world bank document - bhutan calcium carbide limited blc - bhutan logging corporation ... 1. this is...

TRANSCRIPT

Documeut Of

The World Bank

FOR OMCLAL USE ONLY

tpnt No. 12484

PROJECT COMPLETION REPORT

KENYA

KLAMBERE HYDROELECTRIC POWER PROJECT(LOAN 2359-KE)

NOVEMBER 16, 1993

FILE COPY

Report No: 12484Type: PCR

Public and Private Enterprise DivisionCountry Department IIAfrica Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir offcial duties. Its contents may not othenrise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSCurrent SAR

January 1993 March 1984

Ngultrum (Nu) = US$0.036 US$0.10US$1 N Nu 28.0 Nu 10.0

WEIGHTS AND MEASURES

1 kilometer (km) - 0.62 miles1 meter (m) = 1.09 yards1 square kilometer (km2) = 100 hectares (ha)1 hectare (ha) = 10,000 m2 = 2.47 acres (ac)1 cubic meter (m3) = 35.32 cubic feet (cu ft)1 cubic meter = 28.28 cubic feet (for true

board measurement)

ABBREVIATIONS AND ACRONYMS

AAC - Annual Allowable CutADB - Asian Development BankBCCL - Bhutan Calcium Carbide LimitedBLC - Bhutan Logging CorporationDCA - Development Credit AgreementDOF - Department of Forestry

of the Ministry of AgricultureERR - Economic Rate of ReturnFAO - Food and Agriculture OrganizationGDP - Gross Domestic ProductGEP - Global Environment FacilityIRR - Internal Rate of ReturnLCB - Local Competitive BiddingMOA - Ministry of AgricultureNu - NgultrumPCR - Project Completion ReportRGOB - Royal Government of BhutanSAR - Staff Appraisal ReportTCP - Technical Cooperation ProgramUNDP - United Nations Development Program

BHUTAN - FISCAL YEAR

July 1 to June 30

FOR OFFICIAL USE ONLY

THE WORLD BANKWashington, D.C. 20433

U.S.A.

flce of Dlrector-CeneralOperations Eva.uation

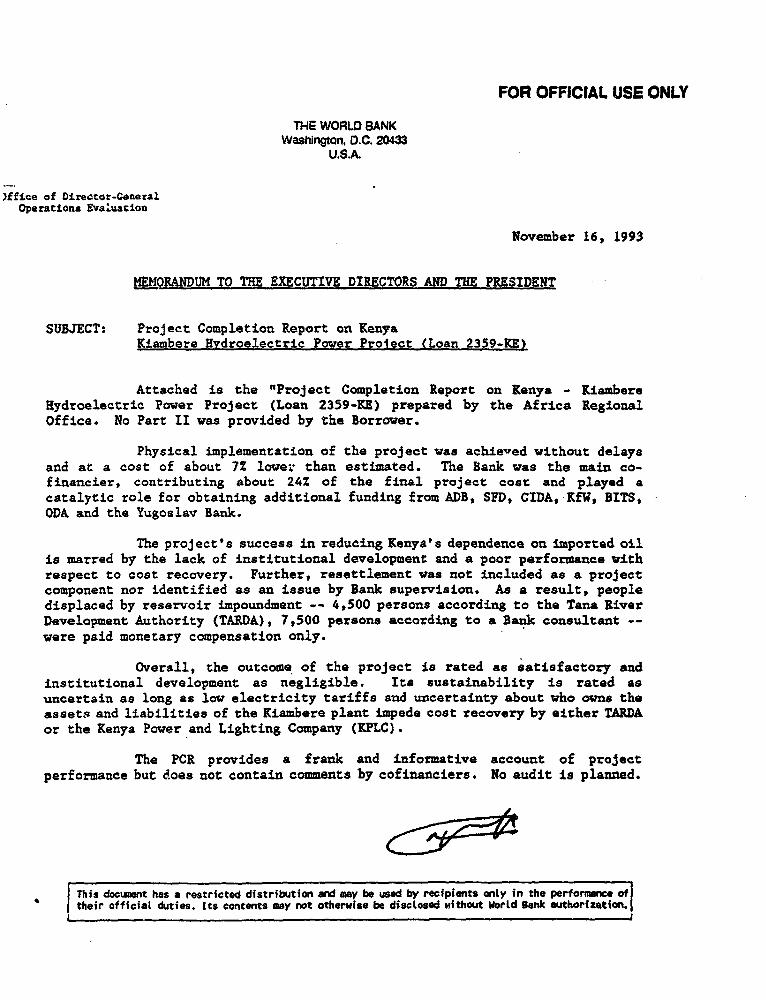

November 16, 1993

MEIORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on KenyaKiambere Hydroelectric Power Prolect (Loan 2359-RE)

Attached is the "Project Completion Report on Kenya - KiambereHydroelectric Power Project (Loan 2359-KE) prepared by the Africa Regionaloffice. No Part II was provided by the Borrower.

Physical implementation of the project was achieved without delaysand at a cost of about 72 lower than estimated. The Bank was the main co-financier, contributing about 24% of the final project cost and played acatalytic role for obtaining additional funding from ADB, SFD, CIDA, KfW, BITS,ODA and the Yugoslav Bank.

The project's success in reducing Kenya's dependence on imported oilis marred by the lack of institutional development and a poor performance withrespect to cost recovery. Further, resettlement was not included as a projectcomponent nor identified as an issue by Bank supervision. As a result, peopledisplaced by reservoir impoundment -- 4,500 persons according to the Tana RiverDevelopment Authority (TARDA), 7,500 persons according to a Bank consultant --were paid monetary compensation only.

Overall, the outcome of the project is rated as satisfactory andinstitutional development as negligible. Its sustainability is rated asuncertain as long as low electricity tariffs and uncertainty about who owns theassets and liabilities of the Kiambere plant impede cost recovery by either TARDAor the Kenya Power and Lighting Company (KPLC).

The PCR provides a frank and informative account of projectperformance but does not contain comments by cofinanciers. No audit is planned.

I This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents mey not otherwise be disclosed without Uorld Bank autherfzation.I

FOR omcia USE (ONLY

RENYA

KIAMBlBE HYDROELECTrIC POWER PROJECr

LOAN 2359 KE

PROJECr COMLETION REPORT

Table of COntents

PREFACE iEVALUATION SUMMARY ii

PART I:. PROJECr REVIEW FROM BANK'S PERSPECTIVE

Project Identity 1Background 1Proect Objectives and Description 3Project Design and Organization 4Project Implementation 5Project Results 7Project Sustainability 10Bank Performance 10Borrower Performance 12Project Relationships 13Consulting Services 13Lessons Learned 14

PART II: PROJECI REVIEW FROM BORROWER'S PERSPECTIVE 15(not available)

PART IIL: PROJECT PROFILE

Related Bank Loans and Credits 16Project rTmetable 17Loan Disbursements 18Project Implementation 19Project Costs 20Project Financing 21Project Results 22Status of Covenants 23Use of Bank Resources 24

This document hu a restricted distibution and may be uied by recipiens only in the performaneof their official duties Its contents may not otherwise be dbclosed without World Bank authodzaion.

-1-

KENYA

KIA1MBERE HYDROELECTIRC POWER PROJECr

LAN 2359-KE

PROJECr COMPLETION REPORT

PREFACE

1. This is the Project Completion Report (PCR) for Kenya's Kiambere HydroelectricProject, for which Loan 2359-KE in the amount of US$95 million was approved on December6,1983. In October 1989 US$15 million were canceled and in January 1990 US$1 million wasanceled. The loan closed on June 30, 1992.

2 Parts I and m were prepared by the World Bank, and submitted to the Tana and AthiRiver Development Authority (TARDA) for comment and the preparation of Part 11, andto the Kenya Power and Lighting Company (KPLC) for comment.

KENYA

C[AMBERB HYDROELECIRIC POWE PROJECT

LOAN 2359KLB

PROJECr COMPLUT1ON REPORT

EVALUATION SUMMARY

Prjec object amd desciption

1. The objective of the project was to reduce Kenya's dependence on himported oil, andto increase the power generation of the Kenyan system, at least economic cost, by adding anew, and fifth, hydroelectic power station on the Tana rrier, wnth the least envionmentalimpact reasonably possible.

2. The project consists of a 110 m high main dam and a 40 m high saddle dam, anunderground power station housing two 75 MW turbine generators, an outdoor switchingstation, and 220 kV transmission lines to connect the plant to Kenya's grid.

Pwject suhs,

3. The project was completed ahead of time, and below the estimated cost. Specifically,the second of the turbine generator units, to be installed, was commissioned in February 1988,about six months prior to the schedule identified at the time of appraisal, and the final costof the project (US$269 mfllion excluding interest during construction) was 86% of thatestimated at appraisal.

4. Fnancing was provided by IBRD (US$79 mfllion), the African Development Bank(US$19 million), the Saudi Fund for Development (US$8 million), Canada (US$36 milior),KfW (US$51 mfllion), Sweden (US$63 million), United Kingdom (US$20 million), YugoslavBank (US$11 million) and Kenya (US$43 million).

5. Two issues detract from an otherwise very successful project. The resettlement ofsome of those displaced by the project was not adequately dealt with, and the electricity tariffsremain well below the long run marginal cost of production.

conduons

6. Implementation of the project is judged to be successf with an acceptable level ofnet benefits, and excellent sustainability.

7. Under the present mandatory requirements for the environmental assessment ofhydroelectric project the oversight, which led to the resettlement inadequacies could nolonger occur. A sector dialogue linked to sector or macroeconomic incentives would havebeen apprpriate to help resolve some of the institutional and financial asnects which havebeen a problem in the Kenya power subsector.

KENYA - KLAMBERE HYDROELECTRIC POWER PROJECT (Loan 2359-KE)

Africa Region - Project Completion Report - Part I

1. rroject Identity

1.1. With a capacity of 140 MW the Kiambere hydroelectric scheme is the second largestpower plant in Kenya. It is located on the Tana river in a semi-arid area 150 km r'orth-west ofNairobi. Kiambere is the latest of a string of five plants regulated by the Masinga reservoir,which is near the headwaters of the Tana river. Feasibility and engineering studies began in1979, construction started in 1984 and was successfully completed in 1988. The plant isoperating satisfactorily.

1.2. The owner of the plant is TARDA, the Tana and Athi Rivers Development Authority,a state owned regional authority charged since 1974 with planning and maintaining developmentprojects in the Tana and Athi river bLins. The operator and lessee of the plant is KPLC, theKenya Power and Lighting Company Limited, a private corporation controlled, but not fullyowned (60 percent) by the state, who transmits and distributes electricity throughout Kenya.

2. Background

2.1. Sector development objectives: Kenya has one of the better developed power sectorsin Africa, and the consumption of electricity (130 kWh per capita per year), while modest byindustrial country standards, is higher than in many other African countries. When the Kiambereproject was appraised in 1982 the demand for electricity was forecast to grow at 6 percent peryear, a figure that is borne out by the statistics of the last 10 years. To support this grou^ :I theKenyan authorities have pursued a program of developing the domestic energy resources, bothhydro and geothermal. The World Bank has supported this effort with several loans and credits,see part III, Table l. It has been Government policy that the electric power sector shouldexpand its production by developing mainly domestic resources within the limits of the financialsupport it can marshall from foreign lenders and donors.

2.2. Context: As the number of users expands and demand grows, so do the financialrequirements of the sector. Costs are slowly but surely on the increase. Most of the lessexpensive hydro sites are now developed, and generally only the less favorable ones remain forfuture investments. Most of the people close to KPLC's system are connected, but the peoplein more distant locations which are more costly to serve demand e'ectricity as well. The quantityof external concessional financing is finite, and so are the possible resources from the treasury.The ever-increasing remainder of the investment must be provided by the users themselves,through higher tariffs, which are unpopular; and, tariffs have surfaced consistently as an issueduring the course of this project.

2.3. Linkages: The contribution to electricity projects of funds from government sourceshas been modest. For this project the Government provided no financing. Government'scontribution consisted of th& amount of notional duties and taxes t'lat might have been due on theimport of goods and services. A part of the local fiuds was supplied directly by KPLC toTARDA. Foreign inflation had a modest impact. It was zero between 1983 and 1985, the crucialyears for this project's procurement; it began rising only in 1986; the exchange rate of the Kenyashilling to the foreign currencies increased in line with inflation. Since a large part of the projecthad been financed with foreign currency, its cost did not strain the local resources at that time.The Government was acutely aware of the advantages of foreiEn financing, and managed to

2

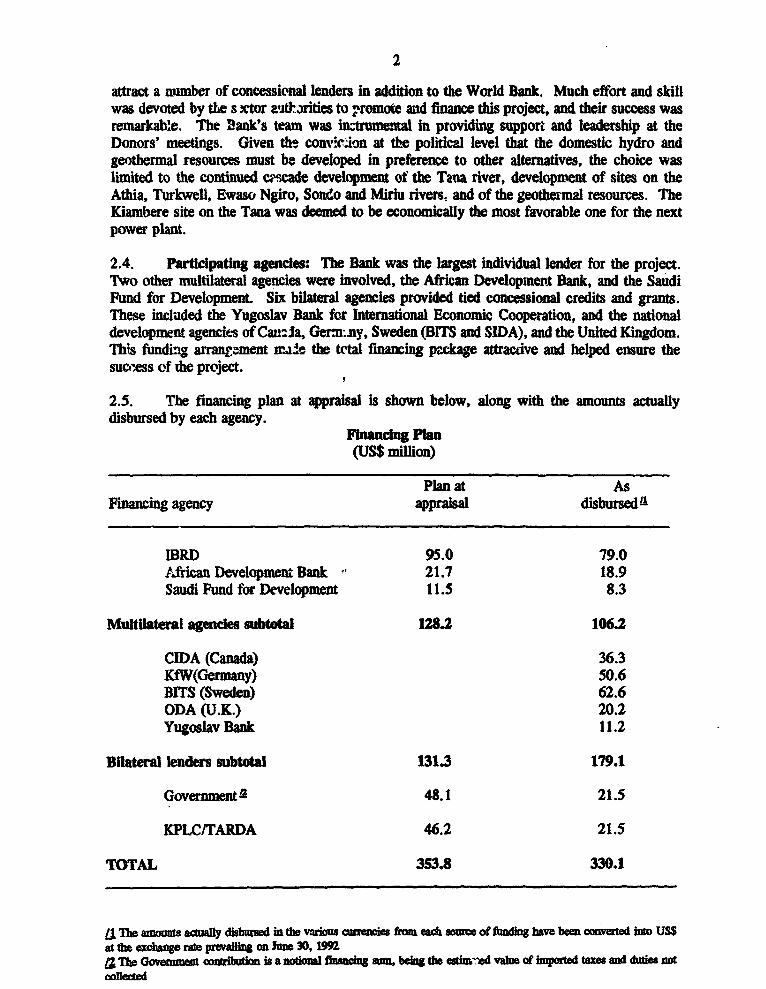

attract a number of concessional lenders in addition to the World Bank. Much effort and skillwas devoted by the s x:o ntkx,ities to qpromote and fiance this project, and their success wasremarkable. The 2anks team was inmtrumenal in providing support and leadership at theDonors' meetings. Given th- conv.qrion at the political level that the domestic hydro andgeothermal resources must be developed in preference to other alternatives, the choice waslimited to the continued c.cade development of the Tana river, development of sites on theAthia, Turkwell, Ewaso Ngiro, Sondo and Miriu rivers, and of the geothermal resources. TheKiambere site on the Tana was deemed to be economically the most favorable one for the nextpower plant.

2.4. Partidpating agencdes: The Bank was the largest individual lender for the project.Two other multilateral agencies were involved, the Arican Developmtent Bank, and the SaudiFund for Development. Six bilateral agencies provided tied concessional credits and grants.These included the Yugoslav Bank for Inteonatinal Economic Cooperation, and the nationaldevelopment agencies of Cat=s, Germnmy, Sweden (BITS and SIDA), and the United Kingdom.This fimding arrang.ment iraJe the tetal fmancing package attractive and helped ensure thesuccess of the project.

2.5. The financing plan at appraisal is shown below, along with the amounts acuallydisbursed by each agency.

,andg Plan(US$ million)

Plan at AsFinancing agency appraisal disbursed'4

IBRD 95.0 79.0African Development Bank 21.7 18.9Saudi Pund for Development 11.5 8.3

Multilateral agcies subtl 128.2 106.2

CIDA (Canada) 36.3KiW(Gernmy) 50.6BITS (Sweden) 62.6ODA (U.K.) 20.2Yugoslav Bank 11.2

Bilateral lenders subtotal 131.3 179.1

Government 2 48.1 21.5

KPLC/TARDA 46.2 21.5

TOTAL 353.8 330.1

L 11i. amouts sauaL disbursed m therius ais oies fom ead seam of fandg bhve bn coverted into USSat the enchae rate prevailing on Jon 30, 1992a The Govemmt contbuion Is a notiol Snaiog ambeg the eatmmed value of imported buses and dudes notcnflected

3

2.6. The flnancing plan indicates the amounts actually disbursed in the various currencisfrom each source of funding as recorded by TARDA up to June 30, 1992, and they have beenconverted into US$ at the rate of exchanrg prevailing on that date, the closing date of the B&nkloan. The difference between the pk^-ned and the actual disbursement is due to the projecthaving been completed below the orig'nal cost estimate. Paragraphs 5.3 and 8.5 below discusspossble reasons.

3. Project Objectives and Description

3.1, The objective of the project was to reduce Kenya's dependence on imported oil, and toincmase the power generation of the Kenyan system, by adding a new hydro plant on the Tanarive. This is the major river in Kenya, with ten hydro sites along its 750 meter drop btweenthe Masinga dam and the plains. A string of five power plants Including Kiambere has now beenbuik, and four additional sites are available, down to Korah Hills, the lowest commerciallyfeasible site. The reservoir at Masinga is large enough (1,500 million m!) to store sufficientwater to even out the flow between the wet and dry seasons, and thus to regulate the productionof all thc downstream power stations.

3.2. The specific goals of the Kiaber project were to increase by 140 MW the generatingcapacity of the Kenyan system, and to increase by 910 GWh (million kilowatt-hours) the energyavailable during a year of average rainfall. The dry year energy production at the site wasforecast at 683 GWh. For the Kenyan system in 1983, these goals represented substandalincrases; 25 % in MW capacity, 33 % and 22 % in the energy production during an averagean a dry year respectively.

3.3. The main physical components of the project include:

(a) the main dam, approximately 110 m high and 840 m long, which, together withthe saddle dam creates a reservoir of 585 million tn gross storage in the Tanari er valley. The dam is rock faced, zoned earth-filled with impermeable coreand gramuki shell;

(b) the saddle dam, approximately 40 m high and 1470 m long with a fsibleplugge ' aergency spillway. This spillway has a capacity to dicharge, in two500 m' sUages, 1,000 m'

(c) a concrete lined free overfall side channel spillway with flip bucket. Three highlevel mechanical gates are insalled in the overflow weir to maintain river flowswhen the power station is rPt operating and when no natural spillage is takingplace. This spillway, sited at the end of the main dam, will pass 3,600 rnnormally, and 4,500 mn at maximum dischage;

(d) a low level outlet facility installed in one of the two diversion tunnels, tomaintain river flows when the power station is not operating and when thereservoir level is bekw the high level mechanical gates;

(e) water passages including a power tunnel 4,100 m long and 6.1 m in diameter,complete with itake strucre and surge tank, and a tailrace tunnel 1400 m longand 8.6 m high of horse-shoe shape, which discharges the flow from thepowerhouse back into the river;

4

(f) an underground powerhouse equipped with two 75 MW turbines and 85 MVAgenerators;

(g) an outdoor rjnsforn:;r and switching station to step-up the voltage to 220 kV;

(h) two sections of 220 LV-' high volt .pi transmission line totalling 80 kIn in lengthto connect the Kiambere switchyat.. v ith the existing system of KPLC.

3.4. The project also included three components of a managerial nature:

(g) consulting engineering services for the technical design and supervision of theproject;

(h) a panel of experts to supervise the consulting engineering firm, and to providi.a s cond opinion on important technical matters; a financial expert and atechnical leader for the TARDA team charged with the implementation andmanagement of the project;

(i) activities to protect the environment and to compensate displaced populations

3.5. To ensure the financial viability of the power system the following policy componentwere detailed in the SAR, agreed to at negotiation, and translated into conotactul clauses:

(a) the aggregate of the power companies that comprise the electricity sector inKenya would earn a stated financial rate of return;

(b) TARDA would submit each year the data required to make this calculation.

4. Project Design and Organization

4.1. By 1983 the physical components of the project were clearly defined, and had beenthoroughly preparedl. Feasibility stLdies had been completed during 1979 and 1980, and thedesign was optmized and finalized by December 1981. An environmentl impact study had beenconmpleted and its main report was finalized by September 1983; ample field investigations, accessroads, and the construction workers' camp, which had been financed from TARDA's ownresources were readied in preparation for a quick start on the project. Both layout and designwere conventional and thus well proven. The scope and scale of the project were suited to thesite, and the scheme was designed to use the same flow as the other plants on the Tana river.The timing was appropriate and all parties agreed that Kiambere was part of the least cost powerdevelopment plan at that time.

4.2. The roles and responsibilities of the agencies involved were well defined on paper.TARDA was to be both the owner of the project, and its executing agency. Upon completionKiambere would be leased to KPLC which would operate it and pay TARDA sufficient rent tocover TAPDA's financial obligations towards its lenders, plus a contribution to TARDA towardsthe project costs, the "devtlopment surcharge". Thus KPLC was the key to the financialjusification of the project, and to the solvency of TARDA. KPLC only complied with itscommitments during the period of construction of the project upto November 1987 when itstopped its payments to TARDA. The problems this caused are described in 6.8 below.

4.3. A discrepancy worth noting is the difference between the consultant engineer's estimateof construction costs, and the lowest bids received, which were between 50 and 60 peMent of the

5

engineer's estimate. The Borrower and the consultant evaluated the bids very thoroughly, toextract the maximum advantage from the concessional financing and grs wbich were availablefor some of the bids. Consequently, the contracts were awarded to the most advatages bidwhen financing was taken in*; account. The aggregate of the contracts awarded was 72 percentof the engineer's estimate, a chown -m the table below.

Comparison of engineer's estimatewP.h flnal contract amnounts

(US$ million)

Estimate Contract amountsComponent Dec. 1982 Dec. 1983

Dams 84.9 54.4Tunnels 41.2 34.8Powerhouse and ac'xss 38.1 27.9Mechanical and electrical Works 32.3 25.6Transmission line 9.1 6.2

Total base cost of the faclities 205.6 148.9

4.4. The engineer's estimates were based on a rate of exchange of KSh 12.5 to the US dollar;although by December 1983 the rate had changed to 13.8. A discussion of the causes of thediscrepancy between estimate and contract amounts follows in paragraph 8.5.

3. ProJect Inplementation

5.1. The physical imp on of the project was completed on schedule. Unit number2 was used for cowrmercial operation Irom Februay 21, 1988 and Unit number 1 from March17, 1988. Manufacturing falts came to light in the turbine runner, but this did not cause muchloss of output because repairs and replacement operations took place mainly over weekends. TheCertificates of Completion, after taking account Use-Before-Taking-Over were, for Units 1 and2 respectively May 18, 1988 and June 7, 1988 and the Taking Over Cetficates were respectivelydated March 24, 1989 and February 28, 1989. In summary:

(a) the power facilities were completed on schedule im May 1988 and the costs were belowbudget. Both generating units were commissioned by February 1988, althoughproduction at full capacity was delayed one year due to having to replace and repair twodefective turbine runners;

(b) the final cost of the project was substially lower than anticipated, and thisfacter and the devalua- on of the Kenya shilling, which required a redced draw-doi^n of the dollar loa, led to the cancellation of $16 million of the World Bankloan amount;

(c) the tariff issue was the subject of many discussions, reminders, and negotiations;

6

(d) durng the disbursment period of the loan KPLC did not comply with thefinancial covenant contained in the project agremet concerning rate of return,and tariff levels. Moreover, since May 1988 KPLC has neglected to comply withthe Project Agreement to pay TARDA the amounts due for the lease ofKiambere; and

(e) the resettlement of the populations displaced by the project has not been exeutein an acceptable manner.

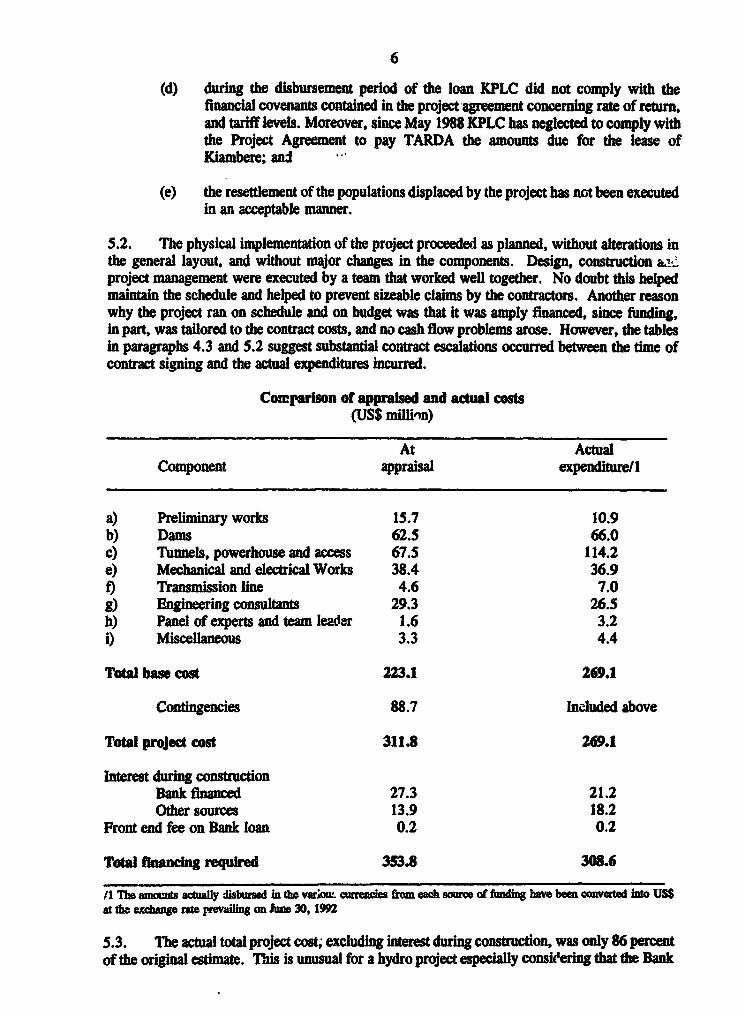

5.2. The physical implementation of the project proceeded as planned, without alterations inthe general layout, and without major changes in the components. Design, construction aaiCproject management were executed by a team that worked well together. No doubt this helpedmaintain the schedule and helped to prevent sizeable claims by the contractors. Another reasonwhy the project ran on schedule and on budget was that it was amply financed, since funding,in part, was tailored to the contract costs, and no cash flow problems arose. However, the tablesin paragraphs 4.3 and 5.2 suggest substantial contract escalations occurred between the time ofcontract signing and the acual expenditures incurred.

Compjarison of apprased and actual costs(US$ milliin)

At ActualComponent apprais expendtr/l

a) Preliminary works 15.7 10.9b) Dams 62.5 66.0c) Tunnels, powerhouse and access 67.5 114.2e) Mechanical and electrical Works 38.4 36.9f) Transmission line 4.6 7.0g) Engineering consultants 29.3 26.5h) Panel of experts and team leader 1.6 3.2i) Miscellaneous 3.3 4.4

Total base cost 223.1 269.1

Contingencies 88.7 Included above

Total project cost 311.8 269.1

Interest during construconBank financed 27.3 21.2Other sources 13.9 18.2

Front end fee on Bank loan 0.2 0.2

Totl fhncing required 353.8 308.6

/1 The amocmts wlafly disbursed in the variour rendclss from each souse of #-Aing have been converted iho USSat the exdne rate prevailig on June 30, 199Q

5.3. The actual total project cost; excluding interest during construction, was only 86 percentof the original estimate. This is unmusual for a hydro project espeially considering that the Bank

7

took the precaution of finalizing the project estimate six months after the construction bids hadbeen received. The first cost estimaes for the project were prepared in 1979, and they wererevised periodically up to 1983, during the period just after the second oil crisis of 1979/80,when inflation rates were high and were expected to remain so. Every time the costs wererecalculated, the total increased until it exceeded $500 million. The files indicate that both theborrower and the Bank were :oncernt.J by this. A firm of consulting engineers was called in toreview the costs; and their D)cember ')82 report confimed the estimate. A second opinion byanother cost estinator reconfirmed it three months later, and even increased it by a fewpercentage points. Yet when tenders were opened in May 1983, the low bids were almost halfof the engineers' estimates. Paragraph 8.5 below discusses possible reasons.

5.4. While the physical implementation proceeded without delay or difficulties, the lack ofattention to the resettlement issue at appraisal and the somewhat complicated institutional situationin Kenya led to a substantial staff input and effort by the Bank to deal with the consequences (seesection 6 below).

6. Project Results

6.1. The project objectives remained unchanged during the implementation of the project.Thorough preparatihn of the p oject's physical design (see paragraph 4.1 above) meant that theborrower was ready to awarl the construction contracts as soon as the loan was approved.However, the lack of attentian to social issues during project preparation and appraisal led theborrower to implement project activities without proper resettlement planning. Project objecivesand activities should have been revised during implementation to include adequate benefits forthe affected people, but this was not done.

6.2. The production of energy at Kiambere is expected to be - )out 790 GWh per year as along term average for a year with average rainfall, compared with a figure of 910 GWh per yearquoted in the SAR. In fact, the average for the first four years of operation has beea 873 GWh.The 13 percent discrepancy between 910 and 790 GWh is not due to any shortcoming in thedesign or implementation of the project, but rather to the fact that the earlier estimate wasoptimistic. The 1992 National Power Development Plan has confirmed the figure of 790 GWhas the most probable considering, among otber factors the water withdrawals from the Tana riverup to 1995, the station's own use, and the system constrains on how the station may be operated.

6.3. The economic viability of the project was confirmed with a 10.2 percent actual economicrate of return as compared with the 10 percent forecast at the time of the SAR. The economicrate of return of Kiambere was rclulated based on actual costs and updated productionestimate. Benefts were estimated at 5.4 US cents/kWh (the cost of producing the same amountof electricity in a low speed diesel plant). Had the benefits been estimated using willigness topay deduced from actual tariffs, the rate of return would have been lower since a tarff of only4.4 US cents/kWh was charged to the users in 1990. The economic rate of retu for the projectwould have been reduced, but by less than 1%, if the resettlement issues had been addressed tocurrent acceptable standards.

6.4. The financial rate of return in the SAR had been calulated for the aggregate of theelectricity sector. In order to reconfrm whether the projected financial returs were actuallyachieved, it was necessary to have consolidated financial statements for all the Power Companies.Without such submissions, which were not required under the financial covenans, it would beextremely difficult to calculate the financial rate of return from the individual financial samentswhich were required per section 5.03,(c) of the Loan Agreement. This reflects a fault in the

8

design of the financial covenants. And, since the individual statements have not been submittedas well, it is not possible to calculate the financial rate of return.

6.5. Environmental Impact: The issues related to the environment and resettlement havebeen inadequately dealt with. An area of 132 square kilometers was expropriated by TARDAfor the Kiambere project. Of this 25 sq.km represent the area inundated by the reservoir, andthe remainder is a buffer zor. aroune the lake and the project facilities where settlement andhuman activity are no longer :'lowed, a:nd where teforestation is being undertaken. The projectaffected indirectly other area; of undetermined size where the several thousand displaced peoplehad to move in the administrative districts of Embu and of Kitui, which border on the Tana riverat Kiambere.

6.6. The number of people displaced or affected by the project is not known with accuracy.The census taken before the beginning of construction, as part of the environmental impact study,gave about 3,000 as the number "directly affected". The SAR relied on an earlier consultant'sreport that there were no permanent settlers in the reservoir area, and that only about 1000 peoplelived downstream of the dam. This particular report dealt with a different project layout thanwhat was eventually built. While the earlier proposal included a low dam and a 4.9 km2

reservoir, the project as appraised had a still higher dam and a much larger reservoir. Theaddition of an extensive "buffer zone" brought the expropriated area to a total of 132 kmi2, andgreatly increased the number Jf peoplet Jisplaced. After the filling of the reservoir began in 1987the matter acquired some urgeqcy. lI 1988 the Bank's and TARDA's consultant estimated thenumber cf persons at 7,000, v.hile 1'ARDA reports that it compensated about 4,500 claimants.TARDA paid out KSh3 I million and feels that it has fully complied with Kenyan law, which onlyrequires monetary compensation. This resettlement approach was not in compliance with theBank's guidelines, in force at time of appraisal (OMS 2.33), and is not considered sufficientunder the Bank's current directives which require that any involuntary resettlement should beplanned with the participation of the affected people, and should ensure that their welfare is atleast not negatively affected.

6.7. Had the presence of permanent settlers in the reservoir areas been taken into account,the Bank's resettlement guidelines would have required having a workable resettlement plan readyat the loan negotiation stage, and that its implementation be made part of the borrower'sobligations. The SAR notes that a detailed environmental study was underway, presumablyreferring to the Pre-construct:on Envi.-onmental Impact Study. This study, the main report ofwhich was co)mpleted in September :983 (after negotiations but before Board presentation),recommended cash compensaion and proposed elements of a resettlement plan However,neither the loan agreement, nor the agreements listed in the staff appraisal report include anymention of resettlement activities.

6.8. Issues relating to the Allocation of the Benefts of the Concessional FinancingUnder the loan and related project agreements, the lease payments due from KPLC consist of twocomponents; an amount sufficient to cover TARDA's financial obligations to its lenders, and adevelopment surcharge to finance part of the local costs of the Kiambere project. Thejustification for the latter is that the financing received by TARDA is at concessional terms tohelp regional (including river) development rather than to subsidize KPLC. In any case KPLCceased to remit its lease payments to TARDA in May 1988, ostensibly on the grounds thatownership of the assets had been tranm:erred to KPC by Government. This action prevented thelatter from servicing its debt to the Bauk and prevented it also from carrying out its developmentprograms, including any of the resettle:nent initiatives which were discussed after October 1986.Consequently neithir KPLC nor TARDA are now in compliance with the Project Agreement norwith the Loan Agreement, and the Kenyan Treasury as guarantor has had to step in to fulfill

9

TARDA's obligations. It has been poinated out repeatedly to the Kenyan authorities that theownership of assets should not be at issue here; but what should be at issue is the spirit behindthe loan agreements with the donors, which call for the benefits of the concessional loan termsto be used for regional development. As of May 1993 no action had been taken. In thecircumstances unless the benefit of the commercial terms are passed on to TARDA, in atransparent manner, Government will remain in violation of the legal agreements.

6.9. Electricity Tariffs Government has not allowed tariffs to increase to a level whichcovers the cost of el& tricity supplies - tariffs have remained consistently and significantly belowthe long run marg:nal cost of supplics for most of the 1980's. Indeed, the inadequacy of thetariffs has adversely affected KPLC's ability to service its obligations to TARDA, to cover itscosts, such as the servicing of its loans, which are affected by the deteriorating exchange rate,and to compensate for a decline of its operating efficiency. However, tariff levels have been acontinuing concern of this project. A tariff increase was agreed with the Bank in 1983 in orderto meet the rate of return requirements of the power companies. The Government authorized itin May 1985, rescinded it in July 1986, and finally implemented an increase in January 1987.Moreover, as discussed in para 6.4, the absence of reporting requirements for consolidatedfinancial statements for the power companies has made it difficult to verify compliance with rateof return requirements. Based on the fmancial statements of KPLC, it appears that the stipulated8% ROR for the years up to 1990/91 was probably not met. KPLC has also not been successfulin submitting its finzticial statements vwithin the agreed six months period from the end of thePlnancial year.

6.10. TARDA's Finances As lesee of the Kiambere plant KPLC is committed to payapproximately Kenyan Shillings 300 million per year plus the equivalent, in Kenyan shillings, ofUS$14 million, which would be used to service the loans from IBRD and the Yugoslav bank, andto contribute to TARDA's development budget. KPLC contributed certain amounts during theconstruction period, but ceased remitting power payments since May 1988. A payment of KSh10 million per month was resumed in February 1991. As of April 15, 1993, The TARDAaccounts showed KSh 1,616 million in accumulated receivables from KPLC for the Kiambereproject. Another KSh 476 million were due by KPLC for energy from the Masinga project.

6.11. As a consequence of the refusal of KPLC to honor these debts TARDA is nowtechnically insolvent. The latest available financial statements (unaudited) show that as of June30, 1991, TARDA's liabilities exceeded its assets. These assets do not include the outstandingamounts due by KPI C, but neither do the expenditures include adequate depreciation. TARDAhas never recorded any depreriation for Kiambere, and ceased to record depreciation for itsMasinga power project in 1988/89. The financial accounting of TARDA for the project must bequalified as irregular.

6.12. There is a discrepancy between the KPLC accounts and those of TARDA. The AuditorGeneral's reports which accompany both sets of accounts do not deal with it. The TARDAaccounts are qualified for a number of reasons, including TARDA's failure to record asreceivable accrued revenues due by KPLC in the amount of KShl,165.1 million. Yet the KPLCaccounts, which do not show the full indebtedness to TARDA, are certified withoutqualifications. It appears that KPLC is not in compliance with the Project Agreement of June 28,1984, wherein it accepted a commitment to enter into a leasing agreement with TARDA. Noris the Government in compliance with the Guarantee Agreement of the same date wherein itaccepted to cause KPLC to carry cut its obligations under the Project Agreement. Areconciliation of the 3ccounts 4f all rover Companies, of TARDA and of KPLC is necessary,as well as a fundamental reconciliation of their and the Government's positions. This will requirea detailed review of the accounting conventions and practices of all the Power Companies.

10

6.13. Project Management The management of the physical implementation of the projectwas executed satisfactorily. Being mainly an adminstrative and a planning entity TARDA hiredtwo expatriates to act as the key project management staff for the duration of the project. Itappears that their function was mainly administrative and of liaison and that both the constructionmanagement and the bulk of the project management were handled by the staff of the consultingfirn. As neither they nor the consultant have issued specific activity reports, it is unclear whoperformed which function. In any case there was excellent coordination between owner andconsultant and the project's physical implementation was completed successfully.

6.14. Soclal Impact The social impact of the project was evidently favorable for the largeconsumers and for the million and a half town dwellers who are served by KPLC and whoreceive the benefit of an improved supply of electricity at a price that has not increased in realterms since 1981. The impact of the project was far less favorable for the estimated 7,000 peoplewho were dispossessed and/or displaced by the project (see 6.05 to 6.07 above). In 1987TARDA, the World Bank and ODA cooperated on a resettlement survey which was led by aKenyan social scientist. On the basis of interviews with an estmated 15% of resettler householdsand an equal number of non-resettler households, results showed the resetflers averaged a lossof about half their land, had reduced their livestock by more than a third and had reduced accessto pasture, firewood, water and trees for building. The cash compensatdon for lost land wasinadequate for buying land in the more densely populated resettlement area where land wasscarce.

7. Project Sustalnablity

7.1. The project is most likely to maintain an acceptable level of net benefits over itseconomic life.

7.2. Technical risks are remote. The engineering design has taken into account any possibleearthquake risks, and the foundation rock is of good quality, thus minimizing geological risks.There is no indication that river flow, and siltation may cause any problems in the foreseeablefuture.

7.3. A reduction of the availability of the generating sets, and therefore of producton and ofthe quality of service, is always a risk; availability depends on the quality of management atKPLC, which is good today, and on the availability of fumds for proper maintenance. The lattermay be at risk only if the KPLC tariffs continue to remain inadequate for a period of years.

8. Bank Performance

8.1. The Bank was both the major lender and the coordinator and leader of the group of co-lenders. The Bank performed both tasks efficiently regarding the physical aspects of projectimplementation, as is indicated by the smooth implementation of the project. Greater emphasisand possibly stronger action should have been requird on financial policy issues (includingtariffs). The Bank could have provided a better lead in respect of the resetement issues.

8.2. The Bank's role as lender of last resort was evident during the early stages of projectpreparation. The Kenyan prospective borrowers were firmly convinced that Kiambere was theproject to build, promoted it with determination to the prospective lenders from 1980 onwards,and financed the preparatory work with local funds. TRDC, a predecessor agency of TARDA,hired the engineering consultant in February 1981, called for prequalification of contracto inAugust, and had the tender documents ready by November 1982. The Bank, which had followedthe progress of the project with preparatory missions since 1980, began to study the least cost

II

issue in April 1982, held a pre-appraisal mission in August, an appraisal mission in November1982; the tariff issue and the social and enviromental issues were raised in March 1983. Bythen the project had acquired a momentum of its own, and was buoyed by the submission ofunexpectedly low bid prices, and by attractive offers of financing from a number of co-lenders.The Bank was ready to proceed with the loan approval as soon as some agreement was reachedon the financial/tariff conditions. After six months of hesitation the Kenyans agreed to the tariffclauses and the project was approved in November 1983.

8.3. The appraisal process was norrnl, except that it lacked resettlement expertise and theTOR for the appraisJ missicn 'lid not :;ention resettlement or the environment. The Bank hireda consultant to check that Ki=nbert- vs indeed the least cost alternative, and to finalize theeconomic evaluation. The main altern 4ive to Kiambere was then a coal burning steam plant; thepossible alternative of diesel generation was excluded a priori. This is noted because the latest(1992) issue of the Kenyan power development plan recommends a diesel plant as the nextcomponent in a least cost development sequence; and this may possibly have been true even in1983. The overestimate of the cost of the project in the appraisal report has been discussed inparagraph 4.05 above. The appraisal underestimated the size of the resettlement problem (see6.6 above) by relying on unqualified opinion. Furthermore, this underestimation remainedunchanged even when the results of the environmental study became available.

8.4. The Bank supervised the project most diligently and there were no technical orprocurement problems to speak of. Svpervision missions were undertaken frequently, see table8 B of part III. Th. missions could ri itly charactize the project technically as a success. Itwas very difficult fit the sui -rvision :iissions to solve the two major problems, the electricitytariffs of KPLC, which was n .t the borrower, and the resettlement issue. The tariff issue wasbrought up repeatedly in follow-up ccmnmunications from headquarters; the resettlement issuewas the object of a number of meetings at headquarters, and gave rise to four missions byresettlement experts between late 1986 and 1989. In March 1990 the Bank reviewed a proposalfrom TARDA for the development of the Kiambere project area to benefit the local population.However, neither issue has been be resolved to the Bank's satisfaction, and both are pendingtoday.

8.5. From the experience with these three problems the following conclusions can be drawn.The overestimate of the cost occurred despite having excellent iformation on the cost of thework. At 52 percent of the total, the local component should have appeared unusualy large forthe capacity of Kenyan subcontractors. Part of the overestimate has to do with including taxesand duties which were not due because tf the type of financing selected. The price contingenciesforesaw the effect of inflation in Kenya, but did not account for a compensating variation of therate of exchange to the Dollar. The foreign component was basicaUy overestimated, seeparagraph 4.3; in addition the increase in value of the US dolar during the construction periodhad the effect of countering any cost increases in the currency of the contractor. The rise in theexchange of the dollar was not foreseeable by the staff. A point that deserves notice is that whatappears to be an overestimate may have been in part the result of an astute procurement policy.The specifications were well prepared,and left little scope for doubt, and little risk for the bidder;TARDA had made sure that bilateral financing was available from five countries, but had notassigned any contract package a priori to any donor country. Therefore each supplier had to bidagainst a number of foreign competitors, and the bilateral funds were considered only during thebid evaluation. This produced very competitive bids, to the advantage of the project.

8.6. The design of the tariff/rate-of-retrn covenants did not allow for easy monitoring andcorrective action. First, as mLntioned '.arlier, there were no requirements to submit consolidatedfinancial statenent2 for the aggregat- of the power companies making the calculation of RoR

12

difficult. Second, even if such calculations had been undertaken and Rate of Return found to bebelow appraisal estimates, there were no specific tariff covenants which would have allowed theBank to require the initiation of corrective actions. A related issue was the lack of studies orsystem of calculation to determine the tariff changes needed. Third, in addition to the generalproblem with initiating tariff increases in state owned utilities, there was a specific problem inthe Kiambere case since the responsibility was divided among the agencies involved. Theborrower, TARDA, has no influence, nor is directly affected by the level of tariffs, and the utilityhas little power either, since tariff decisions are a prerogative of the cabinet of ministers if notof the president.

8.7. The resettlement iss-.te could perhaps have been dealt with more effectively if the Bankhad not relied on a statement (which was not verified) by a power consultant chosen for hisexpertise in designing structuies, but w}o neither had, nor claimed any special skill in handlingpeople problems. Nowadays, the Bank gives these matters a high profile and there is no reasonwhy they should not have been handled with the same care as other components of this hydroproject as was provided under the then current Bank guidelines. Just as it was perfectly normalto invest huge sums in topography or in geotechnical investigations, it should have been necessaryto carry out land surveys, a census of the population and sociallethnological investigations beforereservoir constuction was considered; and the pre-appraisal and appraisal missions should haveincluded an expert in agricultre, or other relevant discipline to assess the problem and itssolutions so that this issue could have been dealt with fully. The environmental impact studywhich dealt with the resettlement issue should not have been ignored by the Bank. Based on it,a resettement plan should have been devised, described, and explained in detail in the appraisalreport for the resettlement and environn.antal problems just as tender specifications are preparedand precise estimates are prod-ced for the major physical project components. The costs thoughsmall were not negligible, and should have been treated precisely. The resettlement structures,be these houses, schools, water projects, or roads, could have been part of one of the civil workspackages, and should have been executed at the same time. Such matters are now dealt withmore rigorously by the Bank.

9. Borrower Performance

9.1. The Borrower TARDA worked diligently to carry out its duties. During the projectpreparation stage TARDA (and its predecessor TRDC) promoted the project energetically, ralliedan impressive list of willing donors and co-financiers, and had the benefit of a good cooperationwith KPLC. It supervised the pre-construction environmental impact study but, having sent itto the Bank, failed to follow rp and bring its conclusions to the Bank and other donors. Afterthe completion of the project the relationship with KPLC became less close, possibly linked withthe fact that the two institutions were no longer under the same ministry; and in the end KPLC'sfailure to make its lease payments to TARDA jeopardized TARDA's ability to function as adevelopment authority.

9.2. The physical implementation of the project was well prepared thanks to the decision ofTARDA to finance feasibility and design engineering with their own resources, and to finaneeenough preparatory work. This resulted in timely preparation of tender specifications, insufficient detail to eliminate uncertnties, which in turn allowed to maintain the selected scheduleand to promote competition among bidders, and to achieve excellent bid prices. The procurementwas executed skillfully.

9.3. The project management finction was entirely satisfactory, and TARDA deserves muchcredit for having chosen twvo competent outside experts as leaders, and having hired a good

13

consulting engineering team for the supervision/construction management. The cost of the latterwas substantial, but the work was well executed.

9.4. The conclusion can be drawn that even a borrower without strong background in projectmanagement can have a project implemented well if he is prepared to chose and pay for goodmanagers. Another conclusion is that TARDA's regional development fction was too weakfor it to perform better than it did in relation to resettlement issues witiout reinforcement by thedonors.

10. Project Relationship

10.1. The relationship of the Bank with the borrower was good; as the physical aspects of theproject were implemented satisfactorily, no major problems had to be solved which could havecreated stresses between the Bank and the borrower. TARDA responded cooperatively to theBank's belated efforts on behalf of the "resettlers", but, with mixed signals from the Bank, and,without finds, TARDA was unable to solve the problem.

10.2. The problem of the inadequacy of KPLC's tariffs could not be solved, neither during theimplementation period nor thereafter.

10.3. The borrower and the Bank enjoyed good relations with the other co-fmanciers, whoprovided the bulk of the financing for the project.

11. Consulting Services

11.1. The consulting firm charged with the design and supervision of the project performedwell. TARDA followed their advice and financed sufficient preliminary surfce and sub-surfaceinvestigations which eliminated uncertinttes from the specifications, and enabled a goodmnnelling route to be chosen which probably avoided claims by the conractors. The consultassigned a large number of staff to the job, which assured good supervision and management.The final cost of the engineering consultants plus the cost of the panel of experts was a little onthe high side, 11 percent of the total project cost but it was probably cost efective because thecost of the project was consideraly less tha the appraisa estimate.

11.2. The contractors performed well. Only the dam contractor needed some prodding toensure that the schedule was kept. The suppliers delivered and instled satisctory goods andequipment. An initial problem was a defective turbine runner, which affected full production fora year until it was eventually replaced.

11.3. Local consultants were used for the environmenta impact study, funded and supervisedby TARDA. The Bank did not comment on this crucial work which, although late, wassubstantially completed before the loan was approved and was satisfactory in that it containedenough information to provide the basis of a resettlement plan.

14

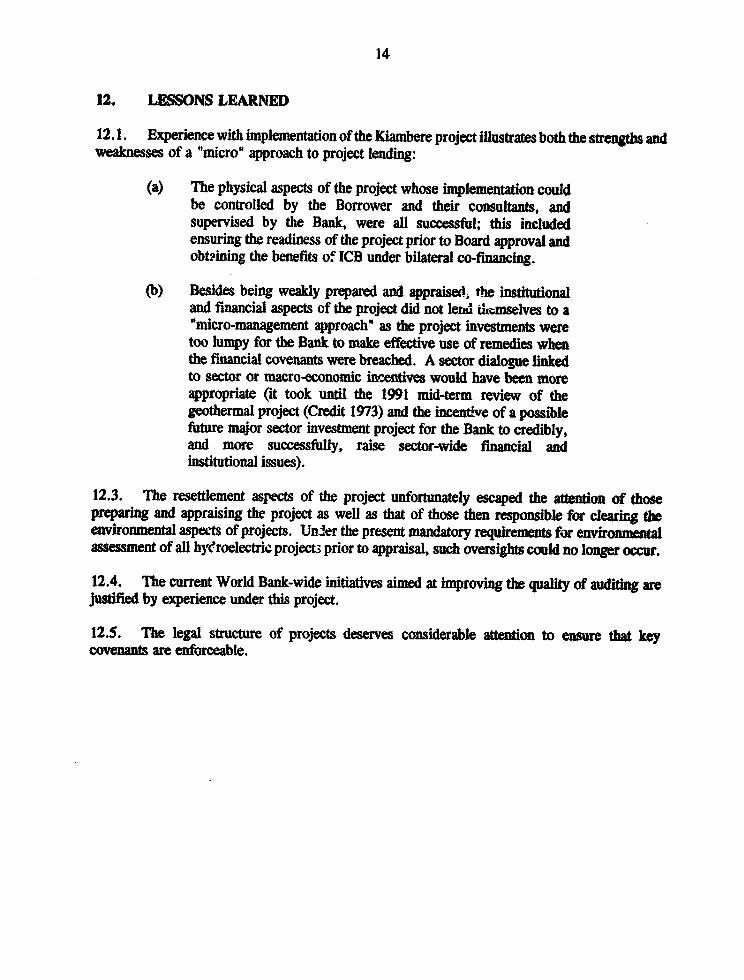

12. LESSONS LEARNED

12.1. Experience with implementation of the Kiambere project illustrates both the strengts andweaknesses of a 'micro" approach to project lending:

(a) The physical aspects of the project whose implementation couldbe controlled by the Borrower and their consultanuts, andsupervised by the Bank, were all successful; this includedensuring the readiness of the project prior to Board approval andobtsining the benefits of ICB under bilateral co-financing.

(b) Besides being weakly prepared and appraisei. the institutionaland fnacial aspects of the project did not lend dwmselves to a"micro-management approach" as the project investments weretoo lumpy for the Bank to make effective use of remedies whenthe financial covenants were breached. A sector dialogue linkedto sector or macro-economic mcentives would have been moreappropriate (it took until the 1991 mid-term review of thegeothermal project (Credit 1973) and the incentive of a possiblefuture major sector investment project for the Bank to credibly,and more successfully, raise sector-wide financial andinstitutional issues).

12.3. The resettlement aspects of the project unforunately escaped the attention of thosepreparing and appraising the project as well as that of those then responsible for clearing theenvironmental aspects of projects. UnJer the present mandatory mquirments for environmentalassessment of all hWroelectric project; prior to appraisal, such oversights could no longer occur.

12.4. The current World Bank-wide initiatives aimed at improving the quality of audiing arejustified by experience under this project.

12.5. The legal structure of projects deserves considerable attenion to ensure that keycovenants are enforceable.

15

PART II - Project Review from the Borrower's Perspective

No comments have been received from the Borrower.

16

XENYA - KIAMBERE HYDROELECTRIC SCHEME (Loan 2359KO)

Africa Region - Project Competion Report - Par UI

PROF:LE OF THE PROJECI

1. Related Bank Loans or Credits

LN 745-KE of 1971 Kamburu Hydroelectric ProjectTRDC (Tana River Development Co.)US$23 million -Fully disbursed

2 LN 1147-KE of 1975 Gitaru Hydroelectric ProjectTRDCUS$63 million - 573 milion disbursedLast disbursement in 1980

3. LN S-12-KE of 1978 Olkaria Geothermal Engineering Project,KPC (The Kenya Power Company)US$9 million - Fully disbursedLast disbursement in 1980 - transferred to LN 1799?

4. LN 1799-KE of 1980 Olkaria Geothermal Power ProjectiKPCUS$40 million - 387 million disbursedLast disbursement in 1987

5. LN 2237-KE of 1983 Geothermal Power ExpansionKPCUS$12 million - $7.5 disbursedLast disbursement in 1987

6. CR 1486-KE of 1984 Geothermal Exploration ProjectKPLC (Kenya Power and Lighting Company)US$24.5 million - fuly disbursedLast disbursement in 1990

7. CR 1973-KE of 1988 Geothermal Development and Energy PreinvestmentProject Government of Kenya - US$40.7 credit.US$31.1 disbursed as of May 25,1993.Credit closes June 30, 1994

17

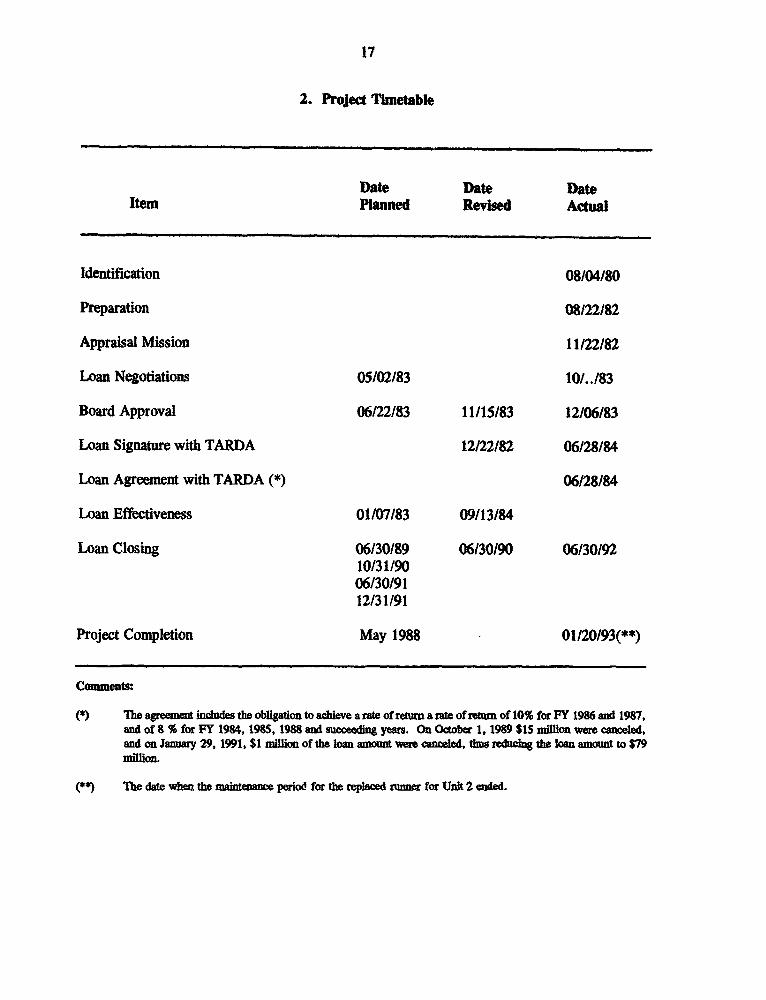

2. Project Tebtable

Date Date DateItem Planned Revised Actual

Identification 08/04/80

Preparation 08S22/82

Appraisal Mission 11/22/82

Loan Negotiations 05/02/83 10/. ./83

Board Approval 06/22/83 11/15/83 12/06/83

Loan Signature with TARDA 12/22/82 06/28/84

Loan Agreement with TARDA (*) 06/28/84

Loan Effectiveness 01/07/83 09/13/84

Loan Closing 06/30189 06/30/90 0613019210/31/9006/30/9112/31/91

Project Completion May 1988 01/20/93(**)

Comments:

(*) ne agreement ince the obligation to achieve a rate of return a rate of return of 10% for FY 1986 and 1987,and of B % for FY 1984, 1985, 1988 and succeeding years. On October 1. 1989 $15 million were canceled,and on Jamuy 29, 1991, $1 million of the loan amount were canceled, thus reducing the loan amount to $79million

(5*) The date wben the makienae period for the replcd runner for Unt 2 ended.

18

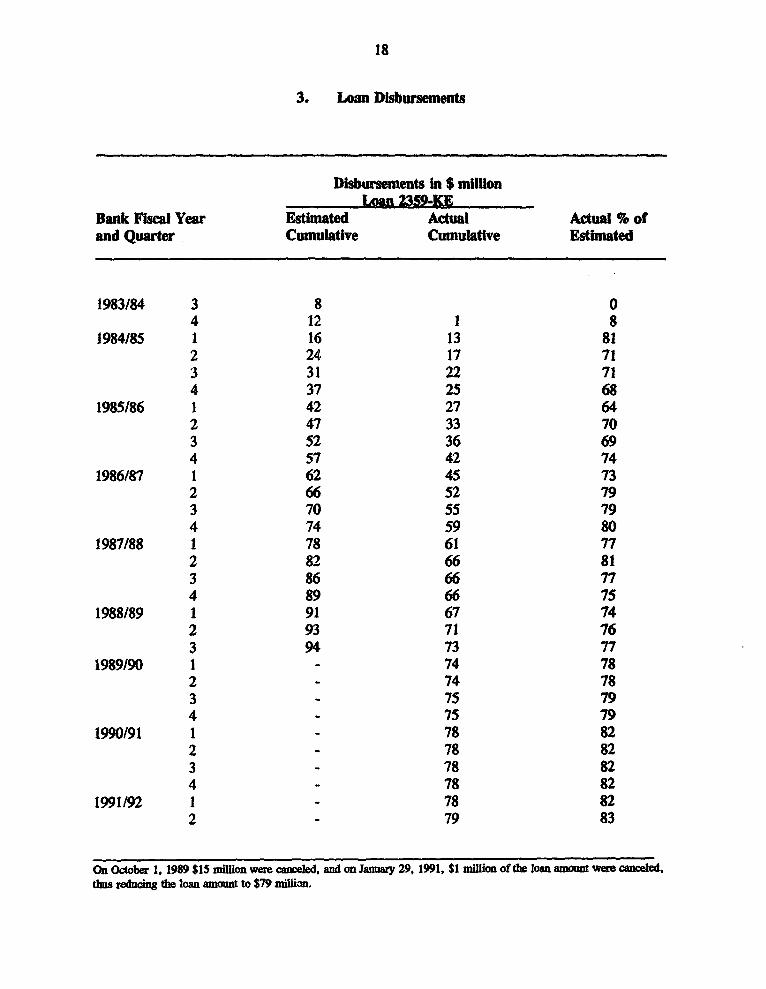

3. Loan Disbursements

Disbursements In $ millionLoan 23S9-S E

Bank Fiscal Year Estimated Actual Actual % ofand Quarter Cumulative CumulatIve Estimated

1983/84 3 8 04 12 1 8

1984/85 1 16 13 812 24 17 713 31 22 714 37 25 68

1985186 1 42 27 642 47 33 703 52 36 694 57 42 74

1986/87 1 62 45 732 66 52 793 70 55 794 74 59 80

1987/88 1 78 61 772 82 66 813 86 66 774 89 66 75

1988/89 1 91 67 742 93 71 763 94 73 77

1989/90 1 - 74 782 - 74 783 - 75 794 - 75 79

1990/91 1 - 78 822 - 78 823 - 78 824 - 78 82

1991/92 1 - 78 822 - 79 83

On October 1, 1989 $15 million were canceed, and on Jamay 29, 1991, $1 million of the loan amount were canceled,dms reducitg the Joan amount to $79 milhin.

19

4. Project Implementation

Indiators Appraial Estimate Actual

Bid Closing May 1983 May 1983

Construction Start Dec. 1983 Feb. 1983

Completion of the Dam June 1987 June 1987

Commissioning of Unit No.1 Feb. 1988 Feb.1988

Commissioning of Unit No.2 June 1988 Feb.1988

Comineus Whie both geneating units were installed in 1988, exensive repairs had to be caied out on the turbinernnr, which had been supphed with defective castigs. ITis procem delayed full availability of both uoits until1989.

20

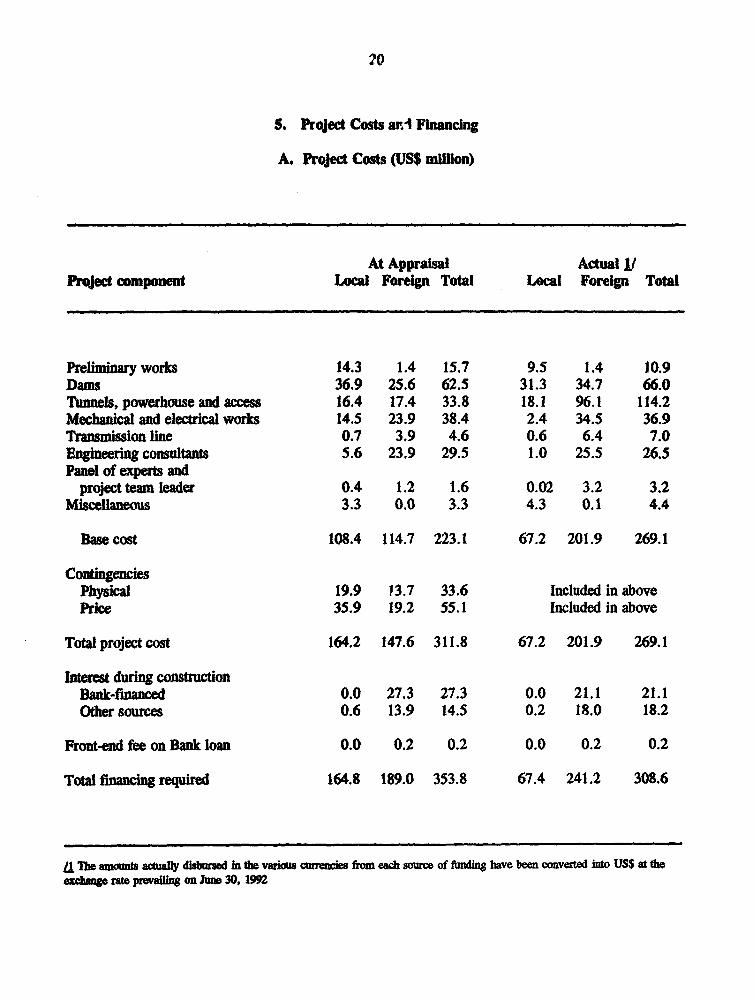

5. Project Costs ar.- FLncing

A. Project Costs (US$ mnllion)

At Appraisal Actual I/Project component Local Forelgn Total Local Foreign Total

Preliminary works 14.3 1.4 15.7 9.5 1.4 10.9Dams 36.9 25.6 62.5 31.3 34.7 66.0Tunnels, powerhouse and access 16.4 17.4 33.8 18.1 96.1 114.2Mechanical and electrical works 14.5 23.9 38.4 2.4 34.5 36.9Transmission line 0.7 3.9 4.6 0.6 6.4 7.0Engineering consultants 5.6 23.9 29.5 1.0 25.5 26.5Panel of expvts and

project team leader 0.4 1.2 1.6 0.02 3.2 3.2Miscellaneous 3.3 0.0 3.3 4.3 0.1 4.4

Base cost 108.4 114.7 223.1 67.2 201.9 269.1

ConingenciesPhysical 19.9 13.7 33.6 Included in abovePrice 35.9 19.2 55.1 Included in above

Total project cost 164.2 147.6 311.8 67.2 201.9 269.1

bnteest during constuctonBank-fianced 0.0 27.3 27.3 0.0 21.1 21.1Other sources 0.6 13.9 14.5 0.2 18.0 18.2

Front-end fee on Bank loan 0.0 0.2 0.2 0.0 0.2 0.2

Tota financin required 164.8 189.0 353.8 67.4 241.2 308.6

L lme amounts acually disbursed in the various currencies from each source of funding have been comverted into US$ at theexasuge rate pevailig on June 30, 1992

21

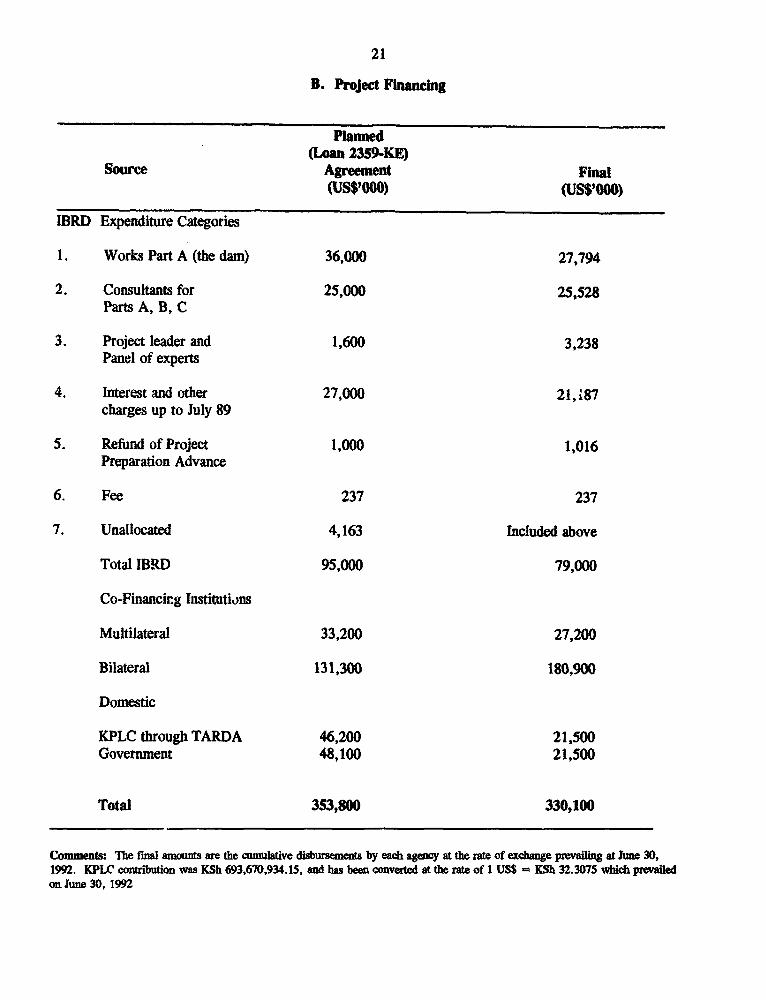

B. Project Financing

Planned(Loan 23591-KE)

Source Agreement Final(US$'000) (US$'000)

IBRD Expenditure Categories

1. Works Part A (the dam) 36,000 27,794

2. Consultants for 25,000 25,528Parts A, B, C

3. Project leader and 1,600 3,238Panel of experts

4. Interest and other 27,000 21,i87charges up to July 89

5. Refund of Project 1,000 1,016Preparation Advance

6. Fee 237 237

7. Unallocated 4,163 Included above

Total IBRD 95,000 79,000

Co-Financing Tstitutions

Multilateral 33,200 27,200

Bilateral 131,300 180,900

Domestic

KPLC through TARDA 46,200 21,500Government 48,100 21,500

Total 353,800 330,100

Comments: The fnal amounts are the amulative disbursemb_ by each agency at fte rste of exchange prevailing at Jhe 30,1992. KPLC contibution was KSh 693,670,934.15, and has been converted at fte rate of 1 USS - KSh 32.3075 which prevailedon Jume 30, 1992

22

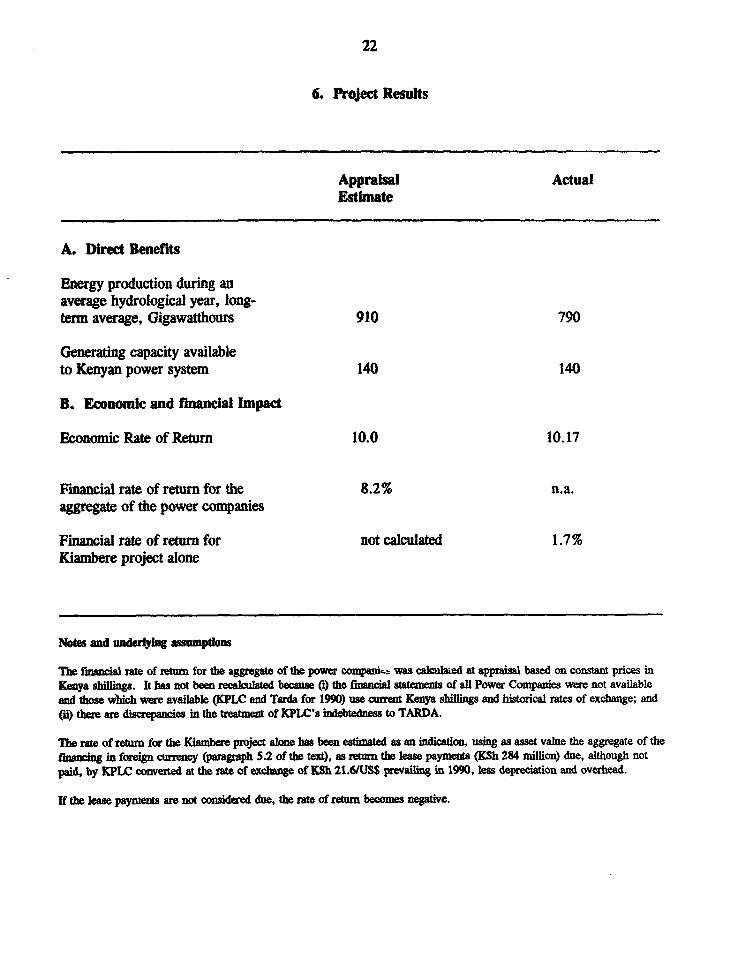

6. Pro3ect Results

AppraLsl ActualEstimate

A. Direct Benefits

Energy production during anaverage hydrological year, long-term average, Gigawatthours 910 790

Generating capacity availableto Kenyan power system 140 140

B. Economic and finandal Impact

Economic Rate of Retun 10.0 10.17

Financial rate of return for the 8.2% n.a.aggregate of the power companies

Financial rate of return for not calculated 1.7%Kiambere project alone

Notes and udeln assump

Mr. fina rate of retum for te aggrgat of the power compan, was v lcalcuied at appraisal based on constant prices inKenya shIm. It has not been recalculated beause ) the finncl stments of all Power Companies were not availableand those which were available (KPLC and Tarda for 1990) use curreat Kenya shillings and histoncal rates of exchange; and(i) ther are disorpancis in the tratmet of KPLC's indebdnss to TARDA.

The rate of return for the Kiambere prject alone has been estaimaed as an indication, using as asset value the aggregate of thefinancing in foreign cuency (paragrph 5.2 of the text), as return the lease payments (KSh 284 million) due, although notpaid, by KPLC converted at the rate of exchange of KSh 21.61USS prevailing in 1990, less depreiation and overhead.

If the lease paymes are not considered due, the rate of rehum becomes negative.

23

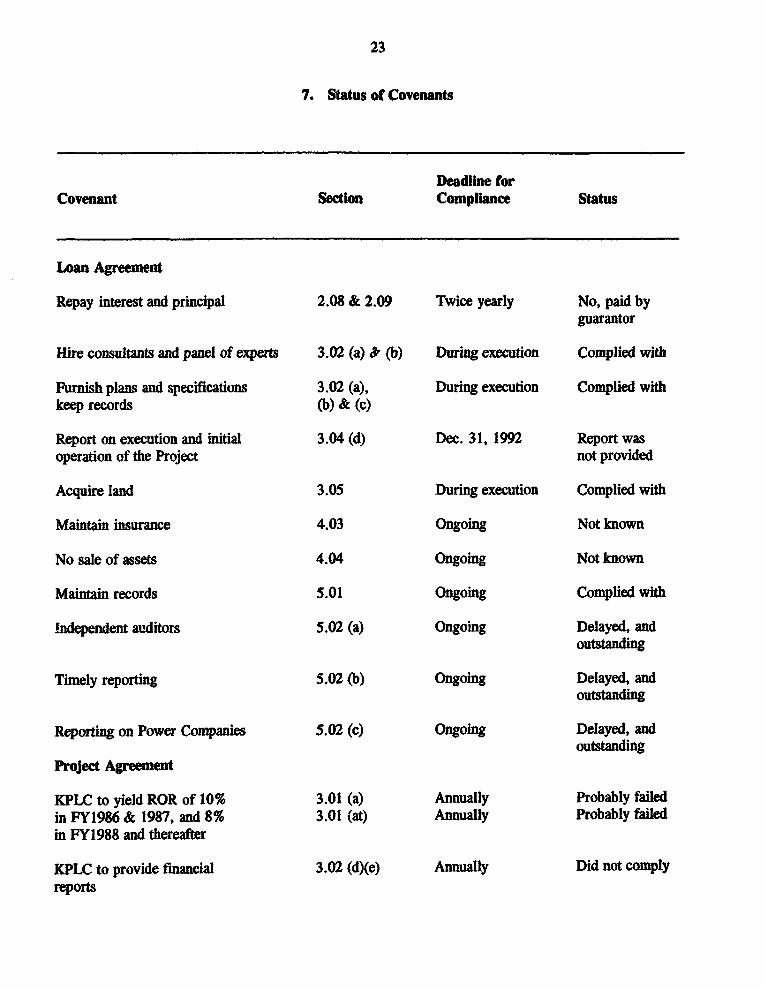

7. Status of Covenants

Deadline forCovenant Section Compliance Status

Loan Agreement

Repay interest and principal 2.08 & 2.09 Twice yearly No, paid byguarantor

Hire consultants and panel of experts 3.02 (a) & (b) During execution Complied with

Furnish plans and specifications 3.02 (a), During execution Complied withkeep records (b) & (c)

Report on execution and initial 3.04 (d) Dec. 31, 1992 Report wasoperation of the Project not provided

Acquire land 3.05 During execution Complied with

Maintain insurance 4.03 Ongoing Not known

No sale of assets 4.04 Ongoing Not known

Maintain records 5.01 Ongoing Complied with

!ndependent auditors 5.02 (a) Ongoing Delayed, andoutstanding

Timely reporting 5.02 (b) Ongoing Delayed, andoutstanding

Reporting on Power Companies 5.02 (c) Ongoing Delayed, andoutstanding

Project Agreement

KPLC to yield ROR of 10% 3.01 (a) Annually Probably failedin FY1986 & 1987, and 8% 3.01 (at) Annually Probably failedin FY1988 and thereafter

KPLC to provide financial 3.02 (d)(e) Annually Did not complyreports

24

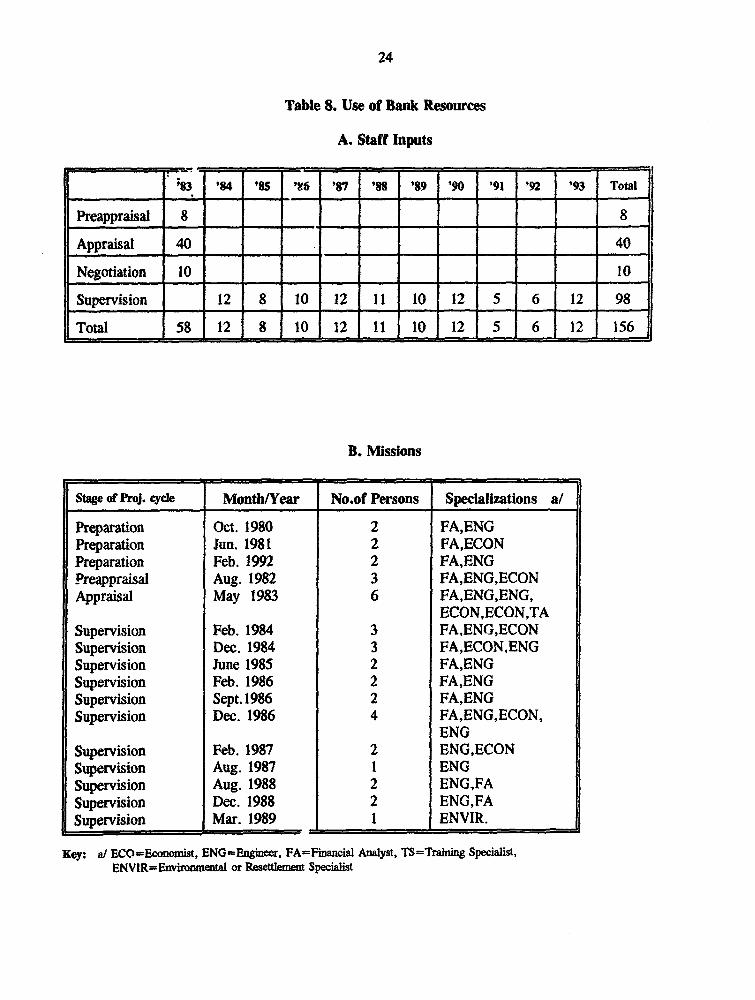

Table 8. Use of Bank Resources

A. Staff Inputs

- _= = _ - - -... _ =

'83 '84 '85 'sft 87 '88 '89 '"0 '91 '92 '93 Total

Preappraisal 8 8

Appraisal 40 40

Negotiation 10 10

Supervision 12 8 10 12 -I 10 12 5 6 12 98

Total 58 12 8 10 12 11 1O 12 5 6 12 156

B. Missions

Stage of Proj. cycle Month/Year No.of Persons Specializations a/

Preparation Oct. 1980 2 FA,ENGPreparation Jun. 1981 2 FA,ECONPreparation Feb. 1992 2 FA,ENGPreappraisal Aug. 1982 3 FA,ENG,ECONAppraisal May 1983 6 FA,ENG,ENG,

ECON,ECON,TASupervision Feb. 1984 3 FA,ENG,ECONSupervision Dec. 1984 3 FA,ECON,ENGSupervision June 1985 2 FA,ENGSupervision Feb. 1986 2 FA,ENGSupervision Sept.1986 2 FA,ENGSupervision Dec. 1986 4 FA,ENG,ECON,

ENGSupervision Feb. 1987 2 ENG,ECONSupervision Aug. 1987 1 ENGSupervision Aug. 1988 2 ENG,FASupervision Dec. 1988 2 ENG,FASupervision Mar. 1989 I ENVIR.

Key: a/ ECO=Economist, ENG=Engineer, FA=Fincial Analyst, TS=Training Specialist,ENVIR=11wmtimenta or Resdeeme Specials