worldcom fraud

TRANSCRIPT

Siddharth MallDeepika Bajaj

Rohit MallTeam ID : 630432

IIT Kharagpur

Capital Edge || Kshitij 2012

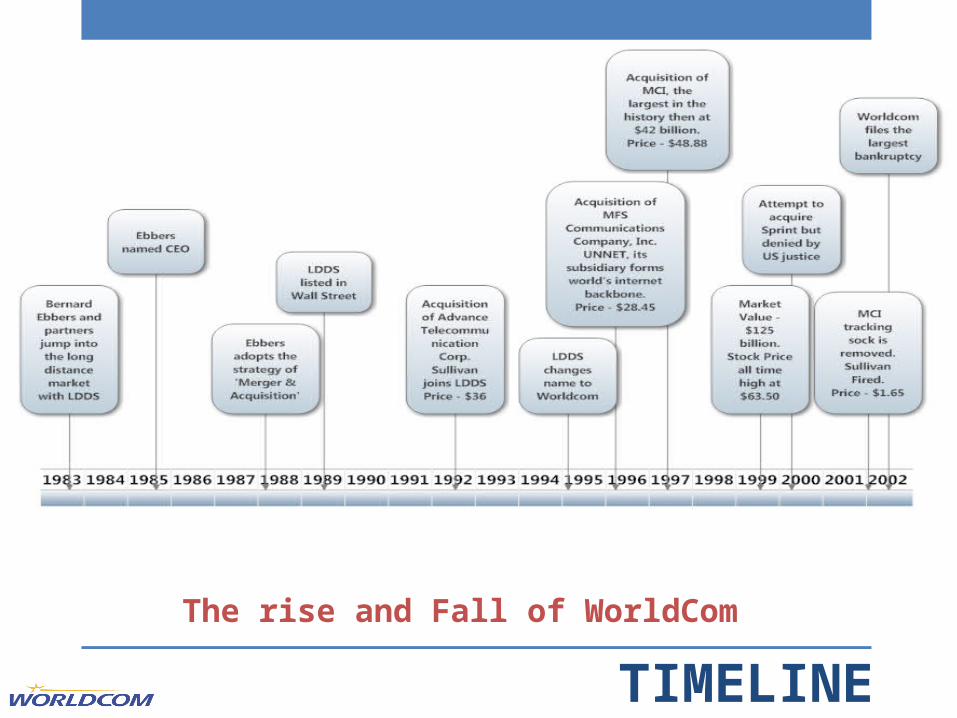

The rise and Fall of WorldCom

TIMELINE

Major aspects concerning the industry, their part in the growth and consequent fall

COMPANY

STRATEGIES

CULTURE

It was more than questionable whether WorldCom has effective, transparent process of application, evaluation, justified decision making, monitoring, risk assessment and follow up acquisition.

CORPORATE GOVERNANCE

•Habit of rubber stamping senior management’s decisions without scrutinising detailed performance indicators.

•Never met outside board meetings.•No vent for employees for reporting malfunctioning even if they felt so..

•Not bothered to look into the accounts of the company

Board of Directors

•Internal audit•Limited scope and power.•Perform mostly operational audits rather than financial audits.•Reported directly to the CFO

•External Audit: Arthur Anderson Firm•Limited its testing of account balancing relying on the adequacy of WorldCom's control environment.

•Overlooked serious deficiency in the accounting ledgers, which were exploited.

•Considered WorldCom as a “flagship client” and a “crown jewel” of its firm.

Audit

•Many senior executives, including the CEO Ebbers had private finances and debts taken on stocks of the company.

•The board (Compensation Committee)approved ‘sweetheart loans’ (over $400 million) to Ebbers, without any collaterals or assurances or knowledge of use of those funds.

Personal Finances

DOT COM Bubble Burst

Failure of Telecommunications

Industry

INDUSTRY GROWTH

• Prices for long-distance communication services were falling

• Local markets with high access charges were unprofitable

Graph: Telecommunication Revenue Growth

TECHNOLOGY

Lower demand for Long Distance services in market.

WorldCom was weak in wireless network and Technology

Attempted to achieve economies of scale by acquisitions Refusal of merger with Sprint (Largest wireless network company then) by US Justice Department to regulate the Telecommunications Industry.

LINE COSTS

Increase in E/R ratio

• WorldCom outsourced some portions of its calls

• Paid the outside service providers for carrying WorldCom customers’ calls on their lines.

• Took majority of its lines on lease.

Anticipated high demand in the industry. Increased their leased networks

Decline in the growth of telecommunication industry reducing the demand

Hefty fines for unutilized leased networks.

RELEASE OF ACCRUALS

Avoided recognizing standard operating expenses when they incurred, instead postponed them into future saying “work in progress”Improperly shifted these expenditures from income statement to balance sheet, increasing current income and inflating assets.

Reducing line costs and capitalizing entries significantly improved the line cost E/R ratio.

OTHER ADJUSTMENTS

Improperly booked of $312 million in revenue associated with Minimum Deficiency Charges.

Accounted for over $215 million of credits that it had issued to Telecommunications Customers.

Recognized $22.8 million in revenue from Early Termination Penalties.

CAPITALIZATION AND OTHER ADJUSTMENTS

CAPITALIZATION

Reduction to Line Costs by capitalization and other adjustments

(in % of the total line cost)

REACTIONS

“Our goal is not to capture market share or be global. Our goal is to be the No. 1 stock on Wall Street”

– Ebbers, CEO

“I guess the only way I am going to get this booked is to fly to D.C. and book it myself. Book it right now, I can‘t wait another

minute” – Myers, director of General Accounting, to Schneeberger on his refusal of releasing accruals.

One senior executive described the pressure as

“unbearable—greater than he had ever experienced in his fourteen years with the company”

Senior staff described the target of maintaining 42% E/R ratio as

“wildly optimistic, pure fantasy and impossible”

CFO Sullivan talked to Vinson and Normand about their resignation plans: “Think of us as an aircraft carrier. We have planes in the air. Let‘s get the planes landed. Once they are landed, if you still want to leave, then leave. But not while the planes are in the air”

The business unit managers were sceptical about the fraudulent accounting practices but some, because of their timid nature and the existence of the stringent hierarchy in WorldCom, were suppressed while others silenced by a disguised view of reality and lucrative incentives.

WHISTLE-BLOWER CYNTHIA COOPER

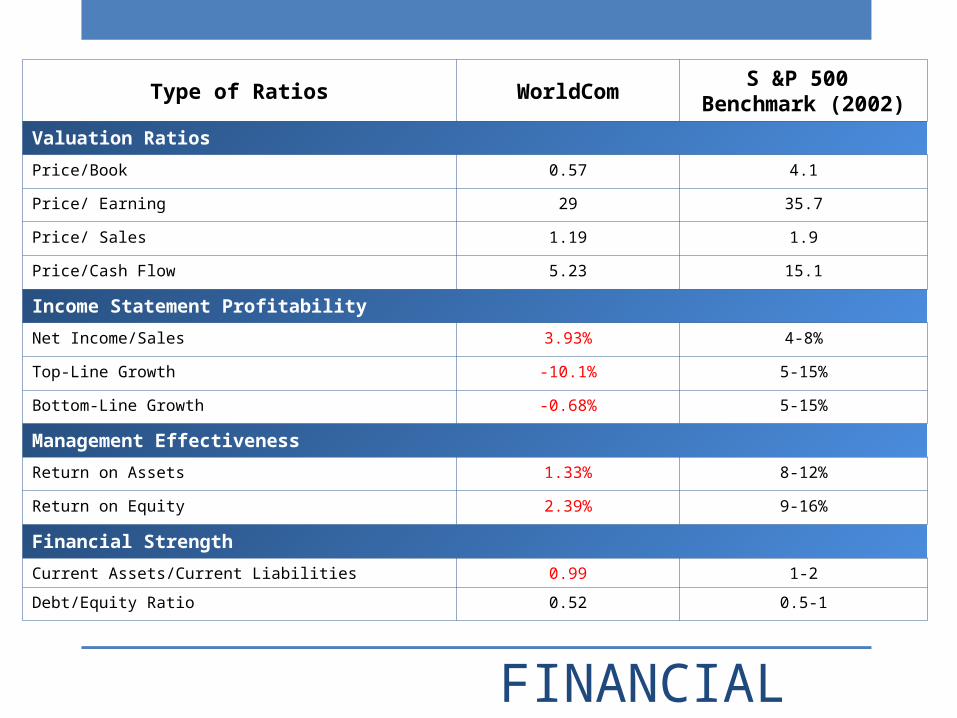

Type of Ratios WorldComS &P 500

Benchmark (2002)

Valuation Ratios

Price/Book 0.57 4.1

Price/ Earning 29 35.7

Price/ Sales 1.19 1.9

Price/Cash Flow 5.23 15.1

Income Statement Profitability

Net Income/Sales 3.93% 4-8%

Top-Line Growth -10.1% 5-15%

Bottom-Line Growth -0.68% 5-15%

Management Effectiveness

Return on Assets 1.33% 8-12%

Return on Equity 2.39% 9-16%

Financial Strength

Current Assets/Current Liabilities 0.99 1-2

Debt/Equity Ratio 0.52 0.5-1

FINANCIAL RATIOS

FINANCIAL ANALYSIS

RATIO DEFINITION 1999 2000 2001

X1 Working Capital/Total Asset (0.08) (0.08) (0.00)

X2 Retained Earning/Total Assets (0.01) 0.03 0.02

X3 EBIT/Total Assets 0.08 0.08 0.04

X4 Market Value of equity/Book Value of Assets

3.58 1.13 0.54

X5 Sales/Total Assets 0.39 0.40 0.34

Z Z-Score 2.697 1.274 0.798

Z SCORE ANALYSIS OF WORLDCOM

Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + X5

ACCOUNTING CONSULTANT

Recommendations an accounting consultant would have given on being commissioned:

SWOT ANALYSIS

QUESTIONS ?