your partner in paper 2006 - international color … february 2, 2006 2 contents your partner in...

TRANSCRIPT

Your Partner in Paper 2006

February 2, 2006UPM 2

Contents

Your Partner in PaperKey figuresPaper capacitiesPaper marketsPaper gradesPositioning - WorldPositioning – EuropeTrade flowsDemandGeneral informaation

UPM – Key figuresUPM – Key figures

February 2, 2006UPM 4

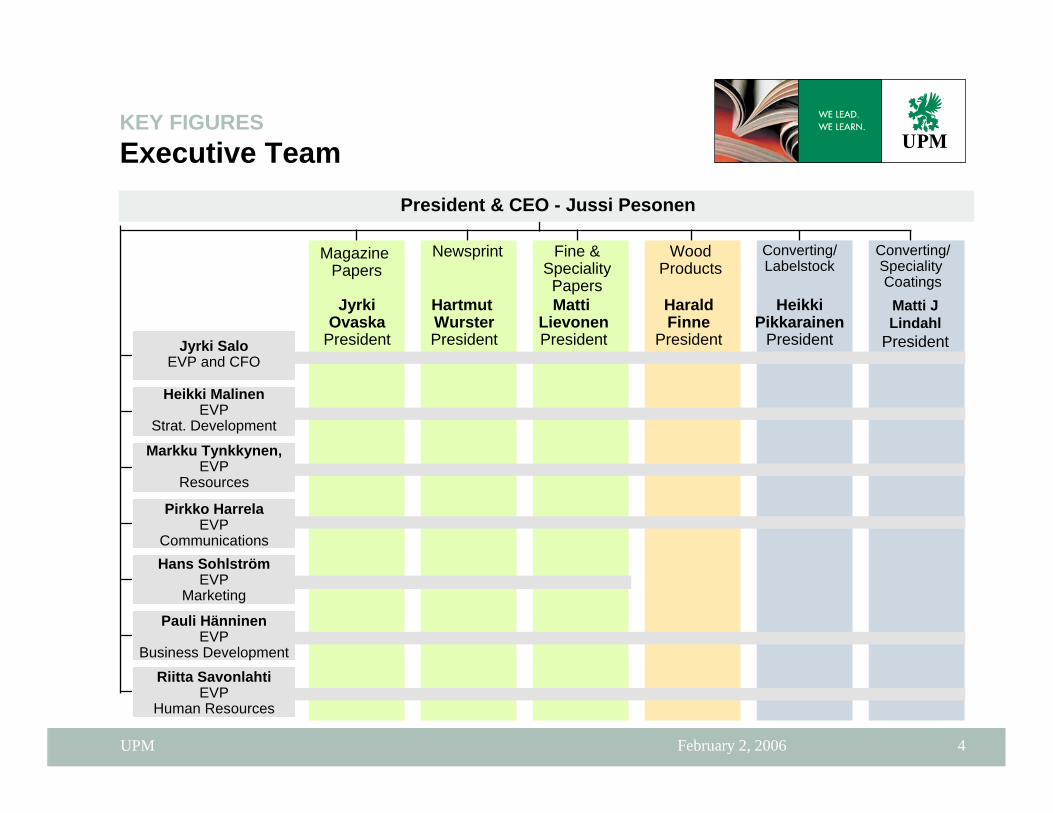

KEY FIGURESExecutive Team

President & CEO - Jussi Pesonen

Magazine Papers

Newsprint Fine & Speciality Papers

Wood Products

Jyrki SaloEVP and CFO

Riitta SavonlahtiEVP

Human Resources

Pauli HänninenEVP

Business Development

Hans SohlströmEVP

Marketing

Pirkko HarrelaEVP

Communications

Markku Tynkkynen,EVP

Resources

Heikki MalinenEVP

Strat. Development

Converting/Speciality Coatings

Converting/Labelstock

HartmutWursterPresident

JyrkiOvaska

President

MattiLievonenPresident

HaraldFinne

President

Matti JLindahl

President

HeikkiPikkarainen

President

February 2, 2006UPM 5

1,000 tons1,000 m3

1,000 m3

1,000 tons

EUR million

EUR million

31,500

10,2202,150

9701,840

260

9,348

2005

9,7909,820Sales total

10,2302,410

9402,030

10,8902,410

9702,240

Paper productionSawn timberPlywoodChemical pulp

430560Profit before tax

34,500

2003

33,400Personnel at 31.12

2004

KEY FIGURESUPM – Key figures 2005-2002

February 2, 2006UPM 6

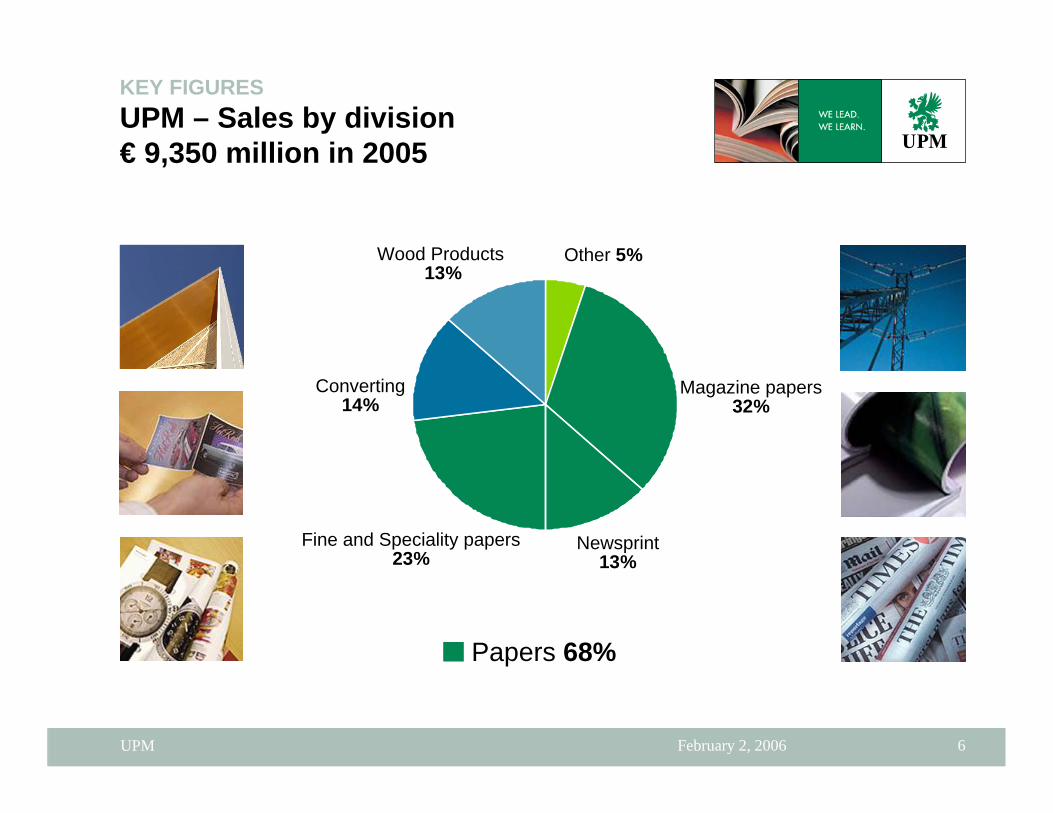

Papers 68%

Converting14%

Wood Products13%

Other 5%

Newsprint13%

Magazine papers32%

Fine and Speciality papers23%

KEY FIGURES UPM – Sales by division € 9,350 million in 2005

February 2, 2006UPM 7

Other EU 22%France 7%

Asia 9%

North America 14%

Germany 16%

Finland 10%

UK 13%

KEY FIGURES UPM - Sales by market area 2005

Other Europe 5%

Other 4%

Total sales € 9,350 millionEU 70%, Europe 74%

February 2, 2006UPM 8

Converting11%

Other operations11%

Magazine papers26%

Fine and speciality papers21%

Newsprint11%

KEY FIGURES UPM – Personnel by division 31.12.2005

Wood Products20%

Total personnel 31,500

February 2, 2006UPM 9

Other EU 5%

France 5%

Asia Pacific 5%North America 6%

Germany 14%

Finland 55%

UK 5%

KEY FIGURES UPM – Personnel by area 31.12.2005

Other Europe 5%

Total personnel 31,500

February 2, 2006UPM 10

Paper capacitiesPaper capacities

February 2, 2006UPM 11

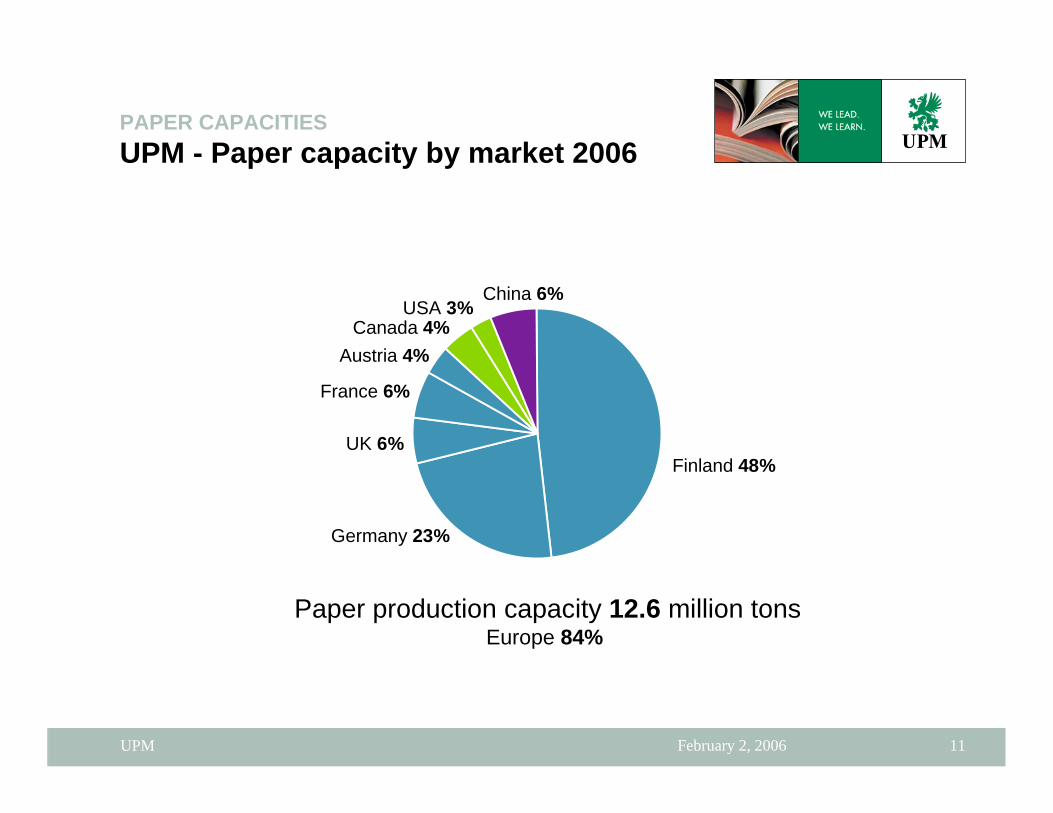

USA 3%

France 6%

Canada 4%

China 6%

Germany 23%

Finland 48%UK 6%

Paper production capacity 12.6 million tonsEurope 84%

PAPER CAPACITIESUPM - Paper capacity by market 2006

Austria 4%

February 2, 2006UPM 12

PAPER CAPACITIESUPM – paper capacity by market 2006

350

450

490

780

800

800

2930

6020

0 1000 2000 3000 4000 5000 6000 7000

Finland

Germany

China

Great Britain

France

Austria

Canada

USA

'000 tons

Total 12.6 mill. tons of which 52% outside Finland

February 2, 2006UPM 13

PAPER CAPACITIESUPM – Total paper capacity by paper division 2006

0 1000 2000 3000 4000 5000 6000

Magazine Papers

Newsprint

Fine and SpecialityPapers

Total 12.6 mill. tons of which 52% outside Finland

Coated mech. 3,870 SC Magazine1,850

Newsprint 2,810

Coated WF1,680

Uncoated WF1,620

Specs790

'000 tons

February 2, 2006UPM 14

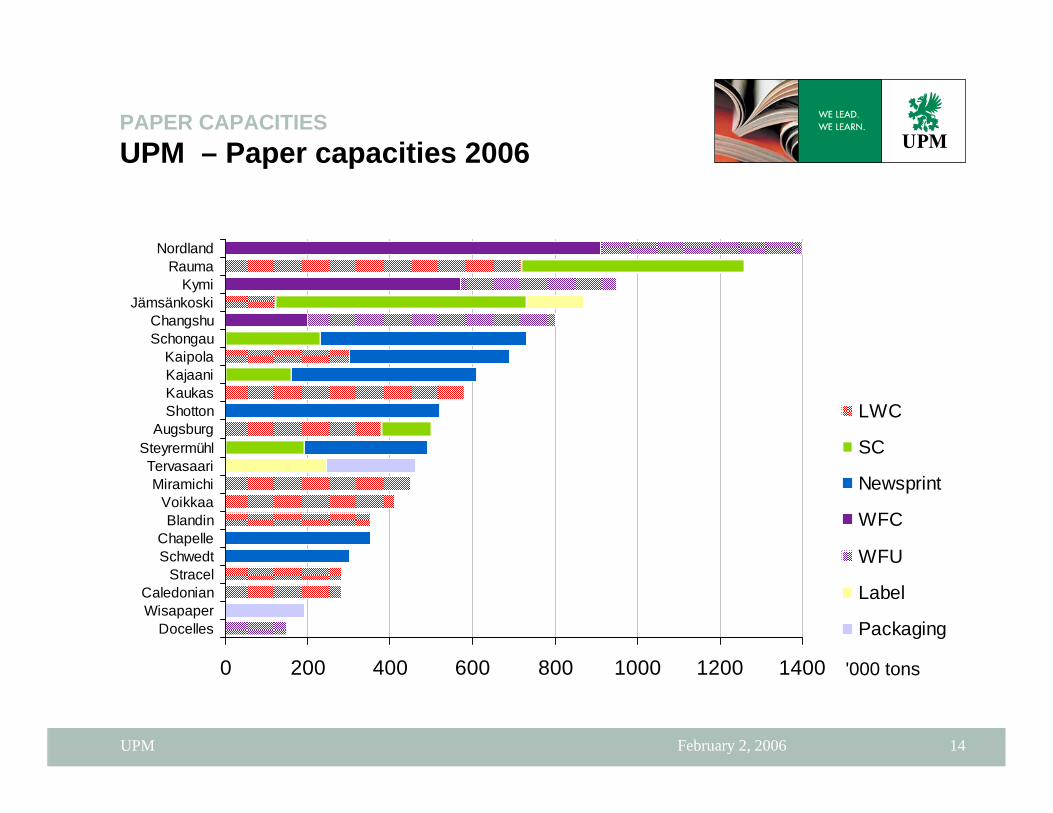

PAPER CAPACITIESUPM – Paper capacities 2006

0 200 400 600 800 1000 1200 1400

NordlandRauma

KymiJämsänkoski

ChangshuSchongau

KaipolaKajaaniKaukasShotton

AugsburgSteyrermühlTervasaariMiramichi

VoikkaaBlandin

ChapelleSchwedt

StracelCaledonianWisapaper

Docelles

LWC

SC

Newsprint

WFC

WFU

Label

Packaging

'000 tons

February 2, 2006UPM 15

3870

1850

2810

1680

1620

790

Coated Mechanical

SC

Newsprint

WF Coated

WF Uncoated

Speciality Papers

PAPER CAPACITIESUPM – Total paper capacity 2006

Total 12.6 mill. tons

’000 tons

February 2, 2006UPM 16

PAPER CAPACITIESUPM Paper DivisionsPaper and pulp capacities 2006

450Miramichi

775190Wisapaper/Wisapulp4,090

460

1,400

950

140150

800

Fine &Specs.

2,295

240

520740

Pulp

Tervasaari

Docelles

300190Steyrermühl

1,260Rauma500230Schongau

500Augsburg

2,8105, 720Total capacity

410Voikkaa

280Stracel

520Shotton300Schwedt

Nordland

Kymi580Kaukas

450160Kajaani390300Kaipola

730Jämsänkoski

350ChapelleChangshu

280Caledonian350Blandin

NewsMag'000 tons

UPM paper marketsUPM paper markets

February 2, 2006UPM 18

Changshu

MiramichiBlandin

PAPER MARKETS UPM - Paper and pulp mills in the world

KajaaniVoikkaaKymi(also pulp)Kaukas(also pulp)

Pietarsaari (also pulp)Jämsäkoski

KaipolaTervasaari (also pulp)

Rauma

Augsburg

Caledonian

Shotton

ChapelleDocelles

Stracel Steyremühl

SchwedtNordland

Schongau

February 2, 2006UPM 19

PAPER MARKETS UPM – Paper Mill Heads

Timo SuutarlaMiramichi

Raimo SärkeläVoikkaa

Jari A VainioWisapaper

Eero KuokkanenTervasaari

Philippe GaudronStracel

Walter PillweinSteyrermühl

David InghamShotton

Juha KääriäinenSchwedt

Artur StöcklerSchongau

Pertti AsunmaaRauma

Hannu JokisaloNordland

Harry Sundqvist =>1.3.2006Kaukas

Leo LindroosKaipola

Kari PasanenKajaani

Sebastian LoewenbergAugsburg

Michel ChakaïDocelles

Yngve LindströmKymi

Erkki PuruJämsänkoski

Timo HeinonenChapelle

Hannu JokisaloChangshu

Gordon MitchellCaledonian

Joe MaherBlandin

February 2, 2006UPM 20

Uncoated Woodfree11%

Speciality Papers7%

Coated Papers31%

Newsprint25%

SC Magazine15%

PAPER MARKETS Paper sales by product category 2005

Coated Woodfree11%

Total 10.1 million tons

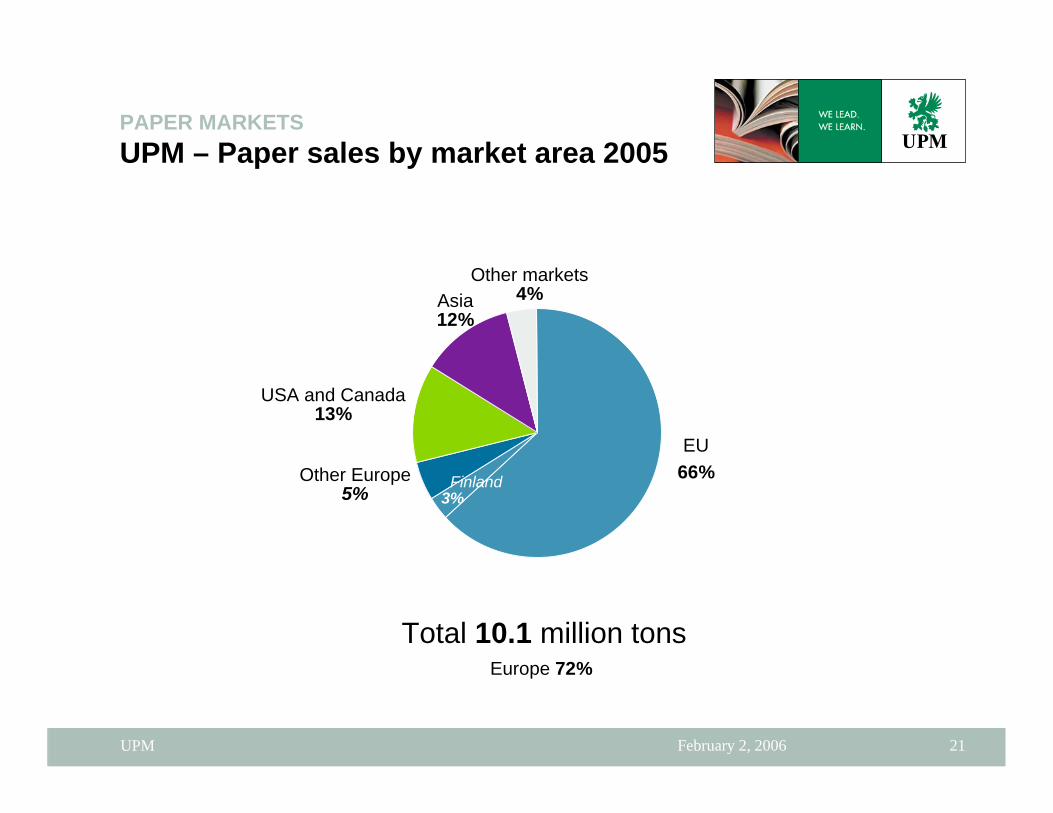

February 2, 2006UPM 21

USA and Canada13%

Other markets4%

Finland3%

Europe 72%

PAPER MARKETS UPM – Paper sales by market area 2005

Asia12%

Total 10.1 million tons

EU66%Other Europe

5%

February 2, 2006UPM 22

UPM – Top market areas 2005

7988100103115117133

178199205215226

345368395

477738

12281443

19361. Germany2. Great Britain

3. USA4. France

5. Italy6. China7. Spain

8. Finland9. Japan

10. Netherlands11. Austria12. Poland

13. Belgium14. Switzerland

15. Australia16. Russia

17. Denmark18. Turkey

19. India20. Korea

Total paper sales 10.1 million tons

’000 tons

February 2, 2006UPM 23

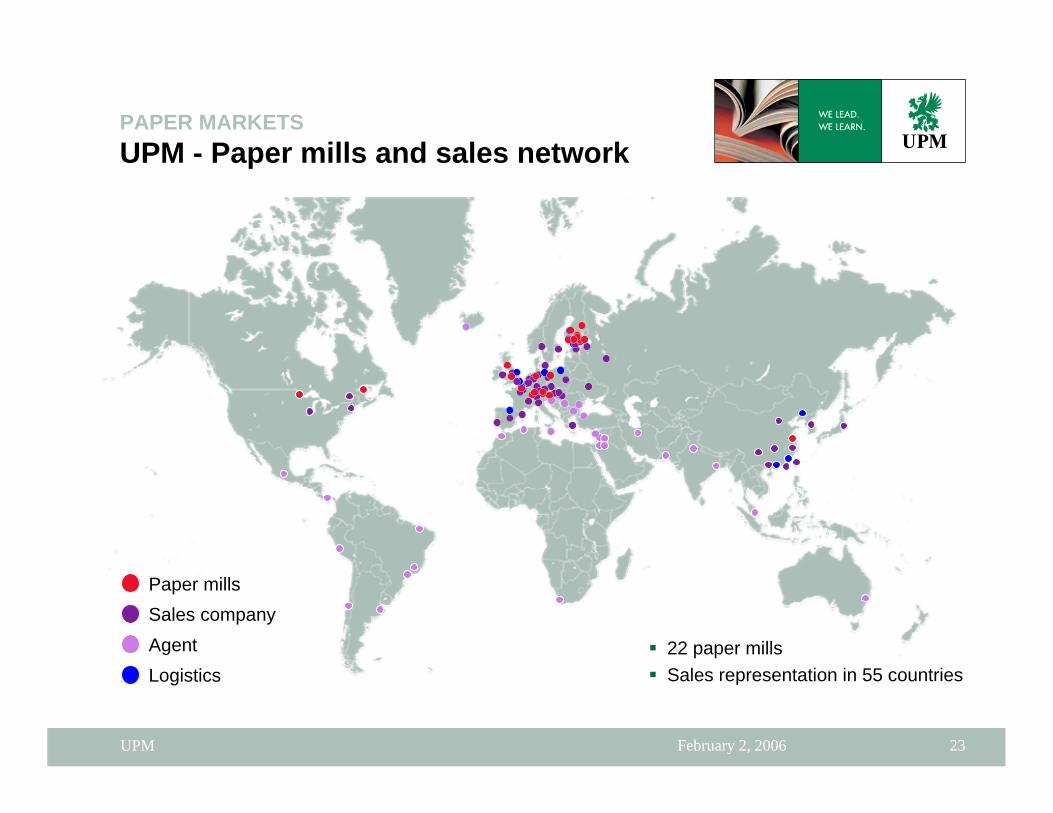

PAPER MARKETS UPM - Paper mills and sales network

Sales companyAgentLogistics

Paper mills

22 paper millsSales representation in 55 countries

February 2, 2006UPM 24

PAPER MARKETS Paper supply chain from mills to customers

Austria 1Canada 1China 1Finland 9France 3Germany 4Great Britain 2USA 1

Sales representationin 55 countriescustomers in 120 countries

22 paper mills in

12.6 million tons, 51 PMs

February 2, 2006UPM 25

Paper grades

February 2, 2006UPM 26

Relative quality

Relative price

KAUKAS, RAUMA

JÄMSÄNKOSKI, STRACEL, VOIKKAA

CHAPELLE, KAIPOLA, KAJAANI, SCHONGAU

CHAPELLE, KAIPOLA, KAJAANI, SCHONGAU, SCHWEDT, SHOTTON, STEYRERMÜHL

CHANGSHU, KYMI, NORDLAND

UPM News

UPM Brite, UPM Opalite,UPM Color

UPM Smart, UPM Cat,UPM Lux, UPM Max, UPM Eco

UPM Satin, UPM Matt

UPM Ultra, UPM Cote

UPM Star

UPM Fine

UPM Finesse

JÄMSÄNKOSKI, KAJAANI, RAUMA, SCHONGAU,STEYRERMÜHL

AUGSBURG, BLANDIN, CALEDONIA, KAIPOLA, KAUKAS,MIRAMICHI, RAUMA, STRACEL, VOIKKAA

CHANGSHU, KYMI, NORDLAND

News

MFS

SC

MFC

LWC

MWC

WFU

WFC

PAPER GRADES Relative quality and price of paper grades

February 2, 2006UPM 27

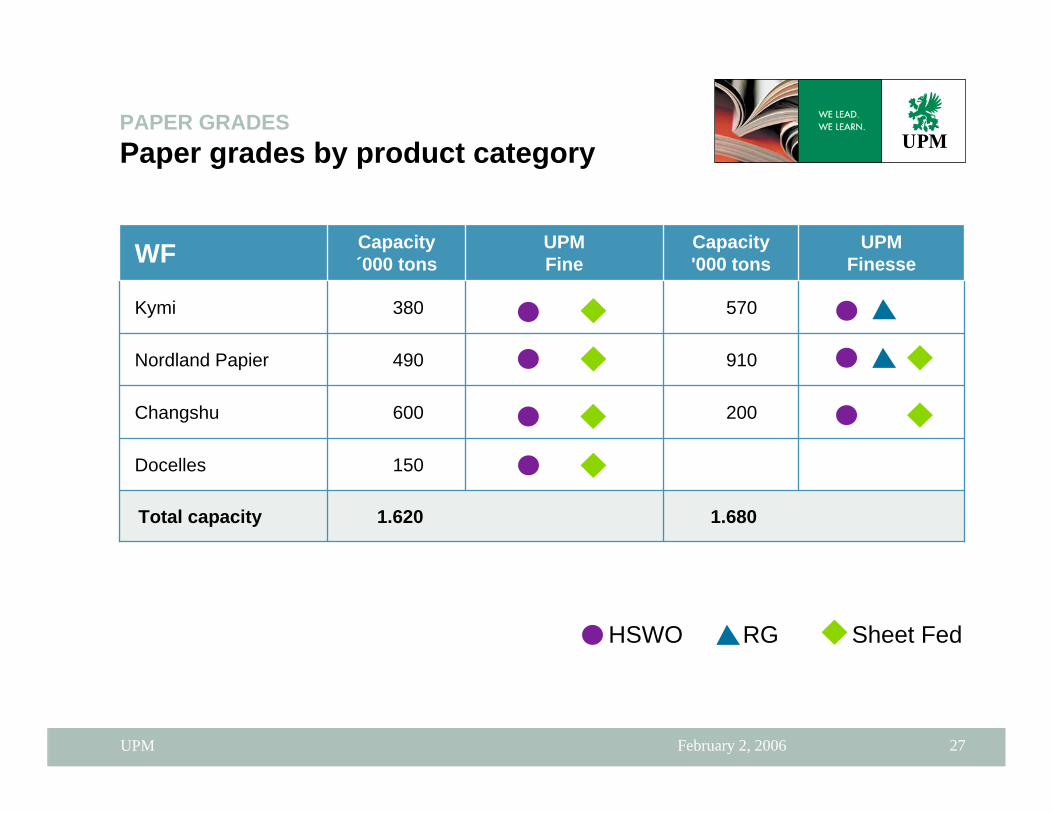

PAPER GRADES Paper grades by product category

1.680

200

910

570

Capacity'000 tons

UPMFinesse

150Docelles

1.620

600

490

380

Capacity´000 tons

UPMFine

Kymi

Changshu

Total capacity

Nordland Papier

WF

HSWO RG Sheet Fed

February 2, 2006UPM 28

PAPER GRADES Paper grades by product category

350Blandin

UPMSatin

UPMCote

3,870Total capacity410Voikkaa280Stracel720Rauma450Miramichi580Kaukas300Kaipola120Jämsänkoski280Caledonian Paper

380Augsburg

UPMMatt

UPMUltra

UPMStar

Capacity'000 tons

MWC, LWC, MFC

HSWO CSWO RG

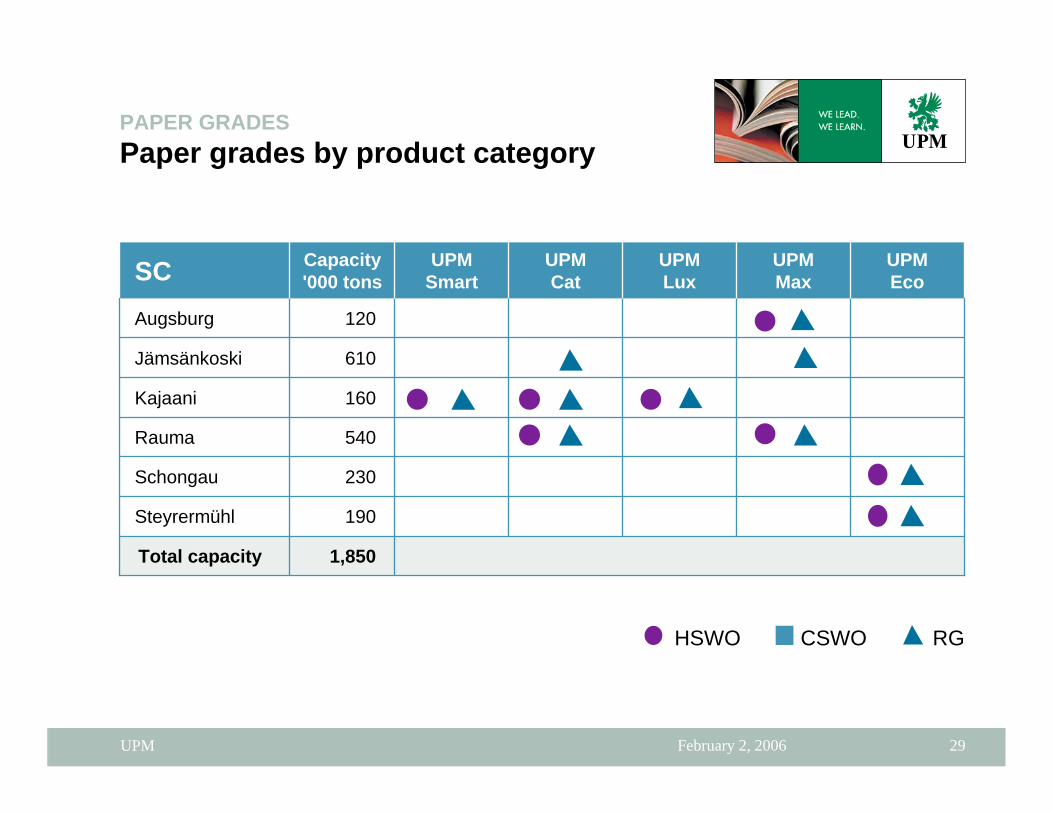

February 2, 2006UPM 29

1,850

190

230

540

160

610

120

Capacity'000 tons

UPMSmart

UPMLux

Augsburg

Steyrermühl

Schongau

UPMEco

Total capacity

Rauma

Kajaani

Jämsänkoski

UPMMax

UPMCatSC

PAPER GRADES Paper grades by product category

HSWO CSWO RG

February 2, 2006UPM 30

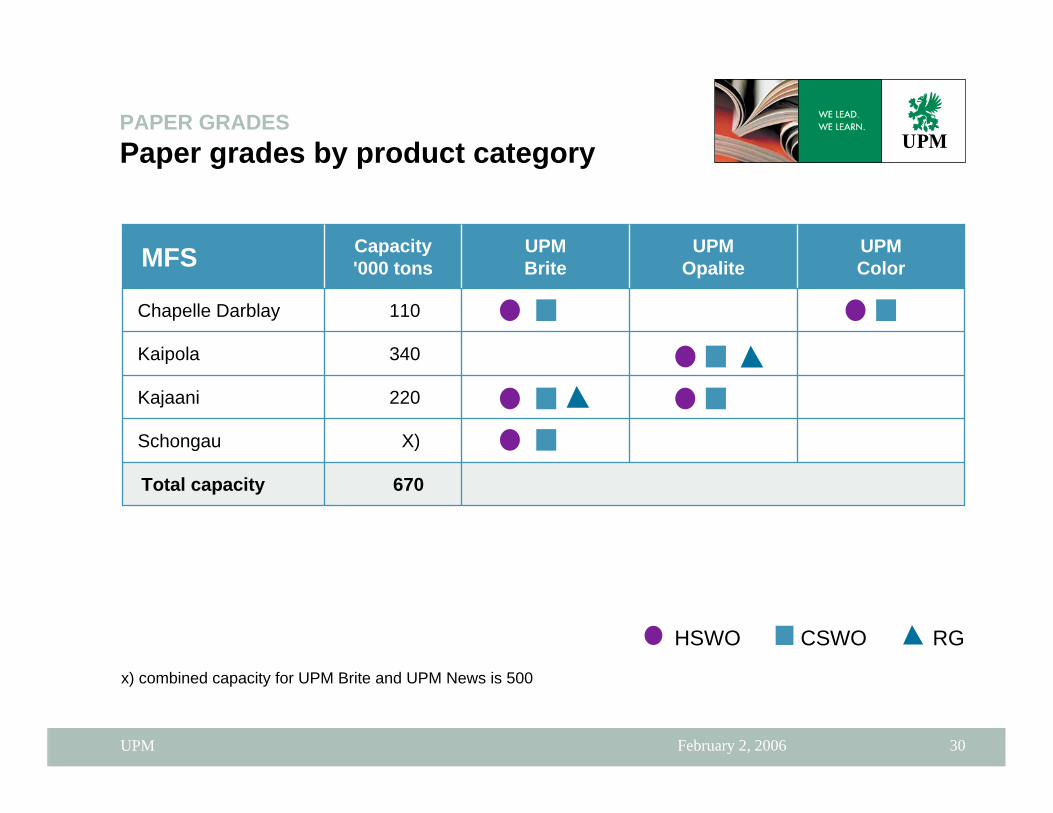

PAPER GRADES Paper grades by product category

110Chapelle Darblay

X)Schongau

UPMOpalite

UPMBrite

670Total capacity

220Kajaani

340Kaipola

UPMColor

Capacity'000 tonsMFS

x) combined capacity for UPM Brite and UPM News is 500

HSWO CSWO RG

February 2, 2006UPM 31

PAPER GRADES Paper grades by product category

240 Chapelle Darblay

500 x)Schongau

230Kajaani

2.140Total capacity

300Steyrermühl

520Shotton

300Schwedt

50Kaipola

UPMNews

Capacity'000 tonsNews

x) combined capacity for UPM Brite and UPM News is 500

HSWO CSWO RG

February 2, 2006UPM 32

PAPER GRADES Reel papers for various end uses

UPM SmartSCUPM Matt

UPM Lux

UPM NewsNewsUPM ColorUPM OpaliteUPM BriteMFSUPM EcoUPM Max

UPM Cat

UPM SatinUPM CoteUPM UltraUPM StarMWC,

LWC,MFC

UPM FinesseUPM FineFine

Mag

azin

es

Cat

alog

ues

New

s-pa

pers

Spe

cial

N

ewsp

.

Sup

ple-

men

ts

Inse

rts

Dire

ctor

ies

Dire

ct m

ail

Adv

ertis

ing

Mat

eria

ls

Boo

ks

Oth

er

end-

uses

February 2, 2006UPM 33

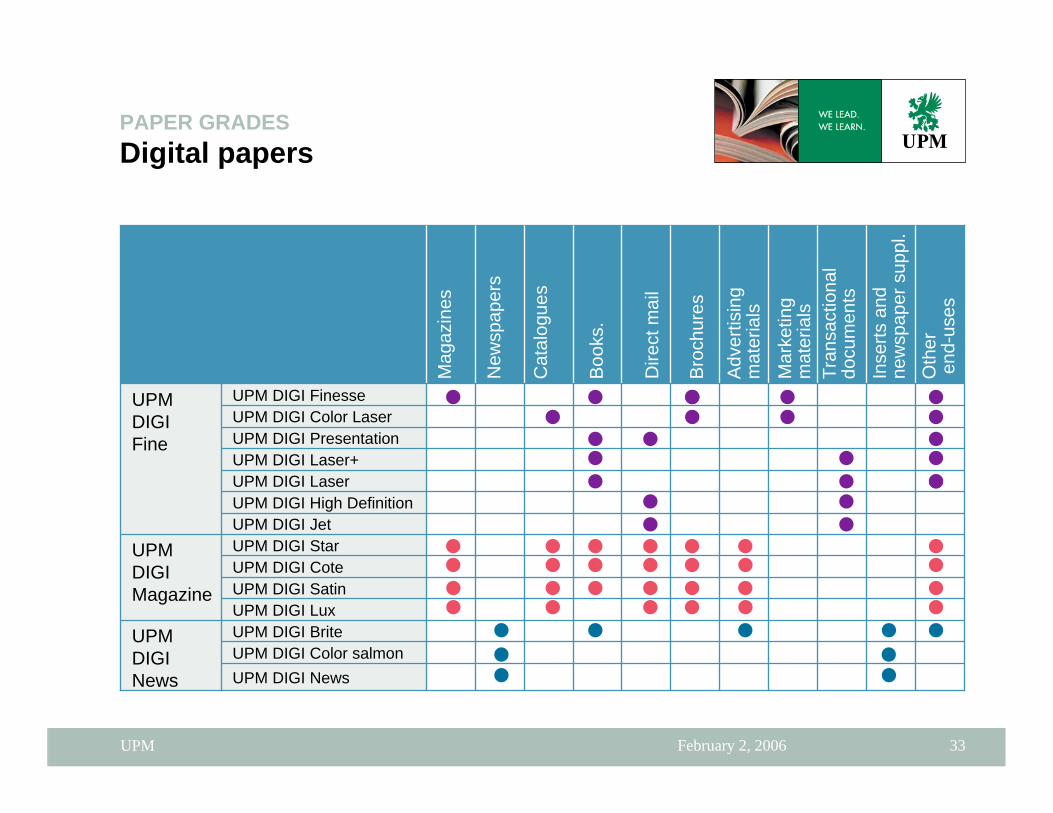

PAPER GRADES Digital papers

UPM DIGI High DefinitionUPM DIGI Laser

UPMDIGIFine

UPM DIGI Jet

UPM DIGI CoteUPM DIGI Star

UPM DIGI Lux

UPM DIGI NewsUPM DIGI Color salmonUPM DIGI BriteUPM

DIGINews

UPM DIGI Satin

UPM DIGI Laser+UPM DIGI PresentationUPM DIGI Color LaserUPM DIGI Finesse

UPM DIGIMagazine

Mag

azin

es

Mar

ketin

g m

ater

ials

Cat

alog

ues

Boo

ks.

Dire

ct m

ail

Bro

chur

es

Adv

ertis

ing

mat

eria

ls

Tran

sact

iona

ldo

cum

ents

Inse

rts a

nd

new

spap

er s

uppl

.O

ther

en

d-us

es

New

spap

ers

February 2, 2006UPM 34

PAPER GRADES Office papers

UPM LetterUPM PosteUPM PrestigeUPM PrintUPM FormulaUPM Natura

UPM PrelaserUPM PrePersonalUPM PrePersonal+UPM PrePremiumUPM PreInsertUPM FormUPM Finesse Matt

Yes Professional Photo paperYes Photo paper

Yes Professional Business cardYes Premium Business card

Yes ColorinkjetYes ColorcopyYes HeavyweightYes Gold presentationYes silver multifuctionYes Bronze copy/print

Future colorinktechFuture imagetechFuture smoothtechFuture inktechFuture multitechFuture lasertech

UPM Officecolor inkjetUPM Office color laserUPM Office presentation plusUPM Office presentationUPM Office multifunctionUPM Office copy/print

UPM MailPrePrintPapers

Photo-realistic printing

SpecialendusesYesFutureUPM Office

Papers for copying and printing (A4, A3)

February 2, 2006UPM 35

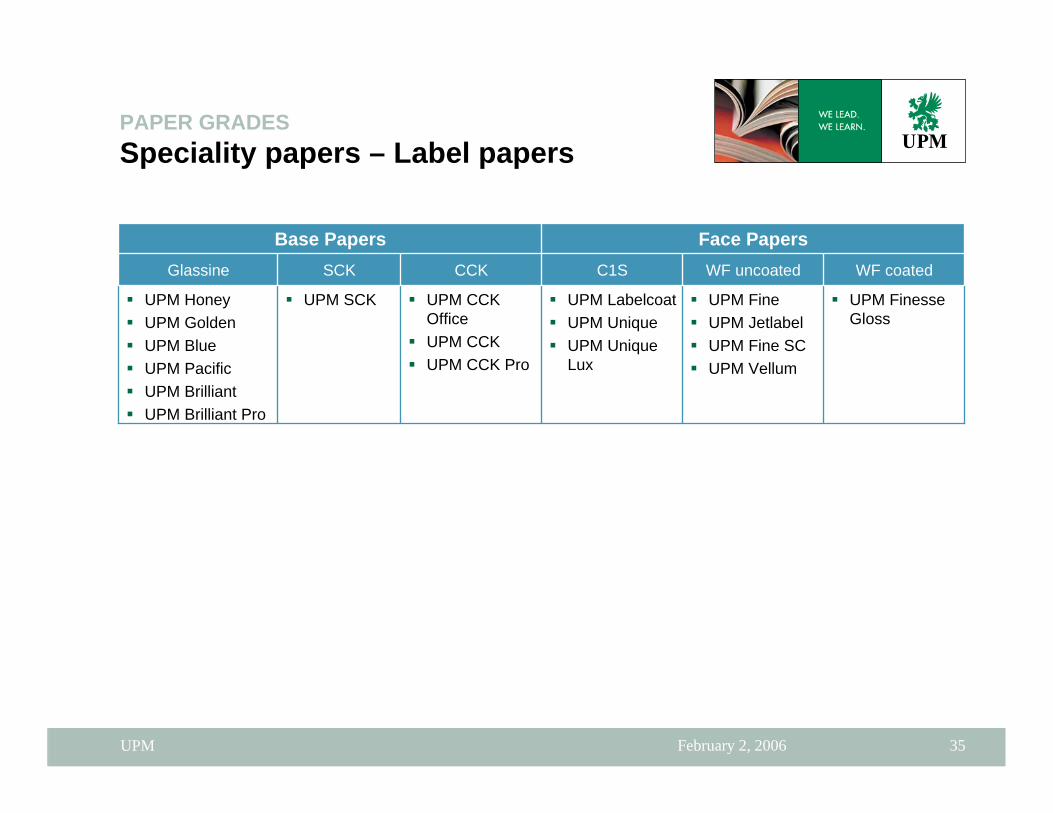

PAPER GRADES Speciality papers – Label papers

WF coatedWF uncoatedC1S

UPM Finesse Gloss

UPM FineUPM JetlabelUPM Fine SCUPM Vellum

UPM LabelcoatUPM UniqueUPM Unique Lux

UPM CCK OfficeUPM CCKUPM CCK Pro

UPM SCKUPM HoneyUPM GoldenUPM BlueUPM PacificUPM BrilliantUPM Brilliant Pro

Face PapersCCKSCKGlassine

Base Papers

February 2, 2006UPM 36

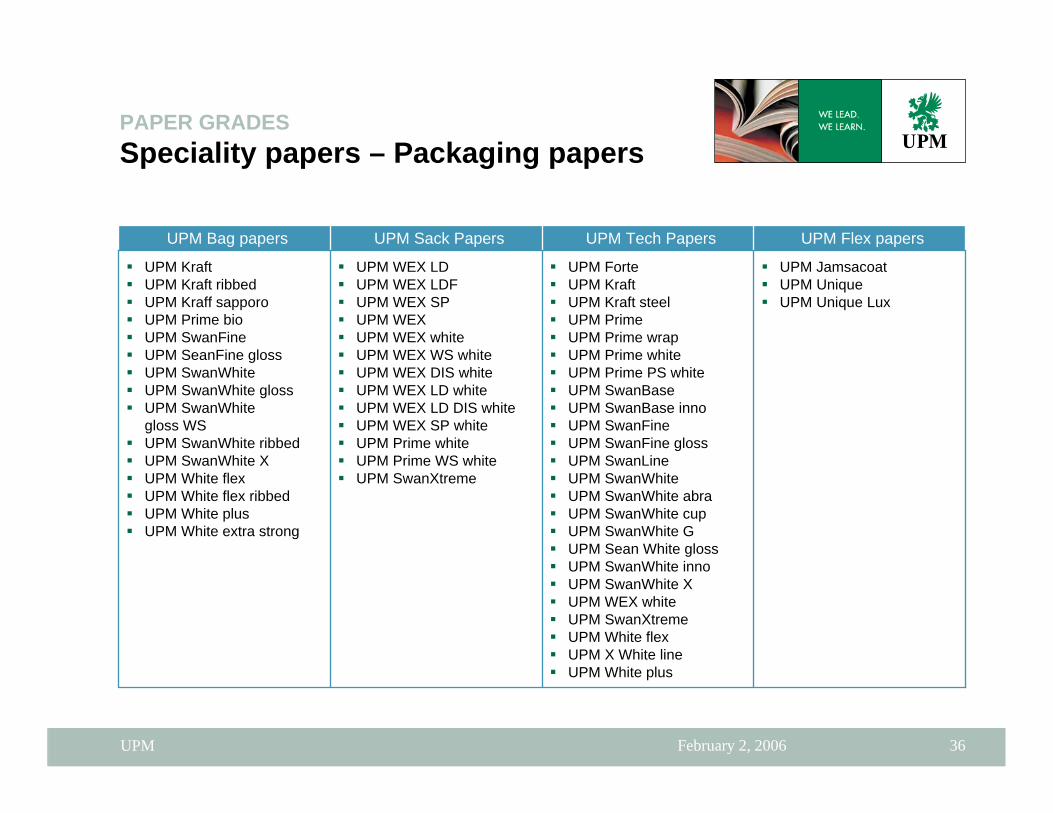

PAPER GRADES Speciality papers – Packaging papers

UPM Flex papers

UPM JamsacoatUPM UniqueUPM Unique Lux

UPM ForteUPM KraftUPM Kraft steelUPM PrimeUPM Prime wrapUPM Prime whiteUPM Prime PS whiteUPM SwanBaseUPM SwanBase innoUPM SwanFineUPM SwanFine glossUPM SwanLineUPM SwanWhiteUPM SwanWhite abraUPM SwanWhite cupUPM SwanWhite GUPM Sean White glossUPM SwanWhite innoUPM SwanWhite XUPM WEX whiteUPM SwanXtremeUPM White flexUPM X White lineUPM White plus

UPM WEX LDUPM WEX LDFUPM WEX SPUPM WEXUPM WEX whiteUPM WEX WS whiteUPM WEX DIS whiteUPM WEX LD whiteUPM WEX LD DIS whiteUPM WEX SP whiteUPM Prime whiteUPM Prime WS whiteUPM SwanXtreme

UPM KraftUPM Kraft ribbedUPM Kraff sapporoUPM Prime bioUPM SwanFineUPM SeanFine glossUPM SwanWhiteUPM SwanWhite glossUPM SwanWhitegloss WSUPM SwanWhite ribbedUPM SwanWhite XUPM White flexUPM White flex ribbedUPM White plusUPM White extra strong

UPM Tech PapersUPM Sack PapersUPM Bag papers

February 2, 2006UPM 37

PAPER GRADES Examples of end uses

Mechanicalpulp and/ordeinked pulp

magazines, brochures, direct mail, annual reports,books, advertising materialWoodfree coated papers

sacks, bags, wrapping and packaging, envelopesKraft papers

office papers, writing papers and envelopes, direct mail, magazines, books, advertising materialWoodfree uncoated papers

label paper, label release papers, food wrapping,household and sanitary papers, baking paper,packaging material

Speciality papers

Chemical pulp

magazines, catalogues, newspaper supplements,advertising material, books, direct mailCoated mechanical papers

magazines, catalogues, newspaper supplements,inserts, advertising materialSC papersChemical

and mechanicalpulp

newspaper supplements, newspapers, directories,magazines, books, catalogues, advertising materialmechanical speciality paper

newspapers, inserts, flyersnewsprint

End use examplesPaper gradeRaw material

February 2, 2006UPM 38

PAPER GRADES UPM Printing Papers

February 2, 2006UPM 39

PAPER GRADES Fine papers

high-brightness, double coated woodfree paper (WFC)

matt or calendered,uncoated woodfree paper (WFU)

February 2, 2006UPM 40

PAPER GRADES MWC, LWC, MFC

high-brightness, double coated mechanical paper (MWC)

high-brightness,coated mechanical paper (LWC)

coated mechanical paper (LWC)

matt finished, coated mechanical paper (MFC)

mechanical speciality paper (MFC) for CSWO

February 2, 2006UPM 41

PAPER GRADES SC papers

high-brightness, supercalenderedmechanical paper (SCA+)

high-brightness, silk finished, supercalendered mechanical paper (SCA+)supercalenderedmechanical paper (SC-A)

on-line calenderedmechanical paper (SC-B)

high-brightness, uncoated groundwood paper

February 2, 2006UPM 42

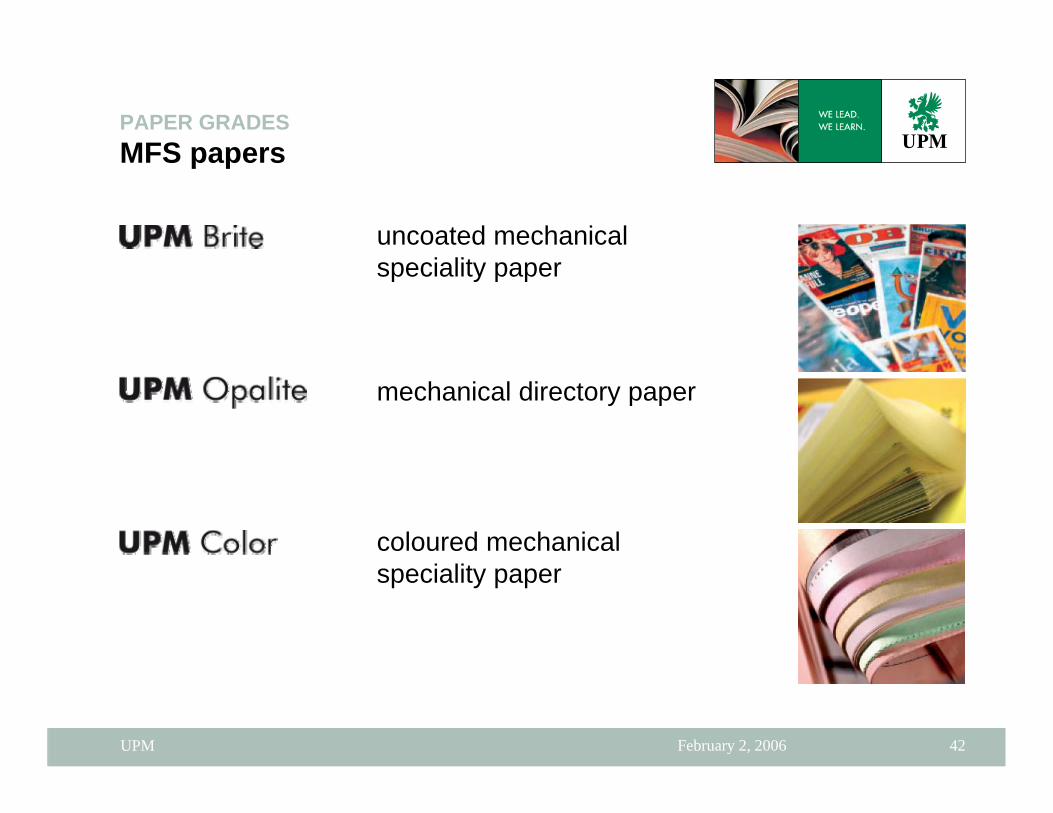

PAPER GRADES MFS papers

uncoated mechanical speciality paper

mechanical directory paper

coloured mechanical speciality paper

February 2, 2006UPM 43

PAPER GRADES Newsprint

newsprint

February 2, 2006UPM 44

PAPER GRADES Digi range

Woodfree Fine Papers

Mechanical Newsprint Papers

Mechanical Magazine Papers

UPM DIGI Fine

UPM DIGI Magazine

UPM DIGI News

Positioning - WorldPositioning - World

February 6, 2006UPM 46

0

10

20

30

40

50

60

Newsprint Coated mech. SC WF coated WF uncoated

Rest of the world

Other Europe

UPM

POSITIONING – WORLDUPM’s share in graphic papers capacity 2006

Source: Jaakko Pöyry, UPM

49

mill. tons

2.8UPM 3.9 1.9 1.7 1.6

20

8

28

46

February 2, 2006UPM 47

UPM's market positionBusinesses

3Sawn goods

1PlywoodWood products

1Industrial wrappings

22Self-adhesive labelstockConverted products

3Packaging papers

11Label papers

53Fine papers

52Newsprint

11Magazine papersPaper

GlobalEurope

POSITIONING – WORLDUPM's market positions 2006

February 2, 2006UPM 48

***1Envelope papers

45Woodfree coated papers

11Coated mechanical

***1-3**Packaging papers

11Label papers

86Woodfree uncoated papers

52Newsprint

21SC magazine papers

in the Worldin Europe

POSITIONING – WORLDUPM's paper market positions in 2006*

*) based on capacities **) depending on the product ***) no ranking available

February 6, 2006UPM 49

POSITIONING – WORLDWorld’s biggestgraphic papers producers 2006

0 2000 4000 6000 8000 10000 12000

Stora Enso

UPM

International Paper

Norske Skog

Nippon Paper Group

Abitibi-Consolidated

Asia Pulp & Paper

M-real

Oji

Bowater

’000 tons

Source: JP, UPM

February 6, 2006UPM 50

POSITIONING – WORLDWorld’s biggestgraphic papers producers 2006

0 2000 4000 6000 8000 10000 12000

Stora Enso

UPM

International Paper

Norske Skog

Nippon Paper Group

Abitibi-Consolidated

Asia Pulp & Paper

M-real

Oji

Bowater

News

SC Paper

Coated mech.

WFC

WFU

’000 tons

Source: JP, UPM

February 6, 2006UPM 51

POSITIONING – WORLDWorld’s biggest paper and paperboard producers 2006

0 2 4 6 8 10 12 14 16 18

Stora Enso

International Paper

UPM

Georgia-Pacific

Oji

Weyerhaeuser

Nippon Paper Group

Smurfit Kappa Group

Smurfit-Stone

Asia Pulp & Paper

GraphicPapers

Other paperand board

mill. tons

Source: JP, UPM

February 2, 2006UPM 52

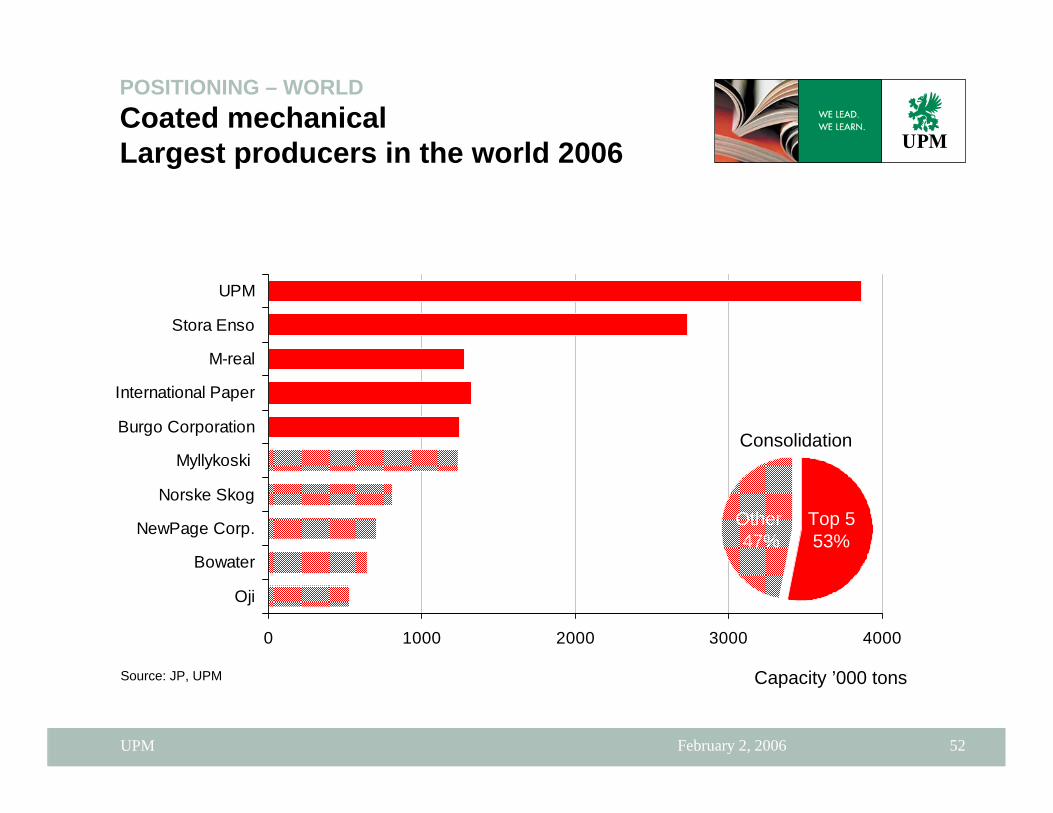

POSITIONING – WORLDCoated mechanicalLargest producers in the world 2006

0 1000 2000 3000 4000

UPM

Stora Enso

M-real

International Paper

Burgo Corporation

Myllykoski

Norske Skog

NewPage Corp.

Bowater

Oji

Capacity ’000 tons

Consolidation

Other 47%

Top 553%

Source: JP, UPM

February 2, 2006UPM 53

POSITIONING – WORLDSC magazineLargest producers in the world 2006

0 500 1000 1500 2000 2500

Stora Enso

UPM

Myllykoski Corporation

Norske Skog

SCA

Irving Pulp & Paper Ltd.

Abitibi-Consolidated

Belgravia Investments Ltd.

Katahdin Paper Co. L.L.C.

Bowater

Capacity ’000 tons

Consolidation

Other 23%

Top 577%

Source: JP, UPM

February 2, 2006UPM 54

POSITIONING – WORLDNewsprint*)

Largest producers in the world 2006

0 1000 2000 3000 4000 5000 6000

Norske Skog

Abitibi-Consolidated

Stora Enso

Bowater

UPM

Nippon Paper Group

Holmen

Catalyst Paper Corp.

Oji

Kruger

Capacity ’000 tons

Consolidation

Other 60%

Top 540%

Sour

ce: J

P, U

PM

*) including TD, improved newsprint, superimproved newsprint and book papers

February 6, 2006UPM 55

POSITIONING – WORLDWoodfree coated paperLargest producers in the world 2006

0 1000 2000 3000

Sappi

Stora Enso

Asia Pulp & Paper

UPM

M-real

Lecta Group

Oji

Burgo Corporation

Nippon Paper Group

NewPage Corp.

Capacity ’000 tons

Consolidation

Other 64%

Top 536%

Source: JP, UPM

February 2, 2006UPM 56

POSITIONING – WORLDWoodfree uncoated paperLargest producers in the world 2006

0 1000 2000 3000 4000 5000 6000

International Paper

Weyerhaeuser

Mondi

Asia Pulp & Paper

Domtar

Stora Enso

Nippon Paper Group

UPM

M-real

Boise Cascade, L.L.C.

Capacity ’000 tons

Consolidation

Other 72%

Top 528%

Source: JP, UPM

August, 2005UPM 57

POSITIONING – WORLDBiggest paper and paperboard producing countries 2004

80,241,7

30,320,119,3

13,111,110,49,99,4

7,97,7

6,36,25,4

59,8

1. USA2. China3. Japan

4. Canada5. Germany

6. Finland7. Sweden

8. Korea,9. France

10. Italy11. Brazil

13. Russia

15. SpainOthers

World production 339 mill. tons change 2004/2003: +2.8%

mill. tons

Source: PPI

12. Indonesia

14. Great Britain

August, 2005UPM 58

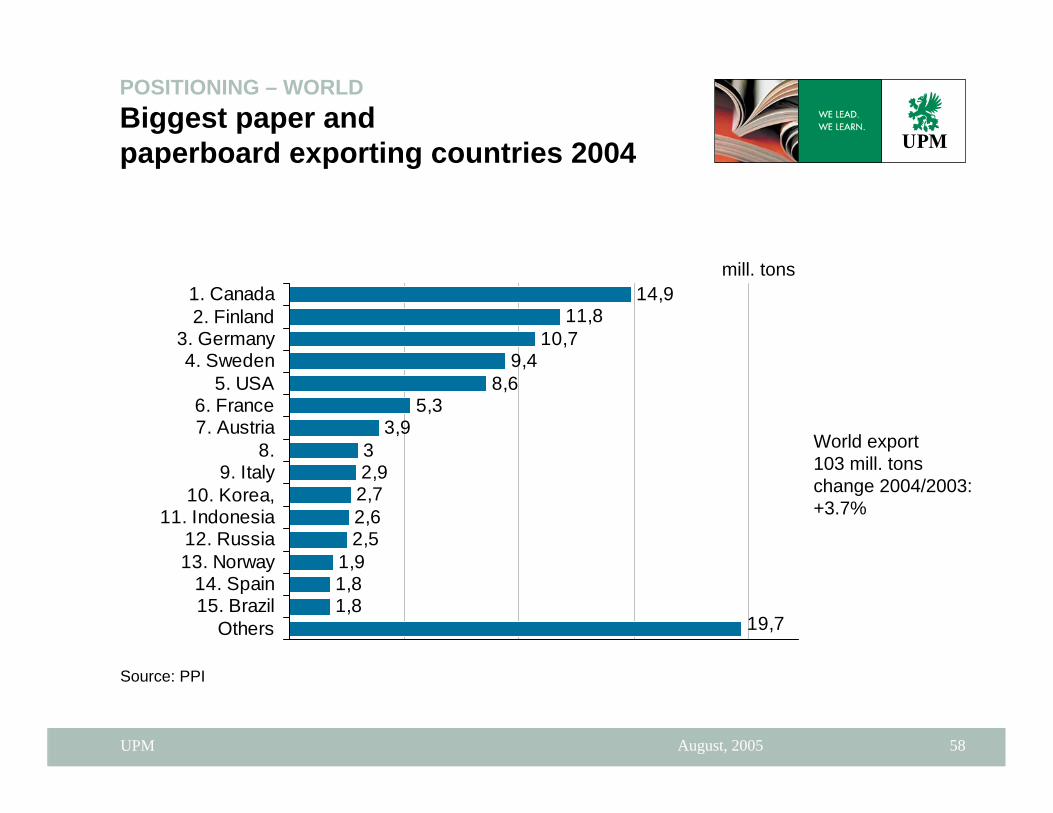

POSITIONING – WORLDBiggest paper and paperboard exporting countries 2004

14,911,8

10,79,4

8,65,3

3,932,92,72,62,5

1,91,81,8

19,7

1. Canada2. Finland

3. Germany4. Sweden

5. USA6. France7. Austria

8.9. Italy

10. Korea,11. Indonesia

12. Russia13. Norway

14. Spain15. Brazil

Others

World export103 mill. tonschange 2004/2003: +3.7%

mill. tons

Source: PPI

August, 2005UPM 59

POSITIONING – WORLDMain paper and board importing countries 2004

16,69,9

7,66,26

4,63,6

3,12,9

2,52,1

1,81,8

1,51,5

1. USA2. Germany

3. Great Britain4. France

5. China6. Italy

7. Spain8. Netherlands

9. Belgium10. Hong

11. Canada12. Mexico13. Japan 14. Poland15. Taiwan

mill. tons

Source: PPI

August, 2005UPM 60

World consumption kg/capita 56 kg

World population million inhabitants6 430

N. AmericaW. Europe

L. America

Oth. Europe

Africa

Oth. Asia

China Japan

OceaniaSource: PPI

POSITIONING – WORLDPaper and paperboardconsumption per capita 2004

31

187267

329

455

33552

6

882

39 280

27

1388

1306

42

247

127

203

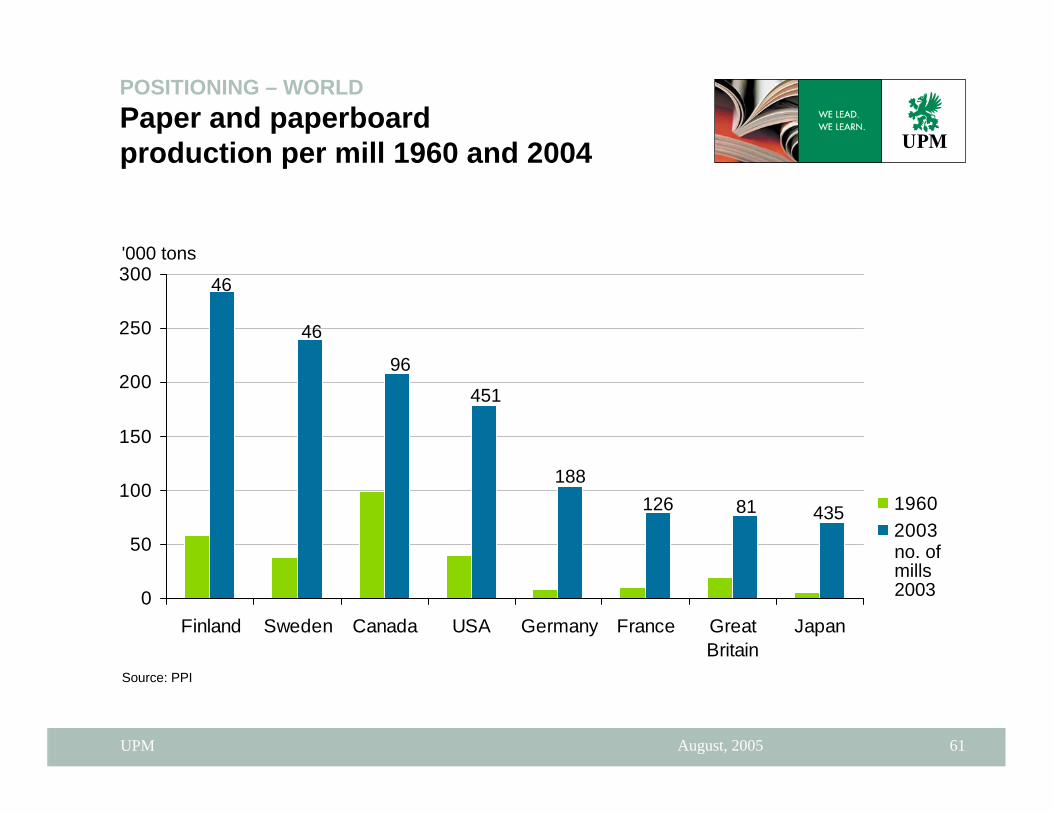

August, 2005UPM 61

0

50

100

150

200

250

300

Finland Sweden Canada USA Germany France GreatBritain

Japan

19602003no. of mills2003

46

'000 tons

96

18881126

Source: PPI

451

435

POSITIONING – WORLDPaper and paperboard production per mill 1960 and 2004

46

March 23, 2006UPM 62

POSITIONING – WORLDAverage capacity of printing paper machines

0 50 100 150 200 250 300

UPM

Nordic countries

Other Western Europe

Canada

USA

Japan

Asia-Pacific region

Average

'000 t/a

Source. Jaakko Pöyry

February 2, 2006UPM 63

POSITIONING – WORLDWorld demand trends of graphic papers 1983-2007

0

10 000

20 000

30 000

40 000

50 000

60 000

'83 '85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '07

WF unctd+1,8 % p.a.

Newsprint+1.0 % p.a.

WF ctd +3,7 % p.a.

Ctd mech.+1.4 % p.a.

Unctd mech.+1.5 % p.a.

Growth rate2004-07

Source:Cepiprint, PPPC, EMGE, JP

'000 tons

February 2, 2006UPM 64

POSITIONING – WORLDWorld capacity trends of graphic papers 1990-2007

0

10 000

20 000

30 000

40 000

50 000

60 000

'90 '92 '94 '96 '98 '00 '02 '04 '06

WF uncoated2,2 % p.a.

Newsprint 1.1 % p.a.

WF coated2.3 % p.a.

Ctd mech. 2.0 % p.a.

Unctd mech.1.6 % p.a.

Growth rate2003-07

Source:Cepiprint, PPPC, EMGE, JP

'000 tons

Positioning - EuropePositioning - Europe

February 2, 2006UPM 66

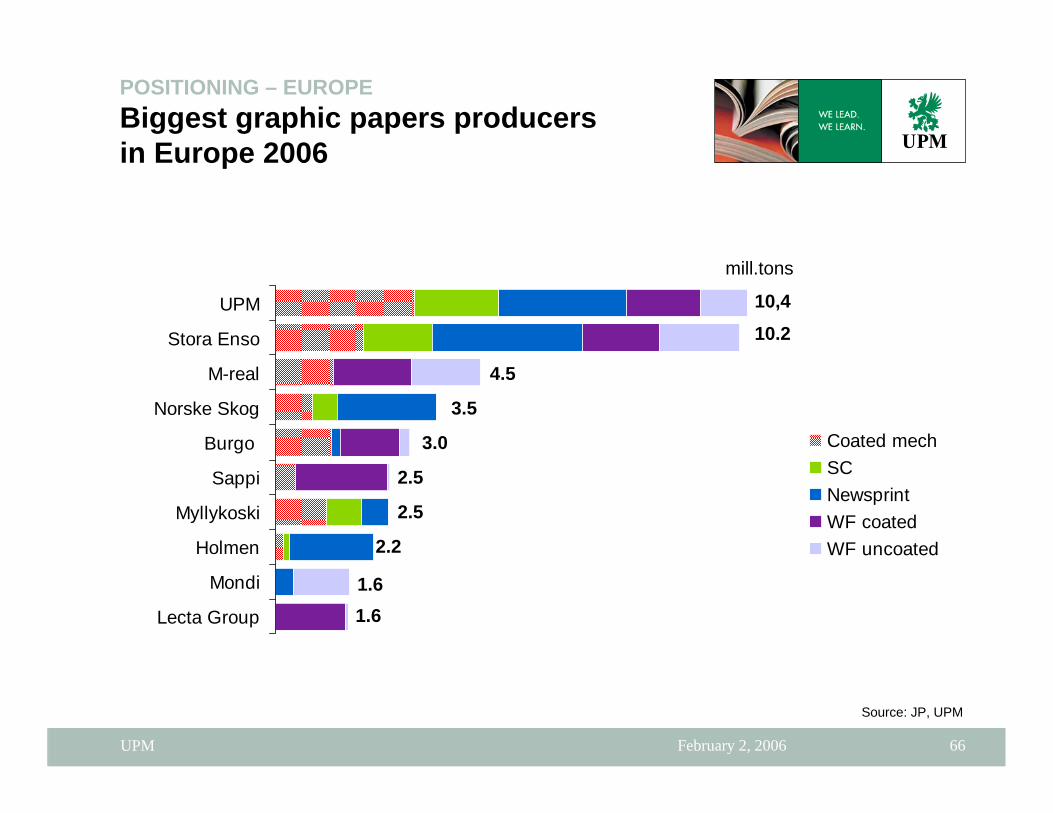

POSITIONING – EUROPEBiggest graphic papers producers in Europe 2006

UPM

Stora Enso

M-real

Norske Skog

Burgo

Sappi

Myllykoski

Holmen

Mondi

Lecta Group

Coated mechSCNewsprintWF coatedWF uncoated

mill.tons

4.5

3.5

3.0

2.5

2.5

2.2

1.6

10,4

10.2

1.6

Source: JP, UPM

February 2, 2006UPM 67

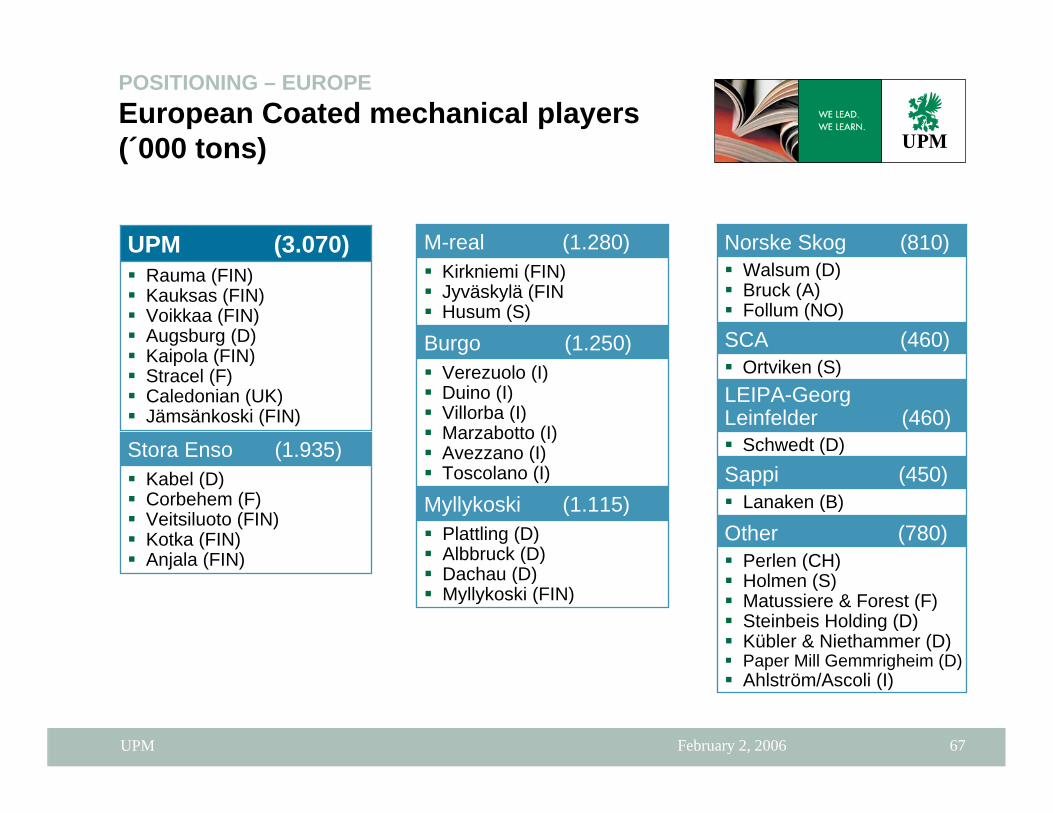

POSITIONING – EUROPEEuropean Coated mechanical players(´000 tons)

Rauma (FIN)Kauksas (FIN)Voikkaa (FIN)Augsburg (D)Kaipola (FIN)Stracel (F)Caledonian (UK)Jämsänkoski (FIN)

UPM (3.070)Kirkniemi (FIN)Jyväskylä (FINHusum (S)

M-real (1.280)

Verezuolo (I)Duino (I)Villorba (I)Marzabotto (I)Avezzano (I)Toscolano (I)

Burgo (1.250)

Plattling (D)Albbruck (D)Dachau (D)Myllykoski (FIN)

Myllykoski (1.115)Other (780)

Perlen (CH)Holmen (S)Matussiere & Forest (F)Steinbeis Holding (D)Kübler & Niethammer (D)Paper Mill Gemmrigheim (D)Ahlström/Ascoli (I)

Ortviken (S)SCA (460)

Schwedt (D)

LEIPA-GeorgLeinfelder (460)

Walsum (D)Bruck (A)Follum (NO)

Norske Skog (810)

Lanaken (B)Sappi (450)Kabel (D)

Corbehem (F)Veitsiluoto (FIN)Kotka (FIN)Anjala (FIN)

Stora Enso (1.935)

February 2, 2006UPM 68

POSITIONING – EUROPEEuropean SC-magazine paper players(´000 tons)

Jämsänkoski (FIN)Rauma (FIN)Schongau (D)Steyrermühl (D)Kajaani (FIN)Augsburg (D)

UPM (1.850)

Lang (D)Myllykoski (FIN)

Myllykoski (790)

Halden (NO)Norske Skog (550)

Kvarnsveden (S)Maxau (D)Reisholz (D)Langerbrugge (B)Wolfscheck (D)

Stora Enso (1.525)

Vetrni u CeskehoKrumlova (CZ)

JIP –Papirny Vetrni (40)

Holmen (140)Hallstavik (S)

Laakirchen (A)SCA (500)

February 2, 2006UPM 69

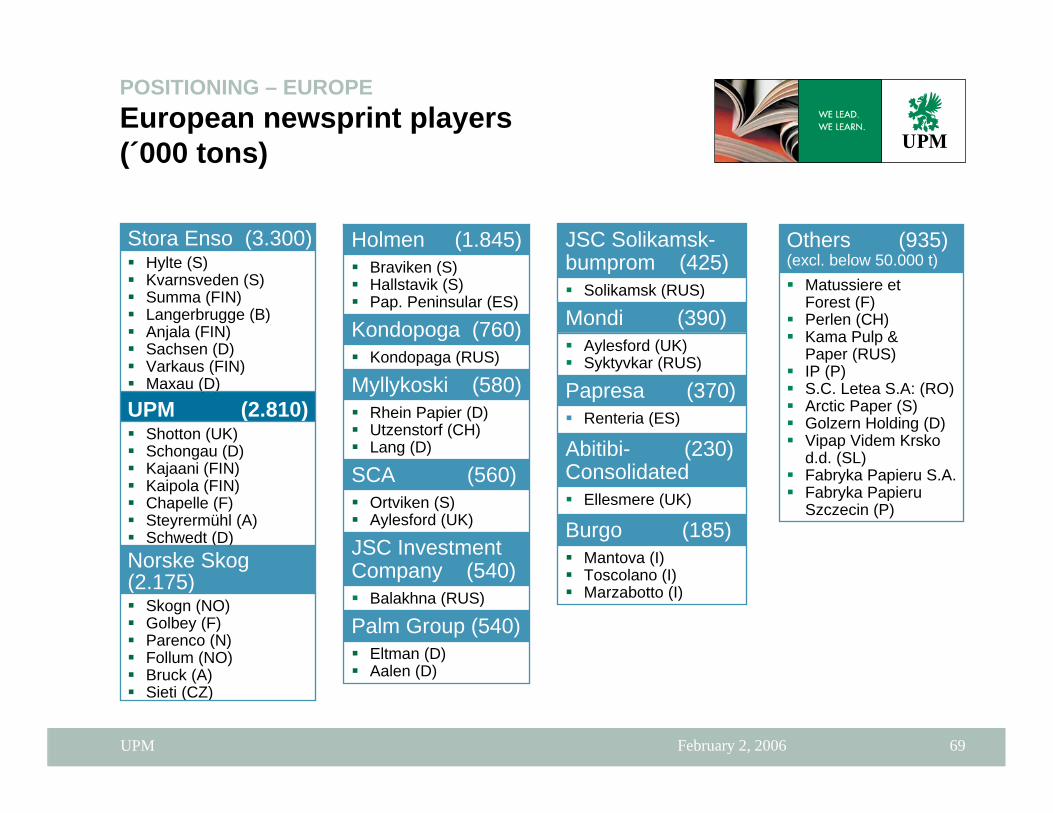

POSITIONING – EUROPEEuropean newsprint players(´000 tons)

Skogn (NO)Golbey (F)Parenco (N)Follum (NO)Bruck (A)Sieti (CZ)

Norske Skog (2.175)

Shotton (UK)Schongau (D)Kajaani (FIN)Kaipola (FIN)Chapelle (F)Steyrermühl (A)Schwedt (D)

UPM (2.810)

Hylte (S)Kvarnsveden (S)Summa (FIN)Langerbrugge (B)Anjala (FIN)Sachsen (D)Varkaus (FIN)Maxau (D)

Stora Enso (3.300)

Eltman (D)Aalen (D)

Palm Group (540)Balakhna (RUS)

JSC InvestmentCompany (540)

Ortviken (S)Aylesford (UK)

SCA (560)

Rhein Papier (D)Utzenstorf (CH)Lang (D)

Myllykoski (580)

Kondopoga (760)Kondopaga (RUS)

Braviken (S)Hallstavik (S)Pap. Peninsular (ES)

Holmen (1.845)

Mantova (I)Toscolano (I)Marzabotto (I)

Burgo (185)

JSC Solikamsk-bumprom (425)

Solikamsk (RUS)

Mondi (390)Aylesford (UK)Syktyvkar (RUS)

Ellesmere (UK)

Abitibi- (230)Consolidated

Renteria (ES)Papresa (370)

Matussiere et Forest (F)Perlen (CH)Kama Pulp & Paper (RUS)IP (P)S.C. Letea S.A: (RO)Arctic Paper (S)Golzern Holding (D)Vipap Videm Krskod.d. (SL)Fabryka Papieru S.A.Fabryka PapieruSzczecin (P)

Others (935)(excl. below 50.000 t)

February 6, 2006UPM 70

* Cap. min. 250.000 t/a

POSITIONING – EUROPEEuropean fine paper players* ('000 tons)

M-real (3.085)Biberist (CH)Stockstadt (D)Husum (S)Hallein (A)Alizay (F)Berg.Gladbach (D)Kemsley (UK)Sittingbourne (UK)Äänekoski (FIN)Wifstavarf (S)Pont St. Max (F)

Oulu (F)Veitsiluoto (F)Nymolla (S)Varkaus (FIN)Grycksbo (S)Wapenweld (NL)Imatra (FIN)Uetersen (D)

StoraEnso (3.300)

Le LardinSaint Lazare (F)Riva del Garda (I)Motril (ES)Zaragoza (ES)St Joan les Fonts (ES)Sarria de Ter (ES)

Lecta (1.530)

Sappi (1.970)Gratkorn (A)Maastricht (NL)Nijmegen (NL)Alfeld (D)Ehingen (D)Blackburn (UK)H.Hempstead (UK)Lanaken (B)

Nordland (D)Kymi (FIN)Docelles (F)

UPM (2.500)

Kwidzyn (POL)Svetogorsk (RUS)Saillat sur Vienne (F)Inverurie (UK)Maresquel (F)

IP Europe (1.170)

Mondi (1.220)Syktyvkar (RUS)Ulmerfeld-H. (A)Ruzomberok (SLO)Szolnok (HUN)Dunaujvaros (HUN)Kematen/Ybbs (A)

Virton (B)Sora (I)Avezzano (I)Chieti (I)Tolmezzo (I)Sarego (I)Toscolano (I)Lugo di Vicenza (I)

Burgo (1.480)

Lenningen (D)

Pap. Scheufelen(290)

Portucel (1.075)Figueira da Foz (P)Setubal (P)

Hernani (I)

Pap. Guipuzcoana(250)

Arjo Wiggins (420)Bessé sur Braye (F)Wizernes (F)Saint-Mars-la-Briére (F)Annat Point (UK)+ 14 mills(cap. below 50.000 t/a)

Kostrzyn (POL)Åsensbruk (S)Munkedal (S)

Arctic Paper (480)

Excl. WF specialities

February 6, 2006UPM 71

POSITIONING – EUROPEEuropean WFC players ('000 tons)

Matussiere & Forest (F)Dalum Papir A/S (DK)Smurfit Kappa Group (UK)Aconda Paper S.A.)

Other (320)(excl. below 50.000 tons)

Åsensbruk (S)Arctic Paper (150)

Scheufelen (270)Lenningen (D)

Bessé sur Braye (F)Wizernes (F)

Arjo Wiggins (375)Le Lardin Saint Lazare (F)Riva del Garda (I)Motril (ES)Zaragoza (ES)St Joan les Fonts (ES)Sarria de Ter (ES)

Lecta (1.510)

Nordland (D)Kymi (FIN)

UPM (1.480)

Virton (B)Sora (I)Avezzano (I)Chieti (I)Sarego (I)Lugo di Vicenza (I)Toscolano (I)

Burgo (1.260)

Gratkorn (A)Maastricht (NL)Nijmegen (NL)Alfeld (D)Ehingen (D)Blackburn (UK)Lanaken (B)

Sappi (1.930)

Biberist (CH)Hallein (A)Bergisch Gladbach (D)Stockstadt (D)Sittingbourne (UK)Äänekoski (FIN)Pont St. Maxence (F)

M-real (1.585)

Oulu (FIN)Grycksbo (S)Uetersen (D)Varkaus (FIN)

Stora Enso (1.550)

Excl. WFC specialities

February 6, 2006UPM 72

UPM (1.410)

POSITIONING – EUROPEEuropean WFU players ('000 tons)

Mondi (1.220)Syktyvkar (RUS)Ulmerfeld-Hausmening (A)Ruzomberok (SLO)Szolnok (HUN)Dunaujvaros (HUN)Kematen an Ybbs (A)

Veitsiluoto (FIN)Nymölla (S)Berghuizer (NL)Varkaus (FIN)Imatra (FIN)

Stora Enso (1.750)

Husum (S)Alizay (F)Kemsley (UK)Stockstadt (D)Wifstavart (S)St. Maxene (F)Biberist (CH)

M-real (1.500)

UPM (1.020)Nordland (D)Kymi (FIN)Docelles (F)

Pap. Guipuzconade Zicuña (250)

Hernani (ES)

Kwidzyn (POL)Svetogorsk (RUS)Saillat (F)Inverurie (UK)Maresquel (F)

IP Europe (1.170)

Figueira da Foz (P)Setubal (P)

Portucel (1.075)

Kostrzyn (POL)Munkedal (S)

Arctic Paper (320)

Tolmezzo (I)Toscolano (I)

Clairefontaine (F)Steinbeis Holding (D)Cart. Fedrigoni (I)Paperalia S.A. (ES)

Other (550)(excl. below 100.000 tons)

Velsen Noord (NL)

Crown Van Gelder N.V. (205)

Burgo (220)Ruzomberok (SL)

Eco-Invest. (250)

Excl. WFU specialities

February 2, 2006UPM 73

Trade flows

February 17, 2006UPM 74

Capacity27,2 mill. tons

Demand23,9 mill. tons

N. America W. Europe

L. America

Oth. Europe

Africa

Oth. AsiaJapan

Oceania

1,6

0,3

0,2

Source: Cepiprint, PPPC, EMGE, RISI

TRADE FLOWSMagazine papers Demand and capacity 2006 preliminary

8,0 8,5

0,2 0,6 0,03 0,1

0,07 0,4

16,1

10,7

2,0 1,9

0,04

0,1

0,9 0,20,4

0,4

0,1

0,7 0,8

0,05

0,1 1,0

February 17, 2006UPM 75

Capacity19,5 mill. tons

Demand17,0 mill. tons

N. America W. Europe

L. America

Oth. Europe

Africa

Oth. Asia Japan

Oceania

1,0

0,2

0,02

0,3

Source: Cepiprint, PPPC, JP

TRADE FLOWSCoated mechanical paper Capacity and demand 2006 estimate

5,7 5,9

0,2 0,5- 0,1

0,1 0,3

10,9

7,3

- 0,7

1,9 1,8

0,04

0,1

0,7 0,20,3

0,2

0,1

0,8 0,70,1

February 17, 2006UPM 76

Capacity7,7 mill. tons

Demand6,9 mill. tons

N. America W. Europe

L. America

Oth. Europe

Africa

Oth. Asia Japan

Oceania

0,7

0,05 0,3

Source: Cepiprint, PPPC, JP

TRADE FLOWSSC magazine paperCapacity and demand 2006 estimate

2,32,7

- 0,1 0,06

- 0,1

5,2

3,5

0,1

0,08 0,1

0,03

0,3 0,02

0,1

0,1

0,4

- 0,1

0,06

February 17, 2006UPM 77

Capacity40,2 mill. tons

Demand37,7 mill. tons

N. America W. Europe

L. America

Oth. Europe

Africa

Oth. Asia

Oceania

0,2

0,3

Source: Cepiprint, PPPC, JP

TRADE FLOWSStd newsprint Capacity and demand 2006 estimate

13,2

10,2

1,01,8

0,8 0,9

10,39,2

2,9

3,8 3,90,6

0,8

1,3 6,24,41,3

0,5 0,6

1,8

China

3,3 3,2

1,4

0,9

Japan

0,2

0,1

February 17, 2006UPM 78

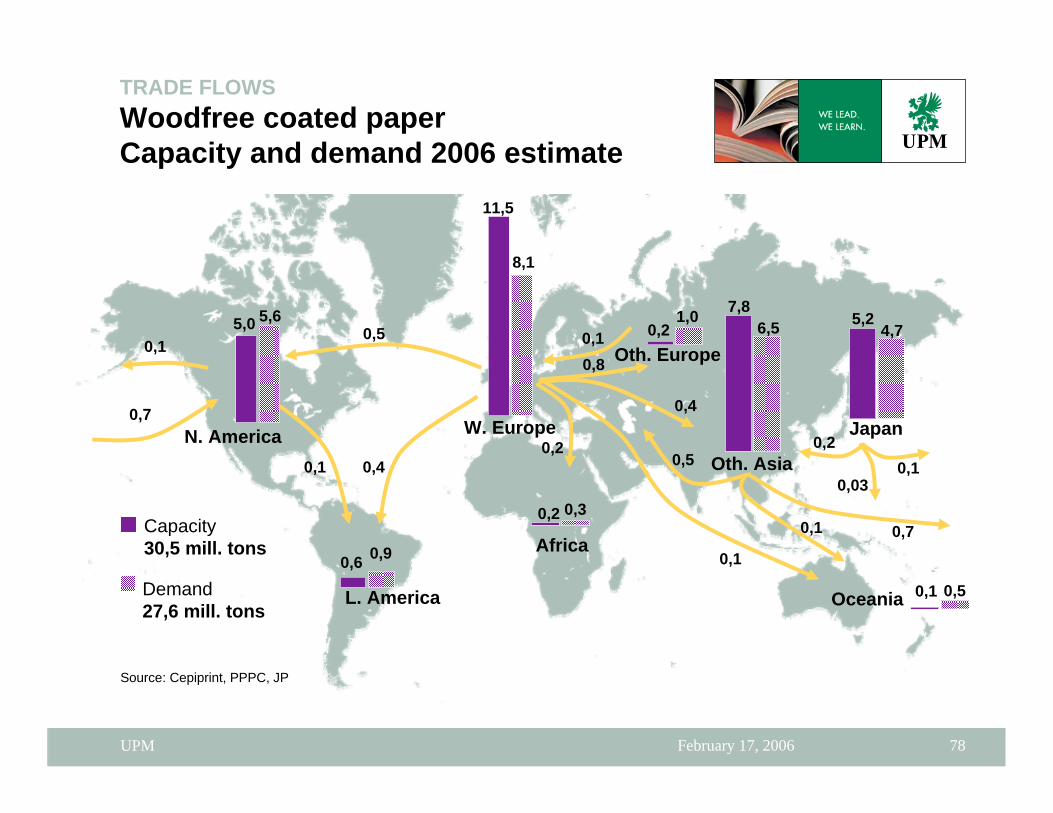

Capacity30,5 mill. tons

Demand27,6 mill. tons

N. America W. Europe

L. America

Oth. Europe

Africa

Oth. Asia

Japan

Oceania

Source: Cepiprint, PPPC, JP

TRADE FLOWSWoodfree coated paperCapacity and demand 2006 estimate

5,0 5,6

0,9

0,2

0,1

11,5

8,1

5,24,7

0,1

0,8

0,20,5

0,10,6

0,3

1,0

0,5

0,4

0,1

0,4

0,20,1

0,03

7,86,5

0,2

0,7

0,1

0,1 0,7

0,5

February 17, 2006UPM 79

Capacity57,1 mill. tons

Demand50,5 mill. tons

N. America W. Europe

L. America

Oth. Europe

Oth. Asia

Oceania

Source: Cepiprint, PPPC, JP

TRADE FLOWSWoodfree uncoated paperCapacity and demand 2006 estimate

13,512,6

3,2

1,0

0,4

10,89,6

3,6 3,6

0,2

0,5

3,0

0,2

0,033,3

1,2 China

13,011,21,8 8,9

6,7

0,6

0,1 0,2

0,1

0,8

0,30,2

0,2

0,6

*) 7 500 Cepifine demand (Cepifine bulk grades, i.e. excl. spec. grades) 8 400 (Cepifine capacity)

0,1

0,1

Africa

Japan

February 2, 2006UPM 80

Demand

February 2, 2006UPM 81

DEMANDWestern EuropeCoated mechanical - Demand forecast

0

2

4

6

8

'98 '99 '00 '01 '02 '03 '04 '05 '06e

mill. tons Demand change from previous year

Demand growth rate 2003-2006: 3%

1% 4%13%

-6% 1%5% -1%4%

4%

Lockout in Finnish mills 2005 Source: Cepiprint, UPM

February 2, 2006UPM 82

DEMANDWestern EuropeSC magazine - Demand forecast

0

1

2

3

4

'98 '99 '00 '01 '02 '03 '04 '05e '06e

5%

9% 6%9% 0% 1% 3% -2%

-1%

mill. tons Demand change from previous year

Demand growth rate 2003-2006: 2%Lockout in Finnish mills 2005 Source: Cepiprint, UPM

February 2, 2006UPM 83

DEMANDWestern EuropeNewsprint - Demand forecast

0

3

6

9

12

'98 '99 '00 '01 '02 '03 '04 '05e '06e

5%3%

-5% 0%1%-3%5% 5% 1%

mill. tons Demand change from previous year

Demand growth rate 2003-2006: 2%Lockout in Finnish mills 2005 Source: Cepiprint, UPM

February 2, 2006UPM 84

DEMANDWestern EuropeWoodfree coated - Demand forecast

0

2

4

6

8

'98 '99 '00 '01 '02 '03 '04e '05e '06e

8%10% 3%

-7% 1% 1% 8% 2% 4%

mill. tons Demand change from previous year

Demand growth rate 2003-2006: 5%Lockout in Finnish mills 2005 Source: Cepiprint, UPM

February 2, 2006UPM 85

DEMANDWestern EuropeWoodfree uncoated - Demand forecast

0

2

4

6

8

'98 '99 '00 '01 '02 '03 '04e '05e '06e

3%3% 5% 2% -4% -1% -1%

6% 1%

mill. tons Demand change from previous year

Demand growth rate 2003-2006: 3%Lockout in Finnish mills 2005 Source: Cepiprint, UPM

February 2, 2006UPM 86

General informaation

February 13, 2006UPM 87

0

10

20

30

40

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

- Paper consumption, million t/a -

Newsprint

Printing and writing papers

Expansion of Internet/WWW

PCs

RadioCinemaTV

Laser PrintersCD-ROMs

MainframeComputers

ColourTV

Cable TVVCR

Satellite TVMini Computers

Newsprint and printing & writing paper consumption and the Proliferation of Electronic Media in Western Europe

Source: Jaakko Pöyry Consulting

High speed Internet access

February 2, 2006UPM 88

Printing papers' life cycle

Paperproduction

Waste paper/ waste

Productionof recycled

fibres

Fresh fibreproduction

Forest

Biodiversity

Reader

Distribution

Printing

Incineration/landfill

February 2, 2006UPM 89

Structural changes of the forest industry in Finland

EnsoGutzeit

Veitsiluoto

Stora Enso

Varkaus(Ahlström)

Myllykoski

Rauma-Repola1991

Rosenlew1987

Kajaani1989

Kymmene

Kaukas1986

UnitedPaper Mills

1991

UPM-Kymmene1996

Repola

Serlachius

MetsäliitonTeollisuus

Schauman1988

Ahlström ==> Jujo Thermal

Metsäliitto

Metsä-Botnia

Kemi

Joutseno-Pulp

Metsä-Sellu

Finnforest

TampellaForest and

Tambox

Oulu

EnsoStora

Corenso

Sunila

Georgia-Pacific Finland (Nokia),

Stromsdal

Georgia Pacific

M-realMetsä-liitto

Kyro

Metsä-Rauma

February 2, 2006UPM 90

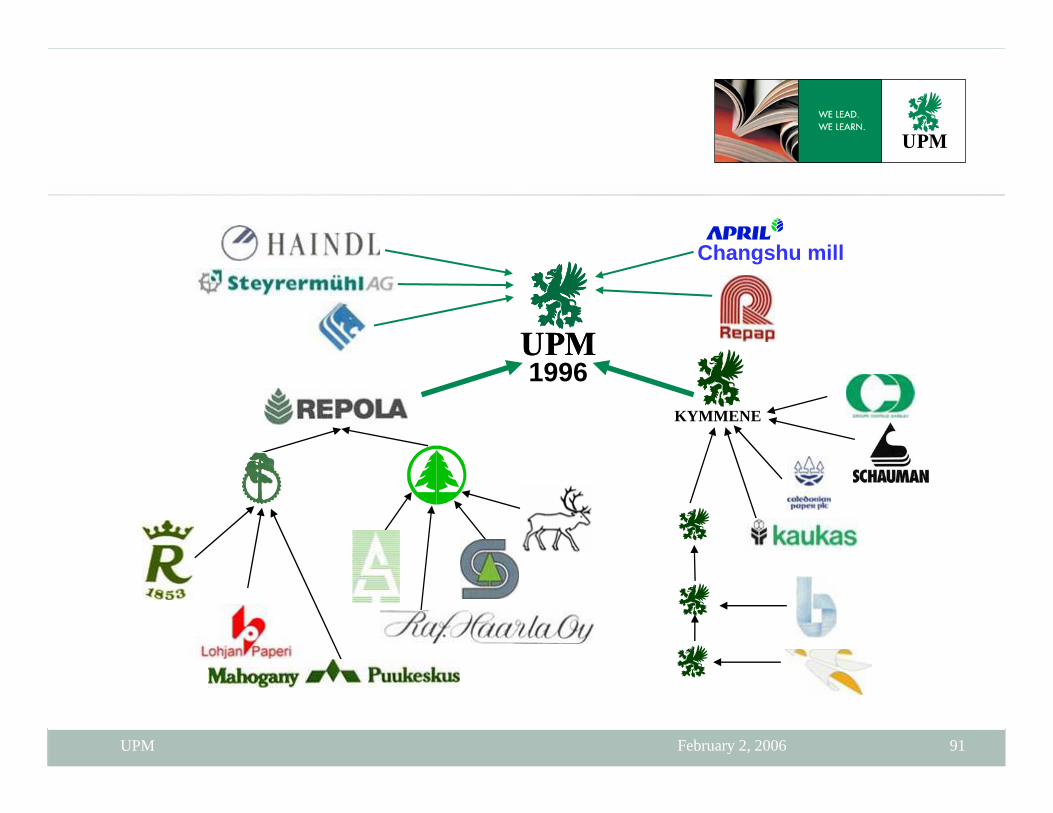

1996 KYMMENE

Changshu

February 2, 2006UPM 91

1996KYMMENE

Changshu mill

February 2, 2006UPM 92

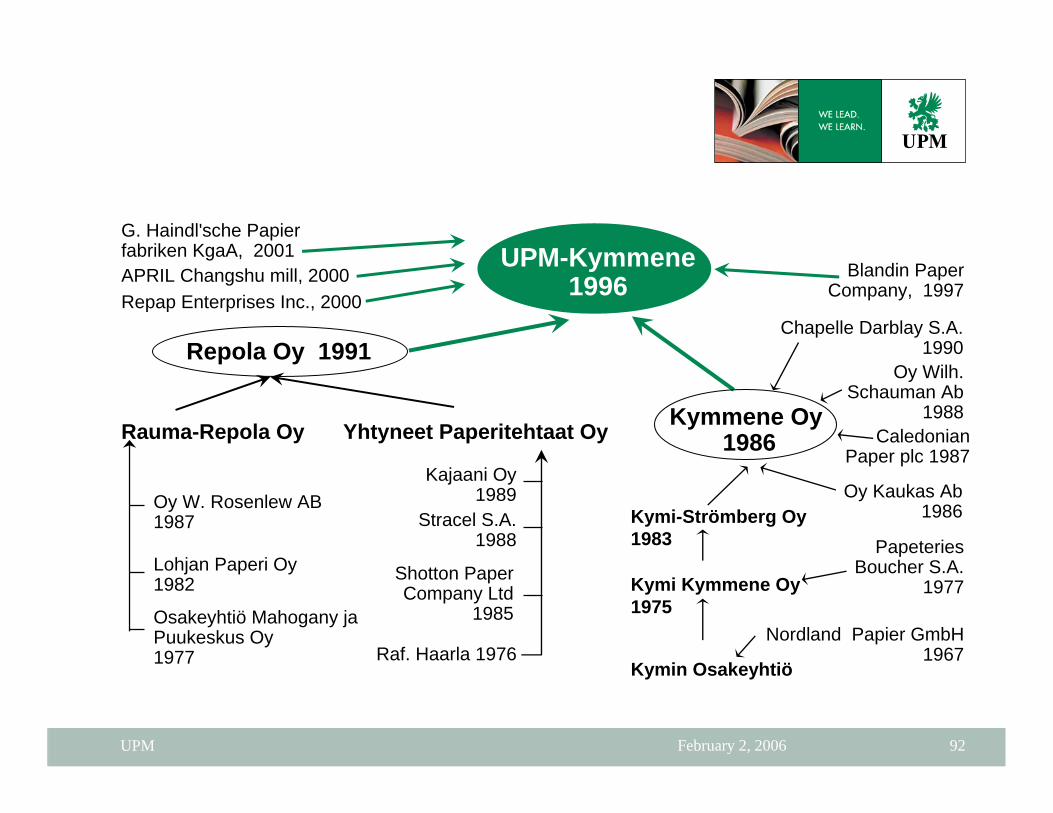

APRIL Changshu mill, 2000

G. Haindl'sche Papierfabriken KgaA, 2001

Repola Oy 1991

Yhtyneet Paperitehtaat OyRauma-Repola Oy

Chapelle Darblay S.A.1990

Lohjan Paperi Oy1982

Osakeyhtiö Mahogany ja Puukeskus Oy 1977

Oy W. Rosenlew AB1987 Stracel S.A.

1988

Shotton PaperCompany Ltd

1985

Raf. Haarla 1976

Repap Enterprises Inc., 2000

Blandin PaperCompany, 1997

UPM-Kymmene1996

Kymmene Oy 1986

Oy Wilh.Schauman Ab

1988Caledonian

Paper plc 1987

Kymi-Strömberg Oy 1983 Papeteries

Boucher S.A.1977

Nordland Papier GmbH1967

Kymi Kymmene Oy1975

Kajaani Oy1989 Oy Kaukas Ab

1986

Kymin Osakeyhtiö

February 2, 2006UPM 93

From forest to office paper –one hour / paper machine

105 m3 95 m3

Birch pulp 24 000 kg Pine pulp 16 000 kg

8,5 m

50 000 per hour 20 000 reams A4

Speed 75 km/h

Fillers 10 000 kg

February 2, 2006UPM 94

From forest to coated paper –one hour / paper machine

65 m3 95 m3

Birch pulp 16 000 kg Pine pulp 16 000 kg

Fillers & coating colours25 000 kg

8.5 m

Speed PM 8: 80 km/h &C3: 110 km/h (record 130 km/h)

60 000 kg per hour

100 reelsin size 90 x 120 cm

February 2, 2006UPM 95