world bank documentdocuments.worldbank.org/curated/en/463841468035510013/pdf/multi...document of the...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

bSwt No. 9162

PROJECT COMPLETION REPORT

INDIA

SECOND SINGRAULI THERMAL POWdER PROJECT(CREDIT 1027-IN)

NOVEMBER 30, 1990

Transport and Energy Operations DivisionCountry Department IVAsia Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir oMcial duties. Its contents may not otl arwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

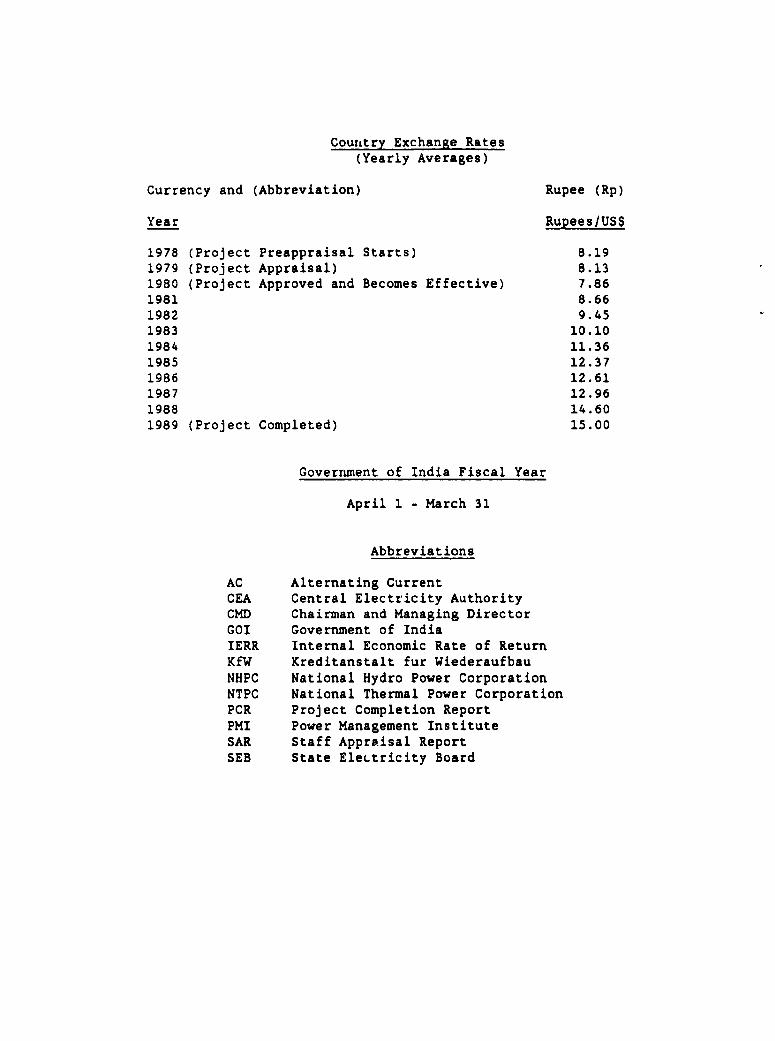

Country Exchange Rates(Yearly Averages)

Currency and (Abbreviation) Rupee (Rp)

Year Rupees/US$

1978 (Project Preappraisal Starts) 8.191979 (Project Appraisal) 8.131980 (Project Approved and Becomes Effective) 7.861981 8.661982 9.451983 10.101984 11.361985 12.371986 12.611987 12.961988 14.601989 (Project Completed) 15.00

Government of India Fiscal Year

April 1 - March 31

Abbreviations

AC Alternating CurrentCEA Central Electricity AuthorityCMD Chairman and Managing DirectorGOI Government of IndiaIERR Internal Economic Rate of ReturnKfW Kreditanstalt fur WiederaufbauNHPC National Hydro Power CorporationNTPC National Thermal Power CorporationPCR Project Completion ReportPMI Power Management InstituteSAR Staff Appraisal ReportSEB State EleLtricity Board

TFf WORLO OgbX FOR OFFICIAL USE ONLYWdvwnon. 0 C. a0433

U.S A

Otfie of Director-amoralOpaetatlma Uvalueati

November 30, 1990

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on IndiaSecond Singrauli Thermal Power Proiect (Credit l027-IN)

Attached, for information, is a copy of a report entitled "ProjectCompletion Report on India - Second Singrauli Thermal Power Project (Credit 1027-IN)" prepared by the Asia Regional Office. No audit of this project has beenmade by the Operations Evaluation Department at this time.

Attachment

The document ha a mtrgU datnbuton and may be tmmd by nm snm msh i tUN psvfwmameof their otkacS duum. It cont nu may not othetrw be dwine without Wul lAk XUtnoon.

FOR OFFICIAL USE ONLY

INDIA

SECOND SINGRAULI THERMAL POWER PROJECT(CREDIT 1027-IN)

2ROJECT COMPLETION REPORT

TABLE OF CONTENTS

Page No.

PREFACE ........................................................... i

EVALUATION SUMMARY ................................................ ii

PART I: PROJECT REVIEW FROM BANK's PERSPECTIVE .1Project Identity .1Background. 1Project Objectives. 1Project Description. 1Project Design and Organization. 2Project Implementation. 3Environment, Resettlement and Rehabilitation. 4Project Results. 5Project Sustainability ....................... , 6IDA Performance. 7Borrower Performance ...................... 7Project Relationship ................................... 8Consulting Services .................................... 8Procurement ............................................ 9Project Documentation ana Data ......................... 9

PART III: STATISTICAL SUMMARY .................................... 10

ANt'EXES ........................................................... 221 Ex-post Internal Economic Rate of Return2 Consolidated Income Statements3 Sources and Applications of Funds4 Balance Sheet

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

INDIA

SECOND SINGRAULI THERMAL POWER PROJECT

(CREDIT 1027-IN)

PROJECT COMPLETION REPORT

Preface

This is the Project Completion Report (PCR) for the Second SingrauliThermal Power Project in India, for which Credit 1027-IN in the amount ofUS$300 million was approved on May 22, 1980. The credit was closed on June30, 1989, one year and three months behind schedule. It was fully disbursedand the last disbursement was on March 15, 1990. Cofinancing in the amount ofDM 240 million was provided by Kreditanstalt fur Wiederaufbau (KfW) of FederalRepublic of Germany.

The PCR was jointly prepared by the Transport and Energy OperationsDivisicns, Country Department IV (India) and the Energy Division, TechnicalDepartment, both of the Asia Regional Office (Preface, Evaluation Summary,Part I and III). The Borrower did not prepare Part II as requested.

Preparation of this PCR was started by the Borrower during theAssociation's Supervision Mission in October, 1989. Subsequently, based onthe revised guidelines for PCRs, a fresh draft was begun on arrival of theAssociation's final Supervision Mission in February 1990, and is based,inter alia, on the Staff Appraisal Report (No. 2745b-IN), the Credit andProject Agreements, supervision reports, correspondence between IDA and theBorrower and internal IDA memoranda.

- ii -

INDIA

SECOND SINGRAULI THERMAL POWER PROJECT

(CREDIT 1027-IN)

PROJECT COMPLETION REPORT

Evaluation Summary

Objectives

The two main objectives of the project were: (i) to provide theNational Thermal Power Corporation (NTPC) assistance to construct two 200 MWand two 500 MW coal fired thermal power generating units as the second stageof NTPC's Singrauli Thermal Power Project to mitigate power shortages in theNorthern Region Interconnected system of India and (ii) to assist theGovernment of India (GOI) in achieving its objective of further advancing theregional and national integration of the power subsector (Part I, paras. 2 and3).

Implementation Experience

NTPC successfully implement.d the project. The first 200 MW unit(Unit No. 4) was commissioned three months behind schedule and the second 200MW unit (Unit No. 5) was commissioned as scheduled. The two 500 MW unitswhich were NTPC's first pithead coal fired 500 MW units were commissioned 10months (Unit No. 6) and 9 months (Unit No. 7) behind schedule after overcomingmany difficulties (Part I, paras. 11 and 14).

Results

The project fully achieved its main objectives through successfulcompletion of two 200 MW and two 500 MW units of the second stage of Singraulistation and associated 400 kV transmission lines. Following this completion,and with the addition of the three 200 MW units built within the first stage,the Singrauli fhermal Station became the first of the 2,000 MW class coal

K fired thermal stations of NTPC and, at that time, the largest power station inthe country.

NTPC's financial rate of return on historically valued net fixedassets for the last four years was between 14? and 172 against the covenantedrate of return of 9.5? for the period FY89 and beyond. The economic rate ofreturn of the project was about 20? against the estimated figure of 102 (PartI, paras. 18, 22 and 31).

Sustainability

The operational efficieuicy of NTPC in this power station as well asin other NTPC plants is good in spite of the continuing high growth rate ofthe utility, and thus contributes to sustaining the benefits from the projectsNTPC carries out (Part I, paras. 23 to 26).

- iii -

Findings and Lessons Learned

Major finding was as follows:

(a) The project management and construction management of NTPCexecuted the project very competently and were "forced,"through actual experience, to construct the first 2,000 MWcoal fired plant, including two 500 MW units, which werebeing installed in India for the first time. (Part I,para. 29).

Major lessons learned were as follows:

(a) To improve implementation performance and consequently toaccelerate disbursements, key actions should be taken up-front. In the case of this project, the projectconsultants should 2-.ve been requested to be appointed asearly as possible, id.t-lly before negotiations. Similarly,by the time the credit was presented to the Board, the biddocuments should have been ready. (Part I, para. 13).

(b) The Association could have been more forceful in seekingNTPC's compliance with the receivables covenant, a criticalelement to ensure NTPC's liquidity. (Part I, para 31).

(c) Similarly, the Association could have been more convincingin its efforts to improve the revenue covenant. (Part I,para 31).

(d) The Association should have acted earlier in identifyingremedies to alleviate the environmental and resettlementproblems and having them implemented by the authorities,and in enhancing NTPC's ability to address adequatelyenvironmental and resettlement matters. In this context,the implementation of the Environmental Action Plan agreedwithin the proposed Regional Power Systems Project shouldbe monitored by the Bank very closely (Part I, paras. 15 to17).

INDIA

SECOND SINGRAULI THERMAL POWER PROJECT(CREDIT 1027-IN)

PROJECT COMPLETION REPORT

PART I: PROJECT REVIEW FRUM BANK'S PERSPECTIVE

Project Identity

Name Second Singrauli Thermal Power ProjectCredit Number : 1027-INRVP Unit Asia RegionCountry : IndiaSector EnergySubsector : Power

Background

1. Power shortages of the 1970s and the adverse effect these were havingon the productive sectors of the economy prompted the Government of India(GOI) to intensify its efforts to balance the demand and supply ofelectricity. The strategy of the GOI was to supplement efforts of StateElectricity Boards (SEBs) in increasing installed capacity and theestablishment of high voltage transmission lines. Emphasis was laid in thepower subsector in: (a) accelerating the development of the hydropowerpotential and large coal fired power plants at both pithead locations and inthe proximity of load centers; (b) improving the efficiency of thermal powerplants and reducing losses in the transmission and distributionl networks;(c) expanding the rural electrification program; and (d) strengthening theorganizational and management capabilities of the SEBs. In 1974 GOI decidedto proceed with the construction of the first stage of four large thermalpower stations of 600 MW each at Singrauli, Korba, Ramagundam and Farakka,located near coal fields and supplying bulk power to the beneficiaries throughinterconnected 400 kV transmission systems. GOI established in 1975 two powergenerating companies, the National Thermal Power Corporation (NTPC) and theNational Hydro Power Corporation (NHPC) to construct and operate large thermaland hydro power stations and associated transmission systems. The feasibilitystudy of the Singrauli project was prepared by NTPC in 1978 and the projectappraisal was made by the Association in 1979.

Project Objectives

2. The primary objectives of the project were to: (a) provide NTPC withassistance needed to assume its envisaged role, including the mitigation ofpower shortages in the Northern Region of India; and (b) assist GOI inachieving its objective of further advancing the regional and ultimately thenational integration of the power subsector.

Project Description

3. The Second Singrauli Thermal Power Project (Credit 1027-IN) formedpart of NTPC's second stage thermal power aevelopment located on the fringe ofthe Rihand Reservoir close to the Singrauli coal field deposits in the Stateof Uttar Pradesh and consisted of the installation of two 200 MW and two 500

- 2 -

MW mine-mouth thermal power generating units and associated transmissionfacilities, including the followirg components:

(a) Two 700 tonnes/hour boilers and two 200 MW turbogenerating unitscomplete with all a.xiliaries and ancillary electrical and mechanicalequipment including switchyard; and

(b) Tvo 1,700 tonnes/hour boilers and two 500 MW turbogenerating unitscomplete with all auxiliaries and ancillary electrical and mechanicalequipment including switchyard;

(c) 400 kV Alternating Current (AC) Transmission System consisting of1,826 kms of lines 1/ and complete with all auxiliaries and ancillaryelectrical and mechanical equipment including switchyard.

Acquisition of steel for structural works, cement and reinforcementsteel under the scope of NTPC's ongoing other projects, was subsequentlyincluded under the scope of this project in 1986.

Project Design and Organization

4. As in the case of the first stage, the expansion phase of SingrauliDevelopment comprised a number of major works (including NTPC's first two 500MW units) and required careful coordination to ensure efficient progress.Much of the detailed power station engineering and design work had beencarried out for the first stage. NTPC had already acquired adequateexperience in the area of design and engineering of 200 MW units, especiallyfrom the first stage of the Singrauli power plant, and therefore there was noneed to appoint consultants for the 200 MW units. As for coal fired 500 MWunits, which were being installed for the first time in India, a consultantwas employed by NTPC to assist in the design, the preparation ofspecifications and bidding documents, the evaluation of bids and the projectmanagement for part of the project covering the two 500 MW units.

5. Under the first Singrauli project, GOI agreed to take necessary stepsto make available adequate coal supplies for the 2,000 MW power plant. Coalsupply has so far not hindered the operation of all units.

6. The project was prepared and timed by the Association in a manner toenable the Borrower to reduce the gap between the demand and supply of powerin the Northern Region Interconnected System, as well as to further strengthenthe institutional developmient of NTPC.

I/ 400 kV transmission lines consisted of the following circuits:

(Circuit km)Singrauli - Lucknow 402 (470)Lucknow - Moradabad 322 (330)Moradabad - Muradnagar 132 (150)Muradnagar - Panipat 36 ( 95)Singrauli - Kanpur II 384 (455)Kanpur - Agra-Jaipur 500 (475)

Total: 1,826 (1,975)

Figures in parentheses show estimation at the time of appraisal.

7. At the time of appraisal, NTrC had ad3pted a two-tier organizationalstructure--one at the central/corporate~± level and the otner at the projectsites. Technical services, contract and procu:ement services and qualityassurance, etc. were centralized. For each of four power plants, a projectcrganization group under the control of a General Manager was organized tomanage the implementation of the particular project.

8. NTPC was recrganized, subsequently, after the appraisal to have athree-tier organizational structure:

(1) Corporate level;(2) Regional level; and(3) Project level.

9. The Corporation is headed by a Chairman and Managing Director (CMD),who is assisted by five full-time functional Directors, namely, Director(Projects), Director (Operation), Director (Technical), Director (Finance) andDirector (Personnel). At the Corporate Office, corporate planning, centralprocurement and vigilance functions are headed by Executive Directorsreporting to the CMD. For the purpose of the administration and execution ofwork at the sites, the Corporation is divided into five regions (North, West,East South and National Capital) whose headquarters are at present located atAllahabad, Nagpur, Patna, Hyderabad and Delhi, respectively. These regionsare under the control of Regional Executive Directors whc are responsible forthe implementation and operation and maintenance of power plants andtransmission systems iL their respective regions. Ev3ry power piant andregional transmission unit is headed by a General Manager.

10. The new structure has the advantage of reducing and optimizing thespan of control of the CMD. The structure provides for decentralization ofline responsibility while retaining centralized systems in areas such as long-term planning, basic engineering, procurement of critical equipment andspares, quality assurance, co-ordination with the World Bank and otherfinancing agencies, inspection, etc.

Project Implementation

11. The fi.rst 200 MW unit (Unit No. 4) was commissioned in November 1983,three months behind the original schedule and the second 200 MW unit (Unit No.5) was commissioned in February 1984 as scheduled. (Dates of commissioning atthe appraisal estimate were August, 1983 and February, 1984 respectively.)The three months' slippage for the No. 4 unit was largely on account ofcyclonic damage caused to tower crane in May, 1982 which hampered the physicalprogress of the boiler erection. Subsequently, the project management groupperformed well to opt.imize utilization of available resources and preventingfurther delay. The boiler erection work was efficiently managed by use ofmobile cranes and winches. The No. 5 unit was commissioned as planned inFebruary, 1984.

12. The first 500 MW unit (Unit No. 6) had been planned for commissioningin February, 1986, followed by the second unit (Unit No. 7) one yearthereafter (February, 1987), whereas the actual commissioning took place inDecember, 1986 and November, 1987 respectively.

13. The selection and appointment of the consultants for the 500 MW unitstook more time than envisaged at the appraisal stage. Instead of September,1979 as forecast in the SAR, the actual appointment was done in April, 1980.

Consequently, in order to allow for review of technical specificationg forsteam generator package, the Notice for Invitation to Bids was released onlyin December, 1980, thirteen months later than the scheduled d'ate of November,1979 (SAR), and the contract was awarded in January, 1982 instead of May, 1980(SAR).

14. Considering the implementation of India's first coal fired 500 MWunits involving 70,000 cu m. of concreting work, 32,000 MT of structurel steelerection. 79,000 MT Boiler parts erection, 30 kms of piring and 3,400 kms ofcable work with peak manpower of 11,000, not to mention the numerous problemsfaced in the field, e.g.. transportaticn damage to boiler ceiling girder, useof specially designed rail trolley wagons for generator stations, etc., theslippage of 10 months may be considered reasorable.

Environment, Resettlement and Rehabilitation

15. The project was designed to comply with the applicable environmentalquality standards prevalent in India at that time. The increasing demand forelectricity in India has required the construction of either largehydroelectric schemes or coal-fired thermal power stations, most of themlocated close to associated open cast coal mines, which in general have animportant impact on the surrounding communities and on the balance ofecological systems. The Singraufi regional area i.s a particular case in point-- and has been labeled 'The Energy Capital of India." The association ofextensive coal reserves and a large water reservoir, created in the 1960sfollowing the construction of the Rihand dam for the purpose of powergeneration and irrigation, has favored the implementation of several thermalpower stations - six at present totaling around 7,200 MW and more are eitherunder construction or planned, - as well as other industries (i.e., sevencement plants, an aluninum smelting and a chemical plant) and the developmentof several coal mines. Although the region was rather arid and sparselypopulated, rapid industrial development, the lack of basic infrastructure, andthe absence of coordination between different public administrations - theSingrauli area lies on the border of two states, Uttar Pradesh azid MadhyaPradesh - have exacerbated the impact on the indigenous population as well ason the process of industrial urbanization. The deteriorating situation hasbeen a source of serious concern as.:eng local, national and internationalenvironmv-%talists.

16. The implementation ot the Project, including the expansion phase of1400 MW, required the acquisition of 1,901 hectares (4,752 acres) resulting incompensation of 1,450 families affecting 15 villages. Part of the requiredarea, located at about eight km from the plant, was needed for dumping theash. A limited number of shops were also allotted to oustees in the NTPCsh:-pping complex. NTPC has also provided civil amenities in the relocationcolonies, including medical facilities, periodic visits by medical officersand preventive check up, public health is increasingly deteriorating in thecolonies, partly as a result of a larger squatter settlement, which has grownaround the area. Limited rnmbers of oustees were given employment and on-the-job training by NTPC, and employed through various contractor3 working for theprojec;.. However, no employment opportunities have been provided to amajority of the oustees, because of their low level of skills. However, ithas to be recognized that there are limits to NTPC's ability to resolve allthe environmental issues associated with a power developmen. -project and thatthe local government authorities should be responsible for the public

- 5-

infrastructure needed in the context of a large project deve.apment. NTPC hasalso t'.keri appropriate measures with regard to stack emissions and watereffluents. They regularly monitor these aspects of environmental protectionand comply so far fully with environmental quality 3tandards prescribed by theGovernment. In addition, through a continuous afforestation program, a largenuzioer of trees of various species have been planted and this will be expandedin the future, notably in order to rehabilitate the ash pond area.

17. As a result of problems encountered and experience gained inSingrauli, as well as in other projects, including the Bank-financed Korba,Ramagundam and Farakka thermal-power plants, the Bank encourabed NTPC. tobecome more aware oc the particular complexities associated with environmentaland especially -ith resettlement issues. The recent projects -- e.g. theTalcher Thermal Power Pioject (Ln. 2845-IN) and the proposed NTPC-RegionalPower Systems Project -- the approach has been from the beginning morecomprehensire. In the Talcher project a detailed environmental impactassessment was prepared prior to beginning the construction works. In thecase of the proposed NTPC-Regional Power Systems Project, NTPC first recruitedstaff specialized in social and environmental sciences and then undertook areview of the environmental aspects at the four above-mentioned Bank-financedpower stations in order to Implement corrective measures to adequatelyrehabilitate and preserve the physical and social environment in those areasaffected by these proiects. To achieve this, NTPC has prepared anEnvironmental Action Plan (EAP) addressing aspects related to:(i) preparation of Environment Impact Assessments for existing and futureprojects; (ii) resettlement and improvement of living conditions of thedisplaced population, and (iii) development of afforestation plans. InSingrauli, an element of the EAP is the Regional Environmental ImpactAssessment (EIA) financed by the Bank dnd presently being carried out byconsultants. In addition to the Singrauli power plant, the Regional EIA alsocovers the 1000 MW Rihand and 1200 MW Vindhychal thermal power stations, whichare owned and operated by NTPC in this area. The purpose of the study is toidentify critical environmental factors and exarine alternative ways tomitigate them. It is expected that the Regional EIA would be completed byFebruary 1991. The recommendations of the EIA will be inco-porated into theEAP.

Project Results

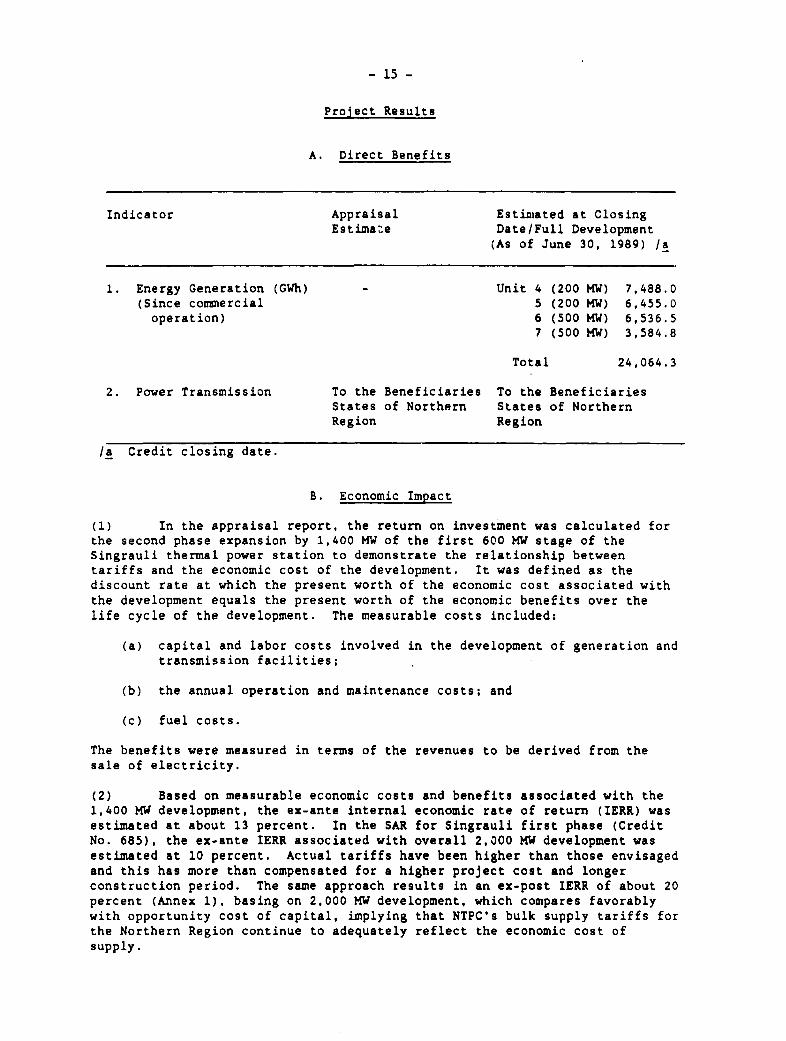

18. The project fully achieved its main objectives of meeting growingdemand of Northern Region through successful completion of additional powergeneration of 1,400 MW and associated 400 kV transmission lines. As a resultof completion, the Singrauli Thermal Station has become the first 2,000 MWclass coal-fired thermal power station among four projects which were assignedto NTPC under the power expansion plan identified by GOI in 1974. Thecumulative generation from Singrauli II units, from the beginning ofcommercial operation up to June 30, 1989 (the date at which the credit wabclosed) was 24,064 GWh. The unit details are given in Part III.

19. The estimated cost of the project at appraisal and actualdisbursements is given in Part III. The appraisal cost estimate ofRs. 8,20Q.0 million had increased to Rs. 10,668.40 million representing 302increase. An increase of Rs 1,356.3 million was due to price escalation andRs 652.8 million due to change in scope for power stationi facilities. Theincrease of Rs 35.7 million was due to change in price of transmissionfacilities while Rs 306.1 million change was due to scope change in price of

transmission lines. The remainiing increase of Rs 108.5 million was on accountof engineering, administration, consulting, interest during construction andworking capital requirements.2/ The price escalation was mostly due to theincrease in foreign exchange rate for the dollar which went up Rs 8.4 per US$at the time of appraisal to around Rs 15 per USS when the project wascompleted. When considering the total project cost estimates in dollar value,however, they amount to US$977.2 million in the appraisal and US$927.7 millionactually, rest.lting in a decrease of 5X, due to the rapid decrease of therupee value against the dollar. The average exchange rate for the period ofdisbursement from the IDA credit vas Rs 11.5 per USS (para. 34), resulting ina depreciation of about 35% in the value of Indian Rupees to US dollars.Thirty percent was reflected in the project cost expressed in local currencyand 5% was reflected in the decrease of costs expressed in U.S. dollars.

20. The estimated disbursements at appraisal and actual disbursements aregiven in Part III. The original closing date of the Credit was March, 1988.Actually the Credit was closed on June 30, 1989, one year and three monthsbehind schedule. Disbursements against commitments were made until March 15,1990.

21. The allocation of the Credit into various categories and actualdisbursement by category is shown in Part III.

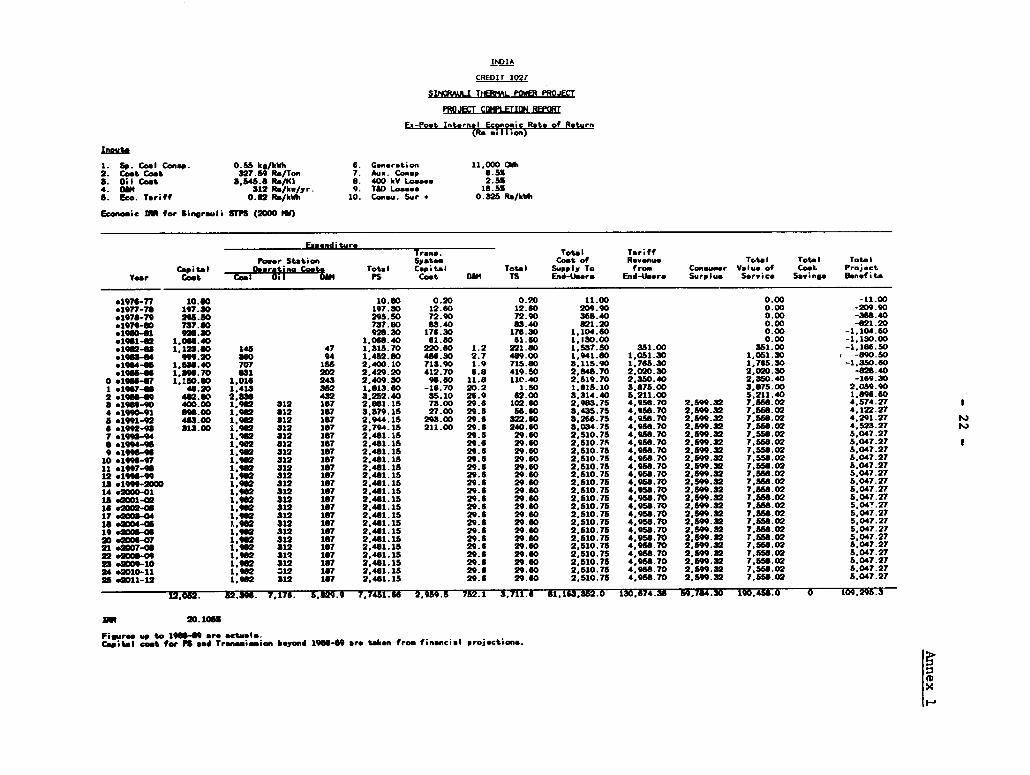

22. In the SAR, the e.-ante internal economic rate of return (IERR) forthe project was estimated at about 13 percent, based on measurable ecjnomiccosts and benefits associated with the 1,400 MW development. In the SAR forthe Singrauli first phase (Credit No. 685), the ex-ante IERR associated withoverall 2,000 MW development was estimated at 10 percent. The ex-post IERRfor the 2,000 MW development is about 20 percent as shown in Annex 1.

Project Sustainability

23. As in most power projects, the economic evaluation of the project inboth the SAR and the PCR, uses revenues from sales as a proxy for economicbenefits and therefore does not give a full picture of all the benefits.Further, sustainability of benefits from power projects is closely linked to

that of the sector and of the utility. Therefore, in the present context, ithas to be ascertained in a rather qualitative way, through the factors thataffect it.

24. The political and economic environment has been stable and is

expected to continue to be so. For many years there have been shortages in

the supply of electricity. These are likely to persist, because, although GOIis strongly committed to the development of the power sector as one of thebases for both industrial and rural development, the Government is not inposition to allocate the full amount of funds the sector would require to meet

the demand. The unresolved discrepancies between the states' and GOI'spositions concerning the organization and the roles of the various entities ofthe sector may tend to lead to economically sub-optimal solutions, but not toan extent that they would endanger sustainability of benefits from existingfacilities, in general, and from the Singrauli power plant, in particular.

25. The institutional let up of the sector is progressing, albeit slowly,towards a structure c3mbining as muc.'. as possible regionalization of

2/ Including increase of working capital requirements of NTPC (Rs 99.9million), which were not taken into account in the appraisal.

operations with countrywide optimization of the use of resources. There isstill a long way to go to achieve such optimization.

26. The project was successful in that all the four units were completedsatisfactorily and are generating the much needed electricity for the NorthernRegion. NTPC's capacity in designing and implementing 200 MW units wasstrengthened and successfully tested, while the Corporation obtained its know-how in the design and implementation of 500 MW units. Operational efficiencyof Singrauli and NTPC's other power plants and transmission system is good inspite of the continuous high growth rate of the utility and thus contributesto sustaining benefits from the projects NTPC carries out. Strengthening ofNTPC's project design, implementation, operation and maintenance capabilitiestogether with the realization of successfully operating 1400 MW additionaloperating capacity are indicators that show that benefits from the projectwould be sustained over the long-term.

IDA Performance

27. The performance of the A;sociation from the project preparationthrough project completion was satisfactory. The Association maintained goodrelations with the beneficiary throughout the execution of the project andfostered an environment conducive to increased Bank Group involvement withNTPC. To date, the Bank Group has assisted NTPC in implementing a total of 13projects with a total assistance of about 4 billion dollars. Through theseoperations the Bank Group has been strengthening the institutional andfinancial viability of the corporation. It is important to highlight that,during this initial decade of development, NTPC and the Bank Group developed aclose relationship, during which the Bank Group has endeavored to support NTPCin each step of its development, in a manner that goes much beyond thesubstantial financial assistance extended to its expansion plan.

28. The Bank Group has also continued addressing a number of shortcomingsof broader sectoral concern. The major items are:

(a) During the preparation of the recent projects, a more comprehensiveand up-front approach towards environmental protection, resettlementand rehabilitation issues has been adopted and an EnvironmentalAction Plan, aimed to complement earlier efforts, has already beendrawn up for Singrauli, Korba, Ramagundam and Farakka projects, underthe recently negotiated NTPC-Regional Power Systems Project;

(b) Implementation of an Action Plan to liquidate accumulation of arrearsreceivable from SEBs; and

(c) Development of the Power Management Institute (PMI) to providespecialized training in management and other aspects of the powersector.

Borrower Performance

29. The performance of NTPC was generally commendable and met most of theexpectations of the appraisal report. Although some delays in procurement forthe 500 MW units were experienced as stated in para 13 Part I, the first 500MW units in NTPC projects could be successfully completed under the wellestablished control of NTPC project management by encountering numerousdifficulties.

30. As a direct outcome of development of Singrauli and other subsequentprojects, NTPC has made good progress in building up its organization andmanpower resources. NTPC had accorded special importance on the training ofengineers, and operating staff as well as managerial staff. This success ofNTPC's first sulper thermal power project had been primarily as a result of theimplementation of a well planned training program with concentration on pre-operational spheres of activity such as planning, design and construction.

31. The financial performance of NTPC during this period ofimplementation and initial years of operation were satisfactory. Inparticular, NTPC has been able to expand and diversify its sources of projectfinancing. Recently, NTPC has floated bonds in the domestic market in threepublic issues, as well as two private placements, for a total of aboutRs 16.83 billion (US$990 million at the exchange rate at the time of thefinancial operations). Further data on NTPC's finances are given in Part III.The covenanted rate of return from April 1, 1988 on historically valued fixedassets in operation was 9-1/2 percent. Against this, the rates of return forNTPC from FY84 to FY89 are as given below:

FY84 FY85 FY86 FY87 FY88 FY89

Financial Rate 11.2 12.7 16.8 17.0 16.4 14.8of Return

This high level of rates of return, however, did not translate intoadequate self-financing ratios (the average for the last six years was 6.7%),partially because of NTPC's ambitious expansion program and partially becausethe actual cash flow generated by operations was adversely affected by poorcollections, which during the last four years have increased to levelsequivalent to up to five months of sales, above the covenanted two monthsceiling. Th.'s highlights a shortcoming of the rate of return covenant whichdoes not differentiate between income accrued and income actually received.Suggestions to modify the revenue covenant were not agreed to by GOI and NTPC.To correct the collection problem an action plan has been drawn up inconsultation with the Association.

Project Relationship

32. Good relationships were maintained by the Association with theBorrower.

Consulting Services

33. Since NTPC had acquired adequate experience in the area of design andengineering of 200 MW units especially from the first stage of the Singraulipower plant, there was no need to appoint consultants for the engineering ofthe 200 MW units. For 500 MW units which were installed for the first time inIndia, foreign consultants (a USA firm) were employed to provide NTPCtechnical assistance in the design, the preparation of specification andbidding documents and the evaluation of bids and the project management forthis part of the project. The performance of the consultants wassatisfactory.

_-9

Procurement

34. Bank guidelines were strictly adhered to by NTPC for procurement of39 contracts involving international competitive bidding. Rs 3,449.9 millionequivalent was disbursed from the IDA Credit as against USS 300 million.Thirteen contracts were awarded to foreign firms for an amount estimated atUS$46.0 million. The average procurement time per contract -- from theissuance of bid documents to contract award -- was nearly one year, consistingof around 3.1 months for bidding and about 8.4 months for bid evaluation.This latter time is certainly too long and constitutes a major source ofimplementation delay. However, some progress in this regard has been made sofar in subsequent projects undertaken by NTPC (e.g. Farakka II). NTPC is inthe process of finalizing with the Bank a standard bidding document which isexpected to cut down the time lag substantially. Several contracts wereamended to include either supply of spare parts for equipment or additionalquantity of material. No significant claims were raised by bidders.

Project Documentation and Data

35. The project's legal agreements adequately reflected the Association'sinterests in a satisfactory execution of the project. The staff appraisalreport was comprehensive, well prepared and provided a useful framework forthe Association and NTPC during the project implementation. The Borrowerregularly submitted Quarterly Progress Reports for the project. This has beenused for review of physical and financial performance and it was generallyused for planning visits of the supervision missions to India, which oftenincluded site visits in addition to review meetings at NTPC Corporate Office,New Delhi.

- 10 -

PROJECT COMPLETION REPORT

SECOND SINGRAULI THERMAL POWER PROJECT(CREDIT 1027-IN)

PART III. STATISTICAL SUMMARY

Related IDA Credit

Credit No. Year ofTitle Purpose Approval Status Comments

Closed inCredit 685-IN To help reduce the April 1977 June 1984 The projectSingrauli power shortage in was success-Thermal Power the Northern Region fully

through the completedconstruction of thethree 200 MW initialphase of the NTPC'sfirst large coalfired thermal powerplant withassociated 400 kVtransmission lines.

Project Timetable

Date Date DateItem Planned Revised Actual

Appraisal Mission 05/79 05/79Credit Negotiation 05/80Board Approval 05/22/80Credit Signature 06/05/80Credit Effectiveness 07/30/80Credit Closing 03/31/88 06/30/89 06/30/89Credit Completion 12/31/89 L1

/1 The last disbursements weLe made in February 1990, witi. authorization onan exceptional basis by the Regional Vice President.

- 11 -

Credit Disbursements

Disbursements (in $ million)Credit 1027-IN

IDA Fiscal Year Estimated Actual Actual Z ofand Semester Cumulative Cumulative Estimated

1981 1 20 10.78 53.902 50 20.85 41.70

1982 1 75 24.70 32.932 140 59.35 42.39

1983 1 180 61.41 34.122 220 80.43 36.56

1984 1 250 92.93 37.202 265 129.70 48.94

1985 1 275 140.38 51.052 280 182.45 65.16

1986 1 285 192.68 67.612 290 234.00 80.69

1987 1 295 240.19 81.422 300 273.77 91.26

1988 1 280.07 93.362 285.18 95.06

1989 1 285.18 95.062 292.84 97.61

1990 1 293.26 97.752 300.00 100.00

- 12 -

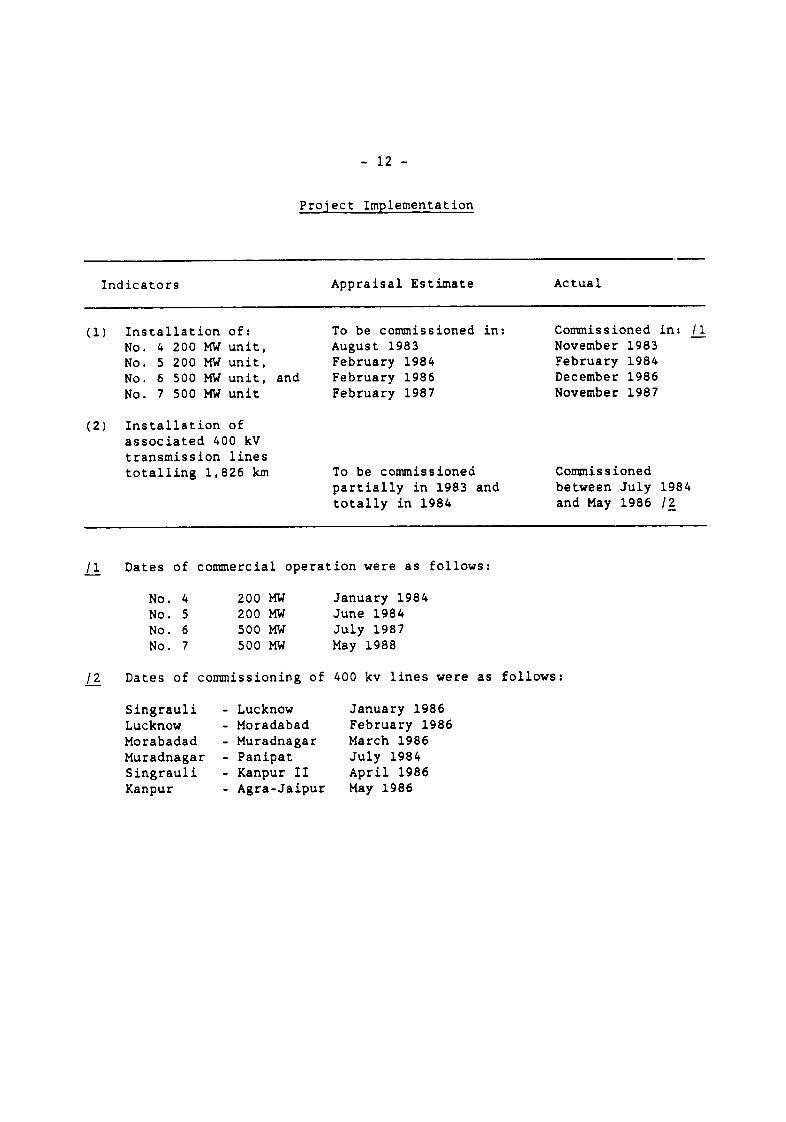

Project Implementation

Indicators Appraisal Estimate Actual

(1) Installation of: To be commissioned in: Commissioned in: /1No. 4 200 MW unit, August 1983 November 1983No. 5 200 MW unit, February 1984 February 1984

No. 6 500 MW unit, and February 1986 December 1986

No. 7 500 MW unit February 1987 November 1987

(2) Installation ofassociated 400 kVtransmission linestotalling 1,826 km To be commissioned Commissioned

partially in 1983 and between July 1984totally in 1984 and May 1986 /2

/1 Dates of commercial operation were as follows:

No. 4 200 MW January 1984No. 5 200 MW June 1984No. 6 500 MW July 1987No. 7 500 MW May 1988

/2 Dates of commissioning of 400 kv lines were as follows:

Singrauli - Lucknow January 1986Lucknow - Moradabad February 1986Morabadad - Muradnagar March 1986Muradnagar - Panipat July 1984Singrauli - Kanpur II April 1986Kanpur - Agra-Jaipur May 1986

- 13 -

Project Costs and Financing

A. Comparison of Estimated and Actual Projects Costs

SAR Actual SAR Actual-- Rs million -- -- US$ million --

Prelimir.ary Works 2.7 /1 0.3 /1

Civil Works 457.0 1,558.1 54.4 135.5

Electrical and Mechanical Plant 3,050.7 5,865.1 363.2 510.0

Coal Handling and Transportation 120.0 184.8 14.3 16.1

Transmission (400 kV) 1,162.3 1,989.9 138.4 173.0

Engineering and Administration 434.4 785.1 51.7 68.3

Miscpllaneous Tools - 56.2 - 4.9

Contingency (Physical) 262.4 /2 31.1 /2Contingency (Price) 1,685.2 /2 200.7 /2

Duties and Taxes 505.9 /2 60.2 /2

Total Project Cost 7,680.5 10,439.2 914.3 907.8

Interest during Construction 528.4 129.3 62.9 11.2

Working Capital Requirements - 99.9 - 8.7

Total Financing Required 8,209.0 10,668.4 977.2 927.7

/1 Included in civil work cost./2 Covered under respective package costs.

Comments: The reasons for cost overruns have been explained underpara. 19 Part I.

- 14 -

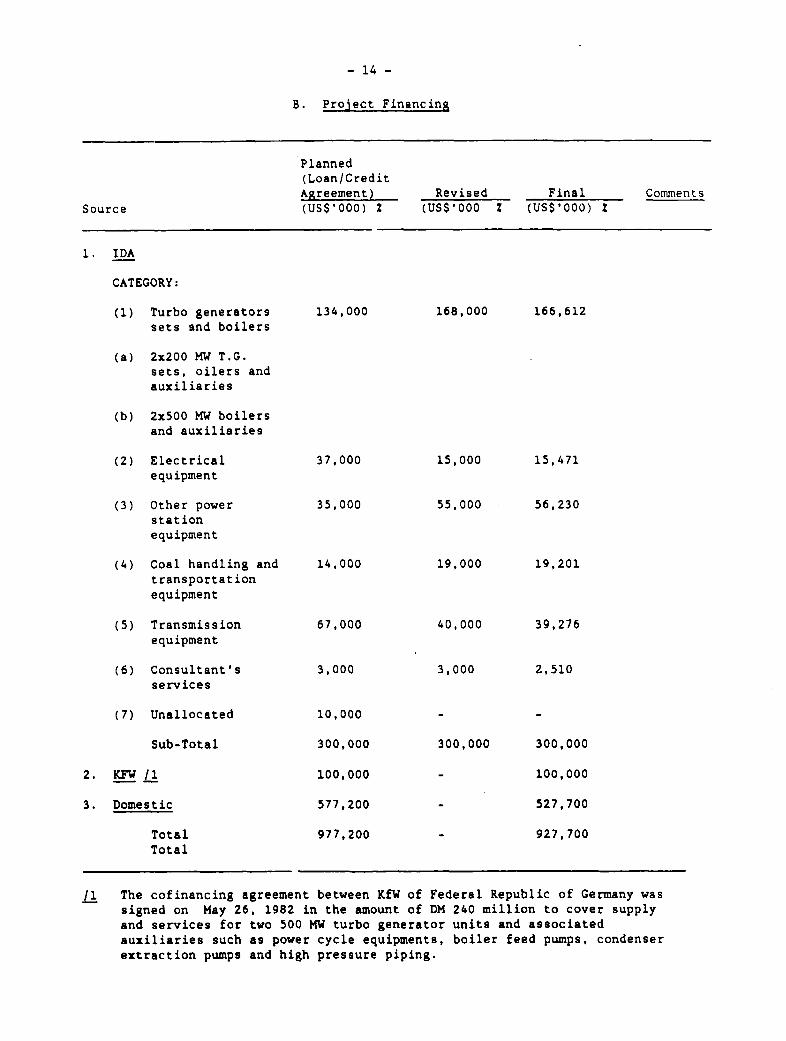

B. Project Financing

Planned(Loan/CreditAgreement) Revised Final Comments

Source (US$'000) Z (US$'000 Z (US$'000) i

1. IDA

CATEGORY:

(1) Turbo generators 134,000 168,000 166,612

sets and boilers

(a) 2x200 MW T.G.sets, oilers andauxiliaries

(b) 2x500 MW boilersand auxiliaries

(2) Electrical 37,000 15,000 15,471

equipment

(3) Other power 35,000 55,000 56,230

stationequipment

(4) Coal handling and 14,000 19,000 19,201

transportationequipment

(5) Transmission 67,000 40,000 39,276

equipment

(6) Consultant's 3,000 3,000 2,510

services

(7) Unallocated 10,000 - -

Sub-Total 300,000 300,000 300,000

2. KFW /1 100,000 - 100,000

3. Domestic 577,200 - 527,700

Total 977,200 - 927,700

Total

/1 The cofinancing agreement between KfW of Federal Republic of Germany was

signed on May 26, 1982 in the amount of DM 240 million to cover supply

and services for two 500 MW turbo generator units and associated

auxiliaries such as power cycle equipments, boiler feed pumps, condenser

extraction pumps and high pressure piping.

- 15 -

Project Results

A. Direct Benefits

Indicator Appraisal Estimated at ClosingEstimate Date/Full Development

(As of June 30, 1989) /a

1. Energy Generation (GWh) - Unit 4 (200 MW) 7,488.0(Since commercial 5 (200 MW) 6,455.0operation) 6 (500 MW) 6,536.5

7 (500 MW) 3,584.8

Total 24,064.3

2. Power Transmission To the Beneficiaries To the BeneficiariesStates of Northern States of NorthernRegion Region

/a Credit closing date.

B. Economic Impact

(1) In the appraisal report, the return on investment was calculated forthe second phase expansion by 1,400 MW of the first 600 MW stage of theSingrauli thermal power station to demonstrate the relationship betweentariffs and the economic cost of the development. It was defined as thediscount rate at which the present worth of the economic cost associated withthe development equals the present worth of the economic benefits over thelife cycle of the development. The measurable costs included:

(a) capital and labor costs involved in the development of generation andtransmission facilities;

(b) the annual operation and maintenance costs; and

(c) fuel costs.

The benefits were measured in terms of the revenues to be derived from thesale of electricity.

(2) Based on measurable economic costs and benefits associated with the1,400 MW development, the ex-ante internal economic rate of return (IERR) wasestimated at about 13 percent. In the SAR for Singrauli first phase (CreditNo. 685), the ex-ante IERR associated with overall 2,000 MW development wasestimated at 10 percent. Actual tariffs have been higher than those envisagedand this has more than compensated for a higher project cost and longerconstruction period. The same approach results in an ex-post IERR of about 20percent (Annex 1), basing on 2,000 MW development, which compares favorablywith opportunity cost of capital, implying that NTPC's bulk supply tariffs forthe Northern Region continue to adequately reflect the economic cost ofsupply.

- 16 -

C. Financial Impact

(1) As per the agreement, NTPC was to sell power from the project to SEBsin the Eastern Region 1/ under bulk supply contracts satisfactory to the BankGroup and GOI was to ensure that all necessa.y steps were taken to obtain anundertaking from respective State Governments to purchase, in the aggregate,not less than 85Z 2/ of the output of power from the Project. GOI and NTPChave complied with their commitment despite an initial delay in the signing ofthe bulk supply contracts. NTPC's operating and financial performance,however, was not adversely affected by this delay.

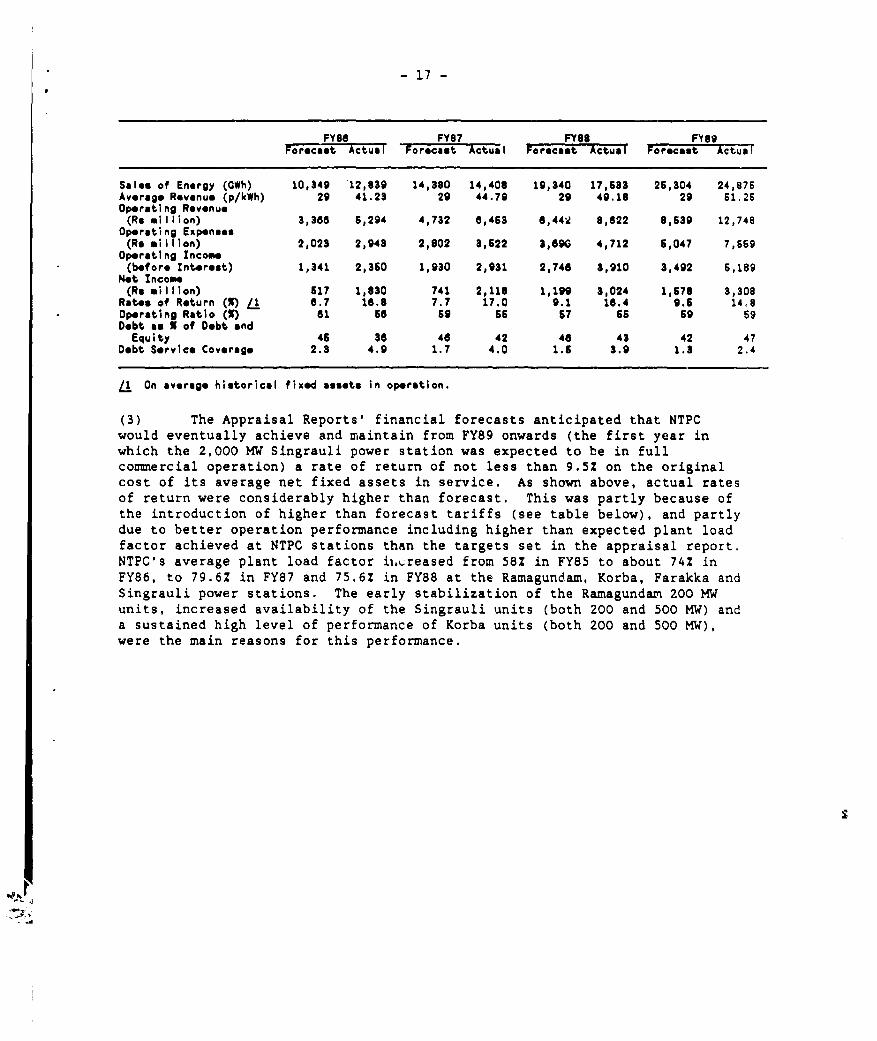

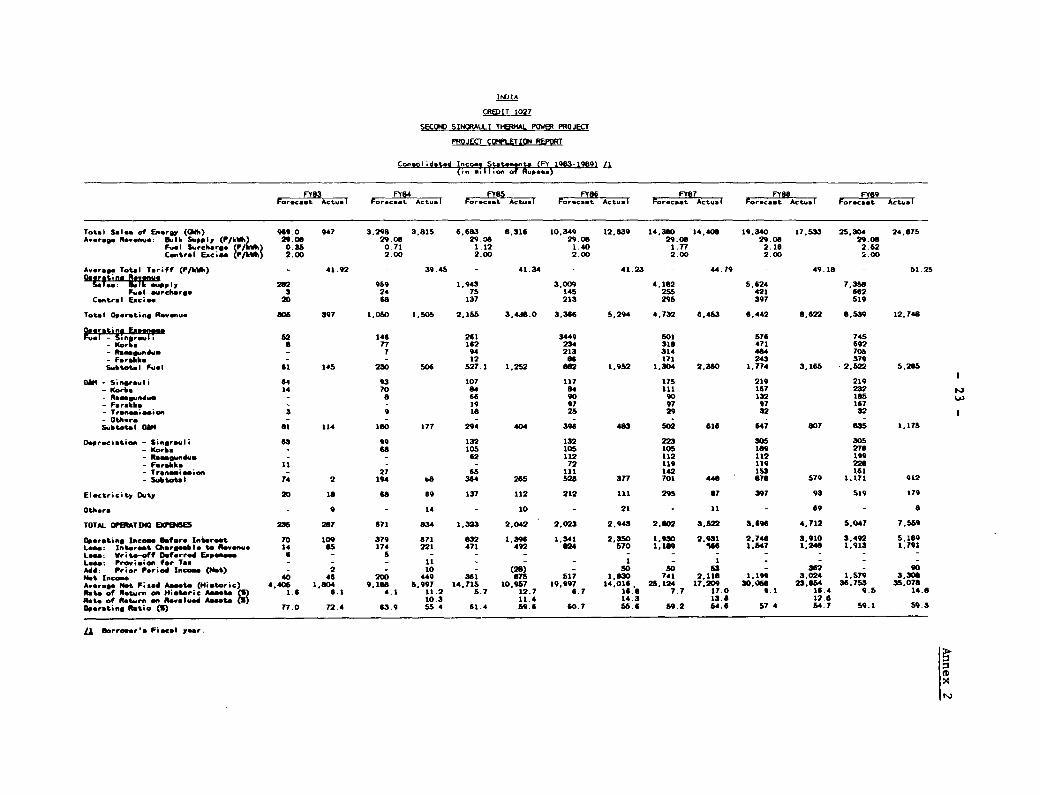

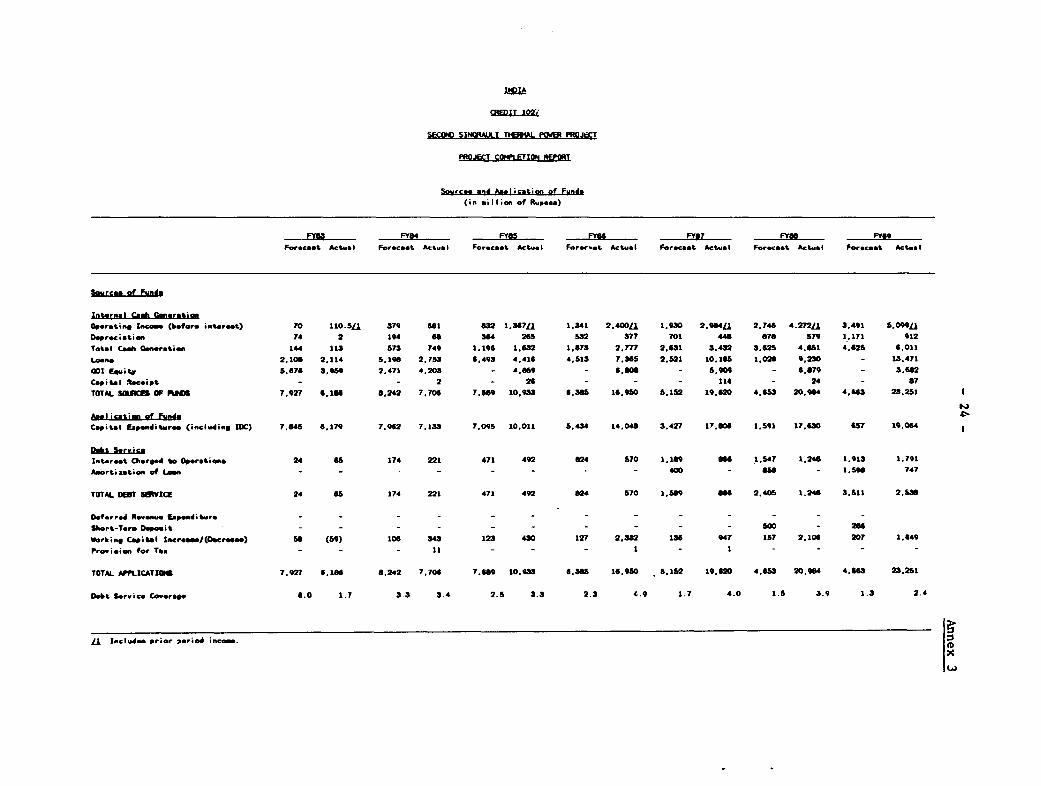

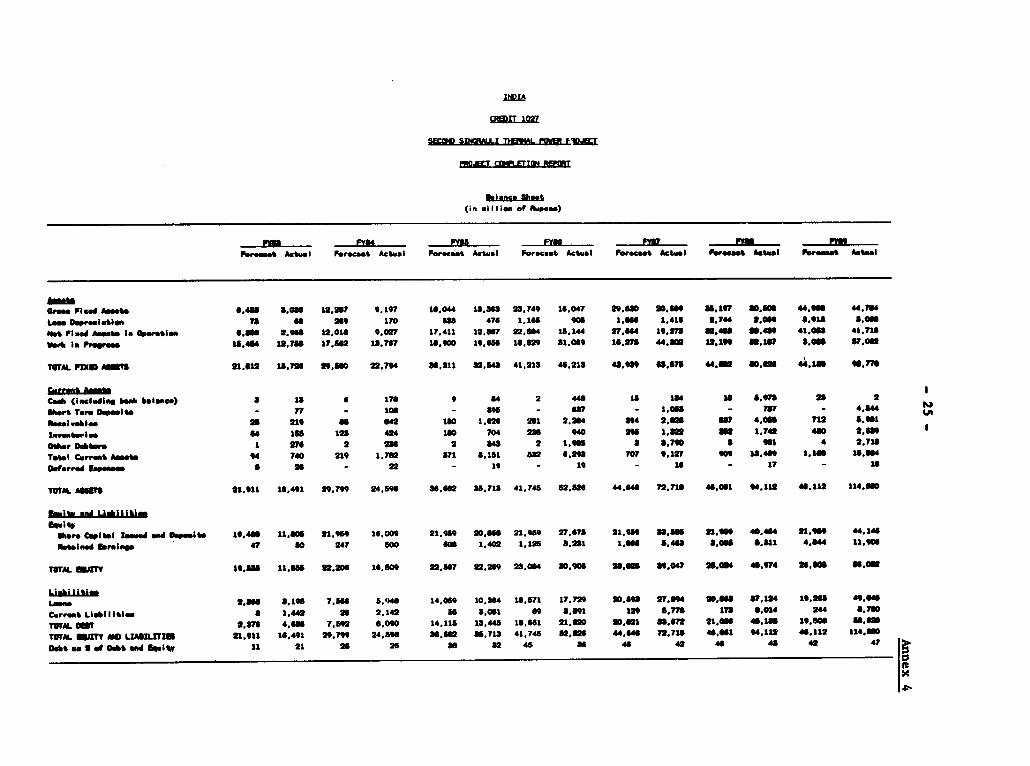

(2) NTPC's actual and project financial statements for the periodFY83-FY89 are presented in Annexes 2 to 4. The most salient feature of NTPC'soperations during the period FY84-FY88 is the spectacular growth thecorporation experienced. While net fixed assets in operation has increased4.62 times, sales of electricity increased by more than 6 times. Even morestriking is the high level of investment in projects under construction.Work-in-progress at the end of the period was almost 1.37 times that of assetsin operation. This reflects the continuation of a highly acceleratedexpansion program which, in turn, explains why the self-financing ratioremained modest during the period, representing only 6.7Z of the totalfinancing requirements, despite the reasonable rates of return achieved(around 16Z in the last three years, well in excess of those projected in theappraisal reports, and much higher than the 9.5Z required under the loan as atarget for FY89). Debt service coverage was very comfortable during tneperiod because repayment of debt started only in FY89. Current ratio, whichwas below one during the earlier part of the period improved to 1.8 by FY89.However, a closer look at the working capital position of NTPC reveals,starting in FY83, a very unsatisfactory collection performance. Under recentloans, a covenant was introduced that requires that NTPC's receivables shouldnot exceed the equivalent of two months of sales. However, despite its bestefforts, NTPC has not been able to achieve this covenanted target. The GOI,Bank and NTPC have agreed on a set of actions that are expected to correct thesituation. Satisfactory first steps of this action plan is a condition forthe presentation to the Board of the proposed Regional Power Systems Project,which would cover NTPC's further investments. The following table representsthe key operational results forecast in the appraisal report compared withactuals:

1/ Power from the Project was to be sold in bulk to the State ElectricityBoards of Bihar, West Bengal and Orissa and the Damodar ValleyCorporation.

2/ The remaining 15Z was to be sold in accordance with priorities to bedetermined by CEA.

- 17 -

FY86 FY87 FY88 FY89Forecast Actual Forecast Actual Forecast Actual Forecast Actual

Sales of Energy (OWh) 10,349 12,839 14,380 14,408 19,340 17,633 26,304 24,876Average Revenue (p/kWh) 29 41.23 29 44.79 29 49.18 29 61.26Operating Rovenue(Ru million) 3,366 6,294 4,732 6,463 6,442 8,622 8,639 12,748

Operating Expenses(Rs million) 2,023 2,943 2,802 3,622 3,690 4,712 5,047 7,669

Operating Income(before Interest) 1,341 2,360 1,930 2,931 2,746 3,910 3,492 6,189

Net Income(Rs million) 617 1,830 741 2,119 1,199 3,024 1,678 3,308

Rates of Return (%) /I 8.7 168. 7.7 17.0 9.1 16.4 9.6 14.8Operating Ratio (1) 61 6G 69 66 67 66 69 69Debt as X of Debt andEquity 46 36 46 42 46 43 42 47

Debt Service Coverage 2.3 4.9 1.7 4.0 1.6 3.9 1.3 2.4

/l On average historical fixed assets in operation.

(3) The Appraisal Reports' financial forecasts anticipated that NTPCwould eventually achieve and maintain from FY89 onwards (the first year inwhich the 2,000 MW Singrauli power station was expected to be in fullcommercial operation) a rate of return of not less than 9.52 on the originalcost of its average net fixed assets in service. As shown above, actual ratesof return were considerably higher than forecast. This was partly because ofthe introduction of higher than forecast tariffs (see table below), and partlydue to better operation performance including higher than expected plant loadfactor achieved at NTPC stations than the targets set in the appraisal report.NTPC's average plant load factor ii.reased from 58X in FY85 to about 742 inFY86, to 79.6X in FY87 and 75.6Z in FY88 at the Ramagundam, Korba, Farakka andSingrauli power stations. The early stabilization of the Ramagundam 200 MWunits, increased availability of the Singrauli units (both 200 and 500 MW) anda sustained high level of performance of Korba units (both 200 and 500 MW),were the main reasons for this performance.

' _

-18 -

Financial Average Tariffs Percentage increaseYear Forecast Actual over forecast (2)

(P/KWh) (P/KWh)

FY86 32.52 41.23 26.8FY87 32.91 44.79 36.1FY88 33.31 49.18 47.6FY89 33.75 51.25 51.9

(4) During the FY85-FY89 period, NTPC financed 572 of its rapid growth byborrowing. GOI financed about 532 of NTPC's total requirements, two-thirds ofit through equity contributions and the balance as loans. This denotes aheavy reliance on GOI support, which during NTPC's initial period of growthwas a sound policy. The Bank Group has financed approximately Rs 18.37billion, or nearly one-fifth of NTPC's total financial requirements over thepast five years. GOI's loans have a total maturity of 20 years, including 5years of grace and an interest rate which has changed over time and currentlyis 152 p.a. It is worth noting that NTPC has floated bonds in the domesticmarket in three public issues, as well as two private placements, for a totalof about Rs 16.83 billion (US$990 million at the current exchange rate), whichhelped to finance about 212 of NTPC's total investment in the past five years.The latest issue included two types of bonds: one carries a 13Z p.a. rate ofinterest and a maturity of 7 years; the other pays 92 p.a., tax free, and isredeemable in 10 years. In addition, NTPC has raised funds in Japan through asyndicate of banks and financial institutions. Finally, NTPC has receivedfinancing directly or through GOI, from the OPEC Fund, the Saudi Fund, theGovernments of the Federal Republic of Germany, the United Kingdom, the Sov.atUnion, Sweden, France, Norway, Italy and most recently, untied funds fromJapan. In FY88, NTPC completed two interest rate swaps from fixed to floatinginterest rates. GOI's policy requires a return of not less than 102 on NTPC'sequity. However, this return on equity has thus far not been translated intodividend payments and the totality of NTPC's profits has been retained in theCorporation to help finance its large expansion program. This policy will bemaintained in the foreseeable future,

- 19 -

Status of Covoeiants

COVENANT SUBJECT STATUS

Prolect Agreement dated June 6. 1980

PA 2.02 NPTC *hall engage consultants to assist in tho Compiled withd-eign and engineering of the Project.

PA 2.04 NPTC shall take out insurance on goods imported Complied withfor tho Project.

PA 2.05 NTPC shall maintain appropriate records on the Complied withProject and furnish regular progroxe reports tothe Association.

PA 2.06 NTPC shall furnish a completion report within six Complied with Lmonths after the closing date of the Project.

PA 2.08 NTPC shall properly acquire all necessary land Complied withfor the Project.

PA 2.09 NTPC shall ensure compliance with appropriate Complied with /Lenvironmental standards in execution andoperation of the Project.

PA 2.10 NPTC shall enter into bulk supply contracts with Complied withSED customers allocated a share of electricitysupply from tho Project.

PA 3.01 NTPC shall tako out insurance against risk in Complied withsuch amounts as will be consistent withappropriate practice.

PA 3.04 NTPC shall inform the Association in advance, of Complied withany proposal to change NTPC's limitation toborrow funds.

PA 4.02 NTPC shall submit audited financial statements Complied withand auditors report within 7 months of FY end.

PA 4.03NTPC shell achieve an annual rate of return of Superseded bynot loss than 9-1/2 from FY88/89 onwards. covenants under

subosquent NTPCProjects requiring 7XROR in FY84/86 throughFY89/90 and 9-1/2X RORfrom FY90/91 toFY94/96 and asatisfactory levelthereafter - beingcomplied with. 2

/1 Based on the revisod guidelines dated June, 1989.

/2 Rutt of return means operrting incom (before interest after taxes) as a percentage of theaverage of the net fixed assets in operation at the beginning and at the end of the fiscalyear.

/3 In terms of project implementation this covenant was complied with, however, subsequently,such problems as explained in pares. 13 and 16 of Part I has been experienced.

- 20 -

DevuloDpmnt Credit A9r _mnt Dated June S. 1980

CA 2.02 (b) 00G shall maintain a spocialAccount in Dollar, CompiledAs amended 3/18/06) (Opened 3/86 813.0 M)

CA 2.02 (b) GOI shall enter into a subsidiary Complied withCA 3.01 (b) loan agreeent with NTPC under terms

satisfactory to the Association.

CA 3.03 GOI shall grant import permission Complied withfor goods financed under the Projectand make available foreign exchangefunds requirod therefor.

CA 3.04 GOI shall ensure adequate supply of Complied withcoal by the tim the first unit iscom_issioned.

CA 3.0S GOI to furnish to the Associationnot later than 6 months after the 85/86: Compliedend of the FY the auditor's report 66/67: Compliedin rospect of the special account 87/86 Complied(Amended 2/14/87) 08/89 Complied

CA 3.05 (b) 00! to submit the Association not Complied withlater than 6 months after end of ~Fauditor's opinion in regards to th0statements of expondituro submittedduring the year.(Amended 3/13JS7)

- 21 -

Use of Bank Resources

A. Staff Inputs

Staff inputs in carrying out the various tasks through the project

cycle from preparation in FY79 to completion in FY89 were as follows:

Task Input (Staff-weeks)

Project Preparation 3.7

Project appraisal 33.2Loan Negotiations 11.5

Loan Processing 17.4Project Supervision 47.4Project Completion Report 2.4

Project Administration 2.0Total 117.6

B. Missions

Project Cycle Month/ Number of Days Speciali- Performance Type of

Year Persons in Field zation /1 Rating /2 Problems /3

Through Appraisal

Identification /4Preparation /4Preappraisal /4Appraisal 05/79 4 25

Supervision 1 12/84 2 20 E,FA 1

Supervision 2 05/85 1 ENV

Supervision 3 03/86 1 ENV

Supervision 4 09/86 4 18 E 1

Supervision 5 09/87 4 10 E,FA 1

Supervision 6 01/88 4 20 E,FA 1

Supervision 7 09/88 4 29 E,FA,EC,ENV 1

Supervision 8 07/89 1 11 E 1

PCR 02/90 1 9 E

/1 E: Engineer, FA: Financial Analyst, EC: EconomistENV: Environmental Engineer

/2 1 = No or minor problem, 2 - Moderate problem, 3 - Major problem

/3 PR: Procurement problems and delays, I - Implementation delays,

D - Disbursement delays.

/4 Identification was made by GOI in 1974. Preparation and preappraisal were made

by NTPC in 1978.

I-I-IA

CREDIT 1027

SINQEfALI THBIAL POWER PROJECT

PROJECT COMPLETION REPORT

a-Poet Intarn 2 Ecpnricn Rate of Return

1. Sp. Coal Coanep 0.55 kg/kWh s. Concretion 11.000 owh2. Coat Cost 327.59 Re/Ton 7. Au.. Conep 8.550. Oil Coat 3,546.8 Re/KI 6. 400 kV Loass 2.5Y4. 034 312 Re/h eyr. 9. TAD Lones 18.5Y5. Eeo. Tariff 0.62 Re/kgh 10. Coneu. Sur * 0.325 Re/kWh

Economic e_i for Singrauli STPS (2000 W)

Eacendi tureTrans. Total Tariff

Poser Station Systam Coot of Revenue Total ToteaI TotealCaPi tal ......... brsiatjnStk Total Capital Total Supply To from Consumer Value of cost Project

YVer Coet coal0IT DAM PS Coet 0M TSl End-SIare End-Wore Surplue Service Savings Benefits

e1976-77 10.00 10.60 0.20 0.20 11.00 0.00 -11.00e1977-70 10.30 197.30 12.60 12.60 209.90 0.00 -209.90e1973-79 295.80 295.50 72.90 72.90 368.40 0.00 -364. 40elm-so 787.00 737.60 83.40 83.40 321.20 0.00 -621.20elO9O-Il 920.80 920.30 176.30 176-30 1,104.60 0.00 -1,104.60e1961-62 1.0".40 1,0"0 40 62.60 61.60 1,130.00 0.00 -1,130.00

e°241 1.123.00 146 47 1,315.70 220.60 1.2 221.00 1.537.50 351.00 351.00 -1,1_6.50e196804M 999.20 360 94 1,452.60 4061.30 2.7 489.00 1,941.60 1,051.30 1,051.30 r -90.50oe1964-86 1,30.40 707 158 2,400.10 713.90 1.9 715.00 34115.90 1.763.30 1,765.30 -1.350.60e19864-0 1.896.70 6"1 202 2,429.20 412.70 6.8 419.50 2,346. 70 2,020.30 2,020.30 -82840

0 elI"S-O 1,160.00 1,016 248 2,409.30 90.60 11.6 11C1.40 2,519.70 2,380.40 2,350.40 -169.301 e1987-06 40.20 1,418 852 1,613.60 -13.70 20.2 1.50 1,618.10 3,078.00 3,675.00 2.069.902 e198849 402.60 2,382 482 3.252.40 33.10 26.9 62.00 3,314.40 5,211.00 5,211.40 1,M696608 eluOg-go 400.00 1,902 812 167 2,061.15 73.00 29.6 102.60 2,983.75 4,956.70 2,1599.32 7,550.02 4,574.274 e1O9909 396.00, 1,9112 012 167 3,579.15S 27.00 29.6 56.60 3,436.75 4,956. 70 2,599.32 7,560.02 4,122.276 e1991-92 408.00 1.982 312 167 2,944.15 293.00 29.6 322.60 3,266.75 4,956.70 2,599.52 7,556. 02 4,291 27 0 e19-98 310.00 1.962 312 167 2,794.15 211.00 29.6 240.60 3,034.75 4,950.70 2,599.32 7,598.02 4,523. 277 e1l9394 1,1612 312 137 2,401.15 29.6 29.60 2,510.76 4,98M..70 2,599.52 7,556.02 5,047.27S e1994-96 1,962 812 167 2,401.15 29.0 29.60 2,510.715 4,930. 70 2,599.52 7,1580.02 5,047.279 .1995-96 1,90 312 167 2,401.15 29.6 29.60 2,510.73 4,956.70 2, 599.532 7,556.02 5.047.27

10 .19961-97 1,96 812 167 2,401.15 29.6 29.60 2,1. I.75 4,956.70 2,594.532 7,558.02 6,047.271 1 1997-916 1,902 812 167 2,401.18 29.6 29.60 2,510.75 4,956.70 2,599.52 7,556. 02 5.047.2712 *1011-91 1.9612 812 167 2,481.15 29.6 29.60 2,510.75 4,956.70 2,599.52 7s558.02 5,047 2718 .1999-2000 1.962 012 107 2,401.16 29.6 29.60 2,510.75 4,950.70 2,599.32 7,5156.02 5.047.2714 elOO-O12 1,902 312 107 2,401.15 29.6 29.60 2,510.75 4,956.70 2w,99.32 7,563.02 5,047 2715 Sim01-OR 1.902 312 167 2,481.15 29.6 29.60 2,510.75 4,956.70 2,599.32 7,556.02 5.047.2710 .2002-00 1.9012 812 167 2,401.13 29.6 29.60 2,510.75 4,950.70 2,599 .32 7,586.02 5.04'.2717 eSOOB-Ci 1.962 312 167 2,401.15 29.6 29-60 2,510.75 4,958.70 2.599.32 7, 566.02 5,047.2710 2004-CS 1,962 312 167 2,481.15 29.6 29.60 21,310.75 4,958.70 2,599.32 7,5561.02 5,047.2719 .200646 1.9gm 812 167 2,401.15 29.6 29.60 2,510.75 4,958. 70 2,599.52 7,666. 02 5,047.2720 eMO01-07 1,902 812 167 2,401.1IS 29.6 29.60 2,510.75 4,956.70 2,599.52 7,566.02 5,047.2721 e2007-CS 1,962 812 167 2,401.15 29.6 29.60 2,15110.75 4,956.70 2,599.82 7,666.02 5,047.2722 .2006-09 1,66 311 107 2,401.15 29.6 29.60 2,510.7S 4,958.70 2,599.232 7,56.02 5,047.2723*2eROO-lO 1.96 812 167 2,401.15 29.6 29.60 2,510.75 4,958.70 2,599.32 7,55.02 5,047.2724 .2010-11 i, 902 3Z12 187 2,401.16 29.6 29.60 2,510.75 4,938.70 2,599.532 7,556.02 5,047.2723 *1011-12 1,602 812 107 2,401.16 29.6 29.60 2,610.75 4,958. 70 2,599. 32 7,1556.02 5,047.27

12,062. 32.396. 7,176. 5,829..9 7,7451.66 2,959.5 752.1 3,711.6 311i63,352.0 130,674.36 59,764.30 190,456.0 0 109,295.3

IR 20. 106

Figuren up to 196;-6 are *ctuajle.Capital coat for PS and Transmiesion beyond 1966-8 are taken from financial projectione..

MD

INDIA

CREDIT 1027

SECOND SINCRAUDI TKtAL PaWE0 PROJECT

PROJECT COMPLETION REPORT

Coneolide1.d no9 . .Qf oton- (PY 1983-19091 LI

F FY.AoR83A F. 8t4A.t For.-et ATtua I F FY86A FrA8t7 Fooi-PA.T FY8t9Ac

T.at. 5.1.. of Energyi (Wh) 909.0 947 3.298 3,015 6.683 8.316 10,349 12.839 14,300 14,400 19.340 17.533 25.304 24,075

Ae-rage R5enen-- : ° 8k Supply (P/kWh) 29.06 29 C8 29 06 29.08 29 08 29 08 29.08

Fu.I S ..rchere*(~k 0.35 0 71 1.12 1.40 1.T7 2.10 2.62

Cantrel E ci- / (P1kWh) 2.00 2.00 2.00 2.00 2 00 2.00 ,200

A-eral Total Tariff (P/1Wh) - 41.92 - 39.45 - 41 34 - 41.23 - 44.79 - 49.18 - 51.25

5Gm*10a bm -I' 202 959 1.943 3,009 4.182 5.624 7.350

Fuel Z,Chorue 3 24 75 145 255 421 662

Central Ec e;- 20 66 137 213 295 397 519

Total Operating RP,.. Ws06 397 1,060 1.505 2,155 3,4J0.0 3,366 5,294 4.732 6,453 6.442 8.622 8.539 12.748

Fuel 5inE000¶¶.. 52 146 261 3449 501 576 745

Kor- r!. 5 77 162 234 318 471 692

- Re_ gena..- 7 94 213 314 484 705

- Forokka - 12 86 171 243 379

Subtotal Fu.l *1 145 230 506 527.1 1,252 002 1.952 1.304 2.360 1.774 3.165 2.522 5,205

O"- Singra.li 64 93 107 117 175 219 219

- K.orb 14 70 84 84 111 167 232

- Ra_e,4d..a 8 66 90 90 132 1 05

- FaraIk - - 19 97 97 97 167

- Tranoe.eion 3 9 10 25 29 32 32 1

- Other - - - - -

S.btotsl OA" e1 114 180 177 294 404 396 483 502 616 647 807 U35 1.175

Depreciation - Singro.li 63 99 132 132 223 305 305

- Korb - 68 105 1OS 10 189 278

- Ralt n.. - - 62 112 112 112 199

- Fer,kka 11 - - 72 119 119 228

- Tranai.sion - 27 65 111 142 153 161

- Subtotal 74 2 194 bt 364 265 523 377 701 448 878 579 1.171 912

Electricity Duty 20 18 68 09 137 112 212 111 295 87 397 93 519 179

Oth.er - 9 - 14 - 10 - 21 - 11 - 69 - 6

TOTAL OPERATDN EXPENSES 236 207 671 034 1,323 2.042 2,023 2,943 2.002 3. 22 3,696 4,712 5.047 7.559

Operating Incree eftore Intreet 70 109 379 071 832 1,396 1.341 2.350 1.930 2.931 2.746 3.910 3.492 5.189

Lose Interest Chargeable to Roenen. 14 aS 174 221 471 492 024 570 1,189 M6 1.647 1.240 1,913 1.791

LEao: Write-off Deferod Epenee 6 - S - - - - - - - - -

Lees Preo;.on for Toa - - - 11 - I 1 - -I

Add: Prior Period Income (Nt) - 2 - 10 - (28) - 50 50 53 - 362 - 90

Net Incose 40 46 200 449 361 875 517 1,e30 741 2.110 1.199 3,024 1.579 3.306

A.er.g. Net FPi.d Aaeeto (Historic) 4.406 1.804 9,188 5,997 14.715 10.957 19,997 14,016, 25.124 17.209 30.00U 23.864 36.753 35.078

Rete of Rturn en Historic Aae.te (S) 1.6 6.1 4.1 11.2 5.7 12.7 6.7 16.0 7.7 17.0 9.1 16.4 9.5 14.0

Rete of Return en Renelued Ameets (5) 10.3 11.4 14.3 13.6 12.6

Operating Ratio (6) 77.0 72.4 63.9 55.4 61.4 59.6 60.7 55.6 59.2 64.6 57.4 54.7 59.1 59.3

D Sorroeer's Fiscal year.

N1

CRIEDIT 102i

SEcOND SINtALI TIH4AL FPW5 PROJECT

F110JECT COMfLETION REPORT

Source- &rd Application of Fund-

(in i llion of Rupees)

PrS3 FYo4 PYo5 PYS" PYg1 FYoo Pr 9

Fo,ecest Actual Forecast Actual For.csst Actual Fo-.rnst Actu-l Fo,rcmat Actual For.cst Actual Forec.st Actual

Sourcon af Funds

Internal Cash CaeratiorOperating Incmeo (before intre,et) 70 11O.SLI 379 681 632 1.367L1 1,341 2.400L& 1.930 2.964L1 2,746 4.2721 3.491 s.009LI

Depreciation 74 2 1°4 64 364 265 52 377 701 446 676 579 1.171 912

Totel Cash Generation 144 118 673 749 1.196 1.6S2 1.673 2,777 2.631 3.432 3.625 4.051 4,625 6.011

Loane 2,106 2.114 5.19S 2,753 6,493 4,416 4.513 7.365 2.521 10.166 1.026 9.230 - 13.471

00C Equit, 5.676 3.,60 2.471 4.203 - 4.659 - 6.SOS - 5.094 - 6.679 - 3.62

Capital teceipt - - 2 - 26 - - - 114 - 24 - B7

TOTAL SLCES OF FkPs 7.927 6.1in 8.242 7,706 7.669 10,933 6.365 16.950 5.152 19.620 4, s6 20,964 4,663 23.251

AspI ic-tian of Funda 4

Capitel Expsnditurse (includi4n MC) 7.,46 6.179 7.962 7,.33 7.095 10.011 5,434 14,048 3.427 17.6,6 1.591 17.630 657 19,064

Int.rset Charged to Oprationa 24 65 174 221 471 492 824 570 1,160 S6 !s47 1,246 1.913 1,791

Amortization of Leon - - - - - 400 - 6S6 - 1.596 747

TOTAL OWlI SVICE 24 S 174 221 471 492 624 570 1.569 S" 2.406 1.248 SS.11 2.536

Def.r,ed Reven.ue Ependitor-Short-Term D it - - - - - - - - - - 500 - 266

Working Capitel Incrsese/(Omcrssse) 56 (59) 106 343 123 430 127 2.332 136 047 157 2.106 207 1.649

Proviion for Tas - - - 11 - - - I - 1 - - - -

TOTAL APPLICATI6O 7.927 6,166 8,242 7.706 7.669 10.633 6.365 16.950 5,152 10,620 4.63 20.984 4. a" 23.251

Debt Ser,ice Covereag 6.0 1.7 3.3 3.4 2.5 3.3 2.3 4.9 1.7 4.0 1.5 3.9 1.3 2.4

LI Includes prior period income.

W

INDIA

SmO SIXWALI l RttI rAvn P,

PRJ.T COMPLErImN 1EPT

aIIzInce Shoot

(in million of Rupees)

FM FY4 FlOUI FY rYW FMr

Pereat Actual e rcAst Actual Foreasat ActUal Forecast Actual Forecast Actual F_rees Acual Paremet Actsl

Ore.. Fled As ets 6.46 $.on 12,267 9.197 1.044 1u.363 2=.749 16,047 29.880 .6111 . r117 0. 44".9 44.764

Lem 0.pre.atlen 751 6 269 170 3 476 1.165 05 1.6 1.416 u .7*44 3.06 8.918 &.

Nat Floed Ames" In roratlem 6.3 2.966 12.018 9.027 17.411 12.887 226.54 15.144 27.64 l.m =.d4 36.49 41.068 41.716

War I a Prerm 111414 1,r76 17.563 13.767 1a.90 II.6$ is.6r 31.060 16.27, 44".m1 3. 11 3,1U. I.066 87.003

TOTAL FINS *27N 231.612 1.M 29.8 22.794 38,611 82.f48 41.213 4.231 42.986 68,576 4".M3 O.6 ".in 9.770

Ca& (including back bulmac) a 18 6 176 9 64 2 448 1s 134 is 8.97S 16 2

short Term OD.peelt - 77 - 106 - 89 - 687 - - 787 - 4.,644

Pew 1e blea a 219 U 642 1SO 1.62 21 2.24 94 2., W 4.m 7132 S.1

Iaaentee 64 155 126 424 16o 704 286 94 25 1.8112 M 1.743 480 3.68

oer Debtmre 1 376 2 26 2 848 2 1.96 S 790 a us 4 23.71

Tota Current meet. 94 740 219 1'm 871 S. 11 M2 6.M9 707 9, 909 18.4n 1.186 1U8,4

Def.rrdEpensese a #6 - 22 - 19 - 19 - 16 - 17 - 16

TrTAL A6sI 21.911 16.491 29.7 24.9 36.662 3.713 41.745 82.836 44".6 72.71 46.061 4.113 4.11 114.m

share capitel _emid and Do..llb. e 19.46 11.,60 1.99 16.009 21,939 20.666 21.959 27.676 21.981 =.M 3.99 48.464 n1.9 441

metal"" , brninq 47 60 247 a0 60 1.402 1.126 8.231 1.6 8.46 8.M .811 4.644 11.90

T37AL MMr 1O.5 11.65i 22.206 16.50 22.547 22.269 23.064 30.906 211161, 6.047 25.04 46.974 86.6 s6.062

Lee"a 3m 8.195 7.864 S. 46 14.059 10.664 18.571 17.729 30.6 37.54 20.6 57.184 19.265 49.66

CurrntbLl m llltW a 1.442 26 2.142 66 8,01 so *.nl 19 6.776 1s .014 S"44 0.780

TOTAL OT 2,376 4.m 7.M2 ,o090 14,115 13.44 1.66l 21.60 20.621 a.672 n .n 4.16 19.1c6 U.m

TOTAL MM NO LZAIIT1 31.911 16,491 ".7M9 24.596 34.662 35,718 41.745 526 44"646 72.716 46.061 94.112 46.112 114.0

Debt as dof De SwifN 11 21 25 26 86 82 45 W 46 42 48 48 42 47

X4