young drinkers fuelling development of new alcoholic beverage categories and brands 0906

TRANSCRIPT

think actbeyond mainstream

2016

August

Young drinkers fuelling develop-ment of new alcoholic beverage categories and brands

2 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

3t h E B i g

BEEr volumE is shrinkingwhile imported premium beers and new low-proof alcopops are emerging.

Page 4

spEcific occasions and EmotivE nEEdsare sought after by young drinkers.

Page 6

loyalty issuEsare faced by early successes in new brands and categorie.

Page 9

3THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

Young people born after the 1980s and 1990s (the post-90s and post-90s generations) have become a key consumer group, and are pursued by many consumer goods and retail brands. The population is enormous and their upbringing is very different to that of the post-70s generation that drove consumption in the past. A relatively abundant and internet-influenced childhood shaped them into a distinct consumer group in China. These young consumers embody four characteristics in terms of their consumption behavi-ours. Firstly, the niche market is emerging, and al-though they grew up in an era of mass consumption, they prefer products that have a personal touch. Typi-cal products often shout “for me” or “better me”. Se-condly, ‘lazy-consumption’ is prevailing; ease and con-venience rule. Thirdly, the stories behind brands and products are no longer constants; the motives for purchasing go beyond functions and features in this age of abundance. This is causing marketers to cons-tantly reiterate brand stories and bombard mobile so-cial networks with high frequency and varied content aimed at creating emotive associations. This form of communication is rapidly replacing the standardised approach of mass TV advertisements. Fourth, advances and credit consumption is increasing. The youths are aware of their own affordability limits and carefully seek credit financing when purchasing items that they deem necessary.

Driven by these four characteristics, young consumers have fueled a consumption revolution in various indus-tries. In the clothing industry, for instance, consumpti-on relies heavily on the internet and e-commerce. ‘Fast-fashion’ is emerging, where there is a focus on shorter product cycles and larger assortments to fit everyone's needs. In the food industry, ‘new catering' pays more attention to specialities and the personali-sed consumption experience. In the entertainment in-dustry, consumers emphasise the common experien-ces of social life and embrace innovation of recreational products – especially those on the internet. This diver-se, convenient and highly personal new type of consumption is marked by innovation and is pro-foundly influencing the landscape of alcohol consump-tion.

young consu-

mErs EmBody

four charactE-

ristics

highly Personal

diverse

innovation

convenient

slowEr growth in thE ovErall alcoholic BEvEragEs industry

nEgativE growth in BEEr and dramatic slowdown of spirits, including Both chi-nEsE and importEd spirits

EmErgEncE of importEd prEmium BEErs and nEw low-proof alcopops Bring nEw opportunitiEs

As China's economy transitions from high-speed de-velopment to the ‘new normal', national production and household consumption are changing according-ly. Alcoholic products, an important consumer goods category, have been experiencing slower growth in re-cent years. In 2014, the sales volume of major alcohols was about 86,016 million litres. From 2011 – 2014, the compound annual growth rate stood at 3%, compared to 8% from 2005 – 2011. Beer, as a major category of overall alcohol consumption, accounted for 60% of the market share, followed by wines, foreign wines and Chinese spirits. Compared with other product types, the consumption of new alcoholic beverages is relatively insignificant. a

the landscape is changing as the whole alcoholic beverages industry is growing more slow-ly

a2005-2014 salEs volumE of thE liquor mar-kEt [million-liter]

Source:IWSR database, Roland Berger analysis

'11-'14

+2%

+5%

+1%

+0%

+129%

Beers

'05-'11

+7%

+14%

+14%

+3%

+8%

cagr

WinesForeign Wines

Chinese spirits

cagr=3%cagr=8%

New alcoholic products

59%

17%

2005 2011 2014

17,3737,813

3,557

<1%10%

67%

7%<1%

13%

22%

60%

5% 1%

12%

23%

5%// //

4 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

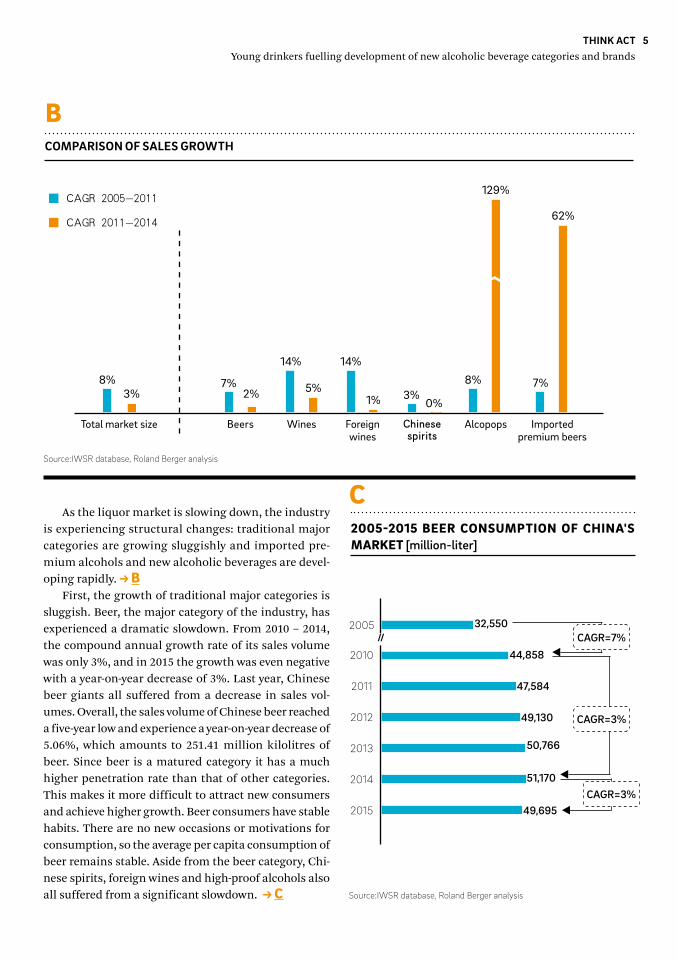

As the liquor market is slowing down, the industry is experiencing structural changes: traditional major categories are growing sluggishly and imported pre-mium alcohols and new alcoholic beverages are devel-oping rapidly. B

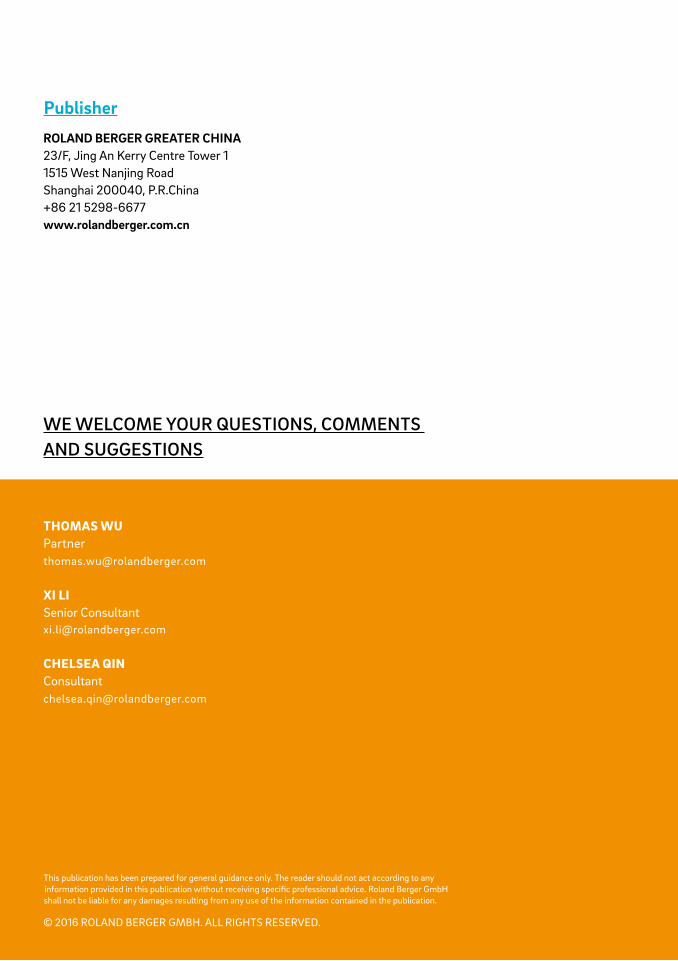

First, the growth of traditional major categories is sluggish. Beer, the major category of the industry, has experienced a dramatic slowdown. From 2010 – 2014, the compound annual growth rate of its sales volume was only 3%, and in 2015 the growth was even negative with a year-on-year decrease of 3%. Last year, Chinese beer giants all suffered from a decrease in sales vol-umes. Overall, the sales volume of Chinese beer reached a five-year low and experience a year-on-year decrease of 5.06%, which amounts to 251.41 million kilolitres of beer. Since beer is a matured category it has a much higher penetration rate than that of other categories. This makes it more difficult to attract new consumers and achieve higher growth. Beer consumers have stable habits. There are no new occasions or motivations for consumption, so the average per capita consumption of beer remains stable. Aside from the beer category, Chi-nese spirits, foreign wines and high-proof alcohols also all suffered from a significant slowdown. c

BCompArIsoN of sAles growTH

CAGR 2011-2014

CAGR 2005-2011

8%

129%

8%3%

7%2%

14%

5%

14%

1% 3%0%

7%

62%

Beers Wines Foreignwines

Chinese spirits

Alcopops Imported premium beers

Source:IWSR database, Roland Berger analysis

Total market size

c2005-2015 BEEr consumption of china's markEt [million-liter]

2015

2014

2013

2012

2011

2010

2005

49,695

51,170

50,766

49,130

47,584

44,858

32,550cagr=7%

cagr=3%

cagr=3%

//

Source:IWSR database, Roland Berger analysis

5THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

leading brands. From the point of sales perspective, however, this they will remain stable and develop soundly. Big stores and supermarkets remain optimis-tic about the future of alcopops and most are even con-sidering increase the shelf space dedicated them. Be-sides, flavoured beers have a relatively small market size, but the introduction of imported brands is causing this market to become a second highlight. Some do-mestic alcohol companies are investing in the develop-ment and sales of flavoured beers with the hope of gain-ing a head start in the market. E

Compared with the beer market’s sluggish growth, imported premium beer and new low-proof alcopops experienced fast development and are becoming two highlights in the currently depressed market.

Imported beers and premium beers have been booming, which is driven by the trade-up from stan-dard beer. In 2014, sales volume of imported beers reached 3,168 million litres compared to 504 million li-tres in 2011. From 2011 to 2014 the average year-on-year increase was 62% compared to 7% from 2005 to 2011. In light of this, Chinese beer giants are restructuring their product mix and focusing on the development of premi-um beers. Zhujiang Beer has forged its premium brand ‘Supra’ and brought it to market. Similarly, Tsingtao Beer’s ‘Whole Wheat White Beer’, Snowbeer’s ‘Lianpu’ and Yanjing Beer’s draught beer products have also been introduced. d

With the rapid development of new low-proof alco-pops (or RTDs), diversified and personalised products further accelerated the trading-up from standard beer. The alcopops, led by brands like RIO, have realised a compound growth rate of 153% over the past five years. In 2015, the alcopop category experienced some fluctu-ations due to misjudgement and overstocking of the

d2005-2014 salEs volumE of importEd BEErs of thE chinEsE markEt [million-liter]

2005 2011 2014 // //

3,168

747504

cagr=62%

cagr=7%

Source:IWSR database, Roland Berger analysis

E2005-2014 salEs volumE of alcopops of thE chinEsE markEt [million rmb]

2015

2014

2013

2012

2011

2010

2005

3,920

1,600

760

242

77

81

116 cagr=153%

//

Source:IWSR database, Roland Berger analysis

6 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

In general, young consumers primarily purchase low-proof alcoholic beverages. Among such products, beers are still the main consumption choice for the younger population: When we studied last consumption occa-sions, for the under 30s, over 50% of consumption was beer, 18% was new alcoholic beverages. Traditional high-proof alcohols only took up a limited proportion of their choices. New alcoholic beverages, on the other hand, are mainly consumed by young people: 50% of the category was consumed by under 30s within their last alcohol con-sumption occasions. This is significantly higher than the comparable figure for other alcohol categories.

Young consumers’ preference for low-proof alco-hols is attributable to two things. First, as budding alcohol consumers, their tastes and consumption hab-its for high-proof alcohols have yet to be developed. Second, and more importantly, alcoholic beverages are more of a networking facilitator. Young consumers tend to go for these drinks on networking occasions so as to maintain a relaxing and enjoyable social vibe rather than simply trying to get drunk. f

With respect to consumption occasions, regular beers and high-proof alcohols remain relatively stable. Family and friend get-togethers, as well as ready-to-

young drinkErs mainly purchasE low-proof alcoholic BEvEragEs

nEw alcoholic BEvEragEs arE incrEasingly focusEd on family and friEnds gEt-togEth-Ers as wEll as fEm alE consumption occasions

for family and friEnds gEt-togEthErs, thErE is a tEndEncy towards morE mixEd-gEndEr consumption occasions and thErEforE a grEatEr nEEd for product divErsification (particularly alcoholic BEvEragEs for womEn); nEw alcoholic BEvEragEs arE fit for thE consumption occasions of young consumErs

nEw alcoholic BEvEragEs can satisfy thE Emotional valuEs of young consumErs via concEpts of individualisEd and fashionaBlE products; thEsE products activEly sprEad such concEpts.

young consumers’ individual-ised and diversified consump-tion habits promote the indus-try’s up-trading from standard beer and category development

7THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

fhaBits of young alcohol consumErs

sHAres of AlCoHol CoNsUmpTIoN for THe popUlATIoN UNDer 30 [%]

beers chinese sPirits Foreign wines

g

Beers Wines Foreign wines

Chinese spirits

Flavored beers

Alcopops

32 34

50 48

28 27

Source:Roland Berger market research, Roland Berger analysis

high-proof alcohols Traditional low-alcohol products New low-alcohol products

52%Beers

13%Wines

11%Alcopops

7%Flavored beers

8%Chinese spirits

7%Others2%

Foreign wines

get-togethers of a few friends at home

large family reunions

tasting at home

drinking while playing poker or board games or watching matches at home

get-togethers atKtvs or nightclubs

18get-togethers of a few friends at home

get-togethers at medium- level restaurants

tasting at home

large family reunions

drinking at homefor relaxation

13

11

10

10

9

22

13

13

11

7

13

7

7

7

Ready-to-drink/Alcohol consumption in restaurants or entertainment facilities Family/Friend reunions

consUmPtion oF the PoPUlation Under 30 for DIffereNT proDUCTs [%]

top 5 scEnarios of tradition alcoholic BEvEragEs consumption [%]

Source: Roland Berger market research, Roland Berger analysis

get-togethers of a few friends at home

high-end restaurants

Fansy parties atdisco bars/downtempo bars

get-togethers atKtvs or nightclubs

get-togethers atmedium-level restaurants

8 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

are equally important occasions for consumers of all ages. However, each age band exhibits different feature within the scenario. The most distinctive characteristic of young consumers' get-togethers is the mix of both genders, which even out in such occasions. Conse-quently, taking the consumption experience of women into account, these consumers tend to choose new alco-holic beverages that are similar in taste to soft drinks with a light alcoholic flavour. According to the survey, the proportion of female consumers that purchase new alcoholic beverages is markedly higher than for other categories; they account for 70% of alcopops and 58% of flavoured beers. For regular beers, the proportion stands at only 45% and is even lower for high-proof al-coholic beverages. J

Finally, the younger population’s pursuit of emo-tional values and diverse, individualised and trendy products is satisfied by the product concept and experi-ence of new alcoholic beverages.

Compared to traditional beverages, new alcoholic beverages offer product flavours that are different and more varied. The alcopops and fruit beers on the mar-ket often have multiple flavours. They use syrups and juices to produce flavours that are similar in taste to

drink occasions, are of equal importance. Regular beers, Chinese spirits and foreign wines are consumed in a number of different ready-to-drink consumption occasions, and the consumption habits of each scenar-io tend to be relatively stable. Regular beers are mainly consumed at banquets and casual karaoke get-togeth-ers with friends; Chinese spirits are most often bought at restaurant and banquet occasions; foreign wines ap-pear largely at restaurants, bars, parties and get-togeth-ers. g

In contrast, new alcohol beverages tend to be more focused on family and friend get-togethers, with particu-lar importance attached to female consumptions occa-sions. Take the example of alcopops: according to the survey four of the top five consumption occasions are family and friend get-togethers, which is significantly more than for other categories. In addition, new alcohol beverages place a greater focus on female consumption, and so the proportion of female consumption occasions is extremely high compared to that of other alcohols. Oc-casions such as ‘get-together with girl besties’ top the charts of scenario rankings in this category. h i

In terms of alcohol consumption occasions seg-mented by age bands, family and friend get-togethers

h

11

10

10

Ready to drink/Alcohol consumption in restaurants or entertainment facilities

Family/Friends reunions

10

10

16

8

8

7

6

Consumption of females

top 5 scEnarios of nEw alcoholic BEvEragEs consumption [%]

get-togethers of a few friends at home

get-together of femalebesties at home

tasting at home

get-togethers atKtvs or nightclubs

drinking at homefor relaxation

get-togethers of a few friends at home

get-together of femalebesties at small bars

get-together of femalebesties at home

high-end restaurants

get-togethers atKtvs or nightclubs

Source: Roland Berger market research, Roland Berger analysis

9THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

alcoPoPs Flavored beers

i

Bar-related scenarios

KTVs scenarios

10%

Restau-rant-related

scenarios

Family/Friend

reunions

19%14%

55%

16%11%

22%

48%

16%12%

24%

46%

13%9%

27%

47%

<=20 yeArs olD 21-30 yeArs olD

31-40 yeArs olD >40 yeArs olD

Source: Roland Berger market research, Roland Berger analysis

proportion of consumption of diffErEnt agE groups [%]

Bar-related scenarios

KTVs scenarios

Restau-rant-related

scenarios

Family/Friend

reunions

Bar-related scenarios

KTVs scenarios

Restau-rant-related

scenarios

Family/Friend

reunions

Bar-related scenarios

KTVs scenarios

Restau-rant-related

scenarios

Family/Friend

reunions

10 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

believe they are reasonably prices. This is because they have established an independent brand image in the eyes of young consumers through flavour diversification, individualised packaging and a differentiate product concept. As a result, the prices of these products do not get compared with the those of regular beers. The high profit margin brought about by the high price leads to valuable opportunities to increase ROIs at the initial de-velopment stage of new alcoholic beverages. l m

soft drinks, thereby catering to the needs of young fe-male consumers in particular. Our survey suggests that 40% of new alcoholic beverage consumers purchase these products to ‘try out new and different flavours’, and another 45% buy them because they ‘taste good’.

In terms of product concept and packing, new alco-holic beverages also appeal emotionally to young con-sumers. In contrast to traditional beers, they use bright colours for packaging to meet aesthetic preferences: 24% of consumers choose them because ‘the bottle or pack-age looks attractive'. Meanwhile, for publicity campaigns, new alcoholic beverages tend to choose younger pop idols, directly advertise in reality shows, and use online programs that young people like to spend time on. They spread emotional messages such as ‘freedom', ‘indepen-dence', and ‘fun', and therefore cater better to the values of young people; 18% of consumers choose these prod-ucts because they ‘identify with the product'. k

Considering the above factors, young consumers more easily accept the higher price levels of new alcohol-ic beverages. Even though they are four to five times more expensive than regular beers, 90% of consumers

J k

Low-alcohol products

Alcohols Flavored Beers

100% 100% 100%

30%

70%

42%

58%45%

55%

Female MaleFlavor

Tasting good

Trying something new

Good for health

45

40

29

28

24

Packaging and product positioning

20

20

19

18

17

gEndEr distriBution of consumErs [%]

Source: Roland Berger market research, Roland Berger analysis

top 10 rEasons of drinking nEw alcoholic products [%]

Not easy to get drunk

Attractive packaging

Friends’ recommendation

Other friends may like it too

Authentic ingredients

Match for the ordered food

Not losing face

All the guest will like it

Source: Roland Berger market research, Roland Berger analysis

11THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

l

CeIlINg of prICe ACCepTANCe

m

beers

Flavored beers

alcopops

imported beers

23

45

67

89

1011

1212.5

1314

1516

1718

Top price

Average price

Lowest price

RMB 0

100%

RMB 5 RMB 10 RMB 15 RMB 20 RMB 25 RMB 30 RMB 35 RMB 40 RMB 45 RMB 50

100% 100%

86%

70%

51%43%

26%20%

10% 7%

pricE comparison of low-proof alcohols [rmb/275 milliliter]

pricE accEptancE of nEw alcoholic BEvEragEs [rmb/bottle]

Source: Roland Berger market research, Roland Berger analysis

Source: market investigation, case study, Roland Berger analysis

12 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

within the last three years. Amazingly, 27% only drank them for the first time within the last year. This shows that new alcoholic beverages are excellent at bringing in new consumers. Since they mainly target young con-sumers, this could be the key transitional category; it transitions young people from mainly drinking non-al-coholic beverages towards frequent alcohol consump-tion. New alcoholic beverages, therefore, provide an opportunity to bring in young consumers and shape their consumption habits, and in so doing, drive the sales of other mature alcohol categories.

In fact, the industry giants have already tasted the sweet taste of the success of new alcoholic beverages on a global level. Motivated by the fast growth of China's market, they are exploring their business in China by tailoring them to its unique consumption demands. Budweiser, for example, tailored its already globally successful alcopops for the Chinese market, putting them on sale in 2015. Compared with the standard global products, China's version of Mixxtail has bright-er and more vibrant packaging. When it comes to branding, Mixxtail tends to go for young and popular idols for commercial endorsement and promotes itself via the internet. Backed by the brand Budweiser, Mixx-tail sells the alcopop concept, attracting a lot of atten-tion and achieving fast growth in only a few months.

For new alcoholic beverages to develop, the key is to meet young consumers' diversified consumption re-quirements through the constant introduction of inno-vative products into the market. During this process, category management will become increasingly diffi-

nEw alcoholic BEvEragEs catEr to thE uniquE consumption haBits of young con-sumErs. this not only of grEat importancE for capturing nEw consumEr groups But also for shaping consumption haBits and Building Brand loyalty

thE industry giants havE achiEvEd gloBal succEss aftEr vEnturing into nEw alcohol-ic BEvEragEs, and thEy achiEvEd fast growth in china through a sEriEs of locali-sation attEmpts

nEw alcoholic BEvEragEs can win thE mar-kEt through product innovation. thEy also nEEd maturE managEmEnt of catEgoriEs and thE supply chain

thE ExpEriEncE of thE gloBal markEt indi-catEs that nEw alcoholic BEvEragEs still havE hugE potEntial in china

New alcoholic beverages cater to the unique consump-tion habits of young consumers. This is of great signifi-cance as it not only allows new consumer groups to be covered but could also play an important part in culti-vating consumption habits and brand loyalty. Since the development of new alcoholic beverages is very recent, over 60% of consumers drank them for the first time

new alcoholic beverages are the key to the growth of the industry

13THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

AlCopop mArKeT sIze AgAINsT beer mArKeT sIze [%]

n

Australia Japan The UK ChinaThe United States

22.4%

1.1%

12.1%

5.5%4.5%

cult and so mature management will be demanded from these companies. They must come up with a tar-geted strategy of category planning based on market demand, their products' traits and their channels' fea-tures. They should also try and reach equilibrium be-tween the promotion of a single category and the total sales of all their products. As product variety and SKU increase, companies must become increasingly compe-tent at supply chain management. The supply chain must respond quickly to changes, and production and sales must be integrated to minimise the cost pressure resulting from a long tail of products. The management difficulty will surpass that of traditional wines and

come close to that of soft drinks such as ready-to-drink tea beverages.

New alcoholic beverages have experienced explosive growth, but their growth potential should not be under-estimated. New low-proof alcohols are still in their in-fancy in China compared with mature markets in other countries. Currently, sales volumes of alcopops at points of sales stand at 6 billion RMB, only 1.1% of that of beer. The ratio between the two markets is high in America, Japan and Australia. This is a strong indica-tion that in China, there is still enormous potential for new alcoholic beverages that can be tapped into. n

markEt pEnEtration ratE of nEw alcoholic BEvEragEs

Source: market investigation, case study, Roland Berger analysis

14 THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

aBout usRoland Berger, founded in 1967, is the only leading global consultancy of German heritage and European origin. With 2,400 employees working from 36 countries, we have successful operations in all major international markets. Our 50 offices are located in the key global business hubs. The consultancy is an independent partnership owned exclusively by 220 Partners.

orDer AND DowNloADwww.rolandberger.com

links & likes

15THINK ACTYoung drinkers fuelling development of new alcoholic beverage categories and brands

We Welcome your questions, comments and suggestions

publisher

thomas wu [email protected]

xi liSenior [email protected]

chElsEa [email protected]

This publication has been prepared for general guidance only. The reader should not act according to any information provided in this publication without receiving specific professional advice. Roland Berger GmbH shall not be liable for any damages resulting from any use of the information contained in the publication.

© 2016 ROlANd BERGER GMBH. All RIGHTS RESERVEd.

rolAND berger greATer CHINA23/F, Jing An Kerry Centre Tower 11515 West Nanjing RoadShanghai 200040, P.R.China+86 21 5298-6677www.rolandberger.com.cn