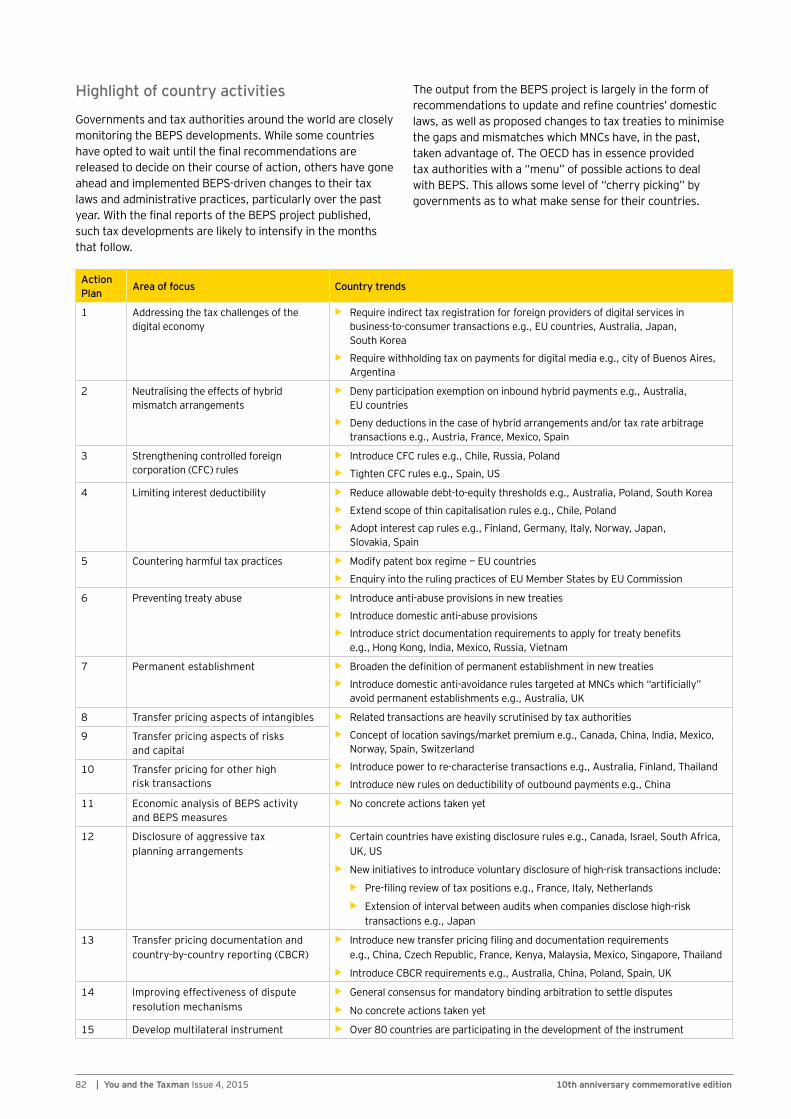

you and the taxman - issue 4, 2015 - ernst &...

TRANSCRIPT

You and the Taxman Insights on tax issues that matter Issue 4, 2015

anniversary commemorative edition

10th

Abo

ut10 years50 issues400 articles156 thought leaders

From insights into current and emerging tax issues to practical tips for tax planning and tax risk management

A unique publication written by EY’s tax professionals that’s about You and the Taxman

Cutting edge thought leadership

Diverse range of topicsYour resource for the latest tax trends and issues

1You and the Taxman Issue 4, 2015 |

Issue # – Month Year

110th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Abo

ut You and the Taxman had its roots as a weekly tax column by EY in The Business Times. Running for a year from September 2004 to August 2005, the column provided tax tips and updates on tax issues of the day.

After the end of the column’s run, EY’s then Head of Tax — Pok Soy Yoong — decided to turn it into a magazine as a continued showcase of EY’s tax thought leadership and in-depth knowledge on tax matters. The publication was to include practical and up-to-date analysis and commentary of tax issues and trends. To the best of our knowledge, we were the only Big 4 firm at that time to publish a full-fledged tax magazine.

A small committee was formed to chart the direction of the magazine, brainstorm topics, assign writers, allocate resources and sort out logistical issues — in short, to get the magazine up and running as soon as possible.

The inaugural bi-monthly issue was published in November 2005. The magazine was subsequently changed into a quarterly publication at the beginning of 2011.

For 10 years, You and the Taxman has been providing our clients with insights on a broad range of current and emerging tax issues and trends in Singapore and beyond. With updates, commentary and analysis on a wide range of tax topics written by EY’s tax partners and directors, the magazine reaches out to CEOs, CFOs and Tax Directors of listed companies, MNCs and SMEs in Singapore. You and the Taxman is an authoritative and informative guide and your resource on the key tax issues affecting companies today.

Past and present issues of You and the Taxman can be found at: www.ey.com/SG/en/Services/Tax/EY-you-and-the-taxman

You and the Taxman

2 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

You and the Taxman

2 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition2 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

“You and the Taxman would not have had its success had it not been for all our contributors from our tax team — both past and present.“

3You and the Taxman Issue 4, 2015 |

Issue # – Month Year

310th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

This year, Singapore celebrates its 50th year of independence. The nation has celebrated its Jubilee anniversary with great pomp

and pageantry.

Here at EY, we celebrate a milestone of a different kind. It is our pleasure to present you with this special 10th year commemorative issue of You and the Taxman — EY Singapore’s flagship tax magazine with insights on tax issues that matter. Coincidentally, this edition (Issue 4, 2015) is also the 50th issue of the magazine!

As of this edition, we have published 400 articles over 50 issues, written by 156 thought leaders! As we were planning this issue and reviewing our past articles, I was struck by the amount of coverage in such breadth and depth of tax developments throughout the years.

In this issueThis commemorative edition is anchored by the theme Singapore taxation: past, present and future. It contains our observations on the trends and changes that are shaping the tax landscape today.

It is befitting that Pok Soy Yoong, You and the Taxman’s Founding Editor, kicks off this commemorative edition. With his vast experience in the field of taxation, Pok provides his take on how the tax profession has evolved and what he feels make a trusted and competent tax professional.

The world is changing quickly and Singapore has to adapt. Tax policy has to shift in response to or in anticipation of changing business trends both locally and globally. We explore how Singapore’s tax policy has evolved overall and specifically in areas such as transfer pricing, tax incentives, real estate investment trusts, and goods and services tax. We also take a fresh look at certain tax legislation to consider, whether certain areas could be further refined to enhance Singapore’s competitiveness.

This issue wouldn’t be complete without considering the impact of base erosion and profit shifting. We also cover the tax issues to consider in going global and in adopting certain growth strategies, impact of certain business models, and tax issues in specific industries such as shipping, oil and gas and cloud computing.

Special thanksYou and the Taxman would not have had its success had it not been for all our contributors from our tax team — both past and present. It is a huge commitment to take time out from our client work and busy schedules to pen these articles. Thank you to you all.

Special thanks goes to Pok who launched this magazine and laid the foundations for its direction. And my heartfelt thanks goes to Russell Aubrey who has diligently edited each issue since end-2006.

I would also like to thank our guest contributors from IE Singapore, the Economic Development Board and the Monetary Authority of Singapore.

Looking ahead, we can continue to expect more changes, more challenges and more shifts in the tax landscape. As a tax profession, we must continuously adapt and embrace change.

We hope you will enjoy this special edition of You and the Taxman. Thank you for your support.

Tax watch

Mrs Chung-Sim Siew MoonPartner and Head of Tax Ernst & Young Solutions LLP

Looking back, looking ahead

4 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition4 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

© 2

015

Erns

t & Y

oung

Sol

utio

ns L

LP. A

ll R

ight

s Re

serv

ed. E

D N

one.

Is your biggest tax burden the one you can’t see?Taxes can quickly become prohibitive. Find out how we can help navigate your tax complexities at ey.com/tax #BetterQuestions

5You and the Taxman Issue 4, 2015 |

Issue # – Month Year

510th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

It’s been a pleasure and privilege to edit You and the Taxman and to bring the magazine to you. Tax can be an interesting subject and our readers are not limited to

the tax and finance community.

I am grateful to all the contributors who have kept us going. Their dedication and enthusiasm

has been inspiring. In bringing you the latest tax developments and thought leadership, I hope we have provoked your thoughts in the process.

The tax landscape is changing at an ever-increasing pace, so I am sure we will have enough material for another 10 years.

Preface

Russell AubreyTax PartnerTransaction Tax LeaderErnst & Young Solutions LLP

| You and the Taxman Issue 4, 2015 10th anniversary commemorative edition6 | You and the Taxman Issue 4, 2015

Managing EditorChung-Sim Siew Moon

EditorRussell Aubrey

Founding Editor and guest contributor Pok Soy Yoong

Guest contributorsGina Lim Jillian Lim Carolyn Neo

Acknowledgements

ContributorsAmy Ang Ang Lea Lea Ang Sau TzeRussell Aubrey Aw Hwee Leng Andy Baik Samir BediHelen Bok Stephen BruceJohanes Candra Chai Wai Fook Kerrie Chang Michele Chen Chew Boon Choo Chia Seng Chye

Chionh Huay KhengChua Xiu MeiRandy Chung Chung-Sim Siew Moon Luis Coronado Goh Siow Hui Goh Su Ling Jow Lee Ying Darryl Kinneally Kor Bing KeongStephen Lam Lee Poh KwangLeow Yuet Yong Lim Gek Khim Latha Mathew

Shubhendu MisraBen MuddRajesh NathwaniIvy Ng David Ong Louise Phua Senaka Senanayake Soh Pui MingMonica Sum Henry Syrett Angela Tan Cedric Tan Jessica Tan Sharon Tan Tan Bin Eng

Tan Ching Khee Tan Lee Khoon Teh Swee Thiam Desmond TeoDonald Thomson Toh Shu HuiJerome van Staden Chester WeeWong Hsin Yee Grahame Wright Wu Soo MeeSandie Wun Yeo Kai EngYeo Ying

Project Manager/Editorial Karen Lew

DesignIrene LeeSoo Soon Tat BCS — Creative Design Services

7You and the Taxman Issue 4, 2015 |

Issue # – Month Year

710th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Singapore Tax Partners, Tax Executive Directors and Asia-Pacific Tax Centre Leaders From left to right

Row 1 (seated): Yeo Kai Eng, Lim Gek Khim, Russell Aubrey, Tan Lee Khoon, Chung-Sim Siew Moon, Soh Pui Ming, Amy Ang, Angela Tan, Grahame Wright

Row 2: Goh Siow Hui, Kerrie Chang, Jeffrey Teong, Helen Bok, Wu Soo Mee, Choo Eng Chuan, Chester Wee, Kor Bing Keong, Nadin Soh, Lim Joo Hiang, Ivy Ng

Row 3: Ang Lea Lea, Tan Bin Eng, Chia Seng Chye, Teh Swee Thiam, Chai Wai Fook, Hugh von Bergen, Latha Mathew, Grenda Pua, Tina Chua, Desmond Teo

Row 4: Stephen Lam, Tan Ching Khee, Kenji Ueda, Paul Griffiths, Samir Bedi, Jerome van Staden, Henry Syrett, Barbara Voskamp, David Scott, David Ong

Absent: Andy Baik, Adrian Ball, Stephen Bruce, Cheong Choy Wai, Luis Coronado, Graham Frank, Rick Fonte, Darryl Kinneally, Gagan Malik, Shubhendu Misra, Nick Muhlemann

8 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition8 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

14

20

24

30

34

Founding Editor’s contribution

14 Straight from the gut: a retired taxman shares a few thoughts EY’s former Head of Tax shares his insights on what it takes to

succeed in the tax profession and how to instil confidence and trust in the client-advisor relationship.

In this issueYou and the Taxman

Evolution of Singapore’s tax policies

20 The role of tax policy: what works, what stays, what changes?

The primary purpose of taxation is, of course, to raise revenue. But tax policy is also used to enhance competitiveness and shape social behaviours.

24 Singapore tax incentives: the Jubilee vantage point Singapore’s incentive schemes have always been refined

in line with economic priorities. Government agencies have played a critical role in administering these incentives to attract and retain businesses with substantive activities in Singapore.

30 The evolution of transfer pricing in Singapore The transfer pricing scene in Singapore has progressed since

the first guidelines were introduced in 2006. With base erosion and profit shifting in the international limelight, the tax authority’s focus on transfer pricing will continue to intensify.

34 Singapore GST: past, present and future Since its introduction, the goods and services tax (GST) rate

has increased and self-review programmes have been introduced. The future is likely to bring increasing use of data analytics to enforce GST.

9You and the Taxman Issue 4, 2015 |

Issue # – Month Year

910th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

39

52

44

48

Issue 4, 2015 10th anniversary commemorative edition

39 Expatriate taxes: past, present and future Drawing talent from abroad helps Singapore to inject greater

vibrancy into the economy and retain its position as a key business hub in Asia. In reviewing the tax regime for expatriate taxation, the key is to strike the correct balance.

44 Singapore REITs: the next lap The regulatory and taxation framework for Singapore real estate

investment trusts (REITs), including tax transparency, has contributed to the sector’s success. Going forward, other key taxation areas that can be reviewed include the sunset clause.

48 Singapore thrives as a fund management hotspot Singapore’s tax incentive regime has been instrumental in

positioning Singapore as an attractive fund management centre. Despite this, there’s still room to encourage further fund domiciliation in Singapore.

52 Keeping taxes competitive for the insurance industry Targeted tax policies have helped to create a vibrant insurance

sector in Singapore. An area that could be refined is to allow the application of general tax principles to evaluate the tax implications of business operations and transactions.

10 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition10 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

A fresh look at Singapore taxation

56 Demystifying the 2015 Singapore Transfer Pricing Guidelines The release of the 2015 Singapore Transfer Pricing Guidelines in

January 2015 has been a game-changer, requiring companies to prepare annual transfer pricing documentation.

60 Enhancing the renovation and refurbishment deduction scheme To further support small and medium-sized enterprises, the

renovation and refurbishment deduction scheme can be refined by increasing the spending cap, amongst other measures.

63 Defining the status of an investment holding company In determining the tax treatment of an investment holding company,

it is important to differentiate between a pure investment company and a section 10E company which “carries on a business of making investments”.

67 Nailing withholding tax compliance Withholding tax is a key concern in cross-border transactions.

Companies need to consider the various withholding tax compliance requirements, as well as the developments in this area, in multiple jurisdictions.

70 Broadening deductions for intangible assets In tax, the line between capital and revenue expenditure is

difficult to draw. For telecommunication providers, it would be helpful if the payments for spectrum rights and licences can be deducted or amortised for tax purposes.

73 In the spirit of giving Despite their contribution to society, voluntary welfare organisations

in Singapore do not receive special GST relief or status. Perhaps it is time to fine-tune the GST legislation to reverse this.

60

67

73

70

63

56

11You and the Taxman Issue 4, 2015 |

Issue # – Month Year

1110th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

7676 Finding tax upside with accounting reclassification In determining whether a receipt is capital or revenue in nature,

taxpayers need to examine the facts and circumstances surrounding the transactions and consider these against guidance developed through case law.

Impact of base erosion and profit shifting (BEPS)

80 The big deal about BEPS The Organisation for Economic Co-operation and Development’s

(OECD) BEPS project affects businesses with overseas operations. Companies need to assess the impact of BEPS and implement measures to mitigate any negative impact.

84 Going global: consider before you leap Before going global, companies need to consider these tax

issues: the holding and financing structure for new investments, local tax considerations in the foreign country, transfer pricing and supply chain issues, and expatriate tax implications.

87 Preserving Singapore’s status as a regional hub for business In light of growing transfer pricing scrutiny worldwide, Singapore

has to defend its stature as an international business hub by ensuring that companies anchored here have sufficient business substance.

90 Recent trends in the application of tax treaties Recent trends observed in tax treaties of late include the narrowing

of permanent establishment exclusions and the inclusion of anti-abuse provisions to disallow treaty benefits. The fight against BEPS is also likely to impact the negotiation of tax treaties.

87

84

80

90

12 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition12 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

Growth strategies and going global

94 Staying competitive in an evolving global tax landscape Many countries are embarking on tax reforms, driven by the OECD’s

BEPS Action Plan and the move towards greater transparency. Multinational enterprises thus need to keep themselves updated on these tax policy shifts.

97 Venturing abroad: five tax issues SMEs need to consider Before going overseas, SMEs need to consider the local tax

implications of the entity structure, the local tax impact of funding arrangements, tax deductibility of borrowing costs, future profit repatriation, and the tax implications of disposal of the investment.

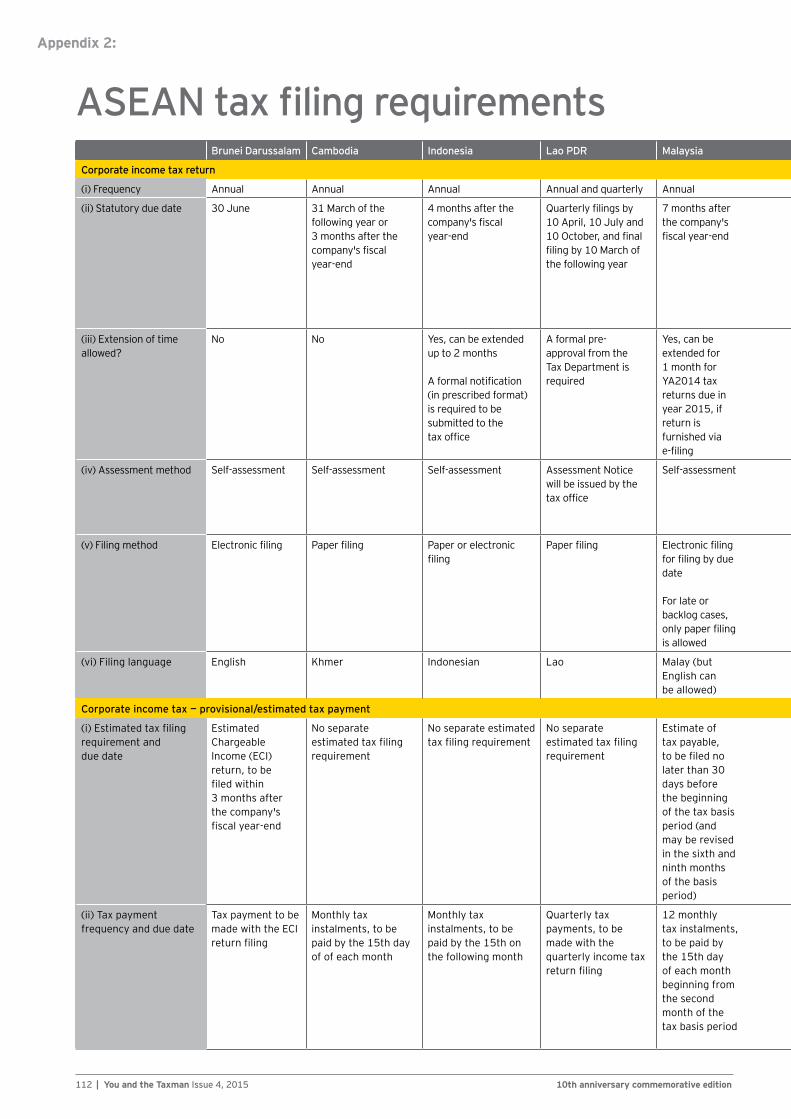

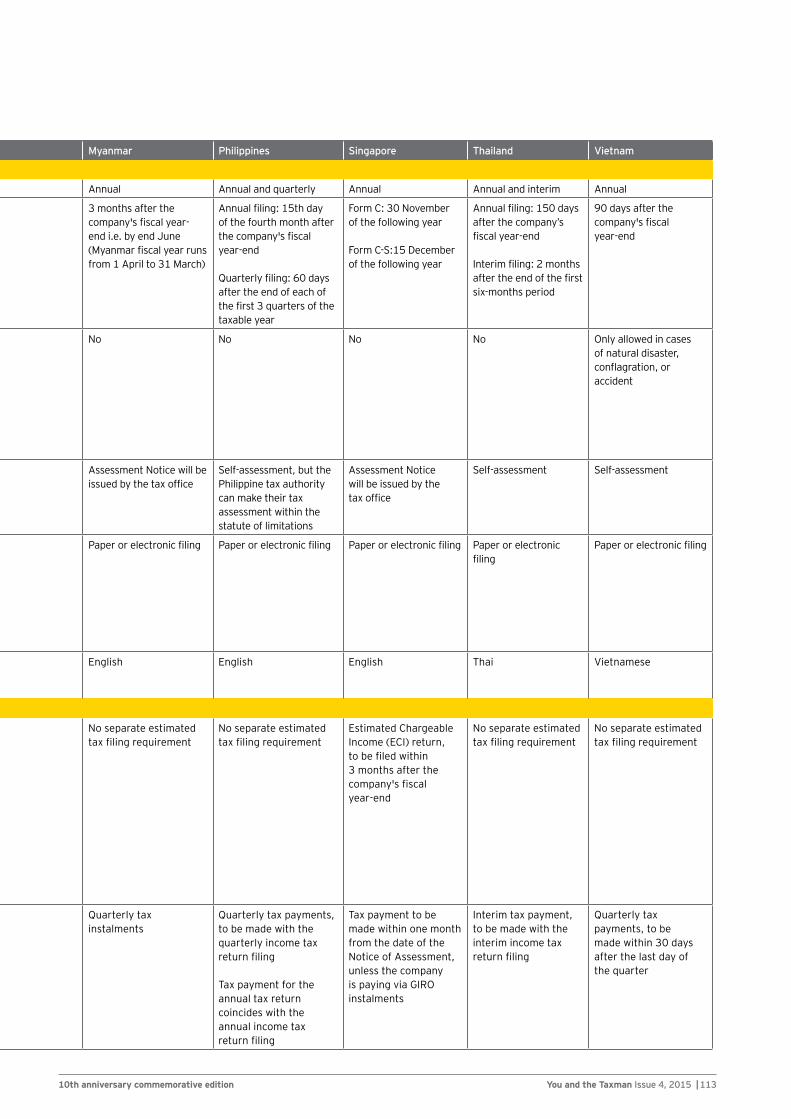

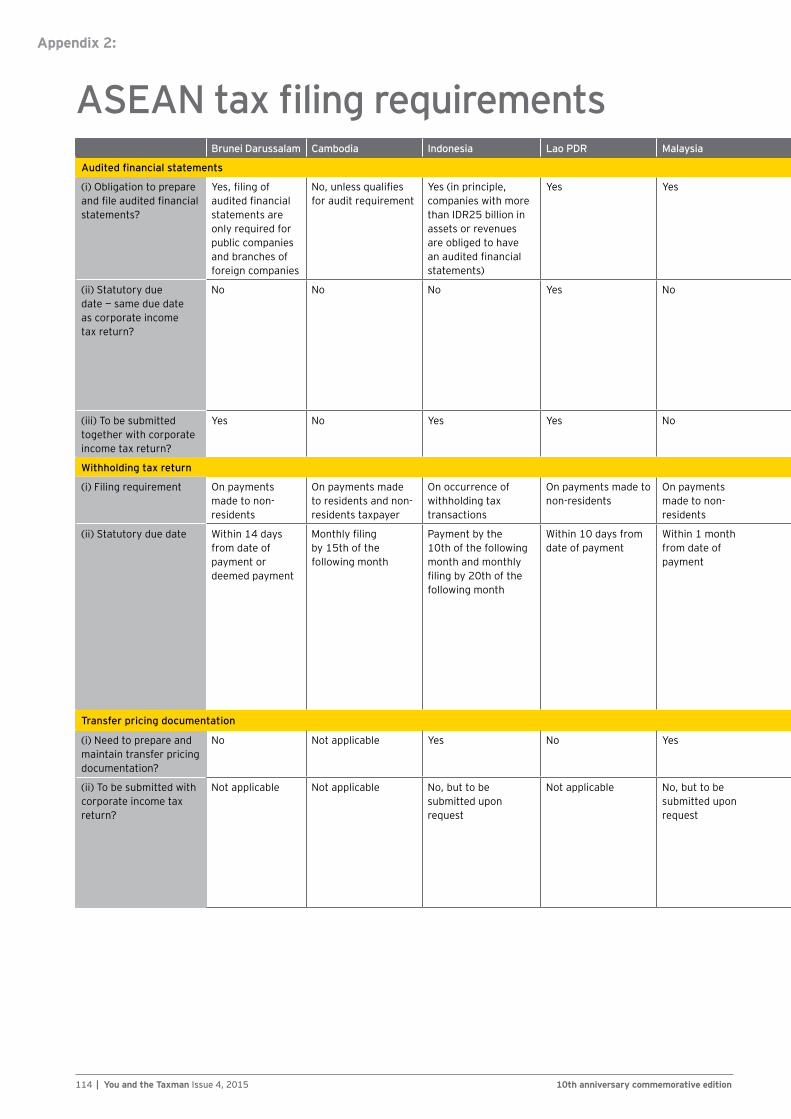

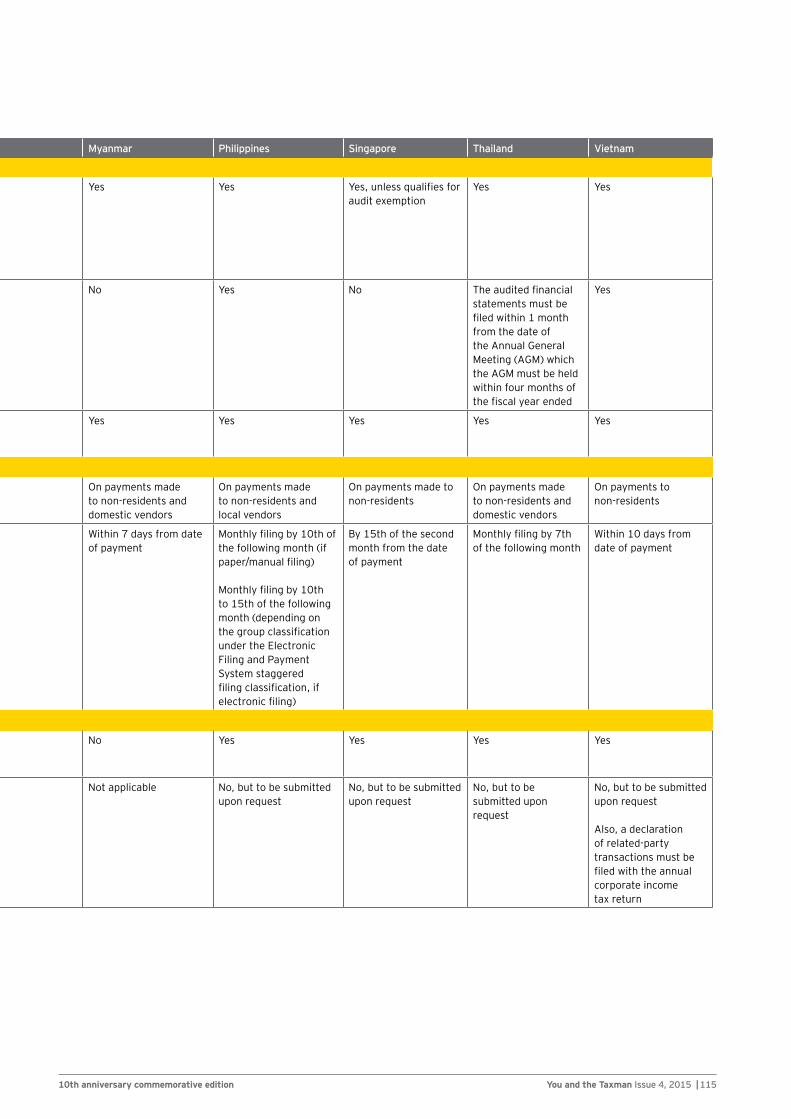

100 The “art” of investing in ASEAN While the ASEAN region offers a plethora of opportunities

for foreign investors, they need to be aware of the diverse regulatory and tax compliance requirements in the region.

116 Divestments: the new black? Divestments can catalyse growth as the funds from a sale

can be deployed into more exciting opportunities. To maximise value, businesses need to ensure that the divestment is tax-efficient.

Business models

120 Singapore centralised business models and transfer pricing documentation

The centralisation of managing transfer pricing documentation can ensure a coherent and consistent messaging across groups, which is increasingly important given the BEPS requirements.

125 Top four customs implications of cross-border structuring Singapore’s customs environment can be just as complex as

other customs jurisdictions in Asia-Pacific. Redesigning operating models with a Singapore element therefore requires careful consideration of customs issues. 125

116

120

100

94

97

13You and the Taxman Issue 4, 2015 |

Issue # – Month Year

1310th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

129 Embracing a data driven era Tax departments face challenges in mining and managing data

for better decision making. Tax functions can harness the use of big data to make better decisions, meet transparency demands and reduce tax risk.

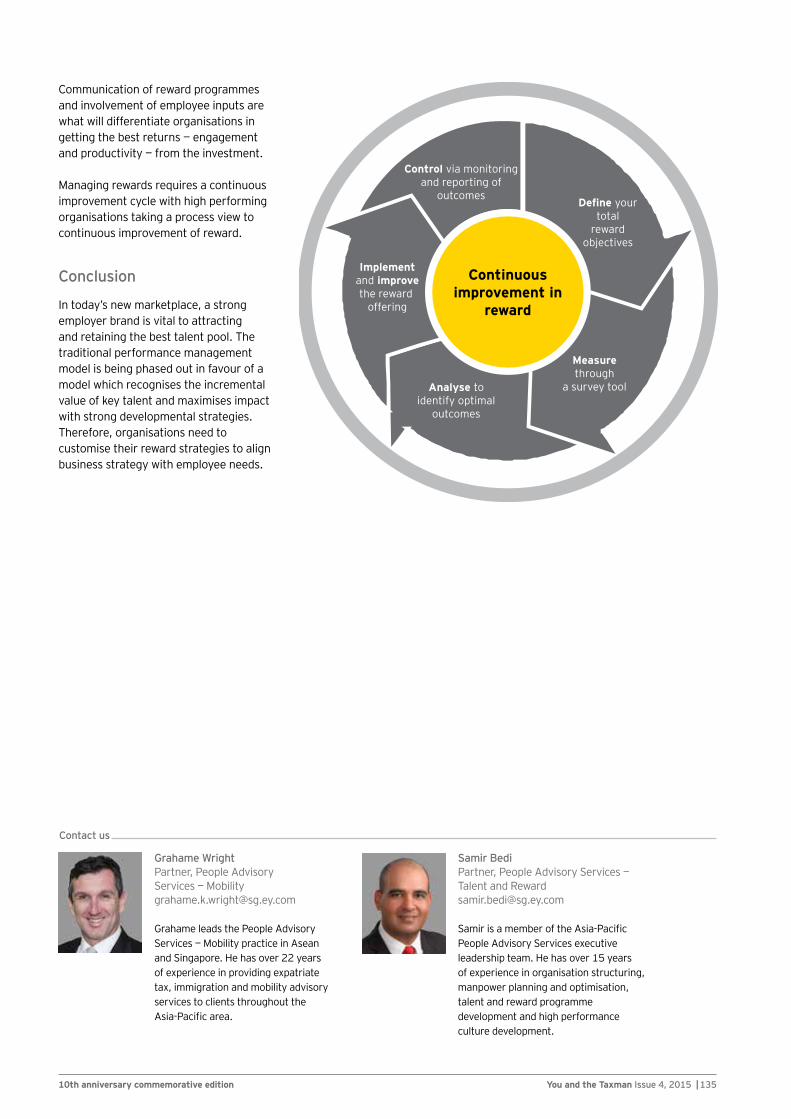

132 Managing the talent and reward agenda To grow talent, organisations need to emphasise their future

competencies and align their development with business plans. Organisations should also customise reward programmes and align these with business strategy and employee needs.

Industry trends

136 Navigating new tax headwinds in the shipping industry As the international tax landscape evolves, players in the

shipping industry need to assess their business models to ensure that they can proactively manage tax risks and support their adopted tax positions.

140 Oil and gas sector facing structural shift Oil and gas players will need to consider the tax implications of

further consolidation in the sector, amid a backdrop of falling oil prices.

143 Top five considerations in entering transactions in the financial services sector

Before proceeding with a transaction, financial services institutions should consider the following: reputational concerns and internal governance, codes of conduct, BEPS concerns, transfer pricing and anti-avoidance provisions.

146 Tax and the cloud: is the sky clearing? Cloud computing has increased exponentially, but uncertainty

remains on its tax treatment. Key tax issues relating to cloud computing include the sourcing of income and the characterisation of payments.

146

143

140

136

132

129

14 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

You and the Taxman

14 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

Founding Editor’s contribution

“Mastery of the IRAS statements of practice is not a mastery of the

tax law. To get there one starts with knowing and understanding the

legislative provisions.”

Education is an admirable thing, but it is well to remember from time to time that nothing that is worth knowing can be taught.”

Oscar Wilde wrote this in “A few maxims for the instruction of the over-educated”, first published anonymously in November 1894.

Knowing, as in knowing how and what to do, comes from an accumulation of actual experience. It is hands on. It is personal. Fully absorbed into our memory muscles.

What is experience? It is knowledge or practical wisdom gained from what one has observed, encountered, or undergone. And honed over time to crisp sharpness. Deeply fused into one’s gut.

So how can I teach another what and how I know in my gut? How could I transplant my personal experiences into the gut of another person so that he or she could apply the same experience in the way as I did?

The reality is that none of us could.

Straight from the gut: a retired taxman shares a few thoughtsFormer EY Singapore Head of Tax and guest contributor Pok Soy Yoong shares his views on what it takes to succeed in the tax profession

“

15You and the Taxman Issue 4, 2015 |

Issue # – Month Year

1510th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Often I am asked what are my secrets. It is as if I have discovered clever shortcuts to gaining knowledge and experience. But I know of no secrets or shortcuts. Whatever I know I gained from long years of immersion in the profession and walking the hard journey every inch of the way.

Be that as it may, I am convinced that it is possible to lead a person towards the path of knowing, of experience, and thus experience the observation, the encounter, or feeling. And on this path one gets a chance to flourish. Edmund Phelps put it well in Mass Flourishing1 — “A person’s flourishing comes from the experience of the new; new situations, new problems, new insights, and new ideas to develop and share”.

I would go a step further though. I would say that a person’s “flourish” or “experiential growth” comes not only from the new. Even a seemingly repeated situation is a new situation. It is new because the context around it is

different. The circumstance around it is different. Or the players involved are different. Just as client after client approached me over the years for advice on, say, withholding tax, the contexts of the withholding issue were invariably different. And so I approached each advice as a “new” situation and gained a new shade of insight each time.

I come back to the question — How can knowing be taught, even if indirectly?

Awareness. That’s the key.

Again I quote Edmund Phelps in Mass Flourishing — “I believe the sole problem (of not flourishing) as the terrible unawareness”. (Words in brackets added.)

What is awareness? It is the state of ability to perceive, to feel, or to be conscious of events, objects or sensory patterns; having knowledge; consciousness.

With awareness we plant in our mind the seed of change. But will it germinate and grow? It depends. It depends on how much will we garner to make the change. Awareness does not make the change. It makes change a possibility.

And so it is with the object of creating awareness that I share a few of my thoughts on what I think hinder our capacity to flourish to our full potential as a tax professional.

You don’t learn from cutting and pasting. Your experience is just that — cutting and pasting

They say you must work smart. They say if it is already invented, you should not reinvent it. They say if it is already written, you just copy it and paste it. You save time. You increase your productivity. And why not if you can bill for what you cut and pasted? The same piece of material is recycled for more fees, with less effort. Indeed, why not?

1Phelps, E. (2013). Mass flourishing: How grassroots innovation created jobs, challenge, and change. Princeton: Princeton University Press.

16 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition16 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

Just that if we want to cut and paste, we better make ourselves a top in class expert in this. And one more thing. Never get caught, whether we are in the profession or in commerce and industry. I am not against all forms of cut and pastes. But we need to know the effect of indiscriminate cutting and pasting over time. We stop thinking. We stop analysing. We stop seeing pitfalls and opportunities. Without knowing it we restrict our creativity to touch only the surface. As we accept the cut and pasted materials at their face value, as correct we leave our deep thinking ability undeveloped.

In other words, we stop experiencing new insights. But our experience in cutting and pasting increased multifold. But what happens if the situation is new? What if there aren’t existing materials for us to cut and paste? So we fall back on our deep thinking ability and creativity? But what if we have never bothered to practice and hone these traits over time?

We may have covered the same subject matter 50 times with 50 cuts and pastes. It is just the very first experience repeated another 49 times. We do not achieve mastery of our subject matter. We do not develop the gut feel that a maestro exhibits all the time.

Over the years I made it a habit to write all my tax advices, tax opinions, tax memorandums, technical position papers and what not from scratch, with minimal cuts and pastes2. It did not matter that I had dealt with the subject matter umpteen times before. I invariably started the analysis from scratch. I try to make what I learnt come alive, in the context of the facts and circumstances that I was looking at. So each time I wrote on a subject matter I had dealt with before, I gained new insights. I honed my creativity. I learnt to look at the same or similar thing from different angles and different perspectives. I became better at handling the nuances. I became better at making the complex simple. I became better at figuring out what matters

and what not. I became sharper in my decision-making. It is hard work. But it helps my brain revs and keeps it in good shape. More importantly, increased mastery of the subject matter aided me in the speed and quality of my written work. Tremendously.

Beware. We cannot achieve mastery with cuts and pastes, except as a maestro of cuts and pastes. Instead, it holds back the development of our deep thinking ability and creativity; and our ability to articulate effectively.

Work smart but not work hard

We read about this in books. We are lectured on this. Literally, we grew up on this.

Over the years I know of many people that embraced this teaching fervently, and practiced it quite religiously.

But what does this mean? Invariably, it means one or more of these — look for the easiest way to get something done; find the best way to get things done to make life simpler; figure out the quickest and most effective way to rise in ranks without having to toil. By and large, it means minimum effort or pain but maximum upsides or glory. No wonder this teaching has such wide following.

Practitioners of this teaching have found it a rewarding practice as they rise in rank in their careers. That is, until they are promoted to their level of incompetence. At that level, they are no longer confident of what to do, even less of the how to do. And so they persistently keep doing what they used to do before the promotion to the level of incompetence.

The point is that practitioners of this teaching unknowingly shortchange their own potentials in longer run. They become grand masters in shifting their own burdens to others. They delegate when they should have done it themselves3. They become grand

champions at talking but have great difficulty walking their talks (because they just don’t have the skills to do the walk). Some even acquire the fine skills of taking others’ credit. Then some days they wonder why they stagnate while their peers ignorant of the teaching are still rising.

How do practitioners of this teaching shortchange themselves?

They rob themselves of hands-on experience. Without enough hands-on experience they leave their gut feels undeveloped relatively to others.

Hands-on hard work is what that gives experience. This is what that gives the acute sensing of the most likely issues well ahead of others. It is this sensing that helps us derail the issues before those issues derail us. This is also the sensing that helps us focus our energy and resource only on things that count in producing the output we wanted.

How can we smarten up if we have not made the mistakes and distressed over these? How can we figure out where we slipped and why we slipped if we have not made enough mistakes? How can we ever learn from mistakes if we have not rolled up our sleeves and thrown ourselves into the problems and manage them?

Practitioners of this teaching focus on finding short cuts in life. The harshest fact of life is that there aren’t many short cuts in the mastery of life. Indeed, as they rise in their career they become increasingly ineffective. Why? It is simply because they make others learn new skills and accumulate those skills. They just act as middlemen getting their jobs done through others. Now, in a world that focuses on productivity there is very little room for the middlemen!

For me, the rule has always been Work Hard and Work Hard, and experience every aspect of the subject matter that I could possibly experience. And before long, I seemed to be Working Smart without Working Hard. Or so it seemed!

2Even on those occasions I did cut and paste, the “imported materials” became the start point of my draft and was rewritten to follow my technical analyses.3Some of them even excel at delegating upwards to their bosses!

17You and the Taxman Issue 4, 2015 |

Issue # – Month Year

1710th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Ben Horowitz said it all in The Hard Thing About Hard Things4: “There are no shortcuts to knowledge, especially knowledge gained from personal experience. Following conventional wisdom and relying on shortcuts can be worse than knowing nothing at all.”

Learn the law and the practice

Learn the law, then the practice. That’s how I learnt my craft.

But for some years now a different trend has taken hold. It is even more evident in recent years. Increasingly, tax positions taken are based on practice statements of the Inland Revenue Authority of Singapore (IRAS), with the provisions in the Income Tax Act (ITA) taking second place or no place at all.

IRAS statements of practice evince the interpretation the IRAS places on the law. But these are not necessarily the only interpretations of the law. For that matter, these may not even be the only correct interpretations of the law. As Yong Pang How CJ famously said in Comptroller of Income Tax v GE Pacific Pte Ltd [1994] 2 SLR(R) 948, “Practice is not law”.

Mastery of the IRAS statements of practice is not a mastery of the tax law. To get there one starts with knowing and understanding the legislative provisions. And a very good grasp of all or nearly all the landmark decisions in case law, both local and foreign.

We need to build a firm grasp of what the law is. Then fortify this with a strong grounding in the tax principles from case law. Then develop a good working knowledge of the IRAS statements of practices; bearing in mind always that practices are not law and that the IRAS’ interpretations in these statements do not cover every conceivable situation. Otherwise, as tax professionals we heighten the risk of taking the incorrect or inappropriate tax positions. And bear the consequences, including that of a potential negligence suit.

AVD v Comptroller of Income Tax [2011] SGTTBR is a good example. A tax practitioner honing his craft based on statement of practices of the IRAS only would have accepted the outcome described in the 1993 IRAS Circular. Understanding the law in Section 37(16) of the ITA, however, should prompt the tax practitioner to enquire whether that Circular should have been interpreted as if it were the law. Admittedly the AVD case was concerned with the exercise of a discretion by the IRAS. But if the veracity of the Circular was not challenged based on the legal provisions in Section 37(16), this case would never have been heard.

And so, learn the law, then the practice.

But how to get there?

The vast majority of the tax practitioners are accountants turned tax consultants. Unlike their counterparts in the legal profession, they are not trained to read the law or read into the nuances of the law. So they claimed. But this has not stopped the older generation of the tax accountants from some impressive mastery of the tax laws.

For those aspiring to hone their craft with the tax law, I recommend they take to heart two chapters in The Law and Practice of Income Tax, second edition. Chapter 1 deals with “Framework of Interpretation in Tax” and Chapter 2 focuses on “Analysing Tax Decisions”. Both chapters were written with the tax accountants in mind. So that is a good starting point for the journey into the lore of taxation.

The older generation of tax accountants have another trick in their hats — their deep knowledge in case law, both local and foreign court cases. Reading, understanding and analysing case law is the other area to invest time and effort in.

The rest of the learning comes from the actual practice of the law and a keen enquiry of the statement of practice

especially whether in the context it was written it has overtly narrowed down the meanings and intents of the words in the legislation.

One does not achieve mastery within a short period of time. If this is possible I am yet to hear or see one. There is no work smart here. There is only work hard to gain the mastery inch by inch.

About key performance indicators (KPIs)

KPIs can be extremely effective in shaping performance behaviours at the workplaces. Just google it and you will find lots of entries about it. I want to focus on only one behavioural aspect of the KPIs.

It has the powerful effect of shaping our behaviour to protect our own interest and pursue this to the exclusion of almost anything else. I have seen and personally experienced instances where clients’ senior executives push the tax advisors for unrealistic targets or positions. When what they pushed for could not come about, they threatened to seek second opinions or issue an RFP. A few even deliberately spoke untruths and put all the blame on the tax advisors when some or all of the trails for the faults could be traced directly back to them. To be fair, I have also had the good fortune to serve many clients with a keen sense of fair play and integrity.

But these self-centered and self-interested behaviours are not confined to the clients’ executives. They are prevalent also in the workplaces of the tax advisors, whether in the profession or otherwise.

KPIs are supposed to be measures of level of performance. Increasingly they are construed as targets. Since rewards or threats of dismissals are pinned to achieving targets (a la KPIs), self-serving behaviors emerge, and emerge strongly.

4Horowitz, B. (2014). The hard thing about hard things: Building a business when there are no easy answers. New York, NY: Harper Collins

18 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition18 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

And so we have multiple tax advisors from the same organisation competing to serve the same clients but do not talk to each other on what serves the best interest of the client. Or who should best serve the client. And so we have tax advisors serving clients in areas out of their area of competence rather than parading before the clients the subject matter specialists that could serve the interest of the client far better. And so we have tax advisor or advisors hoarding a client list that is far more than they can realistically attend to the interests and needs of these clients. And so on and so forth.

I am not certain whether those practicing such behaviours are even aware of their self-interested traits. Some probably do but justify these on some righteous grounds. But quite certainly, they have little or no understanding how these behaviours affect how they serve their clients in the longer term and their standing in the marketplace.

Plainly, self-serving or self-interest guarding behaviors are major hindrances to achieving a trusted tax advisor status. And this leads me to the next thought.

Trusted tax advisors

Many of us aspire to be a trusted tax advisor and be recognised as such by our clients and in the marketplace. More often than not, we embark on that journey without a road map. I will not even attempt to re-craft what is bountifully available in the internet. A Google search will give you more materials than you can reasonably handle on the traits, and therefore behavioural patterns, of a trusted tax advisor5.

I will share only a few of my thoughts.

There is a strong but misplaced perception that a rainmaker or a superstar salesman is a trusted tax advisor.

In my experience, a trusted tax advisor does not sell. Rather, he sells by not trying to sell. When presented with a tax issue by the client or potential client, he typically offers his thought quite fully and outlines what he thinks are the options available. In so doing, he demonstrates to the client his grasp of the tax and related business issues, the depth of his tactical and technical experience. He does not, for example, say “I know the solutions to the issue. Sign the appointment letter first and I will tell you the answer.”

“It is not what you know but who you know” brings to the fore another misconception. There is this perception that relationship building ability is key to achieving the trusted tax advisor status. Ability to connect with others is one of the many traits of a trusted tax advisor. But relationship alone does not translate to trust. More likely than not, the existence of this relationship turns us into the touch point for an enquiry that may lead to a wider relationships with others in our organisation.

Bending backwards all the way to meet every want and desire of a client is not the trait of a trusted tax advisor. I had come across clients dictating the outcome of tax opinions or advices even before these were written! Some of them even threatened to disengage us or go to the competitors for a more palatable piece of opinion or advice6.

In the early 90s, the tax manager of a US MNC was in town to “interview” the tax partners in the then major public accounting firms. I met her with two of my colleagues. The meeting was pleasant enough. As the meeting drew to an end, she remarked casually

that she was “looking for the most aggressive tax advisors to represent us in Singapore”.

I was silent for a moment trying to bite my tongue. But then I decided to say what I thought ought to be said — “If you are looking for the most aggressive tax advisors, you have come to the wrong place”. When the initial shock was over, I explained that our philosophy was to look after the long term best interest of our clients. For that, we only took technically sustainable tax positions that aligned to the business objectives of the organisation, not aggressiveness for the sake of aggressiveness.

After the meeting, all three of us thought we had lost the opportunity.

A couple of weeks later, we received the letter to confirm our appointment! I continued to serve this client till my retirement and was amply rewarded for our services over those years.

This example is anecdotal of the issue of our self-interest or self-serving behaviours. The more of such behaviours we exhibit, the more likely that our relationship with a client is short term. The drive is primarily to meet the revenue KPIs. In so doing our focus is on the fee potential and anchoring it. The fear of losing the fee holds us back from doing the right thing. And so we seldom pause to ask questions such as whether the best interest of the client would be better served by not going ahead with a piece of work or by scoping down the work or whether the client should re-frame the issue appropriately? Would we have asked these questions if that entails foregoing a large fee?

To further understand and learn the behavious of a trusted advisor two of the books that offer good grounding are The Trusted Advisor7 and The Trusted

5For example, follow this link to a very comprehensive set of materials by David Maister — http://davidmaister.com/wp-content/themes/davidmaister/pdf/pm_clients.pdf 6There is a different perspective to this. We might have taken a conservative or a strict technical view on the issue. But a professional opinion is just that. It is a professional’s judgement call. If we are technically sound, have a firm grasp of the circumstances and issues and consider that an aggressive or more liberal reading of the law is not tenable, I see no reason not to hold firm to our views. This is one of the risks that a trusted tax advisor takes — not bending backwards when he has no conviction in the position he is asked to take. 7Maister, D., Green, C., & Galford, R. (2002). The trusted advisor. New York, NY: Free Press.

19You and the Taxman Issue 4, 2015 |

Issue # – Month Year

1910th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Advisor Fieldbook: A Comprehensive Toolkit for Leading with Trust8. You really want to read them and figure out where you are on your journey to becoming a trusted tax advisor.

I quote what the authors said in The Trusted Advisor Fieldbook:

“ Over and over again, you will discover that the things that create trust are the opposite of what you may think. That is why we say trust is paradoxical — in other words, it appears to defy logic. The best way to sell, it turns out, is to stop trying to sell. The best way to influence people is to stop trying to influence them. The best way to gain credibility is to admit what you do not know.

The paradoxical qualities of trust arise because trust is a higher-level relationship. The trust-creating thing to do is often the opposite of what your baser passions tell you to do. Fight or flight, self-preservation, the instinct to win — these are not the motives that drive trust. The ultimate paradox is that, by rising above such instincts, you end up getting better results than if you had striven for them in the first place.”

Profound. But true. I wish this book was published twenty years earlier!

Final thoughts

I begin my final thoughts with what Edmund Phelps said:

“ I believe the sole problem (of not flourishing) as the terrible unawareness”. (Words in brackets added.)

“If I am not aware that there is a problem, as far as I am concerned, there is no problem.” I quipped this often. Sometimes, as a sarcasm. Other times, meaning every word of it, gravely serious.

Unawareness, or not knowing, often robs us of the chance to develop and hone our experience. Cut and paste is one example. This rising tide is almost an uncheckable trend. Yes, doubtlessly it increases productivity. Yet, if we do not fully understand the contents of the cut and paste materials, we could not leverage on it to create new materials, new insights, new knowing and therefore experience. It is just a mindless exercise of cut and paste.

Clearly work smart but not work hard works, to some extent. But practicing this persistently and pervasively means we rarely ever roll up our sleeves to do the heavy lifting. We place a limit on our accumulation of experience. At some point in time our prior experiences will put a limit on our potential to flourish. There is nothing very much we can do with KPIs. With extreme focus on revenue and profitability growth, KPIs are nowadays increasingly considered as targets rather than measures of performance levels. This is what it is, if it is.

There is nothing to stop us from getting keenly aware of how relentless pursuit of these KPIs may heighten our self-interested behaviours. Some argue that these are moralistic and ethical issues. They probably are. But I do not intend to take on this debate here. My message is simply this — awareness of these tendencies helps keep our behaviours in check. It offers us the chance to think about what are the right things to do

8Green, C., & Howe, A. (2012). The trusted advisor fieldbook: A comprehensive toolkit for leading with trust. Hoboken, N.J.: Wiley.9You will see many of the traits described in the pdf materials by David Maister — http://davidmaister.com/wp-content/themes/davidmaister/pdf/pm_clients.pdf. See also notes 5 and 6 above.

and what ought not to do. And by the way, doing the right thing takes a lot of courage and practice.

Trusted Tax Advisor is not an award. It is the confidence and trust our clients have in us over long years of the client-advisor relationship.

A trusted advisor embodies a long string of traits9. The more we are aware of what these traits are, and practice them as consistently as possible, the faster we accumulate the experience and strengthen our reputation in the marketplace.

Knowing and developing gut feel takes much more than awareness of the five thoughts in this little piece. There are many others. Not getting emotional with a tax issue is one. The knack to simplify the complex is another. Writing clearly, plainly, investing in extensive reading (and for those claiming to have no time, re-prioritise our time to make this investment), learning to admit and say we do not know to the clients are some of the others.

Awareness of these and more, in my experience, is what that shaped my personal development and my career in tax. I hope these little thoughts are of some help to you, whether you are in the profession or in commerce and industry.

And my best wishes to you on your journey to knowing, experiencing and flourishing.

Pok Soy Yoong was Head of Tax in EY Singapore from 2002 to 2008. He retired in 2008 after more than 30 years in the tax profession, 20 of which were spent with EY. Pok is currently a Board Member of the IRAS. He is also the Technical Editor of the book “The Law and Practice of Singapore Income Tax”, second edition.

The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.

20 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition20 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

Evolution of Singapore’s tax policies

“The fundamental tenet of Singapore’s tax policy is to maintain the nation’s competitiveness in the global arena for corporations and individuals by

keeping tax rates competitive for both, amongst other measures.”

The history of taxation can be traced as far back as over 3,000 years ago. For centuries, taxation has been generally used as a

method for governments to raise revenue to finance public sector spending. Indeed, higher taxes were levied during and after the two World Wars to help pay for the cost of these wars. Some reports even cited that the withholding tax system was introduced during World War II to meet the higher demand for revenue.

The evolving use of tax policy

Even today, the main objective of tax policy is still revenue raising. However, taxation is now no longer just a means of funding for government operations. Over time, it has evolved into a tool widely used by governments to influence business, social and regulatory behaviours.

Most textbooks, scholars and policymakers agree that the overarching goals of tax policy are raising sufficient revenue, equity, efficiency and simplicity. Through

The role of tax policy: what works, what stays, what changes?Chung-Sim Siew Moon and Russell Aubrey review how Singapore’s tax policy has evolved throughout the years and consider the likely direction of future tax policy

21You and the Taxman Issue 4, 2015 |

Issue # – Month Year

2110th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

these goals, governments try to, amongst others, influence social behaviour, whether aggressively or subtly through tax provisions, incentives and disincentives built into the country’s tax policy.

Closer to home — Singapore’s tax policy

In Singapore, the government sees tax policy as a cornerstone of Singapore’s fiscal policy. According to the Inland Revenue Authority of Singapore, the main objectives of tax policy in Singapore are revenue raising and the promotion of economic and social goals.

Understandably, revenue raising is the traditional aim of tax policy as tax revenue is a substantial source of funding for government operations in Singapore. As for the promotion of economic and social goals, tax has been used to influence the behaviour of corporations and individuals in Singapore towards desirable social and economic goals.

For example, to encourage mechanisation and automation, Singapore allows accelerated capital allowances for most assets used for business purposes. Elsewhere, property cooling measures, such as the Additional Buyer’s Stamp Duty and the Seller’s Stamp Duty on properties together with total debt servicing ratio framework, were introduced to moderate the property market and encourage greater financial prudence among property purchasers. To boost Singapore’s birth rate, the government has also enhanced procreation measures and the Marriage and Parenthood package over the years such as removing the cap on the number of children qualifying for child reliefs.

The fundamental tenet of Singapore’s tax policy is to maintain the nation’s competitiveness in the global arena for corporations and individuals by keeping tax rates competitive for both, amongst other measures. For corporations, this helps to ensure that Singapore attracts

a good share of foreign investments. For individuals, the rates are purposefully kept low and progressive to encourage a hardworking society, and to foster entrepreneurship by making risk-taking worthwhile.

Corporations in Singapore enjoy a suite of tax “baits” targeted at the various stages of a corporation’s life, implemented to encourage certain economic or social behaviours.To spur entrepreneurship, the start-up exemption scheme was introduced to provide newly incorporated companies with some level of tax exemption in their initial years. To help small and medium-sized enterprises (SMEs) grow, a partial tax exemption scheme (with the exemption threshold targeted to benefit the SMEs) is in place to lower the taxable profits of these SMEs.

As companies expand their operations and organise into multiple entities within a group, the government introduced the loss transfer system of group relief. This relief recognises group companies

22 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition22 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

as a single economic entity by allowing the unabsorbed tax losses, unabsorbed capital allowances and unabsorbed donations from one company to offset the profits of another company in the same group, thereby reducing the overall tax burden for the whole group. This is to facilitate risk-taking and entrepreneurial activities by entities within a group.

To further support companies in going global and earning a large share of their income from overseas operations, exemption from tax is given to foreign-sourced dividend income, foreign-sourced branch profits and foreign-sourced service income, subject to prescribed conditions. This aims to simplify the tax system — a key focus of the tax legislation. Over the years, tax breaks in the form of grants, financing and tax incentives have been enhanced by the government to support companies in expanding overseas and entering into new markets. Singapore recognises that businesses need to innovate and internationalise to remain commercially competitive and viable in a knowledge-based economy. To encourage businesses to conduct high value-added activities and to create value-added activities, tax deduction is provided on spending on qualifying research and development activities. Tax allowance is also granted on the acquisition of qualifying intellectual property rights.

Introduced in Budget 2010, the Productivity and Innovation Credit provides additional tax deduction or allowance for qualifying activities to spur a broader range of innovative activities. These generous tax deductions or allowances are no doubt given to push for and inculcate an innovative culture in Singapore. It has not been easy — Singapore’s quest for productivity growth has not

yielded significant fruits fast enough. We remain hopeful that the planting of these innovation seeds will eventually make innovation pervasive in our economy.

Singapore’s move towards a fair and inclusive society

Tax policy can play a major role in making post-tax income distribution more equal. As the government moves to build a more inclusive society and mitigate inequality, the use of tax policy for social purposes has become more prevalent over the past decade. The government’s emphasis is not about how much to redistribute but about strengthening the core values that sustain a fair and inclusive society.

To temper inequality, a permanent Goods and Services Tax voucher scheme was introduced as a redistributive policy tool to help the lower-income households. To encourage the community to take responsibility, the enhanced deductions scheme was introduced for donations.

To help the lower-income households, various schemes were introduced. For example, the Workfare scheme is a permanent feature in our social security system. It includes the Workfare Training Support (WTS) which helps older lower-wage workers upgrade their skills through training. For employers, WTS also provide generous absentee payroll funding to encourage employers to send their lower-wage older workers for training. The Workfare Income Supplement (WIS), part of the Workfare scheme, is a tool used to redistribute incomes and temper inequality. It aims to reward older lower-wage workers in regular work and individual effort by providing Central Provident Fund (CPF) payouts. Let’s not forget the housing grants, education subsidies

and healthcare subsidies which have benefitted the middle-to-low income Singaporeans.

To transform our people with deep skills and knowledge, the government introduced the SkillsFuture programme. SkillsFuture emphasises a culture of lifelong learning for Singaporeans — this extends from the schooling years into their careers and even further into their silver years. It provides a whole array of education and training options for Singaporeans to develop their fullest potential, involving employers, unions and industry associations. This initiative speaks volumes of the inclusiveness and investment in Singaporeans — one of the economy’s greatest assets.

Tax policy — a continuous refinement and what’s to come

Clearly, Singapore has been refining its tax policy to raise revenue and to support and promote various economic and social goals. For example, a progressive property tax regime for residential property was introduced in Budget 2010 and enhanced subsequently. Prior to this progressive tax regime, property tax was levied at a flat rate for all residential properties.

Property tax is now the only form of tax on asset after the removal of estate duty in 2008. Then, the government felt that the estate duty was unduly impacting the middle and upper-middle groups disproportionately compared to wealthier ones. The government is of the view that a moderately progressive tax regime on property wealth is socially equitable — taxpayers with more valuable properties pay higher property tax. The same logic probably applies to more taxes on high-end assets, such as luxury cars.

23You and the Taxman Issue 4, 2015 |

Issue # – Month Year

2310th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Chung-Sim Siew Moon Partner and Head of Tax [email protected]

Siew Moon leads the Singapore Tax practice and is an International Tax Services Partner. She has over 30 years of experience providing tax compliance, controversy and advisory services to her multinational and local clients. She is experienced in negotiating and applying for tax incentives, advanced tax rulings, tax clarifications and remissions.

Russell Aubrey Partner, Transaction [email protected]

Russell leads the Transaction Tax practice in Singapore. He has more than 25 years of experience in providing tax due diligence and structuring advice on M&A. His experience includes corporate tax structuring for effective operating, ownership and financing structures. Russell pioneered the development of the tax regime for registered business trusts as listing vehicles in Singapore.

Contact us

As Singapore’s tax policy keeps pace with global reforms and developments, overarching this is the Organisation for Economic Co-operation and Development’s (OECD’s) Base Erosion and Profit Shifting (BEPS) project. Without doubt, Singapore is proactively responding to BEPS by ensuring that its tax policy and administration are aligned with global rules and OECD principles.

Singapore has rules and guidelines in place to address the BEPS concerns. These include general anti-avoidance provisions, transfer pricing provisions, guidance on income tax treatment on hybrid instruments and a robust incentive tax regime which is based on real substance and where business value is created. In addition, Singapore is committed to implementing the international standard on transparency and exchange of information on request, as well as participating and contributing to the peer review process.

From taxing income to taxing wealth?

The move to tax wealth, instead of income, is perhaps a step in the right direction. After all, “most researchers agree that wealth is much more unevenly distributed than income”, according to a report by American think tank Pew Research Centre published

in 2013. We have already seen tweaks to property taxes, stamp duties on properties and levies on car ownership. Further, a tweak was made to the marginal income tax rates of the top 5% of Singapore income earners. The tax rate increase for high-income earners from 20% to 22% in Year of Assessment 2017 will strengthen Singapore’s revenue position and enhance progressivity.

We may see more use of tax policy to redress inequality in wealth in time to come.

Perhaps using “sin taxes” in conjunction with wealth taxes could be an option in funding safety nets, including the social transfers. Higher duties on alcohol, betting and cigarettes mean more revenue, quite substantially when added together, for the government.

Use of tax policy in future

In his Budget Debate Round-up Speech 2015, Deputy Prime Minister and then Minister for Finance, Mr Tharman Shanmugaratnam said: “We cannot solve problems if we leave things entirely to the market and the natural workings of society. … But neither can we think that social policy interventions alone can create a fair and cohesive society, without a culture of personal responsibility …”

Inevitably, economic strategies are closely bound with social strategies and the use of tax policy to drive social and economic trends of the country is here to stay. The key is to continuously balance the collective responsibility with personal and family responsibility while maintaining relevance and competitiveness in a fast changing environment.

24 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition24 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

Evolution of Singapore’s tax policies

The tale of Singapore’s economic miracle — how a small country with no natural resources made the

leap from third world to first — has been recounted many times in the press. Indeed, Singapore’s GDP per capita increased a stunning 109 fold in the 49 years up to 20141. Out of more than 240 countries, Singapore’s absolute growth rate in the past 50 years is among the highest in the world. Putting the numbers in context, Singapore’s nominal GDP was on par with Mexico and Jamaica in 1965, but it has since caught up with the likes of developed nations like Germany and the US in 2014.

To promote its economic development, Singapore has successfully implemented astute policy decisions to ensure political stability, a robust regulatory system, superior infrastructure and a skilled workforce with the aim of encouraging investment

and international trade. All this, combined with pragmatic social policies, to improve the living standards of Singaporeans.

Singapore’s economy is powered by four main engines of growth: manufacturing (our largest sector), wholesale and retail trade, finance and insurance, and business services. Together, these sectors contributed to more than 60% of Singapore’s total GDP in 2014.

The sectors did not grow overnight nor by accident. With much foresight, the Singapore government recognised the importance of active industry development policy as a cornerstone of economic strategy. It assigned the responsibilities to promote and develop these sectors to mainly three government statutory boards: the Economic Development Board (EDB), International Enterprise Singapore (IE) and the Monetary Authority of Singapore (MAS).

Singapore tax incentives:

the Jubilee vantage point

Tan Bin Eng and Johanes Candra take stock of the success of Singapore’s incentives

schemes to promote investment, with guest contributions by EDB, MAS and IE Singapore.

1GDP per capita data published by the World Bank.

25You and the Taxman Issue 4, 2015 | 2510th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

The EDB is the lead agency that promotes, facilitates and supports investment in the manufacturing and services sectors of Singapore. EDB promotes investment in various industrial sectors that include but are not limited to electronics, petrochemical, pharmaceutical, transport engineering and clean technology.

As Singapore’s central bank, the MAS has a dual mandate to develop and supervise Singapore as a sound and progressive international financial centre.

IE is the government agency that spearheads the overseas growth of Singapore-based companies and promotes wholesale trade. Its vision is to establish a thriving business hub in Singapore with Globally Competitive Companies (GCCs) and leading international traders.

These agencies work with existing businesses as well as future investors to identify industry development priorities and strategies, and to develop tools required to achieve their goals. One such tool is the suite of incentives administered by these agencies to attract and retain businesses with substantive activities in Singapore.

Some of the incentive schemes have existed for a number of years — with some even pre-dating Singapore’s independence. But the scope and roles of these incentive schemes have since evolved and have been refined in tandem with Singapore’s economic development and priorities.

Here, we have invited leading policy makers from the EDB, MAS and IE to provide their views on the following:

• How Singapore’s business environment, tax policies and tax incentive schemes have contributed to Singapore’s economic success over the years

“The scope and roles of these incentive schemes have since evolved and have been refined in tandem with Singapore’s economic development and priorities.”

• How the incentives are likely to evolve over the next 10 years as Singapore enters a new phase of economic development

• The impact and results of the incentives to the growth of the economy

• Other critical factors that Singapore needs to maintain or grow to ensure our continued success

26 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition26 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

By Ms Jillian Lim, Executive Director, Business Environment, Economic Development Board (EDB)

Singapore accomplished a number of economic milestones over the last five decades. Faced with high unemployment rates and a reliance on entrepot trade in the 1960s and 1970s, to complement various measures to create an environment conducive to investments, the Economic Expansion Incentives Act was enacted to encourage industrial activities. In the 1980s and 1990s, the pressing need to upgrade our skills and move up the value chain prompted measures to encourage plant and machinery upgrading, while we continued to enhance our competitiveness by gradually reducing our corporate income tax rate. As the economy continued to evolve, Singapore turns to initiatives to promote skills, innovation and productivity to achieve sustained and inclusive growth.

The government continues to recognise the strong synergies between the manufacturing and services sectors and the need to diversify to cope with Singapore’s inherent vulnerabilities as a small, open economy. Since the late 1980s, Singapore has adopted policies to promote both sectors as twin engines of growth. Emphasis on growing our innovation and R&D base has drawn top scientific and creative talent and nurtured R&D collaborations between the public and private sectors. From the very start, EDB recognises that competitive and effective tax policies, while important, cannot in themselves attract and retain quality investment, skills and jobs if the non-tax factors

are not conducive for businesses. EDB works closely with the private and public sectors to improve the overall competitiveness of Singapore as a business hub in Asia and in the world. Today, Singapore is recognised as an internationally competitive business environment:

• Since 2007, Singapore has continued to top the global ranking on the ease of doing business in Doing Business reports by the World Bank

• Since 2011, Singapore rose to rank as the second most competitive in the world in the Global Competitiveness reports by the World Economic Forum

The achievements of Singapore’s economic development efforts are reflected in the leadership positions across a number of sectors:

• In oil trading and export refining, Singapore is among the top five hubs globally, with 1.38 million barrels per day of refining capacity

• In marine engineering, jack-up rigs accounting for 55% of global market share by value are built in Singapore

• In biomedical sciences, 6 out of the top 10 drugs are manufactured in Singapore

• In electronics, 40% of global hard disk drive media is manufactured in Singapore

• In aerospace, Singapore’s maintenance, repair and overhaul sector accounts for 10% of global MRO spend

• In logistics, Singapore is the world’s busiest transhipment hub, handling over 30 million TEUs a year and connected to 600 ports

Jillian Lim Executive DirectorBusiness EnvironmentEconomic Development Board (EDB)

EDB remains committed to attracting high quality and sustainable investments that are in line with Singapore’s stage of economic development, manpower and resource policies. EDB is also committed to helping existing companies and sectors strengthen their competitiveness and make more productive use of their resources. We are committed to supporting Singapore-based companies create new businesses through innovation, and in so doing, generate economic growth and good jobs for Singaporeans. Our tax incentives and policies will continue to evolve in order to meet the needs of the Singaporean economy, and to ensure that Singapore remains a conducive location from which businesses with substantive economic activities can grow.

27You and the Taxman Issue 4, 2015 |

Issue # – Month Year

2710th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

By Ms Carolyn Neo, Head, Financial Centre Development Department, Monetary Authority of Singapore (MAS)

The financial sector contributes significantly to Singapore’s economic growth, with its share of GDP doubling from an average of 6.4% in the 1970s to 11.8% in 2014. The financial sector has also contributed to employment growth. Its share of total employment has risen from an average of 4.2% in the 1990s to 5.4% in 2014. In absolute terms, employment in financial services has grown more than three-fold since 1990, to almost 200,000 finance professionals in 2014.

Singapore’s financial sector offers a broad range of financial services including banking, insurance, capital markets, asset management as well as treasury services to support the economic and financial activities of corporates and investors in Singapore and the region. Today, more than 700 financial institutions operate in Singapore. This has come about through strong and consistent efforts of MAS and the Singapore Government, to continuously enhance our business environment, strengthen our regulatory regime, develop excellent infrastructure, and build a rich pool of financial talent. MAS works closely with the industry to put in place a comprehensive range of training programmes to enhance the competencies of financial sector professionals and to strengthen the local talent pipeline of finance professionals and leaders.

Carolyn Neo Director and Department Head Financial Centre Development DepartmentMonetary Authority of Singapore (MAS)

Many jurisdictions have tax incentives to promote the financial sector. In Singapore, we believe that good tax incentives must be built on substance, and be properly designed and administered so as to ensure their effectiveness. The Financial Sector Incentive (FSI) scheme offers concessionary tax rates on income from qualifying financial activities. The FSI is granted for a limited period of time, and only to financial institutions with plans to establish or expand their substantive operations in Singapore. Incentive recipients are required to demonstrate growth of activities through increased headcount or business spending. They are also subject to annual reviews on the scale and quality of their economic contributions. The FSI scheme has a sunset clause to ensure that the relevance of the scheme is reviewed periodically.

Over the years, Singapore has provided a conducive environment for financial institutions that want to establish and grow their regional businesses in a strong and credible jurisdiction.

In the coming years, the growth of Singapore’s financial centre will be driven by key trends such as Asia’s rising economic importance, growth of a strong middle class, rising urbanisation, and rapid developments in financial technology and innovation. Singapore will continue to build strong capabilities across asset classes, maintain a strong and robust regulatory regime, and leverage on technology and innovation to achieve high-quality growth in the financial services sector.

28 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition28 | You and the Taxman Issue 4, 2015 10th anniversary commemorative edition

By Ms Gina Lim, Group Director, Trade Group, International Enterprise (IE) Singapore

Internationalisation With a limited domestic economy, venturing overseas enables Singapore companies to access a wider and more diversified consumer base. With economies of scale, Singapore companies are better able to innovate, develop new products and services and improve on their productivity.

IE Singapore has been supporting Singapore companies’ internationalisation efforts via the Double Tax Deduction for Internationalisation (DTDi). Expenses incurred during overseas market expansion and investment development activities such as trade fairs and market feasibility studies are eligible under the DTDi. In Singapore Budget 2015, this was expanded further to support the posting of Singaporeans to work abroad.

The International Growth Scheme (IGS) introduced in Budget 2015 supports Singapore companies with high growth potential to expand overseas, while their headquarters remains anchored in Singapore. The scheme aims to encourage companies to create international or international-facing job opportunities for Singaporeans. In doing so, companies are encouraged to grow their overseas presence and develop more Singaporeans as global business leaders.

Trade Services is one of the twin engines of the Singapore economy alongside manufacturing, and the wholesale trade is in turn the largest value-add contributor amongst the entire services sector, generating value-add of 16% of Singapore’s GDP in 2013.

Trade has been the lifeblood of Singapore’s economic journey, on account of our strategic geographical location. Singapore is a natural gateway to the expanding Asian markets and offers a robust, vibrant and advanced trading ecosystem. We have strengthened the value proposition of Singapore by building a vibrant trade infrastructure which includes but isn’t limited to areas such as financing, air and sea connectivity as well as anchoring key players from various geographies and commodities.

To continue building on our strength as a trading hub and to boost Singapore’s development as a regional hub for oil refining and commodities trading, the Global Trader Programme (GTP) was introduced in June 2001. The objective of GTP is to promote investments by international trading companies that are looking to set up an Asian headquarters, to serve the emerging Asian markets. The wholesale trade sector consists of more than 34,000 establishments in 2013 and only about 1% of these are under the GTP. Singapore is home to a large number of trading companies, spanning energy, agriculture and metals sectors. The wholesale trade sector is the second largest employer among service sector, with 327,100 employees and forms an integral part of our economy.

As GTP recipients’ trading operations in Singapore stabilise and mature, we urge them to consider growing further qualitative aspects of their trading operations. This would benefit all industry players and help contribute to the development of Singapore’s trading ecosystem. It includes tapping Singapore’s bond and capital markets, partnering with tertiary institutions on trading courses and/or providing internship opportunities for local students.

The trading community has also driven demand in ancillary services, such as the financial sector and the shipping and logistics sectors. Trade is interlinked with finance and the two sectors have a mutually beneficial relationship. Singapore is one of the largest corporate banking centres in Asia, with about 200 financial institutions providing services such as trade finance, corporate finance, loan syndication, cash management and transaction services. Many banks are expanding their trade finance offerings. Many trading companies have also expanded beyond trading activities to locate their logistics management functions to manage their supply chains or even set up separate shipping arm to charter vessels to transport their products, thereby increasing the vibrancy of the shipping and logistics sector in Singapore.

Singapore has a proven track record for delivering what businesses need. We are also a proven leading hub for global commodities trading in Asia. Singapore offers global businesses access to low-cost trade financing, sophisticated risk management solutions, world-class logistics and top trading talent. Besides a sophisticated financial infrastructure, our legal and regulatory framework is reliable and transparent. We also have a stable political environment that supports long-term business planning.

Gina Lim Group DirectorTrade GroupInternational Enterprise (IE) Singapore

29You and the Taxman Issue 4, 2015 | 2910th anniversary commemorative edition You and the Taxman Issue 4, 2015 |

Our view

Our interactions with multinational and Singapore clients alike suggest that Singapore’s stable and robust business environment are critical contributors to Singapore’s past and future successes. Tax incentive support for new investments certainly helps to sweeten the business case for selecting Singapore over other jurisdictions, but they are neither the sole nor the most important factor. New expansion or investment into unknown markets or regions is often fraught with uncertainties. It is no surprise that Singapore’s predictable business and investment policies are valued at a premium by businesses even as cost structures rise in step with the economic progress. Singapore continues to be recognised as the preferred manufacturing and headquarters outposts for multinationals within Southeast Asia or even the Asia-Pacific region.

While Singapore continues to fine-tune its policies to ensure that the investment environment remains conducive, the constantly changing economic and international tax landscape poses immediate and mid-term challenges to Singapore’s continued success. The on-going transformation of the Chinese economy could affect growth across Asia over the short term and might negatively influence the scale and timeline of companies’ expansion into the region — including Singapore.

In addition, the ongoing discussion among Organisation for Economic Co-operation and Development (OECD) members over base erosion and profit shifting (BEPS) is expected to yield a profound impact on the global tax environment. While the immediate impact of the BEPS project to Singapore remains uncertain and limited at most at this point, it adds a new layer of complexity and uncertainty to any new investment or expansion decision to be made by companies. This could translate to additional headwinds for Singapore’s growth.

To some observers, the challenges faced by Singapore today are unprecedented. Yet to many, it is perceived to be no greater than what Singapore’s founding members encountered and successfully overcame 50 years ago. If history is of any indication, Singapore’s willingness to face its challenges head-on, its careful planning and the ‘can-do’ spirit of its people will ensure that Singapore will continue to punch above its weight for at least another 50 years to come.