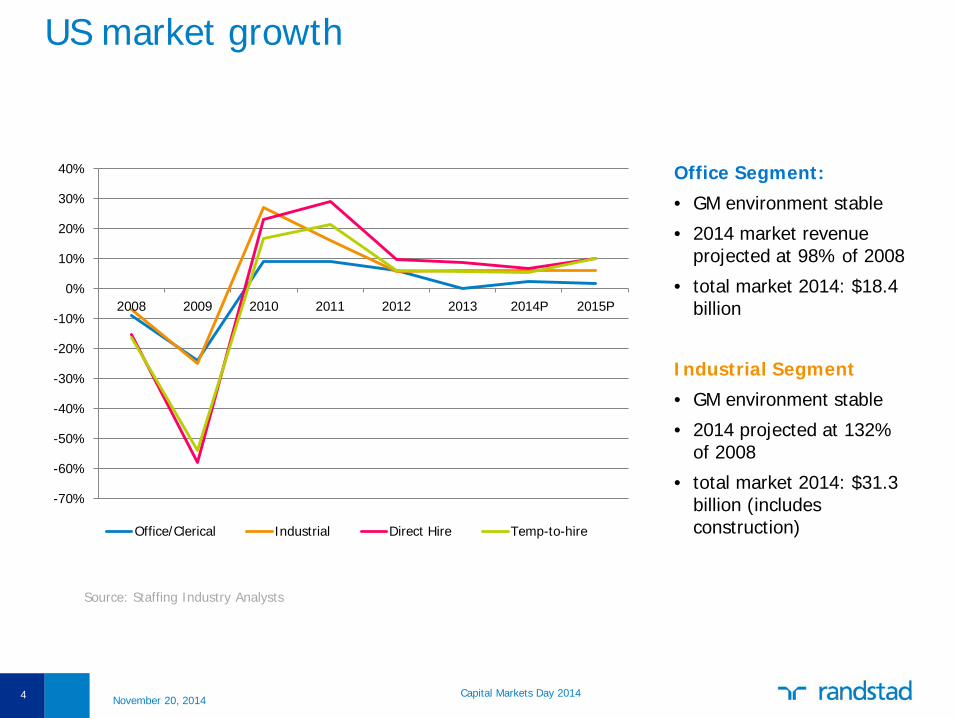

US market growth

4

Office Segment:

• GM environment stable

• 2014 market revenue projected at 98% of 2008

• total market 2014: $18.4 billion

Industrial Segment

• GM environment stable

• 2014 projected at 132% of 2008

• total market 2014: $31.3 billion (includes construction)

Source: Staffing Industry Analysts

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2008 2009 2010 2011 2012 2013 2014P 2015P

Office/Clerical Industrial Direct Hire Temp-to-hire

Capital Markets Day 2014 November 20, 2014

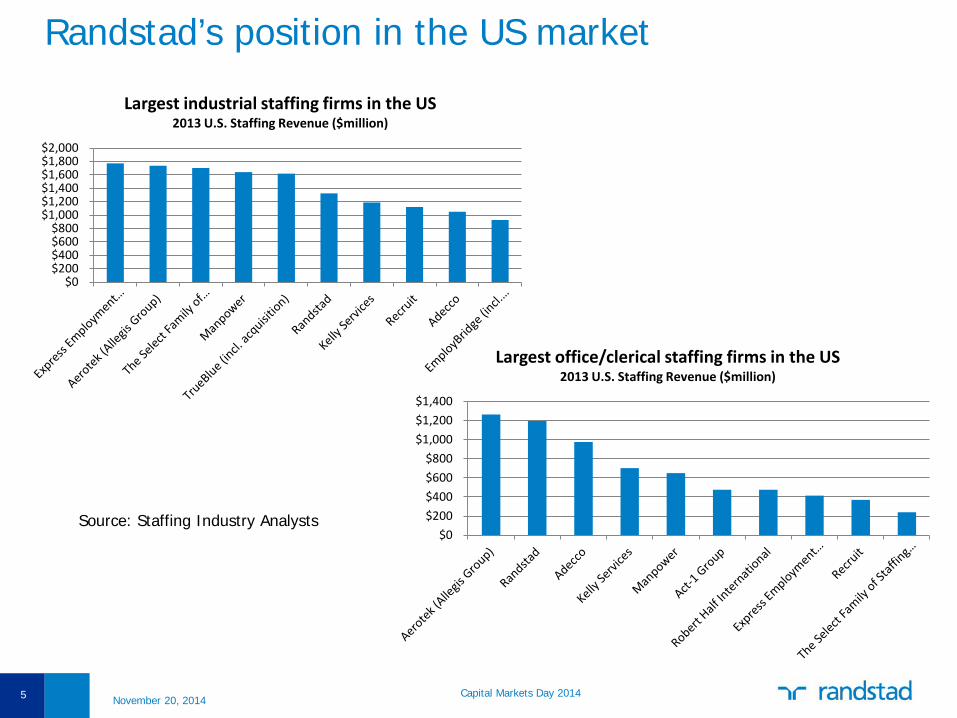

Randstad’s position in the US market

5

$0$200$400$600$800

$1,000$1,200$1,400$1,600$1,800$2,000

Largest industrial staffing firms in the US 2013 U.S. Staffing Revenue ($million)

$0$200$400$600$800

$1,000$1,200$1,400

Largest office/clerical staffing firms in the US 2013 U.S. Staffing Revenue ($million)

Source: Staffing Industry Analysts

Capital Markets Day 2014 November 20, 2014

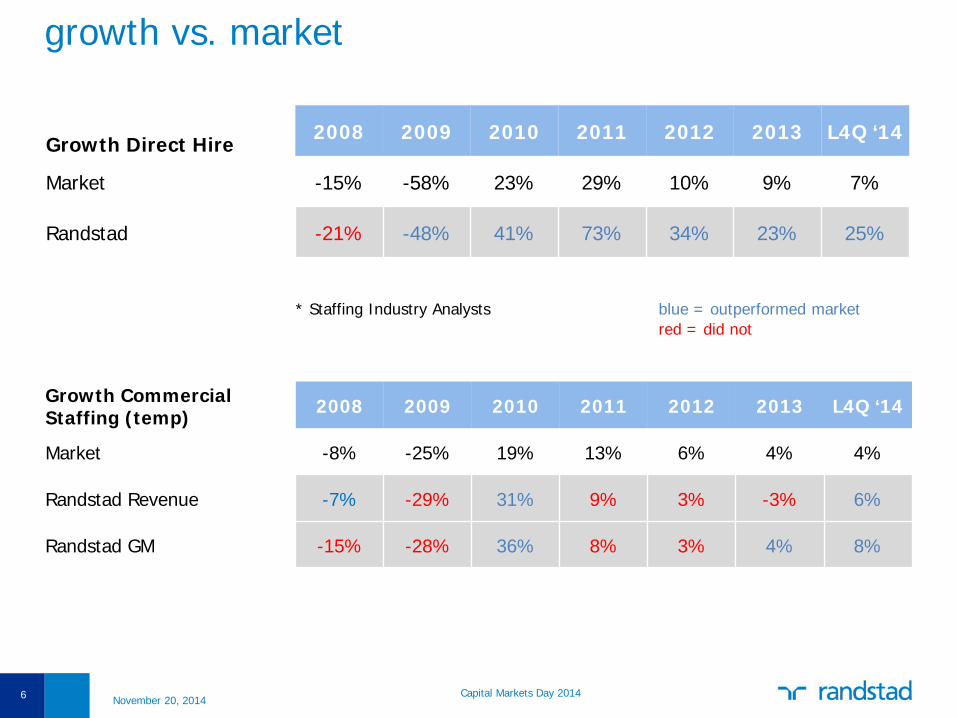

growth vs. market

6

Growth Direct Hire 2008 2009 2010 2011 2012 2013 L4Q ‘14

Market -15% -58% 23% 29% 10% 9% 7%

Randstad -21% -48% 41% 73% 34% 23% 25%

Growth Commercial Staffing (temp) 2008 2009 2010 2011 2012 2013 L4Q ‘14

Market -8% -25% 19% 13% 6% 4% 4%

Randstad Revenue -7% -29% 31% 9% 3% -3% 6%

Randstad GM -15% -28% 36% 8% 3% 4% 8%

blue = outperformed market red = did not

* Staffing Industry Analysts

Capital Markets Day 2014 November 20, 2014

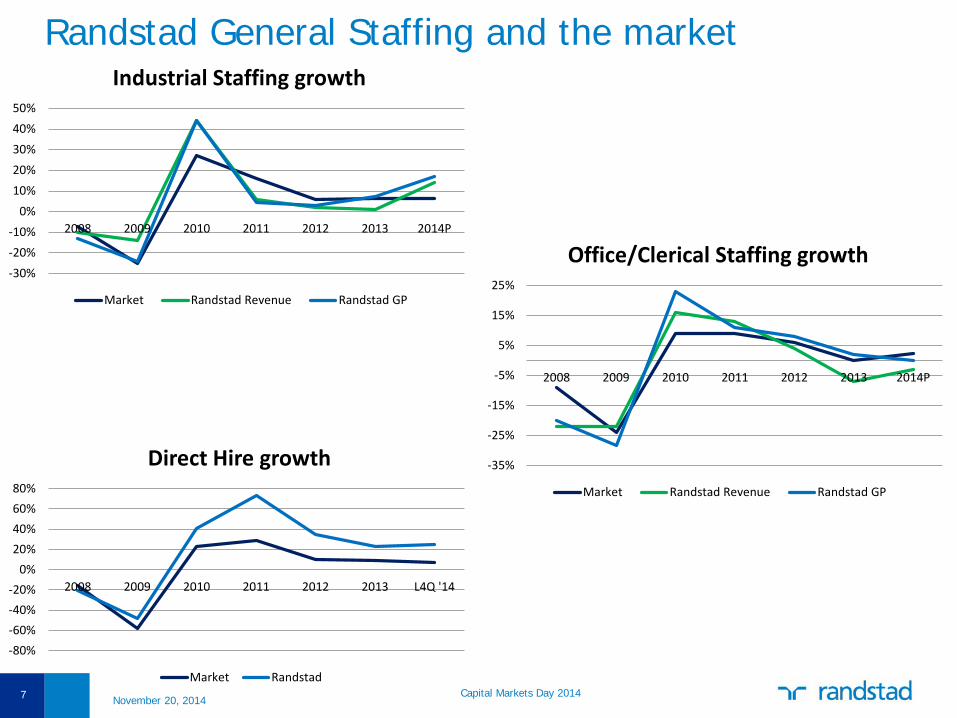

Randstad General Staffing and the market

7 Capital Markets Day 2014 November 20, 2014

-80%-60%-40%-20%

0%20%40%60%80%

2008 2009 2010 2011 2012 2013 L4Q '14

Direct Hire growth

Market Randstad

-30%-20%-10%

0%10%20%30%40%50%

2008 2009 2010 2011 2012 2013 2014P

Industrial Staffing growth

Market Randstad Revenue Randstad GP

-35%

-25%

-15%

-5%

5%

15%

25%

2008 2009 2010 2011 2012 2013 2014P

Office/Clerical Staffing growth

Market Randstad Revenue Randstad GP

how did we get here?

8

segmentation

delivery model field steering

Capital Markets Day 2014 November 20, 2014

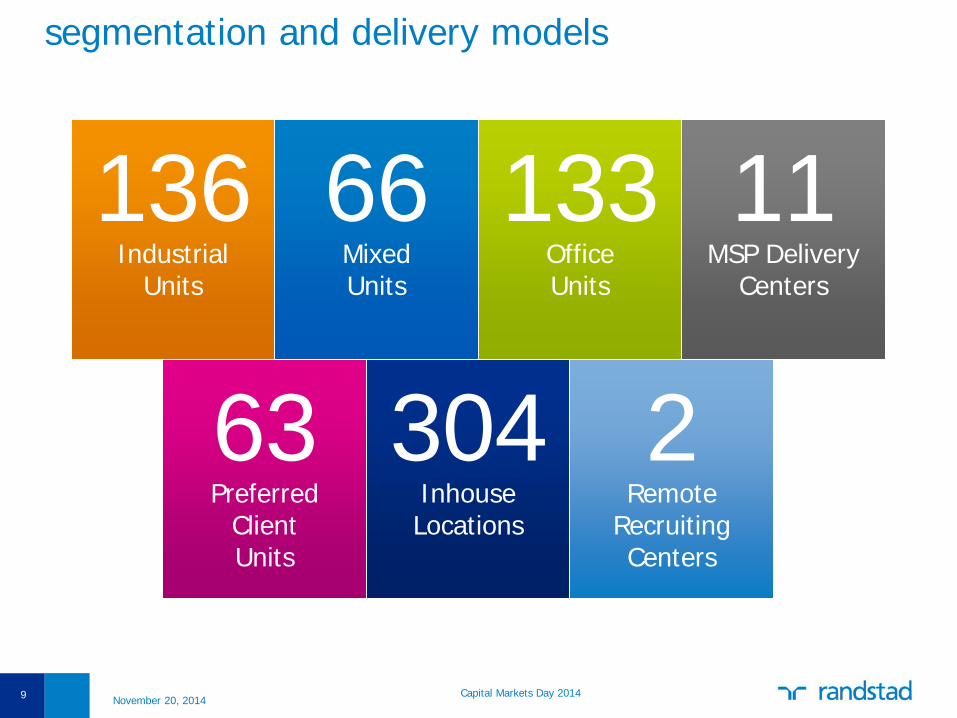

segmentation and delivery models

9

136 Industrial

Units

66 Mixed Units

133 Office Units

11 MSP Delivery

Centers

63 Preferred

Client Units

304 Inhouse Locations

2 Remote

Recruiting Centers

Capital Markets Day 2014 November 20, 2014

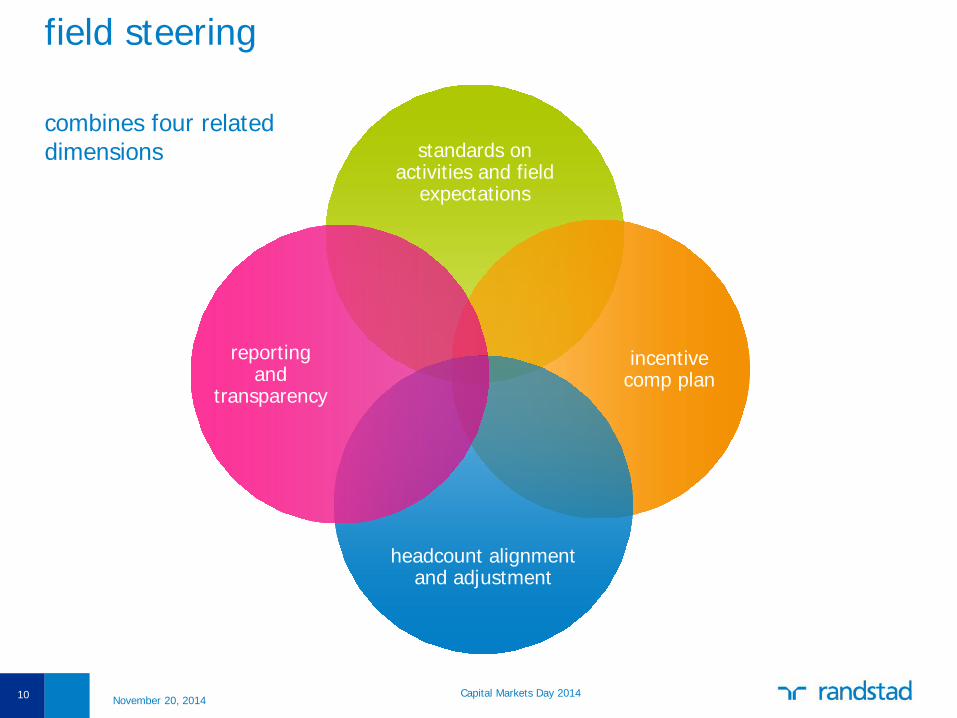

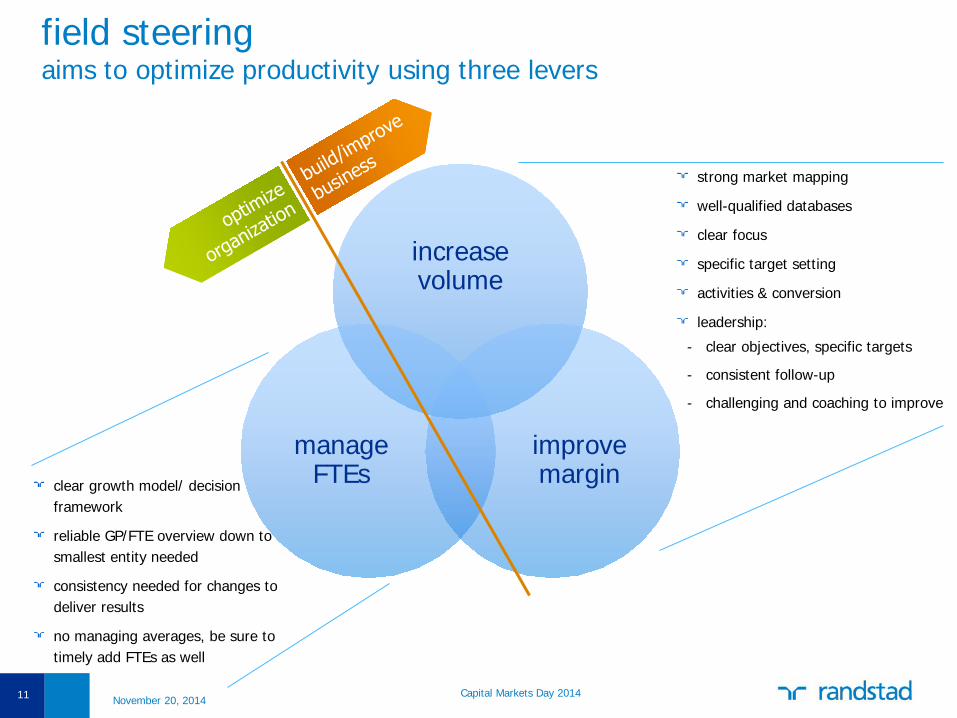

field steering

10

standards on activities and field

expectations

incentive comp plan

headcount alignment and adjustment

reporting and

transparency

combines four related dimensions

Capital Markets Day 2014 November 20, 2014

11

strong market mapping

well-qualified databases

clear focus

specific target setting

activities & conversion

leadership:

- clear objectives, specific targets

- consistent follow-up

- challenging and coaching to improve

increase volume

improve margin

manage FTEs clear growth model/ decision

framework

reliable GP/FTE overview down to smallest entity needed

consistency needed for changes to deliver results

no managing averages, be sure to timely add FTEs as well

field steering aims to optimize productivity using three levers

Capital Markets Day 2014 November 20, 2014

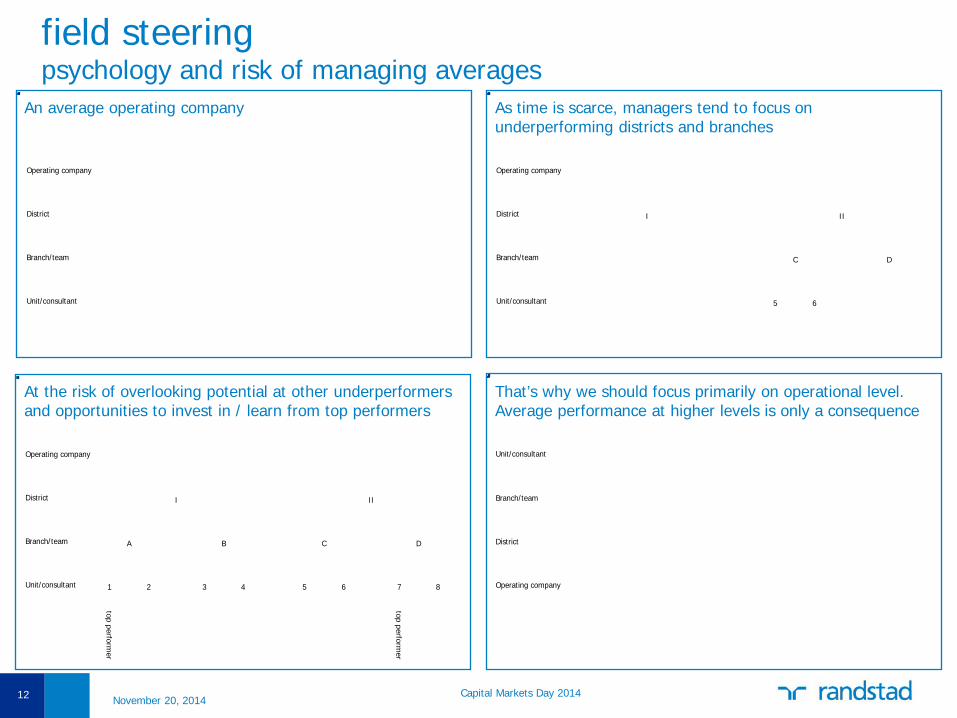

field steering psychology and risk of managing averages

12

An average operating company

District

Branch/team

Unit/consultant

Operating company

Where would any manager tend to focus?

I IIDistrict

Branch/team

Unit/consultant

Operating company

C D

5 6

What improvement potential would they have overlooked?

1 2 3 4

A B

I

5 6 7 8

C D

II

top performer

top performer

District

Branch/team

Unit/consultant

Operating company

That’s why we like to draw our company upside down

District

Branch/team

Operating company

Unit/consultant

As time is scarce, managers tend to focus on underperforming districts and branches

An average operating company

At the risk of overlooking potential at other underperformers and opportunities to invest in / learn from top performers

That’s why we should focus primarily on operational level. Average performance at higher levels is only a consequence

Capital Markets Day 2014 November 20, 2014

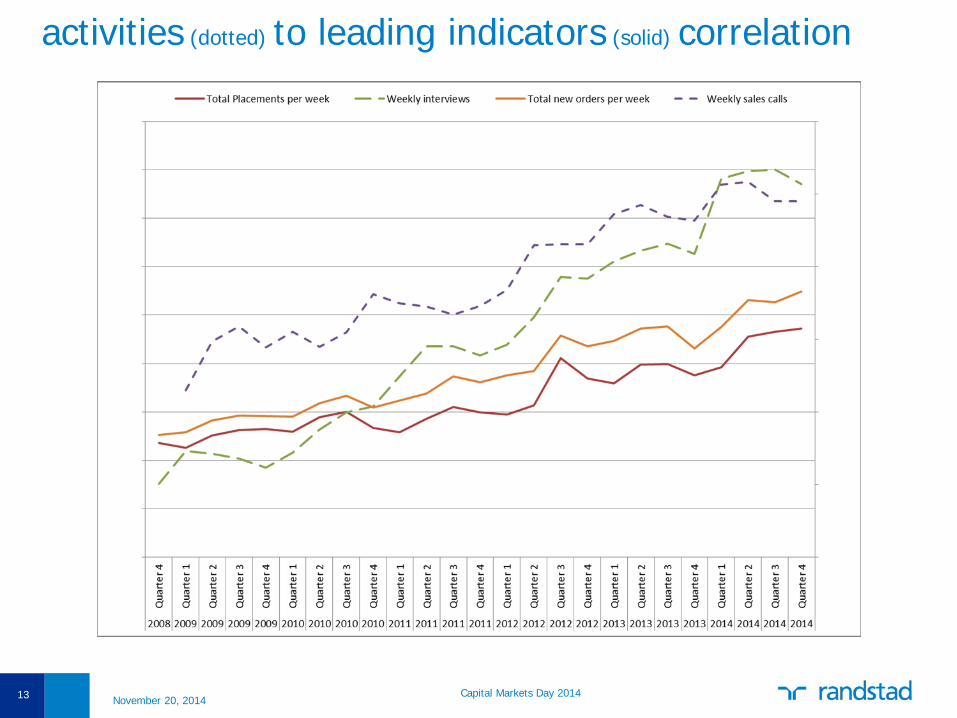

activities (dotted) to leading indicators (solid) correlation

13 Capital Markets Day 2014 November 20, 2014

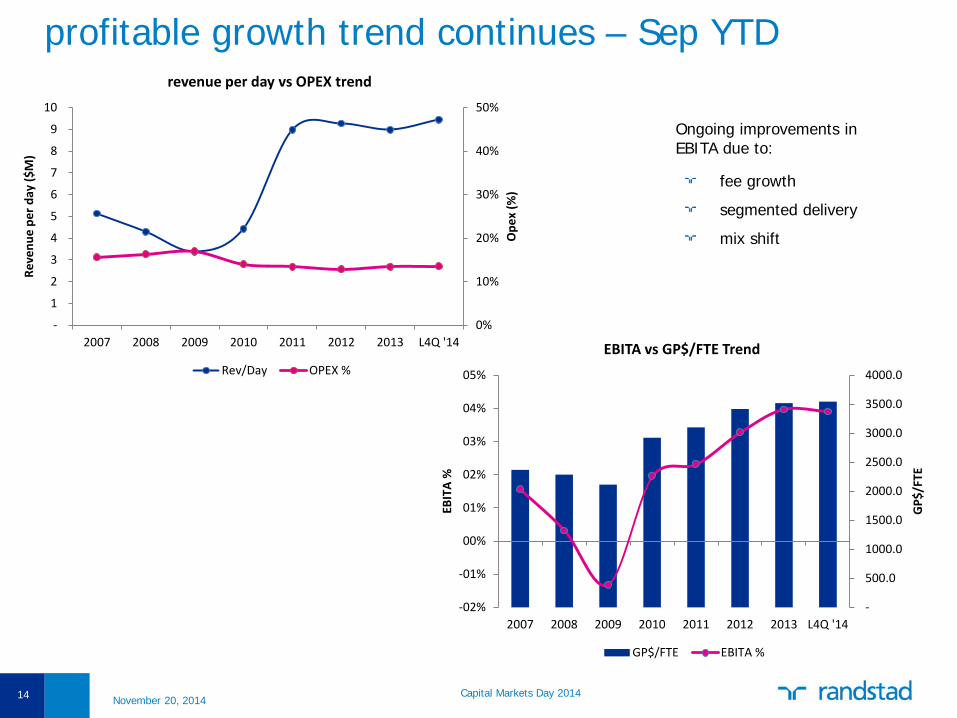

profitable growth trend continues – Sep YTD

14

Ongoing improvements in EBITA due to:

fee growth

segmented delivery

mix shift

Capital Markets Day 2014 November 20, 2014

0%

10%

20%

30%

40%

50%

-

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012 2013 L4Q '14

Ope

x (%

)

Reve

nue

per d

ay ($

M)

revenue per day vs OPEX trend

Rev/Day OPEX %

-

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

-02%

-01%

00%

01%

02%

03%

04%

05%

2007 2008 2009 2010 2011 2012 2013 L4Q '14

GP$

/FTE

EBIT

A %

EBITA vs GP$/FTE Trend

GP$/FTE EBITA %

continued accelerated growth in perm fees

15

-0.5%

0.5%

1.5%

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013 2014 annualized

Mill

ions

Fees Fees % of GM

L4Q ’14

Capital Markets Day 2014 November 20, 2014

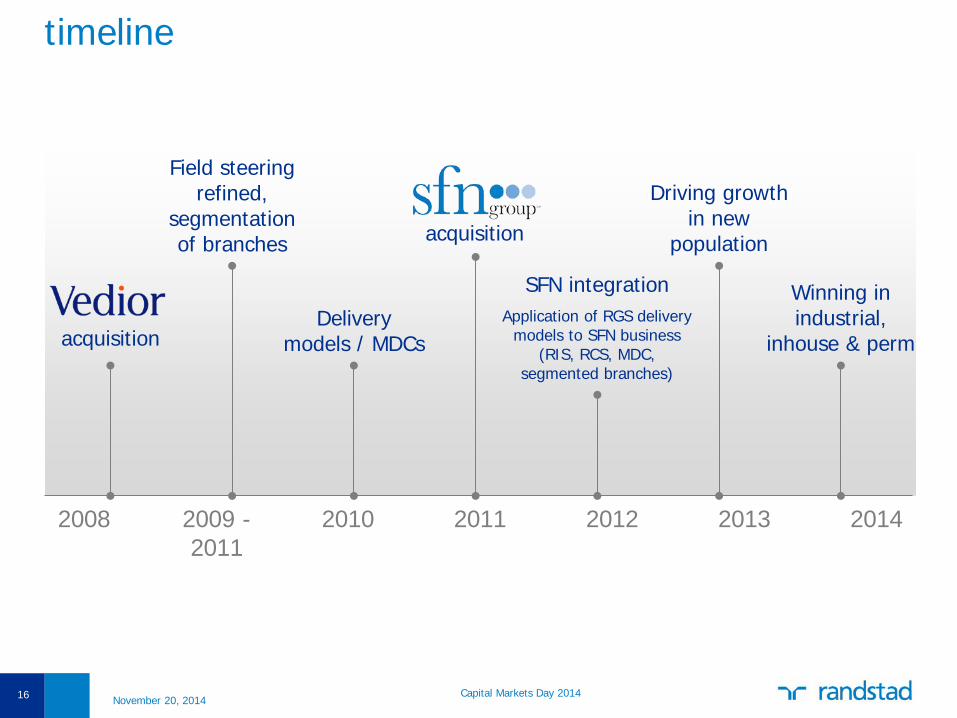

timeline

16

2008 2009 - 2011

2010 2011 2012 2013 2014

Field steering refined,

segmentation of branches

Delivery models / MDCs acquisition

SFN integration Application of RGS delivery

models to SFN business (RIS, RCS, MDC,

segmented branches)

Winning in industrial,

inhouse & perm

acquisition

Driving growth in new

population

Capital Markets Day 2014 November 20, 2014

going forward

17 Capital Markets Day 2014 November 20, 2014

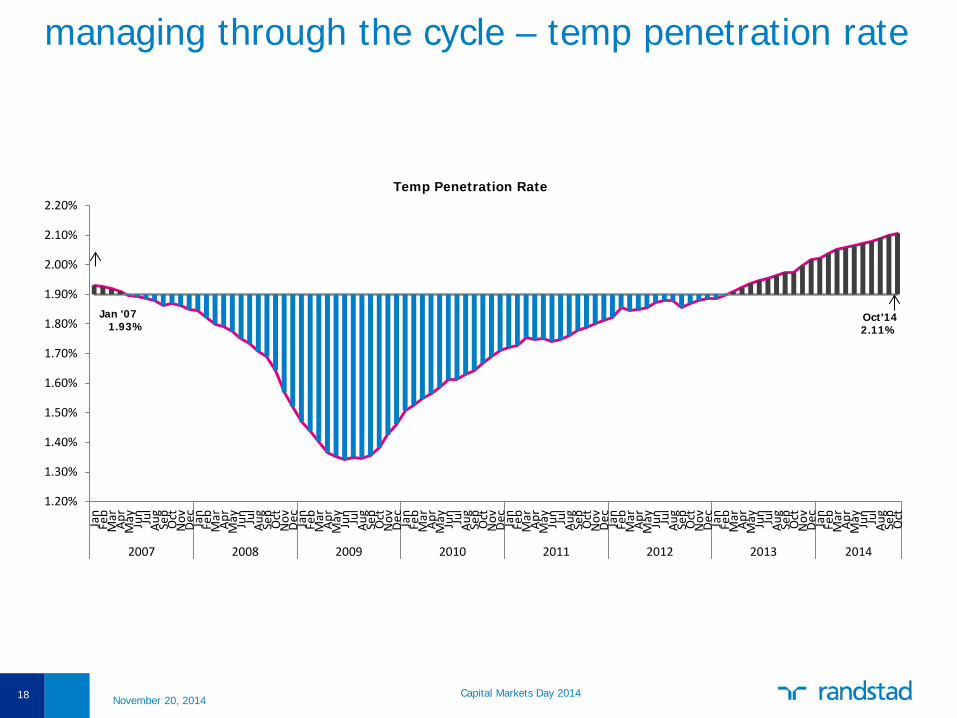

managing through the cycle – temp penetration rate

18

1.20%

1.30%

1.40%

1.50%

1.60%

1.70%

1.80%

1.90%

2.00%

2.10%

2.20%

Jan

Feb

Mar Ap

rM

ay Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

2007 2008 2009 2010 2011 2012 2013 2014

Temp Penetration Rate

Jan '07 1.93%

Oct'14 2.11%

Capital Markets Day 2014 November 20, 2014

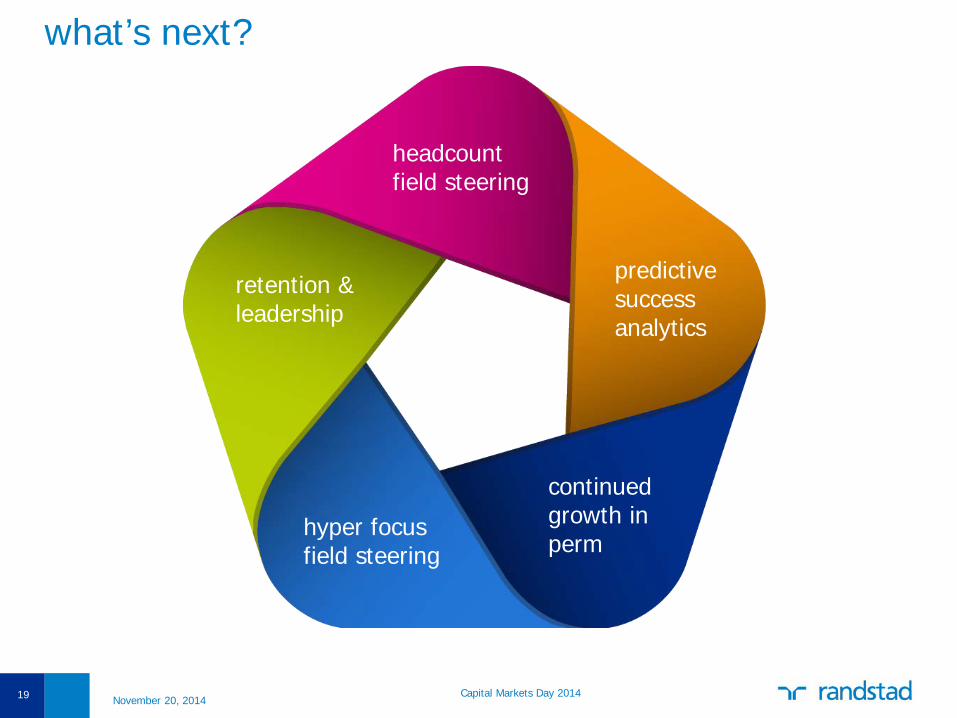

what’s next?

19

headcount field steering

retention & leadership

hyper focus field steering

continued growth in perm

predictive success analytics

Capital Markets Day 2014 November 20, 2014

20 Capital Markets Day 2014 November 20, 2014