workshop 28: pooling of pension fund assets 27 th may, 2009 | 11:15 – 12:30 corinne merla...

TRANSCRIPT

WORKSHOP 28: POOLING OF PENSION FUND ASSETS

27TH May, 2009 | 11:15 – 12:30

Corinne Merla (Belgium); Brian Buggy (Ireland);Wijnanda Rutten (The Netherlands); Philip Bennett (UK); Howard Pianko (USA)

Note: Our thanks to Jacques Elvinger of Elvinger Hoss & Prussen, Luxembourg, who has reviewed the summary of the Luxembourg law position in these slides

PN091250055

2

Part 1:

Introduction: Why Bother?

3

Part 1: Introduction: Current Position

Multinational Employer Group

Pension Fund 1 Pension Fund 2 Pension Fund 3

Custodian 1

Investment Manager 1.1

Investment Manager 1.2

Investment Manager 1.3

Custodian 2

Investment Manager 2.1

Investment Manager 2.2

Investment Manager 2.3

Custodian 3

Investment Manager 3.1

Investment Manager 3.2

Investment Manager 3.3

Diagram 1

4

Part 1: Introduction: Desired Position*

Diagram 2

EU Employer Group

Pension Fund 1 Pension Fund 2 Pension Fund 3

Pooling Vehicle Custodian

Equity Sub-Fund

Bond Sub-Fund

Equity Manager 1

Equity Manager 2

Bond Manager 1

Bond Manager 2

Sub-Custodian 1 Sub-Custodian 2

*Assumes no U.S. plan participation

5

Part 1: Introduction: U.S. Master Trust Structure

Diagram 3

U.S. Employer

U.S. Pension Fund 1

U.S. Pension Fund 2

U.S. Pension Fund 3

Master Trust Master Trustee

Equity Sub-Fund

Bond Sub-Fund

Equity Manager 1

Equity Manager 2

Bond Manager 1

Bond Manager 2

Sub-Custodian 1 Sub-Custodian 2

Investment Committee

6

Part 1: Introduction: Desired Position with U.S. multinational overlay

Diagram 4

U.S. Company 1

EU Pension Fund 1

EU Pension Fund 2

Pooling VehicleCustodian/Master

Custodian

Equity Sub-Fund Bond Sub-Fund

Equity Manager 1 Equity Manager 2 Bond Manager 1 Bond Manager 2

Sub-Custodian 1 Sub-Custodian 2* If the parent of the multinational employer group is a U.S. entity, the developing model addresses ERISA by structuring the pooling vehicle and the commingled sub-funds to comply with ERISA (a “safe harbor” approach). If the parent of the multinational employer group is a non-U.S. entity and a “safe harbor” approach is not adopted, the pooled vehicle and the commingled investment sub-funds could be subject to ERISA if 25% or more of their respective assets are attributable to U.S. benefit plans.

Investment Committee

Management Company

Master Trust

U.S. Pension Fund 1

U.S. Pension Fund 2

EU Company 1 EU Company 2 U.S. Company 2

U.S. Parent Company

7

Part 1: Introduction: Hoped-for efficiencies

Source of Efficiency

Existing Position Use of Pooling Vehicle Comment

1. Investment management fees

1.1 Each pension fund appoints its own investment managers

1.2 More investment management agreements, so more management time and legal fees and higher management fees

1.3 Multiple investment managers

1.1 Reduction in number of investment managers

1.2 Reduction in number of investment management agreements

1.3 Volume discount on investment management fees. Savings in legal fees and management time

1.1 Possible for sponsoring employer group to achieve number of the savings if pension funds used the same investment managers (as fees can be negotiated on a bulk basis)

2. Custodian 2.1 Each fund appoints its own custodian

2.2 More custodian agreements, so more management time and legal fees and higher custody fees

2.3 Multiple custodians

2.1 Reduction in number of custodians

2.2 Reduction in number of custody agreements

2.3 Volume discount on custodian fees. Saving in legal fees and management time

2.1 Possible for sponsoring employer group to achieve number of the savings if pension funds used the same custodian managers (as fees can be negotiated on a bulk basis)

8

Part 1: Introduction: Hoped-for efficiencies (cont'd)

Source of Efficiency

Existing Position Use of Pooling Vehicle Comment

3. Governance 3.1 Higher consumption of management time in relation to investment matters for each of the different pension funds

3.2 Dilution of available internal investment knowledge and expertise

3.3 Duplication of purchase of investment consulting services

3.1 Group investment expertise can be focused in governance committee of pooling vehicle

3.2 Better use of management time

3.3 De-duplication of investment consulting advice

Pooling vehicle has a clear advantage (if not outweighed by disadvantages)

4. Reduction in dealing costs

4.1 Each pension fund will have to buy or sell investments separately

4.2 In some cases, one pension fund will be selling the same shares (to raise cash) at the same time as the other pension fund is buying shares

4.1 Transactions are, by definition, aggregated via pooling vehicle

4.2 Funds wishing to withdraw cash can net against funds wishing to invest cash with only the net position then giving rise to a transaction external to the pooling vehicle in buying or selling investments

Pooling vehicle has a clear advantage

9

Part 1: Introduction: But watch out for potential inefficiencies

– Pooling may increase legal compliance responsibilities and risk due to overlay of different legal systems (e.g., E.U. IORP and U.S. ERISA); complicates administration of pooling vehicle and increases legal risk and cost

– Possible disconnect between local country finance and HR functions and parent entity personnel responsible for pooling vehicle investment decisions

– Concentration of assets within the pooling vehicle structure could decrease diversification and increase risk exposure in a turbulent economy

– Not a “holy grail”; can’t freely apply overfunding in one plan to offset liability in another

10

Part 2:

Introduction to types of

pooling vehicles

11

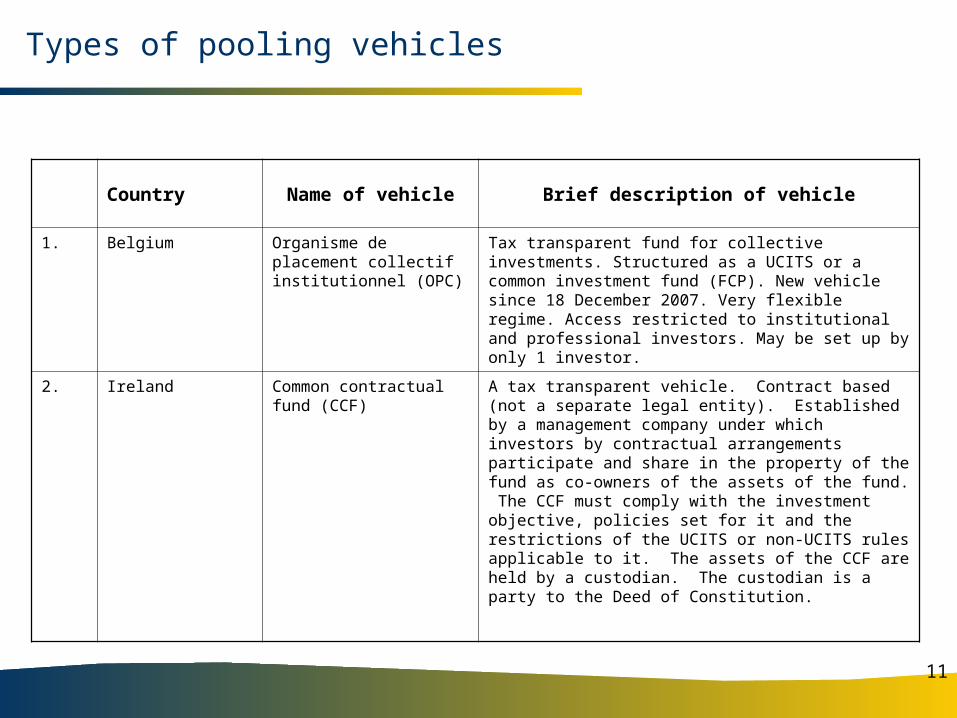

Types of pooling vehicles

Country Name of vehicle Brief description of vehicle

1. Belgium Organisme de placement collectif institutionnel (OPC)

Tax transparent fund for collective investments. Structured as a UCITS or a common investment fund (FCP). New vehicle since 18 December 2007. Very flexible regime. Access restricted to institutional and professional investors. May be set up by only 1 investor.

2. Ireland Common contractual fund (CCF)

A tax transparent vehicle. Contract based (not a separate legal entity). Established by a management company under which investors by contractual arrangements participate and share in the property of the fund as co-owners of the assets of the fund. The CCF must comply with the investment objective, policies set for it and the restrictions of the UCITS or non-UCITS rules applicable to it. The assets of the CCF are held by a custodian. The custodian is a party to the Deed of Constitution.

12

Types of pooling vehicles (cont'd)

Country Name of vehicle Brief description of vehicle

3. Luxembourg Fonds commun de placement (FCP)

Tax transparent fund for collective investment.

Contract based (not a separate legal entity). Established by a management company under which investors by contractual arrangements participate and share in the property of the FCP as co-owners of the assets of the FCP (but the co-owners have limited liability in the sense that they can only lose the amount invested in the FCP). The assets of the FCP are held by a custodian which is normally party to the management regulations as its appointment by the management company is a pre-condition for any participant subscribing in it.

Note: Can be established:– under Part I of the Luxembourg law of 20th December, 2002 regarding undertakings for collective investment to qualify as an Undertaking for Collective Investment in Transferable Securities ("UCITS") under the EU Directive 85/611/EC (as amended), or– under Part II of the 2002 law, or– under the law of 13th February, 2007 regarding Specialised Investment Funds.

13

Types of pooling vehicles (cont'd)

Country Name of vehicle Brief description of vehicle

4. The Netherlands Fonds voor Gemene Rekening (FGR)

Tax transparent mutual fund for collective investments

5. UK Pension fund pooling vehicle (PFPV)

See Note 1

Must be established as a trust which would amount to a "unit trust scheme" (but which is then de-natured as a unit trust scheme for tax purposes by the Income Tax (Pension Funds Pooling Schemes) Regulations 1996. Unitholders are limited to UK registered pension schemes, "Section 615 funds" and recognised overseas pensions schemes. Operator (usual trustee) of a PFPV will require authorisation to undertake this activity under the Financial Services and Markets Act 2000 . In practice, cannot invest directly in land or buildings, tangible assets (e.g. works of art or gold bars) or insurance contracts

Investments in limited partnerships may be possible so long as the property of the limited partnership is one in which a PFPV could invest in directly

Note 1: The PFPV has not, in practice, been used for a cross-border pension fund asset pooling and so is not considered further (because of problems with tax transparency in relation to non-UK investments and non-UK tax authorities.

14

Types of pooling vehicles (cont'd)

Country Name of vehicle Brief description of vehicle

6. USA – No specific vehicle for cross-border pension investing has been established; no prohibition against cross-border pooled investments exists either. See Note 2.– U.S. employers typically use a master trust to commingle assets of group’s U.S. plans for investment.– Some U.S. based global custodians are developing vehicles for global pooling.

– In the master trust structure, an ERISA fiduciary (typically an investment committee appointed by the parent entity) directs the master trustee as to the sub-funds to be established, appoints the investment manager of each sub-fund and allocates assets on a plan by plan basis among the sub-funds. All of the assets in the master trust are treated as “plan assets” under ERISA– A recent Advisory Opinion published by the U.S. Department of Labor has been referenced as evidencing regulatory approval of a new cross-border investment vehicle. Others assert that the Advisory Opinion represents no change. For a U.S. multinational entity, the developing global pooling structure adopts a “safe harbor” approach treating all commingled subfunds as subject to ERISA, e.g.

ERISA’s “indicia of ownership” rules restrict how investments may be held outside of the U.S.;ERISA’s “plan asset” rules apply;ERISA’s prohibited transaction rules apply; andall managers of the sub-funds are “investment managers” as defined under ERISA.

Note 2: A US master trust may only hold assets of certain US retirement arrangements (i.e. code section 401(a) tax qualified plans, IRAs and governmental plans) to benefit from US tax exemptions

15

Part 3:

Legal and tax constraints

16

Legal and tax constraints: overview

– Can the pension fund invest in the pooling vehicle?– Restrictions on marketing the pooling vehicle to the

pension fund– Constraints imposed by the legal structure of the

pooling vehicle– Constraints imposed by the regulatory regime of the

country of establishment of the pooling vehicle– Tax hurdles– Legal risk

17

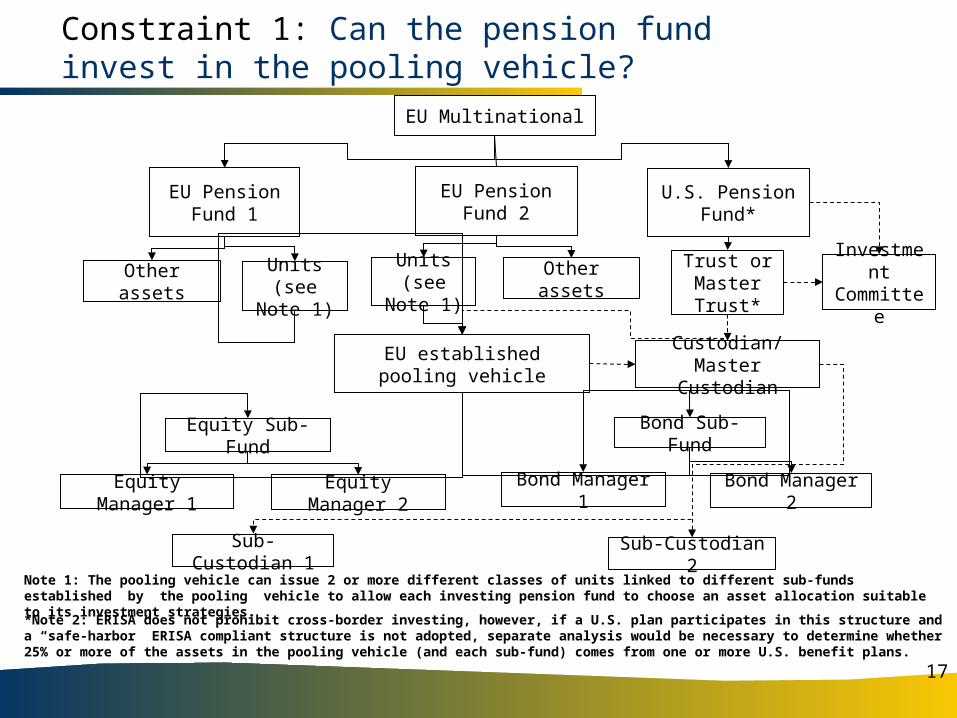

Constraint 1: Can the pension fund invest in the pooling vehicle?

EU PensionFund 1

EU Pension Fund 2

Other assets Units (see Note 1)

EU established pooling vehicle

Custodian/Master Custodian

*Note 2: ERISA does not prohibit cross-border investing, however, if a U.S. plan participates in this structure and a “safe-harbor” ERISA compliant structure is not adopted, separate analysis would be necessary to determine whether 25% or more of the assets in the pooling vehicle (and each sub-fund) comes from one or more U.S. benefit plans.

Note 1: The pooling vehicle can issue 2 or more different classes of units linked to different sub-funds established by the pooling vehicle to allow each investing pension fund to choose an asset allocation suitable to its investment strategies.

Other assetsUnits (see Note 1)

EU Multinational

U.S. Pension Fund*

Trust or Master Trust*

Bond Sub-Fund

Bond Manager 2Bond Manager 1

Sub-Custodian 2

Equity Sub-Fund

Equity Manager 2Equity Manager 1

Sub-Custodian 1

Investment Committee

18

Constraint 1: Can the pension fund invest in the pooling vehicle? (cont'd)

* A Qualifying Investor Fund where the minimum investment is €250,000 and the investor has assets of €25,000,000.

Country of establishment of pension fund

Restrictions as to type of

investment that may be held

Restrictions as to percentage of

portfolio invested in particular investments

Currency restrictions

Other

1. Belgium None specific – prudent man rule

UCITS – restrictions may be applicable

Investments in the sponsoring company: max 5%

Maximum 10% in companies belonging to same group

None No

2. Ireland None if QIF*

Yes, if UCITS (limitations under UCITS Directives – e.g. no property or commodities)

QIF – None

UCITS – investment restrictions

None No

19

Constraint 1: Can the pension fund invest in the pooling vehicle? (cont'd)

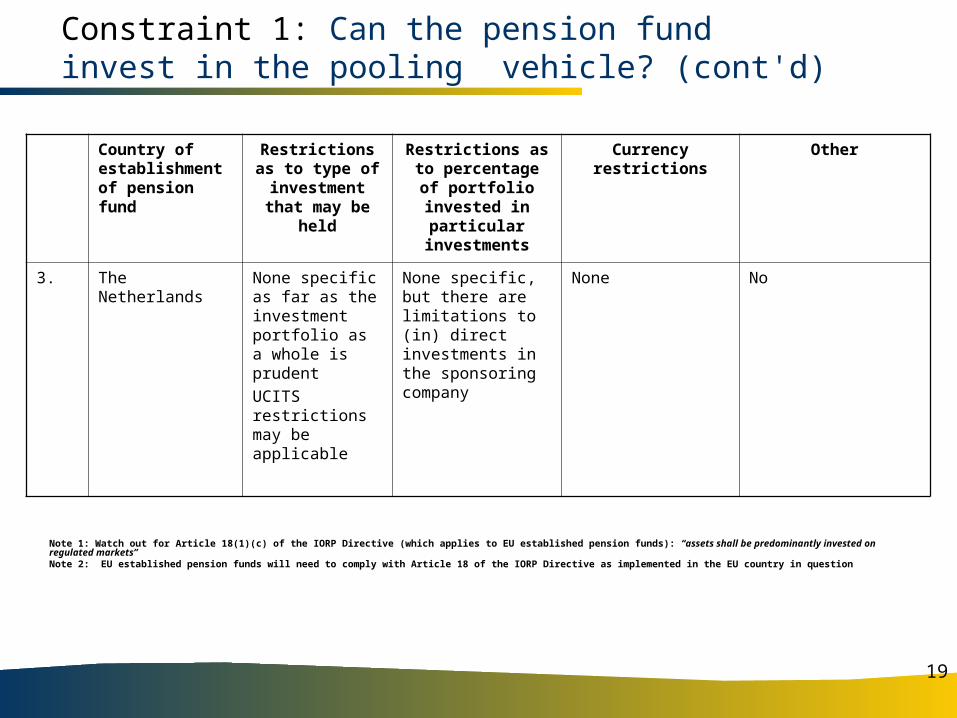

Note 1: Watch out for Article 18(1)(c) of the IORP Directive (which applies to EU established pension funds): “assets shall be predominantly invested on regulated markets”Note 2: EU established pension funds will need to comply with Article 18 of the IORP Directive as implemented in the EU country in question

Country of establishment of pension fund

Restrictions as to type of

investment that may be held

Restrictions as to percentage of

portfolio invested in particular investments

Currency restrictions

Other

3. The Netherlands None specific as far as the investment portfolio as a whole is prudent

UCITS restrictions may be applicable

None specific, but there are limitations to (in) direct investments in the sponsoring company

None No

20

Constraint 1: Can the pension fund invest in the pooling vehicle? (cont'd)

Note 1: Watch out for Article 18(1)(c) of the IORP Directive (which applies to EU established pension funds): “assets shall be predominantly invested on regulated markets”Note 2: EU established pension funds will need to comply with Article 18 of the IORP Directive as implemented in the EU country in question

Country of establishment of pension fund

Restrictions as to type of

investment that may be held

Restrictions as to percentage of

portfolio invested in particular investments

Currency restrictions

Other

4. UK None specific – prudent person rule applies. However, necessary to make sure that general restrictions imposed by Article 18 of IORP Directive (2003/41/EC) as implemented into UK legislation

None specific, but there are limitations to (in) direct investments in the sponsoring company (including person connected or associated with a sponsoring company)

None No

21

Constraint 1: Can the pension fund invest in the pooling vehicle? (cont'd)

Country of establishment of pension fund

Restrictions as to type of

investment that may be held

Restrictions as to percentage of

portfolio invested in particular

investments

Currency restrictions

Other

5. US ERISA fiduciaries have a duty to act prudently (a comparable fiduciary standard); no specific statutory or regulatory list of approved investments a plan may hold

ERISA fiduciaries have a duty to diversify plan investments; there are no specific statutory or regulatory restrictions as to the percentage of a portfolio that can be invested in particular assets

There are no specific currency restrictions, but ERISA fiduciaries are subject to fiduciary standards of prudence, diversification, etc

– A pooling vehicle and commingled sub-funds may be subject to ERISA if 25% or more of their respective assets are attributable to U.S. pension plans– Some multinational employers with U.S. parent companies have unilaterally adopted a structure whereby all assets invested via the pooling vehicle are treated as subject to ERISA (a “safe harbor” approach)

22

Constraint 1: Can the pension fund invest in the pooling vehicle?

Country of establishment of pension fund

Amend statement of investment principles?

Obtain investment advice

Other regulatory requirements

Comment

1. Belgium Probably, depends upon content of strategic investment plan of the fund

No If SIP to be amended: prior advice of works council, health committee or trade union delegation of sponsoring company

2. Ireland Yes Yes Not on fund's side

3. The Netherlands Probably, depends upon content of strategic investment plan of the fund

No No

4. UK Yes Yes (Section 36 of the Pensions Act 1995)

Comply with UK Financial Services and Markets Act 2000: Needs to be a strategic decision (not day to day) or fall within "with advice" exception

Due process to follow before investing:

23

Constraint 1: Can the pension fund invest in the pooling vehicle? (cont'd)

Country of establishment of pension fund

Amend statement of investment principles?

Obtain investment

advice

Allocation of Fiduciary Responsibility

5. USA Prudence, diversification and other requirements must be satisfied. This requires appropriate process and consideration including, for example, adopting appropriate investment guidelines

The sub-funds should be managed by an “investment manager” as defined under ERISA. Also, the “management company” could be an ERISA fiduciary

Under ERISA, fiduciary responsibility can attach by designation or by operation. U.S. pension plans typically designate a “named fiduciary” to establish the plan’s investment structure, asset allocation, selection of managers, etc– For a U.S. multinational, it is logical for: (i) the global custodian function being exercised by the “master trustee” to be expanded as described herein; and (ii) the model for the pooling vehicle structured to comply at all levels with ERISA. In addition, note that: if a U.S. plan designates a U.S. named fiduciary, but actual investment control of its assets is exercised by non-U.S. corporate executives, these non-U.S. individuals also could have ERISA fiduciary responsibility and potential liability if the U.S. plan designates non-U.S. corporate individual or entity as its named fiduciary, the designee will be subject to ERISA fiduciary standards with respect to the decision to invest through the pooling vehicle

Due process to follow before investing:

24

Constraint 2: Restrictions on marketing the pooling vehicle to the pension fund

Restrictions on marketing the pooling vehicle to the pension fund

Comment

1. Belgium No Pension funds = institutional investors

Shares of OPC must be and remain registered.

2. Ireland No restriction for company sponsored CCF. Third Party marketing QIFs would have to be privately placed pursuant to local private placement rules. UCITS would have to be registered for sale in the relevant jurisdictions

Irish funds have been privately placed worldwide

3. Luxembourg UCITS requirement to comply with local marketing rules/ restrictions applicable in the countries of distribution. Luxembourg law restrictions apply if marketed to Luxembourg established pension funds

3.1 No additional Luxembourg law restrictions apply to marketing the UCITS to pension funds established in countries outside of Luxembourg.

3.2 If the pension fund pooling vehicle was to be marketed also to a pension fund established in Luxembourg, there is unlikely to be any additional restrictions, as the contact would be a one to one contact.

25

Constraint 2: Restrictions on marketing the pooling vehicle to the pension fund (cont'd)

Restrictions on marketing the pooling vehicle to the pension fund

Comment

4. The Netherlands No For example, assets of the Italian Pensplan are invested in closed FGR of the APG Group

5. UK Financial Services Market Act 2000, Sections 21 and 238 includes restrictions on invitations to invest in collective investment schemes or otherwise engage in investment activity. Necessary to fall within exemption available for issue of promotional materials to "high value trust"

The pooling vehicle will generally be a collective investment scheme for UK Financial Services and Markets Act 2000 purposes

High value trusts are those with assets in excess of £10 million

6. USA There are no statutory or regulatory restrictions on marketing investments to pension plans. The decision to invest the pension plan’s assets in the pooled vehicle would be a fiduciary decision under ERISA

Marketing typically is considered in the context of managers seeking investment by the U.S. plan in their products

Note: The general rule is that country of location of pension fund sets the rules on marketing restrictions to that pension fund.

26

Constraint 3: Constraints imposed by the legal structure of the pooling vehicle

Country of establishment of pension fund

Does the vehicle have a separate

legal personality?

Is the vehicle tax

transparent?

Restrictions on operation

of pooling vehicle

Nature of supervisory regime

In specie transfers in

and out allowed?

1. Belgium FCP: no

UCIT: yes

FCP: Yes – exempt from corporate income tax on income and/or capital gains.

UCIT: Yes

No quantitative limits or risk-spreading rules apply. Permitted investment assets restricted to financial instruments and liquid assets (should be broadened in near future). See Deed of Constitution.

No direct prudential control by CBFA (indirect control through control on custodian, management firm of OPC and pension fund – direct control on scope of activities: no public offers)

Registration with Belgian Tax Ministry (no control on content of documents)

External auditor/ audit firm

Yes, possible subject to contractual provisions

2. Ireland No Yes Deed of Constitution will set these out

IFSRA (Irish statutory regulator of financial services industry)

Yes

27

Constraint 3: Constraints imposed by the legal structure of the pooling vehicle (cont'd)

Country of establishment of pension fund

Does the vehicle have a separate legal personality?

Is the vehicle tax

transparent?

Restrictions on operation of

pooling vehicle

Nature of supervisory

regime

In specie transfers in and

out allowed?

3. Luxembourg No. Yes, from a Luxembourg perspective and accepted as such in the main jurisdictions

Deed of constitution will set these out

CSSF (Commission de Surveillance du Secteur Financier)

Yes

28

Constraint 3: Constraints imposed by the legal structure of the pooling vehicle (cont'd)

Country of establishment of pension fund

Does the vehicle have a separate legal personality?

Is the vehicle tax

transparent?

Restrictions on operation of

pooling vehicle

Nature of supervisory

regime

In specie transfers in and

out allowed?

4. The Netherlands

No, based on contractual arrangement

Yes Deed of Constitution will set these out

Possible supervision by AFM (Authority Financial Markets) and DNB (Dutch Central Bank) if it involves outsourcing by Dutch pension funds

No supervision if participation is only offered to qualified investors within the meaning of the Prospectus Directive

Yes, possibly made subject to approval of other participants

29

Constraint 3: Constraints imposed by the legal structure of the pooling vehicle (cont'd)

Country of establishment of pension fund

Does the vehicle have a separate

legal personality?

Is the vehicle tax

transparent?

Restrictions on operation of

pooling vehicle

Nature of supervisory

regime

In specie transfers in and

out allowed?

5. USA There is no separate vehicle under US law designed for cross-border pooling of pension assets.

A US master trust may only hold assets of certain US retirement arrangements (i.e. code section 401(a) tax qualified plans, IRAs and governmental plans to benefit from US tax exemptions

Yes; the pooling vehicle should be transparent (e.g. a partnership for U.S. tax purposes)

Pension plans participating in the master trust must be limited to US plans to benefit from tax exemption available for master trust (see Note 1)

N/A; if considered to hold plan assets, pooling vehicle will be subject to ERISA.

ERISA (the Internal Revenue Code for tax considerations)

Yes, but subject to prohibited transaction* rules under ERISA and the Internal Revenue Code

*Securities and other laws also can be applicable

Note 1: A US master trust may only hold assets of certain US retirement arrangements (i.e. code section 401(a) tax qualified plans, IRAs and governmental plans) to benefit from US tax exemptions

30

Constraint 4: Constraints imposed by the regulatory regime of the country of establishment of the pooling vehicle

Country of establishment of pension fund

Minimum capital

requirement

Authorisation for starting business?

Need for prospectus/

listing particulars?

Limits on controls

available to sponsoring employer

Limits on controls

available to investors

Governance structure

1. Belgium None None – Upon confirmation of its registration with Belgian Tax Ministry

No – Information brochure is enough

Through pension fund and SIP

See contract/ Deed of constitution

Deed of constitution – Board of Directors or Manager - Custodian

2. Ireland QIF: €250,000 – minimum investment; €25m per investor. UCITS: no minimum investment

IFSRA approval*

Yes, prospectus

Usually imposed under Deed of Constitution

Usually imposed under Deed of Constitution

Deed of Constitution – Board of Directors of Management Company

*Changes to structure require prior approval, e.g. Investment Managers

31

Constraint 4: Constraints imposed by the regulatory regime of the country of establishment of the pooling vehicle (cont'd)

Country of establishment of pension fund

Minimum capital

requirement

Authorisation for starting business?

Need for prospectus/

listing particulars?

Limits on controls

available to sponsoring employer

Limits on controls

available to investors

Governance structure

3. Luxembourg Minimum net assets € 1,250,000 (to be reached within 6 months of authorisation)

CSSF must authorise the Management Company of the FCP.

CSSF must approve the Deed of Constitution

Yes. Prospectus required

Usually imposed under Deed of Constitution. But direct control not usually possible

Deed of Constitution

Board of directors of Management Company

4. The Netherlands

None None No Custodian is in control

If separate custodians, segregated liability

General assembly and Manager-Custodian

5. USA

No global pooling vehicles developed under U.S. law.

N/A N/A N/A N/A N/A N/A

32

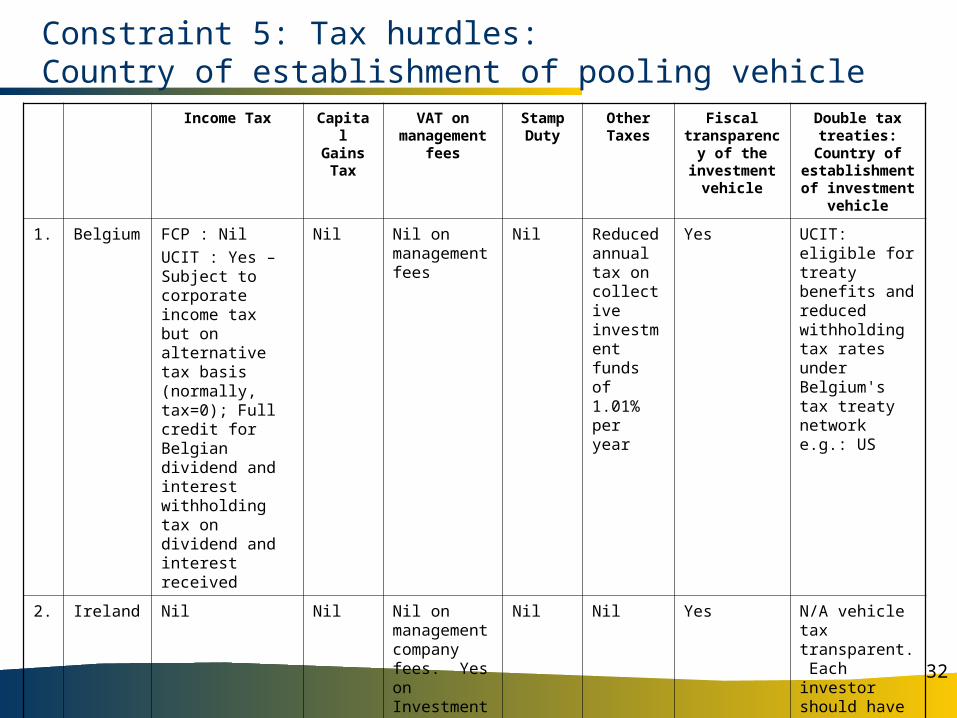

Income Tax Capital Gains Tax

VAT on management

fees

Stamp Duty

Other Taxes

Fiscal transparency

of the investment

vehicle

Double tax treaties:

Country of establishment of investment

vehicle

1. Belgium FCP : Nil

UCIT : Yes – Subject to corporate income tax but on alternative tax basis (normally, tax=0); Full credit for Belgian dividend and interest withholding tax on dividend and interest received

Nil Nil on management fees

Nil Reduced annual tax on collective investment funds of 1.01% per year

Yes UCIT: eligible for treaty benefits and reduced withholding tax rates under Belgium's tax treaty network e.g.: US

2. Ireland Nil Nil Nil on management company fees. Yes on Investment Managers fees

Nil Nil Yes N/A vehicle tax transparent. Each investor should have to look to tax treaties of its own home jurisdiction

Constraint 5: Tax hurdles: Country of establishment of pooling vehicle

33

Constraint 5: Tax hurdles: Country of establishment of pooling vehicle (cont'd)

Income Tax

Capital Gains Tax

VAT on management

fees

Stamp Duty

Other Taxes Fiscal transparency

of the investment

vehicle

Double tax treaties:

Country of establishment of investment

vehicle

3. Luxembourg Nil Nil Exempt (as management services in relation to collective investment scheme)

Nil Capital duty, previously €1,250, was abolished with effect from 1st January, 2009

Taxe d'abonment:

(a) Exemption if only pension funds of companies in the same corporate group invest (but see Note 1)

Yes, in Luxembourg. But need to check position of local tax authorities of:- investors,

and- investment

FCP does not benefit from Luxembourg double tax treaties if it is accepted as tax transparent

Instead, investors/ investments need to look at double tax treaties between country of investor and country of investment

Note 1: If the pooling vehicle is established as a SIF, exemption will also apply if investors are all pension funds (whether or not in the same group).

34

Income Tax Capital Gains Tax

VAT on management

fees

Stamp Duty

Other Taxes

Fiscal transparency

of the investment

vehicle

Double tax treaties: Country of establishment

of investment vehicle

Luxembourg (cont'd)

(b) 0.01% p.a., if only pension funds (not falling in (a) above) invest, payable quarterly on net asset value FCP

4. The Netherlands

Nil Nil Exempt from VAT if management services collective investment funds

Nil Nil Yes Treaties with Austria, Belgium, Denmark, Norway, South Africa, UK and Taiwan. Memorandum of understanding with US

Constraint 5: Tax hurdles: Country of establishment of pooling vehicle (cont'd)

35

Income Tax Capital Gains Tax

VAT on management

fees

Stamp Duty

Other Taxes

Fiscal transparency

of the investment

vehicle

Double tax treaties: Country of establishment

of investment vehicle

5. USA N/A; but note that US income tax could apply at the US trust level if a sub-fund engages in transactions involving leverage or active operation of a business (rather than passive investment)

N/A N/A N/A N/A Should qualify under US tax rules (e.g., as a partnership)

Check tax treaties between country of plan and country of investment with respect to taxes at the subfund level, e.g., (withholding of dividends at the source)

Constraint 5: Tax hurdles: Country of establishment of pooling vehicle (cont'd)

36

Constraint 5: Tax hurdles (cont'd)The existing position

EquitiesEquities

Belgium Ireland The Netherlands UK US Belgium Ireland The

Netherlands UK US

Taxes in country of investor?

Taxes in country of investment?

PensionFund 1

PensionFund 2

37

Constraint 5: Tax hurdles (cont'd)The position on investment pooling

The Netherlands

Units Units

Pooling vehicle

Equities

Belgium Ireland USUK

Taxes in country of investor?

Taxes in country of pooling vehicle?

Taxes in country of investment?

PensionFund 1

PensionFund 2

38

Constraint 6: Legal risk Country of establishment of pension fund

Assets more remote (custody, monitoring

and reporting)

Extra country risk (nationalisation/

expropriation, exchange control)

Complexity

1. Belgium In theory, yes. But, in practice, no.

In theory, yes. But, in practice, no (at least in normal circumstances)

Not particularly complex

2. Ireland In theory, yes. But, in practice, no.

In theory, yes. But, in practice, no (at least in normal circumstances)

Not particularly complex

3. The Netherlands In theory, yes. But, in practice, no.

In theory, yes. But, in practice, no (at least in normal circumstances)

Not particularly complex

4. UK In theory, yes. But, in practice, no.

In theory, yes. But, in practice, no (at least in normal circumstances)

Not particularly complex

5. USA If plan assets and ERISA applies, indication of ownership and other requirements must be met.

Fiduciary making decision is subject to prudence and other ERISA standards.

ERISA is complex; with Internal Revenue Code and other legal overlaps.

39

EquitiesEquities

Belgium IrelandThe

Netherlands UK US Belgium Ireland UK US

Constraint 6: Legal risk (cont'd)The existing position

PensionFund 1

PensionFund 2

The Netherlands

40

The Netherlands

Units Units

Pooling vehicle

Equities

Belgium Ireland USUK

Constraint 6: Legal risk (cont'd)The position on investment pooling

EU PensionFund 1

EU PensionFund 2

Legal risk: Country of investor

Legal risk: country of establishment of pooling vehicle

Legal risk: country of location of investment

41

Conclusions

– Cross-border pension fund asset pooling has happened (e.g. Unilever Group Pension Funds)

– Easier to achieve than cross-border pension fund asset and liability pooling (at least for legacy pension funds)

– So long as pooled assets are sufficiently large, efficiencies are available

– Possible to achieve improvements in governance for the participating group pension funds through better concentration of available expertise within the sponsoring employer group

– Additional compliance and administration to the extent plans subject to other legal systems (e.g. U.S. and ERISA) are to be included in the global pooling structure