zvi wienerconttimefin - 4 slide 1 financial engineering the valuation of derivative securities zvi...

Post on 21-Dec-2015

213 views

TRANSCRIPT

Zvi Wiener ContTimeFin - 4 slide 1

Financial Engineering

The Valuation of Derivative Securities

tel: 02-588-3049

Zvi Wiener ContTimeFin - 4 slide 2

Derivative Security

A derivative security is one whose value depends exclusively on a fixed set of asset values and time.

Derivatives on traded securities can be priced in an arbitrage setting.

Derivatives on non traded securities can be priced in an equilibrium setting.

Zvi Wiener ContTimeFin - 4 slide 3

Derivative Security

Black-Scholes, Merton 1973

Options, Forwards, Futures, Swaps

Real Options

Zvi Wiener ContTimeFin - 4 slide 4

Derivative Security

- the proportion of the value paid in cash.

Pure options: = 1.

Pure Forwards: = 0.

No arbitrage assumption.

Free tradability of the underling asset.

Otherwise one have to find the equilibrium.

Zvi Wiener ContTimeFin - 4 slide 5

Arbitrage Valuation

Primary security X:

dX = (X,t)dt + (X,t) dZ

Derivative security V = V(X,t):

dV = VxdX + 0.5Vxx(dX)2 - Vdt

Zvi Wiener ContTimeFin - 4 slide 6

Arbitrage Valuation

How we pay for a derivative security?

A proportion is paid now (deposited in a

margin account).

If securities can be deposited in margin account, then = 0.

If paid in full, = 1.

Zvi Wiener ContTimeFin - 4 slide 7

Arbitrage Valuation

Arbitrage portfolio: P = V + hX.

dP = dV + h dX

dP = (Vx+h) dX + 0.5Vxx(dX)2- Vdt

In order to completely eliminate the risk, we should choose (Vx+h) = 0.

Such a portfolio has no risk, thus it must earn the risk free interest.

Important assumption: X is traded.

Zvi Wiener ContTimeFin - 4 slide 8

Arbitrage Valuation

Set h = -Vx.

dP must be proportional to the investment in the portfolio P. This investment is

V-Xh = V-XVx

Thus

dP = rPdt = r(V-XVx) dt

Zvi Wiener ContTimeFin - 4 slide 9

Arbitrage Valuation

dP = rPdt = r(V-XVx) dt

0.5Vxx(dX)2- Vdt = r(V-XVx) dt

0.5 2Vxx+ rXVx - rV - V = 0

the general valuation for derivatives

Zvi Wiener ContTimeFin - 4 slide 10

Arbitrage Valuation

0.5 2Vxx+ rXVx - rV - V = 0

Note that (X,t) does NOT enter the equation!

In addition to the equation one has to determine

the boundary conditions, and then to solve it.

Zvi Wiener ContTimeFin - 4 slide 11

The Forward Contract

Agreement between two parties to buy/sell a

security in the future at a specified price.

No payment is made now (forward), thus =0.

Let X be the price of the underlying asset.

Assume that there are no carrying costs

(dividends, convenience yield, etc.)

Zvi Wiener ContTimeFin - 4 slide 12

The Forward Contract

Assume that X follows GBM:

(X,t) = X (X,t) = X

The boundary conditions are:

V(X,0)=X immediate purchase

V(0, ) = 0 zero is an absorbing boundary

Vx(X, ) < the hedge ratio is finite

Zvi Wiener ContTimeFin - 4 slide 13

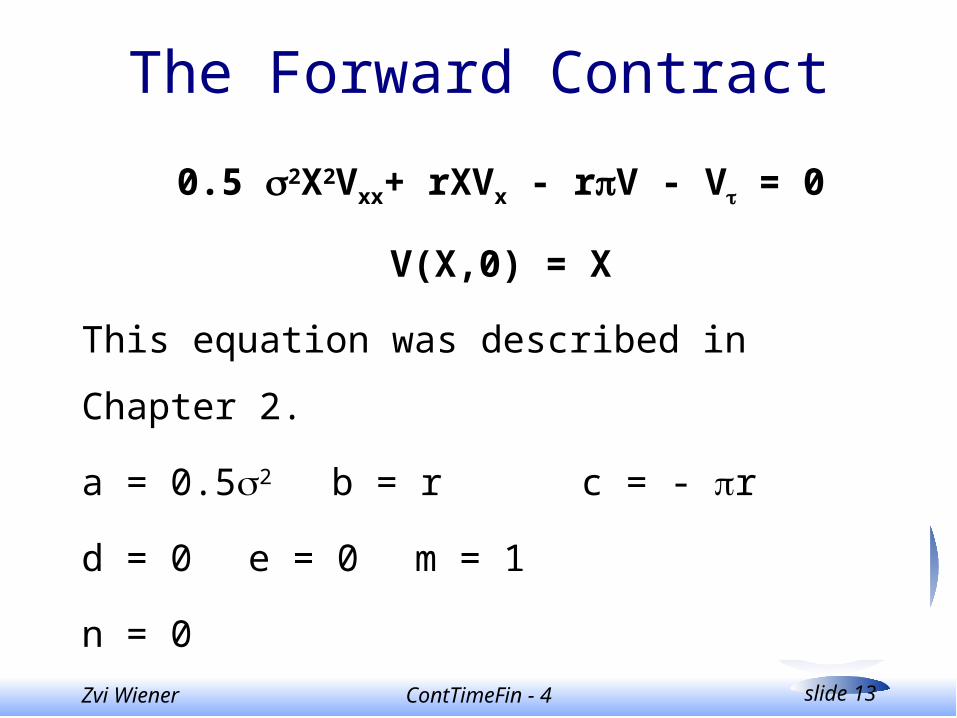

The Forward Contract

0.5 2X2Vxx+ rXVx - rV - V = 0

V(X,0) = X

This equation was described in Chapter 2.

a = 0.52 b = r c = - r

d = 0 e = 0 m = 1

n = 0

Zvi Wiener ContTimeFin - 4 slide 14

The Forward Contract

0.5 2X2Vxx + rXVx - rV - V = 0

V(X,0) = X

The Laplace transform is equal X/(s-(1- )r).

The inverse Laplace transform is V(X,)=Xer(1-).

As soon as <1, the forward price is higher than

the spot price.

Zvi Wiener ContTimeFin - 4 slide 15

The Forward Contract

The hedge ratio is Vx = V/X 1.

A perfectly hedged position holds one forward

contract and is short V/X units of the spot

commodity.

Zvi Wiener ContTimeFin - 4 slide 16

The European Call Option

Strike E.

Time to maturity .

Value of the option at maturity is: Max(X-E,0).

X

V

E

Zvi Wiener ContTimeFin - 4 slide 17

The European Call Option

V(X,0) = Max(X-E,0)

V(0, ) = 0

Vx(X, ) <

Normally the price is paid in full, = 1.

The PDE becomes:

0.5 2X2Vxx+ rXVx - rV - V = 0

V(X,0) = Max(X-E,0)

Zvi Wiener ContTimeFin - 4 slide 18

The European Call Option

0.52X2Vxx+ rXVx - rV - V = 0

V(X,0) = Max(X-E,0)

Can be solved with the Laplace transform.

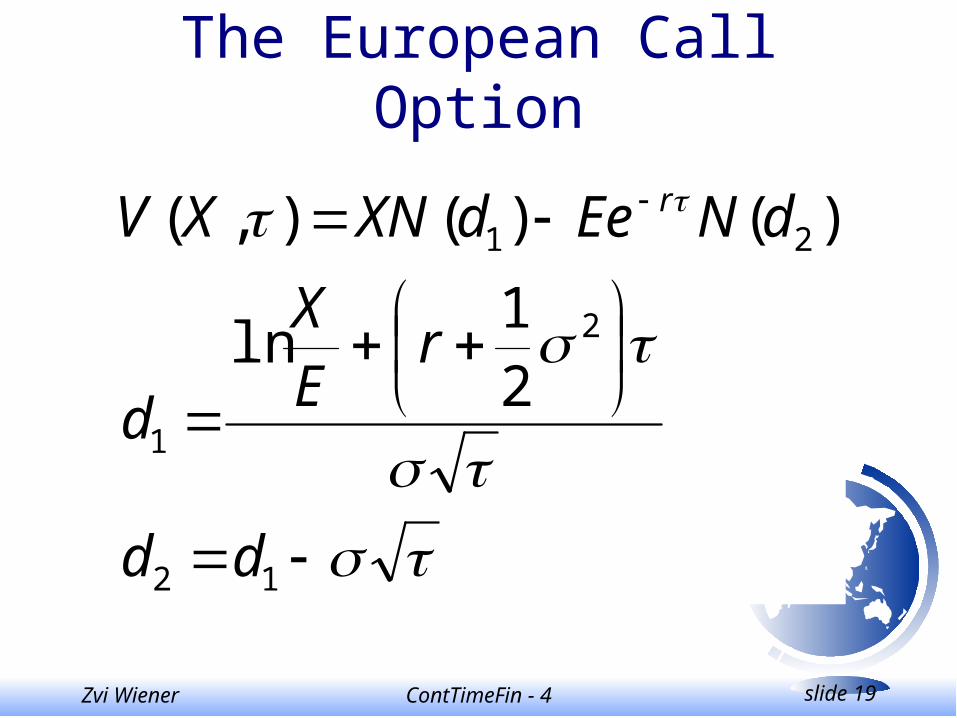

Zvi Wiener ContTimeFin - 4 slide 19

The European Call Option

12

2

1

21

21

ln

)()(),(

dd

rEX

d

dNEedXNXV r

Zvi Wiener ContTimeFin - 4 slide 20

Normal Distribution

x

N(x)

Zvi Wiener ContTimeFin - 4 slide 21

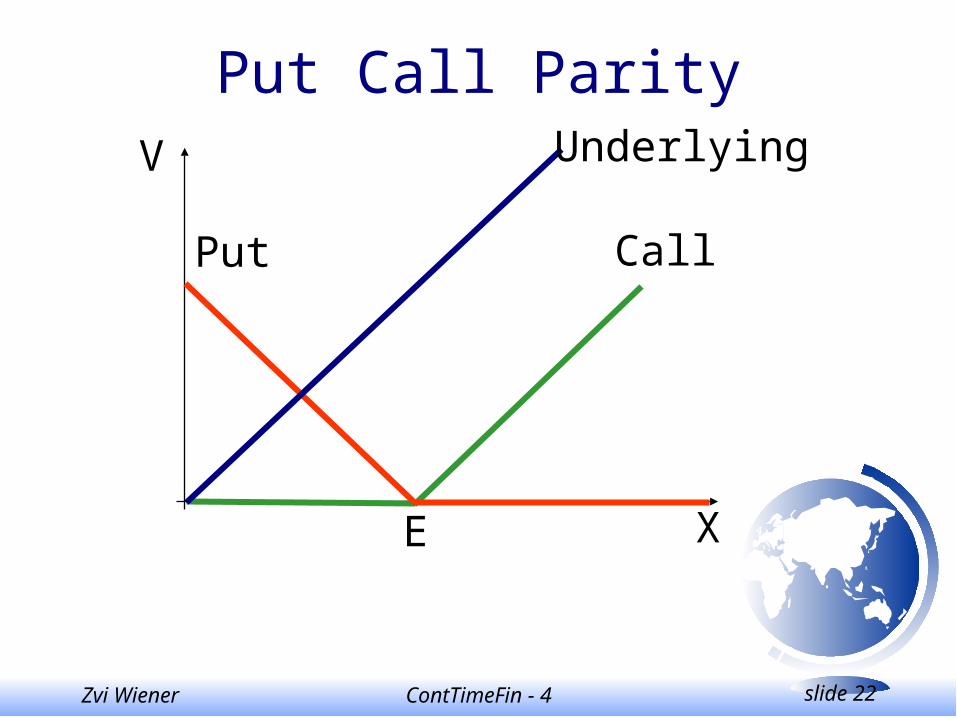

Put Call Parity

0.52X2Vxx+ rXVx - rV - V = 0

V(X,0) = Max(E-X,0)

E X

VPut Option

Zvi Wiener ContTimeFin - 4 slide 22

Put Call Parity

E X

V

CallPut

Underlying

Zvi Wiener ContTimeFin - 4 slide 23

Put Call Parity

Call-Put

E X

V Underlying

Zvi Wiener ContTimeFin - 4 slide 24

Put Call Parity

E X

V

Bond = Ee-r

Underlying =

Call-Put+Bond

Zvi Wiener ContTimeFin - 4 slide 25

Put Call Parity

X = Call - Put + Ee-r

Synthetic market portfolio

Zvi Wiener ContTimeFin - 4 slide 26

Hedging

X - h*Call - riskless

What is h?

hX

C

1

Zvi Wiener ContTimeFin - 4 slide 27

Hedging

CC

XXd

dtX

C

X

C 22

2

2

1

2

2

2

2

1dX

X

C

X

CdX

X

C

C

XdX

Riskless if volatilitydoes not change.

Zvi Wiener ContTimeFin - 4 slide 28

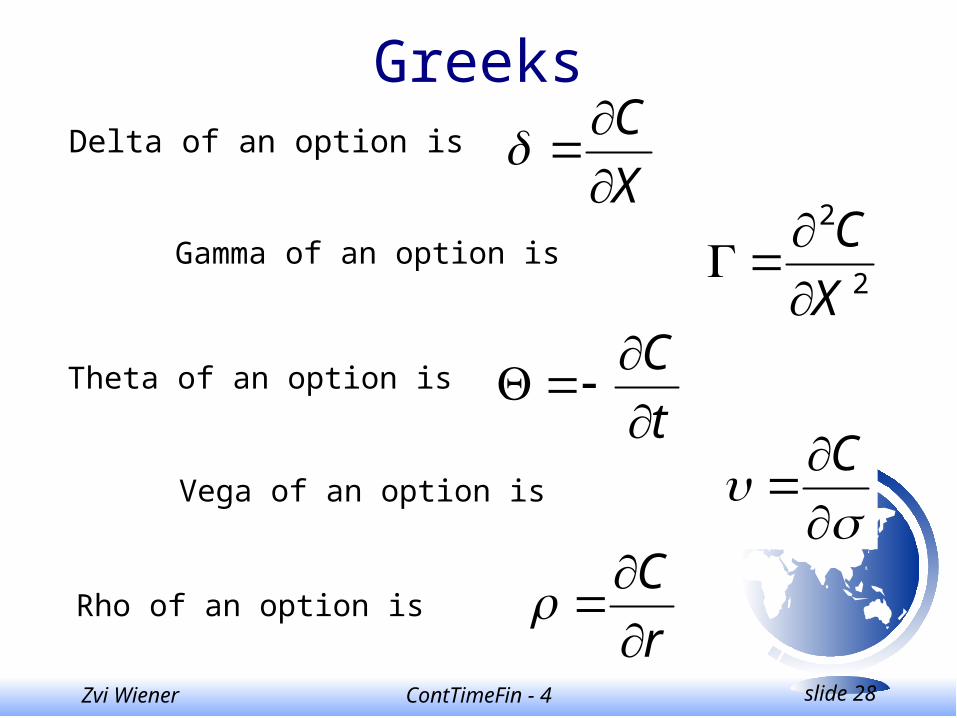

Greeks

Delta of an option isX

C

Gamma of an option is2

2

X

C

Theta of an option is

Rho of an option is

Vega of an option is

t

C

r

C

C

Zvi Wiener ContTimeFin - 4 slide 29

BMS Formula and BMS Equation

Delta of an option is )( 1dNX

C

Gamma of an option is equal to vega.

T

t

dtT )(2

When = (t) the BMS can be modified by

Zvi Wiener ContTimeFin - 4 slide 30

Implied Volatility

The value of volatility that makes the BMS formula to be equal to the observed price.

Volatility smile.

Confirms that the BMS formula is more general than the BMS formula.

Zvi Wiener ContTimeFin - 4 slide 31

Equilibrium Valuation

This corresponds to the case when the underlying security does not earn the risk-free rate r.

Example:

dividends are paid (continuously or discrete)

it is not traded

cost-of-carry

(storage, maintenance, spoilage costs)

convenience yield from liquid assets

Zvi Wiener ContTimeFin - 4 slide 32

Equilibrium Valuation

If the rate of return on X is below the equilibrium rate, i.e. dX = (-)Xdt + XdZ

0.52X2Vxx+ (r-)XVx - rV - V = 0

Can be solved by a substitution and change

of a numeraire.

Y = Xe- V(X, ) = W(Y, )

Zvi Wiener ContTimeFin - 4 slide 33

The American Option

dX = (-)Xdt + XdZ

While the option is alive it satisfies the PDE:

0.52X2Vxx+ (r-)XVx - rV - V = 0

Optimal exercise boundary: Q()

high contact condition = smooth pasting condition

Zvi Wiener ContTimeFin - 4 slide 34

The American OptionWhen X < Q, the equilibrium equation:

0.52X2Vxx+ (r-)XVx - rV - V = 0

When X > Q, the following equation:

0.52X2Vxx+ (r-)XVx - rV - V = rE- X

is derived by substituting V = X-E in the lhs.

V and Vx are continuous at X=Q.

0.52X2Vxx- V is discontinuous at X=Q.

Zvi Wiener ContTimeFin - 4 slide 35

Exercise 3.1V is a forward contract on X. X follows a GBM. Assume that there are no carrying costs, convenience yield, or dividends. Let the rate of return on the cash commodity (X) be

= r+(M-r)

a. Find the expected future cash price.

b. Relationship between the forward price and the expected cash price.

c. Under what conditions the expectation hypothesis is correct?

Zvi Wiener ContTimeFin - 4 slide 36

Solution 3.1XdZXdtdX

22

)(1

2

11ln dX

XdX

XXd

dZdtdtXd 2

)(ln2

tt ZtaXX

2lnln

2

0

tZtt eXX )5.0(

0

2

Zvi Wiener ContTimeFin - 4 slide 37

Solution 3.1

a. E(Xt)=X0et.

b. F0= E(Xt)e (r-)t.

c. r = , or = 0.

Zvi Wiener ContTimeFin - 4 slide 38

Exercise 3.2What are the effects of carrying costs, convenience yields, and dividends?

Zvi Wiener ContTimeFin - 4 slide 39

Solution 3.2

r - risk free rate,

c - carrying cost,

d - dividend yield,

y - convenience yield.

All variables represent proportions of costs or benefits incurred continuously.

tydcrt eXXE )(

0)(

Zvi Wiener ContTimeFin - 4 slide 40

Exercise 3.3Suppose that an underlying commodity’s price

follows an ABM with drift and volatility .

What economic problems will it cause?

What is the value of a forward contract

assuming that a proportion of the price, , is

kept in a zero-interest margin account?

Zvi Wiener ContTimeFin - 4 slide 41

Exercise 3.4Suppose that the value of X follows a mean

reverting process:

dX = (-X)dt+XdZ

When this situation can be used?

Value a forward contract on value of X in periods.

Zvi Wiener ContTimeFin - 4 slide 42

Exercise 3.8Value a European option on an underlying index X,

that follows a mean-reverting square root process:

dX = ( - X)dt+XdZ

When this situation can be used?

Value a forward contract on value of X in periods.

Zvi Wiener ContTimeFin - 4 slide 43

Home Assignment

X follows an ABM. Calculate Et(Xs).

X follows a GBM. Calculate Et(Xs).