yemen arab republic agrcultural strategy paper · for omclfcl use only yemen arab republic...

TRANSCRIPT

*.otN.S574-TAR

Yemen Arab RepublicAgrcultural Strategy Paper

May 1,16

RojeaDepaEurpe meddi Eas ard Nor c a Rein Of fice

FOR OFFICIAL USE ONLY

N; ~ Docomuun of dw II %4 b w

Twis docxment has a restrcted dlsubtrIion and may be used by recipietsonly in the p-o race of the-. o.iadud.. ts co. e may nototherwibedsdaosed witwut VW~d eank aatdwrzatitL-

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALEN7TS

1 Yemini Rial (YRl) = US$ 0.075i US$ = YRls 5.70

(December 1984)

WEIGHTS AND MEASURES

1 meter (m) = 1.09 yarsd = 3.28 feet (ft.)1 kilometer (km) = 1,000 meters = 0.6214 miles (mi.)1 hectare (ha) = 10,000 square meters = 2.47 acres (ac.)1 square kilometer (km2) = 100 ha = 0.386 square miles (sq. mi.)1 kilogram (kg) = 2,205 pou-ads (lbs.)1 metric ton (t) = 1,000 kilograms = 0.98 long tons (1g. ton)1 liter (1) = 0,264 gallons (gal.)

ABBREVIATIONS

ARA - Agricultural Research and Development AuthroityCACB - Cooperative and Agricultural Credit BankCBY - Central Bank of YemenEDWA - Economic Commission for West AsiaFYP - Five Year PlanGDP - Gross Domestic ProductGNP - Gross National ProductIDA - International Development AssociationIFAD - International Fund for Agricultural DevelopmentMlAF - Ministry of Agriculture and FisheriesNIPA - National Institute for Public AdministratiornPPAR - Project Performance Audit ReportSURDP - Southern Uplands Regional Development ProjectTA - Technical AssistanceTDA - Tihama Development AuthorityUK - United KingdomUNCD - United Nations Development ProgramUSAID - United States Agency for International DevelopmentYAR - Yemen Arab Republic

FOR OMCLFCL USE ONLY

YEMEN ARAB REPUBLIC

AGRICULTURAL STRATEGY PAPER

Table of Content

Page No.

SUMMARY AND CONCLUSIONS (English and Arabic)

I_ BACKGROUND . . . . . . . . . . . . . . . . . . i-vii

A. Introduction . . . . . . . . . . . . . . 1B. Major Development Issues . . . . . . . . 1C. Agriculture in the Economy . . . . . . . 2

ML AGRICULTURAL SECTOR

A. Agricultural Performance . . . . . . . . . 4B. Resources and Constraints . . . . . . . . 7C. Present Sector Strategy . . . . . . . . . 10D. Public Investment Under SFYP . . . . . . . 11E. Sector Policies. . . . . . . . . . . . . . 12F. Food Security. . . . . . . . . . . . . . . 13

DL ISSMES, CONSrRAII AND RECOMMENDATIONS

A. The Economics of Crop Production and PriceIncentives for Different Crops. . . . . . 14

B. Expansion of Wheat and OtherCereal Production . . . . . . . . . . 19

C. Role of Qat . . . . . . . . . . . . . . . 20D. Food Security and Improved Distribution. . 22E. Input Supply . . . . . . . . . . . . . . . 23F. Credit . . . . . . . . . . . . . . . . . . 24C. Research . . . . . , . . . . . . . . . . 25R. Extension . . . . . . . . . . .I I I I I 261. Agricultural Education, Training

and Technical Assistance . . . . . . . 28

IV. PROPOSED STRATEGY

A. Strategy . . . . . . . . . . . . . . . . . 30B. Production. . . . . . . . . . . . 30C. Policies. . . . . . . . . . . . . . . . 32D. Implementation . . . . . . . . . . . . . . 34E. Future Investment Program . . . . . . . . 34

Following a mission to TAR in November/December 1984, this report was writtenby r.F. van der Goot (Bank) and P. Harrison (consultant). Contributions fromMessrs. Eisa, Lewis, Rana, Woldu (IDA) and Basu (consultant) are also included.

This document ha a restrited distbution and may be usd by rcpients only in the pefomancof their oiicial dutiesL Its contents may o otherwise be dbckoed without World Bank authorizatioL

Table of Contents (continued)

Page No.

Annex 1

Tables

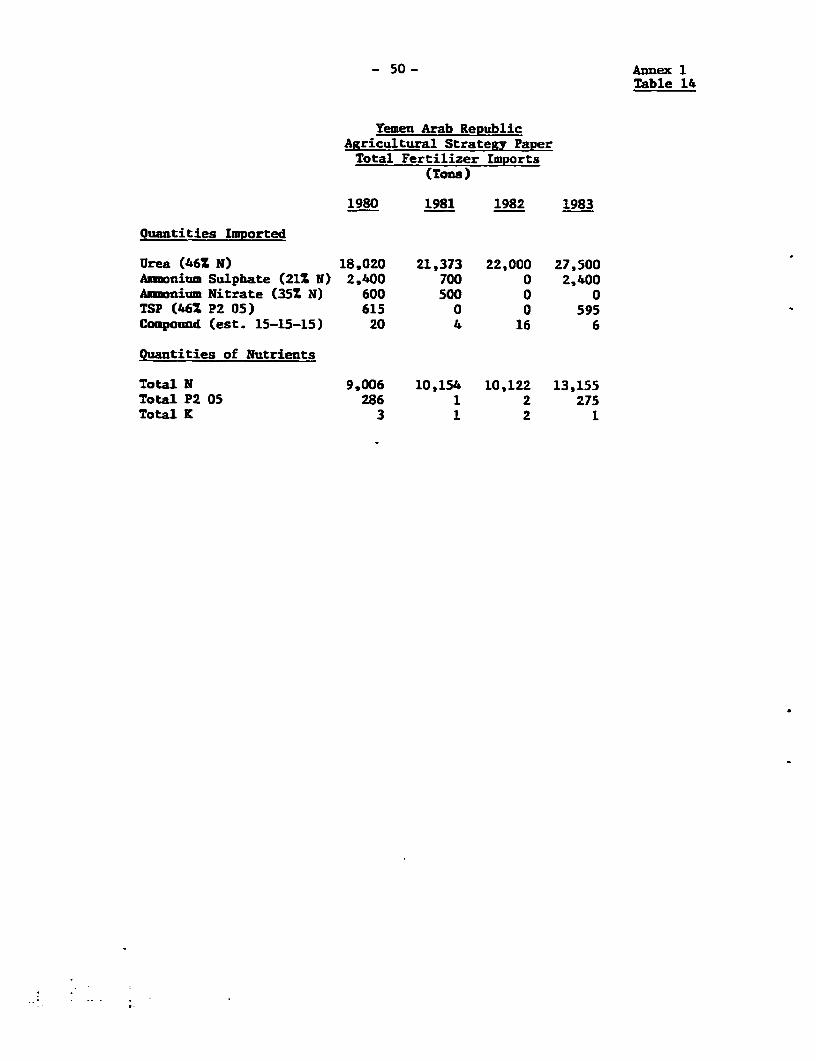

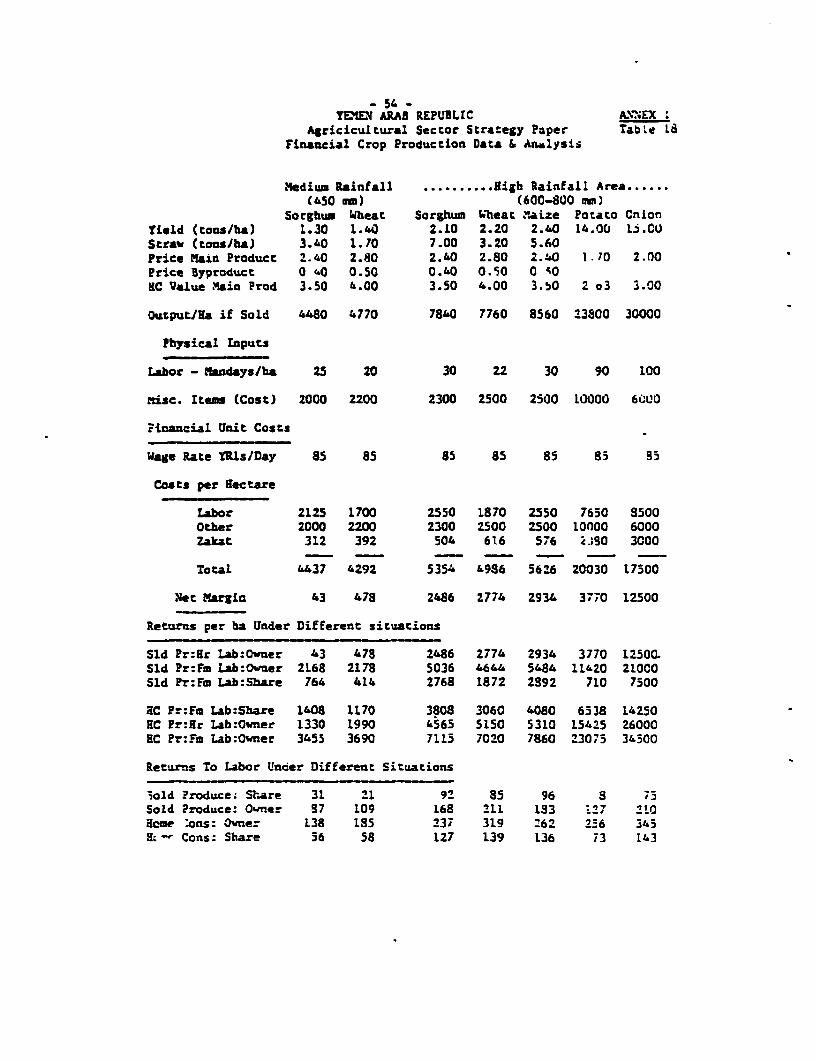

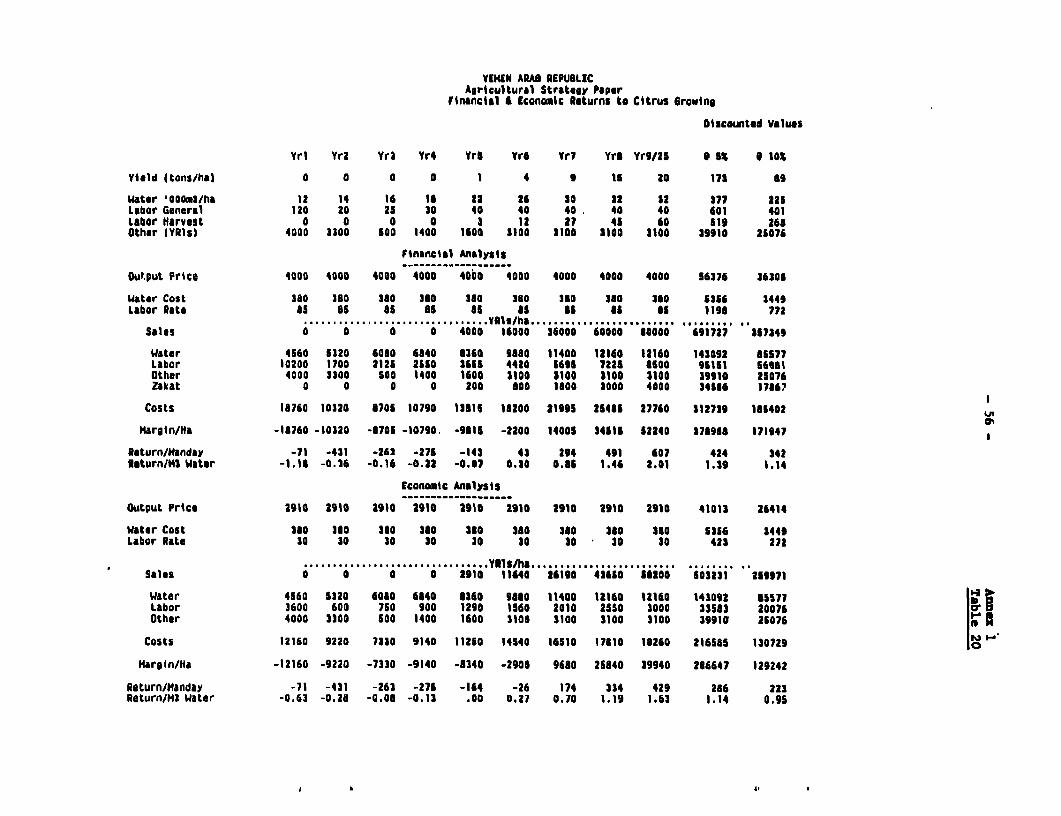

1 Total Cropped Area .... . . . ..... . . . . . 372 Production from Main Crops . . . . . . . . . . . . . 383 Yields of Main Crops . . . . . . . . . . . . . . . . 394 Estimates of Land Resources. . . . . . . . . . . . . 405 Sector GOP, Imports and Remittances. . . . . . . . . 416 Sector GDP, Domestic Prices and Boarder Prices . . . 427 Estimated Crop Areas by Source of Water. . . . . . . 438 Per Capita Income by Sector. . . . . . . . . . . . . 449 Estimated Labor Requirements . . . . . . . . . . . . 4510 Agricultural Labor Supply. . . . . . . . . . . . . . 4611 Qat Consumption and Production . . . . . . . . . . . 4712 Agricultural Imports . . . . . . . . . . . . . . . . 4813 Detailed Agricultural Imports. . . . . . . . . . . . 4914 Fertilizer Imports . . . . . . . . . . . . . . . . . 5015 Analysis of Cereal Production. . . . . . . . . . . . 5116 Estimated Pumping Costs . . . . . . . . . . . . . . 5217 - Growth Potential for Fruits and Vegetables . . . . . 5318 Financial Crop Production Data and Analysis. . . . . 5419 Financial Crop Production Data and Analysis. .5520 Financial/Economic Returns to Citrus Growing . . . . 5621 Economic Crop Production Data and Analysis . .. 5722 Economic Crop Production Data and Analysis . .. 58

Appendix A. Economic Prices of Agricultural Crops in YAR . . . . 59

Appendix B. Completed IDA-Assisted Projects in YAR . . . . . . . 65

Text Tables

1.1 Rural and Urban Income Estimates (1982) . . . . . . . 32.1 Food Imports and Agricultural Value Added . . . . . . 52.2 Estimate of Agricultural Value Added (1982)

At Border Prices . . . . . . . . . . . . . . . . . . 62.3 Breakdown of Agricultural Value Added

By Production Area . . . . . . . . . . . . . . . . . 62.4 Distribution of Agricultural Land . . . . . . . . . . 82.5 YAR National Agricultural Land Tenure . . . . . . . . 82.6 Demand for Agricultural Labor . . .. . . . . . . . 92.7 Agricultural Sector Investment Proposal

Under the Second Five-Year Plan (1982-1986) . . . . 113.1 Prices for Agricu tural Products . . . . . . . . . . 143.2 Suimary of Financial Returns for Selected Crops . . . 163.3 Sunary of Economic Returns1for Selected Crops . . . 173.4 Impact of Sharecropping on Financial Returns . . . . 183.5 Economic Retuvns Per Man-Day for Wheat

And Sorghum . . . . . . . . . . . . . . . . . . . . 203.6 Average Farm Family Income Per Capita . . . . . . . . 214.1 Agricultural Sector Growth Potential 1985-1995. . . . 33

*9i .- ~*5 ._ jjI .ujt ..V

j-oLI J1 _L6..J I jI,I Lh- s

L5L....*~II ~ L..auiI 1i OU* C~ 3 Lg.Zj qej_LZI£.J jq...~Jt '&-Si I ;Lw JI s .a. =.#.t ..... JI

;.61 I ' -- R5, I,_~ t- L;& 11 L" -pllIL .,I JS ?iivz Li 'J2 I

- ii v J:s La J.,. &ZIJ ;jJI Y/l ai- *_ JS 1_s % 1 1j I :LijI j I 11 e

L5..J &J,. Lej Ji.I .i y JI 6 >. J.S - iZ.Ilj LAA L.. yi

II_l {r>f l_,_;. L UJ- '1I) J&l . L,J5 'I a% :,.a

Y,k/ lil ,4 1 4_ , ;- .13 LX c1 3)YI si,-, ' 43 ' - 1

_ - ;L . ei~.J & I r s 5; w . _,& jIjJI 11 0 I II j *:I

-L ,JI -J L;e (.jLI%l I &L C ; j

fA/ 15Y ; ZE- {>* S Fl 1 1 JU1 s *JX~~~~~~~~~~~~~~j H v1 *+

' (<9*=-11 3 tH t-6 *)O - j- * -L--:

'~r~-M-i 1r'~ C-. C.- - irx- t 'r'ir - i rnr I - -:

ir-l =H ir-r w-n.- i^ cV sr - rir,r.-ic- -l ism. z-w *

>'5t- II4 Ic- r~ Ir!" ir' 'T--*V -cf-rq fl -1 (:: tr , ' Cr- 1 r i--- v, -CZ

; .-... _--nC ir- -i2 trt Ir f er" Ir-v fl- l"<iy,-' 'fl f

4Y* S w!_ 1Q I 111I~~ ' c1P" 9r'-i ir4 --- 1r--91 -

~ ~r~rn '~-ir-~-~r'Cic -- ri { rrrs. Irfr , ( I -

n- i-rics -r"O irrs K _r I,>s

g~~i- a ? rrvn-J -1r--`1 irc" -snr-v ir"-ir2 ir-sn- i--,

<P Ir7 lfJ ¢ lsrl = 1 >r l[<SK < - on ~~~P rw-, I- J

rIF .; 9 rr' r r 'n-'" I-r' Ir"e lr (r Ilr-- Y rflT

wv3 111; i nr, r I-rn I p Jr-s-, arc, ir- -

il_ rv;1 f_--br ig} r->> --o ->r, i_r- , ?<[ all

f- rm r -e s ---.; O Arr-,, .r'

~~~~s-r igr; s_ <" Ir 1x--- i rk 1 Ir'j ~r^t C1¢. IO..P

Ir4 1ir--L IrP6_ ir>vIrSI9 r'--r -

-r-

,a..a. 11,. L. ,,J^...J) J--.Li LI . L r -L... L L.J

I I LA-kL,. - , JI >t L . J . jz j L..I _i .j. ;6 I ; I

. cL4 -,i ;i.I *L..JIZ Bit-,I JI ,-~A Ou LJ .i~ C - 3 .a. - ~ -L.. * l_t>Al C. ?7W j, I . -e_ J I IAIm1 J '1 -A .- J

A la I- II I jy .; *,S'l * -* &Lsj-I jI1 JI r.iZ C esJ

. yzlt1SE wl. _- S LA Yl

z -A ii.~~~ --~~ &-L_ -

31;L~_XJ ; .LJbJI * f LIJ I 4..L-a ItJl , LLI ..s%.l j - 1 I

I -- LA ~ .(IqJ j) L..i zIJI oL- c 7s _ I.J LA I ,X SIA.&,Jl, >o &z

I _ 11 J .t5P1 ,.st,z , CS _.- -S" ,. -a Im 1 :i JII LI a JI

,=LS L1---~ 1 Lai t 1 I J.L:%{ A ,1 Y L_k1 o.I

. * *-~~~~~IUL _ f t5;. v IJ 5 I a Ij ,J I I sJI 1_5 lc\ -6 a I:

L-1_m_- 1L 1-. I J I oz ;cLe~. *J-o I1 6

I j_g.-J I ,J I %--I 9 ,&:~~~~~~~~~~~~~~~~~~~~~~~~~~~J I 9 iL~~~~~~~~~ LJLJ I F. L.';.- I~~~~~~~~~~~~~Y -

, -A _ _ 1 c,-JI Xo _- b{0s J 1siJ <l*1 1, _J 16 * _ l j-

| _ . j | J tyI A& L, J_- LS _L 0J-. - oJ I

v~~~~ ' * - a- 1 3iJI ,r =I z :f>L1 1 a ISe;

r - . . , ( | ~~S I riL L : , . :-n

'?~~~~~r- .j '1-

-5 s--t IV f-I r-.-m ' r - X1- s d,

i~~r- i& Mm;r ' ̂ <|Xg1

ICr{-, rr S-4 C.4d%F [< <

isr-s fl -r,' I, zmE 1- rs- 1--:-1-

I 1 _ fI;^ C C 1^'n^1 |- .-_ "V 1 S 1 17,," r,' -'iir

|-i * [w1 z to P-- C r--r, -,' i-- -:-cr-rt1 pl --1 1-

ir-r ~ ~ w-w. .O cri-1¢ 1r-_. -n-- JJ w

,--r -4--ir ir--1:-lpfi- : _ Ir IMJ ;yi,j).f

i~~rwr F n--? 1"12 Irlo Iml. ", it1--r-- i-rr r-

rJ-n- el mr;. ir r. s if i' -r! ,rrr. r n

irri- wmi- z r_P -,r, -- .--G- ir.- - ir--ir-' l-. 2

=< '- ~1 ^-¢ l;5irv ,'>bs; ew<:_ -_

If,-swrv r t r¢l-rr Jr--@wFl -:s del-V jrl n -- l b

X-'rr'5 ir ' -' ,rw51, ; 1f!' Is ' w' 5C ICTw1 Ir:!~l K c1 ,

ir-r ir, rr,,,c .!- K <-48 z :'. -- nv

A- IS"'r s

irC,rv. --" irA - a--r- r r irw" ri-' n4r

N?N~~~~~~~~---n -- ;J .tb

--ir l8 1--r ir4l- irrc <nF t-7em,x , I,r n 2 5i.-

-- f e54_;wr 1 - -w I F|^-7f4IXe]2W _

¢n S~~~~~~~~~~r -- i- 1grr2- > m-; 1,[ srr11|----c l.

A-~~~~- irin i-, r--n -rVm- - rr -- i5,

1.. CMr- r,P Ig Ir _< I5'< ."'r 1r9I sl- fW - l& lIT l I rtn--a- is- cr-r6 r rf r4n

~~~~~~~~~~-1 i4-I -.:b iFwr w - Ir;r ---,. __.,

~~~,r ~ ~ r rr IrF c1 -6 R| o Iron Irfl-rw -I- i<n o 51l-r

,v.c .,rT-, o rX.ri, io z-nrs rir irnn? | p -! - r

-T-~~~c

wfr r.r? Iry-l- ~( r-w' Fr ) - u-1r8 r'O - , Ir>r .< irw~n w~| I r~~I- r ' r r m r a r-*

(l) I -irf Ir~i - w "" '> 'r-) irIr u" u f l' "' K r r

.,~.t~I8:% ET6n? ir~' "~" ~ ~Y, I ~rr Thr 'IT'- ir - , -v -,-zI-m--.^V~~~~ 1.-<

!&¢) *srn r Ira,-rA,- 11 x.. - r1 i-r-

1t1 s~--r -¢ Cb rc? ,- 0 4s-lrV ir _vr-Cp jrr rr..jrr,j crr. 'r t- >@-

--i r -l Il I\ r- I P rvr -, fliv n-rrcP

i2 rro_1 1-_1 ir^~ r z rr 1 r- si-_ri rn |t X1 s i0;c-

-irr ir-> n m IV rAycrg"o r r

4-1 , (-- Or Ir Ir;l, AA, '41r.-¢ s . l@

~~~~~~~~~-0 Cr.: irr 1r-* C|'.-¢<IrVro; t 11 tr>¢8 x

V~~~~~~~~ |r-- lf 1- > I rr < femIr ;

V>|¢ irs 7- lr .rrr .rj- t V "rrrlrr-¢,l->^

Ir¢_ ~Ircrilr" [¢ rmrl I1Sm- f. I., 'r r~ r ; Io"

y

jr _) Co *I ).jQ ik. l %L3JL j ""

6 W W L &.L .I L.""h. LJbj , ;>. ".L 3 .&4_96 a,..b . I iza I ~ .~ I i...JI

, 1 :L.LS~JI aim.A A *.J qJ '.4 I 1 .'j.j J

* &aLuJI *jI JYJI cY_ I >. .L,)A.L a..._ I H1 o L.W ,YI L";L% u1; -J LA W 1 5| j..uJJ

;jI al ; U w L. ,lo tJIjJI L.b j,, oj l I I L 1L L

It %Z"~~l tU AS%il *P. &.JLW.aJ l

: ,e,3t - I \II >. 4 ,sI- J J , L , 1L.-i I -* I I I I jl I* a~ L~..JII ~ J,jJLZj * £.JOL..J IjI 0*. z .p.L.J..J LI J46 ~jj' Ij

_--t Jad ,S >1 t I Ie .uY.I 1 li r I3.i dJ 6 I Z. 6 AI

CA iJ "Lm ~*Li64l a± Jj IjJVIrL-..I V. f.o"IAJIL. &~.Ln.-- -kl MII ).4^ ,*, '- La. L1, ' J I aWI, .JL-I-. lI L'- * - l ,> I

I L.> ,A |a | -* J a_; ,; at t J,sYt L|; - I ai>, - 9 - : I - * a. -_ - I ~,I ,_LAyI I.1IJI 1 J.--t. uL -l Ah5. ,^ * r.~lvs J13~. 1 ;J*I_YSt o;;JI9

9:l -xI U4.Z (j) L,~ L .3"JU - -YI J z sJLa. J * C4,4L I E I

L-J- I L_ I I LXJ U JU ; I I _I | | I 3 L I JI t -

II J..Lj (') JAL,J I *I,J I I - 1 I

s - -11 C5.:Y~~~~~~~~~,I u;;JI ..) i.sw;..L() z JI -fl

JAl- Il;r

r eNP I rw --rr-1 -`1 g I r-.r:c r-r Ir I; r- - I wm.I:

I r--1; IP rvrl i--i --r c-i- Ig w6 r-c- I> -5- l-~@ st; -

-F I, I. .16r r0Ir1

^#;z_) -T-- --- r wrr 1;.IE§-Cl--l 1 i > i

,^ ..r_, -Lr 1¢1, 1- --̂ rr 11

ds ' ~ ' ";"' K -r 5-cr -o. ,,-. Il- -o-

I, On o--- ) 1!^- ir-_-IJ I, -_-. .0^* lrtrrrr ir - O r -`_ 5t,

2 l~ lzrrrirr1 -rr-

rr-1 - ,-r Is-R I itrCr I -1 i r I -r I n- _-- I i~ rr-.--'rl I r-r I

IC. .1 1 < 1r--- f- -rlrr . 5_ - 1. r -. ;nrg I-

z- sv 1,, -^ r ,s,i, r. i--J , , ; r--C .r Q

,~r r-~~' r~-V-~ I1 -- r - rvi 1 V - 1C _- '*q2 r i'zS'ans

- -3nrs 7-- -~ C'i s. ,¢ - 5-

~' '--x.i Ir i nc-re Irrj'~~r ~ ~ 1rr-¶-i (5'--jC, ' nr_{>;? ~~- --- ck1- )- - -is 1 -- >r il%1 1- Ir't*

Ir>>l=^' ~~~~~~~~i-- *- i ¢1;wr-- r (r-r

i.c '-' ir'4- r' i& s' - 'rr 2 c r ir-n4- -

¢r-v *f'r^ ^ _ .'^ 1----=. re-- r --- [n g --- rH -rr i -- g i 1 i 11 -7s -I f cr-7

m9_>?_ * !nirci l-Oe r- 16 'n - <* 1m<

I -n It'-w-) I i,;s w - c I" 1 IrCI-~r jjr-.-.s- i,r J! - s

-er 5np t-t i <n, -J 1 ir-~n w%1v< &- z-r 1---= -- q

sP~~~~ gw->-| 1.1 C. ,Klr' crrn n rCrw *r~~ Ife l:'- <@

.-Q I rt 1 | t? I ir<---. * '"1 r4'rw ~ orA- iLri-n ir ) c1

Bl- _ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~~ircl

I-r-.1--v it~~~~~~~~~~~~~~~~

re~~~~~fcI , -

,n'-4- -_'rHJ < $4 1 r

4 ir I 1 I 1 *. 1rr 1i f -1 ' 1T If n l J I . Y l3 ,

1 IV I 5s- r iW F'.- I T1 -r 1 ', f''-I -.- 1' 1 IT 1 -- -. C 5-

o ¢- . C~., .c,-g .~ rC_ _FI I - IrCc rI --1' Cr. --

Ir -'- - <'~ 11 =1 I ,,1 1IW ,r, If¶ _' c, Icf 1 - -. 1 -- 1

1 'wf 4 C 1 ' * -> - Ir' - i%' 1- P w 11*

!r-~ ~ R(I -4 -r1 I- -4 1 l - '1 ) C| _ - I

C Ir-" Ir i--- 'V r I

incc--,n i-nr i 1- -

~~~~~lr,. i - .. r--- -rir. rl fl ,.4 . ( r sr-s

i r-r s-, i Ir.->1-n-W-- r 1i-- i,r-- r-'1)

_____________> ;A -11 ;iaL tl .1_,1 -cl

:- L.. t_YI ,_ ao1 J c.L. I AS . ,:- ..... L *1 J.u. 1- aj

* ^ Yl* s 1 %--'13,o 4L i bi J..-Lz.&Jtl , cAL ICA 3_

jt I >-- 1 1 I,, I v L , I j)JI -. l * - I I

|~LI~JI~ .,.L..JI cL5t,~.JI 1s a..L..-IJ 1L..I UJS qZ aJ Ijo i J_11j

I x _ .. ,I l _.,. , LZ I . *.Lsy. 11 *±L1 J.6 g .i , ' Jt 1-.-- JL I

* 1 ;8~~LJlI * 3 %J l 6;-1 Is Jl t>e1" Le i-Z Ia &--al*=,9~ U*_n IJ vl t ..W LS;LJ L:. 91 p ,JIs *1 eI L, * LLkJ d^A * - .

*1 1' -~~~~~~~~~; ~L1' J'-"-S ; - 1J-b^SI o 21 -- jl

* .... 1 ... Jt &,4J L; ,___L-- I

I L.* LL . lS1 XI - I I I - (..1

_9.1_1 j)J-I 64 .J.?J i,. I

J_}- PI & - - *.-.-- .IJ.ffL;1l J ,. JLI LjJ,. a>=l JIl

a... L.3 3 . J.?I >. *.. - -I L±..I *... ^J c--L,6;..Z... ..... jJJ Is4 ,a.z 11 .

YEMEN ARAB REPUBLIC

AGRICULTURAL STRATEGY PAPER

SUMMARY AND CONCLUSIONSRecent Performance

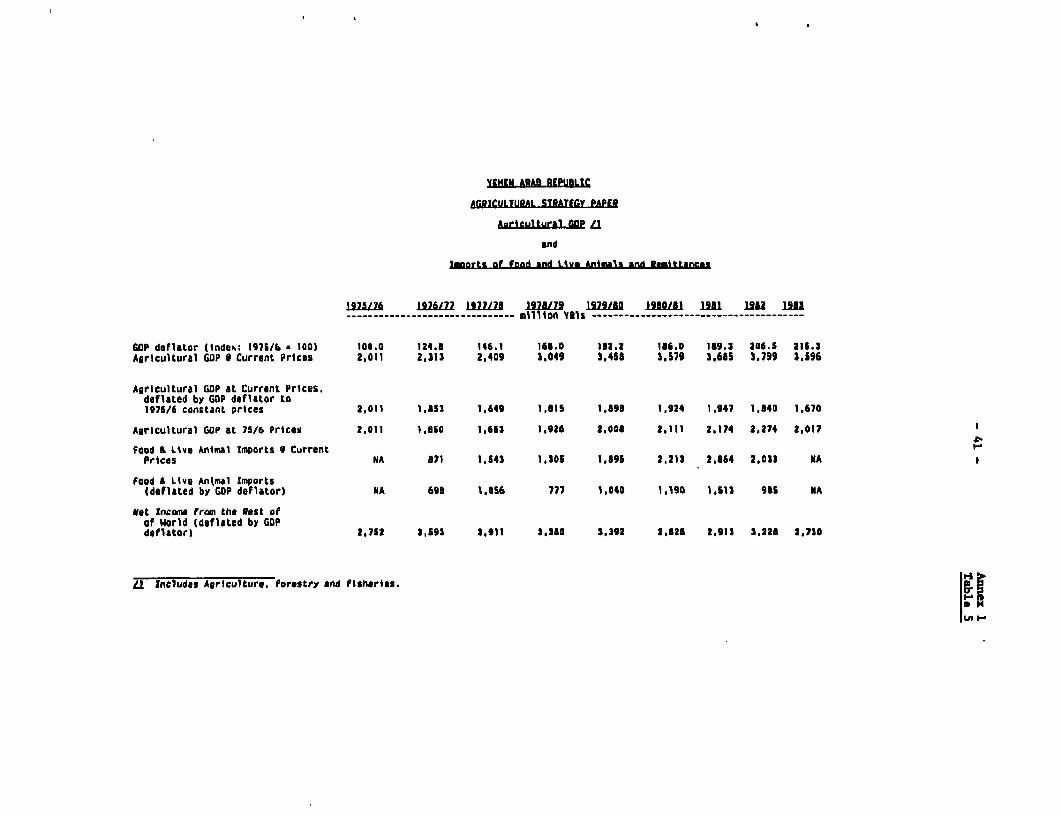

{i) Agricultural performance in the Yemen Arab Republic (YAR) in the lastdecade varied by sub-sector, but overall sector growth averaged about 1% p.a.over the period 1970/71-1982 with large interannual variations resultingmainly from fluctuations in rainfall. In the absence of reasonably longtime-series for measuring the performance of the sector or rainfall to whichit is closely related, it is difficult to determine to what extent adverseweather conditions have constrained growth. Further, aggregate figuresconceal large structural changes in the sector. Marginal cereal areas wentpermanently out of production, though simultaneously, a substantialsubstitution of very profitable qat 1/ and fruit and vegetable production tookplace in better-watered areas, generating substantial additional output. Thataggregate sector growth has been lagging behind the growth in demand for foodis also cleaz from the increase of food imports by about 402 between 1976/78and 1981/82 and from the fact that grain imports in each of the last 3 yearswere somewhat above 500,000 tons (including flour).

Strategy

(ii) Overview. Agricultural potential in YAR is severely constrained bylimited water resources; it is estimated that 90% of sector value added isgenerated on only 40t of its cultivated area (i.e. irrigated land and areasreceiving 600 -m rain or more). Consequently, means to increase theefficiency of existing water use (still very low) and to expand knowledge ofthe nation's overall water resources are vital to YAR sector development.High domestic production costs imply that the country's production advantagedoes not lie with a major expansion of grain output, though measures whichhave helped in the past to increase yields of high rainfall areas should bevigorously continued. Rather, the focus should be on growth of products whichare bulky or perishable and hence difficult to import (e.g. fruits, tubercrops), or for which a strong local preference exists. Nevertheless, severeresource constraints do not permit a sustained sector growth rate commensuratewith the expected increase in demand for agricultural products. Given therelative strength of the private sector and the present paucity of Governmentresources (managerial and financial), public sector involvement in agricultureshould continue to focus on providing essential support functions that cannotbe privately supplied, as well as establishing an environment which wouldallow the private sector in agriculture to function vigorously, by ensuringreasonable competition among suppliers and traders. Because of YAR's limitedagricultural potential, the effective functioning of research and extension isof paramount importance. Government action is also needed to assure foodsecurity by overviewing domestic stocks, building up necessary reserve stocksthrough imports and assisting in the smooth functioning of domestic markets.

1/ a mild stimulant.

- ii -

Special promotional actions and programs for agricultural development shouldbe confined to areas and activities in which sound economic returns can beexpected. Because of severe budget constraints, outlays for purposes whichare not directly productive should be kept to a minimum.

(iii) Policies. As producer prices are already high (generally twice thelevel of import prices), there is no need or justification for introducing aprice support system to stimulate domestic production. The policy of costrecovery for irrigation schemes in the public sector, though reasonableconsidering the stage of development at this stage, should be reviewedperiodically. As there is no mechanism to account for the scarcity value ofprivately pumped water, it is reconmended that Government initiate a licensingsystem and controls to preclude overexploitation of groundwater in thecountry. The policy regarding fertilizer supplies should be to continue toavoid subsidization, while aiming at making available a variety of additionaltypes of fertilizer, without which the ones currently used become increasinglyinefficient. Government should also consider whether subsidies on nurserystock have a continued justification and whether practices currently inoperation in some bilateral projects whereby farmers pay for specializedservices may be adopted elsewhere. The actual yield of the excise-tax on qatappears to fall considerably short of its potential. As this tax outweighs inprinciple the sum of all other agricultural taxes, sector resourcemobilization efforts should focus on increasing present collection levels.

(iv) Production. Fruit and vegetable production should be expanded to thelimit of the domestic market. Overall domestic demand is estimated to grow at5c p.a. and the opportunity exists for domestic production to be doubled overthat of the last decade so as to meet this demand, as well as to substitutefor about US$80 million worth of imports (1982). The strategy for developmentof cereal production should be a cautious one, respecting the economics ofproduction and resource constraints. Efforts should be concentrated onraising productivity in the areas of 600 mm rain and more, particularly thosewhich have a cereal deficit. In the low rainfall areas, cereal production ismarginal and risky, while under most pump irrigation conditions high unitwater costs render cereal production uneconomic. Large-scale programs withGovernment support to use irrigated areas for wheat production are, therefore,not justified. Subject to these principles, efforts should be made toincrease cereal production through further intensification, so as to containthe dependence on imports which constitute a substantial drain on scarceforeign exchange resources (about US$80 million in 1984). Opportunities forlivestock growth are limited. As ruminants (cattle and small animals) in YARare utilizers of by-products (e.g. straw), their production will be determinedby the growth of cereal production. Growing irrigated fodder directly for

- iii -

livestock production, on the other hand, is uneconomic. Though substantialincreases in broiler production have occurred, the advanLages of domesticproduction over frozen imports can be expected to diminish as the presentconsumer preference for live birds is likely to erode over time.

(v) The appropriate strategy for qat is problematic. As the value addedin qat production exceeds that of the rest of the sector, its economicimportance is large. Domestic demand is strong, but qat does not provide anynourishment, uses valuable land and does not generate export revenues.Consequently, views have been expressed to limit or eliminate its consumptionand hence production. Qat being a tree crop, its supply is rather inelasticand prices in the short run would fall sharply if consumption wererestricted. In the long run, qat producers would switch to other crops and,in either instance, the impact on average farm incomes would be substantial.The qat issue is complex and it is recommended that the present research befurthered in order to formulate a well articulated qat policy.

(vi) In summary, overall growth potential in the sector (excluding qat) isrelatively limited; it has been estimated here to be about 2.5% - 3%p.a. atthe very maximum and this would call for a further expansion of current goodlevels of adoption of research packages and adequate growth of supportfunctions. About one-half of the increase would be in expanded fruit andvegetable production for which a large production potential exists. Theoutlook for cereals is however, much less promising and realistically,aggregate supply can hardly be expected to keep up with aggregate demand forfood, as generated by an annual population growth rate of 3 percent. YARagriculture will not be able to make an increased contribution to foodselfsufficiency.

(vii) Food Security and Distribution. Given natural conditions andconstraints, a reliable strategy for achieving food security should bedevised. Imported food grains would continue to be needed to supplement thefood supply for commercial (urban) consumption, whereas in the countrysidelocally held on-farm stocks should mainly be relied upon. Commercialregulations governing the management of imports and of domestic freightmarkets need adjustment in order to enhance competition and efficiency. Also,government institutions involved in food distribution should provide a focusfor working with the private sector as well as a standby capacity in the eventof emergencies. A public investment program will be required to improvedistribution infrastructure, including; (i) bulk handling of all imported anddomestically distributed food and feed grains, and (ii) modern wholesalemarket and storage facilities for perishables to be operated by privatemerchants.

Supporting Services and Implementation.

(viii) Input Supplies. Limited availability of quality inputs is a majorconstraint to successful agricultural development in YAR. Examples ofshortages include non-nitrogenous fertilizer, certified seeds, disease freenursery stock, as well as various agrochemicals and medicines. Given therelative strength of the private sector, yet constrained Government resourcesand skills in commercial operations, input supply problems relating toagro-chemicals need solving through private sector initiatives. It is

- iv -

recommended that MAF determine approximate import requirements and grantimport licenses only to low-bidding importers, who will be entitled to fixedmargins when selling to wholesalers. For a variety of crops, (especiallycereals) seed production by the private sector is not practicable; due tolarge climatic variations, a multitude of varieties is often required. Inthis area, the activities of the research apparatus need considerablestrengthening. The free market for imports of tractors has led to manydifferent makes being available in YAR, often unmatched by effective parts andservice facilities. Some countries have successfully overcome this problem bylimiting imports to four or five approved makes and models. For tractors tobe on the approved list, a competent service agency with skilled personnel andadequate stocks of parts would need to be established. In this way, it ispossible to strike a reasonable balance between competition on the one handand good back-up service on the other. It would be worthwhile for YAR to giveconsideration to such an approach.

(ix) The strategy for the Ministry of Agriculture and Fisheries (MAF)itself should reflect (i) the paucity of available resources in the Ministry,and (ii) the considerable strength of the private sector in YAR. MAF shouldconcentrate on those tasks which are essential for sector development andwhich cannot be easily provided by the private sector; these are primarilyresearch and extension (see below). On the other hand, MAF should assist infurther improving the conditions for the private sector to operatevigorously. This would call for improved procedures for the importation ofadequate quantities and suitable types of farm inputs, notably plant material,fertilizer and machinery. Equally important, MAF should be strengthened,through TA over an extended period, particularly in its functions of planning,monitoring and implementing sector programs and projects and of coordinatingdonor agencies' activities. Considering the very large need for fuxrtherreform of the public administration, TA tasks should really be limited to whatMAF can effectively manage.

'x) Research and Extension. The association of research and extensionwith economic analysis should become much closer for those support functionsto become truly effective. It is recommended that priority be given to ananalysis of production of crops by climatic zones, defining their economicimportance and identifying those research activities which would have thepotential to achieve maximum economic impact for large numbers of producers.Also, Government is encouraged to pursue recent measures towards integratingvarious largely independent, bilaterally financed, research activities intothe national service. The overall strategy advocated here, i.e., focusingpublic investment for agriculture to support directly productive activities,while keeping outlays for not directly production purposes to a minimum, callsfor an efEicient use of scarce extension personnel. Measures recommendedinclude; (i) concentrating expansion of fruit and vegetable production in arelatively small number of production areas, (ii) integration of project basedextension services into regional extension services, coordinated by astrengthened Directorate of Extension to ensure better use of extensionpresence and dissemination of experience-based knowledge among various regionsof the country; and (iii) further training of extension staff.

v

(xi) Credit. The main problems are (i) difficulties in loan collection;(ii) shortage of trained manpower; and (iii) lack of coordination betweencredit and extension. Though shortage of lending funds might become aproblem. enhancing the viability of the credit system clearly should precede arapid expansion of its resources- It would also benefit from higher interestrates as this would improve the incentive for borrowers to repay promptly.Also. conmercial banks should be encouraged into agricultural lending byoffering them greater incentives through increased lending interest rates andspreads. Another method of encouraging the commercial banks to get into thissector would be to exclude deposits equal to outstanding agricultural loansfrom the application of the statuLory reserve requirements.

(xii) Training and Technical Assistance. The basic issue in acceleratingthe pace at which local institutional capability can be developed relates to;(a) striking an appropriate balance between the operational tasks and trainingrole of expatriates, and (b) progress made with Yemenization. Given priorityattention by Government, the pace of Yemenization could be greatlyaccelerated. Such priority is warranted, and should be reflected in projectdesign, as for medium- and long-range development, trained Yemeni manpowerwill be essential. It is recommended that MAF establish (with expatriateassistance) a training unit to coordinate manpower and training needs atproject, regional and national levels. This unit should determine, on arolling basis, MAF's medium and longer term man-power needs and plan how thesecan be reasonably met through; (a) project-based training, and; (b)free-standing training programs. Lhis unit should also define priority TAtasks and attempt to enforce accountability as to their execution.

(xiii) Donor Coordination. A large proportion of sector development takesplace under foreign assistance programs. Hence, it is necessary that strategyimplementation be coordinated, and policies pertaining to input prices, usercharges, etc. be harmonized, in order to facilitate integration of individualprojects into the rural economy, once these are completed. The recentlyestablished local donor consultative group chaired by the UNDP residentrepresentative would be a suitable forum for the purpose.

(xiv) Future Investment Program. Government has indicated to the missionthat it intends the new FYP for the sector (1986-92) to reflect, to the extentpossible, the recommendations made here. This paper's main recommendationswere, accordingly, discussed with both the Ministry of Agriculture as well aswith the Central Plan Organization, to ensure a coherent investment program,in which the activities of Government, IDA and other donors are properlycoordinated. Given the proposed strategy and the shortage of Governmentresources, investment priorities should reflect the need for projects whichare not expensive in terms of recurrent costs, and do not place a heavy demandon the small pool of skilled staff. Therefore, support is not recommended formulti-component area development projects but for regional projects with aspecial focus on production support services such as extension, based on pastinstitution building efforts (as under the SURDP or Tihama projects). Low costspate irrigation projects in the Tihama appear to show good returns and shouldbe pursued, provided water charges can be levied to cover operation andmaintenance costs as a minimum. In other regions, development projects with a

- vi-

specific production orientation, e.g. support to production of fruits andvegetables, or of cereals in higher rainfall areas, could be undertaken. MAF'scapacity to plan, execute and monitor its main functions needs considerablestrengthening. MAF and donors should decide on priority areas and necessary TAshould be provided under future projects. Other possible areas for publicinvestment which are consistent with the strategy proposed here would include;(i) bulk handling facilities for imported food and feed grains; (ii) mkdernwholesale market and storage facilities for perishables to be operated byprivate merchants; (iii) support for establishing regional and nationaloperation and maintenance services for completed agricultural projects;(iv) integration of project-based extension services into larger units; (v)increasing irrigation efficiency in areas already under irrigation; (vi)construction of small "check type" dams to retain flash floods for improvinggroundwater recharge; and (vii) preparation of a national water master plan,see below). These components could be included in the regional agriculturaldevelopment projects to be prepared during the Second Five Year plan.

(xv) While these are important elements of agricultural strategy for whichprovision in the Second Five-Year Plan would be justified, it is also necessaryto consider whether some of these issues and tasks should not be tackled on thebasis of a country-wide approach, drawing on the experience gained, andinstitu";-n-building achieved, through the past and on-going efforts made underthe se , of TIHAMA and SURDP projects and other area development, researchand credit projects. There was, undoubtedly, a need in the early phases ofdevelopment to proceed on the basis of specific programs for limited areas, buta stage is now being reached where it would be worthwhile to review thesituation and the strategy in an integrated, country-wide perspective.Illustrative of this approach is the on-going program for institutionalstrengthening of the Cooperative and Agricultural Credit Bank, in variousaspects such as accounting, lending policies and procedures and data processingwith modern techniques including the use of computers, alongside the provisionof funds for on-lending through the Agricultural Credit project. As is alreadyproposed, donors should assist Government in reviewing the agricultural aspectsof the national plan and, on the basis of past project experience and variousstudies carried out under the different projects and with reference to thephysical and institutional constraints affecting the sector, determine theappropriate courses of future action in the fields of water resourcedevelopment, maintenance, agricultural extension and research, marketing ofagricultural produce, training for agricultural staff, and strengthening theAgriculture Ministry so as to enable it to fulfill adequately the planning andleadership functions for the sector. It is on the basis of a carefulexploration of these critical areas from the point of view of the developmentof the sector and with reference to the emerging pattern and priorities ofinvestment in the sector, that Government should decide on the most effectivemeans through which it can further support the development of the sector.

- vii -

(xvi) Water Resources. In view of the limited known water resources in YAR.and the heavy reliance on irrigated agriculture, an in-depth study of the waterresources potential in the country should be carried out to prepare a watermaster plan for future development. Till then, top priority should be given toprojects which include substantial investment for the purpose of increasingirrigation efficiency (presently very low) in both public schemes, as well ason private holdings.

YEMEN ARAB REPUBLICAGRICULTURAL STRATEGY PAPER

L. BACKGROUND

A. Introduction.

1.01 Since the early seventies, the Yemen Arab Republic (YAR) has been inthe process of transformation from a subsistence economy with a small externalsector to a relatively open market economy, propelled by considerableremittances. Recorded remittances peaked in real terms in 1977/8 whencontributing 40Z to GNP. Since then, the volume has fallen off in real terms,and amounted to US$1.3 billion or 26% of GNP in 1983. If non-recordedtransfers of cash and goods were accounted for, remittances would have beensubstantially higher, although the trend of diminishing importance over thelast 5 years would remain unchanged. So YAR's prosperity is presently partlyinfluenced by the economic fortunes of neighboring countries (in whichremittances are generated), particularly Saudi Arabia, and ultimately bythe world oil market. Oil and gas discovered in 1984 in YAR, could improve thecountry's economic prospects, depending on the volume and price of these andthe level of traditional foreign exchange receipts (workers' remittances andofficial aid). However, the uncertainties regarding these key parameters andthe country's great need for more and better public services, both call forefficient use of oil revenue, as well as caution in fixing growth targets andmanaging the external debt.

B. Major Development Issues.

1.02 Overall Performance. Overall economic performance in recent years hasbeen satisfactory; during the period 1976/77 - 1982 GDP growth averaged about51 p.a. Sectoral growth rates differed widely; agriculture which is thelargest single sector, expanded unevenly over the period at an average rate ofabout 11 p.a. (excluding qat). Wholesale and retail trade, and governmentservices, now the second and third largest sectors, registered annual growthrates of 161 and 14Z, respectively. Investment effort was impressive, averagingaround one-third of GNP. Nevertheless, YAR continues to be one of the world'sleast developed countries. Adult literacy and school enrollment rates arestill very low, whereas the shortage of managerial and skilled manpower is anoverriding constraint to development and severely limits the capacity of thepublic administration to implement an increasingly complex developmentprogram. Health indicators depict serious problems that call for increasedvolume and quality of services. YAR's physical infrastructure remainsunderdeveloped despite the fact that it has received the greater share ofpublic investment under the First and Second Five-Year Plans. Thus, althoughthe length of the main road network has tripled over the last decade, manyareas are still without adequate road connections. The rapid population growth(estimated at about 3X p.a.) necessitates that Government should startanalyzing recent demographic trends to reach a better understanding of itseconomic consequences in order to develop an appropriate policy.

1.03 Budget deficit. The budget deficit has emerged as a major concern inrecent years. Over the past five years, Government expenditures have increasedat more than double the pace of revenues. Whereas capital expenditures increasedby about 57%, recurrent expenditures grew by as much as 2801; provisionalestimates for 1983 suggest chat the latter were nearly twice the level ofcapital expenditures. By 1982, revenues represented only about 401 ofexpenditures and the budget deficit increased to 331 of GDP. At the same time,the share of the budget deficit financed by external loans dropped from an

- 2 -

average 44Z in 1977-81 to only 16X in 1982, which compelled the government toincrease its borrowings from the banking system (mainly the Central Bank). Thecontinuation of such a large budget deficit under these conditions would mostlikely result in higher inflation. Indeed, since 1982 inflation has increasedand is reportedly running presently at about 15Z p.a. (December 1984).

1.04 Reducing the budget deficit calls for; (a) restructuring publicinvestment expenditures according to priorities, and (b) bringing currentexpenditures under control, mobilizing more resources through taxes andestablishing adequate users' fees. Government is increasingly aware of theseriousness of the situation and has taken a number of measures to reducecapital and recurrent expenditures and raise revenues. Government did succeedin curbing the budget deficit in 1983, although it still represents as much as28X of GDP. Austerity measures have been equaLly succesful in improving theforeign exchange position; early 1985 reserves corresponded to about threemonths of imports, a substantial improvement over 1984. With the measurespresently in place this position is expected to be sustained, if not furtherimproved.

1.05 Against this background of government financial austerity, the optionsfor agricultural development, and especially the public sector's role in it,are constrained. Government will need to keep its direct investment in thesector to areas of critical need and encourage the private sector to use itsresources wherever feasible. For services already in operation to continuesuccessfully, Lurther development of user charges as well as tight budgetarycontrol will be required. Cost recovery and enhancing the efficiency of-existing support and maintenance services through cost control are importantissues when evaluating further public investment in the sector.

1.06 Exchange Rates: During tL'. decade 1973-83, the official exchange rateremained at YRIs 4.5 to the US dollar. With these two currencies risingagainst most other currencies, YAR import costs were considerably reduced, andduring the period 1980-'83 relatively cheap food imports may have acted as adisincentive to domestic production. In 1983, the increasing shortage offoreign exchange in YAR led Government to lower the official exchange rate. Aseries of exchange rate changes from November 1983 to August 1984 caused theYemeni Rial to be devalued by 21.6Z to YRls 5.74 to the US dollar.Nevertheless, by November 1984, a substantial difference between the officialand the market exchange rate had developed and the December 1984 exchange ratFfor importers was about YRls 6.5 per US dollar.l/ Currently the marketexchange rate is YRls 6.7 per US dollar, and the effective exchange rate aboutYRls 8.0 per US dollar (base year = 1984). In proposing an agriculture sectorstrategy, it is assumed that a realistic exchange rate policy would continue tobe followed, and that agricultural imports would not be seriously undervaluedrelative to domestic production.

C. Agriculture in the Economy

1.07 YAR agriculture (excluding qat production) was estimated 2/ in 1982to have generated a value added of YRls 3.7 billion (US$0.8 billion), which

1/ This became the official exchange rate on February 11, 1985.2/ Central Planning Organization.

accounts for about one-quarter of GDP. Because of relatively high prices fordomestic agricultural products, however, the sector's value added would beless if it were evaluated in economic (border equivalent) prices, perhaps byas much as 60X. According to the mission's estimates, agricultural valueadded at domestic prices of qat production is approximately US$0.9 billion, orabout the same as that of the sector excluding qat (US$0.8 billion). Hence,the sector's share in total GDP is about 40% when qat is included. The factthat this locally produced and consumed stimulant accounts for about half ofsector value added (and is hardly reflected in the national accounts) is oneof the most unusual Eeatures of YAR agriculture; this has been elaboratedbelow (paras 3.17-3.22).

1.08 The sector employs about 701 of the resident work force. As 0.5million males from rural areas are estimated to be abroad (1982), and anadditional 0.1 million males from the agricultural areas work for much of theyear in YAR's urban areas, females predominate in the agricultural labor forceand frequently make important production decisions. However, the overallagricultural labor supply is, in the aggregate, substantially in excess ofrequirements (para 2.15), though at peak times, local shortages certainlyoccur. It follows that, in such circumstances, average labor productivity iscomparatively low.

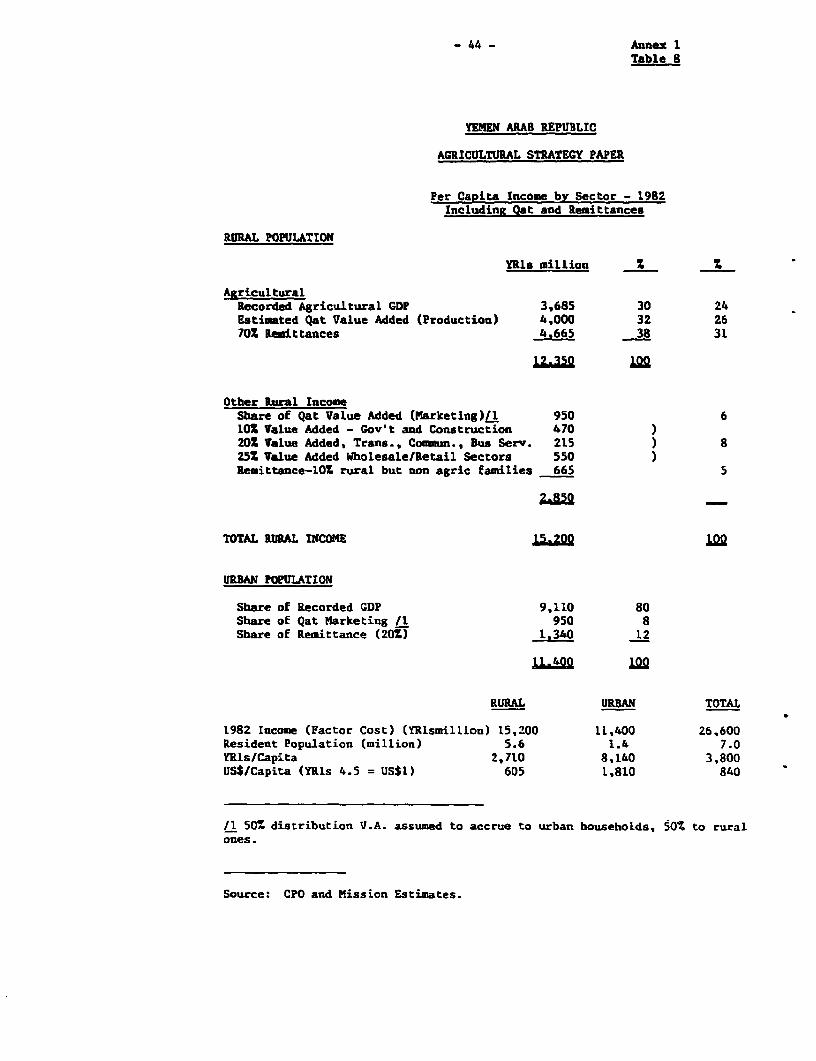

1.09 Rural and Urban Incomes. Estimates of the overall rural/urban incomestructure are presented below. Of rural income, an estimated 321 comes fromqa., 241 from other agriculture, 301 from remittance and 10i from othersources. Because of the very substantial importance of both qat andremittances in the rural economy, large changes in these sources of revenueswould, of course, alter the present situation significantly.

Tahlp 1 .1 - RURAL AND URBAN INCOME ESTIMATES (1982)

Rural Urban Total- (YRls million) - - - - -

Share of Recorded GDP 3,685 9,110 12,795Qat Value Added /1 4,000 - 4,000Remittances 4,665 1,340 6,005Others 2.850 950 3.800Totals 15,200 11,400 26,600

/1 Annex 1, Table 11Source: Annex 1, Table 8.

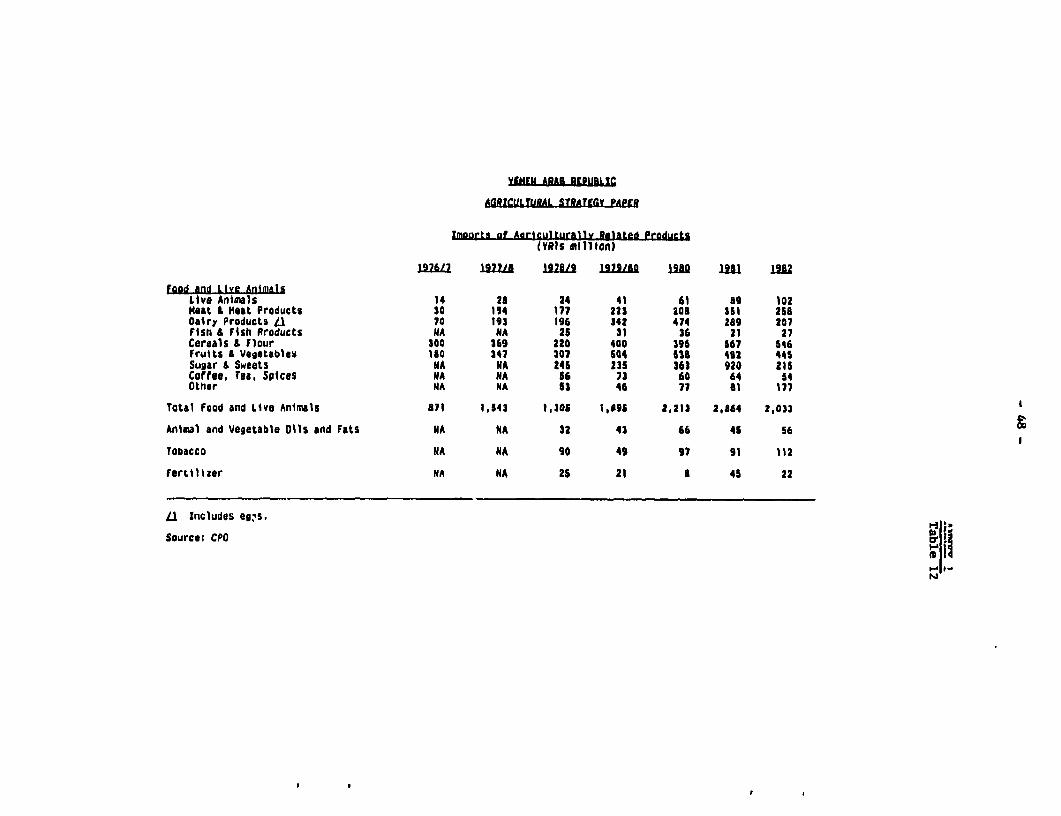

1.10 Agricultural Trade. The rapid increase in demand for foodstuffscaused by the high levels of workers' remittances, together with the high rateof population growth, has not been met by a corresponding increase in domesticproduction (para. 2.01). Consequently, food imports rose rapidly during thelast decade to US$450 million in 1982 1/, corresponding to about 301 of allmerchandise imports. Animal products, cereals and cereal products, as well asfruits and vegetables accounted each for about one-fifth of total foodimports, the balance consisting of sugar, vegetable oils etc. (Annex 1,Tables 12 and 13). Agricultural exports, always small, have now fallen to aninsignificant level.

1/ More recent estimates were not available to the mission.

I. AGRICULTURAL SECTOR

A. Agricultural Performance

2.01 In countries like YAR, sector performance is, of course, closelyrelated to rainfall. In the absence of reasonably long time-series for eitherparameter, it cannot be determined to what extent adverse weather conditionsconstrained growth. Agricultural performance In the last decade varied bysubsector, but overall growth averaged only 1Z p.a. over the period1970/71-1982. Over the period 1975/76 to 1983, the absolute level ofagricultural sector GDP (excluding qat) stagnated, and partly as a consequenceof that, reported agricultural sectoral GDP, which excludes qat, fell in thesame period from 452 of total GDP at factor cost to 25X. Comparing thetwo-year period, 197516 and 1976/7, with the two-year period 1982 and 1983,agricultural GDP growth for the six and a half year interval totalled 112 inconstant 1975/76 prices, but declined by 92 if current prices deflated by theGDP deflator are appLied (Table 2.1). This latter figure is probably the moreappropriate, as it expresses agricultural value added in terms of the wholebasket of national goods; it indicates that agricultural prices relative toother prices declined in real terms over that period.

2.02 The agricultural statistics, though perhaps unreliable in absoluteterms, are useful indicators of the direction in which the sector has moved.These indicate that total cropped area increased from the early to the mid'70s, but declined since (see Annex 1, Table 1). The reported cropped area ispresently some 232 below the peak recorded figure of 1974/5. The main areacontraction has been in cereals, with a much smaller area reduction of therather insubstantial export crops, coffee and cotton.

2.03 The major recent shifts in land use were caused by productivitydifferences between crops. Marginal cereal areas went permanently out ofproduction, especially on tenant-operated farms in low rainfall areas.Simultaneously, a substantial substitution of very profitable qat and fruitand vegetable production for cereals took place in high rainfall and irrigatedareas, generating substantial growth in output of these commodities. Togetherwith the contraction in the cereal area planted, estimated production hasfallen (Annex 1, Table 4), although the very low figures for 1983 and theexpected low figures for 1984 are results of extreme drought conditions. Onthe other side, significant improvements in overall yield levels have beenachieved in some instances (Annex 1, Table 3). Cereal yields which were below0.8 ton/ha during the three year period 1971/72 to 1973/74, were above 0.95ton/ha in 1979/80 through 1981. Similarly, potato yields appear to have risenfrom around 11 ton/ha in 1971/72 to 1973/74 to over 12.5 ton/ha. The evidenceof these overall yield figures is supported by information coming from IDAprojects, e.g., the Southern Uplands Regional Development Project and projectsin the Tihama region, which indicates substantial increases in yields on farmsparticipating in those projects. It is therefore quite possible that, once anormal rainfall year occurs, the benefits which are already being seen at theproject level, will be better reflected in the aggregate figures.

2.04 Import figures which are probably much more reliable than sectoralGDP estimates, indicate sharp increases in food imports over the past sevenyears. This confirms that agricultural sector growth has lagged behind thegrowth in demand for food. Table 2.1 shows the trends of both agriculturalvalue added and food imports over the past few years. The average food import

- 5 -

level in 1981 and 1982 was 42Z higher than that in 1976177 and 1977/78. Thevalue of imported foods and live animals in 1981 and 1982 was equivalent toabout 40X of agricultural value added (excluding qat), compared to aboutone-third in 1976/77-1977/78. Grain imports in the last 3 years were somewhatabove 500,000 tons (incl. flour). In 1984, food imports, in relation toagricultural value added, would probably have been still greater.

Table 2.1: FOOD IMPOPTS AND AGRICULTURAL iALUE ADDED /a

1975/6 1976/7 1977/8 1978/79 1979/80 1981 1982 1983(YRis Million)

Food and LiveAnimal Imports

- Current Prices NA 871 1,543 1,305 1,895 2,864 2,033 NA- Deflated by

GDP Deflator NA 698 1,056 777 1,040 1,513 985 NA(to 1975/6 prices)

Agricultural ValueAdded

- Current Prices 2,011 2,313 2,409 3,049 3,458 3,685 3,799 3,596

- Deflated byGDP Deflator 2,011 1,853 1,649 1,815 1,898 1,947 1,840 1,670(to 197;/6 prices) -

la Includes agriculture forestry and fisheries.

Source: CPO

2.05 The above mentioned aggregate numbers do not reveal, in general, theconsiderable pregress made, both at the project level, as well as iu overallsector management and in the provision of supporting services, e.g. research,extension and credit. The PPAR's of both the first Southern Uplands RegionalDevelopment Project and the Tihama I Project indicate that all major objectiveshave been achieved. Most ongoing IDA-assisted projects in agriculture areprogressing satisfactorily. A sumnmnary account of completed IDA-assistedprojects in YAR is in Appendix B.

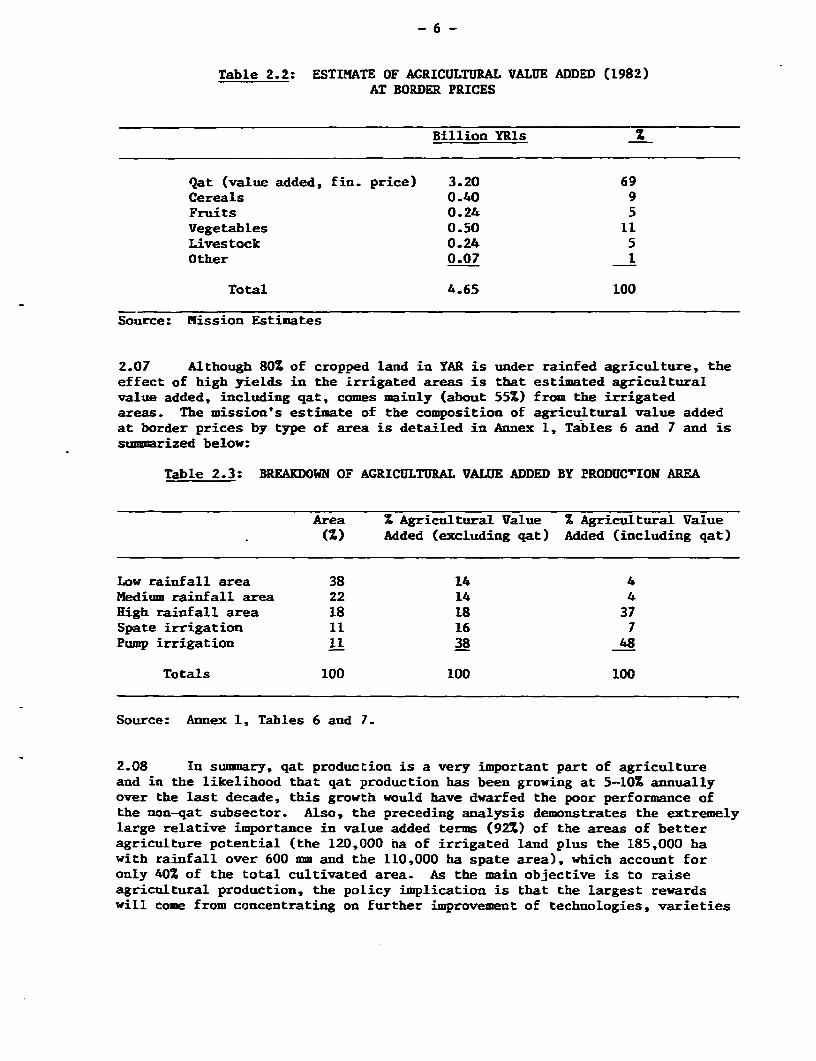

2.06 Sector Value Added and Qat. Any analysis of the agricultural sectoris incomplete without considering qat. Estimates of rural per capita incomegiven in Annex 1, Table 8, indicate that only about 30Z is generated by non-qatagricultural production, with some 38Z coming from remittances and 32Z fromqat. A re-estimate of agricultural sector GDP for 1982 indicates that, atdomestic prices, sector GDP would more than double if qat were included; viz.an increase from 3.7 billion YRis to 7.7 billion YRis (see Annex 1, Table 6),with qat providing 52X of sector value added. At border prices, however,agricultural GDP would be substantially lower (domestic prices of agriculturalproducts are substantially above border prices, viz. para 3.02). At thoseprices, estimated agricultural sector value added would be as follows.

Table 2.2: ESTIMATE OF AGRICULTURAL VALUE ADDED (1982)AT BORDER PRICES

Billion YRls Z

Qat (value added, fin. price) 3.20 69Cereals 0.40 9Fruits 0.24 5Vegetables 0.50 11Livestock 0.24 5Other 0.07 1

Total 4.65 100

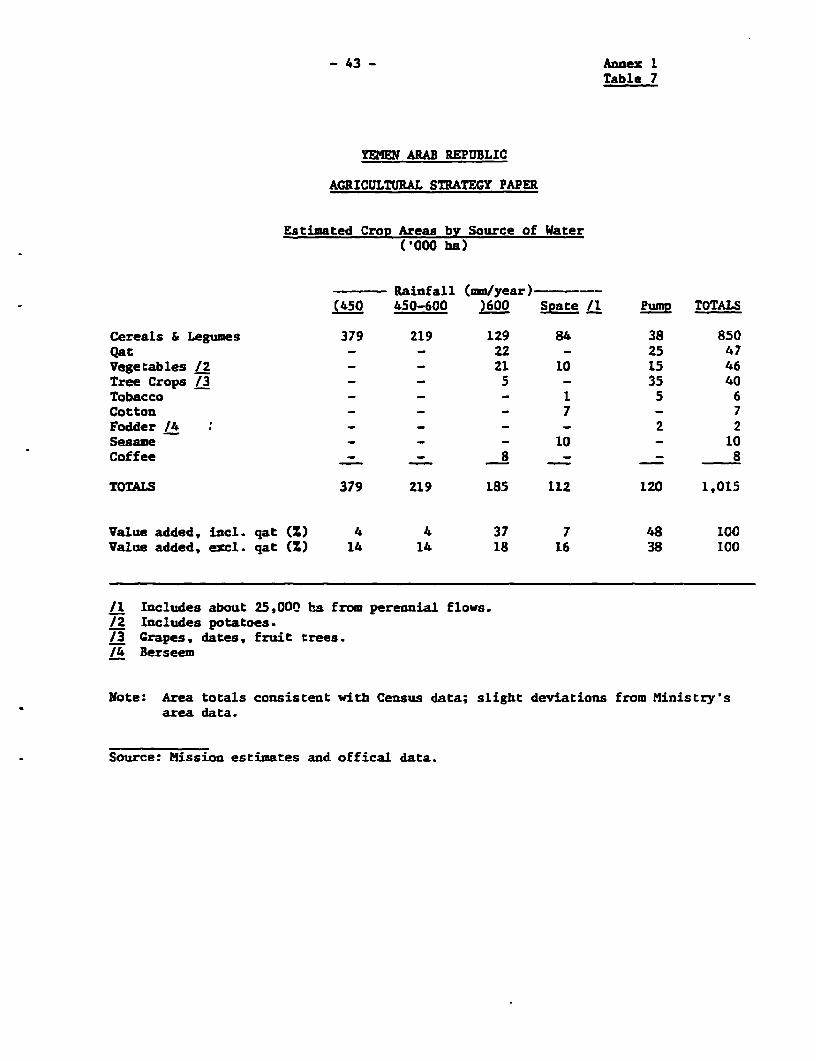

Source: Mission Estimates

2.07 Although 80X of cropped land in YAR is under rainfed agriculture, theeffect of high yields in the irrigated areas is that estimated agriculturalvalue added, including qat, comes mainly (about 55Z) from the irrigatedareas. The mission's estimate of the composition of agricultural value addedat border prices by type of area is detailed in Annex 1, Tables 6 and 7 and issuimmarized below:

Table 2.3: BREAKDOWN OF AGRICULTURAL VALUE ADDED BY PRODUC`ION AREA

Area Z Agricultural Value X Agricultural Value(X) Added (excluding qat) Added (including qat)

Low rainfall area 38 14 4Medium rainfall area 22 14 4High rainfall area 18 18 37Spate irrigation 11 16 7Pump irrigation 11 38 48

Totals 100 100 100

Source: Annex 1, Tables 6 and 7.

2.08 In summary, qat production is a very important part of agricultureand in the likelihood that qat production has been growing at 5-10X annuallyover the last decade, this growth would have dwarfed the poor performance ofthe non-qat subsector. Also, the preceding analysis demonstrates the extremelylarge relative importance in value added terms (921) of the areas of betteragriculture potential (the 120,000 na of irrigated land plus the 185,000 hawith rainfall over 600 mm and the 110,000 ha spate area), which account foronly 40% of the total cultivated area. As the main objective is to raiseagricultural production, the policy implication is that the largest rewardswill come from concentrating on further improvement of technologies, varieties

- 7 -

and methods of operation in these very areas (which also have the highestrural population density). For low rainfall areas without irrigationpotential (for which virtually no extension packages are available) supportfrom the standpoint of human well being may be needed. It is unlikely,however, that productive improvements here can make a major contribution torapid sector growth.

B. Resources and Constraints

Land and Water

2.09 Of the 20 million ha of land in YAR, more than three-quarters istotally unsuited to agriculture, and a further 3.5 million ha is not used foragricultural purposes because of the water constraint, although the sparsebush vegetation in this area is utilized to some extent by livestock. Most ofthe cultivated area is owner-occupied, though a significant proportion,estimated at 10-15Z, is operated under some form of share-farmingarrangement.

2.10 Land. The intrinsic quality of agricultural land varies considerablyby region. It is influenced primarily by topography, elevation and soils.However, given the climate of YAR, the overriding factor determining theeconomic usefulness of agricultural land, is the availability of water.According to surveys undertaken during the 1970s, the potential agriculturalarea in TAR appears to have been about 1.5 million ha. However, this isprobably an overestimate of the area effectively available in 1985, asconsiderable abandonment of terraces occurred in the interval, mostly inlow-rainfall areas where cereal production (especially under sharecroppingarrangements) became increasingly unattractive as wages rose. The 1983Statistical Yearbook 1/ figures indicate that the cropped area declined froman average of 1.32 million ha in 1973/4 - 1975/6 to 1.06 million ha in 1981-1983.- Cropped area at any time is, of course, a function of rainfall andfinancia'l incentives, as well as the size of the effective land resource. Themission estimates the aggregate agricultural land area in TAR to bedistributed follows (detailed in Annex 1, Table 7).

1/ CPO publication.

Table 2.4: DISTRIBUTION OF AGRICULTURAL LAND(Million ha)

Rainfedless than 450 mm (incl. fallow

land) 0.71450 - 600 mm 0.22Over 600 mm 0.19

Total rainfed 1.12

IrrigatedSpate Irrigation 0.11Pump Irrigation 0.12

Total Irrigated 0.23

Total Agricultural Land 1.35

Source: Agricultural Census 1983 and mission estimates.

- 8 -

2.11 Land Tenure. It is often observed that the land tenure situation inYAR is a considerable obstacle for sector development; this is not fullysupported by the recent census results which indicate that over 80X of allfarm land is owner-operated (Table 2.5). Holdings are considerably fragmented,with an average of 4.6 parcels per farm. Because of unusually large variationsin microclimates on steep slopes, however, the general disadvantages of suchfragmentation are in many areas of YAR perhaps balanced by the advantage ofrisk spreading.

Table 2.5: YAR NATIONAL AGRICULTURAL LAND TENURE

Number of Holdings(X) Area of Holdings (Z)

Holdings with One Type of Tenure

Owned 66 77Share Cropped 10 3

Holdings with more then One Typeof Tenure

More than 50Z Owned 14 13Less than 50Z Owned 9 6

Others (Rented etc.) 1 1100 100

Source: Agricultural Census 1983

2.12 Water. Water for agriculture comprises: (a) rainfall; (b) spatesduring heavy surface runoff; (c) base flow in wadis generated from saturatedslopes in highlands and springs; and (d) groundwater from the aquifer. Theagricultural development projects undertaken by the Government to date, withIDA's assistance, were designed as a first step to efficiently manage theknown amounts of surEace water at the source as well as groundwater.Considerable scope exists to further decrease water conveyance and applicationlosses, and thus increasing irrigation efficiency by means of improvedpractices and modern techniques.l/ However, additional irrigation developmentrequiring more water than presently known should await the results of studiesleading toward a water master plan (para. 2.14). Such measures should,therefore, continue to be taken until all irrigated areas have been fullydeveloped.

2.13 The impounding and storage of occasional runoffs in high rainfallareas had been practiced in the past as is evidenced by the existence ofseveral old dams in YAR which are intact even today, though not operativeanymore. The reservoirs of these very old dams have been filled up withsediments resulting in fertile lands on the surface. The deposited alluviumhas created a subsurface storage of ground-water used for irrigation which getsrecharged through seepage of the runoff retarded above the dams. Similardams, of small sizes involving low investment costs, could still beconstructed or the existing ones rehabilitated for conservation of water,

1/ 25-30X as estimated for the present to 50-55X in the future.

-9-

provided such projects would be financially viable and economicallyattractive. However, any substantial investment for large storage dams shouldbe considered only after full investigations based on reliable and sufficientdata, on internationally accepted standards, have been made of thehydrological, geological and environmental aspects to prove the technicalsoundness oE a project.

2.14 The potential for the development of water resources in YAR existsin: (a) efficient management of surface water; (b) use of runoff to rechargethose zones of the aquifer which are subjected to pumping; (c) possibletransbasin diversions; and (d) surface detention of the runoff by checkdamsto: (i) reduce erosion in the watershed, (ii) increase base flows in the wadisfor perennial irrigation, and (iii) reduce spillage into the sea and thedesert. The assessment of the above potential requires in-depth studies ofwater resources in all regions of YAR.

2.15 At present, aside from project related studies, the only large-scalewater resources study being carried out concerns the Tihama region. In orderto fully understand the water resources development potential in YAR, it isrecommended that similar studies be carried out for al1 regions of the countryand which should form the basis for a water master plan for futuredevelopment.

2.16 Manpower. The agricultural labor force in YAR has been substantiallyreduced over the past decade by emigration to Saudi Arabia and other oil richstates. The associated flow of remittances has led to high domestic wages,probably as a result of the reservation wage effect, rather than widespreadlabor shortages or relatively high marginal productivity in the sector. Ananalysis of available agricultural labor and of the likely aggregate sectorlabor requirements (Annex 1, Tables 9 and 10), suggests that averageperson-day equivalent requirements for agriculture amount to about 60person-days for every 275 person-day available; even accounting for seasonalpeak labor demands, this is low. It indicates that in the aggregate, laboravailability is not a serious constraint to agricultural development as isoften alleged, though local shortages in peak periods certainly occur.2/ Thisanalysis is summarized below.

Table 2.6: DEMAND FOR AGRICULTURAL LABOR

Total Person-daysCropped Average Person-days needed perArea Requirements needed effective('000 ha) (days/ha) (million) worker/year

Crop production 1040 54 57 41Livestock NA NA 23 16Total Agric. Labor Demand 80 57

Source: Mission estimates (Annex 1, Tables 9 and 10).

2/ The slow-down in the economies of oil countries may also cause theirdemand for labor to ease.

- 10 -

2.17 Agricultural labor supply is estimated at the equivalent of 1.4 millionafter adjusting for; (i) 501 of the agricultural population of 5.4 millionbeing economically active; (ii) 0.6 million males being away; and (iii) thefact that women's work in agriculture is restricted by custom, household dutiesetc., resulting in their being the equivalent of 501 effective for agriculture.The existence of a large number of women and children who could, if necessary,help at peak times, strengthens the argument that labor availability is not amajor constraint to agriculture. However, unless the cost of labor dropssharply, the very high wage rates (US$10 - US$15 per day) relative to the lowlevels of agricultural productivity must be an inhibiting factor in thedevelopment of commercial agriculture. A modest decline in real wages isexpected for the medium-term (para. 4.01).

C. Present Sector Strategy

2.18 The Second Five-Year Plan document describes the thrust of the presentstrategy as to achieve a reasonable level of food security by modernizing theagricultural sector. More specifically, the strategy comprises the followingmain elements:

(i) Emphasizing mult-component rural development as a means ofraising production and improving living conditions of the ruralpopulation;

(ii) Encouraging the establishment of cooperatives that protect theinterest of the farmers by providing them with agriculturalinputs at low cost, and helping them market their products;

(iii) Creating strategic buffer stocks of staple crops and completingbasic infrastructure along with adopting a price policy thatsupports domestic production and rationalizes consumption;

(iv) Developing agricultural services, with special attention tocredit, agricultural research and extension, marketing,veterinary and other services, to assist farmers, particularlysmall farmers; and

(v) Increasing the efficiency of present water use, mobilizing provenpotential water resources and conducting surveys of resources.

2.19 Whereas modifications of this strategy will be proposed in Chapter IV,some main comments can be summarized as follows. First, there appears to be aninclination towards increasing Government intervention which may perhaps extendto input subsidies. This appears undesirable considering; (i) Government'smodest operational capabilities; (ii) the fact that virtually all productprices are well above import parity levels; and (iii) the undesirability ofsubstantially increasing farm subsidies in view of the large Government budgetdeficit. Second, public sector finance constraints constitute a strongargument against emphasizing generally expensive integrated rural development,as opposed to directly productive investments in areas with potential foragricultural development. Third, the present food security measures do notreflect the rapid changes in consumption patterns, nor do these take fullaccount of the fairly efficient traditional food security system in thecountryside (para 2.31). Food security is essentially a public sectorresponsibility; its execution, however, should continue to rely, to the extentpossible, on the private sector.

- 11 -

D. Publie Sector Investment Under the Second Five-Year Plan (SFYP)

2.20 Originally the public sector investments for the SFYP period 1982-'86were planned as follows:

Table 2.7: AGRICULTURAL SECTOR INVESTMENT PROPOSALS UNDERTHE SECOND FIVE-YEAR PLAN (1982-1986)

Subsector YRls million S

Irrigation (mainly spate) 951 39- of which TDA a/ (456) (19)Rural Development 314 13Livestock 300 12Crop Production Projects 279 11Research & Extension 217 9Institution Building 118 5Others 236 11

Totals 2.4 100

a/ Tihama Development Authority

Source: 2nd FYP Document

2.21 Proposed public sector agricultural investment for the SFYPcorresponded to 13Z of total planned public investment. As particularlycategories such as irrigation and rural development often include elements ofinfrastructure, research, extension and institution building, the breakdowngives only very global information about the distribution of planned sectorinvestment.

2.22 In 1982, the growing budget deficit called, among others, forreduced capital expenditure. Government conducted a public investment reviewand requested IDA to assist in this effort (Report No. 4821-YAR). Thereport's major recommendation, viz. to reduce total investment by about 112has, by and large, been accepted by Government. After revision, agriculture'sshare remained at 13X, despite reductions in activities which could beundertaken commercially, deferrals of some of the costly rural developmentprojects, and consolidation of various smaller projects. Approximately 752 ofplanned investments are for IDA-assisted projects. Though actual capitalexpenditures for public sector development have risen rapidly in recent years(doubling between 1981 and 1983), they are still about one-quarter belowplanned amounts, thus reflecting constraints regarding absorptive capacity.In summary, limited absorptive capacity is likely to limit public expendituresfor sector development to levels commensurate with available resources.

- 12 -

E. Sector Policies

2.23 High commodity prices are generally less the result of directGovernment intervention than of high factor prices (e.g. labor, and pumpedvater), as well as of substantial market imperfections generally associatedvith an early development stage (inefficient marketing, high transportcosts). Indeed, direct government intervention in YAR is still limitedcompared to many developing (or developed) countries.

2.24 ReLiance on Private Sector. While the private sector is far fromperfectly competitive (e.g. transportation cartels), the high growth centersin agriculture, such as relatively high technology poultry or vegetableproduction, as well as marketing services, have been the product of private,rather than government, initiatives. Overall, there is a large pool ofentrepreneurial capacity in YAR, as well as a reasonably capitalized andcapable private sector. The latter dominates all aspects of the foodmarketing pipeline, as well as the provision of inputs (including feed andsmall-scale irrigation capital goods). This orientation partly reflects therather limited administrative capacity of the public sector agenciesinvolved. Further, merchants have been important supporters of the regime,and are able to influence policy changes that would affect their livelihood.

2.25 Government and Imports. Government has a direct involvement in atleast one critical aspect of agriculture, i.e., managing the flow of foodimports. The Ministry of Supply has responsibility for overall planning, on arolling annual basis, of strategic commodity imports through tenders that localgovernment agencies or private firms bid on (this system includes a pricestabilization and cross-commodity subsidy element for wheat, rice, flour andcement). The Ministry of Supply controls the prices for all these strategicimports and fixes relatively attractive profit margins for importers, whole-salers and retailers. The actual quantities, and hence profits, are alsoallocated among the various government agencies and private traders by thisMinistry. On food security grounds, 40% of all strategic food imports arereserved for four government companies, which compete with private importersand maintain also their own retail networks (although normally most of theirallocation is ultimately sold through private retailers). In addition tothese controls over strategic commodities, Government supervises feed imports(that arrive in bags, thus adding 20X-402 to their CIF cost), while meat andlivestock imports are subject to restrictions which partially explain highdomestic meat prices.

2.26 Transportation. Market imperfections, associated with poortransport infrastructure, are amplified by private freight controls whichallocate transport service to small owner/drivers on a first-come first-serve,fixed-price basis. In effect, these measures have led to the creation of atransportation cartel, as a consequence of which cost of transport isrelatively high, while creating at the same time excess freight capacity.While there are no data available to estimate the cost of such high tariffsand over-capacity to the nation, it is believed to be significant. In termsof agricultural prices, a more competitive system could significantly increasepurchaser incentives, while reducing prices paid by consumers.

2.27 Taxation. The general principle applicable to the sector is that ofa religious tithe (zakat), corresponding to 5Z of gross value of production

- 13 -

for well-irrigated areas and 10% on all other land (for qat, see next para),Government revenue data indicate that actual revenues fall considerably shortof projected ones (it is estimated that in 1982, receipts were only aboutone-third of what they should have been). Whereas privately pumped water isnot taxed at all, the cost recovery principle in publicly financedspate-irrigation schemes (i.e. the IDA financed Tihama projects) is to recoverfull capital costs in real terms, but with no interest, over 50 years, as wellas to cover full operation and maintenance costs. Collection is generallymeant to be through zakat and a surcharge of abou'l 2% of gross value ofproduction. According to the Tihama Developement Authority (TDA) management,this surcharge has, as yet, not been collected in schemes already completed.However, Government has recently issued a decree to that effect (April 1984).and the Ministry of Finance has been instructed to collect the surcharge tax.

2.28 Though the excise-tax on qat increased by about 150% p.a. in thelast four years, the potential of this tax appears to substantially exceed itsactual yield. The tax is an ad-valorem one of 10% (recently increased to12%), to be collected at central urban markets and check points on roadsleading into major citris. Actually, only part of urban consumption ispresently taxed, while rural consumption remains virtually untaxed.

2.29 Subsidies. At present, agricultural credit through the Cooperativeand Agricultural Credit Bank (CACB) is subsidized to the extent of three tofive percentage points. CACB lowest agricultural loans are at 9-10% comparedwith a market rate of about 15%, whereas inflation in 1984 was about 11%.

F. FoodSecurity

2.30 The recent changes in YAR's economy, particularly the rapid growthin real incomes, have had a substantial impact on food security. Whileimportant nutrient deficiencies still exist, the overall problem is no longerone of inadequate purchasing power, but rather of nutritionally ill-balancedsupplies. Indeed, the overall food consumption pattern and associated tradeflows are now approaching to those found in many middle-income countries,i.e., YAR currently spends more on non-grain imports (particularly animalproducts) than on food grains. This diversification of food imports is, initself, a major factor in reducing real or perceived risks associated withoverall food supply.

2.31 Local structures of production and marketing have, in general, notchanged as dramatically as consumption. In response to often adverse weatherconditions, farming is still organized to minimize risk, rather than maximizeoutput. As a result, on-farm or village carry-over (buffer) stocks are large,up to one year of a good year's harvest; traditional storage facilities aregenerally ample. Existing stocks held outside government control appear tohave been sufficient to prevent serious problems in drought years. This wasclearly demonstrated in recent years, when domestic grain output fell wellbelow the trend because of drought, whereas grain imports remained at aboutthe same level (somewhat above 500,000 ton/yr) and domestic grain prices(ex-farm) remained at about the same levels.

- 14 -

m. ISSUES. CONSrRAEITS AND RECOMMENDATIONS.

A. The Economics of Crop Production and Price Incentivesfor Different Crops

3.01 Overview. In general, the price structure in YAR is such thatreturns to most crops are substantially more attractive in financial termsthan when expressed in economic prices, and hence, existing price incentivesare, in the main, adequate. The fundamental problem is high resource costs,particularly pumped water, while physical performance potential is relativelylow. Hence, it is extremely difficult for agriculture to be profitable in theabsolute sense.

3.02 Product Prices. As a result of various market imperfections (e.g.import regime, freight cartel) and local preferences, prices of agriculturalproducts in YAR are substantially above their estimated border prices. InTable 3.1 below, estimated economic prices (detailed in Appendix A) arecompared with financial prices used in the appraisal reports of the last twoIDA agricultural sector projects in YAR and in the identification report ofthe proposed SURDP III project. During the mission's November field visit, itappeared that financial prices had, in fact, risen from these levels. Thefigures, which typically show domestic prices to be two to three times theborder level, indicate that strong price incentives are already available tothe agriculture sector. In the aggregate, quite modest agricultureperformance appears to have occurred in spite of generally very favorableproduct prices in the sector. Nevertheless, production of some irrigatedcrops (potatoes, vegetables, grapes) was expanded significantly because offavourable prices.

Table 3.1: PRICES FOR AGRICULTURAL PRODUCTS(YRls/kg)

Estimated Financial PricesEconomic Prices /a Wadi Jawf Center. H.L. SURDP III

1984 1984 1983 1983

Sorghum 1.07 2.80 2.40 2.85Maize 1.13 - 2.40 2.42Wheat 1.14 3.30 2.80 2.00Sorghum Stover 0.27 0.50 0.40 0.95Maize Stover 0.28 - 0.50 1.00Wheat Stover 0.28 0.60 0.50 1.07Alfalfa (green) 0.27 /b 0.80 0.60 0.60Potatoes 1.3 2.50 1.50 2.64Oranges 3.0 3.50 4.00 4.00Onions 1.6 NA NA 1.30Vegetables NA NA 2.0 NACotton 3.8Lamb /c 5.6 20Chicken /d 8.0 17

/a At the December 1984 market exchange rate of YRls 6.5 to US$1./b Assumed 25% dry matter (DM): On DM basis worth 80% of wheat./c Live weight assuming 45% carcass weight/d Carcass weight.

- 15 -

3.03 Water Costs. Water costs depend on source. Until now, spate irriga-tion in Government-supported schemes, costing about US$15/l,OOOm3, has beenfree to farmers (para. 2.27); Government, however, recently issued a decree tocollect charges and TDA has been instructed to collect these. For privatelypumped water, costs amount to about US$60/l,OOOm3. or about US$750/ha.Against this cost structure, it is generally not possible to produceprofitably low-value crops, such as cereals or pulses with pumped water.

3.04 Other Input prices. Given the generally low level of physical produc-tivity, daily labor costs at YRls 85 (US$13) are clearly very high. Althoughfamily labor is important, hired labor is used in varying proportions on about80X of the land. It is estimated that, in the aggregate, about half of allagricultural labor is hired, mostly on a daily basis. The price of hiredanimal power is also high at YRls 100-150/day (US$15-22), and is caused by;(i) the high price of labor, which is included in the daily cost of a hiredanimal team and (ii) the high value of livestock brought about by effectiverestrictions on livestock imports and strong domestic demand. The cost oftractor mechanization at YRls 100/hr (US$15) for a 60-horse power tractor plusimplements does not seem excessive, given high maintenance costs and ofteninefficient use. This cost probably reflects the fact that there is anover-supply of agriculture tractors in various parts of YAR.

3.05 Most other inputs, fertilizers, sprays, etc., are generally priced atlevels comparable to import parity prices. Importation of fertilizer byGovernment at negligible cost appears to be offset by excess profits in themarketing chain. Imported animal feeds are expensive, partly because shippingis in bags rather than bulk, and probably because of a monopolistic supplysituation. Input prices vary substantially by region and by project, as someof the hilateral donors sometimes have different policies regarding thepricing of inputs to farmers. This, in itself, has a distortionary effect andit is important to rationalize these procedures through better donorcoordination (para. 4.15).

3.06 Crop budgets. Unit budgets, at both financial and economic prices,have been prepared for major crops in various ecological zones of YAR(Annex 1, Tables 16-21). These budgets are based on with-project assumptionsand taken from Staff Appraisal Reports and Preparation Reports for variousIDA-assisted agricultural projects in YAR. Therefore, the figures representachievable potential, rather than present performance. Analysis of thesebudgets provides useful indicators of what crops in specific ecological zonesare financially attractive and provide acceptable potential economic returns,assuming a reasonable level of technical performance. From the analysesundertaken in the SURDP projects and the various Tihama projects, it wouldappear that present aggregate levels of performance, in terms of laborproductivity and output per hectare, average around 30X below the figures inthe budget estimates presented here.

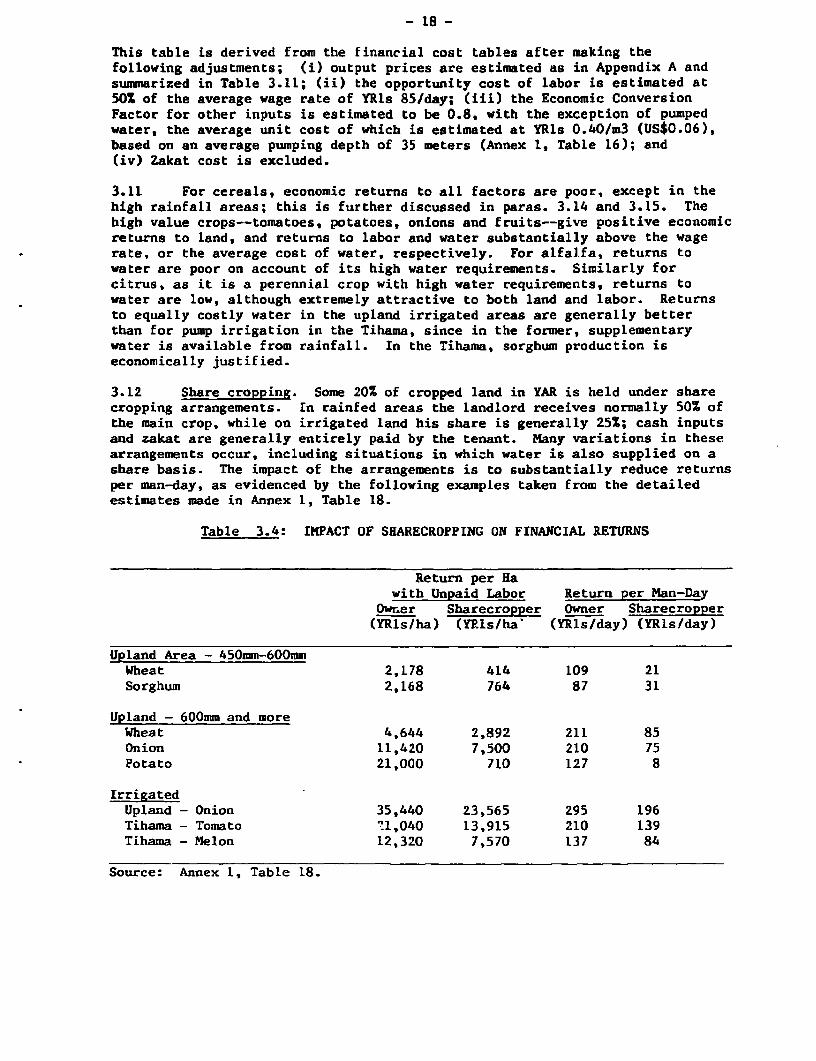

3.07 Financial Returns A summary of the financial returns for selectedcrops to land, labor and water are set out in Table 3.2 below. (details inAnnex 1, Tables 18-20). As is to be expected under the YAR price structure,these returns are generally substantially more attractive than those based oneconomic prices.

- 16 -

Table 3.2: SUMMARY OF NET FINANCIAL RETURNS FOR SELECTED CROPS

Rainfed Rainfed Upland TihamaArea (450mm-600mm) (600mm & more) Irrigated Well Spate

Returns to Land - …- … i ls/ha…----------------------------

Sorghum 43 2,486 Negative 4,469 1,447Wheat 478 2,774 125 - -Maize - 2,934 1,950 - -

Potato - 3,770 11,970 - -Onion/Tomato - 12,500 (0) 25,240/9,940 12,540 (T) 13,125 'O)Alfalfa - - 11,370 - -Cotton - - - NegativeCitrus - 27,070 - -

Returns to Labor -----… -------- YRls/man-day- ----------

Sorghum 87 168 78 145 107Wheat 109 211 89 - -Maize - 183 134 - -

Potato - 127 205 - -Onion/Tomato - 210 (0) 295/184 210 (T) 199 (0)Cotton - - 33Alfalfa - - 161 - -Citrus - - 424 - -

Returns to Water -- YRls/m 3 ----- …

Sorghum - - 0.35 0.43 0.23Wheat - - 0.39 - -Maize - - 0.56 - -Potato - - 1.38 - -Onion/Tomato - - 1.21/2.48 1.04 2.07Cotton - - - - NegativeAlfalfa - - 0.75 - -

Citrus - - 1.39 - -

Source: Annex 1, Tables 18-20.