wrongful debt collection consumer transactions dr. steiner

Post on 19-Dec-2015

219 views

TRANSCRIPT

Wrongful Debt Collection

Consumer Transactions

Dr. Steiner

Debt Collection and the Texas Bar Exam

BLE: Topics tested on Consumer Law“Texas and Federal debt collection acts: Federal Fair Debt Collection Practices Act and Texas Debt Collection Practices Act”

Past Exams Texas Debt Collection Practices Act was tested

on Feb. 2002, July 2002, Feb. 2004, July 2005 bar exams

July 2005 Call of the Question:Debt Collection 1. What conduct or actions, if any, of

NCC and/or Capital were violations of the Texas Debt Collection Practices Act? Explain fully.

2. What remedies, if any, are available to Dan under the Texas Debt Collection Practices Act and the Texas Deceptive Trade Practices Act? Explain fully.

Feb. 2004 Call of the Question:Debt Collection

What rights and civil remedies, if any, does Carlos have under the Texas Debt Collection Act and the Texas Deceptive Trade Practices Act

1. Against Bank? Explain fully. 2. Against Law Firm? Explain fully.

Web Resources: FTC Formal Actions

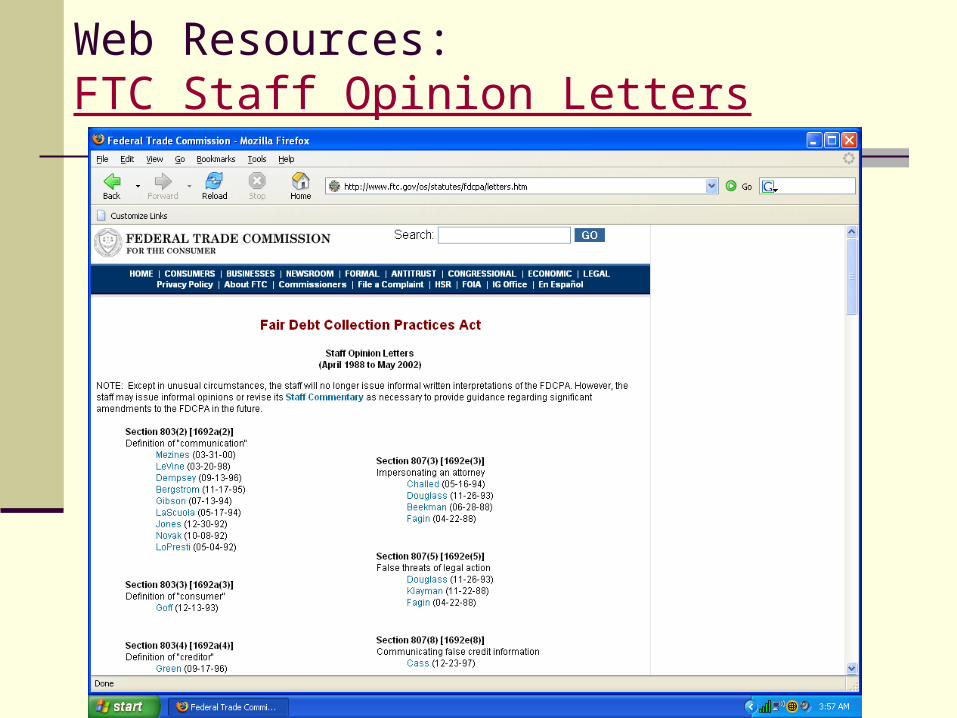

Web Resources:FTC Staff Opinion Letters

Web Resources:FTC Staff Commentary on FDCPA

Web Resources:National Consumer Law Center

Duty v. General Finance Co.

Whether debtors have right to recover damages for mental anguish and physical injury willfully and wantonly inflicted upon them by wrongful conduct by creditors attempting to collect debt

Did these debt collectors love their work or what?

Texas Debt Collection Practices Act

Originally enacted in 1973 Proscribes certain “debt collection methods” Civil remedies include injunctive relief, actual

damages, and attorneys fees Violations of Debt Collection Act are

violations of DTPA

FDCA: 15 U.S.C. § 1692 (1977):Congressional Findings

(a) Abusive practices There is abundant evidence of the use of abusive, deceptive, and unfair debt collection practices by many debt collectors. Abusive debt collection practices contribute to the number of personal bankruptcies, to marital instability, to the loss of jobs, and to invasions of individual privacy.

(b) Inadequacy of laws Existing laws and procedures for redressing these injuries are inadequate to protect consumers.

15 U.S.C. § 1692:Congressional Findings

(c) Available non-abusive collection methods Means other than misrepresentation or other abusive debt collection practices are available for the effective collection of debts.

(d) Interstate commerce Abusive debt collection practices are carried on to a substantial extent in interstate commerce and through means and instrumentalities of such commerce. Even where abusive debt collection practices are purely intrastate in character, they nevertheless directly affect interstate commerce.

Relation of FDCPA to state law: 15 USC § 1692n

This title does not annul, alter, or affect, or exempt any person subject to the provisions of this title from complying with the laws of any State with respect to debt collection practices, except to the extent that those laws are inconsistent with any provision of this title, and then only to the extent of the inconsistency. For purposes of this section, a State law is not inconsistent with this title if the protection such law affords any consumer is greater than the protection provided by this title.

Defining “debt collector”15 U.S.C. § 1692a(6)

The term “debt collector” means any person who uses any instrumentality of interstate commerce or the mails in any business the principal purpose of which is the collection of any debts, or who regularly collects or attempts to collect, directly or indirectly, debts owed or due or asserted to be owed or due another. . . [T]he term includes any creditor who, in the process of collecting his own debts, uses any name other than his own which would indicate that a third person is collecting or attempting to collect such debts.

15 U.S.C. § 1692a(5)

The term does not include— (A) any officer or employee of a creditor while, in the name of the creditor, collecting debts for such creditor; (B) any person while acting as a debt collector for another person, both of whom are related by common ownership or affiliated by corporate control, if the person acting as a debt collector does so only for persons to whom it is so related or affiliated and if the principal business of such person is not the collection of debts; …

Tex. Fin. Code § 392.001(6)

“Debt collector” means a person who directly or indirectly engages in debt collection and includes a person who sells or offers to sell forms represented to be a collection system, device, or scheme intended to be used to collect consumer debts.

15 U.S.C. § 1692a(5)

The term “debt” means any obligation or alleged obligation of a consumer to pay money arising out of a transaction in which the money, property, insurance, or services which are the subject of the transaction are primarily for personal, family, or household purposes, whether or not such obligation has been reduced to judgment.

Miller v. McCalla, Raymar, and the rest

FDCPA coverage Determining whether debt was a consumer debt

or a business debt Statutory interpretation according to Posner

Heintz v. Jenkins

Whether term “debt collector” in FDCPA applies to lawyer who “regularly” through litigation tries to collect consumer debt

Statutory definition of “debt collector” Why does court conclude attorneys may be

“debt collectors”? Implied exemption?

15 U.S.C. § 1692e:False or misleading representations

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

(3) The false representation or implication that any individual is an attorney or that any communication is from an attorney.

Volume debt collection practices and letters “from an attorney”

If law firm handled 55,000 new cases a month, mailing over 110,000 letters, received only limited information, reviewed collection files with such speed that no independent judgment could be found, and then issued form collection letters with the click of a mouse, a reasonable jury could conclude that the law firm lacked sufficient professional involvement with plaintiff’s file that the letters could be said to be “from an attorney” Miller v. Wolpoff & Abramson (2d Cir. 2003)

Tex. Fin. Code § 392.001

(7) “Third-party debt collector” means a debt collector, as defined by 15 U.S.C. Section 1692a(6), but does not include an attorney collecting a debt as an attorney on behalf of and in the name of a client unless the attorney has nonattorney employees who:(A) are regularly engaged to solicit debts for collection; or(B) regularly make contact with debtors for the purpose of collection or adjustment of debts.

Goldstein v. Hutton, Ingram, Yusek, Gainen, Carroll & Bertolotti Is a law firm “regularly” engaging in debt

collection when it had derived only $5000 in revenues (.05% of its $10 million annual revenue) from sending 145 “three-day notices” over the preceding year?

Predicates for “debt collector” status Principal purpose Regularly engaging

Goldstein v. Hutton, Ingram, Yusek, Gainen, Carroll & Bertolotti

(1) the absolute number of debt collection communications issued, and/or collection-related litigation matters pursued, over the relevant period(s),

(2) the frequency of such communications and/or litigation activity, including whether any patterns of such activity are discernable,

(3) whether the entity has personnel specifically assigned to work on debt collection activity,

(4) whether the entity has systems or contractors in place to facilitate such activity, and

(5) whether the activity is undertaken in connection with ongoing client relationships with entities that have retained the lawyer or firm to assist in the collection of outstanding consumer debt obligations.

Romine v. Diversified Collection

Statutory definition of “debt collector” Western Union’s AVT (Automated Voice

Telegram) service Do Western Union’s activities taken together,

amount to a direct or indirect attempt to collect a debt?

15 U.S.C. § 1692a(6)

The term “debt collector” means any person who uses any instrumentality of interstate commerce or the mails in any business the principal purpose of which is the collection of any debts, or who regularly collects or attempts to collect, directly or indirectly, debts owed or due or asserted to be owed or due another.

Zimmerman v. HBO Affiliate Group

Whether cable television companies, by demanding money to settle claims against cable thieves, were seeking to collect a “debt”?

Three problems with plaintiff’s argument

15 U.S.C. § 1692a(5)

The term “debt” means any obligation or alleged obligation of a consumer to pay money arising out of a transaction in which the money, property, insurance, or services which are the subject of the transaction are primarily for personal, family, or household purposes, whether or not such obligation has been reduced to judgment.

Defining Debt

15 U.S.C. § 1692a(5) The term “debt” means any

obligation or alleged obligation of a consumer to pay money arising out of a transaction in which the money, property, insurance, or services which are the subject of the transaction are primarily for personal, family, or household purposes, whether or not such obligation has been reduced to judgment.

Tex. Fin. Code § 392.001. “Consumer debt” means

an obligation, or an alleged obligation, primarily for personal, family, or household purposes and arising from a transaction or alleged transaction.

Bass v. Stolper, Koritzinsky, Brewster & Neider, S.C. Whether transactions under FDCPA’s are

limited to those involving the offer or extension of credit

Court’s stance toward Zimmerman Statutory interpretation

15 U.S.C. § 1692a(5)

The term “debt” means any obligation or alleged obligation of a consumer to pay money arising out of a transaction in which the money, property, insurance, or services which are the subject of the transaction are primarily for personal, family, or household purposes, whether or not such obligation has been reduced to judgment.

Collection of Bad Checks and FDCPA Every circuit court that has addressed this issue has

sided with the Seventh Circuit: Broadnax v. Greene Credit Serv., 106 F.3d 400 (6th

Cir. 1997) Snow v. Jesse L. Riddle, P.C., 143 F.3d 1350 (10th

Cir. 1998) Charles v. Lundgren & Assoc., P.C., 119 F.3d 739 (9th

Cir. 1997) Following the definition of “debt” in Zimmerman,

district courts in the Third Circuit have held that the FDCPA doesn’t apply to the collection of bad checks. See, e.g., Krevsky v. Equifax Check Serv., Inc., 85 F.Supp.2d 479 (M.D. Pa. 2000)

Tex. Gov’t Code § 311.023.Statute Construction Aids

In construing a statute, whether or not the statute is considered ambiguous on its face, a court may consider among other matters the: (1) object sought to be attained; (2) circumstances under which the statute was

enacted; (3) legislative history; (4) common law or former statutory provisions,

including laws on the same or similar subjects;

Tex. Gov’t Code § 311.023.Statute Construction Aids

(5) consequences of a particular construction; (6) administrative construction of the statute; and (7) title (caption), preamble, and emergency

provision.

Validation Notice:15 U.S.C. § 1692g Within five days after the initial

communication with a consumer in connection with the collection of any debt, a debt collector shall, unless the following information is contained in the initial communication or the consumer has paid the debt, send the consumer a written notice containing

Validation Notice:15 U.S.C. § 1692g (1) the amount of the debt; (2) the name of the creditor to whom the

debt is owed; (3) a statement that unless the

consumer, within thirty days after receipt of the notice, disputes the validity of all or part of the debt, the debt will be assumed to be valid by the debt collector;

Validation Notice:15 U.S.C. § 1692g

(4) a statement that if the consumer notifies the debt collector in writing within the thirty-day period that all or part of the debt is disputed, the debt collector will mail verification of the debt or a copy of a judgment to the consumer; and

(5) a statement that, upon the consumer's written request within the thirty-day period, the debt collector will provide the consumer with the name and address of the original creditor, if different from the current creditor.

Swanson v. Southern Oregon Credit Serv., Inc.

IF THIS ACCOUNT IS PAID WITHIN THE NEXT 10 DAYS IT WILL NOT BE RECORDED IN OUR MASTER FILE AS AN UNPAID COLLECTION ITEM. A GOOD CREDIT RATING–IS YOUR MOST VALUABLE ASSETUnless you, within thirty days after receipt of the notice, dispute the validity of all or part of the debt, the debt will be assumed to be valid by us. If you notify us in writing within the thirty-day period that all or part of the debt is disputed, we will mail verification of the debt or a copy of a judgment to the consumer; and upon your written request within the thirty-day period, we will provide you with the name and address of the original creditor, if different from the current creditor.

Swanson:Least Sophisticated Debtor Standard

Was validation notice “overshadowed” by the rest of the letter?

Importance of “visual effect” Would least sophisticated

debtor likely be misled by the notice?

Warnings under 15 USC § 1692e

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section: (11) The failure to disclose in the initial written

communication with the consumer and, in addition, if the initial communication with the consumer is oral, in that initial oral communication, that the debt collector is attempting to collect a debt and that any information obtained will be used for that purpose, and the failure to disclose in subsequent communications that the communication is from a debt collector, except that this paragraph shall not apply to a formal pleading made in connection with a legal action.

Tex. Fin. Code § 392.304.

(a) Except as otherwise provided by this section, in debt collection or obtaining information concerning a consumer, a debt collector may not use a fraudulent, deceptive, or misleading representation that employs the following practices: (5) in the case of a third-party debt collector, failing to

disclose, except in a formal pleading made in connection with a legal action:

(A) that the communication is an attempt to collect a debt and that any information obtained will be used for that purpose, if the communication is the initial written or oral communication between the third-party debt collector and the debtor; or

(B) that the communication is from a debt collector, if the communication is a subsequent written or oral communication between the third-party debt collector and the debtor;

FDCPA Form Letter: Bartlett v. Heibel

Would the letter work in Texas?CPRC § 38.001. A person may recover reasonable attorney's fees from an individual or corporation, in addition to the amount of a valid claim and costs, if the claim is for:(1) rendered services;(2) performed labor;(3) furnished material; …(7) a sworn account; or(8) an oral or written contract.

FDCPA Form Letter: Bartlett v. Heibel

Would the letter work in Texas?CPRC § 38.002. To recover attorney's fees under this chapter: (1) the claimant must be represented by an

attorney; (2) the claimant must present the claim to the

opposing party or to a duly authorized agent of the opposing party; and

(3) payment for the just amount owed must not have been tendered before the expiration of the 30th day after the claim is presented.

Blum v. Fisher & Fisher :Unsophisticated Consumer Standard A consumer who is of

below average sophistication or intelligence or is uninformed, naïve, or trusting

Is standard “ratcheted” up or down to conform to reasonable perception of consumer standing in shoes of plaintiff?

Blum v. Fisher & Fisher

This foreclosure could result in the mortgage lender taking title to your property in approximately 7 months. During that time you may be allowed to stay in the house absolutely rent free. In addition, you have the right to save your house from foreclosure by either catching up your loan or by paying off the total mortgage debt through sale, refinancing or otherwise.

Gammon v. GC Serv. (7th Cir. 1994):Critique of “Least Sophisticated Consumer” Standard

It strikes us virtually impossible to analyze a debt collection letter based on the reasonable interpretations of the least sophisticated consumer. Literally, the least sophisticated consumer is not merely “below average,” he is the very last rung on the sophistication ladder. Stated another way, he is the single most unsophisticated consumer who exists. Even assuming that he would be willing to do so, such a consumer would likely not be able to read a collection notice with care (or at all), let alone interpret it in a reasonable fashion.

“Least Sophisticated” and “Unsophisticated”

Consumer Standards Least Sophisticated Consumer Standard

Swanson v. Southern Oregon Credit Serv., Inc., 869 F.2d 1222 (9th Cir.1989)

Wilson v. Quadramed Corp., 225 F.3d 350 (3rd Cir.2000) Savino v. Computer Credit Inc., 164 F.3d 81 (2nd Cir.1998) Jeter v. Credit Bureau, Inc., 760 F.2d 1168 (11th Cir.1985)

Unsophisticated Consumer Standard Gammon v. GC Services, 27 F.3d 1254 (7th Cir.1994) Duffy v. Landberg, 215 F.3d 871 (8th Cir. 2000)

Fifth Circuit: Peter v. GCServ. L.P., 310 F.3d 344 (5th Cir. 2002)We have explicitly avoided ruling on which of these standards, if either, we use. . . Because the difference between the standards is de minimis at most, we again opt not to choose between these standards.

Jenkins v. Union Corp.: First letter

Our client has requested that we contact you regarding your check which has been returned by the bank and payment refused. We realize this could be an oversight on your part and not willful disregard of an obligation. However, intentional payment with a dishonored check for goods or services can lead to serious consequences.

The amount due includes a service fee, which must also be paid. To avoid any possible misunderstanding, it is important you immediately make payment to or arrangements with [Jerry Montell Pontiac].

Jenkins v. Union Corp.: First letter to Jenkins

Transworld Systems, Inc. is a licensed collection agency and any information obtained from you will be used for the purpose of collecting this debt. All portions of this claim shall be assumed valid unless disputed within thirty days of receiving this notice. If disputed in writing, verification of the debt will be provided to you. If the original creditor is different from the above named creditor, the name and address of the original creditor will also be provided.

Jenkins v. Union Corp.: 2d common letter

IMPERATIVE--Grace period about to expire. Our client shows an unpaid account in the above stated amount appearing legally due and owing by you. This account has been referred to our agency and we are authorized to pursue collection. With offices nationwide, a number of alternatives are available to us to effect settlement. You may eliminate the possibility of additional trouble and make further communication unnecessary by contacting your creditor at once. Be sure to enclose this letter with your payment for proper identification.

Jenkins v. Union Corp.: Third letter to Jenkins

Above claim still due. Federally mandated dispute period will expire within 10 days. Unless we hear from you, at that time we will assume your debt to be legally due. Please be advised that there are two ways of settling a legitimate debt-- timely payment or as the result of protracted and unpleasant collection effort. At this time the choice is still yours. Make further effort on our part unnecessary by making payment to [Jerry Montell Pontiac].

Jenkins v. Union Corp.: First letter to Terrafino

URGENT--This account has been assigned to our agency for immediate collection. Please be advised that we have been authorized to pursue collection and are committed to make whatever efforts are necessary and proper to effect collection. Strongly recommend you contact our client to make payment arrangement.

Threats of Litigation:15 USC § 1692e(5) A debt collector may not use any false,

deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section: (5) The threat to take any action that cannot

legally be taken or that is not intended to be taken.

Jenkins v. Union Corp.: Third letter to Terrafino

As Collection Manager of Transworld Systems Inc., I thought it important to state our intentions regarding your debt. The economic feasibility of some type of litigation by our client has not been determined.

Jenkins v. Union Corp.: Third letter to Terrafino

However, please understand that if legal action were to be undertaken, it would be costly and time-consuming for both parties. The loser of such an action would probably be subject to court costs and/or attorney fees, if applicable. Should such court action occur, and should your creditor prevail, there would be available various avenues to satisfy a judgment. You may wish to check your state laws concerning these remedies.

Jenkins v. Union Corp.: Third letter to Terrafino

It is not my intention to threaten or alarm you about this matter but merely to point out the problems of refusing to pay what appears to be a just and legal debt. We would hope, however, that additional costly collection efforts not be necessary (sic) and that you demonstrate your willingness to resolve this matter by remitting the full amount due to [Glenoaks Medical Center].

Jenkins v. Union Corp.: Reverse side of form letters

COLORADO

If you refuse to voluntarily pay this debt, or you wish our agency to cease communication either written or oral at either your place of employment or residence, and you so advise Transworld Systems Inc. in writing, we will not communicate with you further ....

Jenkins v. Union Corp.: Court’s suggested revision

We are required under state law to notify consumers of the following rights. This list does not contain a complete list of the rights consumers have under state and federal law.

If you refuse to voluntarily pay this debt, or you wish our agency to cease communication either written or oral at either your place of employment or residence, and you so advise Transworld Systems Inc. in writing, we will not communicate with you further ....

Problem 25a. Calling a debtor at her place of employment

Federal § 1692c (a) Without the prior consent of the consumer

given directly to the debt collector or the express permission of a court of competent jurisdiction, a debt collector may not communicate with a consumer in connection with the collection of any debt—

(3) at the consumer’s place of employment if the debt collector knows or has reason to know that the consumer’s employer prohibits the consumer from receiving such communication.

Problem 25a. Calling a debtor at her place of employment

Texas § 392.302 In debt collection, a debt collector may not oppress,

harass, or abuse a person by: (2) placing telephone calls without disclosing the name of

the individual making the call and with the intent to annoy, harass, or threaten a person at the called number;

(3) causing a person to incur a long distance telephone toll, telegram fee, or other charge by a medium of communication without first disclosing the name of the person making the communication; or

(4) causing a telephone to ring repeatedly or continuously, or making repeated or continuous telephone calls, with the intent to harass a person at the called number.

Problem 25b. Calling a debtor’s mother and telling her that her son owes you money

Federal § 1692c. Except as provided in section 1692b [location

information], without the prior consent of the consumer given directly to the debt collector, or the express permission of a court of competent jurisdiction, or as reasonably necessary to effectuate a postjudgment judicial remedy, a debt collector may not communicate, in connection with the collection of any debt, with any person other than the consumer, his attorney, a consumer reporting agency if otherwise permitted by law, the creditor, the attorney of the creditor, or the attorney of the debt collector.

Problem 25c. Sending letter with debtor with return address that includes “Debt Collection Agency”

Federal § 1692f(8) Using any language or symbol, other than the

debt collector’s address, on any envelope when communicating with a consumer by use of the mails or by telegram, except that a debt collector may use his business name if such name does not indicate that he is in the debt collection business.

Problem 25d. Telling a debtor who’s current that his wages will be garnished if he becomes delinquent

Federal § 1692e(5) The threat to take any action that cannot legally

be taken or that is not intended to be taken. Federal § 1692f Texas § 392.301(a)(8).

(a) In debt collection, a debt collector may not use threats, coercion, or attempts to coerce that employ any of the following practices: . . .

(8) threatening to take an action prohibited by law.

Problem 25e. Immediately recalling debtor after debtor hangs up

Federal § 1692d(5) Causing a telephone to ring or engaging any

person in telephone conversation repeatedly or continuously with intent to annoy, abuse, or harass any person at the called number.

Problem 25e. Immediately recalling debtor after debtor hangs up

Texas § 392.302 In debt collection, a debt collector may not

oppress, harass, or abuse a person by: (4) causing a telephone to ring repeatedly or

continuously, or making repeated or continuous telephone calls, with the intent to harass a person at the called number.

Problem 25

F. Telling a debtor that unless immediate payment is made the debtor’s account will be reported to the credit bureau, impacting his credit rating Federal

Validation rights Threatens an action that can’t legally be taken. § 1692e(5)

Texas § 392.301. A debt collector may not use threats, coercion,

or attempts to coerce that employ any of the following practices:

(3) representing or threatening to represent to any person other than the consumer that a consumer is wilfully refusing to pay a nondisputed consumer debt when the debt is in dispute and the consumer has notified in writing the debt collector of the dispute;

Problem 25g. Telling a debtor “we work with the government; you must

surely know what problems you will face if you do not pay” Federal § 1692e

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

(1) The false representation or implication that the debt collector is vouched for, bonded by, or affiliated with the United States or any State, including the use of any badge, uniform, or facsimile thereof.

Problem 25g. Telling a debtor “we work with the government; you must

surely know what problems you will face if you do not pay” Texas § 392.304(a)(9)

(a) Except as otherwise provided by this section, in debt collection or obtaining information concerning a consumer, a debt collector may not use a fraudulent, deceptive, or misleading representation that employs the following practices:

(9) representing falsely that a debt collector is vouched for, bonded by, or affiliated with, or is an instrumentality, agent, or official of, this state or an agency of federal, state, or local government

Problem 25h. Attempting to collect a debt that collector is unaware it’s barred by the statute of limitations

Federal § 1692k(c) A debt collector may not be held liable in any

action brought under this subchapter if the debt collector shows by a preponderance of evidence that the violation was not intentional and resulted from a bona fide error notwithstanding the maintenance of procedures reasonably adapted to avoid any such error.

Problem 25h. Attempting to collect a debt that collector is unaware it’s barred by the statute of limitations

Texas § 392.401. A person does not violate this chapter if the

action complained of resulted from a bona fide error that occurred notwithstanding the use of reasonable procedures adopted to avoid the error.

Problem 25

Harassing debtor about an obligation arising out of small family-owned business

Problem 25J. Wrongful contact with debtor’s relative; can relative of debtor sue? Federal § 1692k. Civil liability

[A]ny debt collector who fails to comply with any provision of this subchapter with respect to any person is liable to such person in an amount equal to the sum of—

Most cases appear to allow any person harmed by collector’s actions, but West v. Costen says debtor’s mom couldn’t recover under FDCPA

Texas § 392.403. Civil Remedies (a) A person may sue for . . .

Problem 25J. Wrongful contact with debtor’s relative; can relative of debtor sue?

Federal § 1692d A debt collector may not engage in any conduct the

natural consequence of which is to harass, oppress, or abuse any person in connection with the collection of a debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section: (2) The use of obscene or profane language or language

the natural consequence of which is to abuse the hearer or reader.

(5) Causing a telephone to ring or engaging any person in telephone conversation repeatedly or continuously with intent to annoy, abuse, or harass any person at the called number.

Problem 25k. Stating that debt collector has convinced creditor to give you another chance when it’s automatic

Federal §1692e False or misleading misrepresentations

Texas § 392.304. (14) representing falsely the status or nature

of the services rendered by the debt collector or the debt collector's business;

Problem 25l. Sending letter with attorney’s signature when the attorney never reviewed file or had any input

Federal § 1692e. A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section: (3) The false representation or implication that

any individual is an attorney or that any communication is from an attorney.

Problem 25l. Sending letter with attorney’s signature when the attorney never reviewed file or had any input

Texas § 392.304. (a) Except as otherwise provided by this section, in debt collection or obtaining information concerning a consumer, a debt collector may not use a fraudulent, deceptive, or misleading representation that employs the following practices: (16) using a communication that purports to be

from an attorney or law firm if it is not; (17) representing that a consumer debt is

being collected by an attorney if it is not;

Problem 25m. Threatening to file for amount “plus interest” where

interest couldn’t be awarded Federal § 1692f A debt collector may not use unfair or unconscionable

means to collect or attempt to collect any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

(1) The collection of any amount (including any interest, fee, charge, or expense incidental to the principal obligation) unless such amount is expressly authorized by the agreement creating the debt or permitted by law.

Problem 25m. Threatening to file for amount “plus interest” where

interest couldn’t be awarded Federal § 1692e. A debt collector may not

use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section: (5) The threat to take any action that cannot

legally be taken or that is not intended to be taken.

Problem 25m. Threatening to file for amount “plus interest” where

interest couldn’t be awarded Texas §§ 392.303. (a) In debt collection, a debt collector may not

use unfair or unconscionable means that employ the following practices: . . . (2) collecting or attempting to collect interest

or a charge, fee, or expense incidental to the obligation unless the interest or incidental charge, fee, or expense is expressly authorized by the agreement creating the obligation or legally chargeable to the consumer;

Problem 25m. Threatening to file for amount “plus interest” where

interest couldn’t be awarded Texas § 392.304 (12) representing that a consumer debt may

be increased by the addition of attorney's fees, investigation fees, service fees, or other charges if a written contract or statute does not authorize the additional fees or charges;

Brown v. Oaklawn Bank

To what extent may a creditor use the threat of criminal prosecution to procure payment of a debt under Texas Debt Collection Act?

15 U.S.C. § 1692a(5)

The term [debt collector] does not include— (A) any officer or employee of a creditor while, in the name of the creditor, collecting debts for such creditor; (B) any person while acting as a debt collector for another person, both of whom are related by common ownership or affiliated by corporate control, if the person acting as a debt collector does so only for persons to whom it is so related or affiliated and if the principal business of such person is not the collection of debts; …

Tex. Fin. Code sec. 392.001(6)

(6) “Debt collector” means a person who directly or indirectly engages in debt collection and includes a person who sells or offers to sell forms represented to be a collection system, device, or scheme intended to be used to collect consumer debts.

Tex. Fin. Code § 392.301

(a) In debt collection, a debt collector may not use threats, coercion, or attempts to coerce that employ any of the following practices:… (2) accusing falsely or threatening to accuse

falsely a person of fraud or any other crime;…

(5) threatening that the debtor will be arrested for nonpayment of a consumer debt without proper court proceedings;

(6) threatening to file a charge, complaint, or criminal action against a debtor when the debtor has not violated a criminal law;

Tex. Fin. Code § 392.301

(b) Subsection (a) does not prevent a debt collector from: (1) informing a debtor that the debtor may be

arrested after proper court proceedings if the debtor has violated a criminal law of this state;

(2) threatening to institute civil lawsuits or other judicial proceedings to collect a consumer debt; or

(3) exercising or threatening to exercise a statutory or contractual right of seizure, repossession, or sale that does not require court proceedings.

Texas Disciplinary R. Prof. Conduct 4.04

Respect for Rights of Third Persons (a) In representing a client, a lawyer shall not

use means that have no substantial purpose other than to embarrass, delay, or burden a third person, or use methods of obtaining evidence that violate the legal rights of such a person.

(b) A lawyer shall not present, participate in presenting, or threaten to present: (1) criminal or disciplinary charges solely to gain

an advantage in a civil matter;

Romea v. Heiberger & Assoc.

Whether back rent is a debt Whether required state law three-day notice

for possessory action is a communication under FDCPA

Whether lawyers sending required state law notices are exempted from FDCPA

Shimek v. Forbes, 374 F.3d 1011 (11th Cir. 2004)(note case) Does filing a lien contemporaneously with

sending the demand letter (with 30-day validation notice) violate the FDCPA?

Does a debt collector violate the FDCPA by failing to prevent the recording of the lien after the consumer has requested verification?

Shorty v. Capital One Bank

§1692e(2)(A) prohibits “false representation” of the “character, amount, or legal status of any debt”

Does a debt collector violate §1692e(2)(A) by sending an otherwise legally sufficient debt validation notice without notifying the debtor that the debt is time-barred?

Randolph v. IMBS, Inc.

Relationship between automatic stay provision of bankruptcy law and FDCPA Is bankruptcy the only recourse against post-

bankruptcy debt-collection efforts? Does the Bankruptcy Code implicitly repeal

the FDCPA in a post-bankruptcy debt collection?

Problem 26 (Feb. 2004 Exam)

What rights and civil remedies, if any, does Carlos have under the Texas Debt Collection Act and the Texas Deceptive Trade Practices Act Against Bank? Explain fully. Against Law Firm? Explain fully.

Problem 26 Bank

Bank as debt collector under Texas Debt Collection Act

Bank’s violations of Texas Debt Collection Act Tie-in statute? Consumer standing under DTPA DTPA violations

Problem 26 Bank

Bank as debt collector under FDCPA § 1692a(6) defines “debt collector”

Assuming debt collector status, did Bank violate FDCPA? § 1692e(4) The representation or implication

that nonpayment of any debt will result in the arrest or imprisonment of any person or the seizure, garnishment, attachment, or sale of any property or wages of any person unless such action is lawful and the debt collector or creditor intends to take such action.

Problem 26 Law Firm

Law firm as debt collector under Texas Debt Collection Act

Violations of Texas Debt Collection Act Tie-in statute Consumer standing under DTPA Professional services exemption and DTPA DTPA violations

Problem 26 Remedies

Damages under Texas Debt Collection Act Damages if tie-in Damages under DTPA Damages under FDCPA

Then article 5069-11.10

(a) Any person may seek injunctive relief to prevent or restrain a violation of this Act and any person may maintain an action for actual damages sustained as a result of a violation of this Act.

(c) A person who successfully maintains an action under this article shall be awarded at least $100 for each violation of this Act.

Elston v. Resolution Serv., Inc.

Is proof of actual damages necessary to successfully maintain a suit for violations of Texas Debt Collection Act?

Does the $100 minimum award provide an independent cause of action?

current Tex. Fin. Code § 392.403

(a) A person may sue for: (1) injunctive relief to prevent or restrain a

violation of this chapter; and (2) actual damages sustained as a result of a

violation of this chapter. (e) A person who successfully maintains an action

under this section for violation of Section 392.101[bond requirement], 392.202[correction of files], or 392.301(a)(3)[threatening to represent that the consumer is refusing to pay nondisputed debt when it’s disputed] is entitled to not less than $100 for each violation of this chapter.

Damages under Texas Debt Collection Act: GreenPoint Credit GreenPoint Credit Corp. v. Perez, 75 S.W. 3d

40 (Tex. App.—San Antonio 2002) Five-million-dollar award for actual damages

upheld. “The compensatory damage issue was asked in the broad form, with the elements of physical pain, mental anguish, medical care and disfigurement listed.”

“This unfair debt collections act case involves an illegal threat by a finance company to put an elderly woman in jail for a debt that she did not owe, on a mobile home she did not own.”

Damages under Texas Debt Collection Act: GreenPoint Credit GreenPoint began calling Mrs. Perez and insisting the

owed money on a mobile home. During the second call, the GreenPoint representative was rude, used obscene language, and threatened if she did not send in a payment that day, a sheriff's deputy was going to come and put her in jail that afternoon, at 2 p.m. “This about did Mrs. Perez in.” Her daughter found her later distraught and crying; she insisted on surrendering to the sheriff because she was going to be put in jail, and apparently was ready to turn herself in. The Sheriff called GreenPoint himself and told them that they had the wrong person. “He informed GreenPoint that Mrs. Perez owned no mobile home and that Mrs. Perez's signature did not match the one on the document. The Sheriff's words also fell on deaf ears.”

Damages under Texas Debt Collection Act: GreenPoint Credit

Approximately two weeks later, GreenPoint sent a field representative to Mrs. Perez's home to investigate the case. The representative completed a Field Contact Form in which he stated that Mrs. Perez continued to deny having signed any contract and that Mrs. Perez provided him with an ID and a social security card. The representative also obtained a handwritten affidavit from Mrs. Perez, signed and notarized, in which she swore that she had never signed any documents for the purchase of a mobile home, and never consented for anyone else to provide her personal information for such. Despite the evidence that they had the wrong person, GreenPoint sued anyway.

Damages under Texas Debt Collection Act: GreenPoint Credit

“This was an extraordinarily traumatic event for Mrs. Perez. Handicapped by advancing age, a demonstrated history of anxiety and nervousness, inability to understand the language, culturally insulated, and uneducated, she had few protection mechanisms available to counter the unexpected threats.”

“Physical evidence of Mrs. Perez's injuries were also before the jury. Graphic photographs of eruptions of her skin and disfiguring, angry running sores were evidence of the turmoil within. There was also evidence of heart palpitations, shortness of breath, nausea, sleeplessness, panic attacks, difficulty in concentrating, irritability, reclusiveness and elevated blood pressure which caused the doctor to prescribe various medications.”

Arbitration and Texas Debt Collection Act

Arbitration clause said “all disputes, claims, or controversies arising from or relating to this contract” were subject to arbitration. Texas Debt Collection Act claims were to be arbitrated. In re Conseco Fin. Serv. Corp., 19 S.W.3d 562

(Tex. App.—Waco 2000, orig. proceeding) (even the issue of the validity of the arbitration clause was to be arbitrated)

In re Conseco Fin. Serv. Corp., 2002 WL 413179 (Tex. App.—Beaumont 2002, orig. proceeding)

15 USC §1692k(a). Civil liability

Except as otherwise provided by this section, any debt collector who fails to comply with any provision of this subchapter with respect to any person is liable to such person in an amount equal to the sum of— (1) any actual damage sustained by such

person as a result of such failure; (2)(A) in the case of any action by an

individual, such additional damages as the court may allow, but not exceeding $1,000

McHugh v. Check Investors, Inc.

FDCPA damages Actual damages Statutory damages Attorneys fees

State law claim Actual damages Punitive damages

Crain v. Unauthorized Practice of Law Committee

Defining the practice of law

Is preparing and filing mechanic’s liens or lien affidavits the unauthorized practice of law?

Tex. Fin. Code §392.301Threats or Coercion

(a) In debt collection, a debt collector may not use threats, coercion, or attempts to coerce that employ any of the following practices: (1) using or threatening to use violence or

other criminal means to cause harm to a person or property of a person;

(2) accusing falsely or threatening to accuse falsely a person of fraud or any other crime;

Tex. Fin. Code §392.301.Threats or Coercion

(3) representing or threatening to represent to any person other than the consumer that a consumer is wilfully refusing to pay a nondisputed consumer debt when the debt is in dispute and the consumer has notified in writing the debt collector of the dispute;

Tex. Fin. Code §392.301.Threats or Coercion

(4) threatening to sell or assign to another the obligation of the consumer and falsely representing that the result of the sale or assignment would be that the consumer would lose a defense to the consumer debt or would be subject to illegal collection attempts;

Tex. Fin. Code §392.301.Threats or Coercion

(5) threatening that the debtor will be arrested for nonpayment of a consumer debt without proper court proceedings;

(6) threatening to file a charge, complaint, or criminal action against a debtor when the debtor has not violated a criminal law;

Tex. Fin. Code §392.301.Threats or Coercion

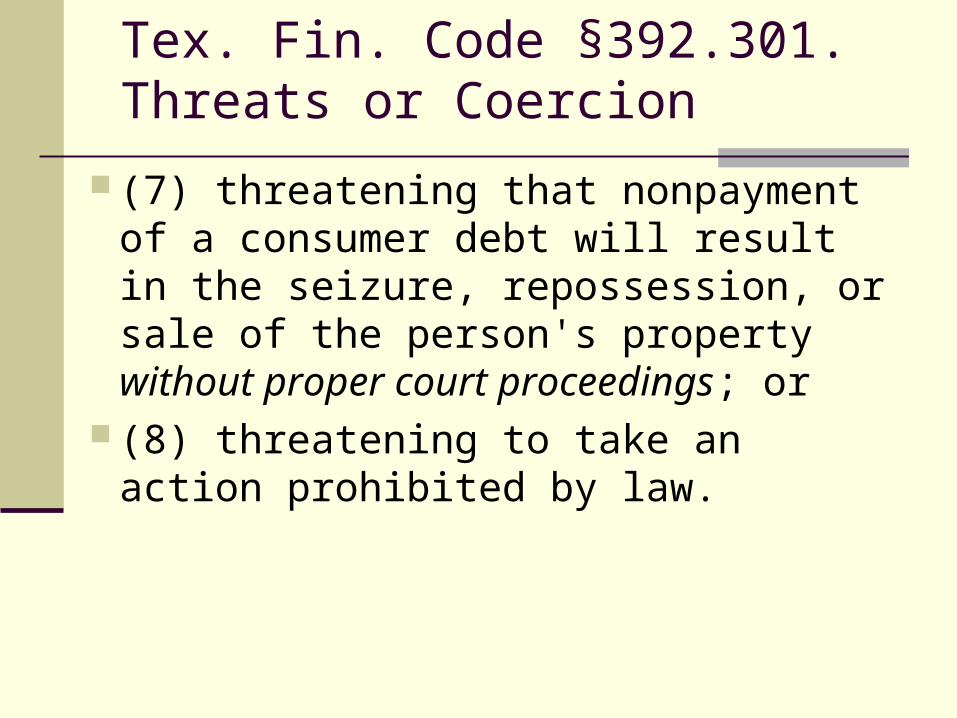

(7) threatening that nonpayment of a consumer debt will result in the seizure, repossession, or sale of the person's property without proper court proceedings; or

(8) threatening to take an action prohibited by law.

Tex. Fin. Code §392.301.Threats or Coercion

(b) Subsection (a) does not prevent a debt collector from: (1) informing a debtor that the debtor may be

arrested after proper court proceedings if the debtor has violated a criminal law of this state;

(2) threatening to institute civil lawsuits or other judicial proceedings to collect a consumer debt; or

(3) exercising or threatening to exercise a statutory or contractual right of seizure, repossession, or sale that does not require court proceedings.

Tex. Fin. Code §392.302 Harassment; Abuse In debt collection, a debt collector may not

oppress, harass, or abuse a person by: (1) using profane or obscene language or

language intended to abuse unreasonably the hearer or reader;

(2) placing telephone calls without disclosing the name of the individual making the call and with the intent to annoy, harass, or threaten a person at the called number;

Tex. Fin. Code §392.302 Harassment; Abuse

(3) causing a person to incur a long distance telephone toll, telegram fee, or other charge by a medium of communication without first disclosing the name of the person making the communication; or

(4) causing a telephone to ring repeatedly or continuously, or making repeated or continuous telephone calls, with the intent to harass a person at the called number.

§392.304. Fraudulent, Deceptive, or Misleading Representations

(a) Except as otherwise provided by this section, in debt collection or obtaining information concerning a consumer, a debt collector may not use a fraudulent, deceptive, or misleading representation that employs the following practices: (1) using a name other than the:

(A) true business or professional name or the true personal or legal name of the debt collector while engaged in debt collection; or

(B) name appearing on the face of the credit card while engaged in the collection of a credit card debt;

§392.304. Fraudulent, Deceptive, or Misleading Representations

(2) failing to maintain a list of all business or professional names known to be used or formerly used by persons collecting consumer debts or attempting to collect consumer debts for the debt collector;

(3) representing falsely that the debt collector has information or something of value for the consumer in order to solicit or discover information about the consumer;

§392.304. Fraudulent, Deceptive, or Misleading Representations

(4) failing to disclose clearly in any communication with the debtor the name of the person to whom the debt has been assigned or is owed when making a demand for money [doesn’t apply to a person servicing or collecting real property first lien mortgage loans or credit card debts];

§392.304. Fraudulent, Deceptive, or Misleading Representations

(5) in the case of a third-party debt collector, failing to disclose, except in a formal pleading made in connection with a legal action: (A) that the communication is an attempt to

collect a debt and that any information obtained will be used for that purpose, if the communication is the initial written or oral communication between the third-party debt collector and the debtor; or

§392.304. Fraudulent, Deceptive, or Misleading Representations

(B) that the communication is from a debt collector, if the communication is a subsequent written or oral communication between the third-party debt collector and the debtor;

§392.304. Fraudulent, Deceptive, or Misleading Representations

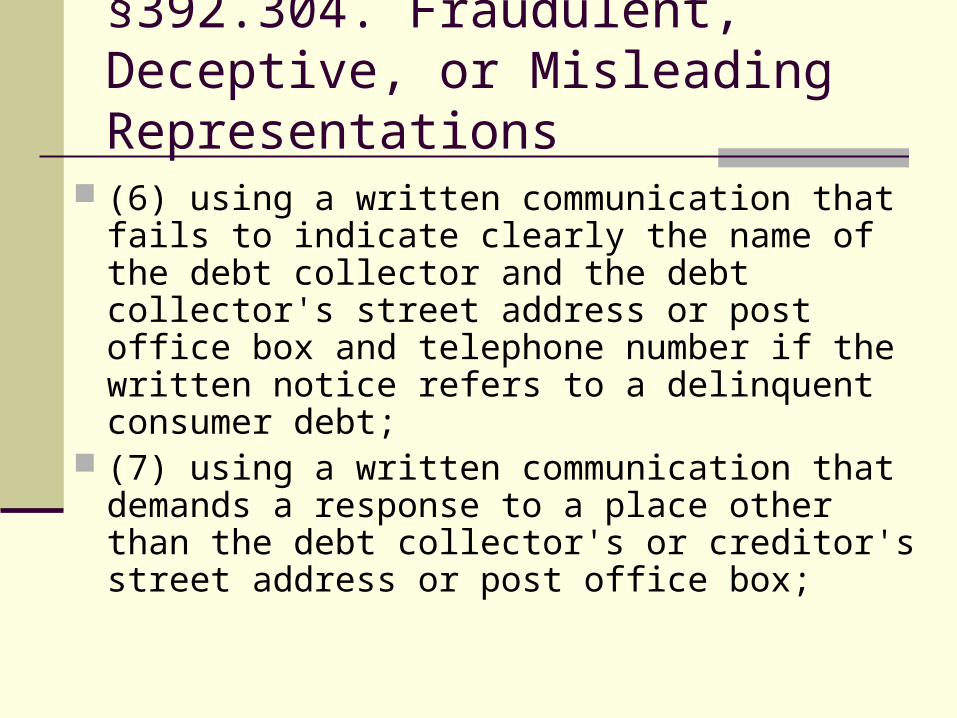

(6) using a written communication that fails to indicate clearly the name of the debt collector and the debt collector's street address or post office box and telephone number if the written notice refers to a delinquent consumer debt;

(7) using a written communication that demands a response to a place other than the debt collector's or creditor's street address or post office box;

§392.304. Fraudulent, Deceptive, or Misleading Representations

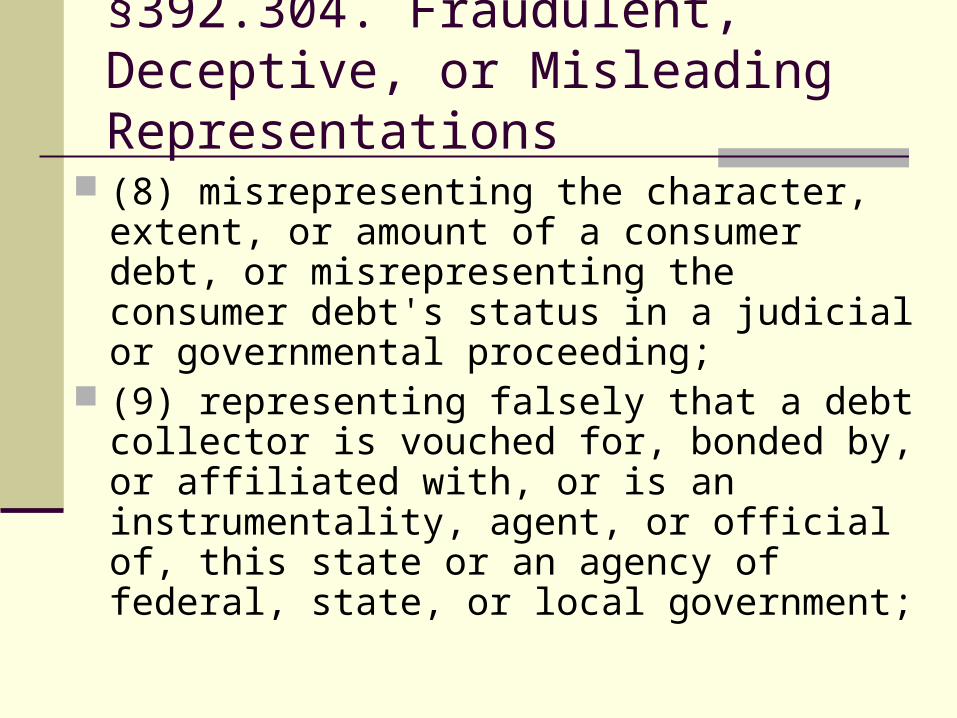

(8) misrepresenting the character, extent, or amount of a consumer debt, or misrepresenting the consumer debt's status in a judicial or governmental proceeding;

(9) representing falsely that a debt collector is vouched for, bonded by, or affiliated with, or is an instrumentality, agent, or official of, this state or an agency of federal, state, or local government;

§392.304. Fraudulent, Deceptive, or Misleading Representations

(10) using, distributing, or selling a written communication that simulates or is represented falsely to be a document authorized, issued, or approved by a court, an official, a governmental agency, or any other governmental authority or that creates a false impression about the communication's source, authorization, or approval;

(11) using a seal, insignia, or design that simulates that of a governmental agency;

§392.304. Fraudulent, Deceptive, or Misleading Representations

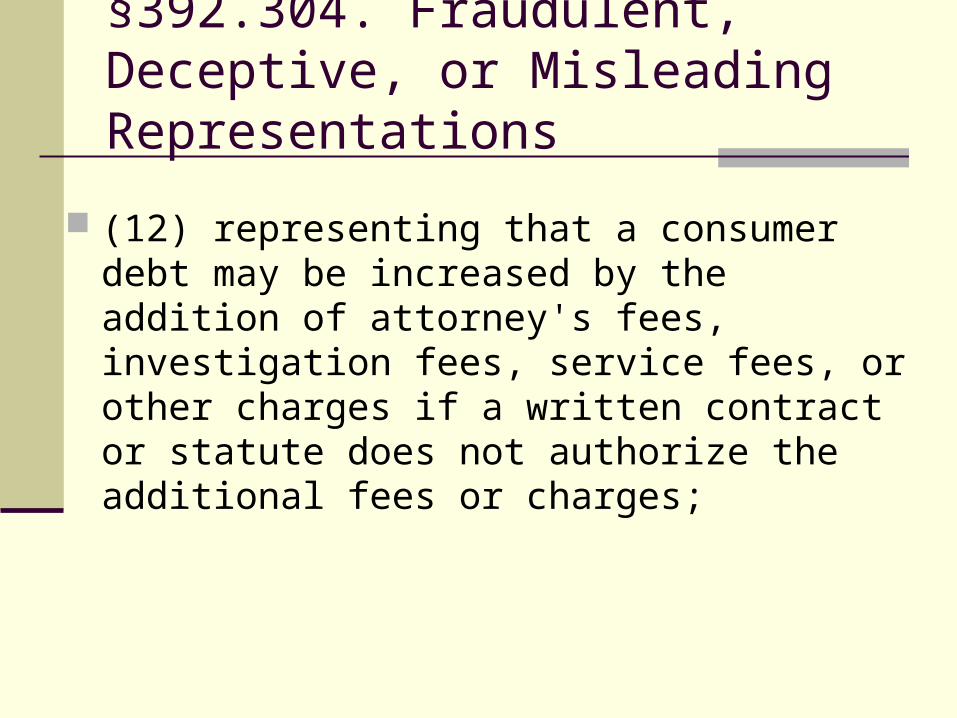

(12) representing that a consumer debt may be increased by the addition of attorney's fees, investigation fees, service fees, or other charges if a written contract or statute does not authorize the additional fees or charges;

§392.304. Fraudulent, Deceptive, or Misleading Representations

(13) representing that a consumer debt will definitely be increased by the addition of attorney's fees, investigation fees, service fees, or other charges if the award of the fees or charges is subject to judicial discretion;

(14) representing falsely the status or nature of the services rendered by the debt collector or the debt collector's business;

(15) using a written communication that violates the United States postal laws and regulations;

§392.304. Fraudulent, Deceptive, or Misleading Representations

(16) using a communication that purports to be from an attorney or law firm if it is not;

(17) representing that a consumer debt is being collected by an attorney if it is not; or

§392.304. Fraudulent, Deceptive, or Misleading Representations

(18) representing that a consumer debt is being collected by an independent, bona fide organization engaged in the business of collecting past due accounts when the debt is being collected by a subterfuge organization under the control and direction of the person who is owed the debt.

§ 392.306.Use of Independent Debt Collector A creditor may not use an independent debt

collector if the creditor has actual knowledge that the independent debt collector repeatedly or continuously engages in acts or practices that are prohibited by this chapter.

§392.401. Bona Fide Error

A person does not violate this chapter if the action complained of resulted from a bona fide error that occurred notwithstanding the use of reasonable procedures adopted to avoid the error.

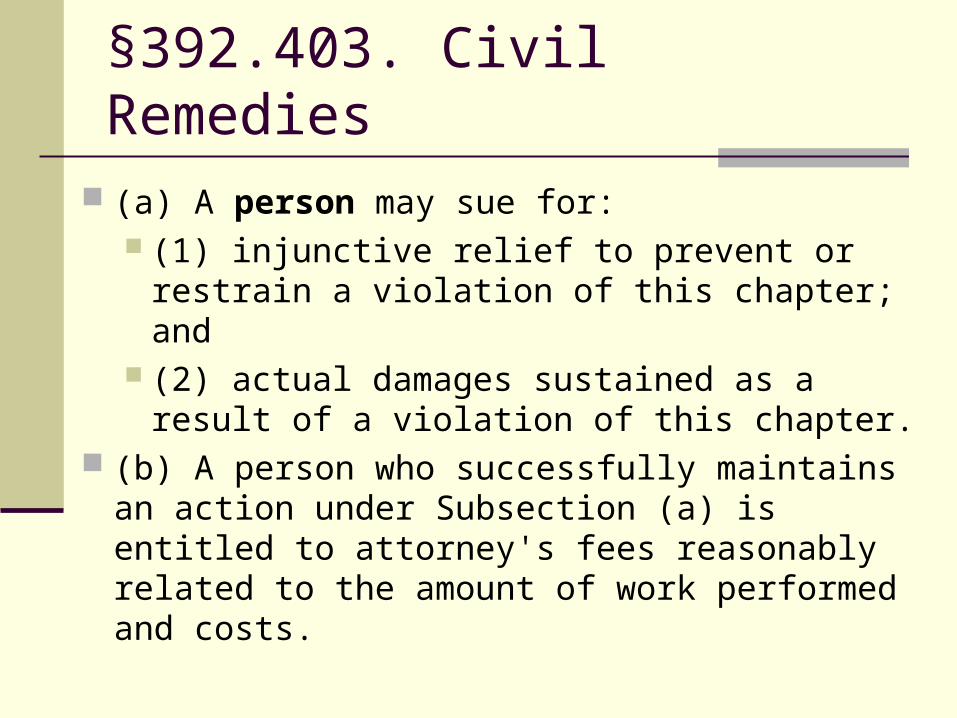

§392.403. Civil Remedies

(a) A person may sue for: (1) injunctive relief to prevent or restrain a

violation of this chapter; and (2) actual damages sustained as a result of a

violation of this chapter. (b) A person who successfully maintains an

action under Subsection (a) is entitled to attorney's fees reasonably related to the amount of work performed and costs.

§392.403. Civil Remedies

(c) On a finding by a court that an action under this section was brought in bad faith or for purposes of harassment, the court shall award the defendant attorney's fees reasonably related to the work performed and costs.

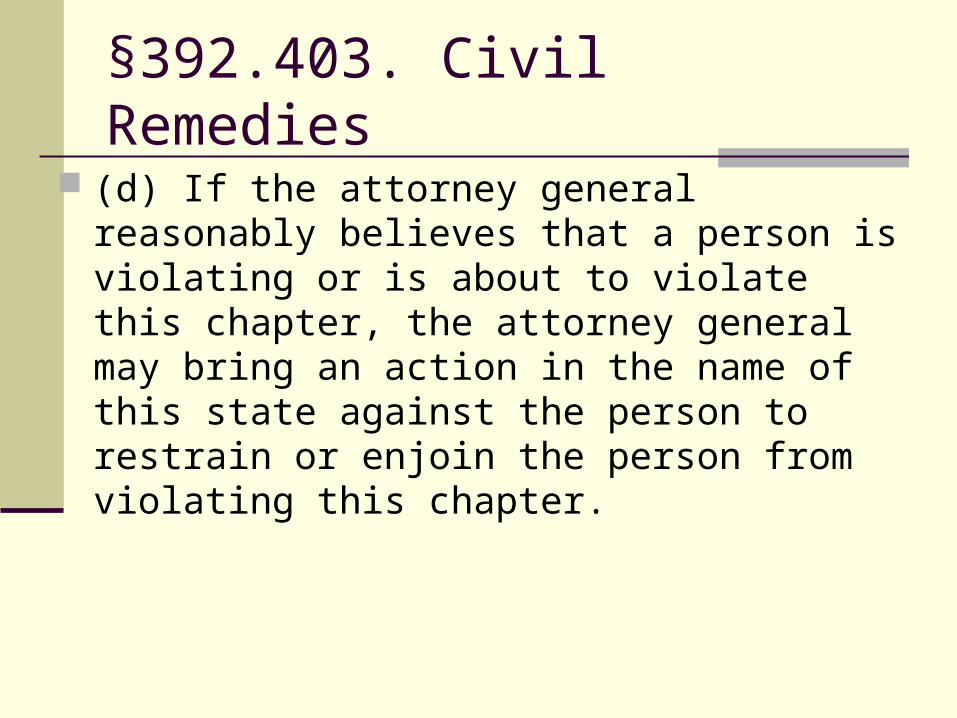

§392.403. Civil Remedies

(d) If the attorney general reasonably believes that a person is violating or is about to violate this chapter, the attorney general may bring an action in the name of this state against the person to restrain or enjoin the person from violating this chapter.

§392.403. Civil Remedies

(e) A person who successfully maintains an action under this section for violation of Section 392.101[bond requirement], 392.202[correction of files], or 392.301(a)(3)[threatening to represent that the consumer is refusing to pay nondisputed debt when it’s disputed] is entitled to not less than $100 for each violation of this chapter.

§ 392.404(a). Remedies Under Other Law

A violation of this chapter is a deceptive trade practice under Subchapter E, Chapter 17, Business & Commerce Code, and is actionable under that subchapter.

Problem 27 (February 2002 Exam)

Did Bank’s collection efforts violate the Texas Debt Collection Act? Explain fully.

Did Best Credit’s collection efforts violate the Act? Explain fully.

If Bank or Best Credit violated the Act, what civil remedies are available to Sid under the Act? Explain fully.

Examiner’s Comments

This question called for familiarity with the Texas Debt Collection Act (TDCA). Some examinees correctly noted that it is not a violation of the TDCA for a collector to threaten to commence a civil action to collect the debt. Many examinees correctly stated that the TDCA generally prohibits deceptive and coercive debt collection practices, but they did not refer to specific prohibitions that the Bank may have violated.

Examiner’s Comments

In the second section, involving Best Credit's collection efforts, most examinees stated the [federal, ed.] time restrictions on telephone contact by debt collectors, as well as the [federal, ed.] rules regarding contact at the consumer's place of employment, but failed to discuss how or whether the facts supported finding a violation of these [federal, ed.] restrictions. In addition, while many examinees concluded that the numerous phone calls were harassing, they did not discuss whether the facts showed the debt collector’s intent to harass, which is required by the statute.

Examiner’s Comments

With respect to damages, most examinees correctly noted that a violation of the TDCA is also actionable as a violation of the Texas Deceptive Trade Practices Act (DTPA). However, some examinees only discussed remedies available under the DTPA and did not address the remedial scheme in the TDCA.