winter 2016 nonprofit fundraising study · overall ... missing goal linked with economy ... figure...

TRANSCRIPT

Winter 2016

Nonprofit Fundraising Study

Covering Charitable Receipts at Nonprofit Organizations in

the United States and Canada in 2015

March 2016

A Study From

Nonprofit Fundraising Survey March 2016

Acknowledgements

The Nonprofit Research Collaborative (NRC) thanks all respondents who took the

survey in January and February 2016. Your willingness to share information about

your organization makes it possible for this report to appear.

Most importantly, we thank every individual who made this report possible, from

concept and survey design through data analysis and proofreading. These include the

NRC committee, Lynn Lukins at Data Analytics & Research Solutions for data analysis,

Linh Preston at Fogus Consulting & Writing for writing and editing assistance, and

Gabrielle Robbins for proofreading.

Members of the Nonprofit Research Collaborative are

© Winter 2016 Nonprofit Fundraising Survey, Copyright 2016

Nonprofit Research Collaborative

Project management by

For permission to cite or reproduce, please contact Melissa Brown at

[email protected]. This report, PowerPoint slides based on graphics in this

report, infographics on selected NRC findings, and links to earlier reports can be found

at www.NPResearch.org.

Nonprofit Fundraising Survey i March 2016

CONTENTS List of Figures .................................................................................................................................... iii List of Tables ...................................................................................................................................... iv KEY FINDINGS ..................................................................................................................................... 1 KEY TRENDS ........................................................................................................................................ 2 INTRODUCTION ................................................................................................................................. 3 SECTION I: 2015 results .................................................................................................................... 4

65% of charities reported growth in charitable receipts ........................................................ 4 Organizations attribute success to major gifts, bequests, and working smarter overall ........................................................................................................................................... 5

Changes in charitable receipts by organizational size ........................................................... 6 Larger organizations more likely than smaller to see increases ....................................... 6 Across size groups, increase in the share of organizations reporting higher fundraising revenue compared with last year at this time ................................................ 7

Changes in charitable receipts by type of organization ......................................................... 8 Health and Arts organizations report greatest fluctuation among subsectors ............. 8

Change in charitable receipts by region .................................................................................. 10 Growth highest in U.S. West, lowest in U.S. South ............................................................. 10

Predicted change in charitable receipts compared with actual results ............................. 12 Nearly three-quarters met 2015 fundraising goal ................................................................. 13 Organizations attribute success to hard work; missing goal linked with economy or leadership challenges ............................................................................................................. 14

Smaller organizations remain less likely than larger ones to meet goals ..................... 15 Canadian organizations most likely to meet fundraising goal ....................................... 17

SECTION II: Fundraising methods FOR 2015 .............................................................................. 19 Direction of change in charitable receipts in 2015 by methods used ........................... 20 Organizations that do not see an increase in overall fundraising results are much less likely to see increases in most fundraising methods .................................... 24

SECTION III: TRENDS SINCE 2005 ................................................................................................. 27 Trends in changes in charitable receipts by methods often asked in person, 2005-2015 ................................................................................................................................................ 28 Trends in changes in charitable receipts via a specific communication medium, and special events, 2005-2015 .................................................................................................. 30 Trends in changes in charitable receipts from institutional donors, 2005-2015 ............ 33

SECTION IV: SPECIAL SECTION ON BEQUESTS ........................................................................... 35 More than 2/3rds of organizations raise funds with bequests .......................................... 35

Higher education organizations are the most likely to receive bequest dollars ......... 36 Larger organizations are more likely to receive bequests ................................................ 37 Bequest amounts received ...................................................................................................... 38 Average bequest amount most frequently between $25,000 and $100,000 ................ 39 Smaller organizations most likely to receive lower total from bequests ...................... 40

SECTION V: Outlook for 2016........................................................................................................ 41 CONCLUSION .................................................................................................................................... 45 METHODOLOGY ............................................................................................................................... 46

Statistical significance ................................................................................................................. 49 About the Nonprofit Research Collaborative ............................................................................. 50

Appendix I: Survey questions

Nonprofit Fundraising Survey ii March 2016

LIST OF FIGURES

Figure 1: Percentage of responding organizations reporting change in charitable receipts, 2015 compared with 2014 ....................................................................................... 5

Figure 2: Percentage of responding organizations reporting change in charitable receipts by size, 2015 compared with 2014 ......................................................................... 7

Figure 3: Share of responding organizations seeing an increase in fundraising revenue by size, 2015 compared with 2014 ......................................................................... 7

Figure 4: Percentage of responding organizations reporting change in charitable receipts by subsector, 2015 compared with 2014 ............................................................... 8

Figure 5: Percentage of responding organizations reporting change in charitable receipts by U.S. region and Canada, 2015 compared with 2014 ..................................... 10

Figure 6: Percentage of responding organizations reporting change in charitable receipts by U.S. region and Canada, 2015 compared with 2014 and 2014 compared with 2013 ................................................................................................................ 11

Figure 7: Predicted results for 2015 compared with actual results ....................................... 12

Figure 8: Did your organization meet its fiscal year 2015 fundraising goal? ...................... 13

Figure 9: Trend in percentage of organizations meeting fundraising goal, 2010-2015 .... 13

Figure 10: Words provided to explain meeting goals ............................................................... 14

Figure 11: Words provided to explain not meeting fundraising goal .................................... 15

Figure 12: Percentage of responding organizations meeting 2015 fundraising goal by organizational size ................................................................................................................... 16

Figure 13: Percentage by whether the responding organization met its 2015 fundraising goal, by region ..................................................................................................... 17

Figure 14: Percentage of responding organizations that use each of 15 fundraising methods ...................................................................................................................................... 19

Figure 15: Percentage of organizations reporting change in charitable receipts by most frequently used fundraising method, 2015 compared with 2014 ....................... 20

Figure 16: Percentage of organizations reporting change in charitable receipts by less frequently used fundraising method, 2015 compared with 2014 .................................. 21

Figure 17: Percentage of organizations reporting change in charitable receipts by least used fundraising method with slight increases, 2015 compared with 2014 ...... 23

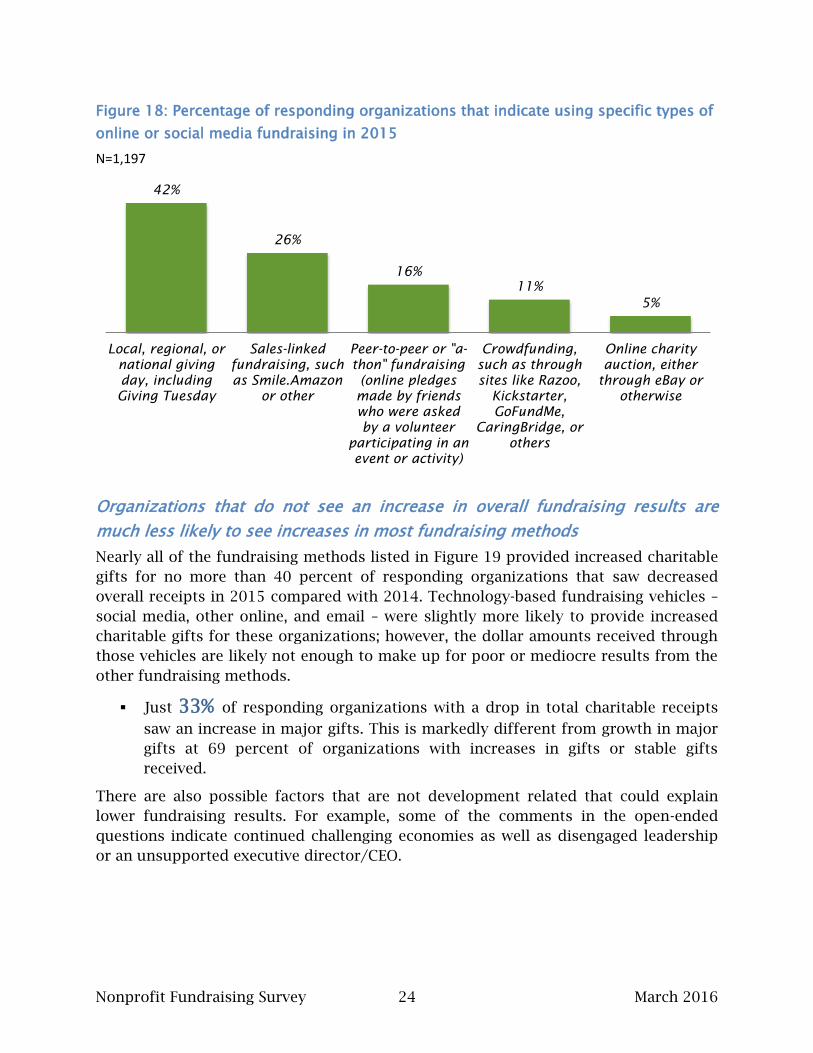

Figure 18: Percentage of responding organizations that indicate using specific types of online or social media fundraising in 2015 ................................................................... 24

Figure 19: Percentage of respondents reporting an increase in funds raised by method and by whether the organization’s overall charitable receipts increased from 2014 to 2015 ................................................................................................................... 26

Figure 20: Percentage of responding organizations reporting change in charitable receipts by year, 2005-2015 ................................................................................................... 27

Figure 21: Percentage of responding organizations reporting change in contributions received from major gifts, 2005-2015 .................................................................................. 28

Figure 22: Percentage of responding organizations reporting change in contributions received through board giving, 2010-2015 ......................................................................... 28

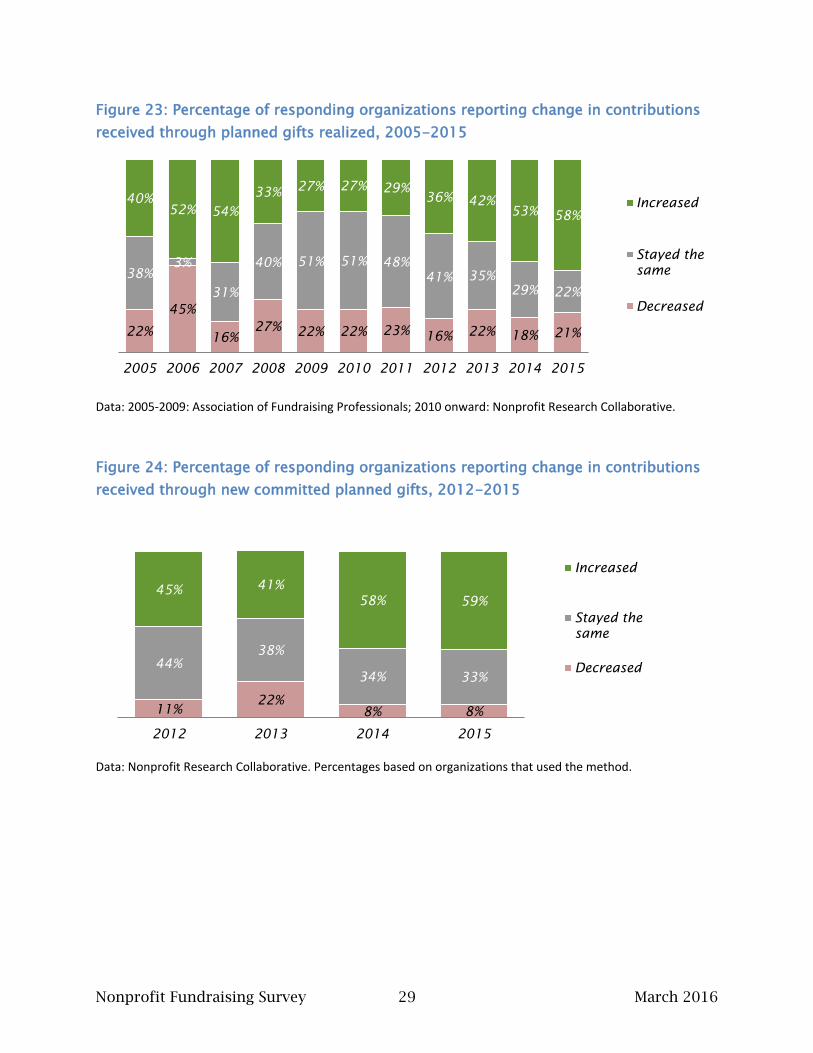

Figure 23: Percentage of responding organizations reporting change in contributions received through planned gifts realized, 2005-2015 ........................................................ 29

Nonprofit Fundraising Survey iii March 2016

Figure 24: Percentage of responding organizations reporting change in contributions received through new committed planned gifts, 2012-2015 ........................................... 29

Figure 25: Percentage of responding organizations reporting change in contributions received through direct mail, 2005-2015 ............................................................................ 30

Figure 26: Percentage of responding organizations reporting change in contributions received by other online, 2005-2015 .................................................................................... 31

Figure 27: Percentage of responding organizations reporting change in contributions received through special events, 2005-2015 ....................................................................... 31

Figure 28: Percentage of responding organizations reporting change in contributions received through telephone appeals, 2005-2015 ............................................................... 32

Figure 29: Percentage of responding organizations reporting change in contributions received through foundation grantmaking, 2010-2015 .................................................... 33

Figure 30: Percentage of responding organizations reporting change in contributions received through corporate giving and corporate foundation grantmaking, 2010-2015 ............................................................................................................................................ 33

Figure 31: Percentage of responding organizations reporting change in contributions received through federated campaigns, 2011-2015 .......................................................... 34

Figure 32: Percentage of responding organizations reporting change in contributions received from congregations, 2011-2015 ............................................................................ 34

Figure 33: Percentage of responding organizations that received bequests in 2015 by subsector .................................................................................................................................... 36

Figure 34: Percentage of responding organizations that received bequests in 2015 by organization size ...................................................................................................................... 37

Figure 35: Percentage of responding organizations that received bequests in 2015 by total amount of bequest dollars ............................................................................................ 38

Figure 36: Percentage of responding organizations that received bequests in 2015 by average size of bequest amount ............................................................................................ 39

Figure 37: Percentage of responding organizations that received bequests in 2015 by greatest and least total amounts and by organization size ............................................. 40

Figure 38: Anticipated direction of change in charitable receipts, 2016 compared with 2015 ............................................................................................................................................ 41

Figure 39: Responses about anticipated challenges to 2016 fundraising, compared with what most negatively affected 2015 results .............................................................. 42

Figure 40: Responses about anticipated positive impact to 2016 fundraising, compared with what most positively affected 2015 results ............................................ 43

Figure 41: Percentage of responding charities by Census region compared with registered charities IRS and Business Master File, July 2013 .......................................... 47

Figure 42: Responding charities expenditure total, compared with reporting charities filing IRS forms ......................................................................................................................... 48

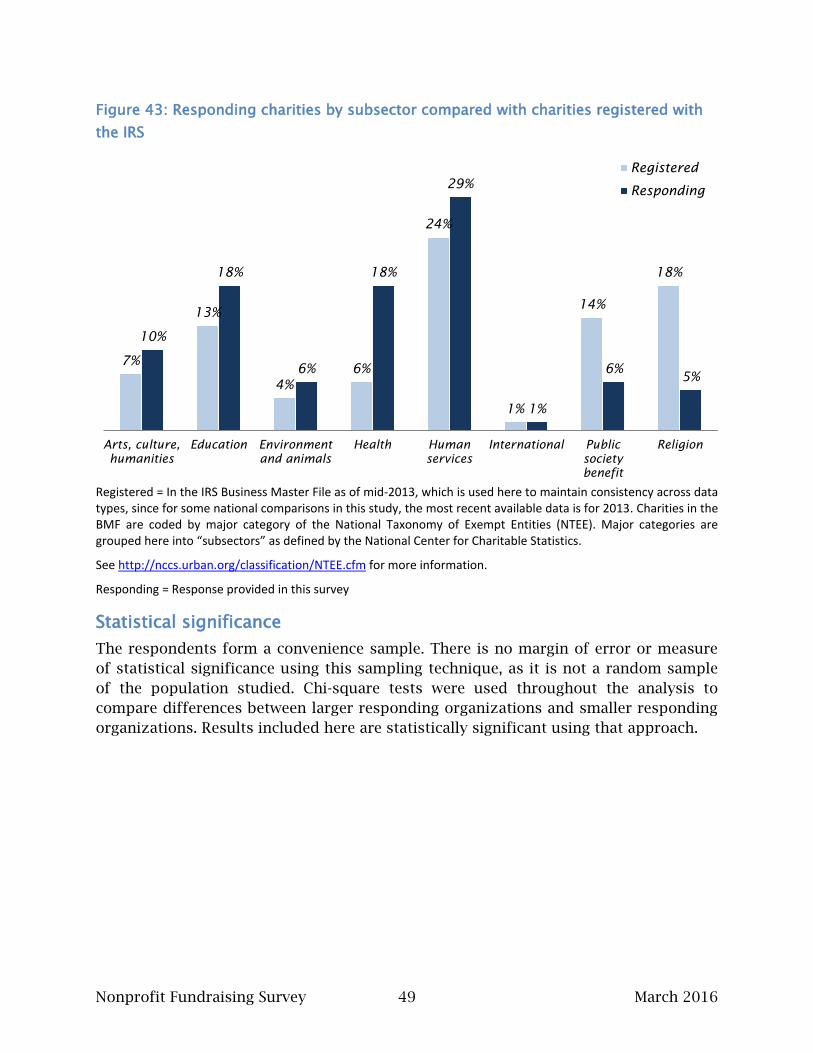

Figure 43: Responding charities by subsector compared with charities registered with the IRS ......................................................................................................................................... 49

Nonprofit Fundraising Survey iv March 2016

LIST OF TABLES Table 1: Trend in percentage of responding organizations reporting an increase in

charitable receipts, 2015-2010 .............................................................................................. 4

Table 2: Trend in percentage of responding organizations reporting a change in increased charitable receipts by subsector, 2015-2013.................................................... 9

Table 3: Trend in percentage of responding organizations reporting increased charitable receipts by subsector, 2015-2013. ..................................................................... 9

Table 4: Trend in percentage of responding organizations reporting decreased charitable receipts by subsector, 2015-2014 ...................................................................... 9

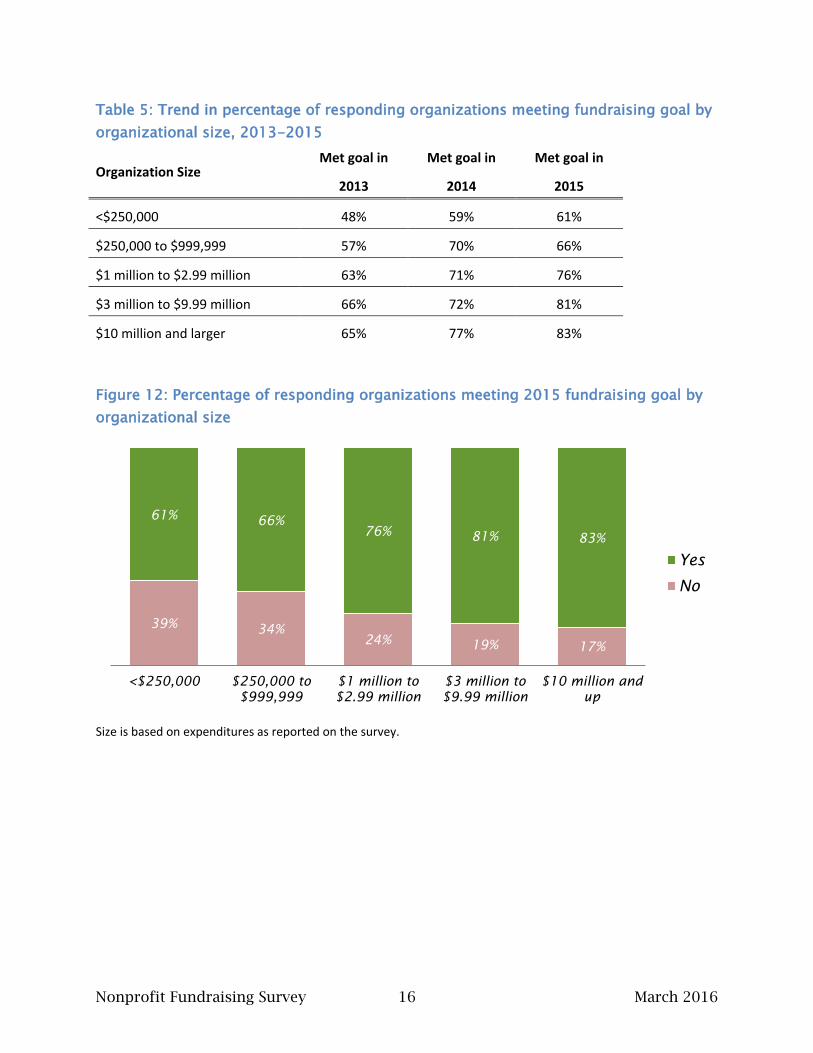

Table 5: Trend in percentage of responding organizations meeting fundraising goal by organizational size, 2013-2015 ...................................................................................... 16

Nonprofit Fundraising Survey 1 March 2016

KEY FINDINGS

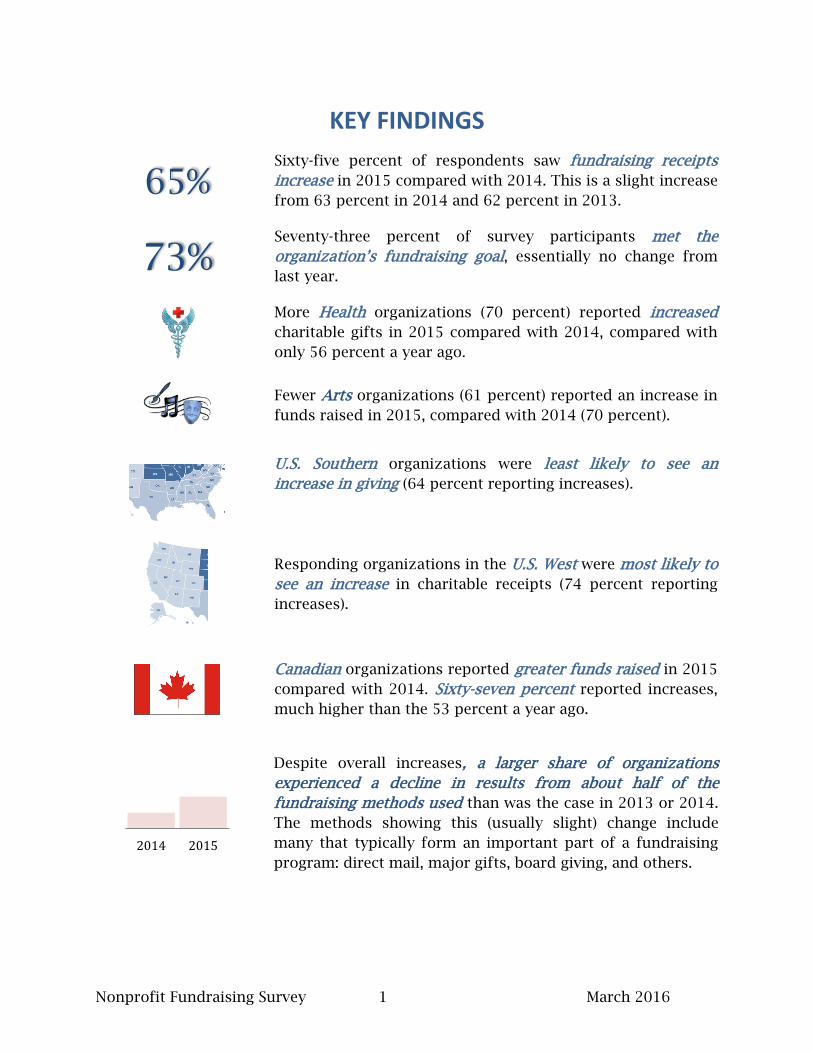

65% Sixty-five percent of respondents saw fundraising receipts

increase in 2015 compared with 2014. This is a slight increase

from 63 percent in 2014 and 62 percent in 2013.

73%Seventy-three percent of survey participants met the

organization’s fundraising goal, essentially no change from

last year.

More Health organizations (70 percent) reported increased

charitable gifts in 2015 compared with 2014, compared with

only 56 percent a year ago.

Fewer Arts organizations (61 percent) reported an increase in

funds raised in 2015, compared with 2014 (70 percent).

U.S. Southern organizations were least likely to see an

increase in giving (64 percent reporting increases).

Responding organizations in the U.S. West were most likely to

see an increase in charitable receipts (74 percent reporting

increases).

Canadian organizations reported greater funds raised in 2015

compared with 2014. Sixty-seven percent reported increases,

much higher than the 53 percent a year ago.

Despite overall increases, a larger share of organizations

experienced a decline in results from about half of the

fundraising methods used than was the case in 2013 or 2014.

The methods showing this (usually slight) change include

many that typically form an important part of a fundraising

program: direct mail, major gifts, board giving, and others. 2014 2015

Nonprofit Fundraising Survey 2 March 2016

KEY TRENDS

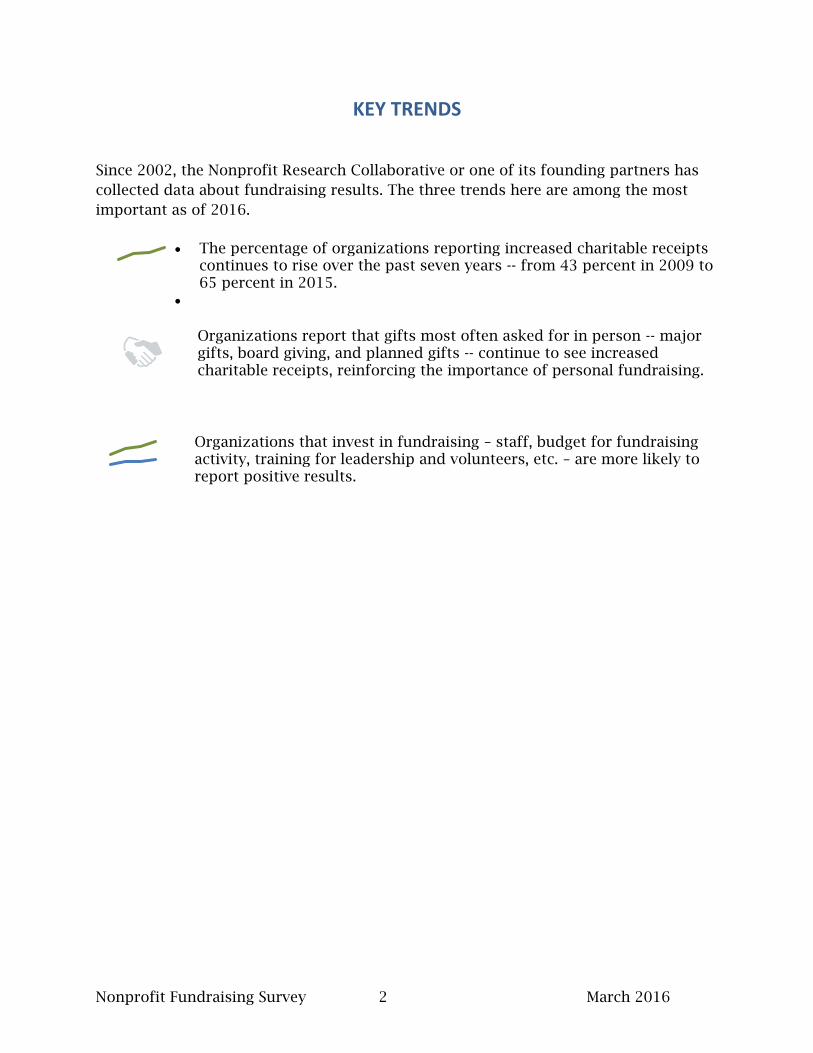

Since 2002, the Nonprofit Research Collaborative or one of its founding partners has

collected data about fundraising results. The three trends here are among the most

important as of 2016.

The percentage of organizations reporting increased charitable receiptscontinues to rise over the past seven years -- from 43 percent in 2009 to65 percent in 2015.

Organizations report that gifts most often asked for in person -- major gifts, board giving, and planned gifts -- continue to see increased charitable receipts, reinforcing the importance of personal fundraising.

Organizations that invest in fundraising – staff, budget for fundraising activity, training for leadership and volunteers, etc. – are more likely to report positive results.

Nonprofit Fundraising Survey 3 March 2016

INTRODUCTION

A stronger economy and lower unemployment rates helped nonprofit organizations

see little change in the amount of charitable gifts received in 2015; however, many are

concerned that growth will actually decrease as donors are uneasy over an unstable

economy and the political environment leading up to the U.S. Presidential election. For

the first time since the Nonprofit Fundraising Survey began tracking Canadian

organizations separately, the results for that nation are very comparable to the results

for the United States. This report reveals to what extent a wide range of charitable

organizations in the United States and Canada saw increases, decreases, or no change

in charitable receipts in 2015.

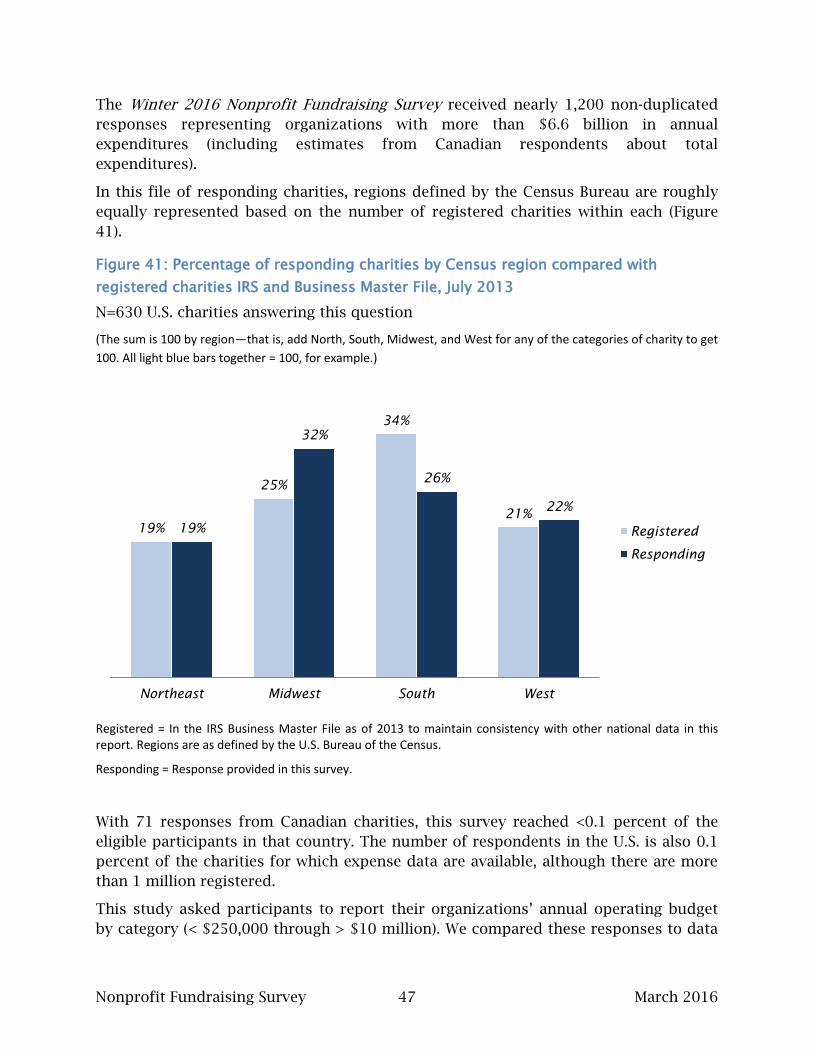

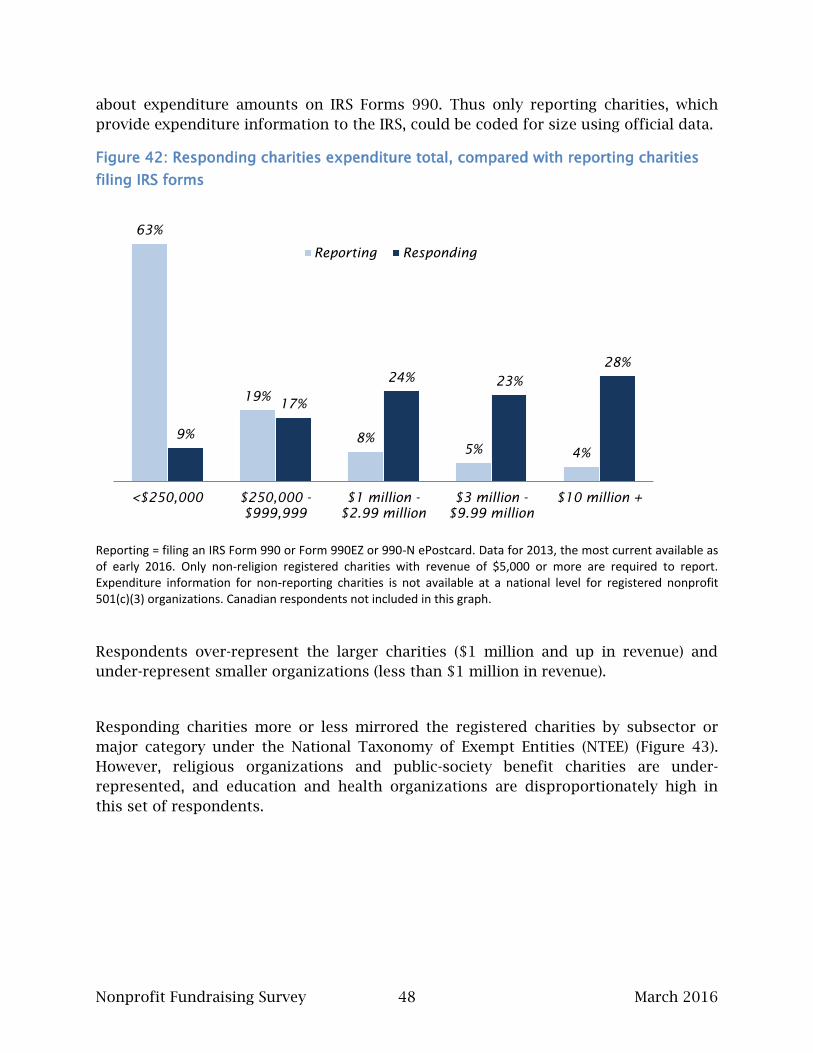

Nearly 1,200 organizations answered Nonprofit Research Collaborative (NRC) survey

questions in early 2016 about charitable receipts from January through December

2015. Responding charitable groups included large and small organizations (by budget

size) and organizations from every subsector, Arts through Religion. Findings are

based on responses remaining after data cleaning, 1,197 total, including 71 from

Canada.

Questions ranged from changes in charitable receipt amounts in 2015, compared with

2014, to expectations for 2016. These findings can help an organization plan for its

fundraising efforts. We share results about charitable receipts in 2015 and compare

those with findings from similar surveys from 2005 through 2014. This section also

compares what charities predicted would happen in 2015 with what actually did.

One of the unique features of the NFS is our trend data, which covers findings about

charitable receipts from more than a dozen different fundraising methods. This report

includes trends for 2005 through 2015 by method.

The survey also asked about expectations for charitable receipts in 2016 and gave

respondents a chance to comment on specific challenges or trends they anticipate

affecting their fundraising this year.

Nonprofit Fundraising Survey 4 March 2016

SECTION I: 2015 RESULTS

This section presents overall results, results by size (determined by expenditures), by

subsector, and by region.

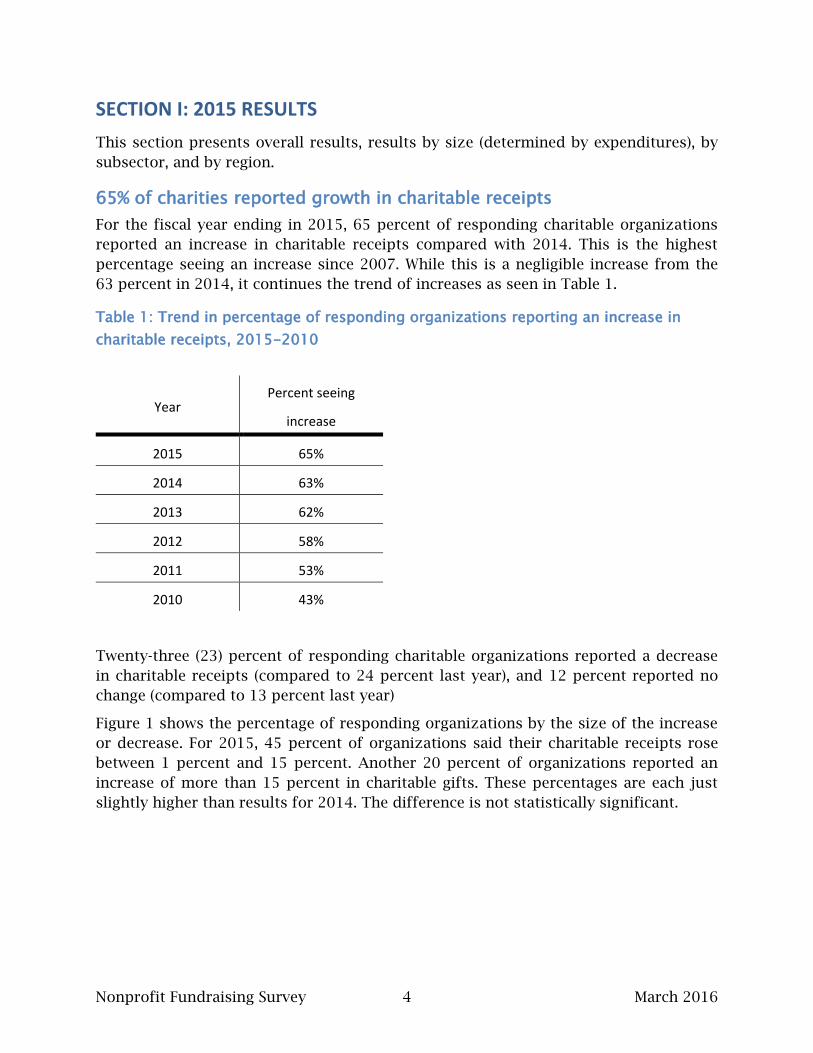

65% of charities reported growth in charitable receipts

For the fiscal year ending in 2015, 65 percent of responding charitable organizations

reported an increase in charitable receipts compared with 2014. This is the highest

percentage seeing an increase since 2007. While this is a negligible increase from the

63 percent in 2014, it continues the trend of increases as seen in Table 1.

Table 1: Trend in percentage of responding organizations reporting an increase in

charitable receipts, 2015-2010

Year Percent seeing

increase

2015 65%

2014 63%

2013 62%

2012 58%

2011 53%

2010 43%

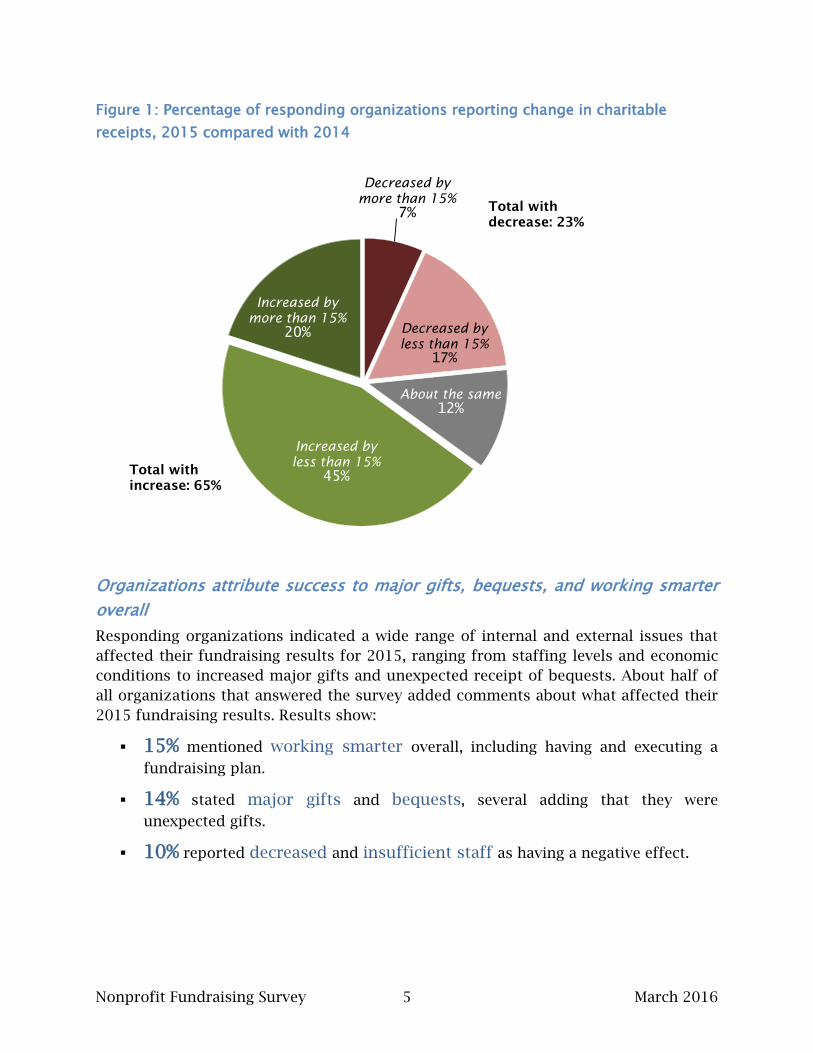

Twenty-three (23) percent of responding charitable organizations reported a decrease

in charitable receipts (compared to 24 percent last year), and 12 percent reported no

change (compared to 13 percent last year)

Figure 1 shows the percentage of responding organizations by the size of the increase

or decrease. For 2015, 45 percent of organizations said their charitable receipts rose

between 1 percent and 15 percent. Another 20 percent of organizations reported an

increase of more than 15 percent in charitable gifts. These percentages are each just

slightly higher than results for 2014. The difference is not statistically significant.

Nonprofit Fundraising Survey 5 March 2016

Figure 1: Percentage of responding organizations reporting change in charitable

receipts, 2015 compared with 2014

Organizations attribute success to major gifts, bequests, and working smarter

overall

Responding organizations indicated a wide range of internal and external issues that

affected their fundraising results for 2015, ranging from staffing levels and economic

conditions to increased major gifts and unexpected receipt of bequests. About half of

all organizations that answered the survey added comments about what affected their

2015 fundraising results. Results show:

15% mentioned working smarter overall, including having and executing a

fundraising plan.

14% stated major gifts and bequests, several adding that they were

unexpected gifts.

10% reported decreased and insufficient staff as having a negative effect.

Decreased by

more than 15%

7%

Decreased by

less than 15%

17%

About the same

12%

Increased by

less than 15%

45%

Increased by

more than 15%

20%

Total with

increase: 65%

Total with

decrease: 23%

Nonprofit Fundraising Survey 6 March 2016

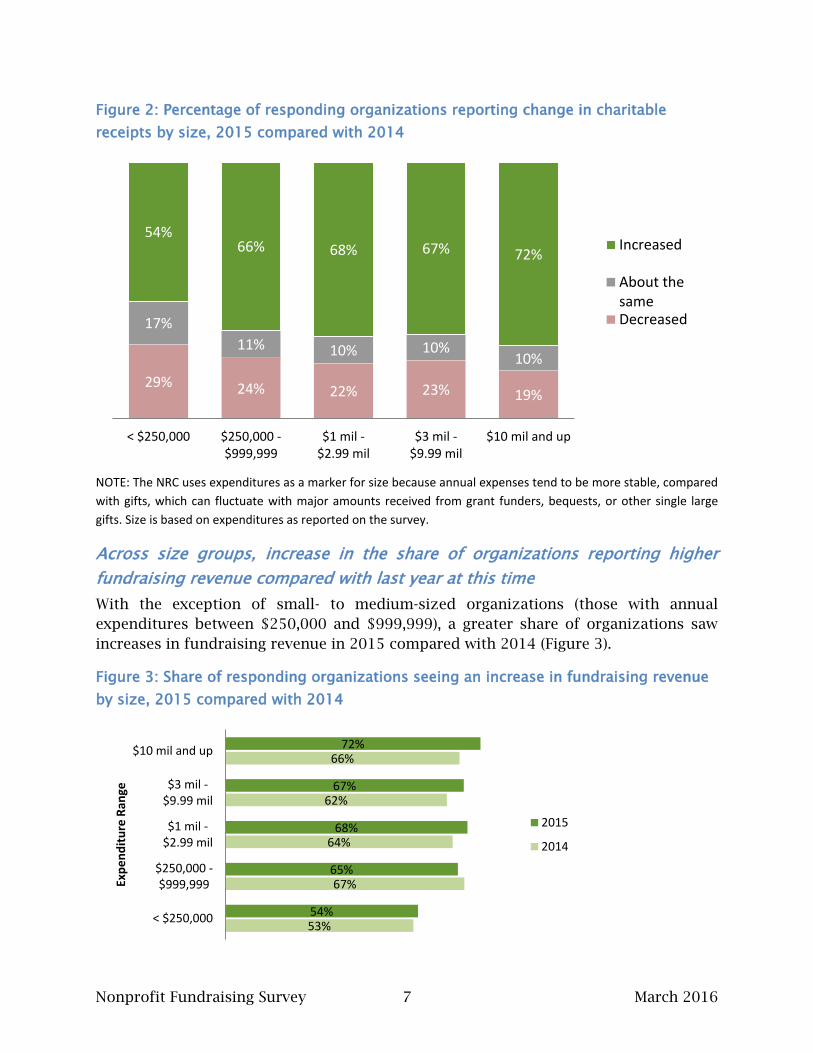

Changes in charitable receipts by organizational size

The one factor associated consistently with a lower probability of raising more in

philanthropic revenue in any one year is having a lower overall organizational budget

from all revenue sources. This has been the case since the NFS began in 2010.

Larger organizations more likely than smaller to see increases

As has been the case in prior waves of the Nonprofit Fundraising Survey, larger

organizations (based on reported expenditures) were more likely to see growth in

charitable receipts than were smaller organizations (Figure 2).

54% of the smallest organizations (expenditures less than $250,000) reported

growth in charitable receipts for 2015.

17% of the smallest organizations reported unchanged charitable receipts in

2015, which is significantly more than the 9 to 11 percent of larger

organizations (any level of expenditure $250,000 or above) reporting no change.

72% of the largest organizations (expenditures $10 million or more) reported

growth in charitable receipts for 2015; this was also the largest group to see

increased giving.

Question: What most affected your organization’s fundraising results in 2015?

“Upgrading, cleaning, and maintaining our database…. Moving forward we have

more carefully tracked EVERY donation and correspondence between the donor and

our organization. We pull better, cleaner mailing lists and every donor is thanked in

a timely manner. Donors are responding!!!”

Small- to Medium-sized Southern human services organization

Met 2015 fundraising goal

“A very successful year for individual major gifts and more sponsorships than

previous years for our signature event as well as a good year for planned giving.”

Large Canadian human services organization

Met 2015 fundraising goal

Nonprofit Fundraising Survey 7 March 2016

Figure 2: Percentage of responding organizations reporting change in charitable

receipts by size, 2015 compared with 2014

NOTE: The NRC uses expenditures as a marker for size because annual expenses tend to be more stable, compared

with gifts, which can fluctuate with major amounts received from grant funders, bequests, or other single large

gifts. Size is based on expenditures as reported on the survey.

Across size groups, increase in the share of organizations reporting higher

fundraising revenue compared with last year at this time

With the exception of small- to medium-sized organizations (those with annual

expenditures between $250,000 and $999,999), a greater share of organizations saw

increases in fundraising revenue in 2015 compared with 2014 (Figure 3).

Figure 3: Share of responding organizations seeing an increase in fundraising revenue

by size, 2015 compared with 2014

29% 24% 22% 23% 19%

17%

11% 10% 10% 10%

54% 66% 68% 67% 72%

< $250,000 $250,000 -$999,999

$1 mil -$2.99 mil

$3 mil -$9.99 mil

$10 mil and up

Increased

About thesameDecreased

53%

67%

64%

62%

66%

54%

65%

68%

67%

72%

< $250,000

$250,000 -$999,999

$1 mil -$2.99 mil

$3 mil -$9.99 mil

$10 mil and up

Exp

en

dit

ure

Ran

ge

2015

2014

Nonprofit Fundraising Survey 8 March 2016

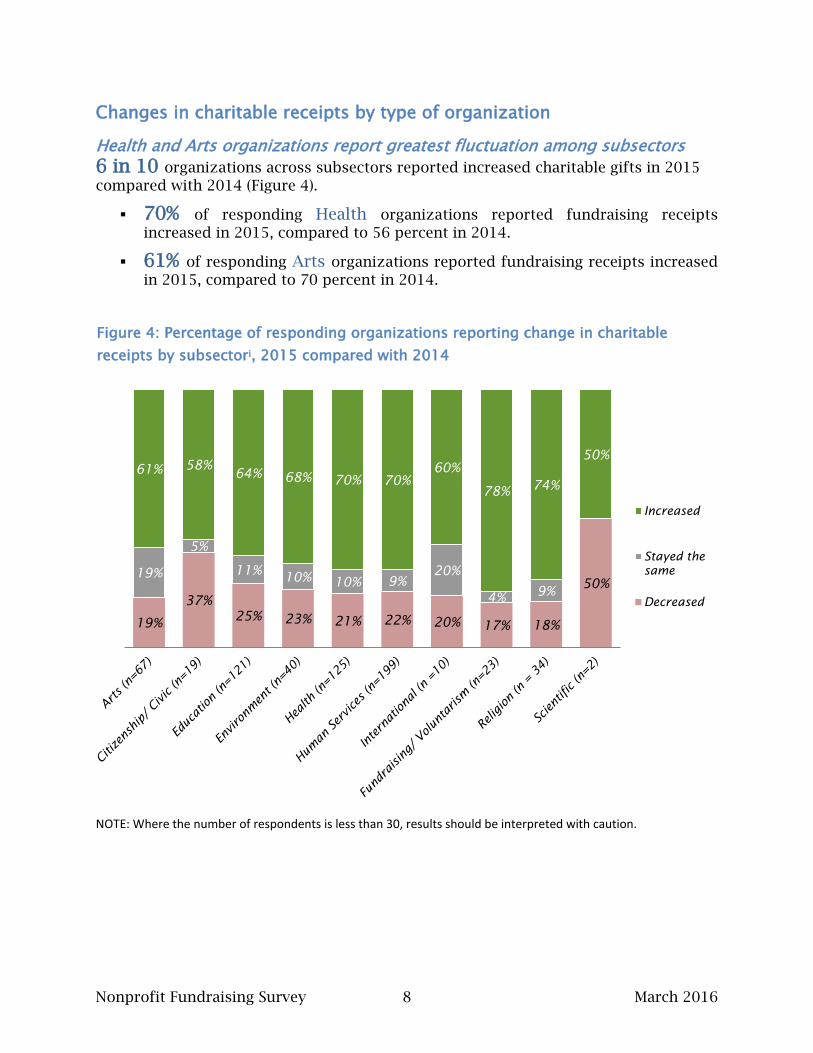

Changes in charitable receipts by type of organization

Health and Arts organizations report greatest fluctuation among subsectors

6 in 10 organizations across subsectors reported increased charitable gifts in 2015

compared with 2014 (Figure 4).

70% of responding Health organizations reported fundraising receipts

increased in 2015, compared to 56 percent in 2014.

61% of responding Arts organizations reported fundraising receipts increased

in 2015, compared to 70 percent in 2014.

Figure 4: Percentage of responding organizations reporting change in charitable

receipts by subsectori, 2015 compared with 2014

NOTE: Where the number of respondents is less than 30, results should be interpreted with caution.

19%

37%

25% 23% 21% 22% 20% 17% 18%

50%

19%

5%

11% 10%

10% 9%

20%

4% 9%

61% 58%

64% 68% 70% 70%

60%

78% 74%

50%

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 9 March 2016

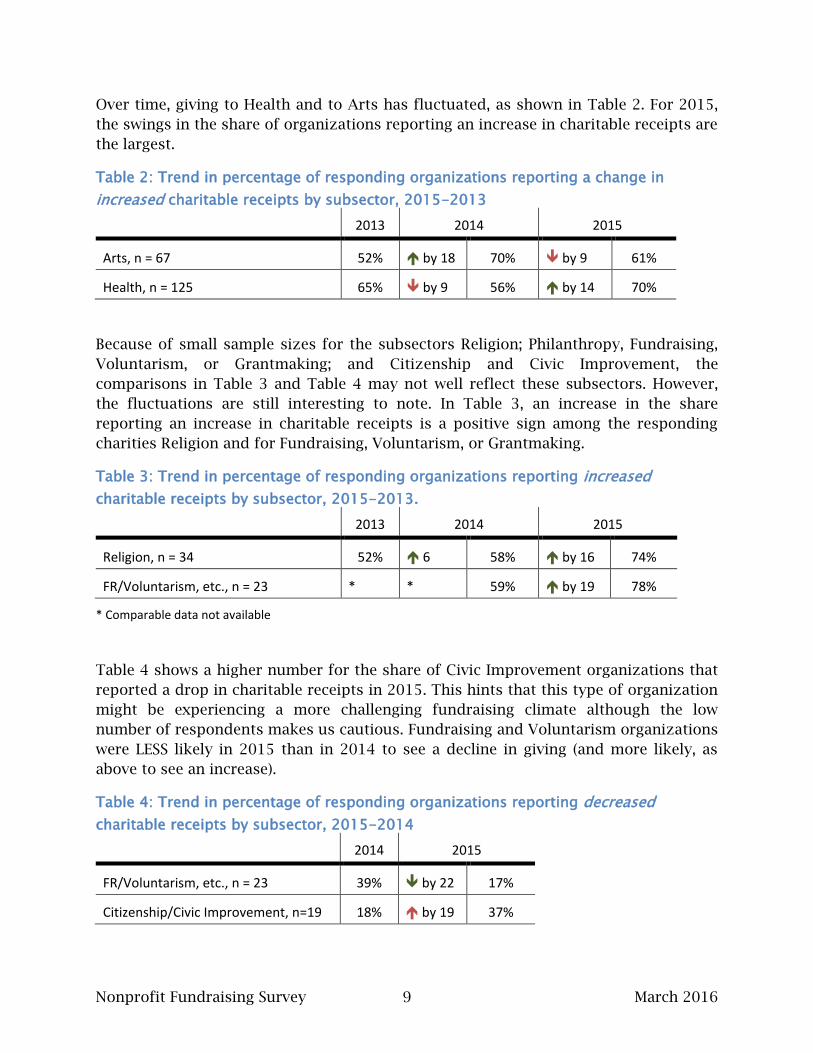

Over time, giving to Health and to Arts has fluctuated, as shown in Table 2. For 2015,

the swings in the share of organizations reporting an increase in charitable receipts are

the largest.

Table 2: Trend in percentage of responding organizations reporting a change in

increased charitable receipts by subsector, 2015-2013

2013 2014 2015

Arts, n = 67 52% by 18 70% by 9 61%

Health, n = 125 65% by 9 56% by 14 70%

Because of small sample sizes for the subsectors Religion; Philanthropy, Fundraising,

Voluntarism, or Grantmaking; and Citizenship and Civic Improvement, the

comparisons in Table 3 and Table 4 may not well reflect these subsectors. However,

the fluctuations are still interesting to note. In Table 3, an increase in the share

reporting an increase in charitable receipts is a positive sign among the responding

charities Religion and for Fundraising, Voluntarism, or Grantmaking.

Table 3: Trend in percentage of responding organizations reporting increased

charitable receipts by subsector, 2015-2013.

2013 2014 2015

Religion, n = 34 52% 6 58% by 16 74%

FR/Voluntarism, etc., n = 23 * * 59% by 19 78%

* Comparable data not available

Table 4 shows a higher number for the share of Civic Improvement organizations that

reported a drop in charitable receipts in 2015. This hints that this type of organization

might be experiencing a more challenging fundraising climate although the low

number of respondents makes us cautious. Fundraising and Voluntarism organizations

were LESS likely in 2015 than in 2014 to see a decline in giving (and more likely, as

above to see an increase).

Table 4: Trend in percentage of responding organizations reporting decreased

charitable receipts by subsector, 2015-2014

2014 2015

FR/Voluntarism, etc., n = 23 39% by 22 17%

Citizenship/Civic Improvement, n=19 18% by 19 37%

Nonprofit Fundraising Survey 10 March 2016

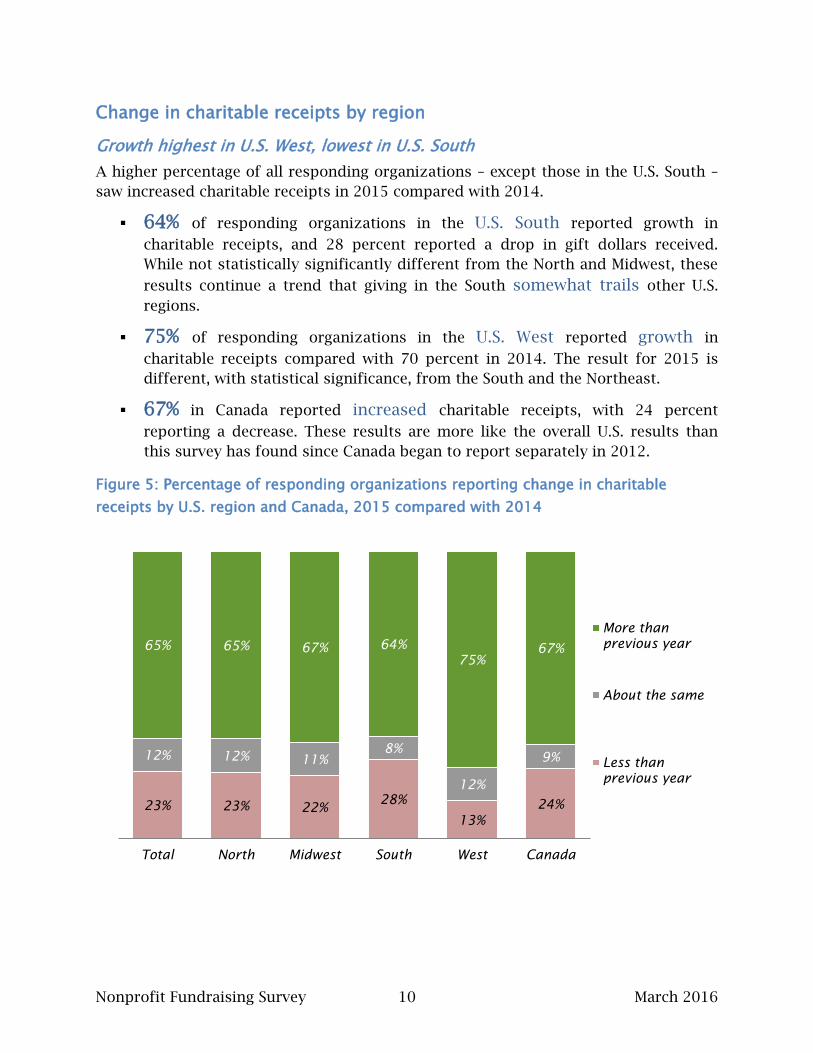

Change in charitable receipts by region

Growth highest in U.S. West, lowest in U.S. South

A higher percentage of all responding organizations – except those in the U.S. South –

saw increased charitable receipts in 2015 compared with 2014.

64% of responding organizations in the U.S. South reported growth in

charitable receipts, and 28 percent reported a drop in gift dollars received.

While not statistically significantly different from the North and Midwest, these

results continue a trend that giving in the South somewhat trails other U.S.

regions.

75% of responding organizations in the U.S. West reported growth in

charitable receipts compared with 70 percent in 2014. The result for 2015 is

different, with statistical significance, from the South and the Northeast.

67% in Canada reported increased charitable receipts, with 24 percent

reporting a decrease. These results are more like the overall U.S. results than

this survey has found since Canada began to report separately in 2012.

Figure 5: Percentage of responding organizations reporting change in charitable

receipts by U.S. region and Canada, 2015 compared with 2014

23% 23% 22% 28%

13%

24%

12% 12% 11%

8%

12%

9%

65% 65% 67% 64%

75%

67%

Total North Midwest South West Canada

More than

previous year

About the same

Less than

previous year

Nonprofit Fundraising Survey 11 March 2016

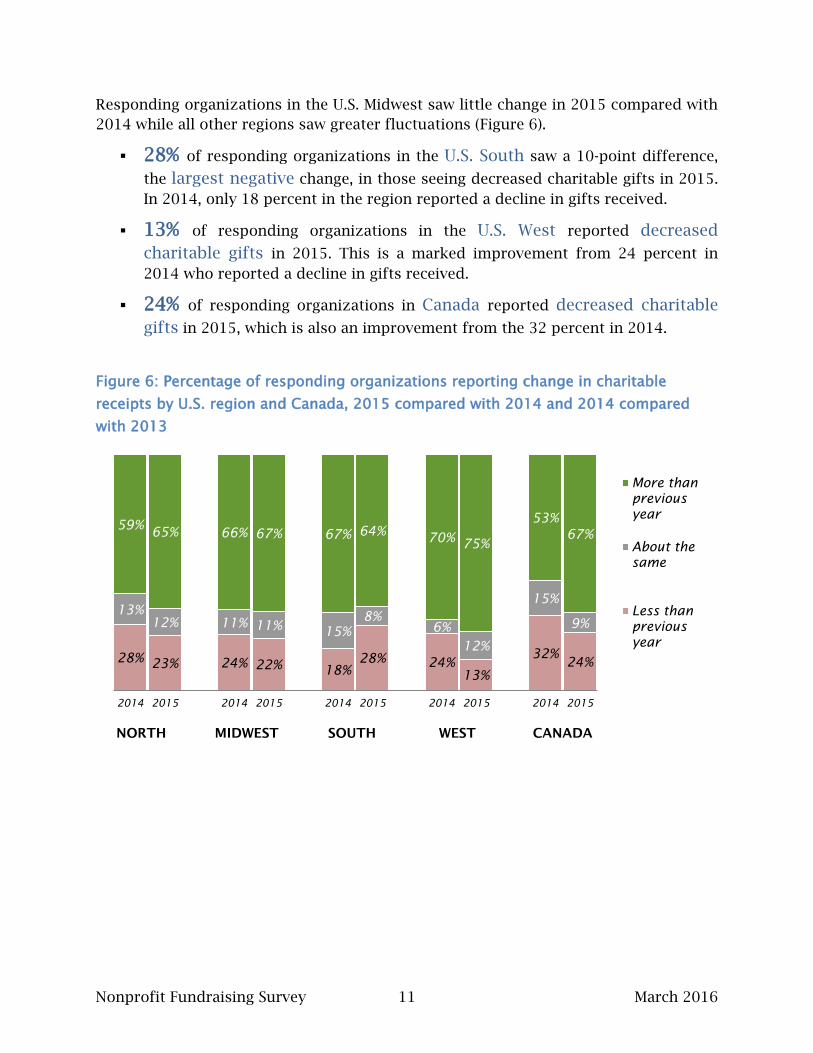

Responding organizations in the U.S. Midwest saw little change in 2015 compared with

2014 while all other regions saw greater fluctuations (Figure 6).

28% of responding organizations in the U.S. South saw a 10-point difference,

the largest negative change, in those seeing decreased charitable gifts in 2015.

In 2014, only 18 percent in the region reported a decline in gifts received.

13% of responding organizations in the U.S. West reported decreased

charitable gifts in 2015. This is a marked improvement from 24 percent in

2014 who reported a decline in gifts received.

24% of responding organizations in Canada reported decreased charitable

gifts in 2015, which is also an improvement from the 32 percent in 2014.

Figure 6: Percentage of responding organizations reporting change in charitable

receipts by U.S. region and Canada, 2015 compared with 2014 and 2014 compared

with 2013

NORTH MIDWEST SOUTH WEST CANADA

28% 23% 24% 22%

18%

28% 24%

13%

32% 24%

13%

12% 11% 11% 15%

8%

6%

12%

15%

9%

59% 65% 66% 67% 67% 64%

70% 75%

53%

67%

2014 2015 2014 2015 2014 2015 2014 2015 2014 2015

More than

previous

year

About the

same

Less than

previous

year

Nonprofit Fundraising Survey 12 March 2016

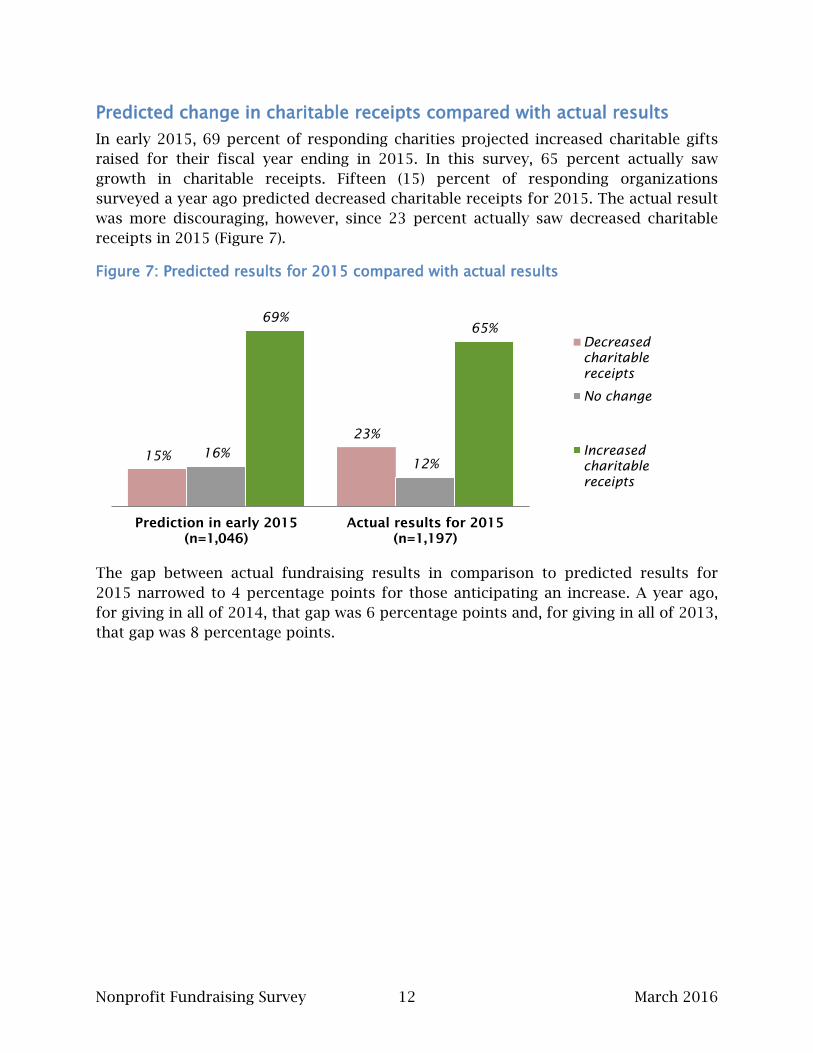

Predicted change in charitable receipts compared with actual results

In early 2015, 69 percent of responding charities projected increased charitable gifts

raised for their fiscal year ending in 2015. In this survey, 65 percent actually saw

growth in charitable receipts. Fifteen (15) percent of responding organizations

surveyed a year ago predicted decreased charitable receipts for 2015. The actual result

was more discouraging, however, since 23 percent actually saw decreased charitable

receipts in 2015 (Figure 7).

Figure 7: Predicted results for 2015 compared with actual results

The gap between actual fundraising results in comparison to predicted results for

2015 narrowed to 4 percentage points for those anticipating an increase. A year ago,

for giving in all of 2014, that gap was 6 percentage points and, for giving in all of 2013,

that gap was 8 percentage points.

15%

23%

16%

12%

69%

65%

Prediction in early 2015

(n=1,046)

Actual results for 2015

(n=1,197)

Decreased

charitable

receipts

No change

Increased

charitable

receipts

Nonprofit Fundraising Survey 13 March 2016

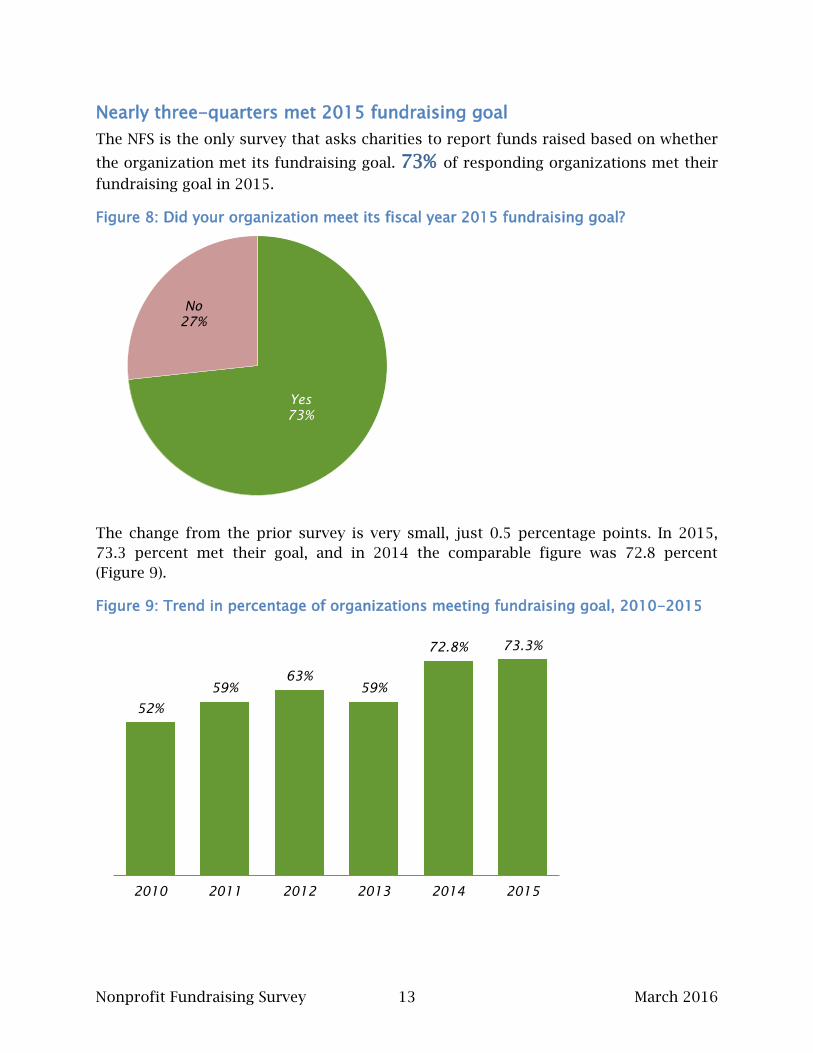

Nearly three-quarters met 2015 fundraising goal

The NFS is the only survey that asks charities to report funds raised based on whether

the organization met its fundraising goal. 73% of responding organizations met their

fundraising goal in 2015.

Figure 8: Did your organization meet its fiscal year 2015 fundraising goal?

The change from the prior survey is very small, just 0.5 percentage points. In 2015,

73.3 percent met their goal, and in 2014 the comparable figure was 72.8 percent

(Figure 9).

Figure 9: Trend in percentage of organizations meeting fundraising goal, 2010-2015

Yes

73%

No

27%

52%

59%

63%

59%

72.8% 73.3%

2010 2011 2012 2013 2014 2015

Nonprofit Fundraising Survey 14 March 2016

Organizations attribute success to hard work; missing goal linked with

economy or leadership challenges

In word clouds the size of each word indicates the frequency that term was mentioned,

which allows the reader to compare the relative importance of various ideas written in

comments. To further aid interpretation, we have added a color code to help

differentiate ideas.

Used by organizations meeting goals AND by organizations not meeting goals.

External factors that organizations cannot change.

Only on the list for organizations that met their goal.

Only on the list for organizations that did not meet their fundraising goal.

Figure 10: Words provided to explain meeting goals

Question: What most affected your organization’s fundraising results in 2015? –

Organization met goal

“Coming off a successful capital campaign and transitioning to ‘regular’ annual

fundraising.”

Large Canadian higher education organization

Nonprofit Fundraising Survey 15 March 2016

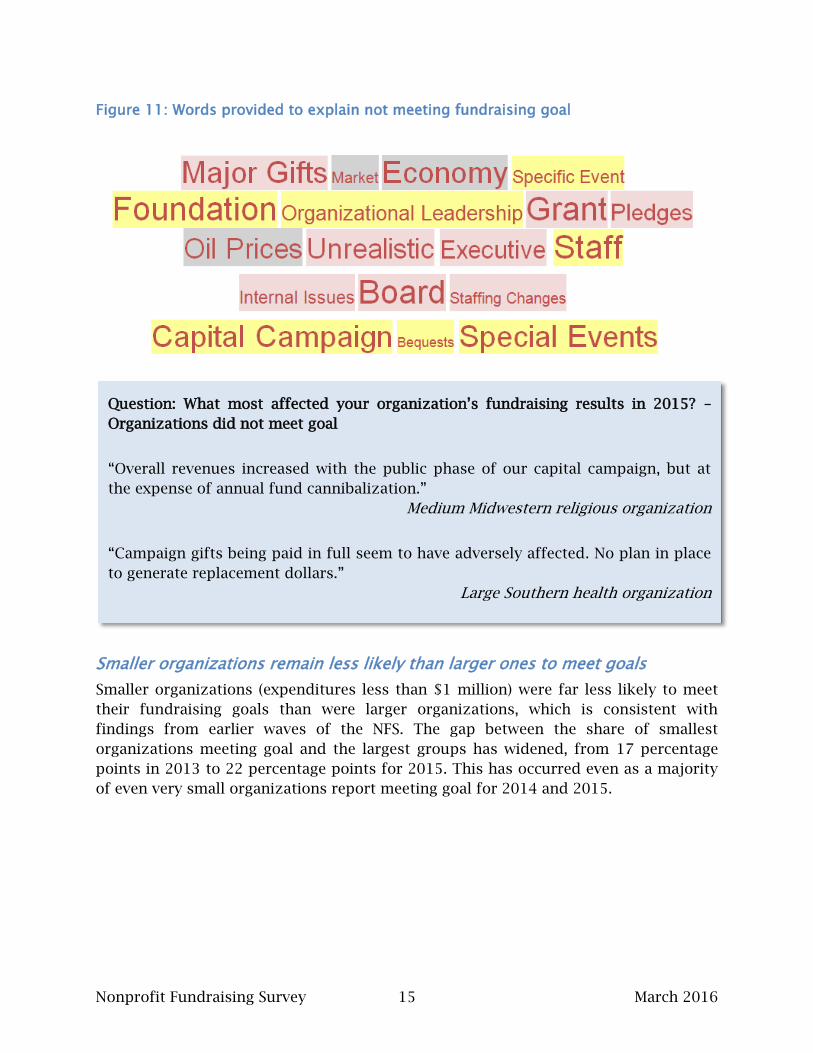

Figure 11: Words provided to explain not meeting fundraising goal

Smaller organizations remain less likely than larger ones to meet goals

Smaller organizations (expenditures less than $1 million) were far less likely to meet

their fundraising goals than were larger organizations, which is consistent with

findings from earlier waves of the NFS. The gap between the share of smallest

organizations meeting goal and the largest groups has widened, from 17 percentage

points in 2013 to 22 percentage points for 2015. This has occurred even as a majority

of even very small organizations report meeting goal for 2014 and 2015.

Question: What most affected your organization’s fundraising results in 2015? –

Organizations did not meet goal

“Overall revenues increased with the public phase of our capital campaign, but at

the expense of annual fund cannibalization.”

Medium Midwestern religious organization

“Campaign gifts being paid in full seem to have adversely affected. No plan in place

to generate replacement dollars.”

Large Southern health organization

Nonprofit Fundraising Survey 16 March 2016

Table 5: Trend in percentage of responding organizations meeting fundraising goal by

organizational size, 2013-2015

Organization Size Met goal in

2013

Met goal in

2014

Met goal in

2015

<$250,000 48% 59% 61%

$250,000 to $999,999 57% 70% 66%

$1 million to $2.99 million 63% 71% 76%

$3 million to $9.99 million 66% 72% 81%

$10 million and larger 65% 77% 83%

Figure 12: Percentage of responding organizations meeting 2015 fundraising goal by

organizational size

Size is based on expenditures as reported on the survey.

39% 34%

24% 19% 17%

61% 66%

76% 81% 83%

<$250,000 $250,000 to

$999,999

$1 million to

$2.99 million

$3 million to

$9.99 million

$10 million and

up

Yes

No

Nonprofit Fundraising Survey 17 March 2016

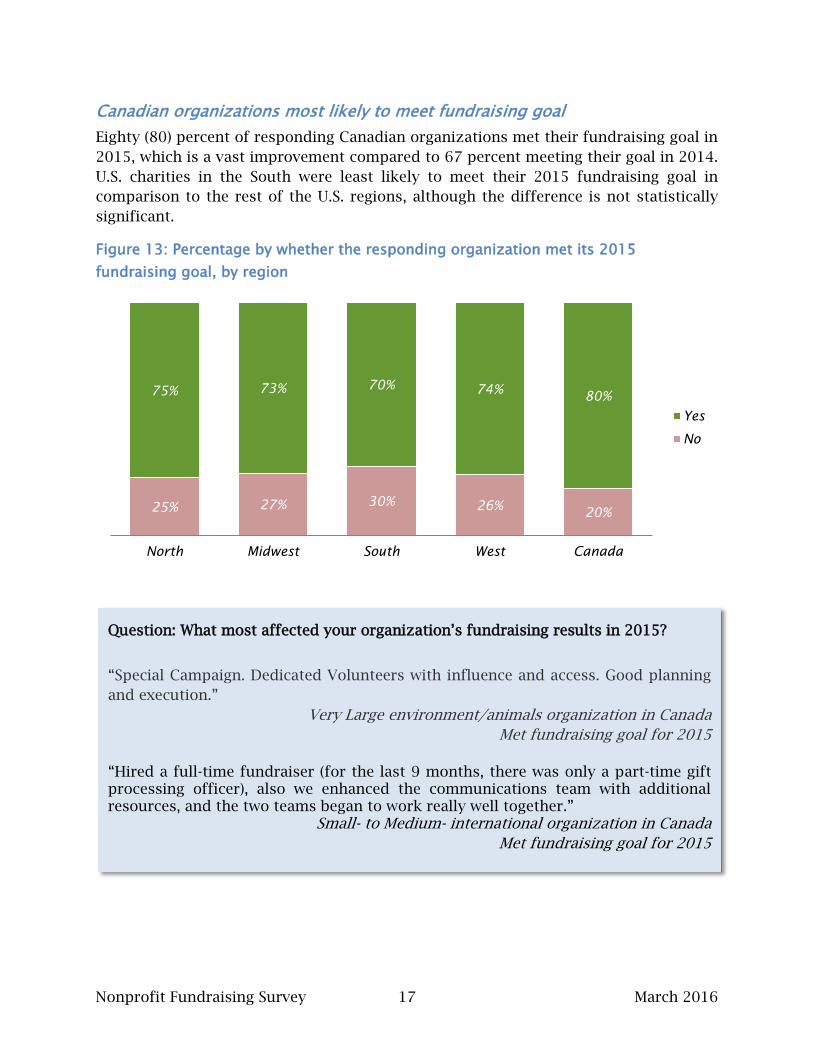

Canadian organizations most likely to meet fundraising goal

Eighty (80) percent of responding Canadian organizations met their fundraising goal in

2015, which is a vast improvement compared to 67 percent meeting their goal in 2014.

U.S. charities in the South were least likely to meet their 2015 fundraising goal in

comparison to the rest of the U.S. regions, although the difference is not statistically

significant.

Figure 13: Percentage by whether the responding organization met its 2015

fundraising goal, by region

25% 27% 30% 26%

20%

75% 73% 70% 74%

80%

North Midwest South West Canada

Yes

No

Question: What most affected your organization’s fundraising results in 2015?

“Special Campaign. Dedicated Volunteers with influence and access. Good planning

and execution.”

Very Large environment/animals organization in Canada

Met fundraising goal for 2015

“Hired a full-time fundraiser (for the last 9 months, there was only a part-time gift processing officer), also we enhanced the communications team with additional resources, and the two teams began to work really well together.”

Small- to Medium- international organization in Canada

Met fundraising goal for 2015

Nonprofit Fundraising Survey 18 March 2016

Question: What most affected your organization’s fundraising results in 2015?

“Consistent and systematic organization and reapplication of formal annual giving

program (2015 is year two); increased donor engagement and recognition,

systematic communication, community outreach; exceeding annual fund (two

primary appeals) expectations; segmentation of data base; strong reception and

attendance at primary annual fundraising event.”

Small- to Medium-sized Northern environmental organization

Met 2015 fundraising goal

“In addition to changes in the economy, our fundraising efforts were affected by

organizational staffing changes in 2014 and 2015 that prevented our Donor

Relations Department from being fully staffed.”

Medium Southern human services organization

Did not meet 2015 fundraising goal

Nonprofit Fundraising Survey 19 March 2016

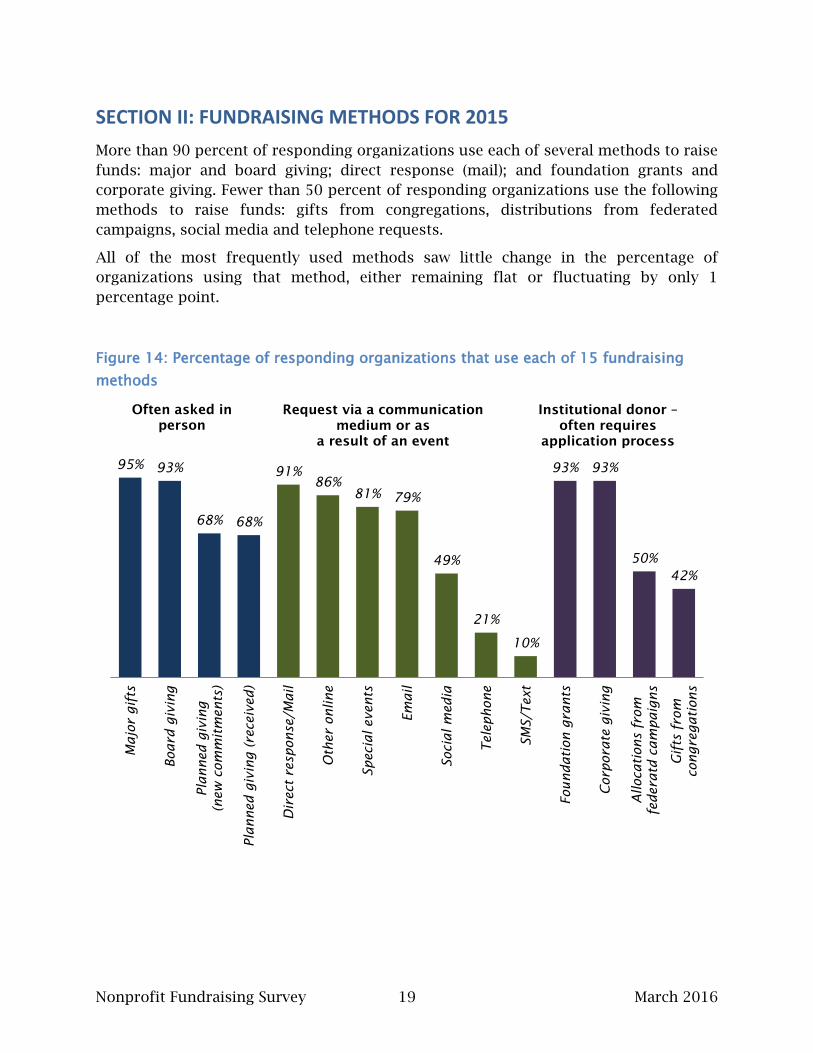

SECTION II: FUNDRAISING METHODS FOR 2015

More than 90 percent of responding organizations use each of several methods to raise

funds: major and board giving; direct response (mail); and foundation grants and

corporate giving. Fewer than 50 percent of responding organizations use the following

methods to raise funds: gifts from congregations, distributions from federated

campaigns, social media and telephone requests.

All of the most frequently used methods saw little change in the percentage of

organizations using that method, either remaining flat or fluctuating by only 1

percentage point.

Figure 14: Percentage of responding organizations that use each of 15 fundraising

methods

95% 93%

68% 68%

91%

86%

81% 79%

49%

21%

10%

93% 93%

50%

42%

Major gifts

Board giving

Planned giving

(new

com

mitm

ents)

Planned giving (received)

Direct response/M

ail

Other online

Special events

Em

ail

Social m

edia

Telephone

SM

S/Text

Foundation grants

Corporate giving

Allocations from

federatd cam

paigns

Gifts from

congregations

Often asked in

person

Request via a communication

medium or as

a result of an event

Institutional donor –

often requires

application process

Nonprofit Fundraising Survey 20 March 2016

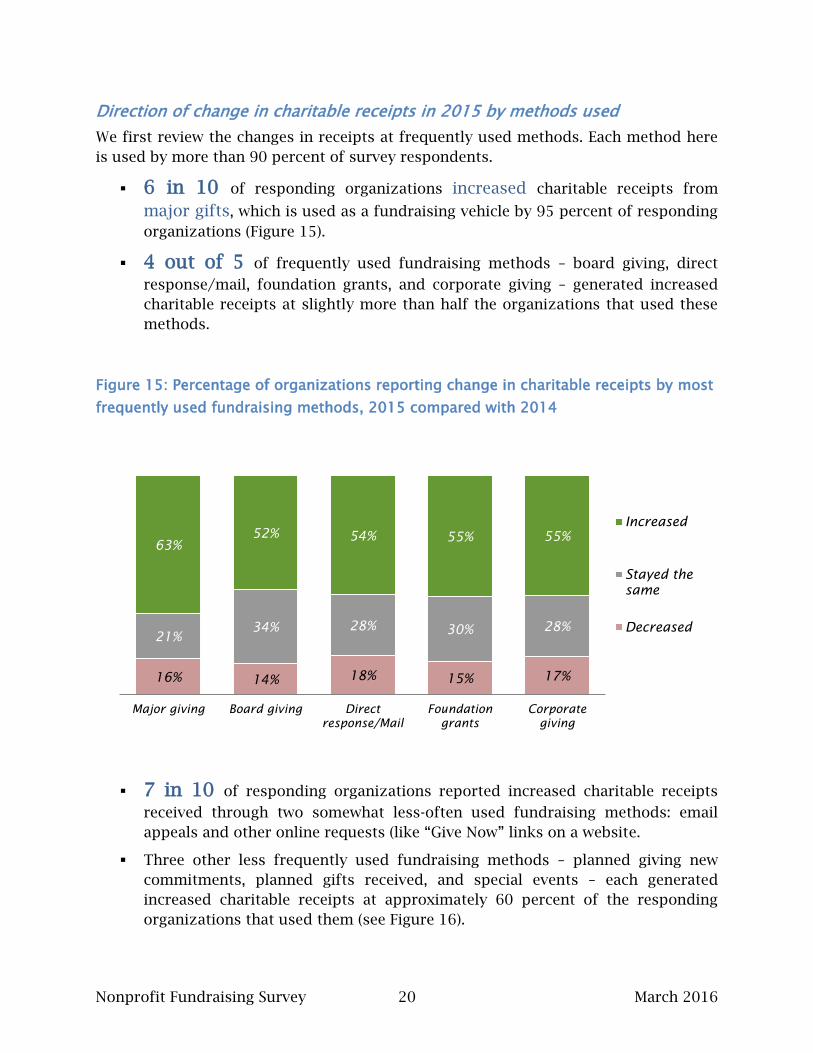

Direction of change in charitable receipts in 2015 by methods used

We first review the changes in receipts at frequently used methods. Each method here

is used by more than 90 percent of survey respondents.

6 in 10 of responding organizations increased charitable receipts from

major gifts, which is used as a fundraising vehicle by 95 percent of responding

organizations (Figure 15).

4 out of 5 of frequently used fundraising methods – board giving, direct

response/mail, foundation grants, and corporate giving – generated increased

charitable receipts at slightly more than half the organizations that used these

methods.

Figure 15: Percentage of organizations reporting change in charitable receipts by most

frequently used fundraising methods, 2015 compared with 2014

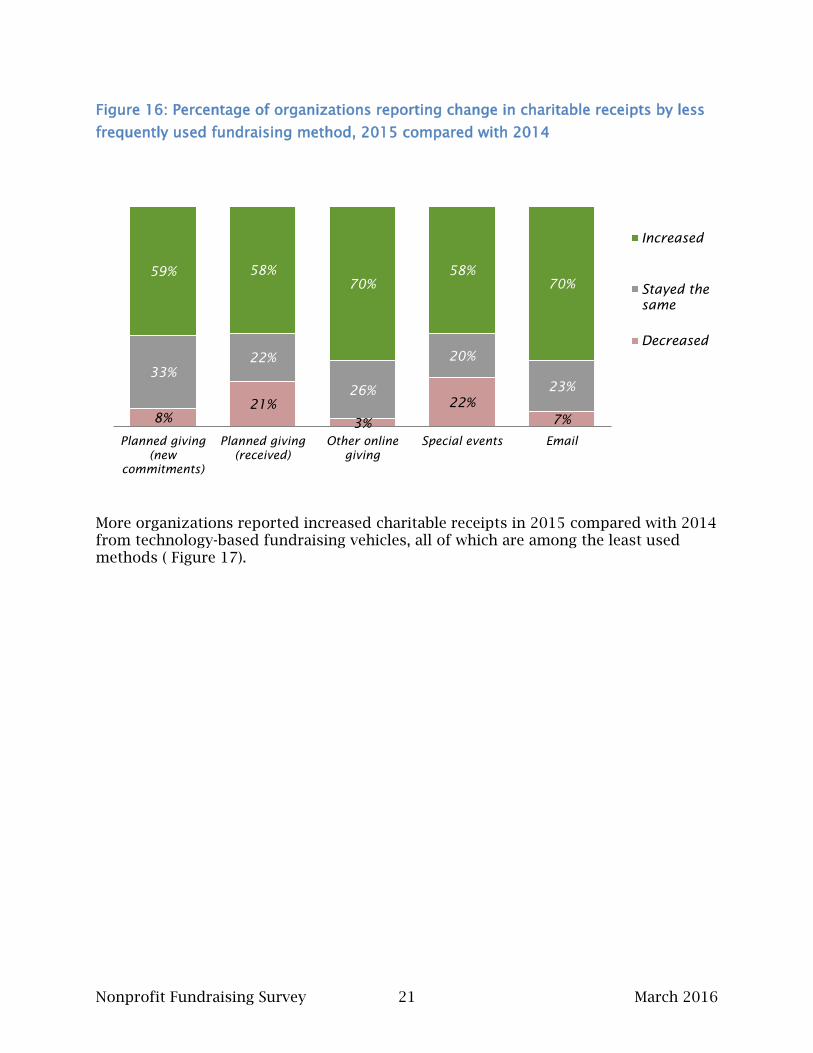

7 in 10 of responding organizations reported increased charitable receipts

received through two somewhat less-often used fundraising methods: email

appeals and other online requests (like “Give Now” links on a website.

Three other less frequently used fundraising methods – planned giving new

commitments, planned gifts received, and special events – each generated

increased charitable receipts at approximately 60 percent of the responding

organizations that used them (see Figure 16).

16% 14% 18% 15% 17%

21%

34% 28% 30% 28%

63%

52% 54% 55% 55%

Major giving Board giving Direct

response/Mail

Foundation

grants

Corporate

giving

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 21 March 2016

Figure 16: Percentage of organizations reporting change in charitable receipts by less

frequently used fundraising method, 2015 compared with 2014

More organizations reported increased charitable receipts in 2015 compared with 2014 from technology-based fundraising vehicles, all of which are among the least used methods ( Figure 17).

8%

21%

3%

22%

7%

33%

22%

26%

20%

23%

59% 58%

70%

58%

70%

Planned giving

(new

commitments)

Planned giving

(received)

Other online

giving

Special events Email

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 22 March 2016

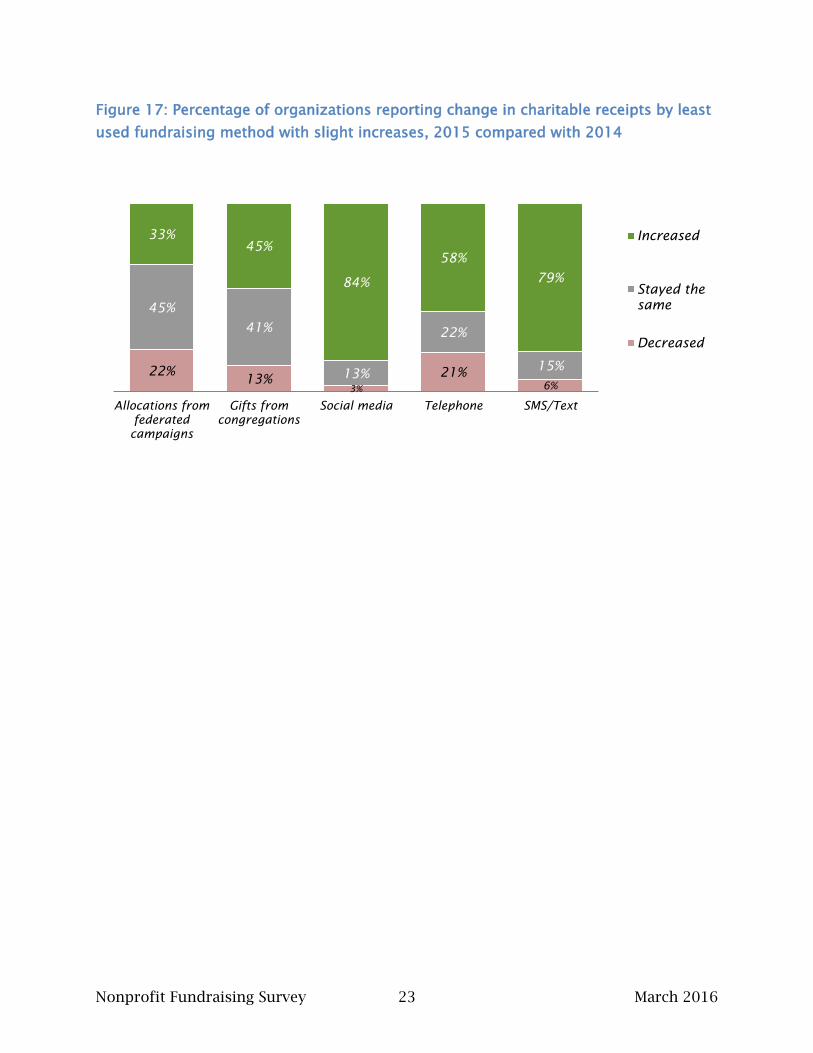

84% of responding organizations indicated growth in charitable gifts received

through social media, which is the highest percentage of any method.

However, still less than half (49%) of responding organizations used social

media as a fundraising method, up from 46 percent reported in 2014.

79% of organizations using the method reported increased gifts received

through SMS/text requests, which is 11 percentage points higher than the 68

percent in 2014. This is the greatest change of any method; it is also the least

used method, reported by just 10 percent of charities in this study.

45% of organizations that use the method reported increased gifts from

congregations in 2015, which is 9 percentage points higher than the 36

percent in 2014.

Nonprofit Fundraising Survey 23 March 2016

Figure 17: Percentage of organizations reporting change in charitable receipts by least

used fundraising method with slight increases, 2015 compared with 2014

22% 13%

3%

21%

6%

45%

41%

13%

22%

15%

33%

45%

84%

58%

79%

Allocations from

federated

campaigns

Gifts from

congregations

Social media Telephone SMS/Text

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 24 March 2016

Figure 18: Percentage of responding organizations that indicate using specific types of

online or social media fundraising in 2015

N=1,197

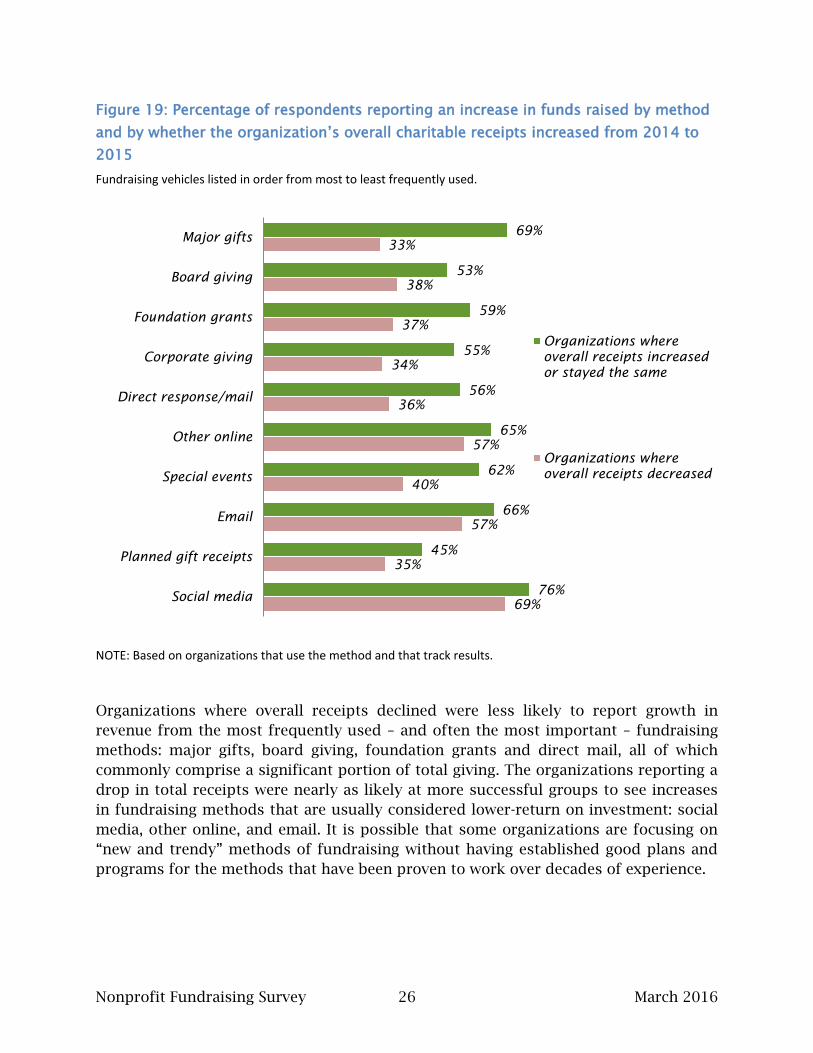

Organizations that do not see an increase in overall fundraising results are

much less likely to see increases in most fundraising methods

Nearly all of the fundraising methods listed in Figure 19 provided increased charitable

gifts for no more than 40 percent of responding organizations that saw decreased

overall receipts in 2015 compared with 2014. Technology-based fundraising vehicles –

social media, other online, and email – were slightly more likely to provide increased

charitable gifts for these organizations; however, the dollar amounts received through

those vehicles are likely not enough to make up for poor or mediocre results from the

other fundraising methods.

Just 33% of responding organizations with a drop in total charitable receipts

saw an increase in major gifts. This is markedly different from growth in major

gifts at 69 percent of organizations with increases in gifts or stable gifts

received.

There are also possible factors that are not development related that could explain

lower fundraising results. For example, some of the comments in the open-ended

questions indicate continued challenging economies as well as disengaged leadership

or an unsupported executive director/CEO.

42%

26%

16%

11%

5%

Local, regional, or

national giving

day, including

Giving Tuesday

Sales-linked

fundraising, such

as Smile.Amazon

or other

Peer-to-peer or "a-

thon" fundraising

(online pledges

made by friends

who were asked

by a volunteer

participating in an

event or activity)

Crowdfunding,

such as through

sites like Razoo,

Kickstarter,

GoFundMe,

CaringBridge, or

others

Online charity

auction, either

through eBay or

otherwise

Nonprofit Fundraising Survey 25 March 2016

Question: What most affected your organization’s fundraising results in 2015?

“The downturn in the economy as a result of the drop in oil prices. Corporations

and individuals from the oil sector were either not able to make donations or were

reluctant to give as much as they could.”

Medium- to Large-sized Canadian human services organization

Did not meet 2015 fundraising goal

“Board president in name only. Non-working. Board was in transition and

uninvolved.”

Small- to Medium-sized Northern human services organization

Did not meet 2015 fundraising goal

“PR scandal with our former CEO limited investment in communications and

development staffing.”

Large Western human services organization

Met 2015 fundraising goal

Nonprofit Fundraising Survey 26 March 2016

Figure 19: Percentage of respondents reporting an increase in funds raised by method

and by whether the organization’s overall charitable receipts increased from 2014 to

2015

Fundraising vehicles listed in order from most to least frequently used.

NOTE: Based on organizations that use the method and that track results.

Organizations where overall receipts declined were less likely to report growth in

revenue from the most frequently used – and often the most important – fundraising

methods: major gifts, board giving, foundation grants and direct mail, all of which

commonly comprise a significant portion of total giving. The organizations reporting a

drop in total receipts were nearly as likely at more successful groups to see increases

in fundraising methods that are usually considered lower-return on investment: social

media, other online, and email. It is possible that some organizations are focusing on

“new and trendy” methods of fundraising without having established good plans and

programs for the methods that have been proven to work over decades of experience.

69%

35%

57%

40%

57%

36%

34%

37%

38%

33%

76%

45%

66%

62%

65%

56%

55%

59%

53%

69%

Social media

Planned gift receipts

Special events

Other online

Direct response/mail

Corporate giving

Foundation grants

Board giving

Major gifts

Organizations where

overall receipts increased

or stayed the same

Organizations where

overall receipts decreased

Nonprofit Fundraising Survey 27 March 2016

SECTION III: TRENDS SINCE 2005

The Association of Fundraising Professionals (AFP) began conducting surveys in 2002

to track the impact of economic changes on charitable receipts. The Nonprofit

Research Collaborative started asking questions similar to AFP’s in 2010. This year’s

overall results are followed by trends for fundraising methods used, grouped by like

methods and in order of most to least frequently used.

Figure 20 shows the trend in overall charitable receipts since 2005. The past five years

shows a steady, upward trend in the percentage of responding organizations reporting

increased total charitable receipts compared to the prior year. However, the percentage

of organizations seeing increases is still less than the 69 percent found for 2006.

This year, while most fundraising methods were successful at a majority of

organizations, percentages reporting growth in revenue fell slightly for Major Gifts,

Special Events, Other Online, and Federated Campaigns. That is, for Major Gifts, in

2014, 65 percent saw higher revenue; in 2015, 63 percent did.

Perhaps more concerning is the fact that more participating charities saw a decline in

fundraising revenue in 2015 than had in 2014 from these methods: Major Gifts; Board

Giving; Planned Gifts; Direct Mail; Special Events; Corporate Gifts and Grants. The one-

to four-point shifts are not signals of significant change, yet a careful plan will

consider alternatives in the event a specific fundraising initiative yields less than

desired.

Figure 20: Percentage of responding organizations reporting change in charitable

receipts by year, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative. Different recruitment methods for respondents beginning in 2010 mean direct comparison in those years with earlier years will not be meaningful.

24% 24% 24%

40% 46%

33% 31% 26%

22% 24% 23%

13% 7%

11%

14%

11%

24%

16%

16%

16% 13% 12%

63% 69%

65%

46% 43% 43%

53% 58%

62% 63% 65%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

over prior

year

About the

same

Decreased

over prior

year

Nonprofit Fundraising Survey 28 March 2016

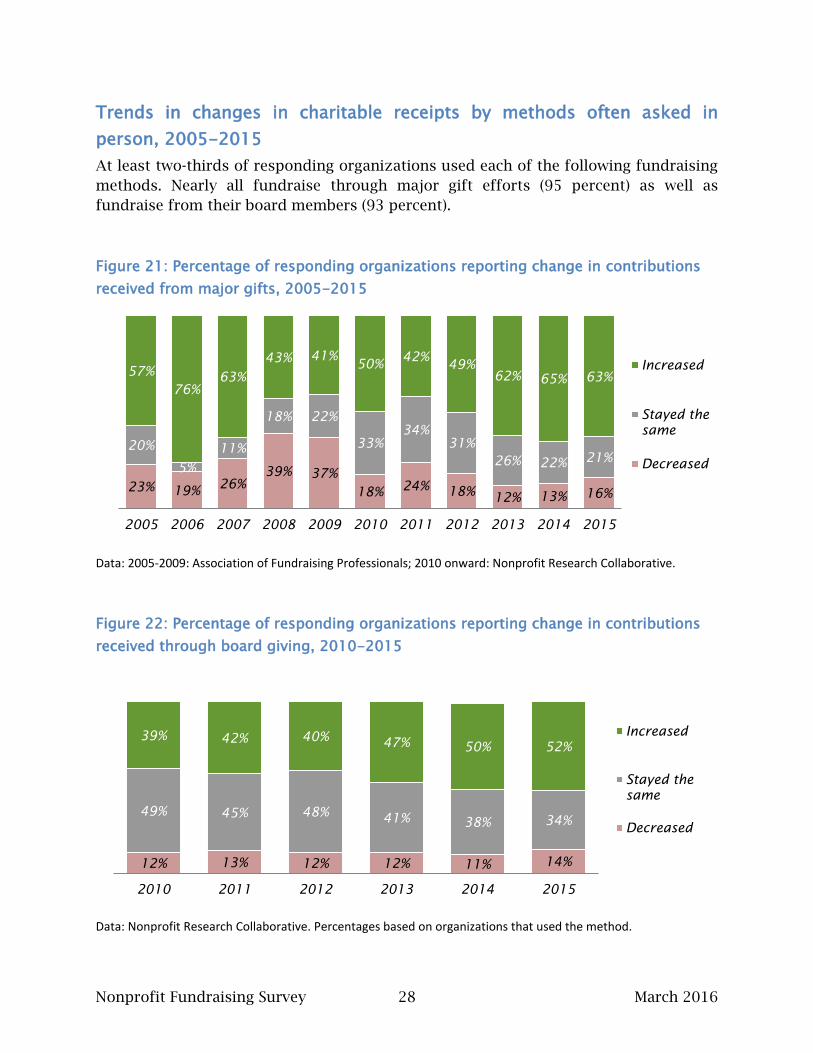

Trends in changes in charitable receipts by methods often asked in

person, 2005-2015

At least two-thirds of responding organizations used each of the following fundraising

methods. Nearly all fundraise through major gift efforts (95 percent) as well as

fundraise from their board members (93 percent).

Figure 21: Percentage of responding organizations reporting change in contributions

received from major gifts, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative.

Figure 22: Percentage of responding organizations reporting change in contributions

received through board giving, 2010-2015

Data: Nonprofit Research Collaborative. Percentages based on organizations that used the method.

23% 19%

26%

39% 37%

18% 24%

18% 12% 13% 16%

20%

5%

11%

18% 22%

33%

34%

31%

26% 22% 21%

57%

76%

63%

43% 41% 50%

42% 49%

62% 65% 63%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

12% 13% 12% 12% 11% 14%

49% 45% 48% 41%

38% 34%

39% 42% 40% 47%

50% 52%

2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 29 March 2016

Figure 23: Percentage of responding organizations reporting change in contributions

received through planned gifts realized, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative.

Figure 24: Percentage of responding organizations reporting change in contributions

received through new committed planned gifts, 2012-2015

Data: Nonprofit Research Collaborative. Percentages based on organizations that used the method.

22%

45%

16%

27% 22% 22% 23%

16% 22%

18% 21%

38%

3%

31%

40% 51% 51% 48%

41% 35%

29% 22%

40%

52% 54%

33% 27% 27% 29%

36% 42%

53% 58%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

11% 22%

8% 8%

44%

38%

34% 33%

45% 41%

58% 59%

2012 2013 2014 2015

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 30 March 2016

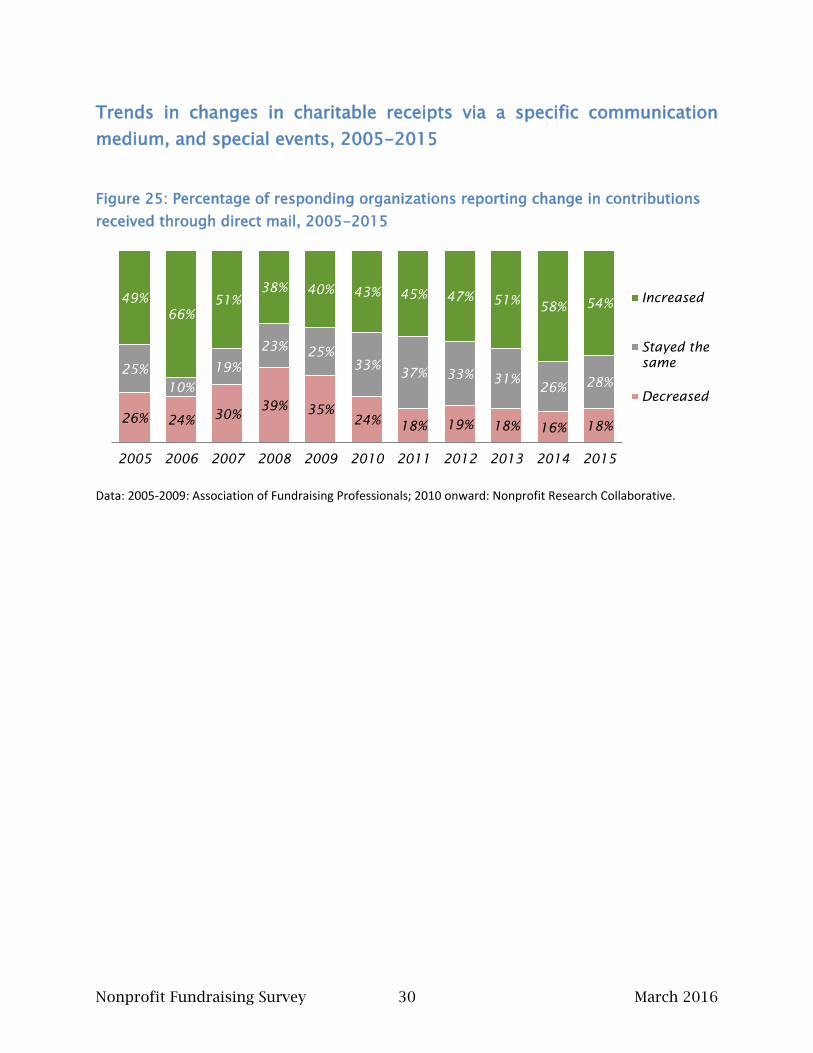

Trends in changes in charitable receipts via a specific communication

medium, and special events, 2005-2015

Figure 25: Percentage of responding organizations reporting change in contributions

received through direct mail, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative.

26% 24% 30%

39% 35%

24% 18% 19% 18% 16% 18%

25%

10%

19%

23% 25%

33% 37% 33%

31% 26%

28%

49%

66%

51%

38% 40% 43% 45% 47% 51% 58% 54%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 31 March 2016

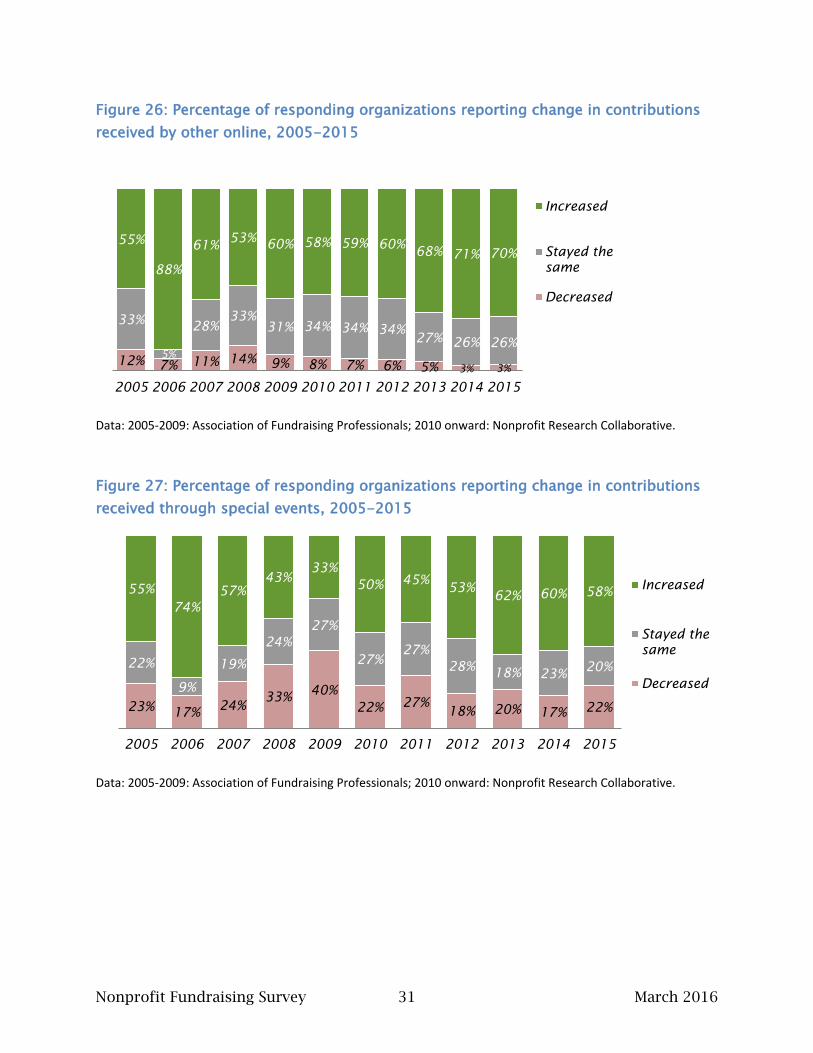

Figure 26: Percentage of responding organizations reporting change in contributions

received by other online, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative.

Figure 27: Percentage of responding organizations reporting change in contributions

received through special events, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative.

12% 7% 11% 14%

9% 8% 7% 6% 5% 3% 3%

33%

5%

28%

33%

31% 34% 34% 34% 27%

26% 26%

55%

88%

61% 53%

60% 58% 59% 60% 68% 71% 70%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

23% 17%

24% 33%

40%

22% 27%

18% 20% 17% 22%

22%

9%

19%

24%

27%

27%

27%

28% 18% 23%

20%

55%

74%

57%

43%

33%

50% 45%

53% 62% 60% 58%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 32 March 2016

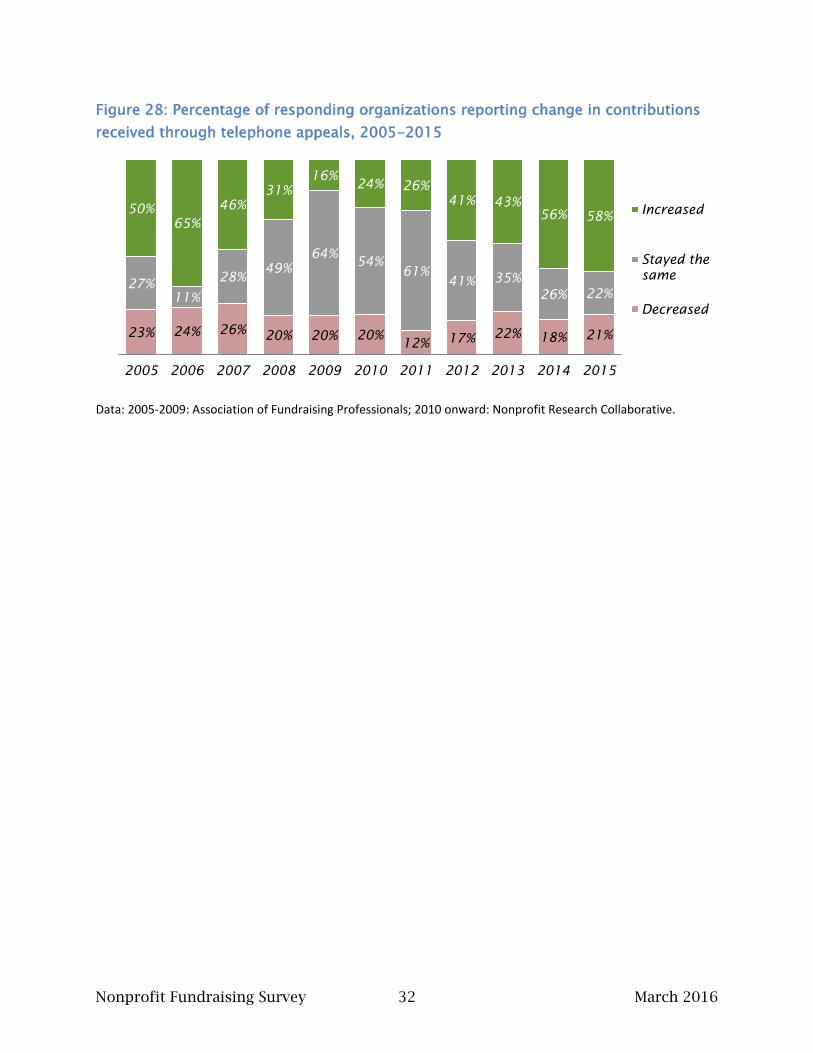

Figure 28: Percentage of responding organizations reporting change in contributions

received through telephone appeals, 2005-2015

Data: 2005-2009: Association of Fundraising Professionals; 2010 onward: Nonprofit Research Collaborative.

23% 24% 26% 20% 20% 20%

12% 17%

22% 18% 21%

27%

11%

28% 49%

64% 54%

61%

41% 35%

26% 22%

50%

65%

46%

31%

16% 24% 26%

41% 43%

56% 58%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 33 March 2016

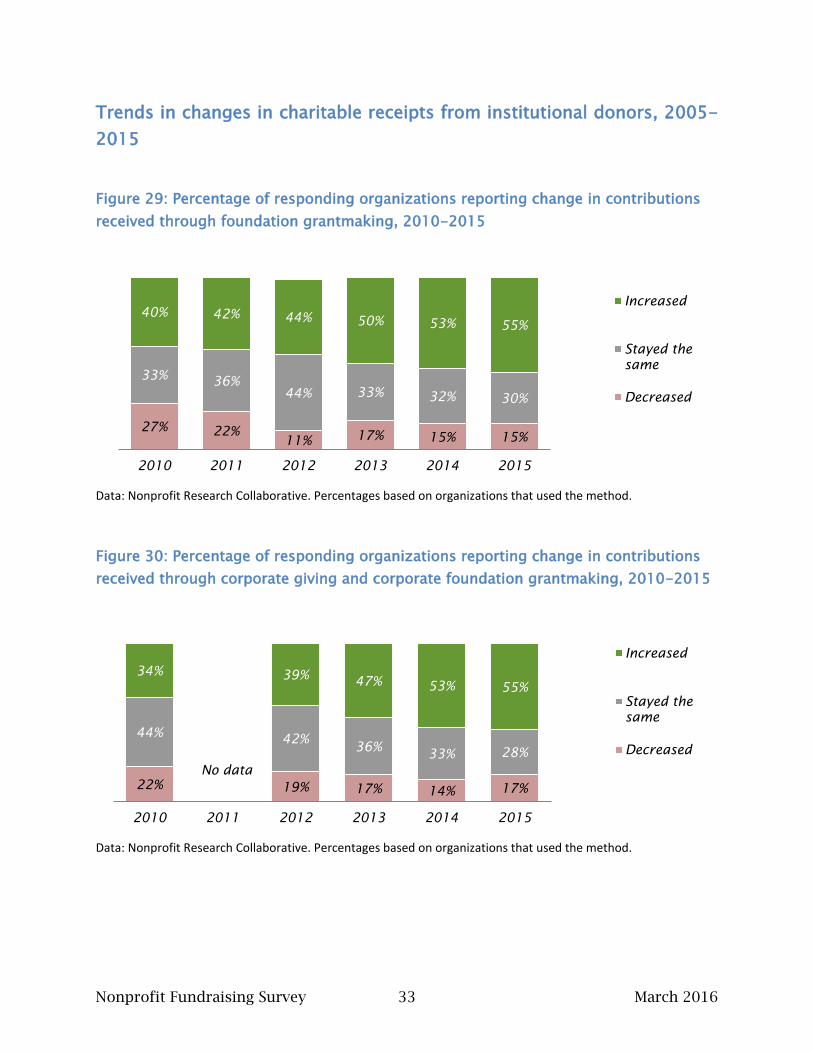

Trends in changes in charitable receipts from institutional donors, 2005-

2015

Figure 29: Percentage of responding organizations reporting change in contributions

received through foundation grantmaking, 2010-2015

Data: Nonprofit Research Collaborative. Percentages based on organizations that used the method.

Figure 30: Percentage of responding organizations reporting change in contributions

received through corporate giving and corporate foundation grantmaking, 2010-2015

Data: Nonprofit Research Collaborative. Percentages based on organizations that used the method.

27% 22%

11% 17% 15% 15%

33% 36%

44% 33% 32% 30%

40% 42% 44% 50% 53% 55%

2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

22% 19% 17% 14% 17%

44% 42%

36% 33% 28%

34% 39%

47% 53% 55%

2010 2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

No data

Nonprofit Fundraising Survey 34 March 2016

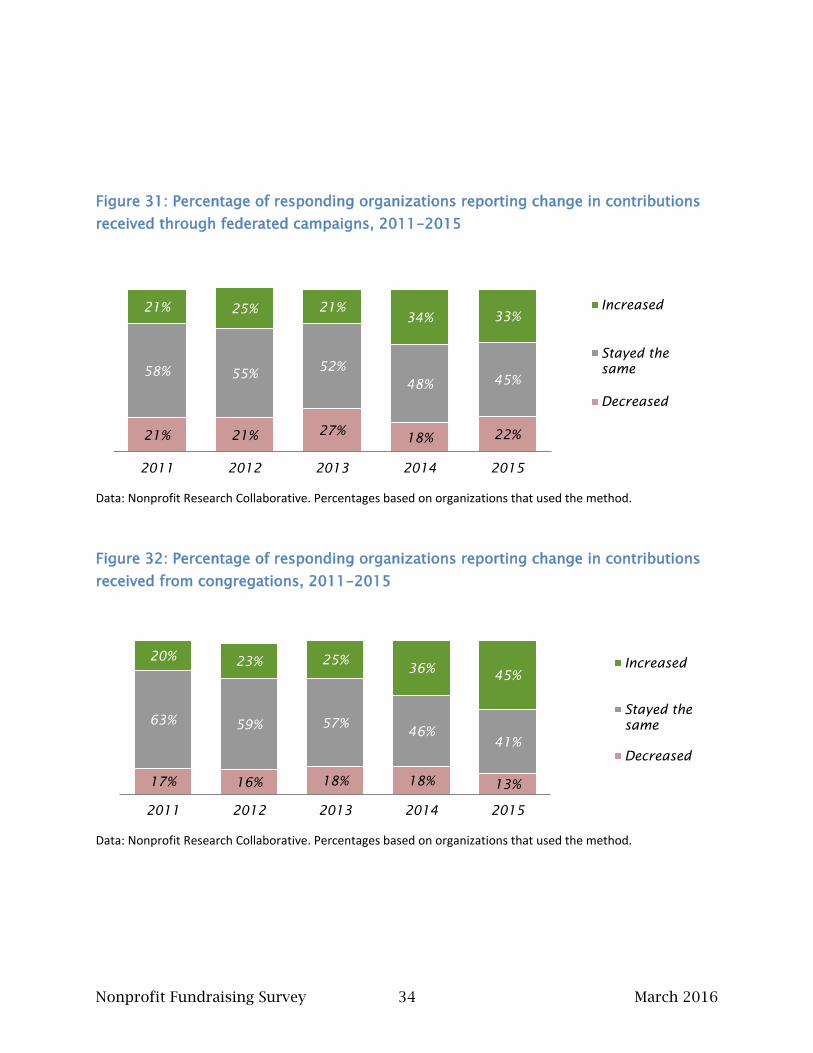

Figure 31: Percentage of responding organizations reporting change in contributions

received through federated campaigns, 2011-2015

Data: Nonprofit Research Collaborative. Percentages based on organizations that used the method.

Figure 32: Percentage of responding organizations reporting change in contributions

received from congregations, 2011-2015

Data: Nonprofit Research Collaborative. Percentages based on organizations that used the method.

21% 21% 27%

18% 22%

58% 55% 52%

48% 45%

21% 25% 21%

34% 33%

2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

17% 16% 18% 18% 13%

63% 59% 57%

46%

41%

20% 23% 25%

36% 45%

2011 2012 2013 2014 2015

Increased

Stayed the

same

Decreased

Nonprofit Fundraising Survey 35 March 2016

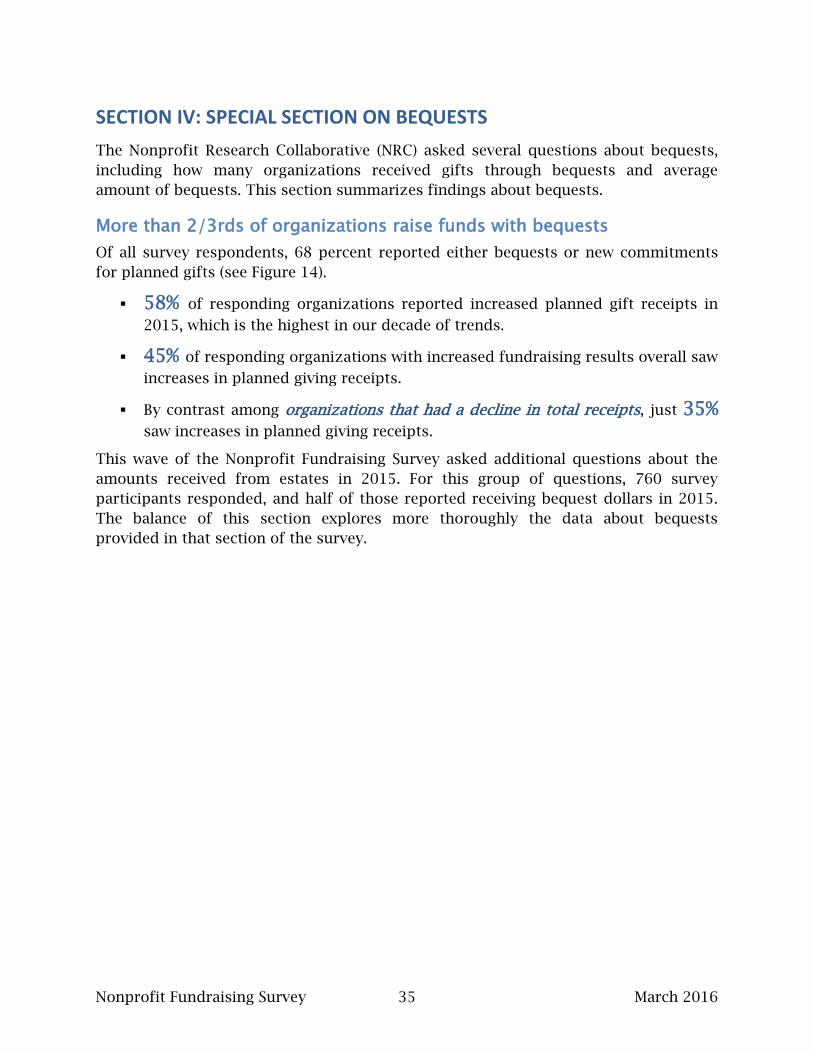

SECTION IV: SPECIAL SECTION ON BEQUESTS

The Nonprofit Research Collaborative (NRC) asked several questions about bequests,

including how many organizations received gifts through bequests and average

amount of bequests. This section summarizes findings about bequests.

More than 2/3rds of organizations raise funds with bequests

Of all survey respondents, 68 percent reported either bequests or new commitments

for planned gifts (see Figure 14).

58% of responding organizations reported increased planned gift receipts in

2015, which is the highest in our decade of trends.

45% of responding organizations with increased fundraising results overall saw

increases in planned giving receipts.

By contrast among organizations that had a decline in total receipts, just 35%saw increases in planned giving receipts.

This wave of the Nonprofit Fundraising Survey asked additional questions about the

amounts received from estates in 2015. For this group of questions, 760 survey

participants responded, and half of those reported receiving bequest dollars in 2015.

The balance of this section explores more thoroughly the data about bequests

provided in that section of the survey.

Nonprofit Fundraising Survey 36 March 2016

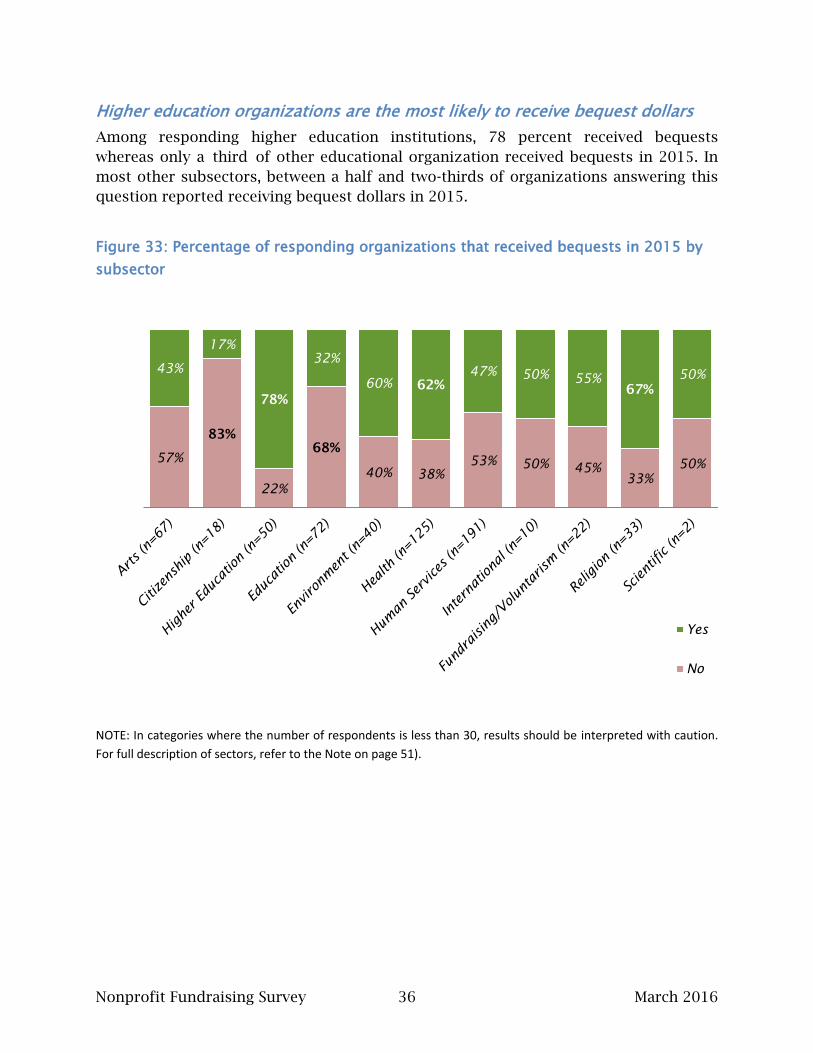

Higher education organizations are the most likely to receive bequest dollars

Among responding higher education institutions, 78 percent received bequests

whereas only a third of other educational organization received bequests in 2015. In

most other subsectors, between a half and two-thirds of organizations answering this

question reported receiving bequest dollars in 2015.

Figure 33: Percentage of responding organizations that received bequests in 2015 by

subsector

NOTE: In categories where the number of respondents is less than 30, results should be interpreted with caution.

For full description of sectors, refer to the Note on page 51).

57%

83%

22%

68%

40% 38%

53% 50% 45%

33%

50%

43%

17%

78%

32%

60% 62%

47% 50% 55%

67%

50%

Yes

No

Nonprofit Fundraising Survey 37 March 2016

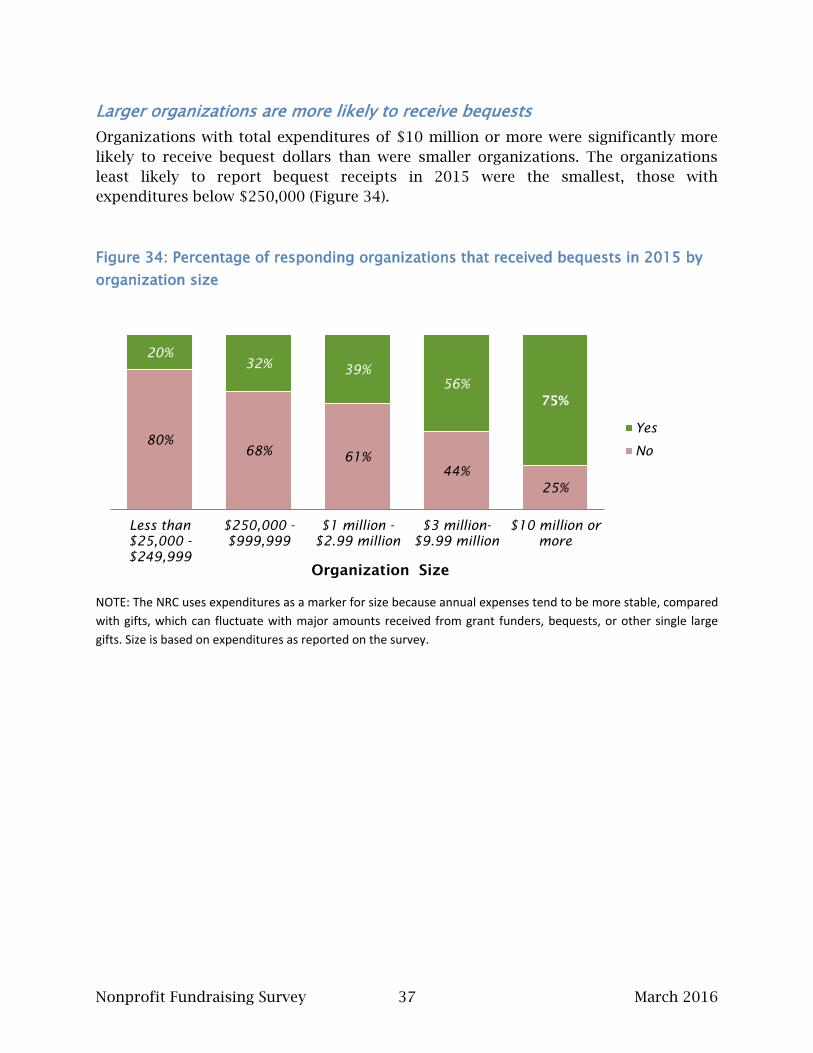

Larger organizations are more likely to receive bequests

Organizations with total expenditures of $10 million or more were significantly more

likely to receive bequest dollars than were smaller organizations. The organizations

least likely to report bequest receipts in 2015 were the smallest, those with

expenditures below $250,000 (Figure 34).

Figure 34: Percentage of responding organizations that received bequests in 2015 by

organization size

NOTE: The NRC uses expenditures as a marker for size because annual expenses tend to be more stable, compared

with gifts, which can fluctuate with major amounts received from grant funders, bequests, or other single large

gifts. Size is based on expenditures as reported on the survey.

80%

68% 61%

44%

25%

20%

32% 39%

56%

75%

Less than

$25,000 -

$249,999

$250,000 -

$999,999

$1 million -

$2.99 million

$3 million-

$9.99 million

$10 million or

more

Yes

No

Organization Size

Nonprofit Fundraising Survey 38 March 2016

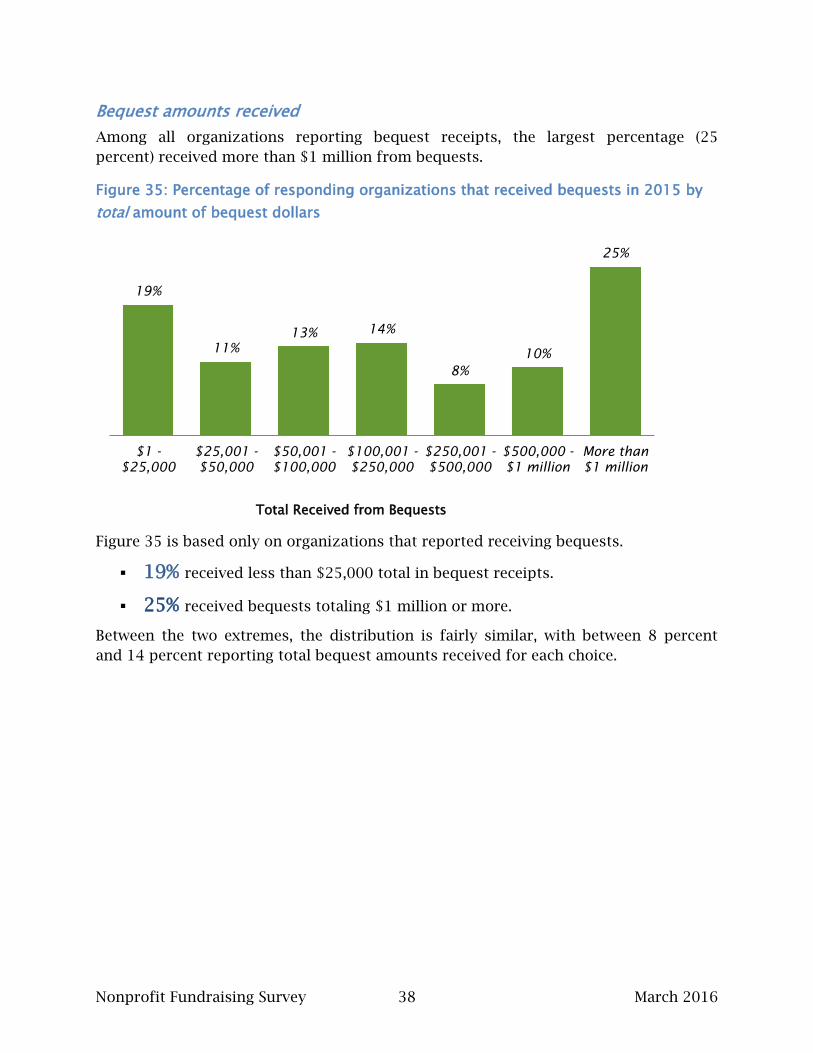

Bequest amounts received

Among all organizations reporting bequest receipts, the largest percentage (25

percent) received more than $1 million from bequests.

Figure 35: Percentage of responding organizations that received bequests in 2015 by

total amount of bequest dollars

Figure 35 is based only on organizations that reported receiving bequests.

19% received less than $25,000 total in bequest receipts.

25% received bequests totaling $1 million or more.

Between the two extremes, the distribution is fairly similar, with between 8 percent

and 14 percent reporting total bequest amounts received for each choice.

19%

11%

13% 14%

8%

10%

25%

$1 -

$25,000

$25,001 -

$50,000

$50,001 -

$100,000

$100,001 -

$250,000

$250,001 -

$500,000

$500,000 -

$1 million

More than

$1 million

Total Received from Bequests

Nonprofit Fundraising Survey 39 March 2016

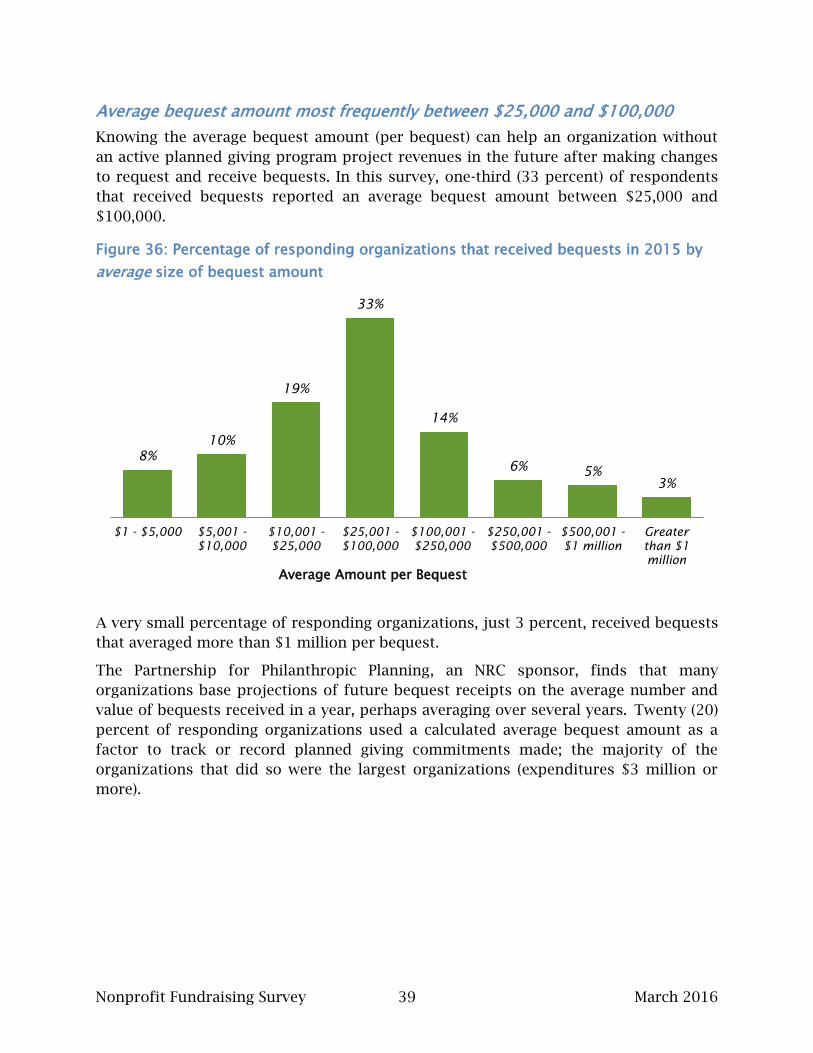

Average bequest amount most frequently between $25,000 and $100,000

Knowing the average bequest amount (per bequest) can help an organization without

an active planned giving program project revenues in the future after making changes

to request and receive bequests. In this survey, one-third (33 percent) of respondents

that received bequests reported an average bequest amount between $25,000 and

$100,000.

Figure 36: Percentage of responding organizations that received bequests in 2015 by

average size of bequest amount

A very small percentage of responding organizations, just 3 percent, received bequests

that averaged more than $1 million per bequest.

The Partnership for Philanthropic Planning, an NRC sponsor, finds that many

organizations base projections of future bequest receipts on the average number and

value of bequests received in a year, perhaps averaging over several years. Twenty (20)

percent of responding organizations used a calculated average bequest amount as a

factor to track or record planned giving commitments made; the majority of the

organizations that did so were the largest organizations (expenditures $3 million or

more).

8%

10%

19%

33%

14%

6% 5%

3%

$1 - $5,000 $5,001 -

$10,000

$10,001 -

$25,000

$25,001 -

$100,000

$100,001 -

$250,000

$250,001 -

$500,000

$500,001 -

$1 million

Greater

than $1

million

Average Amount per Bequest

Nonprofit Fundraising Survey 40 March 2016

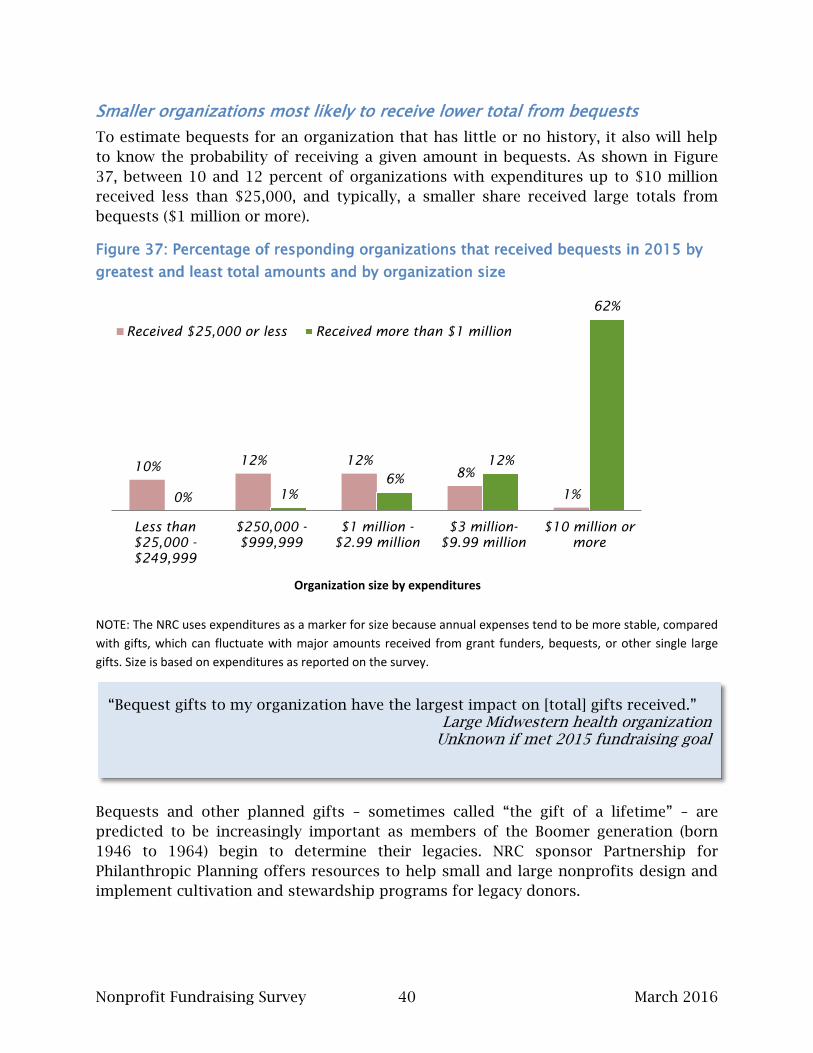

Smaller organizations most likely to receive lower total from bequests

To estimate bequests for an organization that has little or no history, it also will help

to know the probability of receiving a given amount in bequests. As shown in Figure

37, between 10 and 12 percent of organizations with expenditures up to $10 million

received less than $25,000, and typically, a smaller share received large totals from

bequests ($1 million or more).

Figure 37: Percentage of responding organizations that received bequests in 2015 by

greatest and least total amounts and by organization size

NOTE: The NRC uses expenditures as a marker for size because annual expenses tend to be more stable, compared

with gifts, which can fluctuate with major amounts received from grant funders, bequests, or other single large

gifts. Size is based on expenditures as reported on the survey.

Bequests and other planned gifts – sometimes called “the gift of a lifetime” – are

predicted to be increasingly important as members of the Boomer generation (born

1946 to 1964) begin to determine their legacies. NRC sponsor Partnership for

Philanthropic Planning offers resources to help small and large nonprofits design and

implement cultivation and stewardship programs for legacy donors.

10% 12% 12%

8%

1% 0% 1%

6%

12%

62%

Less than

$25,000 -

$249,999

$250,000 -

$999,999

$1 million -

$2.99 million

$3 million-

$9.99 million

$10 million or

more

Received $25,000 or less Received more than $1 million

“Bequest gifts to my organization have the largest impact on [total] gifts received.” Large Midwestern health organization

Unknown if met 2015 fundraising goal

Organization size by expenditures

Nonprofit Fundraising Survey 41 March 2016

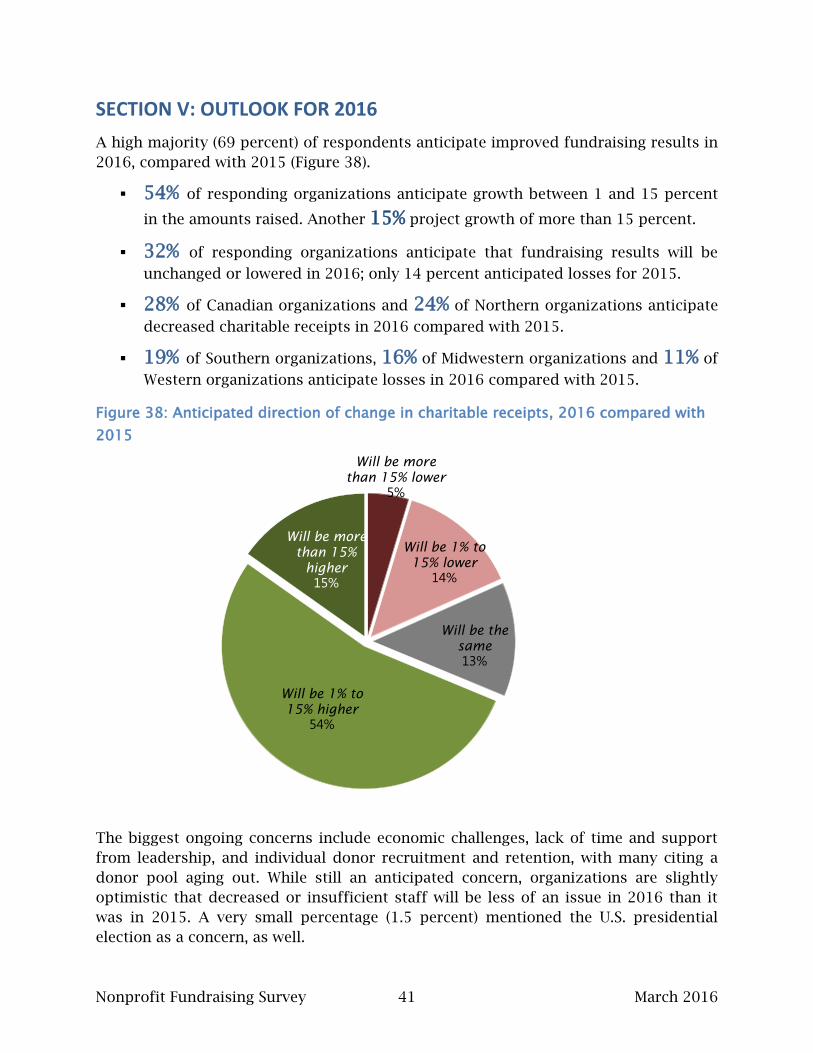

SECTION V: OUTLOOK FOR 2016

A high majority (69 percent) of respondents anticipate improved fundraising results in

2016, compared with 2015 (Figure 38).

54% of responding organizations anticipate growth between 1 and 15 percent

in the amounts raised. Another 15% project growth of more than 15 percent.

32% of responding organizations anticipate that fundraising results will be

unchanged or lowered in 2016; only 14 percent anticipated losses for 2015.

28% of Canadian organizations and 24% of Northern organizations anticipate

decreased charitable receipts in 2016 compared with 2015.

19% of Southern organizations, 16% of Midwestern organizations and 11% of

Western organizations anticipate losses in 2016 compared with 2015.

Figure 38: Anticipated direction of change in charitable receipts, 2016 compared with

2015

The biggest ongoing concerns include economic challenges, lack of time and support

from leadership, and individual donor recruitment and retention, with many citing a

donor pool aging out. While still an anticipated concern, organizations are slightly

optimistic that decreased or insufficient staff will be less of an issue in 2016 than it

was in 2015. A very small percentage (1.5 percent) mentioned the U.S. presidential

election as a concern, as well.

Will be more

than 15% lower

5%

Will be 1% to

15% lower

14%

Will be the

same

13%

Will be 1% to

15% higher

54%

Will be more

than 15%

higher

15%

Nonprofit Fundraising Survey 42 March 2016

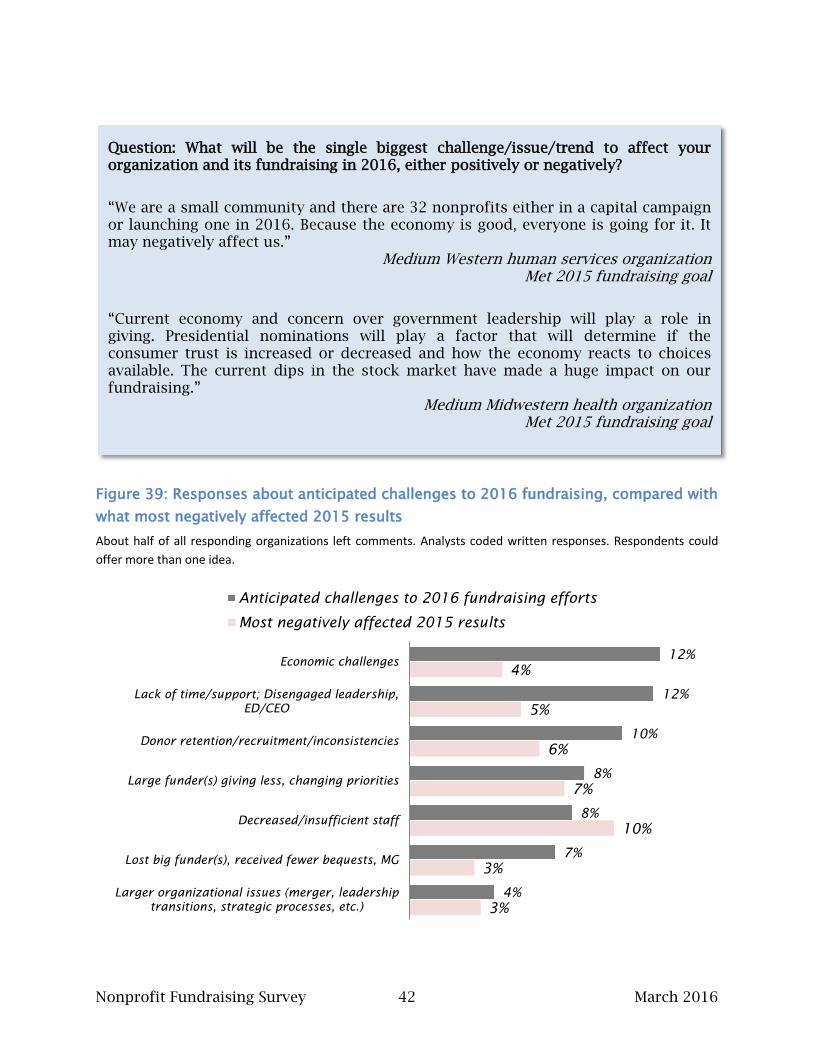

Figure 39: Responses about anticipated challenges to 2016 fundraising, compared with

what most negatively affected 2015 results

About half of all responding organizations left comments. Analysts coded written responses. Respondents could

offer more than one idea.

3%

3%

10%

7%

6%

5%

4%

4%

7%

8%

8%

10%

12%

12%

Larger organizational issues (merger, leadership

transitions, strategic processes, etc.)

Lost big funder(s), received fewer bequests, MG

Decreased/insufficient staff

Large funder(s) giving less, changing priorities

Donor retention/recruitment/inconsistencies

Lack of time/support; Disengaged leadership,

ED/CEO

Economic challenges

Anticipated challenges to 2016 fundraising efforts

Most negatively affected 2015 results

Question: What will be the single biggest challenge/issue/trend to affect your organization and its fundraising in 2016, either positively or negatively?

“We are a small community and there are 32 nonprofits either in a capital campaign or launching one in 2016. Because the economy is good, everyone is going for it. It may negatively affect us.”

Medium Western human services organization Met 2015 fundraising goal

“Current economy and concern over government leadership will play a role in giving. Presidential nominations will play a factor that will determine if the consumer trust is increased or decreased and how the economy reacts to choices available. The current dips in the stock market have made a huge impact on our fundraising.”

Medium Midwestern health organization Met 2015 fundraising goal

Nonprofit Fundraising Survey 43 March 2016

For the most part, more respondents project challenges in 2016 from issues that

negatively affected fundraising results in 2015. The area of most concern – and the

area with the largest change from 2015 actual impact to projected 2016 impact, is the

economy (Figure 39).

Despite predicting growth overall, responding organizations are less optimistic that

issues that positively affected their 2015 fundraising will reoccur in 2016 (Figure 40).

Only 5 percent of responding organizations anticipate major gifts and bequests to help

lift their 2016 fundraising results, whereas major gifts and bequests combined was the

single largest factor (reported by 15 percent) that positively affected 2015 results.

Responding organizations remain cautiously optimistic that intentions to work

smarter, executing a fundraising plan, and gifts from new, ongoing, or ending major or

capital campaigns will be positive impacts to 2016 fundraising. It is interesting to note

that one factor entirely in the organization’s control – asking, stewardship, and

cultivation – is not identified as a key element to make a positive impact in 2016.

Figure 40: Responses about anticipated positive impact to 2016 fundraising, compared

with what most positively affected 2015 results

About half of all responding organizations left comments. Analysts coded written responses. Respondents could

offer more than one idea.

6%

15%

9%

5%

4%

12%

8%

9%

14%

4%

5%

5%

6%

6%

6%

7%

15%

18%

Successful event/anniversary

Major gifts, bequests

Institutional donors giving more

Strong staff, board, volunteers

Media/good PR

Better asking, stewardship, cultivation

Increased staff

Major campaign(s) gifts

Working smarter overall; having/executing

a plan

Anticipated positive impact to 2016 fundraising efforts

Most positively affected 2015 results

Nonprofit Fundraising Survey 44 March 2016

Question: What special circumstances affect the change you anticipate – increased or decreased charitable receipts – in 2016 compared with 2015?

“We are utilizing more opportunities to give and have been in the news recently due to our supported organization’s budget cuts, which has created increased new donors and increased dollars from current/past donors. We also are targeting the corporate market, which had not been cultivated outside of a capital campaign previously.”

Small to Medium-sized Midwestern education organization Did not meet 2015 fundraising goal

“The past two years have been special efforts – first of board, then asking more of major donors and seeking new donors, to meet budget. The approach now is to stabilize this new, higher level of giving in a way that is sustainable, which is to challenge each donor to [make] a larger gift.”

Small to Medium-sized Northern arts organization Met 2015 fundraising goal

Nonprofit Fundraising Survey 45 March 2016

CONCLUSION

Charitable organizations in the United States and Canada report a slight upswing in

the percentage seeing increases in fundraising revenue received in 2015 compared

with 2014. The majority (65 percent) of responding organizations reported an increase

in charitable receipts. Nearly three-quarters (73 percent) said they met their

fundraising goals.

Meeting goal and raising more are both strongly associated with total expenditures in

the organization, with larger organizations more likely to report fundraising success

overall. In this year’s study, unlike some prior years, we do find regional differences.

Organizations in the U.S. West and Canada were likely to report growth in funds raised,

whereas the U.S South was substantially less likely compared with other regions to see

an increase.

Among the fundraising methods used, results are generally similar to 2014, with the

notable difference that in several methods, more organizations report a drop in 2015

than did in 2014. Fewer organizations reported gift receipts remaining the same in

most of these methods. That is, the types of organizations that might have reported

stable fundraising in 2014 become somewhat more likely in 2015 to report a decline

for some methods, including major gifts, direct mail corporate giving, and others that

often form a large portion of an organization’s portfolio.

Bequests play an important role, with about two-thirds of organizations reporting

bequest activity – either actual funds received or new planned gift commitments

documented. The largest portion of organizations (33 percent) reported receiving

bequests that averaged between $25,000 and $100,000 per estate. This information

may be useful for organizations that are just beginning active donor engagement for

legacy gifts.

Despite a highly volatile, and even declining, stock market toward the end of 2015 and

in early 2016 when we were in the field, organizations in this study remain optimistic

that 2016 will be a successful year for fundraising. Nearly 7 in 10 predict growth in

funds received and just 14 percent expect a decline.

Nonprofit Fundraising Survey 46 March 2016

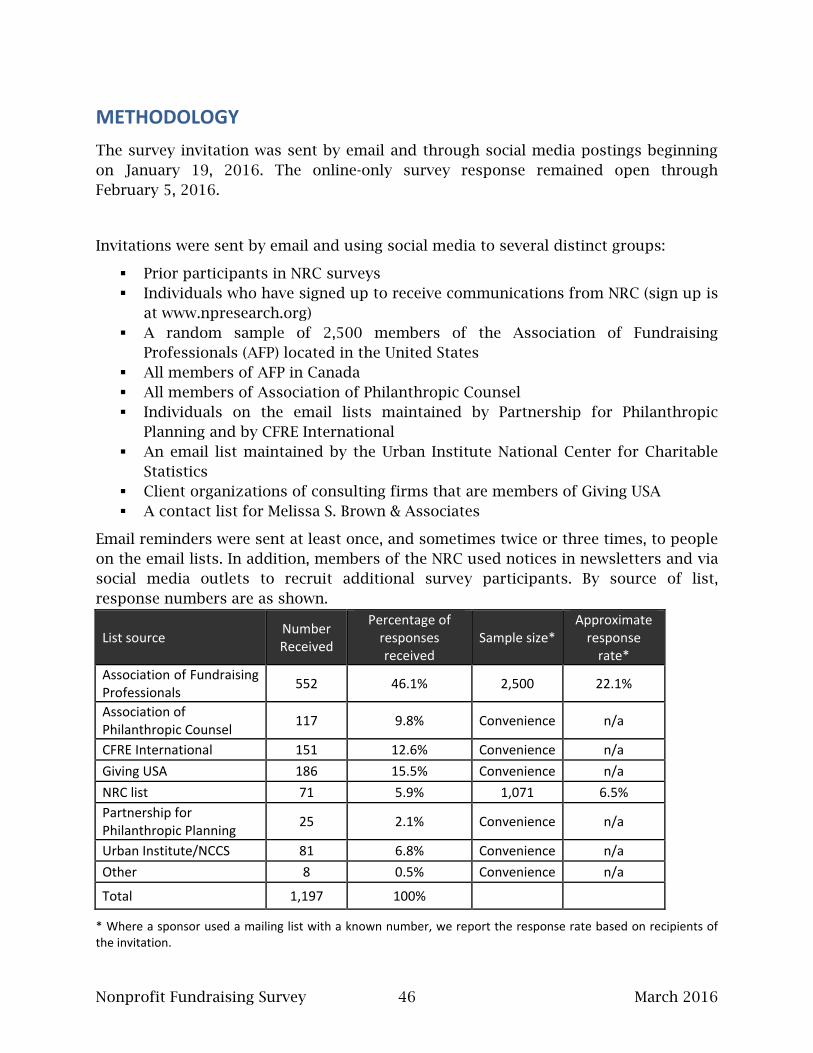

METHODOLOGY

The survey invitation was sent by email and through social media postings beginning

on January 19, 2016. The online-only survey response remained open through

February 5, 2016.

Invitations were sent by email and using social media to several distinct groups:

Prior participants in NRC surveys

Individuals who have signed up to receive communications from NRC (sign up is

at www.npresearch.org)

A random sample of 2,500 members of the Association of Fundraising

Professionals (AFP) located in the United States

All members of AFP in Canada

All members of Association of Philanthropic Counsel

Individuals on the email lists maintained by Partnership for Philanthropic

Planning and by CFRE International

An email list maintained by the Urban Institute National Center for Charitable

Statistics

Client organizations of consulting firms that are members of Giving USA

A contact list for Melissa S. Brown & Associates

Email reminders were sent at least once, and sometimes twice or three times, to people

on the email lists. In addition, members of the NRC used notices in newsletters and via