world bank document - documents &...

TRANSCRIPT

Document ofThe World Bank

Report No: 23868 ME

PROJECT APPRAISAL DOCUMENT

ONA

PROPOSED LOAN

IN THE AMOUNT OF US$64.6 million

TO THE

UNITED MEXICAN STATES

FOR A

SAVINGS AND CREDIT SECTOR STRENGTHENING AND RURAL MICROFINANCE CAPACITYBUILDING

TECHNICAL ASSISTANCE PROJECT

Latin America and Caribbean RegionColombia, Mexico and Venezuela Country Management UnitEnvironmentally and Socially Sustainable Development Sector Management Unit

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective June 3, 2002)

Currency Unit = Pesos (P$).P$ 1 = US$0.10

US$1 = P$ 9.65

FISCAL YEARJanuary 1 - December 31

ABBREVIATIONS AND ACRONYMS

AMSAP Asociacion Mexicana de Sociedades de Ahorro y IPDP Indigenous Peoples Development PlanPrestamo

AMUCSS Asociaci6n Mexicana de Uniones de Cridito del Sector ISA International Standards on AuditingSocial

ANAGSA Aseguradora Nacional Agricola KPI Key Performance IndicatorsBANRURAL Banco Nacional de Credito Rural LAC Latin America and the CaribbeanBANSEFI Banco delAhorro Nacional y Servicios Financieros M&E Monitoring and EvaluationBANXICO Banco de Mexico MIF Multilateral Investment FundBP Bank Procedures NCB National Competitive BiddingCAC Cooperativos de Ahorro y Credito NGO Non Governmental OrganizationCAS Country Assistance Strategy MS National and International ShoppingCGAP Consultative Group to Assist the Poorest O0 Outreach IndicatorCNBV Comisi6n Nacional Bancaria y de Valores OP Operational PolicyCOMACREP Consejo Mexicano de Ahorroy Credito Popular PAD Project Appraisal DocumentCONAPO Consejo Nacional de Poblacion PAHNAL Patronato del Ahorro NacionalCPM Caja Popular Mexicana PATMIR Programa de Asistencia T&nica para el

Microfinanciamiento RuralDO Development Objectives PCD Project Concept DocumentEA Environmental Assessment Pi Performance IndicatorsEMP Environmental Management Plan PSR Project Status ReportFBS Fixed Budget Shopping QCBS Quality and Cost-Based SelectionFIRA Fideicomisos Instituidos en Relaci6n con la Agricultura SAP Sociedades de Ahorro y PrestamoFMR Financial Monitoring Report SAGARPA Secretaria de Agricultura, Ganaderia,

Desarrollo Rural, Pesca y Alimentaci6nFOBAPROA Fondo Bancario de Protecci6n al Ahorro SC Supervision CommitteeFSAP Financial Sector Assessment Program SCI Savings and Credit InstitutionGDP Gross Domestic Product SDI Subsidy Dependence IndexGOM Government of Mexico SEDESOL Secretaria de Desarrollo SocialIBRD International Bank for Reconstruction and Development SHCP Secretaria de Hacienda y Credito PuiblicoIDB Inter-American Development Bank SOE Statement of ExpensesIC Individual Consultants SS Single SourceICB International Competitive Bidding TA Technical AssistanceIFC International Finance Corporation TOR Terms of ReferenceILO International Labour Organization TU Technical UnitINI Instituto Nacional Indigenista USAID United States Agency for International DevelopmentIP Impact Performance WOCCU World Council of Credit Unions

Vice President: David de FerrantiCountry Manager/Director: Olivier Lafourcade

Sector Manager/Director: John RedwoodTask Team Leader/Task Manager: Carlos Cuevas

MEXICOSAVINGS AND CREDIT SECTOR STRENGTHENING AND RURAL MICROFINANCE

CAPACITY BUILDING

CONTENTS

A. Project Development Objective Page

1. Project development objective 32. Key performance indicators 3

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project 42. Main sector issues and Government strategy 53. Sector issues to be addressed by the project and strategic choices 8

C. Project Description Summary

1. Project components 82. Key policy and institutional reforms supported by the project 133. Benefits and target population 134. Institutional and implementation arrangements 15

D. Project Rationale

1. Project altematives considered and reasons for rejection 152. Major related projects financed by the Bank and other development agencies 163. Lessons leamed and reflected in the project design 174. Indications of borrower commitment and ownership 185. Value added of Bank support in this project 18

E. Summary Project Analysis

1. Econornic 192. Financial 203. Technical 214. Institutional 225. Environmental 246. Social 247. Safeguard Policies 27

F. Sustainability and Risks

1. Sustainability 272. Critical risks 283. Possible controversial aspects 29

G. Main Conditions

1. Effectiveness Condition 292. Other 30

H. Readiness for mplementation 30

I. Compliance with Bank Policies 30

Annexes

Annex 1: Project Design Summary 31Annex 2: Detailed Project Description 35Annex 3: Estimated Project Costs 40Annex 4: Cost-Effectiveness Analysis Summary 41Annex 5: Financial Summary for Revenue-Earning Project Entities, or Financial Summary 44Annex 6: Procurement and Disbursement Arrangementsand Financial Management Assessment 46Annex 7: Project Processing Schedule 54Annex 8: Documents in the Project File 55Annex 9: Statement of Loans and Credits 56Annex 10: Country at a Glance 59Annex 11: Social Development Model 61Annex 12: Legal and Regulatory Framework and SCI Supervision 67Annex 13: Savings and Credit Sector Information Systems 71Annex 14: Indicators and Projections for Savings and Credit Institutions in Marginal Areas 74Annex 15: Studies, Infonnation Dissemination, Monitoring and Evaluation 80

MAP(S)IBRD 23547

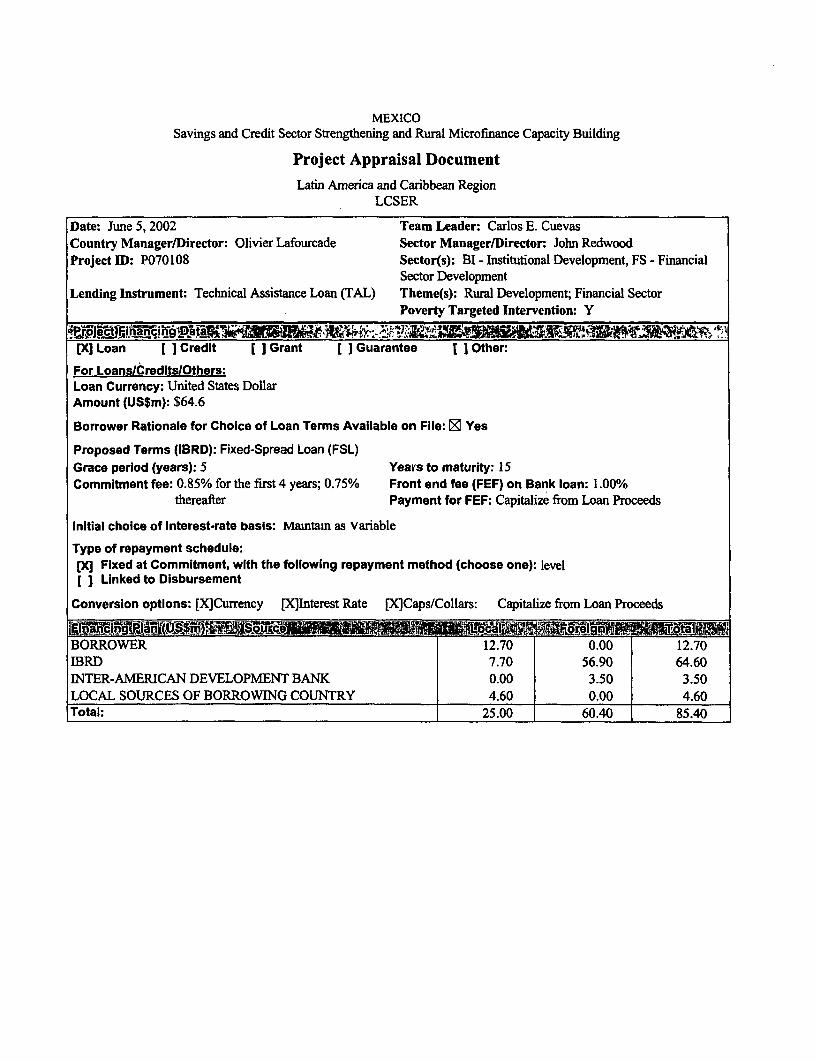

MEXICOSavings and Credit Sector Strengthening and Rural Microfinance Capacity Building

Project Appraisal Document

Latin America and Caribbean RegionLCSER

Date: June 5, 2002 Team Leader: Carlos E. CuevasCountry Manager/Director: Olivier Lafourcade Sector Manager/Director: John RedwoodProject ID: P070108 Sector(s): BI - Institutional Development, FS - Financial

Sector DevelopmentLending Instrument: Technical Assistance Loan (TAL) Theme(s): Rural Development; Financial Sector

Poverty Targeted Intervention: Y

[XI Loan [ ] Credit [ ] Grant [] Guarantee [ Other:

For Loans/Credits/Others:Loan Currency: United States DollarAmount (US$m): $64.6

Borrower Rationale for Choice of Loan Terms Available on File: 1 Yes

Proposed Terms (IBRD): Fixed-Spread Loan (FSL)Grace period (years): 5 Years to maturity: 15Commitment fee: 0.85% for the first 4 years; 0.75% Front end fee (FEF) on Bank loan: 1.00%

thereafter Payment for FEF: Capitalize from Loan Proceeds

Initial choice of Interest-rate basis: Mamtam as variable

Type of repayment schedule:[X] Fixed at Commitment, with the following repayment method (choose one): level[ I Linked to Disbursement

Conversion options: [X]Currency [PXInterest Rate [X]Caps/Collars: Capitalize from Loan Proceeds

BORROWER 12.70 0.00 12.70IBRD 7.70 56.90 64.60INTER-AMERICAN DEVELOPMENT BANK 0.00 3.50 3.50LOCAL SOURCES OF BORROWING COUNTRY 4.60 0.00 4.60Total: 25.00 60.40 85.40

Borrower: UNITED MEXICAN STATESResponsible agency: BANSEFI / SAGARPANational Savings and Financial Services Bank (BANSEFI); Secretariat of Agriculture, Livestock, Rural Development,Fisheries and Nutrition (SAGARPA)Address: BANSEFI: Av. Cuauhtemoc 2, Col. Pueblo de TizapanDel. Alvaro Obreg6n, C.P. 01090, Distrito Federal, Mexico, D. F.; SAGARPA: Insurgentes Sur 489-PHI, Col.Hip6dromo Condesa, C.P. 06100, Mexico, D.F.Contact Person: Javier Gavito (BANSEFI); Gabriela Zapata (SAGARPA)Tel: Javier Gavito: 52-55-5481-3444; Gabriela Zapata: 52-55-5534-1135 Fax: Javier Gavito:52-55-5481-3449; Gabriela Zapata: 52-55-5524-0007 Email: Javier Gavito: [email protected];Gabriela Zapata: [email protected]

Estimated Dlsbursements j Bank FY/US$m):Mg:9Sgti A 90 VO3V' i II w ' i.6VN QQ' 4 K , @g.

Annual 12.40 22.60 14.10 9.20 6.30Cumulative 12.40 35.00 49.10 58.30 64.60

Project Implementation period: June 2002 to June 2007Expected effectiveness date: 09/01/2002 Expected closing date: 12/01/2007

OM:a F*M Fam M. zat-

A. Project Development Objective

1. Project development objective: (see Annex 1)

The proposed project builds upon and enhances the Bank's overall program of strengthening Mexico'sfinancial sector, and providing targeted assistance to the rural poor. The project's main objective is tocontribute to the integration of low-income people into the national economy and to the realization of theirincome generating potential by increasing their access to financial services. To this end, the project aims atimproving the financial stability and outreach capacity of savings and credit institutions (SCIs) nationwide,and especially at expanding financial services in rural areas.

The project also builds upon the recent legal and regulatory reforms the Government of Mexico (GOM) hasenacted to restructure and strengthen the savings and credit sector, a much needed action given the state ofthis sector and especially the loss of confidence in the financial system among the poor. Most notableamong these reforms are the "Popular Savings and Credit Law" (Ley de Ahorro y Credito Popular, June 4,2001), and the law that creates the "National Savings and Financial Services Bank" (Banco del AhorroNacionaly Servicios Financieros, BANSEFI, June 1, 2001, see section B.2).

Specifically, the project will support the strengthening of the SCI sector through specialized assistance tothe retail institutions, enabling these intermediaries to reach more clients with improved services in asustainable manner, and through improving the supervisory capacity of the Comisi6n Nacional Bancaria yde Valores (CNBV) to oversee the SCIs as mandated by the Ley de Ahorro y Credito Popular. Inaddition, as a targeted element of this generalized financial sector strengthening, the project will supportactions to improve the access of low-income rural communities to sustainable financial services. Lastly,the project will include studies and actions designed to increase understanding of the constraints affectingthe extension of financial services to lower-income clients, monitoring the effectiveness of current policyand programs and developing new financial techniques adapted to Mexico.

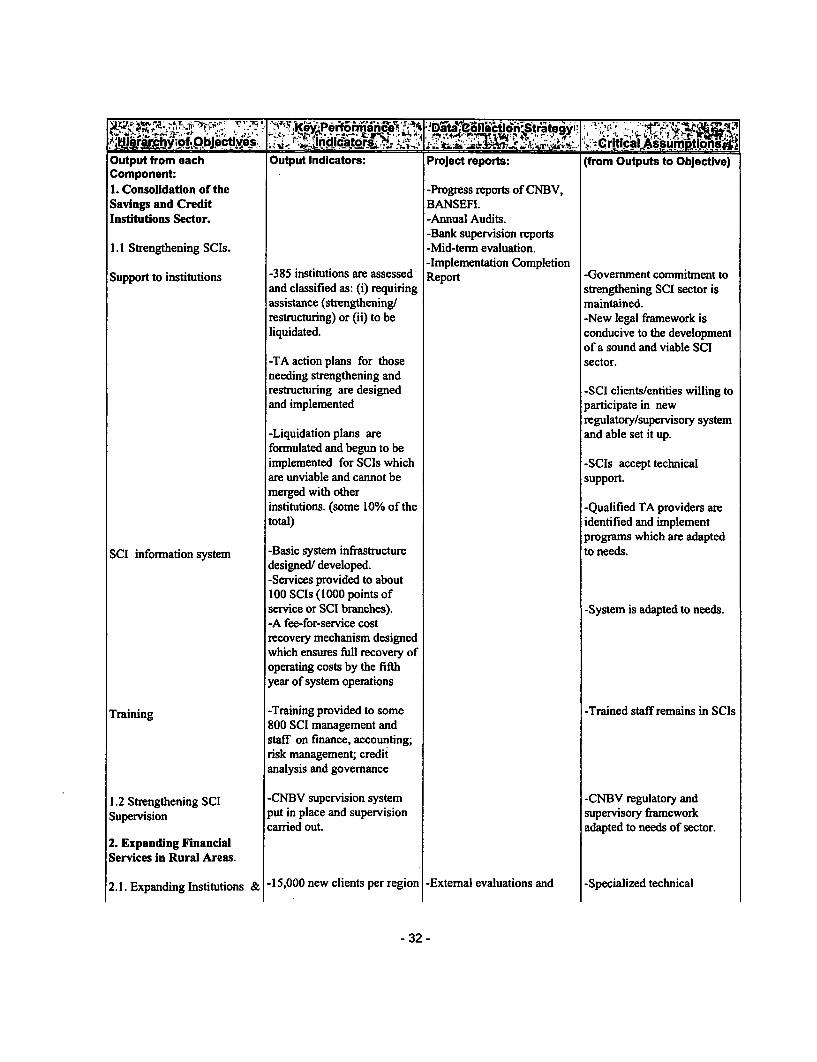

2. Key performance indicators: (see Annex 1)

The key performance indicators listed below are expected to be met by the end of the project and have beenagreed with the implementing institutions. The targets will be monitored throughout the projectimplementation period to assess progress towards achieving project objectives.

Savings and Credit Sector

* The approximately 385 participating savings and credit institutions are assessed and classified intofour categories as follows: (a) qualify for certification into the new legal system (by CNBV) and mayrequire assistance to modernize and expand outreach; (b) require capacity-building to make them eligiblefor certification; (c) require major restructuring (e.g., merger with or acquisition by another SCIs); or (d)are unviable and will be liquidated.

* Technical assistance plans are designed and put in place for those institutions which requirestrengthening or restructuring - categories (a) though (c) above. As required, liquidation plans areprepared and begun to be implemented for unviable institutions. Some 300 or 80 percent of institutions areexpected to benefit from technical assistance for strengthening or restructuring.

* Institutions benefiting from technical assistance qualify for certification.

- 3 -

* Basic information SCI system designed and developed. Services provided to about 100 SCIs thatrepresent approximately 1000 points of service (SCI branches). A fee-for-service cost recovery mechanismwill be designed that will have as objective the full recovery of operating costs by the fifth year of systemoperations.

* Approximately 800 SCI management and staff are trained in accounting, credit analysis, riskmanagement and govemance.

* CNBV supervision system is put in place. Some 200 institutions are expected to be under CNBVsupervision, under the auxiliary supervision system envisioned for the sector, at the end of the project.

Rural Microfnance

* Some 60,000 clients are served in project marginal areas at the end of the project. Participatinginstitutions meet criteria for certification by CNBV.

* Approximately 8,000 families in rural communities receive training (functional education) infinancial matters.

Monitoring and Dissemination

* Monitoring system covering performance of SCIs and federations, including the project-supportedrural microfinance institutions, and the program's social impact is put in place at BANSEFI.

* Dissemination campaign on SCI sector reform designed and put in place.

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project: (see Annex 1)Document number: R2002-0073; IFCR2002-0055 . Date of latest CAS discussion: 05/16/2002

The joint IBRD/IFC CAS is structured along five main thrusts - macroeconomic sustainability,enhancedcompetitiveness, human development, environmental protection, and good governance. It sets forth anintegrated approach to broad-based, sustainable growth for poverty reduction with a strong private-sectorrole. The proposed project contributes to the integration of a broad range of households, includinglower-income and rural-based clients, into a sustainable growth process, reinforcing the social stability andoverall capitalization of those segments of the population, especially rural communities. By improvingaccess to reliable financial services, especially savings, and helping create sustainable financialintermediation networks in rural areas, the project alleviates one of the major constraints to socialintegration and rural development. The project builds upon and complements the financial sectorstrengthening objectives of the Bank Restructuring Facility projects (No. 70600 and 70030), and the ruralpoverty alleviation objectives of the Rural Development in Marginal Areas program (No. 19877). It alsofollows on sector work carried out in 1995 (Rural Financial Markets, Report No. 14599-ME), 1997(Mobilizing Savings for Growth, Report No. 16373-ME) and 2000 (Rural Savings Mobilization, ReportNo. 21286-ME), and uses guidance resulting from the joint Bank/Fund FSAP mission of March 2001.

-4-

2. Main sector issues and Government strategy:

The Savings and Credit Sector

The non-bank financial sector, and savings and loan institutions in particular, has a significant and growingpresence in areas and among clients not traditionally served by banks in Mexico. Non-bank financialintermnediaries in Mexico include a multiplicity of fornal and informal, regulated and unregulatedinstitutions which mobilize deposits from and/or extend credit to the public. Among formal non-bankintermediaries (i.e., licensed under a law) are those which are regulated as financial institutions, includingSociedades de Ahorro y Prestamo (SAPs) and Credit Unions, and those which are not, including CajasPopulares, Cooperativas de Ahorro y Credito , Cajas Solidarias, NGOs and others. Savings and creditinstitutions (SCIs), in this document, refer to both of these types of formal intermediaries. Informalintermediation, on the other hand, which is unregulated and not legally sanctioned, includes rotating savingsand credit associations (tandas), money lenders, savings groups and other personal savings and loanarrangements, which are not dealt with in this document.

It is estimated that the SCI sector, comprised of more than 630 institutions, extends savings and loanservices to approximately 2.3 million people or (about 7 percent of the economically active population) andhas assets of more than US$1.4 billion (or approximately I percent of banking sector assets). The SAPnetwork alone includes nearly 400 retail outlets with 500,000 members in 31 states. For many of theseSCIs, full reliance on mobilized deposits to support their loan portfolios protected them from the 1995cunrency crisis, as they had practically no foreign-currency liabilities. In addition, it gave the savings andloan societies an advantage vis a vis the banling system, as they were able to lend when banks weredrastically contracting credit flows. Well-fimctioning savings and credit institutions were thus able toattract new members and grow in scale when most of the rest of the financial system was shrinking.

While the relative stability and extension of the SCI sector towards lower-income and rural clients hasprovided for alternative access to financial services where commercial and development banks have notbeen successful, the lack of effective regulation and supervision until the passage of new legislation lastyear has meant that these institutions and their depositors are exposed to significant risks. These risks havebeen made apparent by several SCI failures, some of them openly fraudulent, which have seriouslyundermined public confidence in these institutions, especially among small depositors. Restoring clientconfidence, and enhancing the ability of financial intermediaries to reach more people thus became criticalobjectives of the Mexican administration.

Against this background, Government has embarked on a strategy to strengthen financial intermediariesactive among all market segments, including banks and non-bank institutions. The banking sector hasbenefited from a strengthening process supported by the Bank Restructuring Facility. Moreover, the recentBank/Fund FSAP mission has outlined additional strengthening measures, including a framework for therationalization of public development banks. In order to increase access to services and enhance thereliability of those services among lower-income households, which traditionally do not benefit frombanking services, the Government has devised a strategy towards strengthening and effectively supervisingSCIs. This strategy aims at further developing the capacity of these intermediaries, modernizing theirservices, substantially improving their image among the general public and increasing their overalloutreach, especially in rural areas.

To this end, key government entities concerned with financial sector issues, the Secretariat of Finance andPublic Credit (SHCP), the National Banking and Securities Commission (CNBV) and the Central Bank of

- 5-

Mexico (BANXICO), with Bank collaboration, and in close consultation with the practitioners and thelegislature, developed a new legal and regulatory framework for savings and credit institutions andorganizations (instituciones de ahorro y credito popular), perceived to hold a high potential to expandinstitutional outreach to under-served sectors of the population. In reality, the diverse range of non-bankfinancial institutions operating in Mexico serves a continuum of clientele, from the relatively wealthy topoor, marginalized households in rural and urban areas alike. (See Section C.3. for details on SCIs andclient profiles). The Ley de Ahorro y Credito Popular was passed on April 30, 2001 and became effectiveon June 4, 2001. It provides for the incorporation of all savings and credit (non-bank) financial institutionsinto a legal framework that covers the range of their intermediation activities.

The law recognizes two types of retail intermnediaries authorized to mobilize deposits from the generalpublic: Savings and Credit Cooperatives (Sociedades Cooperativas de Ahorro y Credito), and PopularSavings Associations (Sociedades Financieras Populares). After a period of two years from the date of thelaw's effectiveness, only those institutions which are able to demonstrate their financial viability, whichsubject themselves to regulation and supervision and which purchase private deposit insurance will beauthorized to remain in operation. Regulation and supervision will be tailored to four different categories ofSCIs, depending on the scale and types of liabilities and assets, number of shareholders or clients, nunberof branches, geographic coverage and technical operating capacity. More developed institutions will begranted authorization to provide a greater range of services and products, while being subject to stricterstandards than less developed ones. The institutional framework prescribed by the legislation will requireaffiliation in Federations, which will monitor and oversee SCI activities and status according to CNBVguidelines and under its overall sector monitoring.

The CNBV, per mandate of the new law, becomes the sole regulatory and supervisory authority fornon-bank entities providing savings and credit services and has the responsibility of issuing all rules andregulations associated with the new law. In this manner, the law aims at eliminating the opportunities forregulatory arbitrage that have thus far characterized the Mexican legal framework. The regulatory andsupervision framework for "popular savings and credit" institutions has thus been designed to be consistentwith the laws mandating prudential nonus and governing the activities of banks and other financialinstitutions.

While the CNBV is in charge of SCI supervision, the newly created BANSEFI has been charged with theresponsibility of developing the capacity of and preparing SCIs for their integration into the new system,and supporting the fornation and strengthening of the Federation(s) of SCIs and their associated auxiliarysupervisory bodies (Comites de supervisi6n) which will assist CNBV in its supervisory role. BANSEFI, assuccessor of the Patronato del Ahorro Nacional (PAHNAL) will continue to provide secure savingsinstruments to low-income clients and to educate and encourage savings habits among the public, but inaddition to PAHNAL's retail savings services functions, BANSEFI will arrange the provision of technicalsupport to savings and credit institutions, provide second tier central banking services, excluding on-lendingof funds, and will coordinate the Government's programs to develop the SCI sector.

On the practitioners's side and as a reaction to the legal reforms, the numerous entities in the sector created(in February 2001) the Consejo Mexicano de Ahorro y Credito Popular (COMACREP), whichencompasses all major second-level organizations (such as that of the SAPs, AMSAP, of the Uniones deCredito, AMUCSS, of the non-cooperative microfinance institutions, PRODESARROLLO, and the mostimportant confederations of savings and credit cooperatives, e.g., UNISAP, among others). TheCOMACREP, thus claiming at least 80 percent of the SCI sector by any measure of scale (clients, assets,deposits), is carrying the dialogue with the official entities involved, notably CNBV and BANSEFI, on bothregulatory and developmental issues.

-6 -

The Government of Mexico has requested Bank assistance to prepare SCIs for incorporation into thesystem and to build capacity among sector institutions to effectively provide supervision, monitoring andinstitutional strengthening functions. In addition to the SCI sector stabilization, integration and supervisionprogram, the Govermnent has sought Bank support for the preparation of a program to increase theoutreach of savings and credit institutions and organizations in rural areas, as well as to provide technicalassistance and training in poor, rural cornmunities interested in increasing formal savings.

Financial Services in Rural Areas

Rural Finance in Mexico suffers at present two main consequences of past government strategies: (i) ratesof participation in formal financial transactions for rural entrepreneurs and households lower than those incountries with one-half of Mexico's per capita GDP; and (ii) a severe scarcity of viable or potentiallysustainable financial institutions with a significant presence and outreach among low-income households,particularly in rural areas.

Directed credit at subsidized interest rates, subsidized credit guarantees, and debt forgiveness andrestructuring characterized rural credit in Mexico during the 1980s and early 1990s. Key public ruralfinance institutions, namely the Banco Nacional de Credito Rural (BANRURAL) and the FideicomisosInstituidos en Relaci6n con la Agricultura (FIRA) were the main means of intervention. In addition, theAseguradora Nacional Agricola (ANAGSA, closed in 1990) insured most of BANRURAL loans atsubsidized premium rates. These interventions created heavy fiscal outlays, estimated in the period1983-1992 at approximately US$28.5 billion (an annual average of about 13 percent of agricultural GDP),of which US$23.1 billion (81 percent) were associated with subsidized interest rates.

The government began introducing reforns in rural credit policies in the early 1990s, intended to reducetransfers to the sector and improve efficiency of its rural finance institutions. It reduced interest-ratesubsidies, made transfers to institutions more transparent and closed or reorganized inefficient governmententities.

The exchange-rate crisis of early 1995 induced further closings of rural branches by struggling banks, thusdiminishing the already dwindling presence of financial institutions in rural areas (then limited to less thanone third of the country's municipalities, including offices of development banks). Subsequent Bankdialogue with government focused on providing an environment conducive to increasing the outreach andsustainability of formal financial intermediaries in rural areas, as opposed to the traditional directintervention. Specifically, a Rural Finance Technical Assistance loan was approved in 1996 with theobjective of reviewing Government participation in the sector; and developing a package of appropriatefinancial products, lending technologies and incentive schemes to provide sustainable financial services tolow income populations through private, commercial banks. The project was not successfully implementeddue, in part, to the financial crises and controversial rescue package provided by the Banking Fund forSavings Protection (FOBAPROA), which induced commercial banks into much more conservativeapproaches. Banks chose the pursuit of profitable opportunities in their existing urban markets overexperimentation and the substantial investments in infrastructure and staff training needed to move into lessunderstood rural markets. Moreover, a collusive attitude among commercial banks and a struggle betweenGovernment offices for control over the initiative hampered the project viability and resulted in its closingin late 1999.

Currently, the Secretariat of Agriculture, Livestock, Rural Development, Fishing and Food (SAGARPA),and the Secretariat of Finance (SHCP) are concemed with increasing the presence of reliable financial

-7 -

intermediaries in rural areas as an essential base for a healthy development of savings and othermicrofmnance activities, and a restoration of rural people's confidence in the financial sector. In addition,SAGARPA is encouraging the establishment of adequate linkages mechanisms between emerging ruralcommunity funds (usually formed among producers that benefit from SAGARPA's transfer programs) andsustainable intermediaries that conform to the new law. The Secretariat requested Bank support tosubstantially re-structure and re-design a support program initiated in 2000 (the Programa de AsistenciaTecnica para el Microfinanciamiento Rural, PATMIR, which had no Bank support in 2000). This requestprovided an opportunity to ensure that activities under this program are fully consistent with the new legalreform and regulatory fiamework, and that institutional development approaches are coherent with those tobe applied for the implementation of this new framework.

3. Sector issues to be addressed by the project and strategic choices:

The focus on existing SCIs represents a major shift in both the Government and the Bank's strategy tosupport improved access to formal financial services for broad segments of the population in Mexico ingeneral, and for poor rural households in particular. Drawing upon GOM's clear and coherent approach toconsolidating and strengthening the SCI sector, the proposed project addresses the issues associated withthe installed institutional capacity for financial intermediation in the sector, its potential for sustainablegrowth and the public confidence the sector conveys. In addition, the project supports actions thatcontribute to CNBV's capacity to effectively supervise the SCIs.

The project places emphasis on providing sustainable SCI services in rural areas and strengthening thecapacity of communities to mobilize and manage savings in ways which reduce the costs of access toformal savings services. In addressing intermediation capacity in rural areas, the project will work both onthe demand side and the supply side of financial services. On the demand side, it will enhance the abilityand skills of local communities to organize and manage savings programs and capitalization of funds byproviding technical assistance and training to local groups. On the supply side, the project will work withSCIs to enhance their sustainability and incorporate them into the new legal fuamework. In selectedmarginal areas, the project will focus on developing financial instruments adapted to the needs, habits andculture of rural communities.

C. Project Description Summary

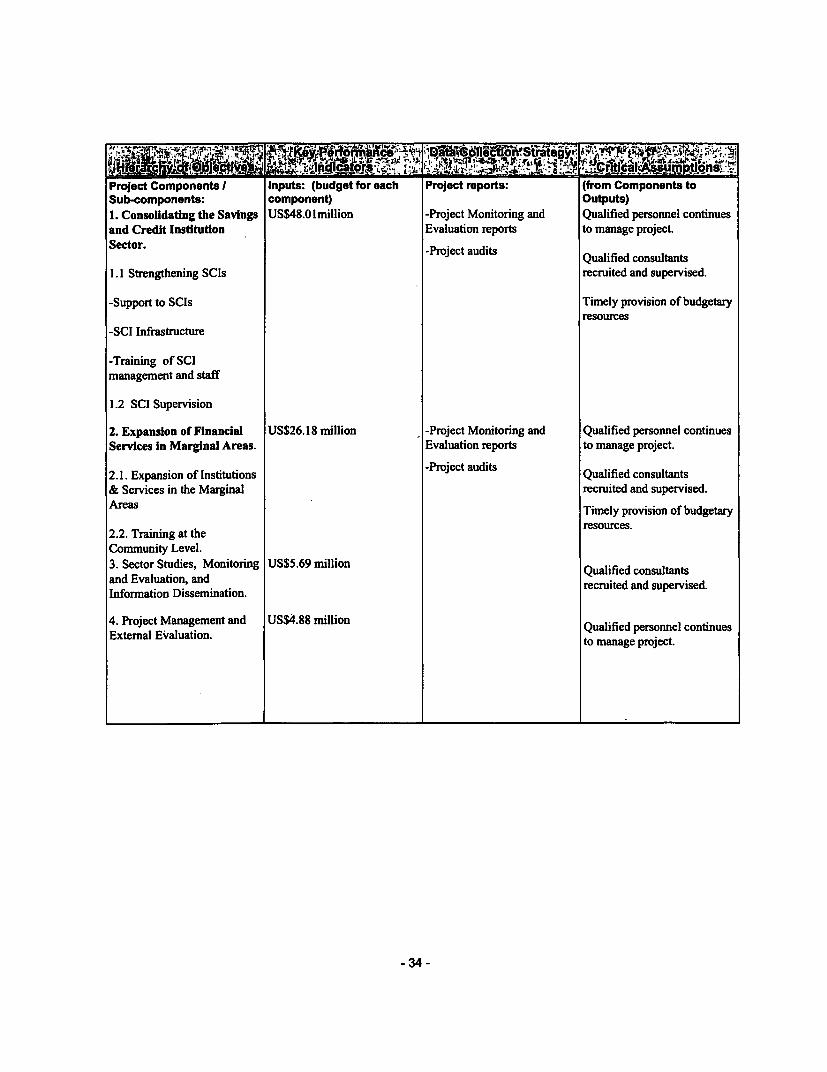

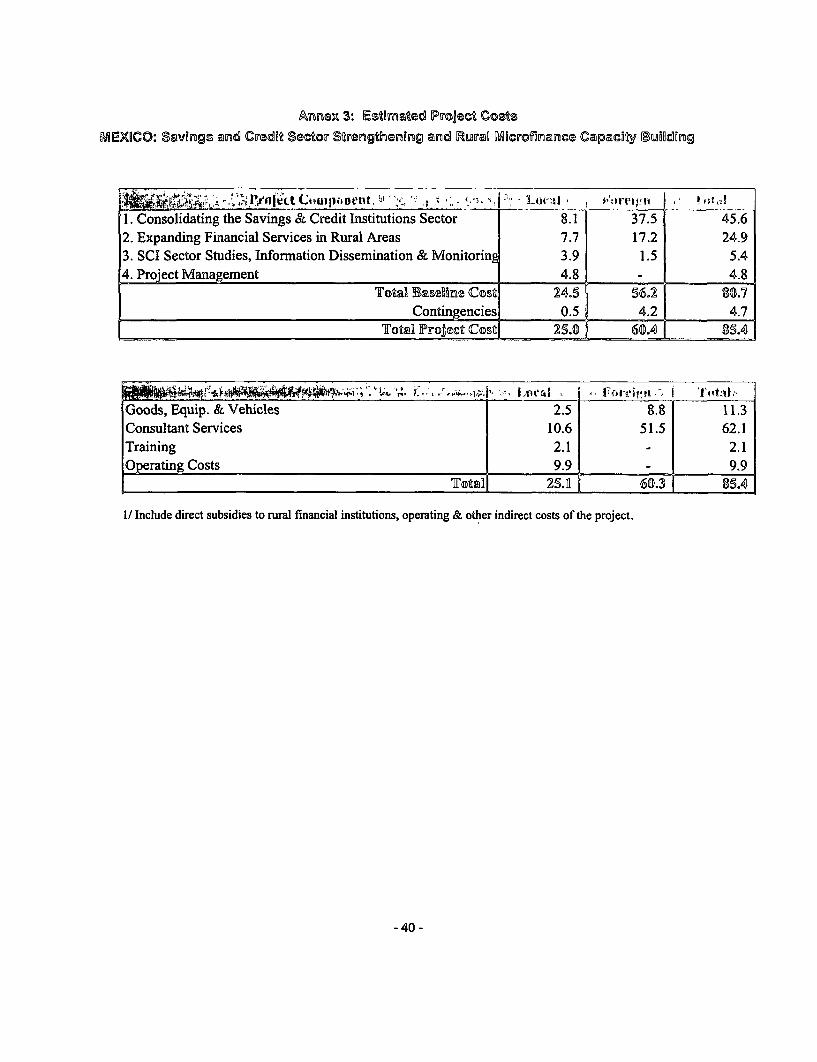

1. Project components (see Annex 2 for a detailed description and Annex 3 for a detailed costbreakdown):

The project supports the Government's efforts to strengthen the SCI sector, which serves the poorersegments of the market, so that sector institutions are able to provide secure and expanded services, andover time, increase their coverage. In addition, because rural areas are seriously underserved and becauseof the intrinsic problems in serving clients in this market, the project includes programs aimed at improvingaccess of rural communities to sustainable financial services. The main components of the project aresummarized below.

Component 1: Consolidation of the Savings and Credit Institutions Sector

The project supports a program to strengthen eligible institutions and liquidate institutions which are notsustainable, to improve SCI sector infrastructure, and to enhance sector supervision. As per its mandate,BANSEFI will manage the technical assistance programs. CNBV is the sole responsible for theauthorization of SCIs to operate as financial intermediaries.

- 8-

1.1 Strengthening SCIs

Support to Institutions. The project will support an assessment of existing SCIs to detennine whether thesequalify for certification by CNBV, require technical assistance either to strengthen or to restructure them(e.g., mergers or acquisitions), or need to be liquidated. Evaluation criteria have been prepared by a teamled by CNBV, and consisting of national and international specialists. It is expected that 385 institutionsoperating in rural and urban areas, with 1.8 million members or 78 percent of total sector membership, willparticipate in the program. Preliminary analysis shows that some 80 percent of institutions would meet thecapitalization requirements for certification provided they take measures to strengthen their management,financial performance and operations, or undertake some form of restructuring.

The project will support the preparation and implementation of plans to strengthen institutions which canbe strengthened or restructured and which have agreed to carry out plans to gain CNBV certification. It isanticipated that the institutional strengthening plans will last between one and two years, depending on thesize of the institution. BANSEFI will recruit institutions which are specialized in the provision of theseservices (referred to as technical assistance providers) to carry out the initial assessment using CNBVguidelines, and to prepare and implement the institutional strengthening plans. The technical assistanceproviders will enter into fornal agreements with the participating SCIs and their corresponding Federationsspelling out the program and the performance standards to be met in a designated time period. BANSEFIwill monitor the results of the technical assistance program and will review progress on a semi-annualbasis. BANSEFI intends to suspend assistance to institutions which do not achieve the agreed semi-annualtargets. In addition, CNBV intends to verify on a sample basis the accuracy of the classification given atthe outset to the institutions participating in the program. The CNBV will conduct its own evaluation of theinstitutions when the technical assistance program is completed, and decide independently whether theinstitutions are to be authorized under the law.

The project will also support, as required, the liquidation of institutions which have been determinedunviable and present risks to deposit-holders. As the legal status of sector institutions is very diverse,support for liquidation will be determiined on a case-by-case basis.

Technical assistance providers will be selected from among specialized institutions with demonstratedexperience in the field. The providers will support all institutions in a Federation (or ascribed to aFederation for supervision purposes) which are willing to enter into specific agreements. The Government,with financing by the Bank, will pay for the costs of the technical assistance program. The beneficiarieswill contribute some logistical support to the consultants. The participating institutions will also pay forthe full cost of the Federations which are being established as required by law. The loan does not includefinancing to shore up the capital, which may be required in the case of a few institutions. The contacts willcover the costs of the international and national specialists required to carry out the institutionaldevelopment plans as well as expenses directly associated with their work, including equipment andmaterials. No vehicles will be financed by the loan.

Providing SCI Information Infrastructure and Services. The project will support the design andestablishment of an information system for the sector as part of an integrated effort aimed at strengtheningthe SCIs, their federations and the sector at large. The informnation system will enable sector institutions toprovide required financial reports to the CNBV as their supervisor, and to other relevant governmentagencies. It will also have the capability to maintain accounts and financial inforrnation, and to provideother operational, control and reporting services, upon request by the institutions.

The core system will reside and will be operated at BANSEFI. The SCIs will link to the system with

-9-

equipment, software, technical assistance and training provided by the project contractors. This componentwill support the design and development of the basic system infrastructure and software, and the provisionof services to about 100 SCIs that represent approximately 1000 points of service (SCI branches). TheGovernment will pay, with Bank financing, for the system development costs. A fee-for-service costrecovery mechanism will gradually be put in place that will have as an objective the full recovery ofoperating costs by the fifth year of system operations. The requisite telecommunications infrastructureexists in Mexico. BANSEFI has confirmned interest and service capacity from data commnunicationsproviders to participate in bids for provision of services to the information systems to be set up byBANSEFI.

It is anticipated that implementation of this component will be canied out in the first year of the project. Acomplementary initiative, expected to be prepared pari pasu with implementation and likely to constitute anew request for financing from the Government of Mexico, will enable the national roll-out of the system.This sequencing of efforts is fully consistent with the expected pace of SCI rehabilitation and strengthening,and follows international good practice in systems development for comparable scenarios.

Trainingprogramfor SCIstaff The project will support the implementation of a training program forSCI management and staff. The program will include modules in the areas of finance, accounting, riskmanagement, credit analysis and govemance and will be offered in six regions. The training, which will beavailable to all participating institutions, will be carried out by specialized consultants (for accounting)and tuaning institutes for the other subjects. It will be implemented over a two year period. Some 800members of participating institutions are expected to participate in the training. The Federations andmember institutions will provide the physical facilities for the courses and will pay for the transportationand living expenses of its participants in the courses.

1.3 Strengthening SCI Supervision.

The project will provide support to CNBV to strengthen its supervision procedures and competencies. Tothis end, it will provide training to CNBV staff on supervision practices and procedures for microfinanceinstitutions and technical assistance to CNBV to develop and adapt regulations as needed. In addition,CNBV will engage the advice of recognized international experts in systems of auxiliary supervision (e.g.,Germany, Canada, Spain) on a regular, semi-annual basis. The project will also provide technicalassistance to strengthen the Supervision Committees (Comites de supervisi6n) at the Federations,specifically charged with the auxiliary supervision flmctions. It will also provide support to theConfederations that group them. This support aims at ensuring clear definition of the functions of theFederations (and the Confederation that will group them), and specifically a demarcation between theauxiliary supervision role and other fimctions. The support to CNBV and the sector will seek to establishrules and procedures that ensure professional and transparent handling of entry and exit, and address andmitigate risks of conflict of interest, adverse selection and other issues that may emerge in the process ofimplementing the supervisory mechanism. The loan will finance technical assistance and training requiredto carry out the activities.

Component 2: Expanding Financial Services in Rural Areas

This component ains at expanding the supply of financial services the marginal areas, and builds uponwork initiated under the marginal areas progrmsu. The project will cover the marginal areas in some elevenstates. Activities under this component will be carried out by specialized international technical assistanceproviders under contract with the implementing agency.

-10-

2.1 Expanding Institutions and Services in the Marginal Areas

The component aims at increasing outreach, ensuring financial sustainability, and improving anddiversifying the financial services offered by existing intermediaries that serve the marginal areas. In areaswhere no intermediaries exist, new institutions will be established using proven methodologies and whichwill fully comply with existing legislation. Participating institutions will be selected on the basis of theirtrack record in terms of outreach and sustainability, and their expansion plans. Institutions supported underthis component are likely to be'regional institutions, as these are the most inclined to serve the targetclientele. The participating institutions would enter into agreements with the technical assistance providerscommitting to perfomiance targets which will be closely monitored. Program activities will encouragecommitment and ownership at the local level while setting up institutional policies and structures thatencourage efficiency and profitability. The process will take time because new habits and skills will needto be developed. All participating SCIs will join or will be assigned to a Federation for supervisionpurposes, as mandated by the law, and will meet the requirements for certification by CNBV. The programdoes not include a line of credit, and it is expected that most of the credit given by participating institutionswill be from members' savings.

The marginal areas will be grouped into regions for developmental purposes. The population of themarginal areas covered total some 17 million people. The program will be implemented in six of thefollowing eight regions: (i) Chiapas, (ii) Huasteca (marginal areas in the States of Hidalgo, San Luis Potosiand Veracruz), (iii) Oaxaca, (iv) Veracruz excluding the Huasteca (v) Guerrro (and adjacent marginalareas in the State of Morelos), (vi) Michoacan (and adjacent marginal areas in the State of Mexico), (vii)Puebla (and adjacent marginal areas in the State of Tlaxcala) and (viii) Sierra Gorda (marginal areas inthe States of Queretaro and Guanajuato). The municipalities covered by the program appear in a documentprepared by SAGARPA which is based on the classification of the CONAPO for levels of marginality. Theregions have been selected taking into account the demand for services identified in market studies, and thewillingness of institutions or groupings of clients in the region to enter into performance agreements withthe technical assistance providers. The sequencing of the regional programs has also been determined onthe basis of the studies, although this order may be modified if developments justify advancing a regionahead of others.

The technical assistance providers will be selected following World Bank procedures. The process ofselection of the technical assistance provider which will implement the program in Chiapas is completeand the program will be initiated this month. The process of selection of the technical assistance providerfor the Huasteca Region is well advanced, and work should start later this year. At the end of five years ofthe project, some 60,000 families will be served in the six regions where the program will have beeninitiated. This figure takes into account that some of the regional programs would only be in their third yearof operation. Given that the regions served under the program have few existing institutions, much of theexpansion of services will come thrugh the establishment of new branches or new institutions. Some15-20 new branches (or local institutions) should be established in each of the marginal areas covered. Thecontracts will cover the costs of the intemational an national specialists required to carry out the regionaldevelopment plans as well as expenses directly associated with their work, including equipment andmaterials. No vehicles will be financed by the loan.

2.2 Community Training Programs (Social intermediation)

The project will provide training to the poorer segments of the population in the marginal areas on basicprinciples of household finance and participation in financial transactions. In some cases, the program willassist communities to set up simple record-keeping for indigenous savings organizations, and introduce

- 1 1 -

them to forrmal institutions where they could set up formal accounts. Activities under this sub-componentwill be organized by the same technical assistance providers that will provide services undersub-component 2.1.

Component 3: SCI Sector Studies, Information Dissemination, Monitoring and Evaluation

This component aims at increasing understanding of the constraints affecting the provision of financialservices to low-income clients, at monitoring and evaluating the effectiveness of policies and programs, andat developing financial innovations adapted to Mexico. The project will finance consulting services andpreparation of information materials under this activity.

3.1. Sector-wide activities

Activities under this component include studies on, inter alia, financial intermediation, sector performanceand auxiliary supervision with a view to identify explanatory factors for performance, draw lessons fromthe Project results and identify areas for improvement and innovation. In addition, the component includesdissemination programs, including workshops and information campaigns, to inform SCIs, their clients andother stakeholders of the sector consolidation and strengthening program, and to disseminate lessons fromexperience in the areas of microfinance, savings mobilization, and auxiliary supervision. Disseminationefforts will also include the general public, with emphasis in the low-income segments of the population.The project will also support the introduction of systems to monitor sector development progress and theimpact of the government's development programs. The sector studies and monitoring function will becarried out at five different levels: (i) SCI supervision mechanism; (ii) SCI performance; (iii)federation/network performance; (iv) social and economic impact; and (v) fiscal impact. Lastly, thecomponent will also support periodic extemal evaluations by national and international consultants.

3.2 Rural microftnance activities

Studies will also cover financial intermediation in rural areas and other areas underserved by the Mexicanfinancial sector, with a view to defining new methodologies which are adapted to local conditions. includingtechnical and financial audits of the rural microfinance institutions supported under the project, and expertadvice to the project management team. This component will support monitoring and evaluation activitiesspecific to the implementation of component 2 (rural areas), including technical and financial audits ofSCIs supported under the rural finance component.

Component 4: Project Management

BANSEFI and SAGARPA are conscious of the importance of a strong project implementation team tocoordinate and supervise the work the consultants contracted to carry out the project activities, and haveassembled a strong team for this purpose. The project will support the operations of a Core Team atBANSEFI and of SAGARPA's technical unit which have been set up to carry out project management andimplementation follow up, including monitoring and evaluation of the activities.

- 12 -

Institutions Sector Development .

2. Expanding Financial Services in Institutional 26.18 30.7 19.48 30.2Rural Areas Development

3. SCI Sector Studies, Information Financial Sector 5.69 6.7 4.67 7.2Dissemination, Monitoring & DevelopmentEvaluation

4. Project Management Institutional 4.88 5.7 1.57 2.4Development

Total Project Costs 84.76 99.3 63.96 99.0Front-end fee 0.64 0.7 0.64 1.0

Total Flnancing Re uhred 85.40 100.0 64.60 100.0Totals may not add up due to rounding

2. Key policy and institutional reforms supported by the project:

Key policy reformns for the savings and credit sector were enacted by GOM in 2001, notably the passage ofthe "Popular Savings and Credit Law" and the law that creates BANSEFI. The project will contribute tothe implementation of this new legal and regulatory framework through: (a) supporting the developmentalrole assigned to BANSEFI vis a vis the SCIs and its organizations (Federations and Confederations), and(b) assisting the CNBV in the acquisition of specialized capacities to carry out its new supervisoryfunctions. At the institutional level, the project is concerned with reforming governance structures,management systems, methods, procedures and instruments of financial intermediaries conducive toenhanced outreach, with an emphasis on rural and lower-income populations, and on substantial progresstowards self-sustainability.

3. Benefits and target population:

At the time of enactment of the new legislation in 2001, the SCI sector consisted of a wide variety ofinstitutions. The approximate number of clients served and indicative figures for average savings accountand loan size (table below) show the importance of the sector and the nature of its clientele, primarilymiddle- to low-income segments of the population which for the most part are not served by the bankingsector. Institutions vary widely in size; some are little more than informal groupings (such as neighborhoodsavings groups with a civil association legal status), while others are fairly sophisticated savings and creditinstitutions.

- 13-

SC I type Aprx. Ap rx. No. al Avg. Savings ANg. OriginalNo (iIII l Cliviits Accomit Size Loin Size

( QwNso ) / pesos )

Credit Unions 32 19,000 $10,000 $47,000Savings and Loan 11 675,000 $7,200 $5,000Societies (SAPs)Savings and Loan 157 1,081,000 $5,800 $4,000Cooperatives (CACs)Cajas Solidarias 210 190,000 $1,000 $1,100Cajas Populares 220 344,000 Not available Not available(estimated)TOTAL 630 2,309,000

The project is expected to benefit the diverse range of households which make up the current and potentialclientele of SCI institutions, by building the capacity of a large subset of these institutions and enablingthem to be certified by the CNBV, which will provide prudential oversight of their activities. Lack ofconfidence in SCIs helps explain the low rates of participation in these institutions, even when they aregeographically accessible. Consolidating the SCI sector and building confidence in these intermediaries isthus expected to increase the number of households that make use of their services.

The project will specifically support approximately 365 institutions which are members of federations, orassociations which will become federations, and are, for the most part, members of COMACREP (see tablebelow). About 210 of the 365 institutions are Cajas Solidarias. Although their legal form varies atpresent, all project institutions which benefit from technical assistance will convert into either cooperativesor "popular financial institutions" (Sociedades Financieras Populares), as required by law.

Regioni I.ederations Instittitijils Mlembuhers Total Assets(Sttlles) Associatiolls N (t1houtsands) (Imillionlls pesos)

National: AMSAP 1/ 1 10 628 5,882Cajas Solidarias 1 216 213 1,226

North-Center: Nuevo Le6n, 4 56 485 3,240Guanajuato, Michoacan, QueretaroWest: Jalisco and adjacent states to 3 51 272 1,324the NorthSouth-Center: Oaxaca, Puebla, 5 40 100 688Veracruz, MorelosSouth-East: Yucatan, Chiapas 1 12 64 591Total 15 385 1,762 12,951

t Includes Caja Popular Mexicana (CPM), with 464 thousand members and assets of $4.1 billion pesos.

Some 800 managers and senior staff of all institutions will participate in the training programs onaccounting, credit analysis, risk management and governance. All institutions will be eligible to purchaseservices from the information systems network supported by the project.

Support to institutions in the rural areas will assist households and micro-enterprises located in themarginal areas to obtain access to secure, liquid savings instruments which protect the value of depositedfunds and to lending and payments services at lower cost than those obtained from informal serviceproviders. By the end of the project it is expected that some 60,000 families will benefit directly from theincreased financial services of institutions supported under the project. SCIs expected to participate in the

- 14 -

program should increase their client base and profitability, and gain authorization to operate under the newlegal framework as a result of project-sponsored technical assistance. At least a third of the branches to beopened in the marginal areas will be those of existing institutions. In addition, some 8,000 low incomefamilies will benefit from training programs in basic financial matters.

4. Institutional and implementation arrangements:

BANSEFI will be responsible for implementation of the project, including the project's financialmanagement and procurement. Key activities under the project will be subcontracted by BANSEFI totechnical assistance providers with demonstrated experience in the implementation of programs similar tothose envisaged under the project. The arrangements between BANSEFI and SAGARPA, which sharesresponsibilities for the rural microfinance component, and CNBV, which will provide technical oversightto the supervision component are described in the sections relating to executing agencies and projectmanagement in Part E of this report.

The project is innovative and ambitious as it seeks to support a major reform in the sector in a relativelyshort period of time. Because of its nature, priority is being given to monitoring activities. A mid-termreview will be carried out in 2004 to review progress on implementation of the SCI legislation, progress inthe technical assistance programs to participating SCIs and to approaches and schedules as required.

D. Project Rationale

1. Project alternatives considered and reasons for rejection:

Strengthening the SCI sector and developing the capacity of these intermediaries to provide safe financialservices to a broad range of Mexican households could conceivably be accomplished using differentdegrees of severity in the consolidation of sector institutions. This choice, in turn, would influence the sizeof the universe of institutions which the project would support through technical assistance. The option ofselecting only those institutions which are currently viable and with little need for additional capacitybuilding was rejected, as this alternative would result in the closure of many SCIs with a potential toimprove their capacity to deliver services and reach hundreds of thousands of people. Given that the newlaw provides for four different levels of institutional scale and scope of services, the project opted forproviding technical support commensurate to the requirements of these different levels of institutionaldevelopment.

Inproving access to finance by the rural population could be sought by means of: (i) financing lines ofcredit through the large government institutions such as BANRUTRAL and FIRA; (ii) supporting theexpansion of commercial banks' rural branch network's; and (iii) focusing solely or primarily on NGOsproviding microcredit. The dismal experience and standing negative image of government intervention ofthe 80s and early 90s, the extremely poor performance of BANRURAL, and FIRA's focus on operatingthrough commercial banks whose presence in rural areas continues to dwindle invalidate the first option.Bank and govermment efforts between 1996 and 1999 to induce the expansion of commercial banks' ruralbranch networks were unsuccessful, due primarily to the banks' critical financial situation, and theirincreased reluctance to intervene in rural areas. The rural NGO sector, on the other hand, is severelyunder-developed and, while the project intends to rely upon some NGOs for the provision of socialintermediation services, their capacity to become reliable financial institutions is extremely limited.

By strengthening the SCI sector at large and by drawing savings and credit institutions and othermicrofinance operators primarily as deposit-mobilizers into the cost-recovery mechanisms established inmany direct transfer programs for rural Mexico, the project aims at establishing a sustainable institutional

- 15-

base for rural finance. The project does not exclude the eventual involvement of commercial banks in thisinstitutional base.

2. Major related projects financed by the Bank and/or other development agencies (completed,ongoing and planned).

. , ,Latest* 0up 0isi,SectorIssue, ,,ProJect , 'WSRiVRintina!

___ ___ ___ ___ __ ___ ___ ___ _ l , _ _ _ _ _ _ __ _ _ _ _ . ;(Bank"flin hebd-prJojects ;on!y)-n:

Implementation DevelopmentBank-financed Prgress (IP) Objective (DO)Small-scale municipal infrastructure, Decentralization and Rural S Sinstitutional strengthening Development (completed)Development of rural financial services, Rural Finance TA (cancelled) U Upolicy context

Small scale municipal infrastructure, Second Decentralization and S Sinstitutional strengthening Rural Development

(completed)Productive investments, community Rural Development in Marginal S Sdevelopment, technical assistance Areas I (ongoing)Productive investments, community Rural Development in Marginal S Sdevelopment, technical assistance Areas II (ongoing)Contractual savings development Contractual Savings II S S

(completed)Technical assistance, financial system Financial Sector TA S Sdevelopment/strengthening (completed)

Banking sector Bank Restructuring Facility HS HSrestructuring/strengthening (completed)

Banking sector Bank Restructuring Facility II S Srestructuring/strengthening (ongoing)Finance and business development Southeast Regionalservices for microbusinesses Development Learning and

Innovation Project (not yeteffective)

Other development agenciesIDB - Direct support to ruralcommunities and rural microenterprisesin Chiapas and OaxacaIDB/MIF - Support to system ofdelegated SCI supervision (training)IDB/MIF - Technical cooperation:US$3 million for BANSEFIinfornation systems equipmentUSAID - Technical assistance to CPM(WOCCU contract), US$2 million

IP/DO Ratings: HS (Highly Satisfactory), S (Satisfactory), U (Unsatisfactory), HU (Highly Unsatisfactory)

- 16 -

3. Lessons learned and reflected in the project design:

The proposed project relies on lessons from experience in fmancial sector development and rural andmicrofinance outreach expansion projects both in Mexico and intemationally. Intemational experience andbest practice strongly indicate the need for an effectively regulated and supervised non-bank sector as aprecondition for the sound growth and development of these financial intermediaries. Lessons have beendrawn from the Canadian and German systems of delegated supervision as a means for providing costeffective prudential oversight for numerous intermediaries, as is the case in Mexico.

The Rural Finance TA Loan closed in late 1999 also provided several important lessons regarding thedevelopment of more broadly accessible financial services in Mexico, which serve as inputs into the designof the proposed project. First, the project now closed was focused solely on encouraging large, commercialbanks to extend their presence in rural areas, which represented a significant investment in newinfrastructure and staff and the development of knowledge of nural economic activities. Partly as a result ofthe financial crisis, but also due to the pursuit of alternative, profitable opportunities, the interest of thecommercial banks was much less than expected. The proposed project will work instead with thosefinancial intermediaries which are already working with clients from a broad range of income groups andgeographic areas, including poor and rural households, and for whom the incremental costs of extendingclient outreach are lower. The focus will be on improving management systems, staff productivity anddesign of appropriate products which will permit increased leverage of the institutions' existing investmentsin infrastructure and staff. Second, the previous project sought to convince commercial banks thatinvestment in rural banking was a profitable opportunity. By contrast, the design of the.marginal areasoutreach expansion component of the proposed project is based on the expressed demand of institutionsalready working in these areas.

Third, experience elsewhere has demonstrated that to reach low-income households where literacy rates arelow and fimctional literacy is practically nonexistent, important efforts need to be made in the area of socialintermediation. This is particularly important given that the history of subsidized credit and lax financialdiscipline practiced by govemment agencies impairs the ability of rural entrepreneurs and households toknowingly and responsibly enter into formal financial transactions. Awareness raising and assistance at thecommunity level, provided for in this project, are therefore essential to improve the likelihood of successfulrural finance. Finally, most previous efforts have excluded the non-bank sector, with the notable exceptionof CGAP's investment in the NGO Compartamos, perhaps the only "success story" in microfinance inMexico. This project builds upon and applies to non-bank financial institutions a model of specializedassistance and advice similar to the one used in Compartamos, in Financiera Calpia (El Salvador),Bancosol (Bolivia) and Banco del Estado (Chile) to name a few in LAC, which offers a reasonablelikelihood of success for rural Mexico.

Several lessons related to provision of TA to develop village and institutional capacity for financialintermediation have been identified and incorporated into the project design. These lessons are consistentwith the general lessons which emerge from technical assistance projects:

* TA should be demand driven;* Beneficiaries of the TA should be involved in the design of the TA product as well as the delivery

mechanism;* Access to TA should be based on expressions of interest either through payment or technical

requirements;* Existing institutional environment should be well understood and inform TA program design;* Program should have a core set of quantitative and qualitative perfornance indicators which are

- 17 -

monitored regularly and providers held accountable;* TA program design should be flexible to pernit modifications in response to feedback from M&E;* TA suppliers have to be well qualified and sensitive to local environment;* External TA providers have to provide strong supervision and management oversight of subcontracted

staff;* Supervision of large and complex TA contracts require sufficient and qualified staff in the project

management units.

4. Indications of borrower commitment and ownership:

The SHCP, CNBV and BANSEFI (formerly PAHNAL) have demonstrated their detennination to overhaulthe SCI sector with the passage of the Popular Savings and Credit Law, and of the complementary lawauthorizing the reform of PAHNAL and its transformation into BANSEFI, both in 2001. The leaders ofeach institution, including the Director General of BANSEFI, the Vice President for Supervision of CNBV,and the Deputy Director General for International Financial Organizations of the SHCP have activelyparticipated in the formulation of a comprehensive and consistent set of proposals to enable theimplementation of the law, and have sought support from the Bank and the 1DB, among other agencies, toleverage the Government's funds for program implementation.

As regards the outreach expansion of non-bank financial intermediaries in rural areas, SAGARPA hasalready requested and obtained a budget allocation to start a program of technical assistance to SCIs andrural communities with substantial input from Bank staff. At the community level, the demand forassistance in establishing savings and capitalization mechanisms has been clearly expressed at regionalawareness-raising workshops carried out under the Marginal Areas Program. For implementation purposes,SAGARPA will enter into an agreement with BANSEFI.

It is important to highlight the fact that in this particular case SHCP took the initiative to request fromSAGARPA (and the Bank) a proposal to develop a rural microfinance program. This is counter to thetraditional flow of program creation, and shows strong borrower commitment to the initiative.

5. Value added of Bank support in this project:

The Bank has been actively involved in stabilizing and strengthening the financial sector and in improvingaccess to productive opportunities in poor and rural areas in Mexico over the last decade, supportingoperations and sector work in banking, pensions, insurance and capital markets, as well as ruraldevelopment and municipal services projects in various regions.

The proposed project will help provide the required multi-year continuity to the policy refonns and capacitybuilding efforts initiated under BANSEFI, CNBV, SAGARPA and SHCP auspices.

Given the non-additionality of Bank lending in Mexico, the value-added of Bank lending consists primarilyin the technical guidance the Bank can contribute to the implementation of the new institutional and policyfiamework for SCI sector development in general, and outreach expansion in rural areas in particular. TheWorld Bank's intemational expertise in rural finance and microfmance, in legal and regulatory frameworkissues, in payments systems, and its increasing experience in institutional capacity building operations arealready being brought forth in its existing dialogue with govemment and practitioners in Mexico. Theproposed project provides a long-term horizon to this dialogue.

E. Summary Project Analysis (Detailed assessments are in the project file, see Annex 8)

1. Economic (see Annex 4):O Cost benefit NPV=US$ million; ERR = % (see Annex 4)* Cost effectivenessO Other (specify)Economic effects are assessed for the most part on a qualitative basis, given the special difficulties thattechnical assistance interventions convey for quantitative analysis. Expected project impacts are assessedon three levels: (i) institutions (including SCIs and their organizations); (ii) clients; and (iii) fiscalimplications, the latter dealt with in section E.2 below.

Institutional Level: Consolidation, Scale Economies and Efficiency Gains. Approximately 385 savingsand credit institutions are expected to participate in the sector consolidation and strengthening activities tobe undertaken by the project. By most measures, these institutions represent at least 80 percent of thesector. The project will fund institutional strengthening for those participating SCIs with the potential tomeet the new financial and operating standards mandated by law, and will support the liquidation ormerging of those institutions which cannot meet the new standards. Preliminary diagnostic work indicatethat approximately 40 percent of the participating institutions may be either liquidated or merged in thesector consolidation process.

The approximately 240 institutions estimated to emerge from the consolidation process will be fullystrengthened and restructured as needed to be compliant with the new law. The liquidations and mergers arelikely to increase the average number of clients served by each of the remaining institutions from 5500 toabout 8700 clients at project's end. This estimated increase of nearly 60 percent in institutional scale, willallow the remaining SCIs to benefit from scale economies thus far unattainable given their limited size.

Efficiency gains will also accrue to the SCIs from staff training, upgrading intemal controls and buildingcredit appraisal and risk management capacity. The information platform for SCIs to be financed by theproject is expected to contribute significantly to the overall increase in operational efficiency and especiallyto a reduction in the costs of control, reporting and back-office functions .

The organizations formed by the institutions of the SCI sector are also expected to benefit from projectactivities designed to automate operations and professionalize the federations and confederations. Inparticular, the formalization of COMACREP into a Confederation where the auxiliary supervisioncapacities and deposit protection functions for the sector are likely to be housed, represents aninstitution-building effect for the sector.

Client Level: Increased Access and Depth of Outreach. The client base of the SCI sector is expected togrow by about 16 percent per year over the course of the project. This would result in the expansion in thenumbers of clients served by the participating SCIs from about 2 million to about 4.2 million at the end ofthe five year project implementation period, an increase in access from about 5 percent to almost 9 percentof the economically active population.

As for the depth of the SCI sector outreach, loan amount averages for the SCI sector were in the rangefrom 4 to 14 percent of GDP per capita in 1999, while average savings balances were between 8 and 12percent of per capita GDP. In contrast, average deposit balances in the banking system are estimated toamount to about 130 percent of GDP per capita. Expansion of the SCI sector, therefore, is likely toincorporate large numbers of the low-income segments of the population.

- 19-

Providing financial services as a means of integrating poor households into the national economy is clearlya poverty-alleviation tool. This is particularly pertinent for the rural microfmance component of the project,in which the population of rural marginal areas is expected to gain from the services provided by thestronger, more efficient SCIs through access to adequate deposit instruments and an improved ability totake advantage of productive investment opportunities. Sector work has shown that transfonning informal,non-earning financial assets, and monetizing even a fraction of the savings held in physical form by ruralhouseholds would have clear benefits in terms of safety and return. Informal means of savings thatdominate in the households' portfolios are, in principle, inferior to financial instruments in terms of safetyand returns. For example, informal lending suffers from a 20 percent arrears-default rate and loans areoften made at zero interest charges; tandas report a 6 percent rate of noncompliance (group members whocease to contribute once they have taken a turn); and the most common forms of livestock holding, pigs andchickens, have mortality rates above 40 percent. Since holding livestock as savings is more prevalent inpoorer areas and among indigenous people than elsewhere, this kind of asset transformation would benefitrelatively more the poorest segments of the population.

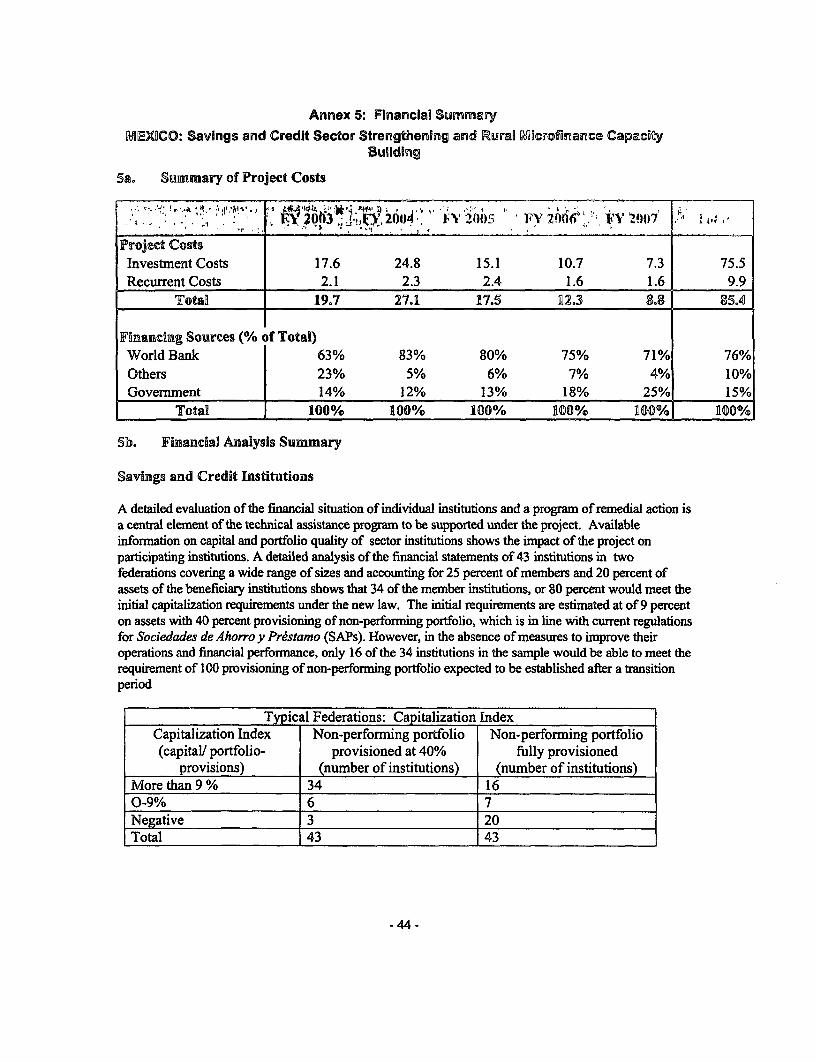

2. Financial (see Annex 4 and Annex 5):NPV=US$ million; FRR = % (see Annex 4)An evaluation of the financial situation of individual institutions and a program of remedial action arecentral elements of the technical assistance to be supported under the project. Available information oncapital and portfolio quality of sector institutions, however, provides insights into the potential projectimpact on participating institutions. A detailed analysis of the financial statements of 43 institutions in twofederations covering a wide range of institution sizes and accounting for 25 percent of mernbers and 20percent of assets of the beneficiary institutions shows that 34 of the member institutions, or 80 percent,would meet the initial capitalization-ratio requirements expected to be set by the regulations. This initialrequirements are estimated at 9 percent of risk assets with 40 percent provisioning of the non-performingportfolio, which is in line with current regulations. However, in the absence of measures to improve theiroperations and financial performance, only 16 of the 34 institutions in the sample would be able to meet therequirement of 100 percent provisioning of non-performing portfolios expected to be established after atransition period.

The enactment of the new legislation has had an impact on sector institutions. Some of the largest arealready part of federations which perform functions not unlike those mandated by the new legislation. Thesmaller institutions which did not belong to federations have begun associating with existing ones or are inthe process of establishing new federations. Existing federations charge for services (I to 4 percent ofassets). The incremental costs to the federation of performing their auxiliary supervision functions and theability to pay among different categories of institutions has been examined. The cost of the supervisory unitat the federation level has been estimated at 0.35 percent of assets. The incremental costs of the supervisoryunits should be affordable to most institutions; this is especially the case as the technical assistance to beprovided under the project is expected to increase substantially the efficiency of participating institutions.Financial projections for very small institutions in the rural areas show that they should be profitable andable to afford payments to the federations.

Financial projections for microfinance institutions (or branches of institutions) in marginal areas supportedunder the project show that these should be financially strong, given the relatively high interest rate marginswith which they are expected to operate. The projections were prepared with lending rates which are moreconservative than the prevailing rates in marginal areas (50 percent annual rate, as opposed to theprevailing 60 percent which is charged by microfinance institutions), as it can be expected that interestrates of microfinance institutions will decline as a result of an increased supply of financial services inrural areas.. Institutions will cover operating costs including depreciation in the fourth year of operations.

- 20 -

This is even taking into account that the institutions must retain a high liquidity position and that they willcontribute to the costs of the federations which they join (estimated at some 7 percent of deposits per year).At the end of the project period, some institutions will just have been established, and the projections werethus extended to ten years, when all institutions supported under the program will be operational. At theend of 10 years, the return on equity of project institutions would be about 20 percent. Savings and creditinstitutions in marginal areas are expected to meet the requirements to be established by the CNBV forauthorization to operate.

Fiscal Impact:

The principal fiscal impact of the project will be the investment costs associated with the project and thecosts associated with the payment to depositors of SCI's which are not viable and would need to beliquidated. The Bank will not finance the bailout, but the Government is making the necessaryarrangements to ensure that the fimds are available.

Government estirates are that total liabilities of the institutions which will need to be liquidated are of theorder of some US$ 330 million (or about 0.06 percent of GDP). The actual cost to Government willdepend on the guarantees held by the institutions, including blocked savings which are customary in SCIs, afigure which is not yet available. Not taldng guarantees into account, the maximum payments todepositors will be US$490 per client, assuming the past practice of reimbursing 70 percent of deposits forsmaller depositors (deposits average US$700 per client). The resulting figures are insignificant whencompared to the bailout of depositors of banks in the late nineties which in 1999 amounted to 13 percent ofGDP, or US$85 billion.

All activities under the project are expected to be self-financing over time and not require Governmentsubsidies after project implementation. The operating costs of the SCI information system will be paid bythe users after a start-up period. Rural institutions will receive a partial subsidy of salaries (50-70 percentof salaries) in their first three years of operations but will be self-financing after the third year.

3. Technical:

Savings and Credit Sector Component

CNBV with assistance from BANSEFI and international and national specialists is designing a system ofclassification of institutions which will be used to evaluate and monitor performance under the project. Inaddition, an inventory of SCIs is being completed to make a preliminary assessment of the financialsituation of the SCIs, and to ascertain the coverage of the program and its priorities. The inventory includeskey financial data, membership and organizational structure of each institution in the sector.

The technical assistance programs will be designed and implemented by specialized institutions(consultants) with demonstrated experience in restructuring and liquidating savings and credit institutions.The specialized institutions will design and implement technical assistance plans initially on the basis ofinformation obtained in the survey. Each participating institution will enter into agreements with thetechnical assistance provider specifying performance indicators which will be monitored semiannually.Assistance will be suspended to institutions which do not meet agreed performance targets. Because of thenumber and geographic dispersion of institutions, it is not technically feasible for a single technicalassistance provider to cover all federations. The contracts for technical assistance will therefore include themember institutions of between one and three federations (depending on their size). It is expected that somesix contracts will be awarded. The above-referred standards, and the follow up by BANSEFI, and to some

-21 -

degree CNBV, will ensure consistency of approach among providers of technical assistance. Technicalassistance providers will work closely with the federations and will provide training to them as part of theirmandate. Terms of reference for a model contract have been prepared. Program costs are consistent withinternational experience in restructuring small banks.

Support to CNBV is designed to increase its competencies in supervision of microfinance institutions. Inparticular, the technical assistance will support CNBV to address issues relating to the auxiliarysupervision anrangements, drawing from international experience where these arrangements are in placeand have proven to be effective.

Expansion of Financial Services in Rural Areas

The approach used in the provision of technical assistance to assist in expanding services in marginal areasis similar to that used successfully in other regions both with Bank financing or supported by bilateraldonor institutions. As the program does not include credit, but focuses on introducing the savings habit anda culture of self sufficiency, in low-income areas, the programs necessarily have a long term horizon.

Preliminary studies have been conducted in the project regions which confinn the feasibility of the proposeddevelopment, given the population density, income levels and perceived demands of the beneficiaries. Workis focused in a specific region as there is ample evidence that institutions focusing on the poor need to beadapted to local conditions. Prior to the contracting of technical assistance, detailed regional market studieshelp determine the program targets in the region, which are then specified in the agreements with thetechnical assistance providers. The providers in turn enter into agreements with the beneficiary institutionsthat establish performance indicators and rules of conduct. Detailed market studies for three regions havebeen prepared (Chiapas, Huasteca and Oaxaca). A model for terms of reference for the consultant contractsis also available. The contract for the Chiapas region was signed at the end of March 2002, and the one forHuasteca was signed in April 2002.