world bank documentdocuments.worldbank.org/curated/en/... · project performance audit report india...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY FLEC OP7

Report No. 1658

PROJECT PERFORMANCE AUDIT REPORT

INDIA ELEVENTH AND TWELFTH RAILWAY PROJECT (CREDITS 280- AND 448-IN)

June 30, 1977

Operations Evaluation Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OFFICIAL USE ONLY

PROJECT PERFORMANCE AUDIT REPORT

INDIA ELEVENTH AND TWELFTH RAILWAY PROJECT (CREDITS 280- AND 448-IN)

TABLE OF CONTENTS

Page No.

PREFACE

PROJECT PERFORMANCE AUDIT BASIC DATA SHEETS

HIGHLIGHTS

PROJECT PERFORMANCE AUDIT MEMORANDUM

I. Project Summary 1

II. Issues 7

III. Conclusions 20

TABLES

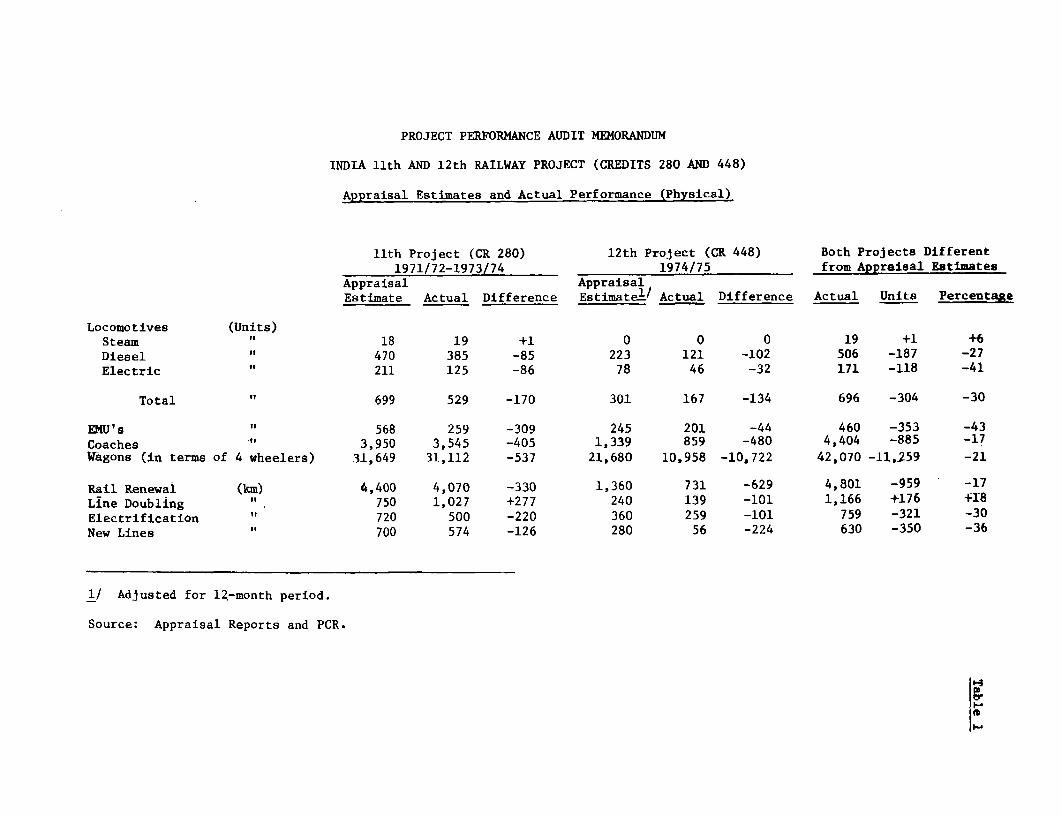

1. Appraisal Estimates and Actual Performance (Physical)

2. Appraisal Estimates and Actual Performance (Financial)3a Operating Performance 1966/67-1975/76 - Broad Gauge3b Operating Performance 1966/67-1975/76 - Meter Gauge4. Freight Traffic: Forecasts and Actual

ATTACHMENT A: PROJECT COMPLETION REPORT (ELEVENTH RAILWAY CREDIT 280-IN)

1. Summary of Bank Group Lending for Transport A.1

2. Summary of Credit 280-IN and Eleventh Railway Project A.13. Major Findings A.34. Recommendations or Action Taken A.45. Bank Group Lending to Transport Sector A.56. The Economy and the Transport Sector A.7

7. IR's Investment Program A.108. Project Execution and Disbursements A.11

9. Operating Results and Physical Performance A.12

10. Financial Aspects A.1411. Borrower's Observance of Commitments and Undertakings A.1712. Economic Evaluation A.18

ANNEX

Summary of Principal Covenants Included in Credit Agreements80-IN, 162-IN and 280-IN (9th, 10th and 11th Railway Projects)

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- 11 -

Page No.

TABLES

1. Statement of Bank Group Loans and Credits for Indian Railways2. Bank Group Lending for Transport Projects Other than

Indian Railways3. IR Freight Traffic 1969/70-1975/76 (Appraisal Estimates

and Actuals)4. IR Passenger Traffic 1969/70-1975/76 (Appraisal Estimates

and Actuals)5. Capital Expenditures during Fourth Plan and in Project

Period (1971/72-1973/74)6. Comparison Between Targets and Achievements of Principal

Project Items (1971/72-1973/74)7. Comparative Unit Costs of Locomotives and Rolling Stock

at the Beginning and End of Project Period 1971/72-1973/748. Estimated and Actual Schedules of Disbursements by Quarter9. Selected Operating Statistics 1965/66-1973/7410. Revenue and Expenditure Accounts for 1957/58; 1960/61;

1965/66 and 1969/70-1973/7411. Statement of IR Expenditure on Capital Account12. Summarized Revenue and Expenditure Accounts During the Years

Covered by the Project

ATTACHMENT B: PROJECT COMPLETION REPORT (TWELFTH RAILWAY CREDIT 448-IN)

I. Sector Background B.1II. The Role of the IBRD/IDA B.1

III. Project Preparation and Appraisal B.2IV. Traffic and Operations B.3V. Project Implementation and Cost B.4

VI. Financial Results B.6VII. Institutional Development B.6

VIII. Economic Evaluation B.7IX. Major Findings and Recommendations B.7

ANNEX

Summary of Covenants and Undertakings and Action TakenThereon

TABLES

1. Comparison Between Appraisal Estimates and Achievements ofFreight Traffic for 1974/75

2. Comparison Between Appraisal Estimates and Achievements ofPassenger Traffic for 1974/75

3. Selected Operating Statistics 1966/67-1974/754. Capital Expenditures for 1974/75

- iii -

TABLE OF CONTENTS (CONT'D)

5. Comparison Between Appraisal Estimates and Achievements ofPrincipal Project Items for 1974/75

6. Wholesale Price Index Numbers for Important Commodities

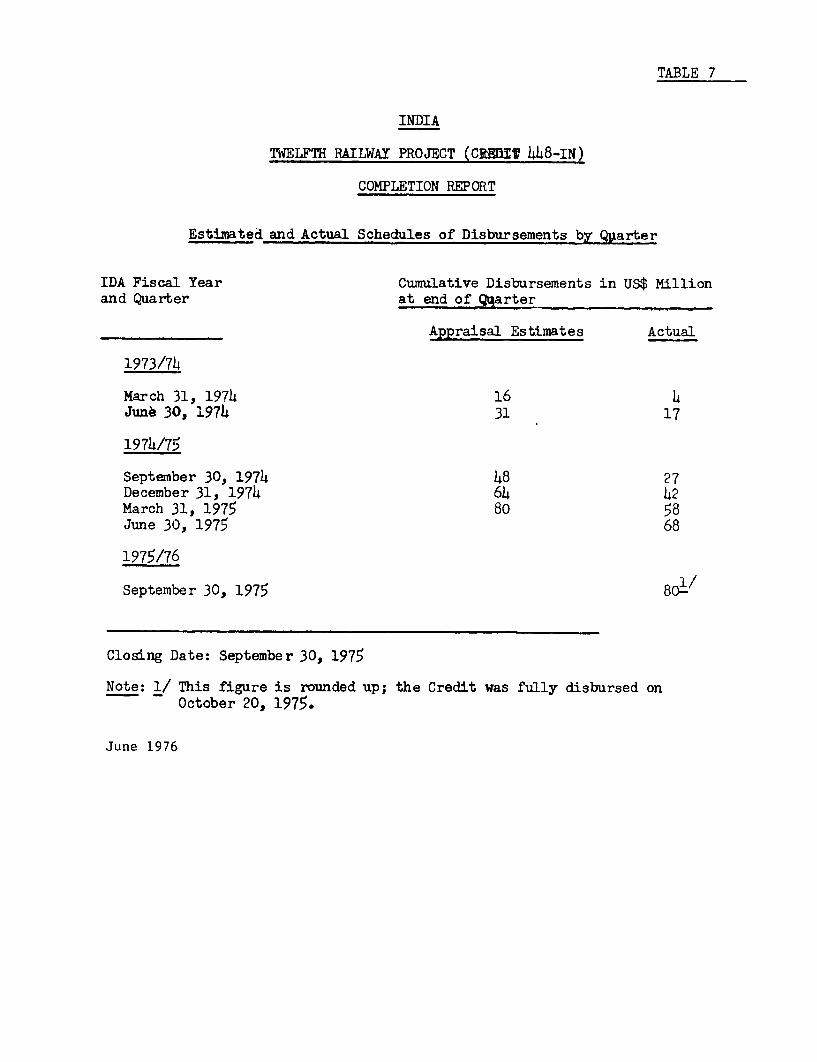

Used by IR7. Estimated and Actual Schedules of Disbursements by Quarter

8. Summarized Revenue and Expenditure Accounts 1973/74-1975/76

CHART

Indian Railways Organization Chart

MAP

India Railways

PROJECT PERFORMANCE AUDIT REPORT

INDIA ELEVENTH AND TWELFTH RAILWAY PROJECT (CREDITS 280 AND 448-IN)

Preface

This report presents the performance audit of the Eleventh andTwelfth Railway Projects for which Credits 280 and 448-IN were fully disbursedin October 1974 and October 1975, respectively. Since the credits formed partof a long-term association, the present report, which is the first audit onBank Group lending to Indian Railways, deals with some matters which werealready of concern in earlier projects. Some references are made to the year1975/76, because it represents a more normal situation than 1974/75, which wasthe last year of the twelfth project.

This performance audit is based mainly on the attached ProjectCompletion Reports (PCRs), prepared by the South Asia Regional Office, areview of IDA files, and discussions with IDA staff. In October 1976, a 2-1/2week visit was made to India on behalf of OED in connection with this per-formance audit. Extensive discussions were then held with officials of theIndian Railways and others in the Government of India. The valuable assist-ance of these officials is gratefully acknowledged.

The Project Performance Audit Memorandum (PPAM) which followshighlights the principal results of the two projects and then draws attentionto some main issues arising from past Bank Group lending to Indian Railwaysin general. More details concerning the projects and their implementation arecontained in the attached PCRs.

PROJECT PERFORMANCE BASIC DATA SHEET

INDIA ELEVENTH RAILWAY PROJECT (CREDIT 280-IN)

Key Project Data

Item Original Plan Actual

Total Project Cost (US$ millions) 1,084 1,200

Overrun () - 11

Credit Amount (US$ million) 75 75

Disbursed (US$ million) - 75Cancelled (US$ million) -Exchange adjustment (US$ million) - 5Outstanding to IDA (US$ million) 12/31/76 - 80First Year Economic Return (%) 10-20 10-20

Other Project Data

Item Original Plan Actual

Board Approval 1/11/72

Credit Agreement - 1/24/72Effectiveness 2/25/72 3/29/72Closing Date 9/30/74 9/30/74Borrower Government of India (GOI)Executing Agency India Railways (IR)

Mission Data

Month, No. of No. of Date ofYear Weeks Persons Manweeks Report

Identification 08/70 1 3 3 09/25/70Appraisal 03/71 3 4 12 10/05/71

Total 4 15

Supervision I 03&04/72 2 2 4 05/25/72Supervision II 03/73 2 3 6 05/15/73Supervision III 12/74 2 3 6 07/31/75

Total 6 16

PROJECT PERFORMANCE AUDIT BASIC DATA SHEET

INDIA TWELFTH RAILWAY PROJECT (CREDIT 448-IN)

Key Project Data

Item Original Plan Actual

Total Project Cost (US$ million) 654 543Underrun () - 17Credit Amount (US$ million) 80 80Disbursed (US$ million) - 80Cancelled (US$ million) - noneExchange adjustment (US$ million) - none

Outstanding to IDA (US$ million) 12/31/76 - 80Economic return (%) 13 13

Other Project Data

Item Original Plan Actual

First mention in files 02/05/73Board approval 12/15/73 12/18/73Credit agreement 12/21/73Effectiveness 03/21/74 02/25/74Closing date 09/30/75 09/30/75Borrower Government of India (GOI)Executing Agency Indian Railways (IR)

Mission Data

Month, No. of No. of Date ofItem Year Weeks Persons Manweeks Report

Identi fication)Preparation ) (Carried out together with the Preappraisal below)

Preappraisal 03/73 2 3 6 05/15/73Appraisal 06/73 3 3 9 12/ 6/73

Total 5 15

Supervision I 02/74 3 2 6 04/24/74Supervision II 06/74 1 1 1 07/10/74Supervision III 12/74 1 3 3 01/15/75Supervision IV 03/75 1 4 4 05/28/75Supervision V 12/75 1 2 2 12/29/75

Total 7 16

Follow-on Project

Thirteenth Railway Project (Credit 582), approved August 1975, for US$110 million.

COUNTRY EXCHANGE RATES

Name of Currency Indian Rupee (Rs)Year: 1971

Exchange Rate: US$ = Rs 7.50

1974 US$ = Rs 7.45

1975 US$ = Rs 8.11US$ = Rs 7.85

PROJECT PERFORMANCE AUDIT REPORT

INDIA ELEVENTH AND TWELFTH RAILWAY PROJECT (CREDITS 280- AND 448-IN)

Highlights

Credits 280-IN and 448-IN financed the 11th and 12th projects in

a continuous program to assist Indian Railways (IR) to modernize and toexpand. The above two credits covered most of the foreign exchange require-

ments of IR's investments from April 1971 to March 1975. The original

investment program was scaled down because of higher costs and lower thanexpected traffic. The projects were implemented on time. The reestimated

rates of return are similar to the appraisal forecast. Because of unusual

economic and political circumstances, the financial situation of IR deterio-

rated during the projects' period, but it has now improved.

Indian Railways constitute a large system which performs a vital

transport function in the country's economy. The system is mostly modern

and reasonably efficient, while efforts to make further improvements continue.

Freight traffic has not grown as rapidly as expected and there is now some

excess capacity; however, that may not be undesirable inasmuch as it would

help avoid transport constraints when economic activity accelerates. Improved

methods to calculate freight capacity would nevertheless help to achieve more

accurate estimates of investment requirements.

In spite of many years of dialogue between the Government and the

Bank, transport planning and coordination remains rather weak. Some progress

is now being made on the national level and IR's corporate planning exercise

has been successful.

The following points may be of particular interest:

- the importance of IR in Indian economy and the Bank Group's

involvement in India's transport sector (paras. 1, 3, 5 and

PCR 11th Project, Tables 1 & 2);

- reasons for lower than forecasted traffic (paras. 17, 18,PCR 11th Project, paras. 6.02, 6.03; PCR 12th Project,para. 4.02);

- risk of overinvestment through insufficient knowledge about

existing freight capacity (paras. 22 and 23);

- difficulties in estimating economic returns for specific invest-

ments in a vast railway system (paras. 26, 27; PCR 11th Project,paras. 12.05, 12.06; PCR 12th Project, para. 8.01); and

- slow progress in transport planning and recent improvements(paras. 24, 37, 38, 42, 45; PCR 11th Project, paras. 6.06-6.09).

PROJECT PERFORMANCE AUDIT MEMORANDUM

INDIA ELEVENTH AND TWELFTH RAILWAY PROJECT (CREDITS 280 AND 448-IN)

I. PROJECT SUMMARY

1. Indian Railways (IR) is the third largest railway system underone management in the world, being exceeded in size only by the railways inthe USSR and China. The system consists of 30,275 route km of broad gauge,25,550 route km of meter gauge and 4,476 route km of narrow gauge track;about 20% of the above routes are double tracked. Seven percent of theroute km is electrified. 1/ In April 1974 IR had about 11,000 locomotives,1,900 electrical multiple units, 34,000 passenger coaches and 390,000 freightwagons. In 1975/76 2/ IR moved 221 million tons and 1,252 million passengersor a total of 148,000 million ton km and 112,123 million passenger km. About80% of IR freight traffic consists of bulk transport. At the start of theproject period, in 1971, IR transported about two-thirds of all freightand about half of all passenger traffic, but there has been a marked shifttoward road transport in recent years. IR has a total staff strength of some1.7 million.

2. Formal jurisdiction over IR rests in the Minister of Railwayswho is a member of the Central Cabinet. Overall management is in the hands ofthe Railway Board (Ministry of Railways). There are nine railway zones, eachwith a General Manager who reports directly to the Railway Board. IR alsooperates manufacturing units consisting mainly of two locomotive and one coachfactory. IR has its own research and design organization (RDSO). Railwayoperating and capital budgets are discussed in detail by Parliament, whichalso frequently has a direct impact on the commercial results of IR by rulingon tariff increases, and on requiring the operation of services on groundsother than purely economic.

3. The two projects, which are now being audited, form part of along-term lending program to IR, started in 1949 and in which the thirteenthproject was approved in 1975. A fourteenth project is under preparationand will probably be appraised in May 1977. The lending so far has involveda total of US$896.5 million equivalent, of which US$379.0 million has beenextended in loans and US$517.5 million in credits, and was initiated to assistIR with its rehabilitation program after World War II. Industrial importcredits have also covered the cost of some parts and components for IR's

1/ All data for 1974/75.

2/ Provisional figures. The freight includes some 15 million tons ofexceptional traffic, required to reinstate normal stockpiles of indus-trial fuel and raw materials, which had been depleted due to transportinterruptions in previous years.

- 2 -

manufacturing activities. The last three credits have covered about 10% ofIR's total investment for the period. Until 1951, when the first steamlocomotives were produced in India, virtually all manufactured components hadto be imported. About 20 years ago foreign exchange expenditures were stillover 50% of investment costs, while this has now been reduced to only about14%.

4. The greatest problem which has faced IR until the early 1970s hasbeen to provide capacity to accommodate the increasing demand, caused byindustrialization and the resulting need for transport of fuel and raw mate-rials. Over the past fifteen years freight traffic has grown from 156 millionto 221 million tons. The Bank has viewed lending to GOI for IR favorably,because there was an established need, it was a well organized entity to lendto, with a role critical to India's overall economic development, and a smoothtransfer of resources was virtually ensured. Issues of IR's own planning andtransport planning and coordination for the entire country were discussedfrequently between Bank Group staff and officials of the GOI and IR. Theseissues have only become prominent, however, during the last five projectswhen they were covered in the Credit Agreements or side letters.

5. There have been seven lending operations amounting to US$254.6 mil-lion equivalent for transport projects other than railways. Except for ashipping loan in 1972, all of these took place between 1957 and 1962. Inaddition the Bank Group has provided US$342.9 million equivalent of indirectsupport to the road transport industry through ten industrial import credits.A small roads component has also been included in a number of agriculturalprojects.

6. The 11th and 12th Railway projects covered the period April 1971to March 1975, and included financing for part of the foreign exchange com-ponent of 18 steam, 693 diesel, and 289 electric locomotives; 813 ElectricalMultiple Units (EMUs); 5,289 coaches; 53,329 freight wagons (in terms of 4wheel equivalent); 1/ 5,760 km of track renewal; 990 km of line doubling;1,080 km of line electrification; and 980 km of new lines (Table 1). The11th project involved an IDA credit of US$75.0 million equivalent, whichcontributed to an investment program of US$1,084 million equivalent. The12th project consisted of an IDA Credit for US$80.0 million equivalent cover-ing part of the investment during the first 15 months (January 1974-March1975) of IR's fifth five-year plan; the total investment projected for thatperiod of 15 months amounted to US$654 million equivalent.

7. The final cost of the 11th project (IR's investment program for thethree years 1971/72-1973/74) increased by about 10%, which covered part ofadditional costs due to inflation, but funds were insufficient and cutsin the program had to be made. The 12th project, consisting mainly of IR's

1/ The official documents for the 11th project (Credit 280) mention twofigures for freight wagons: 31,649 and 21,000 (both in terms of fourwheelers), but we have been assured by the Projects Department that thehigher figure is the correct one.

- 3 -

investments during 1974/75, was reduced because of the lower than expecteatraffic growth and the eventual expenditure was 14% less than the originalestimate. About US$22 million equivalent of the proceeds of the credit wereused for the 13th project (PCR 12th project, para. 5.05 and Table 4). Otherreasons for the reduction in physical investment were cost increases due toproduction problems resulting from strikes, supply difficulties, and delaysresulting from the indigenization process which consists of the change fromimports to local production of parts and components. The funds provided underthe two credits were fully disbursed. In terms of physical output, however,there has been a considerable shortfall (Table 1). Some reallocations betweencredit categories have also taken place (Table 2).

8. Even though IR has experienced some financial difficulties duringthe past few years, its financial status still ranks high among the world'srailways. According to the agreements for the 11th and 12th projects IRis to generate sufficient revenues to cover all operating expenses (includingadequate appropriations for the Depreciation Reserve Fund and Pension Fund)and the dividend on the Government's investment in IR. The dividend rate,set by Parliament, is 5.5% on capital invested before March 31, 1964, and6% on capital invested after that date. Owing to India's economic recession,labor unrest and substantial wage increases for Railway staff, IR had dif-ficulties in meeting this target. IR requested that the earnings covenant bewaived for 1973/74, to which IDA agreed. During negotiations for the 12thproject in 1973, it was realized that time would be required to adjust ratesand fares, and it was therefore agreed that revenues for 1974/75 and 1975/76should be sufficient to cover 70% and 85%,respectivelyof the dividend forthose years (PCR 11th project, para. 10.05 and Annex 2). For 1974/75 IR didnot fully comply with the agreement, but for 1975/76 and 1976/77 the targetshave been met. At the time of presentation of the 12th project, the Boardwas concerned about the proposed waiver of earlier agreements on dividendpayment. It requested management for a report on IR's financial situation3 years later, by which time full recovery was anticipated. A paper on thiswas presented on March 9, 1977 (IDA/SecM77-55).

9. In connection with these projects it was also agreed that:

(a) the borrower would prepare and maintain a long-term "corporate"plan;

(b) the methodology for appraisal of investment projectswould be progressively improved and discounted cashflow criteria for such appraisals would be introduced;

(c) revenues or losses from mass transit systems, if included inthe railways' budget, would be separately identified; and

(d) the content of a timetable and plan of action for the estab-lishment of a framework for future Bank Group participationin the transport sector would be worked out by 1974. Thiswould be based on a full review of the transport sector whichthe Government was intending to do and which was discussedwith the Association during negotiations for the 11th project.

most of these agreements have been carried out. The preparation of a cor-

porate plan has taken more time, however, than was originally envisaged,

but has resulted in a useful framework for further detailed planning.

There was no agreement on the nature and timing of the improvements in the

methodology for appraisal of investment projects, and the covenant itselfis too vague to be meaningful. However, cash flow criteria and shadow

pricing of labor and foreign exchange are now being introduced in project

appraisals. The framework for future Bank Group participation in India'stransport sector has not yet been formulated.

10. The 12 loans and credits have all contributed to progressive

improvements of IR. Most of the achievements are on the technical side:

operations, at least on the main lines, are mostly modern and efficient;

the present carrying capacity seems to be ample for freight traffic, and

also satisfactory for passenger services with the exception of some suburban

services, where overcrowding persists. IR's rates and fares are low and

average receipts are USiO.7 per ton km and USJ0.2 per passenger km. A

major achievement of the 11th project is the introduction of the corporate

planning process, which has focussed on a 15-year planning period, in addition

to the customary 5-year period, and has resulted in a long range perspectiveplan for the period 1974-1989. Some specific planning issues remain to be

solved and are discussed in the next chapter.

11. In the appraisal reports the first year economic return for the 11th

project was estimated to be between 10% and 20%. The economic rate of returnof the 12th project was estimated at 13%. The re-estimation of these returns

in the PCR indicates that the appraisal forecasts have been achieved (PCR 11th

project, para. 12.05 and PCR 12th project, para. 8.01). Further discussion onthis point follows in Chapter II.

II. ISSUES

12. The implementation of the 11th and 12th Railway projects has been

complicated by unusual problems, resulting from the Indo-Pakistani war, the

oil crisis, strikes and other civil unrest. These problems have led to a

work stoppage at the railway for about 20 days in 1974, and also to electric

power cuts and irregular supply of parts and other necessities.

13. In view of the size and complexity of the Indian railways this audit

does not attempt any assessment of the system as a whole. In the following

paragraphs five special problems are discussed, which are directly related to

the implementation of the eleventh and twelfth projects. The audit mission

largely agrees with the PCRs, but feels that some issues deserve more emphasis.

-5-

(a) Project Implementation

14. Para. 7 above and Tables 1 and 2 summarize the physical and finan-

cial performance under the two projects. During the project periods con-

siderable changes were made in the contents of each project. The changes wereprimarily the result of lower than expected traffic, but were also influenced

by other factors such as parts availability and cost increases. A number ofreallocations took place between the different categories specified in sche-dule one of the Credit Agreements (Table 2).

15. In these two projects it is not possible to relate the particular

items financed by IDA to specific aspects of IR's operations. The creditshave really been to assist in the financing of a continuing program of railway

investment, with a specific period of time being regarded as a "project".

The appraisal reports and Credit Agreements do not carry any details as to thesections of line to be doubled and locations of new lines to be built under

the projects. Parts financed under the projects are mostly used for repairsin IR workshops and the building of new diesel and electric locomotives andpassenger coaches in IR's own factories. According to the Appraisal Reportthese production units are generally efficiently operated and produce at areasonable cost. However, the Bank intends to take a closer look at their

operations in connection with the next railway project.

(b) IR's Planning and Operations

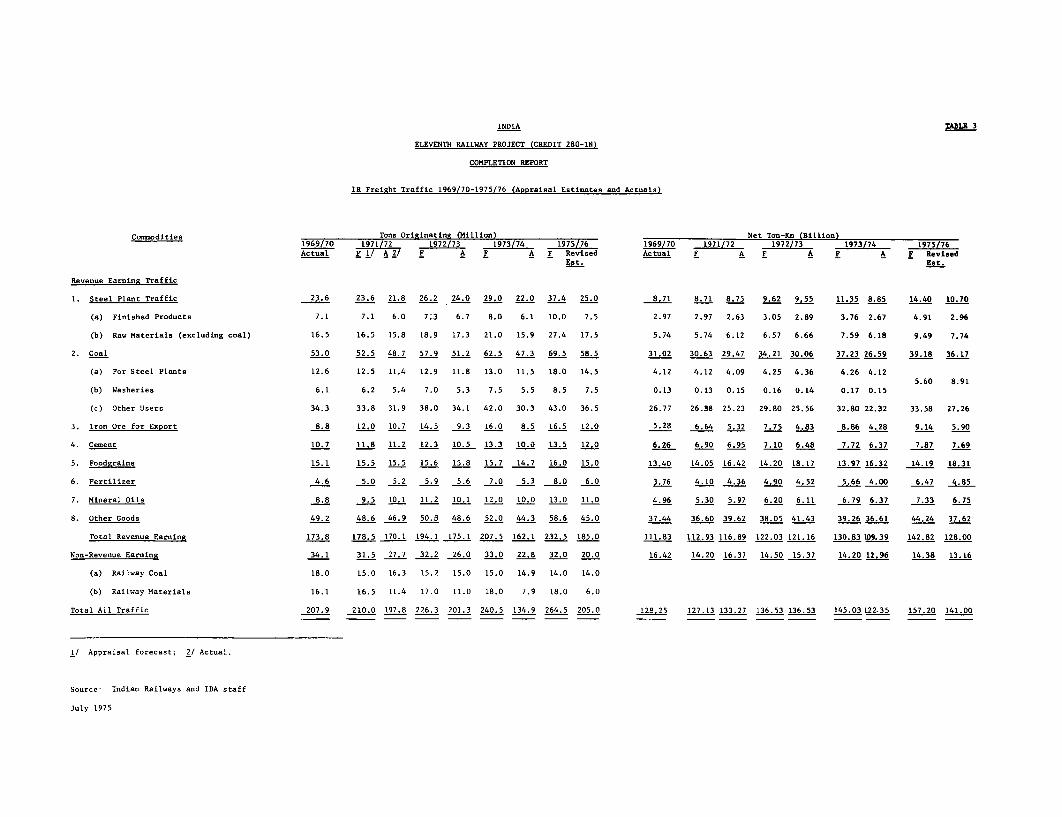

16. As pointed out in the PCR for the 11th project (para. 6.02), at theend of the project period (1973/74), only 185 million tons were carried, com-pared with 240.5 million tons forecast in the appraisal report 1/ and 260 2/million tons forecast for the same year in the original fourth five-year plan.-

However, between 1969/71 and 1973/74 the distance over which the average tonwas carried increased by 7.9% for broad gauge (BG) and by 13% for meter gauge(MG). Passenger traffic forecasts were closer to what actually happened,

which was in part due to a higher than expected growth of suburban traffic.

17. Shortfalls in freight traffic can be partially explained by theevents described in para. 12. Also, in view of the rapidly increasing shareof freight traffic transported by road (28% in 1971 and 40% in 1975, PCR 11thproject, para. 6.04), it seems reasonable to conclude,even though adequate

statistics are lacking, that IR's relative position as goods carrier isdeclining. IR is strong in the field of bulk transport, but general goodstransport has stagnated for many years, while some other short and medium

distance traffic apparently also prefers road transport. It is not clearwhether this development is economically desirable, but some of the reasonsfor diversion are discussed in para. 31.

18. When preparing its investment programs, IR is assigned a task by the

Planning Commission, in terms of tonnage to be carried, which is based on thegeneral plan for the economy as a whole. These plans are usually rather

1/ For forecasts under the 11th, 12th and 13th railway projects and actualtraffic between 1960 and 1976, see Table 4.

2/ The investment plan was based on a traffic forecast of 240.5 million

tons.

- 6 -

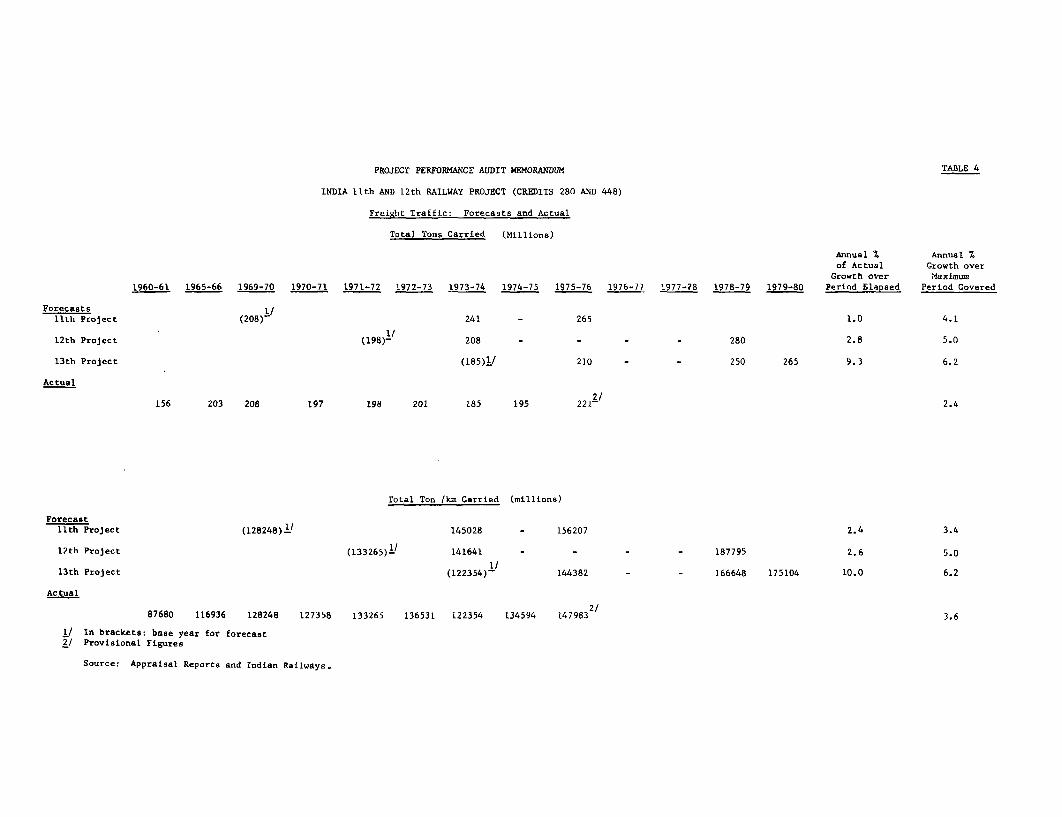

optimistic, and are frequently reduced to more realistic levels during subse-quent consultations between IR and the Planning Commission. Nevertheless,for the two projects traffic forecasts have turned out to be consistentlyhigh. The appraisal forecasts for annual growth in the 11th and 12th projects(made in 1972 and 1973) were 4.1% and 5.1%, respectively, for tonnage carriedand 3.3% and 5.0% for ton km (Table 4). This compares with an actual annualtraffic growth over the last 15 years of 2.4% for tonnage and 3.6% for ton km.During the forecast period of the 11th project (1969/70-1975/76) actual growthwas 1.0% for tonnage and 2.4% for ton km carried. The first 4 years of the12th project, for which data are now available, show a growth of 2.8% fortonnage and 2.6% for ton km carried.

19. In 1966, under the 9th project, an economic unit was set up in theRailway Board. In 1972, under the 11th project, the Bank has speciallystressed the importance of project analysis. Due to the limited economicstaff available much of the planning still appears to be done on the basis oftechnical and financial criteria without much recourse to economic analysis,but the scope of involvement of the Economic Unit is gradually being expanded.

20. IR's planning has been predominantly based on the five yearnational plans. It was felt that a perspective plan which would evaluatethe effects of investments over the longer term was lacking. Under the11th project agreement was reached that a corporate plan for the period1974-1989 would be prepared. A first draft was completed on time and isbeing followed by further refinements.

21. Investments under the two projects were for replacement and toincrease IR's carrying capacity for both freight and passengers. Of thesefreight capacity has clearly greater economic significance since shortagesin freight capacity could lead to serious economic losses through reducedindustrial production and possible loss of export orders, while passengerservices could be curtailed to affect mostly passengers whose trips wouldhave little or no economic value. The crucial factor here is freight wagoncapacity and to a lesser extent motive power, because the latter can, ifnecessary and at the margin, be diverted from passenger services.

22. Most of India's heavy industries have considerable spare capacity.An increase in industrial activity could result in a sudden increasein freight transport. Such a change would not allow enough time to increasethe fleet of freight wagons. During a period of reduced economic activity,therefore, a certain excess capacity of the Railways would be desirable.According to IR's Planning Department the system's freight capacity in April1974 was more than sufficient at 221 million tons, which was calculated,however, by using better turnaround times and a higher average lead thanwere achieved at the time. Apparently no estimates could be provided on the1975/76 freight capacity. Further investments in freight wagons were madebetween April 1974 and 1975/76, when IR carried 223 million tons. Based oninformation for that year, it appeared that freight wagon capacity was ampleand orders could normally be filled immediately. This is also evident from

- 7 -

statistics which indicate that the number of outstanding requests for wagons

was very small. The turnaround time of 13.2 days in 1975/76 for wagons is

still above the target of 12.1 days for the fifth plan, which also points

at the fact that ample stock is available. Reductions in turnaround time are

expected to continue as a result of measures to rationalize yard operations,

the introduction of block trains and the fact that general merchandise, which

requires a much higher wagon capacity to move a ton km than is required for

instance for bulk coal movement to general users (about 2.7:1), is decreas-

ing as a proportion of total traffic. Based on the mission findings, it

appears that IR's knowledge of the carrying capacity of its freight wagon

fleet is not sufficiently detailed for the purpose of sound investment

planning. Improvements in this field would probably require a complete

breakdown for all aspects of freight car use for each major commodity group

(e.g., working in coal yards, loading/unloading, shunting, etc.). For each

activity at least three values should be used:

(a) operating time now required;

(b) shortest time in which activity can take place without

investments or major organizational changes (e.g., in one

colliery loaded wagons were always waiting for 12 hours

before being collected); and

(c) longer term improvements.

The use of a simple computer program would provide immediate information on

the spare freight capacity (difference between (a) and (b)), and the ultimate

capacity (c). It would also enable IR to better compare spare capacity against

changes in the mix of traffic and/or transport demand increases in one or

several sectors of the economy. 1/

23. IR's normal practice for doubling of a particular line is to start

with the most congested sections and delay other sections as long as possible.

IR has also made substantial progress with the introduction of longer andheavier trains in order to postpone the need for extra line capacity.Only a detailed review of terrain conditions, traffic composition, etc.,could lead to firm ex-post judgments on the timeliness of completed line

doubling and gauge conversion. The fact, however, that some lines are now

fully double tracked for about 20 train movements per day in each direction,

while work was started when there were about 10 - 12 train movements in each

direction, may point to an overly cautious, and costly, attitude of IR in

1/ IR feels that their methodology of assessment of freight car require-

ment is fairly comprehensive and that it appears unlikely that any

substantial improvement would result by following the system proposedby the Audit Mission, which they feel prima facie does not appearfeasible of being implemented easily.

-8-

avoiding line capacity constraints. 1_ This attitude probably reflects themany years that IR officials had to work under conditions of serious capacityshortages. As part of the Corporate Plan, IR is now broadening the considera-tion of alternatives to increase line capacity.

24. Little information is available on the new lines which were builtunder the projects (630 km). Some are spurlines serving new industrialand mining activities, while others are development lines, providing moderntransport to areas so far not served. IR suggests that the first categorywill carry large volumes of traffic, but agrees that the development linesdo not always meet economic criteria. On the basis of the audit mission'sfindings, it appears that, the Association has probably made, through the

project, a small contribution to the increase of the uneconomic lines, insteadof being instrumental in their decrease.

25. IR's operations are as a whole modern and efficient. IR is intro-ducing measures to increase the efficiency of equipment utilization. Theseinclude the introduction of block trains for bulk transport, the centraliza-tion of marshalling operations, and a reduction in wagon detentions duringloading and unloading (see PCR 11th project, para. 9.06). Statistics onequipment availability show a slight decrease over the past 10 years (seeTable 3). For locomotives part of this is due to technical problems (PCR 11thproject, paras. 9.04 and 9.05), but even before the deterioration availabilitywas below that of most developed countries. Availability of BG dieseland electric locomotives in India in recent years has been about 84% and 80%respectively, while in several European countries the availability was over90%. 2/ The main reason for this appears to be delays in importing and dis-tributing spare parts and problems with local parts production. The avail-ability of freight wagons has been high throughout. If IR could improveequipment availability significantly, it could substantially reduce futureinvestment requirements.

(c) Economic Evaluation

26. The appraisal reports for the eleventh and twelfth railway projectshave based the calculation of economic benefits on railway operations costreductions and the avoidance of extra cost to the economy for carrying goods

by a more expensive transport mode due to eventual rail capacity shortageswithout the investments. At the time of appraisal of the 11th project, thefirst year economic return was estimated at 10-20%, while a rate of returnwas only calculated for a number of subprojects. The PCR has not reevaluatedthe subprojects and the result would not be of overall significance, becausethey covered only 5% of the total investment. The PCR, however, concludes

that based on findings of the appraisal of the 13th project, the 11th project

1/ IR is of the opinion that their methodology for deciding on double

tracking is still satisfactory.

2/ Some of these countries achieve availabilities over 95%, but sometimes

the methodologies used for the calculations differ.

- 9 -

has met its objectives and has, therefore, had a first year return of at

least the appraisal range of 10-20%. The economic return on the 12th proj-ect was 13%. A reestimate has been made concluding that the expected 13%will be achieved (PCR 12th project, para. 8.01).

27. In view of the complexity of IR's system and the limited timeavailable for audit, the above estimate is considered acceptable. A moreaccurate estimate of the economic return, would require a detailed study todetermine what cost reductions have resulted from the investments. Further-more, economic benefits from avoiding traffic diversion to a more expensivemode cannot be calculated with any degree of accuracy. The first difficulty'is the estimation of the traffic volume which would have been diverted to othermodes without the investment. This requires an estimation of the sparecapacity of the railways without the investments which is not available(para. 22). It can be argued that if there is spare capacity on the railways,nothing would have been diverted and there would be no immediate benefits.However, rail transport investment, as much as planned requirements, haveto be seen in a longer perspective and without the present investments asudden upturn in the economy might have resulted in serious transport con-straints. Some of the excess demand could divert to road transport, butthe spare capacity of the vehicle fleet is apparently limited and productionlosses are likely to occur. Therefore, a simple comparison of the cost oftransporting the diverted traffic on the roads rather than on the railwaysas used in the two projects under consideration is, in our opinion, in thecase of India, a questionable way of assigning benefits. Avoidance ofpossible production loss due to lack of transport also should be consideredas an additional benefit of investment in the railways.

28. A long run perspective is required for a proper analysis of theeconomic returns of the investments in the IR. 1/ In the short run, theremay be fluctuations in the degree to which capacity is used, which may resultin low utilization of capacity in some years and in problems of moving thetraffic in others. If these fluctuations are not too large, the railway hasadequate procedures to face them properly (i.e., reducing or increasing wagonand locomotive scrapping as well as accelerating or reducing the volume andpriority of certain programs). But the problem appears when large discrepanciesdevelop between capacity and demand, something which apparently had not beenthe case in the recent past. Large discrepancies may produce: (a) overinvest-ment for long periods with serious consequences regarding the efficient useof resources or (b) underinvestment with serious consequences on total trans-port costs and the ability of the economy to reach its full productivepotential.

29. The development of a long term Corporate Plan for the IR is in-tended to place the analysis of investments and other policies affectingrailway efficiency and capacity in a long run perspective as well as inthe broader perspective of the complex interrelationships affecting differentactions that may be taken. Preparation of such a plan implies a complex

1/ In the appraisal of the 11th project the economic return calculated forthe subprojects was based on the long term growth of traffic, while this wasalso done for the economic return on the 12th project. Furthermore, theexpost economic return for the 12th project has been calculated consider-ing, as a basis, the average traffic developments over a 5 year periodand the anticipated long range developments.

- 10 -

process of progressive detail and revision on which, on the one hand, theproposed actions of original versions are improved as a result of the con-sideration of more interactions and, on the other hand, the programs aremodified and detailed as a result of the definition and analysis of specificsub-projects and policy measures. It is important that this iterative processbe based as much as possible on sound analytical procedures taking into properconsideration economic as well as technical and financial criteria. Analysisof the procedures in use indicates that more attention should be paid toeconomic criteria.

(d) Finances and Traffic Diversion

30. As has been explained in para. 8 and the PCRs, IR's finances haddeteriorated during the project period, but are now recovering. The factthat IR could not pay the required dividend on the Government capital investedin the Railways in itself is not surprising, because economic and politicalconditions during the period were particularly difficult; moreover, it nowappears that starting in 1975/76, the dividend requirement will again befulfilled. This does not mean, however, that IR's financial situation iswholly satisfactory because IR has received numerous short-term loans from theGOI, some of which have been used to pay dividends to the GOI. Furthermore,under the 10th project, agreement was reached that starting from 1970/71, IR'soperating ratio 1/ would not exceed 80. Subsequent projects no longer mentionoperating ratios. Actual operating ratios for 1970/71 to 1975/76 were 84, 83,85, 94, 94 and 91. 2/

31. No firm information is available on the extent that rates and fareshave been used to achieve a more economic distribution of traffic betweenmodes. Present freight rates are uniform per commodity or commodity group andtaper off when the transport distance increases. The rates are supposed to bebased on the actual cost incurred to carry each commodity plus overheads. Forbulk traffic such as coal, steel and fertilizers, rail transport would becheaper than road transport, assuming good service can be provided. Therefore,charging this traffic the total cost should not normally incur the risk oftraffic diversion. For other commodities and in general for short and mediumdistance traffic, road transport apparently is now taking a greater share.Charging this traffic with the full overheads of IR could easily lead to anuneconomic distribution of traffic between modes because (a) IR has to carry

1/ The operating ratio is the working expenses plus depreciation divided byoperating revenues, expressed as a percentage.

2/ Estimate.

- 11 -

a much heavier social burden than road transporters and (b) in many casessunk investments in track and other facilities would remain underutilizedwhile roads would have to be built or improved. A few years ago, zonalmanagers were authorized to use flexibility in rates as part of improvedmarketing efforts. Costing cells were created in the zonal railways, butthere is still a shortage of data on costs and rates charged by competingmodes.

32. Among the social burdens carried by IR, a major item is the laborforce, which per unit of traffic and in view of the large volume of bulktransport moved, appears very large. IR has been fairly successful over thelast years in slowing down further growth of the labor force. In a countrywith high unemployment it is difficult to reduce the labor force and a highdegree of mechanization would be undesirable. However, taking into accountrecent increases, wages represent over 70% of total operating costs. IR alsooperates hospitals, schools and other social services. It has a number ofuneconomic lines and services which are continued for social or strategicreasons, as well as losses on suburban commuter services. If all thesecosts were charged proportionally to the traffic, it would shift the compe-titive advantage to road transport, where the same social costs are carried bythe national Government. These problems were pointed out in the appraisalreport of the 11th project.

(e) Transport Sector Planning and Coordination

33. As mentioned earlier, agreements on transport planning have beenincluded under the two projects. Investment programs are prepared for eachmode within the appropriate agency and the programs are submitted to thePlanning Commission for approval. However, a comprehensive analysis of theproblem of intermodal coordination has not received the attention that itdeserves.

34. Railway planning has already been discussed earlier in this chapter.The investment plans proposed by IR are probably the most comprehensive in thetransport field, even though more emphasis on economic factors in the planningprocess would be desirable. The highway subsector is handicapped in preparinginvestment plans by the division of jurisdiction over the highway systembetween the Ministry of Shipping and Transport (Roads Wing) and the individualstates, as well as by a serious shortage of traffic data. There is no thoroughand systematic approach to traffic counting and hence inadequate information onpresent traffic volumes and traffic growth. Comprehensive data on trafficorigin and destination are also lacking. This information would be useful forhighway planning, and essential for the formulation of a policy for achievingthe most economic distribution of traffic between transport modes, throughbetter pricing, licensing (or the lack of it) and investment.

35. The Shipping Wing of the Ministry of Shipping and Transport isresponsible for port planning and investment as well as for shipping. Sincethe major investments are made for bulk transport, which have to rely on therailways for movement within the country, there is a definite effort tocoordinate port and railway investment, whenever relevant. Coastal shippingmostly for salt and a small quantity of coal, lightens IR's burden somewhat,

- 12 -

but is not very significant. Occasionally recommendations have been made touse coastal shipping for bulk transport on a large scale, specially for coalfrom the east to the coastal regions in the South and West of India. 1/ These

suggestions have never been carried out largely because of port capacityproblems and a lack of determination to enter into such a venture.

36. A number of Government measures affect the development of transport.This is specially the case for road transport which has been hampered by avariety of local taxes levied as tolls and restrictive licensing. The GOI has

made progress in eliminating some of the taxes, which slow down traffic.

37. There is much room for improvement in transport planning and coordi-

nation, before the optimum use can be made of funds spent on the sector. Theissue has been the subject of a continuous dialogue between the GOI and theBank. Transport planning has been discussed specifically during the negotia-tions for the two projects under review. When the 11th project was negotiatedthe GOI stated its intention to undertake a full review of the transportsector, with emphasis on the need for better coordination and effective insti-tutions to achieve policy objectives. The Association agreed to contribute tothis review by means of a comprehensive sector mission. The review wasexpected to take about 18 months and to lead to an understanding between theGovernment and the Association on the basis of future Bank Group activity in

the transport sector. Work on the review was underway when the 12th projectwas negotiated. At that time, a timetable for the completion of the activitieswas agreed on.

38. The transport review and sector survey were completed as plannedin late 1973. The Planning Commission is currently engaged in exploring thepossibilities of developing an analytical frame-work which may help in improvingthe basis on which resources are allocated to different modes of transport.Recently, a UNDP advisor has been appointed to help the GOI with these efforts.The above as well as the successful exercise of IR in preparing the corporateplan indicate that the considerable efforts made in the past have led to acertain amount of progress.

(f) The Bank Group's Role

39. IR is a very complex organization which for many years had to face ademand much higher than its capacity. In addition, the foreign exchange short-age of India was very serious, which implied that without Bank/IDA support atthe appropriate times, the replacement and expansion program of IR could have beenadversely affected, thus hampering industrial production and the vital supplyof farm inputs and foodstuffs.

I/ A new study was recently completed, but it is too early to know whetherit will lead to increased use of coastal shipping.

- 13 -

40. The Bank has not been very persistent on the specific andgeneral issues of national transport planning. It appears that during theproject periods (11th and 12th) when the capacity shortages were no longerserious, it would have been to India's benefit if agreements could havebeen reached on more rapid and specific improvements in the planning field.

The corporate plan is the most successful institutional result of IR/Bankcooperation. It appears essential that this effort be maintained and ex-

panded upon. In future contacts Bank staff should continue to support this

effort, and more so than in the past the staff should be supplemented byhighly specialized technicians to advise IR on various innovations and guidethe Bank in details of further lending efforts.

III. CONCLUSIONS

41. Bank/IDA lending to IR over the past 28 years has been importantto the development of India, because it provided the foreign exchangeresources without which IR's replacement and expansion program would havebeen very difficult. For a long period practically all IR's resources wereconcentrated on increasing capacity to avoid transport becoming a bottleneckfor economic expansion and the movement of vital food supplies.

42. Under the considerable operating pressures which prevailed overmany years, planning has not received rightful attention, leaving amongstothers traffic forecasting and feasibility studies of sub-projects much weakerthan could be expected from an advanced organization such as IR. For example,the system's freight carrying capacity appears higher than required forthe present demand. Some or maybe all of this excess capacity is desirable,since India's industrial establishment is capable of increasing its produc-tion at short notice. Based on the mission's findings, it appears that bettermethods for calculating the carrying capacity would be desirable. In addition,further improvements in the methods for operations and planning might resultin lower requirements for new investment; in percentage terms, even a smallsaving in the case of IR would amount to substantial sums. The corporate plan-ning exercise, started under the 11th project, is a substantial improvementand should be continued and broadened.

43. In terms of timing and procurement procedures project implementa-

tion has been satisfactory, but there is a lack of exact knowledge on what

has been achieved. When components are provided for an ongoing production

and building process, precise control is difficult, but more details on

what was achieved would be desirable. A better reporting system relatingcomponents financed by IDA more specifically to identified project items (such

as specified lines or particular types of locomotives), should be considered

for future projects, to serve as a management tool for IR and a better system

to account for loan funds.

44. IR has experienced some trouble meeting its financial commitments

during the project period, due to lower than expected traffic, sharplyincreasing costs and a lag in increases of rates and fares, but the

situation is now improving. IR's share of total freight transport has

- 14 -

decreased from 66% to 54% during the project period, to the advantage ofroad transport. In the last few years IR's marketing efforts have improvedand are assisted by a certain flexibility in rates. Moreover, it seemsthat the present rate structure may be conducive to diverting traffic toother modes, because of IR's high social charges which are distributed overtraffic. It appears advisable for IR to specially emphasize marketing andmake full use of flexible rates specially in areas where lines are now usedwell below capacity, and thus retain or regain traffic in areas where com-petition from other modes is very severe.

45. In spite of frequent discussions between the Bank and the GOI,relatively little progress has been made in the field of overall transportplanning and coordination. In its efforts to assist, the Bank has beenhampered by its very limited involvement in the highway sector, as well as bythe shortage of information on road transport. The present lack of coordina-tion of studies and investments for competing modes (mostly rail, road andpotentially coastal shipping) could be logically expected to have resultedin substantial economic losses. The process of coordinating investments indifferent modes of transport is now being improved (para. 38).

46. The Bank's influence on certain aspects of institutional develop-ment has been rather weak (e.g., see paras. 9 and 33). The Bank has beensomewhat hampered in pressing for more rapid progress by its own limitedknowledge of the transport sector and by the fact that lending to IR serveda primary role in transferring resources to the Indian economy. To gainimproved knowledge of problems in the transport field in India, an increaseduse of highly specialized consultants as part of the Bank's transport missionsto India may be useful, as has already been done occasionally (e.g., missions in1977 to review the manufacturing units of IR).

PROJECT PERFORMANCE AUDIT MEMORANDUM

INDIA 11th AND 12th RAILWAY PROJECT (CREDITS 280 AND 448)

Appraisal Estimates and Actual Performance (Physical)

11th Project (CR 280) 12th Project (CR 448) Both Projects Different1971/72-1973/74 1974/75 from Appraisal Estimates

Appraisal AppraisalEstimate Actual Difference Estimatel Actual Difference Actual Units Percentage

Locomotives (Units)Steam " 18 19 +1 0 0 0 19 +1 +6Diesel " 470 385 -85 223 121 -102 506 -187 -27Electric " 211 125 -86 78 46 -32 171 -118 -41

Total " 699 529 -170 301 167 -134 696 -304 -30

EMU's " 568 259 -309 245 201 -44 460 -353 -43Coaches 3,950 3,545 -405 1,339 859 -480 4,404 -885 -17Wagons (in terms of 4 wheelers) 31,649 31,112 -537 21,680 10,958 -10,722 42,070 -11,259 -21

Rail Renewal (km) 4,400 4,070 -330 1,360 731 -629 4,801 -959 -17Line Doubling " 750 1,027 +277 240 139 -101 1,166 +176 f18Electrification 720 500 -220 360 259 -101 759 -321 -30New Lines 700 574 -126 280 56 -224 630 -350 -36

1/ Adjusted for 12-month period.

Source: Appraisal Reports and PCR.

PROJECT PERFORMANCE AUDIT MEMORANDUM

INDIA llth AND 12th RAILWAY PROJECT (CREDITS 280 AND 448)

Appraisal Estimates and Actual Performance (Financial)

Eleventh Project Twelfth ProjectCr 280 Cr 448

Schedule One Final Schedule One Final Both Projects Togetherof Credit Disburse- of Credit Disburse- Percentage Change from

Category Agreement ment Agreement ment Credit Agreement

(in million US dollars)

1. Components and materials (including steel)required for manufacture of Electric Loco-

motives, Diesel Locomotives, Electric Mul-

tiple Units, Coaches and Wagons. 33.0 39.5 49.5 56.4 +16

2. Equipment and material for line capacity

works, electrical works, etc. 3.0 3.2 1.5 4.2 +64

3. Rails 5.0 1.0 2.5 2.0 -60

4. Equipment for signalling and tele-communication schemes. 3.0 2.2 2.0 1.0 -36

5. Equipment and material for electrificationschemes. 4.0 3.1 2.0 1.5 -33

6. Plant and machinery. 3.5 1.6 2.0 1.0 -57

7. Other railway equipment and material. 6.5 7.7 4.5 4.3 +9

8. Non-competitive procurement of components

for manufacture of Diesel Locomotives,

Electric Locomotives and Electric Multiple

Units. 17.0 16.7 16.0 9.6 -20

Total 75.0 75.0 80.0 80.0

Source: IDA files. MC

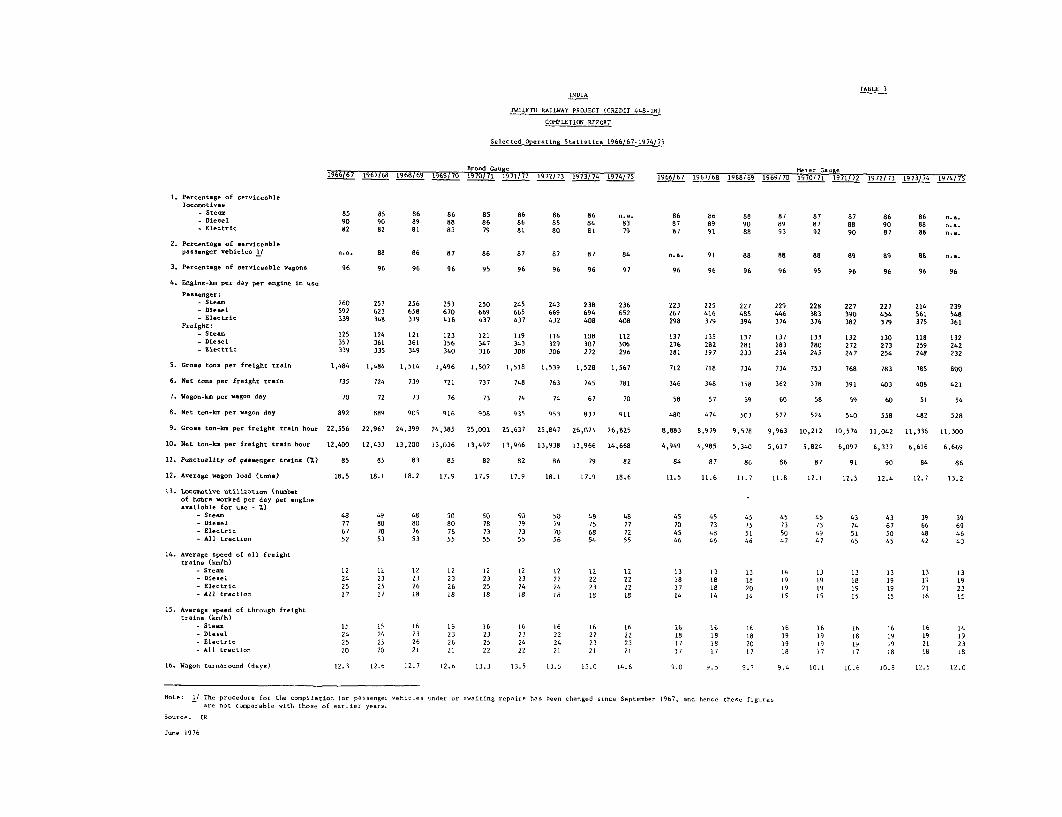

PROJECT PERFORMANCE AUDIT MEMORANDUM Table 3a

INDIA 11th AND 12th RAILWAY PROJECT (CREDITS 280 AND 448)

Operating Performance 1966/67-1975/76

Broad Gauge 1/

1966-67 1967-68 1968-69 1969-70 1970-71 1971-72 1972-73 1973-74 1974-75 1975-7&--

1. Percentage of serviceablelocomotivesSteam 85 86 86 86 85 86 86 86 84 85

Diesel 90 90 89 88 86 86 85 84 83 84

Electric 82 82 81 83 79 81 80 81 79 80

2. Percentage of serviceable

passenger cars 91 88 86 87 86 87 87 87 84 85

3. Percentage of serviceable

freight cars 96 96 96 96 95 96 96 96 96 96

4. Engine - km/day/engine in use

PassengerSteam 260 257 256 253 250 254 243 238 236 238

Diesel 592 623 658 670 669 665 669 694 652 641

Electric 339 348 379 416 437 437 432 408 408 450

FreightSteam 125 124 121 123 121 119 114 108 112 114

Diesel 357 361 361 356 347 343 329 307 306 321

Electric 339 335 349 340 316 308 306 272 296 369

5. Net tons/freight train 735 724 739 721 737 748 763 745 781 840

6. Wagon - km/freight wagon day 70 72 73 76 73 74 74 67 70 77

7. Punctuality of passenger

trains (%) 85 85 83 85 82 82 86 79 82 86

8. Average wagon load (tons) 18.5 18.1 18.2 17.9 17.9 17.9 18.1 17.9 18.6 20.7

9. Average speed of all goods

trains (km/h)Steam 12 12 12 12 12 12 12 12 12 12

Diesel 24 23 23 23 23 23 22 22 23 22

Electric 25 25 26 26 25 24 24 23 22 24

All traction 17 17 18 18 18 18 18 18 18 19

10. Average lead of a ton of

freight (km) 555 581 582 587 615 641 643 631 655 665

11. Wagon turn-around (days) 12.3 12.6 12.7 12.7 13.3 13.5 13.5 15.0 14.6 13.2

1/ Some 1975-76 data are provisional.

Source: Appraisal Reports and IR.

Table 3b

PROJECT PERFORMANCE AUDIT MEMORANDUM

INDIA 11th AND 12th RAILWAY PROJECT (CREDITS 280 AND 448)

Operating Performance 1966/67-1975/76

Meter Gauge

1966-67 1967-68 1968-69 1969-70 1970-71 1971-72 1972-73 1973-74 1974-75 1975-761/

1. Percentage of serviceablelocomotives

Steam 86 86 88 87 87 87 86 86 85 84Diesel 87 89 90 89 87 88 90 88 87 88Electric 87 91 88 93 92 90 87 88 88 85

2. Percentage of serviceable

passenger cars 93 91 88 88 88 89 89 88 87 89

3. Percentage of serviceablefreight cars 96 96 96 96 95 96 96 95 95 96

4. Engine km/day/engine in usePassenger

Steam 223 225 227 229 228 227 217 214 239 221Diesel 267 416 485 446 383 390 454 561 540 533Electric 298 379 394 374 376 382 379 375 361 401

FreightSteam 137 135 137 137 133 132 130 118 132 120Diesel 276 282 281 283 280 272 273 259 242 286Electric 181 197 233 254 245 247 254 248 232 225

5. Net tons/freight train 346 348 358 362 378 391 403 408 421 432

6. Wagon km/freight wagon day 58 57 59 60 58 59 60 51 53 57

7. Punctuality of passengertrains (%) 84 87 86 86 87 91 90 84 86 93

8. Average wagon load (tons) 11.5 11.6 11.7 11.8 12.1 12.5 12.4 12.7 13.2 13.9

9. Average speed of all goodstrains (km/h)Steam 13 13 13 14 13 13 13 13 13 12Diesel 18 18 18 19 19 19 19 19 19 19Electric 17 18 20 19 19 19 19 21 23 20All traction 14 14 14 15 15 15 15 16 15 15

10. Average lead of a ton offreight (km) 379 395 411 415 422 447 469 462 478 n/a

11. Wagon turn-around (days) 9.0 9.5 9.7 9.4 10.1 10.6 10.8 12.5 12.0 11.5

1/ Some 1975/76 data are provisional.

Source: Appraisal Reports and IR.

PROJECT PERFORMANCE AUDIT MEMORANDUM TABLE 4

INDIA Ith AND 12th RAILWAY PROJECT (CREDITS 280 AND 448)

Freight Traffic: Forecasts and Actual

Total Tons Carried (Millions)

Annual % Annual %of Actual Growth over

Growth over Maximum1960-61 1965-66 1969-70 1970-71 1971-72 1972-73 1973-74 1974-75 1975-76 1976-77 1977-78 1978-79 1979-80 Period Elapsed Period Covered

Forecasts 1/11th Project (208)- 241 - 265 1.0 4.1

12th Project (198) 208 - - - - 280 2.8 5.0

13th Project (185)1/ 210 - - 250 265 9.3 6.2

Actual

2/156 203 208 197 198 201 185 195 2212 2.4

Total Ton /km Carried (millions)

Forecast11th Project (128248)1L 145028 - 156207 2.4 3.4

12th Project (133265)1L 141641 - - - - 187795 2.6 5.0

13th Project (122354) 144382 - - 166648 175104 10.0 6.2

Actual

2/87680 116936 128248 127358 133265 136531 122354 134594 1479832 3.6

l/ In brackets: base year for forecast2/ Provisional Figures

Source: Appraisal Reports and Indian Railways.

ATTACHMENT A

INDIA

ELEVENTH RAILWAY PROJECT

COMPLETION REPORT I/

1. Summary of Bank Group Lending for Transport

1.01 A summary of Bank Group lending for Indian Railways (IR) is pro-vided in Table 1. This lending amounts to US$786.5 million equivalent pro-vided through twelve railway projects. A thirteenth project, to be con-sidered by the Board in August 1975, has been appraised and negotiated; itis to be supported by an IDA credit of US$110.0 million equivalent.

1.02 Table 2 provides a summary of Bank Group lending for transportprojects other than railways. There have been seven such lending operationsamounting to US$254.6 million equivalent. In addition, the Bank Group hasprovided indirect support to the road transport industry through ten indus-trial Imports Credits in the amount of US$342.9 million equivalent (para5.06).

1.03 Total Bank Group lending to the transport sector thus amounts toUS$1,384.0 million equivalent, including the US$342.9 million indirectsupport to the road transport industry.

2. Summary of Credit 280-IN and Eleventh Railway Project

2.01 Credit 280-IN

(1) Borrower: Government of India (GOI)(2) Beneficiary: Indian Railways (IR)(3) Amount and Terms of Credit: US$75.0 m. equivalent on usual

IDA terms(4) Date of Credit Agreement: January 24, 1972(5) Effective Date: March 29, 1972(6) Closing Date: September 30, 1974(7) Date Fully Disbursed:

-estimated: March 31, 1974-actual: October 22, 1974

(8) Amount Cancelled: None(9) Current Exchange Rate: US$1.00 - Rs. 8.00

(floating with Pound Sterlingin relation to US$)

(10) Exchange RateNovember 30, 1971 (Date of Appraisal Report);

US$1.00 = Ra. 7.50

I/ This report was completed in July 1975, and is based on data collectedby Bank Missions to India in December 1974 and April 1975, made inconnection with the Thirteenth Railway Project.

- A.2 -

2.02 Eleventh Project

(1) Description:

Eleventh Railway Project - Consisted of IR's investment programfor the three years from April 1, 1971 to March 31, 1974 (end ofIndia's Fourth Five-Year Plan). The Project was a continuationof the previous, IDA financed (Credit 162-IN) Tenth Railway Project.The main Project components were: manufacture and putting intoservice of 700 locomotives, 570 electric multiple units (EMU's),30 diesel railcars, 4,000 coaches and 31,600 freight wagons (interms of 4-wheelers). In addition, the project included trackrenewal, line capacity, electrification and other works andconstruction of new lines and expenditures for workshops, machinery,plants and investories.

(2) Project Cost (appraisal estimate):

US$ millionLocal Foreign Total

Locomotives and Rolling Stock 292.8 142.6 435.6

Track Renewals 172.0 5.0 177.0

Line Capacity Works 160.6 4.5 165.1

Other works, including signalling,electrification, new lines andmachinery 289.0 17.9 306.9

Total 914.0 170.0 1,084.4

US$ million

(3) Financing of Project:

(i) Funds generated by IR 522.0

(ii) Government contribution (including proceedsof IDA credits and bilateral loans) 562.0

Total required funds 1,084.0

- A.3 -

(4) Foreign Exchange Components

US$ million

(i) IDA (Credits 280-IN and 162-IN) 100.0

(ii) Bilateral Assistance 58.3

(iii) GOI foreign exchange reserves 11.7

Total foreign exchange 170.0

(5) Procurement Arrangements: Through ICB except for US$17.0(for components financed million for certain componentsthrough IDA credit only) procured for local manufacture

under license or required to bepurchased from the originalsuppliers in the interest ofstandardization.

(6) Estimated Disbursement US$ million1971/72 1972/73 1973/74

11.0 39.0 25.0

(7) Economic Rate of Return: Ranging from 6% to 20% dependingon subproject.

(8) Appraisal Report: Report No. PTR-96a, Transportation

Projects Department, November 30, 1971.

Note: A comparison between the estimated andactual project cost with foreign ex-change expenditure is shown on theattached form 590 (Annex 1) and in

Table 5 of the present report.

3. Major Findings

3.01 The major findings resulting from project completion review are:

(i) IR's freight traffic, in terms of tons carried, fell considerablyshort of the original forecast during the project period, mainlybecause of the lower than expected growth within the heavy indus-trial sector, which generates the major part of IR's freighttraffic (para. 6.02). However, there was an increase in theaverage freight transport distance (para 9.06) and a higher thanexpected growth in IR's passenger traffic (para 6.02). These twofactors almost compensated, in terms of traffic units, for theshortfall in the tonnage carried (para 7.03);

- A.4 -

(ii) IR's investments during the project period (1971/72-1973/74)corresponded relatively well to estimated needs; in fact, theinvestment program was in physical terms reduced slightly morethan the shortfall in railway traffic (para 7.03);

(iii) operating performance was generally satisfactory over theproject period (para 9.03), although there was a deteriorationin availability of locmotives as well as turnround of freightwagons; corrective measures were subsequently taken (para 9.04to 9.06);

(iv) the Borrower has generally met the various covenants in thepast Credit Agreements (para 11.01); however,

(v) the earnings covenant was not met in 1973/74 because ofexceptional cost increases and interruptions to traffic(the requirement was subsequently waived, para 11.03);in the first two project years the covenant was satis-factorily complied with;

(vi) the results of the economic evaluation undertaken duringthe Eleventh Project appraisal appear generally to becorrect; if anything, the economic rates of return mayhave been higher than those estimated at the time ofappraisal, because recent cost developments have inrelative terms tended to increase the advantage of railtransport over road (para 12.05); and

(vii) as a whole, the Eleventh Railway Project met its objectives(para 12.06).

4. Recommendations or Action Taken

4.01 There are no recommendations to be made regarding the generalapproach used in preparation, appraisal and implementation of the EleventhRailway Project, which would have implications for subsequent appraisals.The review indicates, however, that more efforts could have been devotedto the assessment of future traffic development, to a more detailed ex-amination of various subprojects included in IR's investment program, tothe likely development of investment and operating costs and to an assess-ment of the revisions required in the structure and level of rates and faresin the light of cost trends. All these factors affected the financialposition of the railways and caused changes in the project in real terms.Attempts have already been made during the appraisals of the Twelfth andThirteenth Projects to achieve improvements in these areas and therefore,no further action is recommended other than to continue these efforts inthe future.

- A.5 -

4.02 Assoclatad with railway project issues, those relating to thewhole transport ,ector have been of major importance during the past tenyears. It Is recommended that efforts should continue to improve overallsector management and planning; however, these efforts should not be madeat the cost of solving project related issues, which may to some extenthave been the case in the past. Similarly, it appears to be of lesservalue to try to reach formalized agreements regarding overall issues;attempts should rather be made to reach agreements on performance targetsfor individual projects.

4.03 In respect of future completion reviews of IR projects, it isrecommended that a full review of Bank Group lending operations should beundertaken in 1979/80, after the current IR 1974/75-1978/79 investmentprogram has been completed, while for individual projects, 1/ short sum-mary completion reports should be prepared on the basis of subsequentsupervision and appraisal reports.

5. Bank Group Lending to Transport Sector

5.01 Bank Group lending to India started with the First Railway Loan(17-IN) made in August 1949 in the amount of US$34.0 million equivalent.Since then, the Bank Group has contributed to the financing of 19 transportprojects. 2/, 3/ The total of these loans/credits is US$1,041.1 millionequivalent, which represents 21.0% of the total Bank Group lending to Indiaof US$4,953.3 million equivalent (as of May 31, 1975). This share has de-creased since Credit 280-IN for the Eleventh Railway Project was made inJanuary 1972; at that time, the Bank Group had provided financing for 16transport projects to the total amount of US$803.1 million equivalent,amounting to 28.9% of Bank Group lending to India (US$2,784.0 millionequivalent as of December 31, 1971). All these lending operations havebeen satisfactorily completed. Details on Bank Group lending are providedin Table 1 for railways and in Table 2 for other transport projects.

5.02 As shown in these two tables, most of the Bank Group direct lendingto the transport sector consists of loans/credits to the Indian Railways (IR).These loans/credits amount to US$786.5 million equivalent made through 12lending operations, representing 75.9% of the total lending for transportprojects and 15.9% of total Bank Group lending to India. In January 1972,at the time Credit 280-IN was made for the Eleventh Railway Project, thecorresponding percentages were 79.1% and 22.7%.

5.03 The main reason for IR's large share of total lending has beenits central position within the economy, not only as transport carrier, butas by far the largest enterprise in India, closely involved in the develop-ment of major industries in the country. There have, however, been other

1/ Twelfth, Thirteenth and a possible Fourteenth Railway Project.2/ Excluding the proposed US$110 million equivalent IDA credit for the

Thirteenth Railway Project to be considered by the Board in August 1975.3/ There has, however, been substantial indirect lending to the transport

sector through Industrial Imports credits, as indicated in para. 5.06.In addition, the Bank Group has supported the transport sector throughagricultural projects, some of which have included a substantial com-ponent for rural roads.

- A.6 -

reasons, such as difficulties experienced in preparation of projects in theother modes of transport or in reaching agreements between GOI and the BankGroup on the project implementation and procurement procedures to be followed.

5.04 The most active period of Bank Group lending for the transportsector was between 1957 and 1962 with a total of 11 lending operations inthe amount of US$516.6 million equivalent, which at 1975 prices would pro-bably correspond to at least US$1.0 billion. During this period, fourlending operations were undertaken for ports, one for highways and onefor aviation, in addition to the five lending operations for railways.This was a period when the Second Five-Year Development Plan 1955/56-1959/60was successfully completed, with a considerable increase in traffic demandand with good prospects for a continuation in these trends. However, duringthe Third Five-Year Development Plan period 1960/61-1964/65 economic growthwas slower than expected and there were difficulties in implementation ofBank Group financed highway and port projects.

5.05 During the years following the early 1960's, direct Bank Grouplending for the transport sector has been limited to the railways, exceptfor Credit (328-IN) made in 1972 for the first shipping project. Althoughthere has been talk about a Second Highway Project over the past 5-6 years,the project has not yet reached identification stage. There are someprospects for a Coal Transport Project which has been under preparation forsome time and which may be ready for a Bank Group appraisal within the nextyear.

5.06 The Bank Group has provided indirect support for highway transportsince 1964 through the Industrial Import Program Credits, which have helpedto import parts, components and materials required for indigenous productionby a number of industries. Among these, commercial vehicle and ancillaryequipment and parts manufacturing have been two of the more importantindustries supported through the Industrial Imports Credits. Out of thetotal of US$930 million equivalent made under the first nine fully disbursedCredits from 1964 to 1974, an amount of US$302.9 million equivalent, or32.6%, was allocated to meet import requirements of these two industries 1/.In addition, US$40.0 million equivalent was allocated for the same two in-dustries out of the US$200 million equivalent Tenth Industrial ImportsCredit (528-IN) made in February 1975 2/. Therefore, including this in-direct lending of US$342.9 million equivalent, the total Bank Group supportfor the transport sector amounts to US$1,384.0 million equivalent, represent-ing 27.9% of total Bank Group lending to India (as of May 31, 1975). The in-direct lending can be supported on sector grounds, because shortale of com-mercial vehicles appears to have been an even greater constraint on economicgrowth than deficient highway infrastructure.

1/ Project Performance Audit Report, India, Seventh and Eighth IndustrialImports Projects, Operations Evaluation Department, June 9, 1975.

2/ President's Report No. P-1558-N, Tenth Industrial Imports Program Credit,January 16, 1975.

- A.7 -

5.07 Including the above mentioned indirect support of road transportindustry, the Bank Group lending to the two main modes, rail and road trans-port, has been about equal during the past ten-year period 1964-1974; thelending to railways amounted to US$340.0 million equivalent, while lendingfor road transport amounted to US$342.9 million equivalent.

6. The Economy and the Transport Sector

A. The Economy and Traffic Development

6.01 Credit 280-IN for the Eleventh Railway Project was made inJanuary 1972, about half-way through the Fourth Five-Year Development Plan(1969/70-1973/74). Although some difficulties had been experienced inachieving the Plan targets during the two first years 1969/70 and 1970/71,there were, at the time of the appraisal, prospects for continued economicgrowth: "according to the Bank's latest (1971) economic report on India,there is little question that India's economy should grow substantially inthe remaining years of the Plan and that the transport sector can thereforeanticipate a significant increase in demand for its services." 1/

6.02 However, adverse developments took place in 1971 and in the nextyear's (1972) economic report it was stated that: "it became obvious as1971 wore on that the refugee problem, the war and the uncertain future offoreign aid made a definitive forecast of the last three years of the Planvery difficult." 2/ The Government undertook a Mid-Term Appraisal of thePlan, which resulted in a series of downward adjustments to the 1973/74physical production targets, particularly for the heavy industrial sectorgenerating the major part of the railways' freight traffic. For instance,the target for ingot steel production in 1973/74 was reduced by 2.6 milliontons to 8.2 million tons, which for railways implied a reduction in trafficof about 10 million tons, including the related raw materials.

6.03 As a result of difficulties experienced during the Fourth Planperiod, only 185 million tons of freight was carried by IR at the end ofthe period in 1973/74, compared with 240.5 million tons forecast in theappraisal report 3/ and 260 million tons forecast at the time of preparationof the Plan. However, in terms of ton-km, the shortfall was substantiallyless, because the average load increased from 556 km in 1965/66 to 649 kmin 1973/74 (para 9.06). A comparison with the appraisal forecast and actualfreight traffic is shown in Table 3. On the other hand, IR's passengertraffic did meet the forecast (Table 4), partly because the forecast wasin the first place conservative and partly because passenger traffic isdependent on population growth and was thus less affected by difficultiesexperienced within industries generating most of the railway's bulk freight.

1/ Appraisal of An Eleventh Railway Project, India, Report Nol PTR-96a,November 30, 1971, para. 2.01.

2/ Economic Situation and Prospects of India, Report No. SA-32a, May 10,1972, para. 1.26.

3/ The difference in revenue earning traffic was however smaller, 172.0versus 207.5 million tons, because there was a substantial reduction inIR's non-revenue earning departmental traffic from 33.0 to 22.8 milliontons.

- A.8 -

B. The Transport Sector

6.04 At the time of appraisal of the Eleventh Railway Project, railwaysaccounted for about 66% of freight and about 50% of passenger traffic,while road transport accounted for about 28% and 48% respectively. Of theother modes, coastal shipping and pipelines accounted then about 3% eachof total freight traffic, while air transport accounted for about 1-2% oftotal passenger transport. No great changes have taken place during thepast 4 years, although road transport may have slightly increased its share

to about 40% of freight and 55% of passenger traffic. Overall, both freightand passenger traffic have increased by about 4-5% a year, railway trafficincreasing slightly less and road traffic slightly above this trend. Theother modes are still insignificant in the overall context, but perform anincreasingly important function within their respective, specialized areas.

6.05 The development in recent years which may have the most signif-icant effect on the transport sector was the substantial increase in priceof crude oil, which may continue its upward trend in future. There is notyet any empirical evidence on the effect on traffic distribution betweenthe various modes, but it is bound to reduce the competitive position ofhighway transport, because fuel represents a substantially higher share ofthe total costs for this mode than for railways, shipping and pipelines.Furthermore, India's foreign exchange position may impose additionallimitations on the expansion of road transport, the import content of whosefuel is much higher than that of the railways, which to a large extent usesdomestic energy resources (steam and electric traction). It is safe toassume, on the basis of the above considerations, that any major shift inthe relative importance of the two main modes is unlikely; the railwayswill continue to carry about 60% of the total freight and close to 50% ofpassenger traffic. It will continue to remain the single most importantmode of transport in India.

C. Transport Policy and Planning

6.06 In the course of railway lending, there has been a continuousdialogue between the Government and the Bank Group since the early 1960'son various issues relating to transport policy and planning for the sectoras a whole as well as concerning the individual modes. During this dialogue,the Bank Group has primarily been concerned about an apparent lack of a welldefined Government policy regarding the planning and management of the trans-port sector and about various constraints which may have reduced competitionbetween the various modes. Some particular concern was in the past also ex-pressed about road transport, which appeared to receive too little attentionby the Government.