x l annual report - engie fabricomengineering database smartplant: the introduction of smartplant...

TRANSCRIPT

Annual Report2009

S

M

L

XL

www.fabricom.no

2 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

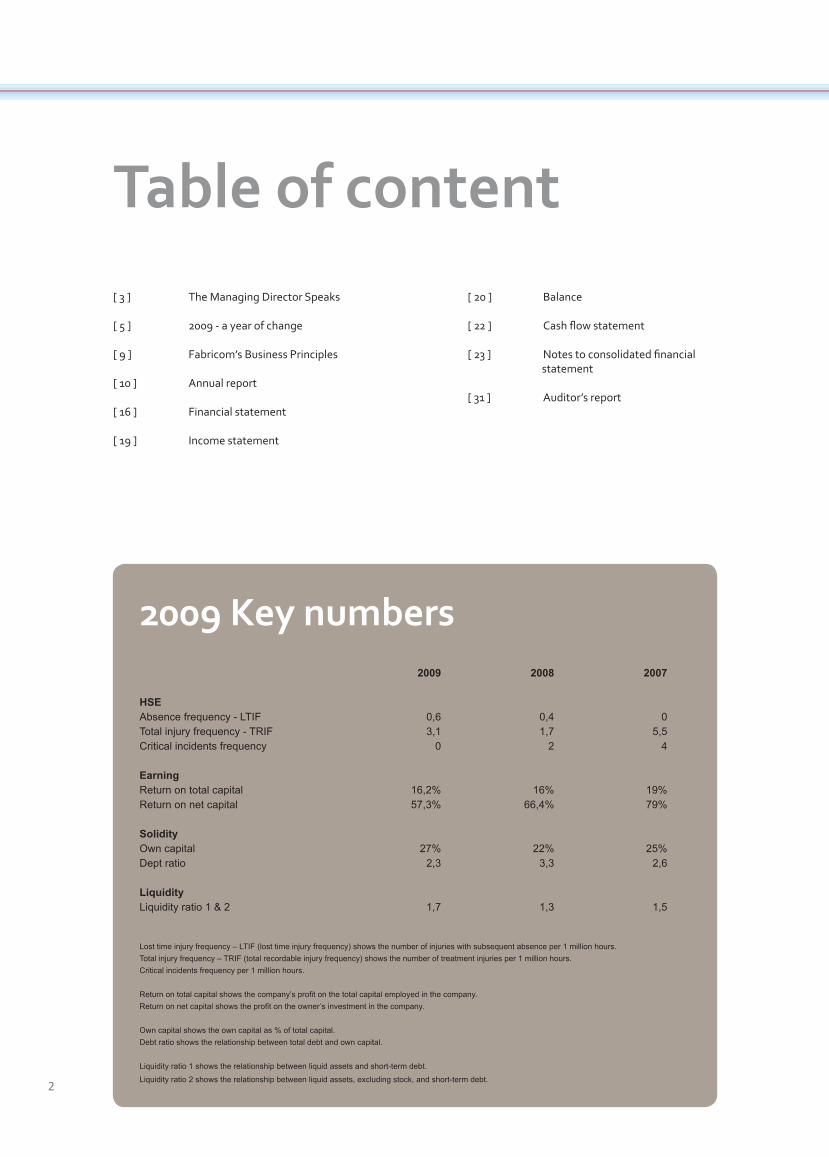

Table of content[ 3 ] The Managing Director Speaks

[ 5 ] 2009 - a year of change

[ 9 ] Fabricom’s Business Principles

[ 10 ] Annual report

[ 16 ] Financial statement

[ 19 ] Income statement

2009 2008 2007

HSEAbsence frequency - LTIF 0,6 0,4 0Total injury frequency - TRIF 3,1 1,7 5,5Critical incidents frequency 0 2 4

EarningReturn on total capital 16,2% 16% 19%Return on net capital 57,3% 66,4% 79%

SolidityOwn capital 27% 22% 25%Dept ratio 2,3 3,3 2,6

LiquidityLiquidity ratio 1 & 2 1,7 1,3 1,5

Lost time injury frequency – LTIF (lost time injury frequency) shows the number of injuries with subsequent absence per 1 million hours.Total injury frequency – TRIF (total recordable injury frequency) shows the number of treatment injuries per 1 million hours.Critical incidents frequency per 1 million hours.

Return on total capital shows the company’s profit on the total capital employed in the company.Return on net capital shows the profit on the owner’s investment in the company.

Own capital shows the own capital as % of total capital.Debt ratio shows the relationship between total debt and own capital.

Liquidity ratio 1 shows the relationship between liquid assets and short-term debt.

Liquidity ratio 2 shows the relationship between liquid assets, excluding stock, and short-term debt.

2009 Key numbers

[ 20 ] Balance

[ 22 ] Cash flow statement

[ 23 ] Notes to consolidated financial statement

[ 31 ] Auditor’s report

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 3

S

M

L

XL

The Managing Director Speaks2009 was another year of great results for Fabricom AS. Projects which were awarded in the period 2007-2008 were all active through the year, or at least part of the year and that secured a great economic result.

However, the turn of the year 2008-2009 was an turning point for the prosperity of the market, and the start of a significant upheaval in the oil and gas industry. A considerable fall in the oil price gave the oil companies an opportunity to review their project and cost control. The net result of this process was the postponement of undeveloped projects and requirements for efficiency and productivity improvements in new projects.

Fabricom met this new “era” with a thorough process of strategy which established ambitious goals and internal requirements for improvements.

The oil companies started sending out project inquiries in the latter part of 2009. Many of these will be awarded late in 2010. The competition is considerably tougher and the ability to meet the new client requirements will decide who will be successful after this period of few project awards and low activity.

Fabricom has already had success by winning a short-term M&M contract for Snorre and Statfjord, but we still need to win new contracts.

2010 is excepted to be a challenging year for our line of business, but hopefully it will open for new long term contracts which create opportunities for growth for Fabricom.

““

Fabricom met this new “era” with a thorough process of strategy

which established ambitious goals and internal requirements

for improvements.

4 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 5

S

M

L

XL

To meet the new market constraints Fabricom started a comprehensive strategy process in the fall of 2008 which was named 4ward 2012.

4ward 2012

Initially, a comprehensive analysis of Fabricom’s business, as well as national and international relations which influenced the company’s business, was undertaken. In this process Fabricom were assisted by external consultant companies in combination with an extensive meeting activity with the company’s key-clients to identify improvement requirements in connection with

2009 – a year of change

existing business, in addition to developing new complementary business areas.

In January 2009 the company gathered more than fifty leaders to go through the current research work. The goal with this gathering was among other things, to engender an understanding of the challenges Fabricom were facing and to identify and prioritize the necessary improvement initiatives. The result of this gathering was an important foundation for the detailing of the company’s revised strategy plan which was completed in April 2009.

Competence ProceduresCore business & strategic goals Culture Tools, methodes

& systems

After years of significant growth and the associated shortage of resources the year 2009 was a year where few new contracts within the core business lines of Fabricom were introduces to the market. This was directly connected to the financial crisis which among others resulted in a drop in the oil-price from over 140$/barrel to less than 40$/barrel in the period from July 2008 to February 2009.

6 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

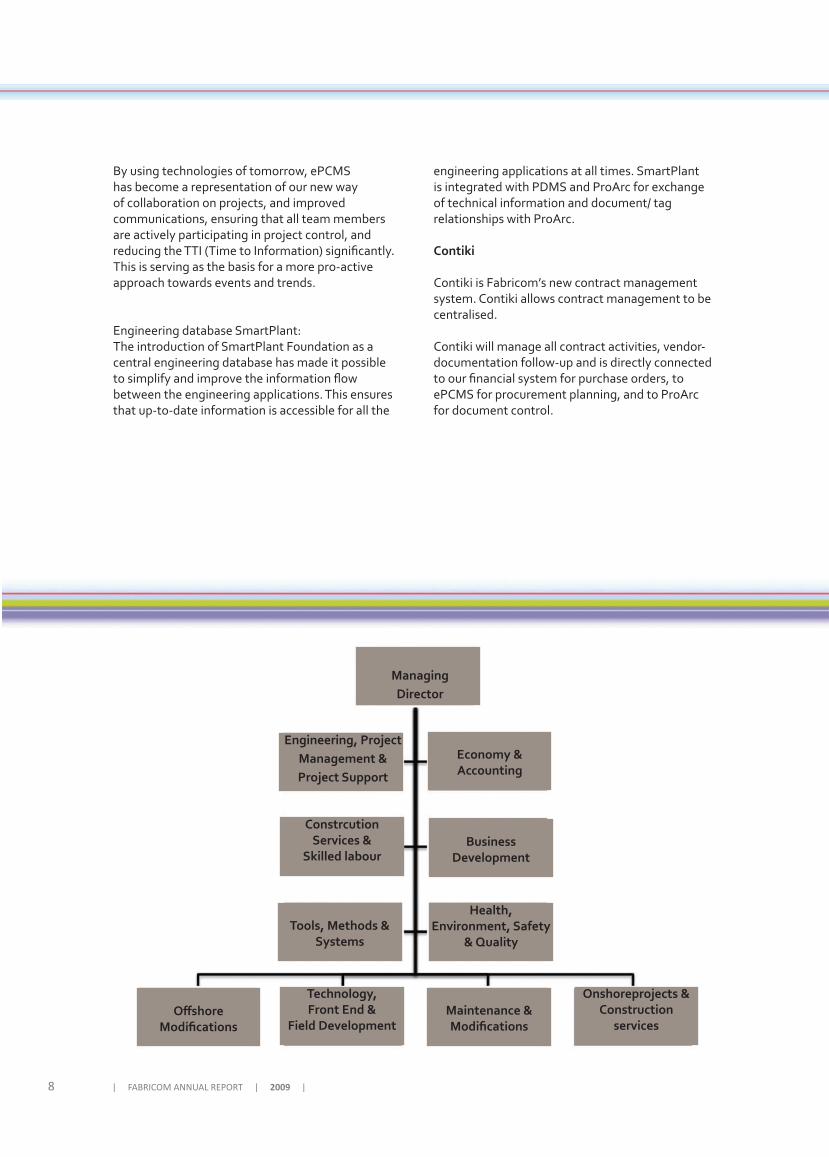

In the new business model Fabricom chose to separate business areas and supporting functions.

The business areas comprise:

• Technology, Front-End & Field Development• Offshore Modification• Modifications & Maintenance• Onshore Projects & Construction Services

These business areas have independent responsibility for tendering and executing work within their business areas. To ensure that these business areas have the necessary frame work to win new projects and execute these according to internal and external requirements and expectations, Fabricom has established the following supporting functions:

• Engineering, Project Management & Project Support

• Construction Management & Operators• Tools, Methods & Systems• Health, Environment, Safety & Quality• Economy and Accounting• Business Development

Programs of improvements

In connection with the strategy plan 4ward 2012 an improvement program, which included a significant number of isolated improvement projects was established. The following describes some of the more important improvement projects.

The strategy process resulted in the following primary improvement goals:

• Improve the company’s execution within business operations and projects

• Secure upcoming M&M contracts• Expand value chain and branch into new

business areas.• Secure a favourable position in the expected

forthcoming industry consolidation

To realize these strategy goals it was found necessary to change Fabricom’s business model / organizational structure and to implement a comprehensive improvement program. New business model / organizational structure

As a foundation for the choice of the new business model, the following were amongst the issues taken into consideration:

• Our clients ask for better project delivery• Our employees ask for a strong and clear

management group• Our owners want the company to grow in both

existing and new markets• Our strategy requires a greater capacity, new

competence and better work processes• We need to have clear roles and distribution of

responsibility across the company• We see vast development potential with better

use of the knowledge and skills within the existing organization

1.• Internal

Analysis• Decision of

change

2.• Client Surveys• Market Analysis• Competition

Analysis

3.• Setting Goals• Choice of Stragegy

4.• Implementation

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 7

S

M

L

XL

Project support:Tools, methods

& systems

Resources:Projecting, project

management & project support

Business development:Tender support, communication

& marketingHSE&Q:

Health, safety, environment& quality

Economy:Economy, finances &

business control

Client

Fabricom projects

Resources:Construction management

& workers

4You

4You was created to improve the foundation for a goal-oriented development of the working environment in Fabricom. 4You includes among other things, development of improved work processes and diverse training initiatives. Initial training is related to how to handle disagreements and discussions to prevent and end potential ongoing conflicts.

In this regard seminars in both Norwegian and English for employees and agency personnel are being held. This work is backed up by Fabricom’s

intranet, myFabricom, which provides a common platform for publishing governing documentation, as well as sharing knowledge and experience across the company’s different business areas and projects.

ePCMS

As a part of the continuous improvements of the project control applications, we have developed a new system, ePCMS (efficient Project Controls Management System). The main functions in ePCMS are integrated reporting, both internal and to clients, centralized maintenance of CTR’s and norms for engineering and construction, and the support of interaction in connection with project control in the project organizations.

ePCMS can also be presented through a dashboard. The purpose of this is to give the management a total overview of project status and to effectively make visible information such as performance, trends, KPIs, progress and prognoses. This can be done on at project level and lower levels, down to individual CTR’s. This reporting is based on the collation and analysis of data collected from all the project control applications.

8 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

By using technologies of tomorrow, ePCMS has become a representation of our new way of collaboration on projects, and improved communications, ensuring that all team members are actively participating in project control, and reducing the TTI (Time to Information) significantly. This is serving as the basis for a more pro-active approach towards events and trends.

Engineering database SmartPlant:The introduction of SmartPlant Foundation as a central engineering database has made it possible to simplify and improve the information flow between the engineering applications. This ensures that up-to-date information is accessible for all the

ManagingDirector

Economy & Accounting

Engineering, Project Management & Project Support

Constrcution Services &

Skilled labourBusiness

Development

Health, Environment, Safety

& QualityTools, Methods &

Systems

Offshore Modifications

Technology, Front End &

Field DevelopmentMaintenance & Modifications

Onshoreprojects & Construction

services

engineering applications at all times. SmartPlant is integrated with PDMS and ProArc for exchange of technical information and document/ tag relationships with ProArc.

Contiki

Contiki is Fabricom’s new contract management system. Contiki allows contract management to be centralised.

Contiki will manage all contract activities, vendor-documentation follow-up and is directly connected to our financial system for purchase orders, to ePCMS for procurement planning, and to ProArc for document control.

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 9

S

M

L

XL

THE FABRICOM BUSINESS PRINCIPLES

HEALTH, SAFETY AND ENVIRONMENT

In all our activities we will focus on HSE in order to be the leader in our industry, through

our experience, attitude and behaviour. We must have a culture which promotes a good

HSE practice.Goal: We shall have no personnel injuries, no

damage to property or the environment and reduced sickness absence.

ETHICS

Every individual acting on behalf of Fabricom shall do this according to the highest ethical standards, within the law and in compliance

with the ethical guidelines of Fabricom.Goal: We shall always act in compliance

with the ethical guidelines of Fabricom to promote honesty, integrity and loyalty.

Corruption and bribery shall not occur in our business activity.

PEOPLE AND WORKING TOGETHER

Our personnel and their competence are the company’s most important asset. We

must have a culture which stimulates their commitment and their desire to work.

We must work together to ensure we are effective and that we take care of, and

develop, the human and social resources and values. We must make time for open

communication on the relevant goals, actions and occurrences.

Goal: We shall be a preferred employer and our culture shall promote wellbeing, a sense of

belonging and togetherness.

QUALITY

We must supply services and products in a safe manner, on time, within budget and to the

expected quality.Goal: We shall do everything right, first time.

CUSTOMERS

Our relationship with our customers must be a cooperation based on mutual respect,

openness and trust. By doing so, we will add value for our customers and

ourselves.Goal: We shall be the preferred supplier for

our customers.

FINANCES

Our finances are a shared responsibility. We must achieve financial results which meet our owners’ expectations, which secure our jobs and which generate

organic growth and possibilities for new investment.

Goal: We shall always be competitive and effective and we shall achieve results

which fulfil the requirements of our owners and the expectations of our employees.

CORPORATE AND MARKET DEVELOPMENT

We are a Norwegian knowledge-based company and contractor that will always evaluate the possibilities for growth in

our market segments and, consequently, we will be able to offer more services to our customers and broader career

opportunities for our employees. We must be familiar with market developments so

that we can always be at the forefront. We must retain and grow our market share

within the oil and gas industry, and use this as a springboard for other opportunities.

Goal: We shall be one of the most important players within our market segments.

10 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

Annual Report 2009

The Company’s activities and locationsGroup Fabricom includes the parent company Fabricom AS and subsidiaries Fabricom PMAE AS, Fabricom Nord AS, Fabricom Vigor AS and VM Alliansen DA. VM Alliansen DA does not employ any personnel.

Fabricom (Company and Group) performs engineering, modification, maintenance and installation work for the oil and gas industry for both onshore and offshore plants and installations. Fabrication work is carried out at workshops in Dusavik, Stavanger, Frakkagjerd outside Haugesund and at Grønøra in Orkanger. The business is managed from the group’s head

office in Stavanger and local branches in Tysvær, Trondheim, Orkanger and Hammerfest. All other subsidiaries are managed from the Stavanger head office. .

During Spring 2009 the business was reorganised in order to improve internal processes and to improve our market profile towards customers. Following this reorganisation Fabricom (Company and Group) now has 4 business areas (Maintenance & Modifications, Offshore Modifications, Onshore Contracts and Technology, Front End & Field Technology). Figure 1 shows the activity in these business areas for 2009 and 2008 (2008 numbers are reallocated).

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 11

S

M

L

XL

2009 was a year of uncertainty in the market; Fabricom’s total activity was lower than that for previous years. In 2009 Fabricom (Company and Group) produced a total of 1 497 000 hours compared to 2 494 000 hours in 2008. Despite less overall activity than previous years the company has achieved close to full utilisation of staff in 2009, except at the beginning of the year. This lower activity resulted in a declining use of hired-in personnel throughout the year. The total number of staff in the Group has been stable throughout 2009 and by the end of the year Fabricom had increased the number of employed engineers.

2009 activities all took place in Norway and offshore on the Norwegian Continental shelf with 36 % for onshore projects and 64 % for projects offshore on the Norwegian continental shelf. Equivalent numbers for 2008 were 42% onshore and 58% offshore.

Main activities Fabricom’s operational areas (company and group) are onshore and offshore modification and maintenance work in Norway, with Fabricom

taking total responsibility for planning, engineering, fabrication, installation and commissioning work. In addition Fabricom (Company and Group) performs studies, FEED (Front End Engineering Design), detail engi-neering services and maintenance activities for the oil and gas industry in Norway.

Fabricom finalized a revised company strategy early in 2009 which resulted in a restructuring of the company’s (and group) main activities into 4 business areas. The main activities within these areas of operations were:

1. Maintenance & ModificationMaintenance & Modifications (V&M) was established as a business area to provide our customers with delivery of V&M commissions on long term contracts. The GEM M&M contract for ConocoPhillips Norway was included in the contract portfolio. This contract originally expired on 31.12.2009 but the duration was extended to 31.08.2010 for smaller projects and closeout activities. The GEM contract was 97% completed by the end of the year.

Figure 1: Activity split in business areas in 2009 and 2008.

Offshore Modifikasjon

Onshore

Teknologi & FEED

V&M

43 %

36 %

19 %

3 %

2009

Offshore Modifikasjon

Onshore

Teknologi & FEED

V&M

34 %

47 %

18 %

1 %

2008

12 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

Following this Fabricom have developed strategic plans and improvements to win new contracts within this business area. During 2009 Fabricom was prequalified to compete for Statoil’s frame agreements for V&M contracts on installations both on the Norwegian continental shelf and onshore. These represent a total contract portfolio of 45 billion NOK. In December 2009 Fabricomreceived the ITT’s from Statoil for a significant share of this portfolio. Fabricom’s tenders were delivered February 2010 and the contracts will be awarded in the middle of 2010.

In the first quarter of 2010 Fabricom was awarded an assignment for time limited Modification capacity for installations on Snorre and Statfjord. The value of this ssignment is estimated at approximately NOK159 million over a 12 month period. The future prospects for V&M activities are promising.

2. Offshore ModificationsAssignments for implementation of modification projects on offshore installations are carried out by “Offshore Modifications”. In 2009 two large projects were ongoing within this business area, Valhall Redevelopment and Snorre Redevelopment.

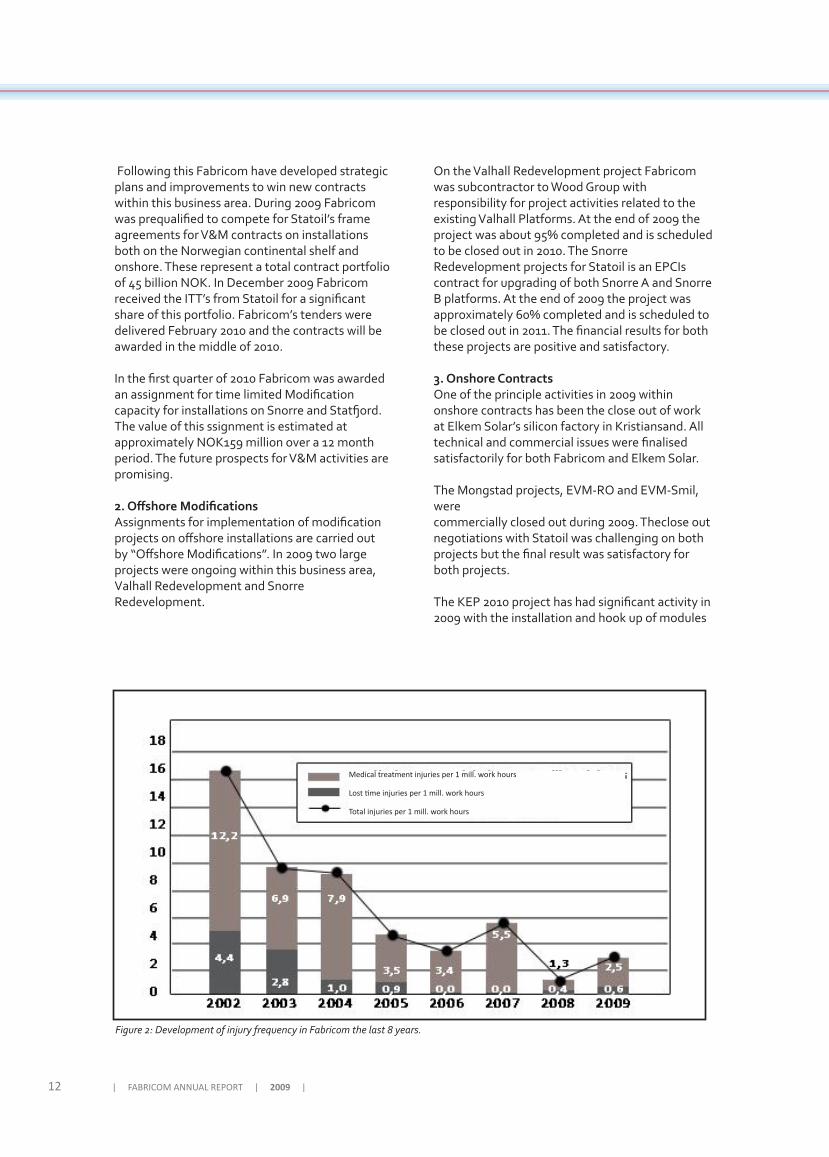

Figure 2: Development of injury frequency in Fabricom the last 8 years.

Medical treatment injuries per 1 mill. work hours

Lost time injuries per 1 mill. work hours

Total injuries per 1 mill. work hours

On the Valhall Redevelopment project Fabricom was subcontractor to Wood Group with responsibility for project activities related to the existing Valhall Platforms. At the end of 2009 the project was about 95% completed and is scheduled to be closed out in 2010. The Snorre Redevelopment projects for Statoil is an EPCIs contract for upgrading of both Snorre A and Snorre B platforms. At the end of 2009 the project was approximately 60% completed and is scheduled to be closed out in 2011. The financial results for both these projects are positive and satisfactory. 3. Onshore ContractsOne of the principle activities in 2009 within onshore contracts has been the close out of work at Elkem Solar’s silicon factory in Kristiansand. All technical and commercial issues were finalised satisfactorily for both Fabricom and Elkem Solar.

The Mongstad projects, EVM-RO and EVM-Smil, were commercially closed out during 2009. Theclose out negotiations with Statoil was challenging on both projects but the final result was satisfactory for both projects.

The KEP 2010 project has had significant activity in 2009 with the installation and hook up of modules

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 13

S

M

L

XL

and prefabricated items delivered from Belgium to the plant on June 1st 2009. 250 people has at the highest been involved in the project. The project is scheduled to be completed by the end of 2010.

4. Technology, Front End and Field developmentAll Fabricom deliveries for early phase studies are undertaken by the business area “Technology, Front End & Field Development”. The goal of this group is to increase the focus on Engineering serv-ices for front end studies, field development stud-ies and studies for onshore plants and also to be a contributor of technology development within our core business areas.

In order to achieve the ambitious goals for this business area, Fabricom has established a separate organisation. This organisation comprises a group of highly qualified Senior Engineers with significant knowledge and experience of leading contracts for such studies. These Contract Leaders will provide continuity to our customers, ensure that ongoing

assignments are properly manned and that best practice, knowledge and experience are incorporated and used efficiently.

In 2009 Fabricom had the following assignments for this business area:

• Concept Study for Veslefrikk Drilling Upgrade with KCAD/RDS

• Technical engineering support to Talisman for the YME field development project.

• Technical engineering support on smaller specialised assignments for Marathon, Cono-coPhillips and Statoil.

In addition Fabricom has established strategic cooperation arrangements with several specialized engineering companies to offer a broader competence range to our clients. Our competence range now covers all areas of relevance to a field study and all relevant competence areas for studies on upstream land facilities.

Tendering activities throughout 2009 have been fairly low since several planned projects have been postponed by clients. At the end of the year tendering activity increased and Fabricom has devoted considerable resources to tendering activi-ties in this period.

Foto: StatoilHydro

14 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

In 2009 several projects were either closed out or were near to close out. As a result of this and low tendering activity, Fabricom (Company and Group) has a reduced order reserve at the end of 2009. Tendering activities are expected to be fairly high throughout 2010 and Fabricom (company and group) expect an increase in the order reserve during the year.

The subsidiaries Fabricom PMAE AS and Fabricom Nord AS are part of the legal structure of the Group but do not represent separate business areas.

OwnershipFabricom AS (Company and Group) is owned 100 % by the Dutch holding company Fabricom Neder-land B.V. This company is a part of the Belgium Group Fabricom which in turn is owned by the French multinational industrial enterprise. GDF Suez has a total of 190 000 employees world-wide and the company delivers solutions globally within the areas of oil and gas production, energy distribu-tion, water and waste management.

The owner’s aim is to take advantage of synergy effects in the GDF Suez through international co-operation and sharing of experience. The GDF Suez’ total resources, competence and products are therefore available to Fabricom (company and group) to facilitate growth and development in the Norwegian market.

Fabricom (company and group) in Norway is part of the Group’s international division, Fabricom Oil, Gas & Power, performing work together with:

• Fabricom Oil and Gas (Holland) which specializes in both on-and offshore drilling and modification work• Fabricom Contracting Ltd. (UK) which

specialises in onshore refinery and petro- chemical works as well as module fabrication

• Fabricom Offshore Services LTD (FEED studies, and engineering for the oil and gas industry)

• Fabricom in Belgium which specialises in piping fabrication, prefabrication of modules and installation work• Fabricom Netherland which specialises in

providing services and maintenance to the oil and gas industry

Synergies between the companies in this division ensure transfer of international competence and experience for the benefit of our clients in the oil and gas industry both onshore and offshore.

Continued activityContinued activity is assumed for Fabricom (Company and Group) and the financial statements for 2009 have been prepared based upon this assumption.The Board confirms that the financial statements give a true picture of properties, debts, financial position and results.

Safety and working environmentIn 2006 Fabricom became an IA company (Inkluderende Arbeidsliv). The company works actively to ensure low absence due to sickness and the IA agreement is a part of this strategy. In 2008, total sickness absence in Fabricom (company and group) was 5,0% (compared to 2,8% in 2007). The increase compared to last year was caused by several factors, including unfavourable, imposed, working schedules for work at onshore plants. The level of sickness absence is however not particularly high in comparison with other companies with a similar activity profile.

Fabricom (Company and Group) has a target of zero injuries to people and the environment. The frequency target for number of LTI’s (Lost Working Time Injuries) follows the primary target

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 15

S

M

L

XL

and is therefore zero. The company’s objective is to avoid injuries to personnel at all times.

During 2009 one LTI and four medical treatment injuries were registered. At the end of the year the LTIF (Lost Work Time Frequency) was 0,6 per Million work hours, while the TRIF (Total Recordable Injury Frequency) was 3,1 per million work hours. The result on TRIF is the second best result ever for Fabricom.

Fabricom’s (Company and Group) Management are aware of the potential safety risks connected to our activities. Therefore we will continue to increase our efforts to develop safe working methods, to invest in new and proper equipment and, not least, to continue to influence attitudes and behaviour promoting HSE in our company culture.

External environmentThe activities of Fabricom (Company and Group) involve only a few minor environmental pollution risks due to the nature of the work and services. However the policy of Fabricom (Company and Group) in this area is that no pollution is insignificant and we have therefore developed an external environmental control system, which is now documented, implemented, certified and followed in accordance with ISO 14001.

This means that Fabricom is conscious of waste handling and the use of raw materials and

non-regenerative natural resources. Our environmental control system covers engineering, fabrication, installation and commis-sioning and enables us to undertake all phases of project execution in accordance with international environmental requirements. During the year, several external audits of the system were performed.

As a part of GDF Suez, Fabricom (company and group) has an extensive reporting duty within the Group within the environment area, as well as to customers and regulatory authorities. In general, preventive action is prioritised in all our activities to avoid and reduce pollution of earth, air and water.

Gender equalityIn 2009 Fabricom (Company and Group) undertook a survey of diversity and equality in the working environment in cooperation with GDF Suez. The purpose of the survey was to establish the status of how our co-workers understand that diversity and equality principles are ensured in the company. The result of the survey was positive, but does show that there is still room for improvement. The Equal Opportunities committee will develop a plan of action to ensure improvement.

Fabricom has implemented the “4You” – the good working environment - campaign during the year for all our co-workers. The campaign will contribute to further development of, and to ensure, a good

16 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

working environment. The company has zero tolerance of attitudes or behaviour that could lead to bullying and harassment of our co-workers.

Fabricom’s line of business is considered to be male dominated and, in 2009, the company has therefore focussed on increasing the number of women, especially in connection with recruitment of newly qualified, higher educated, female co-workers. 2 women out of 9 new higher educated employees were hired in 2009 (higher education is minimum Bachelors degree). The total number of females employed was 19,3 % at the end of 2009, compared to 14 % in 2008.

16,1 % of executive positions were filled by females at the end of 2009 compared to 19,7 % in 2008. There is one (1) woman in the company Management group. There are eleven (11) women in executive positions in the company. There is (1) woman on the company board. One (1) woman is on the GDF Suez (Paris) Group equality committee.

Fabricom has prepared an action plan to promote equality in the various departments and business areas. The 2010 action plan will include a survey to document the numbers of women/men and salary comparisons.

Fabricom’s payroll policy is based on the principle of equal pay for equal work and is gender neutral and is also built on seniority principles. Existing special agreements between employee

representation organisations and the company do however allow for individual payroll evaluations.

Neither the Equal Opportunities committee nor the company has in 2009 received reports on breaches or other equality related cases. The Equal Opportunities committee met 3 times in 2009.

Life phase policyFabricom (Company and Group) is an IA company and endeavours to ensure that employees in all phases of life have a good working situation and development opportunities throughout their career. Arrangements are in place to give opportunities to adapt to the individual co-workers’ needs. No one in Fabricom unwillingly works part time. Part-time co-workers have had their position adapted to their needs.

Senior policyFabricom (Company and Group) has conversations with senior employees over the age of 58 where the employee can address wishes for change in connection with competence, observation, adaptation and more. In 2009 a Senior Club was established for co-workers over 58. A “senior” must be a staff member over 58. There are no age limits above but an employee leaves the club the day the employee relationship ends. One of the main goals for the senior club is to ensure such a good working environment that no one ends the working

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 17

S

M

L

XL

relationship before the age of 67. The activities of the senior club are financially supported by the company. One senior seminar and 2 senior meetings were held during the year. As at 31.12.2009 about 80 employees were over the age of 58.

Child care leaveFabricom (Company and Group) encourages its male employees men to participate in child care and take paid child care leave in excess of the minimum legal requirement. Fabricom achieves this by adapting and dividing work tasks in consultation with department leaders and the employee. Child care leave will not be an obstacle to career or salary development.

Culture, religious and ethnic arrangementsDue to Fabricom’s (Company and Group) substantial growth in the few last years, manpower has been utilised from all over the world. Although we have experienced challenges in connection with cultural and religious aspects, no major individual or collective adjustments have been necessary.

The company has 886 employees with non-Norwegian ethnic backgrounds representing 29 different nations. The company has therefore met new challenges but without any serious individual or collective disagreements.

Our experience so far with employed and hired-in personnel from different cultures has been entirely positive. Integration of foreign cultures has been a challenge but also an informative process for both the company and its employees.

Fabricom’s (Company and Group) personnel policy is inclusive and Fabricom will therefore continue to work within prevailing political guidelines to achieve this.

Financial statementsIn the opinion of the Board of Directors, the profit and loss account and balance sheet with notes give adequate information concerning the financial standing of Fabricom (company and group) at the year-end. After finalisation of the accounts, no events have occurred that materially effect the evaluation of the Company or Group’s result. Concerning allocation and price development for the products included in the Group activities, the Board does not know of any matter that affects the evaluation of the group throughout the financial statement.

Fabricom AS’ financial statements for 2009 are finalised showing a profit of NOK44 882 000. The Board of Directors propose the following applica-tion of the year’s result:

Fabricom ASReserve for valuation variants -14 487 000Dividends 46 939 000Other equity 12 430 000Total disposed 44 882 000

The company’s free equity is NOK 71 095 000 after payment of the proposed annual dividend.

18 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

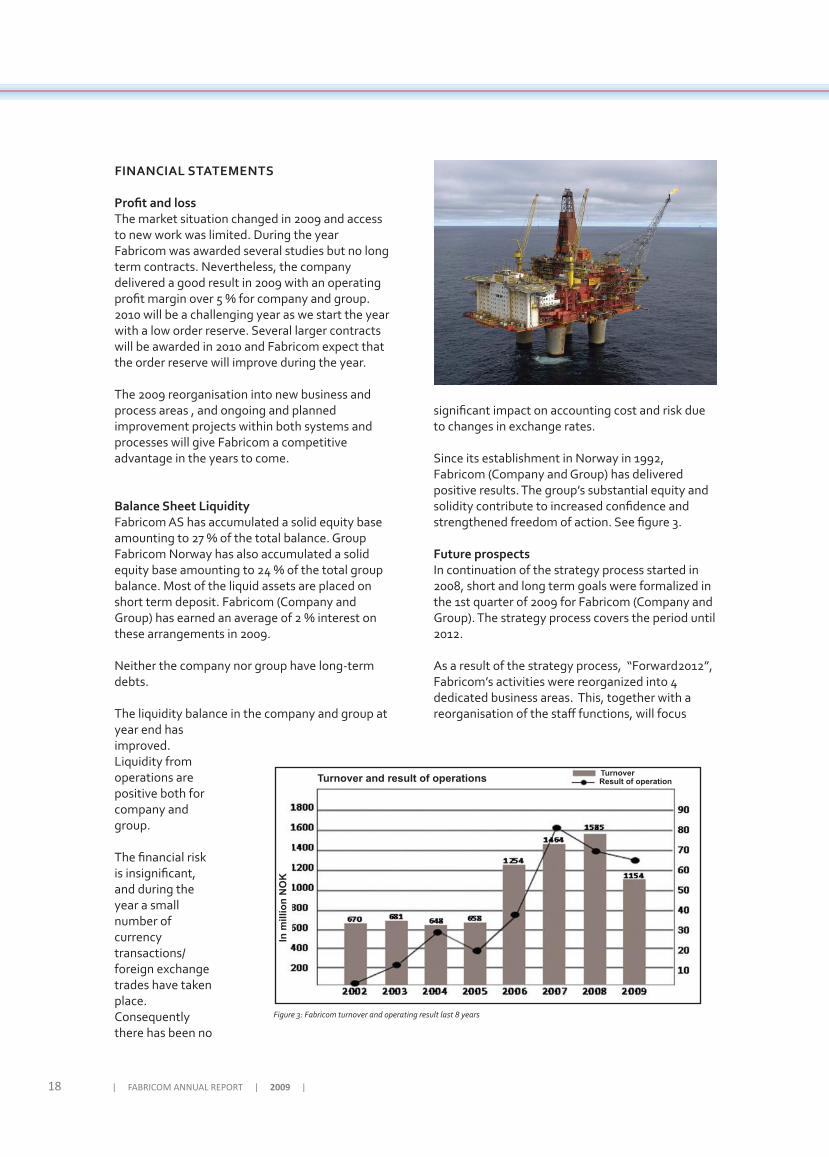

Figure 3: Fabricom turnover and operating result last 8 years

FINANCIAL STATEMENTS

Profit and lossThe market situation changed in 2009 and access to new work was limited. During the year Fabricom was awarded several studies but no long term contracts. Nevertheless, the company delivered a good result in 2009 with an operating profit margin over 5 % for company and group. 2010 will be a challenging year as we start the year with a low order reserve. Several larger contracts will be awarded in 2010 and Fabricom expect that the order reserve will improve during the year.

The 2009 reorganisation into new business and process areas , and ongoing and planned improvement projects within both systems and processes will give Fabricom a competitive advantage in the years to come.

Balance Sheet LiquidityFabricom AS has accumulated a solid equity base amounting to 27 % of the total balance. Group Fabricom Norway has also accumulated a solid equity base amounting to 24 % of the total group balance. Most of the liquid assets are placed on short term deposit. Fabricom (Company and Group) has earned an average of 2 % interest on these arrangements in 2009.

Neither the company nor group have long-term debts.

The liquidity balance in the company and group at year end has improved. Liquidity from operations are positive both for company and group.

The financial risk is insignificant, and during the year a small number of currency transactions/foreign exchange trades have taken place. Consequently there has been no

significant impact on accounting cost and risk due to changes in exchange rates.

Since its establishment in Norway in 1992, Fabricom (Company and Group) has delivered positive results. The group’s substantial equity and solidity contribute to increased confidence and strengthened freedom of action. See figure 3.

Future prospectsIn continuation of the strategy process started in 2008, short and long term goals were formalized in the 1st quarter of 2009 for Fabricom (Company and Group). The strategy process covers the period until 2012.

As a result of the strategy process, “Forward2012”, Fabricom’s activities were reorganized into 4 dedicated business areas. This, together with a reorganisation of the staff functions, will focus

TurnoverTurnoverTurnoverTurnoverTurnoverTurnover and result of operations TurnoverResult of operation

In m

illio

n N

OK

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 19

S

M

L

XL

responsibility and efficiently manage and develop the company’s personnel resource, tools, methods and systems. The background for this re-organisation was linked to feedback fromcustomers, the owner’s requirement to grow in existing and new markets, the need for clarification of roles internally in the organisation and defined improvement goals for quality of delivery and cost efficiency.

New technology, new operating methods, utilisation of existing infrastructure, combined with increasingly stringent requirements related to safety and environmental discharge, have contributed to increased demand in the modification market for the oil and gas industry. Fabricom (company and group) has proven its ability through many projects to find solutions and execute complicated modification projects to meet all such requirements.

The Norwegian modification market is a typical niche market. Clients demand and expect knowledge and experience from work on onshore and offshore installations, geographical proximity to their own organisation and flexibility. Thus Norwegian modification projects are especially suitable for Fabricom’s engineering and production environment (Stavanger). Combined with GDF Suez’ international competence in the fields of cleaning/ treatment, environmental and gas

handling, Fabricom (company and group) will utilise its

experience and competence to win new work from Operating Companies on the Norwegian Continental Shelf and elsewhere in the North Sea.

In general there is con-siderable uncertainty

regarding future market developments. 2009 was a good example of this where, after several years of considerable growth, the activity level declined significantly. This was due to the ongoing global financial crisis which, amongst other things, led to a considerable drop in the oil price. Though the oil price later recovered, there was still considerable uncertainty to how price development would be in the longer term. Also the cost level in the supply chain increased considerably through years of high activity and shortage of resources. As a result of these conditions only a few contracts in Fabricom’s core business were awarded in 2009 and a large part of the supply industry has operated in 2009 consuming the backlog of orders from the beginning of the year.

Foto: StatoilHydro

20 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

S

M

L

XL

Stavanger, 18.03.10

Morten Steenstrup Xavier Sinéchal Styrets leder

Michel Hanson Per Oscar Knudsen

Nils Vidar Johanssen Håkon Fuglestad

However 2009 has introduced several exciting business prospects that will have considerable effect in the years to come. This is includes V&M agreements for Statoil’s offshore and onshore installations and the a considerable portfolio of larger separate studies- and modification contracts. In this connection the upgrading of existing drilling installations will contribute a considerable share of the expected modification portfolio in future years.

Even though the market prognosis for Fabricom’s business area is showing a positive improvement, there will be strong competition for new contracts. It has recently become apparent that some competing companies will increasingly execute engineering and prefabrication delivery in low-cost countries. There is also an increasing use of foreign manpower in connection with assignments undertaken for the shipping industry and onshore installation assignments. This development is expected to continue making it necessary for Fabricom to continue to develop new competitive solutions for delivery.

In 2009 Fabricom carried out a significant improvement programme that will continue into 2010in order to improve our tools, methods and systems to meet the specific needs of the individual business areas. Fabricom will also continue actively to further develop the competence skills in our own organisation. To realise the defined goals to develop the company’s business we plan a considerable amount of recruitment in combination with new acquisitions.

It is our primary goal to strengthen Fabricom’s position in the Norwegian oil and gas market such that we are considered as a preferred supplier by our customers, we secure attractive jobs for our employees and deliver satisfactory profit for our owners.

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 21

S

M

L

XL

FABRICOM ACCOUNTS 2009

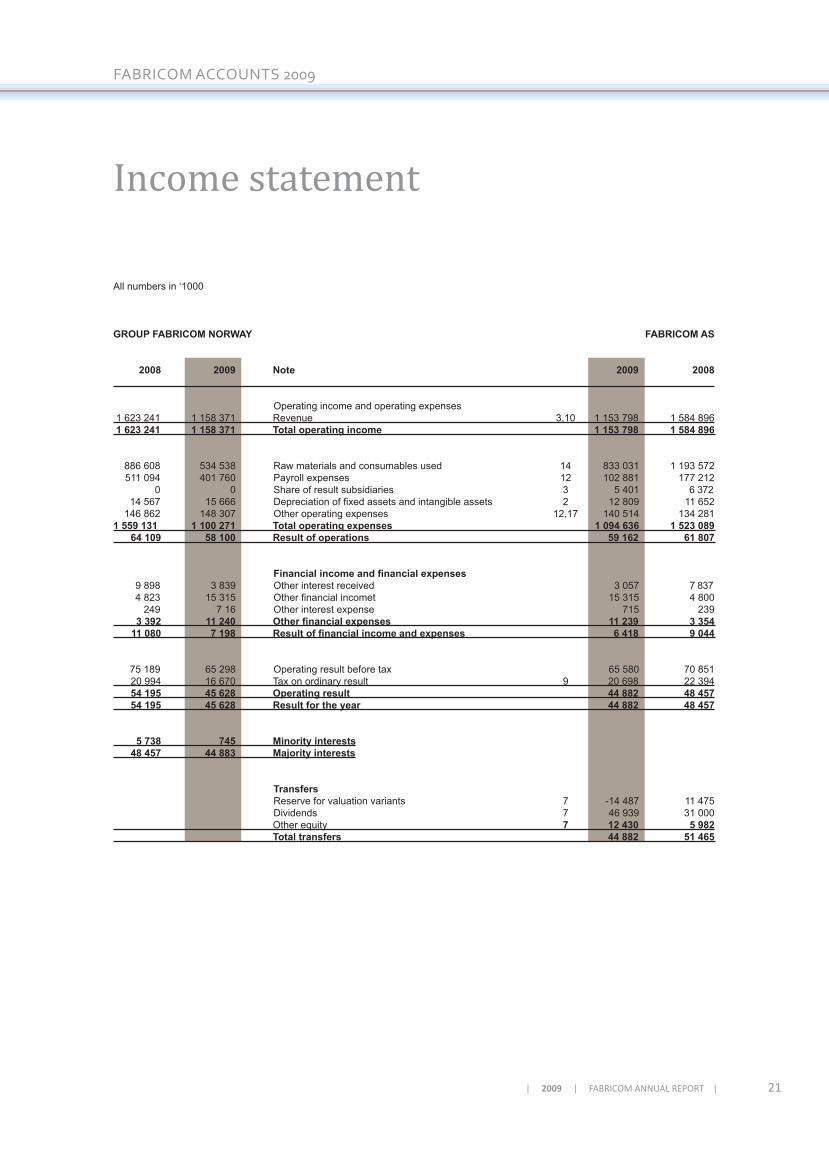

Income statement

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 Note 2009 2008 Operating income and operating expenses 1 623 241 1 158 371 Revenue 3,10 1 153 798 1 584 896 1 623 241 1 158 371 Total operating income 1 153 798 1 584 896

886 608 534 538 Raw materials and consumables used 14 833 031 1 193 572 511 094 401 760 Payroll expenses 12 102 881 177 212 0 0 Share of result subsidiaries 3 5 401 6 372 14 567 15 666 Depreciation of fixed assets and intangible assets 2 12 809 11 652 146 862 148 307 Other operating expenses 12,17 140 514 134 2811 559 131 1 100 271 Total operating expenses 1 094 636 1 523 089 64 109 58 100 Result of operations 59 162 61 807 Financialincomeandfinancialexpenses 9 898 3 839 Other interest received 3 057 7 837 4 823 15 315 Other financial incomet 15 315 4 800 249 7 16 Other interest expense 715 239 3392 11240 Otherfinancialexpenses 11239 3354 11080 7198 Resultoffinancialincomeandexpenses 6418 9044 75 189 65 298 Operating result before tax 65 580 70 851 20 994 16 670 Tax on ordinary result 9 20 698 22 394 54 195 45 628 Operating result 44 882 48 457 54 195 45 628 Result for the year 44 882 48 457

5 738 745 Minority interests 48 457 44 883 Majority interests

Transfers Reserve for valuation variants 7 -14 487 11 475 Dividends 7 46 939 31 000 Other equity 7 12 430 5 982 Total transfers 44 882 51 465

22 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

FABRICOM ACCOUNTS 2009S

M

L

XL

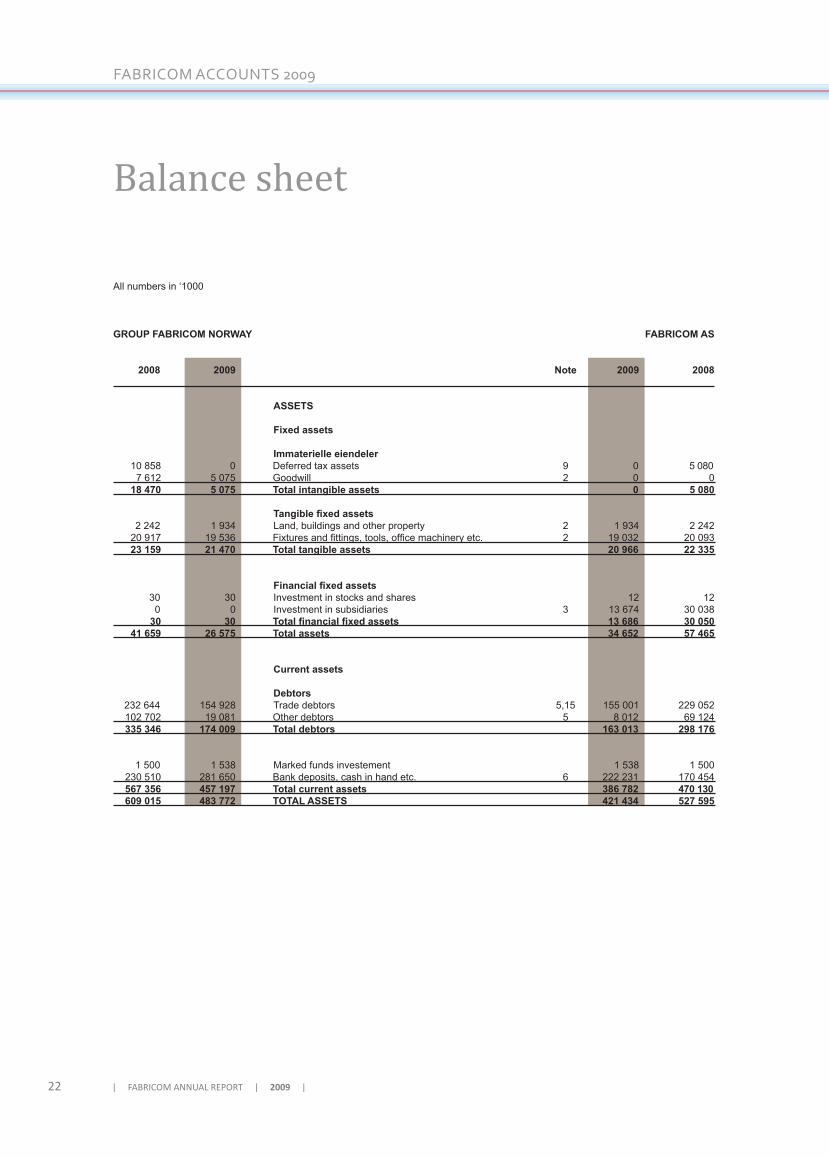

Balance sheet

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 Note 2009 2008 ASSETS Fixed assets Immaterielle eiendeler 10 858 0 Deferred tax assets 9 0 5 080 7 612 5 075 Goodwill 2 0 0 18 470 5 075 Total intangible assets 0 5 080 Tangiblefixedassets 2 242 1 934 Land, buildings and other property 2 1 934 2 242 20 917 19 536 Fixtures and fittings, tools, office machinery etc. 2 19 032 20 093 23 159 21 470 Total tangible assets 20 966 22 335 Financialfixedassets 30 30 Investment in stocks and shares 12 12 0 0 Investment in subsidiaries 3 13 674 30 038 30 30 Totalfinancialfixedassets 13686 30050 41 659 26 575 Total assets 34 652 57 465

Current assets Debtors 232 644 154 928 Trade debtors 5,15 155 001 229 052 102 702 19 081 Other debtors 5 8 012 69 124 335 346 174 009 Total debtors 163 013 298 176

1 500 1 538 Marked funds investement 1 538 1 500 230 510 281 650 Bank deposits, cash in hand etc. 6 222 231 170 454 567 356 457 197 Total current assets 386 782 470 130 609 015 483 772 TOTAL ASSETS 421 434 527 595

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 23

S

M

L

XL

FABRICOM ACCOUNTS 2009

Balance sheet

All numbers in ‘1000

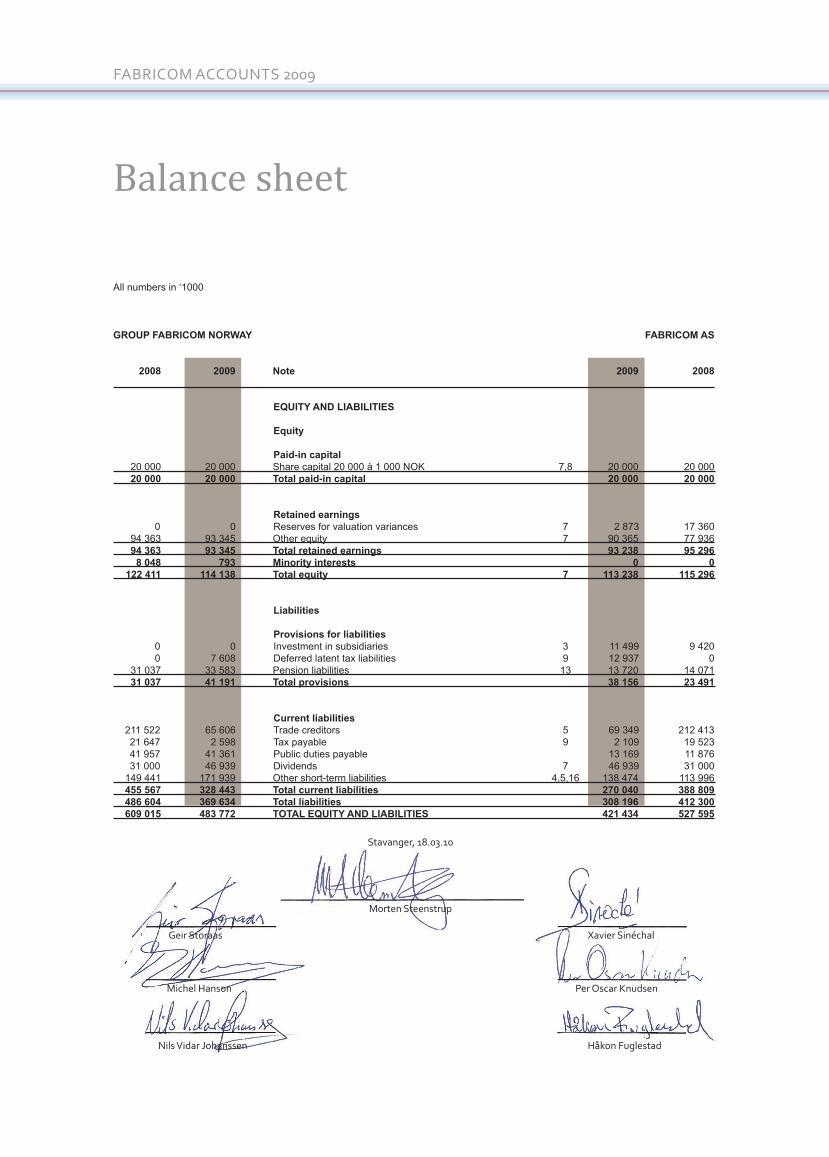

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 Note 2009 2008 EQUITY AND LIABILITIES Equity Paid-in capital 20 000 20 000 Share capital 20 000 à 1 000 NOK 7,8 20 000 20 000 20 000 20 000 Total paid-in capital 20 000 20 000

Retained earnings 0 0 Reserves for valuation variances 7 2 873 17 360 94 363 93 345 Other equity 7 90 365 77 936 94 363 93 345 Total retained earnings 93 238 95 296 8 048 793 Minority interests 0 0 122 411 114 138 Total equity 7 113 238 115 296

Liabilities

Provisions for liabilities 0 0 Investment in subsidiaries 3 11 499 9 420 0 7 608 Deferred latent tax liabilities 9 12 937 0 31 037 33 583 Pension liabilities 13 13 720 14 071 31 037 41 191 Total provisions 38 156 23 491

Current liabilities 211 522 65 606 Trade creditors 5 69 349 212 413 21 647 2 598 Tax payable 9 2 109 19 523 41 957 41 361 Public duties payable 13 169 11 876 31 000 46 939 Dividends 7 46 939 31 000 149 441 171 939 Other short-term liabilities 4,5,16 138 474 113 996 455 567 328 443 Total current liabilities 270 040 388 809 486 604 369 634 Total liabilities 308 196 412 300 609 015 483 772 TOTAL EQUITY AND LIABILITIES 421 434 527 595

Stavanger, 18.03.10

Morten Steenstrup

Geir Storaas Xavier Sinéchal

Michel Hanson Per Oscar Knudsen

Nils Vidar Johanssen Håkon Fuglestad

24 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

FABRICOM ACCOUNTS 2009S

M

L

XL

Cash flow statement

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

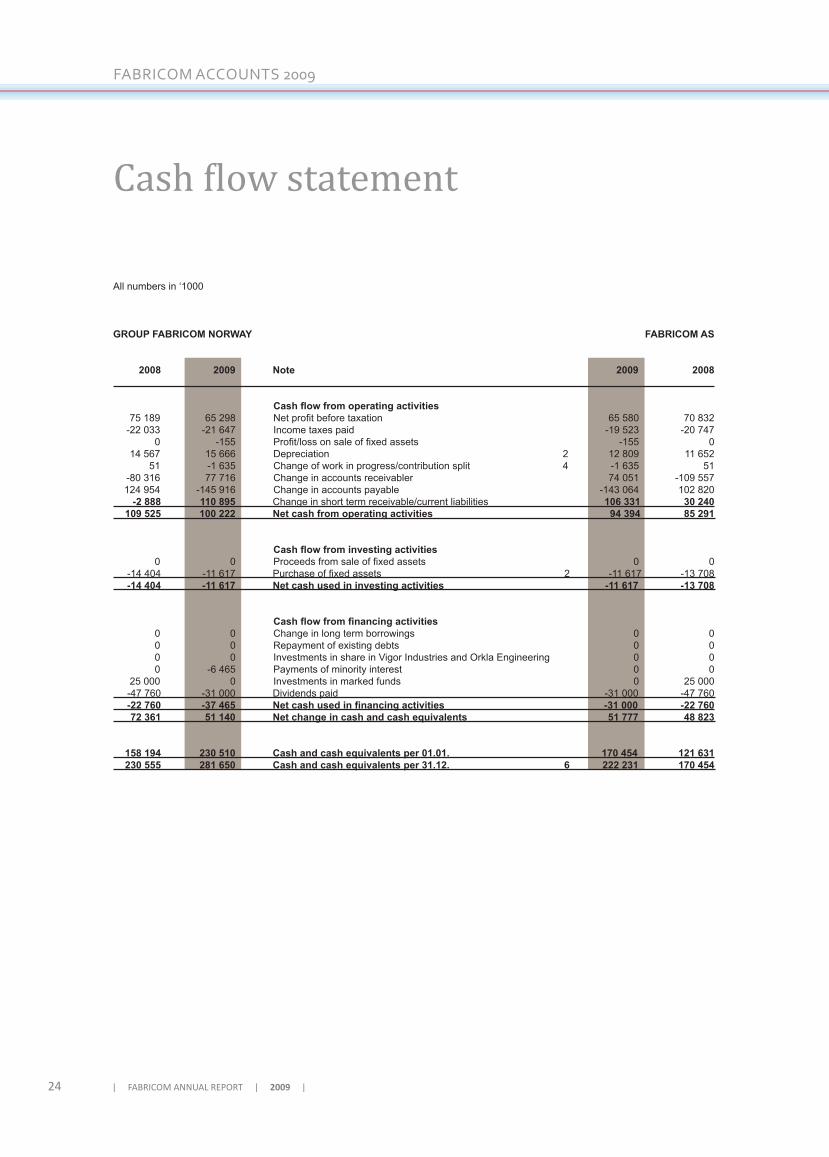

2008 2009 Note 2009 2008 Cashflowfromoperatingactivities 75 189 65 298 Net profit before taxation 65 580 70 832 -22 033 -21 647 Income taxes paid -19 523 -20 747 0 -155 Profit/loss on sale of fixed assets -155 0 14 567 15 666 Depreciation 2 12 809 11 652 51 -1 635 Change of work in progress/contribution split 4 -1 635 51 -80 316 77 716 Change in accounts receivabler 74 051 -109 557 124 954 -145 916 Change in accounts payable -143 064 102 820 -2 888 110 895 Change in short term receivable/current liabilities 106 331 30 240 109 525 100 222 Net cash from operating activities 94 394 85 291 Cashflowfrominvestingactivities 0 0 Proceeds from sale of fixed assets 0 0 -14 404 -11 617 Purchase of fixed assets 2 -11 617 -13 708 -14 404 -11 617 Net cash used in investing activities -11 617 -13 708 Cashflowfromfinancingactivities 0 0 Change in long term borrowings 0 0 0 0 Repayment of existing debts 0 0 0 0 Investments in share in Vigor Industries and Orkla Engineering 0 0 0 -6 465 Payments of minority interest 0 0 25 000 0 Investments in marked funds 0 25 000 -47 760 -31 000 Dividends paid -31 000 -47 760 -22760 -37465 Netcashusedinfinancingactivities -31000 -22760 72 361 51 140 Net change in cash and cash equivalents 51 777 48 823 158 194 230 510 Cash and cash equivalents per 01.01. 170 454 121 631 230 555 281 650 Cash and cash equivalents per 31.12. 6 222 231 170 454

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 25

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009

Notes to consolidated financial statements

Note 1 Accounting principles

The accounts for Fabricom AS and the consolidated Group accounts are prepared in accordance with the Norwegian Accounting Act of 1998 and generally accepted accounting practices. Accounting principles are described below. Consolidation principles The consolidated accounts include Fabricom AS and subsidiary companies in which Fabricom AS has a direct controlling influence in fact and in law. The consolidated accounts is prepared with equal accounting principles for similar transactions in all companies.The companies’ internal sales and internal accounts are eliminated in the consolidated accounts. Shares and interests in associated companies in the consolidated accounts are eliminated according to the acquisition method. This implies that assets and liabilities in the acquired company valuates to actual value at the time of acquistion, and a possible excess price clasifies as goodwill. Principlerulesforevaluationandclassificationofassetsandliabilities Assets intended for permanent possession are classified as fixed assets. Other assets are classified as current assets. Outstanding claims due within one year are classified as current assets. Classification of short-term debt and long term debt are based on the same evaluation. Fixed assets are valued at acquisition cost, but are written-down to real value when the loss in value is considered to be permanent. Fixed assets with limited economic life are written-down according to plan. A few balance sheet items are evaluated according to other principles as explained below. Goodwill Capitalized goodwill in connection with the acquisition of other businesses is determined by the part of the purchase price beyond the value of individual assets at the acquisition date.Goodwill is posted at historical cost price and is depreciated over the first five accounting years in equal amounts. Actual value goodwill is evaluated against written-down value at year end for a possible write-down of booked value. Shares and interests in associated companies Investments in associated companies and subsidiaries are valued according to the equity method. Investments in shares are valued at cost. Trade debtors and other debtors Trade debtors and other debtors are valued at face value. In addition there is an appropriation for unsecured debtors. Projects / Work in progress Projects / work in progress are valued at direct cost for materials and wages, including social cost with the addition of indirect cost based on budgeted administration cost. The company therefore allocates cost on an “as-incurred” basis. Profit are included on projects where there are reliable estimates of outcome. Percentage of completion is based on incurred MHRS in percentage of total estimated MHRS. Profit is taken on large project when percentage of completion is above 20 %. In addition a security margin from 2 % to 5 % is calculated before any result is taken into account.Any losses are taken into account as soon as they are identified. The net value of work in progress/advance invoicing of production is posted in the balance sheet by deducting advance payments from customers from the project value. Work on account is valued at sales value at 31.12. Taxes Tax cost is placed together with the accounting result before tax. Tax cost consists of payable taxes for the year (tax on this years taxable result) and changes in net deferred taxes. The tax cost is divided between ordinary result and extraordinary result according to taxable basis.Deferred tax liabilities and deferred tax assets are shown as net items in the balance sheet. Pension liabilities AFP The company participates in the arrangement for negotiated pension between the trade unions (LO) and the employers’ association (NHO), AFP arrangement. The Company has recorded calculated pension liability included payroll tax in the balance sheet. For further information see note 13. Group pension liabilities The company has a contribution pension plan which complies with compulsory occupational pension. For further information see note 13. Expenses related to contribution pension plan is charged according to received invoices from insurance company. Foreign currency The company calculates foreign currency at the exchange rate on the accounting date. Gains and losses on foreign currency exchange are classi-fied as financial transactions. Estimates The compilation of the result assume that the company use estimate and assumption which affects the result and the valuation of assets, liabilities and commitments on the balance date. These are settled to best estimate based on the information on the balance date according to generally accepted accounting principles. Actual figures can deviate from estimates.

26 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009S

M

L

XL

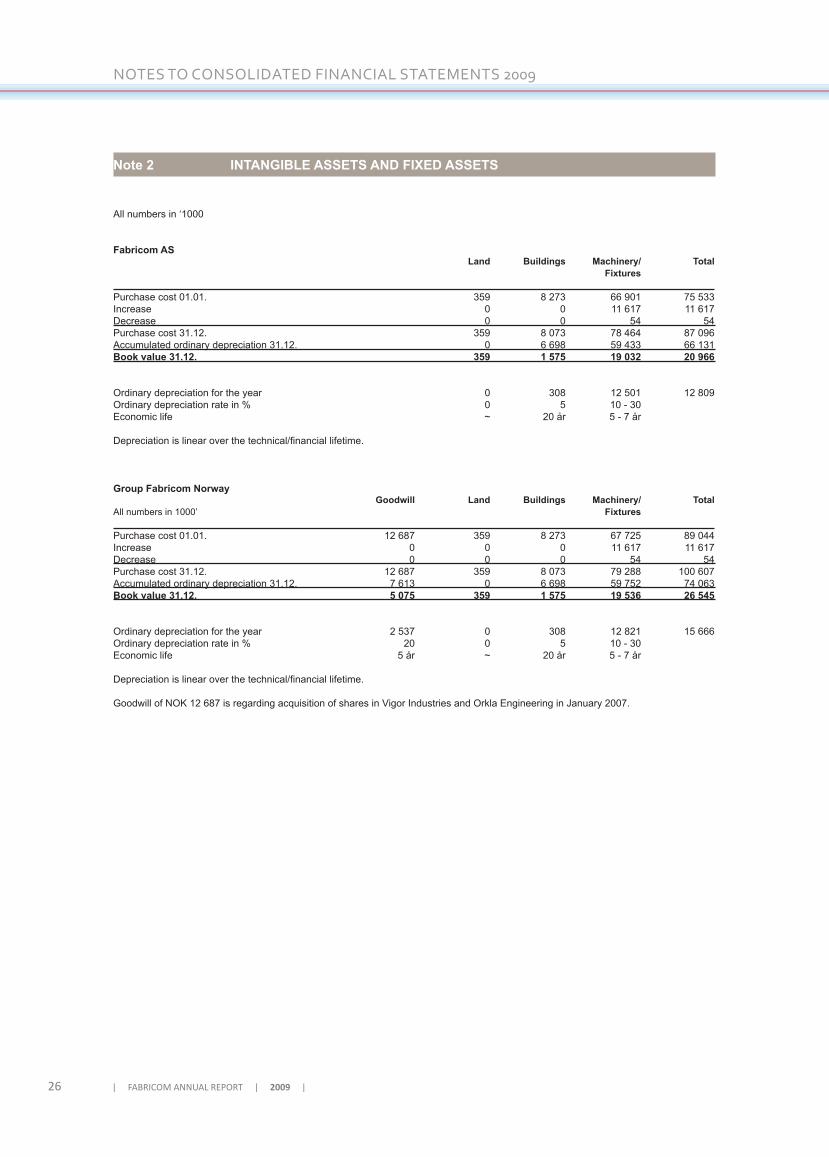

Note 2 INTANGIBLE ASSETS AND FIXED ASSETS

All numbers in ‘1000

Fabricom AS Land Buildings Machinery/ Total Fixtures Purchase cost 01.01. 359 8 273 66 901 75 533Increase 0 0 11 617 11 617 Decrease 0 0 54 54 Purchase cost 31.12. 359 8 073 78 464 87 096 Accumulated ordinary depreciation 31.12. 0 6 698 59 433 66 131 Book value 31.12. 359 1 575 19 032 20 966

Ordinary depreciation for the year 0 308 12 501 12 809 Ordinary depreciation rate in % 0 5 10 - 30 Economic life ~ 20 år 5 - 7 år Depreciation is linear over the technical/financial lifetime. GroupFabricomNorway Goodwill Land Buildings Machinery/ TotalAll numbers in 1000’ Fixtures Purchase cost 01.01. 12 687 359 8 273 67 725 89 044 Increase 0 0 0 11 617 11 617Decrease 0 0 0 54 54 Purchase cost 31.12. 12 687 359 8 073 79 288 100 607 Accumulated ordinary depreciation 31.12. 7 613 0 6 698 59 752 74 063 Book value 31.12. 5 075 359 1 575 19 536 26 545

Ordinary depreciation for the year 2 537 0 308 12 821 15 666Ordinary depreciation rate in % 20 0 5 10 - 30 Economic life 5 år ~ 20 år 5 - 7 år

Depreciation is linear over the technical/financial lifetime.

Goodwill of NOK 12 687 is regarding acquisition of shares in Vigor Industries and Orkla Engineering in January 2007.

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 27

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009

NOTE 3 SUBSIDIARIES

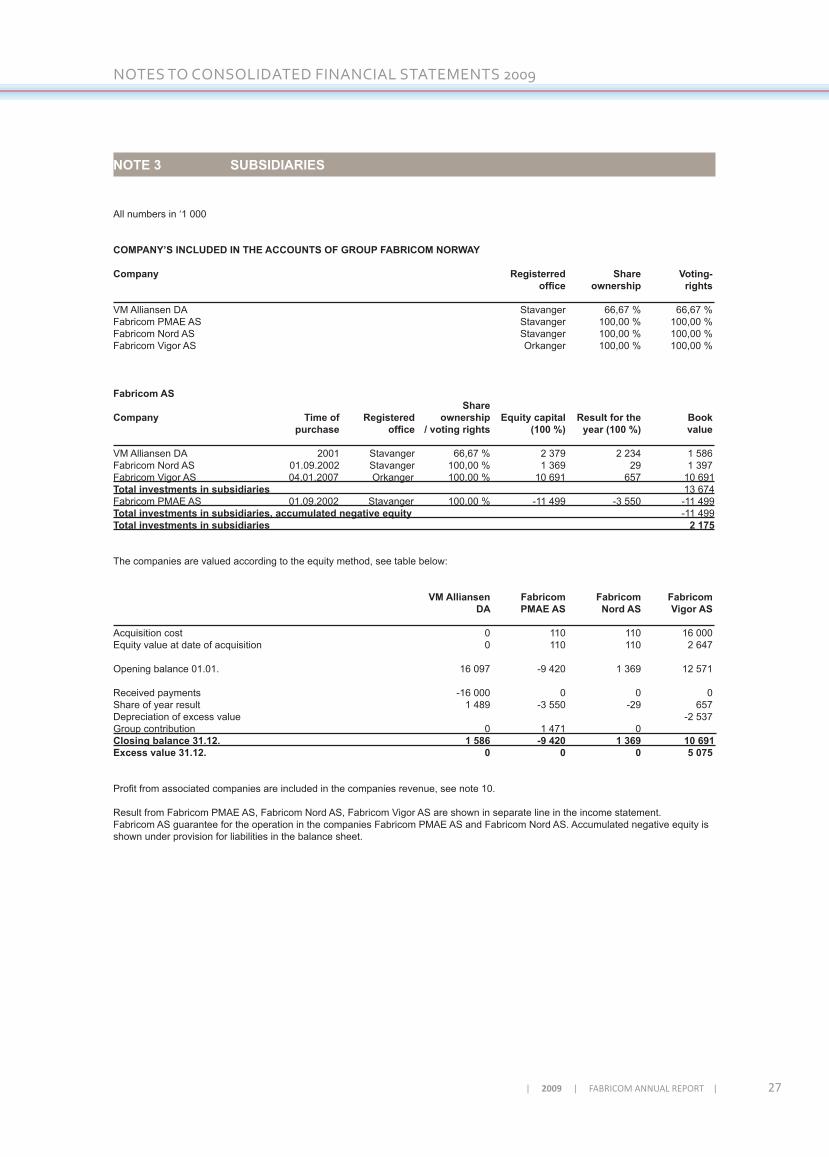

All numbers in ‘1 000

COMPANY’S INCLUDED IN THE ACCOUNTS OF GROUP FABRICOM NORWAY

Company Registerred Share Voting- office ownership rights VM Alliansen DA Stavanger 66,67 % 66,67 % Fabricom PMAE AS Stavanger 100,00 % 100,00 % Fabricom Nord AS Stavanger 100,00 % 100,00 % Fabricom Vigor AS Orkanger 100,00 % 100,00 %

Fabricom AS Share Company Timeof Registered ownership Equitycapital Resultforthe Book purchase office /votingrights (100%) year(100%) value VM Alliansen DA 2001 Stavanger 66,67 % 2 379 2 234 1 586Fabricom Nord AS 01.09.2002 Stavanger 100,00 % 1 369 29 1 397Fabricom Vigor AS 04.01.2007 Orkanger 100,00 % 10 691 657 10 691Total investments in subsidiaries 13 674Fabricom PMAE AS 01.09.2002 Stavanger 100,00 % -11 499 -3 550 -11 499Total investments in subsidiaries, accumulated negative equity -11 499Total investments in subsidiaries 2 175

The companies are valued according to the equity method, see table below: VM Alliansen Fabricom Fabricom Fabricom DA PMAE AS Nord AS Vigor AS Acquisition cost 0 110 110 16 000Equity value at date of acquisition 0 110 110 2 647 Opening balance 01.01. 16 097 -9 420 1 369 12 571

Received payments -16 000 0 0 0 Share of year result 1 489 -3 550 -29 657 Depreciation of excess value -2 537Group contribution 0 1 471 0 Closing balance 31.12. 1 586 -9 420 1 369 10 691 Excess value 31.12. 0 0 0 5 075

Profit from associated companies are included in the companies revenue, see note 10. Result from Fabricom PMAE AS, Fabricom Nord AS, Fabricom Vigor AS are shown in separate line in the income statement. Fabricom AS guarantee for the operation in the companies Fabricom PMAE AS and Fabricom Nord AS. Accumulated negative equity is shown under provision for liabilities in the balance sheet.

28 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009S

M

L

XL

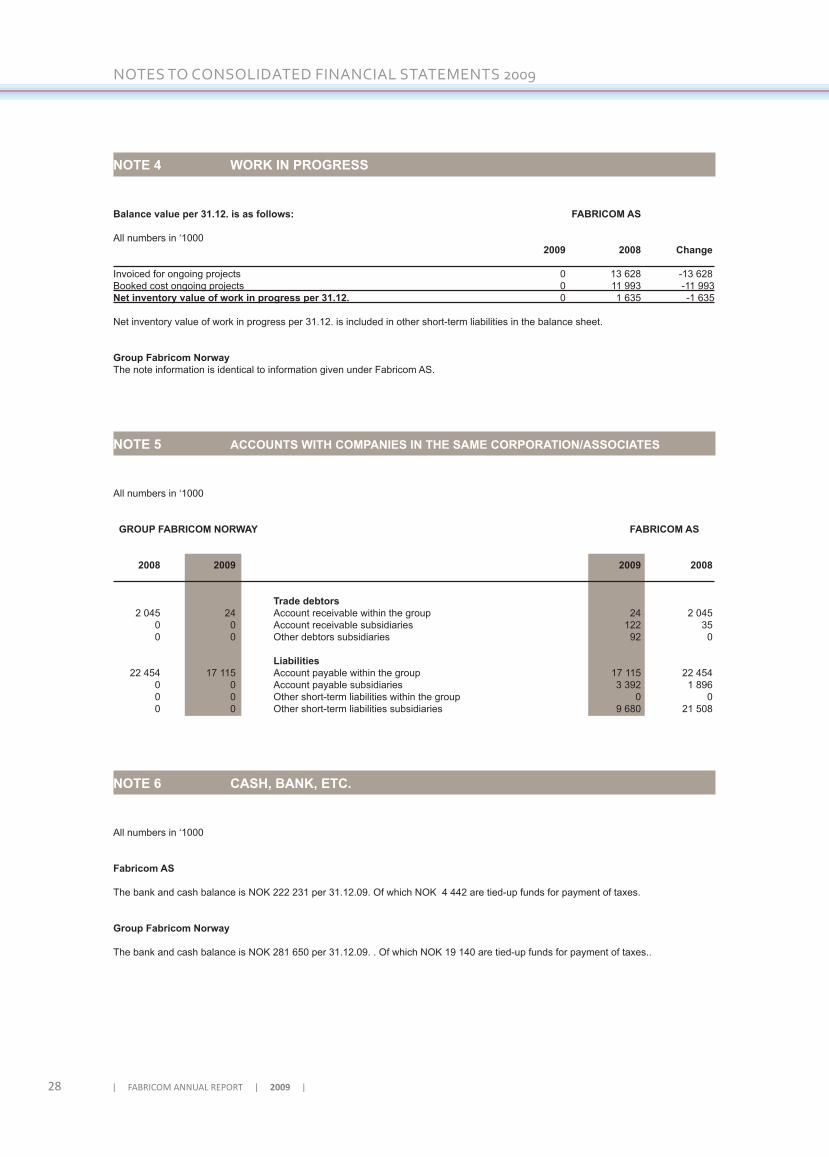

NOTE 4 WORK IN PROGRESS

Balancevalueper31.12.isasfollows: FABRICOM AS All numbers in ‘1000 2009 2008 Change Invoiced for ongoing projects 0 13 628 -13 628Booked cost ongoing projects 0 11 993 -11 993Netinventoryvalueofworkinprogressper31.12. 0 1 635 -1 635

Net inventory value of work in progress per 31.12. is included in other short-term liabilities in the balance sheet. GroupFabricomNorway The note information is identical to information given under Fabricom AS.

NOTE 5 ACCOUNTS WITH COMPANIES IN THE SAME CORPORATION/ASSOCIATES

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008

Trade debtors 2 045 24 Account receivable within the group 24 2 045 0 0 Account receivable subsidiaries 122 35 0 0 Other debtors subsidiaries 92 0

Liabilities 22 454 17 115 Account payable within the group 17 115 22 454 0 0 Account payable subsidiaries 3 392 1 896 0 0 Other short-term liabilities within the group 0 0 0 0 Other short-term liabilities subsidiaries 9 680 21 508

NOTE 6 CASH, BANK, ETC.

All numbers in ‘1000

Fabricom AS The bank and cash balance is NOK 222 231 per 31.12.09. Of which NOK 4 442 are tied-up funds for payment of taxes.

GroupFabricomNorway

The bank and cash balance is NOK 281 650 per 31.12.09. . Of which NOK 19 140 are tied-up funds for payment of taxes..

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 29

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009

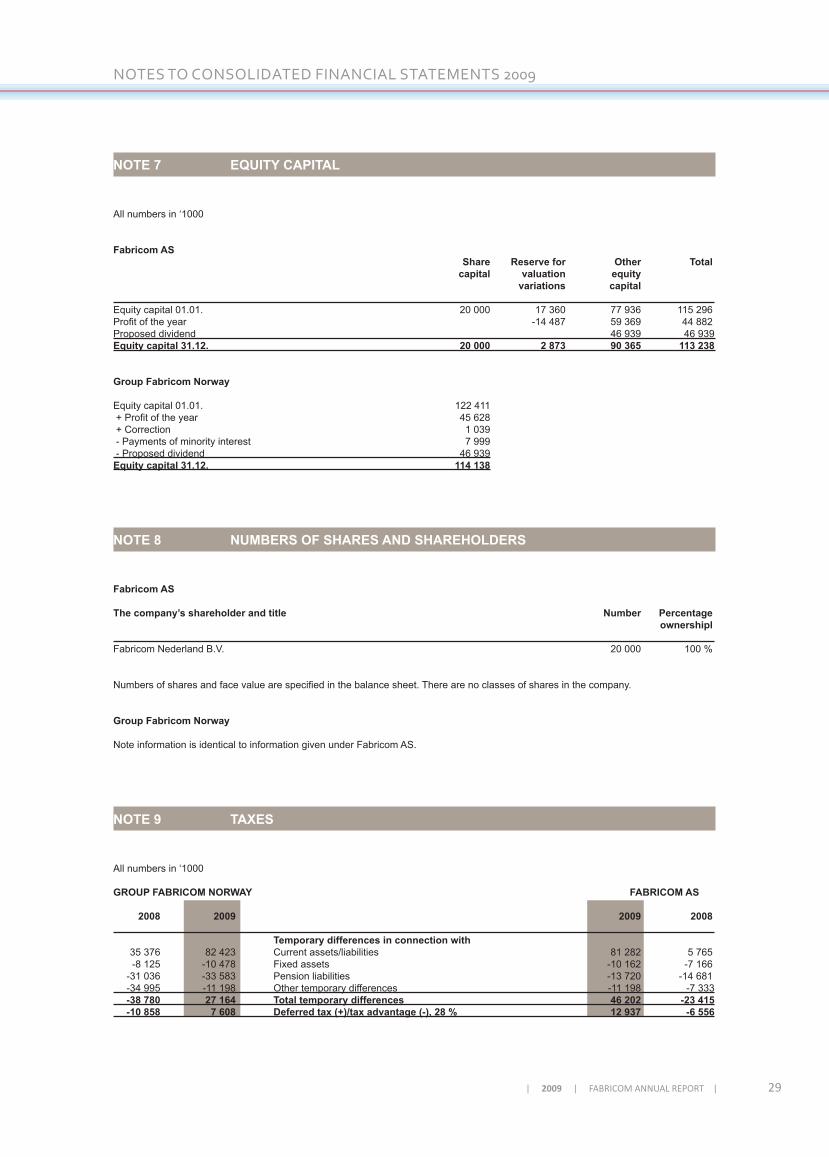

NOTE 7 EQUITY CAPITAL

All numbers in ‘1000

Fabricom AS Share Reserve for Other Total capital valuation equity variations capital Equity capital 01.01. 20 000 17 360 77 936 115 296Profit of the year -14 487 59 369 44 882 Proposed dividend 46 939 46 939 Equity capital 31.12. 20 000 2 873 90 365 113 238

GroupFabricomNorway

Equity capital 01.01. 122 411 + Profit of the year 45 628 + Correction 1 039 - Payments of minority interest 7 999 - Proposed dividend 46 939Equity capital 31.12. 114 138

NOTE 8 NUMBERS OF SHARES AND SHAREHOLDERS

Fabricom AS

The company’s shareholder and title Number Percentage ownershipl Fabricom Nederland B.V. 20 000 100 % Numbers of shares and face value are specified in the balance sheet. There are no classes of shares in the company. GroupFabricomNorway

Note information is identical to information given under Fabricom AS.

NOTE 9 TAXES

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008 Temporarydifferencesinconnectionwith 35 376 82 423 Current assets/liabilities 81 282 5 765 -8 125 -10 478 Fixed assets -10 162 -7 166 -31 036 -33 583 Pension liabilities -13 720 -14 681 -34 995 -11 198 Other temporary differences -11 198 -7 333 -38 780 27 164 Total temporary differences 46 202 -23 415 -10858 7608 Deferredtax(+)/taxadvantage(-),28% 12937 -6556

30 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009S

M

L

XL

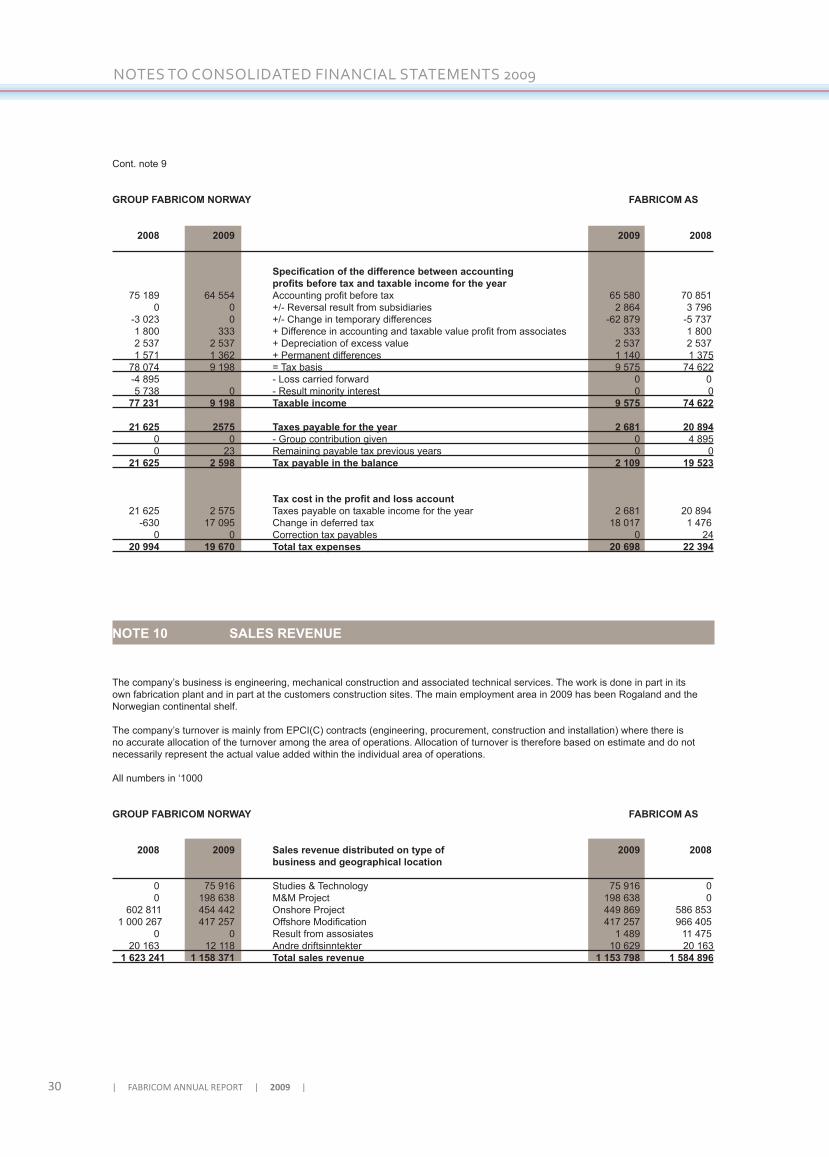

Cont. note 9

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008

Specificationofthedifferencebetweenaccounting profitsbeforetaxandtaxableincomefortheyear 75 189 64 554 Accounting profit before tax 65 580 70 851 0 0 +/- Reversal result from subsidiaries 2 864 3 796 -3 023 0 +/- Change in temporary differences -62 879 -5 737 1 800 333 + Difference in accounting and taxable value profit from associates 333 1 800 2 537 2 537 + Depreciation of excess value 2 537 2 537 1 571 1 362 + Permanent differences 1 140 1 375 78 074 9 198 = Tax basis 9 575 74 622 -4 895 - Loss carried forward 0 0 5 738 0 - Result minority interest 0 0 77 231 9 198 Taxable income 9 575 74 622

21 625 2575 Taxes payable for the year 2 681 20 894 0 0 - Group contribution given 0 4 895 0 23 Remaining payable tax previous years 0 0 21 625 2 598 Tax payable in the balance 2 109 19 523 Taxcostintheprofitandlossaccount 21 625 2 575 Taxes payable on taxable income for the year 2 681 20 894 -630 17 095 Change in deferred tax 18 017 1 476 0 0 Correction tax payables 0 24 20 994 19 670 Total tax expenses 20 698 22 394

NOTE 10 SALES REVENUE

The company’s business is engineering, mechanical construction and associated technical services. The work is done in part in its own fabrication plant and in part at the customers construction sites. The main employment area in 2009 has been Rogaland and the Norwegian continental shelf. The company’s turnover is mainly from EPCI(C) contracts (engineering, procurement, construction and installation) where there is no accurate allocation of the turnover among the area of operations. Allocation of turnover is therefore based on estimate and do not necessarily represent the actual value added within the individual area of operations.

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 Sales revenue distributed on type of 2009 2008 business and geographical location 0 75 916 Studies & Technology 75 916 0 0 198 638 M&M Project 198 638 0 602 811 454 442 Onshore Project 449 869 586 853 1 000 267 417 257 Offshore Modification 417 257 966 405 0 0 Result from assosiates 1 489 11 475 20 163 12 118 Andre driftsinntekter 10 629 20 163 1 623 241 1 158 371 Total sales revenue 1 153 798 1 584 896

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 31

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009

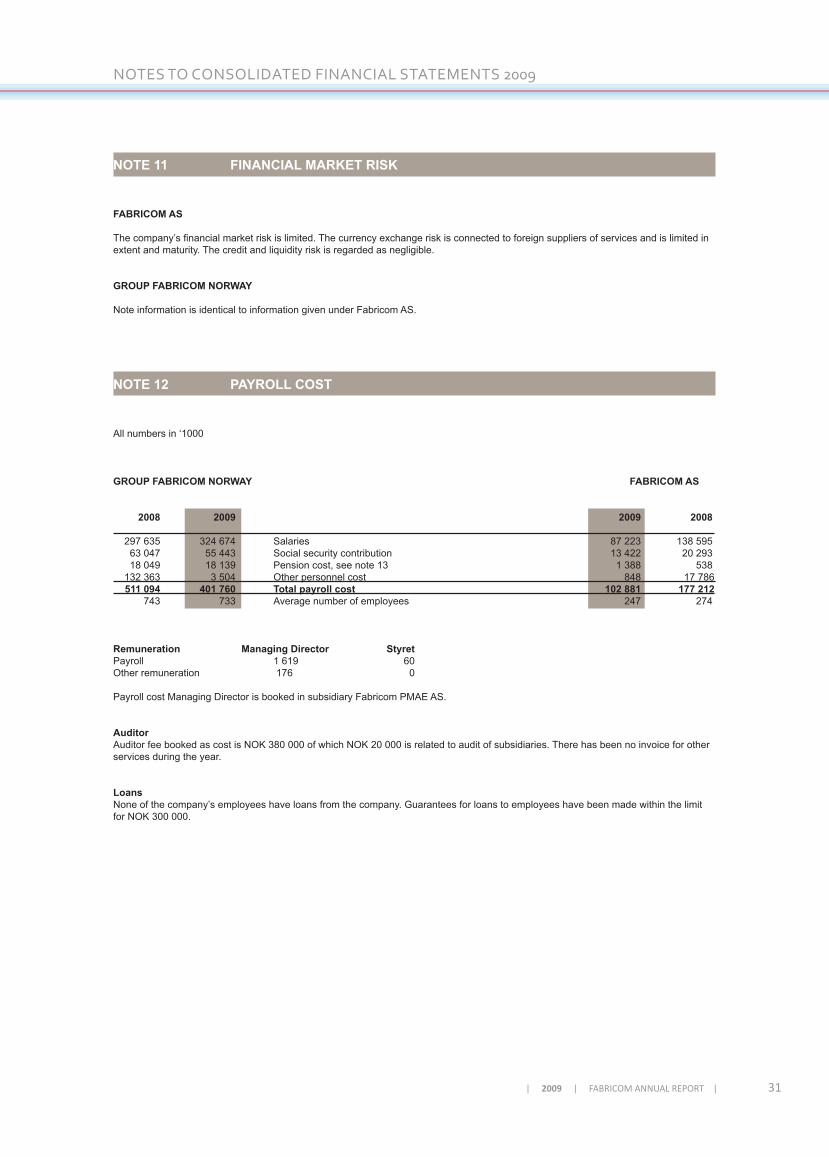

NOTE 11 FINANCIAL MARKET RISK

FABRICOM AS The company’s financial market risk is limited. The currency exchange risk is connected to foreign suppliers of services and is limited in extent and maturity. The credit and liquidity risk is regarded as negligible. GROUP FABRICOM NORWAY

Note information is identical to information given under Fabricom AS.

NOTE 12 PAYROLL COST

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008 297 635 324 674 Salaries 87 223 138 595 63 047 55 443 Social security contribution 13 422 20 293 18 049 18 139 Pension cost, see note 13 1 388 538 132 363 3 504 Other personnel cost 848 17 786 511 094 401 760 Total payroll cost 102 881 177 212 743 733 Average number of employees 247 274

Remuneration Managing Director Styret Payroll 1 619 60 Other remuneration 176 0 Payroll cost Managing Director is booked in subsidiary Fabricom PMAE AS. Auditor Auditor fee booked as cost is NOK 380 000 of which NOK 20 000 is related to audit of subsidiaries. There has been no invoice for other services during the year. Loans None of the company’s employees have loans from the company. Guarantees for loans to employees have been made within the limit for NOK 300 000.

32 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009S

M

L

XL

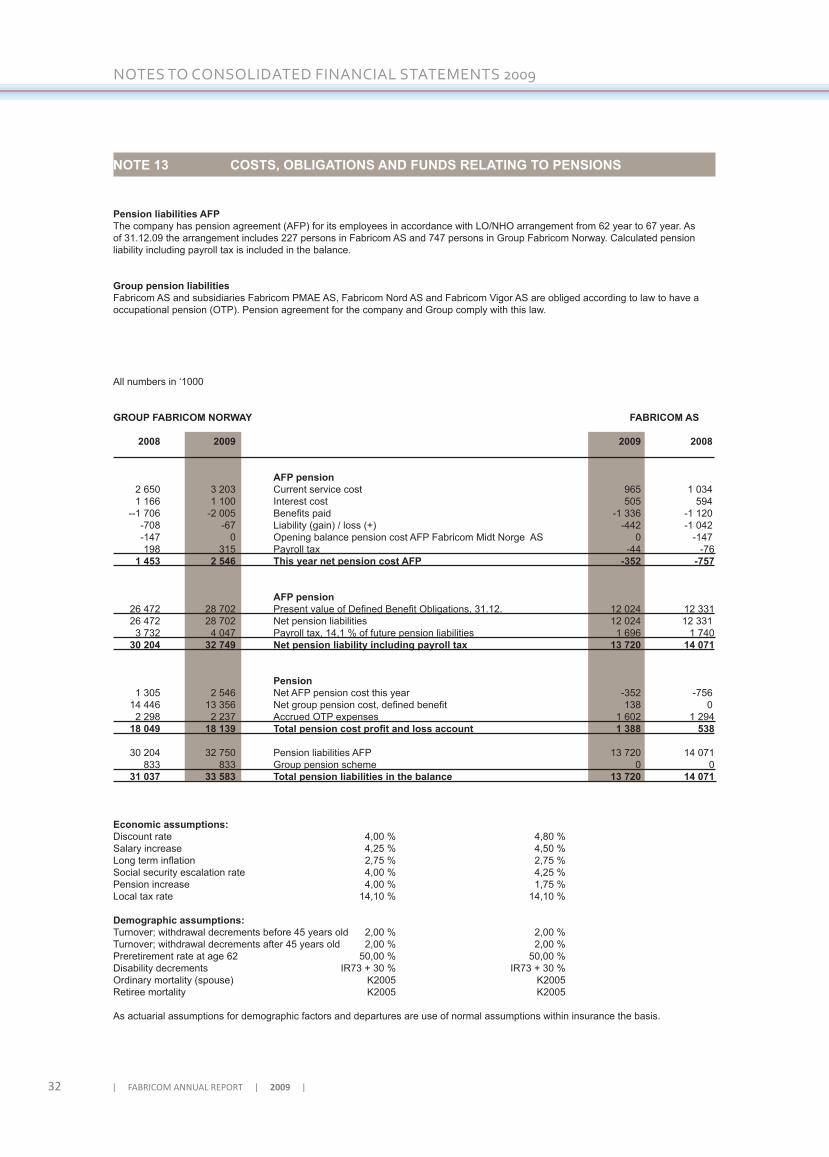

NOTE 13 COSTS, OBLIGATIONS AND FUNDS RELATING TO PENSIONS

Pension liabilities AFP The company has pension agreement (AFP) for its employees in accordance with LO/NHO arrangement from 62 year to 67 year. As of 31.12.09 the arrangement includes 227 persons in Fabricom AS and 747 persons in Group Fabricom Norway. Calculated pension liability including payroll tax is included in the balance. Group pension liabilities Fabricom AS and subsidiaries Fabricom PMAE AS, Fabricom Nord AS and Fabricom Vigor AS are obliged according to law to have a occupational pension (OTP). Pension agreement for the company and Group comply with this law. All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008 AFP pension 2 650 3 203 Current service cost 965 1 034 1 166 1 100 Interest cost 505 594 --1 706 -2 005 Benefits paid -1 336 -1 120 -708 -67 Liability (gain) / loss (+) -442 -1 042 -147 0 Opening balance pension cost AFP Fabricom Midt Norge AS 0 -147 198 315 Payroll tax -44 -76 1 453 2 546 This year net pension cost AFP -352 -757

AFP pension 26 472 28 702 Present value of Defined Benefit Obligations, 31.12. 12 024 12 331 26 472 28 702 Net pension liabilities 12 024 12 331 3 732 4 047 Payroll tax, 14,1 % of future pension liabilities 1 696 1 740 30 204 32 749 Net pension liability including payroll tax 13 720 14 071 Pension 1 305 2 546 Net AFP pension cost this year -352 -756 14 446 13 356 Net group pension cost, defined benefit 138 0 2 298 2 237 Accrued OTP expenses 1 602 1 294 18049 18139 Totalpensioncostprofitandlossaccount 1388 538 30 204 32 750 Pension liabilities AFP 13 720 14 071 833 833 Group pension scheme 0 0 31 037 33 583 Total pension liabilities in the balance 13 720 14 071

Economic assumptions: Discount rate 4,00 % 4,80 %Salary increase 4,25 % 4,50 %Long term inflation 2,75 % 2,75 %Social security escalation rate 4,00 % 4,25 %Pension increase 4,00 % 1,75 %Local tax rate 14,10 % 14,10 % Demographic assumptions: Turnover; withdrawal decrements before 45 years old 2,00 % 2,00 %Turnover; withdrawal decrements after 45 years old 2,00 % 2,00 %Preretirement rate at age 62 50,00 % 50,00 %Disability decrements IR73 + 30 % IR73 + 30 %Ordinary mortality (spouse) K2005 K2005Retiree mortality K2005 K2005 As actuarial assumptions for demographic factors and departures are use of normal assumptions within insurance the basis.

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 33

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009

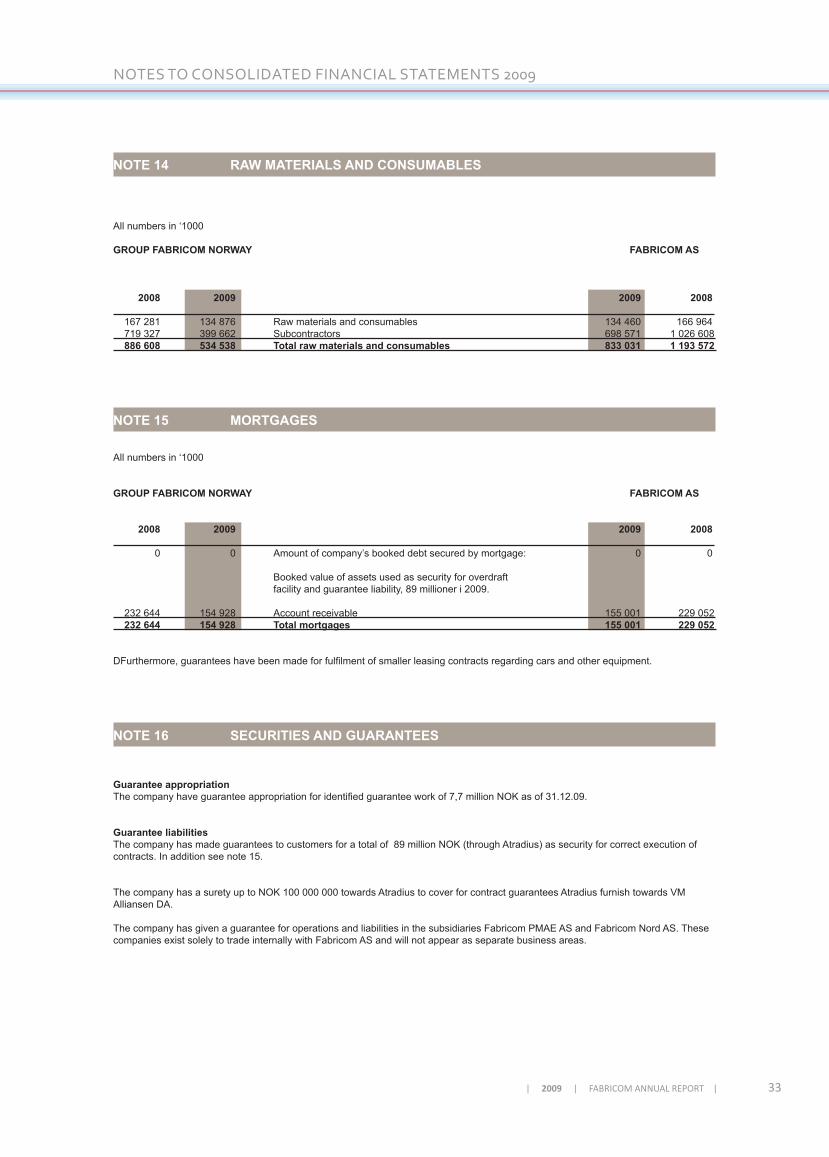

NOTE 14 RAW MATERIALS AND CONSUMABLES

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008 167 281 134 876 Raw materials and consumables 134 460 166 964 719 327 399 662 Subcontractors 698 571 1 026 608 886608 534538 Totalrawmaterialsandconsumables 833031 1193572

NOTE 15 MORTGAGES

All numbers in ‘1000

GROUP FABRICOM NORWAY FABRICOM AS

2008 2009 2009 2008 0 0 Amount of company’s booked debt secured by mortgage: 0 0 Booked value of assets used as security for overdraft facility and guarantee liability, 89 millioner i 2009. 232 644 154 928 Account receivable 155 001 229 052 232 644 154 928 Total mortgages 155 001 229 052

DFurthermore, guarantees have been made for fulfilment of smaller leasing contracts regarding cars and other equipment.

NOTE 16 SECURITIES AND GUARANTEES

Guarantee appropriation The company have guarantee appropriation for identified guarantee work of 7,7 million NOK as of 31.12.09. Guarantee liabilities The company has made guarantees to customers for a total of 89 million NOK (through Atradius) as security for correct execution of contracts. In addition see note 15. The company has a surety up to NOK 100 000 000 towards Atradius to cover for contract guarantees Atradius furnish towards VM Alliansen DA. The company has given a guarantee for operations and liabilities in the subsidiaries Fabricom PMAE AS and Fabricom Nord AS. These companies exist solely to trade internally with Fabricom AS and will not appear as separate business areas.

34 | FABRICOM ANNUAL REPORT | 2009 |

S

M

L

XL

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS 2009S

M

L

XL

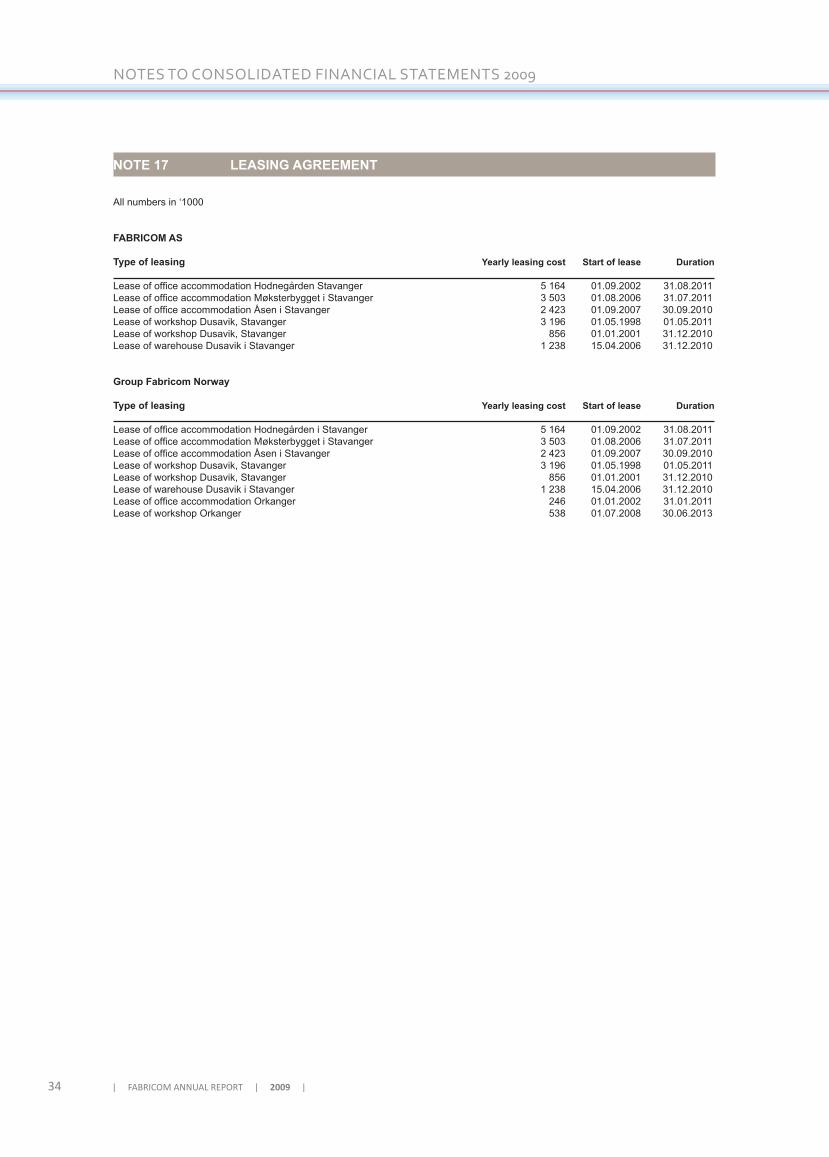

NOTE 17 LEASING AGREEMENT

All numbers in ‘1000

FABRICOM AS

Type of leasing Yearly leasing cost Start of lease Duration Lease of office accommodation Hodnegården Stavanger 5 164 01.09.2002 31.08.2011Lease of office accommodation Møksterbygget i Stavanger 3 503 01.08.2006 31.07.2011Lease of office accommodation Åsen i Stavanger 2 423 01.09.2007 30.09.2010Lease of workshop Dusavik, Stavanger 3 196 01.05.1998 01.05.2011Lease of workshop Dusavik, Stavanger 856 01.01.2001 31.12.2010Lease of warehouse Dusavik i Stavanger 1 238 15.04.2006 31.12.2010

GroupFabricomNorway

Type of leasing Yearly leasing cost Start of lease Duration Lease of office accommodation Hodnegården i Stavanger 5 164 01.09.2002 31.08.2011Lease of office accommodation Møksterbygget i Stavanger 3 503 01.08.2006 31.07.2011Lease of office accommodation Åsen i Stavanger 2 423 01.09.2007 30.09.2010Lease of workshop Dusavik, Stavanger 3 196 01.05.1998 01.05.2011Lease of workshop Dusavik, Stavanger 856 01.01.2001 31.12.2010Lease of warehouse Dusavik i Stavanger 1 238 15.04.2006 31.12.2010Lease of office accommodation Orkanger 246 01.01.2002 31.01.2011Lease of workshop Orkanger 538 01.07.2008 30.06.2013

S

M

L

XL

| 2009 | FABRICOM ANNUAL REPORT | 35

S

M

L

XL

AUDITOR’S REPORT

Fabricom ASSkogstøstraen 254029 Stavanger

51 87 90 00www.fabricom.no

| Design: A

nne Katrine Løklingholm

& G

rete Dubland | Foto: H

ege Hoem

& A

nne Katrine Løklingholm

| Foto side 18: Statoil | Trykk: S

tavanger Bryne O

ffset |