winter 2014-15 us propane supply outlook · winter 2014-15 us propane supply outlook eia/naseo...

TRANSCRIPT

© 2014 IHS

Presentation

ihs.com

IHS

Winter 2014-15 US Propane Supply Outlook EIA/NASEO Winter Energy Outlook Conference

7 October 2014

Bill Veno, Senior Director, Natural Gas Liquids Research, +1 617 866 5118,

NGL RESEARCH

© 2014 IHS 2

Factors Underlying the 2013-14 Propane Shortage

© 2014 IHS

US propane price supply shortage was the result of

a convergence of unfavorable market fundamentals

The price spike in February of this year was the result of a convergence

of several factors:

• High propane demand for crop drying

• An unusually prolonged period of cold weather, leading to high heating

demand

• Rising exports of US propane to international markets

The confluence of these factors led to a rapid fall in primary propane

inventories and supply tightness that resulted in a surge in prices in the

Mid-Continent region.

• PADD II primary inventories dropped sharply starting in October 2013

and remained low through February 2014.

• The price spike was short-lived, as markets adjusted and prices

returned to normal levels relatively quickly.

• Production growth outpaced demand and exports, enabling stocks to

recover for the start of the 2014 - 2015 winter.

3

© 2014 IHS

US propane supply outlook depends primarily on

market fundamentals

Principal factors affecting propane supply and pricing include:

• Inventory levels at start of the heating season

• Winter weather

• Propane production – especially production from prolific wet shale gas

plays

• Demand – incl. weather-related and structural demand (e.g. chemicals)

• Exports – Availability of export capacity (as influenced by US propane

price competitiveness in foreign markets)

These are the principal factors expected to influence the outlook for

propane supply and prices in the winter of 2014-15, as well as in the

years ahead.

4

© 2014 IHS 5

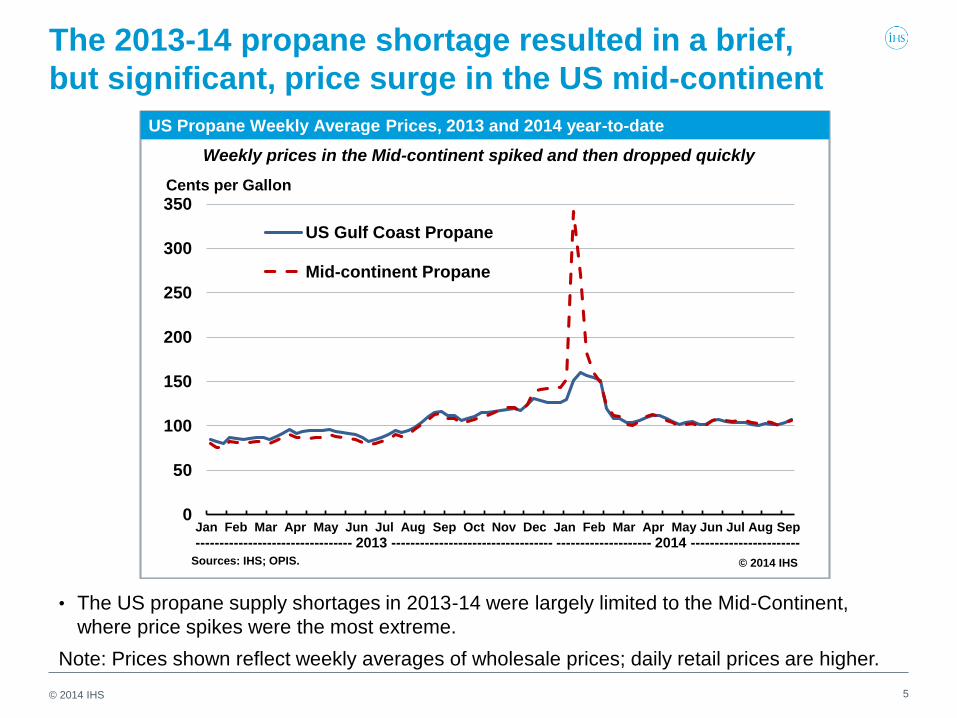

The 2013-14 propane shortage resulted in a brief,

but significant, price surge in the US mid-continent

0

50

100

150

200

250

300

350

JanJanFebMarMarAprMayMayJuneJulyAugAugSepOctOctNovDecDecJanFebMarMarAprMayMayJuneJuneJulyAugSep

US Gulf Coast Propane

Mid-continent Propane

US Propane Weekly Average Prices, 2013 and 2014 year-to-date

© 2014 IHS

Cents per Gallon

Sources: IHS; OPIS.

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

--------------------------------- 2013 ---------------------------------- -------------------- 2014 -----------------------

Weekly prices in the Mid-continent spiked and then dropped quickly

• The US propane supply shortages in 2013-14 were largely limited to the Mid-Continent,

where price spikes were the most extreme.

Note: Prices shown reflect weekly averages of wholesale prices; daily retail prices are higher.

© 2014 IHS 6

Waterborne exports of propane have been rising rapidly,

but dropped in February and March as prices spiked

0

2

4

6

8

10

12

14

Monthly Annual

US Waterborne Propane Exports – Monthly and Annual Averages, 2007 to 2014 ytd

© 2014 IHS

Thousand Barrels per Month

Sources: IHS Waterborne; US Department of Energy.

Waterborne propane exports soared during 2013 and 2014

• When US propane price differentials relative to other regions collapsed, waterborne exports

dropped.

• Exports subsequently rose sharply when the price incentives improved.

© 2014 IHS 7

The North Central US experienced a significantly

colder winter in 2013-14

• PADD II (North Central) region had 25% higher heating degree-days in the 2013-14 heating season

(Oct- Mar) compared to the same period in 2012-13, and 35% higher than in the winter of 2011-12.

• Winter of 2013-14 reflects a period colder and longer period than normal.

• Additional demand for crop drying (primarily for corn prior to storage) exacerbated the demand

impact experienced in PADD II region.

0

200

400

600

800

1,000

1,200

1,400

1,600

Oct Nov Dec Jan Feb Mar

2013-14

2012-13

2011-12

US PADD II Heating Degree Days

© 2014 IHS

Heating Degree Days

Source: IHS

2013-14 less 2012-13

2013-14 less 2011-12

© 2014 IHS 8

US propane demand in 2013-14 trended higher, with

gains in res/com offsetting a decline in chemicals

• Propane demand in both the residential/commercial and agriculture sectors exhibit weather-

related seasonality.

• Upward trend apparent in weather-related demand.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14

Chemicals Residential/Commercial

Farm, Industry, Engine Fuel

US Propane Demand by End-Use Sector

© 2014 IHS

Thousand Barrels per Day

Source: IHS

Trend

© 2014 IHS 9

The residential/commercial sector exhibits the

greatest weather-related seasonality of any sector

• Weather-related and seasonal gains in residential/commercial and agriculture demand were

key contributing factors in the propane supply shortage in 2013-14.

• The rise in propane prices prompted a decrease in chemical feedstock demand, partially

offsetting the increase in res/com and agriculture demand.

0

100

200

300

400

500

600

700

800

900

1,000

Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14

Residential/Commercial Farm, Industry, Engine Fuel

Chemicals

US Propane Demand by End Use Sector

© 2014 IHS

Thousand Barrels per Day

Source: IHS

© 2014 IHS 10

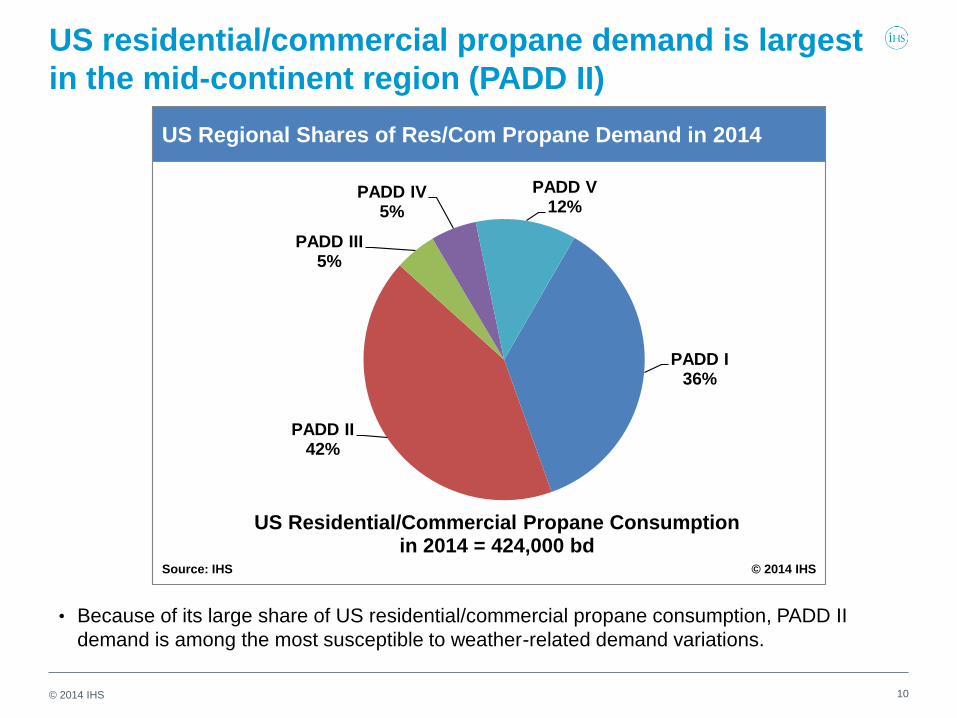

US residential/commercial propane demand is largest

in the mid-continent region (PADD II)

• Because of its large share of US residential/commercial propane consumption, PADD II

demand is among the most susceptible to weather-related demand variations.

PADD I36%

PADD II42%

PADD III5%

PADD IV5%

PADD V12%

US Regional Shares of Res/Com Propane Demand in 2014

© 2014 IHSSource: IHS

US Residential/Commercial Propane Consumption in 2014 = 424,000 bd

© 2014 IHS 11

Mid-Continent inventories dropped sharply starting in

October 2013, but have recovered strongly in 2014

• PADD II primary stocks dropped well below the normal range during the winter of 2013-14 …

… but recovered strongly during the 2nd and 3rd quarters

0

5

10

15

20

25

30

35

Jan 08 Feb 12 Mar 19 Apr 23 May 28 Jul 02 Aug 06 Sep 10 Oct 15 Nov 19 Dec 24

Million Barrels

2014

2013

2012

PADD II Primary Inventories

Source: IHS © 2014 IHS

2007-2011 Range of Maximum and

Minimum Invenories

© 2014 IHS 12

Total US primary inventories also recovered rapidly,

significantly exceeding the 2007-2013 maximum levels

0

10

20

30

40

50

60

70

80

90

Jan 08 Feb 12 Mar 19 Apr 23 May 28 Jul 02 Aug 06 Sep 10 Oct 15 Nov 19 Dec 24

Million Barrels

2014

2013

2012

Total US Propane Primary Inventories

Source: IHS © 2014 IHS

2007-2011 Range of Max and Min Primary Inventories (shaded

range)

• By mid-year, total US propane inventories had climbed rapidly, and are well above the

normal range at the start of the 2014-15 heating season.

© 2014 IHS 13

US Propane Supply Outlook for 2014-15

© 2014 IHS

US propane market in 2014-15: Outlook for the

coming winter depends on market fundamentals

• The US and PADD II markets responded quite well during the 2013-14

shortage, and the price spike was relatively temporary.

• US propane production continues to rise faster than growth in demand

and exports, enabling inventories to recover rapidly.

• US propane inventories have gone from near-record lows in early 2014

to near-record highs at the start of October.

• PADD II primary inventories have recovered to their highest October

levels since the economic collapse of 2009.

• Propane production from gas processing will sustain a rapid pace of

growth through 2015.

• US propane demand growth is projected to be modest, increasing by

just 1% in 2015.

• Propane exports will continue to grow as expanded and new export

capacity comes on line.

14

© 2014 IHS 15

US propane production from gas processing will be

driven by strong growth in shale gas production

• Rapidly rising shale gas production will drive corresponding growth in US propane

production; US propane from gas processing will rise nearly 20% in 2014, followed by 8%

growth in 2015.

0

200

400

600

800

1,000

1,200

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

US Propane Production from Gas Processing

© 2014 IHS

Thousand Barrels per Day

Sources: IHS, US Department of Energy

959

808

1,040US propane production from

gas processing will average

about 960 kbd in 2014, a 19%

increase over 2013

© 2014 IHS 16

US propane production from gas processing will be

driven by strong growth in shale gas production

• Most of the increase in NGL production will come from shale gas development in the

Marcellus, Utica and Bakken plays – all located in proximity to the mid-continent.

0

200

400

600

800

1,000

1,200

1,400

2010 2011 2012 2013 2014 2015 2016 2017 2018

Barnett

Woodford

Niobrara

Eagle Ford

Bakken

Marcellus

Utica

Total NGL Production by Major Shale Play

© 2014 IHS

Thousand Barrels per Day

Source: IHS

Marcellus, Utica and Bakken will account for about half of total

NGL production from shale plays

© 2014 IHS 17

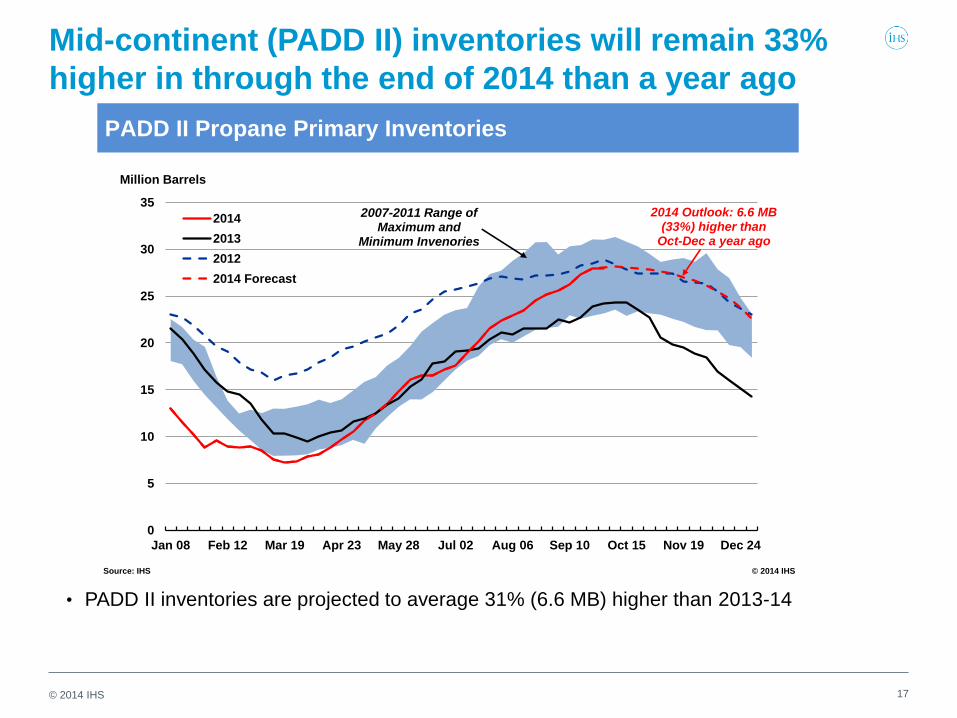

Mid-continent (PADD II) inventories will remain 33%

higher in through the end of 2014 than a year ago

• PADD II inventories are projected to average 31% (6.6 MB) higher than 2013-14

0

5

10

15

20

25

30

35

Jan 08 Feb 12 Mar 19 Apr 23 May 28 Jul 02 Aug 06 Sep 10 Oct 15 Nov 19 Dec 24

Million Barrels

2014

2013

2012

2014 Forecast

PADD II Propane Primary Inventories

Source: IHS © 2014 IHS

2007-2011 Range of Maximum and

Minimum Invenories

2014 Outlook: 6.6 MB (33%) higher than

Oct-Dec a year ago

© 2014 IHS 18

Total US primary inventories through the end of this

year will remain significantly higher than a year ago

0

10

20

30

40

50

60

70

80

90

Jan 08 Feb 12 Mar 19 Apr 23 May 28 Jul 02 Aug 06 Sep 10 Oct 15 Nov 19 Dec 24

Million Barrels

2014

2013

2012

2014 Forecast

Total US Propane Primary Inventories

Source: IHS © 2014 IHS

2007-2011 Range of Max and Min Primary Inventories (shaded

range)

2014 Outlook: 18.1 MB (31%) higher than Oct-Dec

a year ago

© 2014 IHS

US propane market in 2014-15:

Conclusions

Looking ahead at US and PADD II propane availability during the winter

of 2014-15, we expect that, despite an increase in domestic demand and

waterborne exports:

• Inventories will remain comfortable, and ample to meet projected

demand in the US and PADD II without a recurrence of last year’s

shortages.

• There is plenty of propane available to meet market demand.

• The high propane prices experienced last winter lasted only a short

time, roughly one month.

• Logistics capacity expansions and other measures are being taken by

various states in response to last year’s shortage.

19

© 2014 IHS

US propane market in 2014-15 and beyond: Factors

to monitor that could impact the supply outlook

• Propane demand for chemical feedstock use will increase with the

addition of new propane dehydrogenation (PDH) capacity – but these

additions will not affect the outlook for 2014-15.

• Propane exports will grow as new export terminal capacity is added in

the Gulf Coast region (increased during 2nd half 2014 and additional

expansions are scheduled for 2015).

• Logistics capacity changes are needed to accommodate changes in

US propane production, demand and exports in 2015 and beyond.

• Overall, supply and infrastructure additions are expected to keep pace

with production growth.

20

IHS Customer Care:

• Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected]

• Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected]

• Asia and the Pacific Rim: +604 291 3600; [email protected]

© 2014 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS.

Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the

opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. For more

information, please contact IHS Customer Care (see phone numbers and email addresses listed above). All products, company names, or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.