yellowwood african attitudes feb 2015

TRANSCRIPT

© 2015 YELLOWWOOD. All rights reserved. PAGE i www.ywood.co.za

FEBRUARY 2015

African Attitudes:MarketingBeyond TheNumbers

© 2015 YELLOWWOOD. All rights reserved. PAGE ii www.ywood.co.za

Contents

Introduction

The African opportunity

Busting a few myths

about Africa

Understanding African

consumers

Part One:

Some Regional Truths

Part Two:

Understanding African

Attitudes

Part Three:

Connecting with

African Attitudes

10 Things to do differently

Conclusion

1

2

4

9

9

12

19

30

31

© 2015 YELLOWWOOD. All rights reserved. PAGE 1 www.ywood.co.za

In 2011 The Economist produced a now-famous

chart that highlighted the fact that seven of the

world’s ten fastest growing economies were in

Africa and that African economic growth had

overtaken that of Asia.1 This surprising statistic

caught the attention of almost every company in

the world, many of whom were more accustomed

to reading about Africa’s humanitarian crises

than its economic opportunity. In the years

since, the “Africa Rising” narrative has become

commonplace – a meme that is expounded on at

conferences and in articles across the web.

Africa is rising, and while there has been some

controversy of late2 regarding the reliability of particular

GDP statistics and growth rates, the rankings aren’t

really the point. There is no denying that African

economies have been booming for a good few years

now, albeit in many instances off relatively low bases.

Africa is more politically stable than ever before,

African middle classes are swelling, and its consumer

industries are stretching their legs. We’re witnessing

the growth of African entrepreneurialism and

innovation, of increasingly regional and multinational

African brands and businesses as well as the parallel

increasing interest from global brands hoping to

participate in this land of new opportunity.

Introduction

FEBRUARY 2015

African Attitudes:MarketingBeyond TheNumbers

Source: Accenture: The Dynamic African Consumer Market

1990

Eastern Hub Southern Hub Western/Central Hub

0

400

200

600

800

100

500

300

700

900

1,000 1990 - 2000

$ B

illio

ns

3.2% CAGR

3.9% CAGR

4.3% CAGR

Figure: Sub-Saharan African Consumer Expenditure* ($ Billions)

Historic / Forecast - US$ mn - Constant 2010 Prices - Fixed 2010 Exchange Rates*

Source: Euromonitor 2011

2001 - 2010 2011 - 2020

20061998 20141994 20102002 20181992 20082000 20161996 20122004 2020

1“Africa’s Impressive Growth” Daily Chart (January 6th 2011), The Economist. Available:

http://www.economist.com/blogs/dailychart/2011/01/daily_chart2Jerven, M. (2014) “Why saying seven out of the ten fastest growing economies are in

Africa carries no real meaning”, African Arguments. Available: http://africanarguments.org/2014/08/26/why-saying-seven-out-of-ten-fastest-growing-economies-are-in-africa-carries-no-real-meaning-by-morten-jerven/

© 2015 YELLOWWOOD. All rights reserved. PAGE 2 www.ywood.co.za

You would imagine that many of the things said about the opportunities in Africa are obvious to those with an interest in or home on the continent, but sadly many of us seem blind to the business and marketing opportunities on our doorstep. Africa is an enormous and largely untapped market. 1.13 Billion people live in Africa – that’s about one in every six people on earth, and second only to Asia.

With rapid urbanisation and economic growth off a low base, African cities are dynamic melting pots where the traditional cultures of newly arrived residents blend with the value systems of the emerging middle and upper classes. This is spawning new sub-cultures, unleashing creative energy that is fuelling the arts and ensuring the work of researchers, strategists and futurists is never dull. Many consumers are first-time consumers, participating in the market economy

with very little baggage or old competitor brand loyalties to overcome.

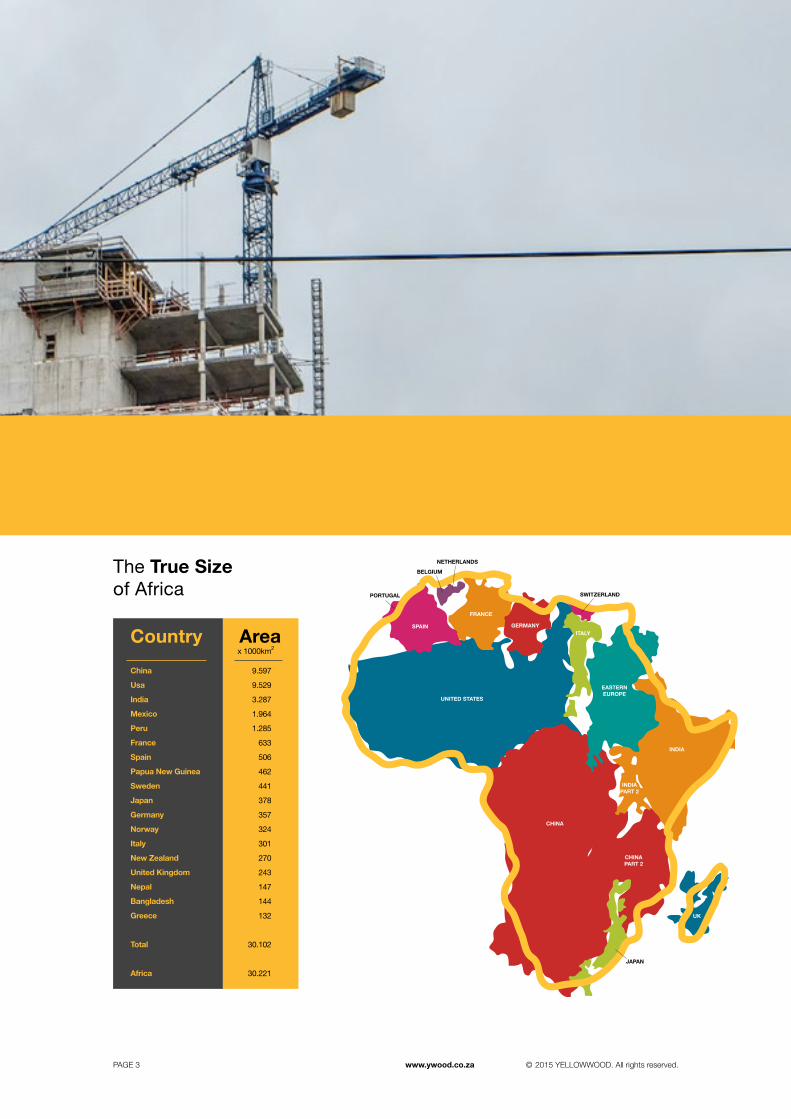

Africa is a continent of continents – both geographically and culturally. The USA, China, India and Western Europe could all fit into Africa with some space to spare. It is the most linguistically diverse continent on earth, with more than 2000 languages spoken at home and dozens spoken as official national languages.

Africa is the birthplace of humanity. It has the longest human history of any continent, and the oldest stories. It’s therefore no wonder that it is so awe-inspiringly diverse.

And yet it is so often misunderstood and portrayed in the most simplistic ways. It’s important, first and foremost, to shatter a few commonly held misconceptions about Africa.

The African opportunity

UNITED STATES

EASTERNEUROPE

INDIA

INDIAPART 2

CHINA

ITALYGERMANY

FRANCE

SPAIN

NETHERLANDS

BELGIUM

PORTUGAL SWITZERLAND

JAPAN

CHINAPART 2

UK

© 2015 YELLOWWOOD. All rights reserved. PAGE 3 www.ywood.co.za

The True Size of Africa

China

Usa

India

Mexico

Peru

France

Spain

Papua New Guinea

Sweden

Japan

Germany

Norway

Italy

New Zealand

United Kingdom

Nepal

Bangladesh

Greece

Total

Africa

9.597

9.529

3.287

1.964

1.285

633

506

462

441

378

357

324

301

270

243

147

144

132

30.102

30.221

x 1000km2Country Area

© 2015 YELLOWWOOD. All rights reserved. PAGE 4 www.ywood.co.za

Have you ever heard of ‘the European consumer’? The world has a strange habit of generalising about Africa. Research by The Guardian newspaper found that a majority of news articles mention “Africa” in general rather than any specific countries within it (with the exception of South Africa). This is unlike any other continent, where stories will feature Japan / China / India rather than Asia, for example, or Brazil / Argentina / Chile rather than South America3. This propensity to treat the whole continent of fifty-five countries as one amorphous mass is not limited to news stories. This is also true in literature and the arts, the business world and marketing.

It makes no sense. African markets are very different from one another. Aggrey Oriwo, COO of Ipsos Kenya, points out that the culture shift between Francophone and Anglophone Africa is enormous, let alone that between individual markets. A consumer in the DRC, for example, will likely be interested in elegant high fashion where Tanzanian consumers may likely want something authentically local and down to earth. What works in one market may well not work in another – whether it’s a neighbouring country or even a different city in the same country.

African consumers are as diverse and complex as consumers in any other region, and the contexts that shape them are significantly different – from expensive suburbs to sprawling megacities, to the rural, traditional, poorer areas. In fact the difference between African markets is perhaps greater than in any other continent – in terms of economic development and language and because intra-African trade is still so insignificant. Kenya’s biggest trading partners, for example, are the UK and China – not Tanzania or Uganda – and so products, tastes and ideas don’t yet travel well across Africa. Nigerian novelist Chimamanda Ngozi Adichie has commented that it was easier to get American and British fiction when growing up than it was to get other African fiction. All of that is changing now, but there remains what Oriwo calls “compartmentalised nationalism.”4 You can’t have a marketing strategy “for Africa” unless you understand the different kinds of consumer segments in each market that you’re interested in.

1. There’s no such thing as ‘the African consumer’

Busting a few myths about Africa

3Kayser-Bril, N. (2014) “Africa is not a country” The Guardian

Online. Available: http://www.theguardian.com/world/2014/jan/24/africa-clinton4Interview with Aggrey Oriwo, January 2015

Africa Generica: works of African fiction get shockingly stereotypical treatments

© 2015 YELLOWWOOD. All rights reserved. PAGE 5 www.ywood.co.za

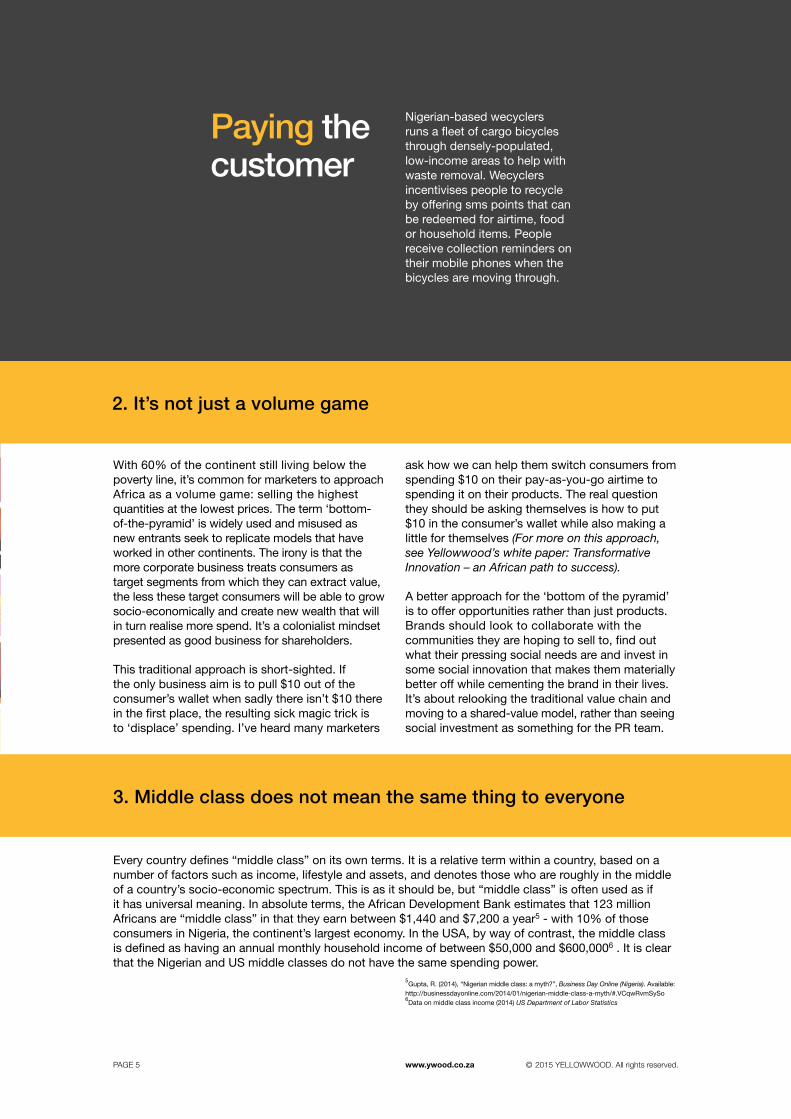

With 60% of the continent still living below the poverty line, it’s common for marketers to approach Africa as a volume game: selling the highest quantities at the lowest prices. The term ‘bottom-of-the-pyramid’ is widely used and misused as new entrants seek to replicate models that have worked in other continents. The irony is that the more corporate business treats consumers as target segments from which they can extract value, the less these target consumers will be able to grow socio-economically and create new wealth that will in turn realise more spend. It’s a colonialist mindset presented as good business for shareholders.

This traditional approach is short-sighted. If the only business aim is to pull $10 out of the consumer’s wallet when sadly there isn’t $10 there in the first place, the resulting sick magic trick is to ‘displace’ spending. I’ve heard many marketers

Nigerian-based wecyclers runs a fleet of cargo bicycles through densely-populated, low-income areas to help with waste removal. Wecyclers incentivises people to recycle by offering sms points that can be redeemed for airtime, food or household items. People receive collection reminders on their mobile phones when the bicycles are moving through.

2. It’s not just a volume game

Paying thecustomer

ask how we can help them switch consumers from spending $10 on their pay-as-you-go airtime to spending it on their products. The real question they should be asking themselves is how to put $10 in the consumer’s wallet while also making a little for themselves (For more on this approach, see Yellowwood’s white paper: Transformative Innovation – an African path to success).

A better approach for the ‘bottom of the pyramid’ is to offer opportunities rather than just products. Brands should look to collaborate with the communities they are hoping to sell to, find out what their pressing social needs are and invest in some social innovation that makes them materially better off while cementing the brand in their lives. It’s about relooking the traditional value chain and moving to a shared-value model, rather than seeing social investment as something for the PR team.

Every country defines “middle class” on its own terms. It is a relative term within a country, based on a number of factors such as income, lifestyle and assets, and denotes those who are roughly in the middle of a country’s socio-economic spectrum. This is as it should be, but “middle class” is often used as if it has universal meaning. In absolute terms, the African Development Bank estimates that 123 million Africans are “middle class” in that they earn between $1,440 and $7,200 a year5 - with 10% of those consumers in Nigeria, the continent’s largest economy. In the USA, by way of contrast, the middle class is defined as having an annual monthly household income of between $50,000 and $600,0006 . It is clear that the Nigerian and US middle classes do not have the same spending power.

3. Middle class does not mean the same thing to everyone

5Gupta, R. (2014), “Nigerian middle class: a myth?”, Business Day Online (Nigeria). Available:

http://businessdayonline.com/2014/01/nigerian-middle-class-a-myth/#.VCqwRvmSySo6Data on middle class income (2014) US Department of Labor Statistics

© 2015 YELLOWWOOD. All rights reserved. PAGE 6 www.ywood.co.za

It is a shallow and tired generalisation to think that the emerging middle classes across Africa are only motivated by status. It is common for newly wealthy consumers around the world to enjoy flashing their wealth to indicate that they have made it and differentiate themselves from the kinds of people that they used to be. There certainly is plenty of that going on in Africa too, but our work on the continent has revealed that

4. New money’s not all bling

there is a community-mindedness in Africa that persists even amongst the newly middle class. They don’t just want to look good; they want to contribute to the success of their community, family, village and even country. The opportunity is there for brands to help accelerate Africa’s upward mobility not through materialism, but through purpose.

Brands that enter Africa with products and services geared for a Western “middle class” will struggle to find scale or relevance. Simply producing cheaper, lower quality versions won’t win over many of the continent’s aspirational consumers either. There is no short-cut. Portfolios, marketing, business models and processes need to be designed with African realities in mind from the start.

$2 trillion

0.54 billion

North AmericaNorth America

Africa

Africa

$20.3 trillion

1.2 billion

Median Age: 18.6 Median Age: 29.8

People GDP

Source:UN Statistics Division, Wolfram-Alpha

Source:IMF Data Mapper, 2014

© 2015 YELLOWWOOD. All rights reserved. PAGE 7 www.ywood.co.za

Although perhaps only the first part of the quote is true in this case, it’s important to remember David Ogilvy’s famous words that “the consumer is not a moron. She is your wife.” There has been an unspoken assumption made in the past that because African markets are underdeveloped, consumers can be treated like fools. Joe Njeru, CEO of Nairobi-based digital marketing agency Zilojo believes that one of the most common mistakes global brands make when entering Africa is “to believe that the customer is dumb. We have a sophisticated market and audience but often advertising is dumbed down. It needn’t be.”7 McKinsey says that “despite the predominance of informal retail across the continent, urban African consumers have modern, sophisticated tastes and in many ways are no different from urban consumers elsewhere.”8

5. The Consumer isn’t ignorant

Entering African markets with an air of superiority is bound to end in failure. No one likes to feel disrespected and, in a continent with a recent colonial past, it is particularly enraging. Marketers hoping to make it in any of Africa’s opportunity markets need to learn to take their cues from the consumers in those countries: listen to the people on the ground and act on their suggestions and advice. Confront and question any preconceptions or prejudices that you may hold, even subconsciously, and ensure you treat the customer with the utmost respect. Most Africans are warm, engaging and welcoming if you approach them as equals not targets for your products and services.

Many businesses look to expand in Africa by taking their existing products, models and marketing and seeing how they can bend and twist it to fit African market conditions. Make once, sell many times is a production-based marketing mindset which is losing relevance in developed economies. First World consumers are looking for customisation and personalisation and consumers in Africa are looking for products and services that meet their real needs and are relevant to their culture and context. No one is interested in barely-localised generic products, even when dressed up as this year’s fashion.

Consumers across most African markets increasingly have choices as to which brands to buy and the era of being successful just because you are there is over. Marketers need to start with the African consumer and work backwards to the products, services and marketing to develop. It’s important to understand the unique context, points of view and needs of African consumers.

Only brands that understand African attitudes and archetypes will survive.

An inside-out approach

It’s not easy

7Interview with Joe Njeru in Mozambique, October 2014

8Hattingh, D., Russo, B., Sun-Basorun, A. & Van Wamelen, A. (2012) The Rise of the African

Consumer, McKinsey & Company

Carol Abade says that “people often think you can just waltz right in and wow people.” You can’t. Succeeding in Africa isn’t easy. It takes hard work and perseverance.

Infrastructure challenges are very real, and add costs to everything from distribution to telecommunications. Although it is rapidly in decline, there is still corruption in many markets.

There are cultural and linguistic barriers between every market, and particularly between the Anglophone / Francophone blocs. Marketing budgets are not as big and consumers have less to spend. Marketers who bring in products, services and campaigns from other parts of the world will struggle to really grasp the African context and consumers. It’s better to start from the inside.

PAGE 8 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved.

Only brands that understand African attitudes and archetypes will survive.

Me

Africa

income

Ex Africa

Me Me

© 2015 YELLOWWOOD. All rights reserved. PAGE 9 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved. PAGE 9 www.ywood.co.za

Understanding African consumers

While generalisations are never completely accurate and Africa, in particular, is hugely diverse, there are a few human truths, needs and contexts that are common to many African consumers and that marketers should be aware of if they hope to create products, services and marketing that are relevant.

Community-mindedness is ingrained in most African cultures and important to most African consumers. The philosophy of Ubuntu states that we are only people because of other people (in isiZulu, umuntu ngumuntu ngabantu), and that compassion and care for others is what makes us whole. This philosophy is common in many other African countries besides South Africa – known as unhu in Zimbabwe and uMunthu in Malawi.

African people often live close to their families, maintain close bonds with extended family and often use their income to support others. Middle class consumers are less financially secure than they would be in other regions due to the support they provide to family. The importance of social structures and sociability can be seen in a number of industries and innovations. For instance, collective informal saving schemes are common on the continent. Called stokvels in South Africa, these schemes work by groups of people pooling their savings together and paying out to each member once a year.

The trust that many Africans feel for their community can be seen in the power of word-of-mouth marketing. McKinsey has found that word of mouth “plays a more central role in the decision journeys of emerging-market consumers than for those in developed markets.”9 In particular, 92% of Egyptians and 49% of Nigerians receive brand recommendations from friends and family before purchasing, compared to just 29% in the

UK. According to a 2007 global study by Millward Brown, 80% of South Africans spread brand stories to friends and family – the highest score of any country.10

While in other continents people have moved from community-mindedness to individualism as income and wealth increase, we believe that in Africa the two are inseparable and that even as priorities shift to the individual, one is still inextricably part of a community.

The strength of these communal ties varies by market, of course. As Victor Ikawa, Head of Market Research and Consumer Insights at Safaricom, told us: “In East Africa it’s becoming a bit more individualistic. In West Africa they have managed to keep sociability pretty tight.”11

Others Others Others

You cannot break a bunch of sticks

Part One: Some regional truths

9Atsmon, Y., Kuentz, J-F., Seong, J. (2012), “Building brands in emerging markets”, McKinsey

Quarterly10

Van Loggerenberg, M. & Herbst, F. (2010), “Word-of-Mouth Marketing to a Female Emerging Market: A South African Perspective”, Journal of Digital Marketing.11

Interview with Victor Ikawa, September 2014, Nairobi, Kenya

© 2015 YELLOWWOOD. All rights reserved. PAGE 10 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved. PAGE 10 www.ywood.co.za

Religion plays an important role in many African societies and is a priority in many consumers’ lives. From traditional African beliefs, to Christianity and Islam in the north, marketers need to understand how influential religion is and how prominent it is in consumers’ social lives and priorities. Unlike the increasingly secular West, most Africans are religious and this shows no sign of reversing. Charismatic mega-churches with celebrity pastors are on the rise across the continent, for example. Places of worship are often central to how and where people socialise - it is not uncommon, for example, for families to spend the whole day at Church on Sundays.

The prominence of religion and religious values influences marketing in these markets and results in many African consumers being conservative and traditional and mistrusting of brands that encourage a decadent, flashy or “Western” lifestyle. It’s surprising for most outsiders to learn that a majority of Africans do not drink alcohol, for instance.12

Religiosity is not restricted to poor and rural consumers either, as many middle class consumers maintain strong religious ties without necessarily being resistant to upward mobility and social change. Kelechi Nwosu, MD of TBWA Concept in Nigeria, says that Nigerians “like to be seen as pious and in accordance with God, even if behaviour does not always match that.”13

The influence of faith is increasingly felt in branding and social media. In 2011, for example, Pastor Oyakhilome of Christ Embassy launched Yookos (You Own Your Kosmos) - a Nigerian social networking site. It now has over 10 million ‘believers’ on it, and they use it to “share prayer points and fellowship with other Christians in over 160 countries worldwide”.14 The CEO of Keroche Breweries in Kenya ends her note on their corporate website with “God bless you all and this nation.”

Many developed markets are grappling with an aging population and shifting their product and service offerings to cater to wealthy and retiring baby boomers. Africa, on the other hand, is a continent of young people. The youth are such an enormous and important bulge in the population that it doesn’t really make sense to talk of a “youth market” segment: the market is the youth. The median age across Africa is 19 years; in the US it’s 37 and in Europe it is 40.15 When up to 70% of the market is under the age of 25, it makes keeping up with what’s cool very difficult

Financial strain is a reality for most African people. A decade of solid economic growth has not eradicated poverty and a number of pressing social problems remain. Infrastructure is poor in most of the continent, making starting and running a business difficult and contributing to the cost of living for consumers – from corruption to the cost of distribution and mobile data.

However, because of the tangible sense of progress in many countries, most Africans are optimistic about the future. Research by McKinsey found that 84% of Africans believe their lives are going to get better in the next two years – and this figure is as high as 97% in Ghana.16

Africans believe their countries will make it and many are motivated by the idea of contributing to that success. There is widespread belief in the power of education to bring a better life, and investing in education is seen as an important thing to do.

Faith like potatoes

Youthful exuberance

Happy is hard work

In most African markets, heritage is being defined and redefined every day as people urbanise and come into contact with different technologies, tribes, languages and people. Heritage is not something found in text books or museums; it is crafted by innovators and trailblazers and the conservatives and traditionalists who fight back. Brands have the opportunity to participate in this dynamic relationship and play a part in defining local pride and culture – something that can be incredibly exciting for marketers, provided it is done with authenticity and respect.

Carol Abade, CEO of EXP, believes there is an increasing pride in local culture across Africa. “It’s not a nationalistic pride, it’s about ownership and relevance,” she says. This can be seen in the growth of the African artistic industries, for example. A decade ago, radio stations would have primarily played Western music. Now, people are listening to as much, if not more, Nigerian music and South African music. The lyrics and style are relevant and are finding an audience in clubs, radio stations and homes. Nollywood, Nigeria’s film industry, produces twice as many movies as Hollywood every year.

Heritage in the making

for marketers. And it means many channels, tastes and technologies will leapfrog into African markets with local twists and none of the slower, older versions that dominate elsewhere.

PAGE 11 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved. PAGE 11 www.ywood.co.za

Africa finds itself in an interesting position given our time in history. Citizens of relatively new democracies are entering the working world at a time when information and knowledge on ‘how not to do things’ abounds and is freely available on the internet. Tools and techniques are there on the shelf and are available for appropriate application, not formulaic replication.

Borrow then buildThis is being borne out in brand choices across the continent. Research by Mckinsey confirmed that most Sub-Saharan Africans prefer local to international brands (whereas 60% of North Africans prefer international brands).17 This puts brands from other parts of Africa in an interesting position where some are regarded as local and trusted and others are seen as foreign and neo-colonialist. It is risky to believe that the political rhetoric of pan-Africanism applies to consumer tastes; many African consumers feel no particular affinity for Nigerian or South African products, for example, and brands from these markets would need to invest as much time and energy localising as brands from elsewhere.

Keroche Breweries is a 100% locally owned beer and spirits manufacturer in Kenya. They have risen to prominence on the back of a “truly Kenyan” positioning and with affordable products that are healthier and purer than the home-made brews of many low-income earners.

East African Breweries’ Tusker beer, likewise, wins consumer loyalty by tapping into rising local pride in Kenya.

Africa’s time to shine

12This figure varies enormously from country to country, but on average, 57% of Africans

are lifetime abstainers according to the World Health Organisation. Nigeria has the highest per capita drinking rate on the continent, but this is only slightly higher than the European average (12.3 litres versus 12.18 litres) – see Wilkinson, K. (2013) “Is Africa the drunk continent? How Time Magazine ignored the data”, Africa Check: Sorting Fact from Fiction, Available: http://africacheck.org/reports/is-africa-the-drunk-continent-how-time-ignored-the-data

13Interview with Kelechi Nwosu, October 2014

14“Ten African Trends for 2015”, Trendwatching.com

15Population Age Demographic Figures, Africa vs. USA & Europe, WolframAlpha.

16Hattingh, D., Russo, B., Sun-Basorun, A. & Van Wamelen, A. (2012) The Rise of the

African Consumer, McKinsey & Company17

Hattingh, D., Russo, B., Sun-Basorun, A. & Van Wamelen, A. (2012) The Rise of the African Consumer, McKinsey & Company

18Feist, J. & Feist, G.J. (2009), Theories of Personality, New York, McGraw-Hill

© 2015 YELLOWWOOD. All rights reserved. PAGE 12 www.ywood.co.za

In our pan-African segmentation and market clustering projects that we have completed over the past few years, we have identified more than 50 consumer segments across the continent. While each is

Based on the work of Freud and Jung, archetypes are universal, not regional. They are the unconscious behaviours and roles that humans have evolved as the “psychic counterpart to instinct”.18

We all instantly recognise and relate to the ‘mother’ archetype, for example, regardless of time, place or culture. And we all shift into various different archetypal roles and needs in different contexts, though we generally have a primary type that feels most natural and is our default setting in the world.

Archetypes are translated into reality through individual and cultural characteristics and different contexts will result in different kinds of behaviour. Our work on the continent has revealed that there are a few key attitudinal segments that are common in African markets, though their particular expression will be localised.

We believe the two key axes that define how attitudes segment in most African markets are a person’s relationship with change – whether they seek improvement and excitement or security and stability – and the relative focus they give to themselves and their community.

Towards African archetypal consumers:

Part Two: Understanding African Attitudes

unique in that they are dependent on the culture, history, language and specific context of that market, a number of common themes started to emerge – attitudes that unite a number of segments across Africa.

My Community

Me

GO GETTER

INV

EN

TO

R

BO

SS

SURVIVOR

OPTIMIST

ME

NTO

R

TRADITIONALIST

CA

RE

GIV

ER

© 2015 YELLOWWOOD. All rights reserved. PAGE 13 www.ywood.co.za

The UPLIFTERS

The AGITATORS

The ACCUMULATORS

The STABILISERS

PAGE 14 © 2015 YELLOWWOOD. All rights reserved. www.ywood.co.za

Survivors TraditionalistsLife is still very hard for many, many people in Africa. The majority of people can’t afford to pay much attention to the esoteric world of brands and marketing. Whether subsisting off the land or living in slums, they are concerned with how to make it to the end of the month, and how to get by day to day. Survivors struggle for the mere basics and are anxious about safety, job security and being able to look after themselves. They take comfort in small things such as their friends and they are not overly concerned with being fashionable.

Survivors typically fall into two camps: those who focus on today and make the best of what they have; and those who have become frustrated and despondent. They can’t join the middle classes or achieve their dreams because of a lack of opportunities, a lack of education and having to support extended families with meagre earnings.

The rapid changes to African society in recent decades have not been universally well received. Traditionalists are sceptical of outside influences and dislike the arrogance of Western and foreign brands. They are proud of local culture and customs, whether these be national, tribal or religious.

Traditionalists would like to preserve the way things have always been done and take comfort in the stability of knowing the rules. They are sociable, value their community and are likely to be religious. They are often closed to new experiences but will engage with brands that respect their culture and offer clear benefits to their life, rather than those that position themselves as ‘cool’ – they are not interested in keeping up with trends.

Kelechi Nwosu comments that “the darker side of [Africa’s] diversity is tribalism.” He believes the best approach for brands to take is to “recognise diversity but seek opportunities to create unity out of this diversity, to find the common ground.”

Segment size: Large

Demographic epicentre: 20 - 40 lower income

Segment size: Large

Demographic epicentre: 35 + lower income

Key needs: Security, control, assurance, escapism, having enough to survive.

Key needs: Belonging, good value, local relevance, cultural respect, stability, familiarity.

How to win: Affordable, durable, more for less. “Help me survive.”

How to win: Functional, affordable, relatable. “Help my community out.”

Key attitudes: Resilient, no-nonsense, resourceful, tenacious, focused on today. Life is hard.

Key attitudes: Conservative, responsible, modest, cautious, West is not best.

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.zaPAGE 15

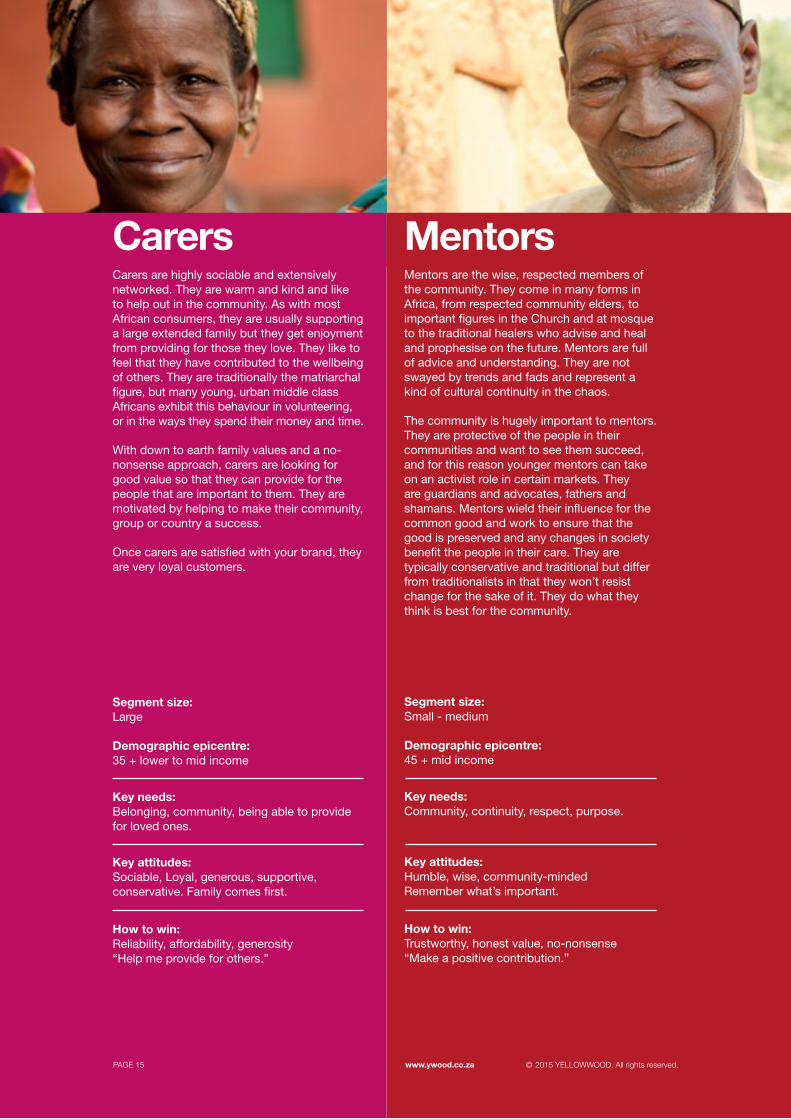

Carers MentorsCarers are highly sociable and extensively networked. They are warm and kind and like to help out in the community. As with most African consumers, they are usually supporting a large extended family but they get enjoyment from providing for those they love. They like to feel that they have contributed to the wellbeing of others. They are traditionally the matriarchal figure, but many young, urban middle class Africans exhibit this behaviour in volunteering, or in the ways they spend their money and time.

With down to earth family values and a no-nonsense approach, carers are looking for good value so that they can provide for the people that are important to them. They are motivated by helping to make their community, group or country a success.

Once carers are satisfied with your brand, they are very loyal customers.

Mentors are the wise, respected members of the community. They come in many forms in Africa, from respected community elders, to important figures in the Church and at mosque to the traditional healers who advise and heal and prophesise on the future. Mentors are full of advice and understanding. They are not swayed by trends and fads and represent a kind of cultural continuity in the chaos.

The community is hugely important to mentors. They are protective of the people in their communities and want to see them succeed, and for this reason younger mentors can take on an activist role in certain markets. They are guardians and advocates, fathers and shamans. Mentors wield their influence for the common good and work to ensure that the good is preserved and any changes in society benefit the people in their care. They are typically conservative and traditional but differ from traditionalists in that they won’t resist change for the sake of it. They do what they think is best for the community.

Segment size: Large

Demographic epicentre: 35 + lower to mid income

Segment size: Small - medium

Demographic epicentre: 45 + mid income

Key needs: Belonging, community, being able to provide for loved ones.

Key needs: Community, continuity, respect, purpose.

How to win: Reliability, affordability, generosity “Help me provide for others.”

How to win: Trustworthy, honest value, no-nonsense “Make a positive contribution.”

Key attitudes: Sociable, Loyal, generous, supportive, conservative. Family comes first.

Key attitudes: Humble, wise, community-minded Remember what’s important.

PAGE 16 © 2015 YELLOWWOOD. All rights reserved. www.ywood.co.za

The jesters, jokers, dancers and lovers of life. Africa is an optimistic and often celebratory continent. Many Africans are quick to express joy and laugh. They believe that life is improving and that there is nowhere else they would rather be.

Whether it’s a Ghanaian taxi driver telling his passenger how Ghana is the best country in the world or a Kenyan teacher who believes that her class will grow up to be great leaders, optimists are proud of where they come from and believe in themselves and their community. They are outgoing and sociable and always looking for a reason to celebrate.

Optimists will connect with brands that give them a reason to smile. They love to see their community succeed. Brands hoping to win over the optimists should celebrate the sports, music, passions and activities that they love and make them feel special for their achievements in life. Osibo Imhoitsihe, Business Director of TBWA\Concept in Lagos says of Nigerians in particular “we are very happy people. Positivity and humour are key to communications for Nigerians.”

These young, energetic and confident consumers are on the way up. Not all of them have much money yet, but they like to feel recognised for their potential as much as for what they’ve achieved . They are in touch with what’s going on in the rest of the world and appreciate international brands, but they are also very proud of Africa’s place in the world and resonate with brands that pioneer new and modern ways to be African. They have access to information and trends through technology and spend a lot of time on their phones. They are the drivers of youth culture, with tastes that are constantly evolving. Whether it’s the music they listen to, the celebrities they want to meet or the brands they buy, it’s hard to keep up with these consumers and marketers need on-going research and on-the-ground immersion to stay relevant.

Go-getters are ambitious but they are also sociable and fun-loving. They go out often to parties, enjoy new experiences and spending time with friends.

To win with go-getter customers, tap into their ambitions and aspirations and get customer service right. New entrants to categories won’t remain new entrants, and how you treat a customer today affects how they respond to your products and services tomorrow.

Segment size: Medium

Demographic epicentre: 35 + low to middle income

Segment size: Small - medium

Demographic epicentre: 20 + lower income

Key needs: Hope, conviviality, a sense of progress, enjoyment.

Key needs: Recognition, status, vitality, the latest tech, progress.

How to win: Affordable, simple, joyful. “Help me enjoy my life.”

How to win: Aspirational, fun, affordable, trendy and cool. “Help me look good and achieve my goals.”

Key attitudes: Sociable, optimistic, spirited, positive, humorous. Always look on the bright side.

Key attitudes: Hard-working, ambitious, determined, fun-loving, energetic. I will make a success of my life.

Optimists Go-Getters

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.zaPAGE 17

Necessity is the mother of invention, as the saying goes, and so Africa is buzzing with inventors - from the tech entrepreneurs in Kenya’s “Silicon Savannah” to street traders who pioneer new distribution models for Nollywood DVDs and Coca-Cola to the artists who make and sell wire and wood creations by the side of the road.

Inventors are the artists and creative spirits of Africa. They have an indomitable energy and determination to get things done. They thrive on the hustle and bustle and chaos of Africa, turning their restlessness into creations and spotting opportunities in the gaps.

Though this resourceful creativity is alive and well in the consumer societies of African markets, the marketing industry often fails to keep up. Joe Njeru, CEO of Zilojo in Kenya, says that marketing’s biggest challenge in Africa is that “nobody wants to be adventurous. Everyone wants to do something safe.”

From the traditional “Big Men” of Africa and the captains of industry to the middle-income and not-yet-at-the-top, bosses have an attitude of power and privilege. They have stable incomes and are no longer financially insecure. Their attention is focused on themselves and their immediate family, but they are often influential in their field and respected in their circles of friends and their community. They expect to be recognised for their success.

Younger bosses are typically looking to reach the top, where older bosses are looking for a relaxed life, free from tension and stress. Many wealthier bosses have travelled to other countries and know, first hand, what to expect from quality brands. They won’t fall for fake status or accept inferior service from global brands operating in Africa. They appreciate the finer things in life and are opinion-leaders and influencers in premium categories.

Their faith is important to them and they are often high-profile figures in their churches or mosques.

Segment size: Medium

Demographic epicentre: 20 - 30 mid income

Segment size: Small

Demographic epicentre: 25 - 40 mid to high income

Key needs: Inspiration, choice, innovation, opportunity.

Key needs: Power, respect, influence, discernment.

How to win: Useful, generous, creative, passionate, new. “Help me create something new.”

How to win: Quality, attention to detail, luxury. “Reward me.”

Key attitudes: Resourceful, energetic, creative, indomitable.There’s always a way to make it happen.

Key attitudes: Confident, secure, informed, commanding, demanding. Only the best will do.

Inventors Bosses

PAGE 18 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved.

Businesses entering Africa may be tempted to expand regionally; starting in one market and spreading to its neighbours. Logistically, this may sound easier, but it makes little sense when African nations are at such vastly different levels of development and require different strategy and skills to market well. Two neighbouring countries may have less in common than two countries at opposite ends of the continent. Carol Abade believes “culture is at a country level. There may be some cross-over in region, but it’s not as much as people think.” McKinsey, on the other hand, advocates for targeting cities rather than countries. However you cut it, brands looking to expand in Africa should undertake a market clustering exercise so as to avoid spreading themselves too thin.

Analyse all potential African markets on their levels of economic development, infrastructure, language, culture and consumer needs. Once you have found the commonalities, group similar markets together and develop a strategy to connect with consumers in that cluster. The strategy will require some localisation in each individual market, but the similarity in context for the cluster will mean that consumers are driven by broadly similar needs, goals and aspirations.

Understanding African markets through their people, common needs and attitudes helps with many marketing decisions. Importantly, it demonstrates that:

It’s about attitude, not proximity.

OthersMe

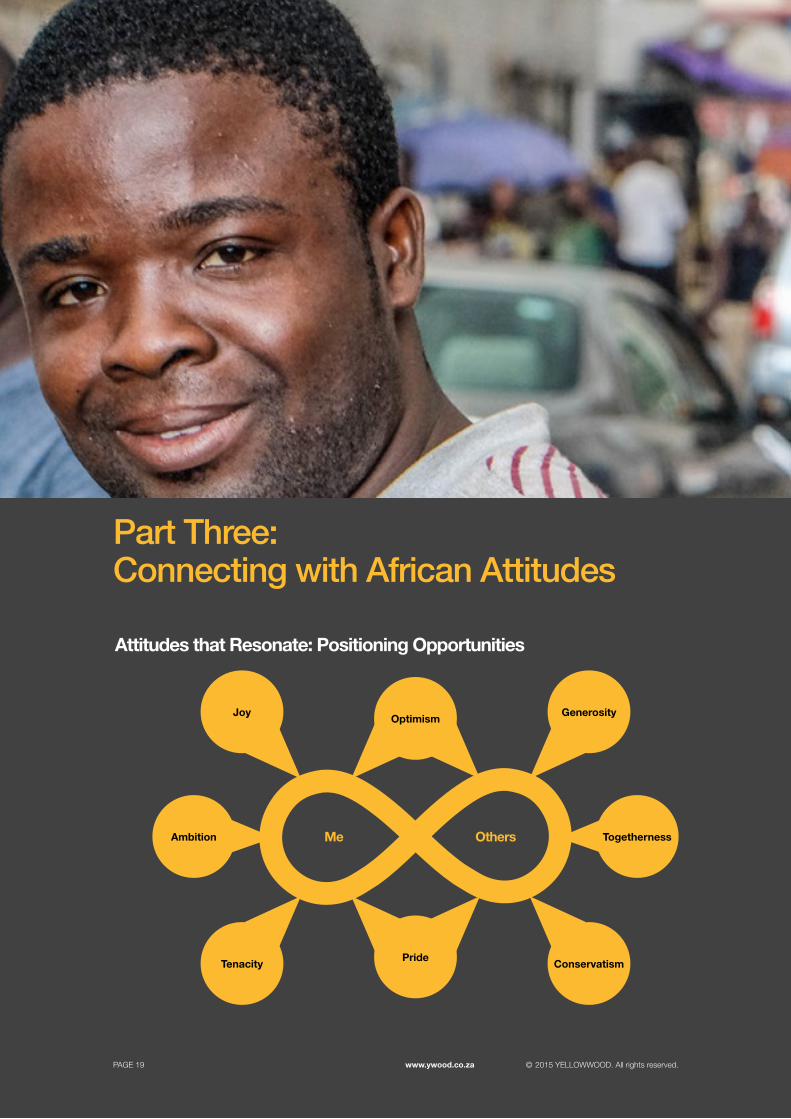

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.zaPAGE 19

Attitudes that Resonate: Positioning Opportunities

Part Three: Connecting with African Attitudes

GenerosityJoyOptimism

TogethernessAmbition

ConservatismTenacityPride

© 2015 YELLOWWOOD. All rights reserved. PAGE 20 www.ywood.co.za

Africa does not need neo-colonial marketing. It needs businesses with a generosity of spirit, that want to help ensure that the markets they operate within succeed. If marketers set themselves the primary objective of making things that customers want rather than making customers want things, they will find many opportunities in Africa and resonate with the attitudes of the locals.

Customer needs and wants in Africa are broader than the traditional category thinking of developed markets and for brands to really matter to these customers, they need to rethink the pyramid. Pay your taxes, find ways to contribute to the most pressing social ills, offer opportunities and paid collaborations to customers and transfer skills to staff on the ground.

It’s critical for marketers to build capacity at a local level. There is a shortage of skills to overcome and importing skills can only achieve half of what needs to be done. Expats cannot hope to offer the kinds of deep cultural insight that is required for relevant and effective marketing. Capacitating local offices is a good investment. It means more effective teams and a better understanding of local innovation needs.

Aliko Dangote, for example, attributes the success of his business to the simple fact that he was willing to invest rather than holding out for more stability. Many businesses in South Africa could learn from this example, as the private sector is often accused of being on an “investment strike”.

Spending money on building communities can be done in a way that embeds your brand in them. From nutrition to education to healthcare, African consumers are working towards a better place to live, and brands can play an exciting role in helping them achieve that.

Despite the growth of African middle classes in recent years, the vast majority of African consumers remain poor and price sensitive. Many consumers, from survivors to carers, are trying to stretch their meagre earnings to provide for multiple dependants and so, brands that can offer them great value (more quantity AND acceptable quality) will do well. Be careful not to try and achieve this through old-fashioned methods of cutting corners, though. “Africa is no longer a dumping ground for average brands and products” warns Carol Abade. There are too many competing producers now and local innovators will find ways of doing things more cheaply and efficiently.

Carers

On the wavelength of:

“I would like to be listed among the great, the gentlemen who made good things for this country, I dream for a better Congo”

Mentors

Survivors

1. Generosity a. Invest, don’t extract

b. Offer more for less

© 2015 YELLOWWOOD. All rights reserved. PAGE 21 www.ywood.co.za

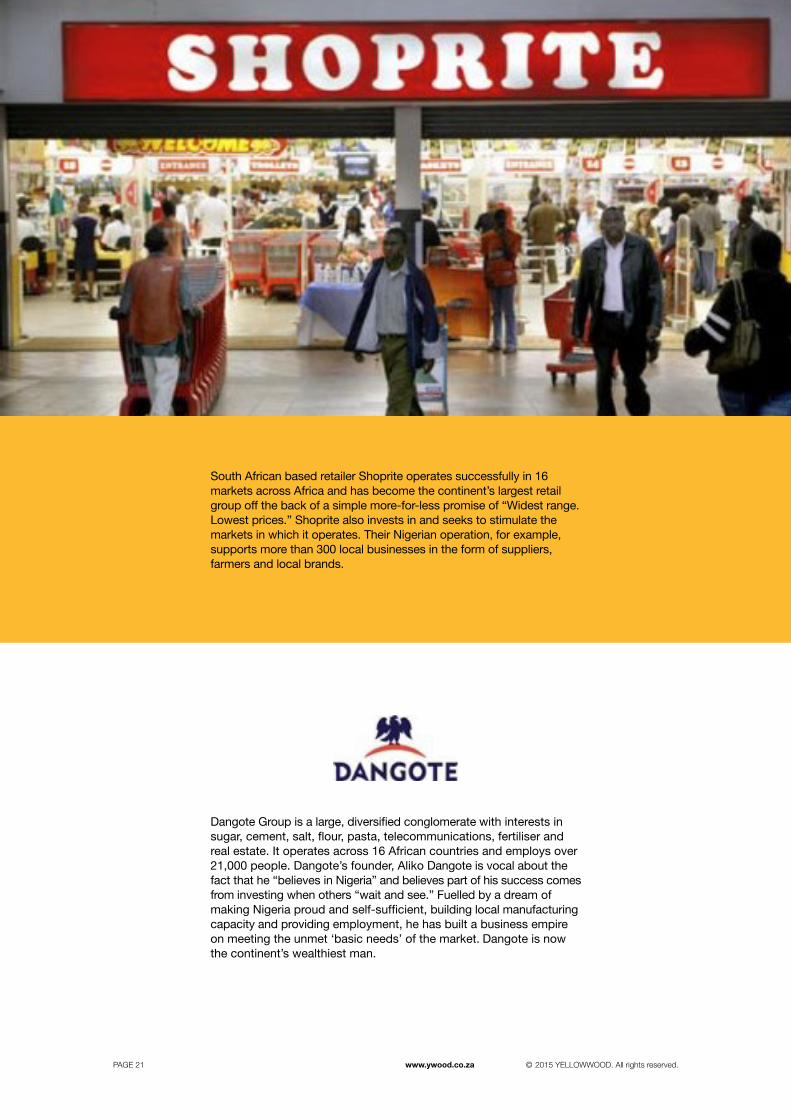

South African based retailer Shoprite operates successfully in 16 markets across Africa and has become the continent’s largest retail group off the back of a simple more-for-less promise of “Widest range. Lowest prices.” Shoprite also invests in and seeks to stimulate the markets in which it operates. Their Nigerian operation, for example, supports more than 300 local businesses in the form of suppliers, farmers and local brands.

Dangote Group is a large, diversified conglomerate with interests in sugar, cement, salt, flour, pasta, telecommunications, fertiliser and real estate. It operates across 16 African countries and employs over 21,000 people. Dangote’s founder, Aliko Dangote is vocal about the fact that he “believes in Nigeria” and believes part of his success comes from investing when others “wait and see.” Fuelled by a dream of making Nigeria proud and self-sufficient, building local manufacturing capacity and providing employment, he has built a business empire on meeting the unmet ‘basic needs’ of the market. Dangote is now the continent’s wealthiest man.

19Interview with Kelechi Nwosu, October 2014

PAGE 22 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved.

Innovation in Africa doesn’t take place in white lab coats with huge R&D budgets – it takes place in a million little experimentations driven by necessity and an understanding of what people need. For this reason, Africa is leading in convergence. Technology, telecommunication and financial services are rapidly pulling together and blurring into one another, spurred on by African innovations such as mobile money players. And many other industries will do the same.

Convergence is easy when you start with the customer – understanding the customer’s unmet needs, priorities and social context allows you to define new industries, rather than recreating what exists in other markets. Call it pre-emptive disruption. Victor Ikawa believes one of the main reasons for Safaricom’s success has been that they “ignored formal boundaries about what you can do and can’t do.”

Use intermediate technologies, leapfrog the conventions used in other markets and partner with local innovators. Ignore traditional category conventions and boundaries and focus on bringing together the right business models, products and services to meet real African needs.

Marketing and communications that bring people together have huge potential in Africa where national identity is still a work in progress. Many consumers feel excited by brands that can give them a sense of broader community, that stitch together different ethnicities, tribes and cultures. Kelechi Nwosu, MD of TBWA \ Concept in Lagos, advises brands to “seek opportunities to create unity out of the diversity. Ask yourself ‘Where is the common ground that will get me some space in the hearts of people?’”19

An enormous advantage of operating in Africa is that businesses get to define the boundaries and extent of their categories, rather than simply replicating old-fashioned conventions from the developed world. In financial services, for example, there have been huge levels of innovation because the branch infrastructure of the developed world was simply leapfrogged.

GT Bank, one of the largest financial services providers in Africa, allows consumers to open bank accounts via Facebook – tapping into the power of social media to get where physical infrastructure can’t.

Likewise, M-Pesa, Safaricom’s mobile money innovation ignores the boundaries between telecommunications and financial services. A quarter of Kenya’s economy now runs on M-Pesa.

Businesses that centre their innovation and their thinking on real customer needs won’t be victims of convergence – they will be the brands that drive it and thrive.

Carers

On the wavelength of:

Mentors

Inventors

2. Togetherness a. Embrace convergence

b. Bring people together

PAGE 23 www.ywood.co.za © 2015 YELLOWWOOD. All rights reserved.

Faiba is a high-speed fibre-optic internet service offering by Jamii Telecommunications in Kenya. Their animated TV ads, conceptualised and created by a local animator, use the mannerisms, habits, language and pronunciation of different tribes in Kenya in humorous ways. The ads went viral in Kenya and have resulted in certain phrases entering into common speech. Viewers have found them funny and are proud of the fact that the animations and talent are local.

Cultural Relevance, In-Jokes and Building Community: Faiba

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.zaPAGE 24

Often getting the marketing basics right – like getting your products to the shelf – can be difficult when infrastructure is poor. It’s important to be practical and to do your homework. Ensure you have a strategy for distribution, sourcing, product quality and pricing before any grand promises are made. Understand your constraints and know what you can’t deliver. Functional benefits may be good enough if you are the only business who can actually deliver them or if you can deliver on them in a more competitive way. Many consumers would prefer a brand that is reliable, of a decent quality and trustworthy rather than one that tries to be clever with its positioning. African consumers have suffered from poor product quality and poor customer service in the past and are willing to reward those that offer consistent reliability.

Show respect to the consumers in your market. Don’t assume you know best. Listen and respond to genuine needs and be honest if those needs are not ‘sexy’. It’s more important to add value to consumers rather than to try and force-fit the latest trend. From a business operations as well as a consumer brand point of view, there are few things as likely to put backs up as an expat attitude of superiority.

Traditionalists

On the wavelength of:

Mentors

3. Conservatism a. Walk before you run

b. Listen before you speak

Coca-Cola is one of the most successful companies in the world and is available in every country in Africa. Part of the reason for their success is their pragmatism and willingness to tailor their operations to the context of each market. In the late 1990s Coca-Cola dropped their traditional distribution model in many African markets with particularly bad infrastructure, opting to create or utilise micro-distribution businesses. Whether pushcarts, donkey carts, bicycles or being carried by hand, these distributors get Coca-Cola to the places where roads don’t go. It’s good for the community too. In fact Bill Egbe, the President of Coca Cola’s SA unit believes “Multinationals cannot operate in Africa without ensuring that the communities in which they do business benefit and have a significant stake in those businesses”

© 2015 YELLOWWOOD. All rights reserved. PAGE 25 www.ywood.co.za

West is not necessarily best. The provenance of certain brands can be advantageous if that country is already associated with positive attributes: German luxury cars, for example, or Scottish whisky. But there is nothing inherently better about being a global brand and African consumers are particularly proud of local culture and success stories.

Certain brands are doing exciting things with traditional culture; remixing it, reinventing it and celebrating it with a modern twist. Africans are proud of their heritage but heritage is not static. Collaborate with local artists, musicians and designers to create marketing that is culturally relevant and celebrates the market you are trying to enter.

One of Carol Abade’s Ten Commandments of Marketing in Africa is “Though shalt not judge. If you chose to live in Africa, don’t spend your expatriate social life moaning about the people and countries that host you.” Whatever you find strange about the market you have entered could be a source for fresh marketing ideas.

Traditionalists

On the wavelength of:

Mentors

4. Pride a. Don’t change the culture

Brands can find huge inspiration in the traditions and cultures of Africa.

South African fashion brand MaXhosa has captivated audiences both locally and internationally.

Laduma Ngxokolo, the creator and designer of MaXhosa says his inspiration came from wanting to “create a modern Xhosa-inspired knitwear collection that would be suitable for Xhosa initiates, prescribed by tradition to dress up in new dignified formal clothing for six months after initiation.”

His dream is to celebrate and preserve his culture and heritage, which he believes is dying out. Collections are named after traditional Xhosa phrases and customs. Maxhosa is available in South Africa and London.

African Cultural Renaissance: In 2014 construction began on the Zeitz Museum of Contemporary African Art in Cape Town. The museum, hollowed out of an abandoned grain silo building, will have more than 9,500 square metres of space over nine storeys. It will be the largest gallery in Africa, set to celebrate and exhibit rising contemporary artists from across the continent.

Diageo in Ghana invests in local raw material sourcing. They are increasingly “looking at alternative raw materials which are more resilient and better adapted to their local climates.” Ruut Extra is a premium beer that caters to local tastes. Instead of using barley, Ruut Extra is made from Cassava, one of Ghana’s most abundant crops and a traditional African staple.

• •• • • •••• • •••• • •• • • • ••• •• ••• ••• • ••• ••• • •••••••••••••••••••••••••••••••••••••••••••• • •••• • ••• • • ••• ••• •• ••• ••• ••••• •••••••••••••••••••••••••••••••••••••

• • • •• •• ••••• • ••• •• •• • •• •• • • •••••••••••••••••••••••••••••• • • • • •• • • • • • • •• • •••••••• • •••• •• • •• • • •• • •• ••• • •• ••• •• ••••• • • ••••••••••••••••••••••••••••••••••••••••• •• •• • ••• • • •••••••••••••••••••••••••••• • • • • • • • • • •• • •• •• •• • • • • • • • ••••• • •••• • •• ••• • • •• • ••• • • ••• ••••••••••••••••••••••••••••••••• • • • • •• • • • • • • ••• •••• ••••• •• ••• ••• • ••• • • •••• • ••••••••••••••••••••••••••••••••• • • ••• • ••• ••••• • •• ••••••••••••••••••••• •• • • • •• •• • • •• • • • • • • • • • • • • • ••••• •• ••• • ••••••••••• • ••• • • •••• ••• •••• • ••• • ••• • • •• •• • ••• ••• • •• ••• •••••••••••••••••••••••••••••••••••••••••••••••••• • • •• ••• •••• •• ••••••••••••••••••••• •• ••••• • • ••••••••••••• ••••• • •••• • ••• •••••••••••••••••• •• •••• • ••• •• • • •• •• • •••• • ••• •• • ••••• •• •• • ••• ••••••••••••••••••••••••••••••••••••••••••••••••••••• • • •• ••• ••• •••• •••• ••• • • • • • • • • • • • • • • • • • • • • • • • • • • • •••••••

• •••• •• • • •••••• •••• •• • •• •• •• • • •• •• •• ••• •• ••••••••••••••••••••••••••••••••••••••••••••••••• ••• •• •• • • •• • •••• • • ••• • ••• •• • •• • ••• •• ••••••••••••••••••••••••••••••••••••••••••••••••• ••• • •• • •••• • ••• •••• • ••• •• •• • • • • •• ••• •••••••••••••••••••••••••••••••••••••••••••• • •••• • • ••• • • •• •• • •• •• ••• • • ••• ••• • ••••••••••••••••••••••••••••••••••••••••••• • • • • •• • • • • • • ••••• •• ••• • •• ••• •• • • •• •• ••••• •• • • •••••••••••••••••••••••••••••••••••• • • • • ••••••••••

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.zaPAGE 26

The sense of optimism in many African markets is palpable. Even as oil prices drop and foreign investment is expected to slow in 2015, many African markets are utterly transformed from a few years ago and citizens are optimistic and excited about the future. Brands that can tap into the celebratory mood, give consumers something to look forward to and enable them to do more with their lives that will generate significant levels of goodwill. The narrative of Africa has shifted from aid to trade in the past decade, and this applies at an individual level as well.

Founded by Ugandan entrepreneur Ashish J. Thakkar, Mara is a multi-sector group with operations in 22 African countries. Mara Foundation is a social enterprise that supports emerging African entrerpeneurs. Mara Foundation launched mentor.mara.com, a social network and multi-lingual online portal for mentorship and entrepreneurship. It connects young African entrepreneurs with established and successful businesses and business leaders who volunteer their time and expertise to help the youngsters build something remarkable.

Optimists

On the wavelength of:

Go-Getters

5. Optimism a. Build something to believe in

© 2015 YELLOWWOOD. All rights reserved. PAGE 27 www.ywood.co.za

Don’t overthink things and hesitate for too long, or you’ll miss the opportunity. Local competition is increasing rapidly and is not to be underestimated. Local competitors have the insight, the agility and the life-or-death determination to make things work. Victor Ikawa believes “you need 80% action and 20% thinking. Move quickly, get things done. Have a simple direction and go with speed to resolve the issues that exist.” It’s good to have an iterative and experimental approach to brand marketing – see what works and adapt quickly.

With rapidly changing consumer contexts and increasing access to information, youth culture and tastes are changing all the time and are different from even three or four years ago. The kind of music and pop culture references that you’ll need to connect with young consumers evolves all the time. Brands need to adapt quickly and be bold and decisive in creating relevant marketing that resonates.

With so much restless energy in markets like Nigeria, brands need to focus their energy on helping consumers attain their aspirations. This requires market insight as not all aspirations are for bigger, better and more bling. Whether it’s access to unique experiences, a chance to meet celebrity preachers and DJs or adult education, marketing that connects with consumers’ ambition and aspiration is increasingly common across Africa.

Marketing that connects with consumer aspiration and ambition is on the increase across Africa’s alpha markets.

Guinness Nigeria’s “reach for greatness” campaign taps into Nigeria’s strongly aspirational culture by telling the story of a village boy dreaming of life in the city and his brother, a strong, proud man who has made it big. The commercial ends with his brother offering him a bus ticket to the city, saying “you know, a boy dreams, but a man does. Are you ready to drink at the table of men?”

Go-Getters

On the wavelength of:

Bosses

6. Ambition a. Be bold, decisive, quick and creative

b. Get them where they’re going

© 2015 YELLOWWOOD. All rights reserved. PAGE 28 www.ywood.co.za

To survive and thrive in the frontier markets of Africa, you’ll need a sense of humour, fun and adventure – both in the marketing that you do and in your attitude towards business. There will be huge challenges. There will be setbacks and misunderstandings and deliveries that don’t arrive. Things may well take longer than you expected and happen in very different ways. While we don’t advocate settling for mediocrity, it is important to let go a little. Lighten up and roll with the punches of Africa. Being able to laugh at your situation and yourself will keep you sane and help you understand the people of Africa better. Most African consumers have put up with much worse than you are dealing with, and they do so with their sense of humour and joy intact.

Recognising that most emoticons in the world represent white faces, Oju Africa released a series of African faces for download. The faces (“Oju” means “face” in Yoruba) cover the whole range of human emotions, with some humorous additions thrown in for good measure – such as smileys that are missing teeth, Rastas and mad love for Africa.

While it met with controversy for replicating instead of challenging the patriarchal attitude of traditional

Optimists

On the wavelength of:

Inventors

Go-Getters

7. Joy a. Lighten up

Nigerian culture, MTN’s “mama na boy” campaign was hugely popular among Nigerian consumers because it was relatable and celebratory. The ad featured an ecstatic new father rushing out to call his family in the village and tell them that the baby is a boy. The celebration and dancing that ensues proves that they could not have hoped for better news.

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.zaPAGE 29

Kenyan non-profit Ushahidi created the BRCK, a self-powered wi-fi device that is designed for African countries with irregular electricity supply. Describing itself as “rugged internet”, the BRCK runs off its own eight-hour battery during power cuts and switches between Ethernet, wi-fi and 3G or 4G networks depending on which signal is available.

Africa is a hard place. It takes guts and perseverance. Channel the tenacity of Africa’s survivors, stay in the game, and create products, services and marketing that will withstand the stark reality of the markets you operate in.

Survivors

On the wavelength of:

Bosses

WE CAN

IF

6. Tenacity Don’t give up

Innovation from Africa’s Beautiful Constraints

Constraints have a bad rap. They are, by definition, negative things that prevent us from acting as we would like to. “Don’t fence me in,” the old song says: if you want me to show what I can do, then leave me unconstrained.

You are bound to come up against many constraints when setting up shop or expanding in Africa – from power supply to distribution infrastructure to skills. Fortunately, a new book by Adam Morgan and Mark Barden of eatbigfish shows that constraints can be fertile, enabling, catalytic forces to stimulate new approaches and possibilities.

In the book they show that banning the phrase “We can’t because” forces people to respond to the question of “How” with “We can if ...” It keeps the focus on how it might be possible not whether it might be possible, generating solutions rather than more problems, and keeping the oxygen of optimism alive in the process.

We Can-If

The Can-If map turns this approach into a usable tool that identifies nine different responses to ‘we can’t because’. Working round the map encourages creative thinking and innovative solutions to seemingly intractable problems. It’s a very handy skill to have in Africa!

The Can-If approach is explored in more detail in A Beautiful Constraint: How To Transform Your Limitations Into Advantages, and Why It’s Everyone’s Business (Wiley 2015).

We think of it as ...

We fund it by ...

We introduce

a ...

We use other

people to ...

We mix together

...

We access the knowledge

of ..

We resource it by ...

We remove ... to allow

us to

We substitute

for ...

© 2015 YELLOWWOOD. All rights reserved. PAGE 30 www.ywood.co.za

10 Things to do differently

Assume nothing – only in Africa

Many things that are taken for granted in global markets are unheard of or simply not done that way in Africa. Whether it’s local customs dictating how things work, or make-do solutions that have grown up around poor infrastructure, you will need to spend time on the ground to get a feel for the context in each market.

Put away your pyramids

Africa may be the home of the pyramids, but they are a blunt marketing tool for understanding the continent. “Bottom-of-the-pyramid” economic status does not define the market. Take the opportunity to define a new way of marketing beyond the numbers that transforms the ‘pyramid’ by Including customers in the distribution chain, for example.

Re-think the impossible

Don’t import the conventions that ‘hold you back’ in your home market into Africa. Disrupt the conventions before they exist. Innovate. Springboard off social and infrastructural challenges to define new products and services that meet real needs. Nothing is impossible.

Ban the word ‘consumer’

You are marketing to people, not consumers. With a scarcity of quality insight and a propensity to generalise about Africa, it’s important to remind oneself of the real job at hand; to understand and delight people. Research for the nuances but empathy for what is common to all of us.

Create your own uniquely African story

With local pride on the rise and cultural identity changing rapidly, it’s a good time to celebrate the Africa in your brand. Play a part in building the unique stories of the markets that you’re in, rather than exporting your home market’s idea of “Africanness”. Be authentic, sensitive and respectful of local stories and avoid the stereotypes (no acacia trees and sunsets!)

Don’t rely. Defy convention

The best practices and case studies that worked in other regions will often not be relevant to your context. Don’t play it safe or follow the established methods and messages from other parts of the world. Think African solutions to African problems. The market is being created not replicated – let go of the conventions.

Never underestimate the power of local knowledge

No two African markets are the same. You may have better infrastructure and skills in your home market, but that doesn’t mean you know better. Did you know, for example, that open-plan living is unpopular in Nigeria because preparing Nigerian cuisine is hard, sweaty work and people prefer their guests not to see it?

Tastes, habits and cultural practices are local not pan-African. Be sure you have local people on your teams that are plugged in and vocal.

Relate, relate, relate

The differences between markets in Africa may be staggering and so finding the nugget of human insight that helps you relate to and identify with the people there is both difficult and is crucial. This to ensure your communications are authentic and your product and service offering is relevant.

Tips for Foreign entrants Tips for African Brands

© 2015 YELLOWWOOD. All rights reserved. PAGE 31 www.ywood.co.za

ConclusionThere are huge growth opportunities for businesses and brands in Africa, and the chance to really do things differently and reinvent some of the more damaging practices of the past. We hope that exploring and exposing the more common attitudes and consumer typologies across the continent will help marketers devise strategies that put human insight and values at their core.

To be successful in pan-African brand building and regional growth, strategy should focus more on attitude than on proximity, since two neighbouring markets may have less in common than markets at opposite ends of the continent. Very few brands are yet able to get under the skin of consumers in most African markets, relying as they do on superficial insight or irrelevant solutions from other parts of the world. We hope this report starts the journey to smarter market clustering, more useful segmentation models and more effective brand-building for the marketers who read it.

Get neck-deep or don’t bother

There has been interest in Africa’s bigger markets for long enough now that just “being there” isn’t going to cut it. Have a good strategy in place for each market cluster and customer segment, and then throw yourself in - to the market research, the experimentation and learning, and the rapid action. It is no place for a timid approach or for “waiting and seeing”.

Use outer-directed human nature to your advantage

The sociable and community-minded aspect of human nature is strong in Africa. This provides wonderful opportunities for brands to earn goodwill and loyalty by bringing people together, helping to build communities and supporting local ambitions. Celebrate the heroes of each community – from the caregivers to the bosses – and you’ll embed yourself in the community with positive word of mouth as your reward.

Nigeria

South Africa

Angola

Kenya

Ghana

Tanzania

DRC

Zambia

Gabon

Malawi

Hustling ambition

Frustrated impatience

n/a - polarised

Serious & striving

Cheerfully active

Proud & hardworking

Hungry for success

Humble generosity

Making it work

Content & easy-going

$521.8 billion

$350.6 billion

$121.7 billion

$ 55.2 billion

$ 47.9 billion

$ 33.2 billion

$ 30.6 billion

$ 22.4 billion

$ 19.3 billion

$ 3.7 billion

1

2

5

9

10

Getting into the headspace of some of Sub-Saharan Africa’s largest economies

Tips for Foreign entrants Tips for African Brands

AFRICAN ATTITUDES

Sources:GDP ranking: World Bank, 2013Attitudinal attributes: Yellowwood projects

© 2015 YELLOWWOOD. All rights reserved. PAGE 32 www.ywood.co.za

References

Acknowledgements

“Africa’s Impressive Growth” Daily Chart (January 6th 2011), The Economist. Available: http://www.economist.com/blogs/dailychart/2011/01/daily_chart

Abade, C. “The Ten Commandments of Marketing in Africa”, excerpts from a speech.

African Economic Data, World Bank.

Aliko Dangote: A Lesson for African Entrepreneurs (2014), Vanguard Nigeria. Available: http://www.vanguardngr.com/2014/03/aliko-dangote-lesson-african-entrepreneurs/

Atsmon, Y., Kuentz, J-F., Seong, J. (2012), “Building brands in emerging markets”, McKinsey Quarterly, Available: http://www.mckinsey.com/insights/winning_in_emerging_markets/building_brands_in_emerging_markets

Data on middle class income (2014) US Department of Labor Statistics

Feist, J. & Feist, G.J. (2009), Theories of Personality, New York, McGraw-HillGupta, R. (2014), “Nigerian middle class: a myth?”, Business Day Online (Nigeria). Available: http://businessdayonline.com/2014/01/nigerian-middle-class-a-myth/#.VCqwRvmSySo

Hatch, G., Becker, P., & Van Zyl, M. (2011), The Dynamic African Consumer Market: Exploring

This paper was written and edited by Alistair Mackay and David Blyth, with contributions from Nomonde Gama, Tumisang Matubatuba, Elsa Gouws and Paul Drawbridge.

Growth Opportunities in Sub-Saharan Africa, Accenture, Available: http://www.accenture.com/SiteCollectionDocuments/Local_South_Africa/PDF/Accenture-The-Dynamic-African-Consumer-Market-Exploring-Growth-Opportunities-in-Sub-Saharan-Africa.pdf

Hattingh, D., Russo, B., Sun-Basorun, A. & Van Wamelen, A. (2012) The Rise of the African Consumer, McKinsey & Company, available: http://www.mckinsey.com/global_locations/africa/south_africa/en/rise_of_the_african_consumer

Interview with Aggrey Oriwo, COO of Ipsos Kenya, January 2015

Interview with Aloysius Chiluba, Creative Director of Altitude Advertising Zambia, October 2014

Interview with Carol Abade, CEO of EXP, September 2014Interview with Victor Ikawa, HOD Research and Consumer Insights at Safaricom, September 2014

Interview with Kelechi Nwosu, MD of TBWA \ Concept Nigeria, October 2014

Interview with Joe Njeru, CEO of Zilojo Kenya, October 2014

Interview with Osibo Imhoitsike, Business Director of TBWA \ Concept Nigeria, October 2014

Special thanks to

Kelechi Nwosu, Victor Ikawa, Carol Abade, Aggrey Oriwo, Aloysius Chiluba, Joe Njeru and Osibo Imhoitsike for the interviews

Catherine Bensard and Johanna Pentecouteau from TBWA\Angola and Eugene Omolo and George Ojing from TBWA\RedHouse Kenya for the consumer vox pops videos

Graham Cruikshanks for helping us access the TBWA \ Africa network

Paul Drawbridge for putting archetypes front and centre of our thinking

Gerhard Reinecke for the excellent photography

Toka Moshesh for designing the beautiful document you are holding in your hands

All of the analysts, strategists, insights teams and designers at Yellowwood whose work this builds on and the clients who keep us thinking and exploring

© 2015 YELLOWWOOD. All rights reserved. PAGE 33 www.ywood.co.za

Jerven, M. (2014) “Why saying seven out of the ten fastest growing economies are in Africa carries no real meaning”, African Arguments. Available: http://africanarguments.org/2014/08/26/why-saying-seven-out-of-ten-fastest-growing-economies-are-in-africa-carries-no-real-meaning-by-morten-jerven/

Kayser-Bril, N. (2014) “Africa is not a country” The Guardian Online. Available: http://www.theguardian.com/world/2014/jan/24/africa-clinton

Maritz, J. (2010) “Doing business in Africa the Coca-Cola Way”, How We Made It In Africa, available: http://www.howwemadeitinafrica.com/doing-business-in-africa-the-coca-cola-way/2433/

Nsehe, M. (2012), “Young African millionaire launches Mara.com, Africa’s first online mentorship network”, Forbes. Available: http://www.forbes.com/sites/mfonobongnsehe/2012/08/07/young-african-millionaire-launches-mara-com-africas-first-online-mentorship-network/

Population Age Demographic Figures, Africa vs. USA & Europe, WolframAlpha. Available: www.wolframalpha.com

Ross, E. (2012) “The Dangers of a Single Book Cover: The Acacia Tree Meme and ‘African Literature’”, Africa is a Country, Available: http://africasacountry.com/the-dangers-of-a-single-book-

cover-the-acacia-tree-meme-and-african-literature/

“Ten African Trends for 2015”, Trendwatching.com

Top Ten Largest Companies (2013), African Business Review. Available: http://www.africanbusinessreview.co.za/top10/1548/Top-10-largest-companies

Trends & innovation ideas from Springwise.com

Van Loggerenberg, M. & Herbst, F. (2010), “Word-of-Mouth Marketing to a Female Emerging Market: A South African Perspective”, Journal of Digital Marketing. available: http://archive.marketingmagnified.com/2011/september/images/article3_wp.pdf

Wilkinson, K. (2013) “Is Africa the drunk continent? How Time Magazine ignored the data”, Africa Check: Sorting Fact from Fiction, Available: http://africacheck.org/reports/is-africa-the-drunk-continent-how-time-ignored-the-data

Yang, L. (2014), “Self-Starters: MAXHOSA by Laduma Ngxokolo”, Between 10 and 5: the Creative Showcase, available: http://10and5.com/2014/04/04/maxhosa-by-laduma-ngxokolo

Yellowwood market clustering, segmentation & consumer typology projects, 2012 – 2015

© 2015 YELLOWWOOD. All rights reserved. www.ywood.co.za

Get in touch

JOHANNESBURG

6TH FLOOR

3 SANDOWN VALLEY CRESCENT

CNR. FREDMAN DRIVE, SANDTON

JOHANNESBURG, 2196

Tel: +27 11 268 5211

CAPE TOWN

3RD FLOOR, BLOCK C

BOULEVARD OFFICE PARK,

SEARLE STREET

WOODSTOCK

CAPE TOWN, 7925

Tel: +27 21 425 0344

Fax: +27 21 425 0338

David Blyth, Group MD

Email: [email protected]

www.ywood.co.za

@askYellowwood