wptc 2010 consumption report 12-10-2010

TRANSCRIPT

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 1/39

1

Survey of world-wide consumption 1999-2009

12 October 2010

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 2/39

2

Survey of world-wide consumption 1999-2009

Table of contents

Executive summary

1. A recap on processing and trade1.1. Trade1.2. Industrial background 2008/2009

2. Global consumption

3. The drivers of growth 4. Regional Consumption Trends

4.1. North America4.2. Brazil4.3. The Far East4.4. Central America4.5. Mediterranean Africa4.6. Europe4.7. Turkey 4.8. Other regions

5. Per capita consumption

6. Areas for potential development 7. Summary and projections for growth

8. ConclusionOther comment

Methodology

Apendices

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 3/39

3

Executive Summary In 2009, for the first time in ten years, the volumes of tomato products exported have beennoticeably lower than the previous year. This worldwide decline happened after the economicdownturn and is probably not attributable to it for several reasons. There is clearly aneconomic dimension to the contraction in world trade during 2009 which partly stems fromthe lower production in 2007 and 2008. However, the mechanisms that were fundamental tothis slowdown clearly seem also to come from strategic and/or commercial approaches offirst and second stage processing companies.

The contraction in trade does not seem to have had an “echo” in the estimated level ofconsumption of tomato products on a global scale. Whereas comparisons of trade between2008 and 2009 show a 4.8% decline, the analysis of global consumption shows a 5.2% riseduring the same period.

In 2009, the USA and Europe still accounted for the consumption of more than half of thevolumes processed worldwide. Nevertheless, the issue that stands out over the last decade

is unquestionably the rise in consumption in other regions. Another encouraging sign for theindustry worldwide is that, in most regions, the main driver for this increase derives from theboom in per capita consumption.

In 2008/2009, despite a slight inflection, worldwide consumption continued to grow but therate of growth was much reduced; finally, the increase was largely due to regions of medium-level consumption which more than compensated for the lack of growth in developedregions.

Drawing on national and regional figures, we can infer that from 1999 to 2009, averageannual consumption worldwide has grown from 5kg to 5.8kg per person constituting a jumpof nearly 16 % in 10 years.

In terms of growth, the annual rise in worldwide consumption is about 3% while per capitaconsumption is rising each year between 1.9% and 2%. It seems that we should now counton an annual growth rate in consumption volumes of around 1.1 to 1.2 million tonnes peryear compared to previous growth projections of 1 million tonnes per year at the end of the1990’s.

Thinking conservatively, if the growth is roughly linear, the individual consumption thresholdof 6kg could be exceeded by 2013/2014 whereas global consumption could pass the 44million tonne mark by 2015/2016.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 4/39

4

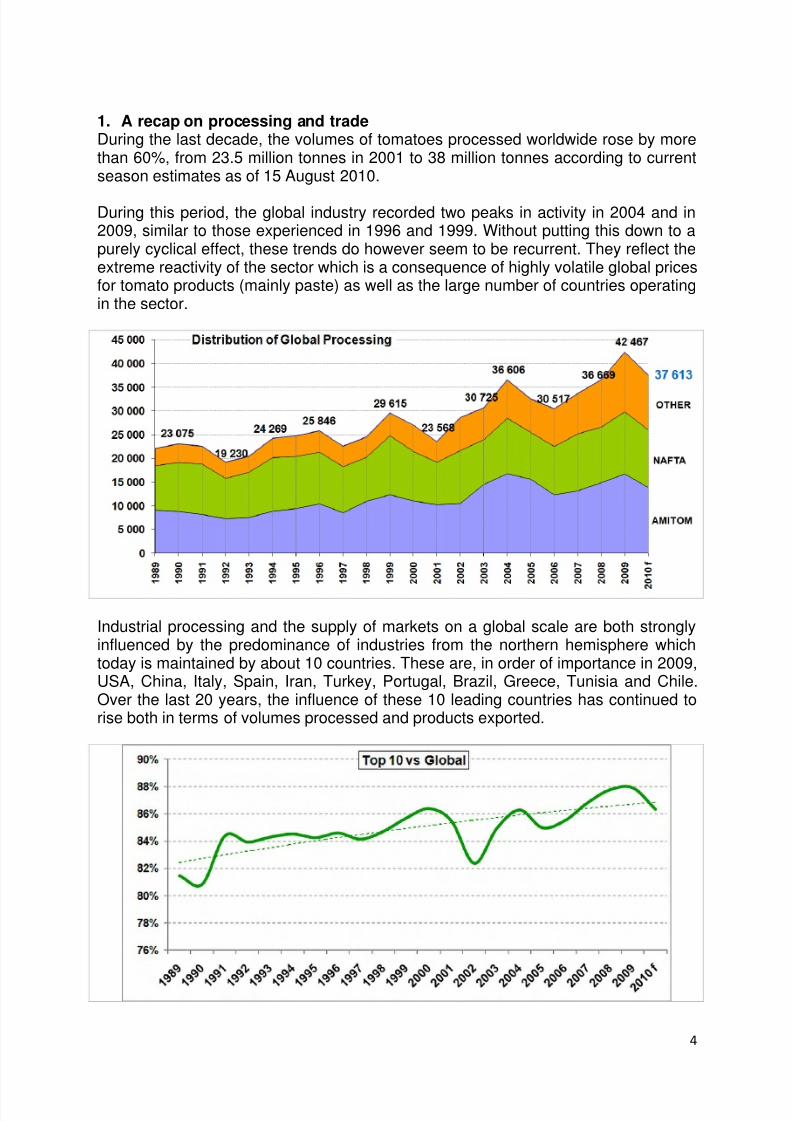

1. A recap on processing and tradeDuring the last decade, the volumes of tomatoes processed worldwide rose by morethan 60%, from 23.5 million tonnes in 2001 to 38 million tonnes according to currentseason estimates as of 15 August 2010.

During this period, the global industry recorded two peaks in activity in 2004 and in2009, similar to those experienced in 1996 and 1999. Without putting this down to apurely cyclical effect, these trends do however seem to be recurrent. They reflect theextreme reactivity of the sector which is a consequence of highly volatile global pricesfor tomato products (mainly paste) as well as the large number of countries operatingin the sector.

Industrial processing and the supply of markets on a global scale are both stronglyinfluenced by the predominance of industries from the northern hemisphere whichtoday is maintained by about 10 countries. These are, in order of importance in 2009,USA, China, Italy, Spain, Iran, Turkey, Portugal, Brazil, Greece, Tunisia and Chile.Over the last 20 years, the influence of these 10 leading countries has continued torise both in terms of volumes processed and products exported.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 5/39

5

1.1. TradeRecently published studies on global trade show, amongst other things, that thesignificant increases recorded since 2000 have been mainly due to the exceptionalgrowth of the Chinese processing industry. Initially, a competitor to larger traditionalindustries in Italy, Spain, Turkey, Chile and the USA, the Chinese industry now has

its share of the market by focusing on relatively low quality finished products enablingaccess to new markets with lower purchasing power, particularly Africa. After 10years, it appears that the quantitative increase in these global markets has alsoenabled the longer established industries to enlarge their markets and thereforeincrease their processing activities.

As concerns the USA and more especially, California, it should be noted thatalthough it has been a world leader in volumes for a number of years now, its entry

into the leading group of exporters is relatively recent. The ambitions declared by theCalifornian industry in 2006 have been attained during the last two years. The USbalance of trade for “tomato products” has gone from an annual average of 1 milliontonnes (fresh equivalent) between 2002 and 2007 to 2.5 million tonnes in 2008 and1.9 million tonnes in 2009.

In comparison, the development of Chinese exports is longer established but it is alsomuch more striking with a regular rate of growth from 816,000 tonnes in 2000 to 6.1million tonnes in 2009.

Over the past decade, global trade has increased sharply due to the growth in

demand and the growing concentration of centres for both processing and supply.The volumes exported on a global scale in 1999/2000 represented some 40% ofamounts processed but now account for nearly 60% of processed products in2008/2009.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 6/39

6

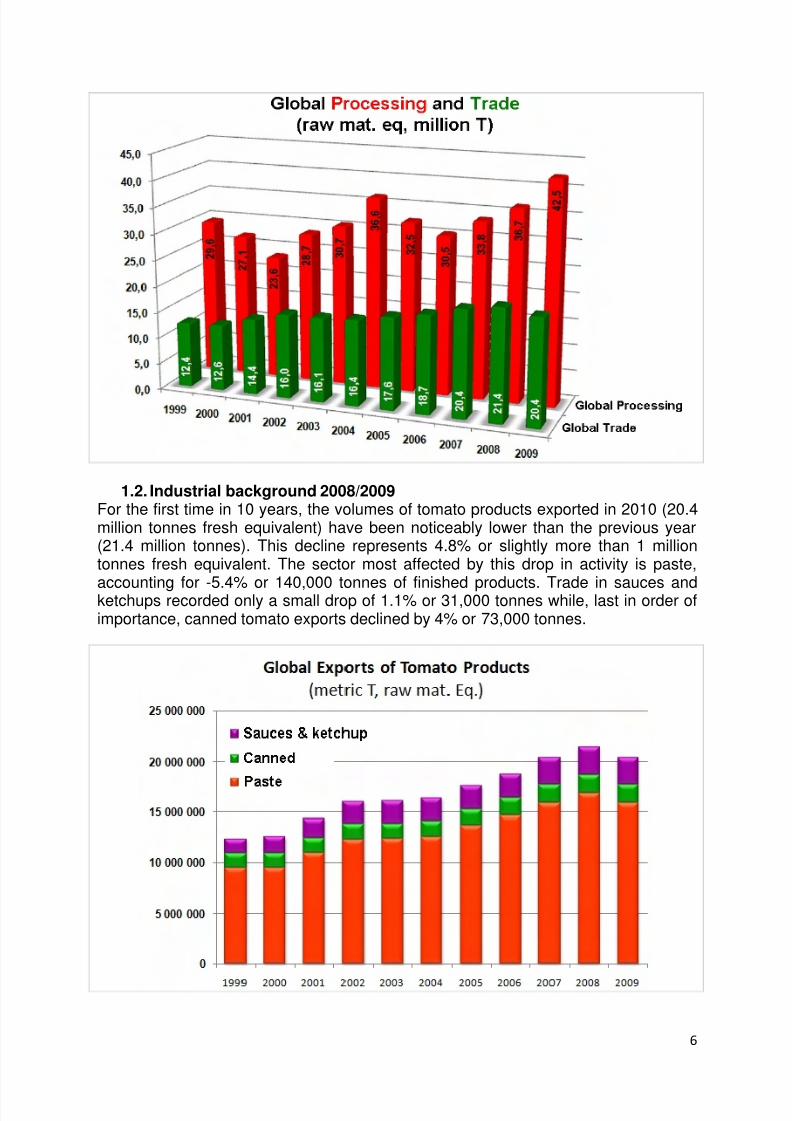

1.2. Industrial background 2008/2009For the first time in 10 years, the volumes of tomato products exported in 2010 (20.4million tonnes fresh equivalent) have been noticeably lower than the previous year(21.4 million tonnes). This decline represents 4.8% or slightly more than 1 milliontonnes fresh equivalent. The sector most affected by this drop in activity is paste,

accounting for -5.4% or 140,000 tonnes of finished products. Trade in sauces andketchups recorded only a small drop of 1.1% or 31,000 tonnes while, last in order ofimportance, canned tomato exports declined by 4% or 73,000 tonnes.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 7/39

7

This worldwide decline happened after the economic downturn and is probably notattributable to it for several reasons. Paradoxically, even though much of thedecrease concerns paste, the slow-down in trade is not simply down to countries withweak purchasing power which are usually significant contributors to global trends inthis type of tomato product. The main countries concerned by this drop are, in order

of importance, the Far East, Europe (in its broad geographical sense), the Emiratesregion and Asia-Pacific (see appendix for geographical zones). Next, is Central,America, Andean America, the Arabian Peninsula and the region of Ukraine-Belarus.The 2008/2009 marketing year saw a high level of trading which enabled undeniablyexcessive requirements to be met. This transpired in a context of fairly averageprocessing activity partly because of a shortage of merchandise following the 2008season and partly because of a ‘wait-and-see’ attitude on the part of global buyerswho were informed very early on that the 2009 season would be plentiful and lead toa crash in prices. These same forecasts of bumper harvests in 2009 promptedseveral processing regions such as the EU to defer, reduce or even suspend certainsupply routes. It is this that explains the strong decline registered by Chinese paste

exports (the largest on a global scale) between the 2007/2008 (850,000 tonnes) andthe 2008/2009 (779,000 tonnes) marketing years, or a historic slump of nearly 9%.

In addition, there is clearly, an economic dimension to the contraction in world tradeduring 2009. The spike in prices recorded between the end of 2007 and the end of2008 probably reduced supply to certain developing regions quite considerably.However, the mechanisms that were fundamental to this slowdown clearly seem tocome from strategic and/or commercial approaches of first and second stageprocessing companies.

Finally, it seems that there are also another analysis of this slow down that makes iteasy to explain. According to experts, this slow down follows on from the generallyshort crops of 2007 and 2008 which lead to a cumulative shortage of supply (andconsequent surge in price). As the logical outcome of this was, that were not enoughproduct to maintain the same level of trade, since the large 2009 crop only becameavailable in the last 3 (or 2) months of 2009. If this hypothesis is correct we shouldsee a compensating increase in shipments during 2010.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 8/39

8

2. Global consumptionThe contraction in trade does not seem to have had an “echo” in the estimated levelof consumption of tomato products on a global scale. Whereas comparisons of tradebetween 2008 and 2009 show a 4.8% decline, the analysis of global consumption

shows a 5.2% rise during the same period which represents the equivalent of nearly2 million tonnes of tomatoes.

Global processing : annual figuresGlobal consumption : 3 year average figures

Despite this rise, there is little doubt that the volumes processed in 2009 considerablyexceeded global consumption capacity and subsequently mark out 2009/2010 as ayear of surplus stocks. The graph above compares annual levels of processing andconsumption and clearly shows identical situations to 2009 in 1999 and 2004 as wellas the periods of shortfalls in 2001/2002 and 2006/2007.

Thus, from 1999 to 2009, global consumption of tomato products grew from 30.2million tonnes (fresh equivalent) to nearly 40 million tonnes. The USA and Europe,two long established processing regions, still accounted for the consumption of morethan half of the volumes processed worldwide, with consumption figures of 11 million

tonnes and 9.7 million tonnes (fresh equivalent) respectively.

As we have seen in our previous studies, these two regions are way ahead of theother main consumer centres. In 2009, the consumption in Mediterranean Africa wasestimated to be nearly 2.5 million tonnes (fresh equivalent), closely followed by theIran-Azerbaijan-Armenia region (2.2 million tonnes), the Far East (2.1 million tonnes)and West Africa (2 million tonnes).

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 9/39

9

Nevertheless, the issue that stands out over the last decade is unquestionably therise in consumption in other regions. Together, these represented 39 % in 1999 (11.2million tonnes fresh equivalent) but sharply increased over the period to now accountfor 48% (18.9 million tonnes) of global consumption.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 10/39

10

3. The drivers of growthAnother encouraging sign for the industry worldwide is that the rise in consumptiongoes way beyond demographic factors alone. In most regions, the main driver for thisincrease derives from the boom in per capita consumption.

This process is furthersubstantiated in marketsthemselves considered ‘young’.Even if we ignore extreme casessuch as Central Asia or Iraqwhere regional consumption wasextremely weak or even non-existent at the start of thedecade, it is both clear andlogical that the most marked

growth comes from rises in percapita consumption which are allthe more spectacular given thatthe markets are displaying initiallevels of consumption which arestill modest. Conversely, maturemarkets, particularly in America,Europe, the Far East andOceania, are registering muchslower growth rates based asmuch on demographics as percapita consumption.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 11/39

11

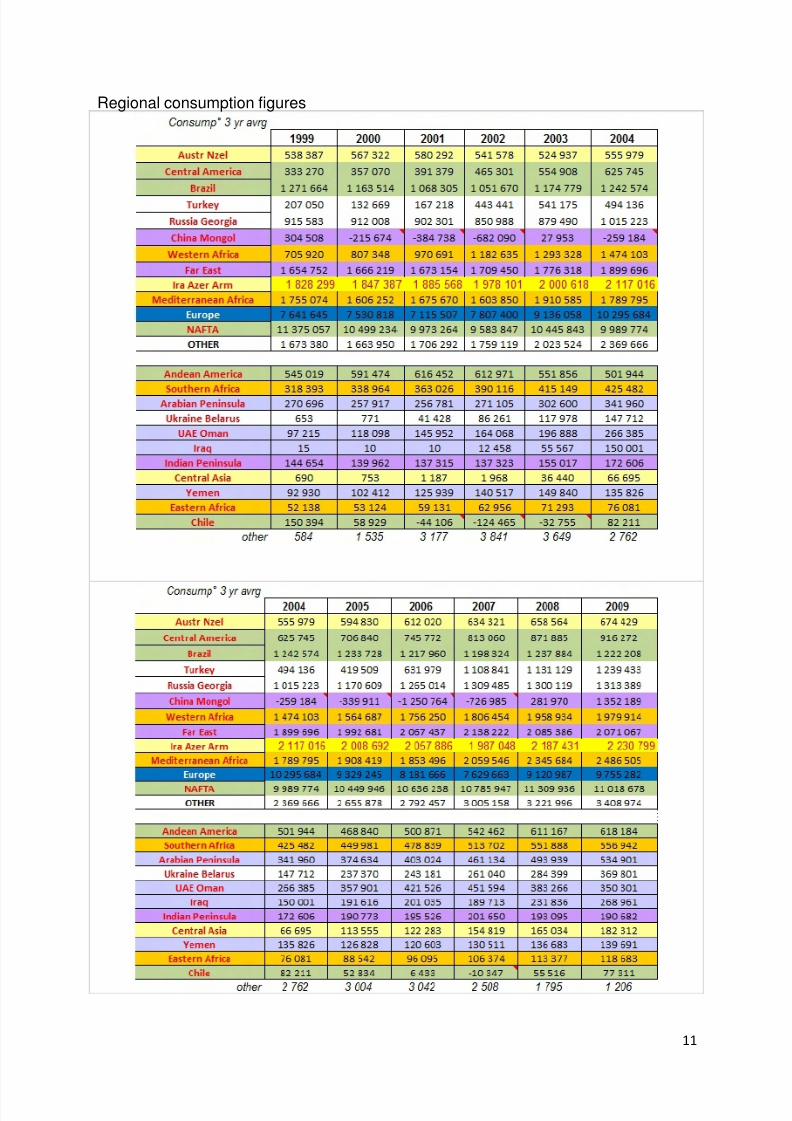

Regional consumption figures

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 12/39

12

The most marked increases are in the regions of Ukraine-Belarus, Iraq, Central Asiaand Turkey where growth for the period 2002/2009 has exceeded 20% and, in somecases, reached almost 50%. The Emirates regions as well as the neighbouringArabian Peninsula and Eastern Africa regions have all registered growth of between

10-15%, similar to Central America.In most cases worldwide, the main reason for this increase is the growth in per capitaconsumption as illustrated in the following diagram comparing regional consumptionbetween 2002 and 2009.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 13/39

13

4. Regional Consumption TrendsA certain number of geographical areas, particularly those which have reached amature level of consumption, only experience minimal variations in volumesconsumed annually. This is the case for North America and Brazil but also for the Far

East and Oceania which together accounted for more than 40% of globalconsumption in 2008.For the period 2002-2009 (chosen so as to have significant data for each of the 23regions studied), the consumption figures for all these regions all show positivegrowth rates of between 15% and 25% (corresponding to 2 to 3.5% annually).However, in 2009, there was a slight contraction and in some cases, even a decline,in regional consumption among certain leading zones such that:

• worldwide consumption continued to grow in 2008/2009 but the rate of growthwas much reduced;

• the increase in global consumptionreferred to above, was largely due to

“secondary regions” which displaytraditionally high growth rates. Despite aslowdown in 2008/2009, fast developingmarkets such as Ukraine, Turkey, theArabian Peninsula, the four Africanregions or Central America have shownpositive growth which has more thancompensated for the lack of growth indeveloped regions.

The following section is set out region by region in order of importance of variationsregistered from 2008 to 2009 from the most significant falls to the most markedincreases in consumption. The values correspond to three-year averages designed tocompensate for the stock effect which can accentuate or tone down certainvariations.

4.1. North AmericaFollowing a ‘trough’ from 1999 to2002, it appears that North

American consumption (USA,Canada and Mexico) has pickedup significantly over the period2003-2008. The figures from thisstudy which represent netconsumption (real volumesaccounted for in the territories inquestion excluding trade),indicate a marked slowdown inconsumption from 2008 to 2009,especially in the USA whereas

as those recorded in Canada and Mexico remain stable or even showing a slightincrease.

in metric Tonnes raw material equivalent

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 14/39

14

4.2. BrazilAs with the USA, the period inquestion starts with a reduction inper capita consumption which istranslated by a marked drop in

volumes accounted for at nationallevel (from 1.27 to 1.05 milliontonnes fresh equivalent). Theupturn in Brazilian consumptionseen in 2003 and 2004 hasrapidly levelled out at about 1.22million tonnes and has remainedvirtually unchanged for the lastfive years.

4.3. The Far EastConsumption in the Far East (Japan, Thailand, South Korea, the Philippines, etc.)has grown regularly from 1999 to 2007. After this date, a drop in per capita (andregional) consumption made itself felt and anticipating somewhat the global trend.

in metric Tonnes raw material equivalent

From this first group of three regions which have been hit by a decline inconsumption, we can add the United Arab Emirates region and Oman as well as the

Indian Subcontinent. The fall is quite marked as concerns the former but only justsignificant for the latter.

The following regions all display gains in consumption from 2008 to 2009 althoughonly those with the most conclusive growth rates are commented on here given thatthe regions of Russia-Georgia, Australia-New Zealand, Western Africa and Iran-Azerbaijan have registered relatively modest growth rates of 1% to 2% (totalling lessthan 100,000 tonnes fresh equivalent) resulting in overall consumption for the fourregions of just over 6.1 million tonnes.

in metric Tonnes raw material equivalent

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 15/39

15

4.4. Central AmericaCentral America is ranked 11th amongst the world’s leadingconsumer regions of tomatoproducts. While it may be thesmallest of the four mostsignificant regions referred to

here, it nevertheless displaysquite respectable levels ofconsumption (more than 900,000tonnes fresh equivalent in 2009).Above all, it has recorded a rateof growth over the decade asexemplary as it is spectacular representing an annual average growth rate for thisgroup of countries of around 17%. This lead to increased overall consumption ofsome 330,000 tonnes to nearly 920,000 tonnes fresh equivalent.

4.5. Mediterranean AfricaAlthough far removed culturallyfrom other regions displayingsimilar trends such as NAFTAand Brazil, North (orMediterranean), Africaexperienced a small reductionin volumes consumed at aregional level between 1999and 2002. After a ratherhesitant rise from 2003 to 2006,

consumption really took off from2007. The overall gain from1.75 million tonnes to 2.5 million

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 16/39

16

tonnes (fresh equivalent) for the whole period is impressive giving MediterraneanAfrica an annual average growth figure of more than 4%.

4.6. EuropeThe significant fluctuations

seen on the European chartare more a reflection ofinaccuracies concerning lack ofawareness of stocks than thereality of consumption trends.As is the case for strongexporting regions or countriessuch as China, Chile, Portugal,etc., the lack of quantifiedstock data strongly alters theoutputs and makes them very

difficult to express.Conversely, data from early2010 taken from the study onconsumption which focusesspecifically on the EU takesaccount of available stocks. Ithighlights near steady growthmarked only by a slowdownbetween 2004 and 2006 andthen a significant increase involumes consumed in Europebetween 2007 and 2009.

4.7. TurkeyFrom 1999 to 2001, domesticconsumption in Turkey wasrelatively weak (less than200,000 tonnes) but then

experienced quite suddenchange between 2002 and2005 which made it rise to540,000 tonnes and then fallback to around 420,000tonnes fresh equivalent. From2006 and 2007 onwards,there was a real explosion inTurkish per capitaconsumption which enabledthe Turkish processing

industry to compensate forlosses in exports.

(corrected for stock variations)

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 17/39

17

4.8. Other regions

in metric Tonnes raw material equivalent The other regions (Andean America and Chile, Southern Africa, the ArabianPeninsula, Ukraine and Belarus, the UAE and Oman, Iraq, the Indian Subcontinent,Central Asia and Eastern Africa), constitute a group in which has experiencedspectacular growth in overall consumption between 2002 and 2009, from 1.7 milliontonnes to 3.4 million tonnes. This doubling in growth does however hide some starkcontrasts between different elements.

In most cases, consumption of tomato products has followed a more or lessconsistent growth trend. In the countries of the Arabian Peninsula, Southern and

Eastern Africa which already showed a certain level of consumption, the last decadehas resulted in unrestrained growth of 100% to 200%. For the remainder (Iraq,Ukraine and Belarus, Central Asia), we can refer to the creation of markets fromalmost nothing which are now demonstrating tremendous growth. In the space of 10years, regional consumption has reached levels identical to, or in some casesexceeding, those of established mature markets (370,000 tonnes fresh equivalent inUkraine and Belarus in 2009, 270,000 tonnes in Iraq and 180,000 tonnes in CentralAsia).

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 18/39

18

in metric Tonnes raw material equivalent

For the last four countries in this group, the trends have been more hesitant andended in quite mixed figures for 2009:

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 19/39

19

The rises and falls succeed each otherin Andean America hitting a troughbetween 2004 and 2006. In the end,the region shows a modest gain 70,000tonnes for the decade (+1.3%) which is

more down to demographic growththan per capita consumption whichrose from 6.9kg/person in 1999 to7.0kg/person in 2009.

The growth in consumption between1999 and 2007 in the United ArabEmirates and in the Sultanate of Omancould have been among the highestrates of growth had it not been followedby just as spectacular a decline

between 2008 and 2009. Growth on thewhole is based upon very high percapita consumption.

The Indian Subcontinent shows veryweak consumption in comparison to itspopulation. Per capita consumption hasgrown more rapidly than the populationin such a way that the overall outcomeis positive, but modestly so (191,000tonnes in 2009 or 120g per person,according to our estimates).

In Yemen, considerable fluctuationshave influenced consumption over thelast 10 years. Initial growth, between1999 and 2003, was due to an increasein per capita consumption but is nowbased upon demographic growth. Thefigures for the last decade have beenpositive with an increase from 93,000

tonnes to 140,000 tonnes freshequivalent or 5.5kg to 6kg per personper year.

These 11 regions account for a little more than one third of the world’s population(stable at 36% for the decade). In 1999, they accounted for just 6% of worldwideconsumption. In the same time period during which 12 leading regions saw theiroverall consumption grow by around 3.6% per year, or 955,000 tonnes freshequivalent, these 11 regions have increased their demand by more than 10%(173,000 tonnes) each year and in 2009, they ‘weighed-in’ at more than 9% of

worldwide consumption.

in metric Tonnes raw material equivalent

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 20/39

20

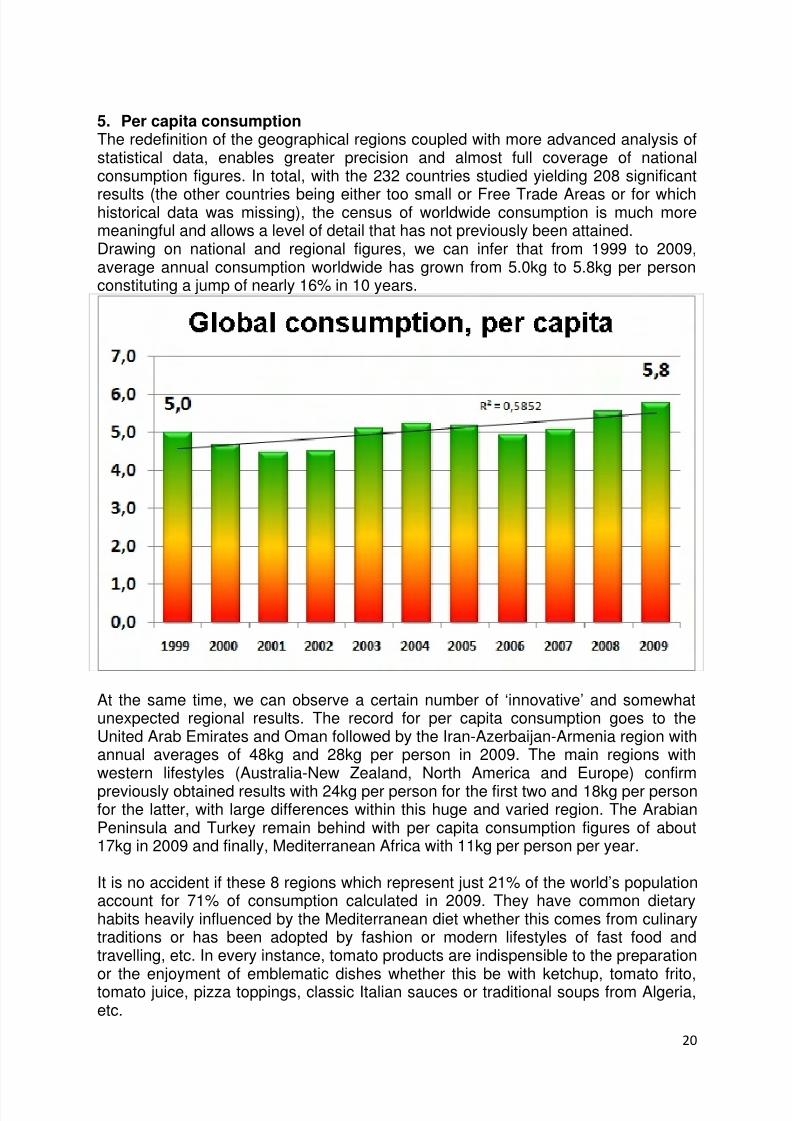

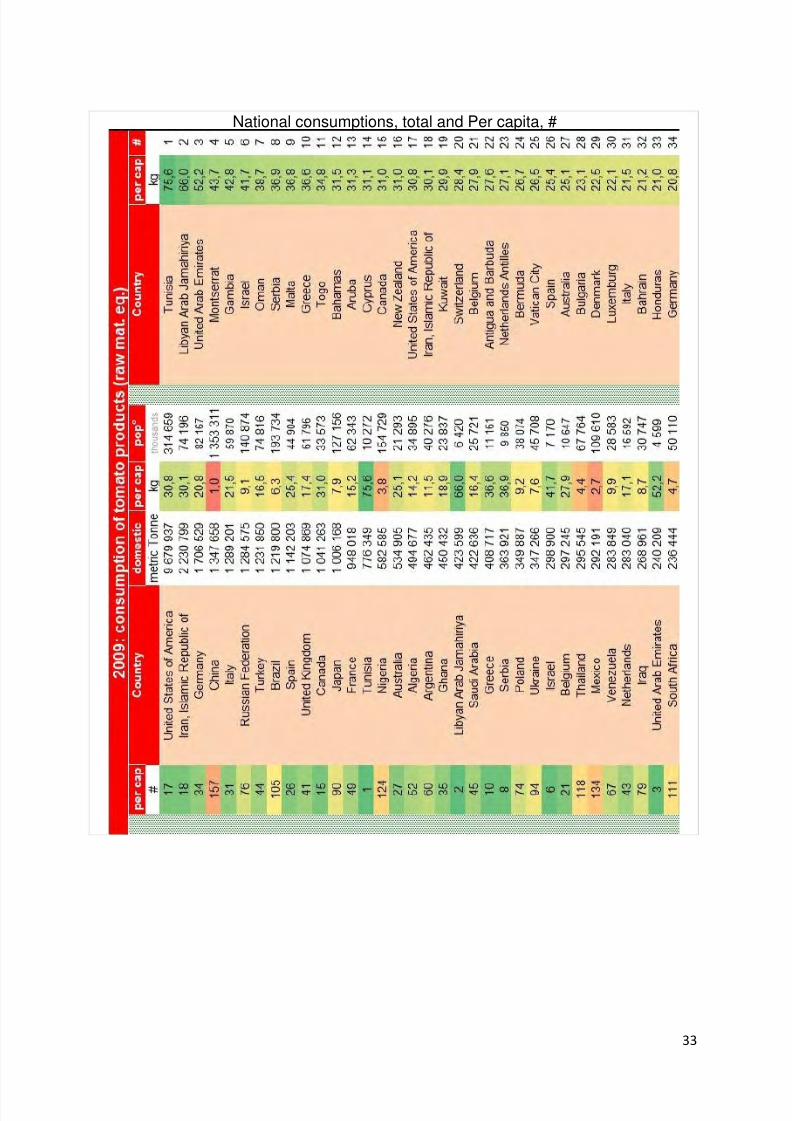

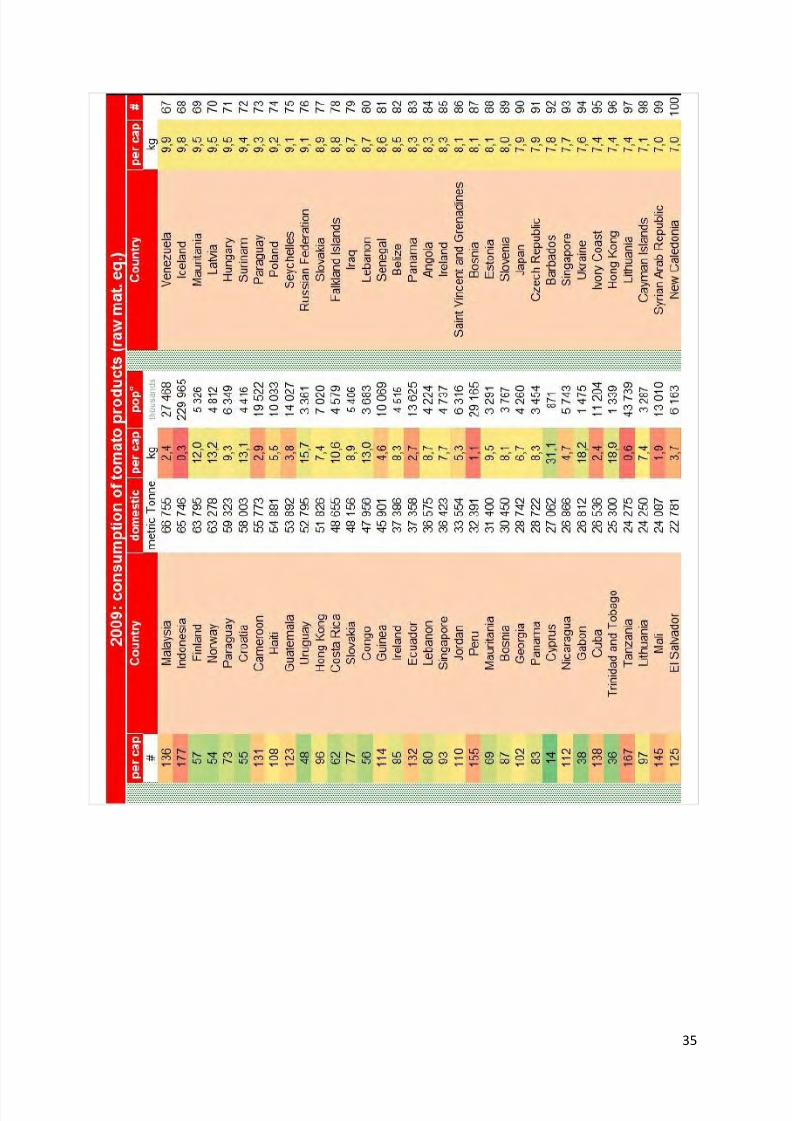

5. Per capita consumptionThe redefinition of the geographical regions coupled with more advanced analysis ofstatistical data, enables greater precision and almost full coverage of nationalconsumption figures. In total, with the 232 countries studied yielding 208 significant

results (the other countries being either too small or Free Trade Areas or for whichhistorical data was missing), the census of worldwide consumption is much moremeaningful and allows a level of detail that has not previously been attained.Drawing on national and regional figures, we can infer that from 1999 to 2009,average annual consumption worldwide has grown from 5.0kg to 5.8kg per personconstituting a jump of nearly 16% in 10 years.

At the same time, we can observe a certain number of ‘innovative’ and somewhatunexpected regional results. The record for per capita consumption goes to theUnited Arab Emirates and Oman followed by the Iran-Azerbaijan-Armenia region withannual averages of 48kg and 28kg per person in 2009. The main regions withwestern lifestyles (Australia-New Zealand, North America and Europe) confirm

previously obtained results with 24kg per person for the first two and 18kg per personfor the latter, with large differences within this huge and varied region. The ArabianPeninsula and Turkey remain behind with per capita consumption figures of about17kg in 2009 and finally, Mediterranean Africa with 11kg per person per year.

It is no accident if these 8 regions which represent just 21% of the world’s populationaccount for 71% of consumption calculated in 2009. They have common dietaryhabits heavily influenced by the Mediterranean diet whether this comes from culinarytraditions or has been adopted by fashion or modern lifestyles of fast food andtravelling, etc. In every instance, tomato products are indispensible to the preparation

or the enjoyment of emblematic dishes whether this be with ketchup, tomato frito,tomato juice, pizza toppings, classic Italian sauces or traditional soups from Algeria,etc.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 21/39

21

Average per capita consumption: Quantified figures

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 22/39

22

6. Areas for potential developmentAs we have already mentioned, it is rather the levels of individual consumption thatprovide a truer reflection of the real trends for growth than the volumes consumed forall the geographical areas studied.

There is clearly no direct link between the level of population and volumesconsumed. Densely populated regions with low consumption like the IndianSubcontinent and China effectively constitute markets full of development potentialbut only due to the high number of inhabitants in these regions.The events of 2009 were marked by a slight dip in areas of high consumption andtherefore consideration for growth of countries of medium-level consumption seemscredible. In fact, it appears more reasonable to bank on development within regionsthat already display a ‘habit’ for tomato products in their culinary traditions rather thanex nihilo growth. Thus, we can identify the Indian Subcontinent, Central Asia, Chinaand the Far East as well as Eastern and Southern Africa and Central America.Although densely populated with 66% of the world’s population, these areas

represent just 12% of global consumption. According to estimates, the average percapita volumes consumed in this group have only increased by 470g over the lastdecade.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 23/39

23

Conversely, North Africa, Western Africa, Russia, Iraq and the Ukraine or evenAndean America and Brazil appear to be more logical areas for growth potential.These regions are less populous and represent just 16% of the world’s population buttogether they account for nearly 21% of global consumption. In addition, averageconsumption per capita grew by 2.2kg fresh equivalent from 1999 to 2009,

unquestionable proof of the existence of a real growth trend in consumption.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 24/39

24

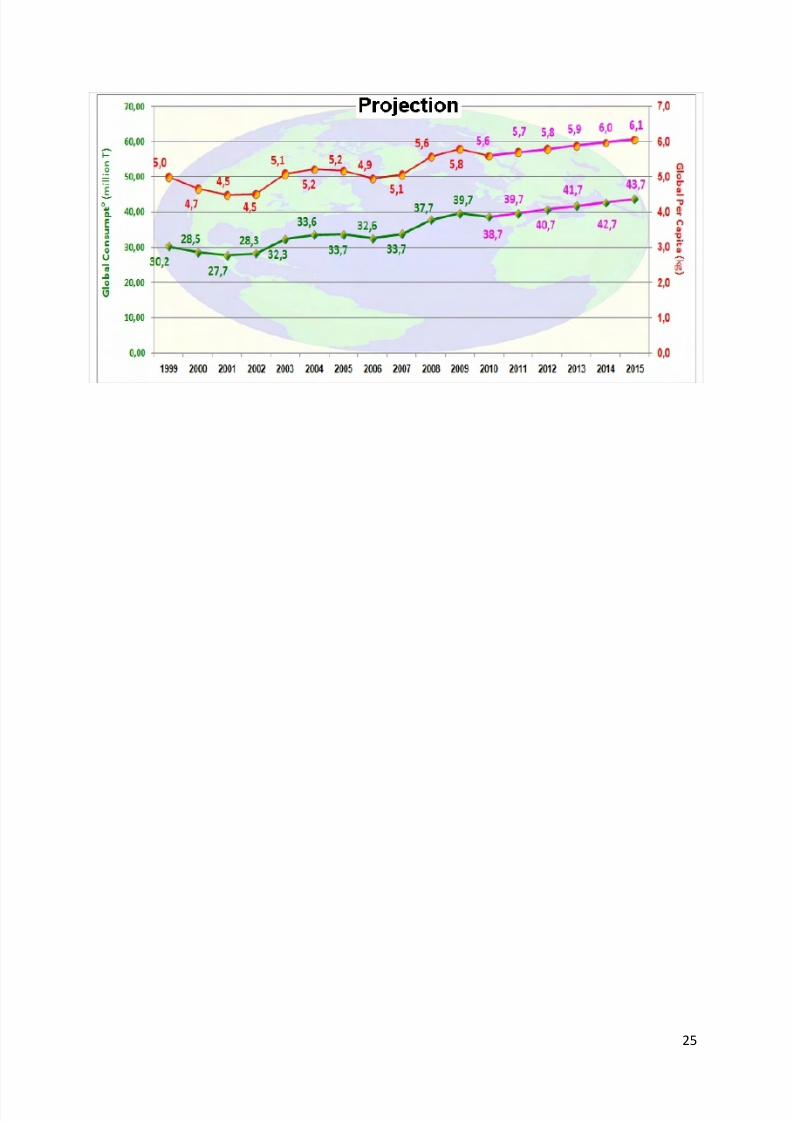

7. Summary and projections for growthTo sum up the quantified figures from this 2010 census on worldwide consumption,we can note that global consumption has increased from 30 million tonnes to 40million tonnes in 11 years mainly due to an increase in per capita consumption which

grew from 5.0kg/year to 5.8kg/year for the same period.

In terms of growth, the annual rise in worldwide consumption is about 3.0% while percapita consumption is rising between 1.9% and 2%. These ratios are slightly higherthan our previous estimates meaning that we should now count on an annual growthrate in consumption volumes of around 1.1 to 1.2 million tonnes per year comparedto previous growth projections of 1 million tonnes per year at the end of the 1990’s.

It is difficult to know whether to give more weight to the hypothesis of a sharpincrease in demand or to an effect amplified by demographic growth. Thinkingconservatively, if the growth in volumes estimated to be consumed each yearworldwide is roughly linear; the individual consumption threshold of 6kg could be

exceeded by 2013/2014 whereas global consumption could pass the 44 million tonnemark by 2015/2016.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 25/39

25

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 26/39

26

8. Conclusion Global trade: there was a slight decrease in 2009 compared with 2008,especially regarding paste (-5% in volumes), but it doesn’t necessarily mean a dropin consumption. The question of whether this slowdown is linked to the recorded

increase in prices or to strategic/commercial parameters remains unanswered. Better geographical zoning method (23 regions) and larger number ofcountries studied (232 of yielding 208 significant results) means more reliable dataand better knowledge and understanding of global trends and outputs.Nevertheless, this also emphasizes the need for more data (see “other comment”)… Consumption versus Processing: global figures are up again in 2008 and2009, confirming previous trend; the census clearly identifies years ofoverproduction (‘99, ‘04) and years of shortages (‘08). Latest results clearlyshow a surplus in processed quantities with regard to consumption whichexplains the current situation in stocks and prices of tomato paste. Obviously two regions are leading and accounting for a large share of global

consumption, but their influence in total figures regularly decreases, while « other »areas are rapidly increasing. There are also “innovative” results regarding per capitaconsumption, with two unexpected leading regions (UAE-Oman, Iran Azerb), followedby Austr-NZ, NAFTA, EU) which consolidate their positions and importance. Thisdistribution also clearly demonstrates the importance of Western andMediterranean diets in global consuming habits. Global per capita consumption is steadily increasing. In most regions, the main driving force of growth is still the increase in per

capita consumption, more than population growth. There is no link between population numbers and consumption levels although

densely populated regions (Indian Subcontinent, China) obviously remainimportant areas for potential development.

This let us consider that development of consumption “ex nihilo” (particularly inthe previously mentioned regions) is less plausible than progress in establishedconsumer (even medium-level) regions.

Estimated annual growth, based on 11 year period: global c.3 %, per capita: 1.9 -2 %: this is slightly more than previous estimates, and may be indicating someacceleration?

Tomato products are globally « crisis proof », but… this latest censusindicates a slight slowdown in consumption in 2009 for developed marketslike NAFTA, Brazil, Far East, Australia-New Zealand (41 % of global

consumption in 2008), with the exception of Europe… while developingmarkets saw their consumption levels increase making up for the decreasein developed countries.

…Does this mean that future development and growth will be located in “medium-level consumption” areas rather than densely populated areas?

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 27/39

27

Other comment

Regarding the reliability of some results, it is obvious that, for some countries like

China, Chile or Portugal, where activity is mainly focused on exports, there is a realneed for more detailed information.

In these three specific cases, we often encounter negative consumption, mainlybecause of the lack of relevant stocks figures. This is an example of the direction inwhich we could improve the quality of such studies.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 28/39

28

Methodology

The aim of this fourth report on worldwide consumption (Melbourne 2004, Tunis2006, Toronto 2008, Sial Paris 2010) is to analyse global consumption and identify

trends over the past 10 years. This new report presents a total of 23 regions basedon the same zoning for the Trade Study published in June 2010 at Estoril whichtogether, comprise 208 countries with relevant data.

Using statistical information on imports and exports supplied by the Global TradeInformation Service (GTIS), and, where applicable, the production (WPTC figures)and the stocks of each category or subcategory of tomato product (pastes, cannedtomatoes, sauces and ketchup) were recorded for each country.

For partner countries (i.e. those figuring in the list of destination countries for exportsbut not retained by the GTIS as data declaring countries, see annex), the volumes

imported have been pieced together from figures supplied by all exporting countries.The differences observed between exports and imports in previous studies have nowbeen reduced almost to 0. For example, the coherence between imports and exportsover the last ten years being 98.2% for pastes, 99.7% for canned tomatoes and92.3% for sauces and ketchup.

For each country, available customs information, processing coefficient data from theWPTC and AMITOM or the analysis of industrial activity among the main players inglobal trade (yearly profiles of fresh tomato equivalent exports) enables us tocalculate the equivalence in terms of volume of raw materials, either shipped in theform of processed goods or expressed in terms of production and stocks (whereapplicable).

The balance of trade has been identified for each country in fresh tomato equivalent(i.e., exports – imports). For each year, apparent domestic consumption in eachcategory has been calculated according to the formula:Apparent consumption = Initial stock + production – balance – final stock

The sum of these national figures allows the apparent consumption for each region tobe identified. Using population figures supplied by the FAO, apparent individualconsumption figures (in kg per capita) can be identified by dividing regional or

national consumption figures.

The collated regional figures provide a way to chart the evolution of worldwideconsumption for the ten year period in question (census).In order to validate the coherence of these results, the values obtained are comparedwith annual production figures supplied by the WPTC. In this way, the volumesprocessed are used directly in their annual form whilst the values for consumption areaveraged over three years so as to take account of any discrepancies and lack ofdetail in stocks.

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 29/39

29

Appendices

in metric Tonnes raw material equivalent

in metric Tonnes raw material equivalent

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 30/39

30

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 31/39

31

Zoning list

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 32/39

32

Regional Population

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 33/39

33

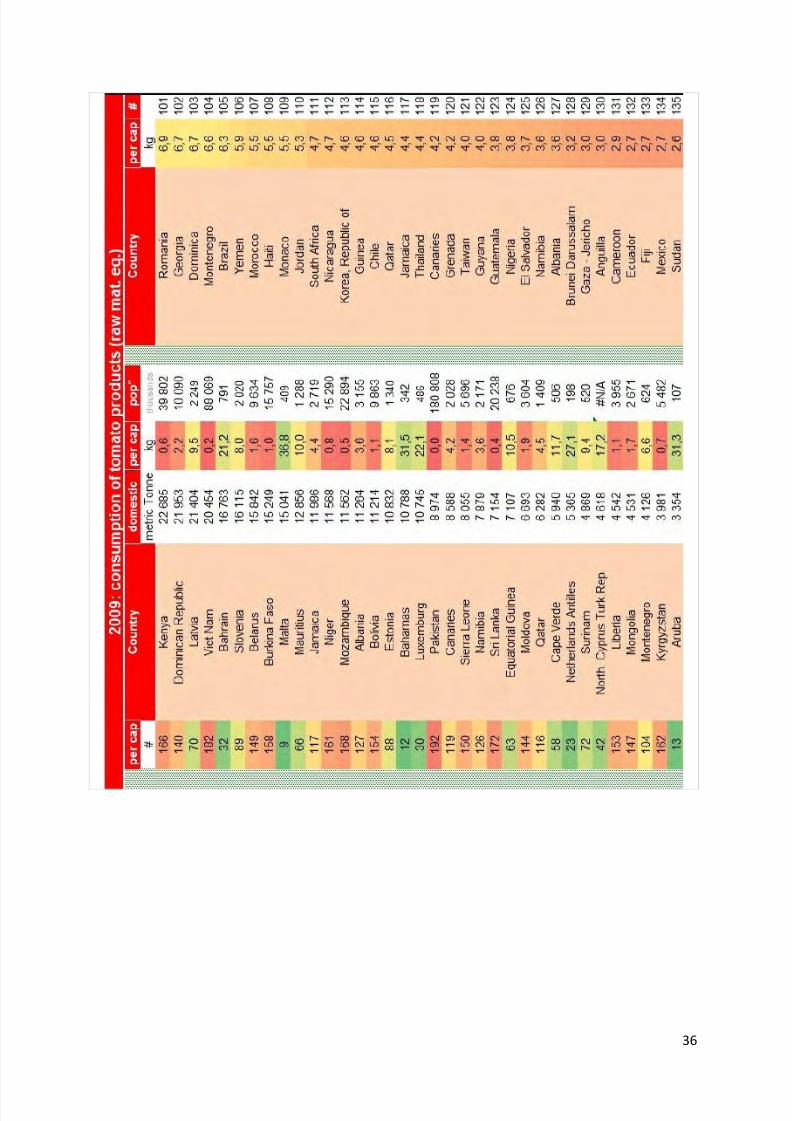

National consumptions, total and Per capita, #

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 34/39

34

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 35/39

35

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 36/39

36

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 37/39

37

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 38/39

38

8/8/2019 Wptc 2010 Consumption Report 12-10-2010

http://slidepdf.com/reader/full/wptc-2010-consumption-report-12-10-2010 39/39

List of 24 countries for which results are considered as unsignificant