www.boc.ie draft for sei review sei workshop on is 393 december 7 th 2005 the potential synergies...

TRANSCRIPT

www.boc.ie

Draft for SEI ReviewSEI Workshop on IS 393

December 7th 2005

The potential synergies between IS 393 and other energy related Drivers and Regulations i.e. IPPC, EU ETS etc. in the light of the recent preparatory work on Ireland’s Second National Allocation

Plan for emissions trading in period 2008-2012

A presentation by

Tom Cleary

Senior Partner

Byrne O Cleirigh

www.boc.ie

Objective of Presentation

To inform group of context of energy use by industry and main drivers to reducing emissions

Examine requirements of the IPPC Directive and IPPC Licensing wrt Energy

Examine overlap and synergies between IS 393 and other drivers particularly IPPC Licensing by EPA, EU ETS and higher energy prices.

Highlight need for a range of support measures to meet challenges

www.boc.ie

How are Developments in Key Sectors likely to influence the role of IS 393

1. Power sector – EU ETS & Security of Supply

2. Trading sector industry energy emissions

3. Trading Sector Process Emissions

4. Non-trading sector industry

Nos. 1, 2 and 4 are main areas for IS 393 though IS

393 disciplines could also assist identify reductions

in process emissions

www.boc.ie

Relevance of IS 393 to Power Sector

Power sector – prices rising due to rising prices of oil and gas and coal

EU ETS will add a cost to power sector which will have knock on impacts on industry and services and competitiveness

Power companies are not immune to the need to reduce energy costs and hence EU ETS costs

We in BOC see great synergies between all drivers – because of escalating energy costs it is nearly impossible to have too many stimuli for energy efficiency. IS 393 potentially important in sector

www.boc.ie

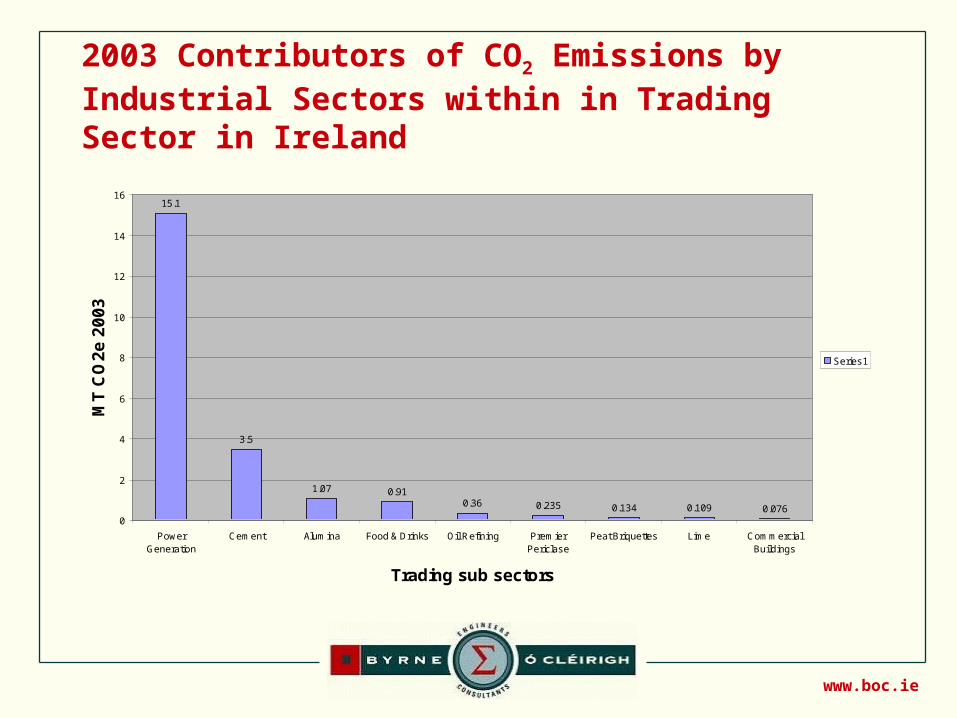

2003 Contributors of CO2 Emissions by Industrial Sectors within in Trading Sector in Ireland

15.1

3.5

1.07 0.910.36 0.235 0.134 0.109 0.076

0

2

4

6

8

10

12

14

16

PowerGeneration

Cement Alumina Food & Drinks Oil Refining PremierPericlase

Peat Briquettes Lime CommercialBuildings

Trading sub sectors

MT

CO

2e

20

03

Series1

www.boc.ie

1990 Emissions Contribution Total 53.974 MT CO2e

ENERGY22%

AGRICULTURE36%

TRANSPORT10%

INDUSTRIAL AND Commercial

17%

RESIDENTIAL13%

WASTE2%

"F" GASES0% SOLVENT AND OTHER

PRODUCT USES0% ENERGY

AGRICULTURE

TRANSPORT

INDUSTRIAL AND Commercial

RESIDENTIAL

WASTE

"F" GASES

SOLVENT AND OTHER PRODUCTUSES

www.boc.ie

1990 Emissions Contribution Total 53.974 MT CO2e

ENERGY22%

AGRICULTURE36%

TRANSPORT10%

INDUSTRIAL AND Commercial

17%

RESIDENTIAL13%

WASTE2%

"F" GASES0% SOLVENT AND OTHER

PRODUCT USES0% ENERGY

AGRICULTURE

TRANSPORT

INDUSTRIAL AND Commercial

RESIDENTIAL

WASTE

"F" GASES

SOLVENT AND OTHER PRODUCTUSES

www.boc.ie

2003 Contributors of CO2 Emissions by Industrial Sectors in Trading in EU ETS in Ireland

RE by Sector

73%

1%1%

3%

0%1%

14%

0%1%4%

1% 1%0%0%

Power

Pharmachem

Food and Drink Dairy

Other Food and Drink

Healthcare

Other Industry

Cement

Lime

Other Ind & Process

Alumina

Energy

Oil Refining

Energy Distribution

Commercial

Cement 17.1%

Power 66%

Alumina 5.2%

Food & Drinks

www.boc.ie

Trading Sector – Manufacturing Industry

Some highly energy intensive firms At least 2 sectors and several installations with

emissions > 1 million tonnes CO2e pa 2003 total of non power generation CO2 emissions in

trading sector (industry plus a small number of commercial / institutional buildings) ~ 6.8 million tonnes (including direct emissions from fossil fuels and process emissions)

www.boc.ie

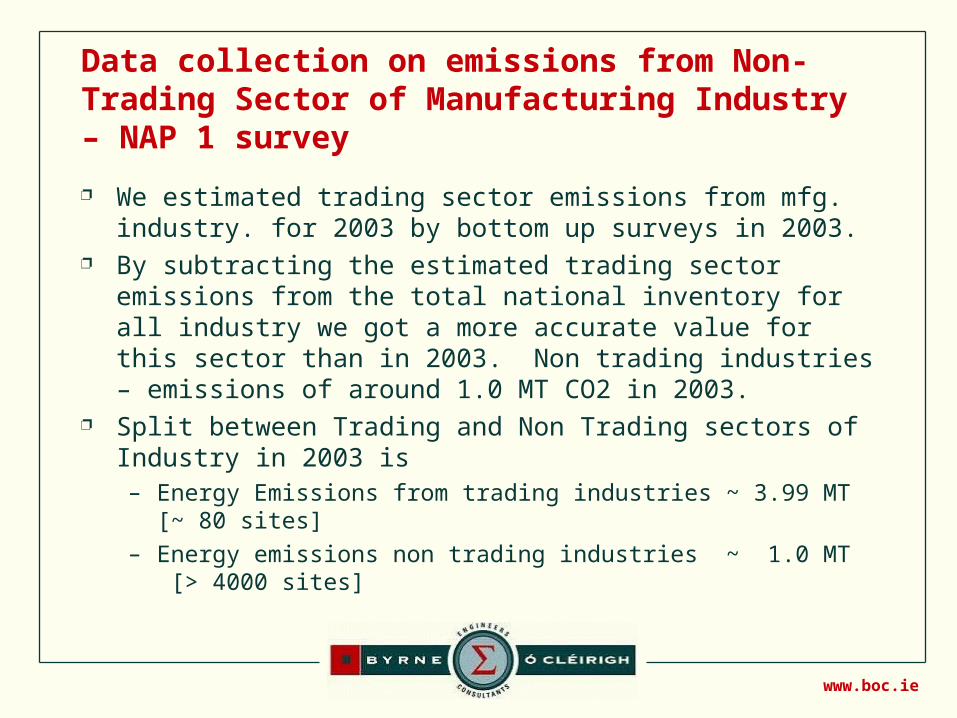

Data collection on emissions from Non-Trading Sector of Manufacturing Industry – NAP 1 survey

We estimated trading sector emissions from mfg. industry. for 2003 by bottom up surveys in 2003.

By subtracting the estimated trading sector emissions from the total national inventory for all industry we got a more accurate value for this sector than in 2003. Non trading industries – emissions of around 1.0 MT CO2 in 2003.

Split between Trading and Non Trading sectors of Industry in 2003 is – Energy Emissions from trading industries ~ 3.99 MT [~ 80 sites]

– Energy emissions non trading industries ~ 1.0 MT [> 4000 sites]

www.boc.ie

Why the Need for IS 393 at this time

In 2003 SEI had reported on potential for negotiated agreements for Industries outside EU ETS. Identified potential energy savings of ~ 640,000 tonnes per annum in 650 firms the non trading sector based on a carbon energy tax of €17.5 and an 80% rebate for undertaking a programme of measures

Carbon tax has been scrapped in meantime

www.boc.ie

Clear from This Mornings Speakers that IS 393 could be an important part of a Suite of Measures

Identification of need for and benefits from IS 393 addressed by other speakers

Other SEI initiatives to assist firms e.g. LIEN, EMAP We in BOC have Identified several groups of

organisations for which IS 393 may be appropriate– Firms and Commercial Sites in EU ETS– High Electricity users whether in EU ETS or not– The largest firms in Non trading sector of industry– Members of LIEN (big overlap with EU ETS firms)– IPC Licensed Sites (480 excluding agricultural sector)

www.boc.ie

IS 393 and IPPC Directive’s Requirement for Efficient Resources Use

EU IPPC Directive 96/61 is concerned with integrated pollution prevention and control

Implemented in Ireland via Protection of the Environment Act 2003

Sections 82(10)(a) and 82 (11) provide power to EPA to review IPC licence and update them to IPPC licence

IPPC Directive has requirements under the headings of Resource Use and importantly Energy Efficiency

www.boc.ie

IS 393 and IPPC Requirements for Efficient Resources Use – Current Position

In 2003 EPA asked BOC to draw up a template for energy auditing in preparation for IPPC

Energy Auditing now a condition of many IPC and all IPPC licences – by June 2005 the energy efficiency condition had been included in 120 IPC licences.

The audit template is now on EPA web site Letters with conditions to create many IPPC Licences have

been issued in the last few months Oct/Nov 2005 Where these letter contain Amendments to older IPC licences

the requirement for energy management is now explicitly listed as is a similar requirement for efficiency water use and efficient use of raw materials.

www.boc.ie

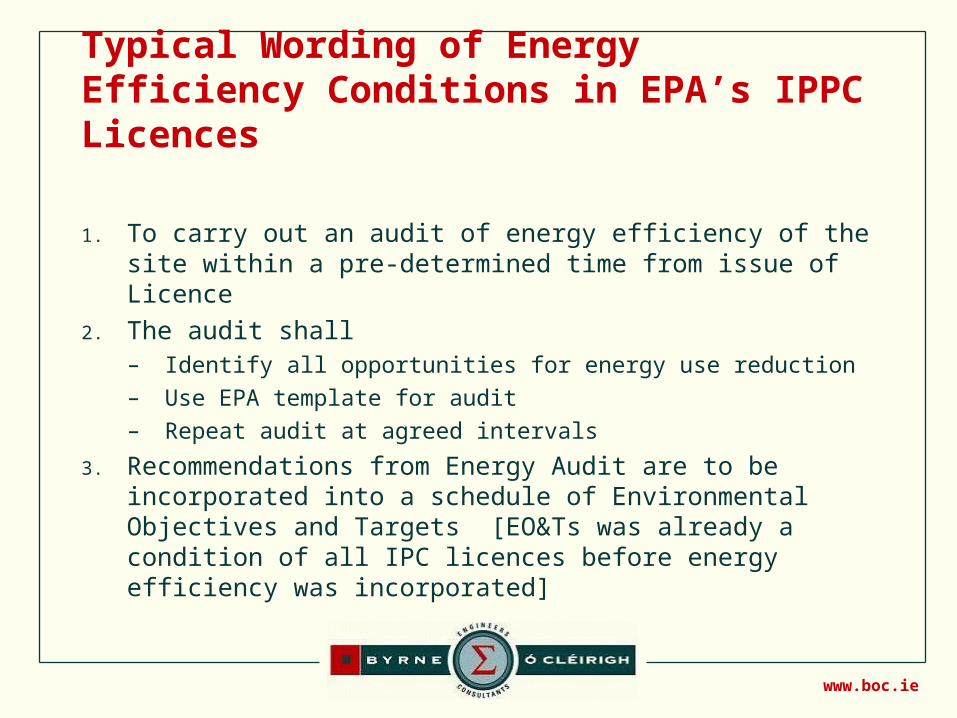

Typical Wording of Energy Efficiency Conditions in EPA’s IPPC Licences

1. To carry out an audit of energy efficiency of the site within a pre-determined time from issue of Licence

2. The audit shall– Identify all opportunities for energy use reduction

– Use EPA template for audit

– Repeat audit at agreed intervals

3. Recommendations from Energy Audit are to be incorporated into a schedule of Environmental Objectives and Targets [EO&Ts was already a condition of all IPC licences before energy efficiency was incorporated]

www.boc.ie

How do Key Requirements of IPPC and IS 393 Compare?

Energy Conditions of IPPC Licences

IS 393 Requirement

Carry Out Energy Audit Covered by Requirement to Review of Energy Aspects

Identify all opportunities for energy use reduction

Explicitly part of review of Energy Aspects

Incorporate recommendations from audit into Objectives and Targets in AER – Annual Environmental Report

Audit to be conducted in accordance with EPA audit template

IS 393 has comprehensive requirements covering all topics in EPA template

www.boc.ie

Reminder of National Projections of BAU Emissions as of Feb 2004 – ICF-BOC – Gap to Kyoto Target 9.1 MT CO2e – latest refinements may reduce slightly

Base Case Scenario - Emission Projections 2002-2012

50

52

54

56

58

60

62

64

66

68

70

72

74

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year

MT

CO

2e

Emissions Excl LUCF

Emissions net LUCF

Kyoto Target

Kyoto Limit 2008-2012 60.365 MT CO2e

www.boc.ie

Most Recent Work in Preparation for NAP 2

New work by EPA and FAPRI on emission factors and activity levels in Agriculture

Recent review by DoEHLG on emissions from waste New work by ESRI on Mid Term Review and Energy

Use Projection New work by COFORD on sequestration New work by EPA on historical emission of “F” gases Transport 21 – will need to ascertain how massive

investment will impact on national emissions

www.boc.ie

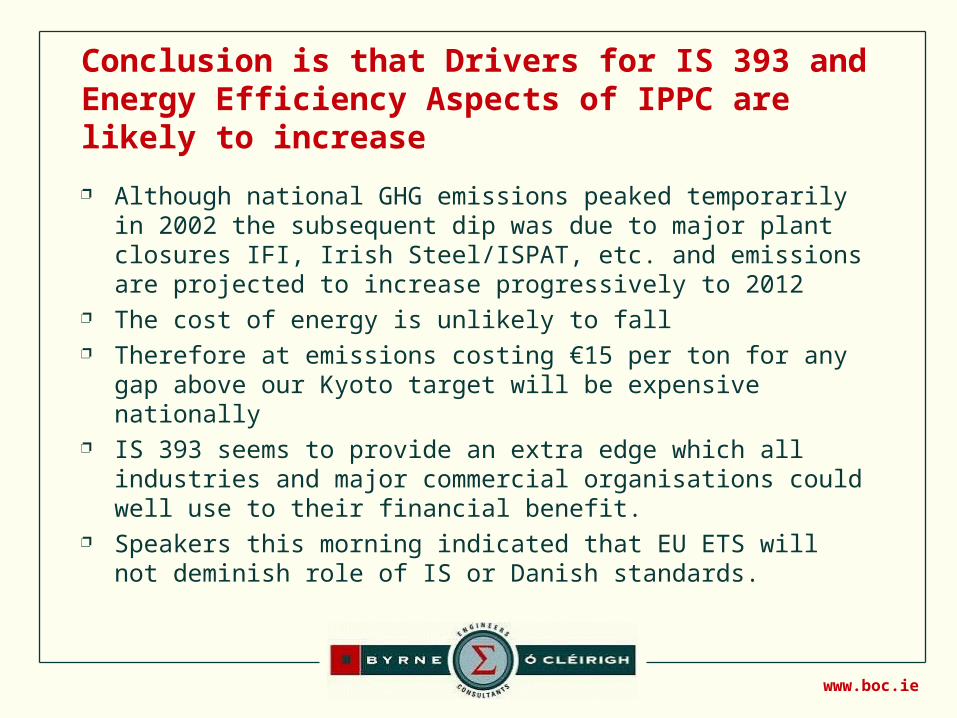

Conclusion is that Drivers for IS 393 and Energy Efficiency Aspects of IPPC are likely to increase

Although national GHG emissions peaked temporarily in 2002 the subsequent dip was due to major plant closures IFI, Irish Steel/ISPAT, etc. and emissions are projected to increase progressively to 2012

The cost of energy is unlikely to fall Therefore at emissions costing €15 per ton for any gap above

our Kyoto target will be expensive nationally IS 393 seems to provide an extra edge which all industries and

major commercial organisations could well use to their financial benefit.

Speakers this morning indicated that EU ETS will not deminish role of IS or Danish standards.

www.boc.ie

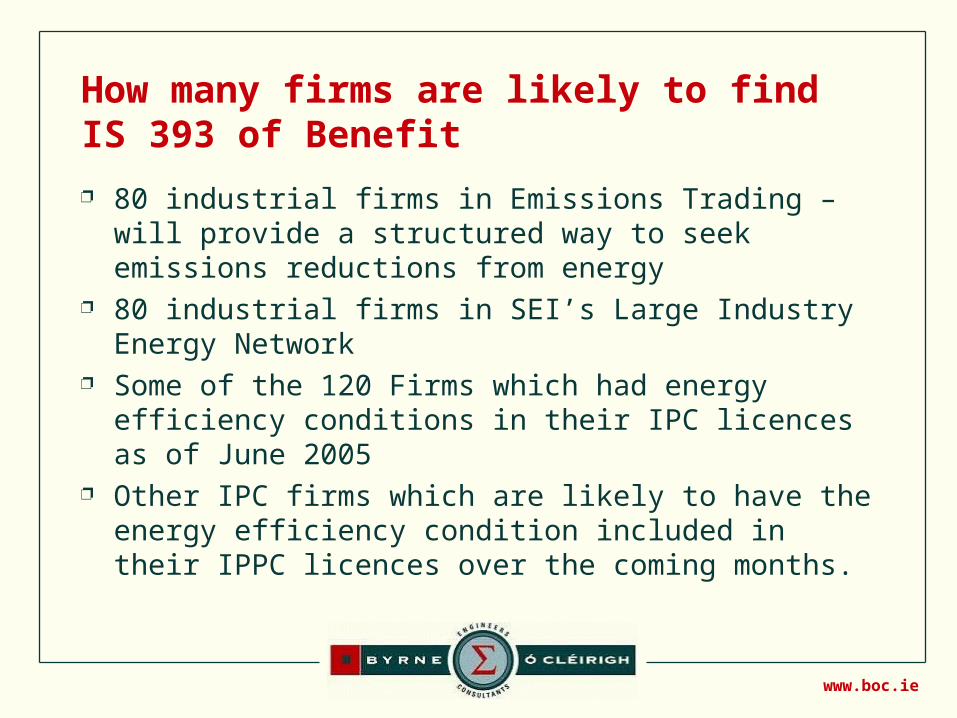

How many firms are likely to find IS 393 of Benefit

80 industrial firms in Emissions Trading – will provide a structured way to seek emissions reductions from energy

80 industrial firms in SEI’s Large Industry Energy Network

Some of the 120 Firms which had energy efficiency conditions in their IPC licences as of June 2005

Other IPC firms which are likely to have the energy efficiency condition included in their IPPC licences over the coming months.

www.boc.ie

Summary

There will be serious and sustained drivers to increase energy efficiency driven by– EU ETS and Kyoto Protocol– Higher energy prices– New EU Directives such as IPPC Directive.

Industries will need a range of initiatives to counter these challenges

IS 393 holds the prospects of providing a structured approach to energy management which will help to meet these challenges.

www.boc.ie

Emission Trends by Sector and Relative Importance of Sectors

Emission Trends by Sector 2003 to 2012

0.000

5.000

10.000

15.000

20.000

25.000

EnergySector

(Pow er,Refining)

Agricultural TransportSector

Residential IndustrialSectorEnergy

(Trading)

Commercial IndustryProcess

Emissions(Trading)

IndustrialSector

Energy (NonTrading)

Waste sector F Gases(Some from

tradingsector)

Solvents &Other

Products

Allow ancefor new

greenfieldindustry(Trading)

Sectors / Emission Types

MT

CO

2e p

er a

nn

um

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

www.boc.ie

September 2005 ICF-BOC Projection of Distance to Kyoto Target 2008-2012

60.991 60.991 60.991 60.991 60.991 60.991 60.991 60.991 60.991 60.991

67.555

68.684

69.848

68.932 69.17569.778

70.278

71.10371.475

72.101

67.555

68.684

69.848

68.932 69.175

68.05868.558

69.38369.755

70.381

54.000

56.000

58.000

60.000

62.000

64.000

66.000

68.000

70.000

72.000

74.000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

KT

CO

2e Kyoto

Excl LUCF

Incl. LUCF

Kyoto Target based on updated 1990 base

Emissions Excl. LUCF

Emissions Incl. LUCF