www.lirneasia.net teleuse@bop teleuse@bop : implications for civil society capacity building and...

TRANSCRIPT

ww

w.li

rnea

sia.

net

Teleuse@BOP: Implications for Civil Society Capacity Building and Democracy

Lorraine Carlos SalazarVisiting Research Fellow

Institute of Southeast Asian Studies (ISEAS)&

Senior ResearcherLirneasia

[email protected], [email protected]

ww

w.li

rnea

sia.

net

ww

w.li

rnea

sia.

net

Outline

Findings from Lirneasia’s 2006 Multi-country Study Background & methodology Everyone has access, but not ownership Usage patterns Who owns phones? Why? BOP is prepaid SMS use and its relative cost Missed calls Internet…what Internet?

Examples of SMS use in the Philippines Akbayan’s use of SMS in election monitoring Among Ed and Grace Padaca, the good and the bad OFW SOS

Reflections and Conclusion

ww

w.li

rnea

sia.

net

Bottom of the pyramid

Background & methodology

ww

w.li

rnea

sia.

net

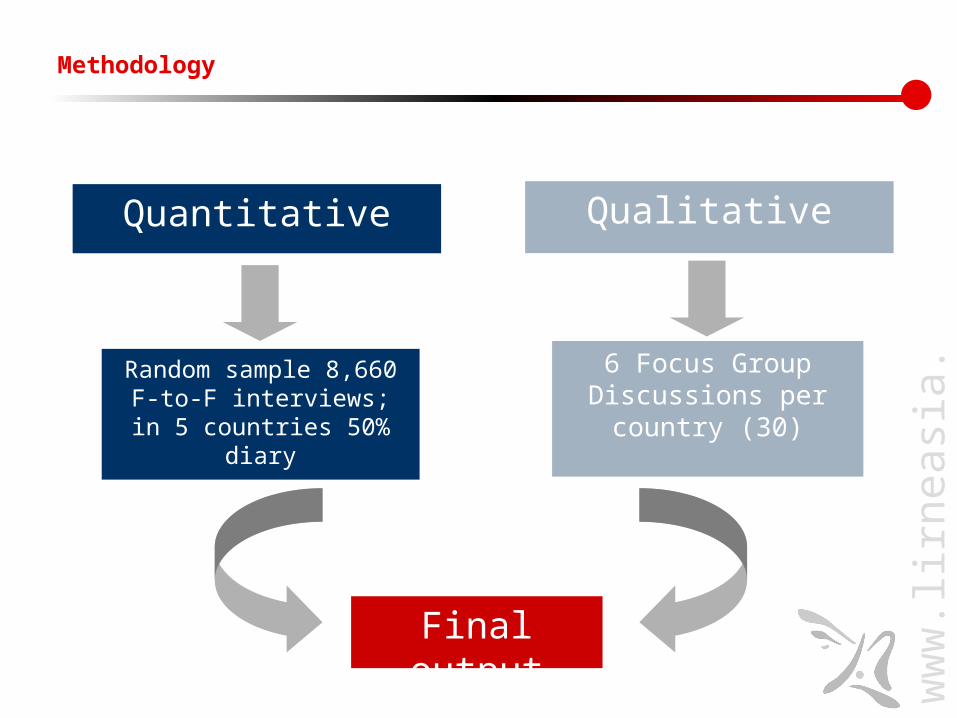

Methodology

6 Focus Group Discussions per

country (30)

Random sample 8,660 F-to-F interviews; in 5 countries 50% diary

Final output

QualitativeQuantitative

ww

w.li

rnea

sia.

net

*excluding FANA/FATA – Tribal Areas; **excluding N&E Provinces

Bottom of the Pyramid (BOP) defined

Many definitions of poverty, but this study uses SEC D and E; between ages 18-60

SEC does not take into account income, but it is closely related to income levels

Pakistan India Sri Lanka Philippines Thailand

Population (million) 165 1,095 20 89 64

Target population of study (million)

77* 260 4** 41 15

SEC D & E

SEC A, B & C

ww

w.li

rnea

sia.

net

Quantitative sample

BOP segment is representative of the BOP population Diary respondents also representative of BOP

Small (non-representative sample) taken of SEC groups A, B & C

SAMPLE

South Asia South East Asia TOTAL

Pakistan India Sri Lanka Philippines Thailand

TOP (SEC A, B & C)

731 652 596 92 348 2,420

BOP (SEC D & E)

1,081 3,348 481 1,008 352 6,269

Total 1,812 4,000 1,077 1,100 700 8,689

Error margin at 95 percent CI

2.7% 1.5% 3.0% 3.0% 7.0%

ww

w.li

rnea

sia.

net

Teleuse@BOP

~9,000 sample survey in five countries India, Pakistan, Sri Lanka, Philippines & Thailand

Understand telecom use at the BOP (= SEC Groups D &E) in Developing Asia

Representative of target population SEC D&E, ages 18-60

ww

w.li

rnea

sia.

net

Country profiles

South Asia South East Asia

Pakistan India Sri Lanka Philippines Thailand

Population165

million 1,095 million

19.6 million

89 million

64 million

GNI per capita (2005), USD (Atlas)

690 720 1,160 1,300 2,750

GNI per capita (2005), USD (PPP)

2350 3460 4,520 5,300 8,440

Population below Poverty Line

32%(est. 2001)

25%(est. 2001)

23%(est. 2005)

40%(est. 2001)

10%(est. 2004)

Fixed teledensity (2006) 4.16(2006 Q4)

4.58(2006 Q1)

9.50(2006 Q4)

4.07(2005 Q4)

10.25(2005 Q4)

Mobile teledensity (2006) 25.22(2006 Q4)

8.82(2006 Q1)

27.1(2006 Q4)

41.30(2005 Q4)

46.45(2005 Q4)

Internet Users7.5

million 50.6

million 0.3

million 7.8

million 8.4

million

Notes: India on an April – March reporting period ; Pakistan on a July – June reporting period; Other countries follow Jan – Dec (calendar year) reporting periods. Sources: India-COAI, TRAI; Thailand–Company Reports; Pakistan–PTA; Philippines–NTC; Sri Lanka- TRC; 2000 onwards from company reports; World Bank (2006); CIA Fact Book (2005)

ww

w.li

rnea

sia.

net

Bottom of the Pyramid

Everyone has access, but not ownership

ww

w.li

rnea

sia.

net

Access (used a phone in the preceding 3 months)

South Asia South East Asia

Pakistan India Sri Lanka Philippines Thailand

Used phone in last 3 months(% of those randomly approached (all SEC groups) who have used a phone in the preceding 3 months)

98% 94% 92% 93% 95%

Most have used a phone in the last 3 months

Kofi Annan’s statement in 1999 that “half of the world’s population has not made a phone call” was not true then and absolutely wrong now

ww

w.li

rnea

sia.

net

Time it takes to reach nearest phone

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f n

on

-ow

ne

rs a

t th

e B

OP

>60 minutes

45-60 minutes

30-45 minutes

15-30 minutes

10-15 minutes

5-10 minutes

3-5 minutes

< 3 minutes

Time to reach nearest phone the BOP

Most can get to a phone in less than 30 minutes

ww

w.li

rnea

sia.

net

Urban-rural divide: Mostly in Pakistan & India

Time to nearest phone: urban vs. rural: Sri Lanka

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural

Sri Lanka

% o

f n

on

ow

ner

s at

BO

P Betw een 45 - 60 minutes

Betw een 30 - 45 minutes

Betw een 15 - 30 minutes

Betw een 10 - 15 minutes

Betw een 5 - 10 minutes

Betw een 3 - 5 minutes

Less than 2 - 3 minutes

Time to nearest phone: urban vs. rural: Philippines

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural

Philippines

% o

f n

on

ow

ners

at

BO

P More than an hour

Betw een 45 - 60 minutes

Betw een 30 - 45 minutes

Betw een 15 - 30 minutes

Betw een 10 - 15 minutes

Betw een 5 - 10 minutes

Betw een 3 - 5 minutes

Less than 2 - 3 minutes

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural

Pakistan

% o

f n

on

ow

ner

s at

BO

P More than an hour

Betw een 45 - 60 minutes

Betw een 30 - 45 minutes

Betw een 15 - 30 minutes

Betw een 10 - 15 minutes

Betw een 5 - 10 minutes

Betw een 3 - 5 minutes

Less than 2 - 3 minutes

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural

India%

of

no

n o

wn

ers

at

BO

P More than an hour

Betw een 45 - 60 minutes

Betw een 30 - 45 minutes

Betw een 15 - 30 minutes

Betw een 10 - 15 minutes

Betw een 5 - 10 minutes

Betw een 3 - 5 minutes

Less than 2 - 3 minutes

Time to nearest phone

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural

Thailand

% o

f n

on

ow

ner

s at

BO

P

ww

w.li

rnea

sia.

net

Most frequently used mode

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%%

at

BO

P

Public phone 35% 71% 30% 8% 7%

Relative / friend's phone 10% 1% 12% 14% 6%

Neighbours phone 8% 7% 14% 7% 1%

Mobile of another householdmember

12% 4% 6% 11% 5%

Household fixed phone 14% 9% 21% 4% 8%

Own mobile 21% 9% 17% 56% 73%

Pakistan India Sri Lanka Philippines Thailand

Access modes among BOP phone users

S Asia BOP mainly used public phones; SE Asia mobiles

ww

w.li

rnea

sia.

net

Ownership and GDP per capita (USD, PPP)

23%

9%

22%

60%

11%

23%

7%

14%

64%

81%

59%

38%

23%

76%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Pakistan India Sri Lanka Philippines Thailand

% a

t b

ott

om

of

pyr

amid

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

GD

P p

er c

apit

a, U

SD

(P

PP

)

Own a mobile Own a fixed phone (household)

Own nothing (but use something) Per Capita GDP PPP (USD)

High access, but low ownership levels at BOP

Phone ownership is low in South Asia, higher in Philippines and Thailand

ww

w.li

rnea

sia.

net

How often phone owners allow others to use their phones

How often other people (excluding family members) use your mobile

62%54%

66%

35%

55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f m

ob

ile o

wn

ers

Never

A few times in a year

Once a month

Once a week

2-3 times per week

ww

w.li

rnea

sia.

net

Number of mobiles in the household

76%

93%84%

57%

79%

15%

6%13%

26%

15%

5%1% 2%

11%

4%3% 1% 1%

3%1%3% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f h

ou

se

ho

lds

at

BO

P

5 mobiles in the house

4 mobiles in the house

3 mobiles in the house

2 mobiles in the house

1 mobile in the house

Number of mobiles within the respondent’s household

ww

w.li

rnea

sia.

net

Bottom of the pyramid

Usage patterns

ww

w.li

rnea

sia.

net

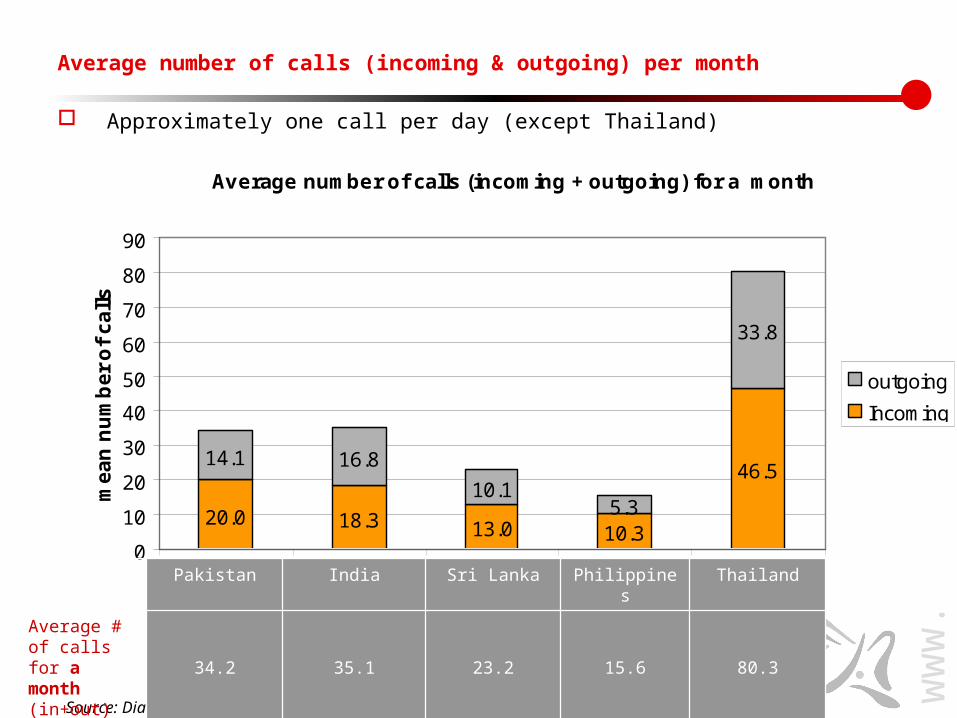

Average number of calls (incoming + outgoing) for a month

20.0 18.3 13.0 10.3

46.514.1 16.8

10.15.3

33.8

0

10

20

30

40

50

60

70

80

90

Pakistan India Sri Lanka Philippines Thailand

me

an

nu

mb

er

of

ca

lls

outgoing

Incoming

Source: Diary

Average number of calls (incoming & outgoing) per month

Approximately one call per day (except Thailand)

Pakistan India Sri Lanka Philippines Thailand

Average # of calls for a month (in+out)

34.2 35.1 23.2 15.6 80.3

ww

w.li

rnea

sia.

net

Average call durations

Average call durations

0%

10%

20%

30%

40%

50%

60%

<1 minute 2-3minutes

About 5minutes

About 10minutes

>15minutes

Duration of the call

% o

f c

alls

Pakistan

India

Sri Lanka

Philipines

Thailand

Source: Diary

ww

w.li

rnea

sia.

net

Call destination (type of call)

Type of call (local, long distance, international)

71%78%

62%

88% 84%

28%22%

34%

6% 16%

1% 0% 4% 6% 1%

0%10%20%30%40%50%60%70%80%90%

100%

Pakistan India Sri Lanka Philipines Thailand

% o

f c

alls International call

Long distance call

Local call

Source: Diary

ww

w.li

rnea

sia.

net

Source: Diary

Call purposes (primary)

Main purpose of call

82%72% 65% 64% 70%

4%14% 27%

21%

14% 14%8%

15%29%

2%

0%

20%

40%

60%

80%

100%

Pakistan India Sri Lanka Philipines Thailand

% o

f al

l cal

ls

Keeping in touch with family & friends To check something / Deliver message

Business

ww

w.li

rnea

sia.

net

Bottom of the pyramid

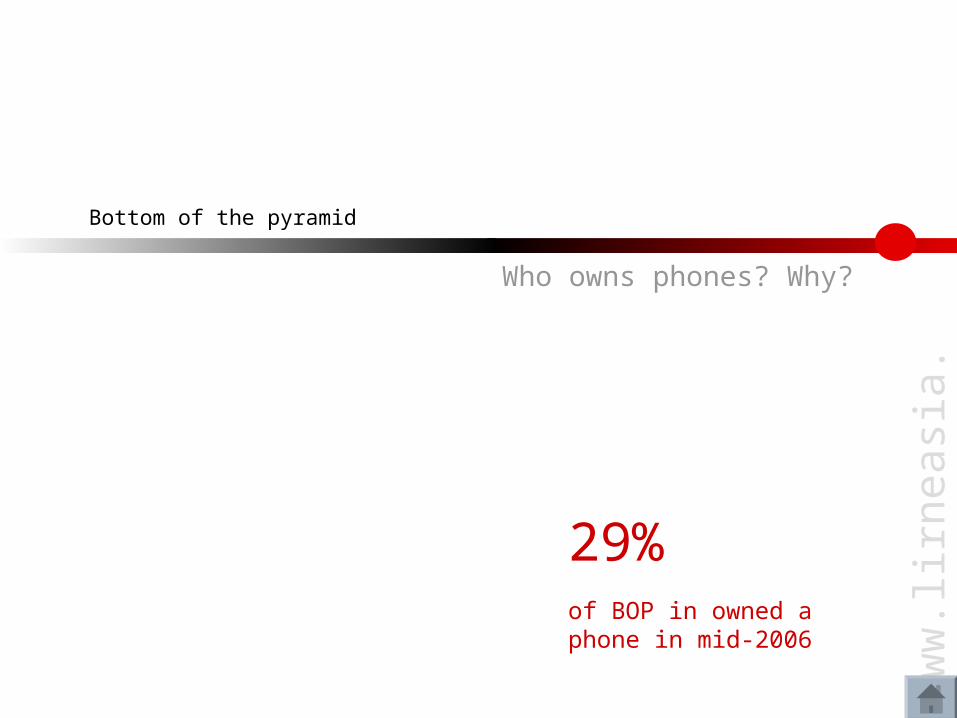

Who owns phones? Why?

29%of BOP in owned a phone in mid-2006

ww

w.li

rnea

sia.

net

Phone ownership: urban vs. rural

48%

22%

50%

63%

88%

24%16%

39%

61%

78%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

Country

Urban Rural

ww

w.li

rnea

sia.

net

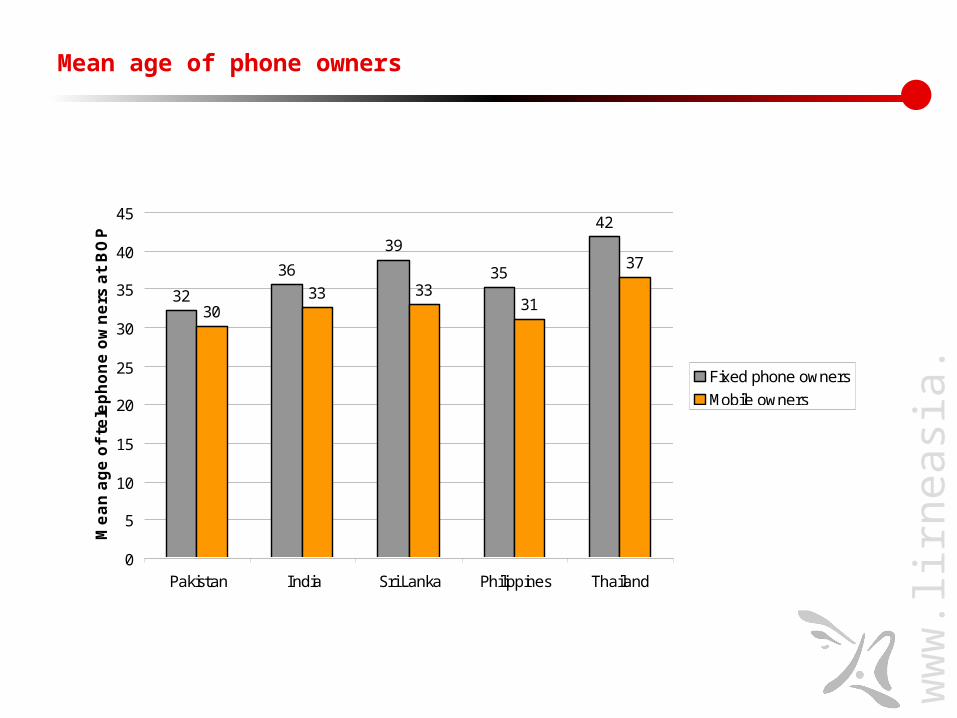

Mean age of phone owners

32

36

39

35

42

3033 33

31

37

0

5

10

15

20

25

30

35

40

45

Pakistan India Sri Lanka Philippines Thailand

Mean a

ge o

f te

lephone o

wners

at

BO

P

Fixed phone owners

Mobile owners

ww

w.li

rnea

sia.

net

Why own a mobile phone?

Convenience is key

Primary reason for choosing to own a mobile

64%71% 66% 68%

92%

11%6%

9% 5%

7% 4%

20%17%

18% 16%

4%10%

3%7%

1%1%

0%

20%

40%

60%

80%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f mob

ile o

wne

rs a

t the

BO

P Other

It is cheaper

For privacy

So I don’t depend onothers

Convenience: accessibileat any time

ww

w.li

rnea

sia.

net

Growth in mobile phone ownership at BOP since 2001

23%

9%22%

60%

76%

0%

20%

40%

60%

80%

100%

before2001

2001 2002 2003 2004 2005 2006(Q1&2)

Year during which connection was obtained

%(c

um

ula

tive

) at

BO

P

Pakistan India Sri LankaPhilippines Thailand

ww

w.li

rnea

sia.

net

Handsets: brand new vs. second-hand

36%28% 28%

40% 34%

64%72% 72%

60% 66%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f m

ob

ile o

wn

ers

at B

OP

USD 0

USD 20

USD 40

USD 60

USD 80

USD 100

USD 120

USD 140

USD 160

Ave

. pri

ce p

aid

fo

r h

and

set

using second-hand using brand new

ave.price paid for second hand ave. price paid for brand new

Handsets

ww

w.li

rnea

sia.

net

Who decides female ownership of phone at BOP? Patriarchal South Asia, more empowered women in Southeast Asia!

74%

9%

26%

91%

0%

20%

40%

60%

80%

100%

South Asia South East Asia

Male Female

% o

f fe

male

mob

ile o

wn

ers

at

BO

P

Who makes the decision to obtain a mobile

(among female mobile owners)?

ww

w.li

rnea

sia.

net

Primary reason for choosing to own a fixed phone

55%65%

60% 63%

80%

24%

18%

14% 8%

11%10%

7%6%

7%6%

17% 22%

1%

0%

16%

3%

0%

20%

40%

60%

80%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f fix

ed o

wne

rs a

t th

e B

OP Other

For privacy

So I don’t depend on others

It is cheaper

Convenience: accessibile at anytime

Why own a fixed phone?

ww

w.li

rnea

sia.

net

Older fixed connections

18%

11%

23%

7%

14%

0%

20%

40%

60%

80%

100%

before2001

2001 2002 2003 2004 2005 2006(Q1&2)

Year during which connection was obtained

%(c

um

ula

tive

) a

t B

OP

Pakistan India Sri LankaPhilippines Thailand

ww

w.li

rnea

sia.

net

Bottom of the Pyramid

BOP is prepaid

ww

w.li

rnea

sia.

net

Prepaid vs. postpaid mobile packages (among mobile owners)

Pakistan India Sri Lanka Philippines Thailand

Pre Paid 99% 95% 92% 99% 96%

Post Paid 1% 4% 8% 1% 4%

ww

w.li

rnea

sia.

net

Reason for choosing prepaid (rather than post-paid)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f p

rep

aid

mo

bile

ow

ner

s at

BO

P

Other

Lower per-minutecharges

No billing procedures

No monthly rentalcharge

To controlexpenditures

Reasons for choosing prepaid

Prepaid helps to ‘control expenditure;’ reasons are largely cost-related

ww

w.li

rnea

sia.

net

Time to travel to location where mobile owner can re-credit mobile

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Phillipines Thailand

% o

f p

rep

aid

mo

bil

e o

wn

ers

at

BO

P

More than anhour

About 60minutes

About 30minutes

About 15minutes

About 10minutes

About 5 minutes

About 2 minutes

ww

w.li

rnea

sia.

net

Bottom of the pyramid

SMS use and its relative cost

ww

w.li

rnea

sia.

net

Use of SMS at the bottom of the pyramid

50

35

60

100

30

0102030405060708090

100

% o

f m

ob

ile o

wn

ers

at

BO

P t

ha

t u

se

SM

S

Pakistan India Sri Lanka Philippines Thailand

Lowest SMS prices ‘SMS capital of the world’

ww

w.li

rnea

sia.

net

Frequency of SMS use

Frequency of SMS use (DE)

50%

65%

40%

70%

0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand

% o

f m

ob

ile

ow

ner

s

Never

Less than once a month

At least once a month

At least once a w eek

Daily

ww

w.li

rnea

sia.

net

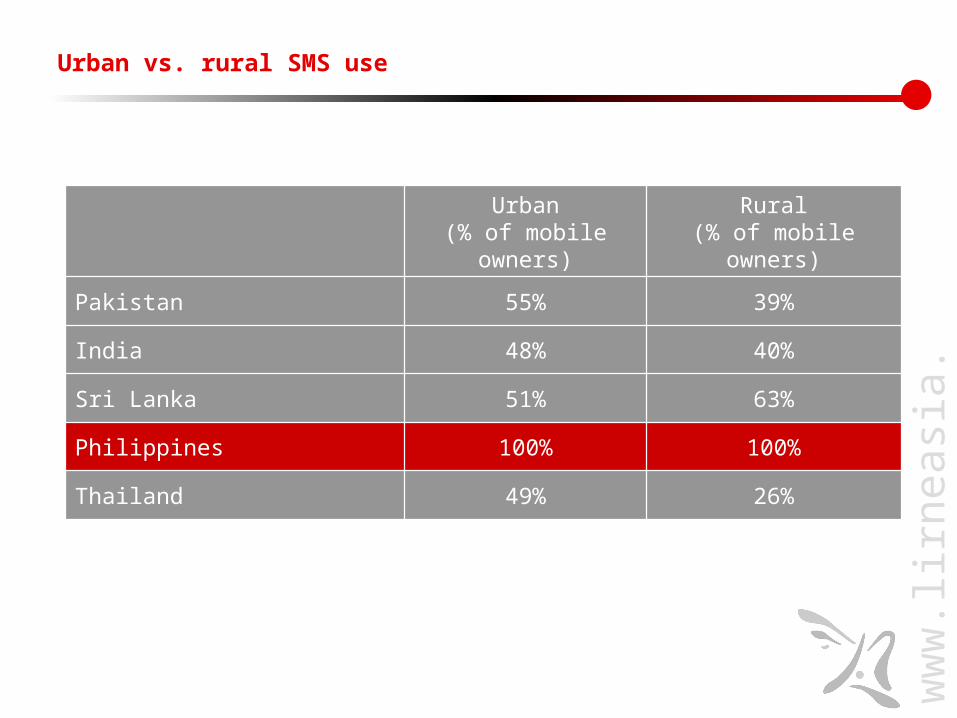

Urban vs. rural SMS use

Urban(% of mobile

owners)

Rural(% of mobile

owners)

Pakistan 55% 39%

India 48% 40%

Sri Lanka 51% 63%

Philippines 100% 100%

Thailand 49% 26%

ww

w.li

rnea

sia.

net

Call vs. SMS charges: Prepaid

Prepaid charges (USD)

Pakistan: Jazz Budget*

India: Airtel regular*

Sri Lanka: Dialog KIT standard

Philippines: Smart TnT

Charge per minute

Call to mobile on-net 0.030 0.030 0.063 0.119

Call to mobile off-net 0.041 0.049 0.063 0.141

Charge per SMS 0.014 0.030 0.018 0.022

* Call charges weighted for local and national calls

•Charges as at June 2007

•Packages selected based on lowest connection charge package of the largest operator

Low cost of SMS in the Philippines compared to India, but also higher literacy, Roman-based language and facility in using SMS

ww

w.li

rnea

sia.

net

Bottom of the pyramid

Missed calls

ww

w.li

rnea

sia.

net0%

20%

40%

60%

80%Pakistan

India

Sri LankaPhilippines

Thailand

Use of missed calls by mobile ow nersat BOP

Use of missed calls by f ixed phoneow ners at BOP

Use of missed calls: by mobile and fixed phone owners!

Missed calls used just as much in the SEC A,B & C samples

ww

w.li

rnea

sia.

net

Use of 'missed calls' to minimise communication costs

0%

10%

20%

30%

40%

50%

60%

70%

Pakistan India Sri Lanka Philippines Thailand

% o

f B

OP Male

Female

Use of missed calls: Males vs. females

ww

w.li

rnea

sia.

net

Other strategies

Use of 'strategies' to minimise call costs

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Make calls at off-peak hours (allowners)

Use phone as an incoming deviceonly (all owners)

Mobile to mobile calls only (all owners)

Fixed to fixed calls only (all owners)

Pakistan India Sri Lanka Philippines Thailand

ww

w.li

rnea

sia.

net

Bottom of the Pyramid

Getting connected

115 millionfrom BOP will get connected between mid-2006 & mid-2008

ww

w.li

rnea

sia.

net

Don't own and don't

plan to buy: 41.7%

(165 m)

Don't own but plan to buy:

28.9 %(115 m)

Already own a phone 29.4 %(116 m)

Those that planned to get connected between mid-2006-2008

Prospective owners

ww

w.li

rnea

sia.

net

Projected BOP penetration

36%

19%

41%

62%

77%

70%

50%

72%78%

86%

0

25

50

75

100

125

150

Pakistan India Sri Lanka Philippines Thailand

Con

nect

ion

s at

BO

P (

mill

ions

)

0%

20%

40%

60%

80%

100%

% o

f ho

useh

olds

at

BO

P w

ith a

tel

epho

ne

Already own something Don't own but plan to buy

Current ownership at BOP (%) Penetration at BOP by mid 2008

ww

w.li

rnea

sia.

net

Most would use phone for emergency communication & keeping in touch

What respondent would use the phone for if given one at an affordable rate

84%

69%

44%

58%

50% 52%57%

17%13%

26%

11%

21%

10%

18%

5% 3%2% 1% 2% 1%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Pakistan India Sri Lanka Philippines

% o

f re

spo

nd

ents

To keep in touch with family andfriends

Only in an emergency

For networking

To enhance my income

Other

ww

w.li

rnea

sia.

net

Type of phone prospective owners would buy

23% 29%

52%

8%

68%67%

40%

91%

9% 4% 7% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines

Not decided yet

Mobile

Fixed phone

Type of phone that prospective owner would buy

ww

w.li

rnea

sia.

net

Bottom of the Pyramid

Not getting connected

165 millionfrom BOP will not get connected between mid-2006 & mid-2008

ww

w.li

rnea

sia.

net

The biggest barrier to ownership at the BOP is affordability

29% plan to get connected between mid-2006 and mid-2008

Potential primary

market for telecenters

BUT, 42% will not

Don't own and don't

plan to buy: 41.7%

(165 m)

Don't own but plan to buy:

28.9 %(115 m)

Already own a phone 29.4 %(116 m)

ww

w.li

rnea

sia.

net

What do we know about this group?

The large majority will be rural

42%53%

14%

46%

8%

58%47%

86%

54%

92%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand% o

f non-o

wners

at

BO

P w

ho d

o n

ot

pla

n t

o b

uy

a

phone

Rural

Urban

ww

w.li

rnea

sia.

net

50%

67%

45%57%

16%

13%

19%

39% 22%

79%

25%

12%15%

13% 14%4% 7% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pakistan India Sri Lanka Philippines Thailand% o

f non-o

wners

at

BO

P w

ho d

o n

ot

pla

n t

o b

uy

a

phone Above 3rd quartile

Median-3rd quartile

1st Quartile-median

Below 1st Quartile

What do we know about this group?

Poorer. E.g. The large majority will have monthly household incomes below USD 75.81

ww

w.li

rnea

sia.

net

Bottom of the pyramid

Benefits of access to telecom?

ww

w.li

rnea

sia.

net

Efficiency of daily activities

BOP in all countries sees efficiency

Efficiency of daily activities

1 2 3 4 5

India (3.90)

Sri Lanka (3.98)

Pakistan (4.17) Thailand (4.37)

Philippines (4.40)

worsened slightly worsened

no change somewhat improved

improved

ww

w.li

rnea

sia.

net

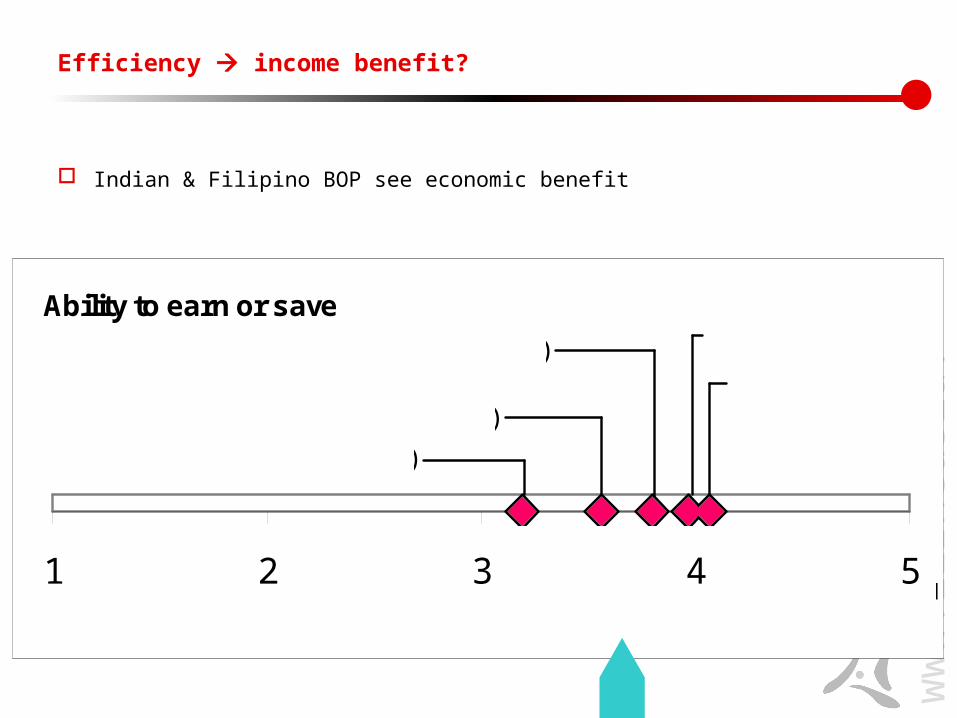

Efficiency income benefit?

Indian & Filipino BOP see economic benefit

Ability to earn or save

1 2 3 4 5

Sri Lanka (3.19)

Thailand (3.56)

Pakistan (3.80) India (3.97)

Philippines(4.07)

worsened slightly worsened

no change somewhat improved

improved

ww

w.li

rnea

sia.

net

But, sense of security is main perceived benefit

Ability to act in an emergency is key

Ability to act in emergency

1 2 3 4 5

India (4.28)

Pakistan (4.48)

Sri Lanka (4.58)

Philippines (4.63)

Thailand(4.83)

worsened slightly worsened

no change somewhat improved

improved

ww

w.li

rnea

sia.

net

Keeping in touch is important

Family and social relations

1 2 3 4 5

India (4.14)

Pakistan (4.30)

Sri Lanka (4.35)

Philippines (4.45)

Thailand(4.66)

worsened slightly worsened

no change somewhat improved

improved

ww

w.li

rnea

sia.

net

Social status and recognition improves in all countries except LK

Social status and recognition

1 2 3 4 5

Sri Lanka(3.47)

India(4.03)

Pakistan(4.05)

Thailand

(4.28)

Philippines(4.29)

worsened slightly worsened

no change somewhat improved

improved

`

ww

w.li

rnea

sia.

net

Bottom of the pyramid

Internet…what Internet?

ww

w.li

rnea

sia.

net

Internet use at the BOP

Pakistan India Sri Lanka Philippines Thailand

Use the Internet1.9% 0.3% 1.5% 8.8% 10.4%

Large gender divide exists, even in South East Asia: for e.g.11.9% of Filipino men at BOP use the internet, but only 5.7 of Filipino women at BOP use the internet

0.5%

2.2%

11.9%

13.6%

0.8%0.1%

2.9%

0.9%

5.7%

7.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Pakistan India Sri Lanka Philippines Thailand

% a

t B

OP

Male

Female

ww

w.li

rnea

sia.

net

Internet use at the BOP cont’d

3.0%

0.2%

2.1%

12.8%

22.0%

0.7%0.1%

1.4%

4.3%

2.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Pakistan India Sri Lanka Philippines Thailand

% a

t B

OP

UrbanRural

Large urban-rural divide also exists in Internet use at the BOP across all five countries

ww

w.li

rnea

sia.

net

Internet awareness at the BOP

Internet awareness at the BOP is poor, especially in South Asia; 36% of Pakistanis at the BOP have not heard of the Internet before.

36.0%

71.9%

28.6%

14.3%

35.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Pakistan India Sri Lanka Philippines Thailand

% o

f bo

ttom

of th

e py

ram

id

Not heard of Internet

ww

w.li

rnea

sia.

net

To Sum up

Access to telecoms is high, though ownership is low

People at the BOP are creative and have various strategies in using telecoms: SMS, missed calls, prepaid, use of second hand handsets, etc

Many people at the BOP prefer the mobile, and use prepaid

High access and use means people are familiar with the technology and thus a platform that can be used in developing services that targets people at the BOP

Examples of SMS use from the Philippines

ww

w.li

rnea

sia.

net

Examples of SMS Use in the Philippines

DOST’s ICT4D cases on Governance Education Social services Commerce

Institute of Popular Democracy’s use of SMS in election monitoringAmong Ed and Grace Padaca, the good and the badOverseas Filipino Workers SOS Project

ww

w.li

rnea

sia.

net

SMS use in the Philippines

ww

w.li

rnea

sia.

net

SMS use in the Philippines

Institute for Popular Democracy’s SMS-based system for anti-poll fraud and election monitoring (May 2007 elections) In the context of rampant vote-buying and cheating, make citizens

guard their votes and return credibility to the system AppliedTechnologies and Information Solutions (ATIS) at

www.atis.com.ph Citizens registered before the elections and send SMS to a designated

number, which are complied in a data base On election day, about almost a hundred messages from local

partners in different provinces were registered in the system. Half of these were verified to contain reliable information on vote-buying, ballot snatching, and election-related threats and violence.

Reports complied in a database and forwarded to the Commission of Elections (COMELEC) and other concerned agencies for action

ww

w.li

rnea

sia.

net

SMS use in the Philippines

Among’s Ed’s (Eddie Panlilio) gubernatorial campaign http://amonged.org/

ww

w.li

rnea

sia.

net

ww

w.li

rnea

sia.

net

SMS Use in the Philippines

Grace Padaca’s campaign

ww

w.li

rnea

sia.

net

SMS use in the Philippines

OFW SOS-SMS project Launched in February 2006, spearheaded by Center for

Migrant Advocacy (CMA) and testing, set-up and database managed by Institute for Popular Democracy

Based on system developed by Filipino workers in the Gulf area during Gulf war

6 months after launch, over 800 messages received , which are automatically transmitted to the Department of Foreign Affairs, Overseas Workers Welfare Administration and Center for Migrant Advocacy

as of April 2007, system helped facilitate the return of 215 Filipinos working overseas who were abused or maltreated by employers

IPD enhanced the system, built the database and distribution mechanism to respective government agencies

ww

w.li

rnea

sia.

net

In sum…

People at the BOP uses telecoms, frugally, intelligently and creatively

Many are using mobile phones and are planning to get connected

Philippines – SMS use in mobilisation, empowering people, connecting people But same tools can also be used for rumor

mongering and to sow misinformation

ww

w.li

rnea

sia.

net

Conclusions

Thus, activists, NGOs, governments should creatively think of how to incorporate the use of mobiles and appropriate ICTs in their work, projects, and campaigns

Bearing in mind of course that social and cultural contexts frame how people adopt and utilise technologies

ww

w.li

rnea

sia.

net

Thank you very much for your attention!

Comments and questions?