© 2013 pearson education, inc. all rights reserved.9-1 chapter 9 life and health insurance

TRANSCRIPT

© 2013 Pearson Education, Inc. All rights reserved. 9-1

Chapter 9

Life and Health Insurance

© 2013 Pearson Education, Inc. All rights reserved. 9-2

Learning Objectives

1. Understand the importance of insurance.

2. Determine your life insurance needs and design a life insurance program.

3. Describe the major types of coverage available and the typical provisions that are included.

© 2013 Pearson Education, Inc. All rights reserved. 9-3

Learning Objectives

4. Design a health care insurance program and understand what provisions are important to you.

5. Describe disability insurance and the choices available to you.

6. Explain the purpose of long-term care insurance and the provisions that might be important to you.

© 2013 Pearson Education, Inc. All rights reserved. 9-4

Introduction

• Health insurance is an issue none of us can afford to dismiss.

• Most of us avoid thinking about and planning for our deaths—most of us do not seek out a life insurance policy.

• When you consider your need for insurance, need to keep in mind its purpose.

© 2013 Pearson Education, Inc. All rights reserved. 9-5

The Importance of Insurance

• An insurance policy spells out what losses are covered, what the policy costs, and who receives payment.

• Health insurance provides protection against devastating medical bills.

• Life insurance protects your family if you die.

© 2013 Pearson Education, Inc. All rights reserved. 9-6

The Importance of Insurance

• Health care is expensive because:– No incentive to economize.– Medical care is extremely sophisticated.– High malpractice insurance costs.

• High costs mean limited insurance coverage, no health benefits, and higher out-of-pocket payments for medical bills.

© 2013 Pearson Education, Inc. All rights reserved. 9-7

Insurance Terminology

• Risk pooling—through insurance, sharing financial consequences of risk

• Premium• Actuaries• Face amount or face of policy—amount of

insurance provided at death.• Policy owner or policyholder.• Beneficiary—designated to receive the

proceeds.• Life insurance doesn’t make sense without

a spouse or dependents

© 2013 Pearson Education, Inc. All rights reserved. 9-8

How Much Life InsuranceDo You Need?

• Priorities and goals

• Crunch the numbers—net worth, inflation and future earnings

• Earnings Multiple Approach

• Needs Approach

© 2013 Pearson Education, Inc. All rights reserved. 9-9

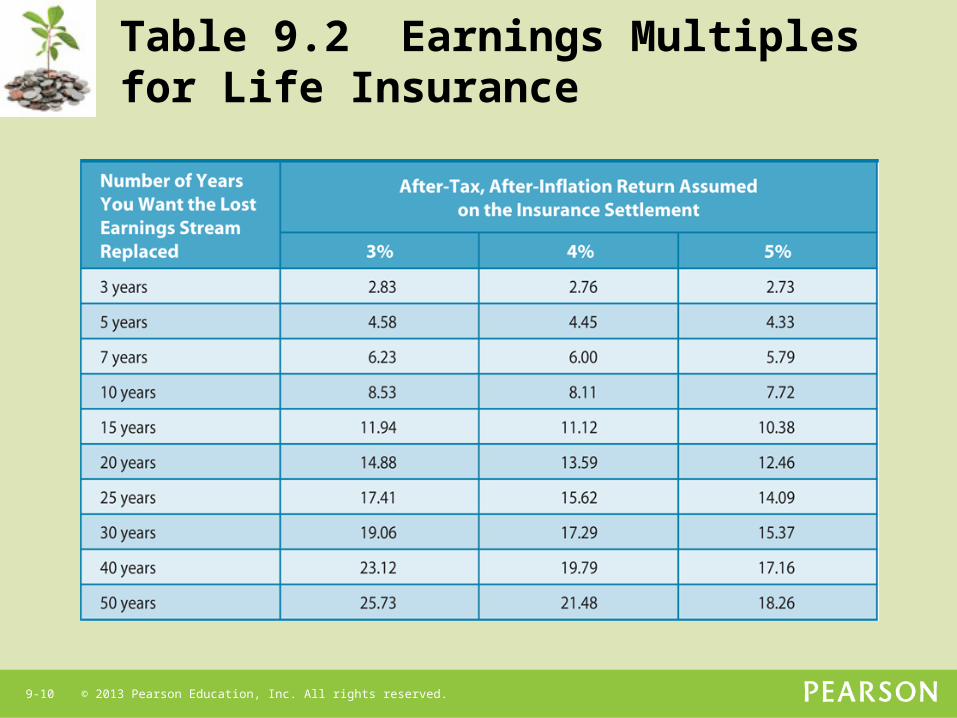

Earnings Multiple Approach

• Replace a stream of lost annual income.

• Tells you a lump-sum needed to replace that stream of annual income

• Multiply present annual gross income by the appropriate earnings multiple.

• Earnings multiple depends on number of years you need the lost income and rate of return

© 2013 Pearson Education, Inc. All rights reserved. 9-10

Table 9.2 Earnings Multiples for Life Insurance

© 2013 Pearson Education, Inc. All rights reserved. 9-11

Needs Approach

• Determine the needs of a family after the death of the breadwinner

• Immediate needs at time of death• Debt elimination funds• Immediate transitional funds• Dependency expenses• Spousal life income• Educational expenses for children• Retirement income

© 2013 Pearson Education, Inc. All rights reserved. 9-12

Major Types of Life Insurance

• Term insurance—pure life insurance that pays beneficiary a specific amount of money if you die while covered

• Cash-value insurance—has a life insurance and a savings plan

© 2013 Pearson Education, Inc. All rights reserved. 9-13

Term Insurance and Its Features

• Pays the death benefit if insured dies during the coverage period.

• Has no face value.

• Primary advantage is affordability.

• Disadvantage is that the cost increases each time the policy is renewed.

© 2013 Pearson Education, Inc. All rights reserved. 9-14

Term Insurance and Its Features

• Renewable term insurance

• Decreasing term insurance

• Group term insurance

• Convertible term life insurance

© 2013 Pearson Education, Inc. All rights reserved. 9-15

Cash-Value Insuranceand Its Features

• Provides both a death benefit and an opportunity to accumulate cash value.

• Permanent—pay the premiums and eventually you will get paid.

• 3 basic types:– Whole Life– Universal Life– Variable Life

© 2013 Pearson Education, Inc. All rights reserved. 9-16

Whole Life Insuranceand Its Features

• Death benefit when the insured dies, turns 100, or reaches the maximum stated age.

• Cash-value—policyholder’s savings

• Nonforfeiture Right—gives the policyholder the right to choose the policy’s cash value in exchange for giving up the death benefit.

• Different premium payment patterns

© 2013 Pearson Education, Inc. All rights reserved. 9-17

Universal Life Insuranceand Its Features

• Combines term insurance with tax-deferred savings with flexible premiums and benefits.

• Flexible—premiums can vary.

• Mortality charge or term insurance, cash value or savings, administrative expenses.

• May not end up with the anticipated amount of savings.

© 2013 Pearson Education, Inc. All rights reserved. 9-18

Term Versus Cash-ValueLife Insurance

• For most individuals, term insurance is the better alternative:– Low cost– High cash-value premiums can lead to less

coverage than you actually need

• Cash-value insurance has tax advantages.– Growth of the cash-value is tax-deferred.– Life insurance is not considered part of your

estate.

© 2013 Pearson Education, Inc. All rights reserved. 9-19

Riders:

• Waiver of Premium for Disability Rider

• Accidental Death Benefit Rider or Multiple Indemnity

• Guaranteed Insurability Rider

• Cost-of-Living Adjustment (COLA) Rider

Fine-Tuning Your Policy: Contract Clauses, Riders, and Settlement Options

© 2013 Pearson Education, Inc. All rights reserved. 9-20

Buying Life Insurance

• Choose an efficiently run life insurance company that will be around when your policy matures.

• Selecting an Agent– Most agents make living through commissions– Be aware of agent’s professional designation– List of prospects from good companies– Interview the agents and get a quote

© 2013 Pearson Education, Inc. All rights reserved. 9-21

Buying Life Insurance

Making a Purchase: The Net or an Advisor• Shop for term life insurance on the Web

• Check at least 2 Web quote services and call an independent insurance agent

• More complicated to compare cash-value policies—different features and assumptions

• Still get quotes on the Web for different cash-value policies

© 2013 Pearson Education, Inc. All rights reserved. 9-22

Health Insurance

• Employer-sponsored health care coverage

• Your choices limited to what employer offers

• Additional coverage, make additional payments

• Pick insurance with only types of coverage you need.

© 2013 Pearson Education, Inc. All rights reserved. 9-23

Basic Health Insurance

• Most health insurance—combination of hospital, surgical, and physician expense insurance

• Hospital insurance• Surgical insurance• Physician expense insurance• Major medical expense insurance

© 2013 Pearson Education, Inc. All rights reserved. 9-24

Health Insurance

• Dental and Eye Insurance—coverage for minor and regular dental, eye examinations, glasses, and contact lenses

• Dread Disease and Accident Insurance—additional coverage for specific disease like cancer insurance or accident

• Provide protection against major catastrophes—make policy comprehensive

© 2013 Pearson Education, Inc. All rights reserved. 9-25

Basic Health Care Choices

• Traditional fee-for-service – reimbursed for medical expenditures and choice of doctor.

• Managed health care – most expenses covered but limited choice of doctors, hospitals, and clinics.

© 2013 Pearson Education, Inc. All rights reserved. 9-26

Private Health Care Plans

• Fee-for-service plan or traditional indemnity plans:– Doctor or hospital bills you directly, company

reimburses– Coinsurance or percentage participation provision– Co-payment or deductible

• Managed health care—offered by health management organization (HMO)– Receive all health care at one location– Visit fee or co-payment

© 2013 Pearson Education, Inc. All rights reserved. 9-27

Private Health Care Plans

Managed Health Care: HMOs– Individual practice association plan (IPA)– Group practice plan– Point-of-service plan (May go outside for service)

• HMOs are cost efficient

• Service can be too quick, waits long

• Lack of choice can be too restricting

© 2013 Pearson Education, Inc. All rights reserved. 9-28

Private Health Care Plans

Managed Health Care: PPOs

• Preferred provider organization (PPO)

• Cross between traditional fee-for-service plan and an HMO

• Doctors and hospitals agree to pricing system

• Allows for health at a discount

© 2013 Pearson Education, Inc. All rights reserved. 9-29

Private Health Care Plans

Group Versus Individual Health Insurance • Group health insurance—sold with no

medical exam required to a specific group of individuals who are associated for some purpose– usually employees.

• Individual insurance policy—tailor-made for you, reflects age and health, after medical exam.

© 2013 Pearson Education, Inc. All rights reserved. 9-30

Government-SponsoredHealth Care Plans

• State Plans—provide for work-related accidents and illness

– Worker’s Compensation

• Federal Plans—Medicare, Medicaid

© 2013 Pearson Education, Inc. All rights reserved. 9-31

Medicare

• Medicare Part A—Hospital Insurance

• Medicare Part B—Supplemental Medical Insurance

• Medicare Part C—Medicare Advantage Plans

• Medicare Part D—Medicare Prescription Drug Coverage

• Medigap Plans (Private Plans)

© 2013 Pearson Education, Inc. All rights reserved. 9-32

Controlling Health Care Costs

• Flexible Spending Accounts

• Health Savings Accounts (HSAs)

• COBRA and Changing Jobs

• Choosing No Coverage—or “Opting Out”

© 2013 Pearson Education, Inc. All rights reserved. 9-33

Finding the Perfect Plan

Important Provisions in Health Insurance Policies:

• Who’s Covered? • Terms of Payment• Preexisting conditions • Guaranteed Renewability • Exclusions• Emotional and Mental Disorders

© 2013 Pearson Education, Inc. All rights reserved. 9-34

Disability Insurance

• Health insurance that provides payments to the insured in the even that income is interrupted by illness, sickness, or accident

• Sources of Disability Insurance

• How much disability coverage should you have?

© 2013 Pearson Education, Inc. All rights reserved. 9-35

Disability Features ThatMake Sense

• Definition of Disability

• Residual or Partial Payments

• Benefit Duration

• Waiting Period

• Waiver of Premium

• Noncancelable

• Rehabilitation Coverage

© 2013 Pearson Education, Inc. All rights reserved. 9-36

Long-Term Care Insurance

• Pays nursing home expenses and home health care.

• Covers costs associated with long-term care for those against the financial costs of Alzheimer’s, strokes, or chronic diseases.

• Most require that insured cannot perform at least two “activities of daily living” (ADLs)

© 2013 Pearson Education, Inc. All rights reserved. 9-37

Long-Term Care Insurance

• Type of Care—nursing home, adult day care, or hospice care for terminally ill

• Benefit Period—can range from 1 year to lifetime

• Waiting Period—0 days – 1 year

• Inflation Adjustment—protected from inflation

• Waiver of Premium—insurance stays in force while receiving benefits

© 2013 Pearson Education, Inc. All rights reserved. 9-38

Summary

• Life insurance controls the financial effect on your family when you die.

• There are two types of life insurance—term and cash-value.

• Basic health insurance provides combination of hospital, surgical, and physician expense insurance.

© 2013 Pearson Education, Inc. All rights reserved. 9-39

Summary

• Major medical expense insurance covers medical costs not covered by basic health insurance.

• Disability insurance provides income in the event of a disability.

• Long-term care insurance covers the cost of long-term nursing home care

© 2013 Pearson Education, Inc. All rights reserved. 9-40

Figure 9.1 The Rising Cost of Yearly Renewable Term Insurance—Annual Premiums for $100,000 Coverage on a 35-Year-Old Nonsmoking Male

© 2013 Pearson Education, Inc. All rights reserved. 9-41

Table 9.5 Major Provisions of the Affordable Care Acta

© 2013 Pearson Education, Inc. All rights reserved. 9-42

Table 9.5 Major Provisions of the Affordable Care Acta (cont.)

© 2013 Pearson Education, Inc. All rights reserved. 9-43

Table 9.5 Major Provisions of the Affordable Care Acta (cont.)

© 2013 Pearson Education, Inc. All rights reserved. 9-44

Table 9.6 Appealing Health Insurance Claim Decisions

© 2013 Pearson Education, Inc. All rights reserved. 9-45

Table 9.8 A Sampling of What Flexible Spending Accounts Can and Cannot Be Used For

© 2013 Pearson Education, Inc. All rights reserved. 9-46

Figure 9.3 Worksheet for Estimating How Much Disability Insurance CoverageYou Need