working capital management - jaipur national universityjnujprdistance.com/assets/lms/lms jnu/dual...

TRANSCRIPT

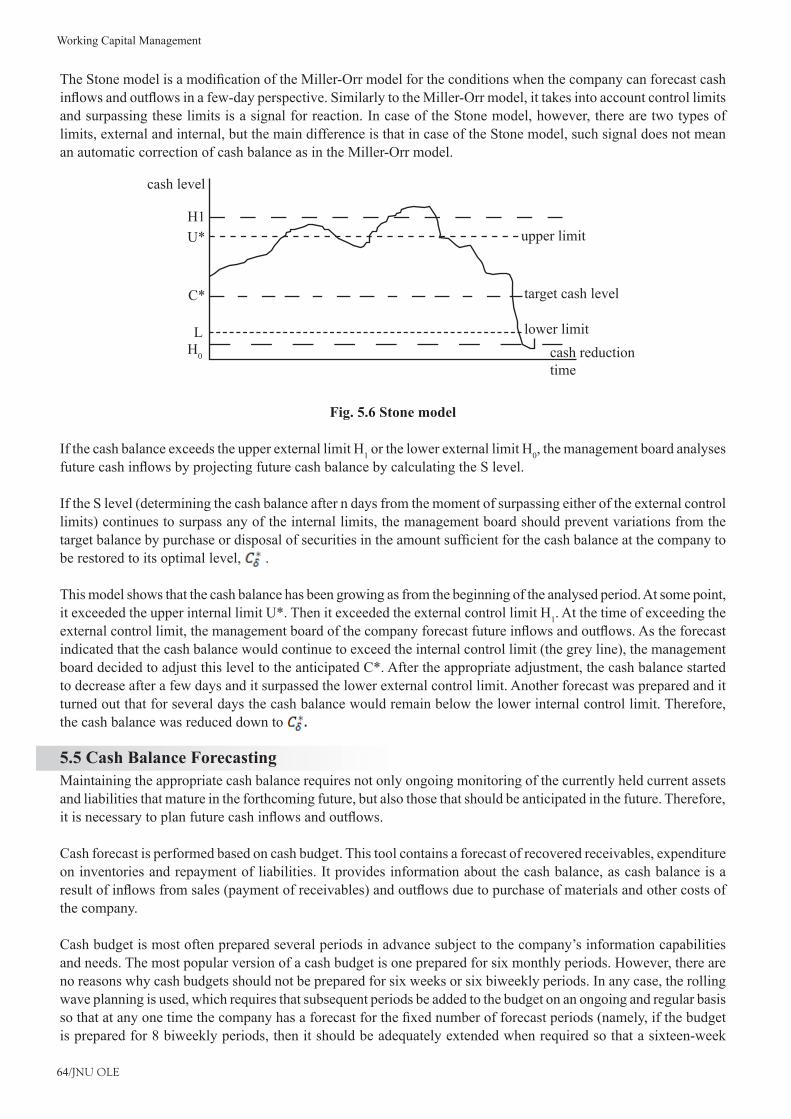

Working Capital Management

This book is a part of the course by Jaipur National University, Jaipur.This book contains the course content for Working Capital Management.

JNU, JaipurFirst Edition 2013

The content in the book is copyright of JNU. All rights reserved.No part of the content may in any form or by any electronic, mechanical, photocopying, recording, or any other means be reproduced, stored in a retrieval system or be broadcast or transmitted without the prior permission of the publisher.

JNU makes reasonable endeavours to ensure content is current and accurate. JNU reserves the right to alter the content whenever the need arises, and to vary it at any time without prior notice.

I/JNU OLE

Index

ContentI. ...................................................................... II

List of FiguresII. .........................................................VI

List of TablesIII. ........................................................ VII

AbbreviationsIV. .....................................................VIII

Case StudyV. .............................................................. 117

BibliographyVI. ........................................................ 122

Self Assessment AnswersVII. ................................... 125

Book at a Glance

II/JNU OLE

Contents

Chapter I ....................................................................................................................................................... 1Working Capital Analysis............................................................................................................................ 1Aim ................................................................................................................................................................ 1Objectives ...................................................................................................................................................... 1Learning outcome .......................................................................................................................................... 11.1 Introduction ............................................................................................................................................. 21.2 Meaning of Working Capital .................................................................................................................... 2 1.2.1 Importance of Adequate Working Capital ............................................................................... 3 1.2.2 Optimum Working Capital ....................................................................................................... 41.3 Determinants of Working Capital ............................................................................................................ 41.4 Issues in the Working Capital Management............................................................................................. 5 1.4.1 Current Assets to Fixed Assets Ratio ....................................................................................... 5 1.4.2 Liquidity versus Profitability ................................................................................................... 61.5 Estimating Working Capital Needs .......................................................................................................... 61.6 Operating or Working Capital Cycle........................................................................................................ 61.7 Concept of Working Capital ................................................................................................................... 71.8 Requirements of Working Capital ........................................................................................................... 71.9 Classification of Working Capital ........................................................................................................... 81.10 Significance of Working Capital Management ..................................................................................... 91.11 Factors Influencing Working Capital Requirements ............................................................................. 91.12 Principles of Working Capital Management ....................................................................................... 101.13 Structure of Working Capital ................................................................................................................11Summary ..................................................................................................................................................... 13References ................................................................................................................................................... 13Recommended Reading ............................................................................................................................. 14Self Assessment ........................................................................................................................................... 15

Chapter II ................................................................................................................................................... 17Cash Management ..................................................................................................................................... 17Aim .............................................................................................................................................................. 17Objectives .................................................................................................................................................... 17Learning outcome ........................................................................................................................................ 172.1 Introduction ............................................................................................................................................ 182.2 General Principles of Cash Management: .............................................................................................. 192.3 Functions of Cash Management ............................................................................................................. 202.4 Motives of Holding Cash ....................................................................................................................... 212.5 Financing of Cash Shortage and Cost of Running Out of Cash ............................................................ 222.6 Financing Current Assets ....................................................................................................................... 23Summary ..................................................................................................................................................... 25References ................................................................................................................................................... 25Recommended Reading ............................................................................................................................. 25Self Assessment ........................................................................................................................................... 26

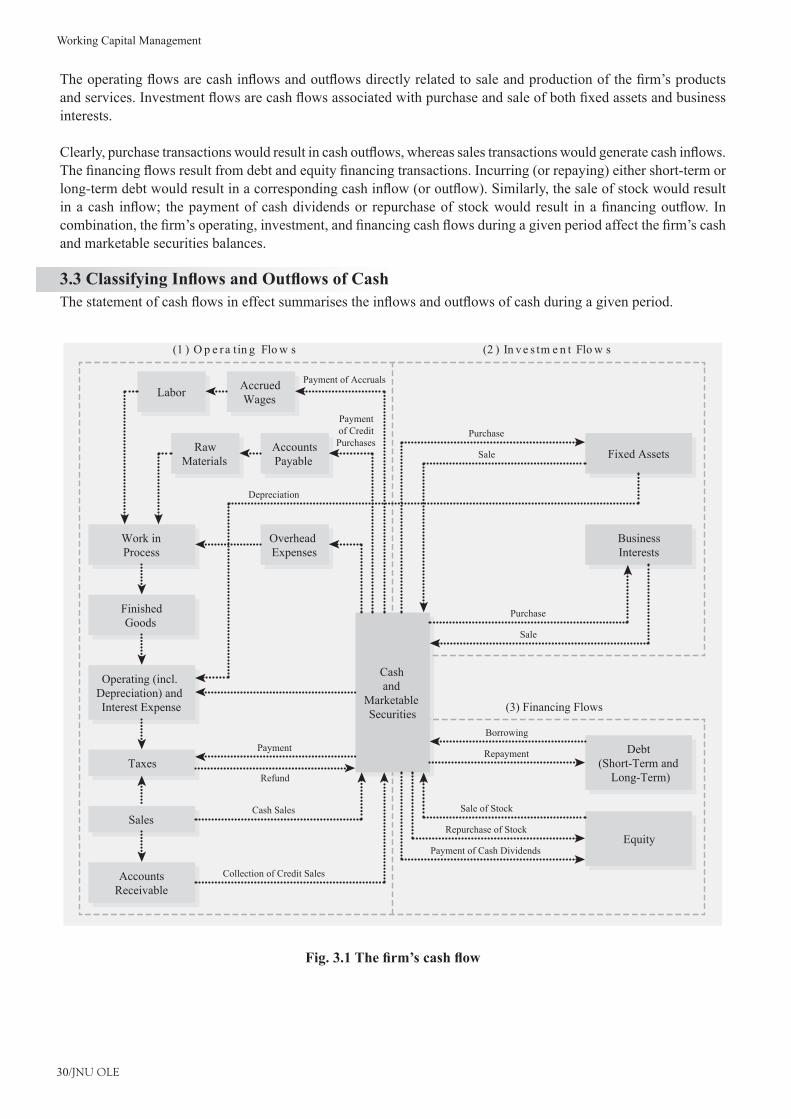

Chapter III .................................................................................................................................................. 28Cash Flow and Financial Planning ........................................................................................................... 28Aim .............................................................................................................................................................. 28Objectives .................................................................................................................................................... 28Learning outcome ........................................................................................................................................ 283.1 Introduction ............................................................................................................................................ 293.2 Depreciation ........................................................................................................................................... 293.3 Classifying Inflows and Outflows of Cash ............................................................................................ 303.4 Preparing the Statement of Cash Flows ................................................................................................. 313.5 Cash Planning: Cash Budgets ................................................................................................................ 32

III/JNU OLE

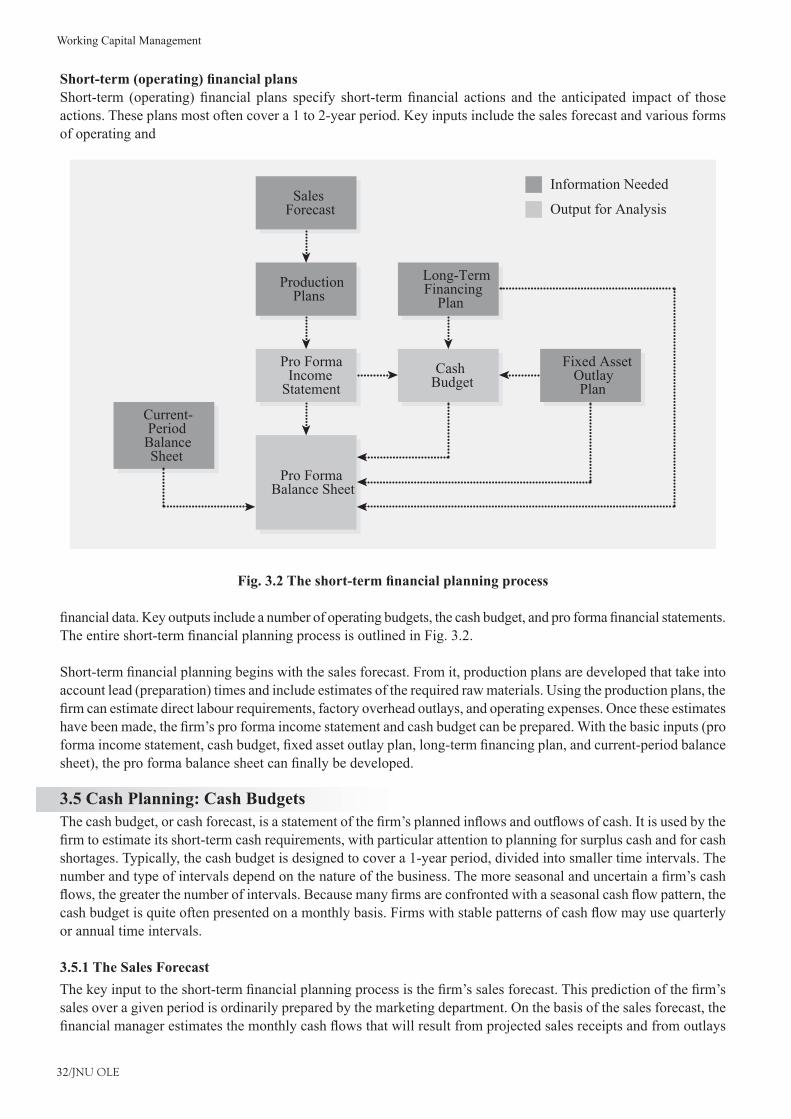

3.5.1 The Sales Forecast ................................................................................................................. 32 3.5.2 Preparing the Cash Budget .................................................................................................... 333.6 Net Cash Flow, Ending Cash, Financing, and Excess Cash .................................................................. 353.7 Cash Forecasting .................................................................................................................................... 36Summary ..................................................................................................................................................... 38References ................................................................................................................................................... 38RecommendedReading .............................................................................................................................. 39Self Assessment ........................................................................................................................................... 40

Chapter IV .................................................................................................................................................. 42Liquidity and Working Capital Financing .............................................................................................. 42Aim .............................................................................................................................................................. 42Objectives .................................................................................................................................................... 42Learning outcome ........................................................................................................................................ 424.1 Introduction ............................................................................................................................................ 434.2 Traditional Measures .............................................................................................................................. 43 4.2.1 An Alternative Method ........................................................................................................... 434.3 Liquidity Ratios ..................................................................................................................................... 44 4.3.1 Types of Liquidity Ratio ........................................................................................................ 444.4 Net Working Capital .............................................................................................................................. 45 4.4.1 Business Uses of Working Capital ......................................................................................... 454.5 Permanent and Cyclical Working Capital .............................................................................................. 464.6 Forms of Working Capital Financing ..................................................................................................... 47 4.6.1 Line of Credit ......................................................................................................................... 47 4.6.2 Accounts Receivable Financing ............................................................................................. 47 4.6.3 Factoring ................................................................................................................................ 484.7 Inventory Financing ............................................................................................................................... 484.8 Term Loan .............................................................................................................................................. 494.9 Sources of Working Capital for Small Businesses ................................................................................. 504.10 Underwriting Issues in Working Capital Financing ............................................................................. 51Summary ..................................................................................................................................................... 52References ................................................................................................................................................... 52Recommended reading .............................................................................................................................. 53Self Assessment ........................................................................................................................................... 54

Chapter V .................................................................................................................................................... 56Cash Management and Financial Flexibility ........................................................................................... 56Aim .............................................................................................................................................................. 56Objectives .................................................................................................................................................... 56Learning outcome ........................................................................................................................................ 565.1 Introduction ............................................................................................................................................ 575.2 Corporate Cash Management ................................................................................................................. 575.3 Value-Based Strategy in Working Capital Management ........................................................................ 605.4 Value-Based Strategy in Cash Management .......................................................................................... 615.5 Cash Balance Forecasting ...................................................................................................................... 645.6 Precautionary Cash Management - Safety Stock Approach .................................................................. 65Summary ..................................................................................................................................................... 66References ................................................................................................................................................... 66Recommended Reading ............................................................................................................................. 67Self Assessment ........................................................................................................................................... 68

IV/JNU OLE

Chapter VI .................................................................................................................................................. 70Inventory Management ............................................................................................................................. 70Aim .............................................................................................................................................................. 70Objectives .................................................................................................................................................... 70Learning outcome ........................................................................................................................................ 706.1 Introduction ............................................................................................................................................ 716.2 Functions of Inventory ........................................................................................................................... 726.3 Classification of Inventory Systems ...................................................................................................... 72 6.3.1 Lot Size Reorder Point Policy ............................................................................................... 72 6.3.2 Fixed Order Interval Scheduling Policy ................................................................................ 73 6.3.3 Optional Replenishment Policy ............................................................................................. 746.4 Other Types of Inventory Systems ......................................................................................................... 746.5 Selective Inventory Management .......................................................................................................... 74 6.5.1 ABC Analysis ......................................................................................................................... 75 6.5.2 VED Analysis......................................................................................................................... 76 6.5.3 FSN Analysis ......................................................................................................................... 766.6 Exchange Curve and Aggregate Inventory Planning ............................................................................. 766.7 Deterministic Inventory Models ............................................................................................................ 77Summary ..................................................................................................................................................... 78References ................................................................................................................................................... 78Recommended Reading ............................................................................................................................. 79Self Assessment ........................................................................................................................................... 80

Chapter VII ................................................................................................................................................ 82Capital and Money Market ....................................................................................................................... 82Aim .............................................................................................................................................................. 82Objectives .................................................................................................................................................... 82Learning outcome ........................................................................................................................................ 827.1 Introduction ............................................................................................................................................ 837.2 Financial Market .................................................................................................................................... 837.3 Capital Market Efficiency ...................................................................................................................... 84 7.3.1 Forms of Capital Market Efficiency ...................................................................................... 857.4 Capital Market Operations ..................................................................................................................... 867.5 Money Market ........................................................................................................................................ 86 7.5.1 Characteristics of Money Market .......................................................................................... 87 7.5.2 Functions of Money Market .................................................................................................. 87 7.5.3 Importance of Money Market ................................................................................................ 887.6 Indian Money Market Instruments ......................................................................................................... 897.7 Drawbacks of Indian Money Market ..................................................................................................... 917.8 Reforms in Indian Money Market .......................................................................................................... 92Summary ..................................................................................................................................................... 93References ................................................................................................................................................... 93Recommended Reading ............................................................................................................................. 94Self Assessment ........................................................................................................................................... 95

Chapter VIII ............................................................................................................................................... 97Receivable Management ............................................................................................................................ 97Aim .............................................................................................................................................................. 97Objectives .................................................................................................................................................... 97Learning outcome ........................................................................................................................................ 978.1 Introduction ........................................................................................................................................... 988.2 Receivable Management ........................................................................................................................ 988.3 Cost of Maintaining Receivables ......................................................................................................... 1018.4 Factors Affecting the Size of Receivables ........................................................................................... 1028.5 Principles of Credit Management ........................................................................................................ 103

V/JNU OLE

8.6 Objectives of Receivable Management ............................................................................................... 1048.7 Aspects of Credit Policy ....................................................................................................................... 1058.8 Determination of Credit Policy ............................................................................................................ 106 8.8.1 Credit Terms ......................................................................................................................... 106 8.8.2 Credit Standards ................................................................................................................... 108 8.8.3 Collection Policy .................................................................................................................. 1088.9 Collection of Accounts Receivables .................................................................................................... 109 8.9.1 Types of Collection Efforts .................................................................................................. 109 8.9.2 Degree of Collection Efforts ................................................................................................ 109 8.9.3 Collection Follow-Up System ..............................................................................................1108.10 Credit Control .....................................................................................................................................1108.11 Control of Receivables ........................................................................................................................111 8.11.1 Payment Pattern Approach ..................................................................................................111Summary ....................................................................................................................................................113References ..................................................................................................................................................114Recommended Reading ............................................................................................................................114Self Assessment ..........................................................................................................................................115

VI/JNU OLE

List of Figures

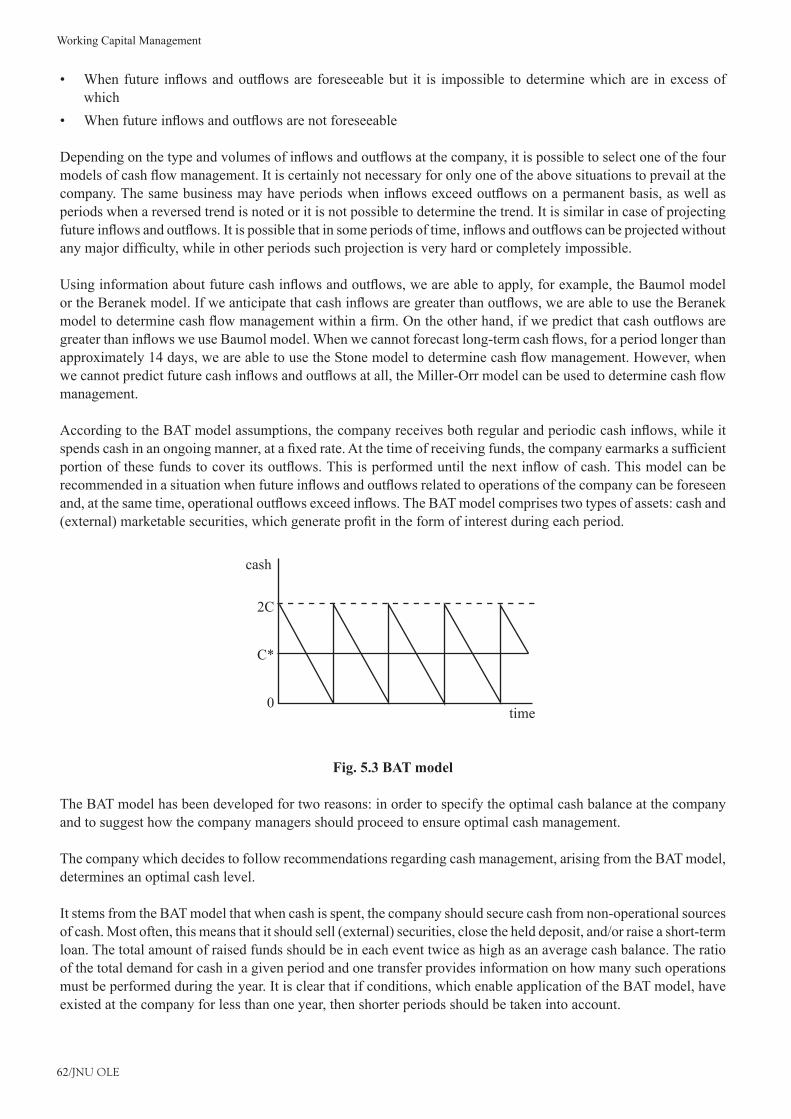

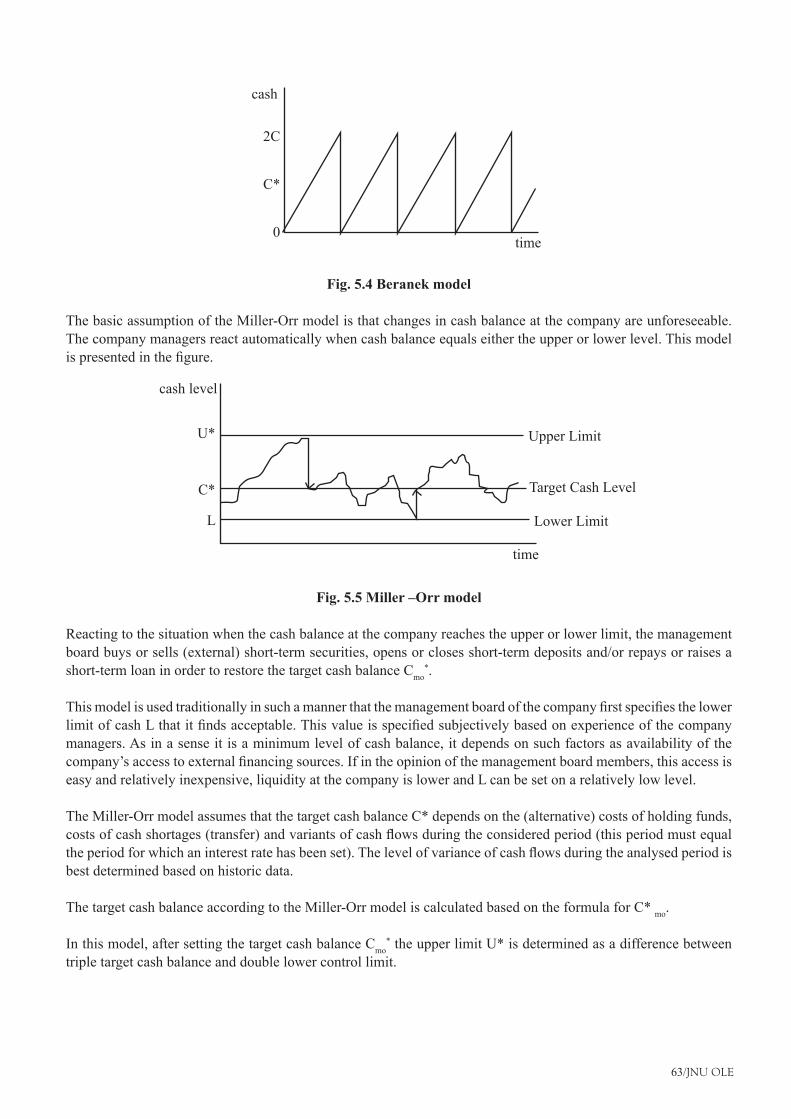

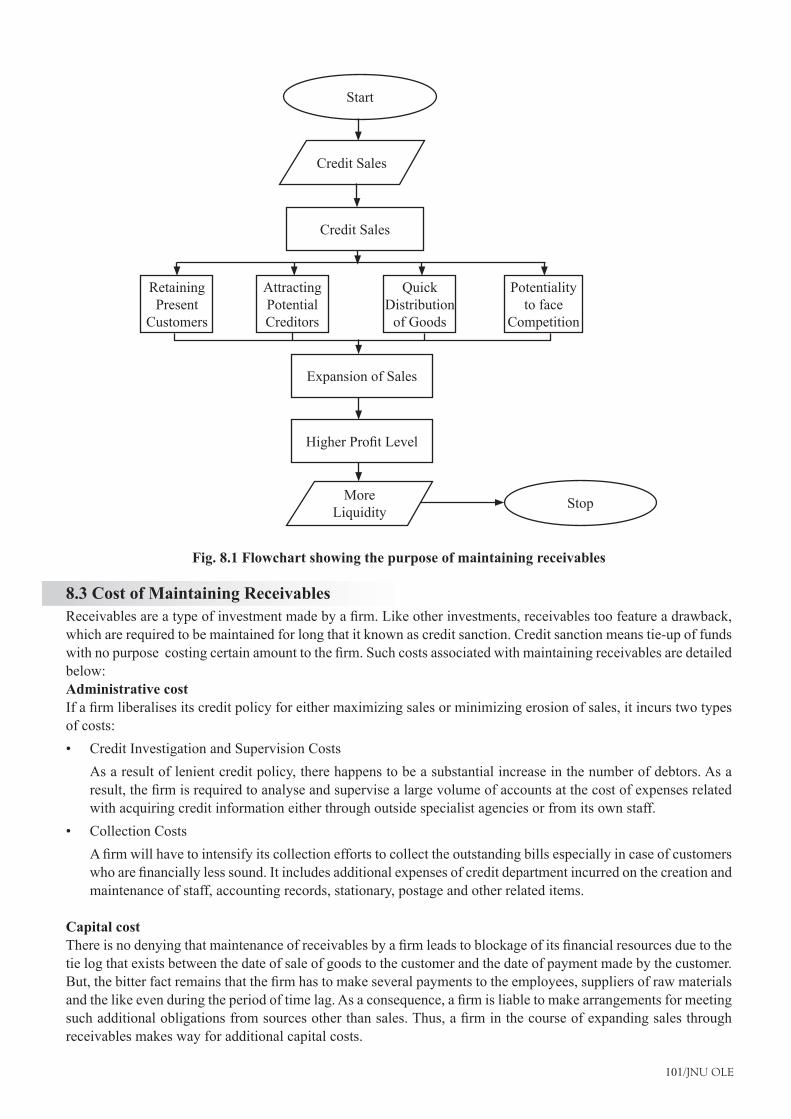

Fig. 1.1 The angles of working capital management ..................................................................................... 2Fig. 1.2 Permanent and temporary working capital ....................................................................................... 3Fig. 1.3 Alternative current assets policies .................................................................................................... 5Fig. 3.1 The firm’s cash flow ....................................................................................................................... 30Fig. 3.2 The short-term financial planning process ..................................................................................... 32Fig. 4.1 Cash flow and the working capital cycle ........................................................................................ 46Fig. 5.1 Liquid assets influence on value of the corporation ....................................................................... 58Fig. 5.2 Reasons for holding cash by companies and their relation to the risk ........................................... 60Fig. 5.3 BAT model ...................................................................................................................................... 62Fig. 5.4 Beranek model ................................................................................................................................ 63Fig. 5.5 Miller –Orr model ........................................................................................................................... 63Fig. 5.6 Stone model .................................................................................................................................... 64Fig. 6.1 Typical inventory balances for EOQ- reorder point policy............................................................. 73Fig. 6.2 Fixed reorder cycle policy. ............................................................................................................. 73Fig. 6.3 Typical inventory balances in policy. ............................................................................................. 74Fig. 6.4 ABC analysis .................................................................................................................................. 75Fig. 7.1 The financial system ....................................................................................................................... 84Fig. 8.1 Flowchart showing the purpose of maintaining receivables ........................................................ 101

VII/JNU OLE

List of Tables

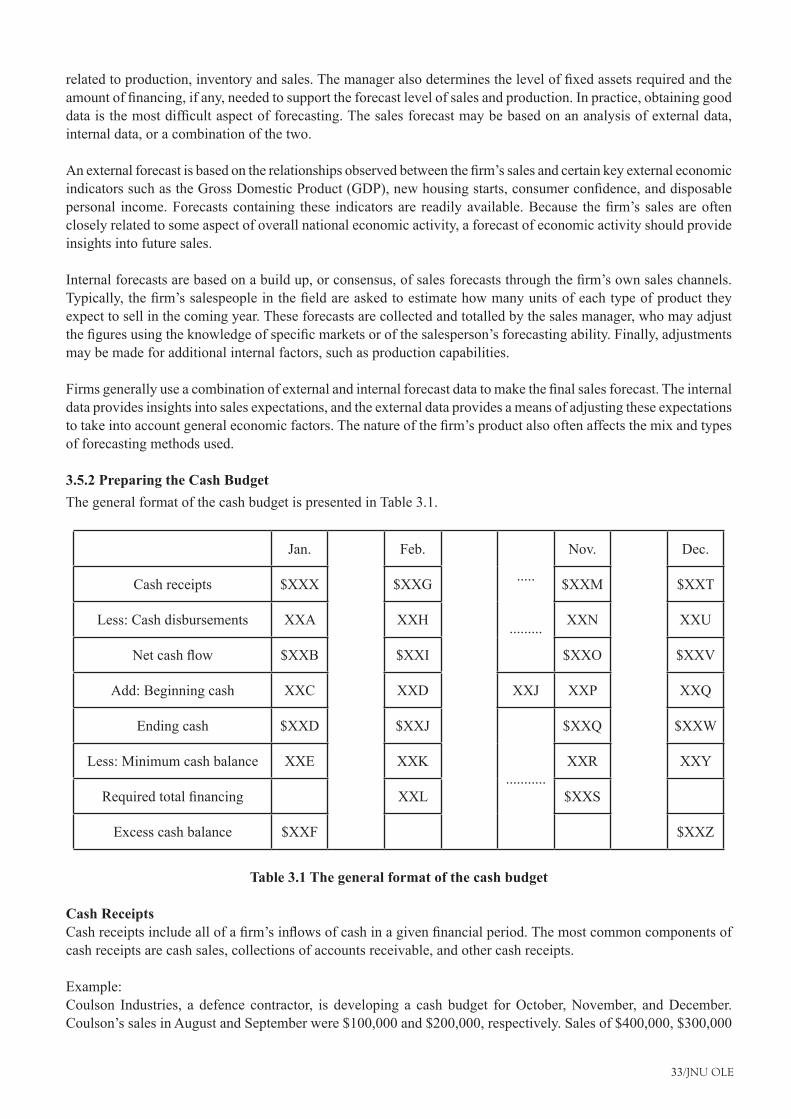

Table 3.1 The general format of the cash budget ......................................................................................... 33Table 3.2 A schedule of projected cash receipts for Coulson Industries ($000) .......................................... 34Table 3.3 A sensitivity analysis of Coulson industries cash budget ............................................................. 35

VIII/JNU OLE

Abbreviations

JIT - Just In TimeEOQ - Economic order quantityMACRS - ModifiedacceleratedcostrecoverysystemOCF - operatingcashflowFCF - freecashflowNFAI - NetfixedassetinvestmentNCAI - Net current asset investmentA/R - accounts receivableR&D - receipts and disbursementsANI - adjusted net incomeEBIT - Earnings Before Interest, TaxesPBS - Pro forma balance sheetARM - Accrual reversal methodFCFF - freecashflowstofirmNWC - net working capital growthCA - Current AssetsCL - Current LiabilitiesCCI - Controller of Capital IssuesCP - Commercial paperAPY - Annual Percentage YieldAPR - Annual Percentage RateMMMFs - Money Market Mutual FundDFHI - Discount and Finance House of IndiaLAF - Liquidity Adjustment Facility

1/JNU OLE

Chapter I

Working Capital Analysis

Aim

The aim of this chapter is to:

definethegoalofworkingcapitalmanagement•

elucidate the concept of work capital•

explain the importance of working capital•

Objectives

The objectives of this chapter are to:

explain the types of working capital•

explicate the issues in the working capital management•

elucidate the determinants of working capital•

Learning outcome

At the end of this chapter, you will be able to:

understandthecurrentassetstofixedassetsratio•

identify the working capital cycle•

recognisethesignificanceofworkingcapitalmanagement•

Working Capital Management

2/JNU OLE

1.1 Introduction WorkingCapitalManagementinvolvesmanagingthebalancebetweenfirm’sshort-termassetsanditsshort-termliabilities.Thegoalofworkingcapitalmanagementistoensurethatthefirmisabletocontinueitsoperationsandthatithassufficientcashflowtosatisfybothmaturingshort-termdebtsandupcomingoperationalexpenses.Theinteraction between current assets and current liabilities is, therefore, the main theme of the theory of working capital management.

There aremany aspects ofworking capitalmanagementwhichmakes it an important function of financialmanagement.

Time:Workingcapitalmanagementrequiresmuchofthefinancemanager’stime.•Investment: Working capital represents a large portion of the total investment in assets.•Credibility:Workingcapitalmanagementhasgreatsignificanceforallfirms,butitisverycriticalforsmall•firms.Growth:Theneedforworkingcapitalisdirectlyrelatedtothefirm’sgrowth.•

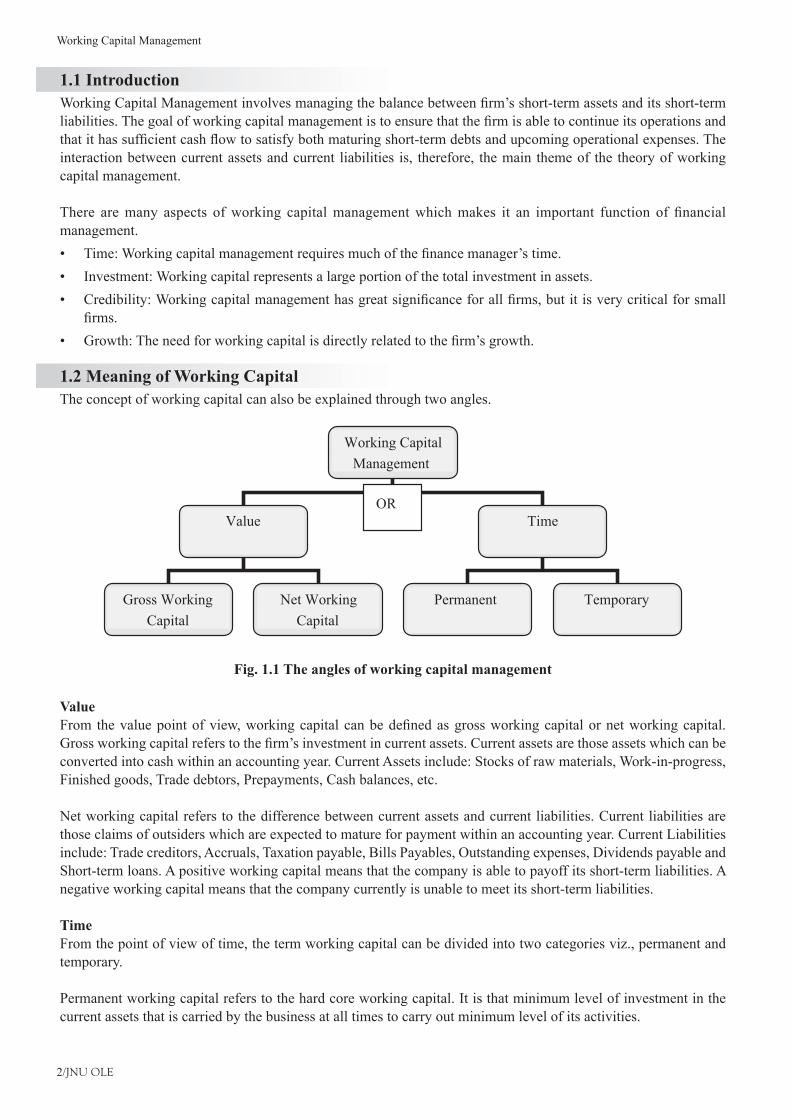

1.2 Meaning of Working CapitalThe concept of working capital can also be explained through two angles.

Working Capital Management

Value Time

Gross Working Capital

Net Working Capital

Permanent Temporary

OR

Fig. 1.1 The angles of working capital management

ValueFromthevaluepointofview,workingcapitalcanbedefinedasgrossworkingcapitalornetworkingcapital.Grossworkingcapitalreferstothefirm’sinvestmentincurrentassets.Currentassetsarethoseassetswhichcanbeconverted into cash within an accounting year. Current Assets include: Stocks of raw materials, Work-in-progress, Finished goods, Trade debtors, Prepayments, Cash balances, etc.

Net working capital refers to the difference between current assets and current liabilities. Current liabilities are those claims of outsiders which are expected to mature for payment within an accounting year. Current Liabilities include: Trade creditors, Accruals, Taxation payable, Bills Payables, Outstanding expenses, Dividends payable and Short-term loans. A positive working capital means that the company is able to payoff its short-term liabilities. A negative working capital means that the company currently is unable to meet its short-term liabilities.

TimeFrom the point of view of time, the term working capital can be divided into two categories viz., permanent and temporary.

Permanent working capital refers to the hard core working capital. It is that minimum level of investment in the current assets that is carried by the business at all times to carry out minimum level of its activities.

3/JNU OLE

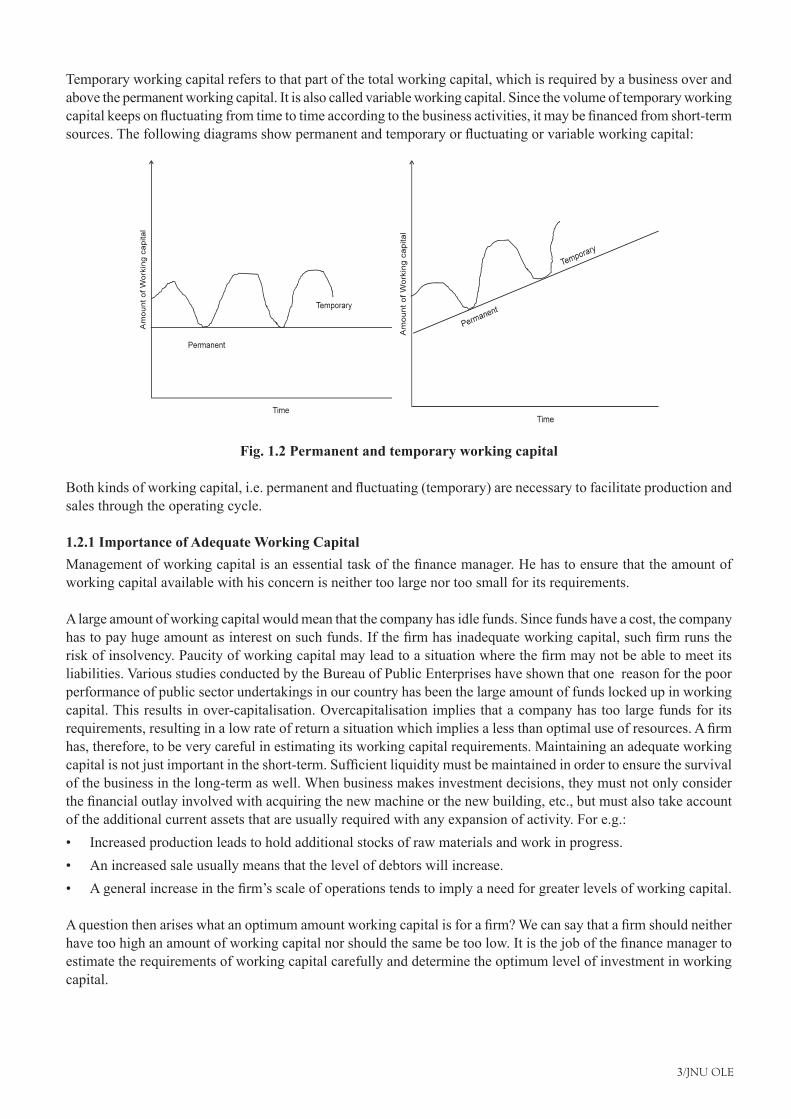

Temporary working capital refers to that part of the total working capital, which is required by a business over and above the permanent working capital. It is also called variable working capital. Since the volume of temporary working capitalkeepsonfluctuatingfromtimetotimeaccordingtothebusinessactivities,itmaybefinancedfromshort-termsources.Thefollowingdiagramsshowpermanentandtemporaryorfluctuatingorvariableworkingcapital:

Fig. 1.2 Permanent and temporary working capital

Bothkindsofworkingcapital,i.e.permanentandfluctuating(temporary)arenecessarytofacilitateproductionandsales through the operating cycle.

1.2.1 Importance of Adequate Working CapitalManagementofworkingcapitalisanessentialtaskofthefinancemanager.Hehastoensurethattheamountofworking capital available with his concern is neither too large nor too small for its requirements.

A large amount of working capital would mean that the company has idle funds. Since funds have a cost, the company hastopayhugeamountasinterestonsuchfunds.Ifthefirmhasinadequateworkingcapital,suchfirmrunstheriskofinsolvency.Paucityofworkingcapitalmayleadtoasituationwherethefirmmaynotbeabletomeetitsliabilities. Various studies conducted by the Bureau of Public Enterprises have shown that one reason for the poor performance of public sector undertakings in our country has been the large amount of funds locked up in working capital. This results in over-capitalisation. Overcapitalisation implies that a company has too large funds for its requirements,resultinginalowrateofreturnasituationwhichimpliesalessthanoptimaluseofresources.Afirmhas, therefore, to be very careful in estimating its working capital requirements. Maintaining an adequate working capitalisnotjustimportantintheshort-term.Sufficientliquiditymustbemaintainedinordertoensurethesurvivalof the business in the long-term as well. When business makes investment decisions, they must not only consider thefinancialoutlayinvolvedwithacquiringthenewmachineorthenewbuilding,etc.,butmustalsotakeaccountof the additional current assets that are usually required with any expansion of activity. For e.g.:

Increased production leads to hold additional stocks of raw materials and work in progress.•An increased sale usually means that the level of debtors will increase.•Ageneralincreaseinthefirm’sscaleofoperationstendstoimplyaneedforgreaterlevelsofworkingcapital.•

Aquestionthenariseswhatanoptimumamountworkingcapitalisforafirm?Wecansaythatafirmshouldneitherhavetoohighanamountofworkingcapitalnorshouldthesamebetoolow.Itisthejobofthefinancemanagertoestimate the requirements of working capital carefully and determine the optimum level of investment in working capital.

Working Capital Management

4/JNU OLE

1.2.2 Optimum Working CapitalIf a company’s current assets do not exceed its current liabilities, then it may run into trouble with creditors that want their money quickly. Current ratio (current assets/current liabilities) (along with acid test ratio to supplement it) has traditionally been considered the best indicator of the working capital situation. It is understood that a currentratioof2(two)foramanufacturingfirmimpliesthatthefirmhasanoptimumamountofworkingcapital.This is supplemented by Acid Test Ratio (Quick assets/Current liabilities) which should be at least 1 (one). Thus it is considered that there is a comfortable liquidity position, if liquid current assets are equal to current liabilities. Bankers,financialinstitutions,financialanalysts,investorsandotherpeopleinterestedinfinancialstatementshave,for years, considered the current ratio at, ‘two’ and the acid test ratio at, ‘one’ as indicators of a good working capital situation. As a thumb rule, this may be quite adequate.

However, it should be remembered that optimum working capital can be determined only with reference to the particularcircumstancesofaspecificsituation.Thus,inacompanywheretheinventoriesareeasilysaleableandthesundrydebtorsareasgoodasliquidcash,thecurrentratiomaybelowerthan2andyetthefirmmaybesound.

Innutshell,afirmshouldhaveadequateworkingcapitaltorunitsbusinessoperations.Bothexcessiveaswellasinadequate working capital positions are dangerous.

1.3 Determinants of Working CapitalWorking capital management is concerned with:-

Maintaining adequate working capital (management of the level of individual current assets and the current •liabilities)Financing of the working capital•

Forthepointa)above,afinancemanagerneedstoplanandcomputetheworkingcapitalrequirementsforitsbusiness.Oncetherequirementhasbeencomputed,heneedstoensurethatitisfinancedproperly.Thiswholeexerciseisnothing but Working Capital Management.

Soundfinancialandstatisticaltechniques,supportedbyjudgementshouldbeusedtopredictthequantumofworkingcapital required at different times. Some of the items/factors which need to be considered while planning for working capital requirement are:

Cash: Identify the cash balance which allows for the business to meet day-to-day expenses, but reduces cash •holding costs.Inventory: Identify the level of inventory which allows for uninterrupted production but reduces the investment •inrawmaterialsandhenceincreasescashflow.ThetechniqueslikeJustInTime(JIT)andEconomicOrderQuantity (EOQ) are used for this.Debtors: Identify the appropriate credit policy, i.e., credit terms which will attract customers, such that any •impactoncashflowsandthecashconversioncyclewillbeoffsetbyincreasedrevenueandhenceReturnonCapital (or vice versa). The tools like discounts and allowances are used for this.Short-termfinancingoptions:Inventoryisideallyfinancedbycreditgrantedbythesupplier;dependentonthe•cash conversion cycle, it may however, be necessary to utilise a bank loan (or overdraft), or to “convert debtors tocash”through“factoring”inordertofinanceworkingcapitalrequirements.Nature of business: For e.g., in a business of restaurant, most of the sales are in cash. Therefore, the need for •working capital is very less.Market and demand conditions: For e.g., if an item demand far exceeds its production, the working capital •requirementwouldbelessasinvestmentinfinishedgoodinventorywouldbeveryless.Technology and manufacturing policies: For e.g., in some businesses, the demand for goods is seasonal. In •that case, a business may follow a policy for steady production through out over the whole year or instead may choose policy of production only during the demand season.

5/JNU OLE

Operatingefficiency:Acompanycanreducetheworkingcapitalrequirementbyeliminatingwaste,improving•coordination, etc.Price level changes: For e.g., rising prices necessitate the use of more funds for maintaining an existing level •of activity. For the same level of current assets, higher cash outlays are required. Therefore, the effect of rising prices is that a higher amount of working capital is required.

1.4 Issues in the Working Capital ManagementWorking capital management entails the control and monitoring of all components of working capital, i.e., cash, marketable securities, debtors (receivables) and stocks (inventories) and creditors (payables). Finance manager has topayparticularattentiontothelevelsofcurrentassetsandtheirfinancing.Todecidethelevelsandfinancingofcurrent assets, the risk return trade off must be taken into account.

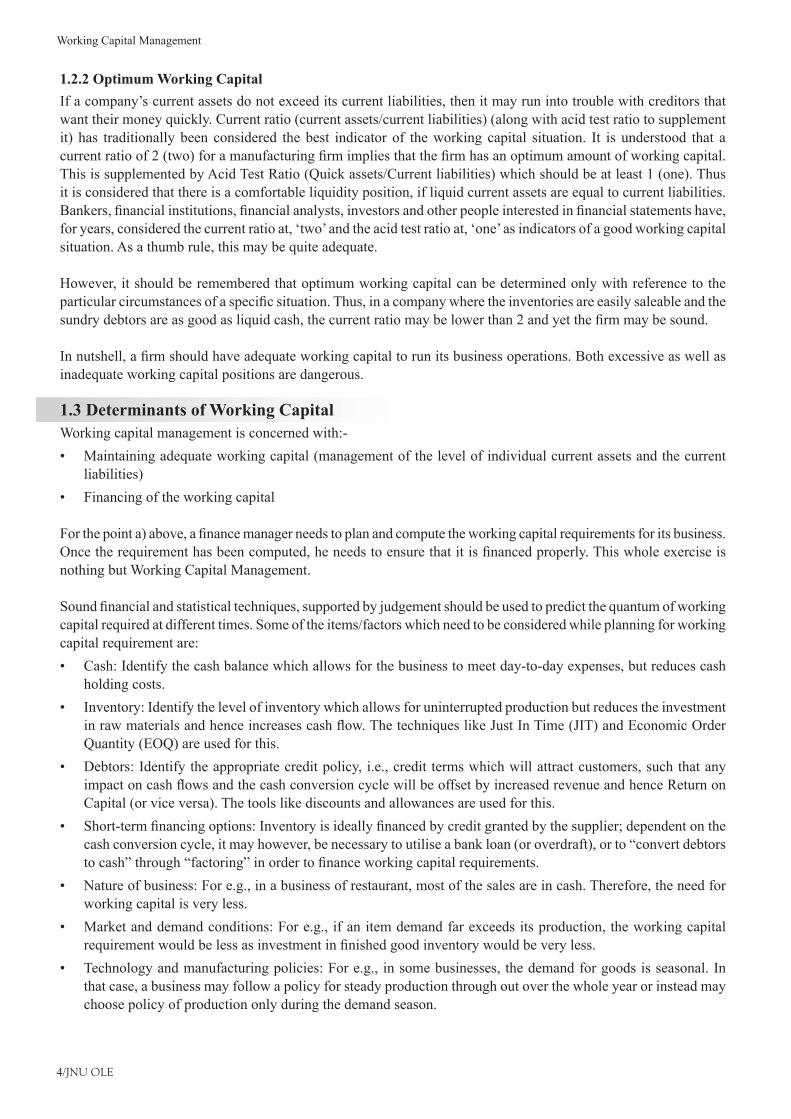

1.4.1 Current Assets to Fixed Assets RatioThefinancemanagerisrequiredtodeterminetheoptimumlevelofcurrentassets,sothattheshareholders’valueismaximised.Afirmneedsfixedandcurrentassetstosupportaparticularlevelofoutput.Asthefirm’soutputandsalesincreases, the need for current assets also increases. Generally, current assets do not increase in direct proportion tooutput;currentassetsmayincreaseatadecreasingratewithoutput.Astheoutputincreases,thefirmstartsusingitscurrentassetsmoreefficiently.

Thelevelofthecurrentassetscanbemeasuredbycreatingarelationshipbetweencurrentassetsandfixedassets.Dividingcurrentassetsbyfixedassetsgivescurrentassets/fixedassetsratio.Assumingaconstantleveloffixedassets,ahighercurrentassets/fixedassetsratioindicatesaconservativecurrentassetspolicyandalowercurrentassets/fixedassetsratiomeansanaggressivecurrentassetspolicyassumingallfactorstobeconstant.

A conservative policy implies greater liquidity and lower risk, whereas an aggressive policy indicates higher risk and poor liquidity. Moderate current assets policy will fall in the middle of conservative and aggressive policies. Thecurrentassetspolicyofmostofthefirmsmayfallbetweenthesetwoextremepolicies.

The following diagram shows alternative current assets policies:

Fig. 1.3 Alternative current assets policies

Working Capital Management

6/JNU OLE

1.4.2 Liquidity versus ProfitabilityRiskreturntradeoff−Afirmmayfollowaconservative,aggressiveormoderatepolicyasdiscussedabove.However,these policies involve risk, return trade off. A conservative policy means lower return and risk. An aggressive policy produces higher returns and risks.

Thetwoimportantaimsoftheworkingcapitalmanagementareprofitabilityandsolvency.Aliquidfirmhaslessrisk of insolvency, that is, it will hardly experience a cash shortage or a stock out situation. However, there is a cost associatedwithmaintainingasoundliquidityposition.However,tohavehigherprofitabilitythefirmmayhavetosacrificesolvencyandmaintainarelativelylowlevelofcurrentassets.Thiswillimprovefirm’sprofitabilityasfewer funds will be tied up in idle current assets, but its solvency would be threatened and exposed to greater risk of cash shortage and stock outs.

1.5 Estimating Working Capital NeedsOperating cycle is one of the most reliable methods of computation of working capital. However, other methods likeratioofsalesandratiooffixedinvestmentmayalsobeusedtodeterminetheworkingcapitalrequirements.Thesemethodsarebrieflyexplainedasfollows:

Current assets holding period: To estimate working capital needs based on the average holding period of •current assets and relating them to costs based on the company’s experience in the previous year. This method is essentially based on the Operating Cycle Concept.Ratio of sales: To estimate working capital needs as a ratio of sales on the assumption that current assets change •with changes in sales.Ratiooffixedinvestments:Toestimateworkingcapitalrequirementsasapercentageoffixedinvestments.•

A number of factors will, however, be impacting the choice of method of estimating Working Capital. Factors such asseasonalfluctuations,accuratesalesforecast,investmentcostandvariabilityinsalespricewouldgenerallybeconsidered.Theproductioncycleandcreditandcollectionpoliciesofthefirmwillhaveanimpactonworkingcapitalrequirements. Therefore, they should be given due weightage in projecting working capital requirements.

1.6 Operating or Working Capital CycleA useful tool for managing working capital is the operating cycle. The operating cycle analyses the accounts receivable, inventory and accounts payable cycles in terms of number of days. For example:

Accounts receivable are analysed by the average number of days it takes to collect an account.•Inventory is analysed by the average number of days it takes to turn over the sale of a product (from the point •it comes in the store to the point it is converted to cash or an account receivable).Accounts payable are analysed by the average number of days it takes to pay a supplier invoice.•

Working capital cycle indicates the length of time between a company’s payment to procure materials, entering it intostockandreceivingcashfromthesalesoffinishedgoods.Itcanbedeterminedbyaddingthenumberofdaysrequired for each stage in the cycle. For example, a company holds raw materials on an average for 60 days, it gets creditfromthesupplierfor15days,productionprocessneeds15days,finishedgoodsareheldfor30daysand30 days credit is extended to debtors. The total of all these, 120 days, i.e., 60 – 15 + 15 + 30 + 30 days is the total working capital cycle.

Mostbusinessescannotfinance theoperatingcycle (accounts receivabledays+ inventorydays)withaccountspayablefinancingalone.Consequently,workingcapitalfinancingisneeded.Thisshortfallistypicallycoveredbythenetprofitsgeneratedinternallyorbyexternallyborrowedfundsorbyacombinationofthetwo.

The faster a business expands the more cash it will need for working capital and investment. The cheapest and best sources of cash exist as working capital right within a business. Good management of working capital will generate cashwhichwillhelptoimproveprofitsandreducerisks.Thecostofprovidingcredittocustomersandholdingstockscanrepresentasubstantialproportionofafirm’stotalprofits.

7/JNU OLE

1.7 Concept of Working Capital There are two concepts of working capital. These are:

Gross Working Capital (Total Current Assets) Thegrossworkingcapital,simplycalledasworkingcapitalreferstothefirm’sinvestmentincurrentassets.Currentassets are the assets, which can be converted into cash within an accounting year or operating cycle. Thus, gross working capital, is the total of all current assets. It includes:

Inventories (Raw materials and Components, Work-in-Progress, Finished Goods, etc.) •Trade Debtors •Loans and Advance •Cash and Bank Balances •Bills Receivables •Short-term Investment•

Net Working Capital (Total Current Assets – Total Current Liabilities)Net working capital refers to the difference between current assets and current liabilities. Current liabilities are those claims of outsiders, which are expected to mature for payment within an accounting year. Net working capital may be positive or negative. A positive net working capital will arise when current assets exceed current liabilities and a negative net working capital will arise when current liabilities exceed current assets, i.e., there is no working capital,butthereisaworkingcapitaldeficit.Itincludes:

Trade Creditors •Bills Payable •Accrued or Outstanding Expenses •Trade Advances •Short-term Borrowings (Commercial Banks and Others) •Provisions •Bank Overdraft •

Working capital represents the amount of current assets that have not been supplied by current, short-term creditors. Gross working capital refers to the amount of funds invested in current assets that are employed in the business process while, Net working capital refers to the difference between current assets and current liabilities.

Working capital is the excess of current assets that has been supplied by the long-term creditors and the stockholders. The two concepts of working capital, gross working capital and net working capital are exclusive. Both are equally importantfor theefficientmanagementofworkingcapital.Thegrossworkingcapitalfocusesattentionontwoaspects,howinvestmentcanbeoptimisedincurrentassetsandhowcurrentassentsshouldbefinanced?Networkingcapitalconceptisqualitative.Itindicatestheliquiditypositionofthefirmandsuggeststheextenttowhichworkingcapitalneedsmaybefinancedbypermanentsourcesoffunds.

1.8 Requirements of Working Capital Therearenosetrulesorformulatodeterminetheworkingcapitalrequirementsofthefirms.Alargenumberoffactorsinfluencetheworkingcapitalneedofthefirms.Allfactorsareofdifferentimportanceandalsoimportancechangeforthefirmovertime.Therefore,ananalysisoftherelevantfactorsshouldbemadeinordertodeterminethetotalinvestmentinworkingcapital.Generally,thefollowingfactorsinfluencetheworkingcapitalrequirementsofthefirm:

Nature and size of the business •Seasonalfluctuations•Production policy •

Working Capital Management

8/JNU OLE

Taxation •Depreciation policy •Reserve policy •Dividend policy •Credit policy: •Growth and expansion •Price level changes •Operatingefficiency•Profitmarginandprofitappropriation•

1.9 Classification of Working Capital The quantitative concept of working capital is known as gross working capital while that under qualitative concept isknownasnetworkingcapital.Workingcapitalcanbeclassifiedinvariousways.Theimportantclassificationsare as given below: Conceptual classificationThere are two concepts of working capital, viz., quantitative and qualitative. The quantitative concept takes into account as the current assets while the qualitative concept takes into account the excess of current assets over current liabilities.Deficitofworkingcapitalexistswheretheamountofcurrentliabilitiesexceedstheamountofcurrentassets. The above can be summarised as follows:

Gross working capital = Total current assets •Net working capital = Excess of current assets over current liabilities •Workingcapitaldeficit=Excessofcurrentliabilitiesovercurrentassets.•

Classification on the basis of financial reportsTheinformationofworkingcapitalcanbecollectedfromBalanceSheetorProfitandLossAccount;assuchtheworkingcapitalmaybeclassifiedasfollows:

CashWorkingCapital–This iscalculated from the informationcontained inprofitand lossaccount.This•conceptofworkingcapitalhasassumedagreatsignificanceinrecentyearsasitshowstheadequacyofcashflowinbusiness.Balance Sheet Working Capital – The data for balance sheet working capital is collected from the balance •sheet. On this basis, the working capital can also be divided in three more types, viz., gross working capital, networkingcapitalandworkingcapitaldeficit.

Classification on the basis of variabilityGrossworkingcapitalcanbedividedintwocategories,viz.,(i)permanentorfixedworkingcapitaland(ii)Temporary,seasonalorvariableworkingcapital.Suchtypeofclassificationisveryimportantforhedgingdecisions.

Temporaryworkingcapital–Temporaryworkingcapitalisalsocalledasfluctuatingorseasonalworkingcapital.•This represents additional investment needed during prosperity and favourable seasons. It increases with the growth of the business. Temporary working capital is the additional assets required to meet the variations in sales above the permanent level.Permanent working capital – It is a part of total current assets which is not changed due to variation in sales. •There is always a minimum level of cash, inventories, and accounts receivables which is always maintained in the business even if sales are reduced to a minimum. Amount of such investment is called as permanent working capital. Permanent working capital is the amount of working capital that persists over time regardless offluctuationsinsales.Thisisalsocalledasregularworkingcapital.

9/JNU OLE

1.10 Significance of Working Capital Management Funds are needed in every business for carrying on day-to-day operations. Working capital funds are regarded as the lifebloodofabusinessfirm.Afirmcanexistandsurvivewithoutmakingprofitbutcannotsurvivewithoutworkingcapitalfunds.Ifafirmisnotearningprofititmaybetermedas‘sick’,but,nothavingworkingcapitalmaycauseitsbankruptcy.Eachfirmmustdecidehowtobalancetheamountofworkingcapitalitholds,againsttheriskoffailure.Workingcapitalhasacquiredagreatsignificanceandsoundpositionintherecentpastforthetwinobjectsofprofitabilityandliquidity.Inperiodofrisingcapitalcostsandscarcefunds,theworkingcapitalisoneofthemostimportant areas requiring management review.

It is rightly observed that, Constant management review is required to maintain appropriate levels in the various working capital accounts. Mainly the success of a concern depends upon proper management of working capital. Hence, working capital managementhasbeenlookeduponasthedrivingseatofafinancialmanager.Itconsumesagreatdealoftimetoincreaseprofitabilityaswellastomaintainproperliquidityatminimumrisks.Therearemanyaspectsofworkingcapitalmanagementwhichmakeitanimportantfunctionofthefinancemanager.Infact,weneedtoknowwhentolook for working capital funds, how to use them and how to measure, plan and control them.

A study of working capital management is very important for internal and external experts. Sales expansion, dividend declaration, plants expansion, new product line, increase in salaries and wages, rising price level, etc., put added strain on working capital maintenance. Failure of any enterprise is undoubtedly due to poor management and absence of management skills. Importance of working capital management stems from two reasons, viz., (i) A substantial portion of total investment is invested in current assets, and (ii) level of current assets and current liabilities will changequicklywiththevariationinsales.Thoughfixedassetsinvestmentandlong-temborrowingwillalsorespondto the changes in sales, but its response will be weak.

1.11 Factors Influencing Working Capital Requirements Numerousfactorscaninfluencethesizeandneedofworkingcapitalinaconcern.So,nosetruleorformulacanbeframed. It is rightly observed that, there is no precise way to determine the exact amount of gross or net working capital for every enterprise. The data and problem of each company should be analysed to determine the amount of workingcapital.Briefly,theoptimumlevelofcurrentassetsdependsuponthefollowingdeterminants.

Nature of business: Trading and industrial concerns require more funds for working capital. Concerns engaged •in public utility services need less working capital. For example, if a concern is engaged in electric supply, it willneedlesscurrentassets,firstlyduetocashnatureofthetransactionsandsecondlyduetosaleofservices.However,itwillinvestmoreinfixedassets.Inadditiontoit,theinvestmentvariesconcerntoconcern,dependingupon the size of business, the nature of the product, and the production technique.Conditions of supply: If the supply of inventory is prompt and adequate, less funds will be needed. But, if the •supply is seasonal or unpredictable, more funds will be invested in inventory. Investment in working capital willfluctuateincaseofseasonalnatureofsupplyofrawmaterials,sparepartsandstores.Productionpolicy:Incaseofseasonalfluctuationsinsales,productionwillfluctuateaccordinglyandultimately•therequirementofworkingcapitalwillalsofluctuate.However,salesdepartmentmayfollowapolicyofoff-season discount, so that sales and production can be distributed smoothly throughout the year and sharp variations in working capital requirements are avoided.Seasonal operations: It is not always possible to shift the burden of production and sale to slack period. For •example, in case of sugar mill, more working capital will be needed at the time of crop and manufacturing.

Working Capital Management

10/JNU OLE

Credit availability: If credit facility is available from banks and suppliers on favourable terms and conditions, •less working capital will be needed. If such facilities are not available, more working capital will be needed to avoid risk. Credit policy of enterprises-- in some enterprises, most of the sale is in cash and even it is received in advance. In other enterprises, mostly credit sales happen and payments are received only after a month or two. In former case, less working capital is needed than the latter. The credit terms depend largely on norms of the industry. In order to ensure that unnecessary funds are not tied up in book debts, the enterprise should follow a rationalised credit policy based on the credit standing of the customers and other relevant factors.Growth and expansion: The need of working capital is increasing with the growth and expansion of an enterprise. •Itisdifficulttopreciselydeterminetherelationshipbetweenvolumeofsalesandtheworkingcapitalneeds.Thecritical fact, however, is that the need for increased working capital funds does not follow growth in business activities but precedes it. It is clear that advance planning is essential for a growing concern.Price level change: With the increase in price level, more and more working capital will be needed for the same •magnitude of current assets. The effect of rising prices will be different for different enterprises.Circulation of working capital: Less working capital will be needed with the increase in circulation of working •capital and vice-versa. Circulation means time required to complete one cycle, i.e., from cash to material, frommaterialtowork-in-progress,fromwork-in-progresstofinishedgoods,fromfinishedgoodstoaccountsreceivable and from accounts receivable to cash.Volume of sale: This is directly indicated with working capital requirement, with the increase in sales more •workingcapitalisneededforfinishedgoodsanddebtors.Itsviceversaisalsotrue.Liquidityandprofitability:Thereisanegativerelationshipbetweenliquidityandprofitability.Whenworking•capitalinrelationtosalesisincreaseditwillreduceriskandprofitabilityononesideandwillincreaseliquidityon the other side.Management ability: Proper co-ordination in production and distribution of goods may reduce the requirement •of working capital, as minimum funds will be invested in absolute inventory, non-recoverable debts, etc.Externalenvironment:Withdevelopmentoffinancialinstitutions,meansofcommunication,transportfacility,•etc., needs of working capital is reduced because it can be available as and when needed.

1.12 Principles of Working Capital Management The following are the principles of working capital management:

Principlesoftheriskvariation:Riskherereferstotheinabilityoffirmtomaintainsufficientcurrentassetsto•payitsobligations.Ifworkingcapitalisvariedrelativetosales,theamountofriskthatafirmassumesisalsovariedandtheopportunityforgainorlossisincreased.Inotherwords,thereisadefiniterelationshipbetweenthedegreeofriskandtherateofreturn.Asafirmassumesmorerisk,theopportunityforgainorlossincreases.As the level of working capital relative to sales decreases, the degree of risk increases. When the degree of risk increases, the opportunity for gain and loss also increases. Thus, if the level of working capital goes up, amount of risk goes down, and vice-versa, the opportunity for gain is likewise adversely affected.Principle of equity position: According to this principle, the amount of working capital invested in each component •shouldbeadequatelyjustifiedbyafirm’sequityposition.Everyrupeeinvestedintheworkingcapitalshouldcontributetothenetworthofthefirm.Principleofcostofcapital:Thisprincipleemphasisesthatdifferentsourcesoffinancehavedifferentcostof•capital. It should be remembered that the cost of capital moves inversely with risk. Thus, additional risk capital results in decline in the cost of capital.Principle of maturity of payment: A company should make every effort to relate maturity of payments to its •flowofinternallygeneratedfunds.Thereshouldbetheleastdisparitybetweenthematuritiesofafirm’sshort-termdebtinstrumentsanditsflowofinternallygeneratedfunds,becauseagreaterriskisgeneratedwithgreaterdisparity. A margin of safety should, however, be provided for any short-term debt payments.

11/JNU OLE

1.13 Structure of Working CapitalThe study of structure of working capital is another name for the study of working capital cycle. In other words, it can be said that the study of structure of working capital is the study of the elements of current assets, viz., inventory, receivable, cash and bank balances and other liquid resources like short-term or temporary investments. Current liabilities usually comprise bank borrowings, trade credits, assessed tax and unpaid dividends or any other such things. The following points relate to the various elements of working capital:

InventoryInventory is a major item of current assets. The management of inventories – raw material, goods-in-process and finishedgoodsisanimportantfactorintheshort-runliquiditypositionsandlong-termprofitabilityofthecompany.Rawmaterialinventories–uncertaintiesaboutthefuturedemandforfinishedgoods,togetherwiththecostsofadjustingproductiontochangeindemandwillcauseafinancialmanagertodesiresomelevelofrawmaterialinventory.Intheabsenceofsuchinventory,thecompanycouldrespondtoincreaseddemandforfinishedgoodsonlybyincurringexplicitclericalandothertransactioncostsofordinaryrawmaterialforprocessingintofinishedgoodstomeetthatdemand. If changes in demand are frequent, these order costs may become relatively large.

Moreover, attempts to purchase hastily the needed raw material may necessitate payment of premium purchases prices to obtain quick delivery and, thus, raise cost of production. Finally, unavoidable delays in acquiring raw material may cause the production process to shut down and then re-start again raising the costs of production. Under these conditions the company cannot respond promptly to changes in demand without sustaining high costs. Hence, some level of raw materials inventory has to be held to reduce such costs. Determining its proper level requires an assessment of costs of buying and holding inventories and a comparison with the costs of maintaining insufficientlevelofinventories.

Work-in-process inventoryThis inventory is built up due to production cycle. Production cycle is the time-span between introduction of raw materialintoproductionandemergenceoffinishedproductatthecompletionofproductioncycle.Tilltheproductioncycle is completed, the stock of work-in-process has to be maintained.

Finished goods inventoryFinished goods are required for reasons similar to those causing the company to hold raw materials inventories. Customer’sdemandforfinishedgoodsisuncertainandvariable.Ifacompanycarriesnofinishedgoodsinventory,unanticipated increases in customer demand would require sudden increases in the rate of production to meet the demand. Such rapid increase in the rate of production may be very expensive to accomplish. Rather than loss of sales,becausetheadditionalfinishedgoodsarenotimmediatelyavailableorsustainhighcostsofrapidadditionalproduction,itmaybecheapertoholdafinishedgoodsinventory.Theflexibilityaffordedbysuchaninventoryallows a company to meet unanticipated customer demands at relatively lower costs than if such an inventory is not held.

Thus, to develop successfully optimum inventory policies, the management needs to know about the functions of inventory, the cost of carrying inventory, economic order quantity and safety stock. Industrial machinery is usually verycostlyanditishighlyuneconomicaltoallowittolieidle.Skilledlabouralsocannotbehiredandfiredatwill.Modern requirements are also urgent. Since requirements cannot wait and since the cost of keeping machine and men idle is higher, than the cost of storing the material, it is economical to hold inventories to the required extent. The objectives of inventory management are:

To minimise idle cost of men and machines causes by shortage of raw materials, stores and spare parts. •To keep down: •

Inventory ordering cost �Inventory carrying cost �Capital investment in inventories �Obsolescence losses �

Working Capital Management

12/JNU OLE

ReceivablesManyfirmsmakecreditsalesandasaresultthereofcarryreceivablesasacurrentasset.Thepracticeofcarryingreceivables has several advantages as follows:

Reduction of collection costs over cash collection•Reduction in the variability of sales, and •Increase in the level of near-term sales. •

While immediate collection of cash appears to be in the interest of shareholders, the cost of that policy may be very high relative to costs associated with delaying the receipt of cash by extension of credit. Imagine, for example, an electric supply company employing a person at every house constantly reading electricity meter and collecting cash from him every minute as electricity is consumed. It is far cheaper for accumulating electricity usage and bill once a month. This of course, is a decision to carry receivables on the part of the company. It may also be true that the extensionofcreditbythefirmtoitscustomersmayreducethevariabilityofsalesovertime.Customersconfinedtocash purchases may tend to purchase goods when cash is available to them. Erratic and perhaps cyclical purchasing patterns may then result unless credit can be obtained elsewhere. Even if customers do obtain credit elsewhere, they must incur additional cost of search in arranging for a loan costs that can be estimated when credit is given by asupplier.Therefore,extensionofcredittocustomersmaywellsmoothoutofthepatternofsalesandcashinflowstothefirmovertimesincecustomersneednotwaitforsomeinflowsofcashtomakeapurchase.Totheextentthatsales are smoothed, cost of adjusting production to changes in the level of sales should be reduced.

Finally,theextensionofcreditbyfirmsmayacttoincreasenear-termsales.Customersneednotwaittoaccumulatenecessary cash to purchase an item but can acquire it immediately on credit. This behaviour has the effect of shifting futuresalesclosetothepresenttime.Therefore,theextensionofcreditbyafirmandtheresultinginvestmentinreceivablesoccursbecauseitpaysafirmtodoso.Costsofcollectingrevenuesandadaptingtofluctuatingcustomerdemandsmaymakeitdesirabletooffertheconvenienceassociatedwithcredittofirm’scustomers.

Cash and interest-bearing liquid assetsCash is one of the most important tools of day-to-day operation, because it is a form of liquid capital which is available for assignment to any use. Cash is often the primary factor which decides the course of business destiny. The decision to expand a business may be determined by the availability of cash and the borrowing of funds will frequently be dictated by cash position. Cash-in-hand, however, is a non-earning asset. This leads to the question as to what the optimum level of this idle resource is. This optimum depends on various factors, such as the manufacturing cycle, the sale and collection cycle, age of the bills and on the maturing of debt. It also depends upon the liquidity of other current assets and the matter of expansion. While a liberal maintenance of cash provides asenseofsecurity,alackofsufficiencyofcashhampersday-to-dayoperations.Prudence,therefore,requiresthatno more cash should be kept on hand than the optimum required for handling miscellaneous transactions over the counter and petty disbursements, etc.

It has not become a practice with business enterprises to avoid too much redundant cash by investing a portion of their earnings in assets which are susceptible to easy conversion into cash. Such assets may include government securities, bonds, debentures and shares that are known to be readily marketable and that may be liquidated at a moment’s notice, when cash is needed.

13/JNU OLE

SummaryWorkingCapitalManagementinvolvesmanagingthebalancebetweenfirm’sshort-termassetsanditsshort-•term liabilities.The interaction between current assets and current liabilities is the main theme of the theory of working capital •management.Grossworkingcapitalreferstothefirm’sinvestmentincurrentassets.•Net working capital refers to the difference between current assets and current liabilities.•A positive working capital means that the company is able to payoff its short-term liabilities.•Permanent working capital refers to the hard core working capital. It is that minimum level of investment in •the current assets that is carried by the business.Temporary working capital refers to that part of total working capital, which is required by a business over and •above permanent working capital.Working capital management entails the control and monitoring of all components of working capital.•Thelevelofthecurrentassetscanbemeasuredbycreatingarelationshipbetweencurrentassetsandfixed•assets.Assumingaconstantleveloffixedassets,ahighercurrentassets/fixedassetsratioindicatesaconservative•currentassetspolicyandalowercurrentassets/fixedassetsratiomeansanaggressivecurrentassetspolicyassuming all factors to be constant.A conservative policy implies greater liquidity and lower risk, whereas an aggressive policy indicates higher •risk and poor liquidity.Thetwoimportantaimsoftheworkingcapitalmanagementareprofitabilityandsolvency.•Operating cycle is one of the most reliable methods of computation of working capital.•A useful tool for managing working capital is the operating cycle.•Working capital cycle indicates the length of time between a company’s payment for materials, entering into •stockandreceivingthecashfromsalesoffinishedgoods.Current assets are the assets, which can be converted into cash within an accounting year or operating cycle.•Net working capital refers to the difference between current assets and current liabilities.•Working capital is the excess of current assets that has been supplied by the long-term creditors and the •stockholders.The quantitative concept of working capital is known as gross working capital while that under qualitative •concept is known as net working capital.Cash is one of the most important tools of day-to-day operation, because it is a form of liquid capital which is •available for assignment to any use.Whilealiberalmaintenanceofcashprovidesasenseofsecurity,alackofsufficiencyofcashhampersday-to-•day operations.

ReferencesWorking Capital• [Online] Available at: <http://www.scribd.com/doc/24525667/Working-Capital-analysis> [Accessed 12 July 2013].Work capital Analysis• [Pdf]Availableat:<http://shodhganga.inflibnet.ac.in/bitstream/10603/705/13/14_chapter5.pdf> [Accessed 12 July 2013].Working capital Management• [Videoonline]Availableat<http://www.youtube.com/watch?v=KQWe-2G23kw>[Accessed 12 July 2013].Working Capital Management Principal and Approaches• [Video online] Available at <http://www.youtube.com/watch?v=zJCiEIqAxbs>[Accessed12July2013].

Working Capital Management

14/JNU OLE

Preve, L. And Allende, V.S., 2010. • Working Capital Management. Oxford University Press, USA.Sagner, J., 2010. • Essentials of Working Capital Management. Wiley.

Recommended ReadingWeide, J. H.V. and Maier, S. F., 1984. • Managing Corporate Liquidity: An Introduction to Working Capita. John Wiley & Sons Inc.Kimmel,P.D.andWeygandt,J.J.,2008.• Financial Accounting: Tools for Business Decision Making. 5th ed., Wiley.Laurens, B., 1998. • Managing capital flows. International Monetary Fund, Monetary and Exchange Affairs Department.

15/JNU OLE

Self AssessmentThegoalof_________________istoensurethatthefirmisabletocontinueitsoperationsandthatithas1. sufficientcashflowtosatisfybothmaturingshort-termdebtandupcomingoperationalexpenses.

investmenta. working capital managementb. credibilityc. gross working capitald.

_________________referstothefirm’sinvestmentincurrentassets.2. Working capitala. Cash balanceb. Current liabilitiesc. Gross working capitald.

_______________referstothedifferencebetweencurrentassetsandcurrentliabilities.3. Net working capitala. Short-term liabilitiesb. Permanent working capitalc. Fluctuating working capitald.

Whichofthefollowingisalsocalledvariableworkingcapital?4. Permanent working capitala. Temporary working capitalb. Current liabilitiesc. Gross working capitald.

Whichofthefollowingisnotafunctionoffinancialmanagement?5. Timea. Credibilityb. Growthc. Assetsd.

Whichofthefollowingisnotafactorwhichisconsideredwhileplanningforworkingcapitalrequirement?6. Credibilitya. Cashb. Inventoryc. Debtorsd.

The___________________isrequiredtodeterminetheoptimumlevelofcurrentassets,sothattheshareholders7. value is maximised.

firma. assetb. current assetc. financemanagerd.

Working Capital Management

16/JNU OLE

A_________________impliesgreaterliquidityandlowerrisk,whereasanaggressivepolicyindicateshigher8. risk and poor liquidity.

current assets policya. return trade offb. risk trade offc. conservative policyd.

Whichofthefollowingisnotamethodusedtodeterminetheworkingcapitalrequirements?9. Ratio of salesa. Ratio of variable investmentb. Ratiooffixedinvestmentc. Current assets holding periodd.

The_______________analysestheaccountsreceivable,inventoryandaccountspayablecyclesintermsof10. number of days.

working capital cyclea. operating cycleb. total current assetsc. total current liabilitiesd.

17/JNU OLE

Chapter II

Cash Management

Aim

The aim of this chapter is to:

definecashmanagement•

elucidate the principles of cash management•

explain the functions of cash management•

Objectives

The objectives of this chapter are to:

explainthefinancingofcashshortage•

explicate the cost of running out of cash•

elucidatetheconceptoffinancingcurrentassets•

Learning outcome

At the end of this chapter, you will be able to:

understandthethreeapproachesoffinancingcurrentassets•

identifythecashflowstatement•

recognise the motives of holding cash•

Working Capital Management

18/JNU OLE

2.1 IntroductionCash, like the blood stream in the human body, gives vitality and strength to a business enterprise. Though, cash holds the smallest portion of total current assets. However, cash is both the beginning and end of working capital cycle - cash, inventories, receivables and cash. It is the cash, which keeps the business going. Hence, every enterprise has to hold necessary cash for its existence. Moreover, steady and healthy circulation of cash throughout the entire business operations is the basis of business solvency. Now-a-days, non-availability and high cost of money have created a serious problem for the industry. Nevertheless, cash like any other asset of a company is treated as a tool ofprofit.Further,todaytheemphasisisontherightamountofcash,attherighttime,attherightplaceandattheright cost.

In the words of R.R. Bari, “Maintenance of surplus cash by a company unless there are special reasons for doing so, is regarded as a bad sign of cash management.” Holding of cash balance has an implicit cost in the form of its opportunity cost.

Cash may be interpreted under two concepts. In narrow sense, cash is a very important business asset, but although coin and paper currency can be inspected and handled, the major part of the cash of most enterprises is in the form of bank checking accounts, which represent claims to money rather than tangible property. While in a broader sense, cash consists of legal tender, cheques, bank drafts, money orders and demand deposits in banks. In general, nothing should be considered unrestricted cash, unless it is available to the management for disbursement of any nature. Thus, from the above quotations we may conclude that in narrow sense, cash means cash in hand and at bank but in wider sense, it is the deposits in banks, currency, cheques, bank drafts, etc., in addition to cash in hand and at bank. Cash management includes management of marketable securities also, because in modern terminology money comprises marketable securities and actual cash in hand or in bank.

Theconceptofcashmanagementisnotnewandithasacquiredagreatersignificanceinthemodernworldofbusinessduetochangesthattookplaceintheconductofbusinessandeverincreasingdifficultiesandthecostofborrowing.Apart from the fact that it is the most liquid of all the current assets, cash is the common denominator to which all current assets can be reduced because the other current assets, i.e., receivables and inventory get eventually converted intocash.Thisunderlinesthesignificanceofcashmanagement.Thetermcashmanagementreferstothemanagementof cash resource in such a way that generally accepted business objectives could be achieved. In this context, the objectivesofafirmcanbeunifiedasbringingaboutconsistencybetweenmaximumpossibleprofitabilityandliquidityofafirm.Cashmanagementmaybedefinedastheabilityofamanagementinrecognisingtheproblemsrelatedwithcashwhichmaycomeacrossinfuturecourseofaction,findingappropriatesolutionstocurbsuchproblemsiftheyarise,andfinallydelegatingthesesolutionstothecompetentauthorityforcarryingthemout.Thechoicebetweenliquidityandprofitabilitycreatesastateofconfusion.Itiscashmanagementthatcanprovidesolutiontothis dilemma. Cash management may be regarded as an art that assists in establishing equilibrium between liquidity andprofitabilitytoensureundisturbedfunctioningofafirmtowardsattainingitsbusinessobjectives.

Cash itself is not capable of generating any sort of income on its own. It rather is the prime requirement of income generatingsourcesandfunctions.Thus,afirmshouldgoforminimumpossiblebalanceofcash,yetmaintainingitsadequacyfortheobviousreasonoffirm’ssolvency.Cashmanagementdealswithmaintainingsufficientquantityofcashinsuchawaythatthequantitydenotesthelowestadequatecashfiguretomeetbusinessobligations.

Cashmanagementinvolvesmanagingcashflows(intoandoutofthefirm),withinthefirmandthecashbalancesheldbyaconcernatapointoftime.Thewords,‘managingcashandthecashbalances’asspecifiedabovedoesnotmean optimisation of cash and near cash items but also point towards providing a protective shield to the business obligations. Cash management is concerned with minimising unproductive cash balances, investing temporarily excess cash advantageously and to make the best possible arrangement for meeting planned and unexpected demands onthefirms’cash.

19/JNU OLE

2.2 General Principles of Cash ManagementHarryGrosshassuggestedcertaingeneralprinciplesofcashmanagementthat,essentiallyaddefficiencytocashmanagement.Theseprinciplesreflectingcauseandeffectrelationshiphavinguniversalapplicationsgiveascientificoutlook to the subject of cash management. While, the application of these principles in accordance with the changing conditions and business environment requiring high degree of skill and tact which places cash management in the category of art. Thus, we can say that cash management like any other subject of management is both science and art.Ithaswell-establishedprinciplescapableofbeingskilfullymodifiedaspertherequirements.Theprinciplesofmanagement are follows: