ye 2015-presentation-final-20160330-8 pm-2

TRANSCRIPT

2015 RESULTS

PRESENTATION

March 2016

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

DISCLAIMER

2

These materials may contain projections and forward-looking statements that reflect the Company’s

current views with respect to future events and financial performance. Readers are cautioned not to

place undue reliance on these forward-looking statements, which involve inherent risks, uncertainties

and assumptions. No assurance can be given that actual results will be consistent with these forward-

looking statements. The Company assumes no obligation to update or revise any forward-looking

statements.

These materials are for information purposes only and do not constitute or form part of any invitation or

offer to acquire, purchase or subscribe for any securities or the provision of any investment advice, and

none of them shall form the basis of or be relied upon in connection with any contract, commitment or

investment decision in relation thereto. These materials do not constitute a recommendation regarding

the securities of the Company.

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

FINANCIAL HIGHLIGHT

3

USD Million3 RM Million3

2015 2014 Change (%) 2015 2014 Change (%)

Revenue 148.6 165.1 (10.0) 580.4 540.3 7.4

EBITDA1 102.8 56.1 83.2 401.4 183.7 118.5

Adjusted EBITDA2 61.3 65.0 (5.7) 239.4 212.8 12.5

Profit for the year 87.4 37.8 131.2 341.2 123.8 175.6

Adjusted Profit for the year2 45.9 46.7 (1.7) 179.2 152.9 17.2

Profit for the year attributable to

owners of the Company

86.8 35.8 142.5 339.2 117.1 189.7

Adjusted profit for the year

attributable to owners of the

Company2

45.3 44.6 1.6 177.2 146.2 21.2

Contract sales 197.5 206.7 (4.4) 771.7 676.6 14.1

1. EBITDA is calculated by adding finance cost and depreciation and amortization to profit before taxation.

2. Adjusted to exclude (a)USD41.5 million (equivalent to RM162.0 million) of net foreign exchange gain in 2015, (b)USD3.3 million

(equivalent to RM10.7 million) in share-based payment expenses in 2014, (c) USD5.3 million (equivalent to RM17.3 million) Listing

expenses in 2014, and (d) USD0.3 million (equivalent to RM1.1 million) of other expenses relating to the Listing in 2014.

3. The above amounts denominated in RM have been translated into USD at the exchange rates of 3.9064 and 3.2733 for 2015 and 2014,

respectively.

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

FINANCIAL HIGHLIGHT

4

206.7 197.5

676.6 771.7

0

200

400

600

800

2014 2015 2014 2015

Am

ou

nt

(Mil

lio

n)

USD

Contract sales

165.1 148.6

540.3 580.4

0

100

200

300

400

500

600

700

2014 2015 2014 2015

Am

ou

nt

(Mil

lio

n)

Decrease 10.0%

Revenue

RM RM USD

Increase in RM terms was primarily due to the increase in sales from

Singapore, and sales contributed from newly launched Nirvana Center Kuala

Lumpur in Malaysia, Thailand and Hong Kong

Increase in revenue are mainly derived from Semenyih and Kulai in

Malaysia.

65.0 61.3

212.8 239.4

0

50

100

150

200

250

300

2014 2015 2014 2015

Am

ou

nt

(Mil

lio

n)

Adjusted EBITDA

44.6 45.3

146.2 177.2

0

50

100

150

200

2014 2015 2014 2015

Am

ou

nt

(Mil

lio

n)

Adjusted profit for the year attributable to

owners of the Company

RM RM USD USD

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

166.6 140.4 226.8 203.1 224.7

110.1 133.3

165.9 202.6

300.1 74.7 84.5

77.5 130.8

107.0

72.0 114.7

84.5

91.4

111.7

14.4 22.6

20.6

48.7

28.2

0

100

200

300

400

500

600

700

800

900

2011 2012 2013 2014 2015(R

M 'm

) 437.8

495.5 575.3

676.6

771.7

54.5 45.4 72.0 62.0 57.5

36.0 43.2

52.6 61.7 76.8 24.4 27.4

24.6 39.9 27.4

23.5 37.1

26.8 27.9 28.6

4.7 7.3

6.6

15.2 7.2

0

50

100

150

200

250

2011 2012 2013 2014 2015

(US

D 'm

)

143.1 160.4

182.6

206.7 197.5

SOLID GROWTH IN CONTRACT SALES

Contract sales evolution

Contract sales growth has continued to be robust

Burial plots Niches Tomb design and construction services Funeral services Others

5

Our contract sales increased at CAGR of 8.4% in USD terms, and 15.2% in RM terms, from 2011 to 2015.

The Group’s contract sales decreased by 4.4% in USD terms, but increased by 14.1% in RM terms with growth recorded for all 5 countries that the

Group is operating. The increase in RM terms was primarily due to the increase in sales from Singapore, and the newly launched Nirvana Center

Kuala Lumpur in Malaysia, Nirvana Memorial Park in Thailand and sales office in Hong Kong, China. Lower contract sales in USD terms was due to

the strengthening of USD against RM during 2015.

USD RM

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

As-need

16.2%

Pre-need

83.8%

As-need

13.4%

Pre-need

86.6%

6

CONTRACT SALES BREAKDOWN

2014

By need type

2015

By need type

By geography By geography

Malaysia

78.6%

Singapore

16.7%

Indonesia

3.3%

Thailand

1.1%

Hong Kong

0.3%

Malaysia

86.7%

Singapore

9.7%

Indonesia

3.6%

Ex-Malaysia countries’ contribution increased by 8.1 percentage points to 21.4% in 2015.

Pre-need contract sales increased by 2.8 percentage points to 86.6% in 2015.

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

139.0 137.8 144.9 177.5 191.1

111.0 115.2 148.8

195.7 201.0 58.5 73.9

83.9

86.8 104.1

33.9 36.9

39.7

43.7

52.4

15.0 19.8

22.9

36.6

31.8

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015(R

M 'm

)

357.4 383.6

440.2

540.3

580.4

Revenue evolution

SOLID GROWTH IN REVENUE

7

45.4 44.6 46.0 54.2 48.9

36.3 37.3 47.2

59.8 51.5

19.1 23.9

26.6

26.5

26.6 11.1

11.9

12.6

13.4

13.4 4.9 6.4

7.3

11.2 8.2

0

50

100

150

200

2011 2012 2013 2014 2015

(US

D 'm

)

116.8 124.2

139.7

165.1 148.6

Revenue increased at CAGR of 6.2% in USD terms and 12.9% in RM terms from 2011 to 2015.

Revenue for 2015 rose by 7.4% despite 14.1% growth in contract sales primarily due to contract sales from Nirvana Center Kuala Lumpur and

substantial amount of contract sales from Singapore which have not been recognised as revenue in 2015.

Lower revenue in USD terms was mainly due to the strengthening of USD against RM.

Burial plots Niches Tomb design and construction services Funeral services Others

USD RM

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

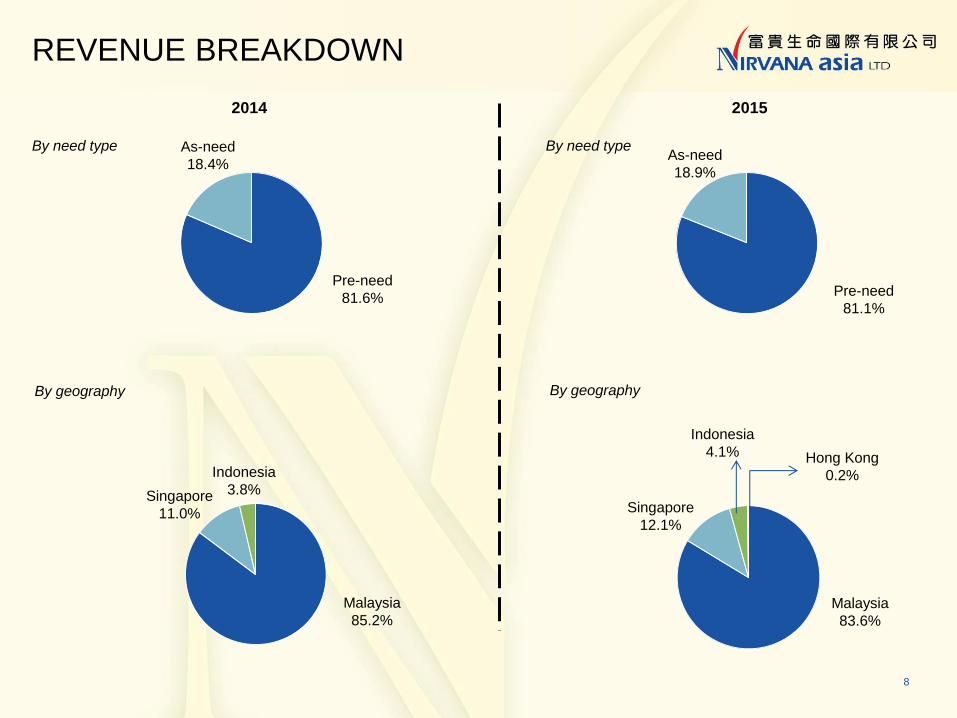

Malaysia

83.6%

Singapore

12.1%

Indonesia

4.1% Hong Kong

0.2%

Malaysia

85.2%

Singapore

11.0%

Indonesia

3.8%

As-need

18.4%

Pre-need

81.6%

As-need

18.9%

Pre-need

81.1%

8

2014

By need type

2015

By need type

By geography By geography

REVENUE BREAKDOWN

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

Burial plots 30.0%

Niches 29.9%

Tomb design and construction

19.3%

Funeral services 13.5%

Others 7.3%

9

2014

By contract sales

2015

By contract sales

By revenue By revenue

BUSINESS SEGMENT

Burial plots 32.8%

Niches 36.2%

Tomb design and construction

16.1%

Funeral services

8.1%

Others 6.8%

Burial plots 32.9%

Niches 34.7%

Tomb design and construction

17.9%

Funeral services

9.0%

Others 5.5%

Burial plots 29.1%

Niches 38.9%

Tomb design and construction

13.9%

Funeral services 14.5%

Others 3.6%

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

Lower contract sales and ASP in USD terms YoY was primarily due to the strengthening of USD against RM. However, in RM terms:

(i) Contract sales increased by 10.6% YoY, primarily contributed by (1) higher sales from (a) Bukit Mertajam and Kulai in Malaysia, and (b)

Indonesia, and (2) the newly launched (a) Nirvana Memorial Park in Thailand, and (b) sales office in Hong Kong, China.

(ii) ASP per sq.m increased by 1.8% YoY largely due to increase in ASP from Semenyih in Malaysia and Indonesia, but partly offset by

lower ASP in Thailand during the initial product launch before the site is ready for interment. Excluding Thailand, ASP per sq.m would

have grown by 3.6% YoY.

BURIAL SERVICES – BURIAL PLOTS

10

Offer single, double, family-sized and garden lot burial plots in our cemeteries

54.5

45.4

72.0

62.0 57.5

675 629

694 686

585

0

200

400

600

800

0

20

40

60

80

100

2011 2012 2013 2014 2015

Contract Sales (USD ’m) ASP per sq.m (USD)

80,635 72,182 103,737 90,501 Sq.m.

sold

Per sq.m. ASP (USD)

54.5 45.4

72.0

27.1

675 629 694 686

0

200

400

600

800

0

50

100

150

2011 2012 2013 1H 2014

Note : ASP means average sales price

80,635 72,182

166.6

140.4

226.8 203.1

224.7

2,066 1,945

2,186 2,244 2,284

0

500

1,000

1,500

2,000

2,500

0

50

100

150

200

250

300

2011 2012 2013 2014 2015

Contract Sales (RM ’m) ASP per sq.m (RM)

98,368 103,737 90,501 98,368

USD RM

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

BURIAL SERVICES - NICHES

11

36.0 43.2

52.6

61.7

76.8

6.7 6.7 6.2

7.0 6.2

0

2

4

6

0

20

40

60

80

100

2011 2012 2013 2014 2015

Offer single, double and family-sized niches in our columbarium facilities

Contract Sales (USD ‘m) ASP per unit (USD '000)

5,391 6,471 8,513 8,850 Unit

sold

Per sq.m. ASP (USD)

54.5 45.4

72.0

27.1

675 629 694 686

0

200

400

600

800

0

50

100

150

2011 2012 2013 1H 2014

12,365 5,391

8

110.1 133.3

165.9 202.6

300.1

20.4 20.6 19.5

22.9 24.3

0

5

10

15

20

25

30

0

100

200

300

400

500

2011 2012 2013 2014 2015

6,471 8,513 8,850 12,365

Contract Sales (RM ‘m) ASP per unit (RM '000)

USD RM

• The Group sold 12,365 niches in 2015, an increase of 39.7% YOY.

• Contract sales increased by 24.5% in USD terms and 48.1% in RM terms YoY, largely attributed to sales growth from Singapore and the

newly launched Nirvana Center Kuala Lumpur in Malaysia.

• Lower ASP in USD terms YoY was primarily due to the strengthening of USD against RM, however in RM terms, ASP for niches increased

by 6.0% YoY primarily due to a higher sales contribution from the Group’s columbarium in Singapore which has a higher ASP.

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

74.7 84.5

77.5

130.8

107.0 1,432

1,733

1,433

1,967 2,046

0

400

800

1,200

1,600

2,000

0

20

40

60

80

100

120

140

160

2011 2012 2013 2014 2015

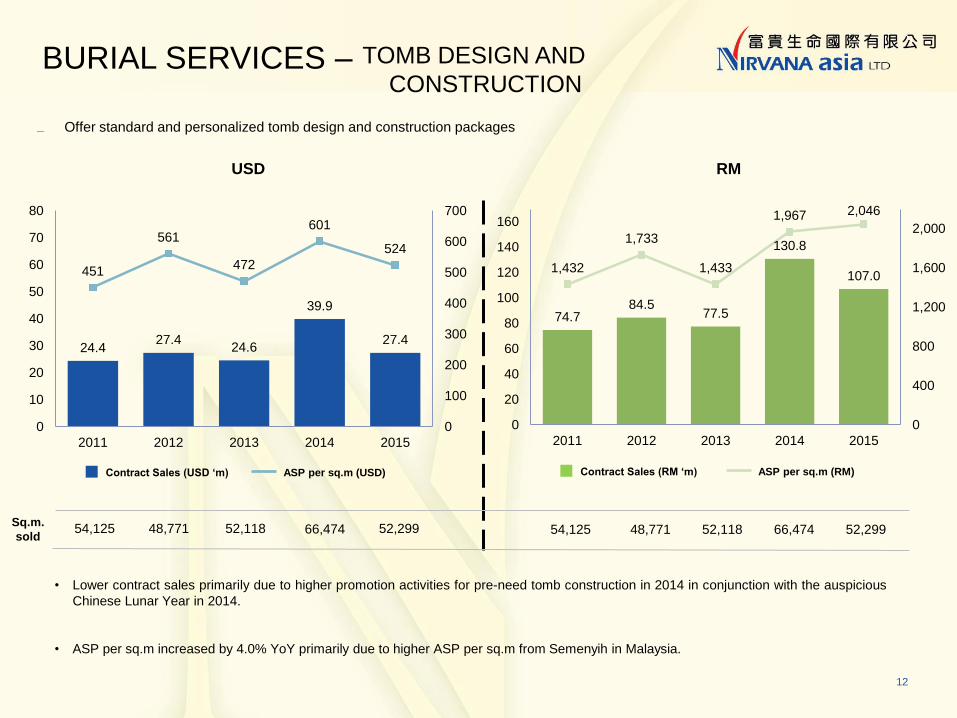

12

TOMB DESIGN AND

CONSTRUCTION

Offer standard and personalized tomb design and construction packages

24.4 27.4

24.6

39.9

27.4

451

561

472

601

524

0

100

200

300

400

500

600

700

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015

Contract Sales (USD ‘m) ASP per sq.m (USD)

BURIAL SERVICES –

54,125 48,771 52,118 66,474 Sq.m.

sold 54,125 48,771 52,299 52,118 66,474 52,299

Contract Sales (RM ‘m) ASP per sq.m (RM)

USD RM

• Lower contract sales primarily due to higher promotion activities for pre-need tomb construction in 2014 in conjunction with the auspicious

Chinese Lunar Year in 2014.

• ASP per sq.m increased by 4.0% YoY primarily due to higher ASP per sq.m from Semenyih in Malaysia.

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

4,054 6,428 4,439 4,617 Cases

sold 4,054 6,428 5,610 4,439 4,617 5,610

13

We provide integrated premium funeral services that include funeral consultation and planning, transportation, embalming, cosmetology and

preparation for viewing, cremation and funeral ceremonies

23.5

37.1

26.8 27.9 28.6

5.8 5.8 6.0 6.0

5.1

0

1

2

3

4

5

6

7

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015

Contract sales & ASP per funeral services

Contract Sales (USD ‘m) ASP per case (USD '000)

Funeral services

FUNERAL SERVICES

72.0

114.7

84.5 91.4

111.7

17.7 17.9 18.9 19.6 19.9

0

5

10

15

20

25

0

20

40

60

80

100

120

140

160

180

2011 2012 2013 2014 2015

Contract Sales (RM ‘m) ASP per case (RM '000)

USD RM

• The Group sold 5,610 funeral services packages in 2015, an increase of 21.5% YOY.

• Contract sales from funeral services increased by 22.2% YoY mainly due to higher sales from as-need funeral services.

• Higher ASP by 1.4% YoY primarily due to increase in ASP of as-need funeral service.

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

76.7 84.8

97.2

116.4 112.4

65.6 68.3 69.6 70.5

75.7

0

10

20

30

40

50

60

70

80

0

20

40

60

80

100

120

140

160

2011 2012 2013 2014 2015

Gross profit (USD 'm) Gross margin (%)

EXPANDING GROSS PROFIT MARGINS We enjoy premium pricing for our products and services through a combination of market leadership,

recognized brand and quality services

14

(%)

• Gross profit margin increased by 5.2 percentage points from 70.5% for 2014 to 75.7% for 2015 was primarily

due to :

(i) higher margin following the acquisition of tomb construction and design business in March 2015

(ii) economies of scale achieved from higher land utilization, and

(iii) better cost management for the funeral services segment.

• Lower gross profit YoY in USD terms was primarily due to the strengthening of USD against RM.

(US

D ‘

m)

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

15

SELLING & DISTRIBUTION EXPENSES

BREAKDOWN

18.8% 16.8% 13.3%

14.1% 13.6%

3.2% 2.7%

2.7%

3.0%

2.9%

3.3%

3.4% 2.7%

3.6%

5.1%

1.5%

0.8% 0.9%

1.1%

1.2%

0.8%

0.7% 0.8%

1.0%

0.8%

0

10

20

30

40

2011 2012 2013 2014 2015

(US

D 'm

)

USD35.0m

USD31.9m

USD30.5m

USD37.5m

USD34.9m

Total as %

of revenue 30.0% 25.7% 21.8% 22.8%

Commissions Incentives Promotion and others

Advertising and newsletter Event and function

The selling and distribution expenses to revenue increased by 0.7 percentage point from 22.8% for 2014 to 23.5%

for 2015. The increase in promotion expenses to revenue is primarily due to certain expenses in connection with the

newly-launched cemeteries in Thailand and Nirvana Center Kuala Lumpur in Malaysia which cannot be deferred in

proportion to contract sales not recognized as revenue during the year.

(% represents % of revenue for the year)

23.5%

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

ADMINISTRATIVE EXPENSES BREAKDOWN

16

Administrative expenses reduced by USD1.6 million, or 5.4%, from USD30.4 million for 2014 to USD28.8 million for

2015, primarily due to one-off share-based payment expenses of USD3.3 million in relation to pre-Listing employees

share rights scheme, which were fully vested in 2014. The increase in staff cost in 2015 was mainly due to the

integration of work force from the newly acquired tomb design and construction business in March 2015.

Staff cost

Administrative and general Depreciation and amortization Others

(% represents % of revenue for the year)

18.0% 18.4% 15.8% 18.4%

10.0% 9.6% 9.7% 9.2%

11.4%

4.5% 5.4%

1.7%

3.7%

3.7%

1.6%

1.6% 1.5%

1.3%

1.2%

2.2%

3.1%

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015

(US

D 'm

) 1.9%

1.9%

USD30.4m

1.8%

USD21.0m USD22.9m

USD22.1m

2.0%

USD28.8m

Employee share right scheme

Total as %

of revenue

1.0%

19.4%

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

EXPANDING EBITDA MARGINS

17

Adjusted EBITDA1,2

We enjoy premium pricing for our products & services through a combination of market leadership,

recognized brand and quality services

31.1

43.9

55.0

65.0 61.3

26.6

35.3

39.4 39.4 41.2

0

5

10

15

20

25

30

35

40

45

0

10

20

30

40

50

60

70

80

90

2011 2012 2013 2014 2015

EBITDA (USD 'm) EBITDA margin (%)

(%)

95.1

135.6

173.3

212.8

239.4

26.6

35.3

39.4 39.4 41.2

0

5

10

15

20

25

30

35

40

45

0

50

100

150

200

250

300

2011 2012 2013 2014 2015

EBITDA (RM 'm) EBITDA margin (%)

(%)

USD RM

Notes:

1 Adjusted to exclude (a) USD41.5 million (equivalent to RM162.0 million) of net foreign exchange gain in 2015, (b) USD3.3 million (equivalent to RM10.7 million) in share-

based payment expenses in 2014, (c) USD5.3million (equivalent to RM17.3 million) Listing expenses in 2014, (d) USD0.3million (equivalent to RM1.1 million) of other

expenses relating to the Listing in 2014.

2 EBITDA is calculated by adding finance cost and depreciation and amortisation to profit before taxation.

• As a result of the foregoing, EBITDA margin improved to 41.2% from 39.4% YoY, and registered a CAGR of

18.5% and 30.0% in USD and RM terms respectively between 2011 and 2015

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

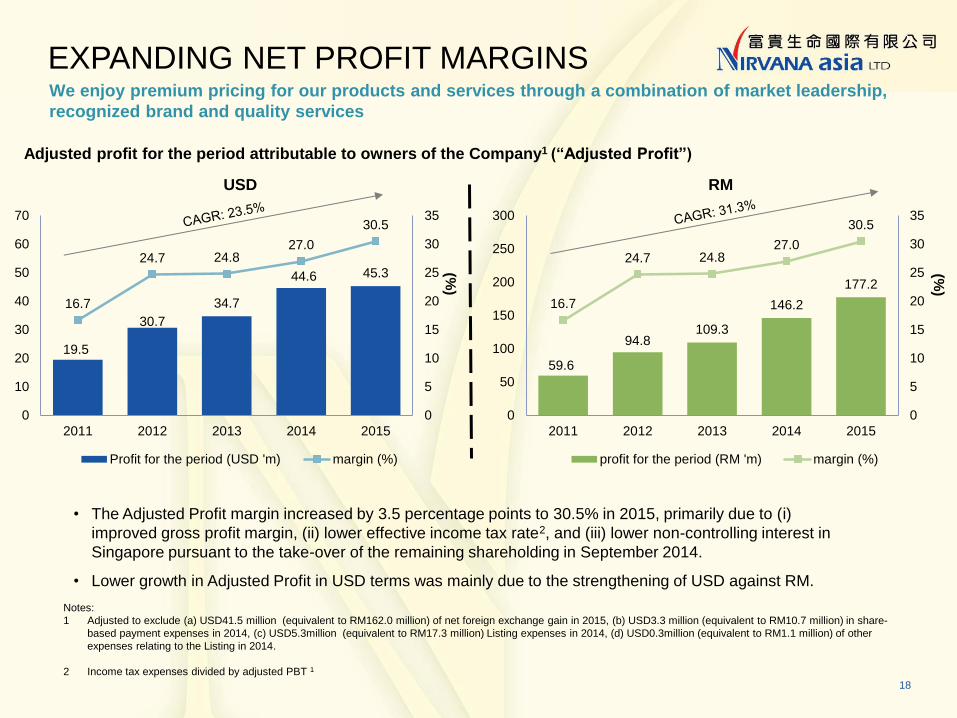

19.5

30.7

34.7

44.6 45.3

16.7

24.7 24.8 27.0

30.5

0

5

10

15

20

25

30

35

0

10

20

30

40

50

60

70

2011 2012 2013 2014 2015

Profit for the period (USD 'm) margin (%)

EXPANDING NET PROFIT MARGINS

18

Adjusted profit for the period attributable to owners of the Company1 (“Adjusted Profit”)

Notes:

1 Adjusted to exclude (a) USD41.5 million (equivalent to RM162.0 million) of net foreign exchange gain in 2015, (b) USD3.3 million (equivalent to RM10.7 million) in share-

based payment expenses in 2014, (c) USD5.3million (equivalent to RM17.3 million) Listing expenses in 2014, (d) USD0.3million (equivalent to RM1.1 million) of other

expenses relating to the Listing in 2014.

2 Income tax expenses divided by adjusted PBT 1

We enjoy premium pricing for our products and services through a combination of market leadership,

recognized brand and quality services

(%)

59.6

94.8 109.3

146.2

177.2

16.7

24.7 24.8 27.0

30.5

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

2011 2012 2013 2014 2015

profit for the period (RM 'm) margin (%)

(%)

• The Adjusted Profit margin increased by 3.5 percentage points to 30.5% in 2015, primarily due to (i)

improved gross profit margin, (ii) lower effective income tax rate2, and (iii) lower non-controlling interest in

Singapore pursuant to the take-over of the remaining shareholding in September 2014.

• Lower growth in Adjusted Profit in USD terms was mainly due to the strengthening of USD against RM.

USD RM

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

PRUDENT CASH FLOW MANAGEMENT AND

SOLID FINANCIAL PROFILE

Net cash from operating activities

Solid cash flow generation & a strong balance sheet provides flexibility for debt financing in the future

Gearing ratio1 Net cash/(debt)2

Notes:

1 Gearing Ratio = Net Debt/Total Equity

2 Net Debt = Total bank borrowings – Bank Balances and Cash and cash equivalents

27.2

37.6 37.8

21.1

-5.4 (10)

(5)

0

5

10

15

20

25

30

35

40

2011 2012 2013 2014 2015

(US

D 'm

)

177.5

31.1

5.9

0

40

80

120

160

200

2011 2012 2013 2014 2015

(%)

NIL NIL

-22.2 -10.6 -3.4

214.8

183.6

(50)

0

50

100

150

200

250

2011 2012 2013 2014 2015

(US

D 'm

)

In 2015, higher net cash used in

operating activities was primarily

attributable to payment for land

acquisitions and premium in relation to

increase in built-up capacity in

Singapore totalling USD28.5 million.

As at December 31, 2015, excluding

the restricted cash amount of USD5.6

million held under the pre-need funeral

service contract and maintenance

service contract’s trust account, the

Group had total fixed deposits, bank

balances and cash, and financial

instruments classified under financial

assets through P&L of USD235.0

million and a bank borrowing of

USD46.0 million.

Net cash decreased from 2014 to

2015 primarily due to the payment for

land acquisition and premium in

relation to increase in built-up

capacity in Singapore.

19

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

WORKING CAPITAL OVERVIEW

Trade receivables turnover days1 Trade payables turnover days2

Notes:

1 Trade receivables turnover days are calculated by dividing the arithmetic mean of the opening and ending balance of trade receivables for the period by revenue in that period

and then multiplying by the number of days within the period.

2 Trade payables turnover days are calculated by dividing the arithmetic mean of the opening and ending balance of trade payables for the period by cost of sales and services in

that period and then multiplying by the number of days within the period.

96 106

116

133

159

0

20

40

60

80

100

120

140

160

180

2011 2012 2013 2014 2015

65

80 91

116

162

0

20

40

60

80

100

120

140

160

180

2011 2012 2013 2014 2015

The increase was primarily due to an increasing number

of clients electing for longer installment payment periods.

To manage the increasing trade receivables, the

Company has further incentivized sales agents to

promote shorter installment periods to customers.

As a result of installment payment, revenue is discounted

at an effective interest rate ranging 6.8% to 13.5% (2014:

8.5%) per annum.

The increase was in line with the increase in trade

receivables turnover period as payment to certain land

owners of cemeteries in Malaysia were made after the

Group collected payments from customers.

20

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

In addition to strengthening our market leadership in home

markets, we are also actively pursuing expansion

opportunities in China, Vietnam, Thailand and Indonesia.

DEVELOPMENT UPDATE

21

In November 2015, the Group entered into a JV

agreement with Klang Kwong Tung Association to

develop a columbarium cum funeral homes in Klang

city centre.

This project is targeted to commence sale in the

second half of 2016.

Klang

P. 153, 154, 177

Existing cemeteries and columbarium facilities

In May 2015, the approved

capacity of our columbarium has

increased from 11,000 sq.m to

43,000 sq.m

In January 2016, the lease

expiry date of our columbarium

was extended from August 2029

to August 2098

Singapore 2

In Febuary 2015, the Group

commenced construction of a

funeral parlour cum columbarium

complex

Approximately 100,000 double

niches equivalent

Sales commenced in April 2015

Estimated completion by end of

2017.

Nirvana Center Kuala Lumpur

Malaysia 1

c

a

1

2

Future new site

In October 2015, the Group acquired approximately

66.8 hectares of land, adding the total land banks

owned by the Group in the same district to 100

hectares.

We target to commence sale in the second half of

2016.

Kuala Selangor b

Sites under development

In March 2015, the Group acquired the downstream

business of tomb design and construction from its tomb

contractor.

Others d

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

Indonesia

DEVELOPMENT UPDATE

22

In November 2015, we commenced sales of

Huizhou’s cemetery product and services via

our sales office in Hong Kong

Hui Zhou, China/ Hong Kong

In July 2015, we entered into an

agreement with a local land owner to

develop a parcel of land at Dong Nai

Province

We target to commence sales in the

first half of 2017

Total Area: approximately 40.5

hectares

Dong Nai Province, Vietnam

In May 2015, started selling burial

plots on a pre-need basis at our

cemetery near Bangkok

Acquired additional lands measuring

2.7 hectares adjacent to existing site

Total Area: approximately 39.4

hectares

Banbueng, Thailand

Acquired 27 hectares of land and in the process

of acquiring further 23 hectares of land and

obtaining approval to commence selling

Tangerang, Jakarta

3

6

4

5

3

a

5

P. 153, 154, 177

Note

1 Absolute numbers represent double burial plots equivalent and double niches equivalent

Existing cemeteries and columbarium facilities

Sites under development

Future new sites

4

In September 2015, our Group entered into a

conditional sale and purchase agreement to

acquire 63 parcels of lands measuring

approximately 75.2 hectares in Medan to

develop a cemetery with a local partner

Target to commence sales in 2Q of 2016

Medan b

6

Accent 5

(140,181,92)

Text

(26,83,163)

Accent 1

(26,83,163)

Accent 3

(31,73,125)

Highlight

(209,33,48)

Accent 2

(149.188.207)

Accent 4

(104,172,186)

Accent 6

(69,132,133)

OUR CEMETERIES AND COLUMBARIUM

23

As of December 31, 2015:

• The Group had approximately 3.0 million sq.m of net saleable burial land available for

sale as burial plots and available for future development (excluding cemetery land of

400,000 sq.m in Vietnam), and approximately 400,000 units of niches for sales.

• For the year under review, the Group acquired approximately 2.0 million sq.m of land for

cemetery development and has received formal approval from the relevant authority to

expand the built-up capacity of its columbarium in Singapore from 11,000 sq.m to 43,000

sq.m. As a result, Nirvana Singapore will have an unsold niches capacity of

approximately 70,000 units.

Q & A