wood energy final

DESCRIPTION

wood energyTRANSCRIPT

April 2004 ISSN 1239-1336ISBN 952-457-151-X

National Technology AgencyP.O. Box 69, (Kyllikinportti 2), FI-00101 Helsinki, Finland

Tel. +358 105 2151, fax +358 9 694 9196e-mail: [email protected]

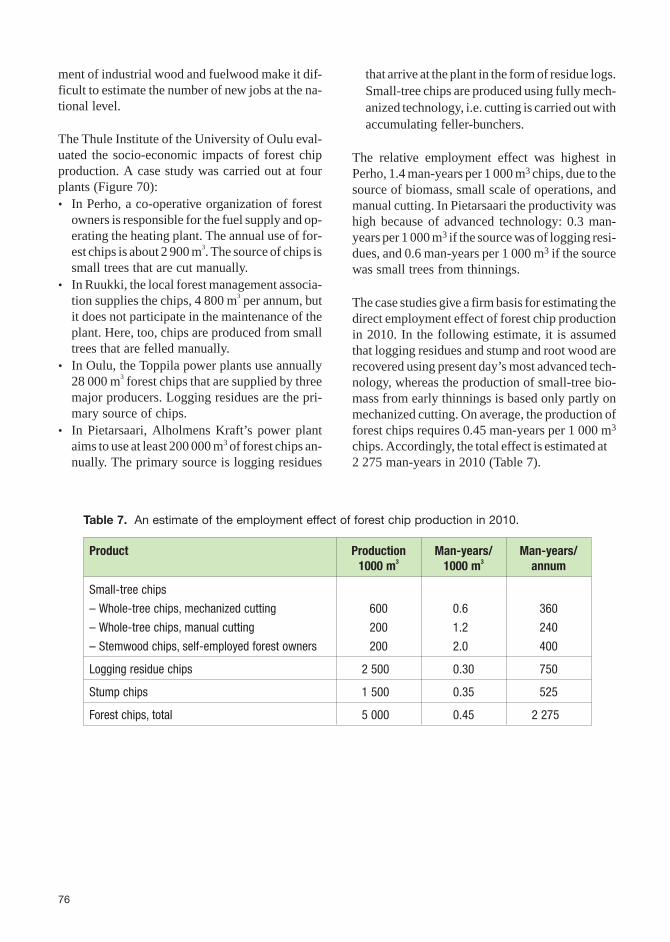

www.tekes.fi

Developing technology for large-scale production of forest chipsWood Energy Technology Programme 1999–2003

Final Report

Tekes• D

eveloping technology for large-scale p

roduction of forest chip

s – Wood

Energy Technology P

rogramm

e 1999–2003

Final Rep

ort

6

04

Developing technologyfor large-scale productionof forest chipsWood Energy Technology Programme1999–2003

Final ReportTechnology Programme Report 6/2004

Developing technology for large-scaleproduction of forest chips

Wood Energy Technology Programme1999–2003

Final Report

Pentti HakkilaVTT Processes

National Technology Agency

Technology Programme Report 6/2004Helsinki 2004

Tekes – your contact for Finnish technology

Tekes, the National Technology Agency, is the main funding organisation forapplied and industrial R&D in Finland. Funding is granted from the statebudget.

Tekes’ primary objective is to promote the competitiveness of Finnish in-dustry and the service sector by technological means. Activities aim to diver-sify production structures, increase production and exports and create afoundation for employment and social well-being. Tekes finances appliedand industrial R&D in Finland to the extent of about 400 million euros annually.The Tekes network in Finland and overseas offers excellent channels for co-operation with Finnish companies, universities and research institutes.

Technology programmes – part of the innovation chain

The technology programmes are an essential part of the Finnish innovationsystem. These programmes have proved to be an effective form of cooper-ation and networking for companies and the research sector for developinginnovative products and processes. Technology programmes promote de-velopment in specific sectors of technology or industry, and the results ofthe research work are passed on to business systematically. The pro-grammes also serve as excellent frameworks for international R&D cooper-ation. In 2004, 25 extensive technology programmes are under way.

Copyright Tekes 2004. All rights reserved.This publication includes materials protected under copyright law, the copyrightfor which is held by Tekes or a third party. The materials appearing inpublications may not be used for commercial purposes. The contents ofpublications are the opinion of the writers and do not represent the officialposition of Tekes. Tekes bears no responsibility for any possible damagesarising from their use. The original source must be mentioned when quoting fromthe materials.

ISSN 1239-1336ISBN 952-457-151-X

Cover: Oddball Graphics OyPage layout: DTPage Oy

Printers: Paino-Center Oy, Sipoo 2004

Foreword

Finland is the world leader in utilization of bioenergy. The role of wood as a sourceof energy is more important than in any other industrialized country, as 20 % of theprimary energy consumed is derived from wood-based fuels.

The goal is to further increase the use of wood fuels because the mitigation of cli-mate change requires the reduction of CO2 emissions. In Finland, one of the majormeans to meet the challenge is to replace fossil fuels with forest biomass. The targetof the Finnish energy and climate strategies is to raise the annual production of for-est chips to 5 million m3 or 0.9 Mtoe by 2010.

In 1999, the National Technology Agency Tekes established a five-year Wood En-ergy Technology Programme to develop efficient technology for the large-scaleproduction of forest chips for consumption by heating and power plants. In 2002,the programme was extended to include a sub-programme on small-scale produc-tion and use of wood fuels. This final report summarizes the results of theprogramme, excluding the sub-programme, which will continue to the end of 2004.

As of January 2004, the programme consisted of 44 research projects, 46 industrialprojects and 29 demonstration projects, in which 27 research organizations and 53enterprises participated. Close collaboration between researchers and practitionersenabled the programme to focus on key problems, to build-up know-how and to fa-cilitate its rapid application in practice.

Throughout the programme, the operating environment changed. Today, much ofthe population, and decision-makers in government and industry support the in-creased use of forest energy wholeheartedly. Forest industry has adopted a pioneer-ing role, the engineering industry has developed innovative technology and equip-ment, and heating and power plants have adapted their fuel handling and combus-tion facilities for wood fuels. The capacity of these plants is sufficient to consume allavailable wood fuels, as long as the cost is competitive. Furthermore, reliable deliv-ery organizations for forest chips are now in place, and the harmful variation of chipquality has been reduced, although not totally eliminated. At first, the cost of forestchips was lowered, but an increase in the demand for forest chips and lengtheninghauling distances are increasing the cost of production. During the five-year periodof the programme, the use of forest chips was quadrupled.

Finland has strengthened its position among the forerunners in the field of wood en-ergy. This positive development is a result of many factors, and the Wood EnergyTechnology Programme has been one of the links in the chain. Tekes wishes to thankall the parties who contributed to the programme. Special thanks are extended to the

Executive Board for its strong support and supervision, and the coordinating team atVTT Processes: Programme Manager Pentti Hakkila, Product Manager EijaAlakangas and Programme Coordinator Kati Veijonen.

Helsinki, April 2004

Tekes, the National Technology Agency

Summary

The national Wood Energy Technology Pro-gramme was carried out by Tekes during the period1999–2003 to develop efficient technology forlarge-scale production of forest chips fromsmall-sized trees and logging residues. This is thefinal report of the programme, and it outlines thegeneral development of forest chip procurementand use during the programme period. In 2002, asub-programme was established to address small-scale production and use of wood fuels. This sub-programme will continue to the end of 2004, and itis not reported here.

The programme was coordinated by VTT Pro-cesses. As of January 2004, the programme con-sisted of 44 public research projects, 46 industrialor product development projects, and 29 demon-stration projects. Altogether, 27 research organiza-tions and 53 enterprises participated. The total costof the programme was 42 M€ of which 13 M€ wasprovided by Tekes. The Ministry of Trade and In-dustry provided investment aid for the new tech-nology employed in the demonstration projects.

When the programme was launched at the end ofthe 1990s, the major barriers to the use of forestchips were high cost of production, shortage of re-liable chip procurement organizations, and the un-satisfactory quality of fuel. Accordingly, the pro-gramme focused largely on these problems. In ad-dition, upgrading of the fuel properties of bark wasalso studied.

The production of forest chips must be adapted tothe existing operating environment and infrastruc-ture. In Finland, these are charaterized by rich bio-mass potential, a sophisticated and efficient orga-nization for the procurement of industrial timber, alarge capacity of heating and CHP plants to usewood fuels, the possibility to co-fire wood andpeat, and the unreserved acceptance of society atlarge. A goal of Finnish energy and climate strate-

gies is to use 5 million m3 (0.9 Mtoe) chips annu-ally by 2010.

The Wood Energy Technology Programme was animportant link in the long chain of activities that re-sulted in an unforeseen growth in the use of forestchips. The programme provided a frame and forumfor joint research and development efforts. The keyrole was played by the participating enterprises inthe fields of forest industries, production of fuelsand energy, and machine manufacturing. The roleof forest machine and timber truck entrepreneursalso was of utmost importance.

Forest chip production technology matured duringthe programme period. Chips from logging resi-dues from regeneration areas remained the cheap-est and most abundant source. In 2002 they cov-ered 63% of the total production of forest chips. Asthe demand for carbon-neutral wood fuels grew,industry sought for additional biomass sources andextended procurement operations to whole-treematerial from early thinnings and even stump androot wood from regeneration areas.

Special emphasis was placed on the developmentof system know-how. Baling technology revolution-ized the transportation of uncomminuted biomassand opened the way to centralized comminution atthe plant. Several large CHP plants installed a sta-tionary crusher that, in turn, made it possible toprocess stump and root wood. By 2004, some 24residue balers with a total annual capacity of 0.6million m3 were in operation in Finland. The newtechnology was found especially attractive with re-spect to the flexible process control of large-scaleprocurement of forest chips.

The traditional basic solution, comminution atlanding, still held its leading position. The intro-duction of new chipper-trucks helped to cool thehot chain that is normally a weakness of the sys-tem. In addition to its application to logging resi-

dues, this system is suitable for whole-tree chip-ping as well.

Regarding small-tree chips, the problem has beenlow productivity and the high cost of manual fell-ing. After a long period of slow development, theuse of accumulating felling heads is becomingcommon, and the production chain is becomingfully mechanized. Independent forest machine en-trepreneurs now have a possibility to produce chipsfrom young thinning stands independently of theharvesting of industrial timber.

New technologies, the refinement of procurementlogistics and learning through experience each re-duce the cost of production. However, as the pro-duction is increasing rapidly, the operations haveto be extended to more and more difficult standconditions and distant locations. The average costof forest chips has consequently increased in spiteof technical developments. In 2003, the price ofchips at the plant was 10 €/MWh.

Chip production organizations developed rapidly.Biowatti and UPM both produced 0.5 million m3

(1 TWh) forest chips in 2003. Forest chips becamea credible fuel even for large CHP plants. Never-theless, to increase competition small local pro-ducers are also needed, and forest machine entre-preneurs are examining the possibilities of net-working in order to build secure delivery options.

The use of forest chips is increasing in Finlandfaster than in any other country. The positive envi-ronment for growth has been a crucial factor for thedevelopment and deployment of new technology.It has given space to the industry to experiment andmotivated investments, and it has strengthenedFinland’s position as a pioneer.

When the Wood Energy Technology Programmewas launched in 1999, an unofficial goal was to in-crease the use of forest chips fivefold in five years,i.e. 2.5 million m3 in 2003. Consumption statisticsare not yet available, but it is estimated to be 2.1million m3. Thus, the goal will be achieved a yearlate of the schedule, but production will have in-creased fourfold. The official goal, 5 million m3 in2010, seems to be realistic, but the continuous ef-forts of enterprises, research organizations and thepublic sector will be needed to achieve this goal.

Table of contents

Foreword

Summary

1 Wood energy in Finland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.1 Present use of wood fuels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Wood in the energy strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2 The Wood Energy Technology Programme . . . . . . . . . . . . . . . . . . . . . 72.1 The targets of the programme . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82.2 The organization of the programme . . . . . . . . . . . . . . . . . . . . . . . . 82.3 The projects of the programme . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.4 Sub-programme for small-scale production and use of wood fuels . . 102.5 The international dimension of the programme . . . . . . . . . . . . . . . 11

3 The operating environment of forest chip production . . . . . . . . . . . . 133.1 Management of forests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133.2 Procurement of industrial timber. . . . . . . . . . . . . . . . . . . . . . . . . . 163.3 Utilization capacity of forest chips . . . . . . . . . . . . . . . . . . . . . . . . 173.4 Co-combustion of wood and peat . . . . . . . . . . . . . . . . . . . . . . . . 20

4 Raw material base of forest chips . . . . . . . . . . . . . . . . . . . . . . . . . . . 214.1 Stemwood loss from logging operations . . . . . . . . . . . . . . . . . . . . 214.2 Biomass residues from final fellings . . . . . . . . . . . . . . . . . . . . . . . 234.3 Small trees from early thinnings . . . . . . . . . . . . . . . . . . . . . . . . . . 244.4 Stump and root wood from final fellings . . . . . . . . . . . . . . . . . . . . 244.5 Forest chip potential of the Finnish forests . . . . . . . . . . . . . . . . . . 26

5 Production technology of forest chips . . . . . . . . . . . . . . . . . . . . . . . . 295.1 Production systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 295.2 Production organizations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 375.3 Production logistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 405.4 Production equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 425.5 Buffer and security storage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 475.6 Receiving and handling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 495.7 Production costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

6 Quality control of forest chips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 536.1 Moisture content . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 536.2 Other fuel properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

7 Use of forest chips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 597.1 The driving forces . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 597.2 The users . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

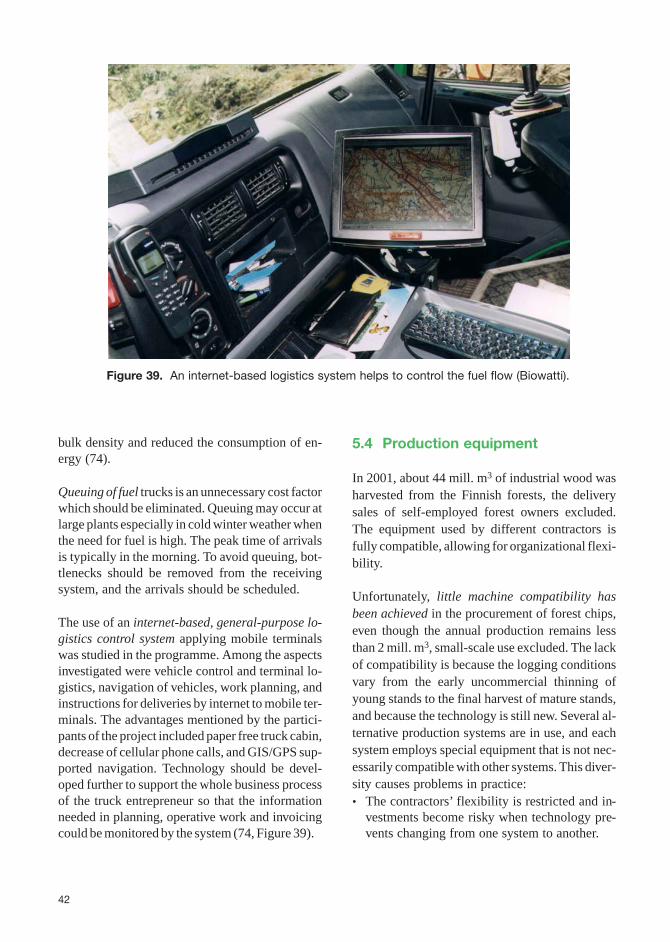

8 Use of bark . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 658.1 Barking residues as a fuel source . . . . . . . . . . . . . . . . . . . . . . . . . 658.2 Improving the fuel properties of bark . . . . . . . . . . . . . . . . . . . . . . 67

9 The impacts of forest chip production . . . . . . . . . . . . . . . . . . . . . . . . 699.1 Impacts on forest increment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 699.2 Impacts on the management of forests . . . . . . . . . . . . . . . . . . . . . 719.3 Socio-economic impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

10 State of the art . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

Appendix 1. The Executive Board of the Programme . . . . . . . . . . . . . . . . . 89

Appendix 2. The Projects of the Programme . . . . . . . . . . . . . . . . . . . . . . . 91

Tekes’ Technology Programme Reports . . . . . . . . . . . . . . . . . . . . . . . . . 99

1 Wood energy in Finland

The harsh climate, long transport distances, highstandard of living and the predominance of pro-cess-type industries raise the annual use of energyin Finland to 6.3 toe per capita. As there are no de-posits of fossil fuels and the country is rich in for-ests, large amounts of wood have traditionally beenused for the production of energy. Before industri-alization, wood crops were used mainly for fuel,charcoal and tar. During the 19th Century, theslash-and-burn agriculture also reduced the forestresources (Figure 1).

It was not until the second quarter of the 20th Cen-tury that more wood was used for raw material thanfor fuel. Even then, wood remained the primarysource of energy, and on the eve of the Winter Warat the end of the 1930s, wood accounted for 70 % ofall fuels in Finland. Fuelwood only lost its domi-nant position in the late 1950s.

1.1 Present use of wood fuels

The total consumption of wood in Finland is about 75mill. m3 annually. Per capita consumption is 20 timeshigher than the average in the EU countries (Figure2). Wood and the entire forest cluster have played avery significant role in the national economy.

At present, over 90 % of the wood harvest is used asraw material by the forest industries. Only 5 mill.m3 per annum is used directly for fuel, but muchmore energy is derived from forest industries´ pro-cessing residues. The proportion of the energycomponent in the timber flow is approximately asfollows:• In sawmilling 15–25 % (sawdust, debarking and

screening residues)• In plywood manufacturing 30–40 % (log ends,

waste from plies, dust, debarking and screeningresidues)

1

100

80

60

40

20

Structure of removal, %

1850

50

1.6

1900

50

2.7

1950

53

4.0

2000

70

5.2Population, mill.

Felling, mill. m /a3

Natural loss andlogging waste

Fuelwood andrural construction wood

Slash-and-burn,tar and charcoal

Export

Pulpwood

Sawlogs

Figure 1. Removal of stem wood from the Finnish forests since the mid-1800s(48, the figure has been extended to 2000).

• In mechanical pulping 10–15 % (debarking andscreening residues)

• In chemical pulping 50–60 % (black liquor, de-barking and screening residues). Black liquor isa lignin-rich byproduct of kraft pulping that con-tains more than a half of the initial heating valueof pulpwood. Black liquor is burnt for simulta-

neous recovery of energy and pulping chemi-cals. It is a significant fuel, particularly in Fin-land and Sweden, where most European kraftmills are located.

Process residues included, almost a half of thewood used in Finland ends up as fuel, either di-

2

2

4

6

8

10

12

14

16

Finland Sweden Austria France Germany Denmark U.K. Holland EUaverage

Net importsIndigenous wood

m / capita3

14.4

7.7

2.5

0.6 0.4 0.4 0.1 0.10.8

Figure 2. Consumption of roundwood per capita in selected EU countries in 1999(56).

5

10

15

20

25

30

Woodpulp

Sawngoods

Compositeboards

Otherproducts

Blackliquor

Sawdustetc.

Pellets,briquets

Bark Traditionalfirewood

Forestchips

25.9

13.3

1.90.3

17.7

8.6

3.1

0.05

5.4

1.7

Industrial end products 53 % Production of energy 47 %

Indirect use Direct use

Mill. m / annum3

Figure 3. The end use of wood in Finland in 2001 or 2002. Recycled wood ex-cluded (56, 80, 103).

rectly or indirectly (Figure 3). Consequently, 20 %of the total consumption of primary energy, corre-sponding to 6.7 Mtoe in 2002, and 11 % of the elec-tricity, is derived from wood-based fuels (Figure4). These shares are greater than in other industrial-ized countries. More than 20 % of the wood energy,however, is derived from process residues from im-ported wood.

Wood fuels thus come from a large number of in-digenous and foreign sources. By far the most im-portant wood-based fuel is black liquor that is ex-clusively used by the producer. Other large sourcesare debarking residues and the traditional firewoodin small-scale use. Forest chips are still a relativelymodest source of fuel, but it has considerablegrowth potential (Figure 5).

3

8.7

5.6

4.5

3.7

1.61.0

2.1

0.90.3

2.4

1.6

1.1

2

4

6

8

10

Oil Nuclearpower

Coal Naturalgas

Residuesfrom

importedwood

Importedelectricity

Peat Hydropower

Others Wood-basedfuels

5.1

Black liquor

Bark, sawdust, etc.

Traditional firewood

Mtoe / annum

Total consumption 33.5 Mtoe / 2002

Imported energy 75 % Indigenous energy 25 %

Figure 4. Consumption of energy by source in 2002.

15.3

4.5

2.5 1.60.7 0.1 0.1

10

2

4

6

8

10

12

14

16

Bark Sawdust Forestchips

Industrialchips

Recycledwood

Pellets andbriquets

Otherwood

Goal / 2010

Total 25 TWh / 2002

TWh / annum

Figure 5. Consumption of solid wood fuels in heating and power plants in 2002 (103).

1.2 Wood in the energy strategy

The objective of the Government´s energy policy isto ensure the availability of energy, to maintaincompetitive energy prices, and to enable Finland tomeet its international commitments with respect toemissions into the environment (44). As a MemberState of the EU, Finland´s obligation is to decreasethe average greenhouse gas emissions in the years2008–2012 to the level that prevailed in 1990, i.e.76.5 Mt of carbon dioxide equivalent. The targetlevel is currently exceeded by more than 10 %. Thegovernment has to find ways to replace fossil fuelswith renewable energy (95).

In 1999, the Ministry of Trade and Industry ap-proved the Action Plan for Renewable EnergySources (45). The goal is to bring an increase of 50% in the use of renewable energy by 2010, com-pared to the level of 1995. As much as 90 % of theincrease is to be derived from bioenergy, mainlywood-based fuels. The plan was revised in 2002, asthe operating environment was experiencing rapid

change. According to the revised plan, of the dif-ferent sources of renewable energy the growth is tobe fastest in the use of forest chips. In 2010, the en-ergy produced from forest chips will correspond to0.9 Mtoe (Table 1). This will require 5 mill m3 for-est biomass.

Energy derived from forest industry liquid andsolid process residues increased rapidly during thelate 1990s. This was possible because of thegrowth in capacity and wood consumption. How-ever, possibilities for a further expansion of the useof indigenous wood for industrial purposes arelimited and, therefore, additional wood energymust primarily be produced from low-quality re-sidual forest biomass. According to the plan, forestchips alone will cover one third of the increase inthe use of renewable energy during this decade.

The advantage of forest chips is that the input/out-put ratio of energy is 1/30. The entire energy con-tent of fuel can thus be used for replacing fossil fu-els, whereas the energy produced from industrial

4

Source of energy 1995 2001 2005 2010 2025

Use Mtoe/annum

Direct use of wood-based fuels

Traditional firewood, small scale 1.0 1.1 1.2 1.3 1.4

Forest chips, inc. small scale 0.1 0.2 0.5 0.9 1.5

Indirect use of wood-based fuels:

Black liquor 2.6 3.2 3.4 3.7 4.0

Solid processing residues 1.2 1.8 1.9 2.0 2.2

Wood-based, total 4.9 6.3 7.0 7.9 9.1

Recycled fuels 0.0 0.0 0.1 0.2 0.2

Biogas, agri-biomass, liquid biofuels 0.0 0.0 0.1 0.2 0.5

Hydro power 1.1 1.1 1.2 1.2 1.4

Wind power 0.0 0.0 0.0 0.1 0.4

Heat pumps, solar energy 0.0 0.1 0.1 0.2 0.5

Renewable, grand total 6.1 7.6 8.6 9.8 12.1

Table 1. The revised plan of the Ministry of Trade and Industry for renewable energy (46).

residues is actually needed primarily for the pro-cess itself. It is not available for replacing fossil fu-els elsewhere.

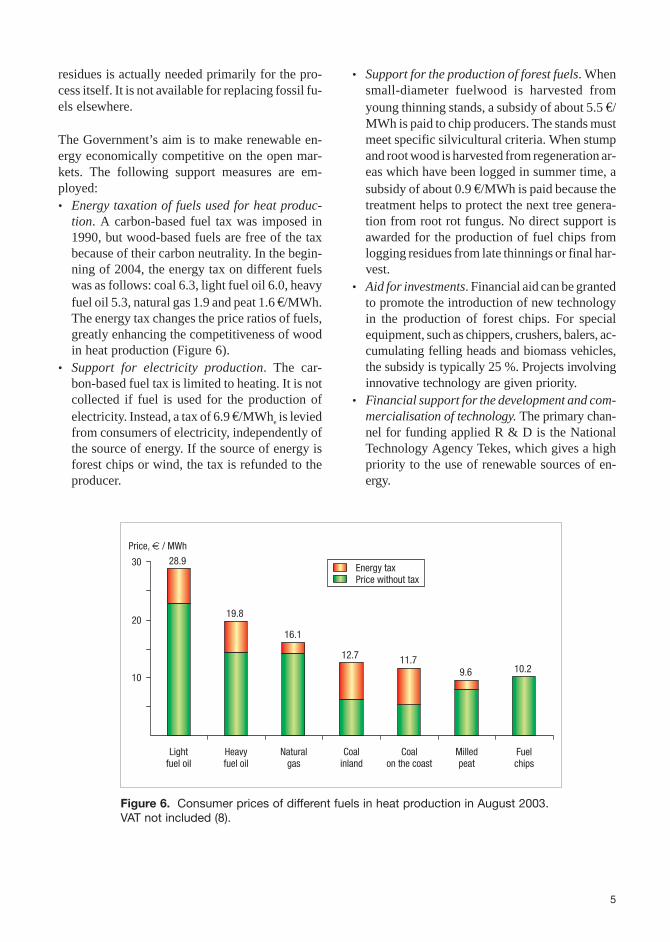

The Government’s aim is to make renewable en-ergy economically competitive on the open mar-kets. The following support measures are em-ployed:• Energy taxation of fuels used for heat produc-

tion. A carbon-based fuel tax was imposed in1990, but wood-based fuels are free of the taxbecause of their carbon neutrality. In the begin-ning of 2004, the energy tax on different fuelswas as follows: coal 6.3, light fuel oil 6.0, heavyfuel oil 5.3, natural gas 1.9 and peat 1.6 €/MWh.The energy tax changes the price ratios of fuels,greatly enhancing the competitiveness of woodin heat production (Figure 6).

• Support for electricity production. The car-bon-based fuel tax is limited to heating. It is notcollected if fuel is used for the production ofelectricity. Instead, a tax of 6.9 €/MWhe is leviedfrom consumers of electricity, independently ofthe source of energy. If the source of energy isforest chips or wind, the tax is refunded to theproducer.

• Support for the production of forest fuels. Whensmall-diameter fuelwood is harvested fromyoung thinning stands, a subsidy of about 5.5 €/MWh is paid to chip producers. The stands mustmeet specific silvicultural criteria. When stumpand root wood is harvested from regeneration ar-eas which have been logged in summer time, asubsidy of about 0.9 €/MWh is paid because thetreatment helps to protect the next tree genera-tion from root rot fungus. No direct support isawarded for the production of fuel chips fromlogging residues from late thinnings or final har-vest.

• Aid for investments. Financial aid can be grantedto promote the introduction of new technologyin the production of forest chips. For specialequipment, such as chippers, crushers, balers, ac-cumulating felling heads and biomass vehicles,the subsidy is typically 25 %. Projects involvinginnovative technology are given priority.

• Financial support for the development and com-mercialisation of technology. The primary chan-nel for funding applied R & D is the NationalTechnology Agency Tekes, which gives a highpriority to the use of renewable sources of en-ergy.

5

10

20

30

Heavyfuel oil

Naturalgas

Coalinland

Coalon the coast

Milledpeat

Fuelchips

Energy taxPrice without tax

Lightfuel oil

Price, / MWh€

28.9

19.8

16.1

12.7 11.79.6 10.2

Figure 6. Consumer prices of different fuels in heat production in August 2003.VAT not included (8).

2 The Wood Energy Technology Programme

The National Technology Agency Tekes is themain public investor in applied and industrial re-search and development in Finland. Renewable en-ergies, an essential issue of subtainable develop-ment, is one of the key strategic areas. About 50 %of Tekes’ funding is focused through technologyprogrammes. Several of the programmes havedealt with bioenergy technology, focusing on areassuch as production of fuels, combustion, conver-sion and environmental impacts (Figure 7).

The production of wood fuels was included for thefirst time in the research cluster under consider-ation in the Bioenergy Research Programme in1993–1998. The programme was aimed at the pro-duction, use and conversion of wood and peat fu-els. When the program was coming to an end, itwas concluded that (98):

• The great potential of bioenergy in Finland hadbeen demonstrated and recognized by the popu-lation at large, and by industry and decisionmakers.

• The use of bioenergy had started to grow.• In the development and application of wood en-

ergy technology Finland, together with Sweden,was among the forerunners.

It was agreed that ensuring further developmentand maintaining the research know-how required anew, coordinated programme. The forest indus-tries and large energy companies were ready to in-crease the use of forest fuels and participate in aforthcoming programme. As many changes wereoccurring in the operating environment, includingthe Kyoto Protocol, the programme had to be re-formed.

7

1990 1995 2000 2005

LIEKKI 2

Combustion

CODEModelling ofcombustionprocesses

Wood combustionin fireplaces

CLIMTECH

Energy formwaste and REF

Artificial dewateringof peat

Use + Conversion

WOOD ENERGYPeat

WoodBIOENERGY

SIHTI

SIHTI IIEnergy and environmental

technology

DENSYDistributedenergy systems

STREAMSWaste management

and recycling

Small-scale wood fuelproduction and use

FINEFine particles

Peat production basedon solar energy

Wood energy clinic Mitigatingof climatechange

JALOFuel conversion

LIEKKI 1

Combustiontechnology

Figure 7. Tekes’ programmes of bioenergy. The area of a rectangle indicates relativeexpenditure (Tekes).

The most abundant reserve of renewable energy isforest biomass, but its utilization was being con-strained by the excessive cost of recovery. Conse-quently, Tekes decided to focus on the develop-ment of production technology for forest chips.The new programme was called the Wood EnergyTechnology Programme, abbreviated in this reportto Wood Energy Programme.

2.1 The targets of the programme

The ultimate target of the Wood Energy Pro-gramme was to create favourable conditions for in-creasing the use of forest chips. Consequently, theprogramme was aimed at developing cost-compet-itive production technologies and procurement lo-gistics for recovering residual biomass. The em-phasis was on developing systems for large-scaleoperations in conjunction with combined heat andpower plants.

Preconditions for a rapid increase in the use of for-est chips are the reduction of costs, improved qual-ity of chips, and reliable delivery systems. Chipsmust also be produced by environmentally soundmethods that support sustainable forest manage-ment. The primary targets of the programme weretherefore:• To integrate energy production into conven-

tional forestry and the procurement of industrialtimber

• To develop production systems and procure-ment logistics suitable for the existing infra-structure

• To develop long-distance transport of chips,uncomminuted loose residues and compositeresidue logs

• To develop technology for receiving, comminuting,handling and storage of wood fuels at the plant

• To encourage the participation of forest machineand truck contractors in the wood fuel branch

• To develop quality control for forest chips andprocessing residues from the forest industries inorder to improve the useability and energy effi-ciency of the plant

• In 2002 a sub-programme was established to ad-dress small-scale production and use of woodfuels.

The programme set for itself an unofficial goal: toincrease the annual use of forest chips from 0.5million m3 in 1998 to 2.5 million m3 in 2003, i.e. afive-fold increase in five years. The final result ofthe consumption in 2003 is not available yet, butthe preliminary estimate is 2.1 million m3. Thismeans that the use of forest chips quadrupled butdid not quintuple during the program period. Thetarget will probably be achieved a year behind theschedule.

2.2 The organization of theprogramme

The programme period was 1999–2003. Theprogramme was composed of projects that typi-cally lasted from 1 to 3 years. There were threetypes of projects:• Projects undertaken by research institutes that

addressed common and general needs. In theseprojects research organizations collaboratedwith industrial partners. The results and know-how achieved are in the public domain.

• Projects dealing with product development, i.e.industrial projects, were related to practical ap-plications. They served specific needs of a sin-gle company or group of companies. Examplesinclude the development of a complete chip pro-curement system, less corrosive combustiontechnique for chips rich in needles, chipper, bun-dler, feller-buncher for small trees, forwarderfor biomass transport, special vehicles for trans-porting forest fuels, and fuel receiving and han-dling system at plant. An industrial project com-monly included co-operation with a research or-ganization. The results and experience fromcompany projects are not necessarily in the pub-lic domain.

• Demonstration projects were aimed to promotethe introduction and deployment of new tech-nologies. Funding was primarily investmentgrant-aid from the Ministry of Trade and Indus-try.

Several research organizations participated in theprogramme: VTT Processes, the Finnish ForestResearch Institute, Metsäteho Oy, University ofJoensuu, University of Jyväskylä, University of

8

Oulu, Helsinki University of Technology, TTS In-stitute, and the Radiation and Nuclear Safety Au-thority of Finland. Each research project had an ad-visory board composed of researchers and practi-tioners from participating organizations. Theboard typically met 2–4 times a year to discuss re-search needs, budget changes and major reportsand to monitor the work programme. The indus-trial projects could also have such a board, but itwas an internal company decision. Altogether, 27research units and 53 enterprises participated in theprogramme. At Tekes Tarja-Liisa Perttala, thenHeikki Kotila and since 2002 Marjatta Aarnialawere responsible for the programme.

The programme was coordinated jointly by MotivaOy and VTT Processes. The former signed the con-tracts and took care of accounting, and the latterwas responsible for daily conducting of the work.The Programme Managers at VTT Processes werein the beginning Satu Helynen and Pentti Hakkilajointly, and since 2000 Pentti Hakkila alone. Since2001, the Programme Coordinator was Kati Vei-jonen. Eija Alakangas was responsible for commu-nications with the interested parties.

Tekes nominated an Executive Board to direct thework. The board was chaired by Pekka Laurila,Managing Director of Biowatti, and cochaired bySeppo Paananen from UPM Forest. The ExecutiveBoard consisted of representatives of the majormarket actors in the forest fuel segment. The fol-lowing organizations were represented:• Biowatti Oy (production and distribution of

wood fuels)• BMH Wood Technology Oy (manufacturer of

receiving and handling equipment)• Forestry Development Centre Tapio (promotion

of private forestry)• Fortum Power and Heat Oy (production of elec-

tricity, heat etc.)• Kvaerner Power Oy (manufacturer of fluidized

bed boilers etc.)• Ministry of Agriculture and Forestry (forest

policy)• Ministry of Trade and Industry (energy policy,

funding of new technology demonstrations)• Pohjolan Voima Oy (production of electricity

and heat)

• Plustech Oy/Timberjack Oy (manufacturer offorest machines)

• Tekes (funding)• Trade Association of Finnish Forestry and Earth

Moving Contractors (forest machine contracting)• UPM Oyj (forest industry, procurement of timber

and wood fuels)• Vapo Oy (production and distribution of peat

and wood fuels)• VTT Processes (programme coordinator)

The total cost of the programme was 42 M€, ofwhich about 13 M€ was provided by Tekes. Themajority of funding was provided by enterprisesfor their own product development projects, andfor public research projects in which industry par-ticipated. Research institutes also provided funds.The Ministry of Trade and Industry promoted thedeployment of new technology by supportingdemonstration projects.

2.3 The projects of the programme

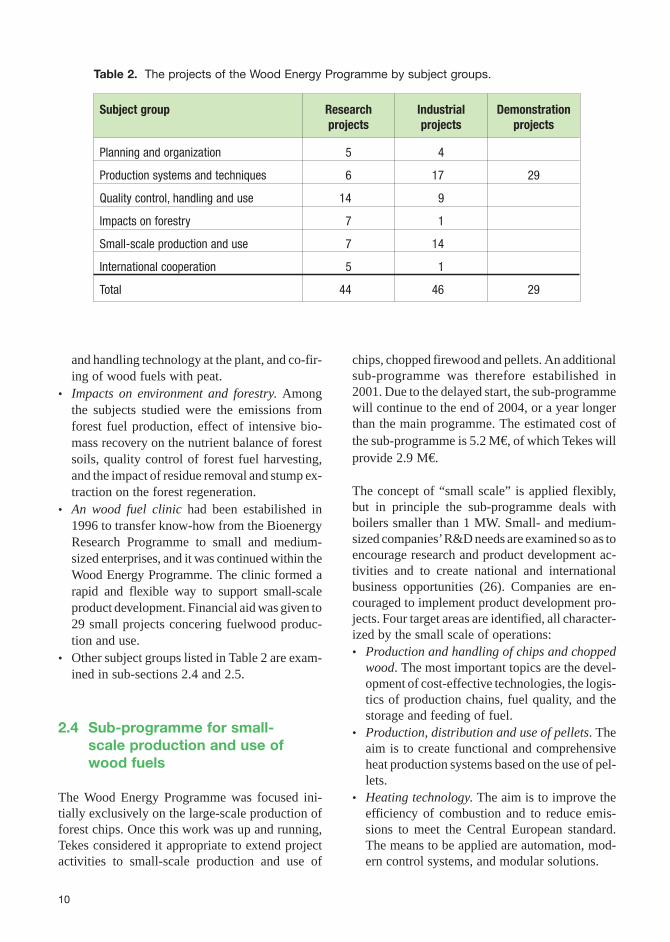

As of February 2004, the programme contained 44research projects, 46 industsry projects and 29demonstration projects. They were divided into 6subject groups (Table 2).• Planning and organization. The subject group

produced the basic information necessary forsystem development and planning of opera-tions. Examples are studies on technical loggingconditions and cost factors of chip procurement,organization of chip procurement, contractornetworks, scaling of fuelwood, and determiningthe boundary between pulpwood and fuelwood.

• Production systems and techniques. This sub-ject group was the core of the programme, and itincluded all demonstration projects. The em-phasis was in the development of machines, ve-hicles, work methods and entire procurementsystems for the production of fuel from forestbiomass.

• Quality control, handling and use. Major topicswere quality control of forest chips and debark-ing residues, the effect of fuel quality on theuseability of a plant, changes in fuel propertiesduring storage, development of fuel receiving

9

and handling technology at the plant, and co-fir-ing of wood fuels with peat.

• Impacts on environment and forestry. Amongthe subjects studied were the emissions fromforest fuel production, effect of intensive bio-mass recovery on the nutrient balance of forestsoils, quality control of forest fuel harvesting,and the impact of residue removal and stump ex-traction on the forest regeneration.

• An wood fuel clinic had been estabilished in1996 to transfer know-how from the BioenergyResearch Programme to small and medium-sized enterprises, and it was continued within theWood Energy Programme. The clinic formed arapid and flexible way to support small-scaleproduct development. Financial aid was given to29 small projects concering fuelwood produc-tion and use.

• Other subject groups listed in Table 2 are exam-ined in sub-sections 2.4 and 2.5.

2.4 Sub-programme for small-scale production and use ofwood fuels

The Wood Energy Programme was focused ini-tially exclusively on the large-scale production offorest chips. Once this work was up and running,Tekes considered it appropriate to extend projectactivities to small-scale production and use of

chips, chopped firewood and pellets. An additionalsub-programme was therefore estabilished in2001. Due to the delayed start, the sub-programmewill continue to the end of 2004, or a year longerthan the main programme. The estimated cost ofthe sub-programme is 5.2 M€, of which Tekes willprovide 2.9 M€.

The concept of “small scale” is applied flexibly,but in principle the sub-programme deals withboilers smaller than 1 MW. Small- and medium-sized companies’R&D needs are examined so as toencourage research and product development ac-tivities and to create national and internationalbusiness opportunities (26). Companies are en-couraged to implement product development pro-jects. Four target areas are identified, all character-ized by the small scale of operations:• Production and handling of chips and chopped

wood. The most important topics are the devel-opment of cost-effective technologies, the logis-tics of production chains, fuel quality, and thestorage and feeding of fuel.

• Production, distribution and use of pellets. Theaim is to create functional and comprehensiveheat production systems based on the use of pel-lets.

• Heating technology. The aim is to improve theefficiency of combustion and to reduce emis-sions to meet the Central European standard.The means to be applied are automation, mod-ern control systems, and modular solutions.

10

Subject group Researchprojects

Industrialprojects

Demonstrationprojects

Planning and organization 5 4

Production systems and techniques 6 17 29

Quality control, handling and use 14 9

Impacts on forestry 7 1

Small-scale production and use 7 14

International cooperation 5 1

Total 44 46 29

Table 2. The projects of the Wood Energy Programme by subject groups.

• Business and service concepts relating to all tar-get areas. Examples include the creation of heatentrepreneurship and energy service companies,and the development of customer-driven in-ternet sales of wood fuels. The networking ofcompanies is promoted.

As of February 2004, altogether 21 projects hadbeen started. Since most of them will continue tothe end of 2004, this final report of Wood EnergyProgramme does not present any results of thesub-programme concerning small-scale opera-tions.

2.5 The international dimension ofthe programme

Although the primary driving force behind thewood energy boom is the global climate change,the Wood Energy Programme and its targets wereessentially national. However, as wood energy ispromoted for the same reasons all over the world,international cooperation opens up useful channelsfor the exchange of information, transfer of tech-nology, and trade. From the Finnish viewpoint aproblem was that corresponding comprehensiveR&D programmes were not ongoing in other coun-tries at the same time. At the programme level itwas not possible to find a foreign partner that wasprepared to fund and carry out an extensive re-search programme concerning the development offorest chip production technologies.

The traditional cooperation partner has been Swe-den. Similarities between the two countries are ob-vious in climate, forest management, forest tech-nology, energy sector, infrastructure, and socio-economic environment. Conditions for profitablecooperation are favorable, as both Sweden andFinland are forerunners in the field of wood energy(7). However, during the programme period the re-search emphasis in Sweden was on environmentalissues such as the effect of biomass recovery on thebiodiversity of forests, whereas the Finnish pro-gramme was focused on the development of tech-nology. There was, therefore, no programme levelcooperation. The cooperation was limited to pro-

jects with Sveriges Lantbruksuniversitet (SLU),Växjö universitet and Värmeforsk.

Three persons from Finland also worked for a yearin the USA as visiting scientists within the frame-work of the programme. The topics studied werethe co-combustion of solid biofuels and coal, max-imum biomass use and efficiency in large-scaleco-firing, and technology transfer on the produc-tion of biofuels. The programme also participatedin the work of a number of international organiza-tions:• IEA Bioenergy Agreement, especially Task 18

(Conventional forestry systems for bioenergy)in 1998–2000 and subsequent Task 31 (Biomassproduction for energy from sustainable forestry)in 2001–2003.

• ALTENER bioenergy network: AFB-net, andsince 2000 the subsequent EUBIONET (Euro-pean bioenergy networks; http://eubionet.vtt.fi),for the exchange of commercial bioenergy in-formation and to spread knowledge of the Finnishbioenergy sector in participating countries. TheAFB-net and EUBIONET were coordinated byVTT Processes.

• OPET network (Organization for Promoting En-ergy Technology) for the exchange of informa-tion about bioenergy technology at internationallevel in cooperation with industry. The OPETFinland was coordinated by Tekes(www.tekes.fi/opet).

• EU cooperation in certain research and industryprojects. This included the preparation of thebioenergy IP project for the 6th frameworkprogramme of the European Commission.

Results were mainly published in Finnish. In addi-tion, results were made available in Englishthrough following means: the www pages of Tekes(www.tekes.fi/english/programm/woodenergy), aprogramme pamphlet, case cards on results, post-ers and a comprehensive interim report (18). Scien-tific articles were presented in international maga-zines, seminars and conferences such as Bioenergy2003 in Jyväskylä, where the programme organizeda specific session and study tour on the large-scaleproduction of forest chips.

11

3 The operating environment of forest chipproduction

In the interests of the Finnish national economy itis of great importance that timber crops are di-rected at forest industries. Export earnings from acubic meter of unbarked softwood is about 100 € ifthe product is sawn timber or kraft pulp, and muchmore if the product is paper or paper board. Thesurplus value is significantly smaller if the wood isused as fuel. The energy from a cubic meter ofwood corresponds to less than 0.2 tons of oil; a sav-ing in foreign exchange of only 30 €.

Energywood is actually a by-product, a leftoverfrom the more valuable industrial timber crops.Therefore, energywood must be harvested at theterms of industrial timber.

3.1 Management of forests

Private persons own 61 % of productive forestland, and 71 % of the annual increment occurs onprivate lands. There are 242 000 forest holdingslarger than 10 ha, and the average area is c. 40 ha.The majority of the domestic timber is thereforeharvested from private forests. The predominanceof non-industrial family forestry strongly influ-ences the care and intensity with which the forestsare managed and utilized. The fragmented natureof the ownership affects the requirements placedon forest machines with respect to their mobilityfrom site to site and friendliness to the forest envi-ronment. The small size of holdings strains the pro-ductivity of mechanized harvesting, increases thecosts and disturbs the logistics.

Thinnings are a standard silvicultural practice. Insouthern Finland, nearly all stands are thinnedcommercially from below twice or three times, andin northern Finland once or twice, during the rota-tion period. Commercial thinnings are preceded by

a pre-commercial thinning, from which timber isnot harvested because of the small tree size.

The correct timing of silvicultural activities is es-sential for maintaining the vitality of the foreststand, to accelerate the diameter growth of the treesand to improve the physical conditions for futuremechanized cuttings. However, where pulpwoodis in over-supply, the early thinnings are a problem.Compared to the final harvest, the productivity ofwork is low and mechanization more complicated.

Early thinnings are a particular challenge to forestowners, timber procurement organizations andmachine manufacturers alike. Demand for small-sized wood and the presence of a well developedand disciplined wood procurement organizationare preconditions for successful early thinning.

Young thinning stands are a potential source offuel. Currently, the richest fuel yields are found instands were silvicultural activities have been ne-glected. These stands are over-dense, and the treesthat have to be removed are too thin for industrialpurposes. As such they are attractive as a fuel har-vest, but if it is based on poor silviculture the avail-ability of fuel will not be sustainable. The FinnishForest Research Institute is therefore examining anew approach to the management of young forests:rescheduling the early tending operations in orderto gain a better and sustainable yield of fuel fromthe thinning treatment prior to the traditional firstcommercial thinning (83).

It is hoped that the use of low-quality biomass as asource of renewable fuel will promote managementof young forests. In later thinnings and regenera-tion cuttings no serious problems occur regardinglogging, but establishment of a new stand after re-generation cutting is also a cause of concern, sinceplanting is still performed manually and forest la-

13

bor is becoming scarce. The presence of abundantlogging residues is one of the factors constrainingthe mechanization of regeneration. Thus, the re-moval of logging residues and stumps for energyproduction could pave way for good post-harvest-ing management practice.

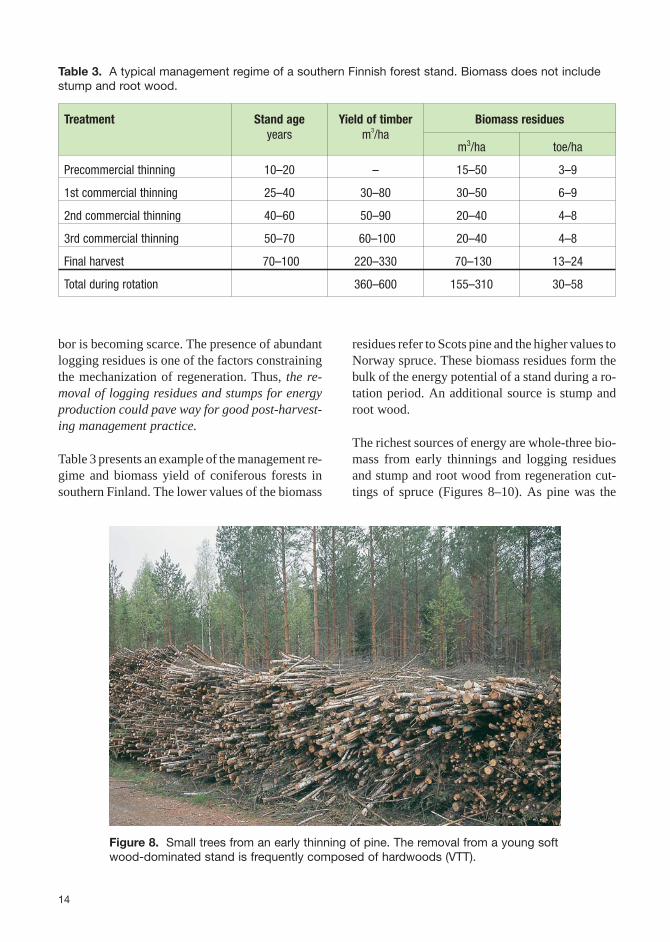

Table 3 presents an example of the management re-gime and biomass yield of coniferous forests insouthern Finland. The lower values of the biomass

residues refer to Scots pine and the higher values toNorway spruce. These biomass residues form thebulk of the energy potential of a stand during a ro-tation period. An additional source is stump androot wood.

The richest sources of energy are whole-three bio-mass from early thinnings and logging residuesand stump and root wood from regeneration cut-tings of spruce (Figures 8–10). As pine was the

14

Treatment Stand ageyears

Yield of timberm3/ha

Biomass residues

m3/ha toe/ha

Precommercial thinning 10–20 – 15–50 3–9

1st commercial thinning 25–40 30–80 30–50 6–9

2nd commercial thinning 40–60 50–90 20–40 4–8

3rd commercial thinning 50–70 60–100 20–40 4–8

Final harvest 70–100 220–330 70–130 13–24

Total during rotation 360–600 155–310 30–58

Table 3. A typical management regime of a southern Finnish forest stand. Biomass does not includestump and root wood.

Figure 8. Small trees from an early thinning of pine. The removal from a young softwood-dominated stand is frequently composed of hardwoods (VTT).

15

Figure 10. Stump and root wood from a final cut of spruce (VTT).

Figure 9. Logging residues from a final cut of spruce (VTT).

preferred species of stand establishment in the1960s and 1970s, a large majority of young standsare dominated by pine (Figure 11).

3.2 Procurement of industrial timber

In 2001, the Finnish forest industries used 54 mill.m3 of indigenous and 13.5 mill. m3 of importedwood. About 83 % of the indigenous wood waspurchased from private forests, mainly on thestump but also delivered to road side by the forestowner.

Three large forest industry companies, Stora Enso,UPM and Metsäliitto-Yhtymä are responsible forthe procurement of more than 80 % of all commer-cial timber. They operate nationwide and performtheir wood procurement through special forestrydepartments that contract the implementation toindependent entrepreneurs. Cutting and off-roadhaulage are included in a single logging contract,whereas secondary transport is subject to a sepa-rate contract. A contractor typically owns 1–4 for-est machines or trucks.

The technology of wood procurement is based ex-clusively on the mechanized cut-to-length system.

Both the delimbing and cross-cutting of stems arecarried out with one-grip harvesters at the stump.An exception is early thinnings where cutting isstill commonly performed with a chainsaw. Tim-ber is transported to the landing with load-carryingforwarders. This Nordic technology differs con-siderably from the North-American technology, anessential feature of which is haulage of wholeundelimbed trees or delimbed stems to the roadside. Conditions for biomass recovery are there-fore very different in the two regions, and this mustbe taken into account when technology is trans-fered.

Figure 12 shows the number of harvesters, for-warders and 60-ton timber trucks employed in2001. The rate of employment varied considerablyover the year. Under-employment in the summertime indicates that machine contractors may haveseasonal capacity for biomass harvesting (23).

The Finnish timber procurement system is effi-cient and cost-competitive, and it is well suited foroperating in small private forests. Due to mechani-zation, sophisticated logistics and motivated ma-chine entrepreneurs, the nominal cost of procure-ment is lower than 15 years ago. The current aver-age is 14 €/m3 from stump to mill.

16

0.5

1

1.5

2

2.5

1.9

2.3

1.71.9

1.7

0.9

0.30.2

1-20 21-40 41-60 61-80 81-100 101-120 121-140 141+

Small trees frompine stands

Logging residues andstump wood from spruce stands

Hardwood-dominatedSpruce-dominatedPine-dominated

Area, mill. ha

Age, years

Figure 11. The age structure and species dominance of the southern Finnishforests according to the 9th National Forest Inventory (Metla).

This is the operating environment of timber pro-curement in Finland. Since forest biomass is to berecovered as a by-product of industrial timber, theintegration of operations is the natural solution. Itfollows that of the utmost importance is the moti-vation of the forest industries to produce and useforest chips. An exception is the early thinningswere fuel is the primary product and pulpwoodonly a side product, if it is recovered at all. In theseyoung stands, machine contractors can operate in-dependently of the forest industry timber procure-ment organizations and form networks for deliver-ing forest chips to local heating and power plants.

3.3 Utilization capacity of forestchips

A precondition for the successful use of forestchips is that the fuel handling and combustion tech-niques of a plant are adapted for the specific prop-erties of the fuel. Two alternative combustion tech-nologies are available for the large-scale conver-sion of forest biomass to heat and electricity.

The traditional grate combustion method is com-petitive when boiler capacity is less than 5–20MW. The Biograte technology of Wärtsilä Bio-power, based on a rotating grate boiler, is also suit-able for wet biomass, such as debarking residuesfrom sawmills.

Larger plants employ the fluidized bed combustion(FBC) technology. In FBC boilers, fuel is fed into afluidized bed of hot sand, which is circulated by astream of high velocity air from below. Combustiontakes place either in a bubbling fluidized bed(BFB) at low air velocity, or in a circulating fluid-ized bed (CFB) at a higher air velocity. As the bedmaterial is massive relative to the amount of fuel,the combustion process is effectively stabilizedand control of burning and pollutants is greatly fa-cilitated.

The majority of the global FBC boiler productionis in the hands of two globally operating Finnishcompanies, Foster Wheeler Energia Oy and Kvaer-ner Power Oy. The technology was originally de-veloped for the combustion of non-homogenous

17

Figure 12. The number of harvesters, forwarders and timber trucks employed incommercial roundwood production in 2001 (56).

biofuels with difficult properties such as unevenparticle size and high moisture content. The FBCprovides the ability to burn low-grade fuels andon-line fuel switching, and reduces the output ofharmful emissions such as NOx and SO2.

A wide range of fuels can be accommodated withhigh efficiency: wood chips, bark, peat, sludge, in-dustrial and municipal waste, coal, oil and naturalgas. The FBC technology is therefore commonlyemployed in new large plants, and a considerablenumber of traditional grate boilers and pulverizedpeat and coal boilers have been converted tofluidized bed technology. In addition, the receiv-ing, handling and feeding techniques have beenadapted for wood fuels. This has significantly in-creased the potential for using biofuels in Finland.

In heating plants where forest fuels are used forheat production only, 85–88 % of the energy con-tent of the fuel is recovered. Typically, heatingplants are smaller than 10 MW. In condensingpower plants designed for electricity generationonly, about 40–45 % of the input energy is recov-ered in the form of electricity, while the remainingheat is lost in cooling water and flue gases. Forestchips are not competitive in these plants because of

their high price and the low overall efficiency of theprocess.

Combined heat and power (CHP) production orco-generation is a single process of a back-pres-sure power plant. Power is generated as in a con-densing plant, but heat is recovered and used in anindustrial process or for the heating of a nearbycommunity. Under conditions of a high all-year de-mand for heat it is often possible to achieve goodfuel efficiency and a high product value by com-bining power and heat production. The annualpeak load time of industrial CHP plants is about6 000 h (full capacity). As the need for space heat-ing is low in the summer time, the peak load time ofdistrict heating CHP plants is only 4 500 h.

CHP plants have an overall efficiency of 85–90 %.About 20–30 % of the energy input is converted toelectric power and 55–70 % to heat. CHP plants areresponsible for 32 % (Figure 13) of the electricitysupply and 75 % of the district heat in Finland. Al-most all large towns use CHP plants for districtheating. These plants are usually large, but theco-generation technology is now being scaleddown for plants with an electricity output of only5–10 MW or less.

18

5

10

15

20

25

30

Nuclearpower

26.9

CO -free production2

Proportion, %

Hydropower

Importedelectricity

Windpower

Districtheating

Industry Condensingpower

16.3

12.3

0.1

17.3

14.313.0

CHP

Use of forestchips possible

Production causingCO emissions2

Figure 13. The sources of electricity in 2001 (43).

Because of its high energy efficiency, CHP tech-nology is a powerful tool for the reduction of CO2

emissions. Therefore, the EU has set a goal to dou-ble the use of CHP during the period 1994 to 2010.However, as CHP technology is already widelyemployed in Finland, the possibilities to expandthe overall capacity are limited. But where an oldplant is being replaced, it may be feasible to shiftfrom fossil fuels to biofuels, even though total ca-pacity is not increased (25).

Pohjolan Voima Oy alone has recently invested620 M€ to biomass CHP plants with a total capac-ity of 559 MWe and 1 038 MWth. These invest-ments made possible the large-scale use of forestfuels. In 2004, the company’s use of forest chipswill exceed 1 TWh (Figure 14).

In the beginning of 2001, the electricity productioncapacity of the Finnish CHP plants was 5 200MWe. The share of district heating CHP was twothirds and industrial CHP one third (43). The totalcapacity of electricity production in Finland was14 990 MWe.

According to VTT, approximately 7 500 MW newelectricity generation capacity has to be installedby 2020 to meet the growth in energy demand or toreplace old plants. Although a 1 600 MW nuclearpower plant will start operating in 2009, a signifi-cant portion of the new capacity will employ CHPtechnology and co-combust peat and wood fuels(Figure 15). The share of forest chips in theseplants will entirely depend on their cost competi-tiveness and availability. It is obvious that the limitof growth will not be determined by the utilizationcapacity but rather the production capacity of for-est chips.

19

Recycled woodand agri-biomassForest chips

1.4

1.2

1.0

0.8

0.6

0.4

0.2

Use of forest chips,TWh / annum

2001 2002 2003 2004 2005

Materialized Prediction

Figure 14. Use of forest chips in the powerplants of Pohjolan Voima (PVO).

0

3 000

6 000

9 000

12 000

15 000

18 000

21 000

2000 2010 2020 2030

Demand of new capacityDemand of new capacityCHP, district heatOther condensingCoal-condensingNuclear powerHydro & wind power

7 500 MW

2040 2050

Nominal power (MW)

Figure 15. Estimated shutdown schedule of the present electricity generatingcapacity and demand for new capacity (99).

3.4 Co-combustion of wood andpeat

Peatlands cover one third of the land surface ofFinland. A half of this peatland area is in its naturalstate, while the other half has been drained for for-estry. About 1.4 % of the area has been designatedfor peat extraction. The area of the extractionworking is currently about 40 000 ha. Nationwide,the growth of peat far exceeds the harvest.

As there are no fossil fuels in Finland, peat playsan important role as an indigenous source of en-ergy. In fact, Finland is the world leader in the tech-nology of peat production and combustion. VapoOy annually produces over 20 mill. m3 and Turve-ruukki Oy about 2 mill. m3 loose peat fuel. In addi-tion, more than 200 small producers operate lo-cally. Some 90 % of the production is milled peatand 10 % sod peat.

Peat was scarcely used prior to the global energycrises in the 1970s. When the Government intensi-fied is support for the technological developmentof peat extraction in the 1980s, an epoch-makingchange took place. By 2001, the consumption offuel peat corresponded to 2.0 Mtoe or 6 % of the to-tal consumption of primary energy. It is usedmainly in back-pressure power plants for com-bined production of heat and power. About 18 % ofdistrict central heating and 5 % of electricity isgenerated from peat.

Large plants burn peat mainly in fluidized bed boil-ers at atmospheric pressure. They are typicallymultifuel boilers that also utilize other solid fuels,such as bark, sawdust, forest chips or coal. It fol-lows that in these plants fuel peat competes withwood fuels. On the other hand, peat and wood fuelsalso complement each other. In large plants, thefollowing benefits may be gained from the co-fir-ing of wood and peat:• The use of more than one type of fuel helps to re-

duce transport distances and costs.

• The inferior storage properties of wood chipsprevent a plant from keeping large inventories.Peat, on the other hand, is easy to store, and itcan be used for securing the fuel supply. In nor-mal conditions nationwide, the inventory of peatis large enough for a year’s consumption.

• The price of fuel peat is stable, and it is not af-fected by the fluctuation of international energymarkets.

• Peat has a rather constant moisture content,40–45 % in the winter time, whereas forest chipstend to be too moist during the winter when thedemand for energy is highest. Blending chipsand peat stabilizes the average moisture contentof the fuel.

• Corrosion problems caused by alkalis and chlo-rine from needle-rich forest chips can be re-duced when the chips are co-fired with peat, andsulphur emissions from peat are reduced inco-combustion due to favourable chemical reac-tions.

In large plants, fuel supply can seldom be based onwood alone. Availability and security are im-proved, and the cost of fuels and harmful environ-mental impacts are reduced, through the co-firingof wood and peat. For example, the world’s largestbiofuelled power plant, Alholmens Kraft in Pietar-saari on the west coast of Finland, uses a 50/50mixture of wood and peat, with 10 % of the totalenergy derived from forest chips. The capacity ofthe plant is 240 MWe power, 100 MWth processsteam for a pulp and paper mill, and 60 MWth dis-trict heat.

The combined use of wood and peat places specialrequirements on the supply logistics, handling andblending the fuels at the plant. Removing the bot-tlenecks from the receiving facilities and schedul-ing the arrival of wood, bark and peat trucks arecrucial issues.

20

4 Raw material base of forest chips

The annual increment of the Finnish forests is 78mill. m3 including bark. The drain, which is com-posed of fellings and natural mortality, is 65 mill.m3 per annum. The balance is positive, but as a partof the forest area is protected and many forest own-ers give priority to recreation and multiple use, thepossibilities for increasing fellings are quite lim-ited. There is potential, however, in young thinningstands where the silvicultural targets are notreached.

The fellings are composed of stemwood removalswhich are recovered, and stemwood losses whichare left in the forest. Removals are divided into in-dustrial wood and fuelwood. The traditional forestinventories are limited to stemwood only. Crownmass and stump and root wood are omitted (Figure16).

4.1 Stemwood loss from loggingoperations

A part of the stemwood drain fails to meet the qual-ity and diameter requirements of industrial wood.Figure 17 shows the proportion of stemwood left atsite as residue in commercial logging operations. Itcan be concluded that:• The proportion of residues is 20–30 % in the first

commercial thinning but only 4–5 % in the finalcutting. The smaller the trees, the greater is theloss.

• The proportion of residues is in spruce standshigher than in pine stands. This is because theminimum diameter requirement of pulpwood isstricter for spruce, and small undergrowth treesare more common in spruce stands.

21

Scots pine Norway spruceProportion, %

Stem 100 69 100 59Crown 23 16 45 27Stump and root 22 15 24 14Complete tree 145 100 169 100

Figure 16. Distribution of biomass between stem, crown and stump-rootsystem in final fellings.

• The primary source of stemwood loss is the un-der-sized tops, especially in the first thinning,where a large number of trees is removed and thestem tapers slowly.

In the integrated harvesting of pulpwood andfuelwood, the quality of both assortments is im-proved if the minimum diameter of pulpwood is in-

creased. The effect is opposite if the minimum di-ameter is decreased. This happened in 2001, as theminimum diameter of pine pulpwood was loweredto 6 cm.

The residual stemwood is potential fuel. The totalamount of stemwood residues from annual loggingoperations in Finland is 4–5 million m3, but as it is

22

0

5

10

15

20

25

30

Defected woodUnder sized topsSmall sized stems

-

-

Firstthinning

Secondthinning

Finalcut

Firstthinning

Secondthinning

Finalcut

Loss of stemwood, %

Pine stands Spruce stands

23

5

16

27

4

13

Figure 17. The relative loss of stemwood in commercial harvesting operations in 1997.

10

20

30

40

50

60

Crown mass / stem mass, %

Dead branchesLive branches

70

59

48

54

34

22 21

Pine stands Spruce stands

Firstthinning

Secondthinning

Finalcut

Firstthinning

Secondthinning

Finalcut

Figure 18. Crown mass in relation to stem mass. Dry weight basis.

scattered over an area of 600 000 ha, the yield persite is too low to make the salvage feasible. Profit-able harvesting for energy requires richer yields.This is achieved with simultaneous recovery of re-sidual stemwood and crown mass.

4.2 Biomass residues from finalfellings

As only stemwood has commercial value, crownmass and stump-root systems are not included inforest inventories. They are difficult to measure,and therefore biomass data on these tree compo-nents tend to be vague.

Crown mass refers to branches with leaves, liveand dead. In conjunction with timber harvesting,the amount of crown mass residues is estimatedusing empirical crown mass/stemwood ratios.When crown mass is used for energy, it is feasible tocompare dry mass rather than volume. Since the ba-sic density of branchwood is higher than that ofstemwood, the ratio is higher on the mass basis. Thecrown mass/stemwood ratio is typically 40–60 %for spruce and 20–30 % for pine (Figure 18).

Although the recovery of stemwood residues is notfeasible as such, it becomes more attractive whenthe recovery of crown mass and stemwood resi-dues are combined. Under Finnish conditions,80–90 % of this mix is crown mass and the remain-ing 10–20 % is stemwood. The presence of stem-wood facilitates the loading, feeding and baling of re-sidual forest biomass. When the mix is comminutedwith a chipper or crusher, the product is called log-ging residue chips.

The availability of logging residue chips is, inpractice, not as plentiful as Figure 18 seems to sug-gest. Some of the logging sites are out of questiondue to small size, long distance, difficult terrain orecological restrictions, and in all cases it is recom-mended that 30 % of logging residues are left atsite. If residues are left to season and shed part ofthe needles before haulage to road side, the yield ofbiomass is further reduced.

According to a common rule of thumb, the recov-ery of logging residue chips from regeneration ar-

eas of spruce is 0.5 MWh per m3 stemwood re-moved, and in pine stands 0.25 MWh correspond-ingly. In typical regeneration cuttings, the averageyield of fuel from logging residues in 100–120MWh/ha for spruce and 50–60 MWh/ha for pine.

Figure 19 shows the logging residue potentialwithin a 100 km radius of plants in different partsof Finland. The national frontiers, coast lines, wa-ter systems, road networks, age structure of forestsand species dominance cause great regional differ-ences in the availability. In the central parts of thecountry, the availability of logging residue chips to agiven location is more than 800 GWh per annum,unless there are competing users. Nationwide, thetechnical availability of logging residues from finalharvests is about 11–12 TWh per annum, of which6–8 TWh is presently economically harvestable.

23

Figure 19. Logging residue potential from finalfellings within a 100 km transport distance, andoptimal location of power plants with an annualconsumption of 300 GWh of forest chips. Small-tree chips and stumpwood chips are not in-cluded (73).

4.3 Small trees from earlythinnings

The production of forest chips for fuel was startedin the mid-1950s. The primary raw material wasthen small trees from young thinning stands. Treeswere carefully delimbed, and the product was ofhigh quality as required by the then existing chipfeeding and combustion techniques.

As the cost of labor increased, the competitivenessof stemwood chips suffered, and the use of chipsstagnated. The introduction of hydraulic crane inthe 1970s made multi-tree handling possible. Onlythen could the production of small-tree chips be ra-tionalized and delimbing was abandoned. The ap-pearance of a new concept, whole-tree chips, re-sulted in many changes:• The yield of chips increased 15–50 %• The productivity of harvesting increased 15–40 %• The cost of procurement was reduced 20–40 %• The loss of nutrients from forest soil reduced

50–150 %• The particle size distribution and other quality

properties of chips suffered• The machines had to be more robust.

The cost of small-tree chips nevertheless remainedhigh. Production was subsidized for silviculturalreasons, but in the 1990s logging residue chips oth-erwise became more competitive. The increase inuse was restricted exclusively to logging residuechips due to their cheaper cost, but a number of rea-sons have gradually appeared for extending theraw material base to young thinning stands:• Tending of young forests needs to be intensified• Broadening the raw material base improves the

availability of forest fuels and shortens transportdistances

• Independence of the timber markets assists theacquisition of fuel during times of depression inthe forest industries when the production ofother wood fuels is reduced

• Independent chip producers who are not in-volved in the harvesting of industrial timberhave an easier access to raw material in youngthinning stands

• Seasonal fluctuation of employment may be lev-elled by performing small-tree harvesting in thesummer time when pulpwood and sawlog oper-ations slow down

• Diameter requirements of pulpwood can bemade more elastic to response the fluctuation ofdemand, if pulpwood and fuelwood are parallelproducts

• Small-tree chips are of better quality comparedto logging residue chips. Small trees are easier tostore and season, and they produce drier chipswith a lower needle content. This is important,especially for small heating plants

• Small-tree operations create more jobs whichare definitely needed in rural areas. However, inthe long term the availability of labor is expectedto decrease, and a higher need for labor may ac-tually become a problem unless the operationsare fully mechanized.

Under-sized small-tree material is available mainlyin young stands where good tending practices havebeen neglected. Two types of fuel harvesting oper-ations occur. If fuel is the primary product, thetreatment is called energywood thinning. If the re-moved trees are thick enough to allow pulpwood tobecome the primary product, with fuelwood as aby-product, the treatment is called first thinning. Inboth cases, technical logging conditions are diffi-cult because of the small size of the trees. Improve-ments in logging conditions by concentrating ofoperations were examined in the programme (82,84).

4.4 Stump and root wood fromfinal fellings

The stump-root system is defined as all wood andbark of a tree below the stump cross-section. Theuse of stump and root wood for fiber and fuel wasstudied actively in Finland and Sweden during the1970s and 1980s, but the cost was found to be ex-cessive. UPM recently started to again develop theproduction of stump wood for fuel, and progresshas been rapid.

24

Stump-root systems can only be salvaged fromclear-cutting areas. Uprooting is carried out withheavy machines and, therefore, only stumps fromsaw timber-sized trees can be accepted. Moreover,thin roots break and stay in the ground. Sand andstones prevent comminution with sharp knives andso crushers are used instead of chippers.

According to the earlier studies by the Finnish For-est Research Institute, the harvestable dry mass ofa stump-root system is 23–25 % of the stem mass,when sideroots thinner than 5 cm are not recov-

ered. In 2003, UPM harvested stump and rootwood from an area of almost 1000 ha. The yield offuel exceeded the FFRI research findings becausestump height has increased following the replace-ment of manual felling by harvesters. A part of theroot section thinner than 5 cm is also recovered.

Figure 20 shows the dry mass and energy contentof a stump-root system as a function of tree size.For example, if the breast height diameter of a treeis 30 cm, the stump-root system corresponds inpine stands to an energy content of 0.35 MWh and

25

40

60

20

80

10 3020 40

kg

Norway spruce

Scots pine

5 cm

5 cm

5 cm

5 cm

0.2

0.3

0.1

0.4

10 200 30

MWh

Stump diameter, cm

Breast height diameter, cm

Figure 20. Dry mass and heating value of a stump-root system as a function ofstump diameter. Stump cross-section at root collar height, under 5 cm root sec-tions excluded (16).

Scots pine Norway spruce

12

StumpSide roots

5 cm 10 cm 20 cm 5 cm 10 cm 20 cm

% %

15 2053

16 27 25

32

Side roots StumpSide roots Side roots

Figure 21. Distribution of dry mass in a stump-root system of sawtimber-sizedtrees. Under 5 cm root sections excluded (16).

in spruce stands 0.40 MWh. If the number of treesis, say, 400 per hectare, the amount of harvestableenergy is 140–160 MWh/ha.

There is an important difference in the structure of astump-root system between pine and spruce (Figure21). Wet peatlands and the northernmost Finlandexcluded, pine typically has a taproot, and only ahalf of the total mass is composed of lateral roots.Spruce, on the other hand, has no taproot at all, butthicker lateral roots. In spruce, therefore, the cen-tral section of the stump-root system covers onlyone third and the lateral roots two thirds of the totalmass. The difference between the species affectsthe techniques of uprooting and splitting. A sprucestump is easier to harvest and causes only a shallowhole in the ground.

The removal of stump-root systems facilitates sitepreparation for regeneration. It also involves an op-portunity to exterminate the root rot fungus fromthe stand, since the fungus survives in a regenera-tion area in the stumps and gradually infects thetrees of the new generation. Removal of stumpsprevents the root-rot fungus from spreading andheals the infected site.

4.5 Forest chip potential of theFinnish forests

Inventory data on forest resources are importantfor the planning of capacity, product lines and loca-tion of new forest industries. A national forest in-ventory has been carried out nine times since theearly 1920s, and precise knowledge is available ofstemwood resources.

The need for basic forest data now includes notonly stemwood but all forest biomass because en-ergy producers are prepared to invest in wood-firedheating and CHP plants, fuel producers are com-peting for market shares of raw material, and pol-icy-makers are setting new targets for renewableenergy. Forest biomass, although it is renewable, isnevertheless a limited resource, and its use must bebuilt on a sustainable basis.

Estimations of availability begin from the theoreti-cal maximum potential. This is composed of twomajor sources. First, it includes all residual bio-mass left in the forest in conjunction with timberharvesting. Secondly, it includes the small-tree bio-mass which is removed, or should be removed, forsilvicultural reasons in precommercial thinnings ofyoung stands. The former is dependent on the mar-kets of forest products, whereas the latter is free ofmarket fluctuations.

Only a part of the maximum biomass potential isrecoverable. Many technological, socio-economicand environmental factors affect the availability:• Price development of alternative fuels, taxes and

subsidies• Development of procurement technology and

logistics• Motivation of forest machine and truck contrac-

tors to participate• Development of the quality requirements of for-

est chips. For example, will the foliage be takenor left?

• The acceptance of private forest owners, whichis affected by the price paid for biomass

• The energy and climate policies at the nationaland EU levels. The trade of CO2 emissions willbe of utmost importance.

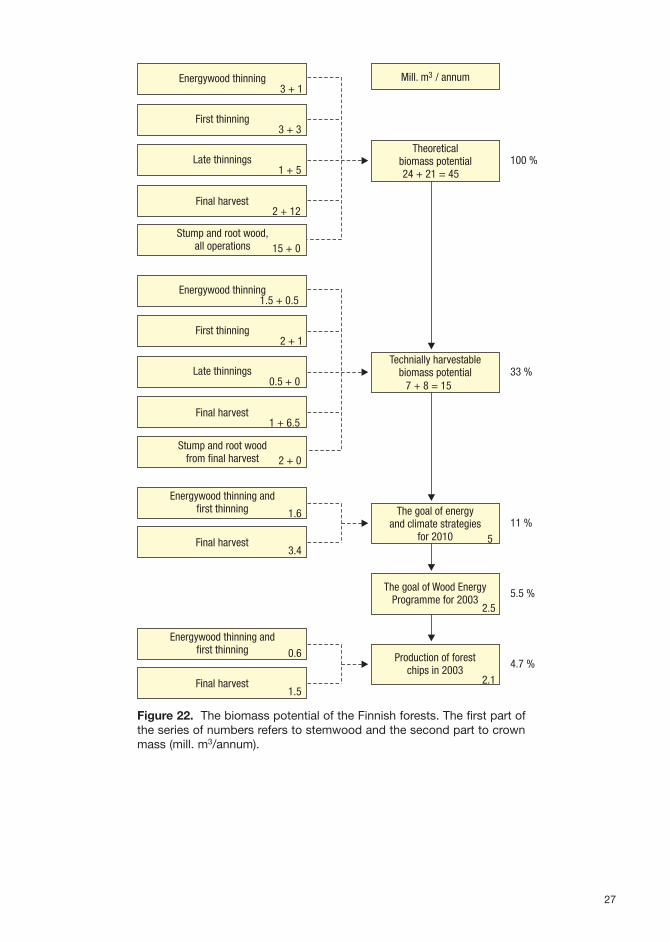

In Figure 22, the technological and environmentalfactors have been taken into account, but no priceassumptions have been applied. The technicallyharvestable potential is estimated separately forfive different types of logging operations:• Energywood thinnings are tending operations in

young stands in which the owner has earlier ne-glected good forest management. Because of thesmall size of the trees, the primary product isfuel. The age of the stands is typically 15–25years and a majority are dominated by pine, butthe removals may be composed of hardwoods.The cost of harvest is high, and subsidies arenecessary to make the recovery possible.

• First thinnings refer traditionally to the firstcommercial logging operation of a stand, nor-mally at the age of 25–40 years. Pulpwood is theprimary product, but as 20–30 % of the stem-wood drain does not meet the minimum dimen-sions of pulpwood, first thinnings may also yieldsubstantial quantities of fuelwood.

26

27

Energywood thinning

First thinning

Late thinnings

Final harvest

Stump and root wood,all operations

3 + 1

3 + 3

1 + 5

2 + 12

15 + 0

100 %

Stump and root woodfrom final harvest

1.5 + 0.5

2 + 1

0.5 + 0

1 + 6.5

2 + 0

33 %

Energywood thinning andfirst thinning

Final harvest

1.6

3.4

The goal of energyand climate strategies

for 2010 5

11 %

The goal of Wood EnergyProgramme for 2003

2.55.5 %

Production of forestchips in 2003

2.1

4.7 %