ws atkins plc/media/files/a/atki… · · 2011-01-31ws atkins plc half year results – six...

TRANSCRIPT

WS Atkins plcHalf year results – six months ended 30 September 2008

Plan Design Enable

26 November 2008

1

Summary

• Very good half year results

• Strong cash generation

• Improving the business

• Progressing in balance and continuing to invest

• Well placed to respond to challenges and opportunities ahead

2

Robert MacLeodGroup Finance Director

3

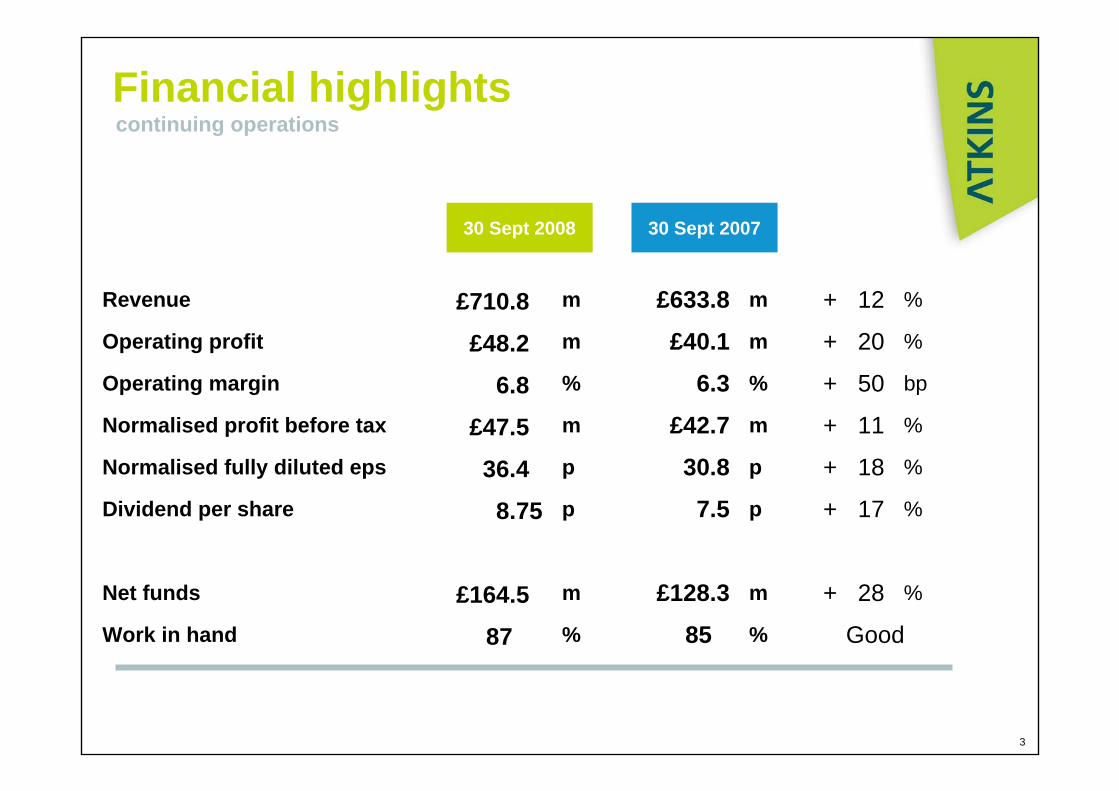

Financial highlights

Good%85%87Work in hand

%28+m£128.3m£164.50Net funds

%17+p7.5p8.75Dividend per share

%18+p30.8p36.40Normalised fully diluted eps

%11+m£42.7m£47.50Normalised profit before tax

bp50+%6.3%6.80Operating margin

%20+m£40.1m£48.20Operating profit

%12+m£633.8m£710.80Revenue

30 Sept 200730 Sept 2008

continuing operations

4

Design and Engineering Solutions

• Businesses performed well in first half

• Markets generally remain robust

• Early signs of softening in the UK design market

• Outlook is positive

30 Sep 200730 Sep 2008

Revenue (£m) 202.6 181.8 + 11 %Operating profit (£m) 16.8 15.7 + 7 %Operating margin 8.3 % 8.6 % - 30 bpWork in Hand 87 % 83 %Staff numbers (FTE inc. agency) 5,176 4,730 + 9 %Average staff numbers 5,057 4,580 + 10 %

Very Good

5

Highways and Transportation

• Results in line with expectations

• Design related business has strong workload (M25, M74, A14)

• Demand continuing for Intelligent Transport Systems enabled solutions

• Outlook remains stable

30 Sep 200730 Sep 2008

Revenue (£m) 133.7 134.0 flatOperating profit (£m) 8.0 8.0 flatOperating margin 6.0 % 6.0 % flatWork in Hand 86 % 89 %Staff numbers (FTE inc. agency) 3,077 3,114 - 1 %Average staff numbers 2,937 3,082 - 5 %

Good

6

Rail

• Results as predicted with significantly improved margin

• Good progress on large contracts (RuN resignalling)

• Growth in enhancement work

• Outlook remains good

30 Sep 200730 Sep 2008

Revenue (£m) 99.6 102.0 - 2 %Operating profit (£m) 7.1 3.9 + 82 %Operating margin 7.1 % 3.8 % + 330 bpWork in Hand 90 % 87 %Staff numbers (FTE inc. agency) 1,627 1,740 - 6 %Average staff numbers 1,643 1,712 - 4 %

Good

7

Middle East

• Excellent results

• Increasing demand for large-scale multi-disciplinary projects

• Dubai metro project progressing well

• Outlook for the rest of the year remains strong

30 Sep 200730 Sep 2008

Revenue (£m) 82.0 52.9 + 55 %Operating profit (£m) 8.7 4.6 + 89 %Operating margin 10.6 % 8.7 % + 190 bpWork in Hand 85 % 77 %Staff numbers (FTE inc. agency) 2,948 2,148 + 37 %Average staff numbers 2,696 1,947 + 38 %

Very Good

8

Management and Project Services

• Faithful+Gould:

• Growth driven by energy, utilities and public sector services

• Challenging UK commercial property market

• Management Consultants:

• Refocused business performing ahead of expectations

30 Sep 200730 Sep 2008

Revenue (£m) 113.3 103.1 + 10 %Operating profit (£m) 7.5 6.5 + 15 %Operating margin 6.6 % 6.3 % + 30 bpWork in Hand 84 % 83 %Staff numbers (FTE inc. agency) 2,433 2,421Average staff numbers 2,449 2,350 + 4 %

FairFlat

9

Asset Management

• Performance impacted by legacy PFI education contract

• £2.5m profit on disposal of interest in Modern Housing Solutions

• Outlook for Managing Agent business remains good

30 Sep 200730 Sep 2008

Revenue (£m) 26.6 25.3 + 5 %Operating profit (£m) (1.2) 1.2 - 200 %Operating margin (4.5) % 4.7 %Work in Hand 90 % 90 %Staff numbers (FTE inc. agency) 708 675 + 5 %Average staff numbers 687 678 + 1 %

Fair

10

Cash Flow

30 Sept 2008 30 Sept 2007

• Working capital improvement in September due to early focus on debt collection

• Last year adversely impacted by extension of payment terms from Metronet

Operating profit 48.2 40.1Depreciation/amortisation 16.0 14.5Working capital (3.3) (48.5)Pension (28.1) (20.7)Provisions/other 5.4 (2.2)Cashflow from operations 38.2 (16.8)

11

Pension

Gross Net of deferred tax

• Decrease in value of plan assets offset by benefit of increased discount rates

• Agreed deficit funding contributions in H1: £12.5m + £16m = £28.5m

• Movement in discount rates likely to reverse – asset value may take longer to recover

• Cash flow fixed for next 2 years

Net deficit at 1 April 2008 (213.1) (154.1)Service cost (4.8)Net finance cost (2.9)Total cost (7.7)Contributions 32.9Actuarial loss (20.7)Net deficit at 30 September 2008 (208.6) (150.8)

12

Keith ClarkeChief Executive

13

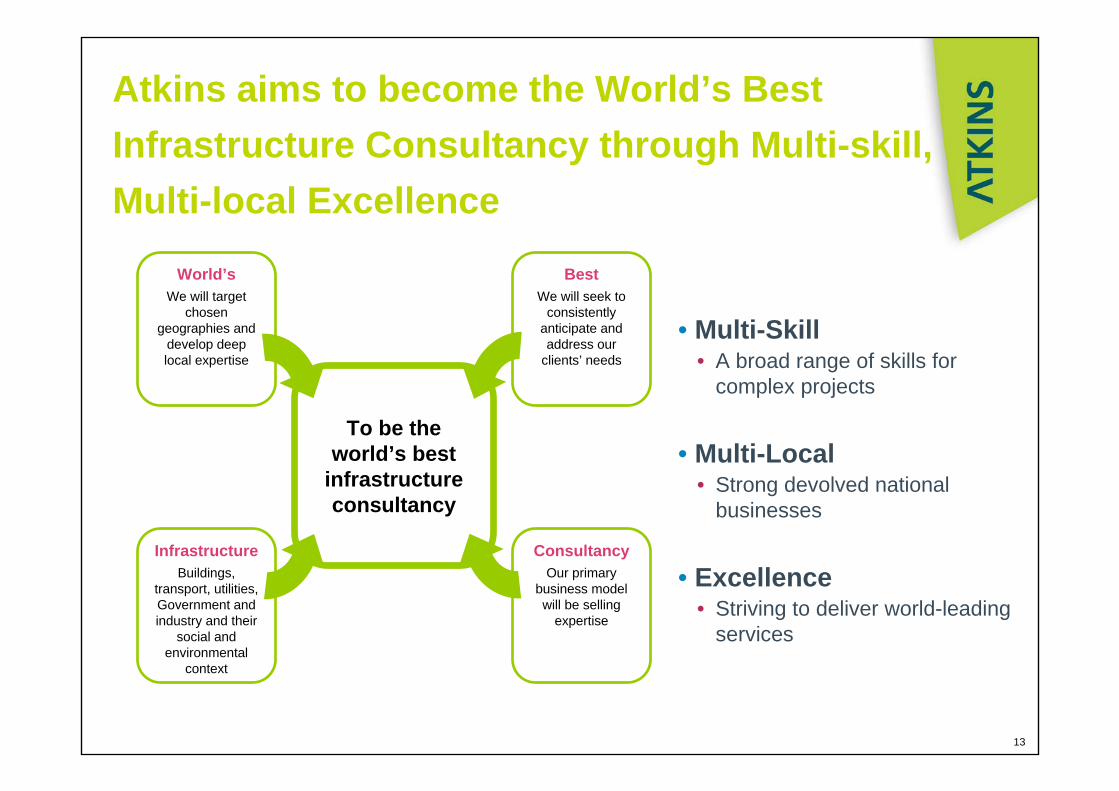

Atkins aims to become the World’s Best Infrastructure Consultancy through Multi-skill, Multi-local Excellence

• Multi-Skill• A broad range of skills for

complex projects

• Multi-Local• Strong devolved national

businesses

• Excellence• Striving to deliver world-leading

services

To be the world’s best

infrastructure consultancy

World’sWe will target

chosen geographies and

develop deep local expertise

BestWe will seek to

consistently anticipate and address our

clients’ needs

InfrastructureBuildings,

transport, utilities, Government and industry and their

social and environmental

context

ConsultancyOur primary

business model will be selling

expertise

14

US UK & Europe RoWTransport, Buildings, Industry Transport, Buildings, Industry Transport, Buildings, Industry

Pet

roC

ost

Hig

hway

sTr

ansi

tH

eavy

Rai

l

Arc

hite

ctur

e &

Pla

nnin

gB

dgE

ngB

dgA

sset

& P

M

Def

ence

& A

ero

Wat

er &

Env

t.

Pow

erN

ucle

ar

Pet

ro.

Cos

t Con

sulta

ncy

Man

Con

Hw

yTr

ansi

tR

ail

Arc

h. &

Pla

n

PM

Bd

Eng

Pet

Atkins has a diverse portfolio

15

Atkins markets are resilient

National Government Regulated PrivateLocal Government

UK Revenue segmentation

TransportOlympic GamesEducation

TransportDefenceEnvironment

TransportWaterUtilities

AerospaceOil and gasBuildings

16

✔ H&T– Mainly long term contracts:

– Gloucestershire CC (2 years to 2011, extension likely)

– Somerset CC (1 year to 2010) – Cambridgeshire CC (7 years to 2016)

✔ D&ES– Olympic Delivery Authority– Education: Design services for colleges

✔ Rail– London Underground: Significant

ongoing work programme

United Kingdom – Local Government

Segmental revenue Drivers

c.£200m

H&T

AM M&PS

D&ES

Rail

17

United Kingdom – National Government

Segmental revenue Drivers

✔ D&ES– Diverse range of clients– Studies likely to continue– Projects may be reprofiled– Carbon agenda: e.g. Environment Agency– Long term contracts: e.g. RSME (4 years to

2013)

✔ H&T– Design of nationally important projects:

e.g. M25, M74, A14– Area 6 MAC (4 years to 2013)– Intelligent Transport Services: in demand to

increase capacity

✔ M&PS– Long term contracts: e.g. GCHQ (2 years to

2011), DCSF (1 year to 2010)

D&ES

M&PS

AM

H&T

c.£125m

18

United Kingdom – Regulated

Segmental revenue Drivers

✔ Rail– £28.5bn investment 2009-2014 (CP4) – Enhancement and signalling markets

robust– Key is ability of Network Rail to bring

projects to market– Large scale projects committed: e.g.

Crossrail, Thameslink

✔ D&ES– Water: AMP5 upcoming– Nuclear: Strong client demand. High barrier

to entry market – Telecom: demand for fixed network cost

efficiency programme

M&PS

D&ESRail

c.£125m

19

United Kingdom – Private

Segmental Revenue Drivers

✔ M&PS– Commercial property sector workload

slowdown (<£10m)– Oil and gas/petrochemicals: strong

portfolio– Financial services clients outlook currently

stable

✔ D&ES– Aerospace: Airbus programmes on A350

and A400M– Oil and gas: continuing demand

✔ AM– Demand driven by requirement for cost

efficiency

AM

D&ES

H&TRail

M&PS

c.£100m

20

Other

OmanQatar

Bahrain

Sharjah

Abu Dhabi

Dubai

Middle East

Segmental Revenue Drivers

✔ Dubai– Growth likely to temper – Higher end market likely to be more resilient– Relationships key

✔ Abu Dhabi– Oil rich state with 2030 plan– Projects with carbon critical focus

✔ Northern Gulf– Urban planning development– Concept design

UAE

£82m

21

Rest of the world

✔China– Hong Kong: Outlook strong with Rail projects – Mainland China: Design and urban planning services in demand

✔ Europe– Denmark: Opportunities in Rail services– Ireland: Continues to be impacted by slowdown

✔USA– Cost consulting: Energy market remains strong– Oil and gas: continuing demand

22

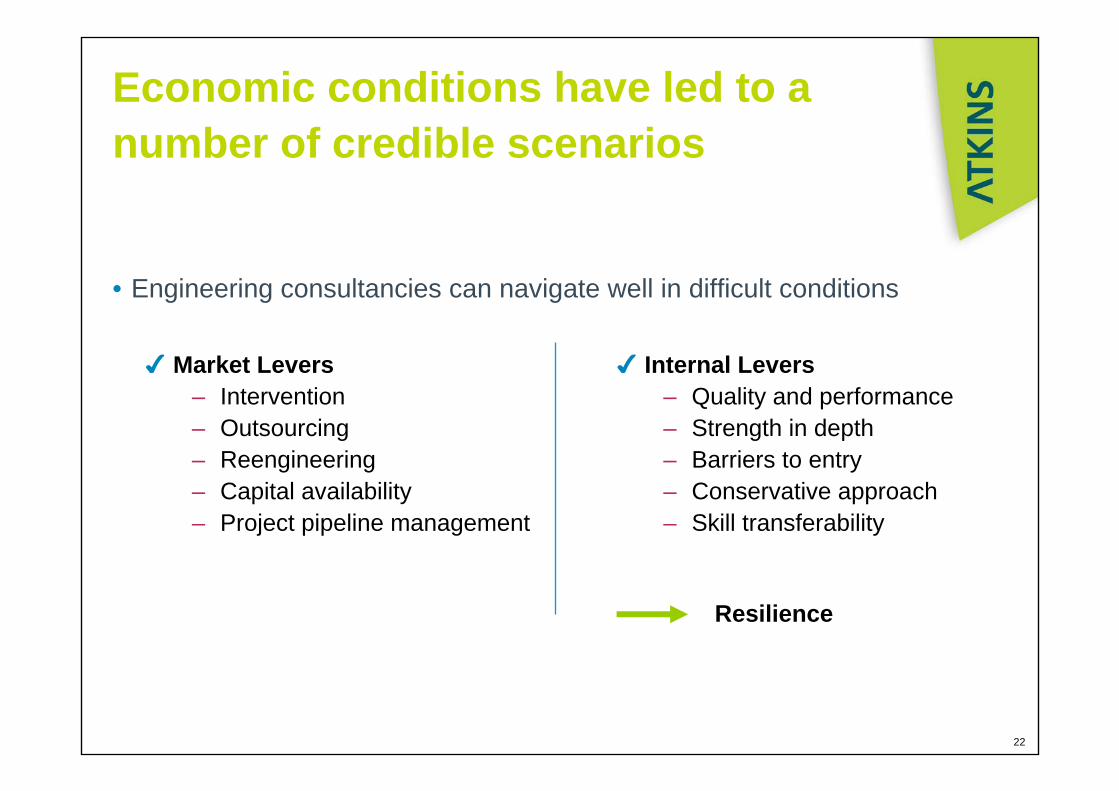

Economic conditions have led to a number of credible scenarios

• Engineering consultancies can navigate well in difficult conditions

✔ Internal Levers– Quality and performance– Strength in depth – Barriers to entry– Conservative approach– Skill transferability

✔ Market Levers– Intervention– Outsourcing– Reengineering– Capital availability– Project pipeline management

Resilience

23

People

• Staff turnover down to 14.5%

• Staff at 30 Sept 2008: over 18,000

• Ongoing evaluation of activities:– Transferability of skills– Shrinking where appropriate– Hiring where required 15,003

15,867

16,90917,278

18,322

Sept2006

March2007

Sept2007

March2008

Sept2008

(Staff numbers exclude LSH: disposed in June 2007)

24

Looking forward

✔ Confident for the full year 2008/09

✔ Demand for infrastructure remains

✔ Well placed:– Depth and breadth– Flexibility and agility

WS Atkins plcHalf year results – six months ended 30 September 2008

Plan Design Enable

26 November 2008

26

The information in this presentation pack which does not purport to be comprehensive has been provided by Atkins, and has not been independently verified. While this information has been prepared in good faith, no representation or warranty, express or implied, is or will be made and no responsibility or liability is or will be accepted by Atkins, as to or in relation to the accuracy or completeness of this presentation pack or any other written or oral information made available as part of the presentation and any such liability is expressly disclaimed. Further, whilst Atkins may subsequently update the information made available in this presentation, we expressly disclaim any obligation to do so.

Disclaimer