zeq 26.pmd - to zenith bank

TRANSCRIPT

EDITORIAL TEAM

MARCEL OKEKEEditor

EUNICE SAMPSONDeputy Editor

ELAINE DELANEYAssociate Editor

CHARLES UJOMUIBRAHIM ABUBAKAR

SUNDAY ENEBELI-UZORAnalysts

JOHN LUCKY ETOHProduction Supervisor

SYLVESTER UKUTROTIMI AROWOBUSOYE

Layout/Design

EDITORIAL BOARD OF ADVISERS

UDOM EMMANUELGIDEON JARIKREPAT NWARACHE

OCHUKO OKITI

ZENITH ECONOMIC QUARTERLYis published four times a year

by Zenith Bank Plc.

Printed by PLANET PRESS LTD.Tel 234-1-7731899, 4701279, 08024624306,

E-mail:[email protected]

The views and opinionsexpressed in this journal

do not necessarily reflectthose of the Bank.

All correspondence to:The Editor,

Zenith Economic Quarterly,Research & EIG,Zenith Bank Plc

7th Floor, Zenith HeightsPlot 87, Ajose Adeogun Street,

Victoria Island, Lagos.Tel. Nos.: 2781046-49, 2781064-65

Fax: 2703192.E-mail:[email protected],

[email protected]: 0189-9732

FROM THE MAIL BOXThis contains some of the acknowledgment/commendation letters from our teemingreaders across the globe.

PERISCOPEThis is a panoramic analysis of majordevelopments in the economy during theperiod under review and the factorsunderpinning them.

POLICYContained here is the conclusion of themonetary, credit, foreign trade and exchangepolicy guidelines for the fiscal years 2010/2011.

GOLBAL WATCHThis is an indepth analysis of developmentsin the global economy during first quarter2011 and their implications for commodityprices and economic growth prospect.

ISSUES (I)This piece examines the post electioneconomy in Nigeria and highlights the newopportunities it presents to take Nigeria tonew heights of development.

ISSUES (II)The series on quality and internal control inbanks highlights some of the criticalcorporate governance issues in someNigerian banks and the clog they pose tothe wheel of industry progress.

ISSUES (III)The Nigerian aviation industry is closelyexamined in this piece, with emphasis onchallenges, prospects and the issues thatmust be addressed if set goals are to beachieved.

FOREIGN INSIGHTSThis is a review of the global marketdynamics in first quarter 2011, impact onmarket performance and the factors andsentiments driving investment decisions.

DISCOURSEThis piece examines the Nigerian electricpower sector and posits options that areavailable to policy makers and otherstakeholders in efforts to achieve stablepower supply by 2015.

FACTS & FIGURESThis contains economic, financial andbusiness indicators with annotations.

2 Zenith Economic Quarterly April 2011

The complementarity of politics and economics(or their mutual exclusivity) has for long been ahoney-pot for scholastic debates, research andstudies. While some scholars postulate and indeed propagate the ascendancy of politics, oth-ers insist on the superiority and independenceof economics. For Frank Chodorov, a formerdirector of Henry George School of Social Sci-ence, New York, in his book ‘The Rise and Fallof Society’: “The intrusion of politics into thefield of economics is simply an evidence ofhuman ignorance or arrogance, and is as fatu-ous as an attempt to control the rise and fall oftides.”

This early Nineteenth Century position ofChodorov is however hardly valid any more,for the reality of various societies, especially de-veloping countries, largely underpin the deter-minant role of politics. However, it has alsobecome almost incontrovertible that the stateof the economy has universally become the keyyardstick for assessing the success or failure ofthe politicians (those who play politics) in alljurisdictions. Therefore, the ability to script aneconomic roadmap and effectively implementsame—and through that advance the state ofwellbeing (real development) of the citizenryremains a ubiquitous challenge of the politi-cians.

In our lead article, ‘Nigeria’s Post-electionEconomy: Yet Another Chance for Develop-ment’, the author, using an in-depth analysisof the economic history of Nigeria, erects a de-velopment compass for the Government thatemerged from the April 2011general electionsin the country. To him, “those who ran the af-fairs of government during the oil boom ofthe 1970s in Nigeria were not the same peoplein charge of the Gulf War windfall of the 1990sand the oil market bull of the 2000s. A differentset of people is now in charge of the affairs ofgovernment in the midst of yet a running oilwealth.” He therefore challenges this “new setof people” to, even if for the very first time,utilize the enormous resources at their disposal

to drive real economic development for Nige-ria.

At the heart of this new development drivebeing clamoured for is the erection of thecountry’s infrastructure—the substructure ofmeaningful development every where. Andwithout doubt, for Nigeria, the most criticalamong all infrastructure categories is electricpower, given the country’s antecedents. Our ar-ticle, ‘Reliable Power Supply: Way Forward forNigeria (2011—2015)’ therefore delves into thepoor state of power supply in the country overthe years. Tracing the very tortuous roads thathad been taken in the efforts to improve powersupply in the country, the author ends on a noteof hope. His masterful analysis of the past andcurrent power sector reforms gives a clear basisfor his very informed recommendations. Forinstance, for him, in pursuit of the power sec-tor reform goals, Nigeria needs to strengtheninternational cooperation and exchange, espe-cially with respect to tapping into opportunitiesin the West African Power Pool.

Beyond all this, we also have a focus on theglobal economy during the first quarter of thisyear, with an analysis of the numerous disas-ters and turmoil in parts of the world. Theimpact of all these on commodity prices andimplications for economic growth prospects arealso surveyed in-depth. With this is also a re-view of the global market dynamics during thequarter as well as the factors and sentimentsdriving investment decisions.

Our other regular sections are not left out;in deed, they contain the usual highly informa-tive, enlightening and educative stuff that is ourtrademark.

Just read, and enrich yourself !

This earlyNineteenthCentury posi-tion ofChodorov ishowever hardlyvalid any more,for the reality ofvarious societ-ies, especiallydevelopingcountries,largely under-pin the determi-nant role ofpolitics.

4 Zenith Economic Quarterly April 2011

We are pleased to note that thisedition is of world standard charac-terized by its intellectual richnessand focus on such burning issuesas fiscal governance, youth and de-mocracy and road infrastructure. Itsreport on Nigerian and globaleconomy is exemplary.

Kindly accept our profound ap-preciation for this wonderful andnoble initiative of yours in theworld of business and journalism.Thank you.Yours faithfully,Abiodun OlamosuDeputy Secretary GeneralAssociation of Senior Staff ofBanks, Insurance and FinancialInstitutions Lagos

I am directed to acknowledge withthanks and appreciation the receiptof your letter dated 4th March, 2011,forwarding the January, 2011 editionof your magazine, which focuseson fiscal governance and treatise onoptions for the transformation ofthe Nigerian road infrastructure aswell as the youth and democracy.

The Mission finds the publicationessential and useful reference ma-terial to our diplomatic assignmentfor Nigeria.

Please accept the assurances of HisExcellency’s highest consideration.Basher I. Ma’ajifor: AmbassadorEmbassy of the Federal Republicof Nigeria, Saudi Arabia

I am directed to acknowledge withthanks the receipt of your January,2011 edition of the Zenith Eco-nomic Quarterly (ZEQ) by the Vice-Chancellor of this University. It ishoped that the journal will as usualbe useful to both staff and studentsof this University for informationand research purposes.

Once again thank you for makingthe University of Uyo one of therecipients of this unique Journal ofyour establishment.Yours faithfully,Winifred I. Ekpo (Mrs.)for: Vice-ChancellorOffice of the Vice-ChancellorUniversity of Uyo, Nigeria

I wish to acknowledge with thanksthe receipt of the above mentionedpublication (January 2011) for use

of our Departmental Library.It is hoped that in the future you

would continue to send similarpublications as you promised toenrich our library.

Thank you for your good ges-tures.Yours faithfully,Dr. Bello Sabo,Head, Department of BusinessAdministrationAhmadu Bello University, Zaria

I am directed to acknowledge thereceipt of the January 2011 editionof the Zenith Economic Quarterly(ZEQ). The information containedin the journal about Nigeria and theglobal economy is quite useful andeducative, particularly in the areasof strategic planning and policy.

Please accept the warm regards ofthe Honourable Minister.O. K. Abegunde (Mrs.)for: Honourable MinisterFederal Ministry of Informationand CommunicationsOffice of the Permanent Secretary

I am directed to acknowledge thereceipt of your January, 2011 edi-tion of Zenith Economic Quarterlypublication with a focus on fiscalgovernance in Nigeria.

Going by the focus of the publi-cation, I have no doubt that it wouldbe a useful reference material to usas an organization especially at thisstage of our practical Democraticgovernance.

While we appreciate your kindgesture, please accept the assurancesof our highest esteem.Felix Dabofor: Director Finance and AdminFederal Capital Development Au-thority Abuja

I am directed to acknowledge withthanks the receipt of a copy of theJanuary, 2011, edition of the abovemagazine.

No doubt, the journal will behandy as a reference point, givingthat it contains critical informationon Nigeria and global economy forstrategic policy decisions.Best regards.A. N. MadubikeHead of Chanceryfor: Ag. High CommissionerHigh Commission of the FederalRepublic of Nigeria, Pretoria

I am directed to acknowledge re-ceipt with thanks, of the ZenithEconomic Quarterly, January, 2011Edition which you sent to us undercover of your letter dated March04, 2011 and to inform that theEmbassy has found the publicationto be highly informative and educa-tive as usual.M. Yusuffor: Charge D’ Affaires, a.i.Embassy of the Federal Republicof Nigeria, Brazil

Your letter dated 4th March, 2011refers. I am directed to acknowledgethe receipt of a complimentarycopy of the Zenith Economic Quar-terly Publication of January, 2011edition.

I must thank you for your ges-ture, even as we are studying thepublication for possible future con-tribution. We continue to commendyou for your consistency and stead-fastness in maintaining the qualityof the magazine.

Please accept my esteemed regardand best wishes.Mrs. Angela K. O. Obo, MCSRfor: Auditor-GeneralGovernment of Cross Rive State

I am directed to acknowledge withthanks the receipt of the abovenamed Magazine forwarded throughyour letter of 4th March, 2011. Asalways, the magazine is enrichingand informative.

Please accept, the assurances ofthe Charge d’ Affaires’ warmest re-gards.(M. S. Ogundero (Mrs.)for: Charge d’ Affaires a.i.Embassy of the Federal Republicof Nigeria, Hungary

April 2011 Zenith Economic Quarterly 5

Periscope

espite the build-up to the April 2011general elections in Nige-ria which was expected to pose some threat to the health ofthe economy, the first quarter recorded continuing good out-put performance (from 2010), modest rise in external reserves,improvement in stock market indicators and moderation ininflation rate. Also, crude oil prices remained high, generallystable naira exchange rate prevailed, while the various planksof reforms in key sectors of the economy continued. Specifi-cally, provisional data from the National Bureau of Statistics(NBS) show that output growth measured in real Gross Do-mestic Product (GDP) terms was projected to grow by 7.43per cent in the first quarter 2011, compared with the 7.36 percent recorded in the corresponding period in 2010. Signifi-cantly, this GDP growth trend is being sustained by the non-oilsector—with major contributions from services, wholesale andretail trade as well as agriculture. The trend is consistently abovethe 7.0 per cent target GDP growth rate of the Federal Gov-ernment for 2011.

The ding-dong affair between the Federal Legislature andthe Executive over the 2011 Appropriation Act continued allthrough the period under review. Thus, although the NationalAssembly passed the Bill and raised the size of the Budget toN4.92 Trillion from a level of N4.42 Trillion proposed, nego-tiations between the two arms of Government for an amend-ment of the Act continued far beyond the first quarter 2011.Similarly, maneuverings and longstanding debates on the Pe-

* By Marcel Okeke

6 Zenith Economic Quarterly April 2011

PERISCOPE Economy:Output Growth Remains Resilient

troleum Industry Bill (PIB),the Sovereign Wealth Fund(SWF), Freedom of Infor-mation (FoI), National Mini-mum Wage and other piecesof legislation raged allthrough the quarter. Theview of the InternationalMonetary Fund (IMF)through its revised ArticleIV consultation with Nigeriaalso impacted the economyduring the review period.While the Bretton Woods in-stitution endorsed thecountry’s growth forecast atseven per cent, it observedthat Nigeria was yet to takeadvantage of the subsistinghigh oil prices to return tofiscal surplus and build itsexternal reserves. In deed,the IMF report highlightedNigeria’s fiscal regime asbeing ‘pro-cyclical’ and lack-ing the discipline to adhereto an oil price-based rule.The Fund also called for amore flexible exchange rateregime in Nigeria—that is,one that will give more roomfor market forces to deter-mine the exchange rates.Overall, the IMF said “eco-nomic outlook remains posi-tive and risks are generallybalanced” for Nigeria.

Apparently in line withthis projection, inflation ratemoderated within the 11 to12 per cent band during thefirst four months this year.From 11.80 per cent as atend-December 2010, it roseto 12.10 per cent in January2011; dropped to 11.10 inFebruary and rose somewhatsharply to 12.80 in March.It however declined to be-low December 2010-level,standing at 11.60 per cent inApril 2011, according to theNBS figures. These levels arehowever viewed as yet high,given the single digit inflationrate target of the monetaryauthorities. The subsisting

trend is attributable to pub-lic sector high spending, in-creases in wages during theperiod, liquidity injectioninto the economy due to theoperations of the AssetManagement Corporationof Nigeria (AMCON) andthe anticipated removalof subsidy on petroleumproducts in the near fu-ture.

All these, in turn, standas reasons for the contin-ued tight monetary policystance of the CentralBank of Nigeria. In deed,the Monetary PolicyCommittee (MPC) of theapex bank at its March22, 2011 meeting “ex-pressed serious concernover the heightened riskof inflation followingfrom the proposed highexpenditure outlay of theFederal Government ascontained in the 2011Appropriation Bill recentlypassed by the NationalAssembly, especially in thewake of rising globalfood and energy prices.”The MPC further notedthat “the current fiscalstance is inconsistent withthe objective of maintain-ing stability in exchangerates, prices and interestrates,” insisting that “un-less this fiscal stand is re-versed the economywould have to bear a highcost in terms of pressureon foreign reserves, highinterest rates and/or higherlevel of inflation.”

Following from this con-cern, the CBN raised itsMonetary Policy Rate(MPR), the benchmark in-terest rate by 100 basispoints, from 6.50 per centin January to 7.50 per centin March—retaining thesymmetric corridor of +/-200 basis points. The apex

bank retained the Cash Re-serve Ratio (CRR) of 2.0per cent and liquidity ratioof 30.0 per cent. It also ex-tended its guarantee on in-terbank transactions andguarantee of foreign creditlines by three months from

June 30, 2011 to September30, 2011.

Also, in line with the fearsof the apex bank, the Nairaexchange rate recorded aconsistent but gradual de-cline all through the firstquarter. This trend was ac-centuated by the supply sideof money supply due to im-port bill pressure. As a re-sult of all these, the monthly

average exchange rate whichstood at N148.57/US$1 inDecember, 2010, droppedto N149.52/US$1 in Janu-ary, 2011. It declined toN149.92/US$1 in February2011 and depreciated fur-ther to N150.49/US$1 in

March 2011. On the otherhand however, the externalreserves recorded marginalaccretion during the quarterunder review: from US$32.4billion as at end-December2010, the reserves shot upto US$33.9 billion in Janu-ary 2011; came to US$33.3billion in February anddropped slightly further toclose the first quarter 2011

http

://uplo

ad.w

ikim

edia

.org

/wik

ipedia

/com

mons/

5/5

3/1

900_P

ennsy

lvania

_A

venue.J

PG

April 2011 Zenith Economic Quarterly 7

PERISCOPE Economy:Output Growth Remains Resilient

at US$33.2 billion. Ironically,this trend in reserves is inspite of consistently high oilprices and improved crudeoil production during theperiod. Thus, the almoststatic level of the stock ofexternal reserves can be at-

tributable to the foreign ex-change management policyof the CBN, which tends todefend the value of theNaira. This policy stance isreflected in the increasedsupply/sale of forex at theWholesale Dutch Auctions

(WDAS) all through theperiod as the apex bankmade efforts to meetforex demand.

While the nation’sstock of external reserveswas depleting, the quan-tum of its domestic andexternal debt was ironicallyincreasing. Thus, duringthe first quarter 2011,Nigeria’s external debt rosefrom US$4.58 billion as atend-December 2010 toUS$5.23 billion in March,according to the DebtManagement Office(DMO) figures. In thesame vein, total domesticdebt increased, by about8.30 per cent, from its po-sition of N4.55 trillion asat year-end 2010 toN4.86 trillion at the endof March 2011. Accord-ing to the DMO, the jumpin domestic debt was as aresult of some increase inthe issuance of publicdebt instruments, includ-ing domestic bonds, trea-sury bills and treasury

bonds—with maturity datesranging from three to 20years. The DMO figuresshow that the FGN bondsaccounted for N3.06 trillionor 62.78 per cent of the to-tal domestic debt stock; Ni-gerian Treasury Bills ac-counted for N1.44 trillion or29.57 per cent, while Trea-sury Bonds made up the re-maining N372.90 billion or7.7 per cent.

On the other hand, theDMO attributed the increasein external debt within thefirst quarter 2011 mostly toactivities surrounding thecountry’s issuance of theUS$500 million Eurobond inthe first month of the year.A breakdown of the total ex-ternal debt of US$4.58 bil-lion as at year-end 2010shows that the 36 states andAbuja (FCT) owed US$2.0billion while the balance ofUS$2.5 billion was owed bythe Federal Government—mostly to multilateral credi-tors. The DMO records alsoshow that Lagos State withan external debt of aboutUS$400 million; Kadunawith a debt of US$157 mil-lion and Cross River withUS$111 million top the listof the indebted states inNigeria as at December 31,2010.

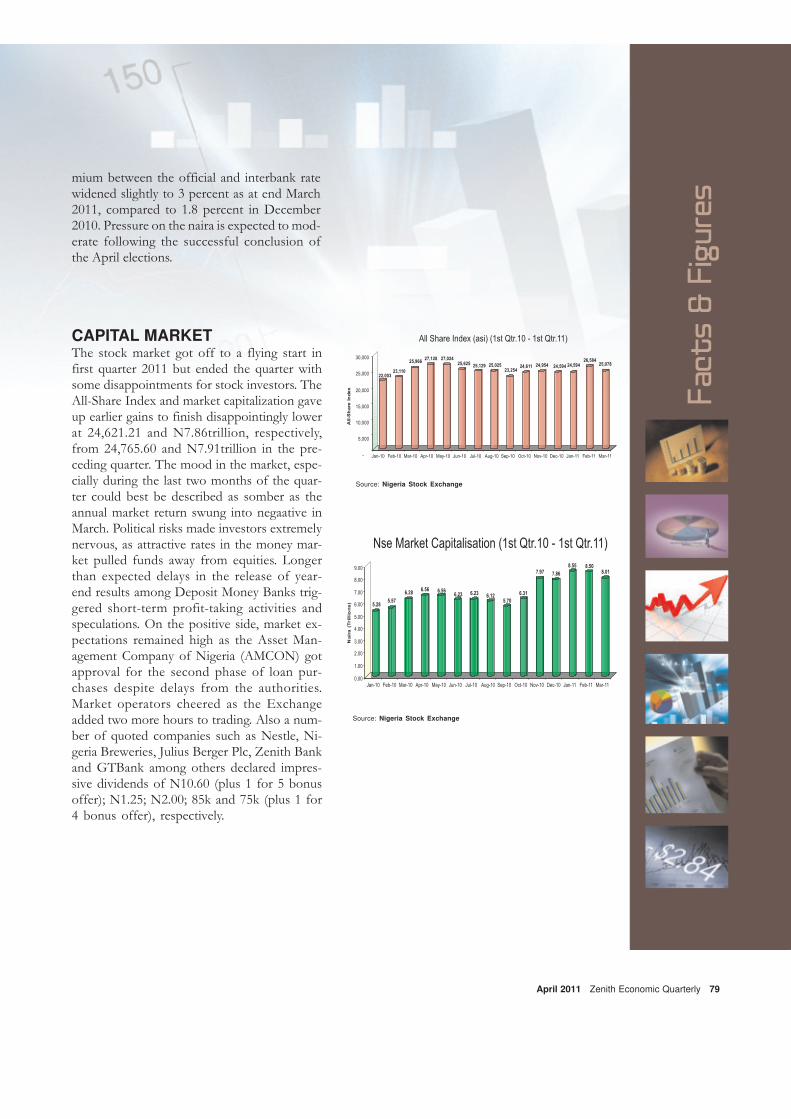

THE CAPITALMARKETDuring the first quarter2011, share prices and mar-ket capitalization recordedsignificant decline due toboth domestic and interna-tional developments. Al-though the quarter startedwith an impressive outlookin January which was char-acterized by positive volumeturnover and record newhighs by most blue-chipstocks, virtually all the indi-ces cascaded in the rest of

In deed, the IMF report highlighted

Nigeria’s fiscal regime as being ‘pro-

cyclical’ and lacking the discipline to

adhere to an oil price-based rule. The

Fund also called for a more flexible ex-

change rate regime in Nigeria—that is,

one that will give more room for market

forces to determine the exchange rates.

8 Zenith Economic Quarterly April 2011

PERISCOPE Economy:Output Growth Remains Resilient

the period. Specifically,profit-taking, growing activ-ity towards treasury bills andbonds and attractive interestrate in the money marketfollowing the tight monetarymeasures by the CBN en-couraged continued sell-offin the market. The recapi-talization of market opera-tors as ordered by the Secu-rities and Exchange Com-mission (SEC) also partlysustained the bearish trendin the market. Many bro-kers/operators sold off toraise capital for their N70million minimum share capi-tal, which led to the suspen-sion of about 58 stockbroking companies by theregulator.

The speculative andbearish sentiment that pre-vailed in most of the quar-ter was also attributable tothe delay in bank earningsreport and the subsistingmonetary policy regime. Thebanking sector had been ex-pected to start year-2010reporting season early inMarch 2011—but this didnot happen. Concerns overthe impact of a one per centNigerian Accounting Stan-dards Board (NASB)-or-dered general provision onbanks’ risk assets and itslikely effect on net earningscaused the delay (in part) andgenerated some debate as to

the applicability of the ruleon 2010 financials. It took alot of time for the issue tobe resolved.

Flight-to-safety senti-ment by foreign investorsduring the period due topolitical uncertainties in thebuild-up to the general elec-tions in the country as wellas seemingly unsettled eco-nomic atmosphere also sus-tained sell activities in themarket. The upshot of allthese was that the marketcapitalization of the Nige-rian Stock Exchange (NSE)which rose from N7.91 tril-lion at year-end 2010 toN8.58 trillion at end-January2011, dropped to N8.32 tril-lion at end-February andended the quarter at yet alower level of N7.87 trillion.Thus, from its level above26,000 points in January, theAll-share Index (ASI) re-corded a loss of about 2.65per cent to stand at25,871.22 points at the closeof February; it furtherdipped by about 4.84 percent to close the first quar-ter at 24,752.21 points. Overall, the market this first quar-ter recorded a total volumeof 26.03 billion units valuedat N214.36 billion ex-changed in 399,753 dealscompared with 26.95billionunits valued atN191.82billion exchanged in

599,411 deals in quarter onein 2010.

Other features of thecapital market during thefirst quarter 2011 include thedelisting of about 12 com-panies due to non-compli-ance with regulatory require-ments; absence of new pub-lic issues or notable privateplacement; build-up to theassumption of office by thenew chief executive officerof the NSE in early April.On its part, the SEC issueda new Code of CorporateGovernance, which becameeffective April 1, 2011; thenew code is prepared tomake Nigerian companiesoperate in line with globalbest practices and standards.

BANKING ANDFINANCEMany policy initiatives in thebanking and finance sectorcame into effect during thefirst quarter 2011, includingtwo-times upward review of

the Monetary Policy Rate(MPR) by the CBN: first,from 6.25 per cent to 6.50per cent in January and fur-ther to 7.50 per cent inMarch. It also altered othermonetary policy indices suchas the Cash Reserve Ratio(CRR) and Liquidity Ratio.The apex bank in its driveto check speculative demand(for forex) and keep thenation’s currency stable alsoapproved four foreign ex-change instruments for fu-tures trading. These includeFX Options, Forwards (Out-right and Non-Deliverable),FX Swaps and Cross-Cur-rency Interest Rate Swaps. Inits guidelines for the ‘for-wards transactions’ with au-thorized dealers, the CBNprovided for twice auctionsa week, with tenors of one,two and three months. Theminimum allowable bid byauthorized dealers for eachtenor stands at US$500,000only while a maximumspread of 50 kobo is al-

THE NSE TRADED VOLUME: Q1, 2010/Q1, 2011

http://www.knight.icfj.org/i/farming.jpg

April 2011 Zenith Economic Quarterly 9

PERISCOPE Economy:Output Growth Remains Resilient

lowed on the sale of ‘for-wards’ with less than threemonths’ tenor and 75 kobofor tenors above threemonths. The apex bank how-ever insists that forex pur-chased from its regularWholesale Dutch Auctions(WDAS) cannot be sold ‘for-wards’ to customers, as itmust be utilized within fivedays after settlement in linewith the WDAS rules.

For direct intervention ineconomic development dur-ing the first quarter, theCBN in concert with theBankers’ Committee pur-sued with vigour, fresh ini-tiatives with foci on agricul-tural and infrastructural de-velopment. Specifically, inaddition to the existing Agri-cultural Credit GuaranteeScheme (ACGS), the apexbank introduced the Nige-rian Incentive-based RiskSharing System for Agricul-tural Lending (NIRSAL).This innovative financingmechanism is intended to

ease access to bank financ-ing for agriculture, especiallythrough the adoption ofrisk-sharing approaches inagric business. Under thisarrangement, eight prioritycommodities have beenidentified with their financialvalue chain analysis con-cluded. The apex bank hasalso secured the collabora-tion of such internationalagencies as the United Na-tions Industrial Develop-ment Organization(UNIDO), the Alliance forGreen Revolution in Africa(AGRA), among others.

Under the other plank ofthe initiative, namely thePower and Transport infra-structure development, theCBN and the banks havecommenced capacity build-ing efforts to effectivelydrive the Public-PrivatePartnership in this regard.The Euromoney has alreadybeen contracted and com-menced training for about250 Nigerian bankers to be-

come more knowledgeablein funding structures,sources of funds, risks andcritical concerns in projectfinancing. They are also tolearn how credit crisis hasimpacted on sources of fi-nance and what alternativesources of funding are avail-able; and gain better under-standing of the core provi-sions in the commercial andfinancial contract frameworkto support successful financ-ing for power and transportinfrastructure.

Furthermore, legislativeinitiatives are also beingtaken. In deed, a Bill hasbeen forwarded to the Na-tional Assembly to constitutea ‘Grievances ArbitrationCommittee’ that will handlegrievances on issues creatingbottlenecks in infrastructuredevelopment. Also beingconsidered is the establish-ment of a Transport Infra-structure Fund with requisiteguarantees from both theFederal Government and

the CBN, among others.The CBN also continued

with its effort at enthroningmobile banking in the coun-try; it extended the pilotphase of the roll-out ofmobile money services bytwo months—after the ex-piration of its earlier dead-line on March 31, 2011. The16 entities to whom it hadissued temporary licenses (orApproval-in-Principle) weregiven up to end-March todemonstrate theircompetences, and be givenfull licenses. The temporarylicensees or consortiums arein two categories: bank-ledand non-bank firms. Thefollowing companies makeup the two groups: UBA/Afripay, First Bank of Ni-geria, GTBank,MobileMoney, StanbicIBTC and Ecobank. Othersare FFortis MFB, Pagatech,Paycom, Chams, E-Tranzact, Funds ElectronicTransfer (FET), Monitiz,Parkway, Corporeti Services,Eartholeum, and M-Kudi.The CBN had earlier issuedthe regulatory frameworkand guidelines for mobilebanking in Nigeria that willconform to internationalbest practices and standards.

A number of DepositMoney Banks (DMBs) dur-ing the quarter under reviewcontinued their recapitaliza-tion drive; many signedMoUs to go into some formof business combinations(mainly mergers and acqui-sitions). Afribank Plc andVine Capital Limited signeda Memorandum of Under-standing (MoU). Others thatalso signed include UnionBank Plc and African Capi-tal Alliance, IntercontinentalBank Plc and Access BankPlc, Bank PHB and HabibBank Pakistan, among oth-ers. However, almost all the

...the CBN inconcert with the

Bankers’ Commit-tee pursued with

vigour, freshinitiatives with focion agricultural and

infrastructuraldevelopment.

10 Zenith Economic Quarterly April 2011

PERISCOPE Economy:Output Growth Remains Resilient

MoUs are affected by some litigationor the other, either by shareholder as-sociations, legacy managers or otherinterested parties. Even the plannedmerger between First Bank of NigeriaPlc and Oceanic Bank Plc had beenstalled as a result of the inability ofthe two banks to reach favourableagreements so far.

The common year-end policy forthe DMBs gained momentum duringthe quarter, with all the banks tidyingtheir 2010 accounts and annual reportsfor scrutiny and approval by the regu-latory authorities. Almost all the banksalso commenced the introduction ofthe International Financial ReportingStandard (IFRS) into their reportingframeworks. Also in line with the newlyintroduced banking model, most banksduring the period under review beganthe process of transforming into aholding company and/or liquidatingtheir investments in non-core bankingsubsidiaries.

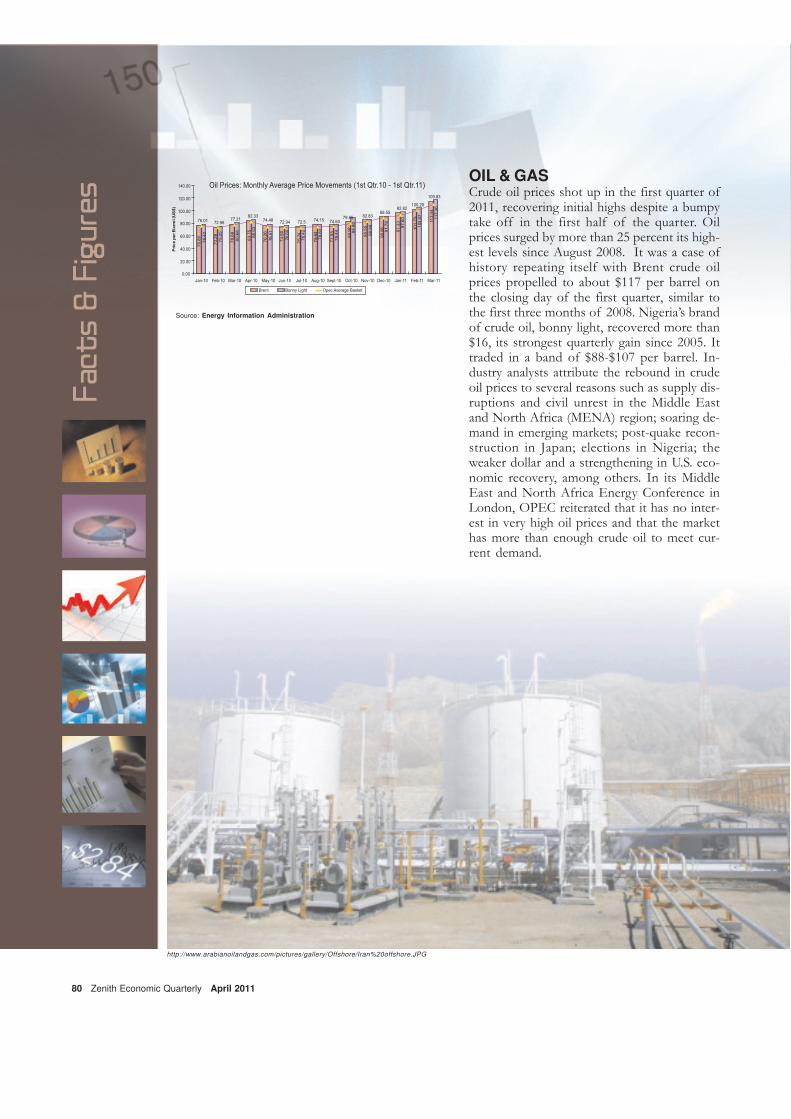

OIL, GAS & POWERAs the turmoil in some of the MiddleEast and North African (MENA) states(especially Libya) lingers, oil prices con-tinue to hang comfortably above theUS$100 per barrel mark. In its March2011 Monthly Oil Market Report(MOMR), the Organization of Petro-leum Exporting Countries (OPEC)noted that events in the MENA re-gion and the associated risk premiumhave pushed oil prices to their highestlevel since September 2008. Specifi-cally, OPEC basket averaged close toUS$110 per barrel in March, upUS$9.55 per barrel from the previousmonth. The OPEC Reference Basket,moved above US$100 per barrel on21 February and continued its upwardtrend in March to average US$109.84per barrel, the highest monthly levelsince the US$112.41 per barrel at theonset of the financial crisis in 2008.

The increase of US$9.55 in Marchwas the sixth in a row and the largestsince the US$11.38 of June 2009. Withthis increase, the OPEC ReferenceBasket averaged US$101.27 per bar-rel in the first quarter, 2011—upUS$17.39 from the last quarter in 2010and US$25.78 from a year earlier. The

strong increase in the OPEC Refer-ence Basket over the previous threemonths, particularly in March, was at-tributed to the bullish sentiment in thefutures market as prices jumped amidworries about supply shortages follow-ing the persisting crisis in Libya andunrest in some countries in the MiddleEast and North Africa (MENA) re-gion.

This turn of events, for Nigeria,has implied improved foreign exchangeinflow; increased demand for the Ni-gerian crude and rise in production andexport volume. Oil prices have com-fortably remained above the 2011 Fed-eral Government benchmark ofUS$65 per barrel while production hasbeen consistently above two millionbarrels per day. These translate intosubstantial inflow into the Excess Crude

Account (or now approved SovereignWealth Fund, SWF). OPEC in itsMarch Monthly Oil Market Report,estimated Nigeria’s crude oil output at2.089 million barrels per day in Febru-ary, a slight drop from the 2.181 mil-lion barrels per day in January, and2.192 million barrels per day in De-cember 2010. However, this did nottranslate into abundance of petroleumproducts; in fact, prices of productslike diesel, kerosene and petrol (tosome extent) have been on the in-crease.

Fuel importation subsists while thelocal refineries have continued to op-erate far below capacity, and remainlargely in a state of disrepair. Yet, theestimated daily demand for petroleumproducts in Nigeria today is 30 millionlitres of petrol (PMS), 10 million litres

htt

p:/

/ww

w.f

loati

ng

pla

nts

erv

ices.c

om

/_fi

les/p

ictu

re_1/1

2.jp

g

April 2011 Zenith Economic Quarterly 11

PERISCOPE Economy:Output Growth Remains Resilient

Kainji Hydro Electric Power Plant

of kerosene (DPK), 18 million litresof diesel (AGO), and 780 metric tons(1.4 million litres) of cooking gas(LPG), and the estimated amount ofcrude oil required daily for domesticrefining, that would satisfy the demandfor petroleum products in Nigeria ad-equately, should be about 530,000 bar-rels per day (bbl/d). This is some85,000 bbl/d more than the combinedrefining capacities of all the state-owned refineries located in Warri, PortHarcourt, and Kaduna. The four re-fineries have combined installed capac-ity of 445,000 barrels per day, but havenever reached full production at anypoint in time. Nigeria spent aboutN1.15 trillion to import an estimated8.1 million metric tons (MT) of petro-leum products in 2010 alone and hasspent about N388.11billion to import

country as the undisputed regional hubfor gas-based industries.” This plan, ac-cording to the President would also leadto the building of a world-scale petro-chemical plant, two fertilizer plants, fivefertilizer blending plants, a methanolplant and a liquefied petroleum gas(LPG) distribution plant. In fact, un-der the plan, Nigeria Agip Oil Com-pany (NAOC) and Oando Nigeria Plcare to jointly build a US$3 billion Cen-tral Gas Processing Facility (CPF) inObiaruku, Delta State, and billed forcompletion in 2012.

In the power sector, the sale of thesuccessor-companies created out ofthe unbundling of the Power HoldingCompany of Nigeria (PHCN) domi-nated the sector during the period un-der review. The Bureau of Public En-terprises (BPE) which continued theconduct of its bidding process for thesale of eighteen power firms, receivedan overwhelming expression of inter-est in the scheme. About 332 entitiesshowed interest by the close of the ex-tended deadline on March 4, 2011. Thecore-investor sales will cover the elevenelectricity distribution companies aswell as the privatization of four ther-mal and two hydro power stations.According the BPE, 157 applicationswere received from prospective inves-tors interested in acquiring the distri-bution companies, while 174 applica-tions came from those interested inacquiring the power stations.

The Nigerian Electricity RegulatoryCommission (NERC) on its part wasengrossed with the development of anew electricity tariff structure thatwould be good incentive to attract andretain investors in the sector as well asmake for affordability for consumers.In this regard, NERC has been con-sulting with relevant government agen-cies –the BPE, PHCN, Ministry ofPower as well as other stakeholders todetermine the level of tariffs thatwould attract the desired investmentsinto the sector. Meanwhile, most ofthe entities granted licenses as Inde-pendent Power Producers (IPPs) areyet to commence serious work, sev-eral years after getting the licenses. Infact, while many are yet to secure sitesfor the power projects, a few others

petrol in the first quarter of this year.However, information from the

Nigerian National Petroleum Corpo-ration (NNPC) shows that plans areunderway for an additional 750,000bpd to be added to the existing refin-ing capacity of 445,000 bpd. In fact,China State Construction EngineeringCorporation Ltd intends to build threenew refineries in Kogi, Bayelsa, andLagos states. Already, the Memoran-dum of Understanding, MoU, has beensigned and the Chinese have inspectedthe proposed sites, as a sign of theircommitment to the project. The dealis said to be worth $23 billion. Alsowhile unveiling his ‘gas revolutionagenda’ in March, President GoodluckJonathan announced plan to “ensuregreater availability of gas for powergeneration and also reposition the

12 Zenith Economic Quarterly April 2011

PERISCOPE Economy:Output Growth Remains Resilient

have only been able to carry out Envi-ronmental Impact Assessment (EIA)on the sites.

TELECOMMUNICATIONA key development within the telecomssector within the period under reviewwas the commencement of SIM cardregistration by the Nigerian Commu-nications Commission (NCC). In thisregard the telecoms regulatory agencysigned a contract agreement with sevenICT firms to drive the registration pro-cess in different parts of the country.These partnering firms whose activi-ties will be coordinated by KPMG, aninternational professional services com-pany, are: SW Global, Private NetworksNigeria (PNN), Chams, JointKomputer Kompany (JKK),DataGroupit, EAGLE/CBC and E-

Kenneth/SageMetrics. On its part, theNCC will be responsible for gatheringand validating the subscriber informa-tion while the National Identity Man-agement Commission (NIMC) will bethe repository of Nigeria’s mobilephone subscriber database.

In a related development, the NCChas also commenced the selection ofa mobile number portability (MNP)operator in the country. This is to en-able mobile phone users retain theirunique numbers when changing fromone mobile network operator to an-other. This initiative is expected toserve as one of the mechanisms todrive competition and stimulate im-provement in quality of service andexpand coverage in the Nigeriantelecoms market.

Meanwhile the total number of

active subscribers in Nigeria’s telecomsmarket has passed the 90 million mark,according to statistics from the NCC.As at end-February 2011, total num-ber of active lines was 90,583,306 linesout of the 122,589,647 connected linesin the country. Market segmentationof the active lines showed that theGlobal System for Mobile Communi-cations (GSM) still dominates the mar-ket with 83,453,999 lines, accountingfor 92 per cent. Code Division Mul-tiple Access (CDMA) has 6,111,669active lines representing seven per cent;while the fixed wireless lines stood at1,014,691, accounting for only one percent of the market share.(* Marcel Okeke is the Editor, Ze-nith Economic Quarterly)

In a related develop-ment, the NCC has

also commenced theselection of a mobile

number portability(MNP) operator in the

country. This is toenable mobile phone

users retain theirunique numbers when

changing from onemobile network

operator to another.

14 Zenith Economic Quarterly April 2011

Polic

y

c. Microfinance Banks (MFBs)In a bid to ensure that the nascent microfinance banksachieve the policy objectives for which they were estab-lished and avoid the pitfalls which characterized the com-munity banking era, the CBN will intensify its surveillanceon the banks. The Bank shall also ensure the full imple-mentation of a Microfinance Certification Programme inNigeria with the objective of enhancing knowledge, im-pacting microfinance skills/competencies and methodol-ogy for service delivery among operators in the sub-sectoron a sustainable basis. In the 2010/2011 period, the Bankshall continue to license new microfinance banks and thecapital requirements of N20million and N1 billion for unitand state microfinance banks shall be maintained.

d. Development Finance Institutions (DFIs)The CBN shall in 2010 and 2011 continue to monitor theoperations of DFIs and intensify efforts aimed at re-capi-talizing the institutions, institutionalizing strong corporate

governance and a risk management system to enable theinstitutions effectively deliver on their core mandates. TheUniform Prudential and Assessment Standards prescribedfor DFIs in Africa, under the aegis of the Association ofAfrican Development Finance Institutions (AADFI) forbenchmarking the DFIs will continue.

e. Bureaux De Change (BDCs)The two categories of BDCs (A and B) currently existingwill remain until further notice. They will continue to ren-der monthly returns on their Assets and Liabilities, as wellas daily returns on utilization of foreign exchange to theCBN through the e-FASS.

Continued from last Edition

April 2011 Zenith Economic Quarterly 15

POLICY | MONETARY, CREDIT, FOREIGNTRADE & EXCHANGE POLICY GUIDELINES FOR FISCAL YEARS 2010/2011

xiv. Compliance with Statutory Regulations/Rendition of ReturnsAll OFIs are required to strictly comply with the pruden-tial requirements (Appendix I) specified in the existing guide-lines/circulars, directives and provisions of BOFIA 2004while appropriate sanctions shall be imposed on any erringOFI.

xv. Penalties for DefaultThe CBN shall in 2010/2011 continue to enforce all thestipulated penalties for non-compliance with regulatoryguidelines as well as the provisions of the CBN Act, 2007and Banks and Other Financial Institutions Act, 2004 asamended. Any financial institution which fails to complywith the existing and revised guidelines as well as otherdirectives that may be issued by the CBN shall be sanc-tioned accordingly.

xvi. Policy on Transparency in FinancialTransactionsIn line with the recommendations of the Basle Committeeon Banking Regulations and Supervisory Practices, all fi-nancial institutions are required to continue to observe thefollowing standards to promote transparency in financialtransactions:

a) Customer IdentificationBanks and other financial institutions are enjoined to in-tensify efforts to determine the true identities of all cus-tomers requiring their services. In particular, financial in-stitutions should not, as a matter of policy, conduct busi-ness transactions with customers who fail to provide evi-dence of their identity. The principle of “Know Your Cus-tomer (KYC)” as specified in the CBN AML/CFT Manual,2009 should be strictly adhered to.

b) Compliance with the LawBanks and other financial institutions shall observe highethical standards as well as comply with the laws and regu-lations governing their operations. In particular, banks shallensure full compliance with the Guidance Note, AML/CFT Manual 2009 and other relevant circulars on moneylaundering surveillance, issued by the Bank, in order toensure the enforcement of the provisions of the MoneyLaundering Act, Cap M18, laws of the Federation of Ni-geria, 2004.

c) Co-operation with Law Enforcement AuthoritiesBanks and other financial institutions are required to co-operate fully with the law enforcement authorities withinthe limits of the rules governing confidentiality. In particu-lar, where financial institutions are aware of facts whichlead to a reasonable presumption that the funds lodged inan account or transactions being entered into, derive fromcriminal activity or intention, they should observe the stipu-lated procedures for disclosure of the suspicious transac-tions in reporting to the law enforcement authorities. Any

contravention of the above-stated guidelines by any finan-cial institution shall attract penalties as stipulated in theBanks and Other Financial Institutions Act, 2004, or theMoney Laundering Act, 2004 as appropriate.

xvii. Risk-Based SupervisionThe Bank recently migrated from the compliance basedsupervisory approach to risk-based supervision (RBS) ap-proach in the supervision of institutions under its purview.The approach is designed to enable supervisors to focusattention on the risks that threaten the achievement ofsupervisory objectives and accordingly devise appropriaterisk mitigation programs. In addition to addressing emerg-ing challenges facing our banks, RBS would assist inNigeria’s drive to fully comply with the Basel Core Prin-ciples on Supervision and also prepare an enabling envi-ronment for the eventual implementation of the Basel IICapital Accord. In the 2010/2011 period the Bank shallcontinue with Risk based supervision.

xviii. Consolidated/ Cross Border SupervisionIn recent years Nigerian banks have established off shorebranches and subsidiaries, in an attempt to increaseshareholder’s wealth. This has exposed them substantiallyto cross border risks. Furthermore, the expansion of Ni-gerian banks into different sectors coupled with the recentturmoil in the world financial system has necessitated con-solidated supervision of banks. In a nutshell, consolidatedsupervision is a comprehensive approach to banking su-pervision which seeks to evaluate the strength of an entiregroup, taking into account all the risks which may affect abank, regardless of whether these risks are carried in thebooks of the bank or related entities. In view of the above,the Bank shall continue with consolidated, cross-bordersupervision in 2010/2011.

xix. Macro-prudential Regulation and StressTestingThe current global banking crisis has underscored the im-portance of complementing the current micro-prudentialapproach to regulation and supervision with the macro-prudential perspective. The latter, which assesses thestrength and weaknesses of the financial system in termsof its overall soundness, will help regulators have a holisticview of the banking system. A key component of themacro-prudential analysis is stress testing which gauges thepotential impact of adverse shocks on banks if macroconditions are weak. As an important risk managementtool, stress testing helps to identify adverse unexpectedoutcomes related to a variety of risks and provides anindication of how such risks might be handled by facilitat-ing the development of risk mitigating or contingency plansacross a range of stress conditions. Accordingly, the Bankshall ensure the use of macro-prudential regulation andstress testing in assessing the health of banks in 2010/2011.

16 Zenith Economic Quarterly April 2011

POLICY | MONETARY, CREDIT, FOREIGNTRADE & EXCHANGE POLICY GUIDELINES FOR FISCAL YEARS 2010/2011

xx. Strengthening Risk Management and CorporateGovernance in Nigerian BanksEffective risk management and corporate governance playa key role in the maintenance of strong financial institu-tions and by extension sound financial systems. Against thisbackground, the CBN issued guidelines for the develop-ment of risk management framework for individual banksin July 2007. Having regard to the dynamic nature of risks,the guidelines shall be constantly reviewed and updated inline with global best practice and the recommendation ofthe Basel II Capital Accord. The Guidelines were designedto enable banks develop their respective strategy for man-aging each risk element as part of the overall strategy forevolving efficient risk management systems. Likewise, theCBN issued a new Code of Corporate Governance in April2006 to assist banks in installing corporate governance struc-tures that meet international best practices. The guidelineson risk management and code of corporate governanceshall remain in force in 2010/2011.

xxi. Additional Disclosures by BanksBanks are required to publish disclosure statements so asto strengthen the incentives for banks to maintain soundbanking practices and assist depositors and other investorsto make well informed decisions on where to invest theirmoney. The current disclosures are inadequate to addressthe contemporary challenges of a complex and dynamicbanking industry. Thus, in order to enhance transparencyin the Nigerian banking system and in light of contempo-rary experiences in the global and Nigerian financial sys-tems, the following additional disclosures shall form partof banks’ regulatory and financial reporting:• Risk Management• Capital Structure/Adequacy• Executive Compensation• Regulatory Sanctions and Penalties• Disclosure of related companies/persons engaged as ser-vice providers/suppliers to a bank• Disclosure on Insider Related Credits• Disclosure on Board of Directors’ Performance• Disclosure on concentration of assets, liabilities and off-balance sheet engagements by sector, geography, and prod-uct• Disclosure on Loan Quality• Disclosure on lending/borrowing to/from subsidiariesand associates• Disclosure on credit collaterals• Disclosure on Fraud and Forgeries• Disclosure on Banks’ Contingency Planning Framework• Disclosure on Loans and Advances/funding or creditlines from institutions outside Nigeria• Balance Sheet and Profit and Loss Account of Banks’Subsidiaries/Affiliates.

A circular detailing the content of each heading and thefrequency of publication/disclosure will be issued soon.

xxii Contingency Planning Framework for BankingSystemic Distress and CrisesIn order to ensure public confidence in the banking sys-tem, the Bank shall develop a set of policies, actions andprocesses necessary for the prevention, management andcontainment of banking systemic distress and crises. Aguideline to aid banks in developing their contingency plans,establish thresholds for supervisory intervention incorpo-rating appropriate action plans and defines the composi-tions and functions of a crisis management unit would beissued soon.

SECTION FOUR

4.0 FOREIGN TRADE & EXCHANGE POLICYMEASURES4.1 New Policy Measures for 2010/20114.1.1 Foreign Exchange Market(i) Retirement benefits of foreign nationals who contrib-uted to the pension scheme are eligible for remittance sub-ject to the following documentation requirements: - Dulycompleted Form ‘A’ - Resident Permit and/or expatriatequota - Retirement Savings Account statement - NationalPension Commission’s (Pencom) approval

(ii) Premium remittances on oil and gas and special riskswhich are handled by foreign broker/insurer can now beundertaken in the foreign exchange market. The documen-tation requirements are: - Duly completed Form ‘A’ - De-mand Note/Debit Note from foreign broker/insurer -Letter of attestation from the National Insurance Com-mission (NAICOM)

(iii) Authorised Dealers are allowed to sell autonomous fundsto Bureaux de Change operators subject to compliancewith the Anti-Money Laundering Act 2004 and disclosureof the sources of such funds to the CBN. In addition,daily returns shall be rendered to the CBN by both theAuthorised Dealers and the BDC.

(iv) Authorised Dealers that engage in importation of for-eign exchange (cash) will henceforth render monthly re-turns of such transactions to the CBN.

(v) For disposal of export proceeds, the instruction of theaccount holder shall be sufficient for own use of the funds.However, where the fund is to be transferred to third par-ties, the purpose for transfer should be provided by theaccount holder.

(vi) Travelers entering and/or leaving Nigeria are requiredto declare any amount above N20,000.00 (twenty thou-sand naira only) in their possession at the time of arrivalor departure from the country.

April 2011 Zenith Economic Quarterly 17

(vii) In accordance with the provisions of Public Procure-ment Act 2007 and subject to the provision of a perfor-mance bond and or bank guarantee by the suppliers’ bankoverseas, down payments in respect of imports into Nige-ria shall not exceed 15 per cent of the free on board (fob)value of the transaction.

4.1.2 Form ‘M’ Procedure(ix) Shipping documents predating Form ‘M’ and Letterof Credit (LC) approval date is liable to sanction in linewith the provisions of BOFIA, as well as other appropri-ate sanctions by the CBN.

4.2 Existing Policy Measures Amended/Retained in2010/20114.2.1 Foreign Exchange Market(i) In order to ensure stability of the exchange rate andconfidence in the market, the Foreign Exchange Market(FEM) shall operate freely, subject to the provisions ofrelevant laws and guidelines.

(ii) Authorised Dealers shall continue to deal freely in au-tonomous funds in their own right subject to compliancewith advised Net Open Position (NOP) limits. Banks are,however, not allowed to purchase funds, including inter-bank, on behalf of a customer without a valid underlyingtransaction and supporting documentation.

(iii) The direct foreign exchange cash sales by BDCs shallcontinue with the maximum limit of US$5000.00 per ap-proved transaction.

(iv) Holders of all categories of domiciliary accounts shallcontinue to have unfettered access to their funds.

(v) To ensure transparency and accountability in foreignexchange dealings, pooling of funds purchased from CBNwith those acquired from other sources is allowed pro-vided their sources are duly segregated and reported. Con-sequently, banks shall continue to render appropriate re-turns on sources of funds and utilization to the CBN.

(vi) Payment in foreign exchange for products and ser-vices provided in Nigeria by Nigerians either as an indi-vidual or a company shall not be allowed in the foreignexchange market. However, where the payer accepts topay in foreign exchange, the funds shall be from his ordi-nary domiciliary account and/or offshore sources.

(vii) All oil and oil services companies shall continue to selltheir foreign exchange brought into the country to meettheir local expenses to any bank of their choice includingthe CBN. Monthly returns via e-FASS by both the oil com-panies and the banks on such sales and purchases shall berendered to the CBN, using the approved format.

(viii) All applications for foreign exchange (valid or not-

valid), shall continue to be approved by banks subject tostipulated documentation requirements before remittanceof funds.

(ix) Payment of interest in respect of bills for collectionshall continue to be on the tenor of the bill but not exceed-ing 180 days at a maximum of 1 per cent above the primelending rate prevailing in the country of the beneficiarybased on London Interbank Offered Rate (LIBOR).

(x) Transactions executed at private sector initiative shallcontinue to have no government guarantee or obligations.

(xi) Business Travel Allowance (BTA) and Personal TravelAllowance (PTA) shall be subject to the maximum ofUS$5,000.00 and US$4,000.00 per quarter respectively.

(xii) WDAS funds shall neither be tradable in the inter-bank foreign exchange market nor sold to BDCs.

(xiii) Only hotels registered as Authorised Buyers shall re-ceive from foreign visitors payment of hotel bills in for-eign currency. However, payment of such bills in foreigncurrency shall be optional and at the discretion of the for-eign visitor making the payment.

4.2.2 Form ‘M’ Procedure(i) Post-landing charges shall continue to be treated as anintegral part of the total cost of projects and that of theForm ‘M’. No direct or separate remittances on Form ‘A’in respect of such charges shall be allowed.

(ii) The initial validity period of an approved Form ‘M’ forgeneral merchandise shall be 180 days. The validity periodof the approved Form ‘M’ and the related Letter of Creditmay be extended for another 90 days by the AuthorizedDealer. For capital goods the initial validity of an approvedForm ‘M’ shall be 365 days and the validity of the formM and related Letter of Credit may be extended by an-other 180 days by the Authorised Dealer. However, anysubsequent request for revalidation of form ‘M’ shall beforwarded to the Director, Trade and Exchange Depart-ment, CBN for consideration.

4.2.3 Destination Inspection of Imports(i) All goods consigned for imports to Nigeria (except thoseexempted) shall be subject to Destination Inspection Scheme(DIS).

(ii) All imports to the country, whether or not exemptedfrom DIS shall require the completion of Form ‘M’.

4.2.4 Import Duty Payment Procedures(i) Import duty payable on items registered under Form‘M’ transactions, whether or not valid for foreign exchange,shall be calculated on the basis of CBN prevailing rate onthe day the Form ‘M’ was approved.

POLICY | MONETARY, CREDIT, FOREIGNTRADE & EXCHANGE POLICY GUIDELINES FOR FISCAL YEARS 2010/2011

18 Zenith Economic Quarterly April 2011

(ii) Payments of import duty and other charges shall bemade through the processing bank provided that it is adesignated bank. However, where the processing bank isnot a designated one, the duty should be paid in anotherdesignated bank of the importer’s choice and the process-ing bank advised accordingly.

4.2.5 Export and Trade Promotion(i) Repatriation of export proceeds (oil and non-oil) andother inflows shall be held in Domiciliary Accounts. Hold-ers of such domiciliary accounts shall continue to haveunfettered access to their funds subject to existing guide-lines.

(ii) Payments for exports from Nigeria shall continue to beby means of Letters of Credit or any other approved in-ternational mode of payment.

In addition, such exports shall be executed on free-on-board(fob) or cost and freight (c&f) basis, depending on thecontract between the Nigerian exporter and the overseasbuyer.

4.2.6 Invisible Trade Transactions(i) Remittances for licences (Trademarks, Patents, Know-how, etc.) or Other Industrial Property Rights shall rangebetween 0.5 to 5.0 per cent of net sales value or profitbefore tax where net sales is not available. Trademarks feeshall not be allowed in respect of any agreement where thetrademarks owner has over 75 per cent of the equity inthe local company. Companies with several product linesshould separate the net sales of each product line in theiraudited accounts so as to pay royalty for specific product(s)covered by the industrial property rights and not on theentire/total sales of the company.

(ii) Technical Services fees shall no longer be tied to netsales. Services such as training, installation and maintenance,etc., shall henceforth be settled on per diem rate or man-hour, man-day or man-month basis while fees for Research& Development and improvement shall attract up to 1 percent of net sales.

(iii) Management Services fees shall range from 2.0 to 5.0per cent of the company’s profit before tax. Managementfees in respect of products where no profit is anticipatedduring the early years shall range from 1 to 2.0 per cent ofnet sales during the first three to five years only.

(iv) Annual Technical Support (ATS) fees payable to In-formation Technology (IT) licensor shall be between 15.0per cent and 23.0 per cent of the license fee (the localcomponent of which must be paid in Naira) and shall notlast for more than 3 years. In addition, indigenous localvendors must be involved in all ATS for Software Agree-ments and the local vendors’ fee shall not be less than 40.0per cent of the ATS fees.

(v) In case of Hotel Services, a basic fee or lump sum notexceeding 3.0 per cent of the net sales plus incentive feesnot exceeding 8.0 per cent of Gross Operating Profit(GOP) shall be applicable. Other payments which are in-ternationally acceptable within the applicable hotel chainsmay be allowed.

(vi) Remittable consultancy fees shall be a maximum of5.0 per cent of project cost and limited to projects of veryhigh technology content for which indigenous expertise isnot available. Service Agreement for high technology jointventures shall continue to include a schedule for trainingof Nigerian personnel for eventual take-over. In addition,Nigerian professionals shall be involved in the project imple-mentation from inception.

4.2.7 Miscellaneous Policy Measures(i) The declaration on Forms TM & TE of foreign cur-rency imports and exports, respectively, of US$5,000.00(five thousand US dollars) and above or its equivalent isrequired for statistical purpose only.

(ii) Appropriate sanctions shall continue to be imposed onAuthorised Dealers who remit funds on the basis of forgeddocuments, engage in fraudulent transactions, fail to trans-fer customs revenue to the CBN in accordance with thelaid down procedures, etc. The banks should, therefore,exhibit professionalism and transparency in handling trans-actions.

(iii) Appropriate sanctions shall also be imposed on bankcustomers who breach any of the foreign exchange opera-tional guidelines.

(iv) All Authorised Dealers are required to refer issues inrespect of the policy which they are in doubt, to the Direc-tor, Trade & Exchange Department of the Central Bankof Nigeria for clarification.

POLICY | MONETARY, CREDIT, FOREIGNTRADE & EXCHANGE POLICY GUIDELINES FOR FISCAL YEARS 2010/2011

20 Zenith Economic Quarterly April 2011

Glo

bal W

atc

h

irst quarter 2011 has come and gone, leav-ing indelible marks on the sand of global his-tory. The natural disasters in Japan andunrests in North Africa and Middle East aretwo developments within the quarter that theworld will not forget in a hurry. For nationaleconomies and other stakeholders in the glo-bal crude oil market, these events becomeeven more unforgettable as they have influ-enced crude oil price movements more thanany other development since the recent re-cession. Little would the world have imag-ined that the act of a simple vegetable sellerin a small Tunisian town would not only sethim but the entire Arab region ablaze. But itdid, and the global economy is now grapplingfor a way out.

The quarter saw nature wreaking colos-sal havoc on human lives and infrastructure.In the first week of January, almost 100 per-sons were declared dead or missing follow-ing a devastating flood in Queensland, Aus-tralia, a development that cost the economyan estimated A$30 billion reduction in GDP.Then the Christchurch earthquake measur-ing 6.3 magnitude that struck in New Zealandon February 21 killing nearly 200 persons.January 11 and 12 saw heavy floods and

mudslides near Rio de Janeiro in Brazil kill-ing over 600 persons and washing awayhomes, businesses and public infrastructureworth billions of dollars, in what has beendescribed as the worst flood in the county’shistory.

On March 11, a caustic 9.0 magnitudeearthquake and a 33-foot tsunami hit Ja-pan almost simultaneously followed by se-ries of aftershocks. This was the worst natu-ral mishap in Japan’s history and measuredby experts as among the five most cata-strophic in modern times, with an estimated18,000 lives lost; about 3,000 injured andover 17,000 people still missing as at the

* By Eunice Sampson

January 11 and 12 sawheavy floods andmudslides near Rio deJaneiro in Brazil killingover 600 persons andwashing away homes,businesses and publicinfrastructure worthbillions of dollars, inwhat has beendescribed as theworst flood in thecounty’s history.

April 2011 Zenith Economic Quarterly 21

end of first quarter. Roads, railways,bridges, dams, schools and other criti-cal infrastructure were destroyed, whilea major accident occurred in threenuclear plants. The World Bank calcu-lates the damage to the Japaneseeconomy and infrastructure at between$122 billion and $235 billion. Japaneseauthorities put the estimate at over$300 billion. For the massive economicsize of Japan and its status in the glo-bal economy, the March 2011 earth-quake and tsunami in that country isperhaps the most costly natural disas-ter in human history.

Thanks to the growing sophistica-tion in modern day seismic technologyand years of consciousness about thecountry’s geological vulnerabilities, theJapanese authorities may have spentthe better part of the last decade pre-paring for a possible earthquake andtsunami. But the same cannot be saidabout the turmoil in the Arab regionwhich took the world completely bysurprise. Perhaps there have been sev-eral analyses in the past comparing thesocio-political and economic structure

in the Arab world to a ticking time-bomb. But not many had expected suchlevel of explosion so soon, nor the rela-tively very mundane manner it wasdetonated.

Arab World Crises: theGenesisDespite his university degree,Mohamed Bouazizi resorted to sellingfruits and vegetables after all effortsto secure a more befitting employmentfailed. On December 17, 2010, localTunisian authorities seized his wares, avegetable cart, on claims that it wasunlicensed. After trying in vain to re-trieve his confiscated cart, in protestthe frustrated 26 year old universitygraduate set himself ablaze outside thepolice provincial headquarters. OnJanuary 4 Bouazizi died of complica-tions from his burns.

Mohamed Bouazizi was the breadwinner in a family of eight. He lost hisfather at the age of three and wassaddled with the responsibility of ca-tering for his widow mum and sevensiblings. The initial hopes that a uni-versity education will afford him agood job and a better life was dashedafter searching in vain for employment.He was compelled to settle for cartpushing, a menial job he was to giveup his life for.

According to reports from Reuters,Bouazizi’s grieving mother, Mannoubiahad one prayer for the ‘killers’ of herson: “I ask God that Ben Ali’s people,and the Trabelsi family, who were rul-ing Tunisia, go completely.” True to herprayers, on January 14, exactly 10 daysafter her son died, Ben Ali and his rul-ing family fled Tunisia to take refugein Saudi Arabia following an unprec-edented uprising as angry demonstra-tors demanding justice for the bloodof Bouazizi and protesting the circum-stances that led to his death hit thestreets of Sidi Bouzid. By January 14,the protesters had gained the upperhand as they succeeded in bringing toan abrupt end the 23-year reign ofPresident Zine al-Abidine Ben Ali.

Before his tragic end, BouaziziMohamed was a resident of SidiBouzid, a small, struggling town in thesuburb of Tunisia 250 km (155 miles)

southwest of Tunis. Sidi Bouzid was atypical small, remote town in a low-income economy characterized bymassive infrastructure decay and highrate of poverty and unemployment.But this town was to gain global promi-nence following Bouazizi’s self-immo-lation. It in fact became the startingpoint of a socio-economic, political andconstitutional revolution, first by ex-tending to other cities in Tunisia and,by the end of the quarter, spreadingto several countries in the Arab world.

In neighboring Egypt, Algeria andMauritania, several nationals, frustratedwith the leadership and living condi-tion resorted to the Bouazizi-style ofprotest by setting themselves ablaze,heightening the growing profile ofBouazizi as the hero of change in theregion. The triumph of the voices ofthe Tunisian people inspired similarprotests in other Arab countries, includ-ing Egypt, Morocco, Syria, Yemen andLibya.

After Ben Ali, Egypt’s HosniMubarak was next to go. Egyptian dem-onstrators took to the streets on Janu-ary 25, protesting against the high costsof food, official corruption,authoritarianism and unemployment;and calling for an end to PresidentMubarak’s 30-year rule. For over twoweeks, Egyptians besieged the Cairo’scentral Tahrir Square daily, defying in-timidations and arrests and voicing theirfrustration with Mubarak’s strong gripon power. On February 11, Mubarakyielded to mounting pressure at homeand abroad to step down as Egyptianpresident.

In near by Morocco, the “move-ment for dignity” on February 20, ral-lied protesters, demanding that KingMohammed VI review the country’sconstitution, give up some of his pow-ers and increase food price subsidy. Butthe protests in Morocco were mostlypeaceful and short-lived, perhaps be-cause some of these demands receivedimmediate government attention; orperhaps because despite being under350 year-old monarchical rule (theAlawite dynasty), Morocco remainsone of the most progressive nations inthe Arab world with a relatively robusteconomy, an elected parliament and a

htt

p:/

/ww

w.m

idd

leto

wn

pre

ss

.co

m/c

on

ten

t/a

rtic

les

/20

11

/01

/13

/bu

sin

es

s/d

oc

4d

2e

37

06

cf4

34

18

05

86

58

8.j

pg

22 Zenith Economic Quarterly April 2011

GLOBAL WATCH | Global Economyin 2011: the oil price factor

monarchy that is open toreforms and tolerates peri-odic public protests.

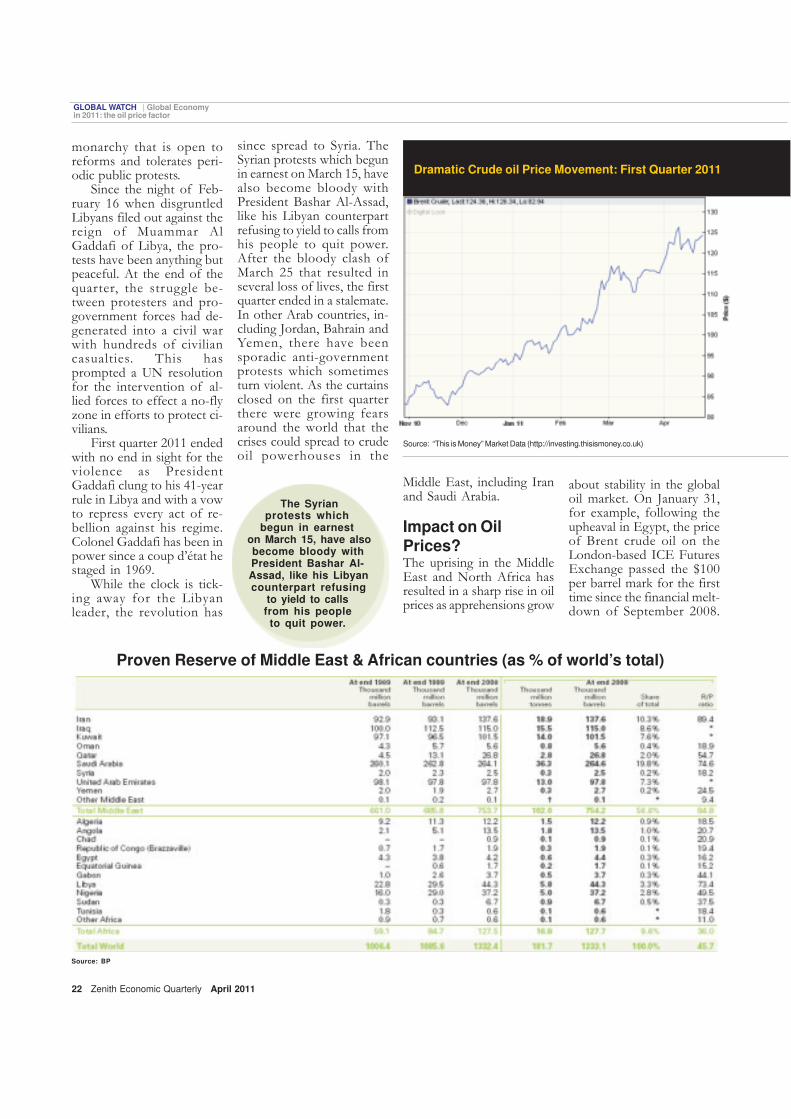

Since the night of Feb-ruary 16 when disgruntledLibyans filed out against thereign of Muammar AlGaddafi of Libya, the pro-tests have been anything butpeaceful. At the end of thequarter, the struggle be-tween protesters and pro-government forces had de-generated into a civil warwith hundreds of civiliancasualties. This hasprompted a UN resolutionfor the intervention of al-lied forces to effect a no-flyzone in efforts to protect ci-vilians.

First quarter 2011 endedwith no end in sight for theviolence as PresidentGaddafi clung to his 41-yearrule in Libya and with a vowto repress every act of re-bellion against his regime.Colonel Gaddafi has been inpower since a coup d’état hestaged in 1969.

While the clock is tick-ing away for the Libyanleader, the revolution has

Source: “This is Money” Market Data (http://investing.thisismoney.co.uk)

Dramatic Crude oil Price Movement: First Quarter 2011

since spread to Syria. TheSyrian protests which begunin earnest on March 15, havealso become bloody withPresident Bashar Al-Assad,like his Libyan counterpartrefusing to yield to calls fromhis people to quit power.After the bloody clash ofMarch 25 that resulted inseveral loss of lives, the firstquarter ended in a stalemate.In other Arab countries, in-cluding Jordan, Bahrain andYemen, there have beensporadic anti-governmentprotests which sometimesturn violent. As the curtainsclosed on the first quarterthere were growing fearsaround the world that thecrises could spread to crudeoil powerhouses in the

Proven Reserve of Middle East & African countries (as % of world’s total)

Source: BP

Middle East, including Iranand Saudi Arabia.

Impact on OilPrices?The uprising in the MiddleEast and North Africa hasresulted in a sharp rise in oilprices as apprehensions grow

about stability in the globaloil market. On January 31,for example, following theupheaval in Egypt, the priceof Brent crude oil on theLondon-based ICE FuturesExchange passed the $100per barrel mark for the firsttime since the financial melt-down of September 2008.

The Syrianprotests which

begun in earneston March 15, have alsobecome bloody withPresident Bashar Al-Assad, like his Libyancounterpart refusing

to yield to callsfrom his peopleto quit power.

April 2011 Zenith Economic Quarterly 23

GLOBAL WATCH | Global Economyin 2011: the oil price factor

Major market concerns were the possibility of the Egyp-tian revolution spreading to other oil-exporting Arab coun-tries and a possible obstruction to the passage of oil-bear-ing tankers through Egypt’s Suez Canal. The Canal remainsa strategic link between millions of barrels of crude oil perday and the global market.

Assurances from market analysts that United States’huge oil stockpiles and Saudi authorities’ massive sparecapacity will check possible supply disruptions did little todouse market tension. Oil prices remained at elevated lev-els all through the quarter, worsening further after the up-rising spread to Libya.

On the last day of the quarter, Thursday March 31,crude oil prices rose to a 30-month high as the battle forrebel-held areas intensified in East-ern Libya. Light crude for April de-livery gained $2.45 (or 2.35%) toclose at $106.72 per barrel. Brentcrude for May delivery also gained$2.23 (or 1.94%) to close at$117.36.

So far, the revolution in NorthAfrica has had the most significantinfluence on oil price movement in2011. Despite being a net importerof crude oil, Egypt’s control of theSuez Canal and the strategic posi-tion it occupies in the oil- rich Arabworld, caused massive price volatil-ity during the civil rebellion there.As for Libya, its position as Africa’sthird-largest oil producer with about1.6 million barrels of crude a day,coupled with its status as the country with the largest provenoil reserves in Africa, make the current civil war in thatcountry a factor in oil price movements. This is furthercompounded by the fact that Libya exports most of its oilto the developed economies of Europe, including Italy, Ger-many, Spain and France.

With proven reserves of 754 million barrels and 127million barrels between them, the Middle East and Africacontrol a total of 66% of global crude oil reserve (at 56.6and 9.6%, respectively), according to recent reportspublished by the British Petroleum, BP. In a worlddominated by an insatiable craving for oil, the tworegions hold the future of the global energy marketin their hands. And should the current uprising spreadto the major oil exporting countries in the region,there’s no saying what the outlook for the globalcrude oil price and supply might be in the short tomedium term.

Impact on Food Prices?No thanks to the ongoing crises in North Africaand the Middle East, crude oil prices increased by10.3% in the month of March alone and by 21% inthe first quarter of 2011.

World Bank’s ‘Global Food Security Update’ publishedthis April reveals that sharp increases in energy price affectthe price of food in three main ways:

•They encourage greater use of food products in theproduction of biofuels;

•They feed into the cost of food production throughhigher fertilizer prices, the cost of irrigation, and other farminputs;

•They increase the costs of crop transportation to mar-kets

According to the report, a 10% increase in crude oilprice is associated with a 2.7% increase in the World BankFood Price Index which is now back to its 2008 peak ow-ing mostly to current oil price upswing. Multilateral organi-zations have raised alarm over the worsening global pov-

erty level as the extreme poor spendhigher percentage of their meagerincome on food (up to 70% in someinstances). Since June 2010, theWorld Bank estimates that an addi-tional 44 million people fell below the$1.25 poverty line as a result of higherfood prices, part of which is due tohigher energy prices.

World Bank reports also show thatglobal maize price (an importantfood staple in Middle East and Af-rica) are 17% higher in the first quar-ter of 2011 compared to the lastquarter of 2010, due to increasingdemand for industrial uses and dwin-dling stocks. Several countries in Sub-Saharan Africa are presently faced

with double-digit increase in maize prices. Year-on-year, thereport identifies key staples that remain significantly higherthan their price level in 2010 to include maize (74%), wheat(69%), soybeans (36%) and sugar (21%). So, while highfood price was one of the key factors that triggered therecent uprisings in the first instance, the impact of the cri-ses has itself led to a further hike in the prices of food andother commodities. Several countries in the crisis-riddenregion, including Iran, Syria and Egypt and also countries

Source: World Bank’s Food Price Watch; April 2011

24 Zenith Economic Quarterly April 2011

GLOBAL WATCH | Global Economyin 2011: the oil price factor

in Sub Saharan Africa now strugglewith double-digit food price inflation.

At the outset of the tragic eventsin Japan on March 11, reports showthat fears of lower import demand haddriven down the futures’ prices ofcorn, soybeans and wheat. But pricesof these food commodities have sincerebounded as market fundamentalscould not sustain the sentiments thatbrought about their drop.

An increasingly disturbing aspect ofthe brewing food and energy price cri-ses is the growing use of food com-modities for bio-fuel productions inboth developed and emerging econo-mies. In its “Food Price Watch” ofApril 2011, the World Bank quotingdata released by the U.S. Departmentof Agriculture (USDA) reports that theuse of corn for biofuels in the US hasincreased from 31% of total corn out-put in 2008/2009 to a projected 40%in the 2010/2011 season. The effortto circumvent the rising price of crudeoil is increasing the diversion of foodfor bio-fuel purposes, further shorten-ing supplies and increasing prices. Ifthe trend persists, the world could beheading back to the crisis period it isonly just emerging from.

Oil price and growthprospects?Experts generally agree that first quar-ter developments could have massiveimpact on global growth outlook for2011. For the regions directly affectedby the recent uprisings, downside risksin growth prospects remain. Also, forJapan which suffered twin natural di-sasters during the quarter, prospect foreconomic expansion for 2011 looksvery dim.

The crises-ridden Arab states, es-pecially the net-importers of crude oil,will likely experience a sharp slowdownin 2011. However, growth in the en-tire Middle East and North Africa re-gion is still achievable, driven by theoil-exporting economies as they lever-age on record high price of crude oilto achieve strong economic advance-ment.

The Business Monitor Internationalforecasts a 4.1% growth for the re-gion in 2011, same as in 2010. Simi-

larly, the IMF has revised its economicgrowth projection for the Middle Eastand North Africa region to 4.1% thisyear, down from a forecast of 4.6%made in January.

Growth in Saudi Arabia – theregion’s largest economy is expected toremain strong for several reasons. Ithas so far been insulated from thesocio-political turmoil going on in theregion; while it also remains a majorbeneficiary in the current high priceof crude oil which is helping to boosteconomic spending and activities. TheIMF recently revised up Saudi’s 2011growth forecast sharply, from an ear-lier 4.5% to 7.5%. For the oil-import-ing Arab economies, the IMF in a newRegional Economic Outlook reportforesees possible fiscal deficits, dete-rioration in investors’ confidence andcapital flight, all resulting from the cur-rent uprising.

The Fund sees Egypt as one of theregion’s economies that would be worsthit by the crisis, especially due to itsvulnerabilities as a net- importer, andalso because of the sharp slowdownexpected from tourism, the country’seconomic mainstay. Egypt’s growthprospect has been lowered from the2010 level of 5.1% to just 0.1% thisyear. In the long term, however, thepositive changes expected from ongo-ing political, economic, social and con-stitutional reforms could mark the be-

ginning of a more rapid economic ex-pansion and competitiveness in the re-gion.

For Sub Saharan Africa, the IMFin its April 2011 Regional EconomicOutlook foresees macroeconomicchallenges for the region arising fromcurrent ‘rapid movements in keyprices’. Though the region is expectedto improve on its 2010 growth perfor-mance this year, from about 4.9% to arobust 5.5% in 2011 and 6.0% in 2012,the report observes that the rising priceof commodities would lead to a sig-nificant imbalance in growth, fromcountry to country. The big losers willbe the net oil importing economieswhile the big winners will be the oil ex-porting economies (Nigeria, Angola,Gabon, etc) which incidentally will bethe propeller of the improved growthprojection for Sub Saharan Africa.

For the developed economies ofEurope and America, growth outlookmay dim slightly despite the recent re-covery from the financial crisis. Theexpected positive impact of the USpayroll tax cut policy on the economyin 2011 notwithstanding, a recent re-port on the economy published byMorgan Stanley (Global EconomicForum) has downgraded the country’sgrowth forecast, from an earlier 3.6%to 3.3%. A major growth factor ob-served in the report is the direction ofthe global energy market this year. As

Source: BMI

April 2011 Zenith Economic Quarterly 25

GLOBAL WATCH | Global Economyin 2011: the oil price factor

it is, gasoline price which started offthe year at $3/gallon now stands atabout $4/gallon. According to the re-port, each $1/gallon change in gaso-line price subtracts about $120 billionfrom discretionary spending power, acritical growth indicator for the USeconomy. The economic gains from thepayroll tax reduction have thereforebeen offset by the recent upward trendin US gasoline price, an offshoot ofthe hike in oil price in the global mar-ket.