world bank group lac trade training peruvian delegation october 21, 2010 logistics performance index...

TRANSCRIPT

WORLD BANK GROUP

LAC Trade Training Peruvian Delegation

October 21, 2010

LOGISTICS PERFORMANCE INDEX AND DOING BUSINESS INDICATORS

Souleymane COULIBALYECA Regional Trade Coordinator

Geneva, June 14th, 2011

The Logistics Performance Index and Doing Business Report

2

Two separate but complementary reports

The Logistics Performance Index

• Measures the trade logistics efficiency of a country

• Fundamental premise: Efficient logistics drives economic performance

3

The Doing Business Report

• Provides measures of the ease of doing business (regulations) for local firms in a given country

• Fundamental premise: economic activity requires effective regulations in all areas of setting up and operating a business

4

Agenda

2. Overview of Doing Business 20112. Overview of Doing Business 2011

1. Overview of LPI 20101. Overview of LPI 2010

3. LPI Results: CIS countries3. LPI Results: CIS countries

5. Want to Learn More?

4. DB Results: CIS Countries4. DB Results: CIS Countries

1. Overview LPI 20101. Overview LPI 2010

6

The Logistics Performance Index

• First report in 2007, every three years

• Source of data is suppliers of logistics services (freight forwarders, express carriers)

• Rates logistical performance on a scale of 1 to 5

7

8

LPI: Key messages

• Trade logistics is an important element of national competitiveness

• A country’s performance is only as good as its weakest link

• The LPI dataset can be used to identify key bottlenecks in your own country

Efficiency of the clearance process

Quality of trade and transport infrastructure

Ease of arranging competitively priced shipments

Logistics competence and quality of logistics services

Ability to track and trace shipments

Timeliness of shipment delivery

The LPI measures six dimensions of country performance:

What are efficient logistics?

9

10

Why Logistics Matter:

Result when a low income country reaches LPI of middle income average

Indicator/policy areaIncrease in trade

(%)

Logistics Performance Index 15.2

All trade barriers reduced to 10% 8.4

Regulatory reform measures 7.4

Tariffs reduced to 5% 5.7

Key Policy Implications:

• Expand the traditional development agenda beyond customs reform and infrastructure to be comprehensive—processes, services, and infrastructure.

• Increase border agency coordination

• Partner with the private sector

• Reform must be tailored to each country’s circumstances

11

The Logistics Performance Index

12

13

2. Overview Doing Business 20112. Overview Doing Business 2011

14

The Doing Business Report

• First report in Sept 2003, yearly

• Covers 183 countries

• Surveys in-country specialists with knowledge of regulatory system

• Provides a basis for measuring, understanding and improving the regulatory environment for business

• creates methodology and a database for policy makers

15

The Doing Business Report

Doing Business does not measure all aspects such as:

• macroeconomic stability• corruption• level of labor skills• proximity to markets, • regulations specific to foreign

investment or financial markets

16

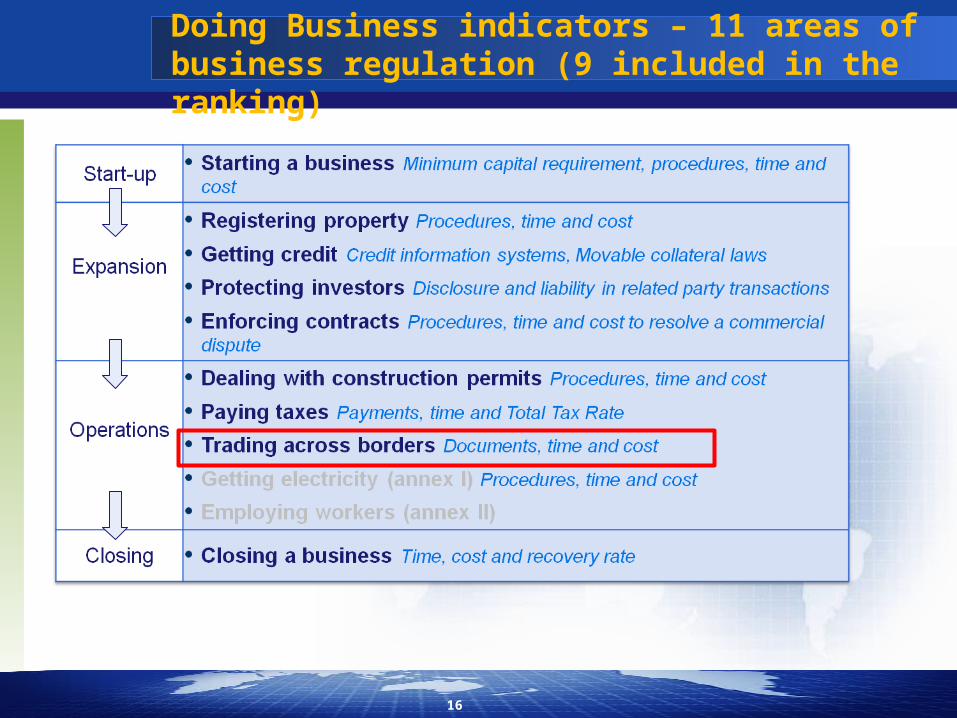

Doing Business indicators – 11 areas of business regulation (9 included in the ranking)

17

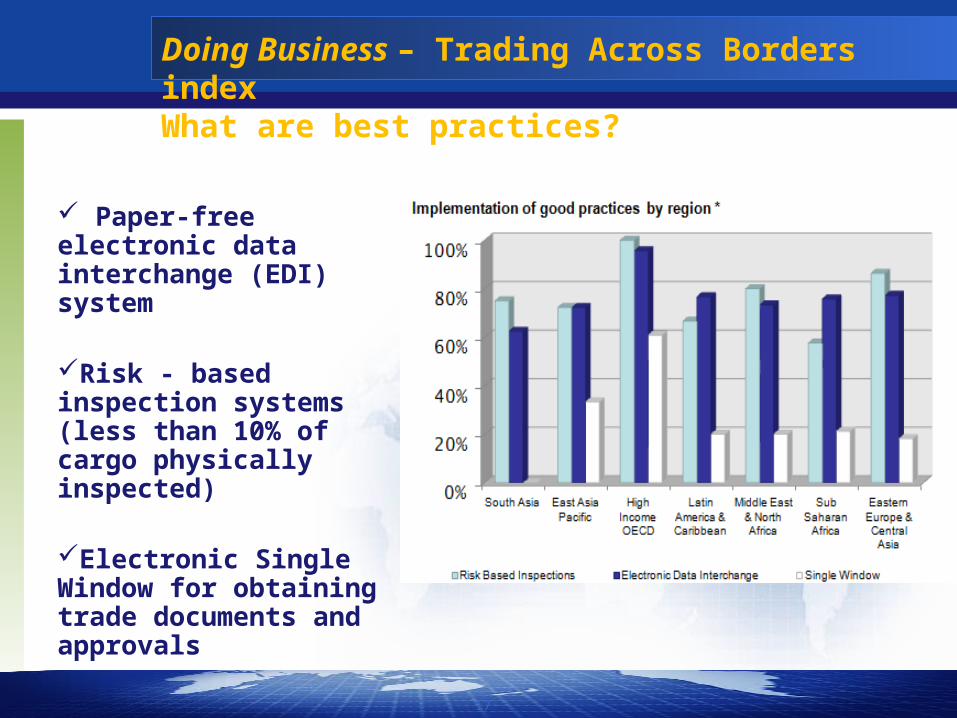

Doing Business – Trading Across Borders indexWhat are best practices?

Paper-free electronic data interchange (EDI) system

Risk - based inspection systems (less than 10% of cargo physically inspected)

Electronic Single Window for obtaining trade documents and approvals

The Doing Business Report

18

LPI and DB – separate but complementary

LPI DB

Source of data3rd country providers of Logistics services

In-country entities with knowledge of business regulations

Concept Performance outcomesAnalytic breakdown in component procedures

Frequency Every 3 years since 2007 Yearly since 2003

SignificanceSeveral indices of logistics performance

Metric of broader business regulatory environment.

Countries 155 183

19

Both indices provide basic input for policy-makers. Neither are in-depth analysis.

20

3. LPI Results: CIS countries3. LPI Results: CIS countries

LPI 2010 – performance varies around the world

Countries are improving around the worldNo data

Logistics friendly

Logistics unfriendly

Partial performersConsistent performers

21

More than income: the “logistics gap”

With the right investment and policies, lower income countries can also be high performers

22

Overperformers and underperformers

23

Country LPI Rank

South Africa 28Malaysia 29Poland 30Lebanon 33Latvia 37Turkey 39Brazil 41Lithuania 45Argentina 48Chile 49

TOP 10 COUNTRIES

LOWER MIDDLE INCOME

Country LPI Rank

China 27Thailand 35Philippines 44India 47Tunisia 61Honduras 70Ecuador 71Indonesia 75Paraguay 76Syrian Arab Republic 80

TOP 10 COUNTRIES

LOW INCOME

Country LPI Rank

Vietnam 53Senegal 58Uganda 66Uzbekistan 68Benin 69Bangladesh 79Congo, Dem. Rep. 85Madagascar 88Kyrgyz Republic 91Tanzania 95

TOP 10 COUNTRIES

UPPER MIDDLE INCOME

LPI 2010 Ranks

24

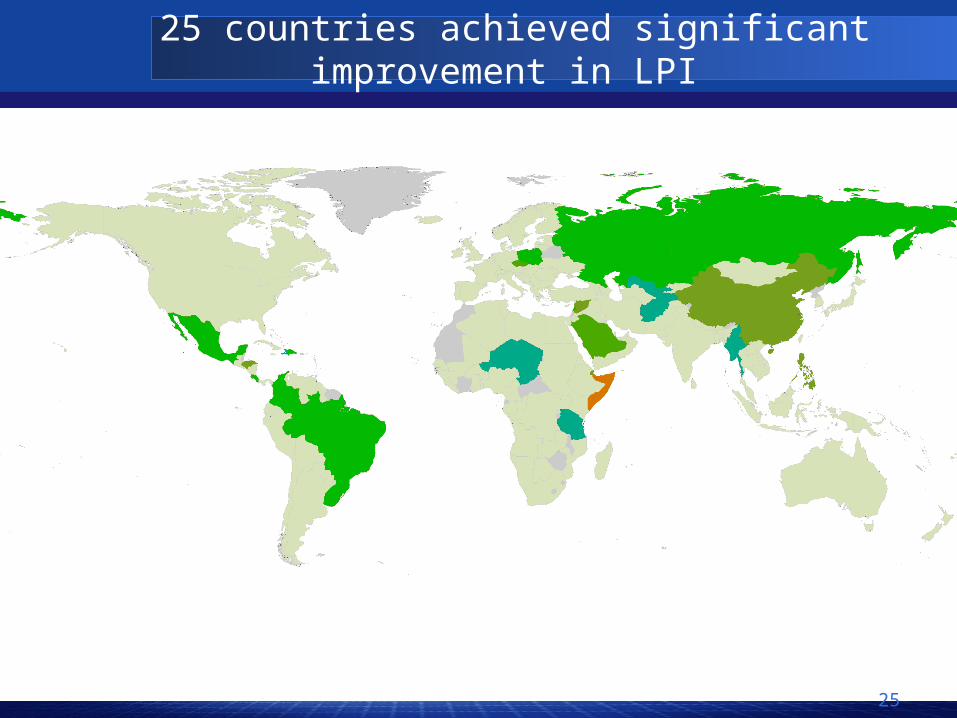

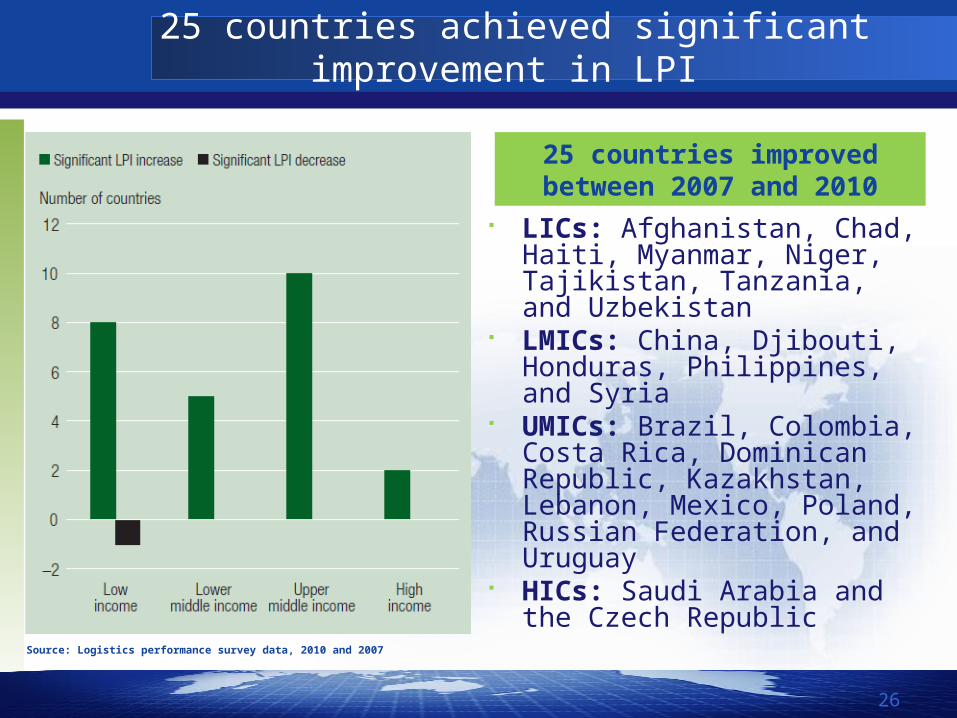

25 countries achieved significant improvement in LPI

25

25 countries achieved significant improvement in LPI

LICs: Afghanistan, Chad, Haiti, Myanmar, Niger, Tajikistan, Tanzania, and Uzbekistan

LMICs: China, Djibouti, Honduras, Philippines, and Syria

UMICs: Brazil, Colombia, Costa Rica, Dominican Republic, Kazakhstan, Lebanon, Mexico, Poland, Russian Federation, and Uruguay

HICs: Saudi Arabia and the Czech Republic

Source: Logistics performance survey data, 2010 and 2007

25 countries improved between 2007 and 2010

26

LPI Scores by Region

27

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8H

igh

inco

me:

O

ECD

Hig

h in

com

e:

nonO

ECD

Cent

ral

Amer

ica

East

Asi

a &

Pa

cific

Sout

h Am

eric

a

CIS

Mid

dle

East

&

Nor

th

Afric

a

Sout

h As

ia

Aver

age

2010

LPI

Sco

re

Lower Middle Income

Low Income

Upper Middle Income

LPI Scores

28

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

Aver

age

2010

LPI

Sco

re

Logisticsunfriendly

Consistentperformers

High Income: OECD

Middle East and N.Africa

Low income

CIS Avg.

Partialperformers

40

45

50

55

60

65

70

75

Kaza

khst

an (6

2)

Uzb

ekist

an (6

8)

Azer

baija

n (8

9)

Kyrg

yz R

epub

lic (9

1)

Geo

rgia

* (9

3)

Russ

ian

Fede

ratio

n (9

4)

Ukr

aine

(102

)

Mol

dova

(104

)

Arm

enia

(111

)

Turk

men

istan

(114

)

Tajik

istan

(131

)

% H

ighe

st P

erfo

rmer

CIS Country (Rank LPI 2010)

% Highest performer 2010% Highest Performer 2007

% of the highest performer

29

LPI 2010

Highest performer Germany 100%

Lowest performer Somalia 11%

Performance in the 6 areas of the LPI

302010 Average LPI Score

2

2.5

3

3.5

4Cu

stom

s

Infr

astr

uctu

re

Inte

rnati

onal

Sh

ipm

ents

Logi

stics

Qua

lity

and

Com

pete

nce

Trac

king

and

Tra

cing

Tim

elin

ess

Int'l

LPI

Com

pone

nts

Scor

e (1

=Ver

y lo

w; 5

=Ver

y hi

gh)

High income: OECD East Asia & PacificSouth America Middle East & North AfricaSouth Asia CIS

Infrastructure quality

31

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Port

s

Airp

orts

Road

s

Railr

oad

War

ehou

sing IC

T

Perc

enta

ge o

f res

pond

ents

indi

catin

g Q

ualit

y of

In

fras

truc

utre

is "

Low

" or

"Ve

ry L

ow"

High income: OECD East Asia & PacificSouth America Middle East & North AfricaSouth Asia CIS

Quality of services I

32

TRANSPORT SERVICES

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Wat

er Air

Road

Railr

oadPe

rcen

tage

of r

espo

nden

ts in

dica

ting

Qua

lity

of S

ervi

ces

(T

rans

port

) is

"Lo

w"

or "

Very

Low

"

High income: OECD East Asia & PacificSouth America Middle East & North AfricaSouth Asia CIS

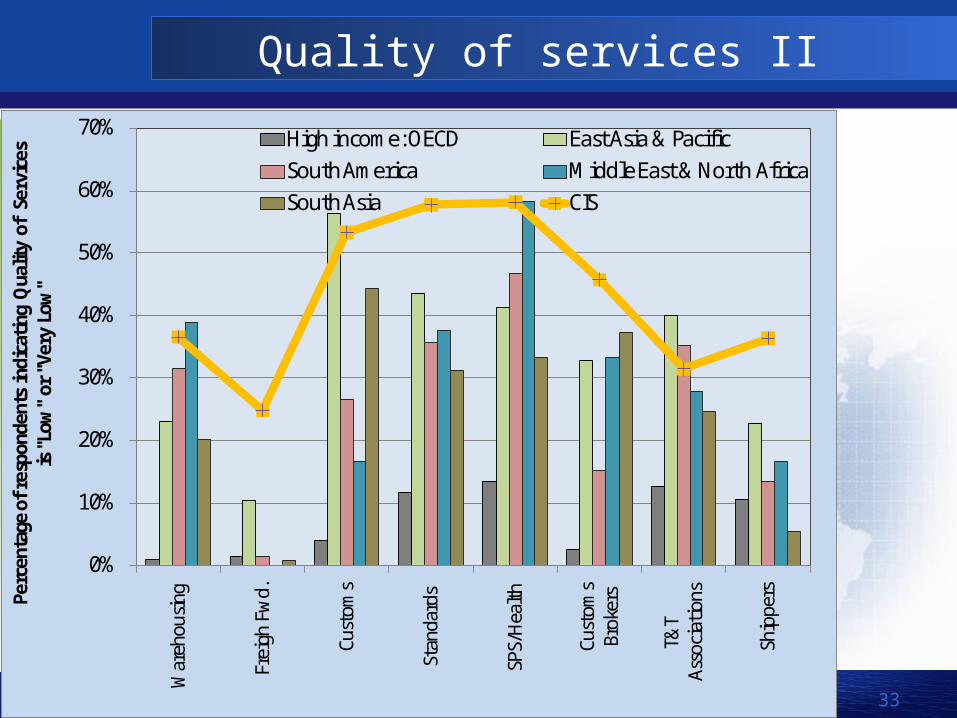

Quality of services II

33

0%

10%

20%

30%

40%

50%

60%

70%

War

ehou

sing

Frei

gh F

wd.

Cust

oms

Stan

dard

s

SPS/

Hea

lth

Cust

oms

Brok

ers

T&T

Asso

ciati

ons

Ship

persPe

rcen

tage

of r

espo

nden

ts in

dica

ting

Qua

lity

of S

ervi

ces

is "

Low

" or

"Ve

ry L

ow"

High income: OECD East Asia & PacificSouth America Middle East & North AfricaSouth Asia CIS

Border clearance procedures / corruption

34

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Tim

ely

Clea

ranc

e an

d D

eliv

ery

of

Impo

rts

(Har

dly

ever

)

Tran

spar

ent

Cust

oms

Clea

ranc

e Pr

oces

s (H

ardl

y ev

er)

Brib

es a

re

sour

ce o

f Del

ay

(Alw

ays o

r ne

arly

alw

ays)

Perc

enta

ge o

f res

pond

ents

High income: OECD East Asia & PacificSouth America Middle East & North AfricaSouth Asia CIS

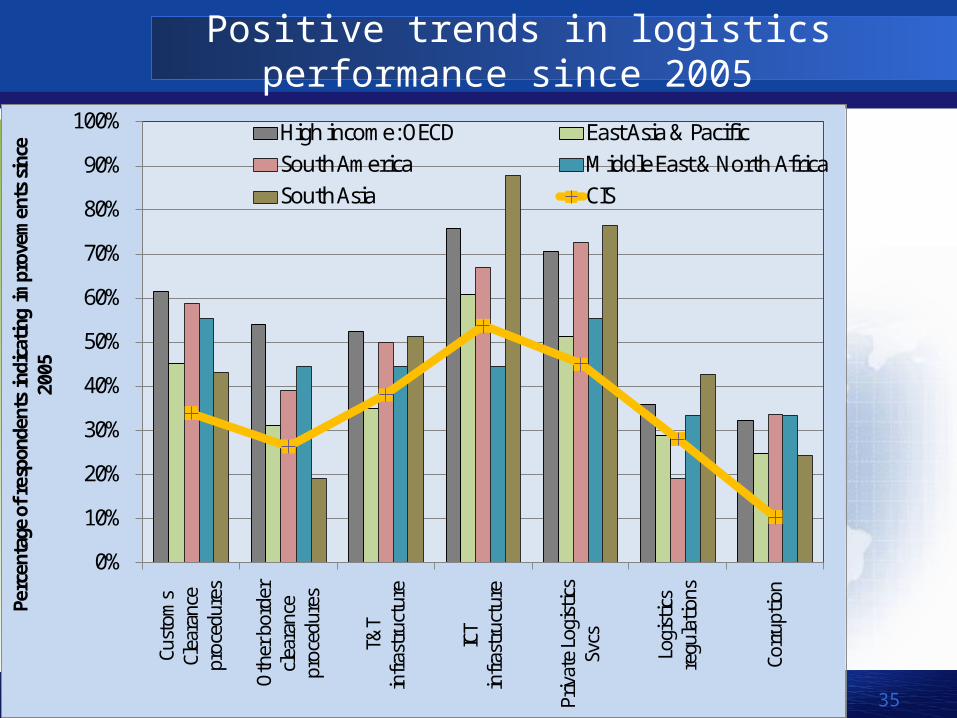

Positive trends in logistics performance since 2005

35

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cust

oms

Clea

ranc

e pr

oced

ures

Oth

er b

orde

r cl

eara

nce

proc

edur

es

T&T

infr

astr

uctu

re

ICT

infr

astr

uctu

re

Priv

ate

Logi

stics

Sv

cs

Logi

stics

re

gula

tions

Corr

uptio

n

Perc

enta

ge o

f res

pond

ents

indi

catin

g im

prov

emen

ts s

ince

20

05

High income: OECD East Asia & PacificSouth America Middle East & North AfricaSouth Asia CIS

36

4. Doing Business Results: CIS Countries

4. Doing Business Results: CIS Countries

Top 30 economies on the ease of Doing Business 2009/10

37

1. Singapore 16. Korea, Rep.

2. Hong Kong SAR, China 17. Estonia

3. New Zealand 18. Japan

4. United Kingdom 19. Thailand

5. United States 20. Mauritius

6. Denmark 21. Malaysia

7. Canada 22. Germany

8. Norway 23. Lithuania

9. Ireland 24. Latvia

10. Australia 25. Belgium

11. Saudi Arabia 26. France

12. Georgia 27. Switzerland

13. Finland 28. Bahrain

14. Sweden 29. Israel

15. Iceland 30. Netherlands

Eastern Europe and Central Asia is the second best performing region in 2008/09

38

CIS economies: 12 Georgia13 Kyrgyz Republic48 Armenia54 Azerbaijan59 Kazakhstan68 Belarus89 Moldova123 Russian Federation 139 Tajikistan145 Ukraine150 Uzbekistan

Kazakhstan improved the most in the ease of doing business in 2009/10

EconomyStarting a business

Dealing with construction

permits

Registering property

Getting credit

Protecting investors

Paying taxes

Trading across borders

Enforcing contracts

Closing a business

Kazakhstan

Rwanda

Peru

Vietnam

Cape Verde

Tajikistan

Zambia

Hungary

Grenada

Brunei Darussalam

39

Percentage of countries with at least one positive reform in 2009/10

84%

61%

OECD high Income

Eastern Europe and Central Asia

Sub-Saharan Africa

Middle East and North Africa

Latin America and

Caribbean

South Asia

East Asia and Pacific

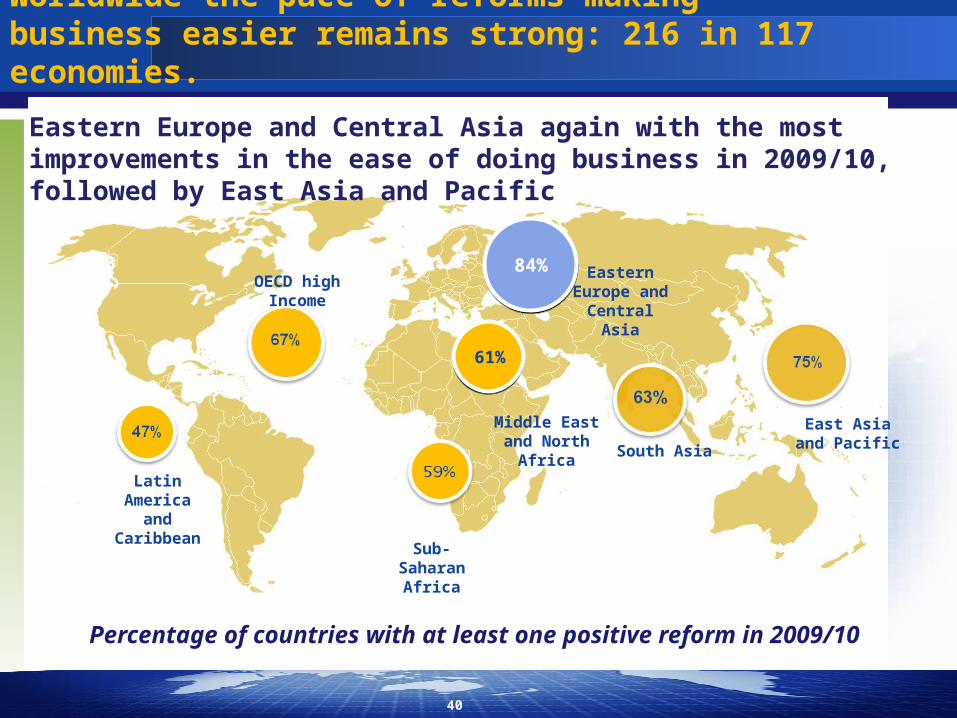

Worldwide the pace of reforms making business easier remains strong: 216 in 117 economies.

Eastern Europe and Central Asia again with the most improvements in the ease of doing business in 2009/10, followed by East Asia and Pacific

40

90% of the economies in the ECA region improved their business environment

While 85% of economies worldwide improved

business regulation over the last 5 years.

41

21 of 25 economies in Eastern Europe & Central Asia improved business regulations this year

6 economies eased trading across borders in the region

42

43

33 economies reformed making it easier to trade across borders in 2009/10

44

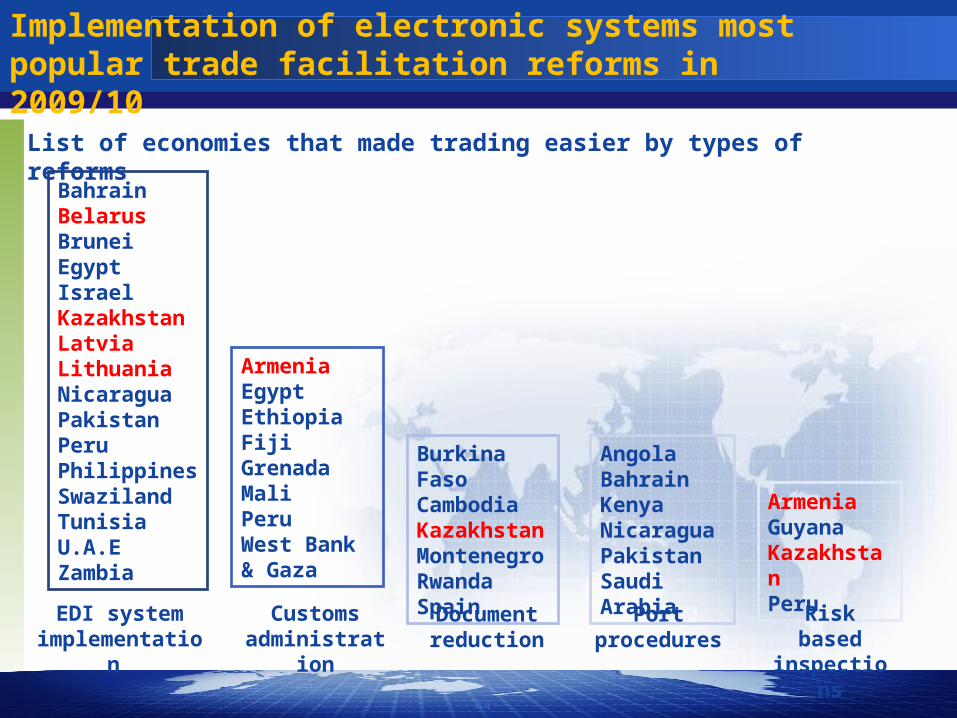

Implementation of electronic systems most popular trade facilitation reforms in 2009/10

BahrainBelarusBruneiEgyptIsraelKazakhstanLatviaLithuaniaNicaraguaPakistanPeruPhilippinesSwazilandTunisiaU.A.EZambia

ArmeniaGuyanaKazakhstanPeru

Burkina FasoCambodiaKazakhstanMontenegroRwandaSpain

AngolaBahrainKenyaNicaraguaPakistanSaudi Arabia

ArmeniaEgyptEthiopiaFijiGrenadaMaliPeruWest Bank & Gaza

EDI system implementation

Risk based inspections

Customs administration

Document reduction

Port procedures

List of economies that made trading easier by types of reforms

45

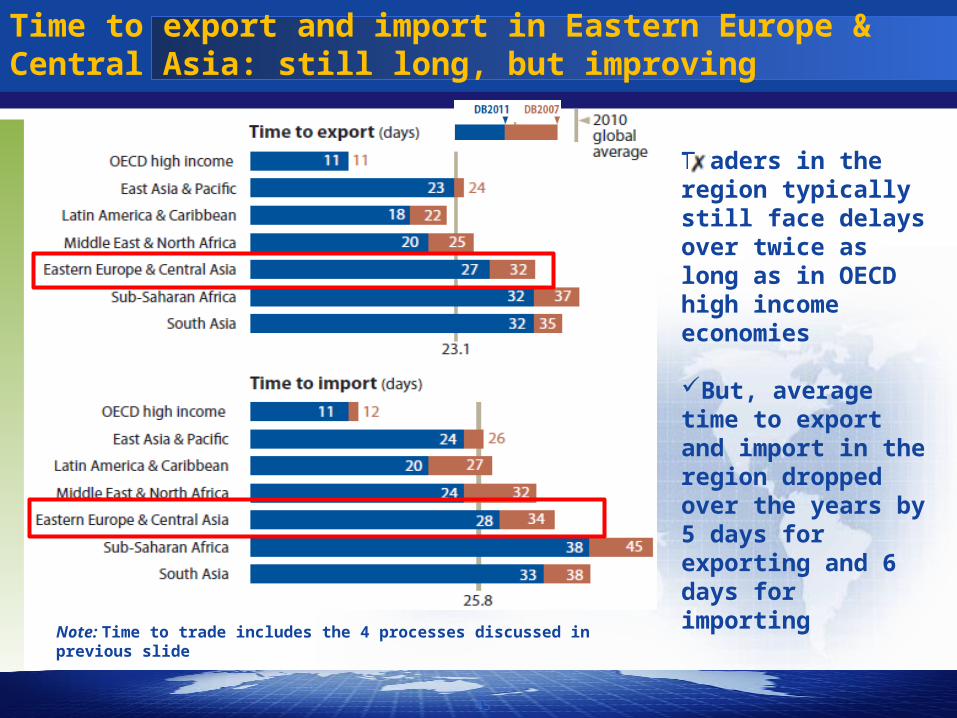

Time to export and import in Eastern Europe & Central Asia: still long, but improving

Note: Time to trade includes the 4 processes discussed in previous slide

Traders in the region typically still face delays over twice as long as in OECD high income economies

But, average time to export and import in the region dropped over the years by 5 days for exporting and 6 days for importing

46

Eastern Europe and Central Asia economies also made improvements in number of required documents

Traders in OECD high income economies require less than 5 documents on average to export and import

Whereas traders in Eastern Europe and Central Africa still require on average 2-3 additional documents

47

Emphasis on trade facilitation in many developing economies

Note: shows number of cumulative reforms easing trade across borders since DB2007 (counted as 1 reform per reforming economy per year)

48

The trade facilitation reforms impacted lower income countries the most

2006

2010

- 4.7 days

- 4.0 days

-2.9 days

- 0.9 days

49

New EDI systemImproved risk-based inspections Payment deferrals of import duties and taxes

Peru: the economy that most eased trade in 2009/10

50

5. Want to Learn More?

Contact Us

www.worldbank.org/tradewww.worldbank.org/tradefacilitationwww.worldbank.org/tradelogisticswww.worldbank.org/lpiwww.worldbank.org/tradestrategy

Washington Office1818 H Street NW

Washington DC 20433

Contact: [email protected]

The World Bank GroupInternational Trade Department

51

Thank you. For more information:www.doingbusiness.org

52