world bank conference the financial sector post-crisis: challenges and vulnerabilities

DESCRIPTION

Eastern Europe, Russia and Central Asia. World Bank Conference The Financial Sector Post-Crisis: Challenges and Vulnerabilities. Scott Bugie Managing Director , Financial Services Ratings +33 (0)1.44.20.66.80 [email protected]. Washington, D.C. April 26, 2005. - PowerPoint PPT PresentationTRANSCRIPT

Scott Bugie

Managing Director, Financial Services Ratings

+33 (0)1.44.20.66.80

World Bank ConferenceThe Financial Sector Post-

Crisis: Challenges and Vulnerabilities

Washington, D.C. April 26, 2005

Eastern Europe, Russia and Central Asia

204/19/23

Global View of Emerging Market Banks

• Broadly speaking, macroeconomic environment and sectoral infrastructure have improved

• Likelihood of future banking crises has receded

• Certain banking systems remain vulnerable

• Key question: Is the improvement secular or cyclical?

304/19/23

FDI and Reduced Corporate Leverage Drive Improvement in

Credit Profile of EM Banks

Foreign Direct Investment

• Accelerated banking and securities reforms

• Brought much-needed banking know-how and capital

• Deepened globalization of world financial sector

• Promoted spread of best practices in bank supervision and risk management (although much work remains)

Reduced Coporate Leverage

• Asian corporates hit by 1997-1998 crisis deleveraged over past several years and reduced industrial overcapacity (that led to crisis)

• Certain governments set up SPVs to purchase bad assets from troubled banks to facilitate restructuring

• Mexico, Turkey, and Brazil have lower levels of debt to GDP in 2004 than at the end of the 1990s

404/19/23

Global Ranking of Emerging Market Banking Systems by Industry and

Economic Risk

* For comparison purposes; Standard & Poor’s classifies these countries as mature markets

Description of industry and economic riskand potential for problematic assets

First group -- Chile Portugal* Relatively good macro environmentGPA Range Hong Kong Singapore* Potential for AQ problems relatively lower than other emerging markets

10-20% J apan* South Africa

Second group -- Czech Republic Kuwait Satisfactory macro environment, some weaknessesGPA Range Greece* Malaysia Potential for AQ problems > than 1st group, but still limited

15-30% Hungary South Korea Israel Taiwan

Third group -- Brazil Philippines Adequate macro environment, several weaknesses but much progress as wellGPA Range Bulgaria Poland Potential AQ problems moderately high

25-40% India Saudi Arabia Mexico UAE

Fourth group -- Kazakhstan Tunisia Many weaknesses in economy and sector, but progress in some areasGPA Range Lithuania Turkey Potential high system-wide AQ problems

35-50% Thailand Venezuela

Fifth group -- Argentina Romania Significant macro weaknesses, several areas require reformGPA Range China Russia Potential very high systemic level of credit losses

50-75% Egypt UkraineIndonesia Vietnam

504/19/23

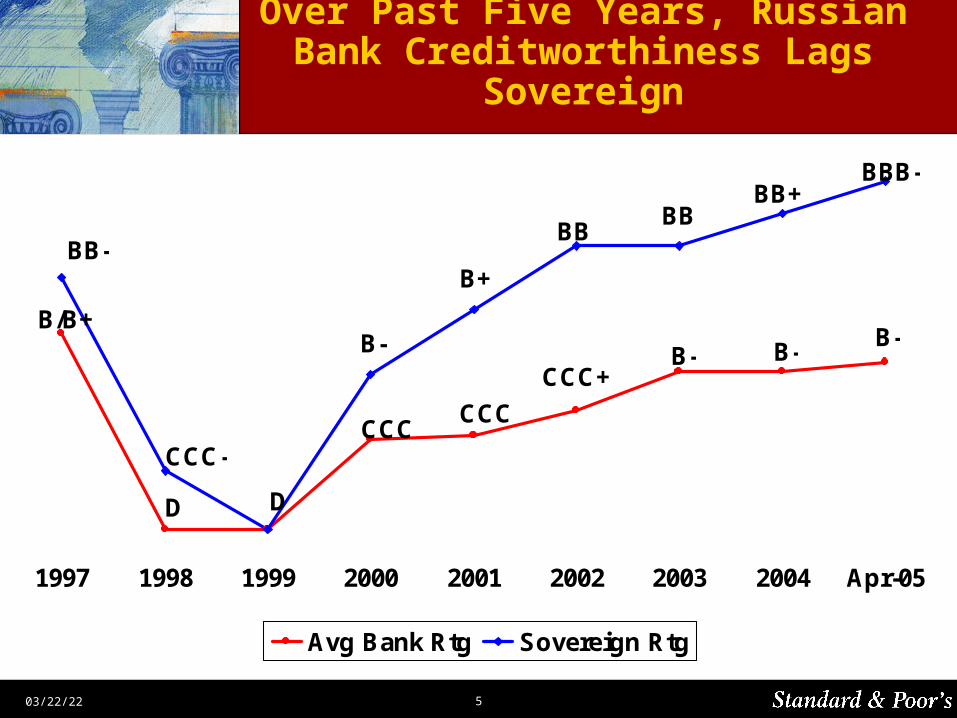

Over Past Five Years, Russian Bank Creditworthiness Lags Sovereign

1997 1998 1999 2000 2001 2002 2003 2004 Apr-05

Avg Bank Rtg Sovereign Rtg

BB-

B/B+

CCC-

D D

B-

CCC

B+

CCC

BB

B-

BB+

B-

BBB-

B-

BB

CCC+

604/19/23

Russian Banking Market Turbulence inSummer 2004

Underlying Causes

Low confidence of households and corporates in Russian banks

Interbank and Veksel (promissory notes) markets highly segmented, volatile, shallow

Prevalence of Financial Industrial Groups (FIGs) maintains mistrust

Mismatch between long-term assets and short-term liabilities

Concentrations in funding Downturn in Russian securities markets (starting April ’04) CBR’s policy to clean-up banking sector, with policy of

withdrawing licenses

704/19/23

Russian Bank FailuresMay – August 2004

Bank name Date of license withdrawal

Total assets mid-2004

Sodbusinessbank May 13, 2004 $245 mln

Novocherkassky Gorodskoy Bank

May 28, 2004 N.A.

Kredittrust Bank July 24, 2004 $234 mln

Guta Bank * $1,224 mln

Promeximbank July 29, 2004 $59 mln

Moszhylstroybank July 29, 2004 $52 mln

Commercial Savings Bank

July 29, 2004 N/A

RIKOM Commercial Bank July 29, 2004 N/A

Dialog-Optim Bank August 10, 2004 $286 mln

Bank Paveletskiy August 12, 2004 $134 mln

* Operations suspended in July 2004, but license not withdrawn

804/19/23

Russian Retail Deposit Growth in 2004

Deposits of individuals at year-end, in billions of Rubles

0

500

1000

1500

2000

2500

1999 2000 2001 2002 2003 2004

Rub

les

billi

ons

Source: Central Bank of Russia

Retail deposits approximately $70 billion at year-end 2004

904/19/23

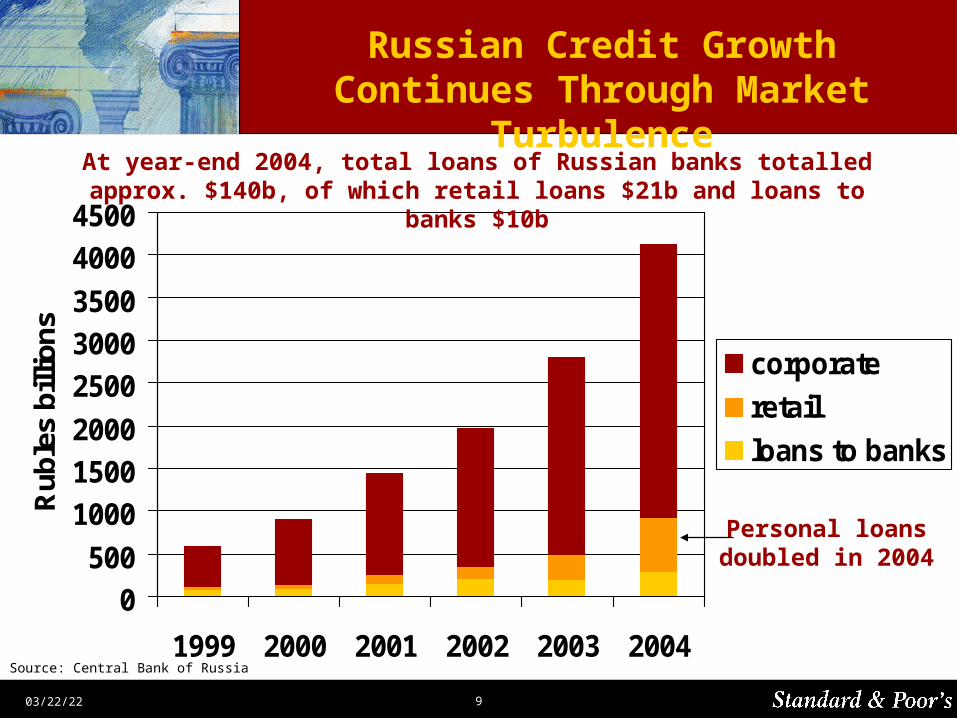

Russian Credit Growth Continues Through Market Turbulence

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1999 2000 2001 2002 2003 2004

Rub

les

bill

ion

s

corporate

retail

loans to banks

Source: Central Bank of Russia

At year-end 2004, total loans of Russian banks totalled approx. $140b, of which retail loans $21b and loans to banks $10b

Personal loansdoubled in 2004

1004/19/23

Russian Banking Industry

Effective measures and policies Tax reform has contributed to the economic boom

Reform of securities markets underpins bank business and funding

Bank deposit insurance step in right direction

Reduction in reserve requirements boosts intermediation

Remaining vulnerabilities/challenges Dominance of state banks Sberbank and VTB distorts market and

holds back its development Limited economies of scale for private sector banks Continued lack of confidence (e.g. banking market panic in 2004) High single-party and related party concentrations create risks Arbitrary legal environment undermines creditor rights Opaque ownership perpetuates lack of trust

1104/19/23

Russian Banking Sector Likely to Consolidate in Medium-term

Over 1,250 banks

No single private sector bank has a market share of more than 6%

Deposit insurance scheme may lead to exit of marginal banks

Recent M&A activity: Nikoil/Avtobank/UralSib; Rosbank/OVK; VTB/Guta; VTB/Promstroi

Key question: will FDI increase?

1204/19/23

Restructuring of Turkish Banking Sector

Comparison with Russia

At beginning of 2000, Turkish financial sector had many similarities with Russian sector of 2005:

Turkish state banks held important position, particularly in retail market

State banks (particularly Ziraat and Halk) unfair competitors for deposits

Banks relied on trading profits Several large FIGs with strong position in banking market (e.g.

Sabançi, Cukurova, Dogus, Is, Koç) Engrained practice of intragroup lending in FIGs Banks profited from large equity holdings Low level of publicly-disclosed nonperforming loans Many marginal banks with weak franchises Ineffective banking supervision

1304/19/23

Restructuring of Turkish Banking Sector

Comparison with Russia

But a few key differences of Turkish banking sector Russia at the beginning of 2000:

Turkish state banks had weak financial profiles, in contrast to Sberbank and VTB

Unlike Russian state banks, Turkish state banks distributed massive subsidies in agricultural, small business, real estate sectors

Many Turkish private sector banks had deeper experience, longer track record, better franchises than today’s Russian private sector banks

Turkey had many fewer banks (79) than Russia

1404/19/23

Massive Restructuring of Turkish Banking Sector in Past Four Years

New regulatory authority created, new banking law adopted Massive supervisory action – Regulators took over weak banks

representing 25% of sector (e.g. Pamukbank, Demirbank Iktisat, Esbank, Ticaret, Interbank, Imar Bank)

Special audit for all private banks, with stricter rules on reporting problem loans, stricter enforcement of limits on intragroup loans and single party concentrations

Number of banks reduced to 50 from 79 Government guaranteed all retail deposits (partially withdrawn this year) Loan subsidies were shifted from state banks directly to government State banks recapitalized and downsized State RE bank Emlak closed, assets transferred to Ziraat and Halk FDI is starting to build (Fortis/Disbank)

Total cost of restructuring: est. $40-50 billion, or 30% of Turkish GDP

1504/19/23

Lessons from Turkey

Clean-up of banking sector costly if problems left unattended many years

Strong, persistent regulatory actions required to break ingrained habits

Level of problem loans during an expansion is poor indicator of potential extent of problems in recession

True extent of intragroup lending difficult to assess

Intragroup exposures increase in downturn

1604/19/23

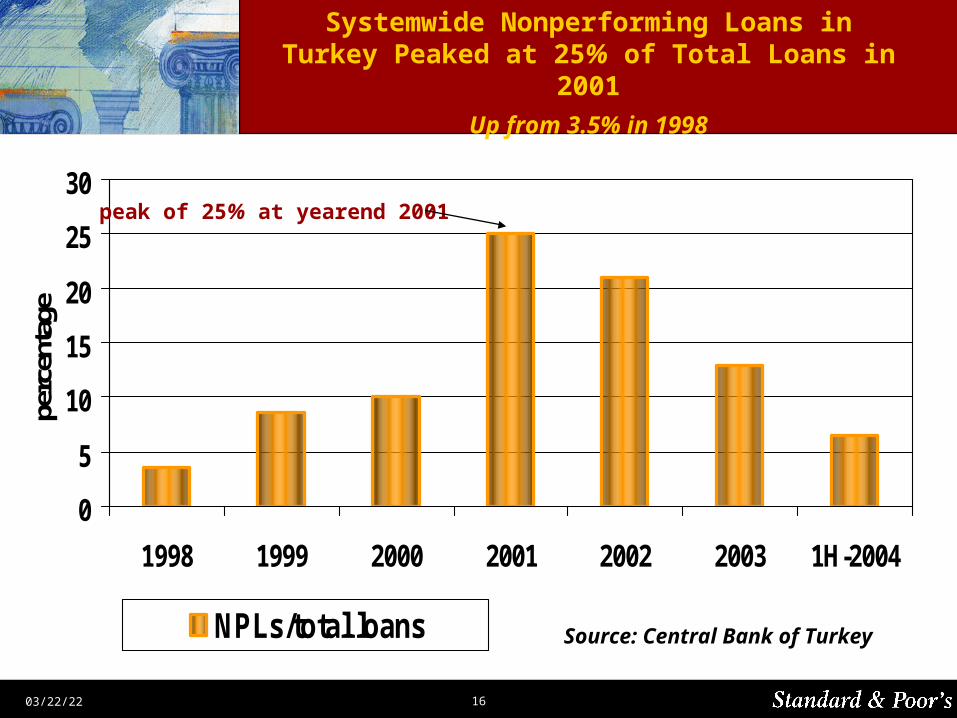

Systemwide Nonperforming Loans in Turkey Peaked at 25% of Total Loans in 2001

Up from 3.5% in 1998

0

5

10

15

20

25

30

1998 1999 2000 2001 2002 2003 1H-2004

perc

enta

ge

NPLs/total loans Source: Central Bank of Turkey

peak of 25% at yearend 2001

1704/19/23

Banking Sector Undevelopped in EEMEA

Domestic Credit to Private Sector to GDP

148 146

119

75 73

4234 32 27 22 21

15

020406080

100120140160180

(pe

rce

nta

ge

)

Source: Standard & Poor’s Data as of year-end 2003

1804/19/23

Domestic Credit to Private Sector to GDPPotential for Growth in EEMEA and LA

0

20

40

60

80

100

120

140

160

180

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Do

mesti

c c

red

it t

o p

rivate

secto

r / G

DP

China

Malaysia

Thailand

Brazil

Saudi Arabia

Poland

Russia

Mexico

Turkey

1904/19/23

Mortgage Lending in Emerging Markets Remains Undevelopped

Chart 12. Estmated Mortgage Lending to Gross Domestic Product (%)

Largest developping markets vs. U.S. and Europe

55

33

8

2 2 1 02

00

10

20

30

40

50

60

USA Eurozone China Brazil India Indonesia Russia Mexico Turkey

Source: Standard & Poor'sData as of 2002 and 2003

2004/19/23

Polish Banking Industry

Effective measures and policies Convergence of regulatory environment with EU Improvements in regulatory policy concerning problem loans (notably

statistical provisions for personal loans) Act on Bankruptcy and Remedy Proceedings strengthened creditor rights Reduction of mandatory reserve requirements

Remaining vulnerabilities /challenges Low average level of wealth High unemployment Inefficient public sector Rapid increase in personal debt Tough competitive environment has reduced margins

2104/19/23

Diversified Foreign Ownership of Polish Banks

Foreign banks control 67% of banking assets as of June 30, 2004

02468

101214161820

(pe

rce

nta

ge

)

% of total banking sector assets by banks by country of origin

2204/19/23

Remaining vulnerabilities/challenges

• Increase lending in a low inflation environment after years of easy profits from trading and investing in government bonds (in high inflation environment)

• Privatization of large state banks will be difficult

• Private sector banks weakened by recession of 2001-2002

• Increasing foreign competition

Turkish Banking Industry

2304/19/23

Kazakhstan Banking Industry

Effective measures and policies Relatively strong and independent regulator

Successive reformist central bankers

Group-level consolidated supervision enhances transparency

Mandatory reporting under IFRS

Enforceable creditor rights to collateral

Remaining vulnerabilities/challenges Fast credit growth undermines asset quality and capitalization

High single-party and sectoral concentrations

Weak transparency with respect to bank ownership

Risky expansion outside Kazakhstan

High proportion of international borrowing (rollover risk)

2404/19/23

Ukrainian Banking Industry

Effective measures and policies New law on securing creditors' rights may improve the legal status of

creditors

Deposit insurance provides limited coverage of deposits at private banks

The draft law on allowing foreign banks to open branches should promote competition

Remaining vulnerabilities/challenges Pervasive practice of intragroup lending

High single-party and sectoral concentrations

Obscure bank ownership

Weak/uncertain creditor's rights

Poor and often tardy disclosure of financial performance