y m ou n c a r bo n t o a i r n e m w a r o...

TRANSCRIPT

RO

CKY MOUNTAIN

INSTIT UTE

WAR R O O M

CARBON

Amory B. LovinsCofounder and Chief Scientist

© 2015 Rocky Mountain Institute

Stanford 2015 Climate and Energy Project Research SymposiumStanford University, 13 October 2015

Oil and Electricity’sDisruptive

Futures

RO

CKY MOUNTAIN

INSTIT UTE

WAR R O O M

CARBON

The rise and fall of the U.S. whaling industry

Lamp retrofits from whale oil to coal oil gain market traction

Drake strikes oilin Pennsylvania

The rise and fall of the U.S. whaling industry

, become commonconsumption of whale oil + sperm oil in American

market (1,000 US gallons)

0

2000

4000

6000

8000

1805 1815 1825 1835 1845 1855 1865 1875 1885 1895

year

0.5

1.0

1.5

2.0annual-average real price of whale oil + sperm oil

(2000 $/US gallon)

50

100

150

Lum

inou

s ef

ficac

y (lm

/W)

Incandescent lamp1879

200

250

300

1900 1950 20000

Years

1996

LED and PV

50

100

150

Lu

min

ous e

ffic

acy (

lm/W

)

Fluorescent lamp

Incandescent lamp

Halogen lamp

Sodium-vapor lamp

1965

1938

1959

1879

200

250

300

1900 1950 20000

Years

1996

50

100

150

Lu

min

ous e

ffic

acy (

lm/W

)

Fluorescent lamp

Incandescent lamp

Halogen lamp

Sodium-vapor lamp

White LED

1965

1938

1959

1879

200

250

300

1900 1950 20000

Years

1996

Sources: L: courtesy of Dr. Yukio Narukawa (Nichia Corp., Tokushima, Japan) from J. Physics. D: Appl. Phys. 43(2010) 354002, doi:10.1088/0022-3727/43/35/354002, updated by RMI with CREE lm/W data, 2015, www.cree.com/News-and-Events/Cree-News/Press-Releases/2014/March/300LPW-LED-barrier;. R: RMI analysis, at average 2013 USEIA fossil-fueled generation efficiencies and each year’s real fuel costs (no O&M); utility-scale PV: LBNL, Utility-Scale Solar 2013 (Sep 2014), Fig. 18; onshore wind: USDOE, 2013 Wind Technologies Market Report (Aug 2014), “Windbelt” (Interior zone) windfarms’ average PPA; German feed-in tariff (falls with cost to yield ~6%/y real return): Fraunhofer ISE, Cost Perspective, Grid and Market Integration of Renewable Energies, p 6 (Jan 2014); all sources net of subsidies; graph inspired by 2014 “Terrordome” slide, Michael Parker, Bernstein Alliance

0

100

200

300

400

500

600

700

800

1990

1994

1998

2002

2006

2010

2014

Coal-fired steam turbine, fuel cost onlyOil-fired condensing, fuel cost onlyNatural gas CCGT, fuel cost onlyUtility-scale solar PV, total costOnshore windpower, total costGerman PV residential feed-in tariff

Real

bus

bar p

rice

or fu

el c

ost,

2011

US$

/MW

h

(Seattle-like climate)

What if the biggest threats weren’t on the radar?

0

50

100

150

200

250

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Intensity decrease has had 31× the impact of renewable growthU

.S. p

rimar

y en

ergy

use

(qua

drilli

on B

TU/y

)

primary energy use if at 1975 efficiency and structure

actual primary energy use

total renewable energy use

1975–2014 savings from intensity reduction:

2,089 qBTU

1975–2014 growth in total renewable output:

67 qBTU

primary energy use, 1965–1975

energy saved by reduced intensity

Who’s the competition?

Rex TillersonChairman and CEO, ExxonMobil

Ali bin Ibrahim al-NaimiSaudi oil minister

Pål KibsgårdCEO, Schlumberger Ltd.

Who’s the competition?

Elon Musk, Tesla, SolarCity, SpaceX

Robin Chase, Zipcar, GoLoco, Buzzcar

Peter Calthorpe, architect

Ferdinand Piëch, Volkswagen (ret.)

Lee Eng Lock, efficiency engineer

Anna Jaffe, Mobi

Michael Brylawski,VisionFleet

Sebastian Thrun, Google’s self-driving car

188.5610 from https://www.thehenryford.org/exhibits/pic/2004/July.asp

“I can’t wait to see what

happens when our industries merge.”

If a problem can’t be solved, enlarge it.

—attributed to Dwight Eisenhower

Volume Production of Electrified Carbon-Fiber Cars

VW XL1 2-seat plug-in hybrid2014 low-volume production

235 mpge, 1,759 lb0.9 L/100 km, 798 kg

BMW i3 4-seat battery-electric hatchback2013– midvolume production, $41–45k

124 mpg, 185+-mile range-extender option1.9 L/100 km, 300+-km range-extender option

Hypercar Revolution 5-seat hybrid SUV2000 virtual design (RMI with two Tier Ones)

67 mpg (gasoline) or 114 mpge (H2), 1,887 lb (–53%)3.6 L/100 km (gasoline) or 2.1 (H2), 857 kg (–53%)

Toyota 1/X 4-seat plug-in hybrid2007 concept car

131 mpge, 926 lb (–70%)1.8 L/100 km, 420 kg (–70%)

!

Batteries’ Costs Continue to Plummet

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050

$/kW

h

US Energy InformationAdministration

Average expert projectionNavigant, Bloomberg New Energy Finance

GTM research

Tesla announcement

2012

!!

Tripled-Efficiency Trucks and Planes

Enabled by IT, multiple transportation methods provide a seamless, cheaper, more pleasant user experience

Autonomous vehicles: from PIGS to SEALs

From PIGS to SEALS

Transportation problems in China

From disorganized chaos to smooth travel experience

From superblock to walking distance

Graphics courtesy of Peter Calthorpe

0

5

10

15

20

25

2010 2015 2020 2025 2030 2035 2040 2045 2050

Mbb

l/d

despite 90% more automobility, 118% more trucking, 61% more flyingTransportation Without Oil

Oil Biofuels Electricity Hydrogen More-Productive Use Efficiency EIA Savings

Source: A.B. Lovins & RMI, Reinventing Fire (2011), Chelsea Green (White River Junction VT), www.rmi.org/reinventingfire.

“We must leave oilbefore it leaves us.”Fatih BirolChief EconomistInternational Energy Agency 2008

Executive Director

U.S. natural gas prices, 1985–2015: official forecasts vs. reality

0

2

4

6

8

10

1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Hen

ry H

ub p

rice

(201

1 $/

MC

F)

Year

85

86 87

89

90

91

92

9495

9697

98

00

02

03

04

05

07

08

0910

11

12

93

1314

01

99

Inde

x of

U.S

. Prim

ary

Ener

gy

Per D

olla

r of R

eal G

DP

Heresy HappensU.S. energy intensity

0

0.25

0.5

0.75

1

1.25

1975 1990 2005 2020 2035 2050

Government and Industry Forecasts, 1975

Reinventing Fire, 2011

Lovins, Foreign Affairs, Fall 1976

Actual

Lovins House, Old Snowmass, Colorado (1983)

U.S. buildings: 3–4× energy productivity worth 4× its cost(site energy intensities in kWh/m2-y; U.S. office median ~293)

284➝85 (–70%)2013 retrofit

~277➝173 (–38%)2010 retrofit

...➝108 (–63%) 2010–11 new

...➝≤50 (–83% to –85%)2015 new

80% energy savings in Hyderabad office, lower capex

Infosys DSB1 (2009): world’s largest side-by-side HVAC experimentRadiant side (11,152 m2): 66 kWh/m2-y (–80%), capex –9%

Courtesy of Peter Rumsey PE FASHRAE (Senior Advisor, RMI) and Rohan Parikh (Infosys, Bangalore)

Radical Efficiencymotors, pumps, and pipes

Saving Electricitymotors, pumps, and pipes

Less CapitalInvestmentsmaller equipment

Power Plant Power Grid Motor/Drivetrain Pump/Throttle Pipe-70% -9% -12% -55% -20%

100Energy units

5 %Delivered flow

Power Plant Power Grid Motor/Drivetrain Pump/Throttle Pipe-70% -9% -12% -55% -20%

Energy units

5 %Delivered flow

50

radically efficient industrial redesign

Netherlands: community connection

Utility revenues

Efficiency Distributed renewables

Storage (including EVs)

Flexible demand

New financial and business models

Regulatory shifts

Customer preferences

Integrative design

$

Utility revenues

Efficiency

Integrative design

$

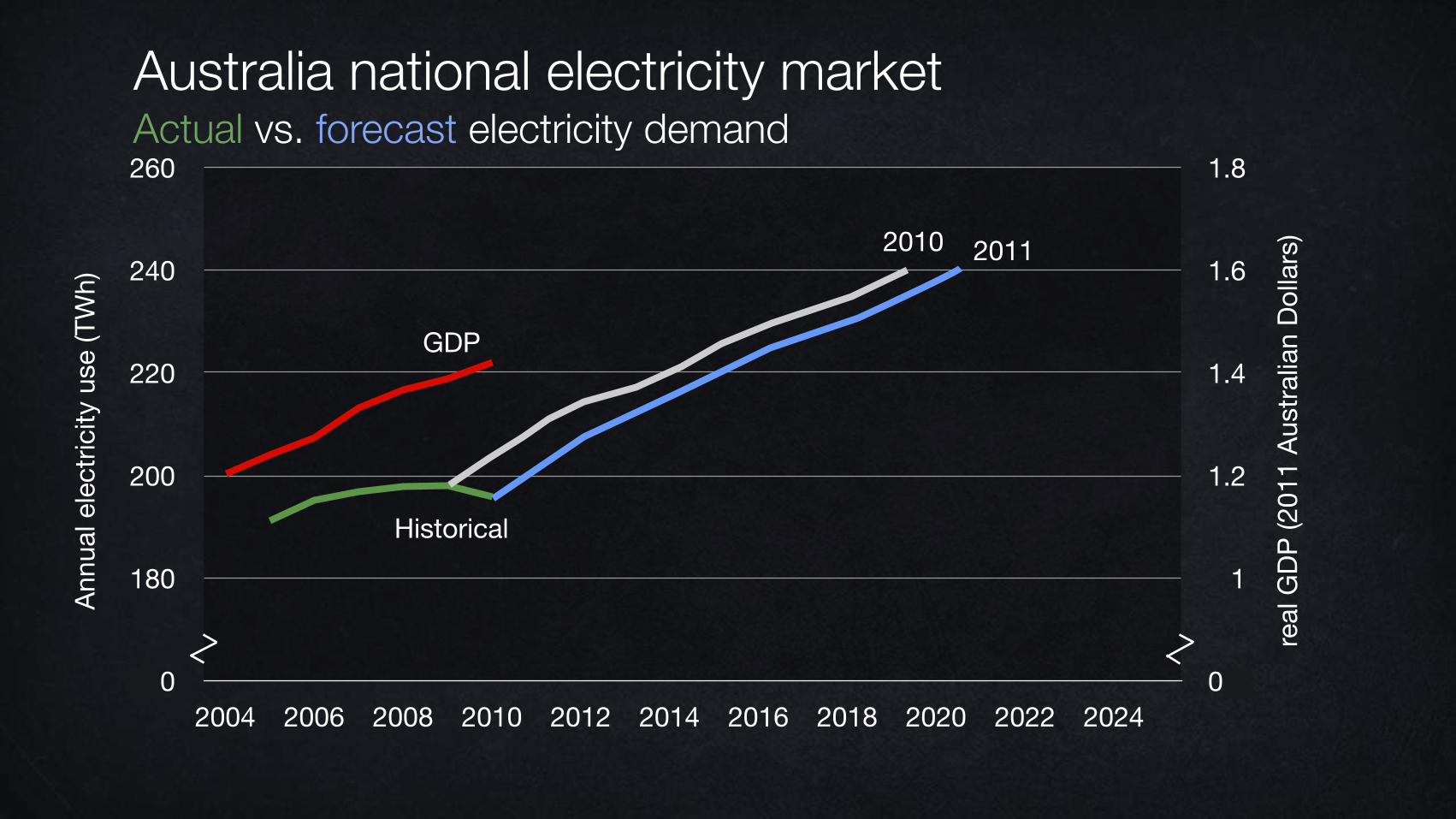

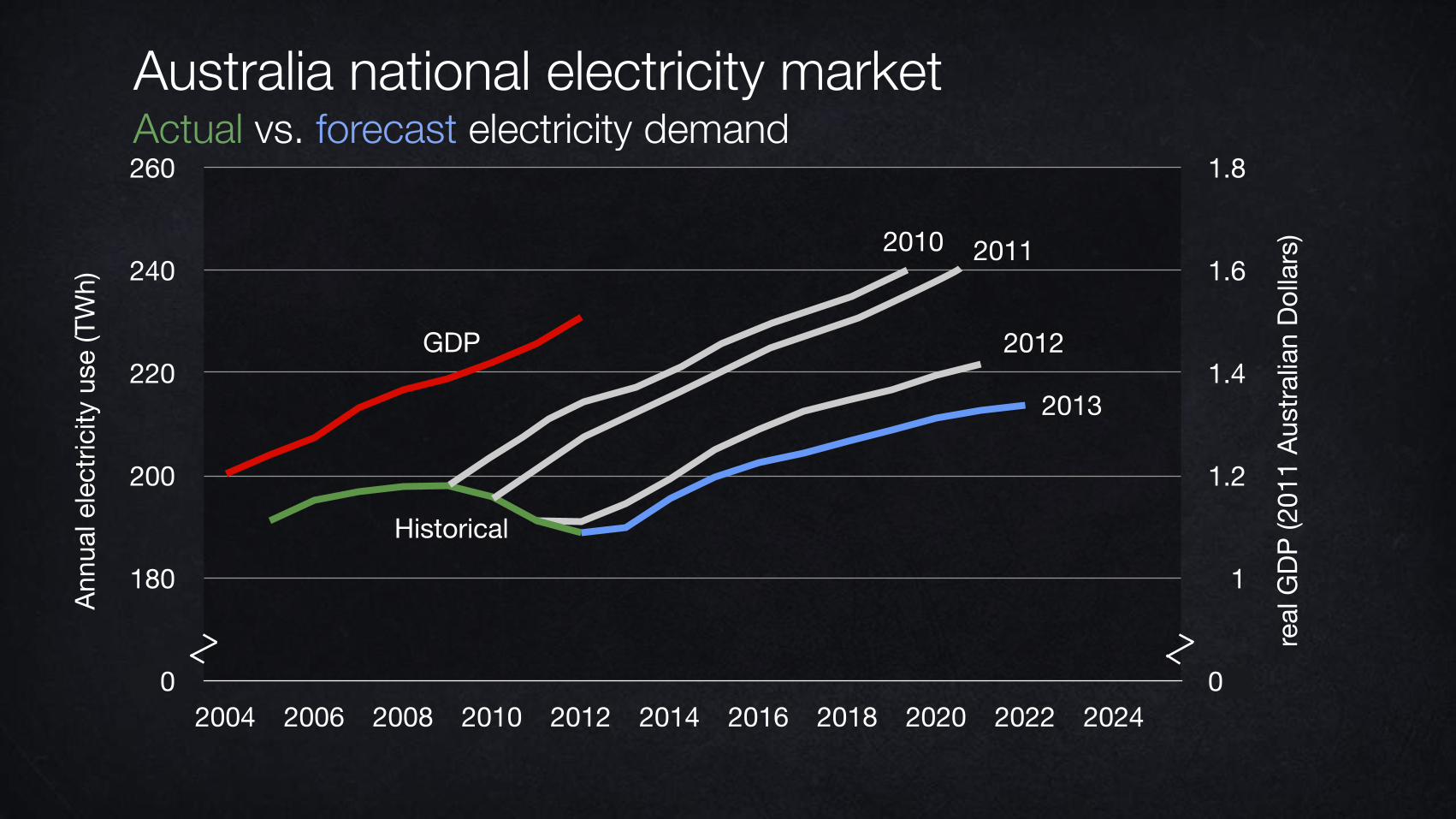

Australia national electricity marketActual vs. forecast operational electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

Source: M. Liebreich, keynote, Bloomberg New Energy Finance summit, April 2015; 2014–15

Actual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2010

Australia national electricity market

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2010

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2013

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2013

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2013

2014

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2013

2014

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

160

180

200

220

240

260

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 20240.8

1

1.2

1.4

1.6

1.8

Annu

al e

lect

ricity

use

(TW

h)

real

GDP

(201

1 Au

stra

lian

Dolla

rs)

GDP

Historical

2012

2013

2014

2010 2011

Australia national electricity marketActual vs. forecast electricity demand

Utility revenues$ Distributed

renewables

Storage (including EVs)

Flexible demand

2002 2004 2006 2008 2010 2012 2014 2016

Renewable Energy’s Costs Continue to PlummetWind and photovoltaics: U.S. generation-weighted-average Power Purchase Agreement prices, by year of signing

U.S. wholesale power price

wind PPAs

utility-scale solar PPAs

250

200

150

100

50Pric

e (le

veliz

ed 2

014

$/M

Wh)

0

Cap

acity

add

ition

s (G

W)

Global power generation capacity additions, 2012–30

0

100

200

300

2012 2013 2015 2020 2025 2030

CoalGasOilNuclear

0

100

200

300

2012 2013 2015 2020 2025 2030

WindSolarHydroBiomass and wasteOther

10687 78

6452

39

Forecast

93 100

146

181

225

290Forecast

Source: Bloomberg New Energy Finance, redrawn from Michael Liebreich’s Summit Keynote, 7 April 2014

0 10 10 91 0Years

“Cathedral” Photovoltaics

0 10 20 30 40 50 60 70 8

0 GW-y1 GW-y3 GW-y6 GW-y10 GW-y15 GW-y21 GW-y28 GW-y36 GW-y45 GW-y0 GW-y3 GW-y1 GW-y2 GW-y

French windpower output, December 2011: forecasted one day ahead vs. actual

Variable Renewables Can Be Forecasted At Least as Accurately as Electricity Demand

Source: Bernard Chabot, 10 April 2013, Fig. 7, www.renewablesinternational.net/wind-power-statistics-by-the-hour/150/505/61845/, data from French TSO RTE

GW

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

!10% Downtime

!12% Downtime

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

Wind (37 GW)

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

Solar (25 GW)Wind (37 GW)

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

Solar (25 GW)Wind (37 GW)

Geothermal etc.

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

Solar (25 GW)Wind (37 GW)

Geothermal etc.Biomass/biogas

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Geothermal etc.

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

HVAC ice/EV storageBiomass/biogas

Solar (25 GW)Wind (37 GW)

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Geothermal etc.

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

HVAC ice/EV storageBiomass/biogas

Storage recovery

Solar (25 GW)Wind (37 GW)

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Geothermal etc.

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

HVAC ice/EV storageBiomass/biogas

Storage recoveryDemand response

Solar (25 GW)Wind (37 GW)

Original loadLoad after efficiency

0

10

20

30

40

50

60

GW

Day

1 2 3 4 5 6 7

Geothermal etc.

Choreographing Variable Renewable GenerationERCOT power pool, Texas summer week, 2050 (RMI hourly simulation)

HVAC ice/EV storageBiomass/biogas

Storage recoveryDemand response

Solar (25 GW)Wind (37 GW)

Spilled power (~5%)

Europe, 2014 renewable % of total electricity consumed

Choreographing Variable Renewable Generation

27%Germany (2013 peak 70%)

≥55%Denmark (33% wind; 2013 windpower peak 136%—55% for all December)

50%Scotland

46%Spain (including 21% wind, 14% hydro, 5% solar)

64%Portugal (peak 100% in 2011; 70% for the whole first half of 2013, incl, 26% wind & 34% hydro; 17% in 2005)

1980

Denmark’s transition to distributed electricity, 1980–2012Central thermalOther generationWind turbines

2012

Source: Risø

Utility revenues

Customer preferences

$

Cascading blackouts threaten security

New Jersey, United States: resilience

Similar DifferentRisksCosts

India: air, reliable electricity, and development

Beijing, China: air

Germany: prosperity, climate, democracy

Stork near Schöneck, Frank Rumpenhorst/EPA, www.theguardian.com/environment/gallery/2014/may/02/the-beauty-of-windfarms-in-pictures

www.earthzine.org/wp-content/uploads/2013/08/solar-power.jpg

Stephen Glassman, https://stevenglassman.files.wordpress.com/2014/07/ballooning-10.jpg

Hawai‘i, United States: affordability and independence

Utility revenues$ Distributed

renewables

Storage (including EVs)

Flexible demand

Cheaper renewables and batteries change the gameIn Westchester, NY, 60% of residential consumption in the next decade could come more cheaply from PV

Source: RMI analysis “The Economics of Load Defection,” 2015

Load control + PVs = grid optional

0"

2"

4"

6"

8"

10"

12"

kW#

Uncontrolled: ~50% of solar PV production is sent to the grid, but if the utility doesn’t pay for that energy, how could customers respond?

EV-charging

!"!!!!

!2.00!!

!4.00!!

!6.00!!

!8.00!!

!10.00!!

!12.00!!

kW#

Unc!Load! Smart!AC! Smart!DHW! Smart!Dryer!

0"

2"

4"

6"

8"

10"

12"

kW#

Controlled: flexible load enables customers to consume >80% of solar PV production onsite. The utility loses nearly all its windfall and most of its ordinary revenue.

AC

DHW

Dryer

Other

Solar PVAC

DHW

Dryer

Other

Solar PVEV-charging

Source: RMI analysis “The Economics of Load Flexibility,” 2015

Utility revenues$

New financial and business models

Regulatory shifts

How can incumbents respond to the electricity shift?

http://recruitingdaily.com/wp-content/uploads/sites/6/2014/09/ostrich-in-sand.jpg

The Koch Attack on Solar EnergyBy THE EDITORIAL BOARDAPRIL 26, 2014

Solar Companies Sue Over New Rooftop Solar Tax In Arizona

No Free Sun for You! Why Arizona Wants to ‘Tax’ Solar PowerA new proposal would slap existing solar-paneled homeowners with a fee of up to $100 per month for the privilege of selling excess power back to the grid.

The world's dumbest idea: Taxing solar energy

Conservative group ALEC pushes stealth tax on homeowners who install solar panels

The German exampleSh

are

pric

e ($

/sha

re),

Euro

pean

Util

ities

Sha

re P

rice

50

70

90

110

130

150

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: Morgan Stanley Capital International

European utilities lost $500

billion market cap in 6 years

The German example

重 能 :中源塑 国⾯面向2050年能源消费和⽣生产⾰革命路线图研究

Price > CostValue >

1900: where’s the first car?

Easter Parades on Fifth Avenue, New York, 13 years apart

1913: where’s the last horse?

Images: L, National Archive, www.archives.gov/research/american-cities/images/american-cities-101.jpg; R, shorpy.com/node/204. Inspiration: Tona Seba’s keynote lecture at AltCar, Santa Monica CA, 28 Oct 2014, http://tonyseba.com/keynote-at-altcar-expo-100-electric-transportation-100-solar-by-2030/

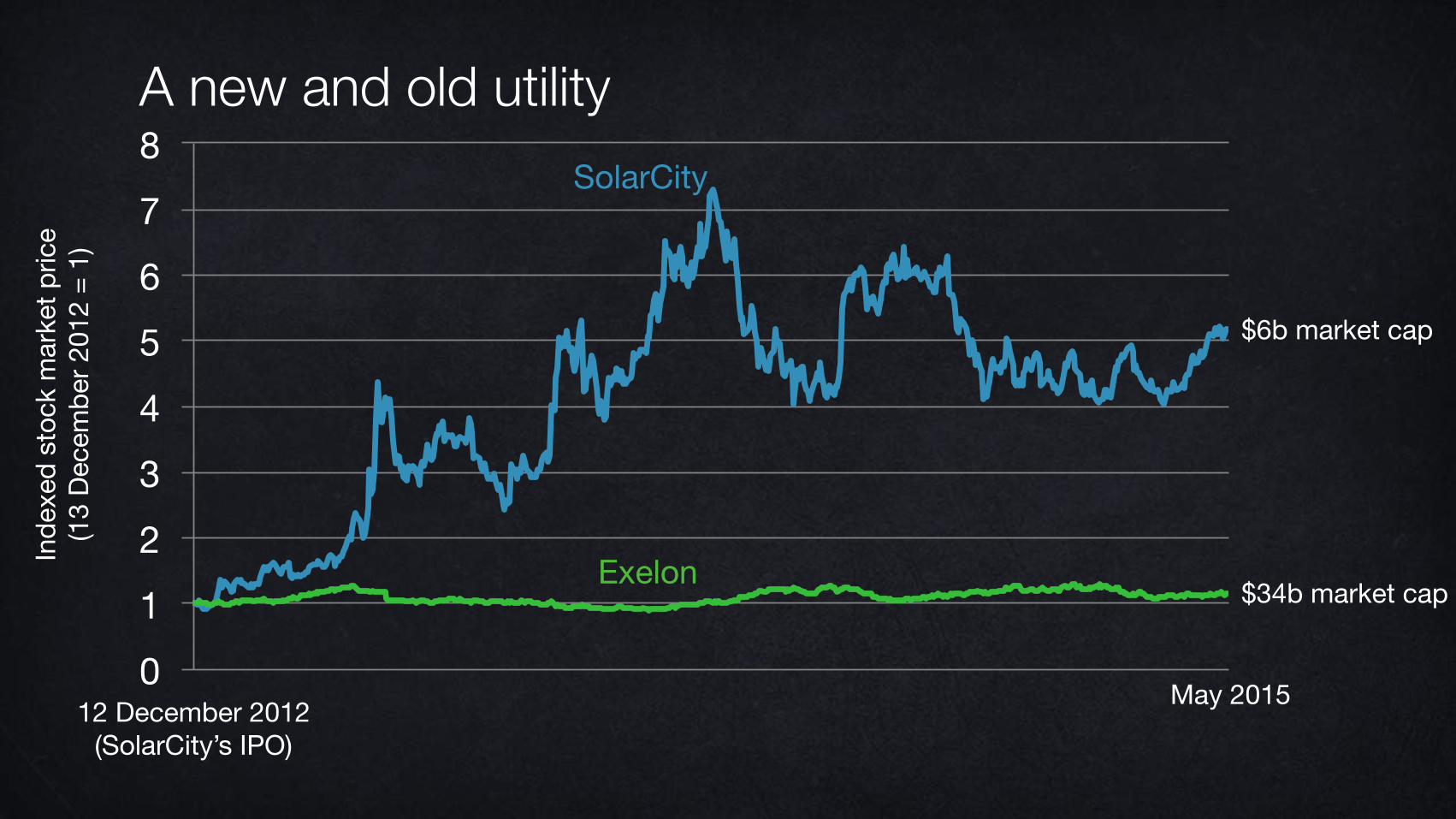

0 1 2 3 4 5 6 7 8

May 2015

SolarCity

Exelon

A new and old utilityIn

dexe

d st

ock

mar

ket p

rice

(13

Dece

mbe

r 201

2 =

1)

12 December 2012(SolarCity’s IPO)

$6b market cap

$34b market cap

29 June 2010(Tesla’s IPO)

May 2015

Tesla

0

2

4

6

8

10

12

14 A new and old automaker

General MotorsInde

xed

stoc

k m

arke

t pric

e(3

0 Ju

ne 2

010

= 1)

$30b market cap

$57b market cap

50 thousand cars per year

8 million cars per year

82

WHERE WOULD YOU INVEST YOUR MONEY?

OR

83

WHERE WOULD YOU INVEST YOUR MONEY?

OR

From the Age of Carbon to the Age of Silicon

Renewables replacing $38b/y kerosene market

reinventingfire.com | www.rmi.org, [email protected] | Twitter @AmoryLovins

www.ted.com/talks/amory_lovins_a_50_year_plan_for_energy.html

www.rmi.org/Knowledge-Center/Library/2012-01_FarewellToFossilFuels

RO

CKY MOUNTAIN

INSTIT UTE

WAR R O O M

CARBON