your member update - liverpool victoria · your member update. 2 2014 highlights £1.3bn £92m...

TRANSCRIPT

Your member update

2

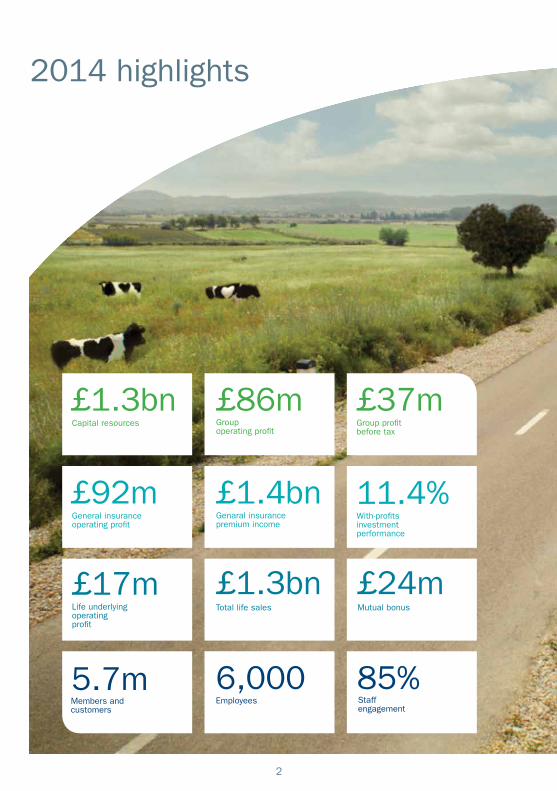

2014 highlights

£1.3bn

£92m

£86m

6,000

£37mCapital resources Group

operating profit

General insurance operating profit

Group profit before tax

£24mMutual bonus

£17mLife underlying operating profit

11.4%With-profits investment performance

£1.4bnGenaral insurance premium income

5.7mMembers and customers

85%Staff engagement

Employees

£1.3bnTotal life sales

3

2014 highlights

LV= a modern mutual

page 4

Chief Executive’s review

page 6Our financial results

page 8

General Insurance business in 2014

page 10Our Life business in 2014

page 12Our Heritage business in 2014

page 14Our people and culture

page 16Showing we care

page 18Your benefits

page 20The LV= board and committees

page 24Directors’ remuneration

page 26The numbers

page 27

Contents

A leading financial mutual

The UK’s largest friendly society

Founded in

1843

Owned by our members

44

LV= a modern mutual

LV= is a modern and leading financial mutual. We were established in 1843 to help families protect and provide for their dependents and cherished possessions. LV= still has this aim at its heart today.

We are owned by and run for the benefit of our members and are different from other organisations which may be owned by shareholders, employees, private equity groups, or government. We believe this difference to be important in serving customers and employees and to fulfil our primary goal of creating long-term value for our members.

Our members are defined as those who have certain financial products with us, such as life insurance or investments. Members can expect to benefit in several different ways:

• They have voting rights and can influence the key decisions in the Society and help provide feedback on our current products and services.

• There is a range of specific benefits, such as product discounts, access to a support fund, free legal advice and the ability to nominate a good cause close to their hearts once a quarter to receive a donation.

• LV= plans that members should receive leading returns on their investments but in addition and when results permit, eligible with-profits members will receive a mutual bonus added to the value of their policies to reflect the overall success of the Society.

We believe that being a mutual without a need to deliver short-term profits to shareholders makes it easier for us to compete in the longer-term, through combining a high level of customer service, with great values and an engaging culture for our staff.

LV= is a modern business, but is based on the traditional and enduring ideas of serving customers well, engendering their trust, encouraging customer ownership and producing and sharing joint benefits. It seems to work well for us and our members.

Being a mutual makes a difference to the way we service customers, look after our employees and fulfil our goal of creating value for our members

Our goal is to grow value for our members Our vision is to be Britain’s best loved insurer and we also want to make insurance something that people can relate to – by achieving our vision and humanising insurance we believe people will trust us to look after their insurance needs.

We have a clear point of difference which we call sharp with a heart. This guides the way we do things and combines the competitive performance of a PLC with the trusted behaviours of a mutual.

Our brand promises reflect aspects that we consider to be important to our customers.

55

Ca

r i ng

G o o d v a l u e , g r e a t va l u

e s

Sk

i lf u

l

Eas y t o do bus i ness w i t h

Ex t r a

ord

ina

ry

The LV= d

iffer

ence

:

Sharp w

ith a

hea

rt

Our brand

prom

ises

To humanise insurance

Our mission:

To b

e Br

itain’s

best

love

d ins

urer

Our

vis

ion:

Our goal:To grow

member value

6

Chief Executive’s reviewDespite challenging market conditions in both general insurance and life, we are reporting good results for 2014.

Over 1,000 new customers joined LV= every day last year across our award-winning range of products and we continue to win industry accolades for our innovation, customer service and technology initiatives.

Our focus on looking after our customers is as important as ever, and in 2014 LV= became the UK’s most recommended insurer according to YouGov. The research amongst 30,000 consumers demonstrates our continued brand strength and great customer service.

Our service proposition was further confirmed in the UK Customer Satisfaction Index published in January 2015 which showed that LV= achieved the top spot in the insurance sector for customer satisfaction. We are now ranked joint seventh across all sectors of the UK economy amongst businesses like Marks and Spencer, John Lewis and First Direct.

Our general insurance business now has 4.6 million customers across a range of products and we have a loyal existing customer base with high renewal rates of 79% and 83% on direct car and home insurance.

We continue to be focused on the over 45s where we already have significant scale and in line with our desire to diversify our business in general insurance, we launched a home insurance TV advert for the first time and as a result we have increased our market share significantly.

We signed partnerships with leading brokers including Jelf and Brightside and grew our broker-only commercial lines business, where we specialise in insuring small to medium enterprises.

Our retirement solutions business was impacted by the changes announced in the March 2014 Budget that means annuities will no longer be compulsory. We took some quick customer focused actions after the announcement to ensure that customers were not negatively impacted.

We were also the first to market with a one year annuity designed to help customers who wanted to take advantage of the greater flexibility the new pension rules offered, but needed an income until April 2015.

We are well placed for the future as we offer a range of at retirement products and, although some retirees will choose to take cash, many more will continue to look for products that provide a level of guaranteed income.

Mike RogersChief Executive

7

We remain the most popular income protection provider amongst advisers in the UK, a product that is more relevant than ever with people moving jobs more regularly and the jobs market still under some pressure. Our cover continues to be amongst the best in class and sales are up year-on-year.

In line with our desire to grow our life business, in December we agreed a transaction with Teachers Assurance, to take over the majority of its business interests, subject to regulatory and Teachers Assurance members’ approval. Teachers Assurance is like LV=, a mutual friendly society and is complementary to our existing business lines. This acquisition is further demonstration of our continued financial strength.

We employ 6,000 people across the UK. We believe a happy, engaged workforce leads to the right behaviours for our customers so we focus on providing our people with a positive place to work, good cultural values, a competitive benefits package and development opportunities so talented individuals are able to progress their career at LV=.

In summary I am pleased with the progress we’ve made in 2014. Our customer focused proposition, wide range of products, and strong brand means we are well placed for continued profitable growth.

Our customer focused proposition, wide range of products, and strong brand means we are well placed for continued profitable growth

8

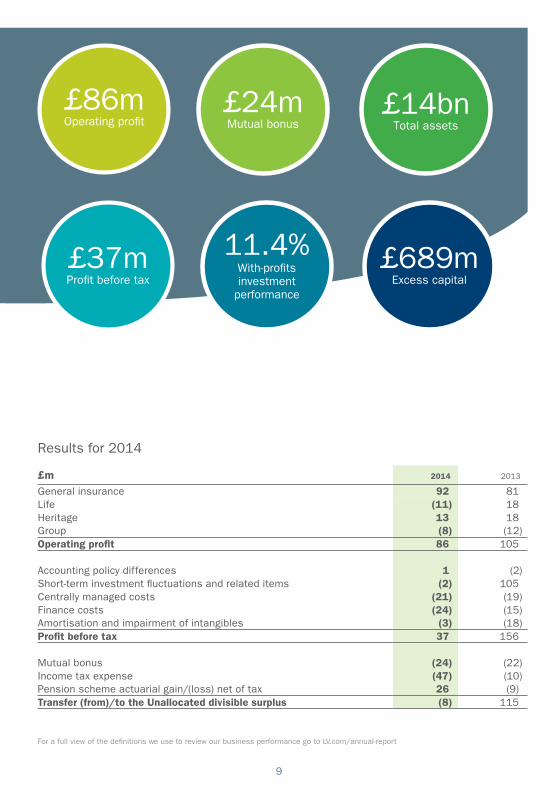

Our financial resultsWe have announced an operating profit of £86 million for 2014

Philip MooreGroup Finance Director

We continue to meet our financial aims of delivering good returns to members, while ensuring a strong capital position on which to base future growth

In our 2014 results we have announced an operating profit of £86 million (2013: £105 million). This was a particularly pleasing result given the challenging industry conditions we faced during the year.

Our general insurance business had an excellent year with good operating profit growth at £92 million (2013: £81 million) despite continuing severe market price competition in motor and reduced investment returns. We saw good increases in customer numbers and profit contribution from our home and commercial insurance businesses as we delivered on our strategy to grow in non-motor business lines.

Our life business generated an operating loss of £11 million (2013: £18 million profit). This was partly due to the changes in pensions freedom announced in the 2014 Budget, which meant we saw significantly lower new business volumes and profit contribution from enhanced annuities. This was partially offset by good profit contribution from our protection and

equity release product lines. We also saw increased sales in pensions.

Economic conditions have affected our results as we witnessed further reductions in interest rates during the year, impacting the outlook for investment returns. We also saw credit spreads widening and the FTSE finishing the year down on the 2013 closing position. This meant that we did not see the large short-term investment gains which we benefited from in 2013. Subsequently, we have seen a reduction in profit before tax to £37 million (2013: £156 million).

Our with-profit investment returns at 11.4% have outperformed the benchmark for the third year running and we have declared a mutual bonus of £24 million which is a £2 million increase on the prior year.

LV= continues to meet its financial aims of delivering good returns to members, while ensuring a strong capital position on which to base future growth.

9

For a full view of the definitions we use to review our business performance go to LV.com/annual-report

£m 2014 2013

General insurance 92 81Life (11) 18Heritage 13 18Group (8) (12)Operating profit 86 105 Accounting policy differences 1 (2)Short-term investment fluctuations and related items (2) 105Centrally managed costs (21) (19)Finance costs (24) (15)Amortisation and impairment of intangibles (3) (18)Profit before tax 37 156 Mutual bonus (24) (22)Income tax expense (47) (10)Pension scheme actuarial gain/(loss) net of tax 26 (9)Transfer (from)/to the Unallocated divisible surplus (8) 115

Results for 2014

£14bnTotal assets

£24mMutual bonus

£86mOperating profit

£689mExcess capital

11.4%With-profits investment

performance

£37mProfit before tax

10

General Insurance business in 2014

John O’Roarke Managing Director of General Insurance

General Insurance products

Personal

Car Car

Motorcycle Van

Specialist Vehicles Truck

Britannia Rescue Fleet

Home Motor Trade

Travel Hire & Reward

Pet

Landlord

Business Insurance

Commercial

Our range of insurance products can be broadly split into two categories. Those aimed at individual insurance needs such as car, home and travel insurance and those developed for business owners such as shop or office insurance and fleet vehicle cover.

3rdlargest car

insurer

A selection of our products available directly from us, via comparison sites or from brokers.

11

In 2014 LV= won Broker Insurer of the Year

Winner of two awards at The Claims Awards 2014

An award for a unique and innovative technological solution which has enhanced customers’ experience

In general insurance we continue to be one of the UK’s largest car insurers and increasingly are a significant force in other products including home and commercial insurance plus road rescue.

2014 was a challenging year for us but one which ultimately proved to be rich with achievements. The market, as a whole, faced continued motor price competition and depressed investment returns; however we delivered a 14% increase in profitability.

We are the third largest private motor insurer in the UK with around 12% market share, based on the number of vehicles insured.

Our in-force policy count grew by 185,000 during the year and we ended the year with over 4.6 million policies in-force. The majority of this growth came from non-motor lines of business, reinforcing our strategy of growing our home and commercial insurance business lines. We deliberately chose not to grow our customer base in personal motor as rates were not favourable. We extended our direct product range with the launch of Landlord Insurance, providing cover for properties owned for rental purposes either by professional landlords or private individuals.

We continue to win numerous accolades for our products and service and during 2014 we won 35 awards. These include Defaqto five star ratings and Which? best buy awards for many of our products. The rapport we have with brokers was clearly demonstrated this year when we were voted Broker Insurer of The Year 2014 at the annual broker awards hosted by Insurance Age magazine.

We believe these derive directly from our ambition of providing genuinely good value insurance products and exceptionally good customer service.

Looking ahead2015 will undoubtedly bring fresh challenges, not least of which will be continued low investment returns and the potential for economic volatility arising from the UK general election. Despite this, our core strengths of highly engaged and motivated employees and a best-in-market customer service offering, mean that we can confidently expect to see continued growth in customer numbers and sustained attractive returns for our members over the medium-term.

4.6mTotal in-force

policies

3mMotor in-force

policies

£1.4bnPremium income

£92mOperating profit

2014 operating profit at £92m is the second highest in the history of the general insurance business

12

Our Life business in 2014

Richard RowneyManaging Director of Life

Life products

Retirement

Enhanced Annuity 50 Plus

Equity Release

Term/Life Assurance

SIPP

Income Drawdown

Income Protection

Critical Illness

Whole of Life

Protection

Fixed-Term Annuity

The products we sell in our life business fall into two categories, retirement solutions and protection, covering people’s lives and incomes. Over 90% of these products are sold through financial advisers.

RetirementWe offer a range of retirement solutions including enhanced and fixed-term annuities, drawdown and equity release.

In the March 2014 Budget the Government announced a number of changes to the way retirees’ are able to access their pension savings and in doing so put an end to compulsory annuities. This had a significant impact on the plans for our retirement solutions business in the short-term, but in the longer-term we are well placed to benefit from these changes.

We took some quick customer focused actions after the announcement to ensure that customers were not negatively impacted. These included extending our annuity quote guaranteed period for cases from 30 days to 45 for customers who were within their 30 day cancellation period, and for new customers buying a product with us, we extended their cancellation period to 60 days.

Just ten days after the 2014 Budget we launched a one year annuity to give customers a short-term option before the changes come into effect in April 2015. We were the first company to bring this product to the market.

13

Our focus on customer service and innovative product development leave us well placed for the future

During the year we also secured a partnership with Reassure, one of the UK’s largest closed book pension providers, to offer an ‘at retirement service’ for their pension policyholders.

ProtectionWe offer a range of products to protect peoples’ income in the event that they are made redundant or are unable to work due to illness or accident. We also provide a variety of life insurance policies, and our popular 50 Plus plan is designed to leave behind a nest-egg for loved ones.

We have maintained our position as the market-leader in advised income protection, and increased the breadth of our product range with the launch of Personal Sick Pay, a new tailored income protection product designed for riskier occupations. This forms part of our strategy to drive growth in areas where we have significant recognised expertise and competitive advantage.

Phoenix Life chose us as a partner to provide a range of protection solutions including our award winning flexible protection plan and whole of life products. With access to over five million customers through brands including Royal & Sun Alliance and Scottish Provident, this partnership will bring us new opportunities to expand within the direct to consumer market.

The futureWe are well placed for the new pensions landscape that comes into place in April this year as we offer a range of at retirement products and, although some retirees will choose to take cash, many more will continue to look for products that provide a level of guaranteed income.

We have already launched a new online tool to assist financial advisers when they are recommending products or a blend of products to their clients. For people who would prefer to deal with LV= directly we are also developing an online tool so they can access advice and information to help them purchase a retirement product that’s right for them.

We expect our protection market to see steady growth, driven in part by product innovation and a recovering mortgage market.

*Underlying operating profit

Underlying operating profit is the key performance measure for profitability for the LV= life business. Executive remuneration in this area is linked to this metric. For the life business this measure represents ‘trading’ profit i.e. new business contributions and the net contribution of servicing in-force policies.

Underlying operating profit can be defined as operating profit before actuarial model and valuation changes and also adjusted for additional margin for credit default risk and other risks.

Most trusted life insurance provider at the Moneywise awards 2014

Voted the best income protection provider for the fifth year running

Winner of an award for innovation at the Cover Excellence awards

+13% Equity release

sales

£636mPensions sales

£1.3bnTotal life sales

£17mUnderlying

operating profit*

14

Our Heritage business in 2014Our heritage business is the area that looks after our members’ savings and investments policies, many of which are invested in our with-profits fund.

Sales in heritage have been strong and the business made an operating profit of £13 million. Our guaranteed bonds have had very good sales and are up 79% compared to 2013. We have seen high levels of interest in these bonds amongst savers using them as part of their retirement plans. For those who are seeking a potential uplift in their pension income and want a level of guarantee, these products are an excellent solution, and we expect this upwards trend to continue as part of the new pensions landscape.

Results for our with-profits members Against a backdrop of record low interest rates for six years, the investment return of 11.4% for our main with-profits fund is great news for investors. This is higher than the market benchmark and means our members are receiving better returns than many investors in other traditional savings products.

The board has also agreed a mutual bonus for 2014 of £24 million. This will be added to eligible members’ policies and brings the total mutual bonuses, since these were introduced in 2011, to £86 million.

UK Equity 31%Overseas Equity 15%UK Gilts 29%Bonds 11%Property 9%Alternative 4%Cash 1%

With-profits 2014 - Asset class breakdown

Growing the heritage business The deal with Teachers Assurance, will add around 70,000 life and pension policies to our heritage business.

This chart shows how the assets from the with-profits fund were invested achieving the 11.4% return.

Lisa MundyHead of Heritage Customer Experience

£2.2bn The amount of money invested

in the LV= with-profits fund

15

Notes

1. The payouts are based on the following policies:• Endowment – Policyholder aged 30 next birthday at entry; monthly premium of £50, maturing 1 February 2014.• Pension (regular) – Policyholder retiring at age 65; monthly premium of £200, maturing 1 January 2014.• FGB* (Flexible Guarantee Bond) and WPB# (With-Profits Growth Bond) – An investment of £10,000 as at 1 November 2014.

2. The industry payouts are taken from the most recent past performance surveys and relate to maturities and bond surrenders during 2014. The sources are:

• Endowment – Money Management survey published 27 March 2014. • Pension (regular) – Money Management survey published 4 March 2014. • FGB* (Flexible Guarantee Bond)and WPB# (With-Profits Growth Bond) – Money Management survey published January 2015.

An impressive track record Recent maturity and surrender values for with-profits policies show that LV= continues to perform in the top 25% of the market when compared against industry pay-outs. Here’s how our 2014 pay-outs compared:

Flexible Guarantee Bond

Pension Income Plus Annuity

Heritage products

Flexible Savings plan

Products which are available from our heritage business either directly from LV= or through a financial adviser.

11.4% Investment

return for the with-profits fund

£24mMutual bonus

for eligible members

1% Added to the value

of eligible members’ policies

£132mTotal bonuses

added to members’ policies

FGB

*W

PB#

£7,732 £7,301£13,337 £12,684£21,837 £21,904£38,881 £39,262

£15,211 £14,959£34,897 £33,701£53,987 £53,930£104,484 £86,899

£13,802 £13,792

£19,653 £17,490

LV= Upper quartile

10yrs

5yrs

10yrs

5yrs

15yrs

10yrs

20yrs

15yrs

25yrs

20yrs

Endo

wm

ent

Pens

ion

(reg

)

=

16

Our people and culture

53% female employees

We employ 6,000 people across the UK. We believe a happy, engaged workforce leads to the right behaviours for our customers so we focus on providing our people with a positive place to work, good cultural values, a competitive benefits package and development opportunities so talented individuals are able to progress their career at LV=.

Every year we run an independent survey amongst our employees to see how they feel about working for LV= and in 2014 we achieved an engagement score of 85%, up from 83% in 2013. Our overall scores not only continue to track above both the UK High Performing and UK Insurance benchmarks, but this year we’ve increased that gap. We also outperform the UK Financial Services norms in every category which is a significant achievement.

How our employee engagement scores compare to other organisations.

The average length of service is five years

90%of our people say they are proud to work for us

6,000employees

We received 27,000 job applications in 2014

78%85% 74%

UK High performing

organisationsLV=

Other UK financial services

organisations

The ‘Engage’ survey is undertaken independently by Towers Watson. The results were taken from a response rate of 92% in October/November 2014. Employee engagement is measured based on responses to questions on our Brand & Values, Supportive Culture and Talent Management.

20%Employee turnover in our call centres compared to industry norm of around 42%

The average age of our employees is 36

94%of our employees fully support our values

17

We’ve built a culture which values and inspires our people and creates opportunities for them to excel

Nicola Short Financial Adviser

18

Showing we care

Community Investment 34.6% Community Sponsorship 10.0% Community Fundraising 37.9% Member Benefits and Support 17.5%

Raised, donated or invested in UK communities

£1,021,915

Miranda Wilkinson, John Sekhar and Dave Cotton. Our Exeter community committee lending a hand at a local pre-school

19

We believe it’s important for us to give something back to society and particularly to the communities in and around where we live and work.

Last year, with the help of our employees, we contributed over £1 million to good causes.

Our regional community committees based in our 13 larger offices are made up of employee volunteers who are passionate about making a positive impact locally. They meet up regularly to decide which local good causes to support, and in 2014 they distributed £175,000 to around 300 good causes in the UK.

We give our employees time off to help out in the local community. By doing so they don’t need to use their holiday allowance to take part in activities and team community days. In 2014 our people clocked up 3,000 hours helping out good causes.

We support national fundraising events including Comic Relief, Sport Relief, Movember and Children in Need and our employees are always willing to come up with new ways of creating a buzz and raising money for these great causes. We’re particularly proud that, for the last seven years BBC Children in Need has chosen LV= to take calls during its annual telethon. Last year we opened the phone lines in our Exeter and Bournemouth offices where 200 of our people volunteered to take donations.

For employees who raise money for the causes they love we add a little extra. To recognise the personal challenges they get involved in our charity matching scheme means they can claim pound for pound what they’ve raised themselves. In 2014, the charities of 445 employees benefited from a further £78,000 from LV=.

Nearly half of our workforce has signed up to our salary sacrifice scheme. This scheme takes the odd pennies from our employees net pay and donates the overall total amount to a charity that their office has voted for. We received a gold award from Pennies from Heaven in recognition of our scheme.

91%of our employees believe we are caring towards our local communities

£175,000 given by our regional community committees to good causes

£78,000added to our employees own fundraising totals

Pennies from Heaven gold award in recognition of our Pennies for Charity scheme

The night of the Children in Need telethon

20

Your benefitsAs a member you can take advantage of benefits such as discounts, free legal advice, our support fund, and community fund.

Car insurance 10% off

Home insurance 10% off

Caravan insurance 7.5% off

Travel insurance 5% off

Classic Car insurance 10% off

Motorcycle insurance 10% off

Pet insurance 5% off

Speak to your financial adviser if you bought your current policy through them or phone us to see how much you could save.

Call

0800 501 158

For textphone dial 18001 first.Open weekdays 8.00am to 9.00pmSaturdays 8.00am to 5.00pmSundays and Bank Holidays 9.00am to 5.00pmWe may record and/or monitor your calls for training and audit purposes.

Get exclusive discounts on the price of your insurance cover.

21

Motorcycle insurance 10% off

Free legal advice around the clockOur legal advice line has helped thousands of members with a legal query.Legal experts are available day and night to answer your questions. So whether you’ve got a dispute with your neighbour, your employer, a tradesperson or a shop, or you just want to know your rights give us a ring.

Simply call us on

08457 336 336 to receive expert advice from a specialist team of solicitors and legal executives.

The phone line is open 24 hours a day, 7 days a week

The Member Care Line is available to all LV= members, 24 hours a day, 365 days a year. Calls are charged at a local rate and might be recorded for quality control and other lawful purposes. Your personal details and any other information will remain confidential and subject to the provisions of the Data Protection Act 1998. Your information will not be disclosed to another party unless required by law. The advice available from the legal helpline is limited to the law and practice of Great Britain, Northern Ireland, the Channel Islands and the Isle of Man.

21

22

A financial lifeline for members in need

To qualify for a non-repayable financial grant you must have been a member of LV= for at least a year. Applications for assistance are reviewed by a small panel of members, not LV=.

The Member Support Fund can provide non-repayable grants to members in financial hardship. This extra benefit is especially for members who have unexpectedly fallen on hard times and need a bit of help getting by.

If you’re in financial hardship find out if you can apply for a grant.

Call

08457 336 336 The phone line is open 24 hours a day, 7 days a week.

22

In 2014 the Fund awarded grants to 72 members and

their families, totalling over £68,000

23

£40,000 awarded to good causes our members loveFour times a year we award £10,000 to a good cause nominated by one of our members.Our Member Community Fund is designed to make a significant and lasting difference to a charity, a good cause or an individual who needs a cash boost. So far this has helped enhance the lives of people up and down the UK. So if something or someone inspires you and you want to nominate them to receive £10,000 please get in touch.

Call

0845 640 5883 for a nomination form or visit

LV.com/MCF for more information.Lines are open 8.00am to 8.00pm, 7 days a week. Please quote ‘MCF’ when you call.

Nominations are assessed by a committee of LV= members who recommend who should receive the money each quarter.

23

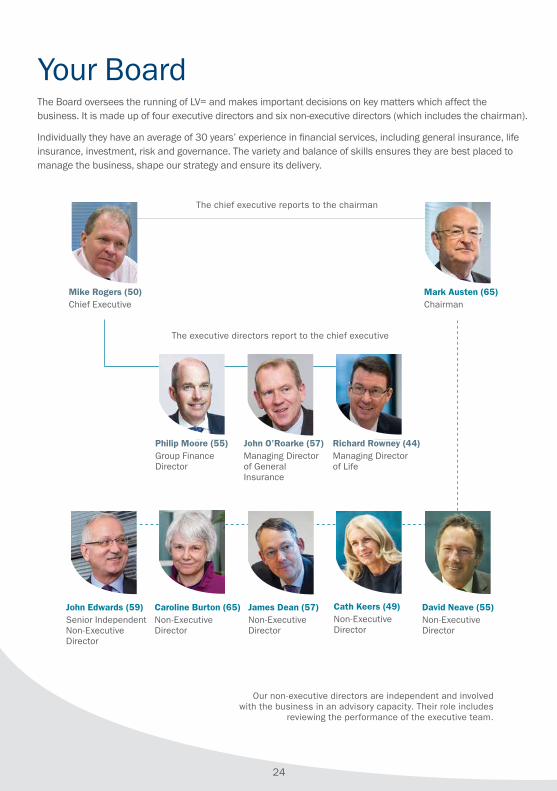

24

Your Board The Board oversees the running of LV= and makes important decisions on key matters which affect the business. It is made up of four executive directors and six non-executive directors (which includes the chairman).

Individually they have an average of 30 years’ experience in financial services, including general insurance, life insurance, investment, risk and governance. The variety and balance of skills ensures they are best placed to manage the business, shape our strategy and ensure its delivery.

Our non-executive directors are independent and involved with the business in an advisory capacity. Their role includes

reviewing the performance of the executive team.

John Edwards (59)Senior Independent Non-Executive Director

Caroline Burton (65)Non-Executive Director

James Dean (57)Non-Executive Director

Cath Keers (49)Non-Executive Director

David Neave (55)Non-Executive Director

Mike Rogers (50)Chief Executive

Mark Austen (65)Chairman

Philip Moore (55)Group Finance Director

John O’Roarke (57) Managing Director of General Insurance

Richard Rowney (44)Managing Director of Life

The chief executive reports to the chairman

The executive directors report to the chief executive

24

25

Rem

uneration Committee Investment Committ

ee

Nom

inat

ion

Com

mitt

ee

With

-pro�

ts Committee Audit Committee

Risk C

omm

ittee

Board

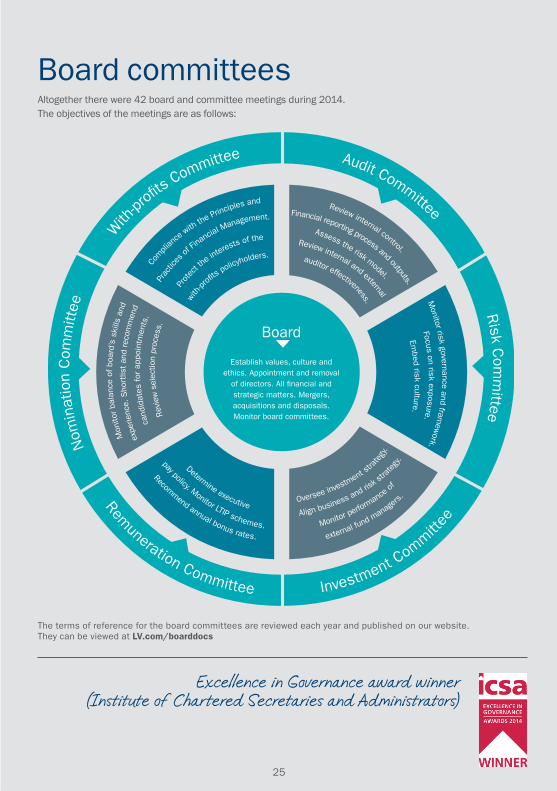

Establish values, culture and ethics. Appointment and removal

of directors. All �nancial and strategic matters. Mergers, acquisitions and disposals. Monitor board committees.

Com

plian

ce with

the Principles and

Prac

tic

es of

Fina

ncial Management.

Prot

ect t

he in

terests of the

with

-pro�

ts policyh

olders.

Review internal control.

Financial reporting process and outputs.

Assess the risk model.

Review internal and external

Monitor risk governance and fram

ework.

Focus on risk exposure.

Embed risk culture.

Determine executive

pay policy. Monitor LTIP schemes.

Recommend annual bonus rates.

Oversee investment stra

tegy

.

Align business and risk s

trate

gy.

Monitor performan

ce of

external fund manage

rs.

auditor effectiveness.

Mon

itor

bala

nce

of b

oard

’s s

kills

and

expe

rienc

e. S

hort

list an

d re

com

men

d ca

ndid

ates

for

app

oint

men

ts.

Rev

iew

sel

ectio

n pr

oces

s.

The terms of reference for the board committees are reviewed each year and published on our website. They can be viewed at LV.com/boarddocs

Board committeesAltogether there were 42 board and committee meetings during 2014. The objectives of the meetings are as follows:

25

Excellence in Governance award winner (Institute of Chartered Secretaries and Administrators)

26

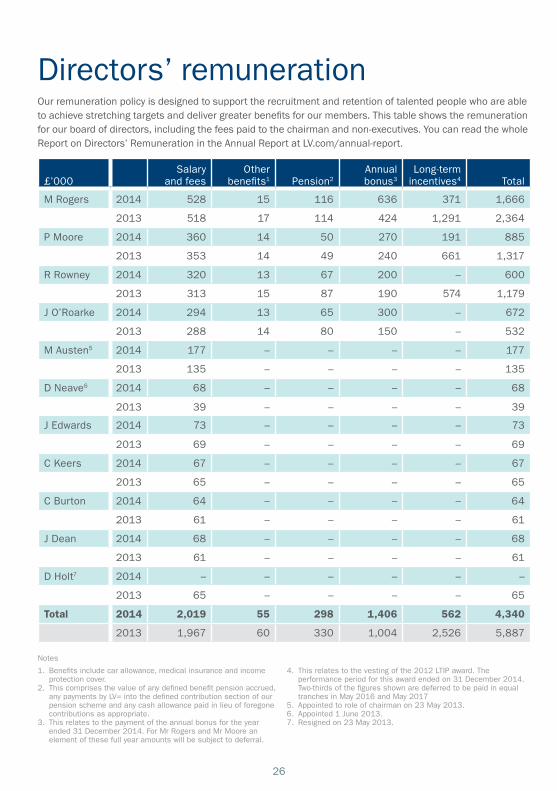

Our remuneration policy is designed to support the recruitment and retention of talented people who are able to achieve stretching targets and deliver greater benefits for our members. This table shows the remuneration for our board of directors, including the fees paid to the chairman and non-executives. You can read the whole Report on Directors’ Remuneration in the Annual Report at LV.com/annual-report.

Directors’ remuneration

Notes

1. Benefits include car allowance, medical insurance and income protection cover.

2. This comprises the value of any defined benefit pension accrued, any payments by LV= into the defined contribution section of our pension scheme and any cash allowance paid in lieu of foregone contributions as appropriate.

3. This relates to the payment of the annual bonus for the year ended 31 December 2014. For Mr Rogers and Mr Moore an element of these full year amounts will be subject to deferral.

4. This relates to the vesting of the 2012 LTIP award. The performance period for this award ended on 31 December 2014. Two-thirds of the figures shown are deferred to be paid in equal tranches in May 2016 and May 2017

5. Appointed to role of chairman on 23 May 2013.6. Appointed 1 June 2013.7. Resigned on 23 May 2013.

£’000Salary

and feesOther

benefits1 Pension2Annual bonus3

Long-term incentives4 Total

M Rogers 2014 528 15 116 636 371 1,666

2013 518 17 114 424 1,291 2,364

P Moore 2014 360 14 50 270 191 885

2013 353 14 49 240 661 1,317

R Rowney 2014 320 13 67 200 – 600

2013 313 15 87 190 574 1,179

J O’Roarke 2014 294 13 65 300 – 672

2013 288 14 80 150 – 532

M Austen5 2014 177 – – – – 177

2013 135 – – – – 135

D Neave6 2014 68 – – – – 68

2013 39 – – – – 39

J Edwards 2014 73 – – – – 73

2013 69 – – – – 69

C Keers 2014 67 – – – – 67

2013 65 – – – – 65

C Burton 2014 64 – – – – 64

2013 61 – – – – 61

J Dean 2014 68 – – – – 68

2013 61 – – – – 61

D Holt7 2014 – – – – – –

2013 65 – – – – 65

Total 2014 2,019 55 298 1,406 562 4,340

2013 1,967 60 330 1,004 2,526 5,887

27

£’000Salary

and feesOther

benefits1 Pension2Annual bonus3

Long-term incentives4 Total

M Rogers 2014 528 15 116 636 371 1,666

2013 518 17 114 424 1,291 2,364

P Moore 2014 360 14 50 270 191 885

2013 353 14 49 240 661 1,317

R Rowney 2014 320 13 67 200 – 600

2013 313 15 87 190 574 1,179

J O’Roarke 2014 294 13 65 300 – 672

2013 288 14 80 150 – 532

M Austen5 2014 177 – – – – 177

2013 135 – – – – 135

D Neave6 2014 68 – – – – 68

2013 39 – – – – 39

J Edwards 2014 73 – – – – 73

2013 69 – – – – 69

C Keers 2014 67 – – – – 67

2013 65 – – – – 65

C Burton 2014 64 – – – – 64

2013 61 – – – – 61

J Dean 2014 68 – – – – 68

2013 61 – – – – 61

D Holt7 2014 – – – – – –

2013 65 – – – – 65

Total 2014 2,019 55 298 1,406 562 4,340

2013 1,967 60 330 1,004 2,526 5,887

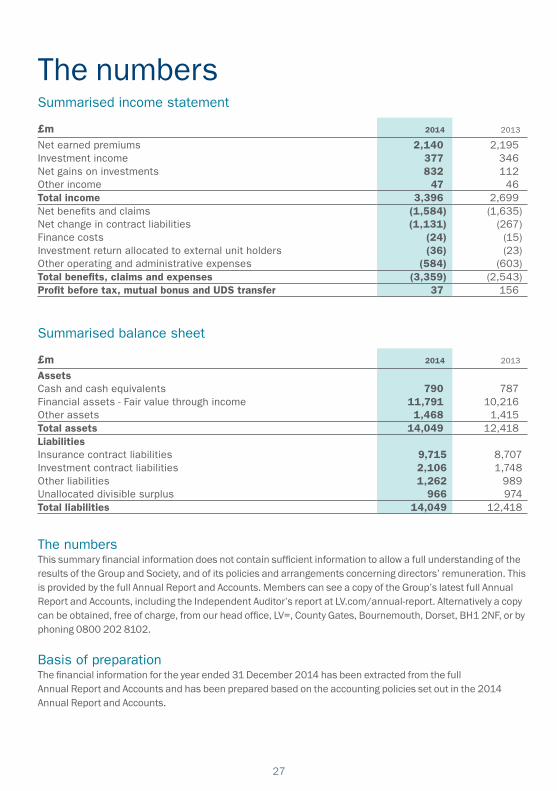

The numbers

£m 2014 2013

Net earned premiums 2,140 2,195Investment income 377 346Net gains on investments 832 112Other income 47 46Total income 3,396 2,699Net benefits and claims (1,584) (1,635)Net change in contract liabilities (1,131) (267)Finance costs (24) (15)Investment return allocated to external unit holders (36) (23)Other operating and administrative expenses (584) (603)Total benefits, claims and expenses (3,359) (2,543)Profit before tax, mutual bonus and UDS transfer 37 156

Summarised income statement

£m 2014 2013

AssetsCash and cash equivalents 790 787Financial assets - Fair value through income 11,791 10,216Other assets 1,468 1,415Total assets 14,049 12,418LiabilitiesInsurance contract liabilities 9,715 8,707Investment contract liabilities 2,106 1,748Other liabilities 1,262 989Unallocated divisible surplus 966 974Total liabilities 14,049 12,418

The numbersThis summary financial information does not contain sufficient information to allow a full understanding of the results of the Group and Society, and of its policies and arrangements concerning directors’ remuneration. This is provided by the full Annual Report and Accounts. Members can see a copy of the Group’s latest full Annual Report and Accounts, including the Independent Auditor’s report at LV.com/annual-report. Alternatively a copy can be obtained, free of charge, from our head office, LV=, County Gates, Bournemouth, Dorset, BH1 2NF, or by phoning 0800 202 8102.

Basis of preparationThe financial information for the year ended 31 December 2014 has been extracted from the full Annual Report and Accounts and has been prepared based on the accounting policies set out in the 2014 Annual Report and Accounts.

Summarised balance sheet

Some legal stuff:

Liverpool Victoria Friendly Society Limited: County Gates, Bournemouth BH1 2NF

LV= and Liverpool Victoria are registered trade marks of Liverpool Victoria Friendly Society Limited (LVFS) and LV= and LV= Liverpool Victoria are trading styles of the Liverpool Victoria group of companies. LVFS is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority, register number 110035. Registered address: County Gates, Bournemouth BH1 2NF. Telephone: 01202 292333.

21546380 04/15

If you have a query about your existing policy

0800 085 4499This phone line is available from 8.30am to 6.30pm on weekdays. For textphone dial 18001 first.

Our website is

LV.comFor useful news from LV=

LV.com/atheartFind out about your member benefits at

LV.com/membersQueries about being a member can be emailed to

[email protected] the community at

LV.com/communityOur address is

County Gates, Bournemouth, BH1 2NF

You can get this and other documents from us in Braille and large print by contacting us.

Check out our full 2014 Annual Report online LV.com/annual-report