workshop slovenian gas market in the region - plinovodi.si · stogit services 21 services contract...

TRANSCRIPT

Workshop Slovenian Gas Market in the Region

Ljubljana, 4th april 2018

Agenda

1. Snam at a glance

2. Italian natural gas transportation infrastructure

3. Network capacities

4. Natural gas transportation

5. Natural gas storage

6. Regasification

Snam at a glance

Agenda

1.

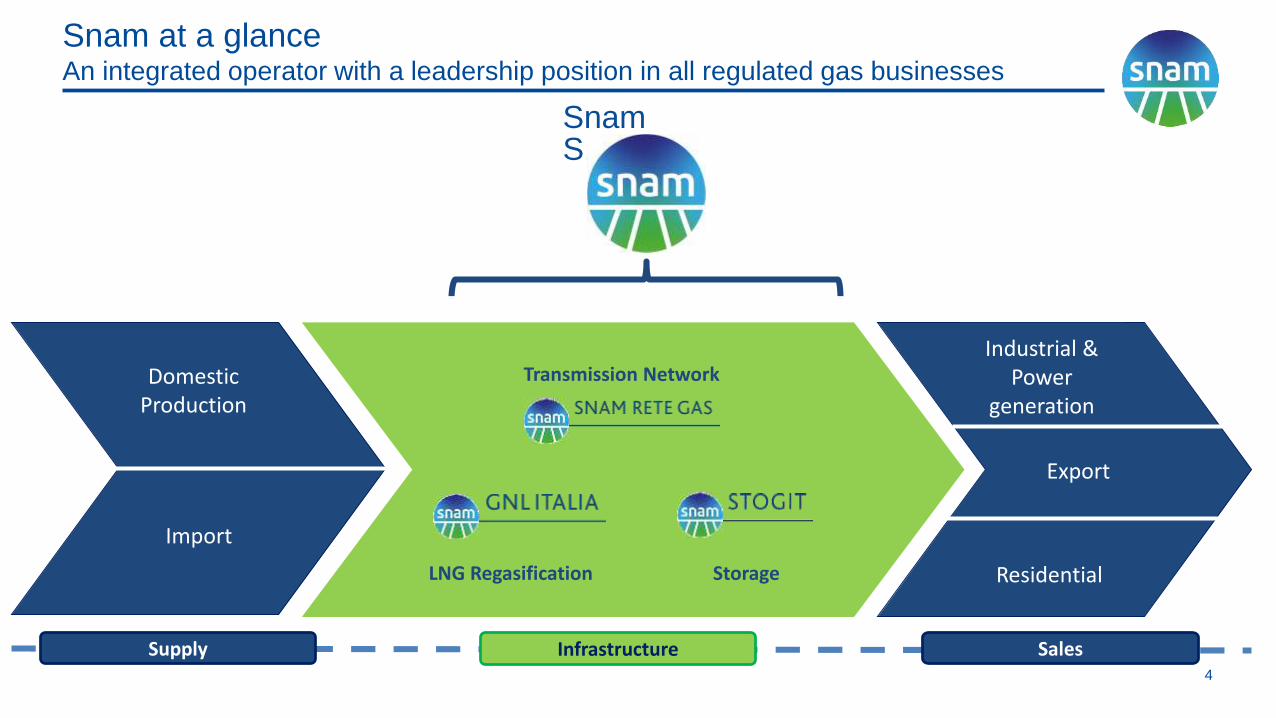

Snam at a glanceAn integrated operator with a leadership position in all regulated gas businesses

4

Snam S.p.A.

Industrial & Power

generation

Export

Residential

Stoccaggio Trasporto e dispacciamento

Rigassificazione StorageLNG Regasification

Sales

DomesticProduction

Import

Transmission Network

InfrastructureSupply

Snam at a glanceSnam international development

5

International assets

Domestic pipelinesLNG Terminals

100 % in IUK owned through a 24-

76 JV with Fluxys

• 235 km subsea natural

gas pipelines between

Bacton (UK) and

Zeebrugge (Belgium), 40

inches diameter

• 1 receiving terminal and

compression station in

Bacton

• 1 receiving terminal and

4 compressors in

Zeebrugge

40.5% participation in TIGF

• 5,000 km transmission

network, 14% of France

gas transmission grid

• Total storage capacity of

around 5.7 bcm, ca. 20%

of French capacity

20.0% participation in TAP

• 880 km transmission network

84.47% participation in TAG

• 1,140 km transmission network

• 5 compression stations

19.6% participation in GCA

• 900 km transmission network

• 5 compression stations

15.5% participation in Prisma

Italian natural gas Infrastructures

Agenda

2.

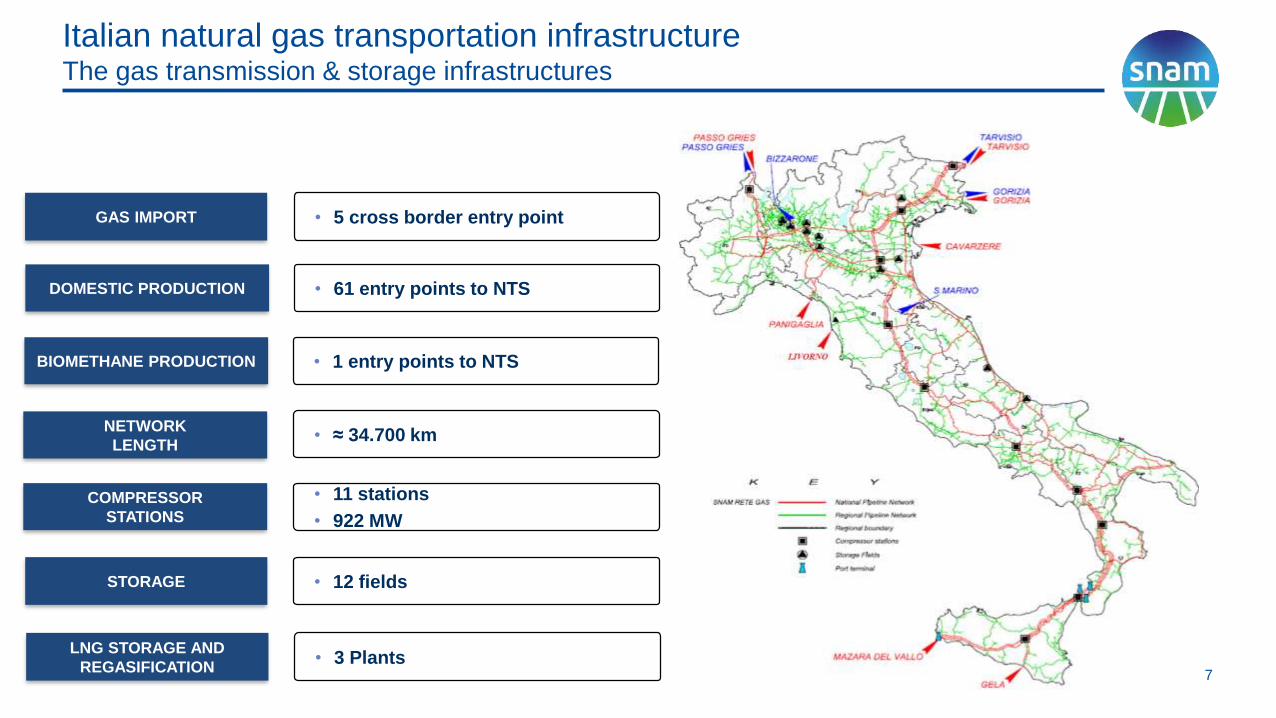

Italian natural gas transportation infrastructureThe gas transmission & storage infrastructures

7

• 5 cross border entry point

• 61 entry points to NTS DOMESTIC PRODUCTION

GAS IMPORT

• 11 stations

• 922 MW

COMPRESSOR

STATIONS

• ≈ 34.700 kmNETWORK

LENGTH

• 12 fieldsSTORAGE

• 1 entry points to NTS BIOMETHANE PRODUCTION

• 3 PlantsLNG STORAGE AND

REGASIFICATION

Network capacities

Agenda

3.

Network capacitiesTY 2017/2018 capacities

9

Firm and winter interruptible capacity [MScm/d]

Entry

capacity

Exit

Capacity

IP NORTH

TARVISIO 113 18

PASSO GRIES 64,4 5

GORIZIA 4,8 4,4

IP SOUTH

MAZARA DEL

VALLO133

-

GELA -

LNG

TERMINALS

PANIGAGLIA 13 -

CAVARZERE 26,4 -

LIVORNO 15 -

Network capacitiesReverse flow project

10

Firm and winter interruptible capacity [MScm/d]

Entry

capacity

Exit

Capacity

IP NORTH

TARVISIO 11340

PASSO GRIES 64,4

GORIZIA 4,8 4,4

IP SOUTH

MAZARA DEL

VALLO133

-

GELA -

LNG TERMINALS

PANIGAGLIA 13 -

CAVARZERE 26,4 -

LIVORNO 15 -

Transportation capacity:

Capacity at the Exit Point of Passo Gries: 40 MSm3/d

from 1 October 2018 (22 MSm3/d at Passo Gries and

18 MSm3/d as competing capacity at Passo Gries and

Tarvisio)

Project DN km/MW Status

Minerbio-Poggio Renatico pipeline 1200 19 km In operation

Development Poggio Renatico compressor station 22 MW In operation

Cervignano-Mortara pipeline 1400 62 km Under construction

New Sergnano compressor station 36 MW Under construction

New Minerbio compressor station 24 MW Under construction

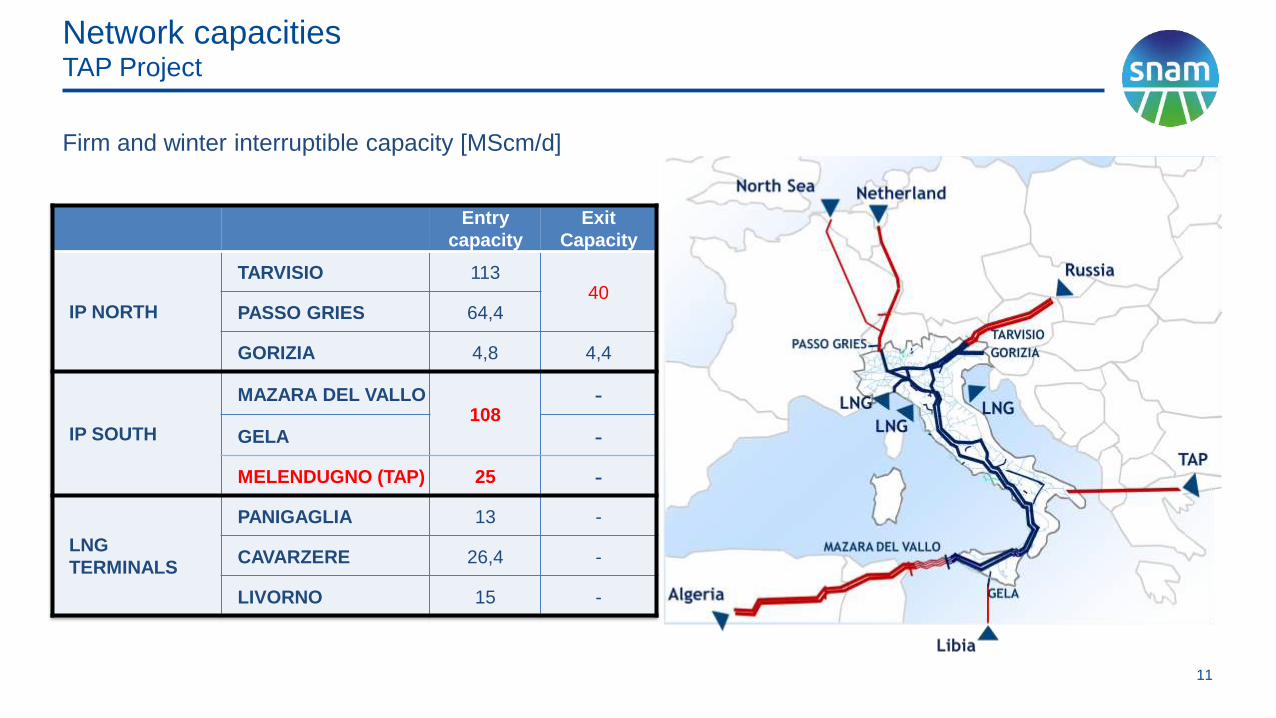

Network capacitiesTAP Project

11

Firm and winter interruptible capacity [MScm/d]

Entry

capacity

Exit

Capacity

IP NORTH

TARVISIO 11340

PASSO GRIES 64,4

GORIZIA 4,8 4,4

IP SOUTH

MAZARA DEL VALLO108

-

GELA -

MELENDUGNO (TAP) 25 -

LNG

TERMINALS

PANIGAGLIA 13 -

CAVARZERE 26,4 -

LIVORNO 15 -

Natural gas transportation

Agenda

4.

0

10

20

30

40

50

60

70

80

90

2014 2015 2016 2017 2020 2026 2030

Bill

ion S

mc

Industrial Civil Power Generation

Natural gas transportationLong term Italian gas demand

13

DomesticPower

generationIndustrial

2015 48% 32% 20%

2016 44% 33% 23%

2017 45% 35% 20%

SOURCE: ten-years network development plan of Snam 2017-2026 (high case scenario)

+9,1% +5,0% +2,2%

• Gas demand increased in the last three years

• Among European countries, Italy is the one with the highest reliance on gas, which

accounts for 35% primary energy consumption: national energy system is mainly

based on gas and renewables, with oil still essential for transport

• Gas assumes a key role in the energy transition, especially in the coal phase out

• Italy is the third European market for gas consumption (≈ 72 bcm in 2017)

Natural gas transportationBooked capacity at importation points

14

2016/2017 2017/2018 2018/2019 2019/2020 2020/2021 2021/2022 2022/2023 2023/2024

Tarvisio 95,8 94,9 69,7 10,6 10,0 - - -

Passo Gries 23,1 14,6 7,3 1,0 1,0 - - -

Gorizia - 0,1 - - - - - -

Mazara 83,8 88,9 66,2 - - - - -

Gela 23,2 18,5 10,9 10,9 10,9 10,9 10,9 10,9

Multi - Annual Capacity

Mill

ion

sm

c

• The above values are the average of the capacity booked for the whole year

• The values for Thermal Year 2017/2018 are the average of the capacity booked until the 16/03/2018

• Gorizia point is booked on a daily basis in case of particular market conditions

Natural gas transportationItalian gas market evolution

15

• From few Shippers with long-term contracts to more than one hundred Shippers making

many gas exchanges and capacity transactions

• Look at the European gas market characterized by liquidity, flexibility and security of supply

0

50

100

150

200

250

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Number of Shippers & Traders

Shipper Shipper+Trader

Natural gas transportationItalian balancing system

16

Shippers are responsible for their own balance position during the gas day through:

• 35 renomination cycles starting from 16.00 of gas day D-1 until 3.00 of gas day D at import, storage and

redelivery point;

• Gas trade on organized market.

Minimization of the actions made by the TSO for balancing the system (Residual role) through:

• Gas trade on organized market

Trading platforms:

• MGAS Platform (MI – MGP – MGS)

• Locational Market

• Virtual Trading Point (PSV)

Creation of Organized market, managed by trading platforms, in which the Market Operator (GME) is the

counterparty

Introduction of dual price for Shippers who have not balanced their positions at the end of the Gas Day:

• Selling price for Users that inject more gas than the gas withdrawal (long position)

• Purchase price for Users that withdraw more gas than the gas injected (short position)

Starting October 2016, the balancing regime foreseen into Network Balancing Code (Regulation UE n. 312/2014) has

been implemented in the Italian gas market.

Natural gas transportationItalian balancing system – SRG vs GME

17

SNAM RETE GAS

• Acts as a Balancing Responsible

• Acts as a Balancing Operator for the Network to be balanced

• Determines authorised Users that can have access to GME Platforms on the basis of: EPSU < MEPSU

• Guaranteed gas < gas in storage

• Provides Shippers the information that enables them to estimate their own balance position and how eventually fix any imbalance.

GESTORE MERCATI ENERGETICI – MGAS EXCHANGE

• Trend publication of the marginal puchase and sell price after any trade

• Allows only authorised Users to post trades on the platform

• Operates a forward physical market (MTE), a day-ahead auction market (MGP), an intraday auction market (MI)

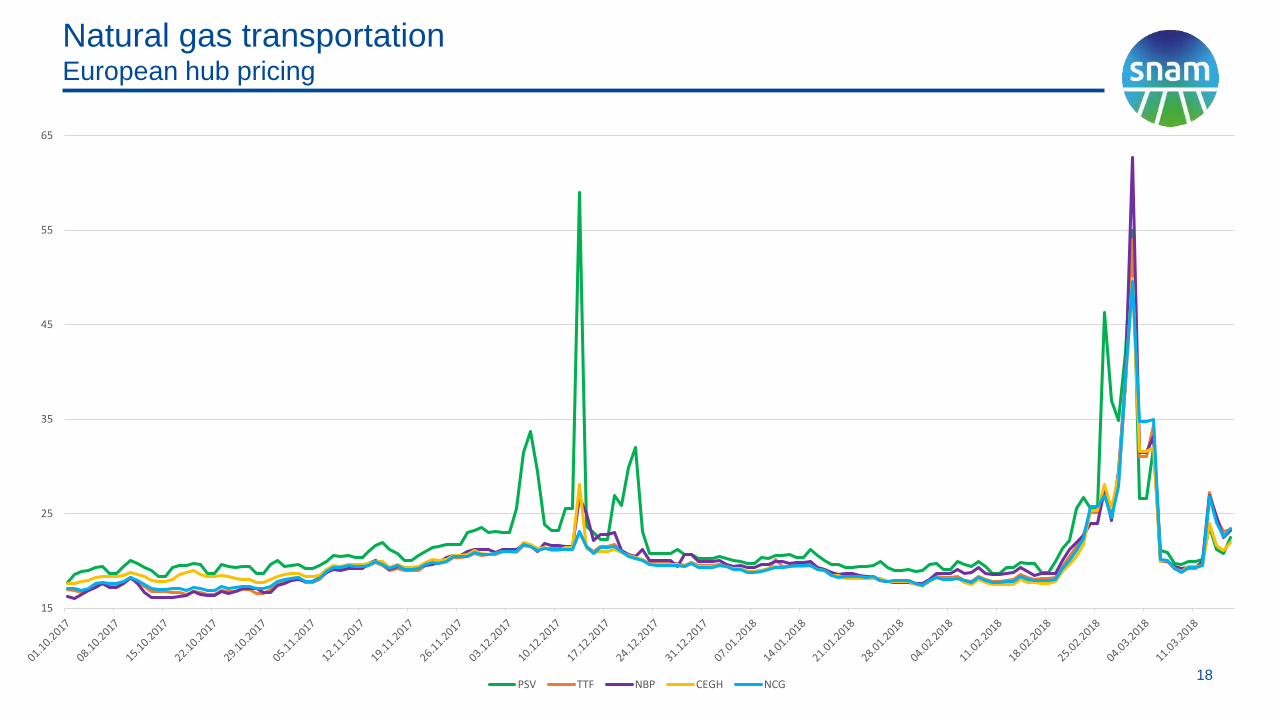

Natural gas transportationEuropean hub pricing

18

15

25

35

45

55

65

PSV TTF NBP CEGH NCG

Natural gas storage

Agenda

5.

Natural gas storageUnderground storage

20

Working gas - Thermal Year 2017/18Strategic Storage: 4.620 MScm

Modulation Service: 13.065 MScm

MSc

m/d

Natural gas storageStogit services

21

Services Contract duration Allocation methodologyType of User

Peak modulation

Seasonal / MonthlyAnnual / Infra annual

Auction

(marginal price or pay as bid)All

Peak

services

Transport network

balancingAnnual Equal to the requestNetwork operators

Hydrocarbon Annual Equal to the requestProduction concession holder

Flat modulation

Seasonal / Monthly

Multi year / Annual / Infra

annualAuction (pay as bid)All

Regasification balancing AnnualPro-rata (regasification

capacity)All

Flat

services

Short Term Capacity Monthly/Weekly/Daily AuctionAll

Strategic Storage Annual / Infra annual

No allocation / Payment of a fee

applied to the gas

imported/produced

Importer/Producer

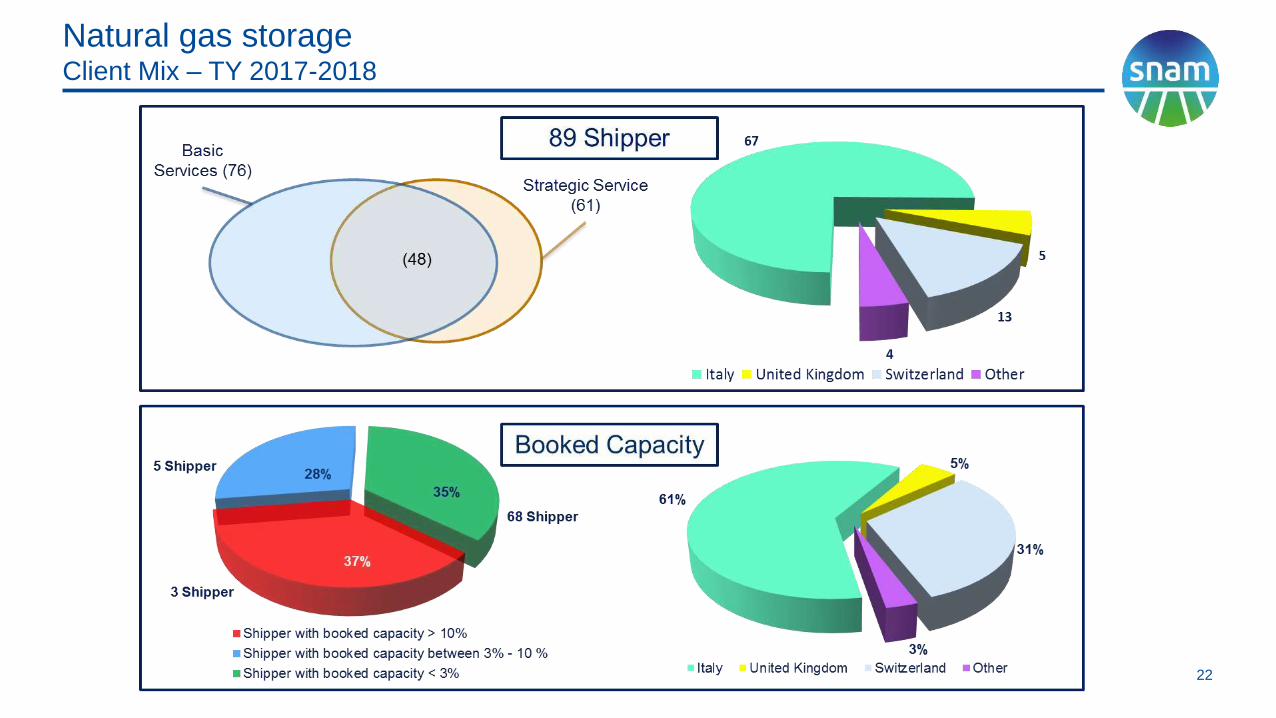

Natural gas storageClient Mix – TY 2017-2018

22

Regasification

Agenda

6.

RegasificationLNG Regasification

24

Owner: Snam

Entry into operation: 1972

Tanks capacities: 90.000 m3li

Carrier: up to 70.000 m3liq

Regasification capacity annual: ≈ 4 billion

m3

Regulated terminal

GNL Italia - On-ShoreAdriatic LNG – Gravity Based OLT – FSRU

Owner: Exxon, Qatar and Snam

Entry into operation: 2009

Tanks capacities: 250.000 m3liq.

Carrier: up to 152.000 m3li.

Regasification capacity annual: ≈ 8 billion

m3

Partially regulated terminal (20%) e

80% in TPA exemption

Owner: Iren and Uniper

Entry into operation: 2013

Tanks capacities: 137.500 m3liq

Carrier: up to 180.000 m3liq

Regasification capacity annual: ≈ 4

billion m3

Regulated terminal

RegasificationThe regasification in Italy

25

NOMINATION=ALLOCATION (Del. 312/2016)

ENTRY

RegasificationThe regasification in Italy

26

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

MW

h/d

LNG imported in 2016

Adriatic LNG OLT GNL Italia

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

MW

h/d

LNG imported in 2017

Adriatic LNG OLT GNL Italia

Contacts

27

• Montanari Claudio

National Network Programming

Tel: +39 02-370.37461

Mail: [email protected]

• Mora Alessandro

Access Contracts

Tel: +39 02-370.39043

Mail: [email protected]