© 2008 ibm corporation the new landscape innovation in a networked world francesco angeleri...

Post on 19-Dec-2015

213 views

TRANSCRIPT

© 2008 IBM Corporation

The New Landscape

Innovation in a Networked World

Francesco AngeleriVice-President IBM ItalyRome, 25th November 2008

© 2008 IBM Corporation2

Corporate Strategy

Innovation in a networked world November 2008

Corporate headquarters: Armonk, NY

387,000 employees

Serving clients in 170 countries worldwide

More than 60 percent of revenue generated outside the United States

8 research laboratories and 24 development laboratories worldwide

Year end 2007, IBM reported:

- $98.4 billion in revenue

- $10.4 billion in net income

IBM Corporation

Percent of IBM’sTotal Revenue in 2007

Services

Software

Other

Hardware

Financing

© 2008 IBM Corporation3

Corporate Strategy

Innovation in a networked world November 2008

IBM Research

Haifa

Almaden Yorktown Heights

Delhi

ZurichBeijing

TokyoAustin

8 research laboratories, over 3,200 scientists and engineers 5 Nobel Prizes Contributes to IBM’s 15 years of patent leadership, yielding more than

37,000 U.S. patents R&D expenses in 2007: $6 billion

© 2008 IBM Corporation4

Corporate Strategy

Innovation in a networked world November 2008

Industry Sectors

Large enterprises Financial services Distribution Manufacturing Communications and

media Public Sector

Small and medium business

IBM operating model

Business Units

HardwareServersStorage

Software Services and solutions

Business Infrastructure

Technology Financing

Geographies

America Europe, Middle East,

Africa Asia Pacific

© 2008 IBM Corporation5

Corporate Strategy

Innovation in a networked world November 2008

Established in 1927

Headquarter in Segrate (Milan), 24 sites in Italy

About 10.000 employees *, over 3,500 business partners

Software Development Laboratory in Rome (500 employees)

Innovation Centers working on leading edge solutions in Naples, Cagliari, Bari, Catania

E-Government Open Solution Center in Rome

IBM Italy Foundation since 1991 operating in social and cultural fields

2007 revenue: € 2.370 million *

IBM in Italy

New IBM Italy Headquarter in Segrate

* figures related to IBM Italy Group

© 2008 IBM Corporation6

Corporate Strategy

Innovation in a networked world November 2008

Bari: Java Technology /Learning Services Technology - Web mission critical applications - Life sciences application - e-learning solutions, knowledge factory

Cagliari: e-Infrastructure Technology - Infrastructure security and performances optimization

Naples: Portal Technology - Web portals development

Catania: Mobile Technology - Wireless e-business solutions

IBM Italy Innovation Centers

© 2008 IBM Corporation7

Corporate Strategy

Innovation in a networked world November 2008

Small & Medium Business Sector WorldWide

Small & Medium Business Worldwide is IBM’s fastest growing IT market opportunity:

- representing the 40% of the total IT Market in 2007

- growing 6% YTY, from $304B to $322B

- generating more than 20% of the IBM revenue

© 2008 IBM Corporation8

Corporate Strategy

Innovation in a networked world November 2008

An overall sales force of 300 people spread over the Italian geography

IBM presence distributed over 7 territories with a complete coverage of our country

An ecosystem of 1900 Business Partner with a working force of 20000

people

3500 IBM specialists working on small & medium business

Small & Medium Business Sector Italy

© 2008 IBM Corporation9

Corporate Strategy

Innovation in a networked world November 2008

In a connected, IT-enabled world, work moves to where it can best be

performed. New market opportunities are opening around the globe.

Chapter 1 Global Backdrop

© 2008 IBM Corporation10

Corporate Strategy

Innovation in a networked world November 2008

Over one billion individuals are using the internet

~17% of global population

Internet Connectedness as of 2006

Source: Computer Industry Almanac http://www.c-i-a.com/pr0899.htm

# of

Inte

rnet

Use

rs (M

)

North America

Western Europe

Asia-Pacific

South Central America

Eastern Europe

Middle East/Africa

0

100

200

300

400

500

600

700

800

1995 2000 2005

Deployment Installation Crash

Worldwide Internet Usage by Region

Source: http://www.internetworldstats.com/stats.htm

Region 1995 2005

North America 69% 30%

Western Europe 20% 28%

Asia-Pacific 8% 25%

South Central America

1% 7%

Eastern Europe 1% 6%

Middle East / Africa

1% 4%

Regional Share

30%

28%

25%

CAGR 30%

© 2008 IBM Corporation11

Corporate Strategy

Innovation in a networked world November 2008

Trade Regulations

Internet and Wireless Communications

Enterprise Resource Planning

Global centers of excellence

Best in class partnerships

Flexible sourcing capabilities

Global marketplaces

Global resource optimization

Streamlined infrastructure

Internal and external collaboration

Open Standards …Enable Global Componentization…

…With Seamless Integration

Open Business Environments:Work flows to the places where it can best be done

© 2008 IBM Corporation12

Corporate Strategy

Innovation in a networked world November 2008

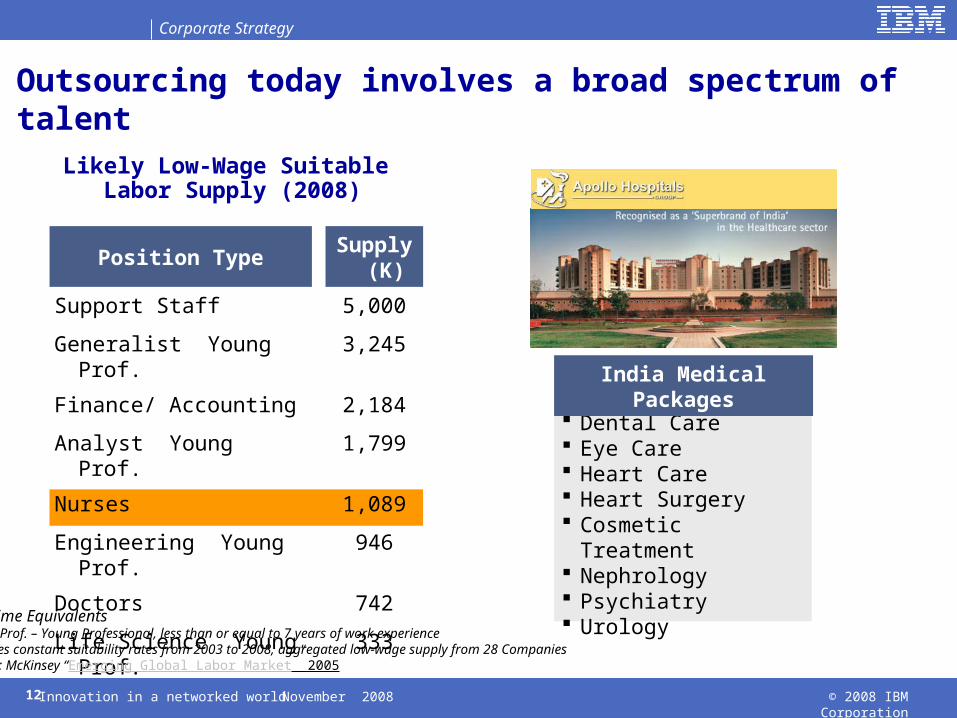

Outsourcing today involves a broad spectrum of talent

Position Type Supply (K)

Support Staff 5,000

Generalist Young Prof. 3,245

Finance/ Accounting 2,184

Analyst Young Prof. 1,799

Nurses 1,089

Engineering Young Prof. 946

Doctors 742

Life Science Young Prof. 333

Full Time EquivalentsYoung Prof. – Young Professional, less than or equal to 7 years of work experienceAssumes constant suitability rates from 2003 to 2008, aggregated low-wage supply from 28 CompaniesSource: McKinsey “Emerging Global Labor Market” 2005

Likely Low-Wage Suitable Labor Supply (2008)

Dental Care Eye Care Heart Care Heart Surgery Cosmetic Treatment Nephrology Psychiatry Urology

India Medical Packages

© 2008 IBM Corporation13

Corporate Strategy

Innovation in a networked world November 2008

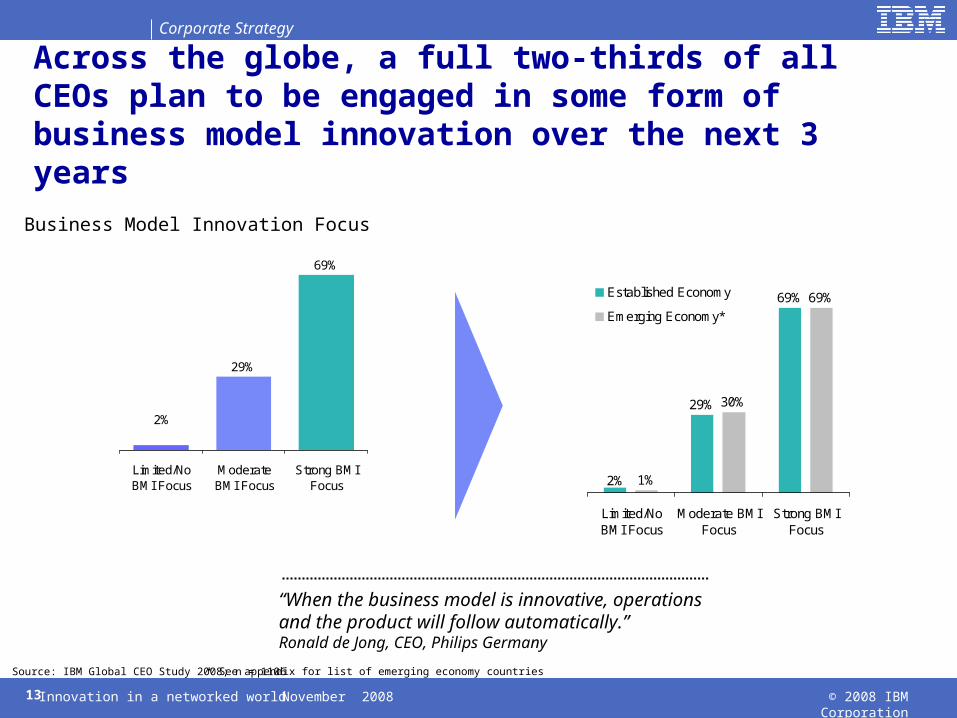

Across the globe, a full two-thirds of all CEOs plan to be engaged in some form of business model innovation over the next 3 years

Business Model Innovation Focus

Source: IBM Global CEO Study 2008; n = 1106 * See appendix for list of emerging economy countries

29%

2%

69%

Limited/NoBMI Focus

ModerateBMI Focus

Strong BMIFocus

“When the business model is innovative, operations and the product will follow automatically.”Ronald de Jong, CEO, Philips Germany

29%

69%

1%

30%

69%

2%

Limited/NoBMI Focus

Moderate BMIFocus

Strong BMIFocus

Established Economy

Emerging Economy*

© 2008 IBM Corporation14

Corporate Strategy

Innovation in a networked world November 2008

24%20% 19%

50%

13% 13%

24%

37%

EnterpriseModel

Innovation

RevenueModel

Innovation

IndustryModel

Innovation

MultipleTypes

Established Economy

Emerging Economy*

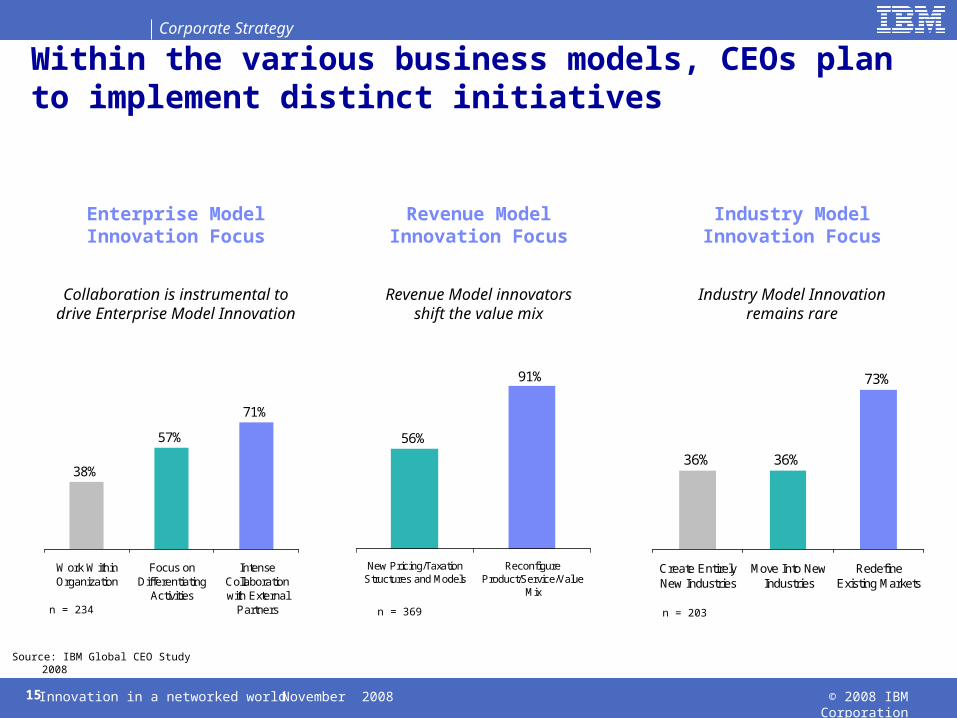

Of CEOs strongly focused on BMI, Enterprise Model Innovation is most common

Business Model Innovation Preferences

Source: IBM Global CEO Study 2008; n = 757; Strong focus on BMI type includes 6 to 7 scores on a 1 to 7 scale (69% of total population)

18%

39%

23%

20%

* See appendix for list of emerging economy countries

“We have become much smarter in how we do our pricing. Our pricing model is now based on customer segmentation and value created for those customers.”Steffen Schiottz-Christensen, Managing Director, Maersk Logistics North Asia

© 2008 IBM Corporation15

Corporate Strategy

Innovation in a networked world November 2008

56%

91%

New Pricing/TaxationStructures and Models

ReconfigureProduct/Service/Value

Mix

n = 234 n = 203

Source: IBM Global CEO Study 2008

38%

57%

71%

Work WithinOrganization

Focus onDifferentiating

Activities

IntenseCollaborationwith External

Partners

Enterprise Model Innovation Focus

n = 369

Revenue Model Innovation Focus

36% 36%

73%

Create EntirelyNew Industries

Move Into NewIndustries

RedefineExisting Markets

Industry Model Innovation Focus

Collaboration is instrumental to drive Enterprise Model Innovation

Revenue Model innovators shift the value mix

Industry Model Innovation remains rare

Within the various business models, CEOs plan to implement distinct initiatives

© 2008 IBM Corporation16

Corporate Strategy

Innovation in a networked world November 2008

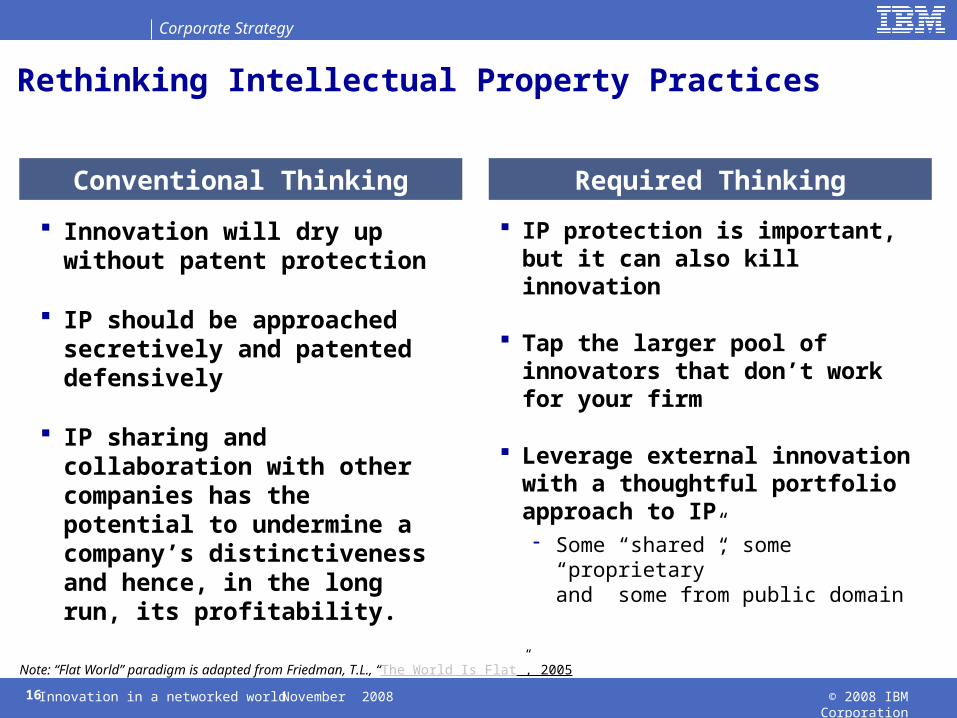

Conventional Thinking Required Thinking

Rethinking Intellectual Property Practices

Innovation will dry up without patent protection

IP should be approached secretively and patented defensively

IP sharing and collaboration with other companies has the potential to undermine a company’s distinctiveness and hence, in the long run, its profitability.

IP protection is important, but it can also kill innovation

Tap the larger pool of innovators that don’t work for your firm

Leverage external innovation with a thoughtful portfolio approach to IP Some “shared”, some “proprietary”

and some from public domain

Note: “Flat World” paradigm is adapted from Friedman, T.L., “The World Is Flat”, 2005

© 2008 IBM Corporation17

Corporate Strategy

Innovation in a networked world November 2008

The financial crisis has pushed advanced economies close to recession, with emerging markets now driving global growth

012

34567

89

10

199719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

Advanced economiesEmerging markets

0%

50%

100% Rest ofthe worldChina

OtherAdvancedUnitedStates

Real Economic Growth by Market Type, 1997-2013f % IMF Projections of Global GDP Growth,

2006-2012 %

Source of Global Growth, 1990-2009f

Source: IMF World Economic Outlook, April 2008, October 2008Note: ‘Advanced economies’ and ‘emerging markets’ broadly correspond to IBM’s major markets and growth markets categories, but with some exceptions

0246

2006

2007

2008

2009

2010

2011

2012

Downward revision, dueto crisisGlobal GDP growth

1990

1994

1995

1999

2000

2004

2005

2009

© 2008 IBM Corporation18

Corporate Strategy

Innovation in a networked world November 2008

The financial crisis is proving what was widely known – that the world has become smaller and flatter

The deep global impact of the ongoing financial crisis confirms that current globalization has made the world both smaller and flatter than before

A smaller and flatter world has meant that the latest information or sentiment from one economy now travels around the world instantly

With more than 60% of world output now traded internationally, a recession in one region has greater consequences globally- 2008 stock exchange

performances from around the world confirm this

Degree of Correlation Between Selected Stock MarketsJanuary 1 - October 22 2008

City New York Tokyo Shanghai Frankfurt Average

New York \\ 87% 69% 92% 83%

Tokyo 87% \\ 55% 92% 78%

Shanghai 69% 55% \\ 75% 66%

Frankfurt 92% 92% 75% \\ 87%

© 2008 IBM Corporation19

Corporate Strategy

Innovation in a networked world November 2008

A Globally Integrated Enterprise addresses key globalization questions with a suite of six capabilities

How do we deliver unique value in an open,

collaborative ecosystem?

How do we tap the power

of globalization?

How do we forge a strategy

for specialization?Leverage

GlobalAssets

Serve Distinct Global

Markets

Build a Specialized Enterprise

Enable Collaboration

Manage Value in an

Ecosystem of Increasingly Specialized

Entities

Address Shared Risk and Control

Globally Integrated Enterprise

© 2008 IBM Corporation20

Corporate Strategy

Innovation in a networked world November 2008

The traditional IT industry is mature – growth has slowedInnovative firms will adopt modular business designs, an open IT infrastructure with SOA, IOD, CBM, etc.IT investments pay off when they are coupled with changes to workflowDramatic opportunity has opened in business services

Broadened IBM opportunityChapter 2

© 2008 IBM Corporation21

Corporate Strategy

Innovation in a networked world November 2008

The traditional IT industry is maturing and will experience a slower rate of growth

-5

0

5

10

15

20

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

InstallationInstallation DeploymentDeployment

Source: IBM Market Intelligence analysis, using GMV2H06 and BPV2H06

Traditional ITTraditional IT

Crash

Real GDPReal GDP

% CAGR Growth

© 2008 IBM Corporation22

Corporate Strategy

Innovation in a networked world November 2008

Today’s Enterprise Realities

E01-EDI

Data Warehouse(Interfaces to and from theData Warehouse are not

displayed on this diagram)

Application Diagram V4

G02 - GeneralLedger

A05 - AP

S01 - SalesCorrections

I01 POReceiving

I03 Return toVendor

I06 WarehouseManagement

M a inframe apps - B luePC/NT apps - G reenUnix apps - Y ellow3rd party interface - Orange

Lines: Colors have no special meaning.They are to help make the diagram easier to

read.For More Information: See the databasecontaining information about each

application: Application V4.mdb

S06 - Credit App

P15 EES EmployeeChange Notice

OTHER APPS - PCAP - Collections/Credit

TM - Credit Card DB

ACCTS REC APPS - PC990CORBad Debt

Benefical FeesBeneficial Reconcil

JEAXFJEBFAJEBKAJEDVAJESOAJEVSAJEVSFNSF

TeleCredit Fees

INVENTORY CONTROL APPS - PCCode Alarm

Debit ReceivingsDevo Sales

Display InventoryIn HomeJunkouts

Merchandise WithdrawlPromo CreditsRTV Accrual

ShrinkAP Research - Inv CntrlAP Research-Addl Rpts

Book to Perpetual InventoryClose Out Reporting

Computer Intelligence DataCount Corrections

Cross Ref for VCB DnldsDamage Write OffDebit Receivings

DFI Vendor DatabaseDisplay Inventory ReconcilDisplay Inventory Reporting

INVENTORY CONTROL APPS - PCDPI/CPI

IC BatchingInventory Adj/Count CorrectInventory Control Reports

Inventory LevelsInventory Roll

Merchandise WithdrawlOpen ReceivingsPI Count Results

PI Time Results from InvPrice Protection

Sales Flash ReportingShrink Reporting

SKU Gross MarginSKU Shrink Level Detail

USMVCB Downloads

Journal Entry Tool Kit

Scorecard - HR

L02-ResourceScheduling(Campbell)

P09 - P17Cyborg

M02 - Millennium

M03 - Millennuim 3.0

Banks - ACH and Pos toPay

Cobra

B01 - StockStatus

S03-Polling

P14 On-line NewHire Entry

CTS

Plan Administrators(401K, PCS, Life,

Unicare, SolomonSmith Barney)

D01 Post LoadBilling

I04 HomeDeliveries

I02 -Transfers

Arthur Planning

I07 PurchaseOrder

I12 EntertainmentSoftware

I05Inventory Info

E13E3 Interface

S04 - Sales Posting

V01-Price ManagementSystem

I10 Cycle PhysicalInventory

I55 SKUInformation

K02Customer Repair

TrackingI35 Early Warning

System

B02 MerchandiseAnalysis

I13- AutoReplenishment

U18 - CTO

Intercept

I09 Cycle Counts

E02-EmployeePurchase

Texlon 3.5

ACH

Stock Options

I17 Customer PerceivedIn-Stock

U16-Texlon

SiteSeer

C02 - CapitalProjects

F06 - FixedAssets

US Bank ReconFile

Star Repair

EDICoordinator

Mesa Data

NEW SoundscanNPD Group

AIG Warranty Guard

Resumix

Optika

Store BudgetReporting

P16 - Tally Sheet

Cash Receipts/Credit

S05 - HouseCharges

Ad Expense

L01-PromoAnalysis

V02-PriceMarketingSupport

BMP - Busperformance Mngt

StoreScorecard

I11 PriceTesting

Valley Media

P09Bonus/HR

I15 Hand ScanApps

Roadshow

POS

S08 - VertexSalesTax

A04 - CustRefund Chks

Equifax

ICMS Credit

CellularRollover

S09 - DigitalSatelliteSystem

NPD,SoundScan

Sterling VANMailbox (Value)

I18SKU Rep

X92-X96Host to AS400

Communication

S02 -Layaways

Washington,RGIS,

Ntl Bus Systems

V04-SignSystem

I14 Count CorrectionsNARM

P01-EmployeeMasterfile

I06 - CustomerOrder

FrickCo

UAR - Universal AccountReconcilliation

DepositoryBanks

S07 - CellPhones

S11 - ISPTracking

AAS

Fringe PO

Cash Over/Short

L60 MDFCoop

SKU SelectionTool

SKUPerformance

SupplierCompliance

1

I35 - CEI

ASIS

Misc Accounting/Finance Apps - PC/NTCOBA (Corp office Budget Assistant)

PCBS(Profit Center Budget System)Merchandising Budget

AIMSMerch Mngr Approval

Batch ForcastingAd Measurement

AIMS Admin

AIMSReportingAd

Launcher

V03- MktReactions

SpecSource

CTO2.Bestbuy.com

RebateTransfer

SignSystem

CopyWriter'sWorkspace

ELTPowerSuite

StoreMonitor

AIS Calendar

Stores & Mrkts

Due Dates

Smart Plus

InsertionsOrders

BudgetAnalysis Tool

Print CostingInvoice App

AIS Reports

BroadcastFilter

Smart PlusLauncher

GeneralMaintenance

Printer PO

PrinterMaintenance

VendorMaintenance

Vendor Setup

Connect 3

Connect 3Reports

Connect 3PDF Transfe

Spec SourceSKU Tracking

S20-SalesPolling

Prodigy

PSP

In-HomeRepair

WarrantyBillingSystem

Process Servers(Imaging)

Prepared by Michelle Mills

Page 1 of 2

Source: IBM client engagement experience

© 2008 IBM Corporation23

Corporate Strategy

Innovation in a networked world November 2008

A Component View of a Business Supports Modular Designs: The IBM Component Business Methodology

A Business Component is a part of an enterprise that has the potential to operate independently, in the extreme as part of another company.

Columns are Business Competencies, defined as large business areas with characteristic skills and capabilities, for example, product development or supply chain.

An Accountability Level characterizes the scope and intent of activity and decision-making. The three levels used in CBM are Directing, Controlling and Executing.

Directing is about strategy, overall direction and policy.

Controlling is about monitoring, managing exceptions and tactical decision making

Executing is about doing the work

© 2008 IBM Corporation24

Corporate Strategy

Innovation in a networked world November 2008

We use evaluation criteria to compare components and we use the comparison to select and prioritise improvement projects. A ‘heat map’ can be used to show the results.

Business Administration

New Business Development

Relationship Management

Servicing and Sales

Product Fulfillment

Financial Control and Accounting

DirectingBusiness Planning

Sector Planning

Account Planning

Sales Planning

Fulfillment Planning

Portfolio Planning

Controlling

Business Unit Tracking

Sector Management

Relationship Management

Sales Management

Fulfillment Planning

Compliance

ReconciliationStaff Appraisals

Product Management

Credit Assessment

Executing

Staff Administration

Product Directory

Credit Administration

SalesProduct Fulfillment

Customer Accounts

Product Administration

Marketing Campaigns

Customer Dialog

Document Managem’n

t

General Ledger

Contact Routing

M L Differentiated

Competitive

Target Competency

Base

Revenue / Cost

RevenueCost

(H, M, or L)

“Hot” Component

M L

L L

M L

M L

M L

L L

M L

M L

M L

M L M L

M L

H L

M L

M L

M L

L H

M L

M L

L M

L M

M L

Revenue/Profit improvement opportunity

L M

Cost control opportunity

© 2008 IBM Corporation25

Corporate Strategy

Innovation in a networked world November 2008

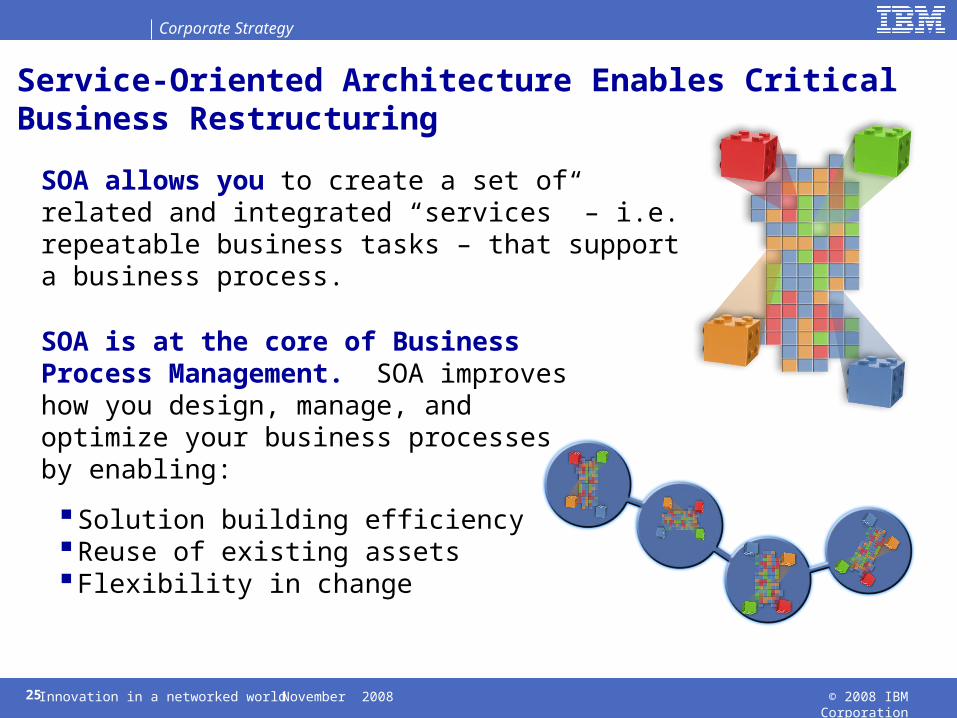

SOA is at the core of Business Process Management. SOA improves how you design, manage, and optimize your business processes by enabling:

Solution building efficiencyReuse of existing assetsFlexibility in change

SOA allows you to create a set of related and integrated “services” – i.e. repeatable business tasks – that support a business process.

Service-Oriented Architecture Enables Critical Business Restructuring

© 2008 IBM Corporation26

Corporate Strategy

Innovation in a networked world November 2008

The IT role: from technological enabler to

generator of solutions that make the “difference” on the

market

© 2008 IBM Corporation27

Corporate Strategy

Innovation in a networked world November 2008

Source: Gartner 2008

IT Strategies

IT Role

The payoff comes from making use of IT to bring new valued ideas to market

© 2008 IBM Corporation28

Corporate Strategy

Innovation in a networked world November 2008

Managing value in an ecosystem of increasingly specialized entities requires a new paradigm

R&D MfgClients

Dist Sales Sup-port

Value Chain Model

R&D

Shared Services

Client

Centric Model

Globally Integrated Enterprise Value Model

Front OfficeBack Office

Traditional frame for understanding value creation

Not sufficient to explore value in the New Landscape

Practical systems view of the value-creating ecosystem – back office and front office

Emphasis is placed on fulfilling client demands

Provides the basis to view and understand value-creating elements

Highlights inter-relationships of front and back office functions

© 2008 IBM Corporation29

Corporate Strategy

Innovation in a networked world November 2008

Source: IBM Market Intelligence and Corporate Strategy analysis, using GMV2H06 and BPV2H06

2000 20102005

1480

1932

Revenue (B$)

2385

1736

1317

Value Migration in an Expanding Opportunity SpaceOperating Profit (B$)

230 13%

16%

9%

23% 5%

8%

20%

25%

6%

20102000

289

95

1736

’05-’10CGR%

7%

’00-’05CGR%

19%

’05-’10CGR%

5%

2005

’00-’05CGR%

6%

2005 OpProf %

Business Value

Infrastructure Value

Component Value

IT Services

MW and Op Sys SW

HW-Not Served

Business Consulting

Application Software

HW-Served

Transaction Processing Services

Business Process Outsourcing

© 2008 IBM Corporation30

Corporate Strategy

Innovation in a networked world November 2008

2006 YTY@ CC

Long Term Revenue Growth Model

Services Revenue Growth Model

Strategic Outsourcing 4% - 6% 3%

Integrated Tech Services 5% - 7% -2%

Maintenance (2%) - 0% 2%

Business Transformation Outsourcing

10% - 15% 17%

Global Business Services 6% - 8% 1%

Acquisitions 2 pts --

Total Services 6% - 8% 2%

Services37%

Software

IBM Pre-Tax Income Mix2006

Hardware &

Financing

© 2008 IBM Corporation31

Corporate Strategy

Innovation in a networked world November 2008

IBM’s strategy is focused on clients that value innovation and is designed to leverage global trends.The IBM Values are foundational to our strategy and well aligned to the realities of the new landscape

IBM StrategyChapter 3

© 2008 IBM Corporation32

Corporate Strategy

Innovation in a networked world November 2008

Your products?Your services?Your financial strengths?Your customer base?Your supply chain?Your management systems?Your business model?Your history?Your brand?Your expertise?

Whatever it is that makes you unique… infuse it with the new enablers of innovation, and you can earn higher profits, penetrate new markets, drive productivity – in a word, differentiate yourself from the competition.

What makes you special?

Focus on Enterprises that Value Integration & Innovation

Pre 1900 1900s 1910s 1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s

IBM through the years

© 2008 IBM Corporation33

Corporate Strategy

Innovation in a networked world November 2008

Changes

in world

markets:

The rising tide

of globalization

Changes in

Information

Technology:

A new computing

architecture

Changes

in client

needs:

Integration and

innovation

Several years ago, we saw change coming

© 2008 IBM Corporation34

Corporate Strategy

Innovation in a networked world November 2008

I. To become the premier Globally Integrated Enterprise

II. To focus on open technologies and high-value solutions

III. To deliver integration and innovation to clients

We made important strategic decisions, and got to work

© 2008 IBM Corporation35

Corporate Strategy

Innovation in a networked world November 2008

Strong Geographic Growth 2007 Revenue byGeographic Region(excludes OEM)

21% Asia Pacific

36%Europe, Middle East and Africa

43%Americas

Countries with IBM revenue growth greater than 10 percent in local currency in 2007

We globally integrated IBM in order to participate in the world’s growth markets and improve our productivity

© 2008 IBM Corporation36

Corporate Strategy

Innovation in a networked world November 2008

SegmentPretaxIncome

Mix

SegmentPretaxIncome

Mix

2007

IBM pretax income $14.5 billionIBM pretax margin 14.7%

2003

IBM pretax income $9.4 billionIBM pretax margin 10.6%

We remixed our businesses in order to move to the emerging higher-value spaces

© 2008 IBM Corporation37

Corporate Strategy

Innovation in a networked world November 2008

policy andsociety

innovation

productinnovation

managementand culture

of innovation

servicesinnovation

business modelinnovation

businessprocessinnovation

We focused on integration and innovation in order to enable our clients’ success

Placing

a Premium

on

Innovation

© 2008 IBM Corporation38

Corporate Strategy

Innovation in a networked world November 2008

Record Cash PerformanceNet Cash from Operations,Excluding Global Financing Receivables ($ in billions)

Record Earnings Per ShareEarnings Per Share (From continuing operations)

Record Revenue($ in billions)

Record Income($ in billions)

As a result, today IBM is a higher-performing enterprise than it was a decade ago

© 2008 IBM Corporation39

Corporate Strategy

Innovation in a networked world November 2008

Primary Uses of Cash overthe Past Five Years

More than $83 billion since 2003

…while continuing to invest in R&D – more than $29 billion over the past five years

That has enabled us to invest in future sources of growth and provide record return to investors…

© 2008 IBM Corporation40

Corporate Strategy

Innovation in a networked world November 2008

Major Growth Opportunities

Area Opportunity

Emerging Markets China, India and Brazil

Small & Medium Business Services, Software

Business Services BPO, Mortgage, Engineering

Information on Demand 3rd Generation BI, Paper Based, Archive and Discovery

Service Oriented Architecture

Solution Flexibility, S&A

Security DVS, Appliances

Services Products Power Management, ISS

Server Consolidation Technology Leadership, Z Growth

© 2008 IBM Corporation41

Corporate Strategy

Innovation in a networked world November 2008

IBM Values

Dedication to every client’s success

Innovation that matters – for our company and for the world

Trust and personal responsibility in all relationships