your guide to bridging finance - gw.legal · your guide to bridging finance ... finance. the most...

TRANSCRIPT

Your guide to Bridging Finance

0345 373 3737

General Terms and Conditions15 - 18

Acceptance of Instructions to Act

Data Protection

Regulation

Copyright

Law and Jurisdiction

Electronic ID

Your File

Call Recording

Copies of Calls

Using your Information

Confidentiality

Money Laundering

Interest

Limitation of Liability

Electronic Communication

Rights

Distance Selling

Your Right to Complain Banking Crisis Client Balances Assessment

Bridging Finance Terms and Conditions18 - 24

Your Mortgage

Cancellation Fee

A Serious Warning

Confirming the Details

Conflict of Interest

Ending the Relationship

Referral

Your Best Interests

Legal and Admin Fee

Block Policies

Unsecured Loans

Local Searches

Stamp Duty Land Tax (SDLT)

Exceptional Expenses

Ambersearches

Telegraphic Transfer Fee

Payment of Costs

Financial Services Insurance

Marketing

Conveyancing Quality Scheme Lawyer Checker

Bank Account Checker

Glossary

1. What you can expect from GWlegal

2. What is Bridging?

3. The Risks Explained 5. The Process

7. Identification

8. Our Fees 9. The GWaccount

10. Everyday Legal 11. Premier Client Club 12. Recommend a Friend

13. Frequently Asked Questions

Contents

You’ve found the perfect property and need to get things sorted quickly! Bridging Finance could be the best way to achieve your goal.Bridging is a highly specialised area and therefore it is vital that you have the best in the business helping you along to make the whole process as simple and as straightforward as it can be. With over 30 years’ experience, GWlegal is a leading national law firm and a bridging legal expert. The firm is a prolific player in the legal property market and has been bestowed with many awards including most recently “Best Legal Service Provider” at the Your Mortgage Awards and “Business Leader in Conveyancing” at the British Mortgage Awards.

By trusting your bridging to GWlegal, you’ll get:

• The whole process explained from the start

• Friendly and knowledgeable staff who are available for extended hours (9:15 – 5:15pm Mon - Fri)

• Regular updates by wphone and/or in writing, was your case progresses

• Fixed costs, so no nasty hidden surprises

With the help of this brochure, we’ll take you step-by-step through your bridging journey.

The first section explains what happens in the conveyancing process, outlining what you need to do and what we’ll do for you as well as highlighting the risks involved.

The second section, called Terms and Conditions of Service, details specific information about GWlegal and your bridging journey. It includes such information about how we use your information, our complaints procedure, information about fees and a glossary. We appreciate that there is a lot of information to take in, but please take the time to read it all. It could be instrumental in helping you complete sooner.

What you can expect from GWlegal

1

What is Bridging?

A bridging loan, or short-term loan as it is often known, is a method of refinancing a property or financing the purchase of a property for a short period of time, typically until the buyer receives an anticipated inflow of cash such as the sale of their existing property.

In other words, this short term secured loan ‘bridges the gap’ until the buyer is in a position to finance the purchase in a more standardised manner (e.g. with a standard mortgage).

When would I take out a Bridging Loan?

For the right client, in the right circumstances, bridging can be a valuable funding tool. There are many situations where bridging could offer a suitable alternative.

Short term loans are used for a number of reasons. These range from conventional bridging, which is where a homeowner wishes to purchase a new home but is unable to sell their current property, to auction finance or business loans.

Short term loans are generally suited to borrowers who want money quicker than can be obtained from mainstream lenders such as banks and building societies, or where they will not lend due to the current state of the property e.g. where it needs a kitchen or bathroom installed to make it habitable, or due to their underwriting criteria.

As the name implies, the loans are only suited to those who need the money for a short time. They are not suitable as a replacement for long term finance. The most important aspect of taking out a short term loan is making sure you can repay it by the due date.

2

If you do not have a viable exit strategy, or think that there is a strong risk the planned exit will not work, you should consider very carefully whether to proceed. You will be at considerable risk of losing the property if you fail to repay the loan at the end of the term.

Secured loans and Law of Property Act (LPA) Receivers

When you take out a bridging loan, you need to provide the lender with some form of security in addition to your promise to pay. For the purposes of a bridging loan, the security offered will be a

The Risks: Explained

GWlegal advises anyone considering a bridging loan to be fully aware of the risks involved and have a realistic exit strategy to minimise the total cost.

legal charge i.e. a mortgage against your land or property. Although the land or property remains in your possession, and you continue to enjoy the use of it, the lender can take steps to repossess it if any of the following occur: • You do not pay the interest due at the agreed time • You fail to repay the loan by the end of the term, and/or • You breach your agreement with the lender in some other way e.g. you let your

property out without consent.

In some circumstances the lender may not wish to repossess the property e.g. there is a slump in the market. If this is the case, the lender has the right but not the obligation to appoint an LPA Receiver who will then manage the property on its behalf.

An LPA Receiver has such powers as the right to sell or receive an income from the property e.g. find tenants to reside in it.

3

The Risks: Explained

Should you find yourself in this position, it is essential you contact your lender as quickly as possible to advise them of your situation and agree a course of action. Avoiding contact will make matters worse; where there is no dialogue; lenders have no real alternative but court action.

Arrears and Repossessions

Should you find that you are unable to make your repayments under the loan agreement and fall into arrears, it is likely you will incur further fees and charges.

Arrears fees may be a set monthly charge, an amount per missed payment or an amount for each month the loan is in arrears. You may also be charged if the lender has to chase a payment or if the payment bounces. This should all be explained to you and set out in writing as part of your loan agreement.

If you fail to keep up your payments, repay your loan on time or breach a condition of your loan, the lender can commence legal proceedings to repossess whichever property or properties the loan is secured against (even your own residential home). Once the lender gains a possession order from the courts it can then seek to obtain an eviction order to make you leave the property. The lender can then sell the property in order to recover the money you borrowed plus any additional costs incurred in recovering the money and any accumulated interest and charges.

While the property does not become the lender’s it does acquire the right to sell it.

If you have more than one mortgage the lender will use the sale proceeds to pay off all or as much as possible of the mortgage debts owed. Any surplus left over will be passed to you.

If the sale proceeds of the property are not enough to repay all of the amounts owed, the lender can pursue you through the courts for the shortfall. This is particularly important to bear in mind when you have other assets e.g. your own home that has not been used as security for the mortgage as a charging order can be placed against these by the courts and an order of sale can be obtained.

4

The Process

Starter for 10 . . .

Now you are fully aware of the risks involved with bridging loans, it’s time to start your journey. It may look complicated but, don’t worry, you’ll be the owner of your property before you know it. Before we get started, there are a few things we need to check off the list. Given the risks associated with taking out a bridging loan, it is essential to make sure you can afford the repayments from the start.

There are a number of things to consider to ensure you can afford to take out a bridging loan and your Introducer will be able to explain them in full detail. Please be aware we are not authorised to give financial advice. The information throughout this brochure is for your general understanding. If you require any further information or have any questions regarding the financial aspects of short term loans you must consult your Introducer.

The APR reflects the true cost of the loan and includes all of the interest together with any other charges. This may make it easier for you to compare the true cost of borrowing between different lenders for the same loan amount and term.

Generally speaking, the shorter the term of the loan the higher the APR is likely to be because there is less of a period to spread the cost of charges and fees.

Most short term loans are on a fixed rate basis. This means the interest you are charged remains the same throughout the term of the loan so you know exactly how much you are required to pay each month and can budget accordingly.

It is possible to get a short term loan on a variable rate basis. Having a variable rate means the amount you are charged can rise and fall each month. It is advisable that you check what basis the loan is set on i.e. the Bank of England base rate.

However some fixed and variable rate loans can have the rate changed if you do not repay the loan on time, fail to make payments on time or breach your agreement in any other way.

It is important to ensure you request the right length of term at the outset as failure to repay the loan on time may incur additional costs. Selling a property and refinancing arrangements often take longer than you think so it is usually best to build in some leeway into the term.

Short term lenders do not generally charge extra for having a longer term at the outset, but you will need to check if there are any charges for repaying the loan before the end of the term.

If you have any further questions, please speak to your Introducer.

Annual Percentage Rate (APR)

Fixed vs. Variable Choosing the term of your loan

5

The Process

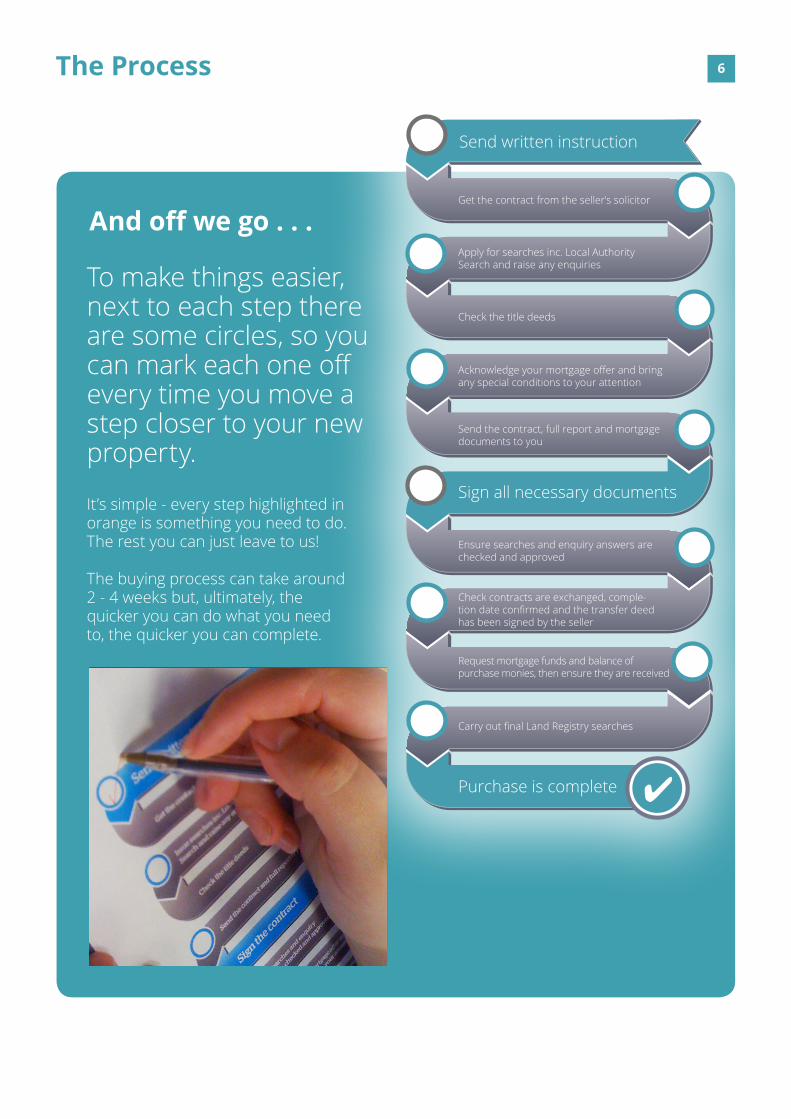

And off we go . . .

Send written instruction

Get the contract from the seller’s solicitor

Apply for searches inc. Local AuthoritySearch and raise any enquiries

Check the title deeds

Acknowledge your mortgage offer and bring any special conditions to your attention

Send the contract, full report and mortgage documents to you

Sign all necessary documents

Purchase is complete

Ensure searches and enquiry answers are checked and approved

Check contracts are exchanged, comple-tion date confirmed and the transfer deed has been signed by the seller

Request mortgage funds and balance ofpurchase monies, then ensure they are received

Carry out final Land Registry searches

To make things easier, next to each step there are some circles, so you can mark each one off every time you move a step closer to your new property. It’s simple - every step highlighted in orange is something you need to do. The rest you can just leave to us! The buying process can take around 2 - 4 weeks but, ultimately, the quicker you can do what you need to, the quicker you can complete.

6

Identification

We must check the identity of all our clients under the Money Laundering Act 2007 for any regulated work that we do. We do this by obtaining Photo ID and Proof of Residence identification.

For the majority of clients using the services of an Introducer, their Introducer will provide us with the appropriate documentation. There may be a small number of cases in which we still need to ask you to provide us with original ID.

If you have come to us directly, we will require you to send us original ID through the post.

We will also need to carry out an additional electronic check of your identification. This is because we have not met you face to face and we want to make absolutely certain that you’re not the victim of mortgage fraud.

We take fraud very seriously and incorporate many anti-fraud measures into our procedures. We hope you feel reassured by our approach.

There may be rare exceptions to the above but we’ll let you know as soon as we can ifthat’s the case.

We require one of the following forms of identification per person from list one and two from list two here:

Any photo ID must be clear and legible otherwise you may be required to resubmit.

Any proof of residence identification must be dated within 3 months of the file instruction.

Please ensure when sending or returning items by Special/Recorded Delivery, your full reference number is quoted on the envelope.

?

List one: Photo I.D.

• Valid passport

• Valid photo driving licence with current address

• A current, signed passport issued by a Non EEA Country with either a passport stamp or a letter from the Home Office giving an indefinite right to reside in the UK.

List two: Proof of Residence

• Utility bill

• Bank or credit card statement

• Official government/ agency correspondence

Important

Our requirements are as follows:

7

At GWlegal, we prefer to be upfront and honest about our costs. After all, if your fees are as competitive as ours, you’ve got nothing to hide.

Our Fees

Our charges will be fully explained in our initial letter to you. However your bridging loan may be subject to a variety of fees and charges levied by the lender and/or your Introducer. The most common fees include:

For more information about any of these charges, please refer to the glossary at the back of this brochure or speak to your Introducer.

• Arrears fees

• Facility fee

• Introducer arrangement fee

• Indemnity insurance

• Valuation insurance

• Arrangement fee

• Valuation fee

• Lenders legal fees

• Telegraphic transfer fee

• Mortgage administration repayment charge

• Exit fee

• Legal fees on redemption

8

Stay up to date with your case as well as upload documents, make payments and ask any questions you have…even when the office is closed with your own GWlegal account.

View and update account detailsView case progressSend messages relating to a case

By creating an account, you’ll be able to:

Make payments relating to a caseLeave feedbackUpload documents

We believe that by enabling you to have access to your case and understand the key milestones which have been or need to be completed will not only improve your experience but also help speed up your case.

Get the AppGet instant access to your case by downloading the free GWapp.

What’s more, enable the push notifications and you’ll receive immediate updates as your case progresses.

Available on Android and iPhone, simply search for ‘GW Solicitors’ in the App Store or on Google Play.

The GWaccount 9

Everyday Legal

Whilst you need our assistance in your current case, not every legal issue needs the professional advice of a solicitor. Often you

Free legal help from GWlegal

That’s what Everyday Legal, our free advice service, is all about… equipping you with the right information so you can solve the problem yourself whether it’s reclaiming unfair charges, resolving disputes or wanting to know your consumer rights.

can handle the situation on your own – you just need a few pointers.

Topics include:

• Energy bill refunds

• How to claim for pothole damage

• Resolving property boundary disputes

• Your legal rights when buying a used car

• Dealing with noisy neighbours.

Everyday Legal is available on our website – gw.legal - as well as through our free mobile app. Simply search GW Solicitors in the App Store or Google Play.

10

At GWlegal, we value loyalty. This is why we created our Premier Client Club – to reward customers who, having already benefitted from our services, come back when they need a solicitor again.

Premier Client Club

As a member, you’ll benefit from all this:

Standard fees for any future conveyancing or remortgage work*

Fees for any Wills and Power of Attorney services*

* not including VAT/Disbursements

But it isn’t just you who can benefit from these discounts!Recommend family and friends to us as we’ll extend these discounts to them too. Now you can’t say fairer than that!

Premier Client Club costs just £40 (+VAT) and could more than pay for itself in just one future transaction.

You’ll be given the opportunity to join during your current case with us. Please visit gw.legal for more information.

11

Recommend a FriendImpressed by our service? We sure hope so! Then why not recommend us to your friends and family and earn up to £250 for your effort.

How much could you earn?Service You get

Conveyancing Up to £100^

Remortgage £25

Wills £20

Personal Injury £250

Financial Claims (PPI) £50

It’s so easy to recommend us to family and friends. Simply log on or create a GWlegal account by visiting gw.legal. Click on the Recommend a Friend button and simply enter your friend’s email address and the service you are recommending. Hit send and off it goes to your friend’s inbox.

You can then keep an eye on if they follow your recommendation and take up our services, and ultimately if and when you’ll get paid, through your own personal dashboard.

Don’t forget, if you’re a Premier Client Club member, your relative or friend will also be entitled to discounts on our services*. Might be worth mentioning that to them as an extra incentive!

^Earn £50 for a single sale or purchase case and £100 for a combined sale and purchase case*Premier client club members and their family and friends are entitled to 25% of our conveyancing and remortgage fees and 10% of our Wills service. Not including VAT and disbursements

12

Frequently Asked Questions

Why is the interest rate on a bridging loan higher than a standard mortgage?

The interest rate on short term loans is generally higher than that of long term loans because short term finance is provided to meet a particular short term need, and a bridging lender does not enjoy the benefit of receiving interest for long term use of its money. The bridging lender is also offering a bespoke service and has to operate at speeds and levels of service which the longer term lenders cannot match. The costs incurred by bridging lenders therefore tend to be higher than those of long term lenders in order to provide the service required.

How do I pay the interest due on my loan?

There are three basic methods which bridging lenders use for borrowers to pay the interest due on the loan: paying monthly, retained interest and rolled up interest.

Paying monthly is, as it suggests, where you pay the interest due each month.

Retained interest is where you borrow the interest payments due on the loan in addition to the loan amount you require. The extra amount is held by the lender (retained) and used to meet your monthly payments. You may be required to pay interest on the amount of interest payments retained.Rolled up interest works by adding the interest due each month to the loan balance. Interest is calculated each month based on the balance then outstanding i.e. interest on the interest.

There are various combinations of these approaches available in the market. Some lenders offer the opportunity to retain interest for only part of the loan e.g. six months of a nine month loan. This approach is sometimes used when a borrower believes he will definitely be able to repay the loan within, say, six months but wants the flexibility of having a bit longer if need be. The borrower will, however, need to make sure they can make the payments for the other three months if they cannot repay after the retained period ends.

When do I have to repay the loan?

Generally the loan will need to be repaid by a set date i.e. the term. This is often referred to as redemption.

It is your responsibility to make sure you can repay the loan on or before the end of the term. You should only enter into the transaction if you are confident that you will be able to achieve this. Remember failure to do so can result in action being taken against you, further costs and fees being added to your loan and, as a last resort, repossession of the property.

Typically loans are repaid either by the sale of the property the loan is secured against or refinancing the loan with another lender. It is important to consider the risk that you may not be able to achieve your planned exit (redemption) in the required timescale before committing to the agreement.

13

Frequently Asked QuestionsWhat happens if I am not able to repay my loan at the agreed time?

Sometimes things do not go according to plan and you may find yourself in a position of not being able to repay your loan at the agreed time. The important thing is to contact your mortgage lender as soon as possible to discuss your position.

Lenders will generally look to reach sensible arrangements with you and extend your loan term unless there are specific reasons why they cannot extend on your particular circumstances.

You should be aware that there may be additional costs and charges incurred if you do not repay on time. Many Bridging lenders charge fees for extending the term or for failure to repay on time. It is therefore possible that the lender may also increase the interest rate when this occurs.

What if I already have a mortgage on my property?

It is possible to have more

than one mortgage on a property. The later, second mortgage is often referred to as second charge or secured loan lending.

The charge is still a mortgage and should not be treated differently.

A charge will be referred to as a first charge (your first mortgage), second charge (your additional mortgage), third charge (a third mortgage) etc. The number of the charge i.e. first, second etc. generally determines the order in which the lenders have the right to any money from the sale of the property. There may be circumstances where this is changed due to deeds of postponement where one lender agrees to postpone the priority of their charge in favour of a ‘later’ charge by another lender.

This does not change the fact that you will still owe the lender the money and they can still seek repossession or hold you personally accountable for any shortfall if the property is sold for less than you owe.

Some lenders restrict the right of a borrower to have a further mortgage and so it may not be possible to obtain a second or third charge mortgage even where there is sufficient equity in the property without your first mortgagee’s consent.

What if my partner wants the loan and I do not?

Sometimes a person may want a loan but their partner does not. One person may pressurise the other to take the loan. Lending companies do not want to lend when this happens.

Can I change my mind and cancel the loan?

You have the right to cancel your loan application up until the time we request the funds from the lenders. However if we have already given an undertaking to meet the lender’s solicitor’s fees, these will still be payable whether or not completion takes place.

Some lenders do include facility fees which are payable whether or not you proceed with finance. Check the terms of your facility very carefully before signing and returning it as at this stage you are committed. Cancelling before this may mean that you are liable for fees that have not yet been paid such as solicitor’s fees and any other fees you have agreed to.

14

Terms and Conditions of ServiceGeneral Terms and Conditions

Acceptance of Instructions to Act

We can decide whether or not to accept instructions from a client. If we receive a referral/nomination from an Introducer, this does not mean that we have to accept the instruction to act for the client(s) referred. If we refuse instructions we do not have to give a reason, though we will never refuse instructions for unlawful or discriminatory reasons.

GWlegal is committed to promoting equality and diversity in all of its dealings with clients, third parties and employees. Please contact us if you would like a copy of our Equality and Diversity Policy.

Data Protection

We will control and process your personal information in accordance with the Data Protection Act 1998. We will use the personal information that you provide to deal with your case and carry out our duties to you. We may disclose your personal information to other companies should the need arise during the progress of your case. We will also use your personal information for administrative, accounting, monitoring, research and marketing purposes; statistical analysis; security vetting and client services.

By providing your personal information to us, you expressly authorise us to process that information for the purposes set out in this paragraph. You can at any time request from us a copy of all information that we have regarding you (for which we may charge a fee of £10.00) and correct any inaccuracies in it. If you provide information to us about another party, you confirm that such party authorised you to do so and consents to our processing that personal information.

Regulation

GWlegal is the trading name of Goldsmith Williams Solicitors who is authorised and regulated by The Solicitors’ Regulation Authority under number 48089. We are not authorised by the Financial Conduct Authority, so we cannot give you investment advice nor can we advise you about mortgage products. Using your information we will process any data with have about you in accordance with the Data Protection Act 1998.

Copyright

We retain copyright in documents that we provide to you or a third party on your behalf. You can use the documents solely for the matter that you have asked us to deal with and not for any other purpose.

Law and Jurisdiction

Our agreement with you to provide legal services and these terms of business are governed by and construed in accordance with English law.

Electronic ID

You may see a charge for carrying out an electronic ID search mentioned in your Terms of Business letter. We may do this because we have to be sure that you are who you say you are and by using the technology available we can search a number of online registers to satisfy ourselves of your identity. You should know that we make a profit on these searches. You will appreciate however that we have a fair degree of administration to do to submit a search, receive the result and consider the result (quite often we need to resubmit some outstanding information or make a judgement if the result is not as clear as it could be). The fees that we charge as outlined in your Terms of Business letter therefore covers all the administrative cost to us of making sure that we deal with the question of your ID as smoothly and efficiently as possible.

Your File

Your file is confidential and we will not let anyone see it without your permission. However, your file may be requested in some circumstances.

Where applicable, your lender

15

has the right to see documents relating to your loan. Many lenders will ask you to sign a waiver which allows them to see the whole file, including letters you have sent us and notes we have taken at meetings and during phone calls. However we will always check to ensure you do give your consent for us to do so.

We are proud to be registered as an ISO 9001:2008 quality assured company and as part of this, it may be necessary for us to allow inspectors to view your files. The inspectors will simply check that we gave your case the appropriate attention. They will not disclose any confidential information to anyone else. You may write to us at any point to say that you do not wish your file to be made available for assessment. This will not affect the service you receive from us in any way. External firms or organisations may conduct audit and quality checks on our practice. These external firms or organisations are required to maintain confidentiality in relation to your files. If you wish us to send a copy of your file to you at any time after your matter has completed please let us know. Such requests must be in writing. Please be aware we are entitled to make a charge that is fair and reasonable taking into consideration the time and effort involved in complying with your request. We can, of course, provide you with a breakdown of

our charges for doing. We keep our files for six years in electronic format only (except Wills & Probate or files relating to minors which are kept in paper format indefinitely) and will destroy them thereafter unless you ask us not to. If you do not go ahead with your case, we may destroy your file at any time.

Call Recording

All inward and outward telephone calls are recorded. This is for two reasons:

1. It helps us to have a record of your instructions to us and any information that we give to you over the telephone.

2. We can also use this to monitor the level of service being provided to clients, which assists us in developing our service to clients by providing staff training where necessary.

Copies of Calls

If you want a copy of a recording please ask the person dealing with your matter. It is not always possible to provide a recording as there can be technical problems which lead to calls not being recorded or where we are unable to trace the call. Using your Information

We will use all information you provide primarily for the provision of legal services.

However we may also use it for related purposes including updating and enhancing our records, analysis to assist in managing our practice, statutory returns, legal and regulatory compliance.

Confidentiality

We have a duty to keep information about you confidential. However, we may be required to allow outside organisations access to our files, such as our Regulator, bankers providing funding for your case, the assessors for our ISO 9001:2008 accreditation, any ‘After the Event’ insurers and/or your Introducer.

Money Laundering

We comply with the Money Laundering Regulations Act 2007 and associated legislation (Terrorism Act 2000 and Proceeds of Crime Act 2002). In a situation where you are sending us funds, we reserve the right not to proceed with a transaction should we receive such funds from a source that is different from one already notified, until we can make the necessary investigations about where the funds have come from and who has sent them to us. Therefore, if you fail to tell us that money will be paid to us by a third party, this will cause a delay in proceeding with your matter. If you fail to satisfy us about the source of the money, we reserve the right to stop acting.

If a third party, who is not our client, is sending us money on your behalf, then we must

16

have identification from that person(s) and we also need to know the source of the funds being sent to us, a copy of the bank statement or passbook will be needed.

Interest

In accordance with the requirements of the Solicitors’ Accounts Rules 2011, any money received on your behalf will be held in a client account. We will pay a sum in lieu of interest on monies held in line with the terms of our payment of interest policy. It is important to note that interest will not be payable in all cases and that the rate received will be lower than that available to you had the monies been invested privately. The written policy is available on request.

Limitation of Liability

We have compulsory indemnity cover of £3m for each and every claim and for most claims this amount will be sufficient, therefore, we limit our liability to this amount, unless there is any fraud or reckless disregard of professional obligations.

For matters where the value of the transaction is more than £3m these will be dealt with by way of a separate agreement.

Electronic Communication

We are happy to use email as a way to communicate with you, but you should be aware that confidentiality cannot be ensured nor is delivery of such mail. If you prefer us not to use email, please tell us in writing.

Rights

Any advice that we give is for your benefit, as our client. Third parties may not use or rely on our advice.

Distance Selling

We may not have met with you, in which case the Consumer Contracts (Information, Cancellation and Additional Charges) Regulations 2013 apply. This means you have a right to cancel your instructions to us within fourteen working days of our receipt of your instruction.

Your Right to Complain

As part of our commitment to customer satisfaction, GWlegal has a rigorous complaints procedure that you can access at any time. Please let us know as soon as possible if you have any problems or you would like a copy of our Complaints Procedure.

If you have a complaint about the service you receive from us, at any time, you should raise this with the person responsible for your case. If they cannot resolve the matter then you should speak to the manager of the team. If, after that, you are dissatisfied with how your complaint has been dealt with, you should contact our Customer Services Manager, Barbara Hillen on 0345 373 3737, by email [email protected] or by writing to us. Your complaint will then be dealt with in accordance with our complaints procedure, a copy of which is available on

request. Please do not store up any complaints, please raise them straight away.

If still unresolved at this stage, you may take your complaint to the Legal Ombudsman. Normally, you will have to bring your complaint to the Legal Ombudsman within six months of receiving a final response from us about your complaint and six years from the date of the act or omission giving rise to the complaint or alternatively three years from the date you should reasonably have known there are grounds for complaint (if the act/omission took place before 6th October 2010 or was more than six years ago). Banking Crisis Please note that we will not accept liability to repay monies lost through any banking failure as all monies are placed by us in accordance with the Solicitors Accounts Rules.

All client monies are deposited with either Barclays or Yorkshire Banks. The Financial Services Compensation Scheme (“FSCS”) limit of £85,000 will apply for an individual’s total monies. Please also note that some deposit institutions have several brands which can be checked with your bank or the FCA (www.fca.org.uk). We would also advise that in the event of a banking failure we may need to disclose clients’ details to the FSCS.

Client Balances

We have a duty under our Code of Conduct to return any monies to you following

17

completion of your matter. If for any reason we are unable to make contact with you, we will therefore need to engage the services of a “tracing agent” who will be able to do this on our behalf. The costs incurred in carrying out this additional work will be deducted from any monies due to you.

Assessment

Under sections 70, 71 and 72 of the Solicitors Act 1974 you are entitled to have our bill of costs assessed by a court. Goldsmith Williams is entitled to charge interest on any outstanding amount of the bill in accordance with article 5 of the Solicitors’ (Non-contentious Business) Remuneration Order 2009.

Bridging Department Additional Terms and Conditions

Your Mortgage

It is important to remember that GWlegal is not in a position to advise you on the suitability of your mortgage offer, or whether it represents a good deal for you. This is a matter for you and your Introducer. Nor are we in a position to advise you on the level of mortgage payment protection or life insurance you need – although we highly recommend that you take appropriate advice on this matter. We will act on instructions from your Introducer as if they had come from you, unless you notify us otherwise.

Cancellation Fee

If you decide not to go ahead before your mortgage offer, we will charge you £250 (plus VAT) for the work we have already done. If you decide not to go ahead after your mortgage offer, we will charge you the full fee, plus any fees we have to pay to other people.

A Serious Warning

When you sign your deeds with us, you are agreeing to make set repayments on your mortgage, which is secured against your property. If you do not keep up these repayments, your lender can take action against you which could mean that you lose your home.

Furthermore, even if the lender does take possession and sells the property, they still have the right to take further action to recover any shortfall between the proceeds of the sale and the amount you owe them. Some lenders cover this risk by asking you to take out a mortgage indemnity policy. However, while this will pay out to cover any shortfall to the lender, the policy provider still has the right to take action against you to recover their loss.

It is vital therefore, that if you are experiencing any difficulties whatsoever in making your mortgage repayments, you let your lender know as soon as possible. They can only help you if you let them know, so you must act quickly and not ignore the situation.

Confirming the Details

When we receive your mortgage offer, we will send you the details and conditions of your mortgage. It is important that you read these in detail and ask your Introducer if you are unsure about any of these conditions. It is not our responsibility to advise you on these conditions, it is simply our job to ensure that the terms and conditions are met so that your lender can release your funds.

If you have an existing mortgage, we will assume that any redemption figures we receive from your lender are correct. We do not have the facilities to check these figures, or to know whether any penalty or added interest is justified. If you are in any doubt, you must ask the lender directly to check their figures before completion.

In any case, you should never cancel any Standing Order or Direct Debit to your lender until we advise you that the loan has been cleared and any charges have been paid in full. If you have any questions about your mortgage or any stage of the process, please do not hesitate to contact us.

Conflict of Interest

We do not act for both the buyer and seller in a conveyancing transaction even where the conduct rules allow us to. In the unlikely event that we are also acting for your Introducer in the same matter and a conflict arises we may be obliged to cease acting. We will notify you in

18

writing if a conflict arises and advise you of your options.

Ending the Relationship

You can tell us to stop acting for you at any time. We can only stop acting for you if we have a good reason and can give you reasonable notice. Examples of when we may stop acting are where:

(i) there is a conflict of interests

(ii) the relationship between us breaks down

(iii) we cannot obtain instructions from you or your instructions constantly change

(iv) you fail to provide the necessary identification; or

(v) you fail to satisfy us about the source of any money that you are sending to us

This list is not exhaustive and it merely gives examples. If either of us ends the relationship, you remain liable for our costs and disbursements we have paid on your behalf plus any costs and disbursements for the transfer of your file to your new advisers.

Referral

It is likely that you will have been referred to us by your Introducer. If so, then this introduction is regulated by a Code of Conduct. This is called the SRA Code of Conduct – you

can ask us for a copy or you can view it at www.sra.org.uk .

It’s our duty to inform you that we have a financial arrangement with your Introducer. Your Introducer should do so as well. Please see our Terms of Business letter for a breakdown.

Despite any financial arrangement, any advice that we give you is independent and you are free to raise questions on any aspect of the transaction and of course you are free to choose another solicitor to act on your behalf. Your Best Interests

If you are charged a fee by your Introducer for arranging your mortgage we will include this on your completion statement and, provided we have your signed authority to do so, will deduct this from you and pay it to your Introducer.

We have had over 30 years’ experience and can say that the majority of our clients have preferred to have a third party Introducer assisting on their behalf through a case. Introducers know us, the procedures involved, the legal language used, what our service levels are and can question us if they don’t believe things are progressing as they should. It is entirely your decision as to whether instructing an Introducer is right for you and that their service is of sufficient value to you in terms of spending the time and effort in seeing your case through. Introducers can remove the

hassle and worry that some legal cases can sometimes create, leaving you to get on with what you need to do.

All our clients are asked at the end of a transaction to complete a “Client Satisfaction Questionnaire” for feedback on how well they rate the over all experience. Our Code also prohibits us from acting for any clients who have been acquired as a result of marketing or publicity or other activities which, if done by a person regulated by the SRA, would be in breach of any of these rules.This means we cannot act where you have been referred to us by an Introducer:

• using misleading or inaccurate publicity;

• making unsolicited visits or telephone calls (“Cold Calling”);

If you feel that either of these points relate to you please let us know as soon as possible as we will be unable to act for you.

We confirm that the information disclosed by you to us will not be disclosed to your Introducer without your consent.

Whether you are recommended to us or not you are always free to choose another solicitor.

Legal and Admin Fee

The “Legal and Administration Fee” comprises our basic fee for the core conveyancing

19

work, without any complicating factors which may lead to unexpected and time consuming additional work, or to further fixed add-on fees relating to specific issues. It also includes (if you have an Introducer who has recommended you to us) the fee the Introducer is charging you for the additional steps they are taking in working together with us. Where applicable, the amount paid to us and the amount paid to the Introducer are clearly distinguished. The Introducer’s fee may be in addition to any fee you have separately negotiated or been charged by your Introducer. If you are in any doubt you should check this with the Introducer direct. If we do not hear from you, this is the fee that we will be paying the Introducer on your behalf, and including in our bill to you. If you require further information about this arrangement please let us know.

Our policy on our fee charging is to be as transparent as possible whilst complying at all times with the SRA Code of Conduct. We are committed to ensuring that you are aware of what our charges are and when we use a separate but connected company why we do so and what that means to your pocket. Where we work with Introducers who refer cases to us we are committed to ensure that they comply with their obligations under the Code of Conduct and for these reasons if you are unhappy in any respect with either the method of our charges or you consider

that any other aspect of our business dealing with you or your Introducer is less than transparent we wish to hear from you and upon hearing we will act on any such concerns.

Block Policies

Occasionally we may be asked to protect your lender by insuring them through one or more of our block policies arranged through our related company Ambersearches Limited. The charge for this includes the policy premium and the Ambersearches Limited administration charge.

Unsecured Loans

If we accept instructions to pay off any loans on your behalf, then we will make a charge additional to those set out in our initial letter.

We cannot tell you what that amount will be until we know how many loans there are and how much work this will involve. Local Searches

We charge a standard fee, which may be more than the local authority fee. However, our search is quicker and does not need to be paid for in advance, and if your case does not go ahead, we will not charge you for it.

Joint Representation

In the event that we are acting for both yourselves and your Lender we will be doing so under a joint retainer. This is unusual in bridging cases as

some Lenders believe that there is an inherent conflict of interest and therefore retain a solicitor to act for them only. In such cases you are required to instruct your own solicitor and generally pay the legal fees of both firms. We consider that it is appropriate in some cases for us to act not only for the Lender but also for yourselves and as such the process can be quicker and cheaper for you. As Joint Representation is unusual it is important that you understand the basis on which we will accept such a retainer:

• It is only appropriate where there is no obvious or potential conflict of interest • Your lender and ourselves both reserve the right at our sole discretion to reject any request to act on a Joint Representation basis (for example where there are family members/ guarantors/ limited companies/overseas assets/ non standard transactions)• That you have freely chosen to be represented by ourselves in addition to our acting for the Lender and that you have the right to change your mind at any time and withdraw your instructions to us to act on your behalf• That you have chosen to instruct us of your own free will without any undue or other influence from any third party and any particular circumstances such as urgency of the transaction

• That you are happy for us to represent you in this case as well as the Lender in the full knowledge that we will

20

be acting for the Lender and looking after their interests as well

• That we reserve the right at any time in our sole discretion during the course of the transaction to withdraw from acting for you in the event that we consider we cannot professionally continue but we nevertheless reserve the right to continue to act for the Lender in our professional judgment

• That in the event that the Lender is obliged or decides to take any enforcement proceedings of whatsoever nature against you that we will be unable to act for you in those proceedings and we may be called to give evidence in those proceedings by either the Lenders solicitors or your own solicitors about the conduct and circumstances of your case and if called to do so will provide any written or oral evidence retained by ourselves ( including telephone recordings between ourselves relevant to your case)

Stamp Duty Land Tax (SDLT)

We will advise you if any SDLT is payable and it will depend on the current rate. If it is payable, then we must receive the amount needed before we complete the transaction. If you

fail to pay prior to completion then we can refuse to complete the transaction. If SDLT is payable it will be deducted from the advance monies on completion. We must also have a signed SDLT form. If you delay in returning the SDLT form to us and penalties are incurred because of this, then you will be responsible for payment of the penalty.

Exceptional Expenses

Outside of our fixed fees included in the legal and administration there are inevitably some extra charges that you need to be aware of. These will often be what we term as exceptional expenses that are non standard such as having to indemnify you against a lack of right of way over the property you are purchasing. It is not always possible to identify these at the start of the case but as soon as we do realise they have to be paid we will of course let you know how much.

We always act in your best interest and for that reason we are happy to explain to you why we place our business with Dual for indemnity policies, as follows:

• This firm specialises in dealing with property- related indemnity policies

• They are competitive in the market place • They have in-depth knowledge of the market

• They undertake proper meaningful comparisons

• They review the market and competitors’ regularly;

• They provide comprehensive cover on a par with other policies in the market place

Ambersearches

You will note from our literature that we may use a separate (but wholly owned) company called Ambersearches Limited to arrange various searches on your behalf in particular a personal local search or insurance in place of carrying out a search. We are required to give you details of the ownership of Ambersearches Limited and other disclaimers under our Code of Conduct.

The Partners of GWlegal have a financial interest in Ambersearches Limited. It is a separate business and as such when Ambersearches Limited does any work for you, you do not get the statutory protection that a solicitor’s client would have under the SRA Code of Conduct.You may be wondering why we are using a separate company rather than dealing directly with suppliers of specialised search products. The reason is that we believe that doing so provides a better and more efficient service for you as the company is a specialist in negotiating and processing cases on behalf of clients.

IT ALSO AVOIDS THE NEED TO REQUEST A PAYMENT ON ACCOUNT FROM YOU TO COVER THE COST OF ANY SEARCH – WHICH COULD BE AS MUCH AS £250.

21

Ambersearches Limited negotiates terms with third party search providers and reviews the market to ensure that it offers competitive terms for clients of GWlegal. Naturally this company will be making a profit on its business and will be receiving commission – all cases are different in the amount of work involved but the net profit is probably an average of £45 per completed case and that will benefit the owners of the Company. The good news is that all of that is taken into account within the fixed fees that we charge and therefore you are not being charged any extra for their work. We believe that it is in your best interests that we have this arrangement in place – it not only secures a very good quality search but you don’t have to pay anything upfront and if the case doesn’t proceed you don’t have to pay anything at all. We will share your details with Ambersearches for this purpose.

Telegraphic Transfer Fee (TT)

On completion of your purchase we have to send your monies by Telegraphic Transfer to the sellers’ solicitors. Where we are dealing with redeeming a mortgage for you then quite often the lender will require the funds due to them to be sent by TT through our bank. The fee is a profit charge for carrying out this important work on your behalf. It is not the fee charged by the bank.

Your new lender may also transfer your money to us electronically and charge you

for this. If so, you may see two sets of transfer fees on your account. Please note that these are separate charges for separate transfers. If you would like us to send any balance to you on completion by money transfer, then we will be happy to do so, saving you normal bank clearing time. There is a charge for this.

Please note that included in this fee is also a charge we are paying to have your bank account details verified by an independent third party. This is to ensure that the money we send to you is directed to your correct bank account. We are bearing the cost of this service for your protection.

Payment of Costs

All costs and disbursements must be paid to us before completion; otherwise we have the right to refuse to complete the transaction.

If you wish to pay our costs or any disbursements by credit card please note that there is an additional surcharge of 2.5% to cover administration costs. The 2.5% will be charged every time a credit card is used for any additional payments. There is no surcharge when using a debit card.

22

Financial Services Insurance

If we carry out a service for you where we, for example, arrange an insurance policy such as for defective title insurance or unoccupied property indemnity then the following notice applies:

GWlegal is not authorised by the Financial Conduct Authority. However, we are included on the register under reference LS 48089 maintained by the Financial Conduct Authority so that we can carry on insurance mediation activity, which is broadly the advising on, selling and administration of insurance contracts. This part of our business, including arrangements for complaints or redress if something goes wrong, is regulated by the Solicitors Regulation Authority. The register can be accessed via the Financial Conduct Authority website at: www.fca.org.uk.

The Law Society in England and Wales is a designated professional body for the purposes of the Financial Services and Markets Act 2000. The Solicitors Regulation Authority is the independent regulatory complaints-handling arm of the Law Society.

We do not conduct an analysis of the market each time we recommend an insurance product to you and we are not contractually obliged to do so.

You can request details of the insurance undertakings that we conduct business with and we will provide you with the relevant details.

Marketing

We may from time to time use your data to market our other products and services or pass your details to reputable third parties to do so. If you do not wish this to happen you may opt-out by ticking the appropriate box in the Client Property Questionnaire.

Conveyancing Quality Scheme

As a member we now have some professional obligations to follow which will apply to your transaction. If you require further information this can be accessed by visiting the Law Society website

www.lawsociety.org.uk/practicesupport/conveyancing.page

Lawyer Checker

You may see in the Fee Sheet sent to you at the start of the transaction an item referred to as Lawyer Checker. This is a fee charged by us to check the bank details of the conveyancers on the other side of your transaction. We do so by requesting this confirmation from a third party. This is for your protection to ensure that we do not send funds to an incorrect or fraudulent bank account.

23

GlossaryAnnual Percentage Rate (APR)

The rate you will be charged including the total interest payable.

Arrangement fee The fee payable to your lender for setting up the mortgage.

Arrears fees

The charges payable if you fail to make payments on time.

Default Failure to meet the terms of the mortgage e.g. miss a payment.

Exit fee (or loan repayment fee / redemption charge)

The fee payable to your lender when the loan is repaid.

Facility fees

The fee payable to your lender for arranging the loan.

Introducer (Broker or Intermediary)

The term used to describe your financial/mortgage adviser who has “introduced” you to our services.

Introducer arrangement fee

The fee payable to your Introducer for the services they provided e.g. finding you a mortgage rate.

Legal fees on redemption The fee payable to the lender to cover the cost of its legal fees for redeeming the loan. This is usually based on a set scale.

Loan to Value (LTV)

Loan to value (LTV) refers to the amount of money the lender is prepared to loan you against the value of the property e.g. If the property is valued at £250,000 and the lender lends £200,000 the loan to value is 80%.

Generally, lenders will either use an ‘open market valuation’ or a ’90 day sale’ (sometimes known as forced sale) value.

Mortgage administration repayment charge (Redemption fee or Deeds release fee)

The fee payable to cover the lender’s cost in dealing with the repayment of your loan.

Open market valuation

The ‘open market valuation’ is based on the price the surveyor believes the property can achieve ifmarketed and sold in the normal manner. The surveyor will generally comment on the demand for the type of property and likely selling time. This may be lower than the estate agent’s and your view of the value of the property.

Procuration fee

The commission paid by the lender to your Introducer for introducing business to them.

Telegraphic transfer fee

The fee payable by you to lender for transmitting the loan electronically to your solicitor’s bank account.

Valuation fee

The fee payable by you to cover the cost of a survey to be carried out on the property

Valuation insurance

This covers the lender and any difference between sale price (in possession) and original valuation.

90 day sale

The ’90 day sale’ value is based on the price the surveyor believes could be achieved if the property had to be sold within 90 days. This is often lower than the ‘open market’ value.

24

Your Notes25

GWlegal is the trading name of Goldsmith Williams Solicitors. Goldsmith Williams Solicitors is authorised and regulated by the

Solicitors Regulation Authority under number 48089. Calls charged at local rate.

0345 373 3737

gw.legal

If our dedicated team of experts can offer any assistance we’d be delighted to hear from you

GWlegal | 4th Floor | 20 Chapel Street | Liverpool | L3 9GW

facebook.com/GWlegalUK

twitter.com/GWlegal

instagram.com/GWlegal

pinterest.co.uk/GWlegalUK

We’re a social bunch...

GWlegal is indebted to the Association of Bridging Professionals for allowing us to reproduce parts of their literature in this Guide.Association of

Bridging Professionals

Affiliate

0184/020/040917